by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1806.95 DOWN $9.20

SILVER: $20.35 DOWN 41 CENTS

ACCESS MARKET: GOLD $1807.40

SILVER: $20.28

Bitcoin morning price: $19,093 DOWN 1224

Bitcoin: afternoon price: $18,926 DOWN 1391

Platinum price: closing DOWN $8.85 to $904.60

Palladium price; closing UP $46.75 at $1930.20

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE:EXCHANGE:

EXCHANGE: COMEX

CONTRACT: JULY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,813.700000000 USD

INTENT DATE: 06/29/2022 DELIVERY DATE: 07/01/2022

FIRM ORG FIRM NAME ISSUED STOPPED

357 C WEDBUSH 8

365 H ED&F MAN CAPITA 3

435 H SCOTIA CAPITAL 14

657 C MORGAN STANLEY 1

657 H MORGAN STANLEY 332

661 C JP MORGAN 205

685 C RJ OBRIEN 5

690 C ABN AMRO 67

737 C ADVANTAGE 10 23

800 C MAREX SPEC 7

905 C ADM 11

TOTAL: 343 343

MONTH TO DATE: 343

no. of contracts issued by JPMorgan: 205/343

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT 343 NOTICE(S) FOR 34,300 Oz//1.0668 TONNES)

total notices so far: 343 contracts for 34300 oz (1.0668 tonnes)

SILVER NOTICES:

1497 NOTICE(S) FILED 7,485,000 OZ/

total number of notices filed so far this month 1497 : for 7,485,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $9.20

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD//

INVENTORY RESTS AT 1052.63 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 41 CENTS

AT THE SLV// ://SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 738,000 OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 541.262 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 2534 CONTRACTS TO 138,309 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.11 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.11) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SOME SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A POOR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.220 MILLION OZ / // V) STRONG SIZED COMEX OI GAIN

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : +199

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTACTS for 21 days, total 18,894, contracts: 94.470 million oz OR 4.500MILLION OZ PER DAY. (899 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 94.470 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2534 DESPITE OUR $0.11 LOSS IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 2725 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ // .. WE HAD A VERY STRONG SIZED GAIN OF5259 OI CONTRACTS ON THE TWO EXCHANGES FOR 26.295 MILLION OZ DESPITE THE LOSS IN PRICE..

WE HAD 1497 NOTICES FILED TODAY FOR 7485,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 1294 CONTRACTS TO 498,299 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: —896 CONTRACTS.

.

THE SMALL INCREASE IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $4.25//COMEX GOLD TRADING/WEDNESDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JULY AT 2.914 TONNES ON FIRST DAY NOTICE

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $4.25 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 5031 OI CONTRACTS 15.64 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3737 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 498,299

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5031, WITH 1294 CONTRACTS INCREASED AT THE COMEX AND 3737 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5031 CONTRACTS OR 15.64TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3737) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (1294,): TOTAL GAIN IN THE TWO EXCHANGES 5031 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JULY. AT 2.914 TONNES 3) ZERO LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) SMALL SIZED COMEX OI GAIN 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

76,560 CONTRACTS OR 7,656,000 OZ OR 238.13 TONNES 20 TRADING DAY(S) AND THUS AVERAGING: 3645 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAY(S) IN TONNES: 238.13 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 238.13/3550 x 100% TONNES 6.70% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 2238.13 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A HUGE SIZED 2534 CONTRACT OI TO 138,309 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 2725 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 2725 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2534 CONTRACTS AND ADD TO THE 2725 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED GAIN OF 5259 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 26.295 MILLION OZ

OCCURRED WITH OUR FALL IN PRICE OF $0.11 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

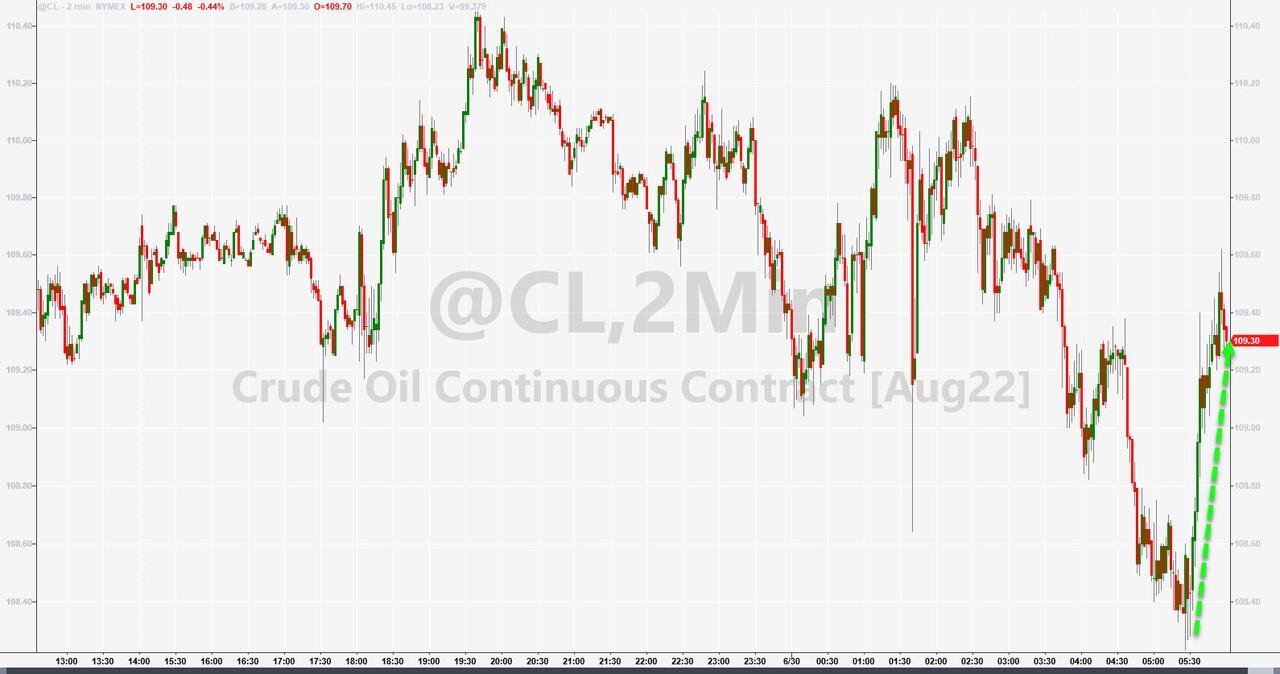

SHANGHAI CLOSED UP 37.10 PTS OR 1.10% //Hang Sang CLOSED DOWN 137.10 PTS OR 0.62% /The Nikkei closed DOWN 411.56 OR 1.54% //Australia’s all ordinaires CLOSED DOWN 1.97 /Chinese yuan (ONSHORE) closed DOWN 6.7002 /Oil DOWN TO 108.28 dollars per barrel for WTI and DOWN TO 111.98 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7002 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7073: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 1294 CONTRACTS TO 498,299 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR LOSS OF $4.25 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (3737 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY.. THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3737 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :3737 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3737 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 5031 CONTRACTS IN THAT 3737 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 1294 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $4.25.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JULY (2.914),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 2.914 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $4.25) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A STRONG SIZED GAIN OF 18.416 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOOD GOLD TONNAGE STANDING FOR JULY (2.914 TONNES)…

WE HAD -896 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 5031 CONTRACTS OR 503,100 OZ OR 15.64 TONNES

Estimated gold volume 213,823/// poor/

final gold volumes/yesterday 167,295 /poor

INITIAL STANDINGS FOR JULY ’22 COMEX GOLD //JUNE 30

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 115,244.695 oz Manfra Brinks Loomis 2004 kilobars (Loomis) |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 343 notice(s)34300 OZ 1.0668 TONNES |

| No of oz to be served (notices) | 594 contracts 59,400 oz 1.847 TONNES |

| Total monthly oz gold served (contracts) so far this month | 343 notices34300 OZ 1.0668 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

0 customer deposit

total deposits: 0 oz

3 customer withdrawals:

i) Brinks: 39,352.830 oz

ii) Loomis: 64,430.604 oz (2004 kilobars)

iii) Manfra: 11,461.264 oz

total withdrawal: 115,244.698 oz

ADJUSTMENTS:0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 937 contracts losing 74 contracts from yesterday.

Thus by definition, the initial amount of gold standing in this non active month of July is as follows:

937 contracts x 100 oz per contract = 93700 oz or 2.914 tonnes

August has a LOSS of 1450 contracts DOWN to 401,466 contracts

We had 343 notice(s) filed today for 34300 oz FOR THE July 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 343 contract(s) of which 205 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2022. contract month,

we take the total number of notices filed so far for the month (343) x 100 oz , to which we add the difference between the open interest for the front month of (JULY 937 CONTRACTS ) minus the number of notices served upon today 343 x 100 oz per contract equals 93,700 OZ OR 2.914 TONNES the number of TONNES standing in this active month of JUly.

thus the INITIAL standings for gold for the JULY contract month:

No of notices filed so far (343) x 100 oz+ (937) OI for the front month minus the number of notices served upon today (343} x 100 oz} which equals 93,700 oz standing OR 2.914 TONNES in this active delivery month of JULY.

TOTAL COMEX GOLD STANDING: 2.914 TONNES (A FAIR STANDING FOR A JULY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,419,784.828 oz 75.26 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 33,062,586.396 OZ

TOTAL ELIGIBLE GOLD: 15,883,167.581 OZ

TOTAL OF ALL REGISTERED GOLD: 17,179,418.215 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 14,792,235.0 OZ (REG GOLD- PLEDGED GOLD)

END

SILVER/COMEX/JUNE 30

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1919.581 oz CNT |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 1,411,397.582 oz CNT Delaware |

| No of oz served today (contracts) | 1497CONTRACT(S) 7,485,000 OZ) |

| No of oz to be served (notices) | 1547 contracts (7,735,000 oz) |

| Total monthly oz silver served (contracts) | 1497 contracts 7,485,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We have 1 deposit into the customer account

i) Into CNT: 1919.881 oz

total deposit: 1919/881 oz oz

JPMorgan has a total silver weight: 170.800 million oz/336.885 million =50.77% of comex

Comex withdrawals: 1

i) Out of CNT: 1919.881 oz

total withdrawal 1919/881 oz

adjustments: 3

i. customer to dealer: Brinks//19,909.630 oz

ii) dealer to customer: JPMorgan: 178,991.900 oz

iii) dealer to customer: Manfra: 258,939.201 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 69.331 MILLION OZ

TOTAL REG + ELIG. 336.855 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JULY OI: 3044 CONTRACTS

THUS BY DEFINITION THE INITIAL AMOUNT OF SILVER STANDING IN JULY IS AS FOLLOWS:

3044 CONTRACTS X 5,000 OZ PER CONTRACT = 15,220 MILLION OZ

AUGUST GAINED 64 CONTRACTS TO STAND AT 1440

SEPTEMBER HAD A GAIN OF 4819 CONTRACTS UP TO 114,215 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1497 for 7,489,000 oz

Comex volumes:61,022// est. volume today// FAIR

Comex volume: confirmed yesterday: 62,045 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 1497 x 5,000 oz = 7,485000 oz

to which we add the difference between the open interest for the front month of JULY(3044) and the number of notices served upon today 1497 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY./2022 contract month: 1497 (notices served so far) x 5000 oz + OI for front month of JULY (3044) – number of notices served upon today (1497) x 5000 oz of silver standing for the JULY contract month equates 15,220,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 30/WITH GOLD DOWN $9.20: big CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 1052.63 TONNES//

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

JUNE 21/WITH GOLD DOWN $2.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1075.54 TONES

JUNE 17/WITH GOLD DOWN $11.25: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.60 TONNES INTO THE GLD.///INVENTORY RESTS AT 1075.54 TONNES

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

GLD INVENTORY: 1052.63 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 30/WITH SILVER DOWN 41 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 738,000 OZ FROM THE SLV//INVENTORY RESTS AT 541.262 MILLION OZ//

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

JUNE 21/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 547.166 MILLION OZ//

JUNE 17/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 739,000 OZ FROM THE SLV./:INVENTORY RESTS AT 543.660 MILLION OZ/

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

CLOSING INVENTORY 541.262 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Zimbabwe Central Bank To Offer Gold Coins As Inflation Ravages The Country (Again)

THURSDAY, JUN 30, 2022 – 01:45 PM

The Reserve Bank of Zimbabwe plans to issue gold coins as a way for investors in the country to store value as inflation runs rampant in the economy.

The United States isn’t the only country battling rapidly rising prices. The inflation rate in Zimbabwe spiked from 132% in May to 191.6% in June, and the Zimbabwean currency is quickly devaluing against other global currencies, particularly the US dollar.

Enter gold.

On Monday, Reserve Bank of Zimbabwe, John Mangudya, announced the new gold coins would be minted by Fidelity Gold Refineries (Private) Limited and available to the public through normal banking institutions.

The Reserve Bank of Zimbabwe’s Monetary Policy Committee (MPC) resolved to introduce gold coins into the market as an instrument that will enable investors to store value.”

The central bank owns Fidelity Gold Refineries (Private) Limited. It operates as the only gold-buying and refining entity in the southern African country.

The RBZ has not announced a timeline for the introduction of the coins.

Batanai Matsika heads research for Morgan & Co., a Zimbabwean brokerage firm. In an interview with Al Jazeera, he called the introduction of the gold coins a “welcome development” in a market starved of options to hedge against inflation.

For a long time, the market did not have many investment options and this is a new asset class. The thinking was inspired by the need to come up with an instrument that addresses the inflation problems in the economy where purchasing power has been eroded. From what we are gathering, this is going to be a store value.”

Matsika went on to say the fundamentals of gold help it hedge against inflation and geopolitical risk, and that the gold coins would open the gold market to “ordinary investors.”

Typical of central bankers, the RBZ is trying to solve a problem it created. The country has labored under an inflationary monetary policy for decades. According to Al Jazeera, the central bank worsened the problem by printing even more new money, reversing gains made in the past two years. Inflation decreased from a peak of 800% in 2020 to 60% in January this year.

Ironically, Zimbabwean investors have turned to the US dollar as a store of value. The dollar has its own inflationary problem, but as the world reserve currency, the greenback is the cleanest dirty shirt in the laundry. One US dollar sells on the Zimbabwean black market for 650 Zimbabwean dollars.

The availability of gold coins will likely ease pressure on the US dollar in the country. After all, gold is a better long-term store of value than another fiat currency. It has no counter-party risk and it cannot be created out of thin air by central banks.

Economist Tatenda Mabhande said the central bank could use the gold coins to ease inflation if it sold them for Zimbabwean dollars. This would mop some of the excess currency out of the economy. But the coins will more likely be indexed in US dollars. It will basically work as a fundraising scheme for the Zimbabwean central bank, pulling in USD from the market.

Mabhande said the gold coins would likely flow out of the country.

Bad money will drive good money out of the market. We are likely to see the coins disappearing as well.”

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg

END

3. Chris Powell of GATA provides to us very important physical commentaries

JPMorgan and Citibank hold 90% of all gold and other precious metals derivatives held by USA banks. How on earth do they allow a convicted felon like JPMorgan hold such a huge amount of these derivatives

(Pam and Russ Martens/GATA)

Pam and Russ Martens: JPMorgan, Citibank hold 90% of all gold and other precious metals derivatives held by U.S. banks

Submitted by admin on Wed, 2022-06-29 11:39Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Wednesday, June 29, 2022

Last Tuesday the U.S. Office of the Comptroller of the Currency released its quarterly report on derivatives held at the megabanks on Wall Street. As we browsed through the standard graphs that are included in the quarterly report, one graph jumped out at us. It showed a measured growth in precious metals derivatives at insured U.S. commercial banks and savings associations over the past two decades and then an explosion in growth between the last quarter of 2021 and the end of the first quarter of this year.

In just one quarter, precious metals derivatives had soared from $79.28 billion to $491.87 billion. That’s a 520% increase in a span of three months.

Having studied these quarterly reports since the 2008 financial crash, we knew where to head next. We went to the graphs in the OCC report showing the breakdown of different categories of derivatives at specific banks. Table 21 showed that precious metals contracts at JPMorgan Chase had spiked to $330.123 billion as of March 31, 2022. The same table showed that Citigroup’s insured commercial bank, Citibank, held $114.148 billion in precious metals derivatives. …

JPMorgan Chase is the last bank in the U.S. that should have a $330 billion involvement in precious metals. On September 29, 2020, the U.S. Department of Justice charged JPMorgan Chase with rigging the precious metals market and charged it with a criminal felony count, to which it admitted. According to the Justice Department, the rigging occurred for more than eight years, from March of 2008 to August of 2016, and involved “tens of thousands” of incidents. …

… For the remainder of the analysis:

END

Bill Murphy interviewed by Chris Marcus

(GATA)

Because of GATA, Russia long has known about gold manipulation, Murphy says

Submitted by admin on Wed, 2022-06-29 14:54Section: Daily Dispatches

2:50p ET Wednesday, June 29, 2022

Dear Friend of GATA and Gold:

Interviewed by Chris Marcus of Arcadia Economics, GATA Chairman Bill Murphy notes that the Russia government has known about gold and silver market manipulation for many years, in part because of GATA’s work.

The interview is 18 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

4. OTHER GOLD STORIES

5.OTHER COMMODITIES

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

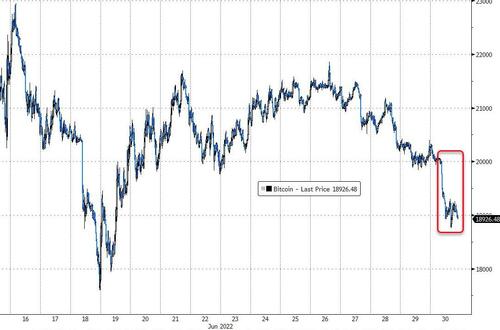

Bitcoin Breaks Below $19k, SEC Rejects Spot ETF, FTX Buys BlockFi, JPM Says ‘Deleveraging Well Advanced’

THURSDAY, JUN 30, 2022 – 01:25 PM

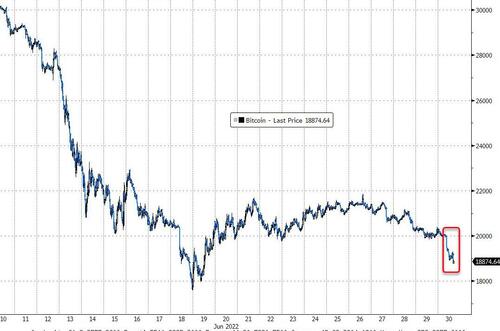

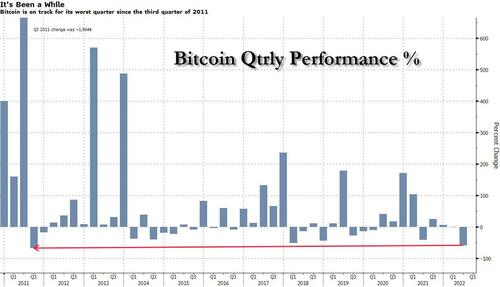

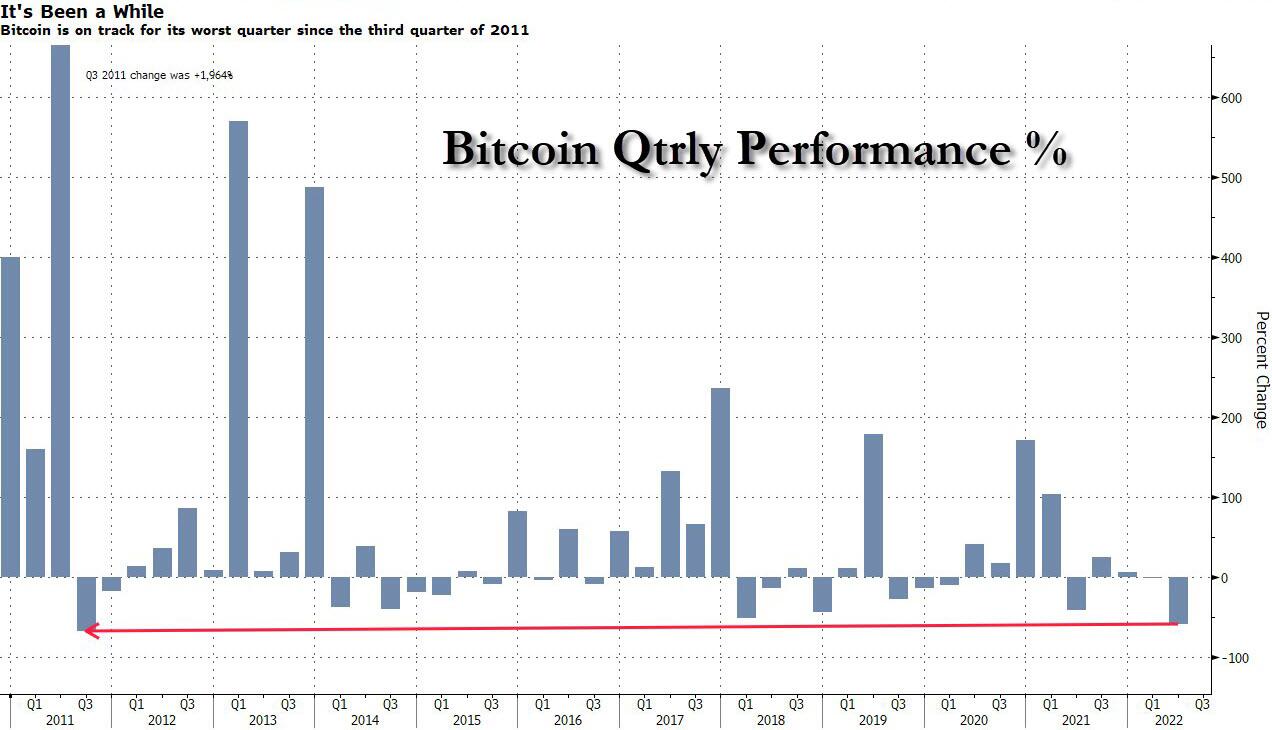

Bitcoin broke back below $19,000 this morning to end its worst first-half of a year ever (and worst quarter since Q3 2011…

The (mostly negative) headlines keep mounting as JPMorgan’s Nikolaos Panigirtzoglou warns that deleveraging continues to reverberate throughout the crypto ecosystem.

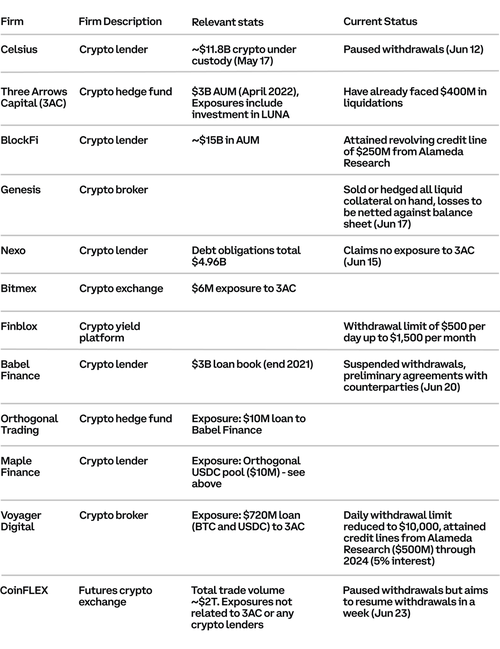

Multiple failures among crypto companies should not be a surprise in the current backdrop of deleveraging, given the crypto market lost 70% of its capitalization cumulatively since last November. The entities that employed higher leverage in the past are now the most vulnerable. Whether it is miners having borrowed to expand operations using their bitcoins as collateral, or corporates such as MicroStrategy having borrowed in the past to invest even more heavily into bitcoin, or hedge funds using futures to lever their positions, or retail investors borrowing via margin accounts to invest into various cryptocurrencies. Three Arrows Capital’s failure is a manifestation of this deleveraging process, a process that appears well advanced, making the bottom formation process in crypto markets more volatile.

In the current phase of deleveraging, the weakest crypto entities, i.e. those with high leverage and low capital appear to be most challenged, while the ones with the strongest balance sheets seem most likely to survive and emerge stronger once the current deleveraging phase is over. How much more deleveraging needs to still happen is hard to assess.

But indicators like our Net Leverage metric suggest that deleveraging is already well advanced.

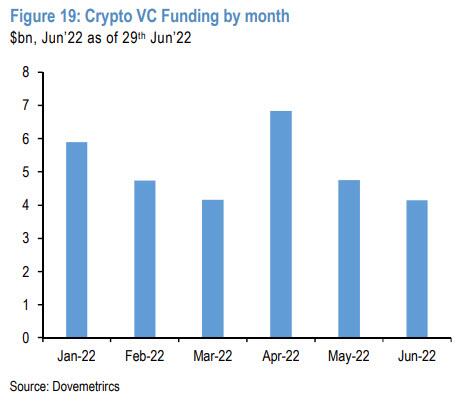

And we find two additional reasons to believe that the current deleveraging cycle may not be very protracted:

1) The fact that crypto entities with the stronger balance sheets are currently stepping in to help contain contagion and;

2) VC funding, an important source of capital for the crypto ecosystem, continued at a healthy pace in May and June.

Still, the crypto ecosystem took another modest blow last night as The SEC rejected Grayscale’s application to convert its Grayscale Bitcoin Trust to an exchange-traded fund late Wednesday, citing concerns about market manipulation, the role of Tether in the broader bitcoin ecosystem and the lack of a surveillance-sharing agreement between a “regulated market of significant size” and a regulated exchange, echoing concerns the regulator has expressed for years in rejecting other spot bitcoin ETF applications.

GBTC responded by suing the SEC, as CEO Michael Sonnenshein said the company was “deeply disappointed” and “vehemently disagree” with the SEC’s decision to deny their application.

“Over 11,400 investors, academics, business leaders, trade associations, and other key stakeholders submitted comments to the SEC in support of Grayscale’s ETF proposal,” wrote Sonnenshein.

As of June 9th, over 99.9% of those comment letters were supportive of the cause.

As CoinTelegraph reports, Grayscale announced that its senior legal strategist, former U.S. solicitor general Donald B. Verrilli Jr., had filed a petition for review with the United States Court of Appeals for the District of Columbia Circuit.

Verrelli stated that the latest decision shows that the SEC is acting “arbitrarily and capriciously” by “failing to apply consistent treatment to similar investment vehicles” and will be pursuing a legal challenge based on the SEC’s alleged violation of the Administrative Procedure Act (APA) and Securities Exchange Act (SEA).

Grayscale Investments, which has $12.92 billion of assets under management in its GBTC, announced its intentions to transition the fund into an ETF in April 2021. A formal request to do so was then submitted later that year, in October. Since then, Grayscale has mounted many efforts to properly inform the public of its intentions and to meet all regulatory requirements.

Essentially, the company will argue that the SEC has to allow products that are like other products already trading, in this case bitcoin futures ETFs.

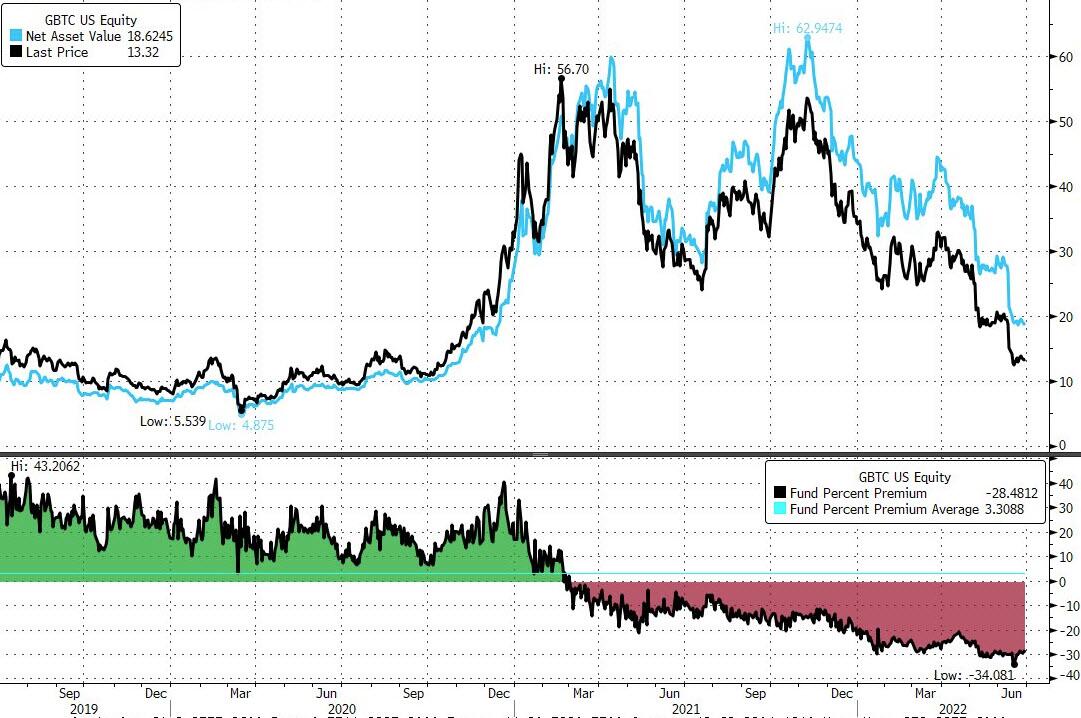

By changing the trust into a spot Bitcoin ETF, Grayscale hopes to correct Grayscale Bitcoin Trust’s “discount” and allow the investment firm to charge lower fees, making it easier to move money in and out of the fund.

The SEC’s ongoing negative response to a spot Bictoin ETF prompted many reactions across social media with some accusing the SEC of “holding GBTC hostage.”

According to Twitter user Ann, since the SEC approved an ETF that shorts Bitcoin, the SEC may be working to “suppress the price of Bitcoin.”

The Twitter user argued that this is not the role of the SEC.

Ironically, on the same day that the SEC rejects GBTC, CoinTelegraph reports that major Dutch stock exchange Euronext Amsterdam, a part of the pan-European marketplace Euronext, is debuting its first Spot Bitcoin ETF.

The Jacobi Bitcoin ETF is positioned as the first spot Bitcoin ETF launched in Europe, Jacobi founder and CEO Jamie Khurshid told Cointelegraph.

“Our product is the first spot or physical-backed Bitcoin fund, and the fund is not allowed to lend, stake or leverage any of the assets it owns. For the first time in Europe, investors buying an exchange-traded Bitcoin product will own the units that own the Bitcoin,” Khurshid said.

“There are other exchange-traded products in Europe but no other spot BTC ETF,” he added.

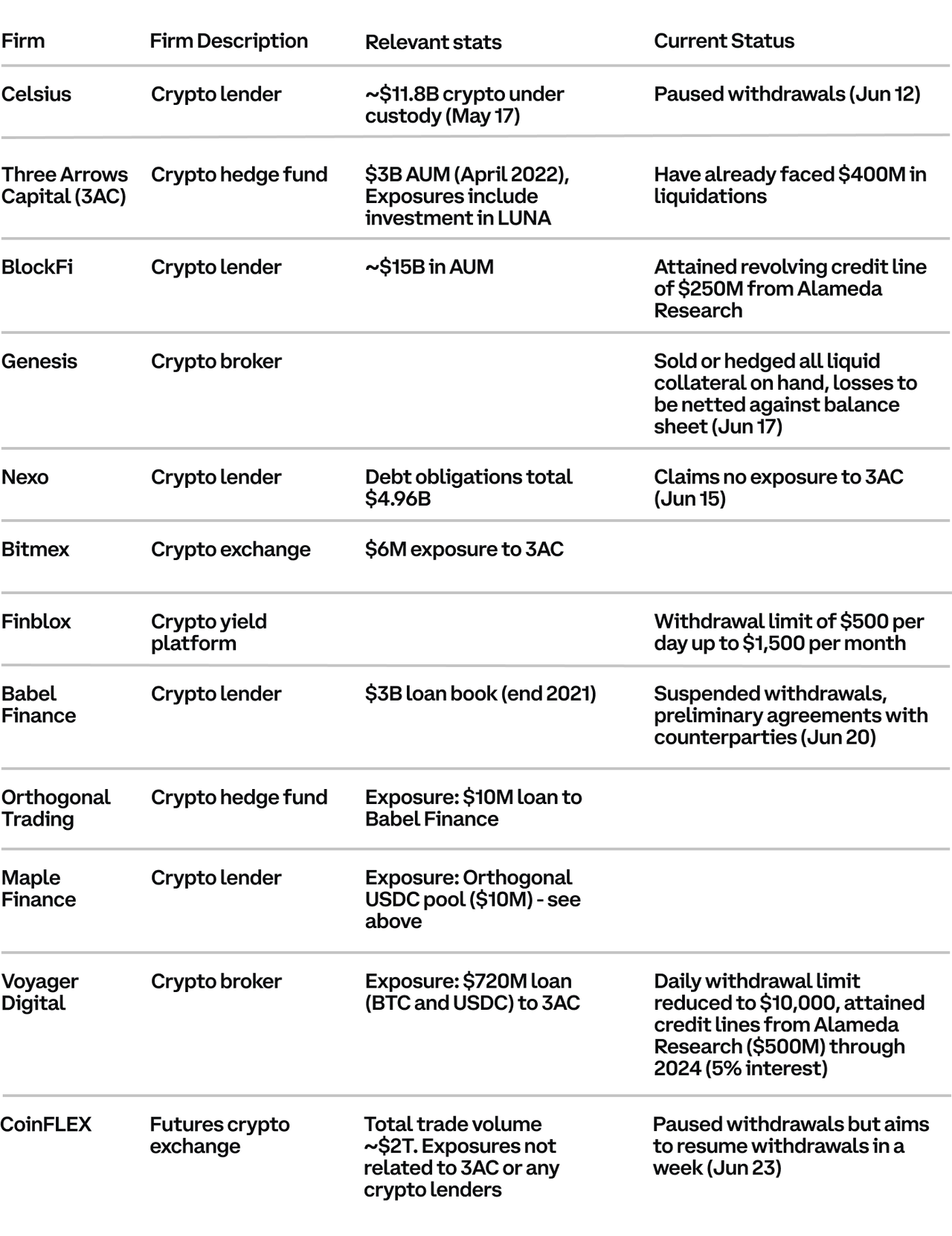

In other news, The Block reports that FTX looked at a deal with Celsius but in the end walked away, citing two people with knowledge of the matter.

FTX held talks with Celsius about providing financial support or making an acquisition but did not proceed to looking at Celsius’s finances. Celsius had a $2 billion hole in its balance sheet and FTX found the company difficult to deal with, one of the sources said.

On a brighter note, it seems FTX was more interested elsewhere as CBNC reports the crypto exchange is swooping in to buy crypto lender BlockFi for pennies on the dollar.

FTX will pay roughly $25 million – 99% below BlockFi’s last private valuation.

Jersey City, New Jersey-based BlockFi was last valued at $4.8 billion, according to PitchBook.

The fire sale comes a week after FTX provided a $250 million emergency line of credit to BlockFi.

FTX CEO Sam Bankman-Fried said at the time that the financing would help BlockFi “navigate the market from a position of strength.”

Finally, we note that, as Anita Posch writes at BitcoinMagazine.com, crypto lending scheme implosions make bitcoin stronger.

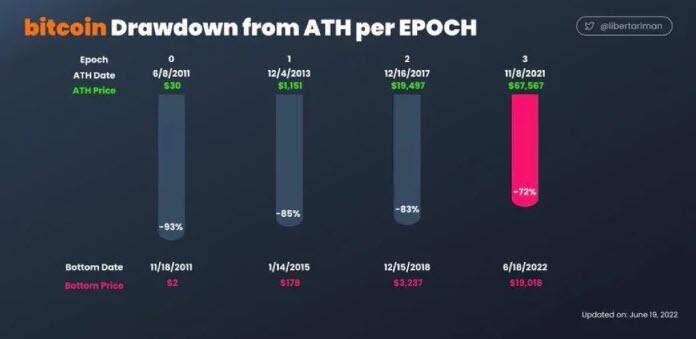

As you can see in the graph above, the recent bitcoin price drawdown is not the first of its kind in the history of Bitcoin. It’s not unusual that the price reaches a low in between two halving events, when the amount of newly-minted bitcoin is split in half, which occurs every four years.

Reckless lending practices brought the whole crypto-lending system down. These centralized services take customers’ bitcoin and promise monthly returns. They lend it out to other DeFi projects, which is risky in the first place, and, on top of that, they lend out more money than they hold in assets. This is essentially a practice that led to the global financial crisis of 2008, which was a reason that Satoshi Nakamoto released the Bitcoin software in the first place.

Now, the cryptocurrency industry is building the same over-leveraged financial products and one has to ask: Did they not learn? Did they think they found a solution to magically make profits, where there is no underlying economic activity?

The failure of these yield-searching companies brought the whole market and bitcoin down in the last weeks. It’s a great reminder that one should have all assets in self custody and that there is no magical solution to money making by over-leveraging. Hopefully, investors and businesses learn from these busts.

Bitcoin is a decentralized technology which is unstoppable. No government nor any bank can change or control it. No one can take it away from you. This is especially important if you live in a country with authoritarian leaders or a broken banking system. Bitcoin has been declared dead several times, but it has been producing new blocks every 10 minutes anyway. It’s unstoppable, like a clock.

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7002

OFFSHORE YUAN: 6.7073

HANG SANG CLOSED DOWN 137.10 PTS OR 0.62%

2. Nikkei closed DOWN 411.56% OR 1.54%

3. Europe stocks ALL CLOSED ALL RED

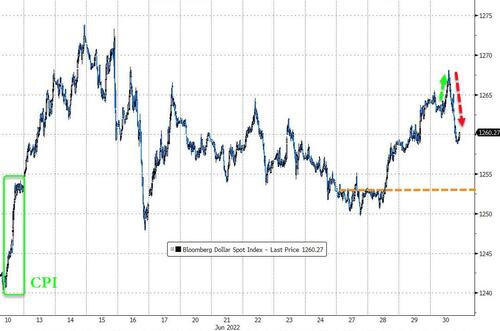

USA dollar INDEX UP TO 105.27/Euro FALLS TO 1.0396

3b Japan 10 YR bond yield: FALLS TO. +.222/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 136.33/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.587%/Italian 10 Yr bond yield FALLS to 3.58% /SPAIN 10 YR BOND YIELD FALLS TO 2.66%…

3i Greek 10 year bond yield RISES TO 3.63//

3j Gold at $1803.90 silver at: 20.34 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 72/100 roubles/dollar; ROUBLE AT 52.51

3m oil into the 109 dollar handle for WTI and 111 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 136.33DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9579– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9955well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

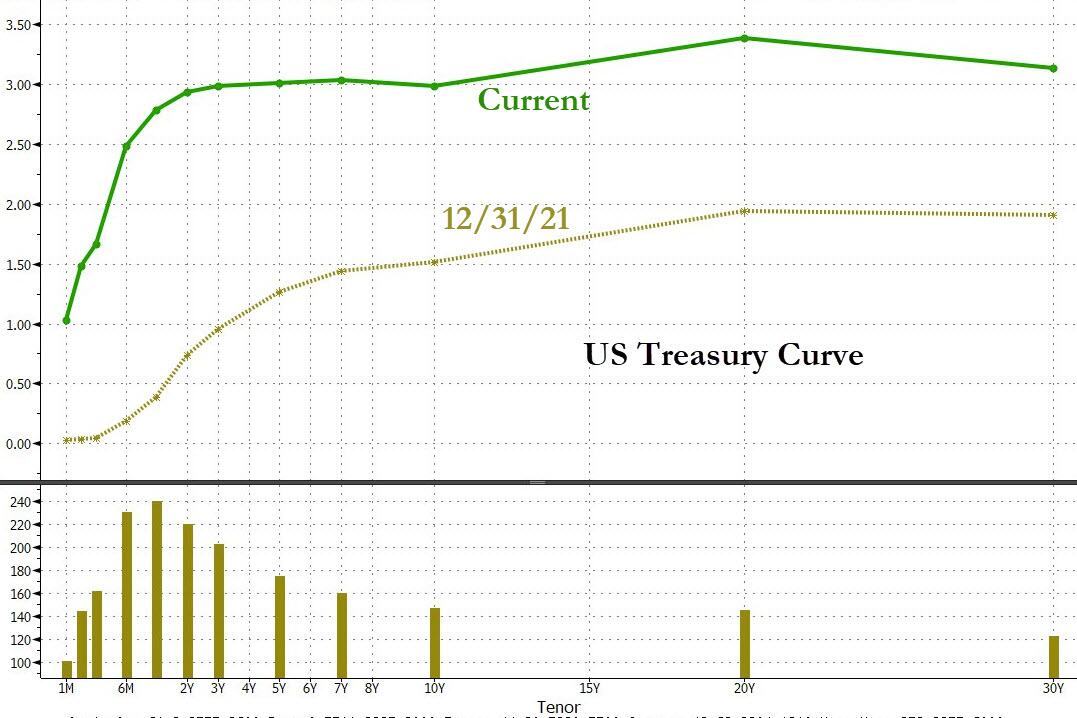

USA 10 YR BOND YIELD: 3.044 DOWN 5 BASIS PTS

USA 30 YR BOND YIELD: 3.182 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 16.67

Stocks, Cryptos Tumble To Close Out Catastrophic First-Half

THURSDAY, JUN 30, 2022 – 07:58 AM

It was supposed to be a 7% ramp into month-end on billions in pension fund residual buying.

Instead, it ended up being more or less the opposite, with crypto-led liquidations dragging futures and global markets lower, and extending Wednesday losses after central bankers issued warnings on inflation and fueled concern that aggressive policy will end with a hard-landing recession, which increasingly more now see as being 2022 business, an outcome that now appears assured especially after yesterday’s disastrous guidance cut from RH, the second in three weeks!

Recession fears and inflation woes may be prolonged by today’s PCE deflator report. The consumer price gauge favored by the Fed may have picked up to 6.4% last month from 6.3%. Personal income growth probably edged up but Bloomberg Economics highlights an anticipated decline in real personal spending as a major worry.

Meanwhile, China’s economy showed further signs of improvement in June with a strong pickup in services and construction, even if the latest Chinese PMI print came slightly below expectations. Also overnight, Russia said it withdrew troops from Ukraine’s Snake Island in the Black Sea after Ukraine said its forces drove Russian troops from the area.

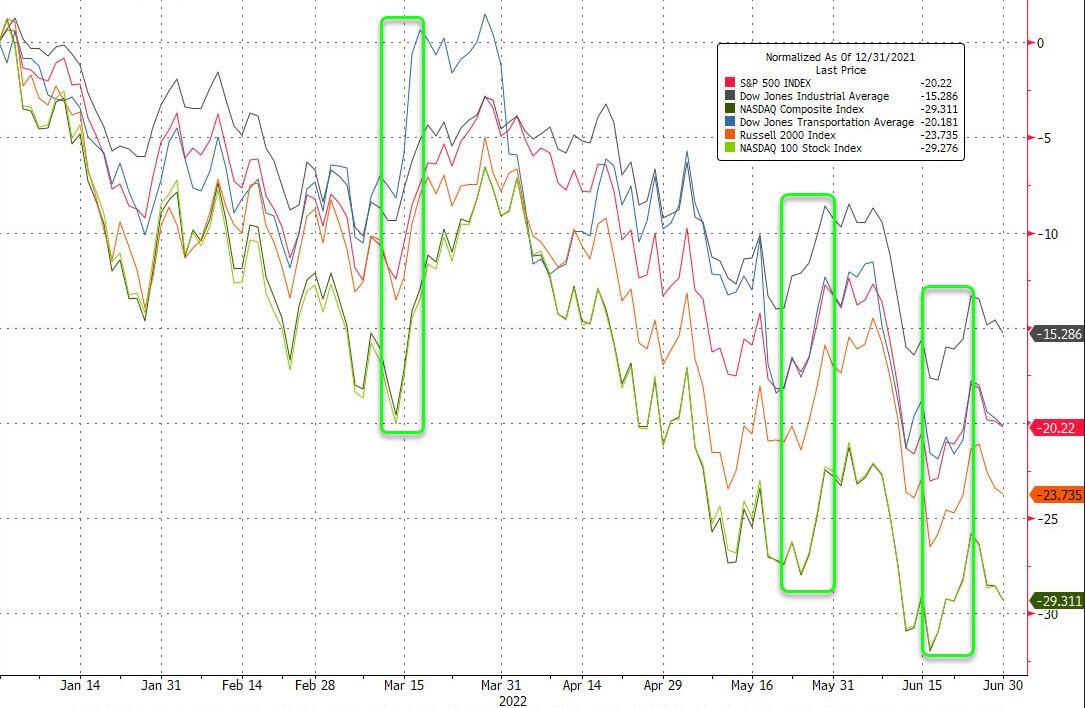

In any case, with zero demand from pensions so far (even though the continued selling in stocks and buying in bonds will only make the imabalnce bigger), overnight Nasdaq 100 contracts dropped 1.8% while S&P 500 futures declined 1.3%, and cryptos crumbled, with bitcoin dragged back below $19000 and Ether on the verge of sliding below $1000. The tech-heavy gauge managed to end Wednesday’s trading slightly higher, while the S&P 500 fell for a third straight day. In Europe, the Stoxx Europe 600 Index slid 1.9%. Treasuries gained, the dollar was steady and gold declined and crude oil futures edged lower again.

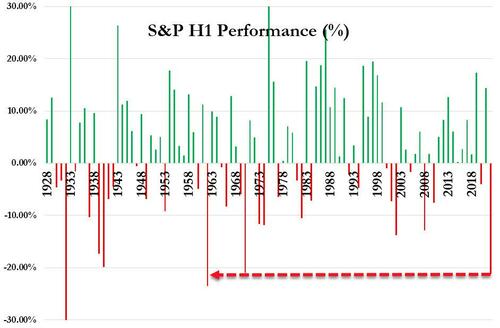

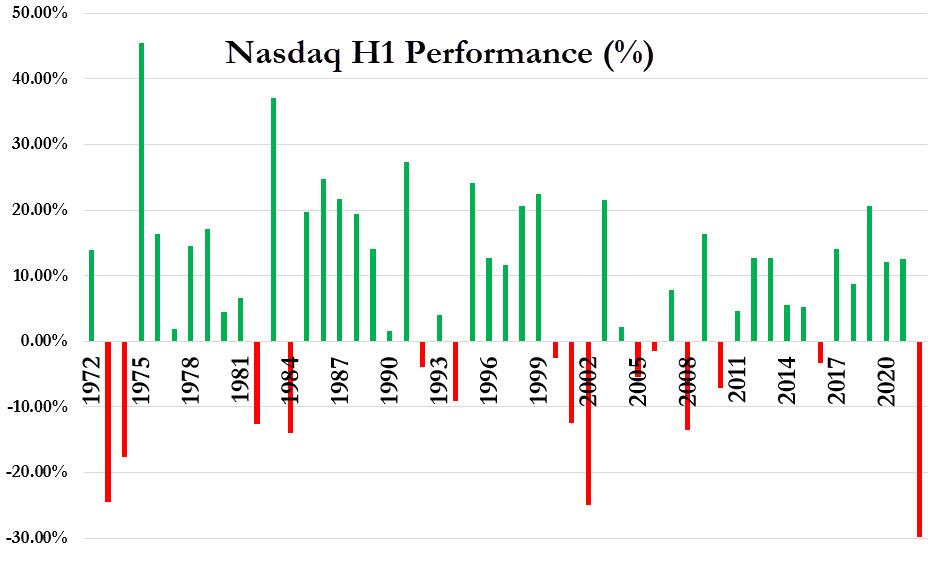

Which brings us to the last trading day of a quarter for the history books: the S&P 500 is set for its biggest 1H decline since 1970 and the Nasdaq 100 since 2002, the height of the dot.com bust. The Stoxx 600 is set for the worst 1H since 2008, the height of the GFC.

Traders have ramped up bets that the global economy will buckle under central bank tightening campaigns — and that policy makers will eventually backpedal. The bond market shifted to price in a half-point rate cut in the Federal Reserve’s benchmark rate at some point in 2023. On Wednesday, during the annual ECB annual forum, Fed Chair Jerome Powell and his counterparts in Europe and the UK warned inflation is going to be longer lasting. A view that central banks need to act fast on rates because they misjudged inflation has roiled markets this year, with global stocks about to close out their worst quarter since the three months ended March 2020.

“Markets are worried about growth as central bankers continue to emphasize that bringing down inflation is their overriding objective, and that it may take time to bring inflation down,” said Esty Dwek, chief investment officer at Flowbank SA. “We still haven’t seen total capitulation in markets, so further downside is possible.”

Meanwhile, the cost of insuring European junk bonds against default crossed 600 basis points for the first time in two years on Thursday.

And speaking of Europe, stocks are also down over 2% in early trading, with all sectors in the red. DAX and CAC underperform at the margin with autos, consumer discretionary and banking sectors the weakest within the Stoxx 600. Here are some of the biggest European movers today:

- Uniper shares slump as much as 23% after the German utility withdrew its outlook and said it was discussing a possible bailout from the German government following Russia’s move to curb natural gas deliveries.

- SAP sinks as much as 6.5% after Exane BNP Paribas downgraded stock to neutral from outperform, saying it sees risks on demand side in the near term as software spending decisions come under increased scrutiny.

- Sanofi shares decline as much as 4.5% after the French drugmaker said the FDA placed late-stage clinical trials of tolebrutinib on partial hold in US because of concerns about liver injuries.

- European semiconductor stocks fell, following peers in the US and Asia lower amid growing concerns that the industry might face a downturn soon as chip stockpiles build. ASML drops as much as 3.4%, Infineon -4.1%, STMicro -3.1%

- Norsk Hydro shares slide as much as 6% amid metals decline and as DNB cuts the stock to sell from hold, citing concerns about rising aluminum supply.

- Stainless steel stocks in Europe fall, with Morgan Stanley saying the settlement on the latest ferrochrome benchmark missed its expectations. Outokumpu shares down as much as 6.6%, Aperam -7.2%, Acerinox -4%

- Saab shares jump as much as 8.4%, after getting an order worth SEK7.3b from the Swedish Defence Materiel Administration for GlobalEye Airborne Early Warning and Control aircraft.

- Orsted shares rise as much as 2.5%, before paring some of the gains. HSBC raises to buy from hold, saying any further downside for the wind farm operator looks limited.

- Bunzl shares rise as much as 2.6% after the specialist distribution company said it now expects very good revenue growth in 2022.

- Grifols shares rise as much as 7.8% after slumping on Wednesday, as the company says that the board isn’t analyzing any capital increase “for the time being.”

Earlier in the session, Asian stocks fell for a second day as tech-heavy indexes in Taiwan and South Korea continued to get pummeled amid concerns over the potential for aggressive monetary tightening in the US to rein in inflation. The MSCI Asia Pacific Index declined as much as 1.2%, dragged down by technology shares including TSMC, Alibaba and Tencent. Taiwan slid more than 2%, while gauges in Japan, South Korea, Australia dropped more than 1%. Stocks in mainland China rose more than 1% after the economy showed further signs of improvement in June with a strong pickup in services and construction as Covid outbreaks and restrictions were gradually eased. Traders are also watching Chinese President Xi Jinping’s trip to Hong Kong, his first time outside of the mainland since 2020.

Asian stocks are struggling to recover from a May low as the threat of higher US rates outweighs China’s emergence from strict Covid lockdowns and its pledge of stimulus measures. While mainland Chinese stocks led gains globally this month, the rest of the markets in the region — especially those heavy with technology stocks and exporters — saw hefty outflows of foreign funds. “Investors continue to assess recession and also inflation risks,” Marcella Chow, JPMorgan Asset Management’s global market strategist, said in an interview with Bloomberg TV. “This tightening path has actually increased the chance of a slower economic growth going forward and probably has brought forward the recession risks.” Asian stocks are set to post a more than 12% loss this quarter, the worst since the one ended March 2020 during the pandemic-induced global market rout.

Japanese stocks declined after the release of China’s data on manufacturing and non-manufacturing PMIs that showed slower than expected improvements. The Topix Index fell 1.2% to 1,870.82 as of market close Tokyo time, while the Nikkei declined 1.5% to 26,393.04. Sony Group contributed the most to the Topix Index decline, falling 3.4%. Out of 2,170 shares in the index, 531 rose and 1,574 fell, while 65 were unchanged. “Although China is recovering from a lockdown, business sentiment in the manufacturing industry is deteriorating around the world,” said Tomo Kinoshita, global market strategist at Invesco Asset Management China’s Economy Shows Signs of Improvement as Covid Eases.

Indian stock indexes posted their biggest quarterly loss since March 2020 as the global equity market stays rattled by high inflation and a weakening outlook for economic growth. The S&P BSE Sensex ended little changed at 53,018.94 in Mumbai on Thursday, while the NSE Nifty 50 Index dropped 0.1%. The gauges shed more than 9% each in the June quarter, their biggest drop since the outbreak of pandemic shook the global markets in March 2020. The main indexes have fallen for all but one month this year as surging cost pressures forced India’s central bank to raise rates twice and tighten liquidity conditions. The selloff is also partly driven by record foreign outflows of more than $28b this year. Despite the turmoil in global markets, Indian stocks have underperformed most Asian peers, partly helped by inflows from local institutions, which made net purchases of more than $30b of local stocks. “Investors worry that the latest show of central bank determination to tame inflation will slow economies rapidly,” HDFC Securities analyst Deepak Jasani wrote in a note. Fourteen of the 19 sector sub-gauges compiled by BSE Ltd. fell Thursday, with metal stocks leading the plunge. The expiry of monthly derivative contracts also weighed on markets. For the June quarter, metal stocks were the worst performers, dropping 31% while information technology gauge fell 22%. Automakers led the three advancing sectors with 11.3% gain.

Australian stocks also tumbled, with the S&P/ASX 200 index falling 2% to close at 6,568.10, weighed down by losses in mining, utilities and energy stocks. In New Zealand, the S&P/NZX 50 index fell 0.8% to 10,868.70

In rates, treasuries advanced, led by the belly of the curve. German bonds surged, led by the short-end and outperforming Treasuries. US yields richer by as much as 5.4bp across front-end and belly of the curve which outperforms, steepening 2s10s, 5s30s by 2bp and 2.8bp; wider bull-steepening move in progress for German curve with yields richer by up to 13.5bp across front-end with 2s10s wider by 3.5bp on the day. US 10-year yields around 3.055%, richer by 3.5bp. Money markets aggressively trimmed ECB tightening bets on relief that French June inflation didn’t come in above the median estimate. Bonds also benefitted from haven buying as stocks slide. Month-end extension flows may continue to support long-end of the Treasuries curve. bunds outperform by 7bp in the sector. IG issuance slate empty so far; Celanese Corp. pushed back plans to issue in euros and dollars, most likely to next week, after deals struggled earlier this week. Focal points of US session include PCE deflator and MNI Chicago PMI.

In FX, the Bloomberg Dollar Spot Index was steady as the greenback traded mixed against its Group-of-10 peers. The yen advanced and Antipodean currencies were steady against the greenback. French inflation quickened to the fastest since the euro was introduced. Steeper increases in energy and food costs drove consumer-price growth to 6.5% in June from 5.8% in May . Sweden’s krona swung to a loss. It briefly advanced earlier after the Riksbank raised its policy rate by 50bps, as expected, signaled faster rate hikes and a quicker trimming of the balance sheet. The pound rose, snapping three days of losses against the dollar. UK household incomes are on their longest downward trend on record, as the nation’s cost of living crisis saps the spending power of British households. Separate figures showed that the current-account deficit widened sharply to £51.7 billion ($63 billion) in the first quarter. The yen rose and the Japan’s bonds inched up. The BOJ kept the amount and frequencies of planned bond purchases unchanged in the July-September period. The Australian dollar reversed a loss after data showed China’s official manufacturing purchasing managers index rose above 50 for the first time since February in a sign of improvement in the world’s second largest economy.

Bitcoin is on track for its worst quarter in more than a decade, as more hawkish central banks and a string of high-profile crypto blowups hammer sentiment. The 58% drawdown in the biggest cryptocurrency is the largest since the third quarter of 2011, when Bitcoin was still in its infancy, data compiled by Bloomberg show.

In commodities, WTI trades a narrow range, holding below $110. Brent trades either side of $116. Most base metals trade in the red; LME zinc falls 3.1%, underperforming peers. Spot gold falls roughly $3 to trade near $1,814/oz. Bitcoin slumps over 6% before finding support near $19,000.

Looking to the day ahead now, data releases include German retail sales for May and unemployment for June, French CPI for June, the Euro Area unemployment rate for May, Canadian GDP for April, whilst the US has personal income and personal spending for May, the weekly initial jobless claims, and the MNI Chicago PMI for June.

Market Snapshot

- S&P 500 futures down 1.2% to 3,775.75

- STOXX Europe 600 down 1.8% to 406.18

- MXAP down 1.0% to 158.01

- MXAPJ down 1.1% to 524.78

- Nikkei down 1.5% to 26,393.04

- Topix down 1.2% to 1,870.82

- Hang Seng Index down 0.6% to 21,859.79

- Shanghai Composite up 1.1% to 3,398.62

- Sensex up 0.2% to 53,136.59

- Australia S&P/ASX 200 down 2.0% to 6,568.06

- Kospi down 1.9% to 2,332.64

- Gold spot down 0.2% to $1,814.91

- US Dollar Index little changed at 105.04

- German 10Y yield little changed at 1.42%

- Euro little changed at $1.0443

- Brent Futures down 0.4% to $115.85/bbl

Top Overnight News from Bloomberg

- The surge in the dollar has set Asian currencies on course for their worst quarter since the 1997 financial crisis and created a dilemma for central bankers

- French Finance Minister Bruno Le Maire said the EU can deliver the global minimum corporate tax with or without the support of Hungary, circumventing Budapest’s veto earlier this month just as the bloc was on the brink of a agreement

- German unemployment unexpectedly rose, snapping 15 straight months of decline as refugees from the war in Ukraine were included in those searching for work

- The SNB bought foreign exchange worth 5.7 billion francs ($5.96 billion) in the first quarter of 2022 as the franc sharply appreciated against the euro and briefly touched parity in March

- The ECB plans to ask the region’s lenders to factor in the economic hit of a potential cut off of Russian gas when considering payouts to shareholders

- European stocks were poised for their biggest drop in any half-year period since 2008, as investors focused on the prospects for economic slowdown and stubbornly high inflation in the region

- New Zealand will enter a recession next year that could be deeper than expected, Bank of New Zealand economists said after a survey showed business sentiment continues to slump

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were varied at month-end amid a slew of data releases including mixed Chinese PMIs. ASX 200 was dragged lower by weakness in energy, miners and the top-weighted financials sector. Nikkei 225 declined after disappointing Industrial Production data and with Tokyo raising its virus infection level. Hang Seng and Shanghai Comp. were somewhat mixed with Hong Kong indecisive and the mainland underpinned after the latest Chinese PMI data in which Manufacturing PMI printed below estimates but Non-Manufacturing PMI firmly surpassed forecasts and along with Composite PMI, all returned to expansion territory.

Top Asian News

- NATO Secretary General Stoltenberg said China’s growing assertiveness has consequences for the security of allies, while he added China is not our adversary, but we must be clear-eyed about the serious challenges it presents.

- US blacklisted 5 Chinese firms for allegedly helping Russia in which Connec Electronic, King Pai Technology, Sinno Electronics, Winnine Electronic and World Jetta Logistics were added to the entity list which restricts access to US technology, according to WSJ.

- Japan’s government cut its assessment of industrial production and noted that production is weakening, while it stated that Japan’s motor vehicle production declined 8% M/M and that industrial production likely saw the largest impact of Shanghai’s COVID-19 lockdown in May, according to Reuters.

- Tokyo metropolitan government will reportedly increase COVID infections level to the second-highest, according to FNN.

It’s been a downbeat session for global equities thus far as sentiment deteriorates further. European bourses are lower across the board, with losses extending during early European hours. European sectors are all in the red but portray a clear defensive bias. Stateside, US equity futures have succumbed to the glum mood, with the NQ narrowly underperforming.

Top European News

- Riksbank hiked its Rate by 50bps to 0.75% as expected, and said the rate will be raised further and it will be close to 2% at the start of 2023. Bank said the balance sheet its to shrink faster than previously flagged, and suggested that policy rate will increase faster if needed. Click here for details.

- Riksbank’s Ingves said inflation over forecast probably not enough for Riksbank to hold extra policy meeting in summer. Ingves added that if the situation requires a 75bps hike, then Riksbank will carry out a 75bps hike.

- Orsted Gains as HSBC Upgrades With Shares Seen ‘Good Value’

- Aston Martin Extends Losses as Carmaker Reportedly Seeking Funds

- Climate Litigants Look Beyond Big Oil for Their Day in Court

- Ukraine Latest: Putin Warns NATO on Moving Military to Nordics

FX

- DXY extends on gains above 105.00, but could see more upside on safe haven demand and residual rebalancing flows over fixes – EUR/USD inches towards 1.0400 to the downside.

- Yen regroups as yields drop and risk sentiment deteriorates to compound corrective price action.

- Franc unwinds some of its recent outperformance and Loonie lose traction from oil ahead of Canadian GDP.

- Swedish Crown unable to take advantage of hawkish Riksbank hike in face of risk aversion – Eur/Sek stuck in a rut close to 10.7000.

- Pound finds some underlying bids into 1.2100 and Kiwi at 0.6200, while Aussie holds above 0.6850 with encouragement from China’s services PMI that also propped the Yuan.

Fixed Income

- Bonds on bull run into month, quarter and half year end – Bunds top 148.00 at best, Gilts approach 113.50 and 10 year T-note just a tick away from 118-00.

- Debt in demand on safe haven grounds rather than duration as curves steepen on less hawkish/more dovish market pricing.

- Italian supply comfortably covered to keep BTP futures propped ahead of US PCE data and yet another speech from ECB President Lagarde.

Commodities

- WTI and Brent front-month futures are resilient to the broader risk downturn, and firmer Dollar as OPEC+ member members gear up for what is expected to be a smooth meeting.

- Spot gold is uneventful but dipped under yesterday’s low, with potential support at the 15th June low at USD 1,806.59/oz.

- Base metals are softer across the board amid the broader risk profile. Dalian and Singapore iron ore futures were on track for quarterly losses.

- Ship with 7,000 tonnes of grain leaves Ukraine port, according to pro-Russia officials cited by AFP.

US Event Calendar

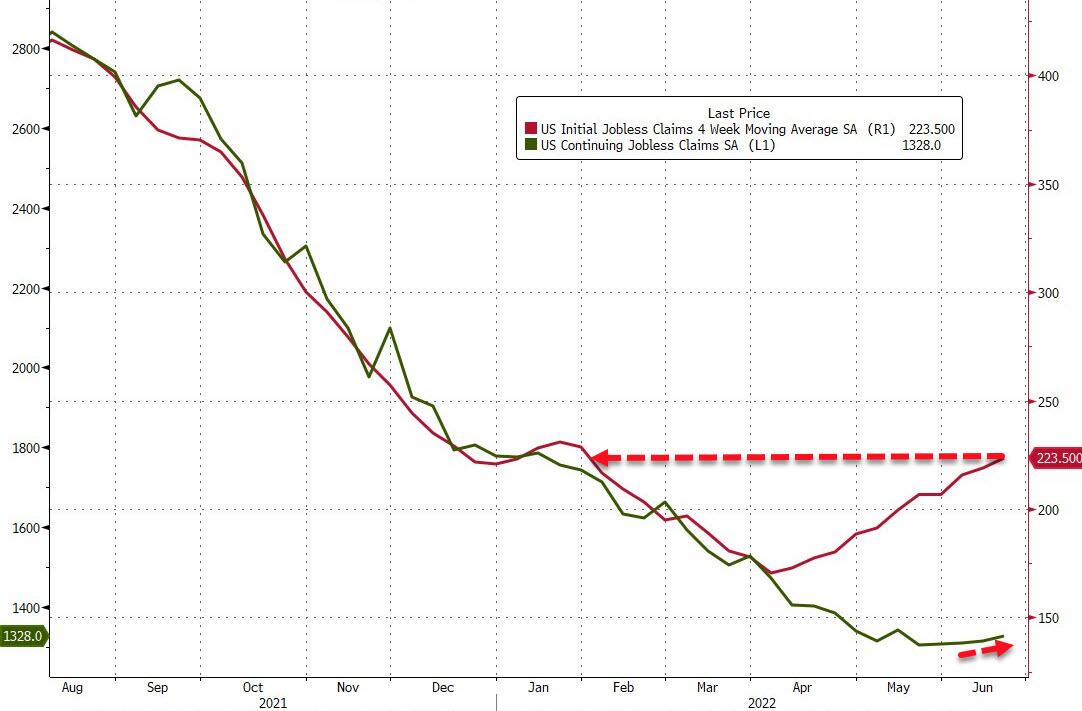

- 08:30: June Initial Jobless Claims, est. 229,000, prior 229,000

- 08:30: June Continuing Claims, est. 1.32m, prior 1.32m

- 08:30: May Personal Income, est. 0.5%, prior 0.4%

- 08:30: May Personal Spending, est. 0.4%, prior 0.9%

- 08:30: May Real Personal Spending, est. -0.3%, prior 0.7%

- 08:30: May PCE Deflator MoM, est. 0.7%, prior 0.2%

- 08:30: May PCE Deflator YoY, est. 6.4%, prior 6.3%

- 08:30: May PCE Core Deflator YoY, est. 4.8%, prior 4.9%

- 08:30: May PCE Core Deflator MoM, est. 0.4%, prior 0.3%

- 09:45: June MNI Chicago PMI, est. 58.0, prior 60.3

DB’s Jim Reid concludes the overnight wrap

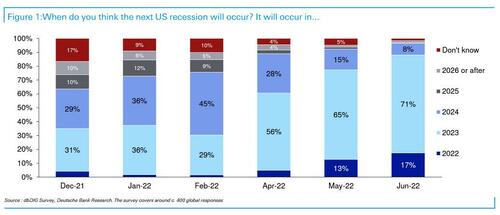

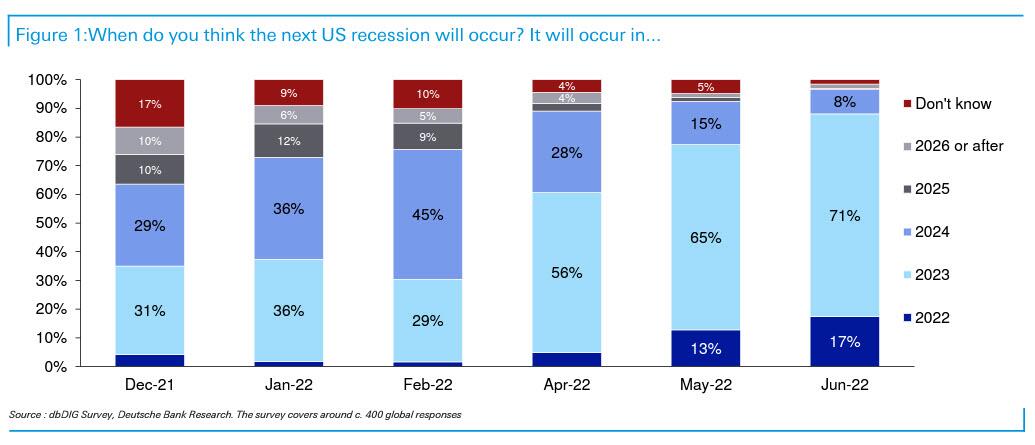

We’ve just released the results of our monthly EMR survey that we conducted at the start of the week. It makes for some interesting reading, and we’re now at the point where 90% of respondents are expecting a US recession by end-2023, which is up from just 35% in our December survey. That echoes our own economists’ view that we’re going to get a recession in H2 2023, and just shows how sentiment has shifted since the start of the year as central banks have begun hiking rates. When it comes to people’s views on where markets are headed next, most are expecting many of the themes from H1 to continue, with a 72% majority thinking that the S&P 500 is more likely to fall to 3,300 rather than rally to 4,500 from current levels, whilst 60% think that Treasury yields will hit 5% first rather than 1%. Click here to see the full results.

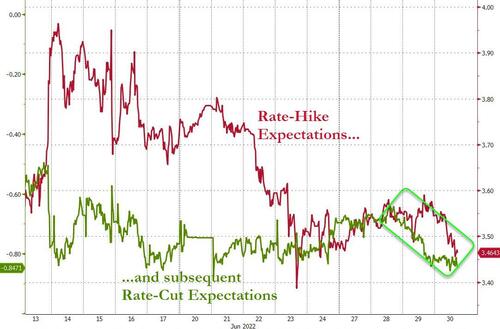

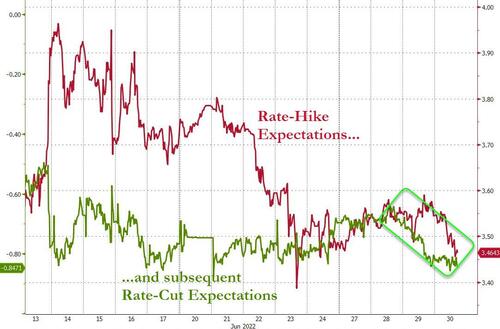

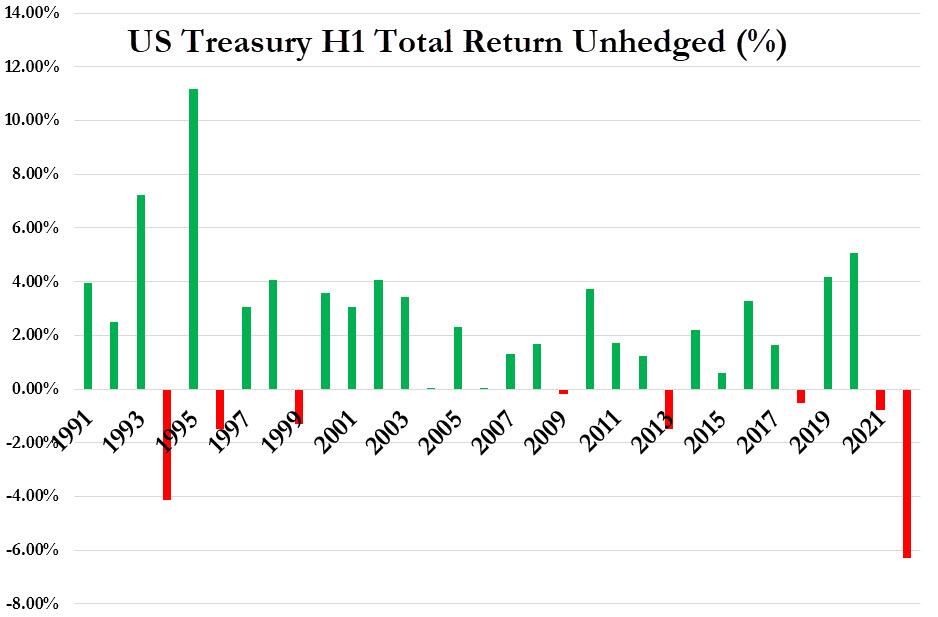

When it comes to negative sentiment we’ll have to see what today brings us as we round out the first half of the year, but if everything remains unchanged today we’re currently set to end H1 with the S&P 500 off to its worst H1 since 1970 in total return terms. And there’s been little respite from bonds either, with US Treasuries now down by -9.79% since the start of the year, so it’s been bad news for traditional 60/40 type portfolios. Ultimately, a large reason for that has been investors’ fears that ongoing rate hikes to deal with inflation will end up leading to a recession, and yesterday saw a continuation of that theme, with Fed Chair Powell, ECB President Lagarde and BoE Governor Bailey all reiterating their intentions in a panel at the ECB’s Forum to return inflation back to target.

In terms of that panel, there weren’t any major headlines on policy we weren’t already aware of, although there was a collective acknowledgement of the risk that inflation could become entrenched over time and the need to deal with that. Fed Chair Powell described the US economy as in “strong shape”, but one that ultimately requires much tighter financial conditions to bring inflation back to target. Year-end fed funds expectations remained steady in response, down just -0.7bps to 3.45%. However, further out the curve the simmering slower growth narrative continued to grip markets and sent 10yr Treasury yields -8.2bps lower to 3.09%, and the 2s10s another -1.1bps flatter to 4.7bps. In line with a tighter Fed policy path and slower growth, 10yr breakevens drove the move in nominal yields, falling -8.2bps to 2.39%, their lowest levels since January, having entirely erased the gains seen after Russia’s invasion of Ukraine, when it peaked above 3% at one point in April. Along with 2s10s flattening, the Fed’s preferred measure of the near-term risk of recession, the forward spread (the 18m3m – 3m), similarly flattened by -5.7bps, hitting its lowest level in nearly four months at 154bps. And thismorning there’s only been a partial reversal of these trends, with 10yr Treasury yields (+1.3bps) edging back up to 3.10% as we go to press. Over in equities, the S&P 500 bounced around but finished off of its intraday lows with just a -0.07% decline, again with the macro view likely skewed by quarter-end rebalancing of portfolios. The NASDAQ was similarly little changed on the day, falling a mere -0.03%.

In terms of the ECB, President Lagarde said on that same panel that she didn’t think “we are going back to that environment of low inflation” that was present before the pandemic. But when it came to the actual data yesterday there was a pretty divergent picture. On the one hand, Spain’s CPI for June surprised significantly on the upside, with the annual inflation rising to +10.0% (vs. +8.7% expected) on the EU’s harmonised measure. But on the other, the report from Germany then surprised some way beneath expectations, coming in at +8.2% on the EU-harmonised measure (vs. +8.8% expected). So mixed messages ahead of the flash CPI print for the entire Euro Area tomorrow.

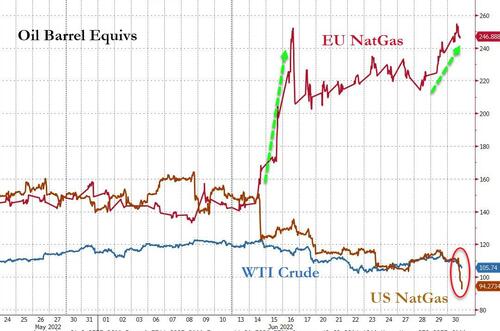

As in the US, there was a significant rally in European sovereign bonds, with yields on 10yr bunds (-10.7bps), OATs (-10.7bps) and BTPs (-16.0bps) all moving lower on the day. Equities also lost significant ground amidst the risk-off tone, and the STOXX 600 shed -0.67% as it caught up with the US losses from the previous session. That risk-off tone was witnessed in credit as well, where iTraxx Crossover widened +21.5bps to a post-pandemic high. At the same time, there were further concerns in Europe on the energy side, with natural gas futures up by +8.06% to a three-month high of €139 per megawatt-hour, which follows a reduction in capacity yesterday at Norway’s Martin Linge field because of a compressor failure.

Whilst monetary policy has been the main focus for markets lately, we did get some headlines on the fiscal side yesterday too, with a report from Bloomberg that Senate Democrats were working on an economic package that had smaller tax increases in order to reach a deal with moderate Democratic senator Joe Manchin. For reference, the Democrats only have a majority in the split 50-50 senate thanks to Vice President Harris’ tie-breaking vote, so they need every Democrat Senator on board in order to pass legislation. According to the report, the plan would be worth around $1 trillion, with half allocated to new spending, and the other half cutting the deficit by $500bn over the next decade.

Overnight in Asia we’ve seen a mixed market performance overnight. Most indices are trading lower, including the Nikkei (-1.45%) and the Kospi (-0.81%), but Chinese equities have put in a stronger performance after an improvement in China’s PMIs in June, and the CSI 300 (+1.62%) and the Shanghai Comp (+1.31%) have both risen. That came as manufacturing activity expanded for the first time in four months, with the PMI up to 50.2 in June (vs. 50.5 expected) from 49.6 in May. At the same time, the non-manufacturing climbed to 54.7 points in June, up from 47.8 in May, which also marked the first time it’d been above the 50 mark since February.

Nevertheless, that positivity among Chinese equities are proving the exception, with equity futures in the US and Europe pointing lower, with those on the S&P 500 (-0.28%) looking forward to a 4th consecutive daily decline as concerns about a recession persist.

When it came to other data yesterday, the third estimate of US GDP for Q1 saw growth revised down to an annualised contraction of -1.6% (vs. -1.5% second estimate). Separately, the Euro Area’s M3 money supply grew by +5.6% year-on-year in May (vs. +5.8% expected), which is the slowest pace since February 2020.

To the day ahead now, data releases include German retail sales for May and unemployment for June, French CPI for June, the Euro Area unemployment rate for May, Canadian GDP for April, whilst the US has personal income and personal spending for May, the weekly initial jobless claims, and the MNI Chicago PMI for June.

THURSDAY /WEDNESDAY NIGHT

SHANGHAI CLOSED UP 37.10 PTS OR 1.10% //Hang Sang CLOSED DOWN 137.10 PTS OR 0.62% /The Nikkei closed DOWN 411.56 OR 1.54% //Australia’s all ordinaires CLOSED DOWN 1.97 /Chinese yuan (ONSHORE) closed DOWN 6.7002 /Oil DOWN TO 108.28 dollars per barrel for WTI and DOWN TO 111.98 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7002 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7073: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

end

3c CHINA

CHINA

Drones are becoming a major component for China’s war machine

(EpochTimes)

China’s War Machine Is Betting The Future On Drones

WEDNESDAY, JUN 29, 2022 – 11:40 PM

By Andrew Thornebrooke of the Epoch Times

A swarm of drones flies through the night sky over the Pacific.

Shrouded in darkness and less than 100 miles from the California coastline, they go in groups of fours and sixes, stalking U.S. Navy vessels. They whir about over the ships’ bows, gathering intelligence to deliver to faceless masters.

They match the speed of the naval vessels, flying unimpeded in low visibility for as long as four hours at a time. The alarmed crews of the ships have no idea where they came from or what their purpose is.

This is not the plot of an up-and-coming spy thriller, but a series of actual events that took place in July 2019.

The chilling encounters raised alarms throughout the Navy and brought forth an investigative apparatus composed of elements of the U.S. Navy, Coast Guard, and FBI. Members of the Joint Chiefs of Staff and the commander of the Pacific Fleet were kept primed with updates on the situation.

“If the drones were not operated by the American military, these incidents represent a highly significant security breach,” said one investigative report based on the ships’ logs.

Yet, the nature of the drones, where they came from, and who deployed them remained a mystery for more than two years.

However, a new investigative report published by The Drive in June shed light on the incidents, which totaled at least eight encounters involving several unmanned aerial vehicles (UAVs) that were previously referred to simply as UFOs in the press.

The report, based on Navy materials newly obtained through multiple Freedom of Information Act requests, pinpoints the launching point of the drones as a civilian bulk carrier operating in the area at the time. That ship, the MV Bass Strait, is owned and operated by Pacific Basin, flagged out of Hong Kong.

“The Navy assessed that the commercial cargo ship was likely conducting surveillance on Navy vessels using drones,” the report said. During its first-ever operational voyage, the ship may have been linked to previously unknown incidents in March and April 2019, including “intelligence collection operations” targeting the USS Zumwalt, America’s most advanced surface combatant.

“Active surveillance of key naval assets is being conducted in areas where they train and employ their most sensitive systems, often within close proximity to American shores,” the report said.

China’s Growing Drone Force