by harveyorgan · in Uncategorized · Leave a comment·Edit

by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1764.95 DOWN $36.55

SILVER: $19.19 DOWN 55 CENTS

ACCESS MARKET: GOLD $1767.00

SILVER: $19.25

Bitcoin morning price: $19,640 UP 240

Bitcoin: afternoon price: $20,203. UP 90-3

Platinum price: closing DOWN $15.70 to $863.96

Palladium price; closing DOWN $312.45 at $1929.60

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

CONTRACT: JULY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,798.900000000 USD

INTENT DATE: 07/01/2022 DELIVERY DATE: 07/06/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 186

365 H ED&F MAN CAPITA 2

657 C MORGAN STANLEY 1

661 C JP MORGAN 181

737 C ADVANTAGE 11 14

800 C MAREX SPEC 11 9

905 C ADM 3

TOTAL: 209 209

MONTH TO DATE: 977

no. of contracts issued by JPMorgan: 181/209

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT 209 NOTICE(S) FOR 20,900 Oz//0.6500 TONNES)

total notices so far: 977 contracts for 97700 oz (3.0388 tonnes)

SILVER NOTICES:

254 NOTICE(S) FILED 1,270,000 OZ/

total number of notices filed so far this month 1892 : for 9,460,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $36.55

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.41 TONNES FROM THE GLD//

INVENTORY RESTS AT 1050.31 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 55 CENTS

AT THE SLV// ://NO CHANGES IN SILVER INVENTORY AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 540.709 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 244 CONTRACTS TO 140.169 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.61 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.61) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SOME SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A POOR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.220 MILLION OZ FOLLOWED BY TODAY’S 575,000 OZ EFP JUMP TO LONDON / // V) SMALL SIZED COMEX OI GAIN

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -18

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTACTS for 2 days, total 2760 contracts: 13.800 million oz OR 6.9MILLION OZ PER DAY. (1380 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 6.9 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 6.9 MILLION OZ

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 262 DESPITE OUR $0.61 LOSS IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 2260 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 15.22 MILLION OZ FOLLOWED BY TODAY’S EFP JUMP TO LONDON OF 570,000 OZ // .. WE HAD A VERY STRONG SIZED GAIN OF 2522 OI CONTRACTS ON THE TWO EXCHANGES FOR 12.610 MILLION OZ DESPITE THE STRONG LOSS IN PRICE..

WE HAD 254 NOTICES FILED TODAY FOR 1,270,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1168 CONTRACTS TO 494,664 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: —838 CONTRACTS.

.

THE SMALL SIZED DECREASE IN COMEX OI CAME WITH OUR FALL IN PRICE OF $5.40//COMEX GOLD TRADING/FRIDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JULY AT 2.914 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 1300 OZ

YET ALL OF..THIS HAPPENED DESPITE OUR LOSS IN PRICE OF $5.40 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 4980 OI CONTRACTS 18.489 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6148 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 494,664

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4980, WITH1168 CONTRACTS DECREASED AT THE COMEX AND 6148 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4980 CONTRACTS OR 15.489TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (6148) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (1168,): TOTAL GAIN IN THE TWO EXCHANGES 4980 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JULY. AT 2.914 TONNES FOLLOWED BY TODAY’S 1300 OZ QUEUE JUMP 3) ZERO LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) SMALL SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

12,121 CONTRACTS OR 1,212,100 OZ OR 37,70 TONNES 2 TRADING DAY(S) AND THUS AVERAGING: 6061 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES: 37.70 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 37.70/3550 x 100% TONNES 1.06% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 2238.13 TONNES FINAL

JULY: 37.70 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A SMALL SIZED 244 CONTRACT OI TO 140,187 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 2260 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 2260 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE:2260 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 244 CONTRACTS AND ADD TO THE 2260 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED GAIN OF 2504 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 12.520 MILLION OZ

OCCURRED DESPITE OUR FALL IN PRICE OF $0.61 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 1.43 PTS OR 0.04% //Hang Sang CLOSED UP 22.72 /The Nikkei closed UP 269.64 OR % //Australia’s all ordinaires CLOSED UP .31% /Chinese yuan (ONSHORE) closed UP 6.7050 /Oil DOWN TO 107.98 dollars per barrel for WTI and DOWN TO 111.64 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7050 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7086: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 1168 CONTRACTS TO 494,664 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS SMALL COMEX DECREASE OCCURRED DESPITE OUR LOSS OF $5.40 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (6148 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 6148 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :6148 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6148 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 4980 CONTRACTS IN THAT 6148 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI LOSS OF 1168 CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $4.25.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JULY (3.216),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 3.216 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $5.40) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A STRONG SIZED GAIN OF 15.489 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR JULY (3.216 TONNES)…

WE HAD -838 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 4980 CONTRACTS OR 498,000 OZ OR 15.489 TONNES

Estimated gold volume 353,881/// STRONG/RAID/

final gold volumes/yesterday 299.284 /STRONG/RAID

INITIAL STANDINGS FOR JULY ’22 COMEX GOLD //JULY 5 (the inventory movements are Friday’s

the jerks have not updated it for today.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 93,612.421 oz Int. Delaware JPMorgan Brinks 10 kilobars and 2690 kilobars |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | 24,581.842 oz HSBC |

| No of oz served (contracts) today | 209 notice(s)20,900 OZ0.6500 TONNES |

| No of oz to be served (notices) | 57 contracts 5700 oz0.1773 TONNES |

| Total monthly oz gold served (contracts) so far this month | 977 notices97700 OZ3.0388 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

| the comex is now completely corrupt: the data below is yesterday’s they have not filed today’s |

total dealer deposit 0

No dealer withdrawals

1 customer deposit

i) Into HSBC xxx oz

total deposits: 24,581.842 oz

3 customer withdrawals:

i) Brinks: 86,679.09 oz

ii) JPMorgan 10,616.821 oz

iii) Int. Delaware: 321.510 oz (10 kilobars)

total withdrawal: 97,617.421 oz

ADJUSTMENTS:3 all dealer to customer

Brinks 2849.366 oz

JPMorgan 302.303 oz

Manfra: 64,628.510 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 266 contracts losing 412 contracts . We had

425 notices filed on Friday so we gained 13 contracts or an additional 81300 oz will stand in this non active

delivery month of July.

August has a LOSS OF 9824 contracts down to 387,697 contracts

Sept. gained 59 contracts to 112.

We had 209 notice(s) filed today for 20,900 oz FOR THE July 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 209 contract(s) of which 181 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2022. contract month,

we take the total number of notices filed so far for the month (977) x 100 oz , to which we add the difference between the open interest for the front month of (JULY 266 CONTRACTS ) minus the number of notices served upon today 209 x 100 oz per contract equals 103,400 OZ OR 3.216 TONNES the number of TONNES standing in this active month of July.

thus the INITIAL standings for gold for the JULY contract month:

No of notices filed so far (977) x 100 oz+ (266) OI for the front month minus the number of notices served upon today (209} x 100 oz} which equals 103,400 oz standing OR 3.216 TONNES in this active delivery month of JULY.

TOTAL COMEX GOLD STANDING: 3.216 TONNES (A FAIR STANDING FOR A JULY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,419,784.828 oz 75.26 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 32,989.550.8 OZ

TOTAL ELIGIBLE GOLD: 15,877,907.178 OZ

TOTAL OF ALL REGISTERED GOLD: 17,111,643.639 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 14,691,859.0 OZ (REG GOLD- PLEDGED GOLD)

END

SILVER/COMEX/JULY 5

data today is Friday’s data

and it will not be out for quite a while

do not have time to wait

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | xx oz |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 254CONTRACT(S)1,270,000 OZ) |

| No of oz to be served (notices) | 969 contracts (4,845,000 oz) |

| Total monthly oz silver served (contracts) | 1892 contracts 9,460,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: x oz

We have x deposits into the customer account

i

total deposit: xxx oz

JPMorgan has a total silver weight: 171.727 million oz/337.321 million =50.90% of comex

Comex withdrawals: 4

i) Out of Brinks 370,852.600 oz

ii) out of Int. Delaware 167,586.840 oz

iii) Out of JPMorgan 791,827.510 oz

iv) Out of Manfra: 191,892.860 oz

total withdrawal 1,522,159.820 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 69.331 MILLION OZ

TOTAL REG + ELIG. 337,321 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JULY OI: 123 CONTRACTS HAVING LOST 256. WE HAD 141 NOTICES FILED

ON FRIDAY, SO WE LOST 115 CONTRACTS OR 575,000 OZ WERE E.F.P.’d TO LONDON

AUGUST GAINED 91 CONTRACTS TO STAND AT 1528

SEPTEMBER HAD A GAIN OF 511 CONTRACTS UP TO 117,506 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 254 for 1,270,000 oz

Comex volumes:82,786// est. volume today// good

Comex volume: confirmed yesterday: 80,883 contracts ( GOOD )

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 1892 x 5,000 oz = 9,460,000 oz

to which we add the difference between the open interest for the front month of JULY(1223) and the number of notices served upon today 254 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY./2022 contract month: 1892 (notices served so far) x 5000 oz + OI for front month of JULY (1223) – number of notices served upon today (254) x 5000 oz of silver standing for the JULY contract month equates 14,305,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JULY 5/WITH GOLD DOWN $36.55//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.41 TONNES FROM THE GLD///INVENTORY RESTS AT 1041.90 TONNES

JULY 1/WITH GOLD DOWN $5.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES//INVENTORY RESTS AT 1050.31 TONNES

JUNE 30/WITH GOLD DOWN $9.20: big CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 1052.63 TONNES//

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

JUNE 21/WITH GOLD DOWN $2.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1075.54 TONES

JUNE 17/WITH GOLD DOWN $11.25: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.60 TONNES INTO THE GLD.///INVENTORY RESTS AT 1075.54 TONNES

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

GLD INVENTORY: 1041.90 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 5/WITH SILVER DOWN 55 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 540.709MILLION OZ//

JULY 1/WITH SILVER DOWN 61 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ//INVENTORY RESTS AT 540.709 MILLION OZ//

JUNE 30/WITH SILVER DOWN 41 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 738,000 OZ FROM THE SLV//INVENTORY RESTS AT 541.262 MILLION OZ//

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

JUNE 21/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 547.166 MILLION OZ//

JUNE 17/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 739,000 OZ FROM THE SLV./:INVENTORY RESTS AT 543.660 MILLION OZ/

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

CLOSING INVENTORY 540.709 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

Von Greyerz: This Implosion Will Be Fast… Hold On To Your Seats

MONDAY, JUL 04, 2022 – 07:10 AM

Authored by Egon von Greyerz via GoldSwitzerland.com,

The massive money creation in the 2000s has led to a debt and asset bubble, which is about to burst. Investors will be shocked by the speed of the decline and won’t react before it is too late.

The massive money creation by central and commercial banks in this century has resulted in a growth of global assets from $450 trillion in 2000 to $1,540 trillion in 2020.

DEBT TO GDP GROWTH

As the chart below shows US debt to GDP held well below 25% from 1790 to the 1930s, a period of almost 150 years. The depression with the New Deal followed by WWII pushed debt to GDP up to 125%. Then after the war, the debt came down to around 30% in the early 1970s.

The closing of the gold window in 1971 ended all fiscal and monetary discipline. Since then, the US and much of the Western world has seen debt to GDP surge to well over 100%. In the US, Public Debt to GDP is now 125%. Back in 2000 it was only 54% but since then we have seen a vote buying system with a money printing bonanza and an exponential increase in debt to 125%.

A major part of the debt increase has gone to finance the rapid growth in property values.

The table below shows that property has grown on average by 250% between 2000 and 2020. So individuals are creating wealth by swapping properties with each other. Hardly a sustainable form of wealth creation.

The exponential growth in property prices has been global although countries like China, Canada, Australia and Sweden stand out with over 200% gains since 2000. Most of the properties bought in the last 20+ years involve massive leverage. When the property bubble soon bursts, many property owners will have negative equity and could easily lose their homes.

So both private and government debt is continuing to grow rapidly. But nobody should believe that it will stop here. The Fed’s intention to reduce the balance sheet is not working and the debt is at best going sideways currently.

BIDEN BANS RUSSIAN GOLD

So it is happening again. The US has decided to ban imports of Russian gold and told the whole G7 to follow suit. President Biden sent the following Tweet last week:

So what will the consequences be?

Russia is the second biggest gold producer in the world after China. Just like with oil, gas and many other commodities, the effect will be higher gold prices over time. The gold trade is international and the major buyers of gold are China and India. So Russia can continue to sell gold to the Far East, the middle East and South America.

Also, when the EU sanctions started, the LBMA (London Bullion Market Association) decided not to accept gold that had been refined in Russia.

So the effect of the G7 ban will be minimal since gold deliveries from Russian refiners to the bullion banks already stopped in early March.

SANCTIONS ARE COUNTER PRODUCTIVE

Biden also signed an executive order on 15 March this year, prohibiting US persons to be involved with gold trading with Russian parties.

Still, more sanctions by the US and Europe will over time create shortages in gold just as it has in other commodities. So Russia will be able to sell its commodities including gold to other markets at higher prices.

But since Russia by far has the greatest commodity reserves in the world at $75 trillion, the value of these reserves are going to appreciate for years as we are now at the beginning of a major bull market in commodities.

The US and EU sanctions of Russia affect around 15% of the world population so there are still plenty of markets where Russia can trade.

The Roman Empire controlled parts of Europe, North Africa and the Middle East. The Empire prospered primarily due to free trade within the whole area with no sanctions. Sanctions hurt all parties involved. And since Russia is such a major commodity country that can continue to trade with major nations, they will over time suffer less than the sanctioning countries.

The consequences of these sanctions especially for Europe where many countries are dependent on Russian oil and gas will be totally devastating. So the US and Europe have really shot themselves in the foot.

GOLD, THE US DOLLAR & STOCK MARKETS

Coming back to gold, the US and G7 move is more likely to have a beneficial effect on gold over time with demand increasing and supply being restricted.

Gold started an uptrend in year 2001 that lasted for 10 years to 2011 when gold reached $1,920. After a major correction for 3 years until 2016, to $1,060, gold has resumed its exponential uptrend as can be seen in the chart below.

Although gold has not yet made sustained new highs in dollars, we have seen much higher highs in gold against most currencies. The temporarily strong dollar is making gold look weak measured in the US currency but that is unlikely to last for long.

MAJOR GOLD MOVE COMING

As the chart below shows, gold is finishing a Cup and Handle technical pattern. It does allow for a slightly lower price before the next move up although that is not certain. Regardless, the major trend for gold is substantial and I expect a sustained move up to at least 2026 but probably for much longer. Obviously there will be major corrections on the way.

DOLLAR FALL NEXT

If we look at the chart of the dollar against the Swiss franc since 1970, we can see that the 78% fall so far has gone sideways for 10 years.

The next move down is likely to be another 50% to 0.45-0.50 at least.

So the feeble and temporary dollar correction up is likely to end soon with a strong down move next.

MAJOR STOCK MARKET FALL AHEAD

Stocks globally are down around 20% this year.

The next move down in stocks could happen within the next few weeks. This is likely be a shocking move which will paralyse investors as they won’t have time to react.

So we could see stocks and dollar strongly down at the same time with the metals up. Even if gold and silver comes down initially, that move will not last. The uptrend in the metals is soon about to resume.

Wealth preservation

Our company made substantial purchases of physical gold at the beginning of 2002 for our investors and ourselves. The price was then $300. We have never sold an ounce since then but added at opportune moments.

There was, as the gold chart above shows, a major move until 2011 and then a vicious 3 year correction to $1,060 before the bull trend resumed. As I mentioned above, gold has made much higher highs above the 2011-12 highs in Euros, Pounds,Yen, Swedish kronor, Australian dollars etc.

US dollar highs are just around the corner.

As we bought gold for wealth preservation purposes, it was essential that it was physical with direct ownership and control for the investor. To be able to inspect your own gold is also a requirement.

It is also imperative to store the gold outside an increasingly fragile financial system. If you buy gold as insurance against such an over-leveraged and weak system, it obviously serves no purpose to store it within that system.

To store your insurance asset in a safe jurisdiction is clearly critical. Especially with the current geopolitical unrest it is essential to take advice on location. Also important is to be able to move the gold quickly if necessary.

The reputation and values of the company that assists you with your gold investments must be impeccable.

It serves no purpose to make your choice based on the lowest cost of storage, insurance and handling when you are protecting one of your most important assets.

BE CAREFUL

So there are likely to be major moves in markets next.

No one can of course time these moves exactly. But what is critical to understand is that risk is now extremely high and investors are not going to be saved by central banks.

And remember that fire insurance can only be bought before the fire starts!

-END-

END

3. Chris Powell of GATA provides to us very important physical commentaries

For your interest…

(BBC/GATA)

Exceptional’ Roman gold coin hoard found in Britain

Submitted by admin on Fri, 2022-07-01 09:39Section: Daily Dispatches

After two millennia, Augustus’ money is still good.

* * *

By Katy Prickett

British Broadcasting Co., London

Friday, July 1, 2022

A hoard of Roman gold coins hidden in the decades before the Roman invasion of Britain has been discovered.

Eleven coins have been found so far, scattered near Norwich in Iceni tribe territory. Their queen Boudica would later rebel against Roman rule

Numismatist Adrian Marsden said the hoard is “really quite exceptional” and more coins might be unearthed.

An inquest at Norfolk Coroner’s Court into the two latest finds deemed them treasure. …

… For the remainder of the report and excellent photos of the coins:

https://www.bbc.com/news/uk-england-norfolk-61984020

end

This will cause more gold smuggling into India

The move to raise import tax on gold is to support the ralling rupee

(Reuters.GATA)

India raises import tax on gold to support rupee

Submitted by admin on Fri, 2022-07-01 09:31Section: Daily Dispatches

By Rajendra Jadhav

Reuters

Friday, July 1, 2022

MUMBAI — India has raised its basic import duty on gold to 12.5% from 7.5%, the government said today, as the world’s second biggest consumer of the precious metal tries to dampen demand and bring down the trade deficit.

Local gold prices jumped to an over-two-month peak of 52,032 rupees per 10 grams today, the highest since April 25.

India meets most of its gold demand through imports. That has put pressure on the rupee, which hit a record low today. …

… For the remainder of the report:

https://www.reuters.com/world/india/india-raises-import-tax-gold-125-75-2022-07-01/

END

A must read: Peter Hambro states that Putin and Xi know the golden rule and are not fooled by paper gold

(Hambro/GATA)

Peter Hambro: Putin and Xi know the golden rule

Submitted by admin on Mon, 2022-07-04 22:19Section: Daily Dispatches

10:20p ET Monday, July 4, 2022

Dear Friend of GATA and Gold:

Gold mining executive and trader Peter Hambro today reviews how the gold derivatives racket — an enterprise of central banks, bullion banks, and futures-trading investment houses — have rigged the gold market for many years using imaginary metal.

But Hambro warns: “Vladimir Putin and Xi Jinping are among those who know the golden rule: Whoever has the gold makes the rules.”

His commentary is headlined “Don’t Forget the Golden Rule: Whoever Has the Gold Makes the Rules” and it’s posted at Reaction here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

4. OTHER GOLD COMMENTARIES

Special thanks to Doug C. for sending this to us:

https://mises.org/wire/contra-ben-bernanke-gold-standard-promotes-economic-stability

Contra Ben Bernanke, the Gold Standard Promotes Economic Stability

Currently the world is on a fiat money standard—a government-issued currency that is not backed by a commodity such as gold. The fiat standard is the primary cause behind the present economic instability, and is tempted to suggest that a gold standard would reduce instability. The majority of experts however, oppose this idea on the ground that the gold standard is in fact a factor of instability.

For instance, the former Federal Reserve Board chairman Ben Bernanke echoed this opposition in his lecture at the George Washington University on March 20, 2012. According to Bernanke, the gold standard prevents the central bank from engaging in policies aimed at stabilizing the economy on account of sudden shocks. This, in turn, according to Bernanke, could lead to severe economic upheavals:

Since the gold standard determines the money supply, there’s not much scope for the central bank to use monetary policy to stabilize the economy…. Because you had a gold standard which tied the money supply to gold, there was no flexibility for the central bank to lower interest rates in recession or raise interest rates in an inflation.

A great merit of the gold standard is that it prevents authorities from pursuing reckless money pumping. Also, in his speech, Bernanke argued that because of the relatively low growth rate in the supply of gold, this could lead to a general decline in the prices of goods and services, which could seriously damage the economy.

What matters is not the growth rate of money as such but its purchasing power. With an expansion in wealth all other things being equal, the purchasing power of dollars is going to increase and every holder of dollars is going to command more wealth.

Bernanke also argued that another major negative of having the gold standard is that it creates a system of fixed exchange rates between the currencies of countries that are on the gold standard. There is no variability as we have it today, argued Bernanke:

If there are shocks or changes in the money supply in one country and perhaps even a bad set of policies, other countries that are tied to the currency of that country will also experience some of the effects of that.

It seems that Bernanke was arguing in support of the floating currency system. He doesn’t understand that in a free market, money is a commodity, and a dollar or other currencies are not independent entities.

Prior to 1933, the name “dollar” was used to refer to a unit of gold that had a weight of 23.22 grains. Since there are 480 grains in one ounce, this means that the name dollar also stood for 0.04838 ounce of gold. This in turn means that one ounce of gold referred to $20.67. Please note that $20.67 is not the price of one ounce of gold in terms of dollars as Bernanke and other experts are saying. Dollar is just a name for 0.04838 ounce of gold. According to Murray N. Rothbard,

No one prints dollars on the purely free market because there are, in fact, no dollars; there are only commodities, such as wheat, cars, and gold.

Likewise, the names of other currencies stood for a fixed amount of gold. Contrary to Bernanke, in a free market, currencies do not float against each other. They are exchanged in accordance with a fixed definition. For example, if the British pound stands for 0.25 ounces of gold and the dollar stands for 0.048 ounces of gold, then one British pound will be exchanged for around five dollars, as Rothbard showed.

Increases in the Gold Supply Don’t Cause Boom-Bust Cycles

According to Rothbard, increases in the supply of gold do not set boom-bust cycles into motion. For Rothbard the key reason behind boom-bust cycles is the act of embezzlement brought about by the monetary policies of the central bank.

Rothbard believed that the business cycle is unlikely to emerge in a free-market economy where money is gold and there is no central bank. According to Rothbard,

Inflation, in this work, is explicitly defined to exclude increases in the stock of specie. While these increases have such similar effects as raising the prices of goods, they also differ sharply in other effects: (a) simple increases in specie do not constitute an intervention in the free market, penalizing one group and subsidizing another; and (b) they do not lead to the processes of the business cycle. (bold added)

To better explain this point, we begin with a barter economy in which John the miner produces ten ounces of gold. The reason why he mines gold is because there is a market for it. John then exchanges his ten ounces of gold for various goods and services.

Over time, individuals have discovered that gold—being originally useful in making jewelry—is also useful for other uses such as to serve as the medium of the exchange. They now begin to assign a much greater exchange value to gold than before. As a result, John the miner can exchange his ten ounces of gold for more goods and services than before.

Observe that gold is part of the pool of wealth and promotes the individual’s life and well-being. Every time John the miner exchanges gold for goods, he is engaging in an exchange of something for something. He is exchanging wealth for wealth.

Contrast this with the paper receipts that are employed as the medium of exchange. These receipts are issued without the corresponding gold deposited for safekeeping. This sets a platform for consumption without contributing to the pool of wealth.

The printing of receipts unbacked by gold sets the exchange of nothing for something. This in turn sets in motion the process of the diversion of resources from wealth-generating activities to the holders of unbacked receipts. This leads to the so-called economic boom.

Stopping the issuing of unbacked receipts arrests the diversion of resources towards activities that emerged because of unbacked by gold receipts. As a result, non-wealth-generating activities come under pressure—an economic bust emerges.

To clarify this point further, consider counterfeit money generated by a forger. No goods were exchanged to obtain the forged money. (The forger just printed the money hence the counterfeit money emerged out of “thin air.”) Once the forged money is exchanged for goods, this results in nothing being exchanged for something, leading to the channeling of goods from individuals that produced goods to the forger.

Now, a forger by embarking on the purchases of various goods provides in fact support for the production of these goods. Observe that the increase in the production of goods would not emerge in the absence of the counterfeit money. Resources are now directed towards the production of goods that are supported by the counterfeiter.

Once the support for goods emerging on account of counterfeiter activities slows down, or comes to a halt, the demand for these goods also slows down or vanishes. Consequently, the production of these goods slows down or is aborted. Observe that on account of the increase in the money with no backing, an increase in the production of goods emerges. A decline in the money created from nothing results in the decline in the production of these goods. Hence, what we have here is a boom of activities that emerged as a result of money out of “thin air” and their bust because of a decline in the supply of unbacked money.

While increases in the supply of gold (when used as money) are likely to cause fluctuations in economic activity, these fluctuations do not occur because of intervention with the free market. Thus, these fluctuations do not cause the impoverishment of wealth generators. A gold miner (wealth producer) exchanges gold for other useful goods. He does not require empty money to divert wealth to himself.

Summary and Conclusion

Boom-bust cycles are the outcome of central bank policies that are aimed at stabilizing the economy. In the past the alleged instability of economies on the gold standard took place because the authorities were issuing unbacked by gold money thereby undermining the gold standard. Contrary to popular thinking, the gold standard, if not abused by the central bank, does not cause instability.

5.OTHER COMMODITIES: NICKEL:

Nickel jumped 6% following news that the UK government as added billionaire and owner of Norlisk to its list of sanctioned individuals.

The LME has not banned Norilsk due to the massive short position of one trader and they do not need another huge rise in price of Ni.

(OilPrice.com)

Nickel Prices Surge As UK Sanctions Major Russian Miner

TUESDAY, JUL 05, 2022 – 03:30 AM

- Nickel prices jumped by 6% following news that the UK government has added Vladimir Potanin, Norisk Nickel’s president, to its list of sanctioned individuals.

- Potanin, the board chairman for Moscow-based conglomerate Interros, holds a 35.9% stake in Norilsk Nickel.

- Norilsk, one of the world’s largest single nickel producers, accounts for approximately 7% of the global supply.

The UK government has added Vladimir Potanin, Norilsk Nickel’s president and chairman of the management board, to its list of sanctioned individuals. The LME nickel price remains in question. A June 29 update notification from HM Treasury’s Office of Financial Sanctions Implementation (OFSI) noted Potanin’s addition. The stated reason was that he would benefit from or support the Russian government by owning or controlling Rosbank.

“Rosbank is carrying on business in the Russian financial services sector, which is a sector of strategic significance to the Government of Russia,” OFSI said in its update. Potanin, the board chairman for Moscow-based conglomerate Interros, holds a 35.9% stake in Norilsk Nickel. That holding group acquired Rosbank from French investment bank Société Générale back in April.

The LME Reacts to Sanction News and Nickel Price

The market quickly voiced concerns over possible supply issues. According to reports, news of the sanctions caused nickel prices on the London Metal Exchange to jump by 6%. The base metal’s official three-month closing price was $23,158 per metric ton on June 28. According to data from the bourse, this represents a decline of 10.8% from June 21, when prices were $25,949.

The sanctions are part of the “Russian Regulations”. This information falls under the Sanctions and Money Laundering Act of 2018. According to the OFSI documents, these stipulate freezing funds and economic resources belonging to entities “involved in destabilizing Ukraine. It undermines or threatens the territorial integrity, sovereignty, or independence of Ukraine. It’s about obtaining a benefit from or supporting the Government of Russia.”

The asset freeze also prevents any UK citizen or business from dealing with any funds owned, held, or controlled by the named individual. “It also prevents funds or economic resources being provided to or for the benefit of the designated person,” a government statement said. Potanin will also not be able to enter the United Kingdom or remain in the country

A Long List of Bans and Sanctions

Norilsk, one of the world’s largest single nickel producers, accounts for approximately 7% of the global supply. Of course, Nickel’s primary application is the production of austenitic stainless steel. However, the metal’s application also extends to batteries, including those designed for electric vehicles. Platinum and palladium are also sourced heavily from Norilsk’s production. Back in May, the UK government imposed a 35% duty on all imports of the rare metals sourced from Russia or Belarus.

That same month, the UK froze the assets of London-headquartered Evraz. As a major steel manufacturer, Evraz has steelmaking and mining assets in Russia. The Financial Conduct Authority had already suspended the group’s shares on the London Stock Exchange two months earlier. This was largely due to the government’s addition of Roman Abramovich to its list of sanctioned individuals.

In March, steel and iron imports from Russia and Belarus were subjected to a 35% import duty. The move was the result of denying the two countries “Most Favored Nation” status for hundreds of their exports.

It Remains Unclear How Much Impact the Move Will Have

The LME has still not banned Russian Nickel. It’s just that the stocks from Russia are lower due to concerns over supply and logistics. So, while things might seem tight in Europe for now, there are ample opportunities to source Nickel from other places and producers.

Indonesia, for instance, has been ramping up its nickel production exponentially. This will effect its nickel price. In fact, estimates put the country’s primary production forecast for 2022 at 1.3 million metric tonnes. That’s a 52% increase on the year. Currently, primary nickel demand within Europe is forecasted at 310,000 metric tonnes for the year. This is a significant increase from 2021, when demand was 300,000. Fortunately, the LME does not require high-quality nickel for all of the nickel it pushes through.

Despite the sanctions, Norilsk Nickel will likely turn its attention towards China as a primary end-user. If demand holds up in that market, the company will not get too broken up about Potanin’s inclusion on the U.K.’s list.

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.7050

OFFSHORE YUAN: 6.7986

HANG SANG CLOSED UP AT 22.72 PTS OR .10%

2. Nikkei closed UP 269.64 OR 1.23%

3. Europe stocks CLOSED ALL RED

USA dollar INDEX UP TO 106.05/Euro FALLS TO 1.0297

3b Japan 10 YR bond yield: FALLS TO. +.205/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 136.04/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: UP -// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.271%/Italian 10 Yr bond yield RISES to 3.35% /SPAIN 10 YR BOND YIELD RISES TO 2.38%…

3i Greek 10 year bond yield FALLS TO 3.45//

3j Gold at $1799.30 silver at: 19.75 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 5 AND 1/4 roubles/dollar; ROUBLE AT 60.52

3m oil into the 107 dollar handle for WTI and 111 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 136.04DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9653– as the Swiss Franc is still rising against most currencies. Euro vs SF 19.99395well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.897 DOWN 1 BASIS PTS

USA 30 YR BOND YIELD: 3.124 DOWN1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.01

Futures Slide As Recesson Fears Trump Tariff Optimism

TUESDAY, JUL 05, 2022 – 12:03 PM

The rally that pushed stocks well above 3,800 during Monday’s illiquid session when US cash stocks were closed for July 4 amid speculation that Biden was about to rollback many Chinese tariffs (unclear how this would help ease inflation but a move that the market clearly read as risk positive), fizzled as soon as Europe opened this morning and alongside the tumbling euro which plunged to a 20-year-low and approached parity with the USD on growing recession fears, also dragged US equity US futures lower as investors turned their focus back to the looming recession, which outweighed optimism around an improvement in Washington’s ties with Beijing. Contracts on the Nasdaq 100 were down 0.7% by 730 a.m. in New York, while S&P 500 futures slipped 0.6%. The cash market was closed for a holiday on Monday. 10Y TSY yields swung from gains to losses before trading 2bps higher around 2.90% while bitcoin rose, and traded around $20K after dropping below $19K over the weekend.

US markets are set to reopen Tuesday after capping 11 declines in the past 13 weeks as an unprecedented first-quarter contraction boosted the prospects of a recession to near certainty. At the same time, consumer prices are far from peaking with inflation surging to 8.6% in May that left little room for the Federal Reserve to slow monetary tightening.

Sentiment was lifted on Monday as senior US and Chinese officials discussed US economic sanctions and tariffs amid reports the Biden administration is close to rolling back some of the trade levies imposed by President Donald Trump. While that came as a relief, investors continued to fret over a potential US recession, stubborn inflation and monetary tightening. Economic reports in Europe, including French purchasing managers’ indexes, came in below estimates.

“The Fed will likely remain aggressive in its fight against inflation for now,” said Joachim Klement, head of strategy, accounting and sustainability at Liberum Capital. “At the same time, European growth is slowing down fast. This just puts additional fire on the growth concerns about the US.”

“The government is very conscious that they need to act on the supply side of the inflation issue because the Fed has been slamming the brakes on the demand side whereas the real issue is on the supply side,” said Deepak Mehra, the head of investments at the Commercial Bank of Dubai. “Trying to fix that issue is giving the market a bit of an ease and comfort that we are finally addressing the problem where it is and not giving the wrong medicine,” he said in an interview with Bloomberg TV.

Among notable moves in premarket trading, cryptocurrency-exposed stocks edged higher as Bitcoin briefly traded above the closely watched $20,000 level. Recession fears echoed in US premarket trading, where Carnival Corp. and ASML Holding NV dropped more than 4% each. Meanwhile, Morgan Stanley strategists led by Michael Wilson said the US economy is firmly in the middle of a slowdown that’s turning out to be worse than expected amid the war in Ukraine and China’s Covid Zero policy. “Any fall in rates should be interpreted as more of a growth concern rather than as potential relief from the Fed,” they wrote in a note. Here are some other notable premarket movers:

- Cowen (COWN US) shares jump as much as 14% in US premarket trading, following a report late Friday that Canadian bank Toronto-Dominion was said to be exploring a takeover of the brokerage. Piper Sandler says that a possible combination would be “reasonable” for Cowen at the right price.

- Antero Resources (AR US) shares rise 2.8% in premarket trading after the stock was upgraded to buy from hold at Truist Securities, with the broker saying that a recent selloff in the oil company is an opportune entry point given gas and natural gas liquids are likely to remain strong.

- Cryptocurrency-exposed stocks are gaining in US premarket trading on Tuesday as Bitcoin trades above the closely watched $20,000 level. Coinbase (COIN US) +1.4%, Riot Blockchain (RIOT US) +1.9%, Marathon Digital (MARA US) +2.4%, MicroStrategy (MSTR US) +2.8%, Ebang (EBON US) +5.9%

- Tesla (TSLA US) shares fall 0.8% in premarket trading, though analysts note that the electric vehicle company’s record production in June is a silver lining in an otherwise disappointing quarter of deliveries.

- Netflix (NFLX US) shares decline 0.8% in premarket trading as Piper Sandler cuts PT to $210 from $293, reiterating neutral recommendations, while estimating that the company’s ad-supported tier, which is expected to launch by year-end, represents a quarterly revenue opportunity of about $1.4 billion.

- HP Inc. (HPQ) shares slip 2% as Evercore ISI downgrades the tech company to in-line, saying PC “headwinds could get more severe.”

Most European equity indexes slumped over 1% with miners, autos and insurance names among the worst-performing Stoxx 600 sectors. CAC 40 and FTSE 100 lag, dropping as much as 1.4%. Miners underperformed the broader European market on Tuesday amid concerns over the risks of a global recession and the blow it would deliver to demand for raw materials. Copper fell to the lowest level in 17 months and traded solidly below $8,000 a ton, as sentiment remains sour toward the industrial material used in everything from construction to new energy vehicles. Stoxx 600 Basic Resources sub-index declines 1.6% as of 9:42am in London, led lower by miners like Antofagasta, KGHM and Anglo American, even as iron ore rises after a four-day slide. Broader European benchmark is down 0.4%. The Stoxx 600 energy sub-index slides 1.3% after rising most since May on Monday. TotalEnergies drops 1.6%, BP -1.1%, Shell -1.3%. Shares in renewable fuel producer Neste outperform, rising 1.3%. The Stoxx 600 Automobiles & Parts Index dropped 1.5%, the third-worst performing subgroup in the broader European equity market. Automakers had their worst June sales in decades in the UK, while German new-car registrations also plunged. Here are some of the biggest European movers today:

- Miners and energy shares underperform the broader European market on Tuesday amid concerns over the risks of a global recession and the blow it would deliver to demand for raw materials.

- KGHM shares decline as much as 6.7%, Anglo American -4.5%, TotalEnergies -2.5%, Shell -2.2%

- Rheinmetall shares fall as much as 6.1%; Deutsche Bank expects 2Q at the lower end of the guidance range for the quarter while most-in-focus unit Defence will likely trend above.

- SAS falls as much as 15% after the company announced it was filing for chapter 11 bankruptcy protection in the US.

- European media stocks slide after Goldman Sachs slashed earnings forecasts across its media and internet coverage to factor in a more cautious macro outlook. Prosieben drops as much as 9.5%, Publicis -4.5%

- Uniper shares edged lower, paring earlier gains of as much as 11%, as analysts speculated on what a possible government bailout might look like.

- Dechra Pharmaceuticals advances as much as 4.5% on Tuesday after RBC upgrades to outperform in note in which it describes the stock as the “pick of the litter.”

- Cellnex Telecom shares rise as much as 5% following a Bloomberg News report that a KKR-led consortium is emerging as the frontrunner to buy a stake in Deutsche Telekom’s tower unit, beating out a rival bid from Cellnex and Brookfield Asset Management that had been viewed negatively by analysts.

- Lonza Group climbs as much as 3.8% after it got upgraded to buy from neutral at Citi, citing the market’s under-appreciation of demand for biologics manufacturing.

- PGS shares soar as much as 20% as Pareto Securities upgrades the oilfield services firm to buy following a period under review, with the broker saying that “the future is looking brighter” for the company.

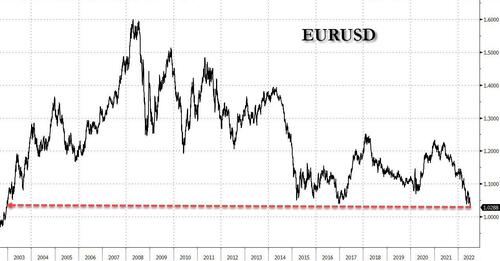

The euro extended its losses, tumbling to the lowest level since 2002 against the dollar. It also slid to the weakest since January 2015 against the Swiss franc.

Earlier in the session, Asian equities were modestly higher Tuesday as China’s stocks gave back early gains after initial enthusiasm about the country’s improving ties with the US waned. The MSCI Asia Pacific Index rose as much as 0.8% before narrowing the advance to 0.2% as of 6:14 p.m. in Singapore. Energy and health care shares were among the gainers. Chinese shares fell, after the province of Anhui reported more than 200 Covid cases for Monday and market participants assessed whether the potential scrapping of US tariffs on Chinese goods would help address global inflation concerns. The US 10-year Treasury yield trimmed an intraday advance over recession worries, giving tech shares a slight boost.

Australia’s main index edged higher as the domestic central bank met market expectations by raising interest rates a half-percentage point and suggesting that inflation may peak this year. Benchmarks in the Philippines and South Korea led gains in Asia, with each rising at least 1.8%. “The easing of tariffs — if confirmed — comes at the dream timing to save its economy from the endless virus battle,” said Hebe Chen, an analyst at IG Markets, referring to the China. “Even though it may not stop the downtrend, it could at least slow the pace and restore the world’s confidence in the second-largest economy.” Meanwhile, Thailand’s gauge was the latest to enter a technical correction. Asian stocks have been stuck in range-bound trading since the end of April as markets digest higher interest rates, the possibility of a recession in advanced economies and continued virus flareups in China. The MSCI regional gauge is down more than 18% this year

In Australia, the central bank raised its key interest rate as expected to 1.35%. It’s among more than 80 central banks to have raised rates this year. The nation’s dollar weakened after the decision.

Key equity gauges in India pared early advances to close lower as worries over an economic recession weighed on the sentiments. The S&P BSE Sensex dropped 0.2% to 53,134.35 in Mumbai, while the NSE Nifty 50 Index also dropped by the same magnitude. Stocks rose earlier in the day, tracking advances in Asian peers on the possibility of US rolling back some levies on China. A fast progress of monsoon rainfall, which waters most farmland in India, along with quarterly earnings for top companies that start this week added to the sentiment. Consumer goods maker ITC was the biggest drag on the Sensex, falling 1.7%. Seven of BSE Ltd.’s 19 sectoral sub-gauges declined, led by information technology companies. Asia’s biggest software exporter Tata Consultancy Services, will kickoff the April-June earnings season for companies on Friday

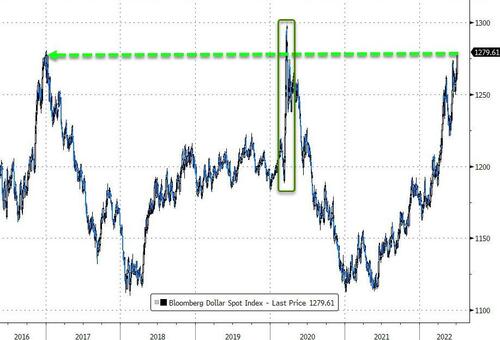

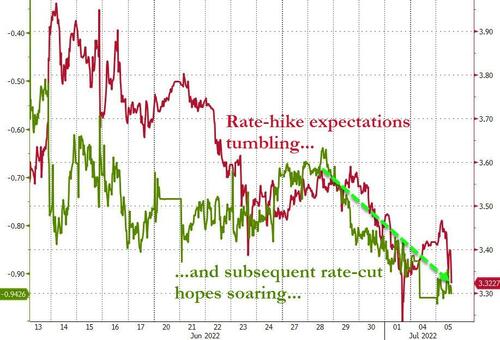

In FX, the Bloomberg Dollar Spot Index advanced for a third day as the greenback gained against all of its Group-of-10 peers. Treasuries were mixed. The single currency fell as much as 0.9% to 1.0331, its weakest level since December 2002, with losses compounded by poor liquidity and selling in euro-Swiss franc. German bond curve bull steepened and money markets trimmed ECB tightening bets to less than 140 basis points this year after French services PMI was revised lower. That’s down from more than 190 basis points almost three weeks ago, widening the interest-rate differential with the Federal Reserve. Scandinavian currencies were also dragged down by the euro sell-off and were leading G-10 losses against the greenback. Cable fell amid broad- based dollar strength. Bank of England rate-setter Silvana Tenreyro speaks later Tuesday and the BOE will issue its financial stability report. The Australian dollar extended a slump on the back of the broad-based US dollar strength. The Aussie had already given up gains after the RBA increased its cash rate to 1.35% as expected. It had risen earlier amid reports the US will roll back tariffs on some Chinese goods. The yen pared an Asia session loss as risk sentiment worsened.

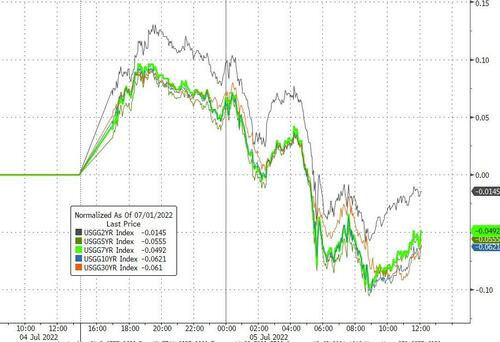

In rates, Treasuries were off session lows reached during Asia session, remain under pressure as US markets reopen after Monday’s holiday, giving back a portion of Friday’s steep gains. Five- and 10-year yields remain below 50-DMA levels while 2- and 30-year are back above. Yields higher by as much as 6bp at short end vs ~3bp at long end after rising as much as 13bp and 9bp, respectively. 2s10s curve is slightly positive after briefly inverting for first time since mid-June; 5s30s spread ~22bp after reaching widest level since May 31 on Friday. Short-end Germany richens over 10bps, outperforming gilts. Cash USTs fade Asia’s gains. Peripheral spreads widen to core with short-end Italy underperforming.

In commodities, brent crude swung between gains and losses, last trading Brent down 1.5% near $111.78, while WTI rose after a long holiday weekend in the US with investors weighing still-strong underlying market signals against concerns a recession will eventually sap demand. Most base metals trade in the red; LME aluminum falls 2.8%, underperforming peers. Spot gold falls roughly $5 to trade near $1,803/oz.

Bitcoin resides underneath the USD 20k mark and at session lows of 19.4k amid the broader risk tone. BoE Financial Stability report said falling crypto markets expose vulnerability, but not stability risk overall.

To the day ahead now, and data highlights include the global services and composite PMIs for June, as well as the ISM services index from the US. Otherwise, there’s French industrial production for May and US factory orders for May. From central banks, the BoE will be releasing their Financial Stability Report and we’ll also hear from the BoE’s Tenreyro.

Market Snapshot

- S&P 500 futures down 0.3% to 3,814.75

- STOXX Europe 600 down 0.3% to 408.04

- MXAP up 0.3% to 157.72

- MXAPJ up 0.2% to 521.38

- Nikkei up 1.0% to 26,423.47

- Topix up 0.5% to 1,879.12

- Hang Seng Index up 0.1% to 21,853.07

- Shanghai Composite little changed at 3,404.03

- Sensex up 0.3% to 53,387.68

- Australia S&P/ASX 200 up 0.3% to 6,629.33

- Kospi up 1.8% to 2,341.78

- German 10Y yield little changed at 1.27%

- Euro down 0.8% to $1.0338

- Brent Futures up 0.4% to $114.01/bbl

- Gold spot down 0.3% to $1,803.33

- U.S. Dollar Index up 0.64% to 105.81

Top Overnight News from Bloomberg

- Senior US and Chinese officials discussed US economic sanctions and tariffs Tuesday amid reports the Biden administration is close to rolling back some of the trade levies imposed by former President Donald Trump

- UK automakers had their worst June sales in decades in the UK as ongoing components shortages kept them from meeting demand. New-car registrations declined by 24% to 140,958 vehicles, the lowest for the month since 1996, according to data from the Society of Motor Manufacturers and Traders

- Italy declared a state of emergency in five northern and central regions devastated by a recent drought, as a severe heat wave takes its toll on agriculture and threatens power supplies

A more detailed summary of global markets courtesy of newsquawk

Asia-Pac stocks traded mostly positive amid a pick-up from the holiday lull although Chinese markets faltered. ASX 200 was led by the tech and commodity-related sectors with further support from a lack of hawkish surprise from the RBA. Nikkei 225 was propelled by a weaker currency but pulled back from early highs after hitting resistance around the 26,500 level and following softer-than-expected wages data. Hang Seng and Shanghai Comp. were both initially lifted following reports US President Biden could make a decision on rolling back some China tariffs as soon as this week and with Vice Premier Liu He said to have had a constructive exchange with US Treasury Secretary Yellen on the economy and supply chains. Furthermore, participants also welcomed the strong Caixin Services and Composite PMI data, although the advances in the mainland were then pared as the central bank continued to drain liquidity and amid lingering COVID concerns.

Top Asian News

- PBoC injected CNY 3bln via 7-day reverse repos with the rate at 2.10% for a CNY 107bln net drain.

- China is to set up a CNY 500bln state infrastructure investment fund and will issue 2023 advance local government special bonds quota in Q4, according to Reuters sources.

- Chinese Premier Liu He spoke with US Treasury Secretary Yellen regarding the economy and supply chains, while the exchange was said to be constructive and both sides believed in the need to strengthen communication and coordination of macro policies between China and the US, according to Reuters.

- US Treasury Department confirmed Treasury Secretary Yellen held a virtual meeting with China’s Vice Premier Liu He as part of efforts to maintain open lines of communication, while they discussed macroeconomic and financial developments in both China and US, as well as the global economic outlook and food security challenge. Furthermore, Yellen raised issues of concern including the impact of Russia’s war against Ukraine on the global economy and “unfair, non-market PRC economic practices”, according to Reuters.

- RBA hiked the Cash rate Target by 50bps to 1.35%, as expected, while it reiterated that the board expects to take further steps in the process of normalising monetary conditions with the size and timing of future interest rate increases will be guided by the incoming data and the board’s assessment of the outlook for inflation and the labour market. Furthermore, the central bank noted that Australian inflation was high but was not as high as in other countries and it forecast inflation to peak this year before declining back towards the 2-3% range next year.

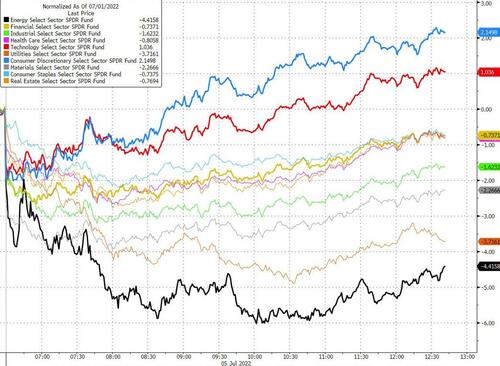

European bourses are pressured across the board, Euro Stoxx 50 -0.8%, as a broader risk-off move takes hold despite a relatively constructive APAC handover and limited newsflow in European hours. A move that has impaired US futures, ES -0.4%, as we await the lead from stateside participants re-joining after the long-weekend with a quiet schedule ahead. European sectors are predominantly in the red, though the clear defensive bias is keeping the likes of Food and Healthcare afloat.

Top European News

- UK faces its first national train drivers’ strike in 25 years with the head of the UK train drivers’ union warning of ‘massive’ disruption as members vote on their first strike since 1995, according to FT.

- BoE Financial Stability Report (July): will raise the counter-cyclical capital buffer rate to 2% in July 2023. Click here for more detail.

- Ukraine Latest: Turkey Renews Threat to Veto NATO Expansion

- Bunds Bull Steepen, ECB Hike Bets Pared After French PMI Revised

- UK Train Drivers Would Make Threatened Strikes National: Union

FX

- DXY sets new 2022 best above 106.000 after taking time out to mark US Independence Day, reaches 106.24 before waning marginally.

- Euro slumps to fresh multi-year lows as EGBs rebound strongly and risk appetite evaporates; EUR/USD probes 1.0300, EUR/CHF sub-0.9950 and EUR/JPY below 140.00.

- Aussie underperforms irrespective of 50bp RBA rate hike as accompanying statement sounds less hawkish on inflation; AUD/USD under 0.6800 from close to 0.6900 overnight and AUD/NZD cross retreats through 1.1050.

- Pound down regardless of upgrades to final UK services and composite PMIs as Buck rallies broadly and BoE’s FSR flags material deterioration in global economic outlook, Cable beneath 1.2050 from circa 1.2125 peak.

- Yen holds up better than others amidst Greenback strength on risk and rate grounds; USD/JPY eyes support into 135.50 vs 136.00+ at the other extreme.

Fixed Income

- Bonds on course for a turnaround Tuesday after marked retreat from pre-weekend peaks on Independence Day.

- Bunds back above 150.00 from 148.72 low and Friday’s 151.65 high, Gilts reclaim 115.00+ status within 116.58-114.60 range and 10 year T-note above 119-00 between 119-20+/118-23 parameters.

- UK 2051 and German 2033 linker supply reasonably well received, but yields considerably higher.

In commodities

- Crude benchmarks were fairly resilient to the broader risk tone, but have most recently succumbed to the pressure and are at the lower-end of a USD 3-4/bbl range.

- Reminder, the lack of settlement due to the US market holiday is causing some discrepancy between WTI and Brent, though they are directionally moving in tandem.

- UAE’s ADNOC set Murban crude OSP for August at USD 117.53/bbl vs prev. USD 109.68/bbl in July, according to Reuters.

- Norway’s Lederne union said the strike in the Norwegian oil sector had begun, according to Reuters.

- Saudi Aramco has increased all oil prices for customers in August; sets Aug light crude OSP to Asia at +9.30/bbl vs Oman/Dubai average, according to Reuters sources; NW Europe set at +USD 5.30 vs. ICE Brent; US set at +USD 5.65 vs. ASCI.

- Russian Deputy Chair of the Security Council Medvedev says the Japanese proposal to cap Russian oil prices would lead to higher global prices, oil prices could increase to over USD 300-400/bbl, via Reuters.