by harveyorgan · in Uncategorized · Leave a comment·Edit

in Uncategorized · Leave a comment·Edit

GOLD; $1752505 UP $31.25

SILVER: $19.91 UP 124 CENTS

ACCESS MARKET:

GOLD $1756.70

SILVER: $20.01

We are now entering options expiry for Comex (tomorrow) and OTC/LBMA (Friday)

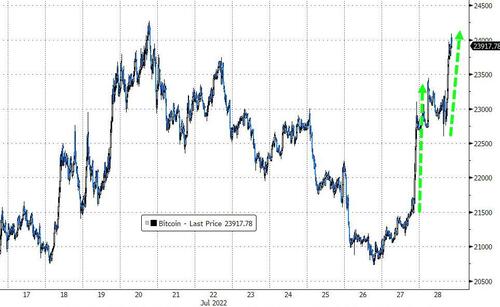

Bitcoin morning price: $23,027 UP 147

Bitcoin: afternoon price: $23,827. UP 947

Platinum price: closing UP $1.15 to $890.25

Palladium price; closing up $83.45 at $2094.20

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

JPMorgan stopped 5/6

EXCHANGE: COMEX

CONTRACT: JULY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,719.100000000 USD

INTENT DATE: 07/27/2022 DELIVERY DATE: 07/29/2022

FIRM ORG FIRM NAME ISSUED STOPPED

323 H HSBC 1

624 H BOFA SECURITIES 3

657 C MORGAN STANLEY 2

661 C JP MORGAN 5

737 C ADVANTAGE 1

TOTAL: 6 6

MONTH TO DATE: 9,641

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR JULY CONTRACT:

6 NOTICES FOR 600 OZ //0.01866 TONNES

total notices so far: 9641 contracts for 964,100 oz (29.987 tonnes)

SILVER NOTICES:

68 NOTICES FILED FOR 340,000 OZ/

total number of notices filed so far this month 4008 : for 20,040,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $31.25

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGE IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 1005.29 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 124 CENTS

AT THE SLV// ://HUGE CHANGES IN SILVER INVENTORY AT THE SLV//:A WITHDRAWAL OF 11.479 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 484.118 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 304 CONTRACTS TO 148,088 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GAIN IN OI WAS ACCOMPLISHED WITH OUR $0.04 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.04) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY COMMERCIAL SILVER LONGS// WE HAD ADDITIONAL SPECULATOR ADDITIONS AS WE HAD A HUGE GAIN OF 2010 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A POOR INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.220 MILLION OZ FOLLOWED BY TODAY’S 10,000 OZ QUEUE JUMP / // V) SMALL SIZED COMEX OI GAIN

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -4

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTACTS for 19 days, total 16,117 contracts: 80.585 million oz OR 4.424 MILLION OZ PER DAY. (848 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 80.585 MILLION OZ

.

LAST 15 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 80.585 MILLION OZ

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 304 WITH OUR $0.04 GAIN IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1700 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER ADDITIONS ////// HUGE SPECULATOR SHORT ADDITIONS// WE HAVE A POOR INITIAL SILVER OZ STANDING FOR JULY. OF 15.22 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 10,000 OZ // .. WE HAD A HUGE SIZED GAIN OF 2004 OI CONTRACTS ON THE TWO EXCHANGES FOR 10.050 MILLION OZ DESPITE THE TINY GAIN IN PRICE..THE SPECS ARE GOING TO THE SLAUGHTER HOUSE.

WE HAD 68 NOTICES FILED TODAY FOR 340,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 5,040 CONTRACTS TO 482,038 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: +437 CONTRACTS.

.

THE STRONG SIZED DECREASE IN COMEX OI CAME DESPITE OUR SMALL RISE IN PRICE OF $1.80//COMEX GOLD TRADING/WEDNESDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT ADDITIONS ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE.//WE HAD INITIATION OF SPREADER LIQUIDATION WHICH TOOK CARE OF ALL OF THE FALL AT COMEX.. WE HAD ZERO LONG LIQUIDATION //AND HUGE SPECULATOR SHORT ADDITIONS//HUGE ADDITIONS TO OUR BANKER LONGS!! THE COMEX IS ONE BIG FARCE

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JULY AT 2.914 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 0 OZ

YET ALL OF..THIS HAPPENED WITH OUR SMALL RISE IN PRICE OF $1.80 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A SMALL SIZED LOSS OF 1414 OI CONTRACTS 3.038 PAPER TONNES) ON OUR TWO EXCHANGES..WITH ALL THE LOSS DUE TO SPREADER LIQUIDATION

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4063 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 482,475

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1414 CONTRACTS WITH 5040 CONTRACTS DECREASED AT THE COMEX AND 4063 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 977 CONTRACTS OR 3.038 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4063) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (5,040): TOTAL LOSS IN THE TWO EXCHANGES 1,414 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT ADDITIONS//STRONG BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JULY. AT 2.914 TONNES FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP 3) ZERO LONG LIQUIDATION AS ALL OF THE COMEX LOSS WAS DUE TO SPREADER LIQUIDATION////SOME SPECULATOR SHORT COVERINGS/ //.,4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

116,922 CONTRACTS OR 11,692,200 OZ OR 363.67 TONNES 19 TRADING DAY(S) AND THUS AVERAGING: 6153 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAY(S) IN TONNES: 363.67 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 363.67/3550 x 100% TONNES 10.22% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 363.67 TONNES (HUGE INCREASE FROM JUNE//WILL CLOSE IN ON THE RECORD EFP ISSUANCE IN MARCH 22//SURPASSED PREVIOUS RECORD HIGH NOV 21)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A SMALL SIZED 304 CONTRACT OI TO 148,088 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1700 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 1700 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1700 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 304 CONTRACTS AND ADD TO THE 1700 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 2004 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 10.020 MILLION OZ

OCCURRED DESPITE OUR RISE IN PRICE OF $0.04

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED UP 6.62 PTS OR 0.21% //Hang Sang CLOSED DOWN 47.36 OR 0.23% /The Nikkei closed UP 99.73 OR % 0.36. //Australia’s all ordinaires CLOSED UP 1.11% /Chinese yuan (ONSHORE) closed UP AT 6.7486//OFFSHORE CHINESE YUAN UP 6.7545// /Oil UP TO 99.26 dollars per barrel for WTI and BRENT AT 108.38// SHANGHAI CLOSED UP 6.62 PTS OR 0.21% //Hang Sang CLOSED DOWN 47.36 OR 0.23% /The Nikkei closed UP 99.73 OR % 0362. //Australia’s all ordinaries CLOSED UP 1.11% / Stocks in Europe OPENED ALL MIXED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 5040 CONTRACTS TO 482,475 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX DECREASE OCCURRED DESPITE OUR SMALL RISE OF $1.80 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (4063 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4063 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :4063 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4063 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED SIZED TOTAL OF 977 CONTRACTS IN THAT 4063 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 5,040 CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR SMALL SIZED GAIN IN PRICE OF GOLD $ 1.80. TODAY, WITNESSED THE CONTINUATION OF SPREADER LIQUIDATION. WE ALSO ARE WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS IS AN ABSOLUTE FARCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JULY (29.987),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $1.80) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AND COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO COVER TO THEIR POSITIONS////ALL THE COMEX LOSS WAS DUE TO SPREADER LIQUIDATION// WE HAVE REGISTERED A SMALL SIZED LOSS OF 4.398 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR JULY (29.987 TONNES)…

WE HAD -XXX CONTRACTS ADDED TO COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 977 CONTRACTS OR 97,700 OZ OR 3.038 TONNES

Estimated gold volume 234,648/// fair/

final gold volumes/yesterday 282,938 / fair

INITIAL STANDINGS FOR JULY ’22 COMEX GOLD //JULY 28

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 257,465.208oz Brinks JPMorgan Manfra 8008 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 6 notice(s) 600 OZ 0.01866 TONNES |

| No of oz to be served (notices) | 0 contracts 00 oz 0.0 TONNES |

| Total monthly oz gold served (contracts) so far this month | 9641 notices 964,100 OZ 29.987 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

Customer deposits: 0

total deposits: 0 oz

4 customer withdrawals:

i) out of Brinks: 257.200 oz Brinks 8 kilobars

ii) out of JPMorgan: 160,755.000 oz (5,000 kilobars)

iv)out of Manfra: 92,453.000 oz 3000 kilobar

total withdrawals: 257,465.200 oz (8,008 kilobars)

ADJUSTMENTS: dealer to customer/Loomis

2314.872 oz

customer to dealer: Manfra 383.812 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 6 contracts having LOST 30 contracts . We had

30 notices filed on Tuesday so we GAINED 0 contracts or an additional NIL oz will stand in this non active

delivery month of July.

August has a LOSS OF 35,104 contracts down to 43,728 contracts. We have 1 more reading day before first day notice. Looks like we will have a strong August standing for gold (JULY 29/22..FIRST DAY NOTICE)

Sept. gained 539 contracts to 3911 contracts.

We had 6 notice(s) filed today for 600 oz FOR THE July 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 6 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 5 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2022. contract month,

we take the total number of notices filed so far for the month (9641) x 100 oz , to which we add the difference between the open interest for the front month of (JULY 6 CONTRACTS ) minus the number of notices served upon today 6 x 100 oz per contract equals 964,100 OZ OR 29.987 TONNES the number of TONNES standing in this active month of July.

thus the INITIAL standings for gold for the JULY contract month:

No of notices filed so far (9641) x 100 oz+ (x6) OI for the front month minus the number of notices served upon today (6} x 100 oz} which equals 958,100 oz standing OR 29.987 TONNES in this active delivery month of JULY.

TOTAL COMEX GOLD STANDING: 29.987 TONNES (A FAIR STANDING FOR A JULY ( NON ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,443,533.842 oz 76.00 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 30,635,105.67 OZ

TOTAL REGISTERED GOLD: 15,449,907.284 OZ (480.5 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 15,185,197.889 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 13,008,303.0 OZ (REG GOLD- PLEDGED GOLD) 404.6 tonnes

END

SILVER/COMEX/JULY 28

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 738,530.160 oz Brinks HSBC JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 901,274.480 oz Delaware JPMorgan |

| No of oz served today (contracts) | 68 CONTRACT(S) 340,000 OZ) |

| No of oz to be served (notices) | 0 contracts (0 oz) |

| Total monthly oz silver served (contracts) | 4076 contracts 20,380,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i) Into Delaware 299,037.840 oz

ii) Into JPMorgan: 602,236.640 oz

total deposit: 802,768.630 oz

JPMorgan has a total silver weight: 175.168 million oz/337.594 million =51.89% of comex

Comex withdrawals:3

i) Out of Brinks: 134,363.360 oz

ii) Out of HSBC 599,144.500 oz

iii) Out of jPMorgan 5022,38o 0z

total: 738,530 oz

adjustments: 4//dealer to customer

Brinks 148,140.660 oz

CNT 180,028.524 oz

JPMorgan: 1,653,528.780 oz

Manfra 64,372.750 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 55.722 MILLION OZ

TOTAL REG + ELIG. 337.756 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JULY OI: 68 CONTRACTS HAVING LOST 32 CONTRACTS. WE HAD 34 NOTICES FILED

ON TUESDAY, SO WE GAINED 2 CONTRACTS OR AN ADDITIONAL 10,000 OZ WILL STAND FOR METAL AT THE COMEX.

AUGUST LOST 45 CONTRACTS TO STAND AT 829

SEPTEMBER HAD A LOSS OF 1940 CONTRACTS DOWN TO 114,986

CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 68 for 340,000 oz

Comex volumes:85,956// est. volume today// very good

Comex volume: confirmed yesterday: 67,961 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 4076 x 5,000 oz = 20,380,000 oz

to which we add the difference between the open interest for the front month of JULY(68) and the number of notices served upon today 68 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY./2022 contract month: 4076 (notices served so far) x 5000 oz + OI for front month of JULY (68) – number of notices served upon today (68) x 5000 oz of silver standing for the JULY contract month equates 20,380,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JULY 28/WITH GOLD UP $31.25; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 27.//WITH GOLD UP $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 26/WITH GOLD DOWN $1.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.29 TONNES

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

JULY 18/WITH GOLD UP $7.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.28 TONNES

JULY 15/WITH GOLD DOWN $3.75:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD///INVENTORY RESTS AT 1016.89 TONNES//

JULY 14/WITH GOLD DOWN $28.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD//INVENTORY RESTS AT 1019.79 TONNES

JULY 13/WITH GOLD UP $10.55:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD//INVENTORY RESTS AT 1021.53TONNES

JULY 12/WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESS AT 1023.27 TONNES

JULY 11/WITH GOLD DOWN $4.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD./INVENTORY RESTS AT 1023.27 TONNES

JULY 7/WITH GOLD UP $1.35: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.61 TONNES FORM THE GLD///INVENTORY REST AT 1024.43 TONNES

JULY 6/WITH GOLD DOWN $26.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 9.86 TONNES FROM THE GLD//INVENTORY REST AT 1032.04 TONNES

JULY 5/WITH GOLD DOWN $36.55//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.41 TONNES FROM THE GLD///INVENTORY RESTS AT 1041.90 TONNES

JULY 1/WITH GOLD DOWN $5.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES//INVENTORY RESTS AT 1050.31 TONNES

JUNE 30/WITH GOLD DOWN $9.20: big CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 1052.63 TONNES//

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

GLD INVENTORY: 1005.29 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 28/WITH SILVER UP $1.24 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 484.118 MILLION OZ/

JULY 27/.WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL 11.479 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 484.118MILLION OZ//

JULY 26/WITH SILVER UP 16 CENTS: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV//: //INVENTORY RESTS AT 495.597 MILLION OZ//

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

JULY 18/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 4.995 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ.

JULY 15/WITH SILVER UP 31 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 3.226 MILLION OZ FORM THE SLV//INVENTORY RESTS AT 510.443 MILLIONOZ//

JULY 14/WITH SILVER DOWN 88 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 OZ FROM THE SLV// //INVENTORY RESTS AT 513.671 MILLION OZ

JULY 13/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SV//INVENTORY RESTS AT 514.501 MILLION OZ.

JULY 12/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.228 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 514.501 MILLION OZ//

JULY 11/WITH SILVER DOWN 17 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 5.533 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 517.729 MILLION OZ

JULY 7/WITH SILVER UP 3 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.889 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 523.262 MILLION OZ/

JULY 6/WITH SILVER UP ONE CENT: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 12.558 MILLION OZ FORM THE SLV///INVENTORY RESTS AT 528.151 MILLION OZ

JULY 5/WITH SILVER DOWN 55 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 540.709MILLION OZ//

JULY 1/WITH SILVER DOWN 61 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ//INVENTORY RESTS AT 540.709 MILLION OZ//

JUNE 30/WITH SILVER DOWN 41 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 738,000 OZ FROM THE SLV//INVENTORY RESTS AT 541.262 MILLION OZ//

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

CLOSING INVENTORY 484.118 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Is The Fed At The End Of Its Rope?

THURSDAY, JUL 28, 2022 – 08:21 AM

Authored by Michael Maharrey via SchiffGold.com,

The Federal Reserve delivered another 75 basis point interest rate hike at its July FOMC meeting. This pushes the federal funds rate over the 2% threshold to between 2.25% and 2.5%.

The mainstream media emphasized the size of the hike. One headline called it “a second super-sized hike,” with many other mainstream pundits noting that it matched a June hike was the biggest since 1994. But it wasn’t as big as the full 1% hike everybody thought was on the table after we got June’s flaming hot Consumer Price Index (CPI) data.

Here’s the question: has the Fed reached the end of its rope? Will this be the last hike in this cycle?

The corporate financial press seems to think the Fed will hike again in September, and the central bank certainly left that impression. The FOMC statement said it “anticipates that ongoing increases in the target range will be appropriate.” Powell said another “unusually large increase” could be appropriate at the September meeting.

But the FOMC state left some wiggle room, saying, “The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals.”

In other words, the Fed can stop hiking at any time.

Federal Reserve Chairman Jerome Powell left even more space to retreat from the inflation fights, saying there is “significantly” more uncertainty right now than normal and the lack of any clear insight into the future trajectory of the economy means the Fed can only provide reliable policy guidance on a “meeting by meeting” basis.

The markets seemed to interpret the Fed’s stance as more doveish. Stocks were up, as was gold.

The Fed may well need that wiggle room.

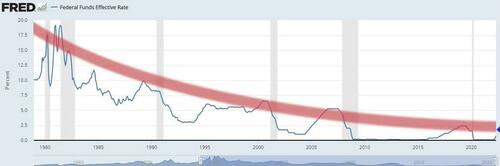

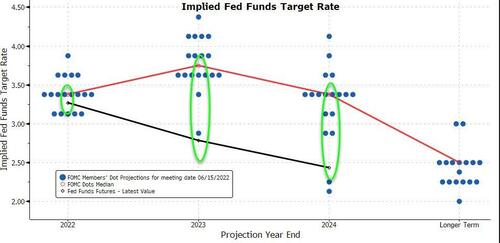

With this 75 basis-point hike, interest rates are now equal to the peak of the last hiking cycle in December 2018.

Passant Gardant published a graph that indicates the current interest rate is above the maximum that the economy can handle before plunging into a recession.

As you can see, the peak of the rate hike cycle gets lower and lower with each subsequent tightening. No matter how emphatically Powell insists that the Fed can raise interest rates, slay inflation and bring us to a soft landing, reality says otherwise. There is nothing to lead us to believe that the Fed can get rates to 2% without crashing the bubble economy, much less hike them to 3.5% or 4%. (And that’s not even enough to slay inflation.)

When interest rates reached this level in 2018, the stock market crashed and economic data went wobbly. In response, the Fed reversed course and put tightening on pause. In 2019, it cut rates three times and relaunched quantitative easing (although it refused to call it that.) This all happened long before the extraordinarily loose monetary policy launched in the wake of the coronavirus pandemic.

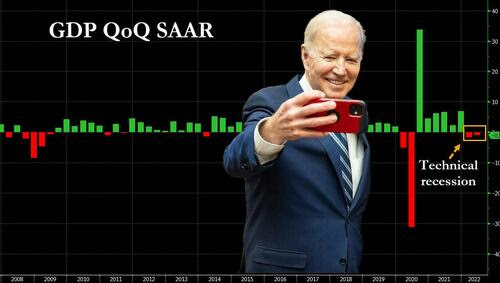

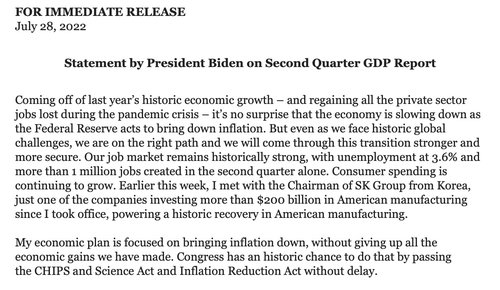

Today, there is even more debt and malinvestment in the economy than there was in 2019. It seems unlikely the Fed can push rates any higher without a complete economic meltdown. And we may already be past that point of no return. Despite claims to the contrary, it appears the US economy is already in a recession and has been all year.

The FOMC conceded that the economy appears to “have softened.” But the committee remains sanguine.

“Nonetheless, job gains have been robust in recent months, and the unemployment rate has remained low,” the FOMC statement said.

During his post-meeting press conference, Powell insisted the economy was not in a recession.

“There are too many areas of the economy that are performing too well. I would point to the very strong labor market. [It is] true that growth is slowing.”

As Peter Schiff noted, the Fed chair apparently picked up its copy of White House talking points declaring that two consecutive quarters of negative GDP growth doesn’t mean the economy is in a recession.

“If you think the Fed is independent, today’s press conference should put that myth to rest. Powell clearly got the Biden administration memo that recession is not defined by two consecutive quarters of falling GDP. Powell even said it’s not his job to declare a recession,” Schiff said.

Powell has to downplay the GDP. In the first quarter of 2022, GDP came in at -1.6 percent. The Atlanta Fed projects another -1.2% decline in Q2. Using the common definition, that would mean we’re in a recession now, and we have been all year.

While Powell and others keep saying the economy is strong, the only data they consistently point to is the labor market. But the job market is a lagging indicator and even it looks shaky. As Schiff pointed out during an interview with Laura Ingraham, we’ve seen three straight weeks of increasing first-time jobless claims, and they’re at the highest level since October last year.

Meanwhile, if you look at that last job report, even though we added about 400,000 jobs in the establishment survey, the household survey lost about that many jobs. But if you actually look at the jobs, almost all of these new jobs were for people who already had jobs. These were people taking second and third jobs because they’re struggling to pay the bills. And you have a lot of retirees who are being forced back into the workforce because inflation has eviscerated their incomes, and now they have no choice but to go to work. So, these are not jobs that people want. These are jobs that people are forced to take because the economy is so weak.”

Meanwhile, we’re seeing big pullbacks in the housing market, manufacturing and retail. And the average American isn’t buying the “economy is fine” narrative. Consumer confidence fell to a 19-month low in July.

This is eerily similar to the early days of the 2008 recession when the mainstream media and government officials kept saying everything was fine even as the economy was going up in flames.

No Stomach for This Fight

This economy was built on easy money and debt. It looks like taking away the easy money punch bowl has already popped the bubble. This latest rate hike will only make the rip in the bubble bigger, letting the air out even faster. It’s only a matter of time before the entire house of cards economy collapses.

In reality, this needs to happen. The economy needs a recession to cleanse all of the misallocations and distortions out of the economy. But that would mean a lot of pain. Despite the recent hikes and all of the tough talk, one has to wonder if the Fed has the stomach to follow through with this inflation fight and allow the economy to crash to the ground.

For now, the central bankers at the Fed and the policymakers in DC can try to spin away the recession in the hope that inflation will magically go away before things get really bad, so they can go back to business as usual. By “business as usual,” I mean borrowing and spending and printing money out of thin air.

The trajectory of balance sheet reduction reveals that the Fed doesn’t really have the stomach for this inflation fight.

The FOMC statement claimed that “the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in the Plans for Reducing the Size of the Federal Reserve’s Balance Sheet that were issued in May.”

The problem with this statement is that it’s now the end of July and the Fed still isn’t reducing the size of its balance as described by the plan.

The balance sheet peaked in April at $8.966 trillion. Since that time, the Fed has reduced the balance sheet by a mere $66 billion. That’s just 0.74%.

The plan announced in May was for $30 billion in US Treasuries and $17.5 billion in mortgage-backed securities to roll off the balance sheet in June, July and August. That totals $45 billion per month. In September, the Fed plans to increase the pace to $95 billion per month.

At the time, I noted that this wasn’t an impressive balance sheet roll-off given the historically high CPI. At $95 billion per month, it would take 7.8 years for the Fed to shrink its balance sheet back to pre-pandemic levels. And it’s not even keeping pace with its own tepid plan.

If the Fed was really serious about fighting inflation, it would be rapidly shrinking the money supply.

So, the question remains: is the Fed at the end of its rope? And when it inevitably reaches that point will it let go, keep tightening to fight inflation, and take the economy into freefall? Or will it surrender to inflation and pivot back to easy money and quantitative easing, letting inflation run wild in order to rescue the economy?

END

Peter Schiff: Americans Paying For Big Government Through The Inflation Tax

THURSDAY, JUL 28, 2022 – 12:40 PM

Rapidly rising prices put the squeeze on everybody’s wallets. A recent study showed that inflation is hitting rural Americans particularly hard. According to the Iowa State University report, people in rural areas now spend 91% of their income on expenses alone. Peter Schiff recently appeared on Rob Schmitt Tonight to talk about the pain of the inflation tax.

Schmitt said the last time Peter was on the show, he painted a “very ugly picture about what’s coming for the American economy.” Peter said the picture is getting uglier.

I think we’re not in recession, which was something that I had been predicting. So, inflation got stronger as the economy got weaker. And I think this recession is just getting started, and it’s going to last a long time.”

Peter said that when you talk about families struggling with inflation, they’re really struggling with government.

Inflation is a tax. It’s the way government finances deficit spending. Government spends money. It doesn’t collect enough taxes, so it has to run deficits. The Federal Reserve monetizes those defiticts – prints money. They call it quantitative easing, but that’s inflation. Government is getting bigger and bigger, and families across America are going to have to bear that burden through higher prices.”

The government has also artificially suppressed interest rates for years. Schmitt said we’re paying the price for those decades of “cheap money.”

Peter agreed, emphasizing that interest rates should reflect the free market, not “price-fixing by the government.” He said that by artificially suppressing interest rates, the Fed “really screwed up this economy.”

Now we’re going to have to pay a heavy price to unwind all those mistakes. That’s why this recession is going to be so severe. That’s why this financial crisis is going to be worse than the one we had in 2008.”

The Fed has raised rates to fight inflation, but Peter said it’s not enough.

That’s still much too low. That’s an inflationary highly stimulative rate when you have the rate so far below inflation.”

Peter said that the inflation situation is far worse than the rigged CPI indicates, and with the amount of money the Federal Reserve has created over the years, we are likely heading for “an inflationary depression.”

Peter said he doesn’t know what it will take for the government to do the right thing.

The only way to solve the inflation problem is to dramatically cut government spending and to allow interest rates to rise to a market level. Now, when that happens, it’s going to be terrible as far as asset prices collapsing, failures, bankruptcies. But we’re going to have to endure that to get to the other side. If we want a real economy then we’re going to have to experience a real recession to get there.”

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

LAWRIE WILLIAMS: U.S. recession or no. Mixed views driving asset prices.

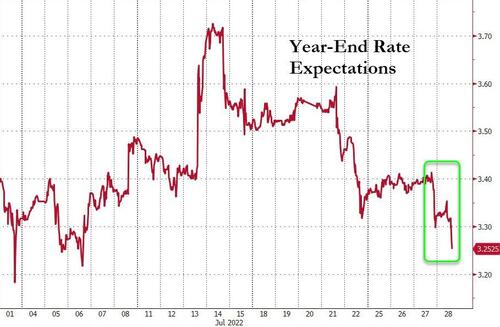

This week’s Federal Open Market Committee (FOMC) meeting in the U.S. is now behind us and it has had a profound outcome on global markets of virtually all kinds. The initial reaction to the meeting decisions and the subsequent statement and press release by Fed chair Jerome Powell had been to drive the dollar index sharply lower, although it was picking up again this morning, and gold, equities and bitcoin all higher. But will this euphoric investor reaction last? Perhaps not once more sober analysis is brought to bear on the actual meeting outcome and on Powell’s somewhat contradictory statements.

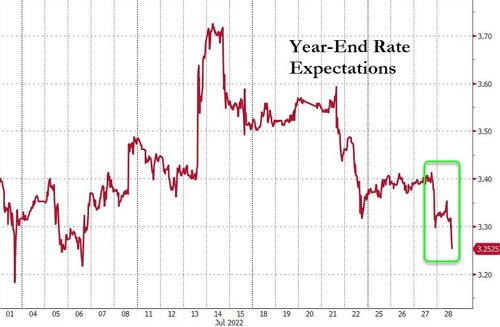

Interest rates were raised, as generally expected, by 75 basis points, but the interpretations of Powell’s subsequent statement and the ensuing press release proved to be somewhat varied. He did state quite categorically that the U.S. was not in a recession, although we are still waiting, at the time of writing, on today’s figures of the latest Q2 GDP estimates to see whether that is really the case as far as official statistics are concerned. Part of his statement was taken as suggesting that the likely September rate increase might be a little lower than the latest 75 basis point rise, although at the same time he intimated that inflation was still a major concern and if it remained high a repeat of the high interest rate increase, or even higher, might be on the cards.

If one goes entirely by market reaction, and the path of the CME’s Fedwatch Tool, the markets are very definitely for now anticipating a lower rate hike in September and have been moving accordingly. According to the Fedwatch Tool today, 70% are expecting only a 50 basis point rate increase and just 30% a 75 basis point rise in September. None appear to be even considering a 100 basis point rise, which Powell did not rule out in his post-FOMC statement. The Fedwatch Tool, though can be prone to over-reaction. For example in the immediate aftermath of the ultra high Consumer Price Index figure of just over a week ago it was strongly (over 70%) predicting a 100 basis point rate hike at this week’s FOMC meeting, but this came down to under 30% within a couple of days as more conservative counsel prevailed.

U.S. equities rose sharply in late trade yesterday, and although European equities opened on a positive note today they fell back as trade progressed. Gold at one time looked to be heading to $1,750, but after this strong start had fallen back quite sharply at the time of writing to below $1,740 – still stronger than it has been of late, but definitely a disappointment to gold followers given its heady start to the day. It will be interesting to see what happens to all the major asset classes in U.S. markets today. We suspect much will depend on the Preliminary Q2 GDP figures from the Bureau of Economic Analysis. If they come in negative, as many forecasts suggest, that will suggest the U.S. is actually in recessionary territory, whatever Powell says, as technically two successive quarters of negative growth define a recession. Q1 GDP was negative 1.6%, so if Q2 also appears to be negative …!

Whether the U.S. is technically in a recession or not, it is certainly teetering on the edge of one. Powell’s more optimistic takes look to be an effort to buoy up the markets and help avoid a hard landing which he is so anxious to do. If inflation does stay elevated, which we fear it may as his 2% target looks to be totally unattainable in the foreseeable future, then equities will suffer as current prices are mostly unsustainable in such an economic environment. Gold, and maybe silver, should go from strength to strength as wealth protectors which should not be prone to the ravages of inflation – particularly if the dollar index declines too as it probably will.

28 Jul 2022

end

3. Chris Powell of GATA provides to us very important physical commentaries

Ronan Manly reports that the LBMA silver inventories have been depleting all year and now are at a 6 year low

(Ronan Manly)

Ronan Manly: LBMA silver inventories near 6-year low

Submitted by admin on Wed, 2022-07-27 11:57Section: Daily Dispatches

By Ronan Manly

Bullion Star, Singapore

Wednesday, July 27, 2022

One trend in the precious metals markets that has yet to get widespread coverage but deserves more attention is the plummeting inventories of physical silver in the London vaults of the London Bullion Market Association.

These comprise vaults in and around London run by the bullion banks JP Morgan, HSBC, and ICBC Standard Bank, as well as the London vaults of three security operators — Brinks, Malca-Amit, and Loomis

Quietly and almost under the radar, the quantity of silver held in the LBMA vaults has been consistently hemorrhaging for seven straight months. Latest data from the LBMA as of the end of June 2022 shows that the LBMA vaults now hold only 997.4 million ounces of silver (31,023 tonnes).

Compared to the end of June 2021 when LBMA silver inventories stood at 1.18 billion ounces (36,706 tonnes), the LBMA vaults’ June 2022 month-end silver inventories are now 182.7 million ounces (5,683 tonnes) lower than a year ago — in other words a whopping 15.48% lower compared to June 2021. …

… For the remainder of the analysis:

(Courtesy Ronan Manly/GATA)

END

A funny article

(New York Sun)

New York Sun: The five top secrets of the Federal Reserve

Submitted by admin on Wed, 2022-07-27 09:44Section: Daily Dispatches

From the New York Sun

Wednesday, July 27, 2022

https://www.nysun.com/article/secrets-of-the-fed

A shocking new report from the Senate Committee on Homeland Security says that the Federal Reserve has been caught flat-footed by Communist Chinese spies trying to find out the secrets of the Fed. We wish them luck. We don’t want to be misunderstood here, but we’ve been trying to get the central bank’s secrets for years and it’s easier to mine for Bitcoin. Here, though, are five of the most closely guarded secrets of the Fed:

The Fed has no idea what’s going to happen. It failed to call the 20008 recession and the current inflation. Several years ago the Wall Street Journal editorial page, one of the biggest retail dealers in secrets of the Fed, published a chart of the Fed’s predictions. Not one of them came within a kiloparsec of what actually happened. The Journal found it “remarkable that the Fed is so wrong so often.”

The Fed might employ as many as a thousand economists. No one knows exactly how many. The Fed claims it has “just over 400 Ph.D. economists.” Estimates have run as high as 3,000. Not even such a well-connected person as Paul Volcker, a former Fed chairman, had any idea what function these employees serve. It can be disclosed that he once demanded of a reporter: “What in the world do they all do?”

The Fed once went seven years without a dissenting vote on monetary policy on its board. This is one of the most explosive secrets ever offered for sale by the Journal. It was discovered by economist Judy Shelton lurking in open sources and electrified Fed watchers. During the tenures of Chairmen Powell and Yellen, no governor cast a dissenting vote on monetary policy. So the Sun referred to the Fed as GosFed, after the Soviet Central Bank.

Inflation has an enormous constituency. This is one of the secrets of the Fed that is least understood. It turns out that inflation is a gift to persons who owe money — and the most indebted entity is the United States government. So it has become inflation’s most faithful friend. With the Chinese regime holding just under a trillion dollars in American treasury bonds, the Fed sees the communist mandarins as chumps.

Finally, the Fed doesn’t know what a dollar is. The word “dollars” appears twice in the United States Constitution, yet it is not defined there. The Founders understood the dollar to have a fixed value in specie. The statutes that once defined the dollar as a fixed weight of silver or gold — a 35th of an ounce of the latter, as recently as 1971 — are gone, though, and the dollar has lost 98.8% of its value since the founding of the Fed.

end

Gold trading in Lagos to begin officially tomorrow. Nigeria is Africa’s largest oil producer so it is natural to include gold. With Russian oil running at huge discounts as many nations scramble to

purchase physical gold in order to obtain this cheap oil.

(Bloomberg/GATA)

Gold trading begins on Nigerian exchange ahead of official launch

Submitted by admin on Wed, 2022-07-27 23:32Section: Daily Dispatches

By Emele Onu and Anthony Osae-Brown

Bloomberg News

Wednesday, July 27, 2022

A newly licensed Nigerian commodities exchange started trading in gold ahead of its official launch this week, the first time the metal will be offered on a bourse in the West African nation.

The Lagos Commodities and Futures Exchange is licensed by the Securities and Exchange Commission to trade gold with the specification of the London Bullion Market Association’s 99.99% purity, targeting globally acceptable pricing and quality, according to Akinsola Akeredolu-Ale, managing director of the Lagos bourse.

The exchange is scheduled for a formal launch on July 28 and will in addition to gold trade other commodities including cashew, shea butter, paddy rice, maize, soybeans. and sorghum, Akeredolu-Ale said in an interview. “The aim is to diversify the asset base of the capital market and improve government revenue sources,” he said.

Nigeria, Africa’s largest crude producer, is encouraging public and private-sector collaboration to develop other mineral resources such as gems, zinc, iron ore, and lead to help curb dependence on oil, which accounts for about 90% of export earnings. Last year Thor Explorations Ltd. recorded the country’s first commercial gold output from its Segilola mine, with a target of 85,000 ounces a year.

The commodities exchange will broaden opportunities for Nigerian stockbrokers and reduce their dependence on the volatile equities market. It was established by the Association of Securities Dealing Houses of Nigeria to provide a platform for its members to diversify trading revenue. …

… For the remainder of the report:

END

4. OTHER GOLD/SILVER COMMENTARIES

Probably the only major that so far can survive as mining costs escalate against a backdrop of gold/silver price manipulation (price is kept from rising due to inflation)

Agnico Eagle Mines: Soaring Above The Peer Group

Jul. 28, 2022 6:02 AM ETAgnico Eagle Mines Limited (AEM)11 Comments10 Likes

Summary

- Agnico Eagle released its Q2 results this week, reporting quarterly production of ~858,200 ounces, a 71% increase from the year-ago period, driven by the recently closed merger with KL Gold.

- While this production growth was to be expected, costs came in below my estimates at $1,026/oz, evidence of Agnico’s superior business model that shines even in an inflationary environment.

- Given this solid performance, AEM remains on track to meet or beat its FY2022 guidance, and costs will remain within guidance at industry-leading levels.

- At a current valuation of less than ~7x cash flow, Agnico has rarely ever been this attractively valued, and I would be shocked if this valuation disconnect persisted, making this an attractive buying opportunity below $42.00 per share.

END

THIS IS AMUST VIEW:

https://lemetropolecafe.com/pfv.cfm?pfvID=17859

Alasdair Macleod: Has Basel III impacted gold & silver Last year the Basel III regulations went into effect, with many expecting an impact on the gold and silver prices.

Obviously we haven’t seen gold and silver shoot higher as some thought, although in today’s call I checked in with Alasdair Macleod of Goldmoney.com to get his thoughts on the policy impact a year later.

In the call he also comments on the latest central bank policies, the problems they’re creating, and how he sees it all playing out.

So to find out more, click to watch the video now!

5.OTHER COMMODITIES: WHEAT

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.7482

OFFSHORE YUAN: 6.7545

HANG SENG CLOSED DOWN 47.36 PTS OR 0.23%

2. Nikkei closed UP 99.73 OR 0.36%

3. Europe stocks CLOSED MOSTLY MIXED

USA dollar INDEX UP TO 106,75/Euro FALLS TO 1.0129

3b Japan 10 YR bond yield: FALLS TO. +.199/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 136.75/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.045%/Italian 10 Yr bond yield RISES to 3.40% /SPAIN 10 YR BOND YIELD FALLS TO 2.27%…

3i Greek 10 year bond yield RISES TO 3.00//

3j Gold at $1739.95 silver at: 19.40 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 75/100 roubles/dollar; ROUBLE AT 60.62

3m oil into the 99 dollar handle for WTI and 108 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 135.62DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9622– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9747well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.779 UP 5 BASIS PTS

USA 30 YR BOND YIELD: 3.079 UP 8 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.91

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Furious Rally Pauses As Sentiment Turns Metaworse Amid Record Earnings Barrage

THURSDAY, JUL 28, 2022 – 08:04 AM

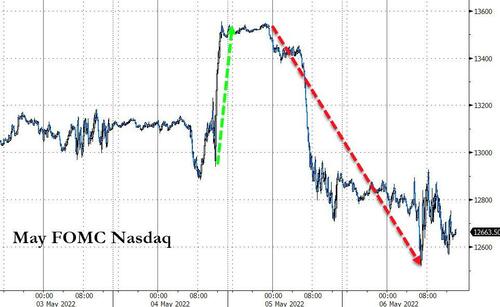

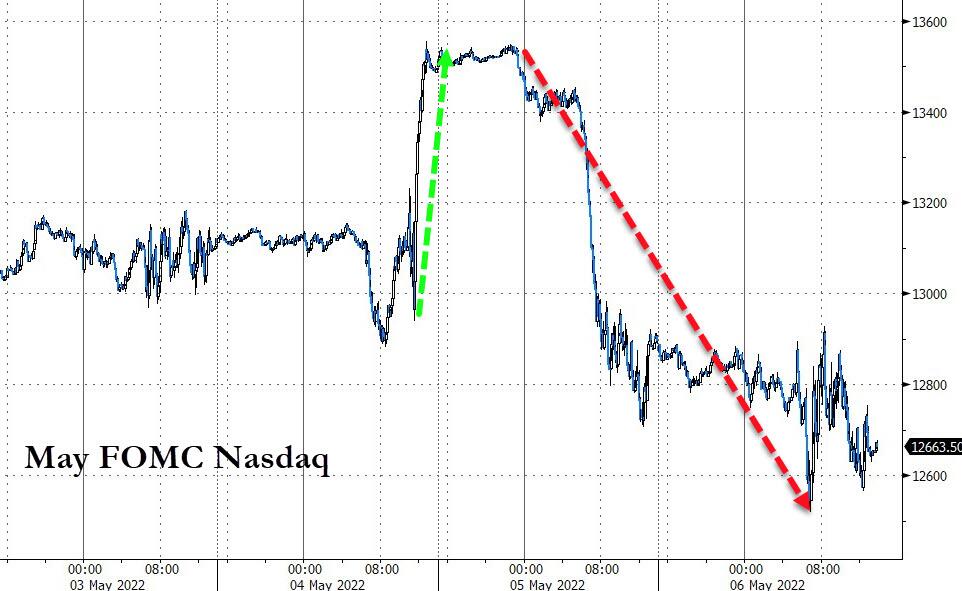

One day after the Nasdaq 100 posted its biggest jump since November 2020 when the market exploded higher after it interpreted Powell’s forward guidance purge and comment that it is “likely appropriate to slow rate increases at some point” as more dovish than expected, US stocks were set to pull back as downbeat earnings and a dire outlook from bad to Metaworse weighed on demand. Futures contracts on the technology-heavy Nasdaq 100 dropped 0.5% by 7:15 a.m. in New York, after the underlying gauge rallied 4.3% in the previous session. S&P 500 futures were down 0.2% after the benchmark index jumped to its highest level in seven weeks. Treasury yields were little changed and the dollar and bitcoin edged up.

In premarket trading, Facebook parent Meta tumbled after it reported its first-ever quarterly sales decline as ad spend by businesses cooled, leading to a far worse than expected forecast. Qualcomm also slipped as it issued a lackluster forecast. Renewable energy companies soared in Europe and premarket trading following a deal by Democrats and Senator Manchin to advance a bill that will spend hundreds of billions of dollars on energy security and climate change. Vestas Wind Systems A/S surged more than 14% as oil also rose. Spirit Airlines Inc. rose in premarket on a deal with JetBlue Airways Corp. Among other individual movers, Best Buy dropped in premarket trading as analysts slashed their price targets on the retailer after it cut its profit and sales outlook. Ford Motor on the other hand, jumped after reporting better-than-expected adjusted earnings per share for the second quarter. Here are some other notable premarket movers:

- Qualcomm (QCOM US) shares fall 4.5% in premarket trading after the chipmaker issued a lackluster forecast for the current quarter as it expects weakening economy to weigh on consumer spending on mobile devices. Watch shares of US chipmakers and semiconductor capital equipment stocks, including Lam Research (LRCX US), Applied Materials (AMAT US), Nvidia (NVDA US), Advanced Micro Devices (AMD US), Intel (INTC US), after Samsung’s quarterly profit missed estimates and Qualcomm’s forecast.

- Meta Platforms (META US) shares are down 5.9% in premarket trading, after the Facebook parent reported its first- ever quarterly sales decline as ad spend by businesses cooled.

- Ford (F US) shares jumped as much as 7.7% in US premarket trading after the carmaker’s adjusted earnings per share for the second quarter beat the average analyst estimate.

- Solar energy and renewables stocks gain in US premarket trading after Senator Joe Manchin and Senate Majority Leader Chuck Schumer struck a deal on a tax and energy policy bill.

- First Solar (FSLR US) +10%, SunRun (RUN US) +12%, Enphase Energy (ENPH US) +3.6%, SolarEdge (SEDG US) +4.0%

- Etsy (ETSY US) rises 6.1% in premarket trading on Thursday after the company posted stronger-than-expected second- quarter results, with most analysts seeing the online retailer retaining its market-share gains made during the pandemic

- ServiceNow (NOW US) shares fall 7.5% in US premarket trading, after the software company cut its full-year revenue forecast due to a stronger dollar and a potential pull back in demand.

- Spirit Airlines (SAVE US) shares climb 4.5% in premarket trading as JetBlue Airways is said to be close to an agreement to buy the carrier.

- Best Buy (BBY US) shares drop 4.4% in US premarket trading as analysts slashed their price targets on the retailer after it cut its profit and sales outlook, with brokers blaming the macroeconomic backdrop.

- Teladoc Health (TDOC US) shares fall about 25% in premarket trading after the virtual- care company’s 3Q Ebitda guidance came in below expectations, with analysts saying the outlook for Teladoc is likely to be revised downward.

- Community Health Systems Inc. (CYH US) shares plummet 52% in premarket trading after the hospital company reported a surprise loss per share for the second quarter.

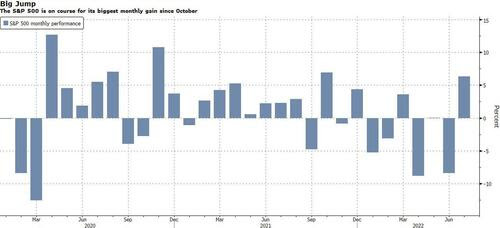

US stocks have rallied in July, putting the S&P 500 Index on course for its biggest monthly gain since October 2021, as the market finally grasps what we have been saying since January, namely that the weaker macroeconomic will prompt the central bank to “pivot” to easier policy, coupled with bets that much of the bad news was now priced in. It could get even worse, er better, today when the US reports Q2 GDP which may confirm that the world’s largest economy is in a technical recession further shortening the Fed tightening phase.

To be sure, the knee-jerk relief in markets on possible crumbs of comfort from the Fed outlook echoes a pattern seen after earlier hikes. Those bouts of optimism stumbled on recession risks from a global wave of monetary tightening, Europe’s energy woes and China’s property sector and Covid challenges. “We do feel the hikes are going to slow from these levels,” Laura Fitzsimmons, JPMorgan Australia’s executive director of macro sales, said on Bloomberg Television. But financial-industry participants are skeptical about the pricing indicating Fed rate cuts in 2023, she added.

“As the tug-of-war between inflation and recession fears plays out in the second half of the year, we expect to see highly volatile markets,” Richard Flynn, UK Managing Director at Charles Schwab, wrote in a note.

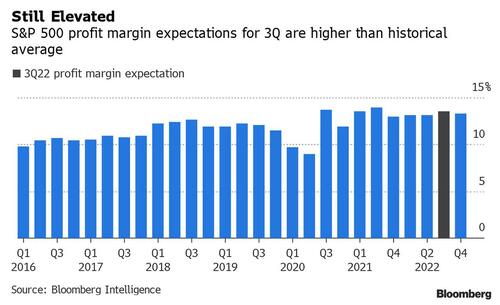

All eyes have also been on corporate earnings for signs of resilience in profit margins to surging inflation and weaker sentiment. A record number of US and European firms worth more than $9.4 trillion will report their results on Thursday.

Of these $6.8 trillion are 55 S&P500 companies if constituents of the Nasdaq 100 are included. That comes on the heels of the Fed raising rates by 75 basis points for a second month, saying such a move is possible but that the pace of hikes will slow at some point. Chair Jerome Powell said policy will be set meeting-by-meeting as he tries to control rising prices amid signs of an economic slowdown. Big Tech will be a particular focus again with results from Amazon, Apple and Intel.

“We see the earning season as a mixed bag and it’s not necessarily very good news looking forward because we have an economic momentum that is this decelerating very fast and we also have central banks all around the world hiking interest rates,” Geraldine Sundstrom, portfolio manager for asset allocation strategies at Pimco, said on Bloomberg TV.

“For financial markets, the risk of the Fed taking an overly aggressive stance has eased over the past week due to mixed growth and inflation data,” said Gurpreet Gill, macro strategist of fixed income and liquidity solutions at Goldman Sachs Asset Management. “Growing evidence of slowing demand has curbed the need for speed –- hence the Fed did not provide forward guidance on its policy path.”

The dovish Fed euphoria also helped lift European stocks, which initially faded a strong opening bounce only to recover all gains. Euro Stoxx 600 rose 0.5%, with the FTSE MIB outperforming, adding 0.8%, IBEX lags, dropping 1.3%. Telecoms, food & beverages and utilities are the worst-performing sectors. The Stoxx 600 Basic Resources index rose as much as 3.6%, the top-performing sub-index in the benchmark, following well-received results and with metals prices gaining. ArcelorMittal jumped following a cash flow beat and new buyback in its results, while Anglo American gains as its earnings and dividend both topped expectations. Other steel stocks SSAB, Voestalpine higher after ArcelorMittal and after beat from Acerinox. Copper miners KGHM and Antofagasta the biggest gainers with copper price up for fifth day. Here are some of the most notable market movers:

Shell rises as much as 2.2% after the company reported what RBC Capital Markets described as strong results and announced that it will repurchase a further $6 billion of shares in the third quarter.

- Renewable energy companies’ shares soared following a deal by US senators to advance a bill that will spend hundreds of billions of dollars on energy security and climate change. Vestas Wind Systems stock gained as much as 15%, Nordex +12%, Orsted +6.5%, SMA Solar +7.6%, Meyer Burger +9.3%

- Schneider Electric shares were up as much as 5.2% after it reported a strong set of results; analysts welcome the increased FY growth targets and the company’s ability to pass on inflation.

- Diageo rises as much as 2.7% after the British distiller’s FY22 organic sales beat estimates. The group reiterated its medium-term guidance even as it expects a challenging environment for FY23.

- Stellantis shares gain as much as 4.3%, after the carmaker reported 1H results that Jefferies called “impressive and clean.”

- TotalEnergies declines as much as 3.8%, after its plan to maintain the pace of buybacks disappointed some analysts amid expectations for accelerated share repurchases in the industry.

- Airbus shares fall as much as 6.6% in Paris after the aircraft maker cut its full-year delivery projections and pushed back ramping up the A320 build rate to 65 a month from summer 2023 until early 2024.

- Nestle shares drop as much as 2.2% after the company cut its margin outlook for the year. The results are “mixed,” given the sales beat and increased FY organic revenue forecast, but there are questions around margin, according to analysts.

- Fresenius Medical Care shares slide as much as 15% after the dialysis services firm issued a guidance downgrade that showed significant cost pressures on many fronts, Truist says in a note.

Ironically, as Europe edges toward a full-blown energy crisis and recession, its manufacturing giants are raking in the cash. Luxury-car leader Mercedes-Benz joined Europe’s biggest chemicals maker BASF, Swiss building-materials producer Holcim, shipping company Hapag-Lloydand others to report a jump in profit and raise earnings forecasts for the year.

The results offered a stark contrast to the wave of grim economic news sweeping across Europe. Confidence in the euro-area fell to the weakest in almost 1 1/2 years as fears of energy shortages haunt consumers and businesses, and the European Central Bank’s first interest-rate increase in a more than decade feeds concerns that a recession is nearing.

Earlier in the session, Asian stocks also advanced after the Federal Reserve said it will slow the pace of interest-rate increases at some point. The MSCI Asia Pacific Index climbed as much as 1.1%, driven by gains in material and energy stocks. Equity benchmarks in the Philippines and New Zealand led gains in the region as a weakening dollar boosted risk appetite. “The stock markets may reverse their recent falls” following the Fed’s decision, said Heo Pil-Seok, chief executive officer at Midas International Asset Management in Seoul.

“Starting today, we should see if there’s any changes in foreign fund flows, as outflows have somewhat eased recently,” he said, adding however that the stock rally may be short-lived as investors remain cautious on earnings. Gains in Asia were small relative to the rally in US stocks overnight, as investors monitored the latest local earnings along with China’s property crisis and the Covid situation. Asian tech bellwether Samsung Electronics provided a weak demand forecast Thursday, citing uncertainties following a rare earnings miss. Chinese benchmarks were flat amid the Politburo meeting and a possible call between Xi Jinping and Joe Biden.

Elsewhere, traders are awaiting a phone call between President Joe Biden and China’s Xi Jinping, which could touch on US tariffs and other points of tension.

Japanese equities climbed, following US peers higher on relief after the Federal Reserve raised interest rates by 75 basis points and indicated that monetary policy tightening will eventually slow down. The Topix rose 0.2% to 1,948.85 as of the market close in Tokyo, while the Nikkei 225 advanced 0.4% to 27,815.48 as the yen gained against the dollar, weighing on exporters such as Toyota. Recruit Holdings Co. contributed the most to the Topix’s gain, increasing 4.4%. Out of 2,169 shares in the index, 1,406 rose and 652 fell, while 111 were unchanged. “It does seem as if the market bottomed out at the end of June,” said Hitoshi Asaoka, a strategist at Asset Management One. “There is a sense that a rise in interest rates is receding worldwide and stocks are also calming down along with that.” Fed Hikes by 75 Basis Points as Powell Sees No US Recession Now

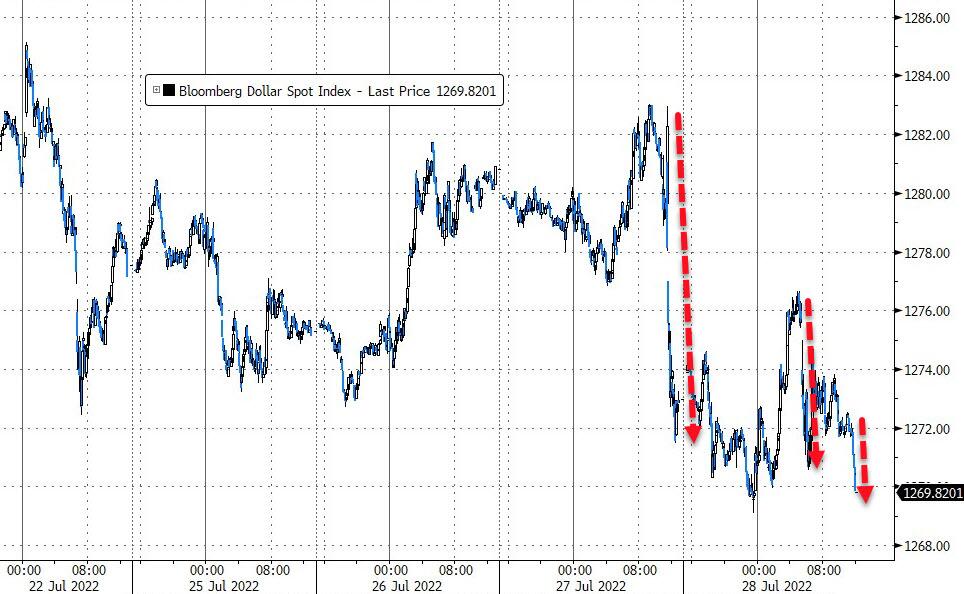

In FX, the Bloomberg dollar spot index revered a drop of 0.6% to trade higher. SEK and DKK are the weakest performers in G-10 FX, JPY maintains outperformance, trading at 135.33/USD. The yen was around 135.40 per dollar, after strengthening more than 1% to 135.11 in Asia, extending an overnight rise to hit a three-week high. It jumped by a similar amount against the euro and the Australian dollar.

In rates, Treasury yields were little changed to 3bps lower in European trading after dropping on Wednesday. German curve steepens with two-year yields lower after some state inflation gauges slow, while rates at the longer end rise. US 10-year yields are steady at 2.79%.

In commodities, WTI drifts 1.7% higher to trade below $99. Spot gold rises roughly $10 to trade near $1,745/oz. Most base metals trade in the green; LME zinc rises 3%, outperforming peers.

Looking the day ahead, in addition to the US GDP we get core PCE, consumption, and jobless claims in the US. In Europe, German CPI and France PPI are due with the first German regional numbers out just after we press send this morning. Our economists expect MoM CPI at +0.8% in Germany, and +0.5% on the EU harmonized MoM measure.

Market Snapshot

S&P 500 futures down 0.3% to 4,011.25

Gold spot up 0.7% to $1,746.23

U.S. Dollar Index down 0.18% to 106.26

Top Overnight News from Bloomberg

- Chair Jerome Powell said the Federal Reserve will press on with the steepest tightening of monetary policy in a generation to curb surging inflation, while handing officials more flexibility on coming moves amid signs of a broadening economic slowdown.

- The yen catapulted higher against major peers on Thursday as lowered expectations for rate hikes caused hedge funds to cover short bets from one of the biggest global macro trades of the year.

- US Stocks Set to Dip After Biggest Tech Gain Since November 2020

- Meta Disappoints With Forecast Miss, First-Ever Revenue Drop

- China Leaders Call for ‘Best’ Growth Outcome at Key Meeting

- US Offers Russia to Swap Jailed Basketball Star for Arms Deale

- US Aircraft Carrier Enters South China Sea Amid Taiwan Tensions

- US Offers Russia to Swap Griner and Whelan for Arms Dealer Bout

- Barclays Latest Bank to Make Provision for US WhatsApp Fine

- Yen Roars Back as Hedge Funds Cut and Run From Big Macro Short

- China-US Deal Needed Soon to Avoid Delistings, Gensler Says

- Alibaba’s Gains From Primary Listing Plan Wiped out in Two Days

- Samsung’s Profit Is Latest Tech Casualty to Recession Fears

- Senate Deal Includes EV Tax Credits Sought by Tesla, Toyota

- Manchin Backs $369 Billion Energy-Climate Plan, Rejects SALT

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks eventually traded higher across the board following the firm lead from Wall Street. ASX 200 saw firm gains across its Tech, Gold, and Mining sectors. Nikkei 225 gained in early trade and briefly topped the 28k mark before recoiling as the JPY saw a sudden bout of strength. KOSPI benefited from Samsung Electronics’ rise post-earnings, although the firm echoed recent remarks from SK Hynix regarding weaker H2 memory demand. Hang Seng moved on either side of breakeven but later saw an upside bias as Hong Kong Finance Secretary said Hong Kong’s H2 economic performance will be better than H1. Shanghai Comp eventually gained despite the recent cautious commentary from Chinese President Xi.

Top Asian News

- Chinese Politburo says it will keep economic operations in a reasonable range.

- Australian Treasurer Chalmers said the final budget outcome for 2021/22 likely to show a dramatically better-than-expected outcome.

- Samsung Electronics (005930 KS) – Q2 2022 (KRW): Revenue 772tln (Co. exp. 77tln); operating profit 14.1tln (exp. 14tln). Net profit 11.1tln (exp. 10.3tln); Chip operating profit 9.98tln (exp. 11.08tln); expects weaker H2 phone/PC memory chip demand.

- South Korean President Yoon has ordered to take steps against illegal activities regarding stock short selling, via Yonhap.

- Hong Kong Finance Secretary said Hong Kong’s H2 economic performance will be better than H1; property market fundamentals remain sound. Hong Kong Monetary Chief expects overnight and one-month interbank rate to continue to rise at a much faster pace; says HKD has been stable and has been operating in an orderly manner; public should be prepared for interbank rate to climb further, via Reuters.

- PBoC injected CNY 2bln via 7-day reverse repos with the maintained rate of 2.10% for a net drain of CNY 1bln.

- PBoC set USD/CNY mid-point at 6.7411 vs exp. 6.7425 (prev. 6.7731).

- Japanese government spokesperson says there is currently no plan to impose restrictions on people’s movements following increasing COVID cases; Tokyo COVID cases reach 40,406 vs. previous record of 34,995.

European bourses are modestly softer, Euro Stoxx 50 -0.10%, but relatively contained now after fading initial gains from the FOMC-inspired upside. Amid numerous earnings updates from Europe & in the US aftermarket. US futures are relatively stable but continue to post modest losses with the NQ -0.8% lagging amid pre-market downside in Meta post-earnings, -6.0%. Meta Platforms Inc (META) Q2 2022 (USD): EPS 2.46 (exp. 2.59), Revenue 28.82bln (exp. 28.95bln), Advertising revenue 28.15bln (exp. 28.53bln). Outlook reflects continuation of weak advertising demand environment it experienced throughout Q2. Guidance assumes FX will be about a 6% headwind to Y/Y total revenue growth in Q3. Co. said the economic downturn will have a broad impact on digital advertising business, says the situation seems worse than it did a quarter ago. -6.0% in the pre-market. Jack Ma intends to relinquish control of Ant Group, via WSJ sources; to transfer some voting power to executives, could push-back IPO timing by over a year.

Top European News

- German consumer energy bill to increase by EUR 1k/year, following a cost shift, via Bloomberg; Effective from October 1st, via Reuters sources; levy will cover 90% of costs. Subsequently, German Economy Minister says the gas level would cost several hundred EURs per household.

- India to Restart Ukraine Sunflower Oil Imports as Trade Eases

- Wind, Solar Stocks Surge After US Energy Bill Agreement

- Vanguard Europe MD Says Climate Is Now ‘the Most Material Risk’

- Schroders Up; Jefferies Says Results Show Resilience of Platform

- EDF Posts $1.3 Billion Loss as State Readies Nationalization

- Turkey Raises 2022 Inflation Forecast to 60.4% on Imports, Lira

Central Banks

- BoJ Deputy Governor Amamiya said we must not loosen our grip in keeping monetary policy easy as there is no prospect yet of sustainably meeting the 2% inflation target. He added that consumer sentiment has been worsening due to rising energy and food prices. BoJ must be vigilant to financial and forex moves and their impact on economy and prices.

- ECB’s Visco refrains from saying whether markets should expect a 25bps or 50bps hike in September; not prepared to say the ECB would go for 50bps in September in order to reach its target quicker. Adds, the ECB doesn’t really know where its target is.

- BoK to strengthen monitoring of FX and capital flows following the FOMC hike, according to Bloomberg.

- HKMA raised its base rate by 75bps to 2.75%, as expected, following the earlier Fed rate hike.