GOLD; $1698.40 DOWN $26.70

SILVER: $17.86 DOWN 58 CENTS

ACCESS MARKET:

GOLD $1797.50

SILVER: $17.81

Bitcoin morning price: $20,015 DOWN 656

Bitcoin: afternoon price: $19,890 DOWN 781

Platinum price closing DOWN $34.80 AT $832.45

Palladium price; closing DOWN $135.05 at $2007.45

END

DONATE

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,712.800000000 USD

INTENT DATE: 08/31/2022 DELIVERY DATE: 09/02/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 169

132 C SG AMERICAS 107

365 H ED&F MAN CAPITA 1

435 H SCOTIA CAPITAL 112

657 C MORGAN STANLEY 26

661 C JP MORGAN 478

690 C ABN AMRO 97

709 C BARCLAYS 691

737 C ADVANTAGE 23 28

800 C MAREX SPEC 4 14

905 C ADM 24

TOTAL: 887 887

MONTH TO DATE: 1,291

JPMorgan stopped: 478/887

_____________________________________________________________________________________

GOLD: NUMBER OF NOTICES FILED FOR AUGUST CONTRACT:

887 NOTICES FOR 88700 OZ //2.7589 TONNES

total notices so far: 1291 contracts for 129,100 oz (4.0175 tonnes)

SILVER NOTICES: 357 NOTICES FILED FOR 1,785,000 OZ/

total number of notices filed so far this month 5601 : for 28,005,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $26.70

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//

INVENTORY RESTS AT 973.37 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $.58

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 465.573 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1742 CONTRACTS TO 136,972. AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE LOSS IN OI WAS ACCOMPLISHED WITH OUR $0.36 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.36) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A GOOD GAIN OF 693 CONTRACTS ON OUR TWO EXCHANGES,; WE HAD MINOR SPECULATOR LIQUIDATION.

WE MUST HAVE HAD:

I) SOME//MINOR SPECULATOR SHORT LIQUIDATIONS ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 475,000 OZ QUEUE JUMP / // V) HUGE SIZED COMEX OI LOSS/(//MINOR SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: -7

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTACTS for 1 days, total 2425 contracts: 12.140 million oz OR 12.140 MILLION OZ PER DAY. (2425 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 12.140 MILLION OZ

.

LAST 16 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 12.140 MILLION OZ///

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1742 WITH OUR $0.36 LOSS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC SIZED EFP ISSUANCE CONTRACTS: 2425 CONTRACTS ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /SOME BANKER ADDITIONS A// MINOR SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 475,000 OZ QUEUE JUMP // .. WE HAD A STRONG SIZED GAIN OF 686 OI CONTRACTS ON THE TWO EXCHANGES FOR 3.430 MILLION OZ AS..THE SPECS STILL BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 357 NOTICE(S) FILED TODAY FOR 1,785,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 242 CONTRACTS TO 459,407 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY:–157 CONTRACTS.

.

THE SMALL SIZED INCREASE IN COMEX OI CAME DESPITE OUR STRONG FALL IN PRICE OF $10.20//COMEX GOLD TRADING/WEDNESDAY / WE MUST HAVE HAD MINOR SPECULATOR SHORT SHORT COVERINGS ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND SOME/M INOR SPECULATOR SHORT COVERINGS//CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S GIGANTIC JUMP OF 43,900 OZ //NEW STANDING 9.7667 TONNES

YET ALL OF..THIS HAPPENED DESPITE OUR FALL IN PRICE OF $10.20 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 3142 OI CONTRACTS 9.773 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 2900 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 459,407

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3142 CONTRACTS WITH 242 CONTRACTS INCREASED AT THE COMEX AND 2900 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3142 CONTRACTS OR 9.773 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2900) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (242): TOTAL GAIN IN THE TWO EXCHANGES 3142 CONTRACTS. WE NO DOUBT HAD 1) MINOR SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 99.272 TONNES FOLLOWED BY TODAY’S QUEUE. JUMP OF 43,900 oz. 3) ZERO LONG LIQUIDATION//// //.,4) SMALL SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

2900 CONTRACTS OR 290,000 OZ OR 9.020 TONNES 1 TRADING DAY(S) AND THUS AVERAGING: 2900 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES: 9.020 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 9.020/3550 x 100% TONNES 0.25% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 9.02 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A HUGE SIZED 1742 CONTRACT OI TO 136,972 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 2425 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 2425 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2425 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1742 CONTRACTS AND ADD TO THE 2425 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 686 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 3.430 MILLION OZ

OCCURRED WITH OUR LOSS IN PRICE OF $0.36

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 17.16 PTS OR 0.54% //Hang Sang CLOSED DOWN 357.08 OR 1.79% /The Nikkei closed DOWN 430.06 OR % 1.53. //Australia’s all ordinaires CLOSED DOWN 2.02% /Chinese yuan (ONSHORE) closed UP AT 6.8907//OFFSHORE CHINESE YUAN DOWN 6.8980// /Oil DOWN TO 88.04 dollars per barrel for WTI and BRENT AT 94.30 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 242 CONTRACTS TO 459,407 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR FALL OF $10.20 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2900 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF AUGUST.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2990 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :2900 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2900 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED SIZED TOTAL OF 3299 CONTRACTS IN THAT 2900 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 242 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG FALL IN PRICE OF GOLD $ 10.20. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (9.7667),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 9.7667 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $10.20) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED TOTAL GAIN ON OUR TWO EXCHANGES // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS////// WE HAVE REGISTERED A STRONG SIZED GAIN OF 10.261 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR AUGUST (9.7667 TONNES)…

WE HAD -157 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3299 CONTRACTS OR 32,900 OZ OR 9.773 TONNES

Estimated gold volume 197,122/// poor/

final gold volumes/yesterday 190,092/ poor

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 1

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 189,471.742 oz Brinks JPMorgan |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 4,469.651 oz |

| No of oz served (contracts) today | 887 notice(s) 88700 OZ 2.7549 TONNES |

| No of oz to be served (notices) | 1849 contracts 184900 oz 5.75 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1291 notices 129,100 OZ 4.0155 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

2 customer withdrawals:

i) Out of Brinks 64,623.510 (2010 kilobars)

ii) Out of JPMorgan: 124,848.232 oz

total: 189,471.742 oz

total in tonnes: 5.893 tonnes

Adjustments:0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of SEPT we have an oi of 2736 contracts having GAINED 35 contracts .

We had 404 notices filed yesterday so we gained a whopping 439 contracts or an additional 43900 oz

will stand for gold in this very non active delivery month of September.

October GAINED 264 contracts UP to 39,159

December lost 429 contracts down to 377,464.

We had 887 notice(s) filed today for 88,700 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 887 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 478 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (887) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 2756 CONTRACTS ) minus the number of notices served upon today 887 x 100 oz per contract equals 314000 OZ OR 9.7667 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (887) x 100 oz+ (2736) OI for the front month minus the number of notices served upon today (887} x 100 oz} which equals 314,000 oz standing OR 9.7667 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 9.7667 TONNES (A GREAT STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

VERY UNUSUAL THAT ON DAY 2 WE HAD A HUGE QUEUE JUMP. (NORMALLY AN EFP JUMP//REDUCTION IN GOLD STANDING ON DAY 2)

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR AUGUST WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,343,125.744 oz 72.88 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 27,771,187.296 OZ

TOTAL REGISTERED GOLD: 13,684,725.139 OZ (425.65 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 14,086,402.157 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 11,450,600. OZ (REG GOLD- PLEDGED GOLD) 356.16 tonnes//rapidly declining

END

SILVER/COMEX/SEPT 1

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1155315.078 oz CNT Brinks CNT Delaware Int. Delaware HSBC JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 357CONTRACT(S) 1,785,000 OZ) |

| No of oz to be served (notices) | 372 contracts (1,860,000 oz) |

| Total monthly oz silver served (contracts) | 5601 contracts 28,005,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

total deposit: nil oz

JPMorgan has a total silver weight: 169.301 million oz/326.647million =51.84% of comex

Comex withdrawals:6

i) Out of CNT: 126,060.710 oz

ii) Out of Brinks: 100,037.480 oz

iii)Out of Delaware 3943.600 oz

iv)Int. Delaware 170,066.680 oz

v) Out of HSBC 158,626.680 oz

vi)JPMorgan 596,580.100 oz

total: 1,155,315.072 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 50.552 MILLION OZ

TOTAL REG + ELIG. 326.647 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR AUGUST

silver open interest data:

FRONT MONTH OF SEPT OI: 729 CONTRACTS HAVING LOST 5147 CONTRACTS. WE HAD

5244 CONTRACTS SERVED UPON YESTERDAY SO WE GAINED 97 CONTRACTS OR AN ADDITIONAL

485,000 OZ WILL STAND FOR METAL IN THIS VERY ACTIVE MONTH OF SEPT.

UNUSUAL THAT IN BOTH GOLD AND SILVER WE WITNESSED A HUGE QUEUE JUMP ON DAY 2 OF THE DELIVERY

CYCLE.

OCTOBER GAINED 3 CONTRACTS TO STAND AT 703

CONTRACTS.

NOVEMBER SAW ITS FIRST INITIAL NOTICE SERVED: STANDING 1

DECEMBER SAW A STRONG 3013 NOTICES INCREASE UP TO 124,912.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 357 for 1,785,000 oz

Comex volumes:63,749// est. volume today// fair

Comex volume: confirmed yesterday: 65,687 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 5601 x 5,000 oz = 28,005,000 oz

to which we add the difference between the open interest for the front month of SEPT(729) and the number of notices served upon today 357 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST./2022 contract month: 5,601 (notices served so far) x 5000 oz + OI for front month of SEPT (729) – number of notices served upon today (357) x 5000 oz of silver standing for the SEPT contract month equates 29,865,000 oz. .

we have inventory of 50 million oz of registered silver at the comex so Sept delivery of 29.855 represents 59.6% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:38,731// est. volume today// poor

Comex volume: confirmed yesterday: 96,524 contracts ( good)

END

GLD AND SLV INVENTORY LEVELS

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 18/WITH GOLD DOWN $5.25: GIGANTIC CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.78 TONNES FROM THE GLD////INVENTORY RESTS AT 985.83 TONNES

AUGUST 17/WITH GOLD DOWN $12.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 992.20 TONNES

AUGUST 16/WITH GOLD DOWN $7.85: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 993.94 TONNES

AUGUST 15/WITH GOLD DOWN $16.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 995.97 TONNES

AUGUST 12/WITH GOLD UP $7.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 995.97 TONNES

AUGUST 11/WITH GOLD DOWN $5.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 997.42 TONNES

AUGUST 10//WITH GOLD UP $2.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES

AUGUST 9/WITH GOLD UP $6.70: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 996.16 TONNES.

AUGUST 8/WITH GOLD UP $13.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FORM THE GLD//INVENTORY RESTS AT 999.16 TONNES

AUGUST 5/WITH GOLD DOWN $14.25: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .33 TONNES FROM THE GLD////INVENTORY RESTS AT 1000.32 TONNES

AUGUST 4 WITH GOLD UP $29.00 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD///INVENTORY REST AT 1000.65 TONNES

AUGUST 2/WITH GOLD UP $3.70; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD//INVENTORY RESTS AT 1002.97 TONNES//

AUGUST 1/WITH GOLD UP $5.75: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1005.87 TONNES

GLD INVENTORY: 973.37 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

AUGUST 18/WITH SILVER DOWN 27 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 369,000 OZ INTO THE SLV////INVENTORY RESTS AT 485.482 MILLION OZ//

AUGUST 17/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.106 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.113 MILLION OZ//

AUGUST 16/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 486.219 MILLION OZ/

AUGUST 15/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.152 MILLION OZ INTO THE SLV/ INVENTORY RESTS AT 486.219 MILLION OZ//

AUGUST 12/WITH SILVER UP 34 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 11/WITH SILVER DOWN 46 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920, 000 OZ FORM THE SLV.//INVENTORY RESTS AT 485.067 MILLION OZ//

AUGUST 10/WITH SILVER UP 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 9/WITH SILVER DOWN 25 CENTS TODAY: TWO CHANGES IN SILVER INVENTORY AT THE SLV: FIRST: A DEPOSIT OF 461,000 OZ INTO THE SLV AND THEN A WITHDRAWAL OF 1.014 MILLION OZ..//INVENTORY RESTS AT 485.159 MILLION OZ//

AUGUST 8/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 5/WITH SILVER DOWN 28 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 922,000 OZ FROM THE SLV//INVENTORY RESTS AT 485.712 MILLION OZ//

AUGUST 4 WITH SILVER UP 21 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 527,000 OZ FROM THE SLV////INVENTORY RESTS AT 486.634 MILLION OZ

AUGUST 2/WITH SILVER DOWN 21 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.504 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.161 MILLION OZ//

AUGUST 1/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE GLD: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 483.657 MILLION OZ//

CLOSING INVENTORY 465.573 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Fed Paper Admits Central Bank Can’t Control Inflation; Finger-Points At Federal Government

THURSDAY, SEP 01, 2022 – 07:20 AM

Authored by Michael Maharrey via SchiffGold.com,

It appears somebody at the Federal Reserve has figured out that the central bank can’t tame inflation, so it’s setting up a scapegoat – Uncle Sam…

A paper co-authored by Leonardo Melosi of the Federal Reserve Bank of Chicago and John Hopkins University economist Francesco Bianchi and published by the Kansas City Federal Reserve argues that central bank monetary policy alone can’t control inflation.

The paper’s abstract asserts, “This increase in inflation could not have been averted by simply tightening monetary policy.”

In a nutshell, Melosi and Bianchi argue that the Fed can’t control inflation alone.

US government fiscal policy contributes to inflationary pressure and makes it impossible for the Fed to do its job.

Trend inflation is fully controlled by the monetary authority only when public debt can be successfully stabilized by credible future fiscal plans. When the fiscal authority is not perceived as fully responsible for covering the existing fiscal imbalances, the private sector expects that inflation will rise to ensure sustainability of national debt. As a result, a large fiscal imbalance combined with a weakening fiscal credibility may lead trend inflation to drift away from the long-run target chosen by the monetary authority.”

There are a couple of startling admissions in this single paragraph.

First, the authors acknowledge that the federal government uses inflation as a tool to handle its debt. In other words, it acknowledges that we’re all paying an inflation tax.

Peter Schiff talked about this inflation tax in an interview on Rob Schmitt Tonight.

Inflation is a tax. It’s the way government finances deficit spending. Government spends money. It doesn’t collect enough taxes, so it has to run deficits. The Federal Reserve monetizes those defiticts – prints money. They call it quantitative easing, but that’s inflation. Government is getting bigger and bigger, and families across America are going to have to bear that burden through higher prices.”

Second, the paper concedes that merely tinkering with interest rates won’t slay inflation if the government continues to spend far beyond its means.

And make no mistake, the US government is spending far beyond its means. Although the budget deficit is shrinking as emergency pandemic spending programs wind down, the Biden administration continues to spend about half-a-trillion dollars every single month, piling onto the ever-ballooning deficit.

This paper admits what I’ve been saying for months. Government spending is a big problem for the Federal Reserve. Powell and Company continue to insist they will stay in this inflation fight until the end. But Uncle Sam depends on the Fed buying Treasury bonds in order to facilitate its borrowing addiction. As the central bank buys bonds, it creates artificial demand and holds interest rates down. The government needs low interest rates when it’s borrowing trillions of dollars. Without the Fed’s big fat thumb on the bond market, Treasury prices will continue to sink as supply outstrips demand, and interest rates will rise.

Melosi and Bianchi also tacitly admit that the Fed isn’t going to win this inflation fight and warns we could be heading toward stagflation.

When fiscal imbalances are large and fiscal credibility wanes, it may become increasingly harder for the monetary authority to stabilize inflation around its desired target. If the monetary authority increases rates in response to high inflation, the economy enters a recession, which increases the debt-to-GDP ratio. If the monetary tightening is not supported by the expectation of appropriate fiscal adjustments, the deterioration of fiscal imbalances leads to even higher inflationary pressure. As a result, a vicious circle of rising nominal interest rates, rising inflation, economic stagnation, and increasing debt would arise.”

This is exactly what is happening.

Melosi and Bianchi call this a “pathological situation.”

Monetary tightening would actually spur higher inflation and would spark a pernicious fiscal stagflation, with the inflation rate drifting away from the monetary authority’s target and with GDP growth slowing down considerably.”

Well hello there, Fed! Welcome to reality.

The Federal Reserve has raised rates to 2.5%. Despite mainstream assertions to the contrary, it appears the economy has already dipped into a recession. Private sector economic activity has dropped to the lowest levels since early in the COVID lockdowns, the housing market is tanking, and the economy has charted two straight months of negative GDP growth.

During his Jackson Hole speech, Jerome Powell said the Fed will “use our tools forcefully” to get inflation under control and even conceded that it will cause some economic pain. But the numbers undercut Powell’s confident assertions. The Fed would have to raise rates to a level that would obliterate this bubble economy in order to cool inflation.

I think the central bankers know this. This paper, co-authored by a Fed official, makes that pretty clear. I think the central bankers are setting the stage to finger point and pass the buck when this whole inflation-fighting scheme blows up in their faces.

The paper states, that the central bank can control inflation “only when public debt can be successfully stabilized by credible future fiscal plans.”

Do you think that is going to happen?

I don’t either.

In fact, the only workable plan is for the Federal Reserve to monetize more debt by buying more Treasuries with more money created out of thin air. This is one reason I’ve been saying for months that the Fed won’t win this inflation fight.

In one sense, I think the Fed is setting the stage for its own failure. It’s already making excuses. And it’s a little pathetic. The central bank put quantitative easing on steroids during the pandemic, injecting nearly $5 trillion into the economy. That is the very definition of inflation. If you want to know who to blame for this inflation mess, the Fed stands at the front of the line.

That said, this paper isn’t completely disingenuous. As I’ve already explained, the federal government plays a role in the inflation game as well. As the saying goes, it takes two to tango. Federal government spending is out of control, and the spending spree necessitates inflation. (It’s not just Biden’s fault — the Trump administration was running massive deficits prior to the pandemic.)

So, even if Melosi and Bianchi are trying to point the finger in another direction, they aren’t wrong when they write, “[Stagflation] is caused by the progressive deterioration of the fiscal authority’s credibility to stabilize its large debt and the realization that the reputation of the monetary authority is incompatible with the expected behavior of the fiscal authority.”

In plain English, the central bank can’t stop inflation when the federal government needs inflation to survive.

This paper won’t get much attention. In fact, it comes with a disclaimer — “The views in this paper are solely those of the authors and should not be interpreted as reflecting the views of the Federal Reserve Bank of Chicago or any person associated with the Federal Reserve System.”

Regardless, they’ve swerved into the truth and we’d do well to pay attention.

end

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

LAWRIE WILLIAMS: Dollar strength vis-a-vis gold not replicated in other key currencies

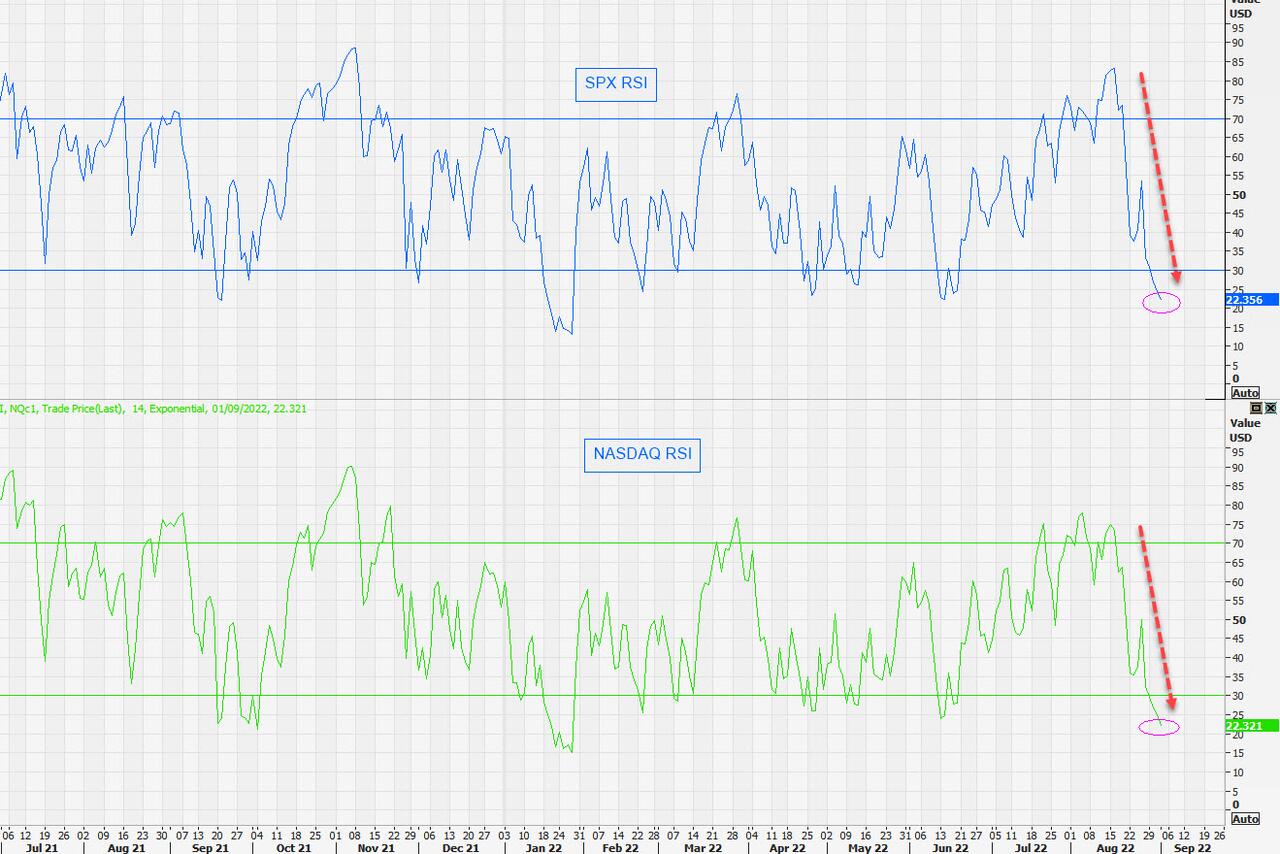

We are all used to assessing movements in the price of gold in U.S. dollar terms, and by this measure gold has not been acting as a great wealth protector in the past month or so. The dollar has been advancing in value in global currency markets, while the gold price has been seemingly more than reluctant to follow this upwards path. Thus in terms of wealth preservation, to those who look to the gold price through greenback tinted spectacles, gold has been something of a disappointment, having fallen in value in U.S. dollar terms by over 4% since the beginning of 2022. That’s actually not too bad a performance considering all the major stock indexes are down by multiples of that amount. The Dow is down around 12% year to date, the S&P 500 down over 15% and the NASDAQ some 23%.

Chart showing gold’s price performance year-to-date in various currencies: Courtesy Bloomberg.

But in this article we’re primarily looking at the gold price performance in U.S. dollar terms. In many other key major global currencies, as can be seen in the Bloomberg chart above, the gold price has actually risen this year so far – in the Japanese yen for example quite substantially so by close on 14%. Even in the Swiss Franc (not shown in the chart), gold is up over 1% year-to-date. All these currencies have fallen in value against the dollar. Indeed in some weaker currencies, like the Argentinian peso for example the price of gold has risen by over 30% since the beginning of the year. Research published by http://www.goldprice.org shows that gold’s value has appreciated year on year on average by between 6 and 11% for virtually all major currencies over the past 15 years. Even in U.S. dollar terms it has averaged a rise of 7.7% over this period. Not bad for a pet rock!

So don’t assess gold’s performance in the short term against a single currency like the U.S. dollar, even if its price is normally quoted in dollar terms. The U.S. dollar is itself a variable and if it falls back again, as some analysts believe it will, particularly if the U.S. economy is seen as moving into recession, then the dollar gold price would probably rise accordingly to match the greenback’s decline in purchasing power – not to mention a continuing likely appreciation against your own domestic currency. What appears to be a price fall as quoted in U.S. dollar terms may hide a price rise in your own domestic situation assuming you bought the metal in your own monetary unit.

True, if you offloaded any gold holdings in the weeks immediately after Russia invaded Ukraine, in retrospect you would have made good gains in any currency at the time, but most holders hang on to the yellow metal as a long term investment/wealth protector. Like any investment, it has its ups and downs, but overall, as the http://www.goldprice.org research demonstrates, it tends to serve this purpose well over time. If you hold gold look upon it primarily as insurance against economic collapse. There are many out there who will tell you that its price will go through the roof, but a majority of these will have almost certainly been singing the same tune for many years and it hasn’t happened yet. Maybe they’ll be right some day, but don’t bank on it!

01 Sep 202

Biden’s Most Enduring Legacy?

THURSDAY, SEP 01, 2022 – 08:45 AM

Authored by James Rickards via DailyReckoning.com,

Central bank digital currencies (CBDCs) are coming fast, and you need to be prepared for them because they’ll mark a major victory in the war against cash — and against your personal privacy.

You’ll see why today.

As the name implies, central bank digital currencies are digital, existing exclusively in electronic form. They’re not physical at all. Central banks would control them.

But it’s important to understand they’re not new currencies. They’re just digital forms of existing currencies. So the central bank digital currency of the European Central Bank will still be the euro. The central bank digital currency of the Fed will be the dollar. The Chinese yuan will be a digital yuan.

They’ll just exist in 100% digital form. A lot of people say, “Wait a second. Isn’t that a cryptocurrency?” The answer is it’s not.

Digital, but Not Crypto

Cryptocurrencies are different in some important respects. Number one, cryptocurrencies operate on a blockchain, or a digital ledger. It’s a way of keeping track of every transaction involving a particular cryptocurrency like Bitcoin.

A central bank digital currency does not have to be on a blockchain. It could be, but it probably won’t be. So it is digital, it is encrypted, but it’s not a blockchain and it’s not a cryptocurrency.

The other thing about cryptocurrencies is that they’re not issued by any central authority. They’re created mathematically. But a central bank digital currency is issued by a central authority. It’ll come from the Federal Reserve, or the European Central Bank, or the People’s Bank of China or other central bank institutions.

So CBDCs and cryptocurrencies aren’t the same.

Slowly, Then Quickly

The idea of CBDCs has gained momentum over the past few years, and they’re actually being implemented in China.

If you had asked me about CBDCs two years ago, I would have said, “Yes, China’s rolling them out. Europe is coming along not far behind. The U.S. was still maybe three or four years away because the U.S. is taking a much more studious approach.”

But that’s changed under Biden, who has fast-tracked their development. We’ve moved fairly quickly from what I would call the research phase to an implementation phase. The Federal Reserve is working with MIT to work out the technological kinks, which shouldn’t take long.

The Bahamas actually has a central bank digital currency, so if they can figure it out the U.S. certainly can.

How CBDCs Will Be Promoted

What are the advantages of a central bank digital currency? Well, the advantages are speed, cost, security and ease of use.

Assume you buy a candy bar at a convenience store. You pay for it with a credit card, which begins a payment process involving maybe five parties including the merchant, the credit card company, the bank and an intermediary called a merchant acquirer (no need to list the details here, but it’s complicated).

Ultimately the bank that issues your credit card sends you a bill and you pay it. You also pay a fee, maybe 3%, all to buy a candy bar. But with a central bank digital currency, you could simply pay for the candy bar with an account you have at the Fed.

You would disintermediate the merchant acquirer, the banks and the credit card company. It would eliminate the fees we currently face.

In a nutshell, the payment system will be faster, cheaper, easier, more streamlined and more secure.

The Real Reasons They’re Pushing CBDCs

The question is why are they doing this? Well, the banks and the government will tell you that it’s cheaper, faster and safer, so it makes sense. And that’s true, as far as it goes, but there are a lot of hidden agendas here.

The first one is to eliminate cash. If you didn’t like the central bank digital currency system for privacy reasons, you might say, “Hey, I feel like I’m under surveillance. This is intrusive. I just don’t trust it. Where’s my alternative?”

Particularly if they eliminate the traditional credit card payment system, you might buy your candy bar with cash. But if you’re the government and you want the central bank digital currency to succeed, you have to eliminate cash because it’s your competition.

The government hates cash because it’s not traceable. If you spend it, they don’t know that you spent it or how you spent it. They can’t put you under surveillance with cash.

Negative Interest Rates

The other thing the government wants is the ability to impose negative interest rates. Instead of earning interest on your money in the bank, you’d be charged to keep it there. Cash stands in the way of negative interest rates because cash doesn’t have a negative interest rate.

Assume you bury $100,000 in cash in your backyard. You come back a year later, you still have $100,000. You might not earn any interest on your money, but at least the government can’t take it away. But if all your money is in digital form within the banking system, they can impose negative interest rates on it.

The government wants to use the banking system for a lot of other things. They might want to freeze your account, they might want to seize your assets, they might also want to put an expiration date on your money.

Imagine you get paid and the government tells you, “That money is going to evaporate or disappear if you don’t spend it in the next six months.” How’s that for a stimulus program?

So the push for central bank digital currencies, which has a full head of steam, should be understood in the context of eliminating cash.

The Total Surveillance State

CBDCs also have enormous political implications, including the culmination of the total surveillance state. This is why China did it. And don’t believe anyone who tells you that the United States won’t do it.

They’ll start out saying, “Oh, it’s cheaper than Mastercard. Sign up here.” They won’t give you a chance. They’ll force you to sign up, but what they’re doing is putting you under a new level of surveillance. They have you at the point of purchase.

What if you’re in a bookstore and buy a book written by Donald Trump or a book by some author who supports Trump, Ron DeSantis, Rand Paul or any of Biden’s political enemies?

Now they can tag you and potentially label you a domestic terrorist or some such. And what if you make a political contribution to a candidate the administration doesn’t like?

Well, now you could really be in trouble. You bought a pro-Trump book. You gave money to a pro-Trump political candidate. You’re on a list. And they know this because of the payment system.

This is the point.

Biden’s Most Enduring Legacy?

Obviously, they can have an FBI agent follow you around and see what you bought at the book counter, but they don’t have enough FBI agents for that. But if they’re using central bank digital currencies in an account that identifies you, then they can pigeonhole you.

And what about these 87,000 IRS agents they’re hiring? Maybe your name will pop up on one of their lists and they’ll audit you.

So I would caution you that CBDCs aren’t just a cheaper, better, faster payment system, although they may be and that is how they’ll be sold. They will also be used to eliminate cash, impose negative interest rates and track your purchases. They can even freeze your account.

I call the dollar version of the CBDC Biden Bucks because Joe Biden will prove to have been responsible for implementing CBDCs at a very quick tempo in the U.S.

They could one day end up as his most enduring legacy.

end

GOLD/SILVER

END

3.Chris Powell of GATA provides to us very important physical commentaries

This is a major story that we have been following. The Eurasian alliance plans a Moscow World Standard for gold to destroy LBMA/Comex monopoly.

And they will win. The group controls most of the world’s above ground gold

(Ronan Manly)

Ronan Manly: Eurasian alliance plans a Moscow World Standard to destroy LBMA’s monopoly

Submitted by admin on Wed, 2022-08-31 09:48Section: Daily Dispatches

By Ronan Manly

Bullion Star, Singapore

Wednesday, August 31 2022

Toward the end of July, news emerged in the Russian media that Moscow and a number of its Eurasian allies are now reviewing a proposal to create an entirely new trading and pricing infrastructure for the international precious metals in order to both destroy London and New York’s monopoly over global precious metals pricing, and to stabilise the Russian gold market.

This infrastructure would take the form of:

— A Moscow World Standard (MWS) for precious metals trading, akin to the London Good Delivery List of the London Bullion Market Association (LBMA)

— A new international precious metals exchange (trading venue) headquartered in Moscow based on the MWS, and known as the Moscow International Precious Metals Exchange

— A Price Fixing Committee, with price discovery and new precious metals price fixings based on the MWS, and reference prices derived in the national currencies of participant countries or in new international settlement units

This article will review these developments, explain who has proposed them, explore the potentially wide range of countries that could participate in such a system, and look at the originators’ thinking on what gold and other precious metals pricing should be based on. …

… For the remainder of the analysis:

end

Free trading gold is liberty, while gold price manipulation is a prerequisite for totalitarianism

(James Turk)

james Turk: A century of fascism

Submitted by admin on Wed, 2022-08-31 19:55Section: Daily Dispatches

7:54p ET Wednesday, August 31, 2022

Dear Friend of GATA and Gold:

In an essay today GoldMoney founder and GATA consultant James Turk reviews some history and concludes that just as free-trading gold is a prerequiste of liberty, gold price manipulation is a prerequisite of totalitarianism. Turk’s analysis is headlined “A Century of Fascism” and it’s posted at the Free Gold Money Report here:

https://www.fgmr.com/a-century-of-fascism/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4. OTHER GOLD/SILVER COMMENTARIES

-END-

.

end

5.OTHER COMMODITIES:

COMMODITIES IN GENERAL/COAL

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.8997

OFFSHORE YUAN: 6.8980

HANG SENG CLOSED DOWN 357.08 PTS OR 1.79%

2. Nikkei closed DOWN 430.06 OR 1.53%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 109.02/Euro FALLS TO 1.00164

3b Japan 10 YR bond yield: FALLS TO. +.234/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 139.18/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: UP -// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.554%/Italian 10 Yr bond yield RISES to 3.94% /SPAIN 10 YR BOND YIELD RISES TO 2.75%…

3i Greek 10 year bond yield RISES TO 4.17//

3j Gold at $1700.90 silver at: 17.73 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 10/100 roubles/dollar; ROUBLE AT 60.12//

3m oil into the 88 dollar handle for WTI and 94 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 136.39DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 9779– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9793well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.191 UP 8 BASIS PTS

USA 30 YR BOND YIELD: 3.314 UP 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 18,19

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Slump In Ugly Start To Ugliest Month Of The Year

THURSDAY, SEP 01, 2022 – 08:13 AM

With September already historically the ugliest month for markets of the entire year…

… an underperformance which this year will likely be on steroids thanks to the Fed’s doubling of QT to $95BN starting today…

… especially with stocks having gone from overbought to oversold in two weeks as bullish sentiment imploded…

… it’s not like stocks needed an additional impetus to dump, yet they got just that overnight when first China announced that it would put 21 million citizens living in its megacity of Chengdu on lockdown (as part of Beijing’s “Zero Covid” policy of blaming China’s slowdown on 1 or 2 cases of covid per city and promptly locking down whole swaths of the economy, you know, for the kids), and second in a major escalation, Taiwan shot down an unidentified drone off the Chinese coast; the news sent S&P 500 futures sharply lower on the first of the month, dropping as much as 0.9%, with Nasdaq futures down as much as 1.3% after another sales warning from Nvidia sent chipmakers in retreat on new China export rules.

The US 10-year Treasury yield rose to 3.20% and threatening to break above the previous level, a move which would be seen as especially bearish. The dollar gained and oil tumbled for a 3rd day amid fears about Chinese demand, even as OPEC+ is preparing to announce some sort of price stabilization intervention. Industrial metals fell after China locked down Chengdu’s 21 million residents, while oil and natural gas retreated as Europe considers various measures to intervene in the energy market. Commodity-linked and Group-of-10 currencies weakened, while the yen dropped to a 24-year low.

The market jitters come after August’s losses, reflecting fears of an economic downturn alongside restrictive monetary policy to choke inflation. A global bond rout saw the two-year Treasury yield touch 3.50% for the first time since 2007.

In premarket trading, US chipmakers fell in premarket trading after Nvidia warned that new rules governing the export of artificial-intelligence chips to China may affect hundreds of millions of dollars in revenue. Nvidia fell 6%, AMD -3.5%, Intel -1.2%, Micron -2.3%. Bank stocks were lower as investors await the release of jobs data. Here are other notable premarket movers:

- Okta shares slumped as much as 15% in premarket trading after results, which analysts said were “muted” and spurred worries over billings growth and demand.

- MongoDB shares fell 17% in premarket trading, after the database software company gave a “conservative” full-year forecast.

- C3.ai shares were down 14% in premarket trading after the application software company cut its full-year revenue forecast amid an uncertain macro environment.

- Bed Bath & Beyond shares slid as much as 6.3% in premarket trading, with other meme stocks also down, as investors continue to assess the home-goods retailer’s turnaround plan.

- Five Below reported second-quarter results that failed to meet estimates. While disappointed, analysts said they weren’t surprised. The stock rose 3.2% in thin premarket trading.

“The Fed effect is now melding with other global factors such as China’s growth slowdown and Europe’s stagflation to create a more fraught global macro environment with higher rates and lower growth,” said Alvin Tan, strategist at RBC Capital Markets in Singapore. “It is this combination of hawkish central banks led by the Fed, China’s slowdown and Europe’s stagflation that is now driving volatility across global markets.”

European stocks also declined, Euro Stoxx 50 slumps 1.6%. IBEX outperforms, dropping 0.9%, CAC 40 lags, dropping 1.7%. Miners, real estate and consumer products are the worst-performing sectors. Miners led declines in Europe as commodities dropped amid concerns that aggressive tightening and China’s slowdown will lower demand. Among individual moves, Reckitt Benckiser Group Plc’s shares fell on news that Chief Executive Officer Laxman Narasimhan will step down at the end of the month to pursue a new opportunity in the US. Here are the other notable European movers today:

- Jet2 shares rise as much as 4.2% with HSBC saying the tour operator’s AGM statement was reassuring for the short- term

- EuroAPI gains as much as 6.1%, the most since June, after the company presented its 1H earnings. Oddo BHF says the strong report shows EuroAPI’s strategy is “beginning to bear fruit.”

- Chrysalis Investments climbs as much as 5.7% as the Telegraph newspaper’s Questor column says now is “the best time to buy” shares in the investment firm

- Basic Resource stocks fall the most in seven weeks, the sector’s longest losing streak since mid-June, as a slide in metal prices accelerated amid demand concerns over fresh Covid lockdowns in China

- The European real estate sector is among the day’s worst performers on the regional equity benchmark, weighed down by concerns around hawkish central banks

- Luxury-goods stocks slide in Europe after a new Covid lockdown in the key market of China and as HSBC downgraded a bunch of the sector’s biggest firms

- Reckitt Benckiser drops as much as 5.7%, the most since July 2021, after the unexpected news that CEO Laxman Narasimhan will step down

- Zur Rose slumps as much as 11% after an offering of shares priced at CHF39 apiece, representing a 15% discount to the last close

- Warsaw’s WIG20 index continues its retreat, widening this year’s drop to 34% as appetite for commodity stocks wanes amid growth fears and a decline in energy prices in Europe

Some of Wall Street’s biggest banks now expect the European Central Bank to hike rates by 75 basis points at next week’s meeting, while the latest economic data underlined a parlous outlook for China. Meanwhile, Russia said it is considering a plan to buy as much as $70 billion in yuan and other “friendly” currencies this year to slow the ruble’s surge, before shifting to a longer-term strategy of selling its holdings of the Chinese currency to fund investment.

Earlier in the session Asian stocks traded mostly lower following the weak handover from global counterparts amid the higher yield environment and following a surprise contraction in Chinese Caixin Manufacturing PMI data. Hang Seng and Shanghai Comp were subdued after weak factory activity data from China and with Meituan among the worst performers in Hong Kong after reports its shareholder Tencent is planning about USD 14.5bln of divestments from its equity portfolio including a partial divestment of its stake in Meituan, while the mainland was cushioned after further policy support pledges by China’s cabinet.

Japanese stocks closed lower ahead of a raft of US data that may back the case for the Federal Reserve to continue raising interest rates. The Topix index fell 1.4% to 1,935.49 at the 3 p.m. market close in Tokyo, while the Nikkei 225 declined 1.5% to 27,661.47, closing beneath the 28k alongside the broader risk aversion with further currency weakness and an upgrade to Japanese PMI data doing little to inspire a turnaround. Toyota contributed the most to the Topix’s decline, decreasing 2.3%. Out of 2,169 stocks in the index, 226 rose and 1,879 fell, while 64 were unchanged. Shares also slid as parts of China went back into lockdown.

In Australia, the S&P/ASX 200 index fell 2%, the most since June 14, to close at 6,845.60, dragged by losses in banks and mining shares. The materials sub-gauge was the worst performer, slumping to the lowest since July 27, as commodity prices tumbled and as BHP, the benchmark’s heaviest-weighted stock, trades ex-dividend. In New Zealand, the S&P/NZX 50 index was little changed at 11,609.83.

In FX, the Bloomberg Dollar Spot Index advanced as the greenback strengthened against all of its Group-of-10 peers apart from the Swiss Franc. The euro slumped but managed to hold above parity against the dollar after Germany July retail sales rose 1.9% m/m vs estimated 0.1% decline. Italian bonds and bunds slid for a fifth day, lifting Italy’s 10-year yield above 4% for the first time since June 15 as money markets continued to raise ECB tightening bets ahead of next week’s policy outcome. The Swiss Franc snapped a four-day loss against the dollar. A report showed that Swiss prices increased by 3.5% in August, above July’s reading of 3.4% — already the highest in three decades. The pound extended declines, dropping to a 2 1/2-year low against a broadly stronger US dollar. Sterling was set for its fifth- straight day of declines, after August saw its worst month versus the greenback since 2016. The yen dropped to 139.68 per dollar, its lowest since 1998 as surge in Treasury yields heaped more pressure on the currency, prompting a warning from a Japanese government official that did little to stem the tide. Australian and New Zealand dollars fell as a stronger greenback boosted by rising Treasury yields and a drop in iron ore prices weighed.

The offshore yuan fleetingly extended gains against the dollar on reports that Russia is considering buying as much as $70 billion in yuan and other “friendly” currencies. The yen pares some declines to trade at 139.24/USD after falling to weakest level since 1998 as US-Japan yield spread keeps widening. Bloomberg dollar spot index rises 0.2%, while CHF outperforms G-10 peers.

In rates, Treasuries were narrowly mixed as US trading gets under way Thursday with the yield curve steeper after the 2-year failed to sustain its first breach of 3.5% since 2007. 2-year yields are lower by 1.4bp at 3.479% after rising as much as 1.8bp to 3.511%; 30-year higher by 2.2bp near day’s high; inverted 2s10s spread steeper by 1.6bp at -29bp, 5s30s by nearly 4bp at -2.2bp. Wednesday’s month-end close entailed bear-flattening that continued until 5pm New York time, an hour after the Bloomberg Treasury index rebalancing, and was especially pronounced in TIPS. The US 10-year trails steeper yield increases for UK and most euro-zone counterparts. Treasuries’ 2.5% August loss was the market’s biggest since April; paced by UK and euro-zone yields, it was driven by more hawkish expectations for Fed policy that lifted 2- and 5-year yields by more than 60bp. Gilts push lower, with the yield on 10-years up 7 bps to 2.87%, while European bonds extend declines. Italian 10-year yield went briefly above 4% for the first time since June 15. Bunds also slipped, leaving the two-year rate within a whisker of its June peak.

In commodities, WTI crude fell to around $88; gold loses ~$5 to near $1,705. European natural gas declines for a fourth day. Spot gold is meandering just north of USD 1,700/oz after testing the figure to the downside. Base metals are lower across the board following the downbeat Chinese manufacturing PMI overnight alongside news of stricter Chinese lockdowns in some regions. US Treasury Secretary Yellen and UK Chancellor Zahawi discussed efforts regarding a price cap on Russian oil to lower global energy prices and restrict Russia’s revenue, according to the US Treasury Department. It was separately reported that US and allies are to set out a plan on Friday to limit the price of Russian oil with a strategy that aims to cut Russian energy revenues without increasing global oil prices, according to WSJ. OPEC+ JTC acknowledges the relevance of the Saudi Energy Minister’s comments on volatility and thin liquidity of crude markets, via Reuters citing a document.

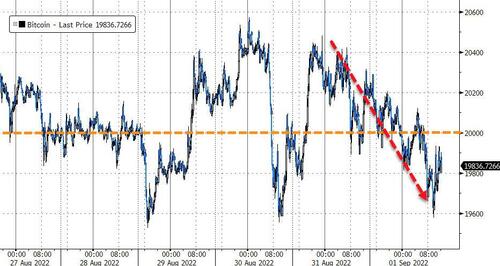

Bitcoin remains under pressure and below the USD 20k mark, fairly in-fitting with its Ethereum peer in residing at the bottom-end of very narrow ranges.

To the day ahead now, data releases include the global manufacturing PMIs for August and the ISM manufacturing reading from the US. Otherwise, there’s also the US weekly initial jobless claims, the Euro Area unemployment rate for July, and German retail sales for July. Central bank speakers include the ECB’s Centeno and the Fed’s Bostic. Finally, earnings releases include Broadcom and Lululemon.

Market Snapshot

- S&P 500 futures down 0.8% to 3,924.25

- STOXX Europe 600 down 1.6% to 408.48

- MXAP down 1.9% to 155.53

- MXAPJ down 1.9% to 510.07

- Nikkei down 1.5% to 27,661.47

- Topix down 1.4% to 1,935.49

- Hang Seng Index down 1.8% to 19,597.31

- Shanghai Composite down 0.5% to 3,184.98

- Sensex down 1.6% to 58,581.55

- Australia S&P/ASX 200 down 2.0% to 6,845.60

- Kospi down 2.3% to 2,415.61

- German 10Y yield little changed at 1.63%

- Euro down 0.2% to $1.0032

- Brent Futures down 1.8% to $93.88/bbl

- Brent Futures down 1.9% to $93.87/bbl

- Gold spot down 0.6% to $1,701.34

- U.S. Dollar Index up 0.19% to 108.91

Top Overnight News from Bloomberg

- The hotly anticipated US jobs report has the potential to tip the scales toward a third jumbo-sized hike in interest rates later this month after a wave of data that point to a resilient consumer and high labor demand

- The Chinese metropolis of Chengdu will lock down its 21 million residents to contain a Covid-19 outbreak, a seismic move in the country’s vast Western region that has largely been untouched by the virus

- Europe is considering various measures to intervene in the energy market, including price caps, reducing power demand and windfall taxes on energy companies as surging prices threaten the economy and push households toward poverty

- PMIs for the 19-nation euro zone slipped to 49.6 in August from 49.8 in July, according to S&P Global — a reflection of dwindling demand as consumers face surging costs for energy and a broadening range of goods and services. Germany and Italy both saw the worst readings in 26 months

- Russia is considering a plan to buy as much as $70 billion in yuan and other “friendly” currencies this year to slow the ruble’s surge, before shifting to a longer-term strategy of selling its holdings of the Chinese currency to fund investment

- Japanese workers’ share of company earnings fell for the first time in four years, suggesting Prime Minister Fumio Kishida’s call for companies to pay more to employees is running into resistance

A more detailed summary of global markets courtesy of Newsquawk

Asia-Pac stocks traded mostly lower following the weak handover from global counterparts amid the higher yield environment and following a surprise contraction in Chinese Caixin Manufacturing PMI data. ASX 200 was dragged lower by the mining-related sectors after recent declines in underlying commodity prices. Nikkei 225 retreated beneath the 28k alongside the broader risk aversion with further currency weakness and an upgrade to Japanese PMI data doing little to inspire a turnaround. Hang Seng and Shanghai Comp were subdued after weak factory activity data from China and with Meituan among the worst performers in Hong Kong after reports its shareholder Tencent is planning about USD 14.5bln of divestments from its equity portfolio including a partial divestment of its stake in Meituan, while the mainland was cushioned after further policy support pledges by China’s cabinet.

Top Asian News

- China’s city of Chengdu will conduct mass COVID testing from September 1st-4th and the city government said all residents will stay at home from this evening, according to Reuters.

- Hong Kong will push ahead with a proposal that will allow more residents to travel to mainland China after completing a quarantine period locally, according to SCMP citing sources.

- UN Human Rights Office issued its assessment of human rights concerns in Xinjiang in which it stated that China’s government has committed serious human rights violations in Xinjiang and recommended China take prompt steps to release all those detained in training centres, prisons or detention facilities, according to Reuters and AFP.

- Chinese mission in Geneva said it expresses strong dissatisfaction regarding the UN report on Xinjiang and firmly opposes the report, while it added that the so-called assessment was a farce planned by the US, western nations and anti-China forces, according to Reuters.

- Hong Kong officials are targeting a conclusion to hotel COVID quarantines in November.

- Macau gov’t intends to gradually reopen the city to foreign travellers, via Reuters.

European bourses are underpressure amid continued hawkish pricing, but off lows as yields ease from highs, Euro Stoxx 50 -1.4%. Stateside, a similar picture to fixed with action in-fitting directionally but steadier in terms of magnitudes ahead of data, ES -07%; NQ -1.1% lags given elevated yields.

Top European News

- Russia is said to be mulling as much as USD 70bln in “friendly” currencies, according to Bloomberg sources; this is in order to slow the RUB surge “before shifting to a longer-term strategy of selling its holdings of the Chinese currency”.

- Lufthansa Pilot Union Calls for One-Day Strike on Friday

- Zur Rose Slumps Amid Offering at Discount, Convertibles Sale

- Russia Mulls Buying $70 Billion in Yuan, ‘Friendly’ Currencies

- Factory Slowdown in Europe and Asia Is Warning for Global Trade

Central Banks

- Fed’s Logan (2023 voter) said the number one priority is to restore price stability, according to Reuters.

- Japan’s Chief Secretary Matsuno provides no comment on every day-to-day FX moves, watching moves with a high sense of urgency; desirable for currencies to move stably, reflecting economic fundamentals.

FX

- DXY sits around USD 109.00 after seeing fresh lows amid Yuan appreciation.

- EUR, GBP AUD, NZD, JPY are all softer vs the USD to similar magnitudes.

- CAD and CHF are the G10 outliers, with the latter supported after Swiss CPI and the former hit by softer oil prices.

Fixed Income

- Core benchmarks are under pronounced pressure once more with yields across the board at fresh near-term peaks

- Pressure occurring despite geopolitical tensions as hawkish ECB pricing continues to increase, ~85% chance of a 75bp hike.

- Though, following the passing of hefty European/UK issuance, the magnitude of this downside has eased.

- USTs are directionally in-fitting but more contained overall awaiting ISM Manufacturing today and then NFP on Friday.

Commodities

- WTI and Brent futures have resumed downward action following an APAC session of consolidation.

- Spot gold is meandering just north of USD 1,700/oz after testing the figure to the downside.

- Base metals are lower across the board following the downbeat Chinese manufacturing PMI overnight alongside news of stricter Chinese lockdowns in some regions

- US Treasury Secretary Yellen and UK Chancellor Zahawi discussed efforts regarding a price cap on Russian oil to lower global energy prices and restrict Russia’s revenue, according to the US Treasury Department. It was separately reported that US and allies are to set out a plan on Friday to limit the price of Russian oil with a strategy that aims to cut Russian energy revenues without increasing global oil prices, according to WSJ.

- OPEC+ JTC acknowledges the relevance of the Saudi Energy Minister’s comments on volatility and thin liquidity of crude markets, via Reuters citing a document.

- EU Commission President von der Leyen will outline ideas on an energy price cap in more detail in a speech on September 14th.

- Four people killed in overnight clashes in Iraq’s Basra, according to security officials cited by Reuters.

US Event Calendar

- Aug. Wards Total Vehicle Sales, est. 13.3m, prior 13.4m

- 07:30: Aug. Challenger Job Cuts YoY, prior 36.3%

- 08:30: 2Q Unit Labor Costs, est. 10.5%, prior 10.8%

- 2Q Nonfarm Productivity, est. -4.3%, prior -4.6%

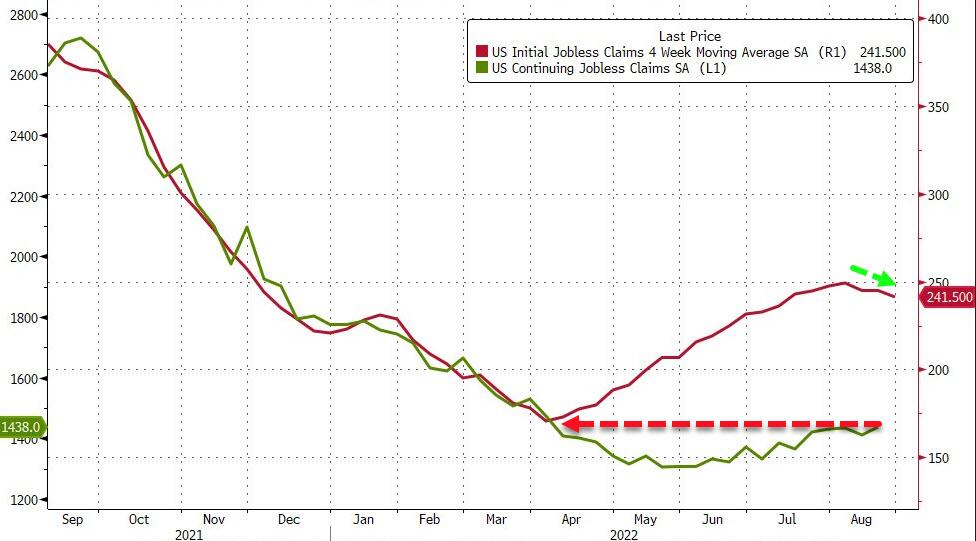

- 08:30: Aug. Initial Jobless Claims, est. 248,000, prior 243,000

- Continuing Claims, est. 1.44m, prior 1.42m

- 10:00: July Construction Spending MoM, est. -0.2%, prior -1.1%

- 10:00: Aug. ISM Manufacturing, est. 51.9, prior 52.8

- ISM Employment, est. 49.5, prior 49.9

- ISM New Orders, est. 48.0, prior 48.0

- ISM Prices Paid, est. 55.2, prior 60.0

DB’s Henry Allen concludes the overnight wrap

Welcome to September. Given it’s the start of the month, we’ll shortly be publishing our regular monthly review of financial assets across for the month just gone. August was very much a month of two halves when it came to risk assets, with most ending the month in negative territory. There were still plenty of headlines though, and in Europe we saw some of the largest rises in short-term yields in decades. For instance, yields on 2yr German debt haven’t risen this much in a month since 1981, and for their UK counterparts you also have to go back to 1986. The full report will be in your inboxes shortly.

When it comes to the last 24 hours, markets have been playing a familiar theme, with risk assets losing further ground as investors price in more rate hikes over the coming months. The big driver behind that yesterday was another stronger-than-expected inflation print from the Euro Area, where the flash CPI reading rose to a record +9.1%. We haven’t seen inflation that strong since the formation of the single currency, and it was also above the +9.0% reading expected by the consensus. The details didn’t look much better either, with core inflation rising to a record +4.3% too (vs. +4.1% expected). So a disappointment for those hoping we might have seen the worst of inflation by now, and another demonstration of how the energy shock is sending European inflation increasingly above that in the US.

Unsurprisingly, the high inflation bolstered the arguments of the hawks on the ECB’s Governing Council, and Bundesbank President Nagel said yesterday that “We need a strong rise in interest rates in September.” In addition, Austria’s Holzmann further said that he saw “no reason to show any kind of leniency in our positioning and our wish to reduce inflation”. That’s more voices bolstering the speakers we’ve heard from in recent days who’ve put a 75bps hike on the table, and investors themselves moved to price in a more aggressive ECB response too. Indeed, overnight index swaps are now pricing in a 69.0bps hike for the next meeting, which is noticeably closer to 75 than 50 now. And for the September and October meetings as a whole, 130.7bps worth of hikes are priced in, which is equivalent to at least one of them being a 75bps move and the other at 50bps.