Options expiry concludes today

GOLD; $1714.90 down $10.20

SILVER: $18.08 down 36 cents

ACCESS MARKET:

GOLD $

SILVER: $

Bitcoin morning price: $20,305 DOWN 366

Bitcoin: afternoon price: $20,671 DOWN 1378

Platinum price

Palladium price;

END

DONATE

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,723.200000000 USD

INTENT DATE: 08/30/2022 DELIVERY DATE: 09/01/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 179

118 C MACQUARIE FUT 150

132 C SG AMERICAS 41

435 H SCOTIA CAPITAL 34

624 H BOFA SECURITIES 107

657 C MORGAN STANLEY 8

661 C JP MORGAN 171

690 C ABN AMRO 32

737 C ADVANTAGE 33 7

800 C MAREX SPEC 4

905 C ADM 42

TOTAL: 404 404

MONTH TO DATE: 404

JPMorgan stopped: 32/91

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR SEPT CONTRACT:

404 NOTICES FOR 40,400 OZ //1.2566 TONNES

total notices so far: 40,400 contracts for 40,400 oz (1.2566 tonnes)

SILVER NOTICES: 5,244 NOTICES FILED FOR 26,220,000 OZ/

total number of notices filed so far this month 1051 : for 5,255,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $10.20

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD//

INVENTORY RESTS AT 973.37 TONNE

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $.44

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 465.573 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 3355 CONTRACTS TO 138,747. AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.44 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.44) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A GIGANTIC GAIN OF 6176 CONTRACTS ON OUR TWO EXCHANGES, AND MINOR SPECULATOR LIQUIDATION.

WE MUST HAVE HAD:

I) MINOR SPECULATOR SHORT LIQUIDATIONS ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 29.380 MILLION OZ / // V) HUGE SIZED COMEX OI GAIN///MINOR SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -XX

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTACTS for 23 days, total 15,826 contracts: 79.130 million oz OR 3.440 MILLION OZ PER DAY. (688 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 79.130 MILLION OZ

.

LAST 16 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 79.130 MILLION OZ //FINAL

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3355 DESPITE OUR $0.44 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC SIZED EFP ISSUANCE CONTRACTS: 2821 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS A// MINOR SPEC SHORT LIQUIDATIONS BUT STRONG BANKER ADDITIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 29.380 MILLION OZ // .. WE HAD AN ATMOSPHERIC SIZED GAIN OF 6176 OI CONTRACTS ON THE TWO EXCHANGES FOR 30.88 MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 5244 NOTICE(S) FILED TODAY FOR 26,220,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1625 CONTRACTS TO 459,474 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:–XXX CONTRACTS.

.

THE FAIR SIZED INCREASE IN COMEX OI CAME DESPITE OUR STRONG FALL IN PRICE OF $12.00//COMEX GOLD TRADING/TUESDAY / WE MUST HAVE HAD ADDITIONAL SPECULATOR SHORT COVERINGS ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND MINOR SPECULATOR SHORT COVERINGS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 8.401 TONNES ON FIRST DAY NOTICE

YET ALL OF..THIS HAPPENED DESPITE OUR FALL IN PRICE OF $12.00 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 5087 OI CONTRACTS 15.822 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3462 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 459,474

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5087 CONTRACTS WITH 1625 CONTRACTS INCREASED AT THE COMEX AND 3462 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 6529 CONTRACTS OR 20.307 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3462) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (1625): TOTAL GAIN IN THE TWO EXCHANGES 5087 CONTRACTS. WE NO DOUBT HAD 1) MINOR SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.401 TONNES 3) ZERO LONG LIQUIDATION//// //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

61,593 CONTRACTS OR 6,159,300 OZ OR 191.58 TONNES 23 TRADING DAY(S) AND THUS AVERAGING: 2677 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 23 TRADING DAY(S) IN TONNES: 191.58 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 191.58/3550 x 100% TONNES 5.40% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 191.58 TONNES (//FINAL//DRAMATICALLY FALLING AGAIN)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT., FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GIGANTIC SIZED 3355 CONTRACT OI TO 138,747 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 2821 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 2821 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2821 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3355 CONTRACTS AND ADD TO THE 2821 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF 6176 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 30.880 MILLION OZ

OCCURRED DESPITE OUR LOSS IN PRICE OF $0.44

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 25.08 PTS OR 0.78% //Hang Sang CLOSED UP 5.36 OR 0.03% /The Nikkei closed DOWN 104.05 OR % 0.31. //Australia’s all ordinaires CLOSED DOWN 0.06% /Chinese yuan (ONSHORE) closed UP AT 6.8960//OFFSHORE CHINESE YUAN UP 6.8956// /Oil DOWN TO 88.92 dollars per barrel for WTI and BRENT AT 95.24/ / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1625 CONTRACTS TO 459,474 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR FALL OF $12.00 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (3462 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF AUGUST.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3462 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :3462 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3462 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED SIZED TOTAL OF 5087 CONTRACTS IN THAT 3462 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 1625 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG FALL IN PRICE OF GOLD $ 12.00. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (8.401),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT: 8.401 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $12.00) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED TOTAL GAIN ON OUR TWO EXCHANGES // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS////// WE HAVE REGISTERED A STRONG SIZED GAIN OF 20.307 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT (8.401 TONNES)…

WE HAD -XXX CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 5087 CONTRACTS OR 508,700 OZ OR 15.822 TONNES

Estimated gold volume 101,420/// extremely poor/

final gold volumes/yesterday 187,676/extremely poor

INITIAL STANDINGS FOR AUGUST ’22 COMEX GOLD //AUGUST 31

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 4989.354 oz Brinks HSBC Manfra |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 4,469.651 oz |

| No of oz served (contracts) today | 404 notice(s) 40400 OZ 1.2566 TONNES |

| No of oz to be served (notices) | 2297 contracts 229,700 oz 7.1446 TONNES |

| Total monthly oz gold served (contracts) so far this month | 40400 notices 40400 OZ 1.2566 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into Brinks: 4469.651 oz

total deposits 4469.651 oz oz

3 customer withdrawals:

i) Out of Brinks 32.15 oz (one kilobar)

ii) Out of HSBC: 487.552 oz

iii) OUT OF MANFRA: 4469.651 oz

total: 4989.354 oz

total in tonnes: 0.1556 tonnes

Adjustments: dealer to customer //3

i) Brinks 8,419.312 oz

ii) JPM: 6,585.067 oz

iii) Manfra: 24,783.421 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of SEPT we have an oi of 2701 contracts having GAINED 29 contracts .

Thus by definition, the initial amount of gold standing for Sept is as follows:

2701 notices x 100 oz per notice = 270100 OZ

or

8.401 tonnes

October LOST 284 contracts DOWN to 38,927

We had 404 notice(s) filed today for 40400 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 404 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (404) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 2701 CONTRACTS ) minus the number of notices served upon today 404 x 100 oz per contract equals 270,100 OZ OR 8.401 TONNES the number of TONNES standing in this active month of AUGUST.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (404) x 100 oz+ (2701) OI for the front month minus the number of notices served upon today (404} x 100 oz} which equals 270,100 oz standing OR 8.401 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 8.401 TONNES (A GREAT STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,344,669.896 oz 72.92 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 28,385,818.612 OZ

TOTAL REGISTERED GOLD: 13,684,523.529 OZ (425.63 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 14,701,295.083 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 11,333,985. OZ (REG GOLD- PLEDGED GOLD) 352.70 tonnes//rapidly declining

END

SILVER/COMEX/AUGUST 31

SEPTEMBER CONTRACT MONTH:

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 572,369.660 oz CNT Brinks |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 5244CONTRACT(S) 26,220,000 OZ) |

| No of oz to be served (notices) | 632 contracts (3,160,000 oz) |

| Total monthly oz silver served (contracts) | 5244 contracts 26,220,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

total deposit: nil oz

JPMorgan has a total silver weight: 170.385 million oz/329.211 million =51.74% of comex

Comex withdrawals:2

i) Out of CNT: 568,507.760 oz

ii) Out of Brinks: 3861.900 oz

total: 572,369.660 oz

adjustments: 1//dealer to customer//JPMorgan

238,958.530 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 51.786 MILLION OZ

TOTAL REG + ELIG. 329.211 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR AUGUST

silver open interest data:

FRONT MONTH OF SEPT OI: 5876 CONTRACTS HAVING LOST 1626 CONTRACTS.

THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER STANDING IN THIS ACTIVE MONTH OF SEPT. IS AS FOLLOWS:

5876 NOTICES X 5000 OZ PER NOTICE =

29,380,000 OZ (THIS IS A HUGE INITIAL STANDING FOR SILVER/SEPTEMBER)

OCTOBER GAINED 71 CONTRACTS TO STAND AT 716

CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 5244 for 26,220,000 oz

Comex volumes:38,731// est. volume today// poor

Comex volume: confirmed yesterday: 96,524 contracts ( good)

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 5244 x 5,000 oz = 26,220,000 oz

to which we add the difference between the open interest for the front month of SEPT(5876) and the number of notices served upon today 5244 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST./2022 contract month: 5,244 (notices served so far) x 5000 oz + OI for front month of SEPT (5876) – number of notices served upon today (5244) x 5000 oz of silver standing for the SEPT contract month equates 29,380,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

AUGUST 10//WITH GOLD UP $2.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES

AUGUST 9/WITH GOLD UP $6.70: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES.

AUGUST 8/WITH GOLD UP $13.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD//INVENTORY RESTS AT 999.16 TONNES

AUGUST 5/WITH GOLD DOWN $14.25: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .33 TONNES FROM THE GLD////INVENTORY RESTS AT 1000.32 TONNES

AUGUST 4 WITH GOLD UP $29.00 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD///INVENTORY REST AT 1000.65 TONNES

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 29//WITH GOLD UP $12.50; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1005.29 TONNES

JULY 28/WITH GOLD UP $31.25; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 27.//WITH GOLD UP $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.29 TONNES

JULY 26/WITH GOLD DOWN $1.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.29 TONNES

JULY 25/WITH GOLD DOWN $7.85: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 1005.87 TONNES

JULY 22/WITH GOLD UP $17.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1005.87 TONNES

JULY 21/WITH GOLD UP $11.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.101 TONNES FROM THE GLD////INVENTORY RESTS AT 1005.87 TONNES

JULY 20/WITH GOLD DOWN $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1009.06 TONNES

JULY 19/WITH GOLD DOWN $.35 :BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.22 TONNES FROM THE GLD//INVENTORY RESTS AT 1009.06 TONNES

GLD INVENTORY: 973.37 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 10/WITH SILVER UP 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 9/WITH SILVER DOWN 25 CENTS TODAY: TWO CHANGES IN SILVER INVENTORY AT THE SLV: FIRST: A DEPOSIT OF 461,000 OZ INTO THE SLV AND THEN A WITHDRAWAL OF 1.014 MILLION OZ..//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 8/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 5/WITH SILVER DOWN 28 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 922,000 OZ FROM THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 4 WITH SILVER UP 21 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 527,000 OZ FROM THE SLV////INVENTORY RESTS AT 486.634 MILLION OZ

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

JULY 29/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 461,000 OZ FROM THE SLV..//INVENTORY RESTS AT 483.657 MILLION OZ/

JULY 28/WITH SILVER UP $1.24 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 484.118 MILLION OZ/

JULY 27/.WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL 11.479 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 484.118MILLION OZ//

JULY 26/WITH SILVER UP 16 CENTS: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.504 MILLION OZ FROM THE SLV//: //INVENTORY RESTS AT 495.597 MILLION OZ//

JULY 25/WITH SILVER DOWN 24 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.383 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 499.101 MILLION OZ//

JULY 22/WITH SILVER DOWN 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 500.484 MILLION OZ//

JULY 21/WITH SILVER UP 5 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.19 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 500.484MILLION OZ/

JULY 20/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 8.253 MILLION OZ FORM THE SLV/INVENTORY RESTS AT 507.585 MILLION OZ//

JULY 19/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 515.838 MILLION OZ//

CLOSING INVENTORY 465.573 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

end

GOLD/SILVER

END

3.Chris Powell of GATA provides to us very important physical commentaries

A super read..

Dan Oliver/Myrmikan

This is where we are heading: The Fed’s rate increases according to Dan Oliver is meant to prevent commodity money

(Dan Oliver)

Myrmikan’s Dan Oliver: Fed’s rate increases may aim to prevent commodity money

Submitted by admin on Tue, 2022-08-30 14:46Section: Daily Dispatches

2:47p ET Tuesday, August 30, 2022

Dear Friend of GATA and Gold:

In his latest market analysis, Dan Oliver, founder and manager of Myrmikan Capital in New York, suspects that the Federal Reserve’s policy of raising interest rates is aimed at protecting the U.S. dollar by aborting the transition of the world monetary system to a commodity basis.

Oliver writes: “The United States will not willingly abandon the global reserve status of its currency, which maintains its global hegemony. It did not when Saddam Hussein proposed selling oil in terms other than the dollar, nor when Muammar Gaddafi proposed setting up a gold-backed pan-African currency

“American neocons publicly call for [Russian President Vladimir] Putin to share a similar fate, but the methods used against Iraq and Libya are too risky against a nuclear-armed Russia — the reason for aiding a proxy war to try to destabilize Russia without direct conflict.

“Another way to undermine the development of a competing, commodity-backed, BRICs currency is by targeting commodity prices. It is perhaps this political prerogative that is driving Fed policy, more than general management of the business cycle and inflation.”

Oliver’s analysis is headlined “The New Bancor” and it’s posted in PDF format at Myrmikan’s internet site here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4. OTHER GOLD/SILVER COMMENTARIES

A very big story!

special thanks to John Adams for his work on this issue

(Financial Review Australia)

and a special thanks to John for providing the article to us:

Financial crimes regulator probes Perth Mint

The financial crimes regulator has launched an investigation into Perth Mint, Australia’s biggest gold and silver refiner, over what it has described as compliance concerns, and ordered the appointment of an external auditor under the Anti-Money Laundering and Counter-Terrorism Financing Act.

The AUSTRAC investigation into Gold Corporation, which trades as Perth Mint and is owned by the West Australian government, comes after a series of reports in The Australian Financial Review into a tainted gold scandal

AUSTRAC has tasked the external auditor with assessing Perth Mint’s compliance with the anti-money laundering and counter-terrorism financing (AML/CTF) laws and related matters.

AUSTRAC said it had identified compliance concerns following a period of engagement with Perth Mint, which is chaired by former Rio Tinto boss Sam Walsh.

The external auditor must report to AUSTRAC within 180 days of being appointed and will examine Gold Corporation’s compliance under the AML/CTF Act, the requirement to have an ongoing customer due diligence program, and suspicious matter reporting obligations.

In June 2020, the Financial Review reported the mint was buying up to $200 million of “conflict gold” annually from a convicted killer in Papua New Guinea, a breach of its global accreditation and internal policies. The series of reports raised other concerns about the mint’s actions.

AUSTRAC chief executive Nicole Rose said AML/CTF compliance requirements were in place to protect businesses, the financial system, and the Australian community from criminal threats.

“AUSTRAC does not hesitate to take action where a business that we regulate is failing to satisfy their responsibility to protect themselves and Australia’s financial system from criminal activity,” Ms Rose said.

“We will continue to work closely with Gold Corporation (Perth Mint) to address compliance concerns.”

AUSTRAC said the audit results would “assist Gold Corporation to comply with anti-money laundering obligations, and inform AUSTRAC whether any further regulatory action is required”.

Perth Mint chief executive Jason Waters said it was constantly identifying areas of improvement, including addressing historic practices that were no longer fit-for-purpose and updating the way it engaged with customers.

“We support the regulator’s decision for the Perth Mint to appoint an external auditor as part of efforts to ensure that our AML/CTF program is robust and appropriate,” he said.

“We are confident our strong and focused program already underway at the Perth Mint will address concerns identified by AUSTRAC.”

Mr Waters, the former boss of the WA government-owned power provider Synergy, took the reins at the mint this year after the departure of Richard Hayes.

-END-

.

end

5.OTHER COMMODITIES:

COMMODITIES IN GENERAL/COAL

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.8969

OFFSHORE YUAN: 6.8956

HANG SENG CLOSED UP 5.36 PTS OR 0.03%

2. Nikkei closed DOWN 104.05 OR 0.37%

3. Europe stocks CLOSED ALL RED

USA dollar INDEX DOWN TO 108.88/Euro FALLS TO 0.9998

3b Japan 10 YR bond yield: FALLS TO. +.221/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 138.71/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: UP -// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.490%/Italian 10 Yr bond yield RISES to 3.78% /SPAIN 10 YR BOND YIELD RISES TO 2.68%…

3i Greek 10 year bond yield RISES TO 4.07//

3j Gold at $1711.05 silver at: 18.03 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 19/100 roubles/dollar; ROUBLE AT 60.12//

3m oil into the 88 dollar handle for WTI and 95 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 138.71DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 9789– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.98005well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.132 UP 2 BASIS PTS

USA 30 YR BOND YIELD: 3.250 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,17

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

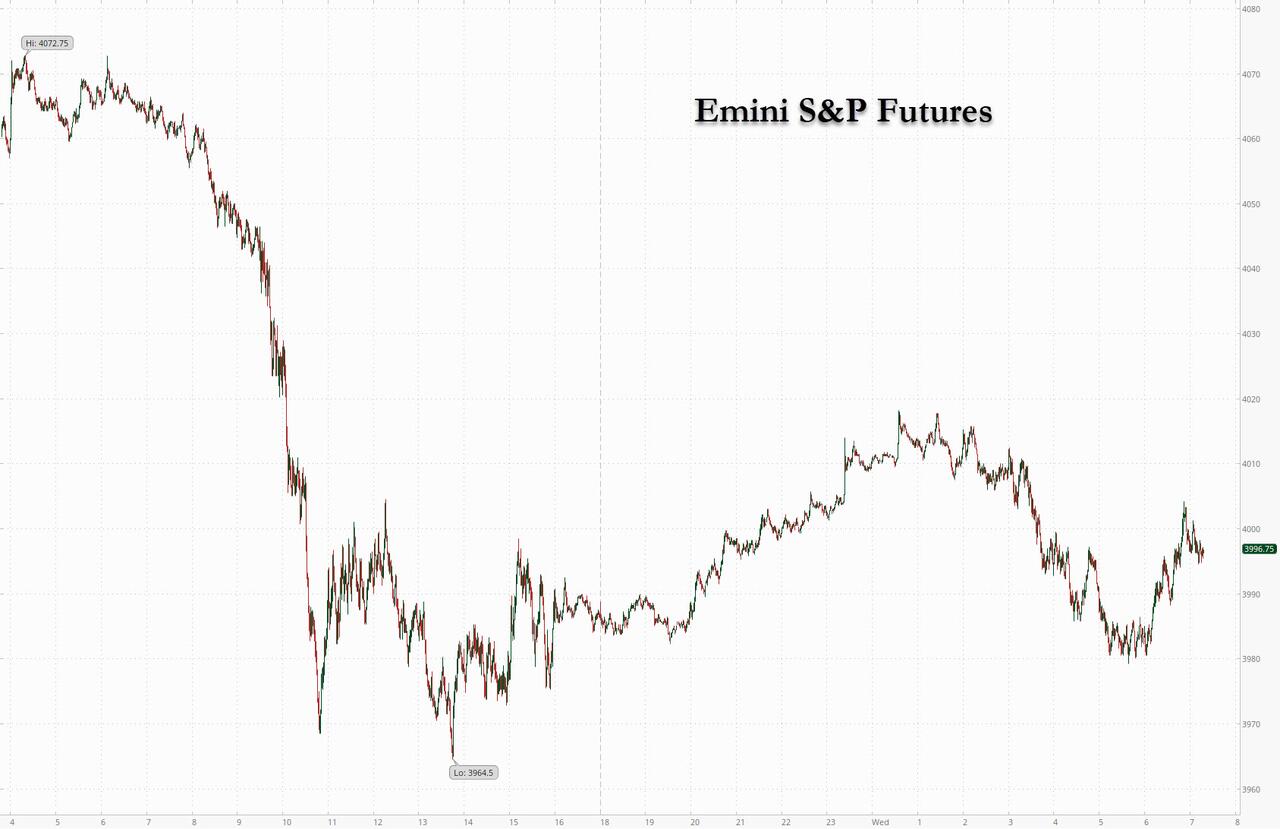

Futures Head For Another Monthly Drop, As Oil Slumps, Yields And Dollar Rise

WEDNESDAY, AUG 31, 2022 – 07:44 AM

After three days of steep declines, S&P futures traded between modest gains and losses as global markets headed for the third consecutive weekly decline and another monthly drop on concerns that aggressive central bank tightening will push the global economy into a hard recession. At 7:15am ET, futures were up 0.2% and Nasdaq futures rose 0.7%, after trading both higher and lower earlier in the session. The dollar rose, Treasury yields jumped after another record CPI print in Europe, while the bizarre oil slump extended.

In premarket trading, Bed Bath& Beyond plunged after the home-goods retailer filed a form to sell an unspecified number of shares.

HP also fell 6.8% after the company reported quarterly sales that missed estimates and cut its annual profit forecast as demand for personal computers and printers slowed. Analysts noted that the PC maker will need a couple of quarters to correct its inventory. Here are other notable premarket movers:

- Robinhood (HOOD US) falls 2.3% as Barclays cut its rating to underweight from equal weight

- ChargePoint (CHPT US) shares rose as much as 2.1% in US premarket trading, after the electric vehicle charging network operator’s second-quarter revenue came in ahead of estimates, with analysts positive on the company’s gross margin performance amid supply-chain woes

- HP Enterprise (HPE US) narrowed its full-year adjusted earnings per share forecast and reported in-line revenue for the third quarter. Analysts were bracing for the worst, after Dell’s disappointing outlook last week. Shares fall 1% in premarket trading

- PayPal shares rise 2.9% in premarket trading after Bank of America upgraded its rating on the payments stock to buy from neutral previously

- Morgan Stanley resumes coverage of Welltower (WELL US) at overweight and a $90 PT with the broker bullish on a recovery for the US senior housing market

“What’s clear is that predicting this market is not clean cut,” Angeline Newman, a managing director at UBS Global Wealth Management, said on Bloomberg Television. “We are living in a world where conflicting economic signals are making the path of monetary policy very difficult to determine.”

Market bets on a shallower trajectory for Federal Reserve tightening are receding, raising the prospect of more losses for stocks and bonds in an already difficult year. Investors are scouring incoming data for clues on the policy path, with August US jobs figures on Friday the next key report.

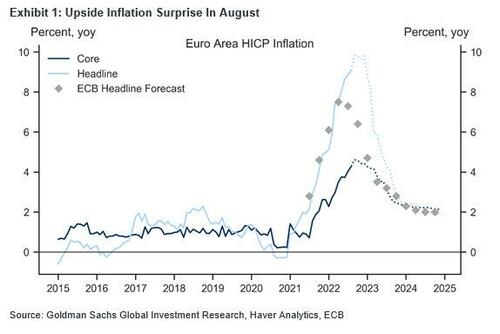

European shares reversed earlier gains to trade at the lowest level in more than six weeks, after Euro-area inflation accelerated to another all-time high, strengthening the case for the European Central Bank to consider a jumbo interest-rate hike when it meets next week. ECB Governing Council member Joachim Nagel urged a “strong” reaction, hinting at a 75bps hike just as Europe braces for an energy disaster with winter coming. Paradoxically this pushed the EUR to session lows.

In Europe, the Stoxx 50 fell 0.7%, with the FTSE 100 lagging, dropping 1%. Energy and autos slump while utilities is the worst-performing sub-index in the European gauge on Wednesday, extending their selloff to a fourth session as investors fret over Russian gas supplies at the start of a three-day halt of the key Nord Stream pipeline. Slump is lead by Drax (-4.3%), National Grid (-4%), Italy’s Terna (-2.3%), Germany’s Uniper (-4%) and Fortum (-3%). Some renewables also take a hit, including Orsted (-2.4%) and Verbund (-1.4%). Citi says utilities had to put up more than EUR100b of additional collateral versus 2020 levels because of record levels of future power and gas prices. Here are the biggest European movers:

- ASML rises as much as 3.4%. It is among the “most attractive names” in the current uncertain macro environment, UBS says in a note upgrading the semiconductor-equipment company to buy from neutral.

- Stadler Rail shares climb as much as 6% after reporting mixed results, with 1H sales beating estimates and a strong order intake, offset by more cautious comments on margins and a negative currency impact, according to analysts.

- CFE shares surge as much as 23% after the Belgian construction and development company’s 1H results, with Degroof raising its estimates.

- Ackermans & van Haaren rises as much as 7.5% after KBC upgrades its rating on the industrial holding company to buy from hold following first-half results, which the broker describes as “resilient” in tough times.

- Lundbergforetagen shares rise as much as 5.5%, the most since May, after DNB reiterated its buy recommendation for the Swedish real estate investment firm, while trimming its PT to SEK485 from SEK530.

- Utilities are among the worst-performing sub-index in the European gauge on Wednesday, extending their selloff to a fourth session as investors fret over Russian gas supplies at the start of a three-day halt of the key Nord Stream pipeline.

- European energy stocks underperform for a second day after oil erased initial gains on Wednesday to head for a third monthly decline as rate hikes by major central banks and China’s Covid Zero strategy increase the likelihood of a global economic slowdown.

- Brunello Cucinelli shares fall as much as 7.2% after the Italian luxury fashion company reported 1H results; Deutsche Bank says the update is “largely as expected” with guidance appearing “relatively conservative.”

Europe’s weakness was sparked by the ongoing rout in oil, which headed for a third monthly drop – the longest losing run in more than two years – hampered by the likelihood of slower global growth, yet which as Goldman says is now the best asset to own having priced in a recession more than any other asset class. European natural gas advanced after a two-day slump, with traders weighing risks to Russian supplies against the continent’s drastic efforts to curb the energy crisis.

Earlier in the session, Asian equities climbed in a mixed day that saw tech shares advance but Japan’s bourses retreat as traders digested China’s weak economic data while technology stocks rebounded. BYD Co. plunged in Hong Kong after Warren Buffett’s Berkshire Hathaway Inc. trimmed its stake in the electric vehicle maker. The MSCI Asia Pacific Index erased an earlier loss to trade up as much as 0.6%. Chinese benchmarks underperformed the region after factory activity contracted on power shortages spurred by a historic drought. Stocks were also weak in Hong Kong as Warren Buffett’s sale of shares in BYD Co. fueled general risk-off sentiment, countered by advances in the city’s tech shares. Traders also weighed US job and consumer confidence numbers, which were seen backing the Federal Reserve’s rate-hike plans.

“The dented risk sentiment from tighter-for-longer central bank policies is likely to weigh on sentiment in the region,” Jun Rong Yeap, a market strategist at IG Asia Pte, wrote in a note. He added that further headwinds including Covid lockdowns may weigh on Chinese equities. Taiwanese stocks rose, even amid a potential escalation of cross-strait tensions, while South Korean shares also advanced on gains in tech names. Indian and Malaysian markets were closed for holidays.

Investors are also contending with mounting friction between Beijing and Taipei after Taiwanese soldiers fired shots to ward off civilian drones and evaluating the latest Chinese data, which indicated factory activity shrank for a second month. Power shortages, a property sector crisis and Covid outbreaks all took a toll.

In Japan, stock dropped amid concerns over the potential for Federal Reserve tightening and data that showed weak factory activity in China. The Topix fell 0.3% to 1,963.16 as of the market close Tokyo time, while the Nikkei 225 declined 0.4% to 28,091.53. Sony Group Corp. contributed the most to the Topix’s decline, decreasing 1.7%. Out of 2,169 stocks in the index, 683 rose and 1,381 fell, while 105 were unchanged. “US stocks, which plummeted on the Jackson Hole meeting last week, have fallen further and Japan stocks are matching that,” said Kiyoshi Ishigane, a chief fund manager at Mitsubishi UFJ Kokusai Asset Management.

In Australia, the S&P/ASX 200 index fell 0.2% to close at at 6,986.80, weighed by losses in mining and energy shares. Asia-Pacific energy-related stocks fell as oil headed for its third straight monthly decline, the longest losing run in more than two years, on prospects for slower global growth. In New Zealand, the S&P/NZX 50 index fell 0.4% to 11,601.10

In FX, the Bloomberg dollar spot index rose again, up 0.2%, as it reversed a loss as the greenback rebounded, with most Group-of-10 peers swinging to a loss in the European session. AUD and JPY are the strongest performers in G-10 FX, NOK and CHF underperform. The euro fell to a session low of $0.9974 as euro-area inflation accelerated to another all-time high of 9.1% from a year ago, exceeding the 9% median estimate in a Bloomberg survey. Norway’s krone plunged by 1% against the euro and even more versus the dollar after news that the nation’s central bank will ramp up its purchases of foreign currency to 3.5 billion kroner ($350 million) a day in September from 1.5 billion in August as it deposits energy revenue into the $1.2 trillion sovereign wealth fund. The pound neared the lowest since March 2020 against the greenback that was touched yesterday, yet options suggest a short-squeeze could be due. The Australian and New Zealand dollars held up well amid month-end demand after earlier gains in US stock futures following China PMI data. The yen was steady. Board member Junko Nakagawa said that the Bank of Japan’s forward guidance for interest rates isn’t necessarily directly linked with its Covid funding program.

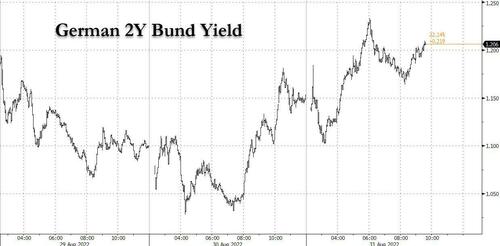

In rates, Treasuries are off session lows as US trading gets under way Wednesday, selloff paced by gilts with UK yields higher by 9bp-13bp. US 2Y barely exceeded Tuesday’s multiyear high. US yields are higher by 3bp-5bp, 2- year rose as much as 5.3bp to 3.275%, Treasury 10-year yield adds 4bps to around 3.14%. Curve spreads are little changed, inverted 5s30s around -5.7bp, near lowest level since mid June; month-end index rebalancing at 4pm New York time will extend the duration of Bloomberg Treasury index by an estimated 0.12 year. European bonds slide across the curve, led by gilts, after hotter-than-expected euro-area inflation data. Gilts 10-year yield is up 11 bps to 2.82%, while German 10-year yield rises 3.6bps to 1.55%. Peripheral spreads widen to Germany with 10y BTP/Bund adding 2.2bps to 233.4bps.

Bitcoin has managed to reclaim USD 20k after slipping to a USD 19.7k low, overall the crypto remains in fairly tight sub-1k parameters.

In commodities, crude futures extend declines. WTI drifts 2.6% lower to trade near $89, while Brent falls 3% to the $96 level. Base metals are mixed; LME tin falls 2.5% while LME nickel gains 1.4%. Spot gold falls roughly $10 to trade near $1,714/oz. Spot silver loses 1.5% near $18.

Looking to the day ahead now, data releases include the flash CPI reading for the Euro Area in August, as well as the country readings for France and Italy. On top of that, there’s the ADP’s new report of private payrolls for August and the MNI Chicago PMI for August. Finally, central bank speakers include the Fed’s Mester and Bostic.

Market Snapshot

- S&P 500 futures little changed at 3,986.25

- STOXX Europe 600 down 0.6% to 417.39

- MXAP up 0.2% to 158.39

- MXAPJ up 0.3% to 519.46

- Nikkei down 0.4% to 28,091.53

- Topix down 0.3% to 1,963.16

- Hang Seng Index little changed at 19,954.39

- Shanghai Composite down 0.8% to 3,202.14

- Sensex up 2.7% to 59,537.07

- Australia S&P/ASX 200 down 0.2% to 6,986.76

- Kospi up 0.9% to 2,472.05

- German 10Y yield little changed at 1.54%

- Euro down 0.1% to $1.0003

- Gold spot down 0.5% to $1,715.78

- U.S. Dollar Index up 0.14% to 108.92

Top Overnight News from Bloomberg

- Forget about a soft landing. Federal Reserve Chair Jerome Powell is now aiming for something much more painful for the economy to put an end to elevated inflation. The trouble is, even that may not be enough. It’s known to economists by the paradoxical name of a “growth recession.”

- France said the nation’s natural gas storage will be full in about two weeks, enabling the country to ride out the coming winter even as Russia turns the screw on deliveries of the fuel

- UK statisticians decided that a £400 ($466) government grant to help households with energy won’t lower headline inflation numbers, a move that will protect the returns of some bond holders but increase payments made by both the Treasury and consumers

- Sweden’s Riksbank hopes to be able to avoid a recession as it is prepared to do what is necessary to bring soaring inflation back to the central bank’s 2% target, deputy governor Anna Breman said

- The People’s Bank of China set stronger-than-expected yuan fixings for six sessions to Wednesday and people familiar with the matter said at least two local banks pushed back against the weakness when submitting data for the reference rate. Traders still expect it to weaken past the psychological 7 per dollar level, even if the moves slowed the decline

- China’s retail activity flatlined in August with e-commerce demand especially weak, according to satellite data, suggesting that consumer caution due to the ongoing Covid Zero policy and elevated unemployment remain major drags on the world’s second-largest economy

- Russia’s seaborne crude shipments to Asia have fallen by more than 500,000 barrels a day in the past three months, with flows to the region hitting their lowest levels since late March

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks were mostly negative following the losses across global counterparts owing to recent hawkish central bank rhetoric and with geopolitical concerns stoked after Taiwan fired warning shots at a Chinese drone. ASX 200 was subdued by weakness in commodity-related stocks with the energy sector the worst hit after the recent slump in oil prices, while a surprise contraction in Construction Work added to the headwinds and feeds into next week’s GDP release. Nikkei 225 declined but held above 28k after encouraging Industrial Production and Retail Sales. Hang Seng and Shanghai Comp were pressured amid a heavy slate of earnings releases and with US regulators said to have selected a number of US-listed Chinese companies for audit inspections including Alibaba, while participants also reacted to the Chinese PMI data in which the headline Manufacturing PMI topped estimates but remained in contraction territory.

Top Asian News

- Japanese PM Kishida said he has fully recovered from COVID-19 and returned to normal duty. Kishida added that they will begin administering Omicron variant targeted vaccines earlier than planned, while he announced to increase the daily upper limit of entrants to Japan to 50k on September 7th and will look into further loosening of border controls.

- South Korean vice-Finance Minister says they received “positive signs” during talks with FTSE Russell, FX environment has not emerged as a hurdle in discussions. Possibility is high for S. Korea’s inclusion to the FTSE’s WGBI watch-list in September

- Chinese NBS Manufacturing PMI (Aug) 49.4 vs. Exp. 49.2 (Prev. 49.0); Non-Manufacturing PMI (Aug) 52.6 vs Exp. 52.2 (Prev. 53.8) Chinese Composite PMI (Aug) 51.7 (Prev. 52.5)

- Japanese Industrial Production Prelim. (Jul P) 1.0% vs. Exp. -0.5% (Prev. 9.2%); Retail Sales YY (Jul) 2.4% vs. Exp. 1.9% (Prev. 1.5%)

- Australian Construction Work Done (Q2) -3.8% vs. Exp. 0.9% (Prev. -0.9%)

Initial upside in Europe faded as broader price action took another hawkish turn amid inflation data, Euro Stoxx 50 -1.0%. Stateside, futures are mixed around the unchanged mark, ES -0.2%, though are similarly well off best levels with data and Fed speak due.

Top European News

- UK’s ONS rules that energy bill rebate does not directly affect inflation statistics directly; “concluded that payments under the scheme should be classified as a current transfer paid by central government to the households sector.” i.e. the payment is being treated as a fiscal transfer as opposed to a price adjustment.

- UK government could reportedly fast-track nuclear power projects to help ease the energy crisis, according to The Telegraph.

- UK government is considering caps on rent to protect social housing tenants as part of a wider effort to ease the soaring costs of living, according to FT.

- Former UK Chancellor Sunak warned that Foreign Secretary Truss’s campaign promises could increase inflation and borrowing costs, according to FT.

- German Economy Minister Habeck said they would reject the idea of ‘capping’ energy prices; Finance Minister Lindner says the hurdle to an excess profit tax is high (re. energy); Chancellor Scholz says the early steps on energy means we will get through the winter period, will take measures to ensure energy prices “do not go through the roof”.

FX

- A session of gains for the DXY with upside spurred by haven bids, as the broader market sentiment deteriorated shortly after the European cash open.

- EUR/USD sits as one of the laggards with minimal immediate reaction seen in wake of hotter-than-expected August flash CPI for the EZ, although the upside for the pair may be capped by Nord Stream 1 jitters.

- The antipodeans are mixed as AUD leads the gains as the outperforming G10 peer on the back of better-than-expected Chinese official PMI metrics; Petro-currencies are softer as the slide in crude oil resumes.

- The JPY remains somewhat resilient in the face of the USD strength, likely amid the risk aversion across the market.

Fixed Income

- Core benchmarks experienced a fairly contained start to the session, though this proved to be shortlived and pronounced action occurred on inflation release.

- Bunds remain sub-147.50, though off worst, as initial French-CPI induced upside was reversed following hot Italian and subsequent EZ-wide Flash August HICP; market pricing for 75bp remains just above 50%.

- Gilts are the standout laggard as on the ONS treats the Energy Support as a fiscal transfer, thus Ofgem Energy adj. will be fully reflecting in CPI; Gilts sub-130 ticks in wake.

- USTs are directionally downbeat but comparably contained in terms of magnitudes, ADP and Fed’s Bostic/Mester due.

Commodities

- WTI and Brent futures resumed selling off in tandem with the broader risk-mood.

- Dutch TTF futures are on a firmer footing today following yesterday’s near-10% slump.

- Spot gold is pressured by the firmer Dollar and approaches USD 1,700/oz to the downside.

- 3M LME copper has been extending on gains with a boost from the above-forecast Chinese PMI metrics, but the contract remains under USD 8,000/t.

- OPEC+ JTC upgrades 2022 oil market surplus forecast by 100k BPD to 900k BPD, according to a report via Reuters; sees market surplus rising to 1.4mln BPD in November from 0.6mln BPD in October.

- OPEC+ JTC report says rising energy costs “may lead to a more significant reduction in consumptions towards year-end”, via Reuters.

- US Private Inventory Data (bbls): Crude +0.6mln (exp. -1.5mln), Cushing -0.6mln, Gasoline -3.4mln (exp. -1.2mln), Distillates -1.7mln (exp. -1.0mln).

- Oman crude OSP calculated at USD 97.00bbl for October vs. USD 103.21bbl in September, according to DME data.

Central Banks

- BoJ’s Nakagawa says the central bank decided to maintain easy policy bias in July, and hopes to discuss at the September meeting whether it should continue doing so based on data. Must remain vigilant to downward economic pressure from pandemic.

- BoJ is to conduct fixed-rate purchase operations for the cheapest-to-deliver 357th JGB notes for an extended period of time as of September 1st.

- ECB’s Rehn says the economic outlook has darkened, normalisation of monetary policy progressing consistently. Rates will increase in September, will be necessary to hike further at future gatherings.

- Riksbank’s Bremen says it is of the utmost importance to defend the inflation target as anchor for price setting and wage formation; adds inflation is too high. Inflation outcomes have been higher than expected recently, inflation risks are on the upside. Does not rule out a 50bps or 75bps hike at the 20th September meeting.

- Norges Bank Currency Purchases (Sep) NOK 3.5bln (prev. NOK 1.5bln)

US Event Calendar

- 07:00: Aug. MBA Mortgage Applications -3.7%, prior -1.2%

- 08:15: ADP resumes publication of jobs report with new methodology

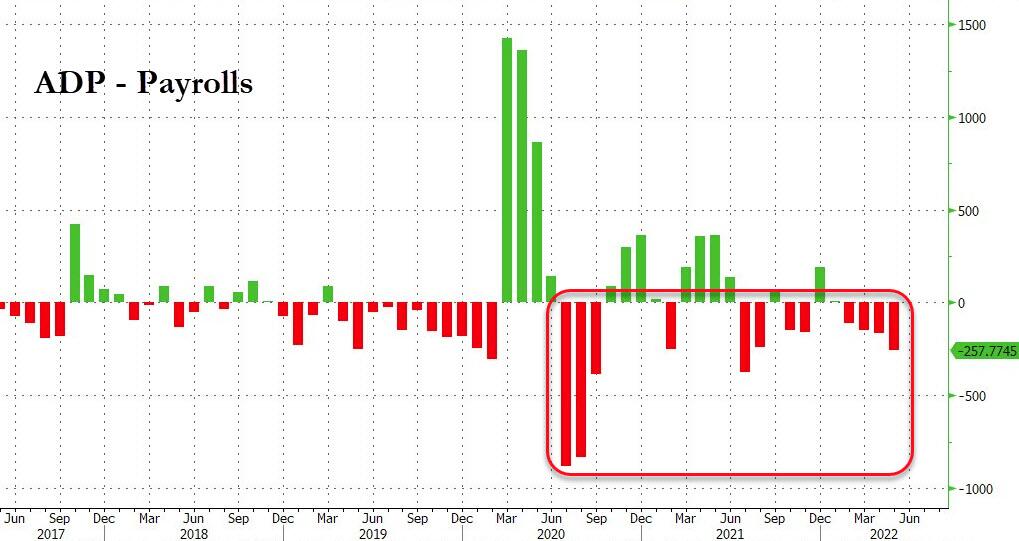

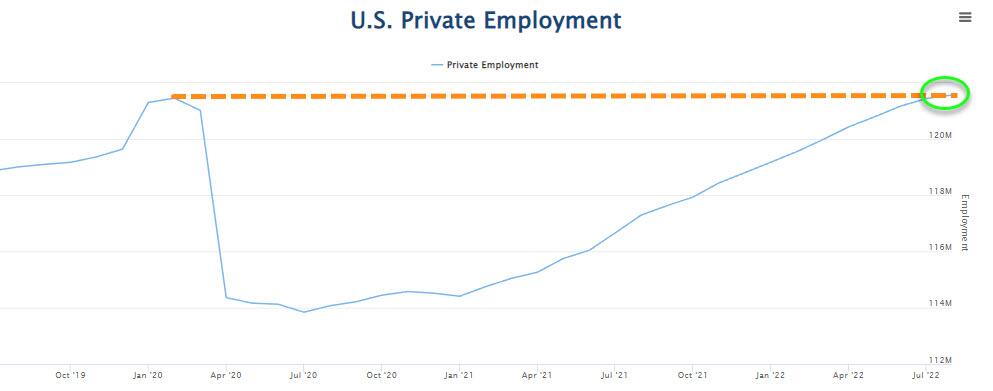

- 08:15: Aug. ADP Employment Change, est. 300,000

- 09:45: Aug. MNI Chicago PMI, est. 52.1, prior 52.1

Central Banks

- 08:00: Fed’s Mester Discusses Economic Outlook

- 18:00: Dallas Fed Holds Event to Introduce New President Lorie Logan

- 18:30: Fed’s Bostic speaks on role of fintech in financial inclusion

DB’s Henry Allen concludes the overnight wrap

Was back in the office yesterday after a two-week break but needed an extra day recovery before I started the EMR again as Monday was the twin’s 5th birthday. To say they were excited would be an understatement. More is to come as they have their birthday party and 30-40 kids coming round our house on Sunday. After another dry spell Sunday brings rain again apparently! We’re used to this adversity as the first day of our Cornwall holiday saw a dramatic storm and the first rain for 2-3 months. A few days of typically chilly, breezy, and slightly wet UK beach weather followed. In my second week off back home I played 5 rounds of golf so that was the proper holiday. My handicap is now the lowest it’s ever been so there’s life in the multiple operated on old dog yet! Back to the real world now though and not only has the world got darker since I’ve been off but so have work hours. I always take these two weeks off every year and it always marks a depressing reality that winter is coming. Before I go away it’s just about light when I get up. However, by the time I get back from holiday it’s firmly dark waking up for the EMR. It’ll be a good 7-8 months before I see light again on the early EMR shift.

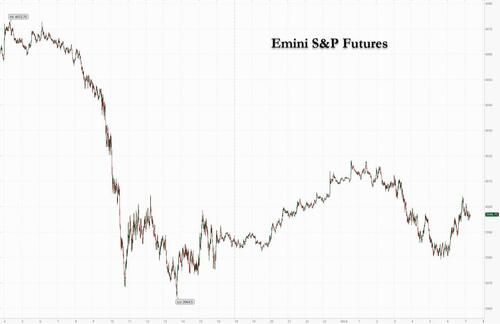

The dark mirrors the mood in markets which has seen a rapid deterioration since Jackson Hole, with the S&P 500 shedding a further -1.10% yesterday to move back beneath the 4000 mark. The index is now -7.85% below its mid-August intra-day highs and -5.08% since last Thursday’s pre Jackson Hole close. We’re still +8.71% above the June lows though. Ironically, strong US data releases prompted the latest sell-off, as they showed that consumer confidence was more resilient and the labour market was tighter than expected. But in today’s high-inflation environment, good economic news is enabling the Fed to be even more aggressive on rate hikes, and the market developments yesterday were very much in keeping with that theme. We actually reached an important milestone yesterday too, as the futures-implied Fed funds rate for December ticked up +3.0bps to 3.73%, which surpasses the previous high of 3.72% seen back in June after the bumper CPI report for May came in. So for 2022 at least, markets are pricing in their most aggressive pace of hikes to date which makes a lot more sense than where we were a few weeks ago.

In terms of the specifics of those data releases, an important one was the JOLTS data, which showed that job openings unexpectedly rose to 11.239m in July (vs. 10.375m expected). That marked a break in the trend of 3 consecutive declines, and shows that the Fed still have significant work to do if they want to bring labour demand and labour supply back into balance. Another indicator we’ve been tracking is the number of job openings per unemployed worker. That also bounced back up to 1.98 in July, which is just shy of its record high of 1.99 in March. So even with 225bps of Fed hikes by the July meeting, that measure of labour market tightness has barely budged. Then we got the Conference Board’s consumer confidence data for August, which came in at a 3-month high of 103.2 (vs. 98.0 expected), with rises for both the expectations and the present situation indicators.

This positive news on the economy gave investors growing confidence that the Fed are set to keep hiking into 2023, and sent yields on 2yr Treasuries up +1.8bps to 3.44%. That’s their highest closing level since the GFC, and on an intraday basis they even hit 3.49% at one point. Longer-dated yields also increased, albeit to a lesser extent, with those on 10yr Treasuries flat. FOMC Vice Chair and New York Fed President Williams emphasised the point, saying that rates will need to stay in restrictive territory “for some time”, so the days of pricing rate cuts early next year are over for now. The fed funds futures curve currently has policy rates peaking around 3.90% in the second quarter of next year, with the first full -25bp cut from those highs not until November of next year, as of last night’s close.

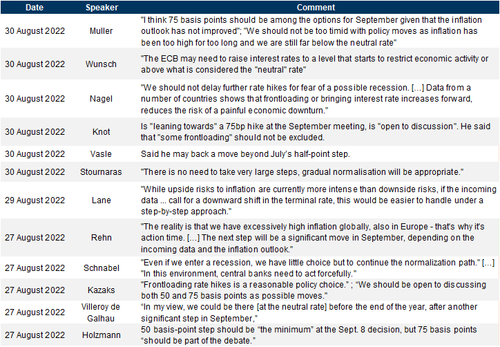

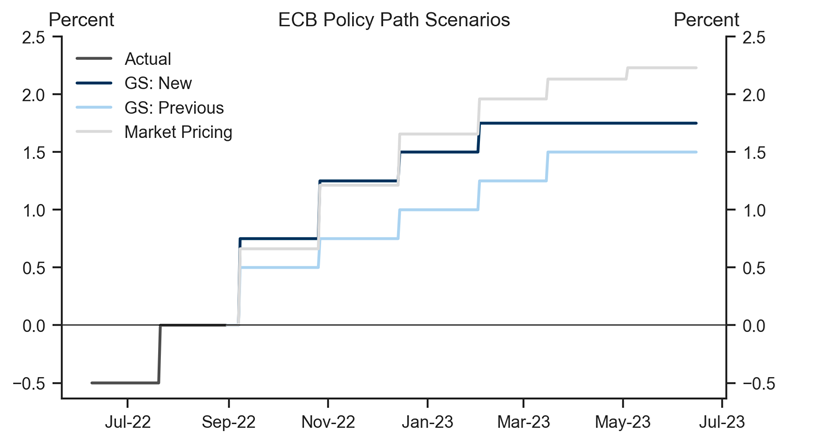

The trend towards increasing hawkishness was echoed at the ECB as well yesterday, where the prospect of a 75bps move next week is being increasingly discussed by officials. In the last 24 hours alone, we heard from Estonia’s Muller, who said that “75 basis points should be among the options for September given that the inflation outlook has not improved”. Furthermore, Slovenia’s Vasle said that he favoured a hike “that could exceed 50 basis points”. Germany’s Nagel echoed the ECB chatter from last week, that they should not delay rate hikes just for fear of recession, instead arguing the call for earlier rate hikes to prevent later pain. Further, Pierre Wunsch of Belgium argued the current bout of inflation had structural roots, which called for a quick move to restrictive policy. While neither Nagel nor Wunsch explicitly endorsed a 75bp hike, their comments don’t push back on it.

So overall it’s clear that officials are contemplating a larger hike, and overnight index swaps continue to price a 75bps move as more likely than 50bps for the September decision, closing yesterday pricing +65.8bps worth of hiking for next week’s meeting. It’s set to be a big one!

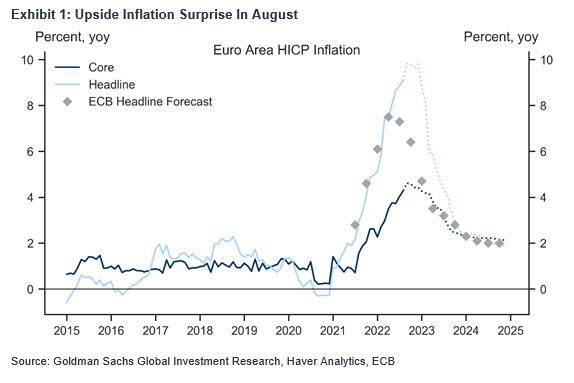

We should get some additional clues on how fast the ECB might hike with the release of the flash CPI data for the Euro Area this morning. But there weren’t any big surprises in either direction from the country readings ahead of that yesterday. In Germany, the EU-harmonised reading rose to a fresh high of +8.8%, but that was as expected, and it was a similar story in Spain where the harmonised reading fell back to +10.3% as expected.

A complicating factor for the ECB relative to the Fed is the stagflationary impulse coming from the ongoing energy shock, where prices have soared to new records in the last week. However, the last 24 hours brought some further declines that built on Monday’s moves lower, with natural gas futures coming down -7.21% to €253 per megawatt-hour. German power prices for next year came down by an even bigger -21.05%, on top of the -22.84% decline on Monday, although even that -39.09% total decline hasn’t erased the previous week’s gains. One other thing to keep an eye out for from today will be the start of maintenance on the Nord Stream pipeline, which is set to last for 3 days if you take the statement at face value. But as with the shutdown in July, there are concerns that gas flows won’t resume again afterwards, so that’s definitely one to watch.

Oil futures took a big slide, with brent futures down -4.79% and WTI down -5.54%. The proximate cause appeared to be unsubstantiated rumours that the US and Iran had reached a deal to reinstate the nuclear deal. However, a US State Department spokesperson later denied the rumours, and we’ve already heard from OPEC+ that any supply increase from Iran would be offset by supply cuts among the cartel. So if oil prices stay around these levels, perhaps the market is pricing in more global demand slowdown than unmitigated supply expansion.

For sovereign bond yields, the more hawkish noises from the ECB outweighed the effect of falling energy prices yesterday, with the 2yr German yield up +6.1bps. Similarly to the US, the increases in yields were concentrated at the more policy-sensitive front end of the curve, with longer-dated yields seeing smaller moves, including those on 10yr bunds (+0.8bps), OATs (+0.7bps) and BTPs (+1.7bps).

On the equity side, the risk-off tone took the major indices lower on both sides of the Atlantic, with the S&P 500 (-1.10%) experiencing a 3rd consecutive decline. The more cyclical sectors led the moves lower, and the more interest-sensitive megacap tech stocks continued to struggle, with the FANG+ index down a further -2.04%. In Europe, the STOXX 600 was down -0.67% yesterday, although that decline was somewhat exaggerated by the fact that London equities were returning after Monday’s declines. Indeed, the DAX actually ended the day up +0.53%, although that was the exception as the CAC 40 (-0.19%) and the FTSE MIB (-0.08%) both posted modest declines.

The more negative mood of the last few days has continued into today’s Asian session, with the Nikkei (-0.40%), Hang Seng (-0.39%) and the Shanghai composite (-1.18%) all losing ground this morning despite earlier better-than-expected economic data from China and Japan. Starting with the former, both manufacturing (49.4 vs 49.2 expected) and non-manufacturing PMI (52.6 vs 52.3 expected) were ahead of estimates but the manufacturing gauge stayed in contraction territory. In Japan, we got strong beats for industrial production (+1.0% vs -0.5% expected, MoM) and retail sales (+0.8% vs +0.3% expected, MoM). US Treasury yields are up across the curve, with the 2y yield (+2.1bps) gains ahead of 10y ones (+0.9bps).

To the day ahead now, and data releases include the flash CPI reading for the Euro Area in August, as well as the country readings for France and Italy. On top of that, there’s German unemployment for August, Canada’s GDP for Q2, and in the US there’s the ADP’s report of private payrolls for August and the MNI Chicago PMI for August. Finally, central bank speakers include the Fed’s Mester and Bostic.

AND NOW NEWSQUAWK

Initial upside fades as hawkish debt action resumed post-EZ CPI/UK ONS – Newsquawk US Market Open

WEDNESDAY, AUG 31, 2022 – 06:40 AM

- Initial upside faded as broader price action took another hawkish turn amid inflation data, Euro Stoxx 50 -1.0%

- Stateside, futures are mixed around the unchanged mark, ES -0.1%, though are similarly well off best levels with data and Fed speak due.

- DXY bid but shy of YTD peak, EUR lags despite HICP with peers generally under modest pressure ex-AUD

- Core benchmarks experienced a fairly contained start to the session, though this proved to be shortlived and pronounced action occurred on inflation releases; Gilts lag post-ONS

- WTI and Brent futures resumed selling off in tandem with the broader risk-mood, Dutch TTF bid after Tuesday’s pressure

- OPEC+ JTC upgrades 2022 oil market surplus forecast by 100k BPD to 900k BPD, via Reuters citing a report

- Looking ahead, highlights include Canadian GDP, US ADP & Chicago PMI, Speeches from Fed’s Mester & Bostic.

As of 11:15BST/06:15ET

For the full report and more content like this check out Newsquawk.

Try a 14 day trial with Newsquawk and hear breaking trading news as it happens.

LOOKING AHEAD

- Canadian GDP, US ADP & Chicago PMI, Speeches from Fed’s Mester & Bostic.

- Click here for the Week Ahead preview.

GEOPOLITICS

RUSSIA-UKRAINE

- IAEA convoy has set off from Kyiv towards the Zaporizhzhia nuclear power plant, according to a witness cited by Reuters; subsequent updates indicate the mission should arrive on Thursday.

- Kremlin spokesperson says there are “signals” about a resumption of New Start Treaty discussions with the US but there has not been any significant progress.

- Nord Stream 1 physical flows at 119.9k kWh/H (prev. 115k kWh/H) between 00:00-10:00BST. Note, flows have been at 0 throughout the morning, given the commencement of three days of maintenance.

- Russia remains committed to its gas supply commitments but cannot meet them due to sanctions, according to Ifax citing a Kremlin spokesperson.

- German Network Regulator (on Nord Stream 1 maintenance) tells Reuters that the body cannot “technically understand” the new maintenance by Russia.

CHINA -TAIWAN

- Taiwan’s Defence Ministry said China’s military continues high-intensity patrols near Taiwan, while it added that Taiwan will exercise the right to self-defence and counter-attack if PLA forces enter air and sea territory within 12 nautical miles of Taiwan or if any Chinese drones pose a threat to security and do not leave after warnings, according to Reuters.

EUROPEAN TRADE

CENTRAL BANKS

- BoJ’s Nakagawa says the central bank decided to maintain easy policy bias in July, and hopes to discuss at the September meeting whether it should continue doing so based on data. Must remain vigilant to downward economic pressure from pandemic.

- BoJ is to conduct fixed-rate purchase operations for the cheapest-to-deliver 357th JGB notes for an extended period of time as of September 1st.

- ECB’s Rehn says the economic outlook has darkened, normalisation of monetary policy progressing consistently. Rates will increase in September, will be necessary to hike further at future gatherings.

- Riksbank’s Bremen says it is of the utmost importance to defend the inflation target as anchor for price setting and wage formation; adds inflation is too high. Inflation outcomes have been higher than expected recently, inflation risks are on the upside. Does not rule out a 50bps or 75bps hike at the 20th September meeting.

- Norges Bank Currency Purchases (Sep) NOK 3.5bln (prev. NOK 1.5bln)

EQUITIES

- Initial upside faded as broader price action took another hawkish turn amid inflation data, Euro Stoxx 50 -1.0%.

- Stateside, futures are mixed around the unchanged mark, ES -0.2%, though are similarly well off best levels with data and Fed speak due.

- Click here for more detail.

FX

- A session of gains for the DXY with upside spurred by haven bids, as the broader market sentiment deteriorated shortly after the European cash open.

- EUR/USD sits as one of the laggards with minimal immediate reaction seen in wake of hotter-than-expected August flash CPI for the EZ, although the upside for the pair may be capped by Nord Stream 1 jitters.

- The antipodeans are mixed as AUD leads the gains as the outperforming G10 peer on the back of better-than-expected Chinese official PMI metrics; Petro-currencies are softer as the slide in crude oil resumes.

- The JPY remains somewhat resilient in the face of the USD strength, likely amid the risk aversion across the market.

- Click herefor more detail.

Notable FX Expiries, NY Cut:

- Click here for more detail.

FIXED INCOME

- Core benchmarks experienced a fairly contained start to the session, though this proved to be shortlived and pronounced action occurred on inflation release.

- Bunds remain sub-147.50, though off worst, as initial French-CPI induced upside was reversed following hot Italian and subsequent EZ-wide Flash August HICP; market pricing for 75bp remains just above 50%.

- Gilts are the standout laggard as on the ONS treats the Energy Support as a fiscal transfer, thus Ofgem Energy adj. will be fully reflecting in CPI; Gilts sub-130 ticks in wake.

- USTs are directionally downbeat but comparably contained in terms of magnitudes, ADP and Fed’s Bostic/Mester due.

- Click here for more detail.

COMMODITIES

- WTI and Brent futures resumed selling off in tandem with the broader risk-mood.

- Dutch TTF futures are on a firmer footing today following yesterday’s near-10% slump.

- Spot gold is pressured by the firmer Dollar and approaches USD 1,700/oz to the downside.

- 3M LME copper has been extending on gains with a boost from the above-forecast Chinese PMI metrics, but the contract remains under USD 8,000/t.

- OPEC+ JTC upgrades 2022 oil market surplus forecast by 100k BPD to 900k BPD, according to a report via Reuters; sees market surplus rising to 1.4mln BPD in November from 0.6mln BPD in October.

- OPEC+ JTC report says rising energy costs “may lead to a more significant reduction in consumptions towards year-end”, via Reuters.

- US Private Inventory Data (bbls): Crude +0.6mln (exp. -1.5mln), Cushing -0.6mln, Gasoline -3.4mln (exp. -1.2mln), Distillates -1.7mln (exp. -1.0mln).

- Oman crude OSP calculated at USD 97.00bbl for October vs. USD 103.21bbl in September, according to DME data.

- Click here for more detail.

NOTABLE HEADLINES