by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSE: UP $1.75 to $1628.90

SILVER PRICE CLOSE: DOWN 7 cents to $18.39

Access prices: closes

Gold ACCESS CLOSE 1629.70

Silver ACCESS CLOSE: 18.41

Bitcoin morning price: $20,240 UP 1102

Bitcoin: afternoon price: $19,055 DOWN 83

Platinum price closing DOWN $4.10 AT $851.00

Palladium price; closing UP $14.85 at $2078.00

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

COMEX//NOTICES FILED

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,623.300000000 USD

INTENT DATE: 09/26/2022 DELIVERY DATE: 09/28/2022

FIRM ORG FIRM NAME ISSUED STOPPED

624 H BOFA SECURITIES 7

661 C JP MORGAN 270 175

690 C ABN AMRO 69

732 C RBC CAP MARKETS 50

880 H CITIGROUP 207

TOTAL: 389 389

MONTH TO DATE: 11,147

JPMorgan stopped 175/389

GOLD: NUMBER OF NOTICES FILED FOR SEPT CONTRACT:

389 NOTICES FOR 38,900 OZ //1.2099 TONNES

total notices so far: 11,147 contracts for 1,114,700 oz (34.6765 tonnes)

SILVER NOTICES: 46 NOTICES FILED FOR 230,000 OZ/

total number of notices filed so far this month 6741 : for 33,705,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $1.75

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: //// A WITHDRAWAL OF 3.76 TONNES FROM THE GLD/

INVENTORY RESTS AT 943.47 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 7 CENTS

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF OF 0.737 MILLION OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 481.194 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1592 CONTRACTS TO 129,935 (ANOTHER ALL TIME RECORD LOW) AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.43 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.43) AND WERE SUCCESSFUL IN KNOCKING OFF SOME SPEC SILVER LONGS AS WE HAD A HUGE LOSS OF 1002 CONTRACTS ON OUR TWO EXCHANGES. WE DID HAVE MINOR SILVER SHORT COVERING.

WE MUST HAVE HAD:

I) MINOR SPECULATOR SHORT COVERING ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 305,000 OZ QUEUE JUMP / // V) HUGE SIZED COMEX OI LOSS/(//MINOR SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: –115

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 18 days, total 13,810 contracts: 69.059 million oz OR 3.835 MILLION OZ PER DAY. (767 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 69.059 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 69.059 MILLION OZ///

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1592 WITH OUR $0.43 LOSS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 475 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /GOOD BANKER ADDITIONS A// MINOR NET SPEC SHORT COVERINGS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 305,000 OZ QUEUE JUMP // .. WE HAD A HUGE SIZED LOSS OF 1117 OI CONTRACTS ON THE TWO EXCHANGES FOR 5.585MILLION OZ AS..

WE HAD 46 NOTICE(S) FILED TODAY FOR 230,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

WE HAVE 3 MORE READING DAYS BEFORE FIRST DAY NOTICE

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 834 CONTRACTS TO 466,797 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED — -462 CONTRACTS.

.

THE SMALL SIZED DECREASE IN COMEX OI CAME DESPITE OUR HUGE FALL IN PRICE OF $17.15//COMEX GOLD TRADING/MONDAY / WE MUST HAVE HAD MAJOR SPECULATOR SHORT COVERINGS ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND //CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 94.100 OZ //NEW STANDING 36.775 TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S)

YET ALL OF..THIS HAPPENED WITH OUR FALL IN PRICE OF $17.15 WITH RESPECT TO MONDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 4037 OI CONTRACTS 12.556 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5333 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 466,335

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4037 CONTRACTS WITH 1296 CONTRACTS DECREASED AT THE COMEX AND 5333 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4037 CONTRACTS OR 12.993 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5333) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (1296): TOTAL GAIN IN THE TWO EXCHANGES 4037 CONTRACTS. WE NO DOUBT HAD 1) CONSIDERABLE SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS/// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.409 TONNES FOLLOWED BY TODAY’S MONSTROUS QUEUE JUMP OF 94,100 oz. 3) ZERO LONG LIQUIDATION//// //.,4) SMALL SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

54,577 CONTRACTS OR 5,457,700 OZ OR 169.75 TONNES 18 TRADING DAY(S) AND THUS AVERAGING: 3032 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAY(S) IN TONNES: 169.75 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 169.75/3550 x 100% TONNES 4.78% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 169.75 TONNES (SLIGHTLY RISING THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER,FELL BY A HUGE SIZED 1592 CONTRACT OI TO 129,935 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 475 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 475 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 475 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1592 CONTRACTS AND ADD TO THE 475 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF 1117 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 5.585 MILLION OZ

OCCURRED WITH OUR STRONG LOSS IN PRICE OF $0.34

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 42.64 PTS OR 1.40% //Hang Sang CLOSED UP 5.17 PTS OR 0.03% /The Nikkei closed UP 140.32 PTS OR 0.53% //Australia’s all ordinaires CLOSED UP 1.44% /Chinese yuan (ONSHORE) closed DOWN AT 7.1727//OFFSHORE CHINESE YUAN DOWN 7.1732// /Oil DOWN TO 77.68 dollars per barrel for WTI and BRENT AT 85.21 / Stocks in Europe OPENED ALL MIXED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 1296 CONTRACTS TO 466,335 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED DESPITE OUR FALL IN PRICE OF $17.15 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (5333 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5333 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :5333 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5333 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED SIZED TOTAL OF 4037 CONTRACTS IN THAT 5333 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI LOSS OF 1296 CONTRACTS..AND THIS GOOD GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $17.15. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (36.790),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 36.790 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $17.15) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A GOOD SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF4037 CONTRACTS // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS TRIED TO COVER ON THEIR POSITIONS WITH SOME SUCCESS////// WE HAVE REGISTERED A GOOD GAIN OF 4499 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT. (36.790 TONNES)…

WE HAD -462 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 4037 CONTRACTS OR 403,700 OZ OR 12.556 TONNES

Estimated gold volume 198,509/// fair//

final gold volumes/yesterday 239,877/ fair

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 27

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 60.726.115 oz BRINKS JPMorgan includes 3 kilobars Brinks |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 389 notice(s) 38900 OZ 1.2099 TONNES |

| No of oz to be served (notices) | 681 contracts 68100 oz 2.118 TONNES |

| Total monthly oz gold served (contracts) so far this month | 11,147 notices 1,114,700 OZ 34.6785 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals: 2

i) Out of Brinks 96.46 o 3 kilobars

ii) Out of JPMorgan: 60,629.655 oz

total: 60,726.115 oz

total in tonnes: 1.88 tonnes

Adjustments: 2

JPM: dealer to customer; 5,121.3470z

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 1070 contracts having LOST 306 contracts .

We had 1253 notices filed on MONDAY so we gained a whopping 947 contracts or an additional 94,700 oz

will stand for gold in this very non active delivery month of September. This queue jump is actually the Londoners exercising efp’s and tendering them to the banks

for the physical!

October LOST a small 931 contracts LOWERING TO 41,044. Oct is generally a poor active delivery month. It WILL change!! (Look for a dramatically large Oct. delivery month.)

WE HAVE 3 MORE READING DAYS BEFORE FIRST DAY NOTICE ( FRIDAY SEPT 30.2022)

November GAINED 39 contracts to stand at 832

December GAINED 244 contracts UP to 377,673

We had 389 notice(s) filed today for 38900 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 270 notices were issued from their client or customer account. The total of all issuance by all participants equate to 389 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 175 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (11,147) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 1064 CONTRACTS) minus the number of notices served upon today 389 x 100 oz per contract equals 1,182,800 OZ OR 36.790 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (11147) x 100 oz+ (1064) OI for the front month minus the number of notices served upon today (389} x 100 oz} which equals 1,182,800 oz standing OR 36.790 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 36.775 TONNES (A HUMONGOUS STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,247,740.885 oz 69.914 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 26,557,244.895 OZ

TOTAL REGISTERED GOLD: 13,127,978.542 OZ (408.33 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 13,429,266.353 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,880,238 OZ (REG GOLD- PLEDGED GOLD) 338.42 tonnes//rapidly declining

END

SILVER/COMEX/SEPT 27

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,942,792.022 oz Brinks CNT Delaware HSBC JPM Malca |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 761,269.460 oz CNT Loomis Manfra |

| No of oz served today (contracts) | 46 CONTRACT(S) 230,000 OZ) |

| No of oz to be served (notices) | 34 contracts (170,000 oz) |

| Total monthly oz silver served (contracts) | 6741 contracts 33,705,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 3 deposits into the customer account

i) Into CNT: 124,174.620 oz

ii) Into Loomis: 599,360.140 oz

iii) Into Manfra:37,734.700 oz

Total deposits: 761,269.460 oz

JPMorgan has a total silver weight: 163.469 million oz/315.317million =51.85% of comex

Comex withdrawals: 6

i) Out of Brinks: 509,137.600 oz

ii)Out of CNT 108,545.320 oz

iii)Out of Delaware: 999.952 oz

iv) out of HSBC 339,645.580 oz

v) out of JPMorgan: 605,733.900 oz

vi) Out of Malca: 379,728.659 oz

total withdrawals: 1,942,791.011 oz

adjustments: // 3

DEALER TO CUSTOMER:

i) Brinks 351,232.310 oz

ii) CNT 118,151.018 oz

iii) Out of Delaware: 76,552.692 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 42.999 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 315.317 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF SEPT OI: 80 CONTRACTS HAVING GAINED 9 CONTRACTS. WE HAD

52 CONTRACTS SERVED ON MONDAY SO WE GAINED 61 CONTRACTS OR AN ADDITIONAL

305,000 OZ WILL STAND FOR METAL IN THIS VERY ACTIVE MONTH OF SEPT.

WE WILL GAIN IN TOTAL SILVER STANDING EACH TRADING DAY UNTIL THE END OF THE MONTH

(CONTINUAL QUEUE JUMPING BY OUR BANKERS SEARCHING FOR SILVER METAL)

OCTOBER LOST 55 CONTRACTS TO STAND AT 365 CONTACTS.

NOVEMBER GAINED 44 CONTRACTS TO STAND AT 192

DECEMBER SAW A LOSS OF 1649 CONTRACTS DOWN TO 114,288

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 46 for 230,000 oz

Comex volumes:77,547// est. volume today// good

Comex volume: confirmed yesterday: 84,973 contracts ( good)

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 6741 x 5,000 oz = 33,705,000 oz

to which we add the difference between the open interest for the front month of SEPT(80) and the number of notices served upon today 46 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT./2022 contract month: 6,741 (notices served so far) x 5000 oz + OI for front month of SEPT (80) – number of notices served upon today (46) x 5000 oz of silver standing for the SEPT contract month equates 33,875,000 oz. .

We have an inventory of 42.999 million oz of registered silver at the comex so Sept delivery of 33.875 MILLION OZ represents 78.17% of that category of silver.

If we add August’s final delivery (to Sept) for silver at 5.51 million oz, we have a total of 39.385 million oz delivered upon with a REGISTERED INVENTORY of 42.99 million oz or 91.59% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:60,617// est. volume today// poor

Comex volume: confirmed yesterday: 83,937contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

GLD INVENTORY: 943.47 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

CLOSING INVENTORY 481.194 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

LAWRIE WILLIAMS: In the UK gold is living up to expectations

If one reads all the headlines about gold one could be forgiven for thinking that 2022 has been a pretty disastrous year for those banking on the yellow metal to preserve their wealth. This is indeed the case for U.S. gold holders where the gold price has declined around 9%, although that is less than half that seen in most U.S. equities since the beginning of the year – even more in the NASDAQ stocks – but in the case of UK gold holders and holdings valued in pounds sterling it has been a very different story altogether due to the fall in value of the pound against the dollar so far this year. This has been a similar experience in other areas of the world where local currencies have been in strong decline against their U.S. counterpart.In pound sterling terms, the gold price has actually appreciated by no less than 13% while the FTSE all share index for comparison has declined by around 10% over the same period. With the Bank of England following the U.S. Federal Reserve with an aggressive interest rate raising policy to fight inflation, and commenting that the UK economy is probably already in at least a mild recession, one can anticipate further equity price slippage, while the gold price can probably still hold its own making it a continuingly good wealth protection choice for investors.Of course the UK is not the only country where the gold price has been appreciating in the local currency due to the U.S. dollar’s strength – there are many others. We have already reported on the resultant strength of the Australian gold mining sector during the most recent quarter due to the almost A$42 per ounce gold price rise during Q2 resulting from a 6 cent movement in the exchange rate between the U.S. and Australian dollars. With producer costs mostly in Australian dollars the miners mostly saw some good cost benefits. Although these would inevitably close over time, the short term advantages will have been beneficial. (see: Australian annual gold output 317 tonnes – Surbiton).Even in the Euro, which has also seen a strong decline in currency parity against the U.S. dollar, the gold price is up a little over 6% and in the Japanese Yen up 13% – a similar level to the UK. Of the other supposedly ‘strong’ currencies, the gold price is down marginally, though, in the Swiss Franc and the Canadian Dollar, but not by as much as in the U.S. currency. In some of the world’s weaker currencies , however, gold’s appreciation year to date will have been far greater, so its wealth protection capabilities in your own domestic situation depends very much on one’s domicile.All currencies fluctuate – even the mighty U.S. dollar and there is a feeling that it may well be flying too high at present. There is the possibility it may start to come down from its peaks when there is a realisation of quite how much the servicing of the huge U.S. debt position will cost at the higher interest rate levels currently in place, and likely to be further increased.-END-

END

3.Chris Powell of GATA provides to us very important physical commentaries

Late last night, the Bank of England prepares an emergency intervention as the pound slumps

(Warrington, London telegraph/GATA)

Bank of England prepares emergency intervention as pound slumps to all-time low

Submitted by admin on Mon, 2022-09-26 10:19 Section: Daily Dispatches

By James Warrington,Tom Rees, and Matt Oliver

The Telegraph, London

Monday, September 26, 2022

The Bank of England is understood to be preparing an intervention after the pound crashed to an all-time low against the dollar.

The Bank is expected to issue a statement as soon as today amid mounting pressure on Governor Andrew Bailey for an intervention to help shore up the economy

This could be a verbal intervention to calm markets or, in a more extreme case, an unscheduled increase in interest rates – which were raised to 2.25pc just last week.

It is understood that a statement today is probable, but not definite. The Bank declined to comment on the nature of any intervention.

The possible intervention comes amid market turmoil after Chancellor Kwasi Kwarteng last week unveiled the biggest package of tax cuts in 50 years and hinted at more to come. …

… For the remainder of the report:

* * *

END

Bank of England rules out an emergency rate hike. The pound temporarily falls

(Warrington/London Telegraph)

Pound falls again as Bank of England rules out emergency rate hike

Submitted by admin on Mon, 2022-09-26 12:10Section: Daily Dispatches

By James Warrington, Tom Rees, and Matt Oliver

The Telegraph, London

Monday, September 26, 2022

The governor of the Bank of England has ruled out an emergency rate rise following a rout in the pound.

In a statement just minutes after a separate one by Kwasi Kwarteng, the chancellor, Andrew Bailey said the bank’s monetary policy committee “will not hesitate to change interest rates by as much as needed” to bring inflation under control.

He added that Threadneedle Street is “monitoring developments in financial markets very closely in light of the significant repricing of financial assets.”

But Bailey stopped short of announcing an emergency meeting of the committee this week and suggested it would stick to its next scheduled gathering in November.

After his statement was released, the pound plunged again, despite having stabilised earlier in the afternoon. …

… For the remainder of the report:

END

Dave Kranzler on the importance of physical vs paper gold/silver

(Dave Kranzler/GATA)

Dave Kranzler: Paper vs. physical and why the monetary metals should rally

Submitted by admin on Mon, 2022-09-26 20:06Section: Daily Dispatches

By Dave Kranzler

Investment Research Dynamics, Denver

Monday, September 26, 2022

I had an interesting dialogue today with a couple of long-time colleagues about this commentary by Pam and Russ Martens of Wall Street On Parade, headlined “Nowhere to Hide: The Fed-Induced Bubble in Stocks and Bonds Is Blowing Up; Even the Typical Safe Havens of Gold and T Notes Are Losing Money.”

The Martenses do an admirable job exposing the corruption on Wall Street and in the Fed and Congress. But they exhibit a profound misunderstanding of the architecture of the global market for gold and silver.

The Martenses write that “the typical safe havens of gold and T-notes are losing money.” Well, yes, all flavors of fixed-income securities are losing money because that’s how bond math works when interest rates and bond yields rise.

However, the Martenses fail to understand that the gold and silver market is bifurcated. …

… For the remainder of the commentary:

END

Bill Murphy interviewed

(Bill Murphy/GATA)

GoldSeek Radio’s Chris Waltzek interviews GATA Chairman Bill Murphy

Submitted by admin on Mon, 2022-09-26 19:22Section: Daily Dispatches

7:21p ET Monday, September 26, 2022

Dear Friend of GATA and Gold (and Silver):

Interviewed by GoldSeek Radio’s Chris Waltzek, GATA Chairman Bill Murphy says the daily bombardment of the gold and silver futures markets has destroyed investor interest in the monetary metals sector. When and if the gold and silver cartels exhaust their supply of real metal needed to control the futures markets, Murphy says, prices will explode.

The interview is 19 minutes long and can be heard at GoldSeek Radio here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

5.OTHER COMMODITIES: URANIUM

Uranium Stocks Rise As German Minister Sees Nuclear Power Plant Extension Increasingly Likely

TUESDAY, SEP 27, 2022 – 11:41 AM

Uranium stocks advanced on Tuesday after Germany’s economy minister expects to extend the lifespan of the country’s last two nuclear power plants to prevent the risks of rolling blackouts in Europe’s largest economy this winter.

“We are already in a place where the stress test says: It may be necessary to use nuclear power plants for grid security,” Economy Minister Robert Habeck said at a climate conference in Berlin, which Reuters quoted.

Earlier this month, Chancellor Olaf Scholz’s ruling coalition approved measures to extend two of the country’s three remaining nuclear power plants through the end of this year and into next if needed, reversing planned shutdowns of the plants.

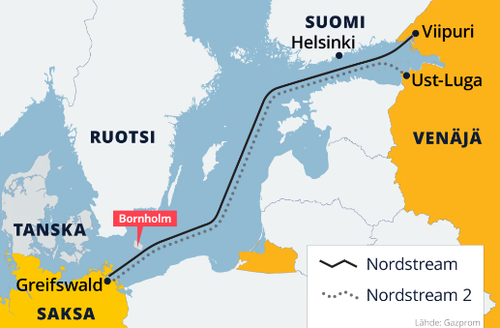

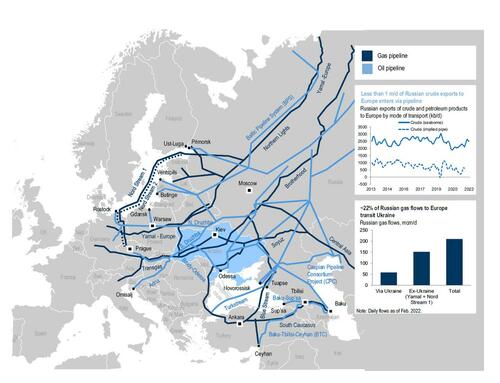

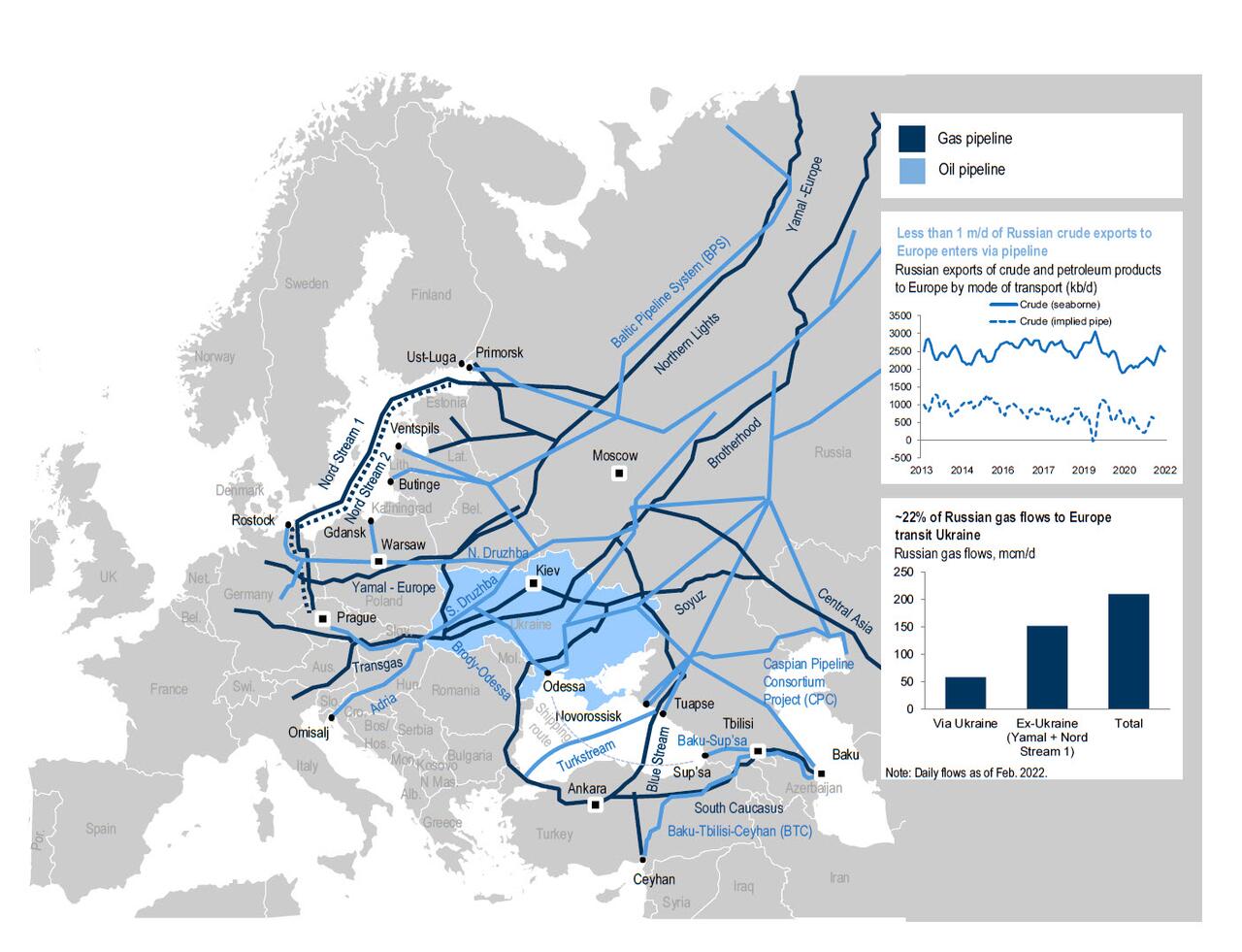

The reversal comes as the historic energy crisis in Europe worsens by the week. Leaks in the Nord Stream pipelines may indicate Nord Stream 1 is indefinitely shuttered.

Habeck said life extensions of the two nuclear plants are to reduce grid bottlenecks.

“It’s not the amount of electricity, but the distribution of power in the grid,” he said, adding he was concerned by the decline of nuclear power from France.

When asked if lifespan extensions of the two German nuclear plants looked possible, Habeck said: “It is certainly not less likely.”

Habeck’s comments generated bullish sentiment across uranium stocks. Global X Uranium ETF (URA) rose 5%, led by Western Uranium & Vanadium, Isoenergy, Energy Fuels, Global Atomic, Uranium Energy, and Forsys.

Support for nuclear continues to gain momentum. And in Germany’s case, it could help with grid stability ahead of what’s expected to be a cold and dark winter.

Remember we outlined in 2020: Buy Uranium: Is This The Beginning Of The Next ESG Craze.

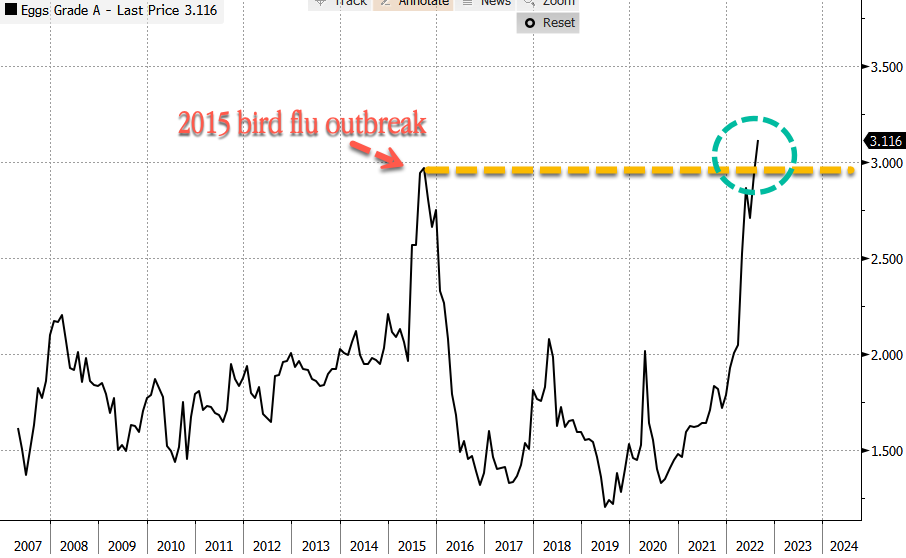

COMMODITIES IN GENERAL/EGGS

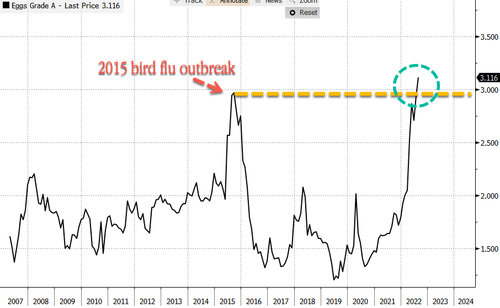

US Egg Prices Hit Record High As Resurgent Bird Flu Dents Production

TUESDAY, SEP 27, 2022 – 04:40 PM

The unseasonable return of avian influenza or bird flu continues to devastate egg production in the US. As a result, retail prices for a dozen eggs at the supermarket have soared to record highs, fueling breakfast inflation.

Bird flu’s return comes as more than 40 million birds were culled in the first half of the year. The disease usually abates during the hot summer months. The current death toll of birds stands at a whopping 45 million and could dramatically worsen, Beth Thompson, South Dakota’s state veterinarian, told Bloomberg. She said the virus is being fueled this fall by the migration of wild birds that fly above commercial farms and leave droppings that get tracked into poultry houses.

Thompson said bird flu “doesn’t seem to have been affected by that hot summer, and in the next probably four to six weeks, we’re going to see those migrating birds coming back from Canada, flying over the US.” She added, “that may increase the viral load that’s out in the environment.”

The culling of millions of birds has dented egg supplies, sending prices sky-high and above 2015 outbreak levels (last major bird flu) to now $3.16 per dozen at the supermarket. Retail prices have doubled since August 2020, straining consumers’ wallets as breakfast inflation soars.

Besides eggs, turkeys sell at a record high price ahead of the Thanksgiving holiday.

According to Urner Barry data, turkey prices were about $1.82 a pound last week, up from $1.42 last year and $1.01 before the pandemic.

“There’s nothing appearing on the horizon to suggest anything new is going to surface to help ease the supply-side pain for Thanksgiving turkeys,” said Russ Whitman, senior vice president at commodity researcher Urner Barry.

Consumers can’t catch a break as food inflation pressures household budgets. There’s nothing the Federal Reserve can do about supply-side food woes because they can’t print eggs or turkey meat. Instead, the Fed can aggressively send interest rates higher, denting demand though it comes at a risk of causing household discontent.

END

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1727

OFFSHORE YUAN: 7.1732

SHANGHAI CLOSED: UP 42.64 PTS OR 1.40%

HANG SENG CLOSED UP 5.17 PTS OR .03%

2. Nikkei closed UP 140.32 [PTS OR 0.53%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 113.52/Euro RISES TO 0.96417

3b Japan 10 YR bond yield: RISES TO. +.247/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 144.32/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

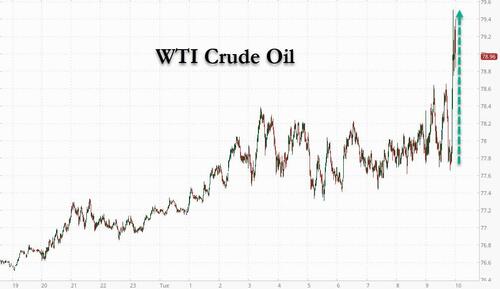

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.052%***/Italian 10 Yr bond yield FALLS to 4.511%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.24%…** DANGEROUS

3i Greek 10 year bond yield RISES TO 4.71//

3j Gold at $1637.50silver at: 18.68 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 9/100 roubles/dollar; ROUBLE AT 58.29//

3m oil into the 77 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 144.32DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9852– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9499well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

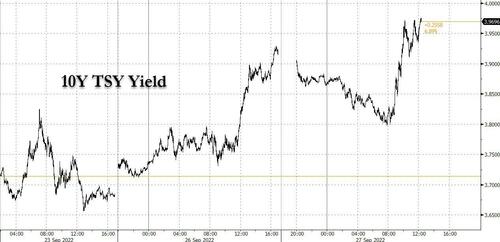

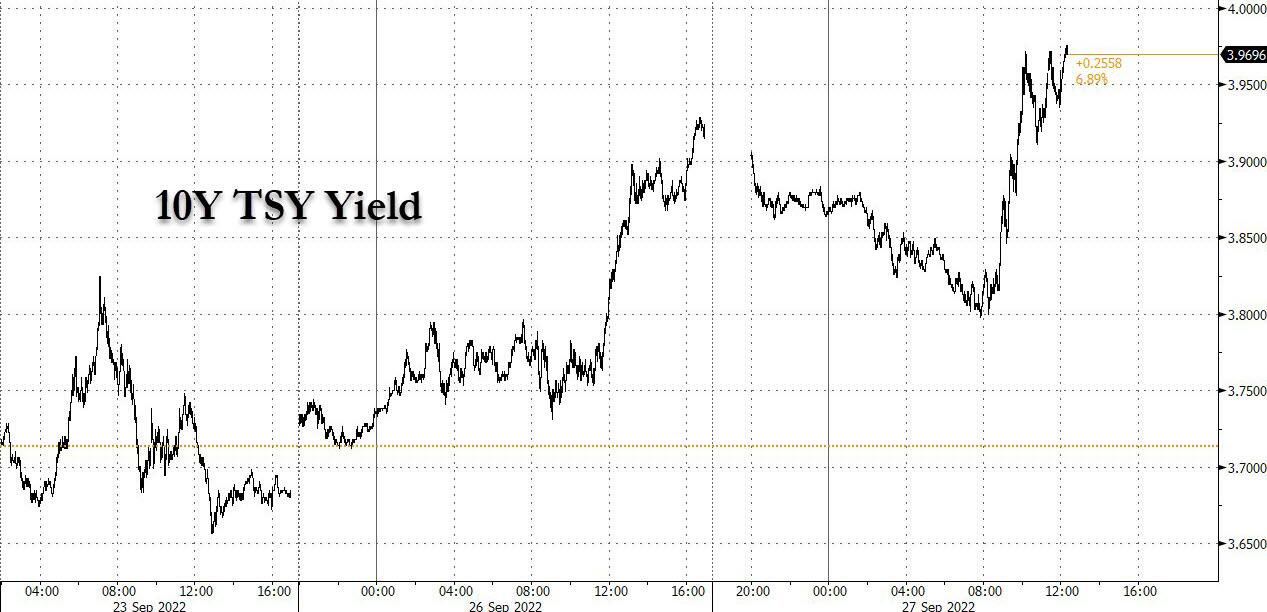

USA 10 YR BOND YIELD: 3.809 DOWN 7 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.685 DOWN 1 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

USA DOLLAR VS TURKISH LIRA: 18,48…GETTTING DANGEROUS

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Jump, Yields And Dollar Slide After Gundlach Says He’s A “Buyer” Of Treasuries

TUESDAY, SEP 27, 2022 – 07:58 AM

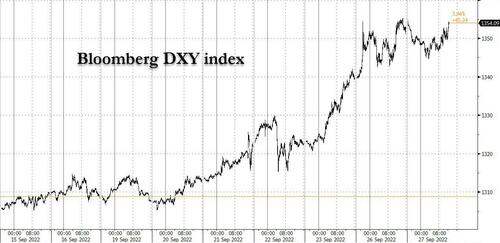

US equity futures and European stocks staged a solid rebound after the recent rout which saw the S&P close at a fresh 2022 low on Monday, as the dollar finally weakened against all of G-10 peers, snapping a five-day gain of new record highs as Treasury yields fell and the pound rebounded from a record low, even as (or perhaps because) Goldman Sachs and BlackRock soured on equities for the short term and Citigroup said bearish positioning continues to rise. As of 715am, S&P Futures traded 43 points, or 1.2% higher, at 3,714 while Nasdaq futures were 1.3% higher. 10Y yields dropped to 3.80% after rising above 3.90% late on Monday.

The dollar gauge dipped but held near the record high set Monday, when a barrage of Fed officials repeated hawkish comments on policy. Meanwhile, European authorities are probing “unprecedented” damage to the Nord Stream pipeline system that transports Russian gas to the region. Benchmark European gas prices climbed as much as 12% on Tuesday, after four days of losses. Oil and gold also rose.

One potential catalyst for the bounce in risk sentiment, and drop in TSY yields, was a tweet from bond king Jeff Gundlach just after midnight EDT, in which we said that “the U.S. Treasury Bond market is rallying tonight. Been a long time. I have been a buyer recently.”

Which is good- it means that there’s at least one major investor who thinks the worst global bond rout in decades is creating a buying opportunity. Now if only all the others shared his sentiment. In any case, his contrarian position was enough to avoid 10Y yields surging above 4% tonight… it remains to be seen if this persists tomorrow and subsequently.

In premarket trading, tech giants such as Apple, Amazon.com and Alphabet advanced more than 1% in premarket trading as US index futures rebounded with Europe’s Stoxx 600. Here are some other notable premarket movers:

- Cryptocurrency-exposed shares rise in premarket trading, as Bitcoin jumped to breach the closely watched $20,000 level. MicroStrategy (MSTR US) +4.9%, Marathon Digital (MARA US) +5.8%, Hut 8 Mining (HUT US) +6.4%, Coinbase (COIN US) +5%, Riot Blockchain (RIOT US) +4.8%.

- Shares in 9 Meters Biopharma (NMTR US) jump as much as 40% in premarket trading, with Oppenheimer raising its price target on the biotech to a Street-high after the company reported data from a Phase 2 study of vurolenatide.

- US-listed Macau casino and China travel stocks are on track to rise for a second day, after those listed in Hong Kong extended gains on growing optimism in a tourism revival. Wynn Resorts (WYNN US) +1.8% and Melco Resorts (MLCO US) +2% in premarket trading.

- Grab (GRAB US) stock climbed 1.1% in premarket trading after the Southeast Asian internet giant said it pursues profitability in 2024, though expects revenue to slow significantly.

- Keep an eye on Keurig Dr Pepper (KDP US) as Goldman Sachs downgraded the stock to neutral, saying that the company is still executing well in a tough environment, but the risk-reward seems more balanced from here.

- Keep an eye on Arcos Dorados (ARCO US) as the stock was initiated with an overweight rating at Barclays, with broker saying that the McDonald’s franchisee is solidly positioned amid headwinds.

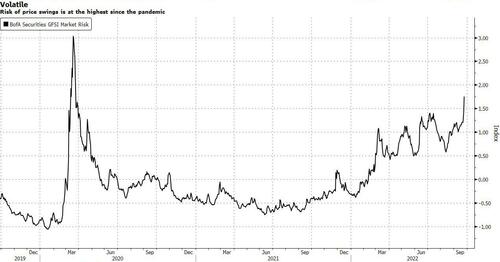

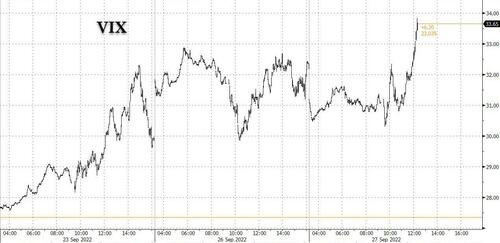

Even as dip buyers emerged on Tuesday, global markets remained on edge as investors braced for a heightened risk of global recession. Volatility across markets was also reflected by the risk of future price swings, which reached the highest since the beginning of the pandemic, as shown by a Bank of America index.

Despite today’s bounce, the turmoil in markets shows little sign of turning Fed officials away from hawkish rhetoric. Boston Fed President Susan Collins and her Cleveland counterpart Loretta Mester said additional tightening is needed to rein in stubbornly high inflation and Atlanta Fed President Raphael Bostic also said the central bank still has a ways to go to control inflation.

“The market is pricing in some Fed increases, but we’re a bit worried that it might not be pricing in everything,” Laila Pence, president of Pence Wealth Management, said on Bloomberg Television. “Everyone is nervous.”

In Europe, the Stoxx 50 rose 0.6%, also bouncing after a rout, but traded off session highs as risk sentiment took a small hit after Nord Stream said the damage to the Russian gas pipeline is unprecedented, even as the pullback of the dollar gave some relief to assets. Travel, miners and tech are the strongest performing sectors. Italy’s FTSE MIB index fell 0.9% as of 11:16am, the worst performer among major European stock markets on Tuesday, with utilities and financials dragging the benchmark lower. The BTP-bund spread widens as much as 256bps, climbing above 250bps for the first time since May 2020. FTSE MIB had climbed as much as 1.4% in early trading. Worst performers on the index include: Terna -3.9%, Enel -3.4%, FinecoBank -3.3%, Saipem -2.8%, A2A -2.3%, Generali -2.2%, Intesa Sanpaolo -1.3%. UK markets clawed back some losses after a meltdown triggered by the government’s fiscal plan late last week. Here are some of the biggest European movers this morning:

- Nexi shares jump as much as 8%, the largest intraday advance in two months, after announcing net revenue and Ebitda growth goals for 2021-2025, which analysts said are ahead of or meet their expectations. Payment peers Adyen, Worldline and Network International also rise

- Biffa shares rise as much as 29% after investment firm ECP agrees to buy the UK waste-management company at 410p/share in cash

- SSP rises as much as 6.8% after the company boosted its full-year forecast, which Goodbody says should provide some near-term relief

- Quadient gains as much as 6.8% after the French postal- and document-services company reported 1H results that Portzamparc says show recovery

- Vitrolife drops as much as 20%, its largest intra-day decline since February, as Bank of America-Merrill Lynch initiates coverage calling the share overvalued, while spotting risks on the horizon

- Close Brothers shares decline as much as 8.1% after the financial services group reported adjusted operating profit for the full year that missed the average analyst estimate

- Akzo Nobel shares slide as much as 3.3% after the company reported preliminary 3Q adjusted operating profit that was well below estimates. Analysts notied that raw material cost inflation is expected to peak in 3Q

- Real estate was the worst performing European equity sector for a second day, dragged down by UK and Swedish property stocks. Segro -3.3%, Rightmove -5.1%, LXI REIT -3.3% and Samhallsbyggnadsbolaget i Norden -4.7%, Fabege -2.9%, Castellum -2.5%

Earlier in the session, Asian stocks rose from their lowest level in more than two years as equities in China and Japan advanced. The MSCI Asia Pacific Index added as much as 0.5%, poised to snap four-days of losses. Consumer staples and materials led the measure higher as Meituan, BHP and Toyota gave the biggest boosts to the measure. Equities in mainland China were notable winners, with the CSI 300 Index finishing 1.5% higher. Several big mutual funds and brokers were asked by Chinese regulators to refrain from large sales of stocks before the party congress in October, Bloomberg News reported. The Hang Seng Tech Index gained, erasing a loss of as much as 1.8%. The region’s stocks suffered days of selling after the Federal Reserve last week signaled more interest-rate hikes are in store, further strengthening the dollar and tightening global finances. Asian currencies tumbled, raising capital outflow risks and driving key equity gauges lower.

“Although we could see quant traders likely to swoop and trigger a rally, we emphasize that headwinds still remain in place,” including higher bond yields as well as the dollar, Saxo Capital Markets analysts including Redmond Wong wrote in a note. Japan’s stocks were among Tuesday’s biggest gainers as the yen weakened, bolstering the profit outlook for exporters. The Philippine benchmark fell to a two-year low, approaching a bear market, as trading resumed after one-day closure due to a typhoon. Key stock gauges in Hong Kong, China, South Korea, Taiwan and Vietnam are all down more than 20% so far this year, along with MSCI’s broadest regional measure. Tech-heavy markets have suffered as rising rates and a stronger dollar fan valuation concerns. Taiwan will evaluate stock-stabilizing measures cautiously as they are a double-edged sword that may help prices but hurt liquidity, the Financial Supervisory Commission chief said Tuesday.

Japanese equities climbed, rebounding from a three day drop, as a weaker yen boosted shares of exporters. The Topix rose 0.5% to close at 1,873.01, while the Nikkei advanced 0.5% to 26,571.87. The yen strengthened slightly after dropping 1% against the dollar Monday. Toyota Motor Corp. contributed the most to the Topix gain, increasing 1.2%. Out of 2,169 stocks in the index, 1,245 rose and 785 fell, while 139 were unchanged. “As long as US stocks don’t fall drastically, Japanese shares have shown an ability to be resilient,” said Hideyuki Suzuki, a general manager at SBI Securities. Japanese stocks have been supported by low valuations as well as Prime Minister Kishida’s moves to raise the limit for tax breaks on individual investment and relax border controls.

In Australia, the S&P/ASX 200 index rose 0.4% to close at 6,496.20, boosted by gains in mining and energy stocks. In New Zealand, the S&P/NZX 50 index fell 1.9% to 11,214.49.

In FX, the Bloomberg Dollar Spot Index retreats as all G-10 peers advance and as treasuries gained led by the belly as Fed tightening wagers were pared.

- The pound bounced, reclaiming 1.08 against the dollar and trading around where it closed Friday against both the euro and dollar, with measures of implied volatility remaining elevated as investors brace for more swings. Focus on possible action from policy makers and a speech by the Bank of England’s Huw Pill. Overnight volatility in cable traded earlier at 44.76%, its strongest level since March 2020. Gilts traded higher led by the front-end of the curve as traders trimmed BOE tightening bets amid UK currency gains

- The euro pared some gains against the US dollar, after Nord Stream reported “unprecedented” damage to the Russian gas pipeline. The common currency still traded above $0.96. Italian bonds extended their underperformance against German peers to a third day, the longest streak since the beginning of the month, as investors continued to digest the right-wing coalition’s election win

- Japan’s yield curve bear steepens as the BOJ’s unscheduled bond purchases are dwarfed by a deepening selloff in global debt. Japan’s 20-year bond yields rose to the highest level since 2015 as global debt markets come under increasing pressure due to expectations of further monetary-policy tightening. The yen rises for the first time in three days as the dollar weakens. Forget the risk of intervention by Japanese officials in the spot market. Yen traders are more concerned over a potential pivot by the Bank of Japan. The volatility term structures in the euro, the pound and the Swiss franc are fully inverted whereas the one in the yen peaks on the two-month tenor

In rates, treasuries rebounded in Asian trading after 10-year yields jumped the most since March 2020 on Monday. Japan 10-year yields edge up to 0.25%, the top of BOJ’s tolerated range, prompting the BOJ to enact another unscheduled bond-buying operation. 10-Year Treasury yields were down 11bps to 3.81%; the 10-year yield surged 24bps Monday, the most since March 2020, after poor demand for a two-year auction triggered renewed selling across the curve. One catalyst for the move was Doubleline’s Gundlach who tweeted that he has been a recent buyer. Still, the selloff is seeing few signs of ending, with UK notes losing a stunning 27% this year. The “bond vigilantes” are back in the saddle, according to the veteran economist credited with coining the term in the 1980s. Gilt yields slid following the biggest-ever surge and the pound rose about 1% after falling to a record low. Traders remained wary of the risk that the currency could slump to parity with the dollar after the Bank of England indicated it may not act before November to stem the rout. Peripheral spreads widen to Germany with 10y BTP/bund widening 10.3bps to 254.1bps.

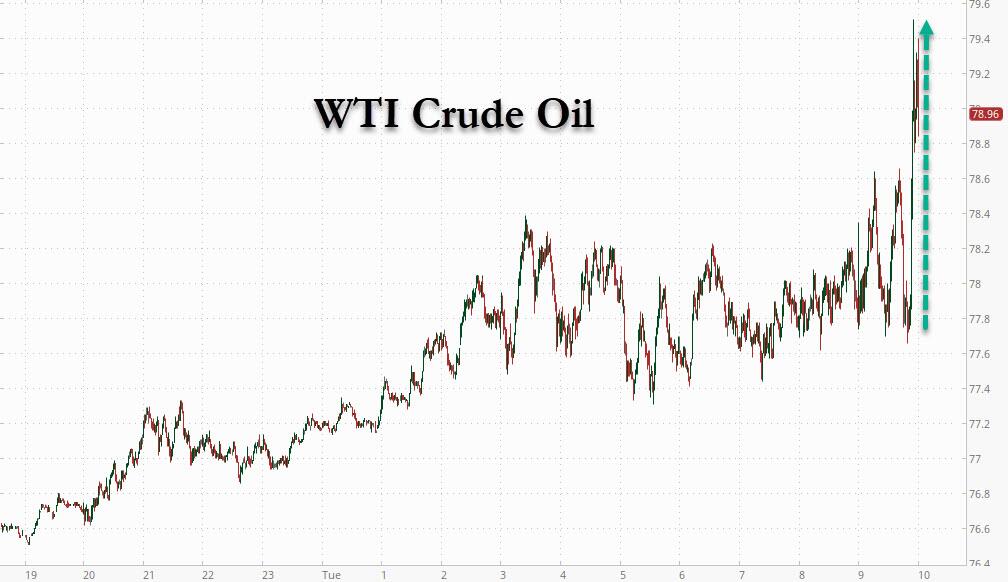

In commodities, WTI climbed 1.6% to below $78, within Monday’s range. Spot gold rises roughly $15 to trade near $1,638/oz. There has been focus this morning on Nord Stream 1 & 2 damage with the cause currently unknown and fresh reporting around a potential EU gas price cap, to be discussed on Friday. The German network regulator later stated that it did not know the cause of the Nord Stream 1 pressure drop but didn’t see any impact on the security of supply, according to Reuters. At least 12 countries have signed a letter which calls on the EU to propose a gas price cap at this week’s Energy Ministers meeting via Politico citing a letter; proposals will be discussed on Friday, September 30th. A completely clueless President Biden said companies running gas stations need to bring down gasoline prices at the pump now,. BP (BP/ LN) halted production and evacuated staff at two offshore oil platforms in the US Gulf of Mexico ahead of Hurricane Ian. Intercontinental Exchange is reportedly planning to accept allowances generated by the carbon market as collateral in its European futures market to ease the pressure on utilities and traders amid the energy crisis, according to FT.

Looking at the day ahead, data releases from the US include the Conference Board’s consumer confidence for September, the preliminary reading for durable goods orders and core capital goods orders for August, the FHFA house price index for July, and new home sales for August. Meanwhile in the Euro Area, we’ll get the M3 money supply for August. Central bank speakers include Fed Chair Powell, as well as the Fed’s Evans, Bullard and Kashkari, ECB Vice President de Guindos, the ECB’s Centeno, Villeroy and Panetta, as well as BoE chief economist Pill.

Market Snapshot

- S&P 500 futures up 1.2% to 3,715.75

- STOXX Europe 600 up 0.8% to 391.77

- MXAP up 0.5% to 142.53

- MXAPJ up 0.4% to 464.38

- Nikkei up 0.5% to 26,571.87

- Topix up 0.5% to 1,873.01

- Hang Seng Index little changed at 17,860.31

- Shanghai Composite up 1.4% to 3,093.86

- Sensex up 0.4% to 57,399.07

- Australia S&P/ASX 200 up 0.4% to 6,496.16

- Kospi up 0.1% to 2,223.86

- German 10Y yield little changed at 2.11%

- Euro up 0.3% to $0.9637

- Brent Futures up 1.8% to $85.61/bbl

- Gold spot up 0.9% to $1,637.52

- U.S. Dollar Index down 0.43% to 113.62

Top Overnight News from Bloomberg

- Options traders haven’t been this busy since the pandemic mayhem in March 2020, according to data from the Depository Trust & Clearing Corporation

- Speculators are betting the UK’s pound will slide to a level that was virtually unthinkable in recent decades: $1 or less. After the pound tumbled as low as $1.0350 Monday, the weakest on record, options markets show traders expect it to keep falling

- The worst bond selloff in decades is seeing few signs of ending, with UK notes losing a stunning 27% this year, as central banks battle to stamp out the strongest inflationary pressures in decades

- “Bond vigilantes” are back in the saddle and riding high again having mostly been on hiatus since the early 1990s, according to the veteran economist credited with coining the term in the 1980s

- Traders are bracing for more pushback from China’s central bank as the yuan approaches the lowest level in 14 years. The onshore yuan has lost about 4% over the past month, trading within 1% of 7.2 per dollar, a level it hasn’t reached since 2008

- China’s shaky recovery continued in September, with a pickup in car and homes sales in the biggest cities compensating for weaker global demand and falling business confidence

- Japan looks to have spent more supporting the yen on Thursday alone than it did during the entire period of boosting its currency during the Asian financial crisis in 1998

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly higher in which the majority of indices shrugged off the negative lead from Wall St as the overhang from the recent FX turmoil dissipated but with the recovery somewhat contained by the higher yield environment. ASX 200 eked slight gains led by the commodity-related sectors as they atoned for yesterday’s underperformance. Nikkei 225 gained after recent comments from BoJ Governor Kuroda who reaffirmed his commitment to maintaining easy monetary policy, while the central bank also announced unscheduled purchase operations. Hang Seng and Shanghai Comp were mixed with the mainland underpinned amid reports that China is to ramp up financial support for new types of infrastructure, while the PBoC conducted its largest cash injection in seven months ahead of next week’s National Day holiday. However, growth concerns lingered with the World Bank forecasting China’s economic growth to lag behind the rest of Asia for the first time since 1990. India will likely be included in the JP Morgan Emerging Market Index early 2023, according to Reuters sources.

Top Asian News

- India Unwilling to Relent on Tax Stance for Debt Index Inclusion

- Australia’s Pinnacle Looks for Deals in Stressed UK and Europe

- Macau Casino, China Travel Stocks in US Extend Gains

- India Mulls $2.5 Billion Aid to Manufacture Grid-Scale Batteries

- Geely’s EV Truck Farizon Said to Seek $300 Million Funding Round

- Jinke Smart Services Jumps 33% After Boyu’s Share Purchase Offer

- TikTok Steers Its Charm Offensive Around Loudest Critics in D.C.

European bourses are mixed, Euro Stoxx 50 +0.2%, as the complex wanes from best levels ahead of a packed Central Bank agenda. Catalysts behind the pullback have been sparse with newsflow focused on geopols/energy; though, GS and BlackRock are turning more bearings on equities in the short-term. Stateside, futures remain in positive territory though have similarly drifted from initial peaks, ES +0.8%.

Top European News

- Euro Pares Gain Versus Dollar After Nord Stream Comments

- Odey Says Pound Still ‘Vulnerable’ as His Hedge Fund Soars 140%

- Kwarteng Heads for a Difficult Meeting With London’s Top Bankers

- Deutsche Bank’s Chief Economist Sees ‘Painful’ UK Recession

- UK Labour Surges to Record 17-point Poll Lead Amid Pound Selloff

- UniCredit Gains as JPMorgan Upgrades on Attractive Risk Reward

- Akzo Nobel Reverses Drop as Analysts See Long-Term Opportunity

Central Banks

- Fed’s Mester (2022, 2024 voter) said further rate hikes will be needed and will need a restrictive stance for some time, while she added it can be better to act more aggressively in an uncertain environment and that pre-emptive action can prevent the worst-case outcome. Mester said this is the time to be decisive and the Fed policy rate may be right below the restrictive level, as well as noted that they are not at neutral yet and need to get above that. Furthermore, Mester said rates are not coming down next year and that at some point they would have done enough and it will be a case of balancing risk at some point, but this is not that moment, according to Reuters.

- Fed’s Evans (non-voter, departing) says US inflation is high, getting it under control is the number one job, via CNBC; Real rate could be around 1.5% by next spring, in Evans’ judgement. By this period, can perhaps sit and wait on rates; end-2022 consensus view on rates is 4.25-4.50%. Tougher rate environment is here for a while.

Geopolitics

- Nord Stream says it has detected damage at three lines of the Nord Stream gas pipeline system; damages are unprecedented and is impossible to estimate when gas transportation infrastructure will be restored. Subsequently, Russia’s Kremlin said pipeline damage is a very concerning development; cannot rule out sabotage.

- Russian Head of Security Council says Russia has the right to use nuclear weapons if necessary, says it is not a bluff, via Reuters.

- US State Department Spokesman Price said the US does not see an Iran deal coming together soon.

FX

- DXY has eased from newly formed peaks as yields ease from highs and broader sentiment stages a modest recovery.

- A pullback that is benefitting GBP in particular, with Cable outperforming after recent pressure as the Pound manages to gain some composure ahead of BoE’s Pill.

- Similarly, NZD is among the best performers following RBNZ Governor Orr stating that further tightening is likely required.

- More broadly, G10 peers are taking advantage of the USD’s pullback though the magnitude of this does differ somewhat; on the flip side, Yuan remains under pressure following a weaker fix, soft data and World Bank updates.

Fixed Income

- Core benchmarks are mixed and feature ‘outperformance’ in Gilts after yesterday’s heft losses with the morning’s I/L relatively robust.

- More broadly, Bunds initially waned a touch from a 138.75 best, though have reverted back towards the top-end of parameters as broader sentiment slips.

- Stateside, USTs are holding firm and similarly at the top-end of ranges ahead of numerous Fed officials and 5yr issuance.

- UK DMO intends to hold 19 Gilt auctions in October through December, now plans three syndications for remainder of year.

Commodities

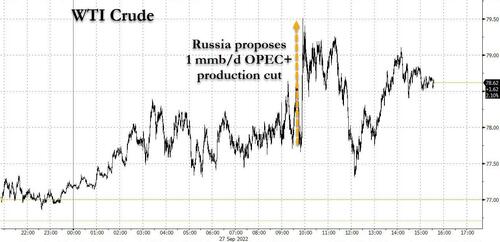

- Crude benchmarks have been meandering higher throughout the session, after yesterday’s lower settlement.

- Focus on Nord Stream 1 & 2 damage with the cause currently unknown and fresh reporting around a potential EU gas price cap, to be discussed on Friday.

- At least 12 countries have signed a letter which calls on the EU to propose a gas price cap at this week’s Energy Ministers meeting via Politico citing a letter; proposals will be discussed on Friday, September 30th

- US President Biden said companies running gas stations need to bring down gasoline prices at the pump now, according to Reuters.

- German network regulator later stated that it did not know the cause of the Nord Stream 1 pressure drop but didn’t see any impact on the security of supply, according to Reuters.

- BP (BP/ LN) halted production and evacuated staff at two offshore oil platforms in the US Gulf of Mexico ahead of Hurricane Ian.

- Intercontinental Exchange is reportedly planning to accept allowances generated by the carbon market as collateral in its European futures market to ease the pressure on utilities and traders amid the energy crisis, according to FT.

- Hurricane Ian has strengthened to a Category 3 storm (major hurricane), via NHC; expected to strengthen further today, has made landfall.

- UBS says that only a production cut by OPEC+ can break the negative momentum within oil in the short-term, adding that to provide a stronger floor in oil prices, Saudi would need to make extra voluntary cuts.

- Metals are deriving support from the USDs relative pullback, though spot gold for instance remains within yesterday’s parameters.

US Event Calendar

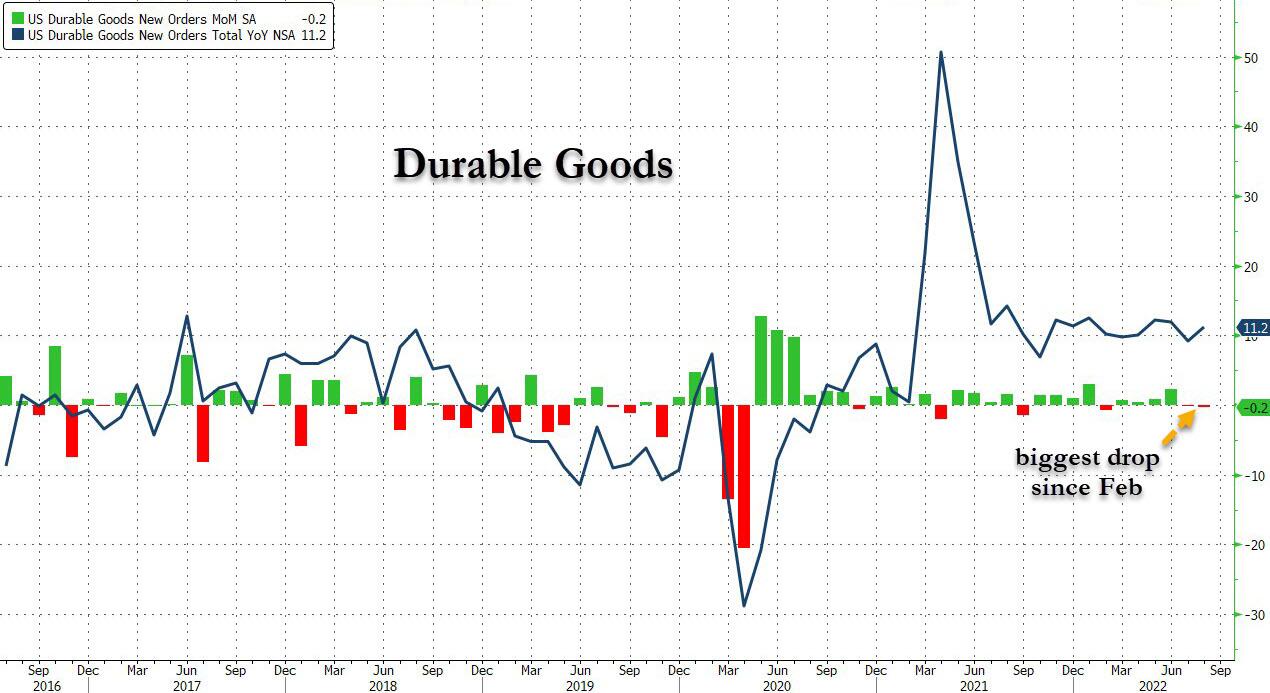

- 08:30: Aug. Durable Goods Orders, est. -0.3%, prior -0.1%;

- Aug. -Less Transportation, est. 0.2%, prior 0.2%

- 08:30: Aug. Cap Goods Orders Nondef Ex Air, est. 0.2%, prior 0.3%

- Aug. Cap Goods Ship Nondef Ex Air, est. 0.3%, prior 0.5%

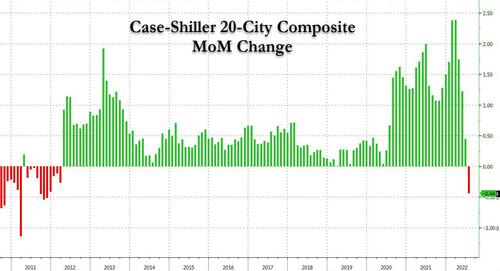

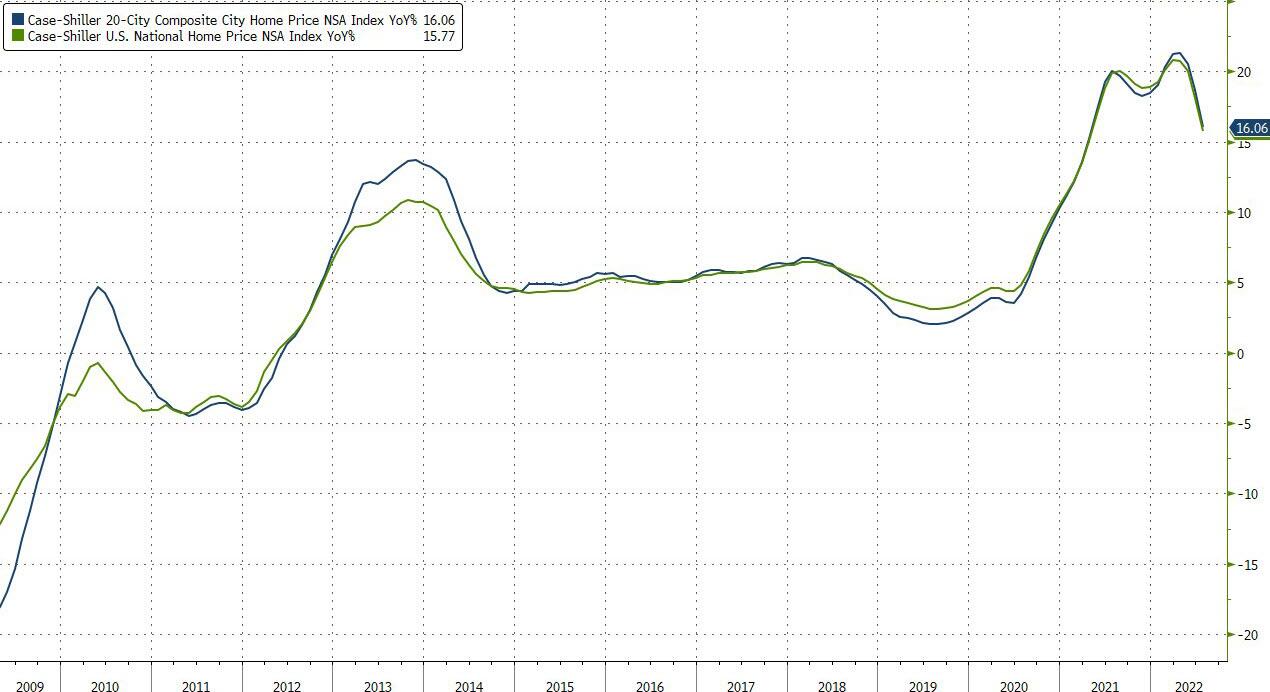

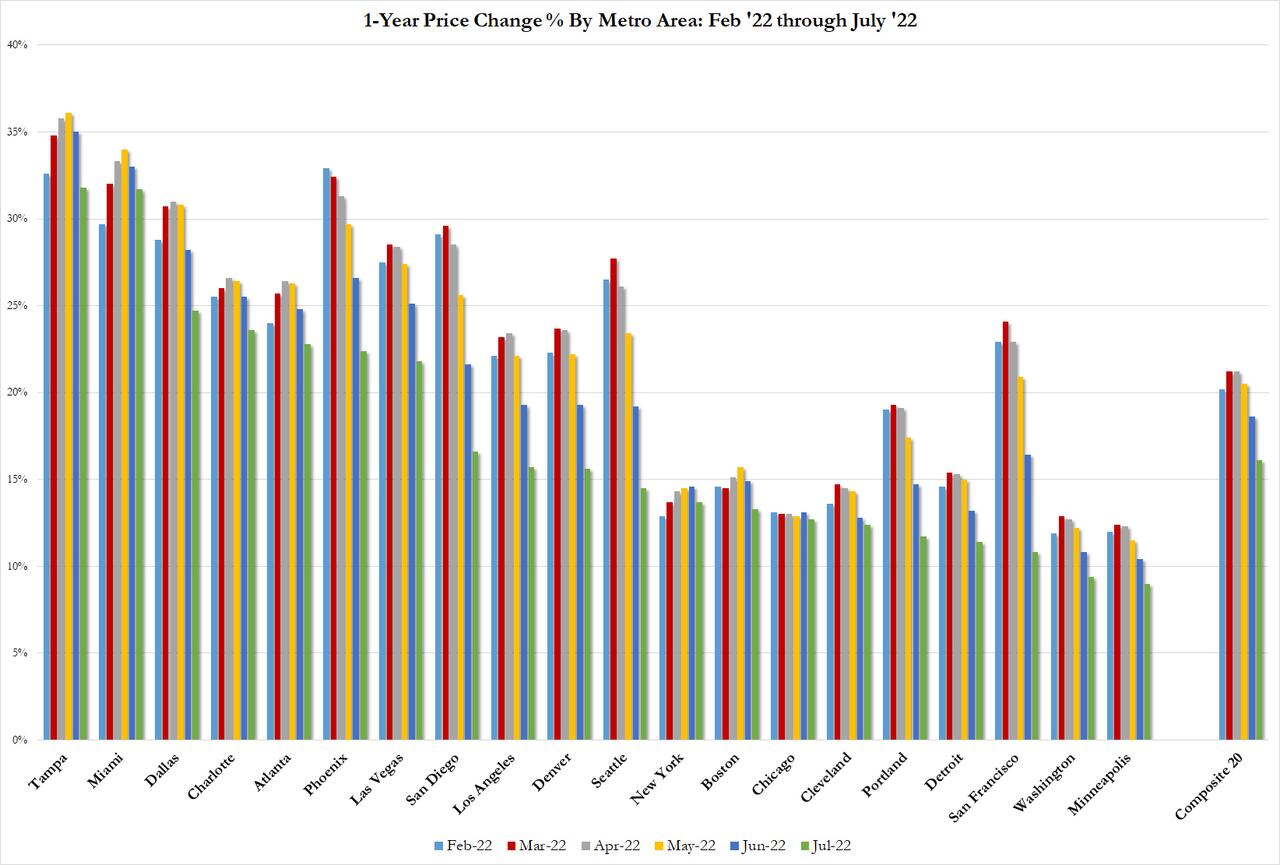

- 09:00: July S&P CS Composite-20 YoY, est. 17.10%, prior 18.65%

- July S&P/CS 20 City MoM SA, est. 0.20%, prior 0.44%

- July S&P/Case-Shiller US HPI YoY, prior 17.96%

- 10:00: Sept. Conf. Board Consumer Confidence, est. 104.5, prior 103.2

- Sept. Conf. Board Expectations, prior 75.1

- Sept. Conf. Board Present Situation, prior 145.4

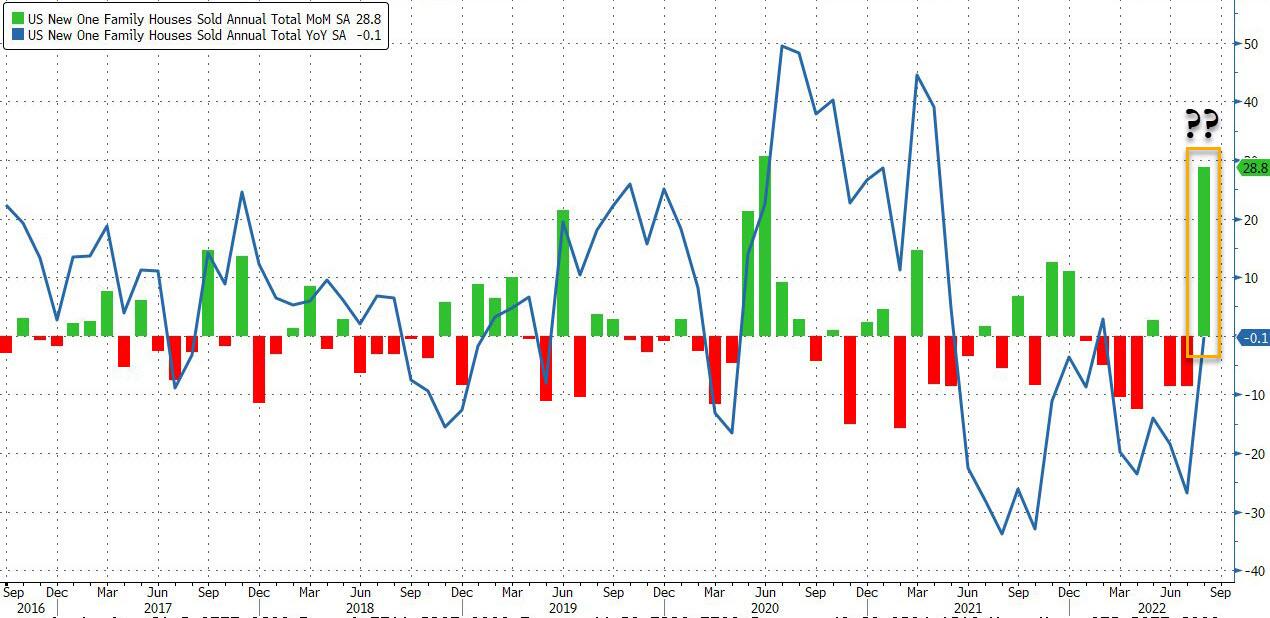

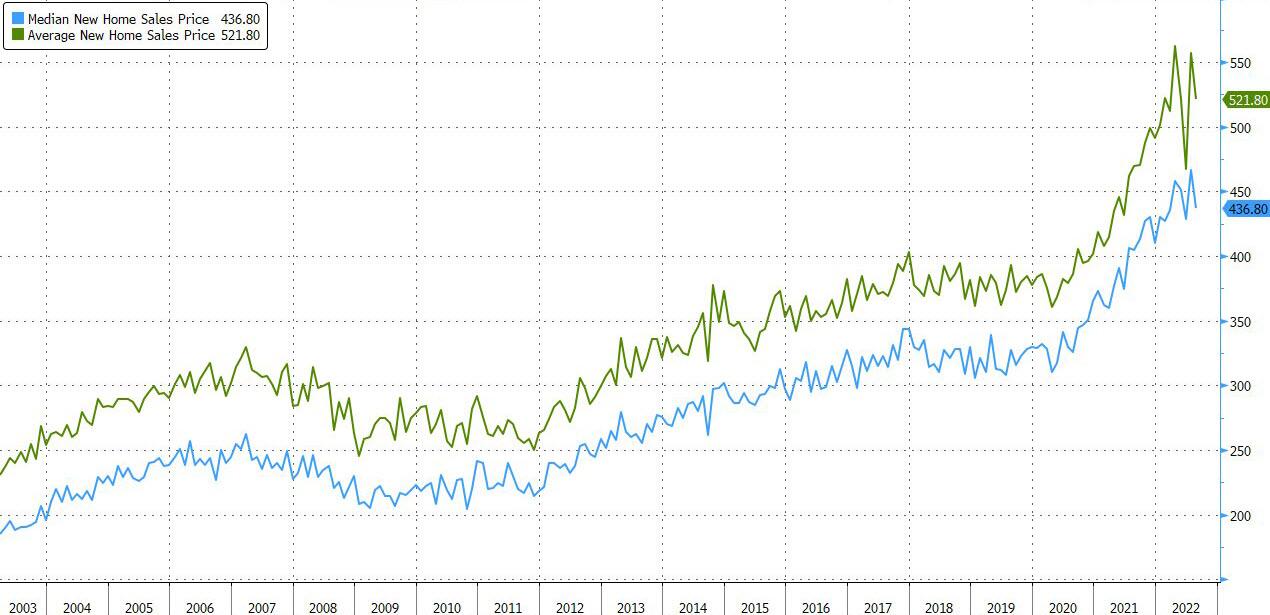

- 10:00: Aug. New Home Sales, est. 500,000, prior 511,000

- Aug. New Home Sales MoM, est. -2.1%, prior -12.6%

- 10:00: Sept. Richmond Fed Index, est. -10, prior -8

DB’s Jim Reid concludes the overnight wrap

Yesterday I published my annual long-term study. It contains over 200 years of nominal and real returns across global bonds, equities, commodities and other assets. We also look at structural themes and this year we put 2022’s terrible year for financial markets into some historical context and try to understand “How we got here and where we’re going”. This year we have also launched it as a presentation pack simultaneously for those who want to flick through the broad themes. You can see the link to this in the executive summary of the full report which you can find here.

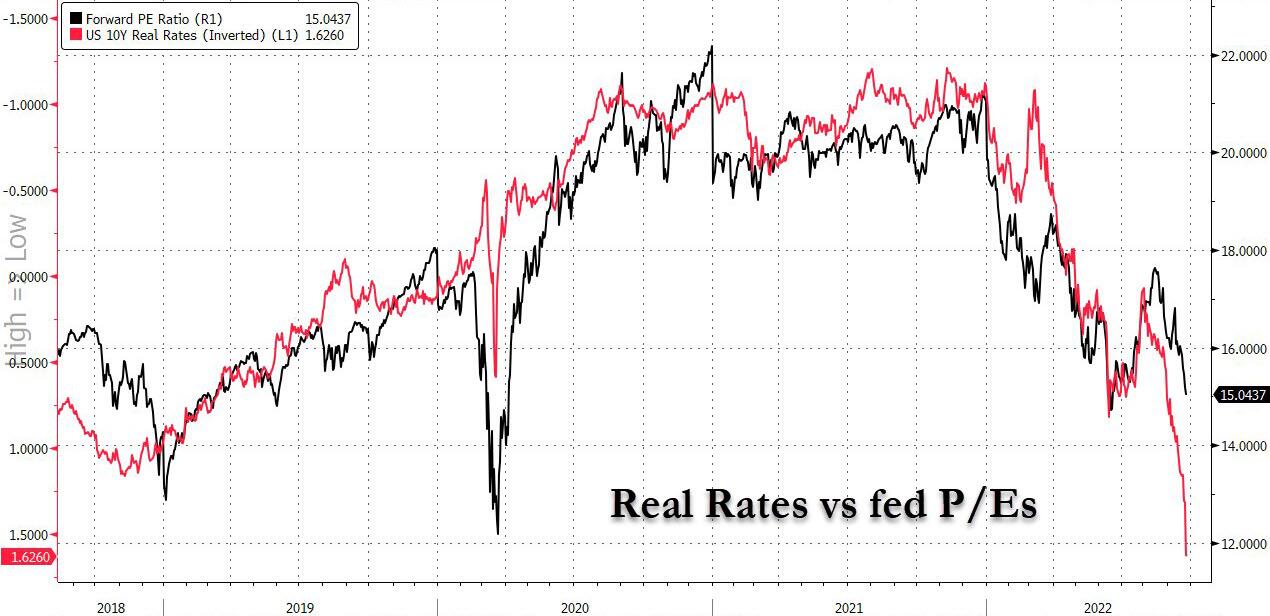

One of the key themes I pick up in the report is that we’re in the first global bear market for government bonds in over 70 years, using the yardstick of a -20% decline from their recent peak. This has also been a disaster for split bond-equity portfolios given the equity selloff as well this year.

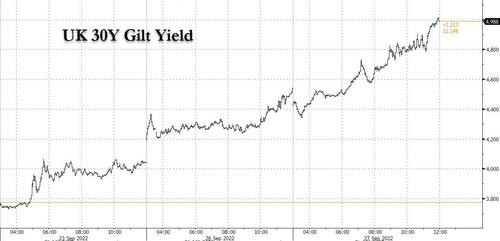

When it comes to the last 24 hours, UK assets have remained at the eye of the storm as the negative reaction to the government’s mini-budget on Friday continued. The country’s government bonds were completely routed for a second day, with yields on 5yr gilts up by +47.8bps to a post-2008 high of 4.52%. Bear in mind that follows on from the +51.0bps move on Friday, which itself was the largest daily rise since January 1985 when there was a 200bps rate hike, so these are not the sort of moves we’re used to seeing every day. Indeed as I showed in an extra CoTD last night (link here) this is now the largest 5 day rolling move for 5yr gilts since our daily data starts in 1979 and the largest 5 day rolling move in 10yr gilts since 1976 (around the IMF loan) and the 5th largest such move since our daily data starts in 1934 (other 4 all around this mid-1970s period). So the global fixed income VAR shocks of the last 12 months keep on coming.

Furthermore, the gap between UK 10yr gilt yields and German 10yr bunds widened to more than 212bps by the close yesterday, which is the biggest spread in available Bloomberg data going back to the early 1990s. We’ll have a look at longer data later.

During yesterday’s session there was much speculation as to whether there might be an intervention or perhaps even an emergency intermeeting hike from the BoE. But it wasn’t until just before European markets closed that we finally heard from the UK Treasury, who put out a statement with a number of lines that looked designed to ease investors’ fears. In particular, there was confirmation that Chancellor Kwarteng would be setting out a “Medium-Term Fiscal Plan” on November 23, which would include details of the government’s fiscal rules and ensure that the debt-to-GDP ratio falls in the medium term. Furthermore, there would be a full forecast from the Office for Budget Responsibility (the government’s independent fiscal watchdog) alongside that fiscal plan in November 23. That contrasts with Friday’s mini-budget, where there wasn’t an independent forecast alongside the announcements.

Shortly after the Treasury statement, BoE Governor Bailey released his own statement, in which he said that the Monetary Policy Committee would “make a full assessment at its next scheduled meeting of the impact on demand and inflation from the Government’s announcements, and the fall in sterling, and act accordingly.” It further said that they would “not hesitate to change interest rates as necessary to return inflation to the 2% target sustainable in the medium term”. But in spite of those two statements, sterling actually lost ground afterwards since investors slashed the odds of an emergency inter-meeting hike. After hitting an all time low in Asia at $1.0392 it rallied to just above $1.09 by early afternoon and slightly higher on a hugely volatile day. After Bailey’s statement, it fell from just over $1.08 to just beneath $1.07, where it ended the day (up at $1.078 in Asia). In the meantime, the selloff in gilts resumed and they hit their lows for the session around the close. Looking forward, markets are still expecting an incredibly fast pace rate hikes ahead, with around 150bps priced in by the time of the next policy meeting on November 3, albeit that was down from 200bps at one point in the day.