by harveyorgan · in Uncategorized · Leave a comment·Edit

by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1703.05 DOWN $8.80

SILVER: $18.76 DOWN 2 CENTS

ACCESS MARKET:

GOLD $1696.70

SILVER: $18.68

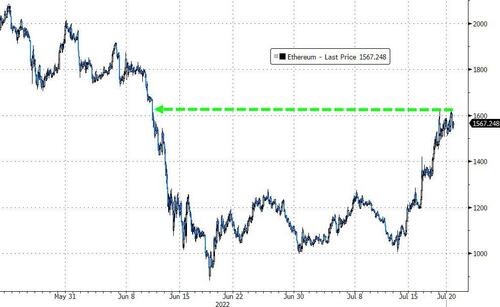

Bitcoin morning price: $23,504 UP 122

Bitcoin: afternoon price: $23,707. UP 326

Platinum price: closing DOWN $12.20 to $863.05

Palladium price; closing DOWN $2.35 at $1868.10

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,710.000000000 USD

INTENT DATE: 07/19/2022 DELIVERY DATE: 07/21/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 100

167 C MAREX 29

435 H SCOTIA CAPITAL 30

624 H BOFA SECURITIES 1547

661 C JP MORGAN 30 1702

690 C ABN AMRO 25

880 C CITIGROUP 1

TOTAL: 1,732 1,732

MONTH TO DATE: 9,214

no. of contracts issued by JPMorgan: 1732/9204

_____________________________________________________________________________________

NUMBER OF NOTICES FILED FOR JULY CONTRACT: 1732 NOTICES FOR 173,200 OZ //15.387 TONNES

total notices so far: 9214 contracts for 921,400 oz (28.659 tonnes)

SILVER NOTICES:

122 NOTICES FILED FOR 610,000 OZ/

total number of notices filed so far this month 3272 : for 16,060,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $8.80

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22

TONNES FROM THE GLD///

INVENTORY RESTS AT 1009.06 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 2 CENTS

AT THE SLV// ://HUGE CHANGES IN SILVER INVENTORY AT THE SLV//:A WITHDRAWAL OF 8.253 MILLION OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 507.585 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1450 CONTRACTS TO 145,248 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE LOSS IN OI WAS ACCOMPLISHED WITH OUR $0.14 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.14) AND WERE SUCCESSFUL IN KNOCKING OFF SOME COMMERCIAL SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS AS WE HAD A STRONG LOSS OF 1264 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A POOR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.220 MILLION OZ FOLLOWED BY TODAY’S 105,000 OZ QUEUE JUMP / // V) HUGE SIZED COMEX OI LOSS

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -1

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTACTS for 13 days, total 11,507 contracts: 57.535 million oz OR 4.423 MILLION OZ PER DAY. (885 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 57.535 MILLION OZ

.

LAST 15 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 57.535 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1450 WITH OUR $0.14 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 185 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A POOR INITIAL SILVER OZ STANDING FOR JUNE. OF 15.22 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 105,000 OZ // .. WE HAD A STRONG SIZED LOSS OF 1265 OI CONTRACTS ON THE TWO EXCHANGES FOR 6.322 MILLION OZ WITH THE LOSS IN PRICE..

WE HAD 122 NOTICES FILED TODAY FOR 610,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 6,966 CONTRACTS TO 524,786 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -192 CONTRACTS.

.

THE STRONG SIZED DECREASE IN COMEX OI CAME WITH OUR TINY FALL IN PRICE OF $0.35//COMEX GOLD TRADING/TUESDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT ADDITION ACCOMPANYING OUR HUMONGOUS SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT ADDITIONS

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JULY AT 2.914 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 1680,200 OZ

YET ALL OF..THIS HAPPENED WITH OUR TINY FALL IN PRICE OF $0.35 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A FAIR SIZED LOSS OF 3079 OI CONTRACTS 9.577 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3695 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 524,786

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3079 CONTRACTS WITH 6,774 CONTRACTS DECREASED AT THE COMEX AND 3695 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 3079 CONTRACTS OR 9.577 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3,695) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (6,966): TOTAL LOSS IN THE TWO EXCHANGES 3,271 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JULY. AT 2.914 TONNES FOLLOWED BY TODAY’S 168,200 OZ QUEUE JUMP 3) SOME LONG LIQUIDATION//CONSIDERABLE SPECULATOR SHORT ADDITIONS/ //.,4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

81,828 CONTRACTS OR 8182,800 OZ OR 254.51 TONNES 13 TRADING DAY(S) AND THUS AVERAGING: 6294 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAY(S) IN TONNES: 254/51 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 254.51/3550 x 100% TONNES 7.18% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 254.51 TONNES (HUGE INCREASE FROM JUNE//WILL CLOSE IN ON THE RECORD EFP ISSUANCE IN MARCH 22)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 1450 CONTRACT OI TO 145,248 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 185 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 185 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE:411 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1450 CONTRACTS AND ADD TO THE 185 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF 1265 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 6.322 MILLION OZ

OCCURRED DESPITE OUR SMALL DROP IN PRICE OF $0.14

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 25.29 PTS OR 0.77% //Hang Sang CLOSED UP 229.16 OR 1.11% /The Nikkei closed UP 718.58 OR % 2.67. //Australia’s all ordinaires CLOSED UP 1.78% /Chinese yuan (ONSHORE) closed DOWN AT 6.75500 /Oil UP TO 102.48 dollars per barrel for WTI and UP TO 105.80 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7550 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7570: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 6,966 CONTRACTS TO 524,786 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX DECREASE OCCURRED WITH OUR FALL OF $0.35 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A HUGE SIZED EFP (17,058 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3695 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :3695 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3695 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED SIZED TOTAL OF 3,271 CONTRACTS IN THAT 17,329 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 6966 CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR FALL IN PRICE OF GOLD $0.35.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JULY (28.712),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 28.712 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $0.35) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SOME SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A FAIR SIZED LOSS OF 9.577 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR JULY (28.712 TONNES)…

WE HAD -192 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 3,271 CONTRACTS OR 327,100 OZ OR 10.174 TONNES

Estimated gold volume 202,897/// poor/

final gold volumes/yesterday 164,536 / poor

INITIAL STANDINGS FOR JULY ’22 COMEX GOLD //JULY 20

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 112,343.726 oz Brinks HSBC |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 1732 notice(s) 173,200 OZ 5.387 TONNES |

| No of oz to be served (notices) | 17 contracts 1700 oz 0.05871 TONNES |

| Total monthly oz gold served (contracts) so far this month | 9214 notices 921,400 OZ 28.659 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

Customer deposits: 1

i) Into Brinks 26,731.160 oz

total deposits: 26,731.160 oz

3 customer withdrawals:

i)Out of HSBC 50,005.045 oz

ii)Out of Manfra: 30,299.921 oz

iii) Out of JPMorgan: 160,457.274 oz

total withdrawal: 240,762.240 oz

ADJUSTMENTS:0 dealer to customer

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 1749 contracts having GAINED 1122 contracts . We had

560 notices filed on Tuesday so we GAINED a WHOPPING 1682 contracts or an additional 168,200 oz will stand in this non active

delivery month of July.

August has a LOSS OF 11,550 contracts down to 224,545 contracts

Sept. gained 10 contracts to 2750 contracts.

We had 1732 notice(s) filed today for 173,200 oz FOR THE July 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 30 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1732 contract(s) of which notices were stopped (received) by j.P. Morgan dealer and 1702 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2022. contract month,

we take the total number of notices filed so far for the month (9214) x 100 oz , to which we add the difference between the open interest for the front month of (JULY 1749 CONTRACTS ) minus the number of notices served upon today 1732 x 100 oz per contract equals 923,100 OZ OR 28.712 TONNES the number of TONNES standing in this active month of July.

thus the INITIAL standings for gold for the JULY contract month:

No of notices filed so far (9214) x 100 oz+ (1749) OI for the front month minus the number of notices served upon today (1732} x 100 oz} which equals 921,400 oz standing OR 28.712 TONNES in this active delivery month of JULY.

TOTAL COMEX GOLD STANDING: 28.712 TONNES (A FAIR STANDING FOR A JULY ( NON ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,443,533.842 oz 76.00 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 31,570,627.446 OZ

TOTAL REGISTERED GOLD: 15,981,719.548 OZ

TOTAL OF ALL ELIGIBLE GOLD: 15,888,807.894 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 13,538,186.0 OZ (REG GOLD- PLEDGED GOLD) 421 tonnes

END

SILVER/COMEX/JULY 20

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 84,934.870 oz Loomis |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 122CONTRACT(S) 610,000 OZ) |

| No of oz to be served (notices) | 56 contracts (280,000 oz) |

| Total monthly oz silver served (contracts) | 3273 contracts 16,060,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

total deposit: nil oz

JPMorgan has a total silver weight: 176.879 million oz/342.347 million =51.67% of comex

Comex withdrawals:1

i) Out of Loomis

total withdrawal 84,934.870 oz

adjustments: 1/dealer to customer jpm

312,407.190 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 61.440 MILLION OZ

TOTAL REG + ELIG. 342.347 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JULY OI: 178 CONTRACTS HAVING GAINED 8 CONTRACTS. WE HAD 13 NOTICES FILED

ON TUESDAY, SO WE GAINED 21 CONTRACTS OR AN ADDITIONAL 105,000 OZ WILL STAND FOR METAL AT THE COMEX.

AUGUST LOST 113 CONTRACTS TO STAND AT 997

SEPTEMBER HAD A LOSS OF 1342 CONTRACTS DOWN TO 117,302

CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 122 for 610,000 oz

Comex volumes:41,599// est. volume today// poor

Comex volume: confirmed yesterday: 39,353 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 3273 x 5,000 oz = 16 060,000 oz

to which we add the difference between the open interest for the front month of JULY(178) and the number of notices served upon today 122 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY./2022 contract month: 3273 (notices served so far) x 5000 oz + OI for front month of JULY (178) – number of notices served upon today (122) x 5000 oz of silver standing for the JULY contract month equates 16,645,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

JULY 18/WITH GOLD UP $7.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.28 TONNES

JULY 15/WITH GOLD DOWN $3.75:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD///INVENTORY RESTS AT 1016.89 TONNES//

JULY 14/WITH GOLD DOWN $28.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD//INVENTORY RESTS AT 1019.79 TONNES

JULY 13/WITH GOLD UP $10.55:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROMTHE GLD//INVENTORY RESTS AT 1021.53TONNES

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

JULY 11/WITH GOLD DOWN $4.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWL OF 1.16 TONNES FROM THE GLD./INVENTORY RESTS AT 1023.27 TONNES

JULY 7/WITH GOLD UP $1.35: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.61 TONNES FORM THE GLD///INVENTORY REST AT 1024.43 TONNES

JULY 6/WITH GOLD DOWN $26.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 9.86 TONNES FROM THE GLD//INVENTORY REST AT 1032.04 TONNES

JULY 5/WITH GOLD DOWN $36.55//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.41 TONNES FROM THE GLD///INVENTORY RESTS AT 1041.90 TONNES

JULY 1/WITH GOLD DOWN $5.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES//INVENTORY RESTS AT 1050.31 TONNES

JUNE 30/WITH GOLD DOWN $9.20: big CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 1052.63 TONNES//

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

JUNE 21/WITH GOLD DOWN $2.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1075.54 TONES

JUNE 17/WITH GOLD DOWN $11.25: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.60 TONNES INTO THE GLD.///INVENTORY RESTS AT 1075.54 TONNES

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

GLD INVENTORY: 1009.06 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

JULY 18/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 4.995 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ.

JULY 15/WITH SILVER UP 31 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 3.226 MILLLION OZ FORM THE SLV//INVENTORY RESTS AT 510.443 MILLIONOZ//

JULY 14/WITH SILVER DOWN 88 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 OZ FROM THE SLV// //INVENTORY RESTS AT 513.671 MILLION OZ

JULY 13/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SV//INVENTORY RESTS AT 514.501 MILLION OZ.

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A IWTHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

JULY 11/WITH SILVER DOWN 17 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 5.533 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 517.729 MILLION OZ

JULY 7/WITH SILVER UP 3 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.889 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 523.262 MILLION OZ/

JULY 6/WITH SILVER UP ONE CENT: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 12.558 MILLION OZ FORM THE SLV///INVENTORY RESTS AT 528.151 MILLION OZ

JULY 5/WITH SILVER DOWN 55 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 540.709MILLION OZ//

JULY 1/WITH SILVER DOWN 61 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ//INVENTORY RESTS AT 540.709 MILLION OZ//

JUNE 30/WITH SILVER DOWN 41 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 738,000 OZ FROM THE SLV//INVENTORY RESTS AT 541.262 MILLION OZ//

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

JUNE 21/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 547.166 MILLION OZ//

JUNE 17/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 739,000 OZ FROM THE SLV./:INVENTORY RESTS AT 543.660 MILLION OZ/

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

CLOSING INVENTORY 507.585 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

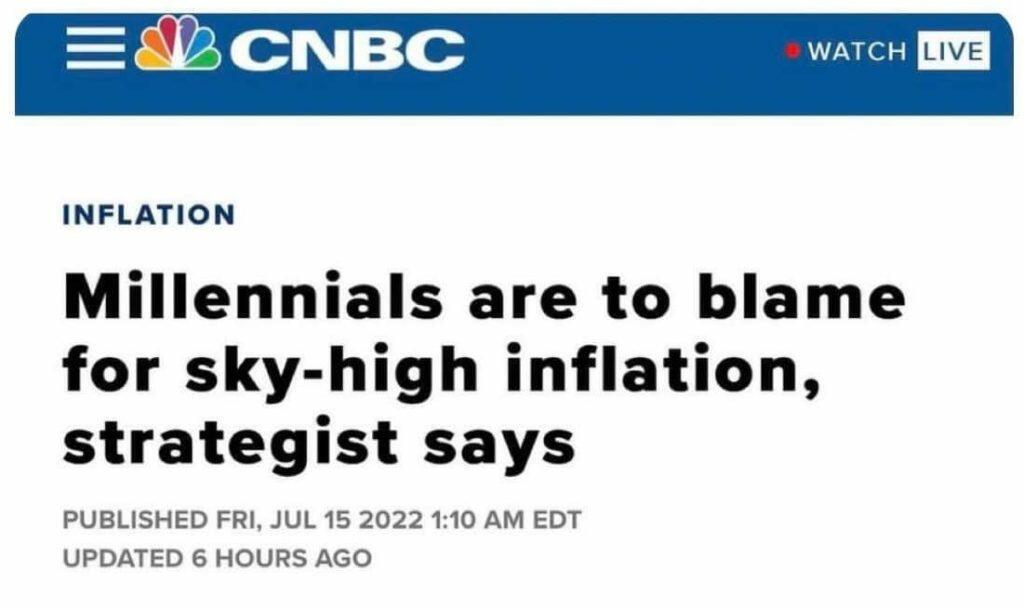

Now Inflation Is The Millennials’ Fault! Or Is It?

WEDNESDAY, JUL 20, 2022 – 12:45 PM

Authored by Michael Maharrey via SchiffGold.com,

Putin is causing inflation. Greedy corporations are causing inflation. COVID-19 caused inflation. We hear all kinds of reasons for the recent spike in prices. And now we have a new one. It’s the millennials’ fault.

This is all wrong and it illustrates the problem with redefining inflation to be something it isn’t.

Smead Capital Investment chief investment officer Bill Smead told CNBC the size of the millennial generation is causing inflation.

“See, what everyone is not including in the conversation is what really causes inflation, which is too many people with too much money chasing too few goods,” he said, explaining that there are roughly 92 million millennials.

“So we have in the United States a whole lot of people, 27 to 42, who postponed home buying, car buying, for about seven years later than most generations. But in the past two years, they’ve all entered the party together,” he said.

Smead actually gets closer to the cause of inflation than most. He at least recognizes that more dollars chasing the same amount of goods and services causes prices to rise. But he leaves the key question unanswered – where are these people getting all of these extra dollars?

If the number of dollars along with the number of goods and services in the system remained stable, rising spending by one generation would necessarily correlate with declining spending in others. As millennials consumed more stuff, there would be less stuff for other people in the other generations to purchase. Prices would remain stable.

More realistically, the larger generation would produce more stuff, adding to the inventory of goods and services. In a stable monetary environment, prices would generally fall as the larger generation produced additional wealth.

But as Smead explains it, the millennials apparently aren’t producing more. But somehow they have more dollars. Meanwhile, every other generation still has the same number of dollars and they continue to spend at the same pace. Therefore we have all of these extra millennial dollars chasing the same amount of stuff.

Voila — inflation!

But it seems like maybe Smead is leaving out a key player in this scenario.

He is — the Federal Reserve.

The only way millennials can have more dollars without taking dollars from other generations is if somebody is creating new dollars. That somebody, of course, is the Fed.

The Root of the Problem

Somehow, the Fed manages to escape scrutiny in any mainstream discussion of inflation. But the central bank is the root of the problem.

The Fed creating trillions of dollars out of thin air over the last couple of years and injecting them into the economy is the primary reason we see consumer prices spiking through the roof today. Yes, oil price shocks, supply chain issues and other factors drive up prices in certain sectors, but the Fed monetary policy lies behind the more general rise in prices.

The federal government also played a role. In the first place, the US government needed the Fed to monetize its pandemic borrowing and spending spree. Meanwhile, both Trump and Biden administrations took a lot of the newly created money and showered it on consumers with stimulus checks. That put money in people’s pockets even as they were sitting at home producing nothing.

So, how did millennials spend a bunch of money while they weren’t working? The Fed “printed” it and the government gave it to them.

The Fed is the engine that drives it all. The central bank creates the dollars. Without all of those extra dollars, people couldn’t have “too much money” to chase too few goods, as Smead explains it.

One question remains — how does the Fed manage to get off scot-free in every inflation discussion when its policies drive inflation?

Because the politicians, bureaucrats, central bankers and mainstream media pundits have successfully redefined inflation.

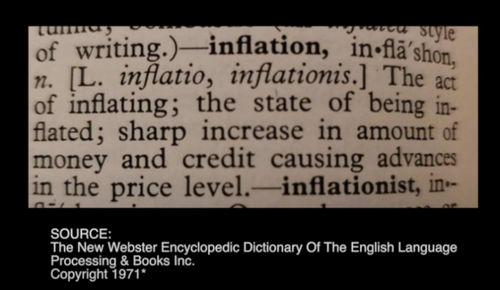

Getting the Definition Right

When people use the term “inflation” today, they mean rising consumer prices as measured by the Consumer Price Index (CPI). You’ll often hear CPI referred to as “an inflation measure.”

But rising prices aren’t inflation. They are a symptom of inflation.

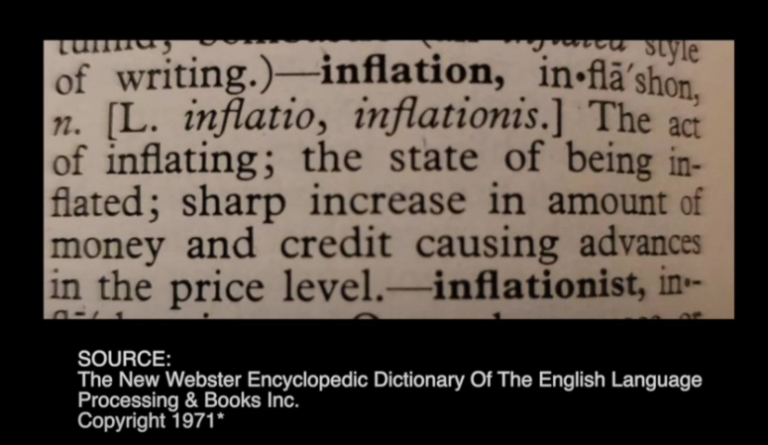

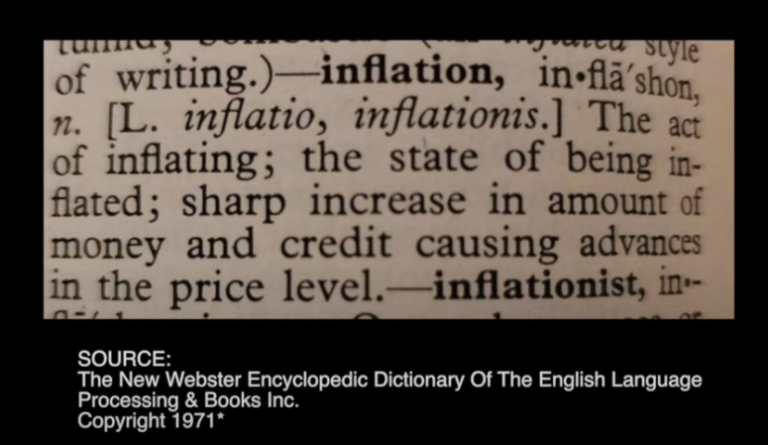

Look at this definition of inflation from a 1971 dictionary.

Notice that the definition mentions rising prices, but only as a symptom of inflation. Inflation itself is defined as “an increase in the amount of money and credit.”

Over the years, the government, along with its apologists in the corporate media and academia, altered the definition to suit government purposes. The standard definition of inflation bandied about today is nothing more than government propaganda.

Why does the government want to define inflation as rising prices?

Because the modern definition allows policymakers to shift the blame. If we use the original definition of inflation as an “expansion of the supply of money,” the culprit becomes clear. Who expands the supply of money? It’s the Fed and the government. So, if you accurately define inflation, you know exactly who’s to blame. But if the government can fool people into believing that an effect of inflation is inflation, they can blame it on whoever, or whatever, is raising the prices – Putin, pandemics and apparently millennials.

The original definition of inflation is the key to understanding inflation. When you misdefine inflation as rising prices, bad monetary policy and bad fiscal policy go on unchallenged.

The inflation blame game is great for the powers that be. It’s not so great for you or me.

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

3. Chris Powell of GATA provides to us very important physical commentaries

Chris Powell is right. Who in their right mind would want Lira. They will take Russian roubles or

Chinese yuan for payment, but not lira.

(Bloomberg/GATA))

Turkey looks to ditch dollar in payments for Russian energy

Submitted by admin on Tue, 2022-07-19 16:23Section: Daily Dispatches

But who really wants Turkish lira?

* * *

By Firat Kozok

Bloomberg News

Tuesday, July 19, 2022

Turkey’s President Recep Tayyip Erdogan will discuss paying for Russian energy imports with currencies other than the U.S. dollar when he meets his Russian counterpart, Vladimir Putin, in Tehran today, according to Turkish officials familiar with the matter.

The two countries have been working on a proposal for local-currency trade payments, including for energy deals, a move that would help the government in Ankara slow the decline in its sovereign reserves, the officials said. …

… For the remainder of the report:

end

Ronan Manly: Why is a criminal organization allowed to dominate the gold industry?

Submitted by admin on Wed, 2022-07-20 11:02Section: Daily Dispatches

By Ronan Manly

Bullion Star, Singapore

Wednesday, July 20, 2022

With a group of former JP Morgan precious metals traders currently on criminal trial in front of a federal jury in Chicago, accused of engaging in a racketeering conspiracy involving precious metals price manipulation, commodities fraud, and trade spoofing, while another group of their colleagues has already pleaded guilty, now is a good time to ask how the bank JP Morgan is still considered fit and proper to not only continue to trade in the precious metals markets but also to continue to dominate the entire precious metals industry in London, Singapore, and New York, with the support of the London Bullion Market Association, the Singapore Bullion Market Association, and the CME Group, operator of the Comex and NYMex.

While JP Morgan made a deferred prosecution deal with the U.S. Department of Justice and Commodity Futures Trade Commission in 2020 and admitted wrongdoing for the criminal conduct of numerous JP Morgan traders and sales personnel on the bank’s precious metals desks in London, Singapore, and New York, while paying $920 million in the form of a criminal monetary penalty, criminal disgorgement, and victim compensation in relation to this criminal precious metals scheme, the LBMA, SBMA, and CME Group, as you will see below, continue not only to welcome the proven criminal bank JP Morgan but to allow it to operate at the highest levels of each organisation. …

… For the remainder of the commentary:

* * *

end

(GATA) Financial letter editor Jay Taylor interviews GATA secretary

11:27a ET Wednesday, July 20, 2022

Dear Friend of GATA and Gold:

Your secretary/treasurer discussed GATA’s work yesterday with Jay Taylor, editor of J. Taylor’s Gold, Energy, and Tech Stocks letter, on his “Turning Hard Times Into Good Times” internet radio program. The main point of the discussion was that gold market manipulation is no mere “conspiracy theory” but longstanding Western government policy extensively documented in government archives and statements and memoirs by central bankers.

The discussion is 18 minutes long and can be heard at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

(GATA) Robert Lambourne: BIS gold swaps keep falling sharply, down 60% in six months

By Robert Lambourne

Wednesday, July 20, 2022

Gold swaps undertaken by the Bank for International Settlements, the major gold broker for central banks, fell substantially again in June, this time by 68 tonnes, bringing the bank’s total swaps down to 202 tonnes from the 501 tonnes on the bank’s books in January, a decline of nearly 60% in six months.

The bank’s June statement of account is posted here:

https://www.bis.org/banking/balsheet/statofacc220630.pdf< /B>

The June total of swaps is the bank’s lowest since October 2019.

Again it is evident that the BIS remains an active trader of large volumes of gold swaps on a regular basis, and the recent data suggests that a downward trend in its swaps is continuing. If the current rate of decline is maintained, the BIS may be reporting zero gold swaps later this year.

The trend may indicate a response by the BIS and bullion banks to implementation of “Basel III” regulations, which make the unallocated gold business more burdensome for bullion banks.

The BIS rarely comments publicly on its gold activities, but its first use of gold swaps was considered important enough to cause the bank to give some background information to the Financial Times for an article published July 29, 2010, coinciding wit h publication of the bank’s 2009-10 annual report.

The general manager of the BIS at the time, Jaime Caruana, said the gold swaps were “regular commercial activities” for the bank, and he confirmed that they were carried out with commercial banks and so did not involve central banks. It also seems highly likely that the BIS’ remaining swaps are still all made with commercial banks, because the BIS annual report has never disclosed a gold swap between the BIS and a major central bank.

The swap transactions potentially create a mismatch at the BIS, which may end up being long unallocated gold (the gold held in BIS sight accounts at major central banks) and short allocated gold (the gold required to be returned to swap counterparties). This possible mismatch has not been reported by the BIS.

The gold banking activities of the BIS have been a regular part of the services it offers to central banks since the establishment of the bank 90 years ago. The first annual report of the BIS explains these activities in some detail:

http://www.bis.org/publ/arpdf/archive/ar1931_en.pdf

A June 2008 presentation made by the BIS to potential central bank members at its headquarters in Basel, Switzerland, noted that the bank’s services to its members include secret interventions in the gold and foreign exchange markets:

https://www.gata.org/node/11012

The use of gold swaps to take gold held by commercial banks and then deposit it in gold sight accounts held in the name of the BIS at major central banks doesn’t appear ever to have been as large a part of the BIS’ gold banking business as it has been in recent years.

As of March 31, 2010, excluding gold owned by the BIS, there were 1,706 tonnes held in gold sight accounts at major central banks in the name of the BIS, of which 346 tonnes or 20% were sourced from gold swaps from commercial banks.

The BIS now operates a much smaller gold banking business, with an estimated 611 tonnes of gold deposited in gold sight accounts as of 30 June. (This excludes 102 tonnes of the gold owned by the BIS itself.)

The present-day role of gold swaps in this smaller business is reducing sharply as the volume of swaps falls. In June the gold held in sight accounts on behalf of the BIS was about 33% provided by gold swaps. In May, excluding the 102 tonnes of gold owned by the BIS, some 39% of the gold held in sight accounts at major central banks on behalf of the BIS came from gold swaps instead of from other central banks.

If the BIS was adopting the degree of disclosure made by publicly held companies, such as commercial banks, some explanation of these changes probably would have been required by the accounting regulators. This irony may not be lost on those dealing with reg ulatory activities at the BIS. Presumably the shrinkage of the BIS’ gold banking business shows that even central banks now prefer to hold their own gold or hold it in earmarked form — that is, as allocated gold.

A review of Table B below highlights recent BIS activity with gold swaps, and despite the recent declines, the latest position estimated from the BIS monthly statements remains large and the volume of trades is significant.

No explanation for this continuing use of swaps has been published by the BIS. Indeed, no comment on the bank’s use of gold swaps has been offered since 2010.

This gold is supplied by bullion banks via the swaps to the BIS. The gois then deposited in BIS gold sight accounts (unallocated gold accounts) at major central banks such as the Federal Reserve.

The reasons for this activity have never been fully explained by the BIS and various conjectures have been made as to why the BIS is facilitating it. One conjecture is that the swaps are a mechanism for gold secretly supplied by central banks to cover shortfalls in the gold markets to be returned to the central banks. The use of the BIS to facilitate this trade suggests of a desire to conceal the rationale for the transactions.

As can be seen in Table A below, the BIS has used gold swaps extensively since its financial year 2009-10. No use of swaps is reported in the bank’s annual reports for at least 10 years prior to the year ended March 2010.

The February 2021 estimate of the bank’s gold swaps (552 tonnes) is higher than any level of swaps reported by the BIS at its March year-end since March 2010. The swaps reported at March 2021 are at the highest year-end level reported, as is clear from Table A.

Table A Swaps reported in BIS annual reports

March 2010: 346 tonnes.

March 2011: 409 tonnes.

March 2012: 355 tonnes.

March 2013: 404 tonnes.

March 2014: 236 tonnes.

March 2015: 47 tonnes.

March 2016: 0 tonnes.

March 2017: 438 tonnes.

March 2018: 361 tonnes.

March 2019: 175 tonnes

March 2020: 326 tonnes

March 2021: 490 tonnes

—–

The table below reports the estimated swap levels since August 2018. It can be seen that the BIS is actively involved in trading gold swaps and other gold derivatives with changes from month to month reported in excess of 100 tonnes in this period.

Table B – Swaps estimated by GATA from BIS monthly statements of account

Month … Swaps

& year … in tonnes

Jun-22 … /202

May-22 … /270

Apr-22 ….. /315

Mar-22 …. /360

Feb-22 …. /472

Jan-22 ….. /501

Dec-21…. /414

Nov-21…. /451

Oct-21…. /414

Sep-21 …. /438

Aug-21 …. /464

Jul-21 …. /502

Jun-21 …./471

May-21 …./517

Apr-21 …. /472

Mar-21…. /490

Feb-21 …../552

Jan-21 …. /523

Dec-20 …. /545

Nov-20 …. /520

Oct-20 …. /519

Sep-20…../ 520

Aug-20…../ 484

Jul-20 ….. / 474

Jun-20 …. / 391

May-20 …. / 412

Apr-20 …. / 328

Mar-20 …. / 326*

Feb-20 …. / 326

Jan-20 …. / 320

Dec-19 …. / 313

Nov-19 …. / 250

Oct-19 …. / 186

Sep-19 …. / 128

Aug-19 …. / 162

Jul-19 ….. / 95

Jun-19 …. / 126

May-19 …. / 78

Apr-19 ….. / 88

Mar-19 …. / 175

Feb-19 …. / 303

Jan-19 …. / 247

Dec-18 …. / 275

Nov-18 …. / 308

Oct-18 …. / 372 Sep-18 …. / 238

Aug-18 …. / 370

The estimate originally reported by GATA was 487 tonnes, but the BIS annual report states 490 tonnes, It is believed that slightly different gold prices account for the difference.

* The estimate originally reported by GATA was 332 tonnes, but the BIS annual report states 326 tonnes. It is believed that slightly different gold prices account for the d ifference.

GATA uses gold prices quoted by USAGold.com to estimate the level of gold swaps held by the BIS at month-ends.

—–

As noted already, the BIS in recent times has refused to explain its activities in the gold market, nor for whom the bank is acting:

https://www.gata.org/node/17793

Despite this reticence the BIS is almost certainly acting on behalf of central banks in taking out these swaps, as they are the BIS’ owners and control its Board of Directors.

This refusal to explain prompts some observers to believe that the BIS acts as an agent for central banks intervening surreptitiously in the gold and currency markets, providing those central banks with access to gold as well as protection from exposure of their interventions.

A recent report published by Bullion Star’s Ronan Manly on the Bank of Portugal’s use of its gold reserves reinforces this point as the Bank of Portugal confirms that 20 tonnes of its gold is stored with the BIS:

https://www.gata.org/node/21950

This disclosure seems a little economic with the truth as the BIS has no gold storage facilities of its own. Gold held by the BIS on behalf of central banks is either deposited into a BIS gold sight (unallocated) account or a BIS earmarked (allocated) gold account and deposited normally with one of the central banks based at a major gold trading center, such as the Federal Reserve in New York.

Since Manly shows that the Bank of Portugal is focused on earning income from its gold, it seems highly likely that this gold is held in a BIS sight account, though its ultimate location is unclear.

It is possible that the swaps provide a mechanism for bullion banks to return gold original ly lent to them by central banks to cover bullion bank shortfalls of gold. Some commentators have suggested that a portion of the gold held by exchange-traded funds and managed by bullion banks is sourced directly from central banks.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the involvement of the Bank for International Settlements in the gold market.

END

4. OTHER GOLD/SILVER COMMENTARIES

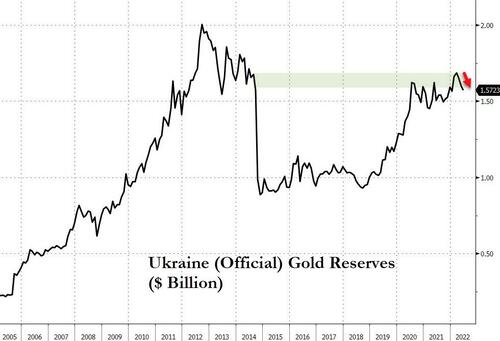

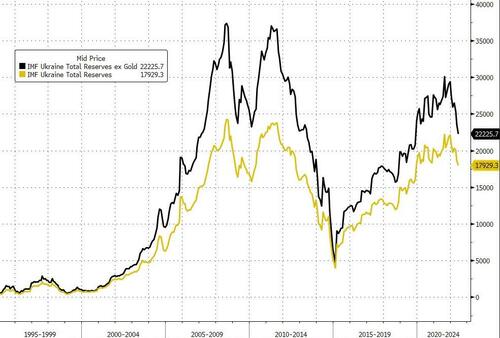

The Ukrainian gold has long been leased out. The total amount of gold held by Ukraine prior to 2014 was 43 tonnes or 1 billion dollars. They did not sell $12 billion dollars worth of gold because they did not have that quantity

(Peter Schiff/zerohedge)

The Price Of ‘Liberation’: Is Ukraine Dumping Its Gold Again?

WEDNESDAY, JUL 20, 2022 – 05:45 AM

It’s “Murky”.

That’s how Peter Schiff describes what is going on with regard Ukraine’s gold reserves currently, and as you’ll see below, he is somewhat understating the uncertainty.

But first, some history…

In March 2014, we wrote about a mysterious operation that took place under the cover of night that sources claimed at the time saw Ukraine’s gold reserves loaded on an unmarked plane, which reportedly took the gold to the US (for safekeeping?).

In the following few months – after we reported this outbound flow – Ukraine’s official (IMF-sourced) holdings of gold collapsed…

There has been no denials of this report since.

With that in mind, Reuters reported that, on Sunday, Ukraine National Bank (UNB) Deputy Governor Kateryna Rozhkova said on national television that the UNB had sold $12.4 billion of gold reserves since the beginning of Russia’s invasion on Feb. 24.

“We are selling (this gold) so that our importers are able to buy necessary goods for the country,” Rozhkova said.

She said the gold was not being sold to shore up Ukraine’s hryvnia currency.

There’s just one problem:

Ukraine doesn’t have $12 billion in gold reserves (according to official IMF data at the end of June).

As Peter Schiff explains, it remains unclear how Ukraine sold so much gold.

When the Russians invaded, UNB held about 27 tons of gold in its reserves valued at about $1.6 billion, according to the WGC.

In other words, according to Rozhkova, the central bank has sold more than 7 times its total gold holdings.

That’s not to say Rozhkova’s statement was misleading.

The country could be tapping into domestic gold supplies held by commercial banks or other institutions. PrivatBank ranks as the largest commercial bank in Ukraine. It was nationalized in 2016.

It’s also possible that other countries or private entities gave Ukraine gold to sell. Countries around the world have sent billions in aid to the Ukrainian government. For example. earlier this month, Sweeden sent 577.7 million SEK to Ukraine. That’s over $55.5 million USD and 1.5 billion UAH.

Less likely is a quick ramp-up in mine production. According to a Mining World report, Ukraine sits on nearly 3,000 tons of gold but the country had few operating mines before the invasion.

Regardless of the mechanism involved, it’s clear that Ukraine is relying on gold sales as an important source of currency as the war drags on.

The thot plickens though (or was Rozhkova caught in a lie?)…

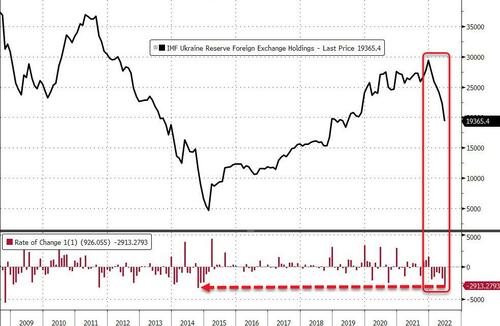

This morning, Bloomberg reports that Rozhkova denied saying that last week and in fact the money came from FX reserves, not gold…

“We were selling foreign currency from our reserves to carry out transactions on our overseas trade contracts and with payment systems.”

Rozhkova explained in a text message that the UNB spent $12b from international reserves to fulfill foreign contracts since Russia’s invasion but also saw $10b inflow during the period (likely mainly from US taxpayers).

Overall, Ukraine’s FX reserves are down considerably this year as exports sink and military spending surges…

“Nowadays a significant pressure on reserves is being caused by the National Bank’s financing of the budget,” central bank Deputy Governor Serhiy Nikolaychuk said by email to Bloomberg News Thursday.

“If there were political will, this financing could be minimized and even stopped via redistribution of the country’s financial flows, and we believe it needs to be done.”

What is rather odd though – and we truly have no explanation for this – is that, according to official IMF data via Bloomberg, Ukraine’s total reserves ex-gold are higher than Ukraine’s total reserves…?

Is Ukraine ‘over-lending’ gold it doesn’t have?

Finally, some reports suggested that Ukraine’s gold has been ‘relocated’ to Poland.

Deputy Head of the National Bank of Ukraine Sergey Nikolaychuk said in an interview with Rabbit Hole magazine that Kyiv sends Ukraine’s gold and foreign exchange reserves to Poland, where they will be stored until the situation normalizes.

At the same time, he did not disclose either the volumes of these same reserves, or what they are. Apparently, this is not about physical gold, but about security.

This action suggests that the leadership of Ukraine is far less optimistic about its own and the country’s prospects in the war with Russia than Zelensky proclaims to the world.

So there we have it – UNB officials said they sold 7 times the amount of gold they have in reserves… then denied it.

Is this ‘relocation’ the cost of the new ‘liberation’? “Murky” indeed…

END

5.OTHER COMMODITIES:

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7550

OFFSHORE YUAN: 6.7570

HANG SANG CLOSED UP 229.16 PTS OR 1.11%

2. Nikkei closed UP 718.56 OR 2.67%

3. Europe stocks CLOSED ALL RED

USA dollar INDEX DOWN TO 106.85/Euro FALLS TO 1.0187

3b Japan 10 YR bond yield: RISES TO. +.244/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 138.14/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN -// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.147%/Italian 10 Yr bond yield FALLS to 3.34% /SPAIN 10 YR BOND YIELD FALLS TO 2.30%…

3i Greek 10 year bond yield FALLS TO 3.38//

3j Gold at $1709.60 silver at: 18.82 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 50/100 roubles/dollar; ROUBLE AT 54.98

3m oil into the 102 dollar handle for WTI and 105 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 138.14DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9702– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9886well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.974 DOWN 5 BASIS PTS

USA 30 YR BOND YIELD: 3.140 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.59

Overnight: Newsquawk and Zero hedge:

Newsquawk:

BTPs bolstered on Draghi’s speech while equities are steady with earnings ahead – Newsquawk US Market Open

WEDNESDAY, JUL 20, 2022 – 06:41 AM

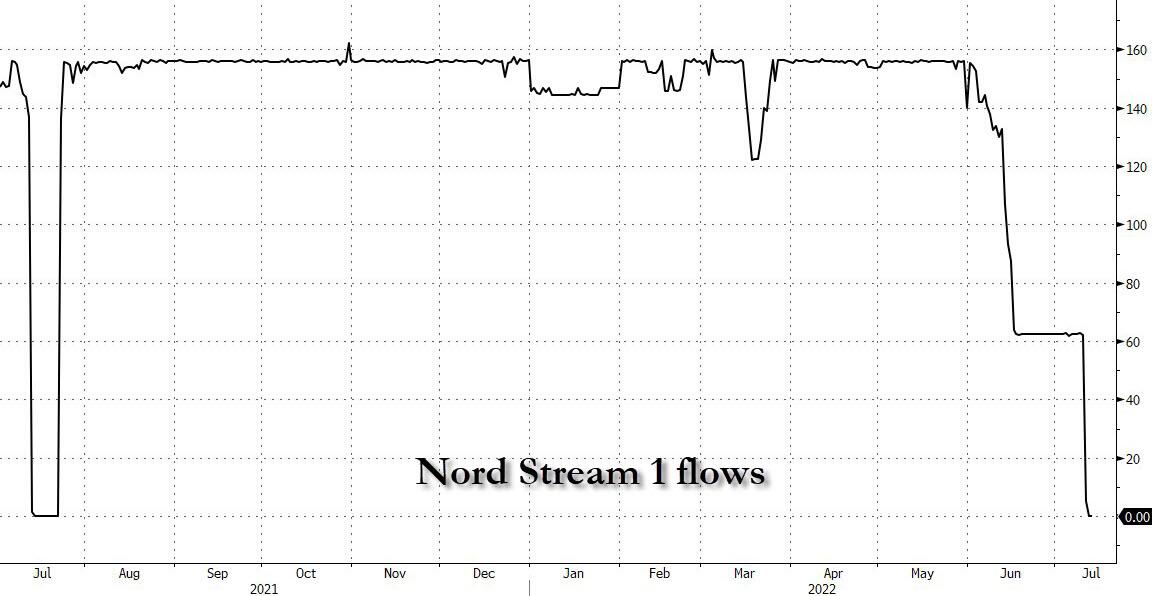

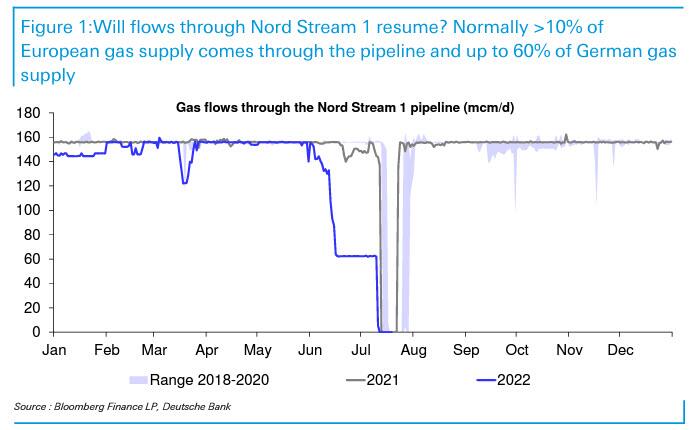

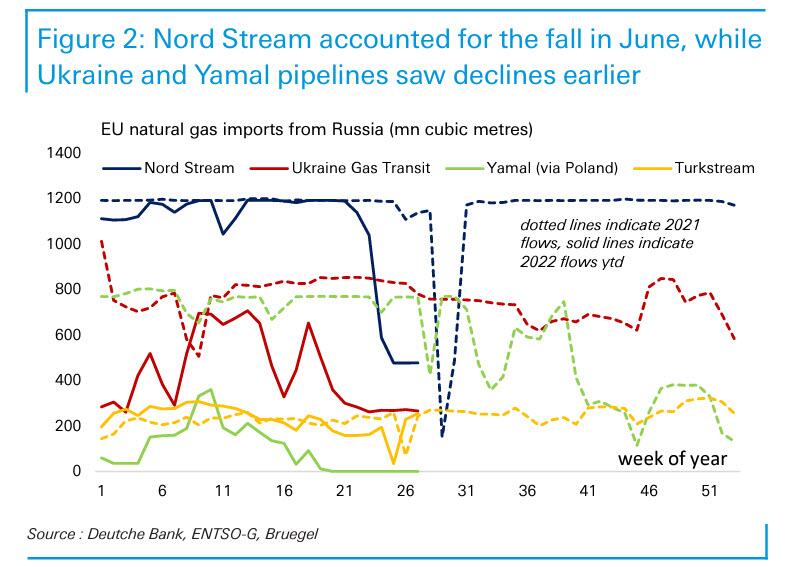

- European bourses are modestly firmer at present as we move towards the week’s key risk events and as participants had already reacted to the Nord Stream developments.

- US futures similarly contained before further earnings releases, including Tesla after-hours.

- The USD is pressured though the DXY has marginally reclaimed 106.50 with peers eking marginal upside.

- Core debt continues to climb and BTPs lead the way after Draghi’s initial Senate speech; US 20yr due

- Commodities continue to consolidate, with newsflow not changing the narrative and focused on familiar themes thus far

- Looking ahead, highlights include Canadian CPI, US Existing Home Sales, New Zealand Trade Balance, Supply from the US and Earnings from Abbott & Tesla.

As of 11:05BST/06:05ET

For the full report and more content like this check out Newsquawk

Try a 14 day trial with Newsquawk and hear breaking trading news as it happens.

LOOKING AHEAD

- Canadian CPI, US Existing Home Sales, New Zealand Trade Balance, Supply from the US, Earnings from Abbott & Tesla.

GEOPOLITICS

RUSSIA-UKRAINE

- Russian President Putin said Saudi Arabia and UAE are offering mediation in Ukraine talks and Russia doesn’t see a desire from Ukraine to stick to the preliminary agreed deal in March, according to Reuters.

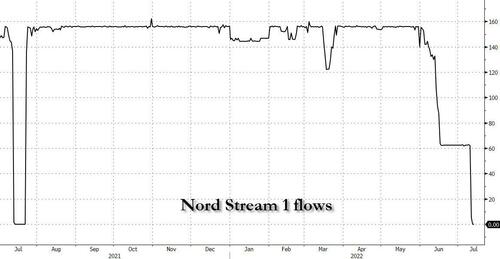

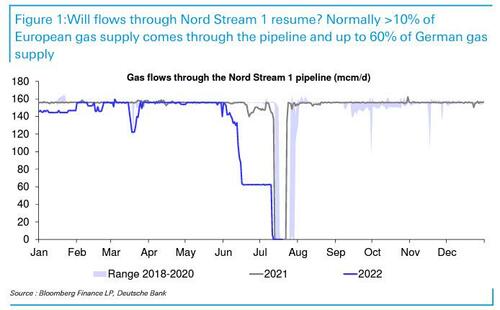

- German government spokesperson says working on the assumption gas will flow again following the Nord Stream 1 maintenance. Subsequently,

- Russia’s Gazprom says it still has not received documentation from Siemens (SIE GY) regarding the Nord Stream 1 pipeline*

- EU is reportedly planning a temporary suspension of tariffs on fertilizer imports, via Bloomberg.

CENTRAL BANKS

- RBI is prepared to spend another USD 100bln to prevent runaway Rupee depreciation, according to Reuters sources; not trying to protect a particular level, buy will not allow jerky movements.

EUROPEAN TRADE

EQUITIES

- European bourses are modestly firmer at present as we move towards the week’s key risk events and as participants had already reacted to the Nord Stream developments.

- Stateside, futures are posting similar price action with key earnings including Tesla on the docket; aside from corporate developments, the US-specific docket is slim.

- German government will pass on some energy costs to consumers, as a component of the Uniper (UN01 GY) rescue package, according to Reuters sources. Subsequently, Handelsblatt reports Germany could take a 30% stake in Uniper.

- Air India is said to be moving toward USD 50bln jet order, to be shared between Airbus (AIR FP) and Boeing (BA), but no deal seen at the Farnborough show, according to Reuters sources.

- Click here for more detail.

FX

- Kiwi extends gains vs Greenback ahead of NZ trade data amidst favourable AUD/NZD cross flows and as Aussie loses momentum against Buck, NZD/USD hovers around 0.6250, AUD/NZD circa 1.1050 and AUD/USD just over 0.6900.

- DXY attempts to draw line in sand and hold around 106.500 before US existing home sales and 20 year note auction.

- Sterling regains 1.2000+ status vs Dollar after post-UK CPI setback.

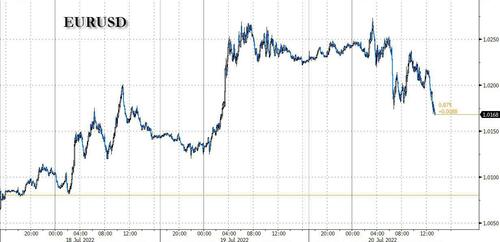

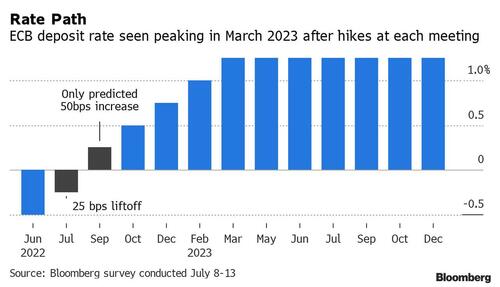

- Euro elevated on eve of 50-50 half or quarter point ECB hike policy meeting, EUR/USD straddles 1.0250.

- Loonie stalls into Canadian inflation update and Yen pauses as BoJ starts two-day policy confab, USD/CAD holds above 1.2850 and USD/JPY off sub-138.00 low.

- Click here for more detail.

Notable FX Expiries, NY Cut:

- USD/JPY: 137.00 (625M), 137.75 (835M), 139.00 (1.05BN), 140.00 (705M)

- Click here for more detail.

FIXED INCOME

- Bonds lay down firm foundations for midweek revival.

- Bunds up to 151.89 from 150.83 low, Gilts recover from 114.67 to reach 115.59 and 10 year T-note touches 118-10 vs 117-27 overnight low ahead of data and 20 year supply.

- BTPs even more resurgent between 124.79-122.84 parameters after Italian PM Draghi’s pre-Senate debate speech.

- Click here for more detail.

COMMODITIES

- Crude benchmarks are modestly softer after Tuesday’s firmer settlement, newsflow has been relatively sparse and focused on, but not adding much, to recent Nord Stream updates ahead of the maintenance period concluding on Thursday.

- US Private Inventory Data (bbls): Crude +1.9mln (exp. +1.4mln), Gasoline +1.3mln (exp. +0.1mln), Distillate -2.2mln (exp. +1.2mln), Cushing +0.5mln.

- Qatar sold September-loading Al-Shaheen crude at USD 9-10/bbl above Dubai quotes which is the highest premium in four months, according to sources.

- India cut the windfall tax on diesel and aviation fuel shipments by INR 2/litre and cut taxes on domestically produced crude to INR 17k/ton.

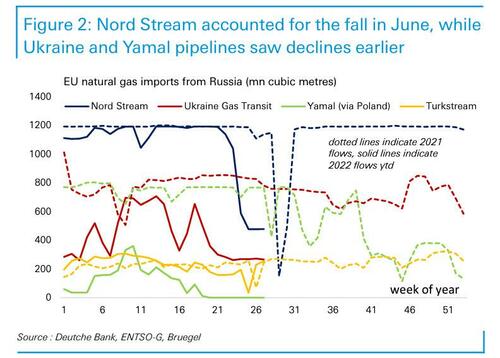

- Russian President Putin said Gazprom plans to fulfil its obligations and that there are no grounds for Ukraine to shut down one of the gas transit routes to Europe, while he added that one more Nord Stream 1 turbine is expected to be sent for maintenance later this month and that Gazprom is ready to pump gas as much as needed. Furthermore, Putin said attempts to cap Russian oil prices will lead to prices skyrocketing and said Nord Stream volume will drop if the turbine return is delayed, according to Reuters.

- Spot gold has been slightly choppy, extending to incremental new highs and lows during European hours, though fairly steady above USD 1700/oz overall.

- Click here for more detail.

NOTABLE EUROPEAN HEADLINES

- Italian PM Draghi asks parties if they are prepared to rebuild their pact. Says unfortunately political parties have growing desire for division, last week’s confidence vote marked the end of the trust in the coalition. The only way to stay together is to rebuild our pact, Italian public is asking for. Need to move towards the introduction of a minimum wage.

- Click here for newsquawk analysis on the overall situation and here for a brief summary on the next focus points.

NOTABLE EUROPEAN DATA:

- UK CPI YY (Jun) 9.4% vs. Exp. 9.3% (Prev. 9.1%); MM (Jun) 0.8% vs. Exp. 0.7% (Prev. 0.7%)

- Core CPI YY (Jun) 5.8% vs. Exp. 5.8% (Prev. 5.9%); MM (Jun) 0.4% vs. Exp. 0.5% (Prev. 0.5%)

NOTABLE US HEADLINES

- USTR is to announce the US is requesting dispute settlement consultations with Mexico under the USMCA trade agreement with the request related to measures taken by Mexico in the energy sector which undermine US companies and US-produced energy, according to Reuters.

CRYPTO

- Bitcoin continues to extend on recent levels, lifting incrementally to a USD 23.8k high.

APAC TRADE

- APAC stocks followed suit to the gains in the EU and the US where sentiment was underpinned by Nord Stream optimism and a weaker buck.

- ASX 200 was led higher by tech outperformance and with miners firmer after further quarterly output updates.

- Nikkei 225 gained with the BoJ expected to stick with ultra-loose policy at its 2-day policy meeting.

- Hang Seng and Shanghai Comp. conformed to the heightened risk appetite with tech encouraged despite reports Chinese authorities will fine Didi more than USD 1bln over data security breaches, as this ends a year-long investigation and paves the way for a Hong Kong listing. However, gains were somewhat capped in the mainland after the PBoC maintained its Loan Prime Rates which was as expected but disappointed outside calls for a cut to the 5yr LPR to assist with the ongoing mortgage strike issue, while China’s daily COVID cases surpassed 1,000 for the first time since May.

- China Evergrande (3333 HK) is yet to reach a deal with foreign bondholders over restructuring, according to WSJ sources.

NOTABLE APAC HEADLINES

PBoC 1-Year Loan Prime Rate (Jul) 3.70% vs Exp. 3.70% (Prev. 3.70%)

- PBoC 5-Year Loan Prime Rate (Jul) 4.45% vs Exp. 4.45% (Prev. 4.45%)

- Chinese Premier Li said China is to keep macro policies consistent and targeted, while he added that as long as employment is relatively sufficient, household income grows and prices are stable, slightly higher or lower growth rates are both acceptable, according to Xinhua.

- Chinese military said it monitored US destroyer Benfold’s crossing of the Taiwan Strait and said frequent provocations by the US demonstrate that the US is a destroyer of peace and stability in the Taiwan Strait, while it added that troops in the theatre remain on high alert at all times, according to Reuters.

- COVID cases in Japan are set to reach a record high in excess of 150k, according to the Nikkei.

- Shanghai is to require residents to take a minimum of one COVID test per week until August 31st, according to an official; while Macau is to reopen some casinos on Saturday, July 23rd, according to Reuters sources.

END

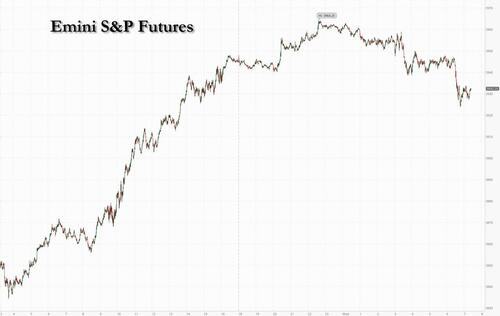

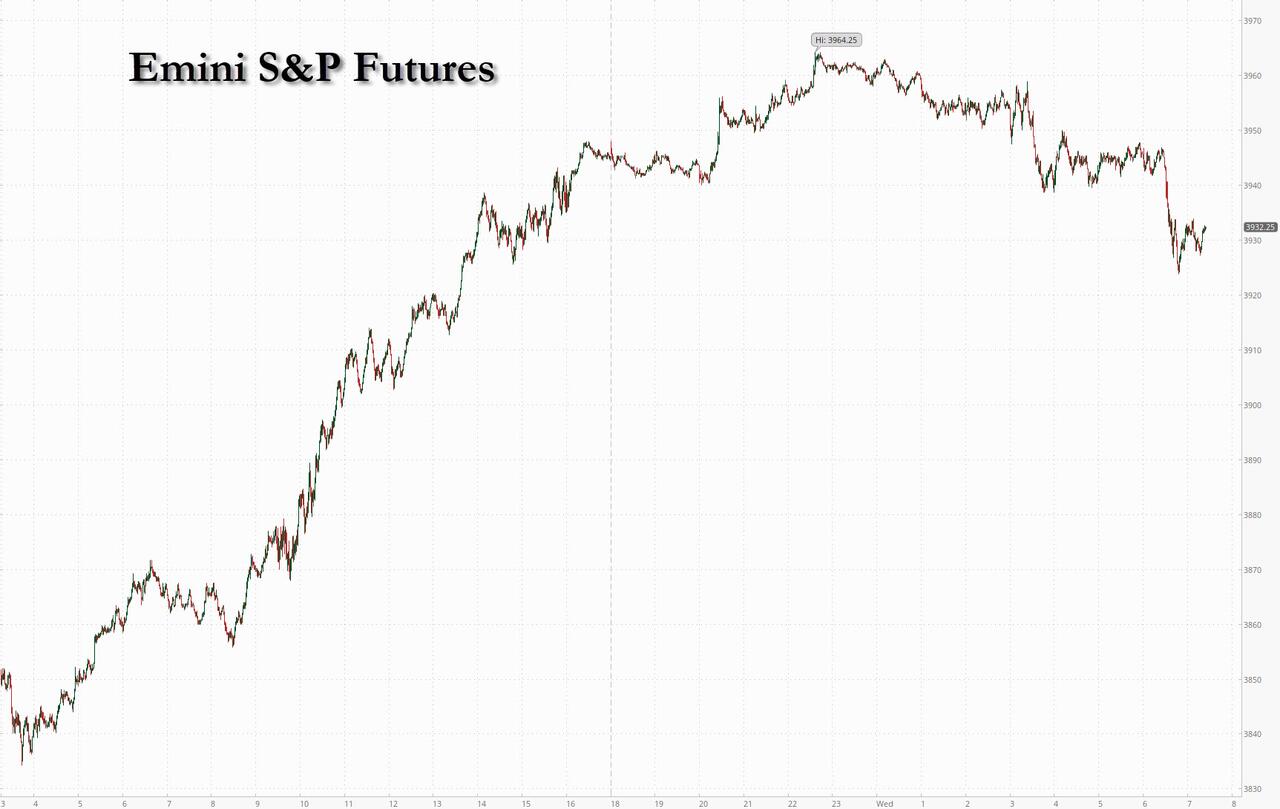

US Futures Rally Reverses After Europe Proposes Cuts To Nat Gas Consumption

WEDNESDAY, JUL 20, 2022 – 08:02 AM

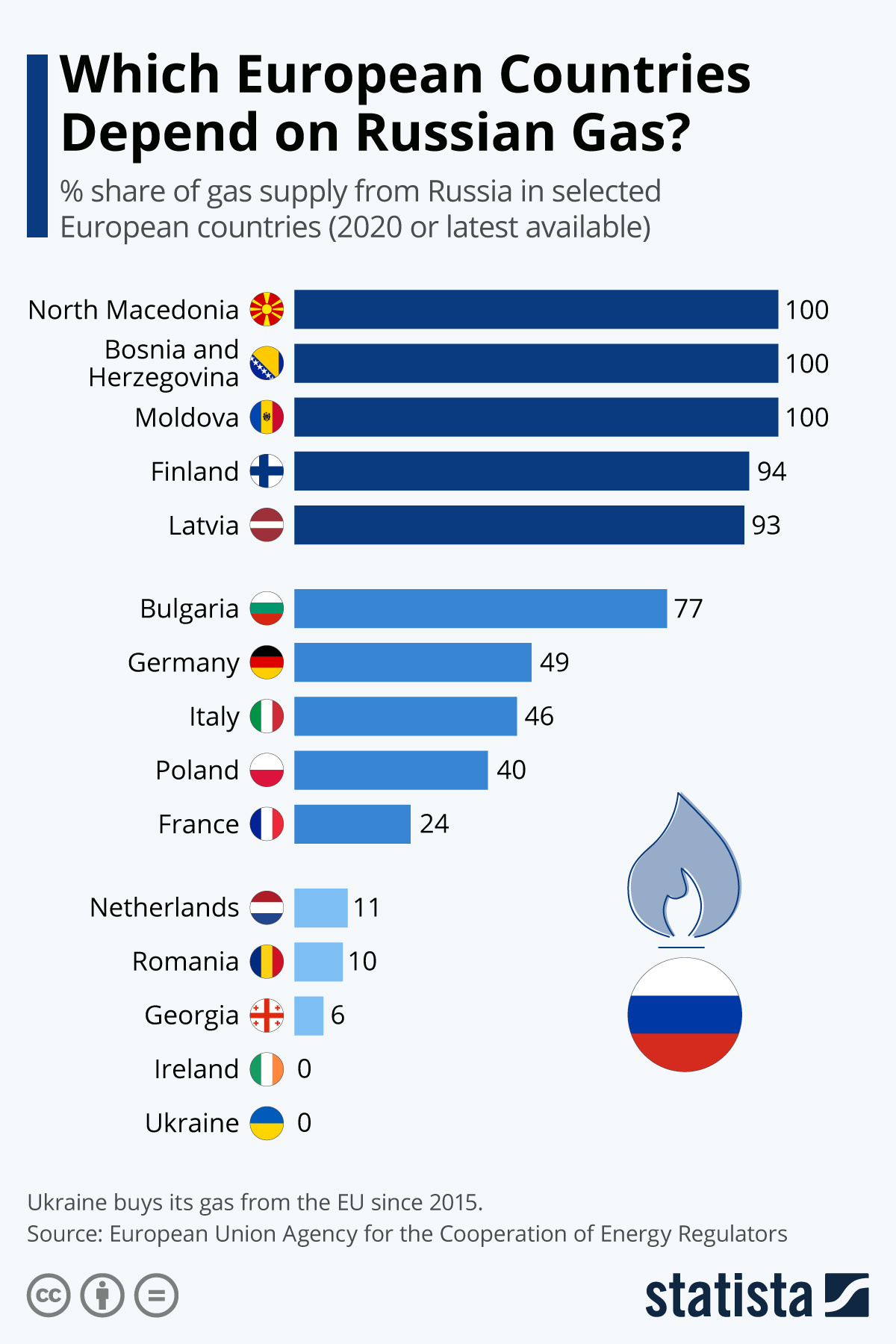

What was a solid overnight rally which pushed global markets higher and US index futures as high as 3,964 after a beat in Netflix subs helped further ease market jitters, fizzled and then reversed around 6:30am ET, when the European Union officially proposed that the bloc cut its natural gas consumption by 15% over the next eight months to ensure that any full Russian cutoff of natural gas supplies won’t disrupt industries over the winter, with Commission president Ursula von der Leyen going so far as suggesting the EU would be able to enforce a slowdown in gas consumption.

The move which saw spoos slide more than 20 points from 3,947 to below 3,925 before rebounding, and sparked a reversal in haven assets, as Treasuries rose with 10Y yields dropping back under 3.0%, and the dollar index stabilizing after three days of declines…

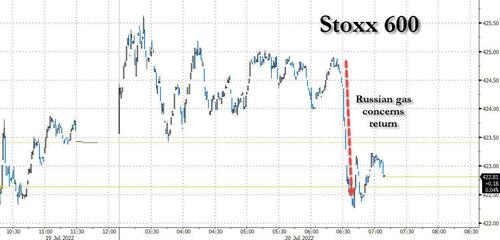

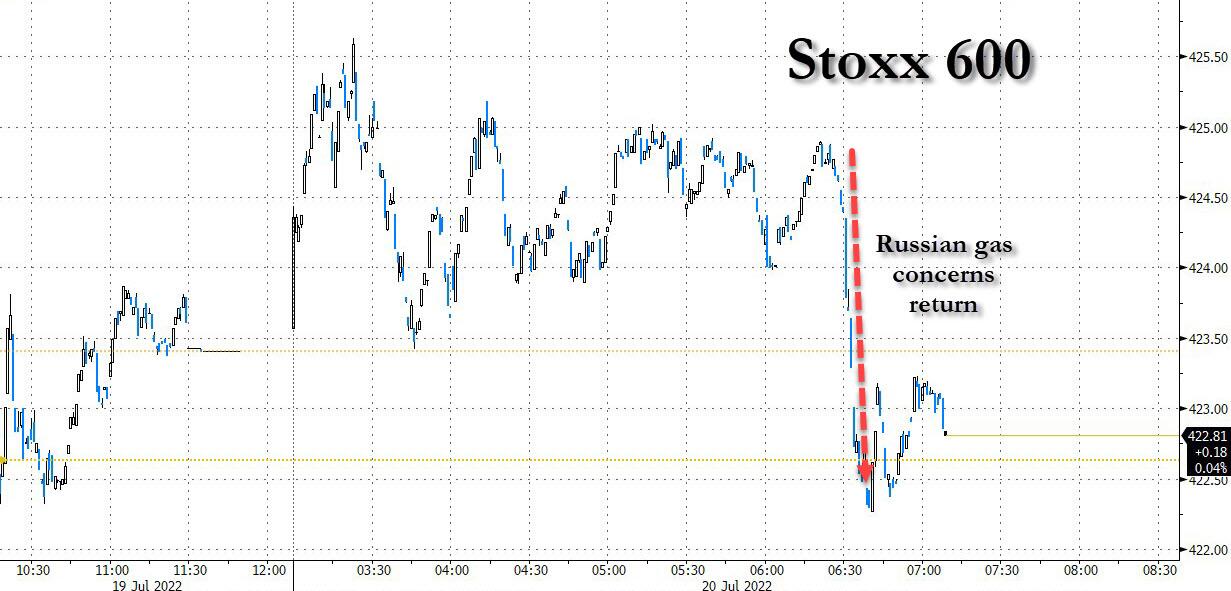

… was driven by European stocks, with the Stoxx Europe 600 Index falling 0.1% at 12:09 p.m. in London, snapping a three-day gaining streak. Auto and insurance stocks led the declines, while technology, energy and real estate gained.

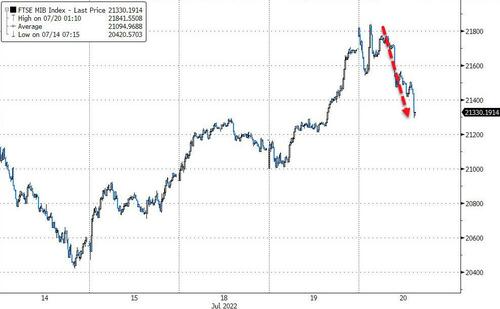

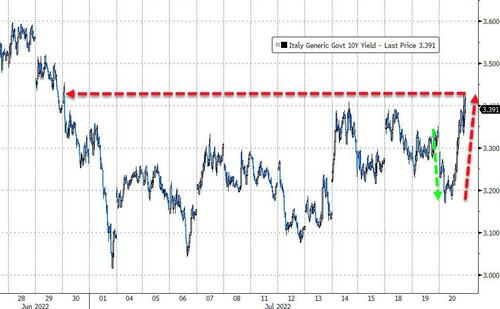

European investor sentiment had been roiled in recent day by prospects that Russian gas supplies could halt entirely, a scenario that strategists said would tip the regional economy into an immediate recession. And while on Wednesday morning Vladimir Putin signaled that Europe will start getting gas again through the Nord Stream 1 pipeline, he warned that unless a spat over sanctioned parts is resolved, flows will be curbed to at little as 20% of available inventory. There was some positive news when Italian Prime Minister Mario Draghi said he is ready to rebuild his governing coalition, helping Italian bonds rise.

Amid the broad-based swoon, European food delivery stocks rose as Citi said that Delivery Hero, Just Eat and Deliveroo’s stocks all have upside potential over the next 12 months, as the broker expects the three firms to record lower FY22 Ebitda losses than the consensus forecasts. Just Eat surges 12% as of 12:37pm CET, Delivery Hero jumps 8.8% and Deliveroo is up 3.5%. Here are some of the other notable European movers today:

- Uniper shares rose as much as 21% after a report that the German government is nearing a bailout deal for the utility. Fortum, which owns 75% of Uniper, rises as much as 4.5%.

- Georg Fischer shares jump as much as 7.8% after 1H earnings. Baader says the company’s resilient business model delivered a result above expectations despite headwinds from China lockdowns and supply chain disruptions.

- Alfa Laval surges as much as 9.4% after the Swedish industrial equipment maker’s second quarter earnings surprised with beats on order growth, adjusted Ebita and sales.

- Wise extends gains since Tuesday’s trading update, rising as much as 5.5% today. Credit Suisse boosts its price target and estimates for the money transfer firm.

- Carrefour shares climb as much as 3.4% after the French grocer agrees to sell a controlling stake in its retail operations in Taiwan to local partner Uni-President for $970 million, a move welcomed by investors.

- Royal Mail shares drop as much as 6.1% after the company posted what Liberum calls an “awful” 1Q trading update, though analysts see the potential separation of its two main business units providing some relief.

- Telia falls as much as 5.6%, as analysts flagged weak free cash flow in its 2Q update. The Swedish telecommunications company beat estimates for net sales and adjusted Ebitda for the second quarter.

- SKF shares fall as much as 3.8% after the Swedish ball bearings manufacturer reported 2Q earnings that missed the average analyst estimate.

The risk of a global downturn and Europe’s energy crisis doused optimism about the US earnings season and confidence the Federal Reserve will avoid very aggressive monetary tightening. “We don’t expect a sustained improvement in market sentiment until investors get greater clarity on the outlook for the economy, central bank policy, and political risks,” said Mark Haefele, chief investment officer at UBS Global Wealth Management.

Going back to the US, in premarket trading Netflix added about 6% after it reported better-than-feared earnings late on Tuesday and said it expects to return to subscriber growth before the end of the year. Below we list some other notable premarket movers:

- VBL Therapeutics (VBLT US) slumps as much as 80% after the biotech firm’s clinical trial for ovarian cancer treatment ofra-vec, or VB-111, didn’t meet its primary endpoints.

- Omnicom (OMC US) rose 6.9% on low volume after second-quarter revenue beat the average analyst estimate and the advertising firm raised its organic sales growth forecast for the year.

- Oil shares could be in focus as HSBC said in a note that a recent correction has left global integrated oil stocks looking attractive again and upgraded Chevron (CVX US) to buy.

- Keep an eye on Cazoo (CZOO US) shares as the stock was initiated with a sell rating at Berenberg, with the broker flagging a more competitive environment in Europe for the online used-car retailer.

- Watch Apple (AAPL US) shares as their price target was lowered to $185 from $205 at Wells Fargo Securities, a move that comes ahead of the iPhone maker’s upcoming results.

- Keep an eye on US home retail stocks as Morgan Stanley cut estimates and price targets on consumer discretionary-exposed retailers, including Floor & Decor Holdings (FND US), Williams-Sonoma (WSM US) and Best Buy (BBY US), amid an expected slowdown in spending in the second half of the year.

Earlier in the session, Asian stocks advanced as a weaker dollar and report of a possible end to China’s investigation into Didi Global boosted sentiment. The MSCI Asia Pacific Index gained as much as 1.7%, the biggest intraday gain in more than three weeks. Alibaba and Tencent were among the biggest boosts to the benchmark after the Wall Street Journal reported that China is expected to fine ride-hailing firm Didi more than $1 billion before wrapping up its year-long probe.

The dollar fell, underscoring waning haven demand, with the euro strengthening on the possibility of a bigger-than-expected rate hike by the European Central Bank. Asian stocks also got a boost from gains in US peers overnight amid optimism on earnings and better-than-feared subscriber numbers from Netflix. “A mix of global and local factors appear to be driving risk-on sentiment in Asia today,” said Chetan Seth, Asia Pacific equity strategist at Nomura Holdings in Singapore. “Stocks have been quite weak of late and investors appear to be very cautiously positioned, so incrementally positive news does help.” Almost all main Asian markets were higher, with the Japan benchmark climbing more than 2% ahead of its central bank’s policy decision Thursday. Key equity measures in Hong Kong rose more than 1%.

Japanese stocks climbed amid investor hopes for better-than-expected earnings and subsiding worry over interest-rate hikes. The Topix rose 2.3% to 1,946.44 at the 3 p.m. close in Tokyo, while the Nikkei 225 advanced 2.7% to 27,680.26. “Earnings from Netflix were not so bad, and this has led to an increase in expectations for better corporate performances,” said Mitsushige Akino, a senior executive officer at Ichiyoshi Asset Management. Sony Group contributed the most to the Topix’s gain, increasing 4.1%. Out of 2,170 shares in the index, 1,966 rose and 143 fell, while 61 were unchanged. “It looks like things that had been sold off are rebounding,” said Hajime Sakai, chief fund manager at Mito Securities

India’s benchmark equity index extended gains for a fourth day in the longest rising streak this month as technology companies led advances. The S&P BSE Sensex rose 1.2% to 55,397.53 in Mumbai on Wednesday, taking its weekly advance above 3%. The NSE Nifty 50 Index advanced 1.1%, taking cues from gains in other Asian markets. A gauge of IT companies rose the most among 19 sectoral indexes, of which 13 sectors gained. Technology stocks rally was led by Tech Mahindra and HCL Technologies that gained 3.8% and 3.1% respectively. Reliance Industries Ltd contributed the most to the index gain, increasing 2.5% after a cut in windfall taxes of fuels triggered gains in oil and energy shares. Out of 30 shares in the Sensex index, 22 rose and 8 fell.

In FX, the Bloomberg dollar spot index is near flat. CHF and NOK are the weakest performers in G-10. The euro held near a two-week high, with expectations buoyed by reports the European Central Bank may consider delivering a 50-basis-point hike at Thursday’s meeting, despite earlier signaling a smaller move. The Swiss franc underperformed other Group-of-10 currencies as appetite for haven currencies waned; a Bloomberg gauge of dollar strength edged lower for a fourth day.

In rates, Treasuries were richer across the curve, adding to gains in early US session as stock futures drop. US yields richer by up to 6bp across front-end of the curve as belly and front-end outperform, steepening 2s10s, 5s30s spreads each by 2bp on the day; 10-year yields around 2.97%, richer by 5bp on the day with bunds outperforming by additional 2.5bp and gilts by 6bp. Italian benchmark 10-year yields fell as much as 16 basis points to 3.17%; the yield spread over German equivalents narrowed to 199bps as Mario Draghi offered to remain as prime minister. Bunds outperformed with gilts, as traders adjust expectations for Thursday’s ECB policy meeting. US auctions resume with $14b 20-year bond reopening at 1pm ET; WI yield around 3.385% is ~10bp richer than June’s stop-out, which tailed the WI by 0.2bp. UK gilts advanced, shrugging off an inflation print that showed consumer price growth accelerated to a new 40-year high in June

In commodities, crude futures dropped with WTI trading within Tuesday’s range, falling 1.7% to trade near $102.40. Brent falls 1.1% near $106.15. Most base metals trade in the green; LME nickel rises 3.1%, outperforming peers. LME tin lags, dropping 0.4%. Spot gold falls roughly $4 to trade near $1,708/oz.

Bitcoin hovered above $23,000 after climbing out of a one-month-old trading range.

To the day ahead now, and data releases include UK and Canadian CPI for June, US existing home sales for June, and the Euro Area’s preliminary consumer confidence for July. Otherwise, earnings releases include Tesla and Abbott Laboratories.

Market Snapshot

- S&P 500 futures up 0.2% to 3,945.00

- STOXX Europe 600 up 0.2% to 424.21

- MXAP up 1.3% to 158.52

- MXAPJ up 1.0% to 520.62

- Nikkei up 2.7% to 27,680.26

- Topix up 2.3% to 1,946.44

- Hang Seng Index up 1.1% to 20,890.22

- Shanghai Composite up 0.8% to 3,304.72

- Sensex up 1.4% to 55,533.19

- Australia S&P/ASX 200 up 1.6% to 6,759.21

- Kospi up 0.7% to 2,386.85

- German 10Y yield little changed at 1.23%

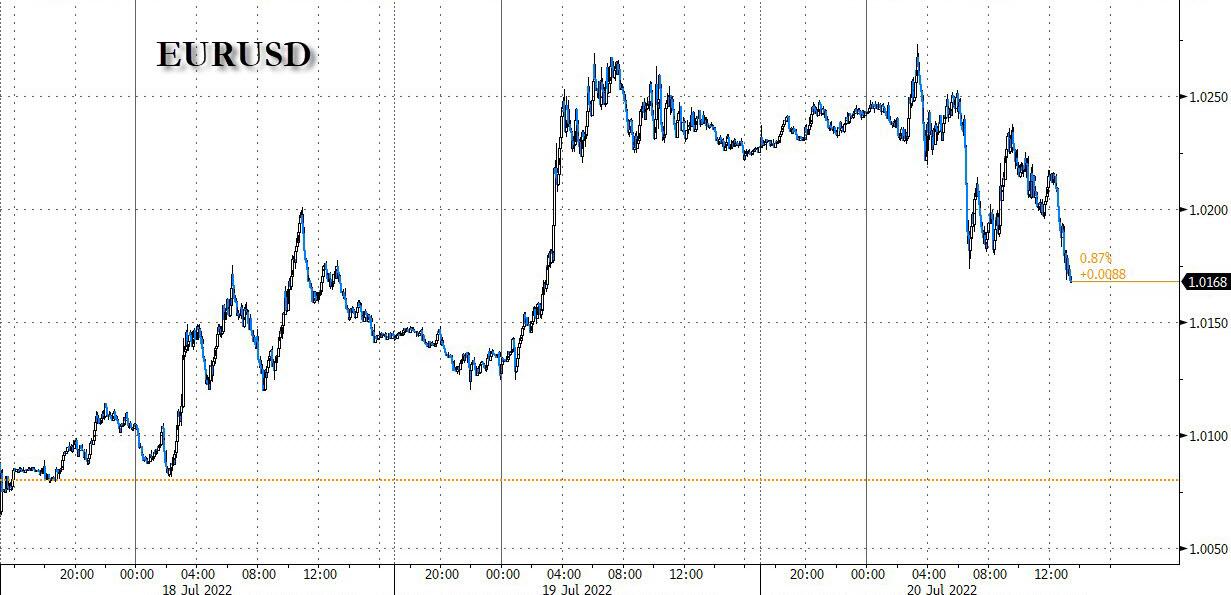

- Euro up 0.1% to $1.0238

- Gold spot down 0.2% to $1,707.69

- U.S. Dollar Index little changed at 106.64

Top Overnight News from Bloomberg

- Prime Minister Mario Draghi told the Rome senate on Wednesday that his fractious coalition can be rebuilt, tamping down concerns he’ll quit the government and throw Italy into chaos. Markets rallied after his comments.

- Russian President Vladimir Putin signaled that Europe will start getting gas again through a key pipeline, but warned that unless a spat over sanctioned parts is resolved, flows will be tightly curbed.

- UK inflation hit a new 40-year high in June, intensifying the cost of living crisis and heaping pressure on the Bank of England to deliver an aggressive interest-rate increase next month

- Some suppliers to Chinese real estate developers are refusing to repay bank loans because of unpaid bills owed to them, a sign that the loan boycott that started with homebuyers is starting to spread.

A more detailed look at global markets courtesy of Newsquawk