by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1801.50 DOWN $5.45

SILVER: $19.74 DOWN 61 CENTS

ACCESS MARKET: GOLD $1809.95

SILVER: $19.89

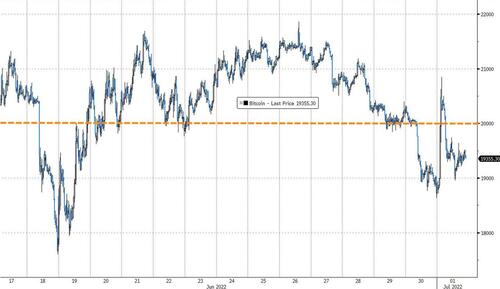

Bitcoin morning price: $19,153 UP 227

Bitcoin: afternoon price: $19,400. UP 474

Platinum price: closing DOWN $15.70 to $888.90

Palladium price; closing UP $31.85 at $1962.05

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE:EXCHANGE:EXCHANGE: COMEX

CONTRACT: JULY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,804.100000000 USD

INTENT DATE: 06/30/2022 DELIVERY DATE: 07/05/2022

FIRM ORG FIRM NAME ISSUED STOPPED

357 C WEDBUSH 8

365 H ED&F MAN CAPITA 4

435 H SCOTIA CAPITAL 2

657 C MORGAN STANLEY 8

661 C JP MORGAN 368 354

685 C RJ OBRIEN 5

690 C ABN AMRO 1 24

737 C ADVANTAGE 19 26

800 C MAREX SPEC 7 11

905 C ADM 7 6

TOTAL: 425 425

MONTH TO DATE: 768

EXCHANGE: COMEX

no. of contracts issued by JPMorgan: 354/425

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT 425 NOTICE(S) FOR 42,500 Oz//1.3219 TONNES)

total notices so far: 768 contracts for 76800 oz (2.3888 tonnes)

SILVER NOTICES:

141 NOTICE(S) FILED 7,05,000 OZ/

total number of notices filed so far this month 1638 : for 8,190,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $5.45

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD//

INVENTORY RESTS AT 1050.31 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 61 CENTS

AT THE SLV// ://SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 553,000 OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 540.709 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A VERY STRONG SIZED 1616 CONTRACTS TO 139,925 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.41 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.41) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SOME SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A POOR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.220 MILLION OZ FOLLOWED BY TODAY’S 340,000 OZ EFP JUMP TO LONDON / // V) STRONG SIZED COMEX OI GAIN

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -1138

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTACTS for 1 days, total 500 contracts: 2.500 million oz OR 2.5MILLION OZ PER DAY. (500 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 2.5 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 2.5 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1616 DESPITE OUR $0.41 LOSS IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 500 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S EFP JUMP TO LONDON OF 340,000 OZ // .. WE HAD A VERY STRONG SIZED GAIN OF 2116 OI CONTRACTS ON THE TWO EXCHANGES FOR 10.580 MILLION OZ DESPITE THE LOSS IN PRICE..

WE HAD 141 NOTICES FILED TODAY FOR 705,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 2467 CONTRACTS TO 495,832 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: —7097 CONTRACTS.

.

THE SMALL SIZED DECREASE IN COMEX OI CAME WITH OUR FALL IN PRICE OF $9.20//COMEX GOLD TRADING/THURSDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JULY AT 2.914 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 8400 OZ

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $9.20 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 3506 OI CONTRACTS 10.905 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5973 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 502,929

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,603, WITH 4630 CONTRACTS INCREASED AT THE COMEX AND 5973 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 10,603 CONTRACTS OR 32.979TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5973) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (2467,): TOTAL GAIN IN THE TWO EXCHANGES 3506 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JULY. AT 2.914 TONNES 3) ZERO LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) SMALL SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

5973 CONTRACTS OR 597,300 OZ OR 32.979 TONNES 1 TRADING DAY(S) AND THUS AVERAGING: 5973 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES: 32.979 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 32.979/3550 x 100% TONNES 0.929% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 2238.13 TONNES FINAL

JULY: 32.979 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A VERY STRONG SIZED 1616 CONTRACT OI TO 139,925 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 2725 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 500 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 500 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1616 CONTRACTS AND ADD TO THE 500 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED GAIN OF 2116 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 10.580 MILLION OZ

OCCURRED DESPITE OUR FALL IN PRICE OF $0.41 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED DOWN 10.98 PTS OR 0.32% //Hang Sang CLOSED /The Nikkei closed DOWN 457.42 OR 1.73% //Australia’s all ordinaires CLOSED DOWN 0.39 /Chinese yuan (ONSHORE) closed DOWN 6.7096 /Oil DOWN TO 107.98 dollars per barrel for WTI and DOWN TO 111.76 for Brent. Stocks in Europe OPENED MOSTLY RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7096 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7113: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 2467 CONTRACTS TO 499,832 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR LOSS OF $9.20 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (5973 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY.. THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5973 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :5973 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5973 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3506 CONTRACTS IN THAT 5973 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI LOSS OF 2467 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $4.25.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JULY (3.1797),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 3.1797 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $9.20) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A FAIR SIZED GAIN OF 10.905 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR JULY (2.914 TONNES)…

WE HAD -7097 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 10,603 CONTRACTS OR 1,060,300 OZ OR 32.979 TONNES

Estimated gold volume 278,012/// fair/

final gold volumes/yesterday 230,782 /fair

INITIAL STANDINGS FOR JULY ’22 COMEX GOLD //JULY 1

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 97,617.421 oz Brinks Int. Delaware JPMorgan includes2696 kilobars//Brinks |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | 24,581.842 oz HSBC |

| No of oz served (contracts) today | 425 notice(s) 42500 OZ 1.3219 TONNES |

| No of oz to be served (notices) | 253 contracts 25,300 oz 0.7869 TONNES |

| Total monthly oz gold served (contracts) so far this month | 768 notices 76,800 OZ 2.3888 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

1 customer deposit

i) Into HSBC 24,581.842 oz

total deposits: 24,581.842 oz

3 customer withdrawals:

i) Brinks: 86,679.09 oz

ii) JPMorgan 10,616.821 oz

iii) Int. Delaware: 321.510 oz (10 kilobars)

total withdrawal: 97,617.421 oz

ADJUSTMENTS:3 all dealer to customer

Brinks 2849.366 oz

JPMorgan 302.303 oz

Manfra: 64,628.510 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 678 contracts losing 259 contracts from yesterday. We had

343 notices filed on Thursday so we gained 84 contracts or an additional 8400 oz will stand in this non active

delivery month of July.

August has a LOSS OF 3945 contracts UP to 397,521 contracts

We had 425 notice(s) filed today for 42500 oz FOR THE July 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 368 notices were issued from their client or customer account. The total of all issuance by all participants equate to 425 contract(s) of which 354 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2022. contract month,

we take the total number of notices filed so far for the month (768) x 100 oz , to which we add the difference between the open interest for the front month of (JULY 678 CONTRACTS ) minus the number of notices served upon today 425 x 100 oz per contract equals 102,100 OZ OR 2.914 TONNES the number of TONNES standing in this active month of JUly.

thus the INITIAL standings for gold for the JULY contract month:

No of notices filed so far (768) x 100 oz+ (678) OI for the front month minus the number of notices served upon today (425} x 100 oz} which equals 102,100 oz standing OR 3.1797 TONNES in this active delivery month of JULY.

TOTAL COMEX GOLD STANDING: 3.1797 TONNES (A FAIR STANDING FOR A JULY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,419,784.828 oz 75.26 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 32,989.550.8 OZ

TOTAL ELIGIBLE GOLD: 15,877,907.178 OZ

TOTAL OF ALL REGISTERED GOLD: 17,111,643.639 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 14,691,859.0 OZ (REG GOLD- PLEDGED GOLD)

END

SILVER/COMEX/JULY 1

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,522,159.820 oz Brinks Int Delaware JPMorgan Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,988,014.647ozCNT Delaware JPMorgan |

| No of oz served today (contracts) | 141CONTRACT(S)705,000 OZ) |

| No of oz to be served (notices) | 1338 contracts (6,690,000 oz) |

| Total monthly oz silver served (contracts) | 1638 contracts 8,190,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We have 3 deposits into the customer account

i) Into CNT: 284m291.861 oz

ii) Into Delaware 5079.386 oz

iii0 Into JPMorgan: 1,698,643.471 oz

total deposit: 1,988,014.647 oz

JPMorgan has a total silver weight: 171.727 million oz/337.321 million =50.90% of comex

Comex withdrawals: 4

i) Out of Brinks 370,852.600 oz

ii) out of Int. Delaware 167,586.840 oz

iii) Out of JPMorgan 791,827.510 oz

iv) Out of Manfra: 191,892.860 oz

total withdrawal 1,522,159.820 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 69.331 MILLION OZ

TOTAL REG + ELIG. 337,321 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JULY OI: 1479 CONTRACTS HAVING LOST 1565. WE HAD 1497 NOTICES FILED

YESTERDAY, SO WE LOST 68 CONTRACTS OR 340,000 OZ WERE E.F.P.’d TO LONDON

AUGUST LOST 3 CONTRACTS TO STAND AT 1437

SEPTEMBER HAD A GAIN OF 2783 CONTRACTS UP TO 116,995 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 141 for 7,05,000 oz

Comex volumes:74.575// est. volume today// good

Comex volume: confirmed yesterday: 65,349 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 1638 x 5,000 oz = 8,190000 oz

to which we add the difference between the open interest for the front month of JULY(1479) and the number of notices served upon today 141 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY./2022 contract month: 1638 (notices served so far) x 5000 oz + OI for front month of JULY (1479) – number of notices served upon today (141) x 5000 oz of silver standing for the JULY contract month equates 14,880,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JULY 1/WITH GOLD DOWN $5.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES//INVENTORY RESTS AT 1050.31 TONNES

JUNE 30/WITH GOLD DOWN $9.20: big CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 1052.63 TONNES//

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

JUNE 21/WITH GOLD DOWN $2.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1075.54 TONES

JUNE 17/WITH GOLD DOWN $11.25: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.60 TONNES INTO THE GLD.///INVENTORY RESTS AT 1075.54 TONNES

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

GLD INVENTORY: 1050.31 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 1/WITH SILVER DOWN 61 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ//INVENTORY RESTS AT 540.709 MILLION OZ//

JUNE 30/WITH SILVER DOWN 41 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 738,000 OZ FROM THE SLV//INVENTORY RESTS AT 541.262 MILLION OZ//

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

JUNE 21/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 547.166 MILLION OZ//

JUNE 17/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 739,000 OZ FROM THE SLV./:INVENTORY RESTS AT 543.660 MILLION OZ/

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

CLOSING INVENTORY 540.709 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg

-END-

END

3. Chris Powell of GATA provides to us very important physical commentaries

Views on gold/recognizing financial repression

USA gold/GATA

USAGold’s ‘News & Views’ letter for July is published

Submitted by admin on Thu, 2022-06-30 11:37 Section: Daily Dispatches

11:34a ET Thursday, June 30, 2022

Dear Friend of GATA and Gold:

USAGold’s “News & Views” letter for July, published today, contains its usual collection of insightful observations about the financial markets and especially gold, some of them recognizing “financial repression” and the like. It’s posted in the clear here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

»

END

Your weekend reading material

(Alasdair Macleod/GATA)

Alasdair Macleod: Inflation, recession, and new currencies

Submitted by admin on Thu, 2022-06-30 12:50Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, June 30, 2022

Central bankers are trying to steer markets away from higher interest rates, citing growing evidence of the harm they are doing to economic growth. Quantitative tightening is dead on arrival.

Predictably — because it is a repetitive cycle — bank credit is beginning to contract. But contracting bank credit is associated with periodic systemic crises. The credit contraction crisis promises to be even worse than the Lehman failure and any that came before it. And because central banks are sure to protect financial asset values from collapsing, their currencies are likely to suffer instead. Being entirely fiat, unbacked by legal money, currencies are dependent entirely on the public faith in a financial system that lacks the backing of real money.

We are all rapidly drifting onto the rocks that sank John Law in 1720. Central bankers, like John Law with his Mississippi bubble, are prioritising support for financial asset values over their currencies, which is what interest rate suppression is all about. Just as Law’s fiat livres rapidly became worthless, so will today’s fiat currencies.

Therefore, for self-protection, it is time to fully understand the difference between legal money, fiat currency, and the importance of bank credit.

Central banks refuse public access to legal money, which is their gold reserves. Nor is access demanded by the investment establishment, which has thrived on monetary inflation. Instead, there is a developing debate about collapsing currencies being backed by commodities instead. This article puts these developments into context. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/inflation-recession-and-new-currencies

END

USA dollar’s share of FX reserves steady in Q1 but euro’s share falls

(zerohedge)

U.S. dollar’s share of FX reserves steady in Q1, euro’s share falls

Submitted by admin on Thu, 2022-06-30 13:14Section: Daily Dispatches

By Gertrude Chavez-Dreyfuss

Reuters

via U.S. News and World Report, Washington

Thursday, June 30, 2022

NEW YORK — The U.S. dollar’s share of currency reserves reported to the International Monetary Fund was 58.8% in the first quarter, unchanged from that of the last three months of 2021, IMF data showed on Thursday.

The greenback remains the largest-held currency reserve by global central banks.

The euro’s share, however, slipped to 20% in the first quarter from 20.6% in the previous three months. In 2009, the euro hit its highest share at 28%.

Global reserves, which are reported in U.S. dollars, are assets of central banks held in different currencies used primarily to support their liabilities. Central banks sometimes use reserves to help support their respective currencies.

“The (IMF) data is not a major surprise after what happened in Ukraine … The dollar only got stronger and the euro got weaker, and I suspect those trends will not change much in the near term,” said Kenneth Broux, an FX strategist at Societe Generale in London. …

… For the remainder of the report:

END

For your interest..

(Comtois/Franklin Templeton Investments/ChrisPowell/GATA)

Invest ‘responsibly’ in gold under rules set by the market’s riggers, the LBMA and JPMorgan

Submitted by admin on Thu, 2022-06-30 22:32Section: Daily Dispatches

Accprding to the fund’s prospectus —

https://www.franklintempleton.com/forms-literature/download/FGLD_P

— the fund’s gold custodian is JPMorgan in London, its gold is not insured, only “authorized participants” and not ordinary shareholders may redeem shares for metal, and the fund’s initial authorized participant is JPMorgan Securities. How responsible!

Franklin Templeton Launches Franklin Responsibly Sourced Gold ETF

By James Comtois

Franklin Templeton Investments

San Mateo, California

Thursday, June 30, 2022

Franklin Templeton today announced the launch of the Franklin Responsibly Sourced Gold ETF (NYSE Arca: FGLD). FGLD seeks to reflect the performance of the price of gold bullion, less the expense of fund operations, and is priced at 15 basis points. The shares will trade on NYSE Arca.

The fund defines “responsibly sourced gold” as London Good Delivery gold bullion bars that were refined on or after January 1, 2012, which have been refined in accordance with London Bullion Market Association’s Responsible Gold Guidance. The LBMA’s Responsible Gold Guidance establishes minimum requirements that are mandatory along the entire gold supply chain for all Good Delivery refiners wishing to trade with the London bullion market, intended to ensure, among other things, that London Good Delivery gold is mined through verified supply chains that meet certain internationally recognized ethical standards.

“We are excited to offer FGLD as one of the most cost-effective gold ETFs in the market,” said David Mann, head of global exchange traded funds capital markets, in a news release. “We believe it’s a fantastic option for investors looking to add gold investments to their portfolios, offering a compelling way to participate in the physical gold market, with the added peace of mind of knowing that this gold is responsibly sourced.”: …

… For the remainder of the announcement:

END

Raging USA inflation is far worse than we are being told according to Daily Mail’s Puzder and Jim Talent

(zerohedge)

Andy Puzder and Jim Talent: Raging U.S. inflation is far worse than we’re being told

Submitted by admin on Thu, 2022-06-30 22:52Section: Daily Dispatches

By Andy Puzder and Jim Talent

Daily Mail, London

Thursday, June 30, 2022

The outlook for the U.S. economy is bad and potentially getting worse.

Today the Commerce Department released new consumer spending numbers showing that the prices Americans are paying for goods and services climbed 6.3% over the past year, as inflation maintained its upward momentum.

Just 24 hours earlier, Federal Reserve Chairman Jerome Powell warned, yet again, that his efforts to rein in runaway price increases by raising interest rates may plunge the nation into recession.

And he said it’s worth the risk.

“The bigger mistake to make — let’s put it that way — would be to fail to restore price stability,” he said at the European Central Bank’s annual economic policy conference in Portugal.

Prior to that revised GDP numbers showed the US economy contracted even more than initially reported in the first quarter of the fiscal year, as more consumers opted to save instead of spending their hard-earned dollars.

Now what if we told you that America’s economic outlook is even darker than that?

What if we told you that the dire statistics splashed across the headlines and your TV screens don’t even come close to accurately describing the reality?

Well, buckle up — because that’s what we’re telling you. …

… For the remainder of the commentary:

END

4. OTHER GOLD COMMENTARIES

“I’m A Fan Of Gold” – Seth Klarman Supports ‘Prudent’ Positioning As Goldman Hikes Precious Metal Price Target

FRIDAY, JUL 01, 2022 – 01:28 PM

Gold broke down this morning below $1800, losing its modest gains for the year (but still outperforming bonds, stocks, and crypto YTD). This move comes amid geopolitical chaos, monetary policy uncertainty (rate-cut expectations soaring), and recession fears growing.

Nevertheless, Baupost’s Seth Klarman said in his latest note to investors that:

“I’m a fan of gold. I think gold’s valuable in a crisis.”

And we suspect few believe we are not in crisis currently.

So why has gold been hammered, and what happens next?

Goldman’s Mikhail Sprogis and his commodities research team believe a ‘wealth shock’ has subdued Gold’s rally and raised their target price for the precious metal to $2500.

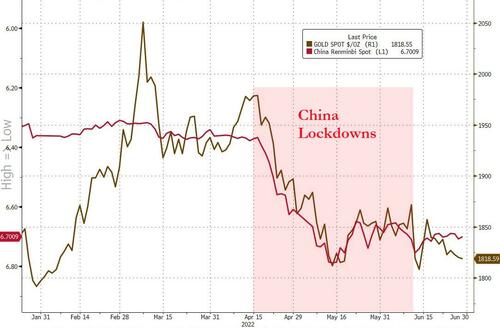

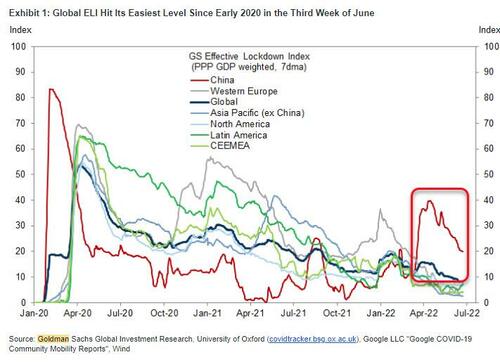

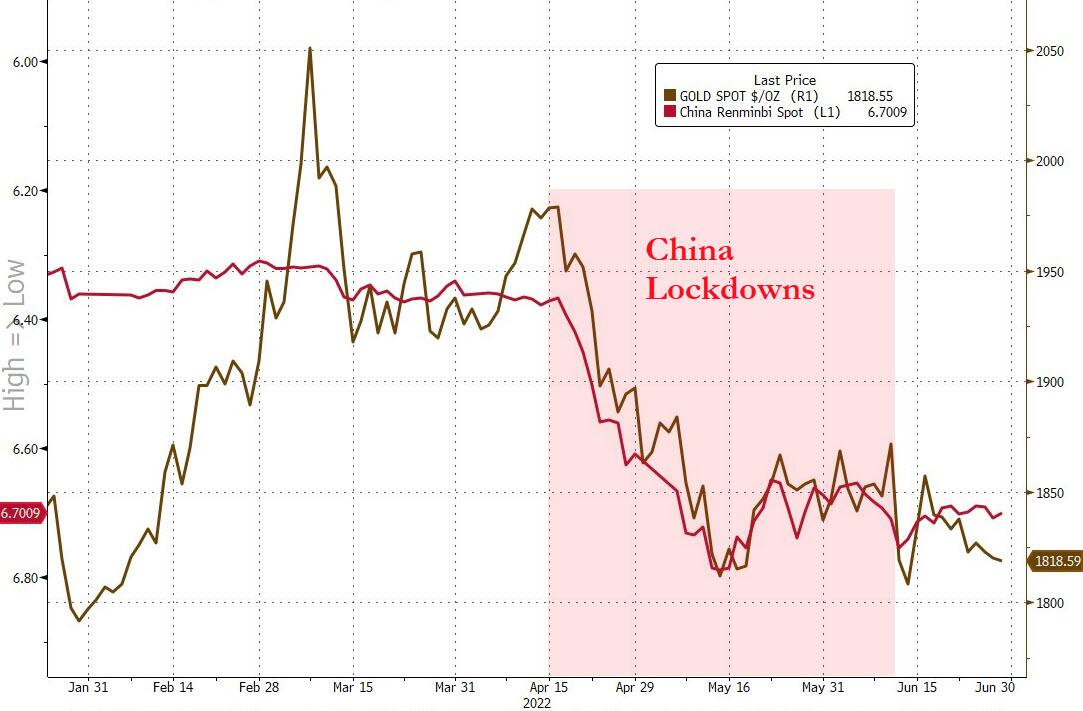

While it is tempting to blame gold’s recent weakness on a lack of investment demand due to higher US rates, we view gold’s sell-off this quarter as in line with a weaker CNY and primarily reflecting the impact of lockdowns on the Chinese economy.

There is little doubt to us that Chinese lockdowns had a large impact on spot gold demand in China, with gold jewelry sales falling by 30% YoY in April. The re-introduction of Chinese lockdowns represented a significant hit to the Chinese economy and the PBOC allowed for some CNY depreciation to ease financial conditions. As the CNY dropped, gold followed it lower.

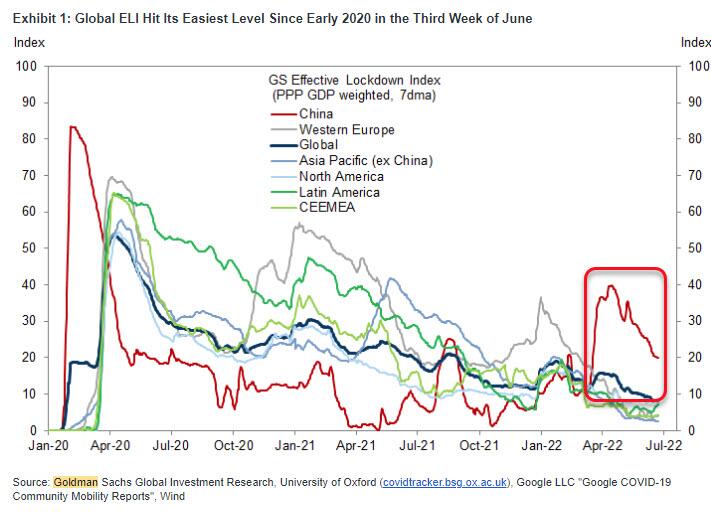

The positive news is that lockdowns are easing in China…

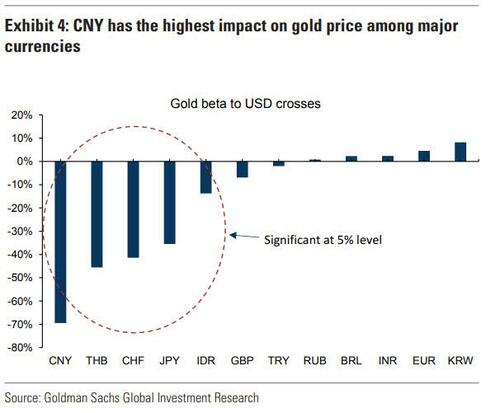

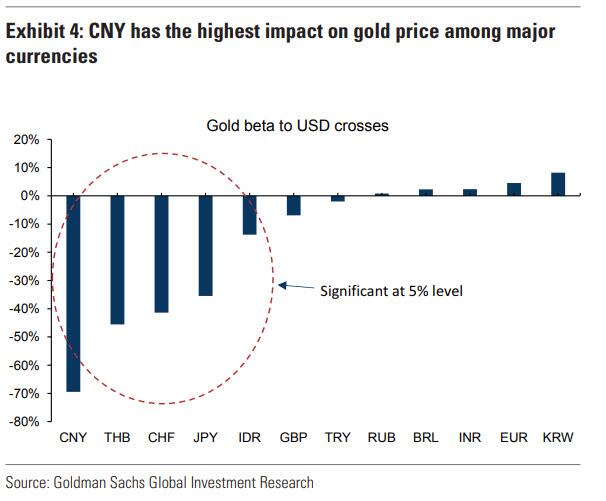

This is not surprising since we find that, historically, the CNY has the largest impact on gold among major currencies…

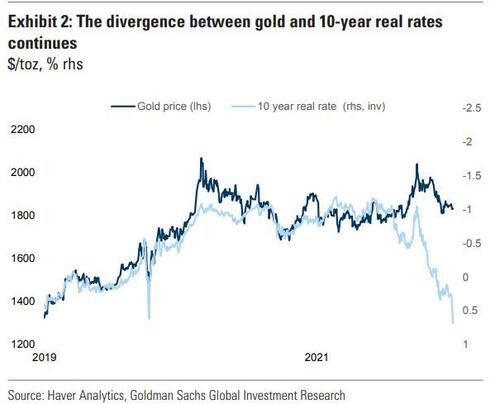

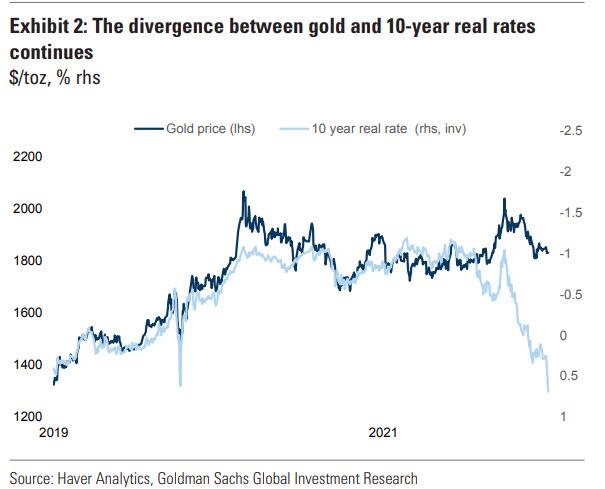

This negative Wealth effect for gold was amplified by a liquidation of short-term-oriented futures and ETF positions,which are very sensitive to trends in the dollar. In turn, the gold real rates correlation remains broken as higher real rates now go hand-in-hand with greater ‘Fear’ of a DM recession which is, on net, positive for gold investment demand, in our view.

Reversal of the Wealth shock will allow focus to shift back to Fear and geopolitical drivers: We believe that the Wealth shock to gold will reverse as China is gradually coming out of lockdowns with growth set to receive a boost from policy support.

In addition, an increasing lack of confidence in a US soft landing should boost Fear demand for gold.

Any transparency on Russian gold purchases should raise the market’s conviction on an upcoming structural geopolitical boost to CB gold demand.

In essence, we believe the bullish gold case was merely delayed rather than derailed. Due to little structural change to our model inputs, we keep our gold price upside but delay the price path.

Finally, we see gold ETF purchases resuming now that the speculative part of the positioning has been cleaned up. The risk to this view would be a continuation of the wealth/liquidity shock until its magnitude matches March 2020 or October 2008. This could lead to a temporary fall in the gold price as market participants cut all positions to increase their dollar liquidity and meet margin calls.

We revise our 3, 6 and 12m targets to $2,100/2,300 and $2,500/toz, from $2,300/2,500 and $2,500/toz.

Finally we circle back to Seth Klarman’s insights:

“If the world turns to hell, the war expands and gets worse, God forbid a nuclear weapon is used, I think people are going to say: ‘How do I know what anything’s worth anymore? I’m going to make sure I have some gold because I don’t want to not have money at a time of desperation.’ It may never come to that, but I think it’s prudent to have a little bit of your portfolio in gold.”

“The market has come to believe in an omniscient Federal Reserve, and it’s no such thing. These guys don’t really know what they’re doing in any deep way. It’s a giant financial experiment, and we’re at the mercy of their experiment that maybe is right now in the process of going wrong, so God help us.”

God help us, indeed!

end

Gold Price Sinks Through $1800 as India Hikes Bullion Import Duty

Friday, 7/01/2022 14:13

GOLD PRICES sank Friday in Asian and London trade, dropping through $1800 per ounce following news of a sharp hike to bullion import duty in No.2 consumer nation India and hitting 5-month lows against a rising US Dollar even as longer-term interest rates fell hard and global stock markets dropped for the 4th session running.

With equities now erasing most of mid-June’s rally from 18-month lows on the MSCI World Index, the yield offered to new buyers of 10-year US Treasury debt fell back below 3.00%.

That was a record low for Washington’s borrowing costs when first reached during the global financial crisis of 2008, and it was a 3.5-year high when recovered this May amid the surge of inflation hitting 1982 levels.

Now lagging inflation by almost 8 percentage points but “attacking” the cost of living with its steepest single rate-hike in 3 decades, the Federal Reserve is “just at the beginning” of a hiking cycle said voting member Loretta Mester this week, backing another 75 basis points rise in the Fed’s short-term interest rate at its July meeting.

Gold prices today fell through $1800 per ounce to reach $1785, the lowest bullion rate since the end of January and almost 14% beneath the near-record high reached in early March after Russia invaded Ukraine.

Chart of gold bullion priced in US Dollars. Source: BullionVault

Shares in major Indian jewellers meantime lost 6% and more for the day after the Finance Ministry in Delhi reversed 2021’s surprise cut to gold import duty – a move aimed at cutting the growth of gold smuggling – and took the levy back up to 12.5%.

Finance Minister Nirmala Sitharaman also imposed export taxes on crude oil and diesel on Friday, aiming to boost domestic energy supplies amid “extraordinary times” which have seen the Rupee sink to fresh all-time lows on the currency market.

Including GST sales duty, “Overall taxes on gold now rise sharply from 14% to around 18.45%,” according to Somasundaram PR, regional CEO for India at the mining- industry’s World Gold Council.

“Unless this is tactical and temporary, [it] will likely strengthen the grey market, with long term adverse consequences for [India’s] gold market.”

India’s legal gold imports jumped to more than 100 tonnes in May, the highest in a year, helping the country’s trade deficit widen to a new all-time record as global investors also pulled money out of what the IMF’s GDP forecasts will be the fastest-growing major economy in 2022.

“Gold smuggling was falling after the duty reduction and because of Covid-19 curbs on movement of people,” says a Mumbai bullion dealer speaking to Reuters. “But now it could rise again.”

With domestic Indian prices rising today following the import duty hike, gold bullion fell against most other major currencies, hitting 1-month lows in Euro terms at €1715 but holding unchanged for the week in UK Pounds at £1487 as Sterling sank yet again on the FX market.

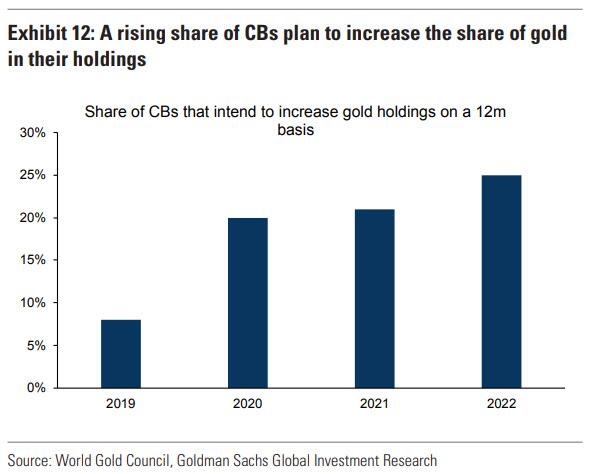

The Reserve Bank of India has been the world’s heaviest central-bank gold buyer over the last 2 years, adding more than 106 tonnes to its holdings, beating Thailand (90 tonnes), Hungary (63), Brazil (62) and Egypt (45).

The Central Bank of Iraq this week said it has added 34 tonnes to its gold reserves so far this summer, a rise of 35% taking its total to 130 tonnes – inside the top 30 central-bank hoards worldwide.

Across the Gulf of Arabia, the Central Bank of Qatar also grew its gold bullion holdings on the latest data, adding more than 4 tonnes to reach nearly 56 in total.

5.OTHER COMMODITIES

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7096

OFFSHORE YUAN: 6.7113

HANG SANG CLOSED

2. Nikkei closed DOWN 457.42 OR 1.73%

3. Europe stocks CLOSED MOSTLY RED

USA dollar INDEX UP TO 104.88/Euro FALLS TO 1.0446

3b Japan 10 YR bond yield: FALLS TO. +.208/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 135.23/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

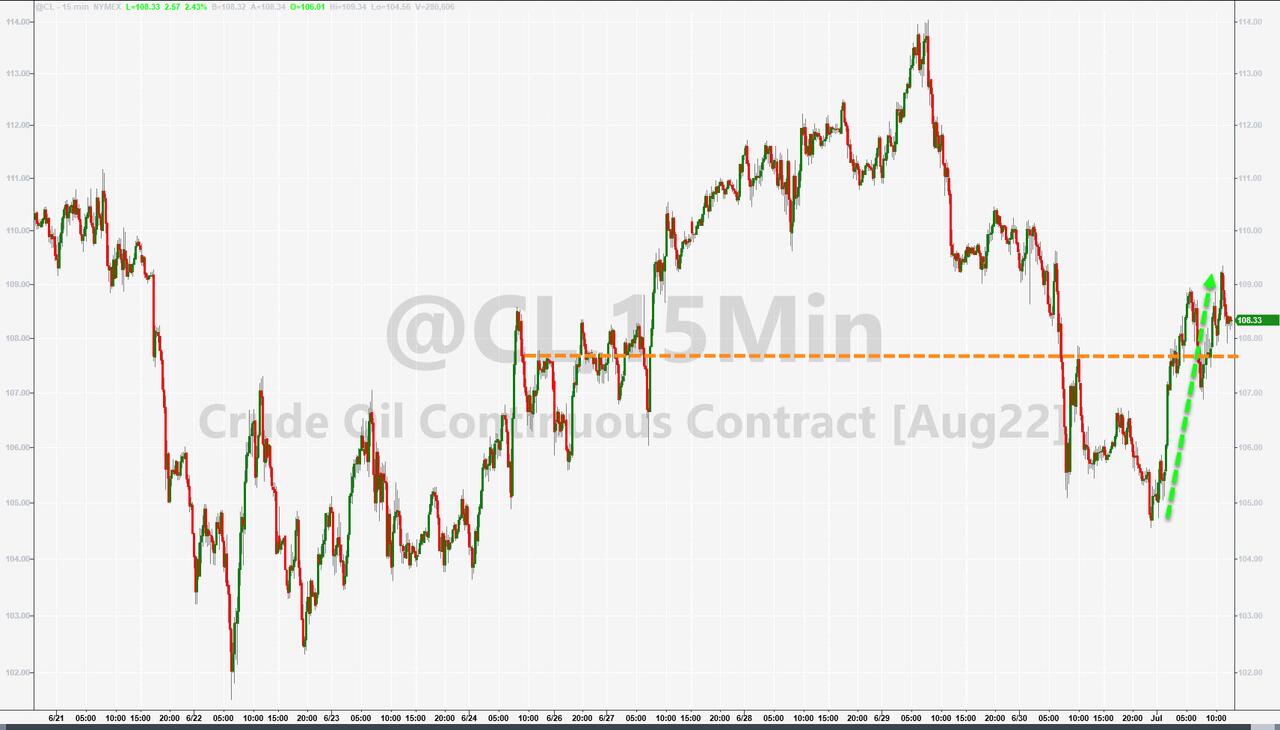

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.301%/Italian 10 Yr bond yield FALLS to 3.30% /SPAIN 10 YR BOND YIELD FALLS TO 2.37%…

3i Greek 10 year bond yield RISES TO 3.53//

3j Gold at $1789.15 silver at: 19.64 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 3 AND 1/4 roubles/dollar; ROUBLE AT 54.68

3m oil into the 107 dollar handle for WTI and 111 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 135.23DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9601– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0031well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.948 DOWN 3 BASIS PTS

USA 30 YR BOND YIELD: 3.149 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 16.75

Futures, Yields Slide In Recessionary Start To New Quarter

FRIDAY, JUL 01, 2022 – 11:57 AM

As DB’s Jim Reid puts it “if you want the good news this morning it’s that H1 is now finally over. If you want the bad news it’s that there’s not much good news around as we start H2 and US equity futures are already down around a percent in the first few hours of the new half year. “

Indeed, just when you thoughts stocks couldn’t possibly slide any more after just concluding the worst first half in 52 years…

… and with investor and consumer sentiment at record lows, you’d be shocked to learn that futures and stocks started the new month and quarter by plumbing fresh lows as fears of soaring inflation and tumbling earnings boosted concerns about an imminent recession, and the resulting risk aversion lifted bonds and havens and sent risk sliding. The “Big Short” Michael Burry said we may only be about halfway through the market’s decline…

Adjusted for inflation, 2022 first half S&P 500 down 25-26%, and Nasdaq down 34-35%, Bitcoin down 64-65%.

That was multiple compression. Next up, earnings compression. So, maybe halfway there.— Cassandra B.C. (@michaeljburry) June 30, 2022

… while Goldman was also downbeat, seeing global equities selling off further in the near term. As of 730am, S&P 500 and Nasdaq 100 pointed to declines of 0.3%, having shaved off as much as a 1% drop earlier…

… while 10-year US Treasury yield slid below 3% to the lowest since early June as markets now price in a record 10bps in rate cuts in Q1 2023 with markets confident the Fed will have to pivot to defeat the coming recession. Every Group-of-10 currency fell against the dollar and the yen, traditional havens, while bitcoin reversed a modest attempt at a breakout that briefly pushed it back over $20K.

In premarket trading, shares of US chip companies fell after Micron Technology issued a downbeat forecast on weaker demand for phones and computers. Bank stocks are also lower in premarket trading, putting them on track for their fifth straight day of losses amid a broader slump in equity markets. Other notable premarket movers:

- Kohl’s (KSS US) plunges 15% in US premarket trading after CNBC reported it’s ending sale talks with Vitamin Shoppe owner Franchise Group.

- Semiconductor companies are falling on Friday after Micron Technology issued a weak forecast for the current quarter due to lower demand for phones and computers. Micron (MU US) -5.5%, Nvidia -1.3% (NVDA US), Qualcomm (QCOM US) -0.7%.

- Cryptocurrency-exposed stocks could be active again on Friday as Bitcoin dip buyers are triggering a rally for the largest digital token. Riot Blockchain (RIOT US), Marathon Digital (MARA US) edge up 2.4% and 2.6%, respectively, in premarket.

- XPeng (XPEV US) burning cash in the short-term is unavoidable, Nomura says in a note that downgrades the Chinese EV maker to neutral from buy. Shares down 0.2% premarket.

Risk assets continued to be the target of sellers Friday as recession worries overtake concern about runaway inflation. With Federal Reserve policymakers resolute on getting price growth back to their 2% target, investors are assessing the hit to the economy from harsh rate hikes.

“Inflation is the key focus of central bankers; investors losing money is way down their list of concerns,” Chris Iggo, chief investment officer at AXA IM Core, wrote in a note to clients. “Interest rate and inflation markets are taking the view that what is priced in terms of monetary tightening will be enough to bring inflation down, but in order for that to happen, there also needs to be a cost to growth.”

Meanwhile, both stocks and bonds were rocked by outflows this week, reflecting investor fears about hawkish central bank policy. About $5.8 billion exited global stock funds in the week through June 29, Bank of America said, citing EPFR Global data. Bonds had redemptions of $17 billion. Separately, global companies have pulled more debt sales in the past six months than in all of 2020. More than 70 deals have been postponed or canceled so far in 2022, according to data compiled by Bloomberg.

In Europe, markets reversed sharp opening losses with the Stoxx 600 briefly turning green before sliding 0.5% lower with retail and utility names supporting on the recovery. Bund yields rose after data showed euro-area inflation hit a fresh record, surpassing expectations. Here are some of the biggest European movers today:

- European airlines rise on Friday, paring some declines from previous sessions, as oil is headed for the third straight weekly drop on concerns that a potential recession will hurt demand. Wizz Air rises as much as +10%, EasyJet +6.2%, British Airways owner IAG +4.4%

- Airbus shares rise as much as 4% after BofA analysts led by Benjamin Heelan added the aircraft manufacturer to the bank’s ‘3Q Best Ideas list,’ according to a note.

- SBB shares advance as much as 21.5% Friday, its largest intra-day gain since April 2017, after the company was included in Nasdaq Stockholm’s OMXS30 index.

- Sodexo shares gain as much as 5.6%, the most since April 8, after the French caterer reported 3Q revenue that beat the average analyst estimate. Morgan Stanley says Friday’s update is a “relief.”

- Maersk shares rise as much as 3.0% after JPMorgan upgraded the stock to overweight from neutral and placed it and Kuehne Nagel on their “positive Catalyst Watch” for Q2, citing increased confidence in the longevity of current earnings.

- European semiconductor stocks tumble after US memory- chip maker Micron 4Q outlook fell short of analyst expectations and said the industry demand environment has weakened. Chipmaker Infineon falls as much as 5.0%, ASML drops 4.9%

- La Francaise des Jeux shares decline as much as 9.0% after Citi cuts the stock to sell from buy, citing concession fee to be paid that is worse than Street expectations.

- Craneware declines as much as 12% after an offering of ~1.2m shares by holder Abry Partners VII priced at 1,600p, a 13% discount to last close.

- OVH Groupe shares drop as much as 6.5% after the analysts adjusted their estimates amid a softening demand outlook.

Earlier in the session, Asian stocks declined for a third day, as traders assessed recession risks in the global economy after weak US consumer spending and soft factories data from the region. Investors are also keeping an eye on developments from the Chinese President’s Hong Kong visit. The MSCI Asia Pacific Index slid as much as 1.1%, adding to nearly 2% weekly loss, weighed down by tech and consumer discretionary stocks. Chipmakers including TSMC and Samsung extended their declines, contributing the most to the measure’s loss along with Australian miner BHP and Indian energy giant Reliance. Taiwan’s benchmark was again the region’s notable underperformer as it is on course for a bear market following more than a 20% fall from its January high, dragged down by technology stocks. Equity benchmarks in Japan and South Korea slipped more than 1%. Stocks in mainland China retreated after meandering between gains and losses while Hong Kong was closed for a holiday as its new chief was sworn in by Chinese President Xi Jinping. A further slide in June purchasing managers’ indexes in Asian countries except China and the drop in US consumer spending for the first time this year in May highlighted the fragile foundation of the world economy. Those data dimmed global economic outlook and further dented investor sentiment already weakened by ongoing worries about global central banks’ aggressive rate hikes to fight inflation.

“Overall, weakened US consumer spending will lead to a drop in global demand. It will affect export-dominated markets like South Korea in particular,” said Cui Xuehua, a China equity analyst at Meritz Securities in Seoul. “Traders are also looking to see if there will be policies benefiting Hong Kong, such as a re-opening of borders and increased trade” as Xi visits Hong Kong. Asian stocks plunged about 18% during the first half of this year, capping the first six months with the worst annual drop since 2008. Asian equities have struggled to rebound from a low in May as global recession worries and aggressive tightening by central banks triggered heavy outflows of funds from emerging markets. Chinese stocks have remained a bright spot last month as Beijing winds down its stringent virus restrictions and investors expected regulatory and monetary support for key sectors.

In Australia, the S&P/ASX 200 index fell 0.6% for the week, as the risk-sensitive Australian and New Zealand dollars slumped to their lowest levels in two years amid ongoing recession worries that boosted haven assets. After a late sell-off Friday, shares swung to a loss of 0.4% to close at 6,539.90, driven by declines in energy and material stocks, with a group of mining shares hitting the lowest since Nov. 22 following commodity price drops. In New Zealand, the S&P/NZX 50 index fell 1.1% to 10,753.16

In FX, the Bloomberg Dollar Spot Index rose by around 0.3% as the greenback traded stronger against all of its Group-of-10 peers apart from the yen. Australian and New Zealand dollars plunged to new two-year lows. The euro fluctuated around $1.0450 after the latest data showed that euro-area consumer prices rose 8.6% from a year earlier in June — up from 8.1% in May. Economists surveyed by Bloomberg saw a gain of 8.5%. The yen rose and the nation’s bonds were steady to higher. One-week options in dollar-yen are once again overpriced as short-term risks make a strong case for long-gamma exposure. Bank of Japan’s quarterly Tankan report of confidence among Japan’s large manufacturers fell to 9 in June from 14 three months ago, the biggest drop since the peak of the pandemic.

In rates, the German curve bear-steepened, with long-end yields ~7bps cheaper after a manufacturing PMIs show notable softness in new orders. Cash Treasuries extended Thursday’s bull steepening move, with front-end and belly dropping over 10bp from prior day’s close while richer by ~4bps at the short end. Ten-year yields fell further to below 3%, breaching the 50-day moving average, while eurodollar strip bull flattens as recession risk and Fed rate cuts continue to be priced in for next year. 10-year yields dropped to as low as 2.937%, the lowest since June 6, before edging back above 2.95% in early US session, outperforming bunds by 5.5bps. The belly and front-end outperformance causing a steepening of 5s30s curve by 6bp on the day and 2s10s by 3bps; 5s30s peaks through 20bp and onto widest levels in a month. Two-year yield fell 10bp to 2.85%. The Eurodollar strip continues to bull flatten as rate hike premium is eased out of next year; Dec22/Dec23 spread drops to -63.5bp and fresh cycle lows. German government benchmark yields rose after data showed euro-area inflation hit a fresh record, surpassing expectations. The Stoxx Europe 600 Index wavered between losses and gains. Gilts are relatively quiet. Most peripheral spreads are modestly wider to core.

In commodities, crude futures advance. WTI drifts 1.9% higher to trade near $107.73. Brent rises 2% near $111.23. Most base metals are in the red. LME copper briefly drops below $8,000 a ton for the first time since February 2021. Spot gold falls roughly $12 to trade near $1,795/oz.

Looking to the day ahead, data releases include the flash Euro Area CPI reading for June, as well as June’s global manufacturing PMIs and the ISM manufacturing reading from the US, along with the UK’s mortgage approvals for May. From central banks, we’ll hear from the ECB’s Panetta and De Cos.

Market Snapshot

- S&P 500 futures down 0.4% to 3,774.25

- MXAP down 1.0% to 156.37

- MXAPJ down 1.0% to 519.11

- Nikkei down 1.7% to 25,935.62

- Topix down 1.4% to 1,845.04

- Hang Seng Index down 0.6% to 21,859.79

- Shanghai Composite down 0.3% to 3,387.64

- Sensex down 0.6% to 52,688.97

- Australia S&P/ASX 200 down 0.4% to 6,539.91

- Kospi down 1.2% to 2,305.42

- STOXX Europe 600 little changed at 407.16

- German 10Y yield little changed at 1.39%

- Euro down 0.2% to $1.0459

- Brent Futures up 0.8% to $109.95/bbl

- Gold spot down 0.7% to $1,794.17

- US Dollar Index up 0.26% to 104.95

Top Overnight News from Bloomberg

- The Bank of Japan’s decision to pass up an opportunity to ramp up its policy defenses points to a fear of triggering a further weakening of the embattled yen

- Japan’s state pension fund, the world’s largest, posted its first quarterly loss in two years as declines in global stock and bond markets during the three months through March weighed down the value of its assets

- After years of subdued price swings caused by central bank intervention, a key gauge of volatility in the 1 quadrillion yen ($7.4 trillion) government bond market has surged in recent weeks to the highest level since 2008. That’s boosting demand for JGB traders, with Nomura Holdings Inc. noting signs of intensifying competition for talent

- Copper sank below $8,000 a ton, hitting its lowest since early 2021, as deepening fears about a global economic slowdown drive a rout in industrial metals markets

- Chinese President Xi Jinping urged Hong Kong to shore up its economy after an era of “chaos,” in a landmark visit that offered few clear answers for how to balance Beijing’s demands for limiting perceived foreign threats with its desire to remain an international financial hub

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks began the new trading month mostly in the red as the region digested a slew of data releases and amid headwinds from the US where Consumer Spending data disappointed and Atlanta Fed’s GDPnow model alluded to a recession. ASX 200 was just about kept afloat by resilience in nearly all industries aside from the commodity-related sectors. Nikkei 225 fell beneath the 26,000 level after the latest Tankan survey mostly disappointed. Shanghai Comp. traded indecisively despite the stronger than expected Caixin Manufacturing PMI data which rose to its highest since May 2021 as sentiment in the mainland was constrained by falling commodity prices, as well as the absence of Hong Kong participants and Stock Connect flows.

Top Asian News

- Chinese President Xi said “one country, two systems” has been successful for Hong Kong over the past 25 years and said Hong Kong is a window and a bridge connecting the mainland to the world, while he added that Hong Kong has to defend against interference and focus on development, according to Bloomberg and Reuters.

- Hong Kong’s new Chief Executive Lee was sworn in and stated the National Security Law brought stability after chaos, while he added the government will strive to control and manage COVID-19 through scientific methods, according to Reuters.

- UK PM Johnson said China has been failing to comply with its commitments on Hong Kong and the UK intends to do all it can to hold China to account, according to Reuters.

- PBoC injected CNY 10bln via 7-day reverse repos with the rate at 2.10% for a CNY 50bln net daily drain, according to Reuters.

- World’s Top Pension GPIF Posts Quarterly Loss on Stock Rout

- Three Arrows Crypto Fund CEO Wants to Sell Singapore Mansion

- Kishida Says LNG Supply From Sakhalin Won’t Immediately Stop

- Japan Mulls LNG From Spot Market to Replace Russian Supply: METI

European bourses are back in the red after briefly recovering from opening losses. Sectors are mixed with no clear theme – Tech is the laggard and Utilities the outperformer. Chip stocks are after sources said TSMC has seen its major clients adjust downward their chip orders for the rest of 2022, whilst Micron’s guidance was underwhelming. Stateside, US equity futures remain in negative territory but off worst levels as the contracts coat-tail on some of Europe’s upside.

Top European News

- French government spokesperson said a possible cabinet reshuffle could take place Monday or Tuesday, according to Reuters.

- Euro-Zone Inflation Hits Record in Boost for Big-Hike Calls

- Food Inflation Gets a Break as Wheat, Corn and Soy Oil Tumble

- UK House Sales Slow as ‘Intense’ Market Starts to Cool

FX

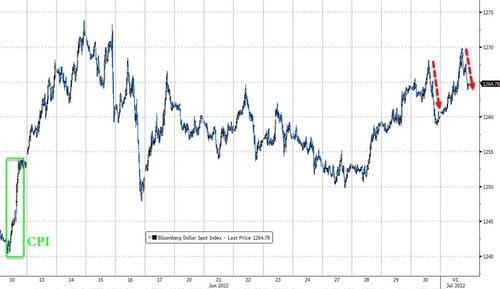

- Dollar regroups after late month end fade amidst broad gains ahead of US manufacturing ISM and construction spending – DXY retests 105.000+ levels from 104.640 low yesterday.

- Yen bucks trend, but off recovery peaks as yields firm up and risk aversion wanes – Usd/Jpy around 135.500 vs 134.74 overnight base.

- Aussie underperforms and hits fresh 2022 trough sub-6800 and Kiwi under 0.6200 after decline in ANZ consumer sentiment.

- Pound undermined by downward revision to UK manufacturing PMI with Cable below 1.2100 and prone to test of Fib support if 1.2050 breached.

- Euro back on 1.0400 handle and propped by better than forecast Eurozone manufacturing PMIs and stronger than expected inflation metrics.

- Rand extends declines alongside Gold as SA power and pay issues rumble on – Usd/Zar above 16.3400, spot bullion below Usd 1800/oz.

Fixed Income

- Debt futures rack up more safe haven gains before recovery in risk sentiment and sharp reversal.

- Bunds recoil from 149.46 to 148.24, Gilts retreat to 113.79 from 114.52 and 10 year T-note pulls back from 118-29+ to 118-06 as benchmark yield retests 3% briefly.

- Bonds subsequently bounce off lows awaiting US manufacturing ISM and construction spending ahead of long Independence Day holiday weekend.

Commodities

- WTI and Brent front-month futures retrace some of yesterday’s losses with upside also spurred the recovery across the stock markets

- Libya’s NOC announced a force majeure over Es Sider, Ras Lanuf Ports and the El Feel oilfield, while it noted that oil production decreased as daily exports ranged between 365-408k BPD which is a decline of 865k BPD, according to Reuters.

- Spot gold is under pressure after the yellow metal breached USD 1,800/oz to the downside – with the next level to the downside at USD 1,786/oz, the May 16th low.

- Base metals are softer across the board as recession woes grapple with the risk-correlated market. LME 3M copper briefly fell beneath the USD 8,000/t for the first time since January.

- India raised the basic import tax on gold to 12.5% from 7.5%, according to BQ Prime citing a Gazette notification.

US Event Calendar

- 09:45: June S&P Global US Manufacturing PM, est. 52.4, prior 52.4

- 10:00: May Construction Spending MoM, est. 0.4%, prior 0.2%

- 10:00: June ISM Manufacturing, est. 54.5, prior 56.1

DB’s Jim Reid concludes the overnight wrap

If you want the good news this morning it’s that H1 is now finally over. If you want the bad news it’s that there’s not much good news around as we start H2 and US equity futures are already down around a percent in the first few hours of the new half year. Having said that it’s eminently possible that whatever age you are reading this you might ALL have now witnessed the worst first half of a year in your career either looking back or forward. So if you’ve survived that it might not all be bad news. Younger readers can come back to me after the awful H1 2055 and tell me I’m wrong.

Henry will put out some more stats in our usual month-end performance review shortly, which reads like a bit of a horror story, but for what it’s worth the S&P 500 has now seen its worst H1 total return performance in 60 years, and also in total return terms it’s fallen for two consecutive quarters for the first time since the GFC. Meanwhile 10yr Treasuries look set (with a final calculation imminent) to have recorded their worst H1 since 1788, just before George Washington became President.

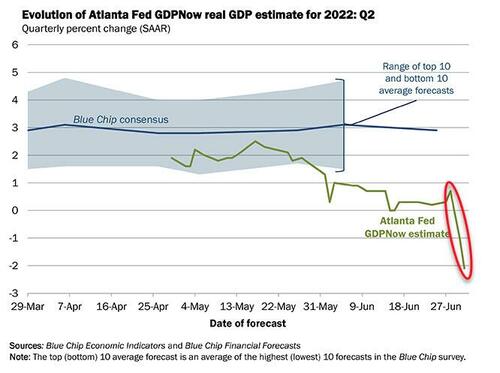

As I mentioned in a previous chart of the day, bad H1’s for equities have tended to be followed by much better H2’s. But with increasing warnings that a recession is round the corner, it isn’t so obvious where things are headed this time round. Indeed, equities saw another significant selloff yesterday as those fears were magnified yet again by another weaker than expected round of data which genuinely puts the US at risk of a technical recession in H1 already. That included the US weekly initial jobless claims for the week through June 25, which although coming in inline at 231k (vs. 230k expected), did send the smoother 4-week moving average up to its highest level so far this year. Our preferred measure, namely containing claims, edged up but is not yet signalling a recession though.

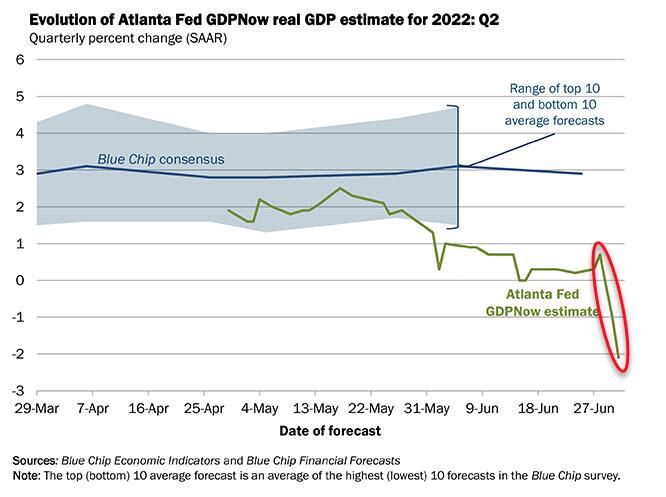

Personal spending also came in at just +0.2% in May (vs. +0.4% expected), and the prior month was revised down three-tenths as well, whilst real personal spending (-0.4%) saw its first monthly decline of the year as well. That translated to a 0.3% MoM Core PCE reading, below expectations of 0.4%, while the YoY reading was 6.3%. The prospect of the Fed being forced into hikes to fight stubborn inflation while growth is rolling over appears to be something the markets will have to wrestle with sooner rather than later. Indeed, the Atlanta Fed’s 2Q GDP nowcast estimate was revised down from 0.3% to -1.0% which if proved correct will signal a technical recession as a minimum. Today’s ISM will be a big sentiment driver on this front.

Against the weak growth backdrop, the S&P 500 (-0.88%) continued its run of having declined every day this week, whilst Europe’s STOXX 600 (-1.50%) saw even sharper losses. Utilities (+1.10%) were the clear outperformer, as investors rotate into defensive sectors. In turn, the NASDAQ underperformed, closing down -1.33%, also finishing in the red every day this week to date. The S&P 500 lost -20.58% in the first half of the year, its worst first half performance since 1970. Meanwhile, the NASDAQ has fared even worse, declining -22.44% this quarter alone and -29.51% in the first half of the year, its worst first half in the data available in Bloomberg.

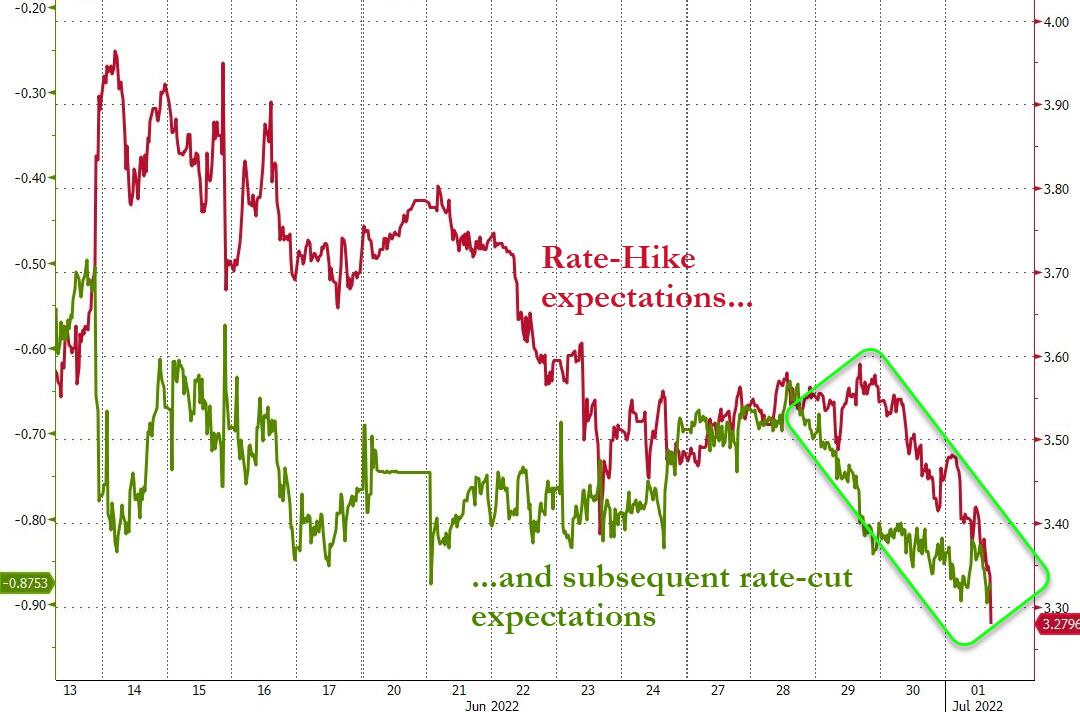

But in some ways the fear was more evident among sovereign bonds, which rallied significantly as investors continued to seek out safe havens and grew more doubtful about whether central banks would be able to persist in taking policy into aggressive territory. Indeed, the rate priced by Fed funds futures for the December 2022 meeting came down -6.5bps to 3.39%, and the rate priced by December 2023 came down an even larger -13.6bps to 2.96%. Those shifting expectations meant that yields on 10yr Treasuries fell back beneath 3% in the session for the first time in nearly 3 weeks, ultimately settling -7.6bps lower on the day at 3.01%. The decline in 10yr yields was split between breakevens and real yields, as both had a volatile session to end the quarter. Breakevens fell -4.7bps to 2.35%, their lowest levels since September. Other recessionary indicators were flashing warning signs of their own, with the near-term Fed spread down another -14.9bps to 142bps, meanwhile the 2s10s curve managed to eek out a marginal steepening, but is still flirting with inversion, closing at just 5.1bps. This morning, 10yr UST yields (-5.92 bps) are lower again, moving back below 3% to 2.95% with the 2s10 curve flattening -1bps at 4.13% as we type.

We saw much the same pattern in Europe yesterday, albeit with even larger moves lower in yields that sent those on 10yr bunds (-18.3bps), OATs (-15.2bps) and BTPs (-13.3bps) sharply lower. As in the US, European sovereign yield declines were driven by falling inflation compensation, with the 10yr German breakeven coming down by -12.3bps to 2.03%, which is its lowest closing level since Russia’s invasion of Ukraine began. That was echoed in a declining oil price with Brent crude down -1.60% yesterday at $109.52/bbl, meaning that oil prices saw a monthly decline in June for the first time since November 2021, back when the Omicron variant first emerged and travel restrictions started going back up again.

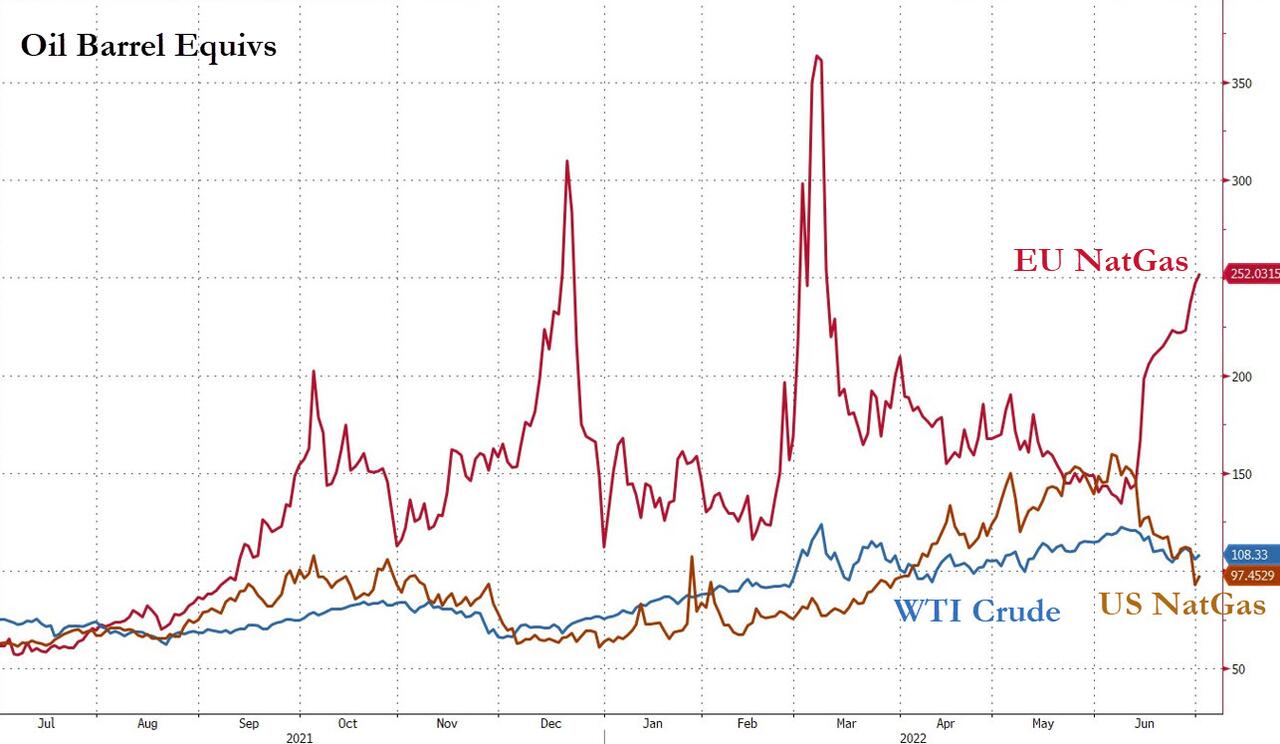

Speaking of energy prices, there were a few interesting headlines on that front yesterday, including a comment from President Biden that he is seeking more production from the Gulf states. Biden is set to travel to the Middle East from July 13-16, so that’s an important event on the geopolitical calendar, and ahead of that, we also saw the OPEC+ group move to ratify yesterday a further supply hike of +648k barrels per day in August. In Europe however there was more bad news on the energy side, with natural gas futures up a further +3.53% to a fresh three-month high of €144.51 per megawatt-hour. My colleague George Saravelos put out a fascinating blog yesterday (link here) that highlighted how worried he’s becoming on the gas supply situation, with year-ahead natural gas prices making fresh record highs and electricity prices skyrocketing. A key event as part of that will be the shutdown of the Nordstream pipeline from July 11-21 for regular annual maintenance, and press reports are suggesting that authorities are attempting to find a solution on sanctions restrictions to move gas turbine components back to Russia. So while we all spend most of our time thinking about the Fed and recessions, what happens to Russian gas over H2 is potentially an even bigger story. Mark July 22nd in your dairies to see whether the gas supply starts getting back to normal or not.

Asian equity markets are reversing early morning gains and are mostly down again. The Kospi (-1.04%) is the largest underperformer across the region followed by the Nikkei (-0.88%). Over in mainland China, the Shanghai Composite (-0.30%) and CSI (-0.20%) are down but are trimming losses, as the nation’s private factory activity rose at the fastest pace in 13 months in June (more on this below). Markets in Hong Kong are closed for a holiday marking the 25th anniversary of Chinese rule. Bucking the regional trend is Australia’s S&P/ASX 200 which is trading +0.26% higher at the time of writing. Outside of Asia, stock futures are once again sliding with contracts on the S&P 500 (-0.84%) and NASDAQ 100 (-0.86%) indicating a disappointing start in the US later today.

Early morning data showed that China’s Caixin/Markit manufacturing PMI advanced to 51.7 in June, returning to expansion territory for the first time in four months against a previous reading of 48.1 and well above analyst expectations for an uptick to 50.1. The recovery as suggested in the survey was propelled by a strong rebound in output, as the easing Covid restrictions sent factories racing to meet recovering demand.

Over in Japan, Tokyo’s June CPI rose +2.3% y/y (v/s +2.5% expected) and against a +2.4% increase in the prior month. Core CPI advanced +2.1% in June from a year earlier, notching the fastest pace of increase in seven years in a sign of broadening inflationary pressure in the world’s third largest economy. Separately, the unemployment rate in Japan surprisingly edged up to +2.6% in May from +2.5% in April. Meanwhile, sentiment at Japan’s large manufacturers deteriorated in the April-to-June period as the headline index worsened to a level of +9, a decline from the previous quarter’s reading of 14.

Looking at yesterday’s other data, French CPI came in at +6.5% as expected on the EU-harmonised measure in June, although German unemployment unexpectedly rose +133k in June (vs -5k expected) as Ukrainian refugees are now being included in those looking for work. Looking back to May however, the Euro Area unemployment rate hit its lowest level since the formation of the single currency at 6.6% (vs. 6.8% expected). Finally in the US, the MNI Chicago PMI came in at 56.0 (vs. 58.0 expected).

To the day ahead now, and data releases include the flash Euro Area CPI reading for June, as well as June’s global manufacturing PMIs and the ISM manufacturing reading from the US, along with the UK’s mortgage approvals for May. From central banks, we’ll hear from the ECB’s Panetta and De Cos.

FRIDAY /THURSDAY NIGHT

SHANGHAI CLOSED DOWN 10.98 PTS OR 0.32% //Hang Sang CLOSED /The Nikkei closed DOWN 457.42 OR 1.73% //Australia’s all ordinaires CLOSED DOWN 0.39 /Chinese yuan (ONSHORE) closed DOWN 6.7096 /Oil DOWN TO 107.98 dollars per barrel for WTI and DOWN TO 111.76 for Brent. Stocks in Europe OPENED MOSTLY RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7096 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7113: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

end

3c CHINA

CHINA/RUSSIA/JAPAN

Not good! Chinese and Russian navies circle Japan in a show of force

(zerohedge)

Chinese And Russian Navies Circle Japan In “Show Of Force”

THURSDAY, JUN 30, 2022 – 10:50 PM

In yet another example of the increasingly close alliance between Russia and China, the Chinese Navy and Russia’s Pacific Fleet have been engaging in war game operations, seemingly in tandem around Japan, according to the Japanese Defense Ministry.

Reports of coordinated military exercises have not been officially acknowledged by Russia or China, though Japan continues to post regular updates on ship movements. The naval exercises were apparently focused around the islands of Miyako and Okinawa, which hold 50,000 US forces, as well as a 70-mile wide corridor between the island of Yonaguni and Taiwan.

While not unheard of, military cooperation in the Pacific between Russia and China has grown in frequency, with naval exercises increasing over the past month. While Japan calls these movements a “show of force,” they may very well be practice for a conflict planned in the near future.

After the recent BRICS summit in Beijing and the reaffirmation of China’s economic support of Russia during its war with Ukraine and NATO sanctions, it only makes sense that the economic relationship would evolve into at least a loose military agreement. The latest decision on the induction of Sweden and Finland into NATO as well as naval escalation in the South Pacific are only going to drive Eastern interests closer together over time.