by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSE: DOWN $17.15 to $1627.15

SILVER PRICE CLOSE: DOWN 43 cents to $18.46

Access prices: closes

Gold ACCESS CLOSE 1623.70

Silver ACCESS CLOSE: 18.37

Bitcoin morning price: $18,902 UP 130

Bitcoin: afternoon price: $19,138 UP 366

Platinum price closing DOWN $8.90 AT $855.10

Palladium price; closing DOWN $14.85 at $2056.55

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,645.300000000 USD

INTENT DATE: 09/23/2022 DELIVERY DATE: 09/27/2022

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 1

624 H BOFA SECURITIES 8

657 C MORGAN STANLEY 12

661 C JP MORGAN 1128 473

686 C STONEX FINANCIA 1

690 C ABN AMRO 61

732 C RBC CAP MARKETS 19

880 H CITIGROUP 770

905 C ADM 33

TOTAL: 1,253 1,253

MONTH TO DATE: 10,758

GOLD: NUMBER OF NOTICES FILED FOR SEPT CONTRACT:

1253 NOTICES FOR 125,300 OZ //3.897 TONNES

total notices so far: 10,758 contracts for 1,075,800 oz (33.4618 tonnes)

SILVER NOTICES: 52 NOTICES FILED FOR 260,000 OZ/

total number of notices filed so far this month 6643 : for 33,215,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $17.15

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: //// A WITHDRAWAL OF 2.90 TONNES FROM THE GLD/

INVENTORY RESTS AT 947.23 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 43 CENTS

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF OF 0.737 MILLION OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 481.194 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A FAIR SIZED 579 CONTRACTS TO 131,511 AND FURTHER FORM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE FAIR LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.68 LOSS IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.68) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPEC SILVER LONGS AS WE HAD A TINY GAIN OF 1 CONTRACTS ON OUR TWO EXCHANGES. WE DID HAVE STRONG SILVER SHORT COVERING. THE SPECS ARE FLEEING AS FAST AS THEIR LITTLE FEET WILL CARRY THEM.

WE MUST HAVE HAD:

I) STRONG SPECULATOR SHORT COVERING ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 60,000 OZ QUEUE JUMP / // V) FAIR SIZED COMEX OI LOSS/(//CONSIDERABLE SPEC LIQUIDATION/)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: +16

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 17 days, total 13,335 contracts: 66.675 million oz OR 3.922 MILLION OZ PER DAY. (784 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 66.675 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 66.675 MILLION OZ///

RESULT: WE HAD A FAIR SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 579 WITH OUR $0.68 LOSS IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 580 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /GOOD BANKER ADDITIONS A// CONSIDERABLE NET SPEC SHORT COVERINGS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 60,000 OZ QUEUE JUMP // .. WE HAD A TINY SIZED GAIN OF 1 OI CONTRACTS ON THE TWO EXCHANGES FOR 0.005MILLION OZ AS..THE SPECS STILL ARE BEING SENT TO THE SLAUGHTER HOUSE.

WE HAD 52 NOTICE(S) FILED TODAY FOR 260,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

WE HAVE 4 MORE READING DAYS BEFORE FIRST DAY NOTICE

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1747 CONTRACTS TO 467,631 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED +91 CONTRACTS.

.

THE FAIR SIZED INCREASE IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $24.60//COMEX GOLD TRADING/FRIDAY / WE MUST HAVE HAD MAJOR SPECULATOR SHORT COVERINGS ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND //CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 97,900 OZ //NEW STANDING 33.844 TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S)

YET ALL OF..THIS HAPPENED WITH OUR FALL IN PRICE OF $24.6 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 6123 OI CONTRACTS 19.095 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4376 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 467,631

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6123 CONTRACTS WITH 1747 CONTRACTS INCREASED AT THE COMEX AND 4376 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 6123 CONTRACTS OR 18.762 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4376) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (1747): TOTAL GAIN IN THE TWO EXCHANGES 6123 CONTRACTS. WE NO DOUBT HAD 1) CONSIDERABLE SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS/// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.409 TONNES FOLLOWED BY TODAY’S MONSTROUS QUEUE JUMP OF 97.900 oz. 3) ZERO LONG LIQUIDATION//// //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

49,244 CONTRACTS OR 4,924,400 OZ OR 153.17 TONNES 17 TRADING DAY(S) AND THUS AVERAGING: 2896 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES: 153.17 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 153.17/3550 x 100% TONNES 4.30% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 153.17 TONNES (SLIGHTLY RISING THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER,FELL BY A FAIR SIZED 579 CONTRACT OI TO 131,527 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 580 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 550 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 580 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 579 CONTRACTS AND ADD TO THE 580 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A TINY SIZED GAIN OF 1 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 0.005 MILLION OZ

OCCURRED DESPITE OUR STRONG LOSS IN PRICE OF $0.68

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)MONDAY MORNING// FRIDAY NIGHT

SHANGHAI CLOSED DOWN 37.14 PTS OR 1.20% //Hang Seng CLOSED DOWN 78.13 PTS OR 0.44% /The Nikkei closed DOWN 722.28 PTS OR 2.66% //Australia’s all ordinaires CLOSED DOWN 1.79% /Chinese yuan (ONSHORE) closed DOWN AT 7.1609//OFFSHORE CHINESE YUAN DOWN 7.1609// /Oil DOWN TO 78.20 dollars per barrel for WTI and BRENT AT 85.53 / Stocks in Europe OPENED ALL MIXED. ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1747 CONTRACTS TO 467,540 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED DESPITE OUR FALL IN PRICE OF $24.60 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (4376 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4376 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :4376 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4376 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED SIZED TOTAL OF 6123 CONTRACTS IN THAT 4376 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 1656 CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $24.60. WE ARE NOW WITNESSING THE SPECULATORS WHO HAVE BEEN MASSIVELY SHORT TRYING DESPERATELY TO COVER WHILE THE BANKERS WHO ARE LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (33.844),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 33.844 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $24.60) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 6123 CONTRACTS // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS TRIED TO COVER ON THEIR POSITIONS WITH SOME SUCCESS////// WE HAVE REGISTERED A STRONG GAIN OF 6032 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT. (33.844 TONNES)…

WE HAD +91 CONTRACTS COMEX TRADES. THESE WERE ADDED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 6123 CONTRACTS OR 612,300 OZ OR 19.045 TONNES

Estimated gold volume 209,391/// fair//

final gold volumes/yesterday 268,240/ fair

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 26

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 161,430.160 oz BRINKS JPMorgan 5000 kilobars JPM |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 1253 notice(s) 125,300 OZ 3.897 TONNES |

| No of oz to be served (notices) | 123 contracts 12300 oz 0.3826 TONNES |

| Total monthly oz gold served (contracts) so far this month | 10,758 notices 1,075,800 OZ 33.4618 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz customer withdrawals:

i) Out of Brinks 675.160 oz

ii) Out of JPMorgan: 160,755.000 oz

total: 161,430.160 oz

total in tonnes: 5.02 tonnes

Adjustments: 2

JPM/ customer to dealer: 96.453 oz

Brinks: dealer to customer; 10,655,857 0z

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 1376 contracts having GAINED 47 contracts .

We had 932 notices filed on FRIDAY so we gained a whopping 979 contracts or an additional 97900 oz

will stand for gold in this very non active delivery month of September. This queue jump is actually the Londoners exercising efp’s and tendering them to the banks

for the physical!

October LOST GAINED 150 contracts LOWERING TO 41,975. Oct is generally a poor active delivery month. It WILL change!! (Look for a dramatically large Oct. delivery month.)

WE HAVE 4 MORE READING DAYS BEFORE FIRST DAY NOTICE ( FRIDAY SEPT 30.2022)

November GAINED 439 contracts to stand at 439

December GAINED 596 contracts UP to 377,429

We had 1253 notice(s) filed today for 93200 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 1128 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1253 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 473 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (10,758) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 1376 CONTRACTS) minus the number of notices served upon today 1253 x 100 oz per contract equals 1,088,100 OZ OR 33.844 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (10,758) x 100 oz+ (1376) OI for the front month minus the number of notices served upon today (1253} x 100 oz} which equals 1,088,100 oz standing OR 33.844 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 33.844 TONNES (A HUMONGOUS STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,263,478.589 oz 70.40 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 26,617,971.010 OZ

TOTAL REGISTERED GOLD: 13,133,099.889 OZ (408.94 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 13,484,877.121 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,869.621. OZ (REG GOLD- PLEDGED GOLD) 338.83 tonnes//rapidly declining

END

SILVER/COMEX/SEPT 26

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 111,487.740 oz Brinks CNT Delaware |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 52 CONTRACT(S) 260,000 OZ) |

| No of oz to be served (notices) | 19 contracts (95,000 oz) |

| Total monthly oz silver served (contracts) | 6695 contracts 33,475,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

Total deposits: nil

JPMorgan has a total silver weight: 164.074 million oz/316.499million =51.80% of comex

Comex withdrawals: 3

i) Out of Brinks: 1,900.750 oz

ii)Out of CNT 107,587,790 oz

iii)Out of Delaware: 200.200 oz

total withdrawals: 111,487.750 oz

adjustments: 4// with 1 customer to dealer

i) out of HSBC 10,402.800 o

3 DEALER TO CUSTOMER:

i) Brinks 14,991.530 oz

ii) Loomis 5001.560 oz

iii) Out of Manfra: 34,728.150 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 43.590 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 316.610 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF SEPT OI: 71 CONTRACTS HAVING LOST 36 CONTRACTS. WE HAD

48 CONTRACTS SERVED ON FRIDAY SO WE GAINED 12 CONTRACTS OR AN ADDITIONAL

60,000 OZ WILL STAND FOR METAL IN THIS VERY ACTIVE MONTH OF SEPT.

WE WILL GAIN IN TOTAL SILVER STANDING EACH TRADING DAY UNTIL THE END OF THE MONTH

(CONTINUAL QUEUE JUMPING BY OUR BANKERS SEARCHING FOR SILVER METAL)

OCTOBER LOST 36 CONTRACTS TO STAND AT 420 CONTACTS.

NOVEMBER LOST 2 CONTRACTS TO STAND AT 148

DECEMBER SAW A LOSS OF 527 CONTRACTS DOWN TO 115,937

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 52 for 260,000 oz

Comex volumes:77,547// est. volume today// good

Comex volume: confirmed yesterday: 84,973 contracts ( good)

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 6695 x 5,000 oz = 33,475,000 oz

to which we add the difference between the open interest for the front month of SEPT(71) and the number of notices served upon today 52 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT./2022 contract month: 6,695 (notices served so far) x 5000 oz + OI for front month of SEPT (71) – number of notices served upon today (52) x 5000 oz of silver standing for the SEPT contract month equates 33,570,000 oz. .

We have an inventory of 43.590 million oz of registered silver at the comex so Sept delivery of 33.570 MILLION OZ represents 77.01% of that category of silver.

If we add August’s final delivery (to Sept) for silver at 5.51 million oz, we have a total of 39.08 million oz delivered upon with a REGISTERED INVENTORY of 43.59 million oz or 89.65% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:50,941// est. volume today// poor

Comex volume: confirmed yesterday: 43,847contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

GLD INVENTORY: 947.23 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

CLOSING INVENTORY 481.194 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

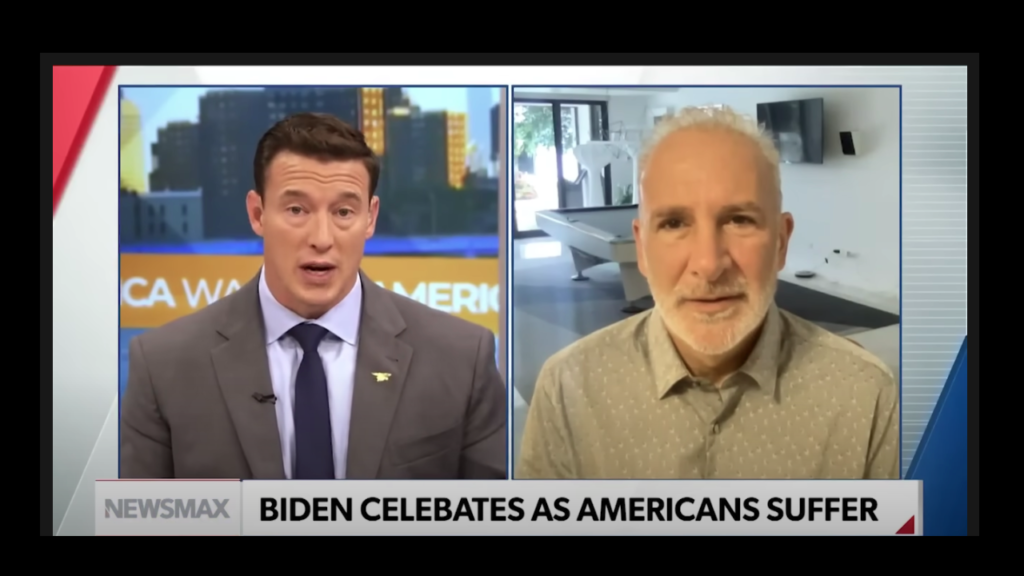

Peter Schiff: Biden Putting America At Risk To Prop Up His Own Image

MONDAY, SEP 26, 2022 – 04:20 PM

Even as the August inflation data was coming out higher than expected, President Joe Biden was bragging about his “Inflation Reduction Act.” Peter Schiff appeared on NewsMax and argued that the president is putting Americans at risk just so he can improve his image as we approach election time.

Peter pointed out that one reason energy prices have come down is because the Biden administration dumped millions of barrels of oil from the strategic reserve into the market.

That’s not going to last. And if you look below the surface, we’re seeing an acceleration in food prices, in shelter, in health care — so, everything is really going up. We just have one thing right now that’s pulled back. But of course, energy prices are still up dramatically from where they were a year ago. So, the inflation tax is falling even more heavy on middle-class Americans now than it was a few months ago.”

Peter said the “Inflation Reduction Act” is inappropriately named. It should be called “The Inflation Acceleration Act.”

That is going to have consequences next year in helping push that inflation rate even higher than the inflation from 2022.”

As far as the strategic oil reserve goes, now Biden will have to refill it at a much higher price. Peter said he doesn’t think they’ll refill it at all.

I think more likely, they’re going to deplete the reserve until it’s empty. And then what are we going to do? Then we’ll have no oil to sell. And what if we have an actual emergency, and we have shortages? We won’t have any strategic reserve to fall back on.”

Peter reminded the audience that inflation is even worse than advertised because the CPI formula is rigged.

You really have to double the CPI to get the actual increase in prices that Americans are experiencing. Take one example, which is shelter, which I think rose about 6.1%, which really was the highest, I think, since the 1980s. If you look at the real cost of housing, … medium home prices are up 30% and mortgage rates have gone from 3.1 to 6.1. So, the cost of buying a home and paying a mortgage in the last two years is up by 84%. … And of course, rents are skyrocketing too. And so, what the government claims as the increase in the cost of shelter is just a small fraction of what Americans are actually paying for shelter.”

The anchor pointed out that interest rates need to rise above the CPI in order to tame inflation. Meanwhile, we’re already technically in a recession. Peter agreed we are in a recession, as much as the Biden administration and others, including the Fed, try to deny it.

We’ve already had two quarters of falling GDP. We’re about to have a third, because I think this quarter is going to be another negative quarter. And I think the fourth quarter will also be negative.”

And Peter said the anchor was also correct in asserting rates need to go much higher to tackle inflation.

You have to have positive real interest rates so you encourage people to save, which means more capital investment and more supply. And you’ve got to discourage people from borrowing, so you have less demand. But we still have negative real interest rates.”

Even with the Fed’s 75 basis point hike at the September meeting (after this interview), real rates are still -5%.

That is fueling an inflation fire. And of course, the only way to really fight inflation would be a combination of tight money and contractionary fiscal policy. We need big spending cuts coming out of Congress. But unfortunately, they’re doing the opposite. They’re stimulating consumption with more deficit spending.”

The Chips Act, the Inflation Reduction Act, and student loan forgiveness all add to demand.

“It’s acting at cross purposes.”

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

LAWRIE WILLIAMS: China, Turkey, India biggest importers of Swiss gold in August

The Swiss Customs Administration has released its figures for gold imports and exports for August and China has retained its position as the top importer, taking in 37.9 tonnes. This was followed by Turkey, which had only been a minor recipient for the previous few months, with 25.3 tonnes, and then India, where imports seem to be recovering again with 19.4 tonnes. If we include Turkey as being in the Middle East, this area and Asia accounted for fully 86.3% of the exported Swiss gold (see chart below).

That Chinese gold demand seems to be running strong again has been evident from our reports on withdrawal figures from the Shanghai Gold Exchange (see: China gold consumption still climbing y-o-y) and an even more recent Bloomberg report that gold benchmark prices in Shanghai have climbed to a premium of more than $43 an ounce over their London equivalent, the highest since 2019, according to data from the World Gold Council. London and Shanghai prices appear to have steadily diverged over the course of the month, with the Chinese market remaining relatively firm despite downwards pressure on international prices. Bloomberg comments that the difference shows how demand in China is outstripping supply, which has been constrained by government policy. Only accredited banks in the country are allowed to import gold, with quantities set by the Chinese central bank.

Bloomberg goes on to note that banks will likely receive new gold import quotas after the Golden Week holiday at the beginning of October, according to a person familiar with the matter. Local importers have recently been struggling to get shipments approved by Chinese lenders, sign they may have used up their existing quotas.

Largely for historic reasons, the Swiss refineries represent an excellent indicator of the direction of gold flow traffic worldwide. They process doré bullion from mines, gold scrap and larger gold bars and refine and re-refine this material mostly into the smaller bar sizes, coins, medallions and wafers most in demand on international markets. Overall an amount of gold equivalent to around half the world’s new mined gold is treated by the Swiss refineries on an annual basis. It used to be a higher percentage, but a number of gold producing and trading countries now operate their own refineries, although some of these are managed and/or operated by the Swiss as the experts in this field.

Of the Swiss gold imports in August these were dominated by gold from the USA which exported 49.5 tonnes of the 170.5 tonne total received, but most came in from other gold producing nations in the form of doré bullion from the mines. As has been the case in recent months important amounts were also received from typical gold trading sources like the UAE (8.6 tonnes) and Hong Kong (6.2 tonnes) although the volumes from these seem to be diminishing suggesting that trade is relatively strong.

Interestingly the Swiss recorded the receipt of 5.8 tonnes of Russian gold. This is believed to have come from gold which was already in London as gold coming directly from Russia would have been blocked from import into Switzerland by sanctions.

END

3.Chris Powell of GATA provides to us very important physical commentaries

The following is extremely important: The premium in GOLD TRADING in Shanghai is now $43 over the price in London. This is due to gold being actually delivered upon, and supply constraints placed by government.

Eventually everything will move to Shanghai and Dubai and Moscow.

(Bloomberg)

Gold fetches huge premium in China as demand improves

Submitted by admin on Fri, 2022-09-23 09:15Section: Daily Dispatches

From Bloomberg News

Thursday, September 22, 2022

Gold in China is trading at a huge premium to international prices as a revival in demand outstrips the country’s imports.

Benchmark prices in Shanghai have climbed to a premium of more than $43 an ounce over their London equivalent, the highest since 2019, according to data from the World Gold Council. Unusually, the two have steadily diverged over the course of the month, with the Chinese market remaining relatively firm despite pressure on international prices.

The difference shows how demand in China is outstripping supply, which is constrained by government policy. Only accredited banks in the country are allowed to import gold, with quantities set by the People’s Bank of China.

Banks will likely receive new imports quotas after the holiday in October, according to a person familiar with the matter. Local importers have recently been struggling to get shipments approved by Chinese lenders, according to people familiar with the matter, a sign they may have used up their existing quotas.

END

With Wall Street Silver, GATA’s Steer discusses frantic moves in monetary metals

Submitted by admin on Fri, 2022-09-23 11:38Section: Daily Dispatches

11:33a ET Friday, September 23, 2022

Dear Friend of GATA and Gold (and Silver):

GATA board member Ed Steer, editor of Ed Steer’s Gold and Silver Digest, was interviewed this week by Wall Street Silver, discussing the frantic movements on the monetary metals exchanges and the switch of commercial traders from short to long positions.

The interview is 19 minutes long and can be heard at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Central banks are buying gold and increasing their reserves. They refuse to sell their gold produced. Ghana bought 3.8 tonnes of gold at year end

(Ghana News Agency/GATA)

Ghana’s central bank to buy another 125,000 oz. of domestic gold by year-end

Submitted by admin on Sun, 2022-09-25 11:00Section: Daily Dispatches

From the Ghana News Agency

via PeaceFM, Accra

Saturday, September 24, 2022

Gold-producing member companies of the Ghana Chamber of Mines will, by December 2022, sell about 125,000 ounces of gold to the Bank of Ghana under the central bank’s Domestic Gold Purchase Programme.

The decision followed a meeting between Vice President Alhaji Dr. Mahamudu Bawumia, some other members of the Economic Management Team, the Bank of Ghana, the Ministry of Lands and Natural Resources, Minerals Commission, the government’s Precious Minerals Marketing Co., as well as the leadership of the chamber to consider the implementation of the central bank’s gold purchase programme in the light of the country’s economic challenges.

Ahead of that meeting, Newmont Ghana had already sold 3,500 ounces of gold to the Bank of Ghana as part of the programme.

Vice President Dr. Bawumia said after the meeting, “It was agreed that to help shore up the foreign exchange reserves of the Bank of Ghana. Starting September 1, the Bank of Ghana will purchase a portion of the output of the gold mining companies on a continuous basis at world market prices, but payment will be made in Ghana cedis.” …

… For the remainder of the report:

https://www.peacefmonline.com/pages/local/news/202209/474762.php

END

5.OTHER COMMODITIES:

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1658

OFFSHORE YUAN: 7.1609

SHANGHAI CLOSED: DOWN 37.14 PTS OR 1.20%

HANG SENG CLOSED DOWN 722.28 PTS OR .226%

2. Nikkei closed DOWN 722.28 [PTS OR 2.66%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 113.49/Euro FALLS TO 0.96449

3b Japan 10 YR bond yield: RISES TO. +.242/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 144.22/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

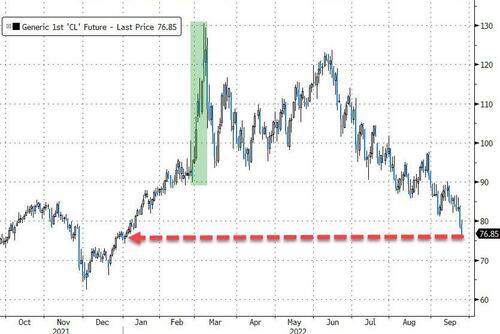

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.109%***/Italian 10 Yr bond yield FALLS to 4.501%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.28%…** DANGEROUS

3i Greek 10 year bond yield RISES TO 4.68//

3j Gold at $1641.45 silver at: 18.73 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 4/100 roubles/dollar; ROUBLE AT 57.88//

3m oil into the 78 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 144.22DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9901– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9554well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.789 UP 9 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.668 UP 6 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

USA DOLLAR VS TURKISH LIRA: 18,45…GETTTING DANGEROUS

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

“Global Gloom”: World Markets Plunge To Start The Week As Global Currency Crash Hits Max Pain And Beyond

MONDAY, SEP 26, 2022 – 08:08 AM

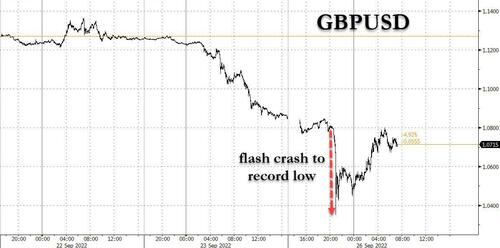

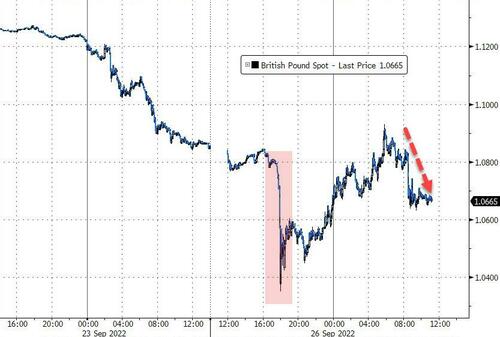

The rout which hammered stocks on Friday, nearly pushing them to close at a new 2022 low, resumed overnight when the global FX crisis returned with a bang, and a flash crash in the British pound which as noted late last night, plummeted 500pips in thin trading, to fresh record lows following Friday’s shocking mini-budget announcement which confirmed the UK has no idea what it is doing and will cut rates and issue more debt just as the BOE is desperately trying to tighten financial conditions.

The plunge in cable was however just one symptom of a bigger malaise, namely the relentless surge in the dollar which overnight hit fresh record highs as the BBDXY rose as high as 1,355 before briefly fading the surge…

… as every dollar-denominated debt issuer in the world is suffering crippling pain and begging Powell to do something to ease the unprecedented shock of the strongest dollar in history just as the world slumps into a global depression.

Alas, so far there is nothing but silence from the Fed – which will likely have to make some announcement on central bank currency swaps at some point before the open today to avoid an even more epic FX rout – and as traders await something to break big time across global markets…

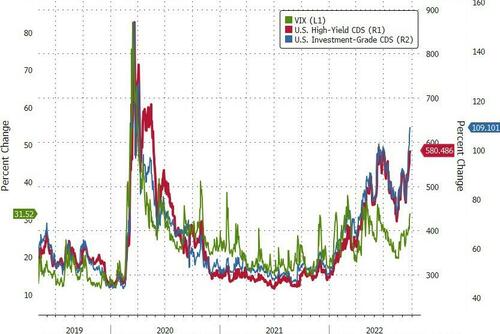

… this morning futures have tumbled another 0.7%, as eminis drop to 3,683 while Nasdaq futures are down 0.8% to 11,290 on fears that Federal Reserve rate hikes to combat persistently elevated inflation will crush the economy into a full-blown recession, or depression, and the VIX soared above 32.

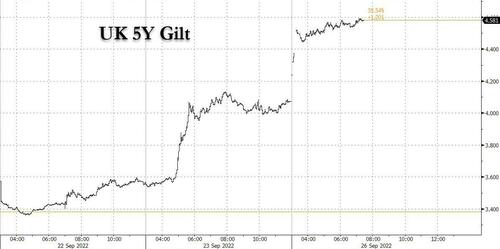

It wasn’t just FX and stocks crashing: British bonds also cratered as yields surged to the highest in more than a decade, sparking talk of emergency action by the Bank of England. For one example of the total chaos look no further than 5Y UK Gilts which have exploded 51bps higher and last traded around 4.58% as the market now prices in

Similar implosions were observed in US TSYs, where the 10Y traded just shy of Friday’s mini blowout, and was last seen at 3.7828% as bond traders are hit by VaR shocks at the same time in every possible market.

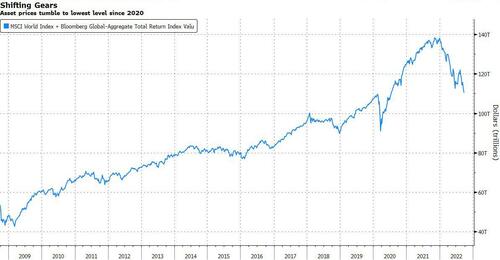

Turning back to stocks, the rout wasn’t isolated to just one market and an index of global stocks traded to the lowest since 2020. European equities extended declines after sliding into a bear market on Friday, with mining and energy stocks underperforming as metals and oil fell.

“We’re in a period of global gloom, with pessimism blanketing different countries for different reasons,” said Ed Yardeni, president of his eponymous research firm, who warned of growing storm clouds for the US economy. “The latest data jibe with our growth recession scenario, but the risks of a full-blown recession are obviously increasing,” he wrote in a note Monday.

In premarket trading, major US tech and internet stocks including Apple, Amazon and Microsoft tumbled. Here are some other notable premarket movers:

- Farfetch (FTCH US) shares fall as much as 4.43% in US premarket trading, after Citi begins coverage of the luxury online retailer with a sell rating, with broker flagging “weak” underlying profitability.

- Shares of US-listed Macau casinos jump in premarket trading, after Macau government said tour groups from mainland China could resume as early as November. Wynn Resorts (WYNN US) jumps 5.4%; Las Vegas Sands (LVS US) +6.9%, Melco (MLCO US) +9.6% and MGM resorts (MGM US) +1.6%

- Cryptocurrency-exposed stocks edged higher in premarket trading on Monday as Bitcoin rose above $19,000.

- Marathon Digital (MARA US) +1.9%, Coinbase (COIN US) +0.4%

- Keep an eye on Diana Shipping (DSX US) and Safe Bulkers (SB US) as Jefferies downgraded them to hold from buy and lowered dry bulk estimates to reflect the decline in dry bulk charter rates.

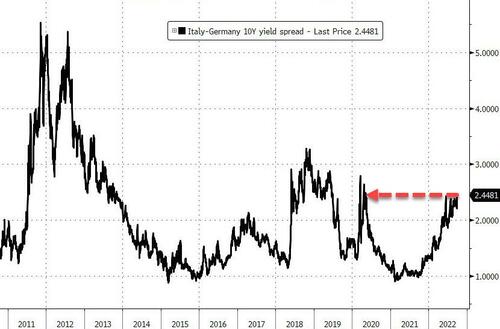

European shares extended their fall to Dec. 2020 lows; sliding 1% and extending losses as investors priced a major economic shock and recession. The Stoxx 600 Index was down 1% by 10:50am in London, touching its lowest since December 2020, with real estate and banks among the worst performing sectors, while technology shares outperformed. Italy’s FTSE MIB bucked broader European declines to trade little changed, after Giorgia Meloni won a clear majority in Sunday’s election, in line with expectations.

Banks and real estate stocks were the worst-performing sectors in Europe on Monday, with declines led by UK stocks as the pound and UK bonds slump. The Stoxx 600 Banks Index and the Stoxx 600 Real Estate are both down at least 2.5% while the benchmark gauge is 1.1% lower. The bank index decline is led by UK names including Virgin Money (-10%), Lloyds (-4.6%) and NatWest (-4.5%). Virgin Money was today resumed with a hold rating at Berenberg; broker said that the lender is expected to see revenue declines and a sector- lagging return on tangible equity which will affect ability to re-rate. Among real estate stocks, the UK’s Safestore Holdings (-4.2%), Assura (-3.9%) and Derwent London (-3.8%) are among the worst performers; non-index member housebuilders, including Persimmon, Bellway and Taylor Wimpey, are also plunging as the pound’s slump prompts talk of emergency action by the Bank of England. Here are the most notable movers today:

- The Stoxx 600 Tech Index rises as much as 2.4%, set for its biggest one-day outperformance against the broader Stoxx 600 since early-August, with semiconductor stocks leading gains. Among chip stocks, ASML rose as much as +3.7% after Santander upgraded the stock to neutral from underperform

- Italy’s FTSE MIB index gains, bucking weaker markets in Europe, after Giorgia Meloni won a clear majority in Sunday’s election. While the outcome was in line with expectations, the fact that the coalition didn’t obtain a super majority needed to change the constitution reassures investors. Telecom Italia rose as much +7.4%, FinecoBank +5.1%, Moncler +4.4%

- Unilever shares rise as much as 3.7% after it announced that CEO Alan Jope will retire from the company at the end of 2023, in a move that Jefferies analyst Martin Deboo (buy) sees as a positive development.

- RPS Group shares rise as much as 13% after Tetra Tech’s agreed deal to buy the company at 222p/share in cash, representing a 7.8% premium to an offer WSP made in August. Liberum does not rule out a counterbid.

- Belimo shares rise as much as 8.5% since the market isn’t fully pricing in its growth outlook, Berenberg says in a note, moving to buy and establishing a Street-high CHF440 target. The stock gains as much as 8.1%, the most since March 2021.

- Zalando shares rise as much as 4.8% after Citi analyst says they like the long-term investment story, short-term earnings risks are still high.

- UK Domestics: the most remarkable reaction to Friday’s not-so-mini budget, however, might be in lenders’ shares. The decline in banking stocks reflects investors’ pessimistic view on Britain’s economy. HSBC fell as much as 2.9%; Lloyds -4.3%, NatWest -4.7% and Barclays -3.0%.

- Virgin Money UK shares drop as much as 10% after Berenberg resumed a hold rating in note, stating that in many ways the UK small banks are “more different than they are alike.”

- Utilities are the day’s worst-performing European sector. Citi analyst Piotr Dzieciolowski says the EU’s funding for its policy response has so far been insufficient and also expects uncertainty to persist for UK names. United Utilities fell as much as -3.4%, Drax -3.8%

Geopolitical risks from the war in Ukraine to escalating tensions over Taiwan and unrest in Iran also weighed on sentiment. Meanwhile, the OECD cut almost all growth forecasts for the Group of 20 next year while anticipating further interest-rate hikes, and a gauge of German business confidence deteriorated.

Earlier in the session, a rout in Asian stocks extended into Monday as rising concerns about a global recession and weak demand hit the region’s exporters and materials producers. The MSCI Asia Pacific Index declined as much as 2.3% to the lowest since April 2020, dragged lower by TSMC, BHP and Toyota Motor. All but one sector traded lower with materials leading the slump. South Korean stocks fell the most in the region, with the benchmark tumbling 3% to more than a two-year low. The Korean market’s heavy tech exposure has proven costly amid rising rates and a stronger dollar, with fears that a looming recession may wreak havoc on global demand. Gauges in Hong Kong and China reversed earlier gains as the region’s selloff intensified. Korea Assets Are Asia’s Biggest Losers on Global Recession Angst “Investor sentiment is again at the stage of extreme fear,” said Lee Kyoung-Min, an analyst at Daishin Investment. “It is becoming solid and clear that Kospi and other global stock markets are on a mid-to-long term downward trend.”

Asian stock benchmarks are being buffeted by global headwinds as well as risks of their own. The Federal Reserve’s relentless rate hike campaign is pushing Asian currencies lower and raising the risk of capital outflows, while China’s adherence to Covid Zero is hurting growth in the region’s economic giant. If Monday’s losses are extended through the week, the MSCI Asia Pacific Index will see its longest run of declines since 2015. Japan stocks declined more than 2% as the nation resumed trading after a holiday on Friday. The Philippine stock market was closed Monday as Super Typhoon Noru barreled into the main Luzon island. Among the key issues investors are watching this week are speeches by central bank officials in US and Europe, including Fed Chair Jerome Powell on Tuesday.

Japanese equities tumbled as the market reopened following a three-day weekend, tracking US peers lower after the Fed’s hawkish comments last week deepened fears of a global downturn. The Topix fell 2.7% to close at 1,864.28, while the Nikkei declined 2.7% to 26,431.55. Toyota Motor contributed the most to the Topix decline, decreasing 3.2% after its monthly production update lagged expectations. Out of 2,169 stocks in the index, 145 rose and 1,985 fell, while 39 were unchanged. “There is a possibility that inflation will not subside and interest rates will rise further, which the markets will not like,” said Shoji Hirakawa, a chief global strategist at Tokai Tokyo Research.

In Australia, the S&P/ASX 200 index fell 1.6% to close at 6,469.40, as energy and mining shares plummeted. An energy gauge including oil and coal linked securities declined by the most since March 2020. The New Zealand market was closed for a holiday

In India, key stocks gauges plunged to their lowest closing levels in almost two months as the global equity rout continues. The S&P BSE Sensex dropped 1.6% to 57,145.22 in Mumbai to its lowest since July 28. The NSE Nifty 50 Index fell 1.8%, its biggest single-day plunge since Sept. 16. Both the indexes, down in four of the past five weeks, have lost almost 6% since this month’s peak. Volatility in domestic equities is likely to remain elevated this week, pending monthly derivatives expiry on Thursday. Of 30 shares in the Sensex index, 24 fell and 6 advanced. All but one of the 19 sector sub-indexes compiled by BSE Ltd. declined, led by utilities and power companies. The Indian rupee weakened to a new record against the dollar amid surging US Treasury yields. The Reserve Bank of India’s rate-setting panel will announce monetary policy later this week.

As noted above, while stocks are ugly, rates are a horrorshow as Treasuries extended their worst bond slide in decades as a dollar gauge rose to yet another record. Treasuries extended losses in a bear flattening move with yields cheaper by up to 10bp across the belly of the curve. US 10-year yields around 3.78%, cheaper by 6bp on the day with 5s30s spread flatter by 5bp, dropping as low as -45.4bp in European session; UK yields cheaper by 60bp to 25bp from front- end out to long-end of the curve. The Move comes as market participants brace for accelerated policy tightening from global central banks and headlines such as this:

- *TRADERS PRICE IN UP TO 200BPS OF BOE RATE HIKES BY NOVEMBER

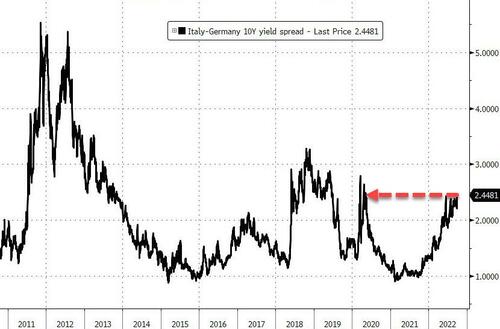

Yields on 2-year gilts are 60bp cheaper heading into early US session, while the pound recovers slightly after reaching a fresh all-time low. US session focus on 2-year auction, while a barrage of Fed speakers are expected for the week. Peripheral spreads widen to Germany with 10y BTP/Bund widening 7bps to 238bps.

FX, of course, is a disaster, with the Bloomberg Dollar Spot Index rising a fifth consecutive day as the greenback advanced versus most of its Group-of-10 peers.

- The pound plunged almost 5% to $1.0350 in Asian trading, the lowest recorded in Bloomberg data going back to 1971, while gilts crashed after the UK government vowed to press ahead with more tax cuts, stoking fears that new fiscal policies will send inflation and debt soaring, triggering emergency rate hikes. The options market signals no respite even as the pound rebounded from a record low hit during the Asia session. The yield on two- year bonds surged more than 55 basis points to 4.51%, while the 10-year yield rose 37 basis points to 4.19%. Money markets price in more than 150 basis points of rate increases by the BoE’s next policy meeting in November

- The euro steadied after earlier dropping to $0.9554; European bond yields rose; Italian bonds underperformed German peers. Giorgia Meloni won a clear majority in Sunday’s Italian election, setting herself up to become the country’s first female prime minister at the head of the most right-wing government since World War II. Germany’s IFO business expectations slid to 75.2 in September from 80.3 in August. That’s the lowest since April 2020. Analysts had predicted a drop to 79. An index of current conditions also fell.

- The Australian and New Zealand dollars pared some losses after earlier touching fresh 2-year lows. Aussie bond yields rose by up to 13bps, led by the front end

- The yen weakened amid a broadly stronger dollar. Bank of Japan Governor Haruhiko Kuroda said the government’s intervention in the foreign exchange market last week was appropriate given the recent volatility in the yen

The currency’s rally is “untenable” for risk assets, according to a note by Morgan Stanley strategists led by Michael Wilson, while Sian Fenner, senior Asia economist for Oxford Economics, said that “It’s a king US dollar…“It’s adding to inflationary pressures and more central banks raising rates more than we have historically seen.”

In commodities, WTI slides almost 1% to trade near $78/bbl. Spot gold mostly unchanged near $1,643/oz. Bitcoin climbs above $19,000.

Trading this week will be punctuated by a number of economic reports including US initial jobless claims and gross-domestic-product data, along with PMI figures from China. Choppiness in price moves is likely with a steady stream of Federal Reserve officials speaking through the week.

Looking at today’s calendar, we get the September Dallas Fed manufacturing activity index, and the August Chicago Fed national activity index. Central bank speakers include the Fed’s Bostic, Collins, Logan and Mester; ECB’s Lagarde also speaks as does Nagel, Guindos, Centeno and Panetta speak, BoE’s Tenreyro speaks.

Market Snapshot

- S&P 500 futures little changed at 3,706.25

- MXAP down 2.0% to 142.24

- MXAPJ down 1.4% to 463.08

- Nikkei down 2.7% to 26,431.55

- Topix down 2.7% to 1,864.28

- Hang Seng Index down 0.4% to 17,855.14

- Shanghai Composite down 1.2% to 3,051.23

- Sensex down 1.2% to 57,378.30

- Australia S&P/ASX 200 down 1.6% to 6,469.41

- Kospi down 3.0% to 2,220.94

- STOXX Europe 600 down 0.2% to 389.70

- German 10Y yield little changed at 2.08%

- Euro little changed at $0.9683

- Brent Futures down 0.7% to $85.59/bbl

- Brent Futures down 0.7% to $85.59/bbl

- Gold spot up 0.1% to $1,645.98

- U.S. Dollar Index little changed at 113.22

Top Overnight News from Bloomberg

- Chancellor of the Exchequer Kwasi Kwarteng must do more to reassure the markets about his plans for the economy after a selloff sent the pound crashing to an all-time low against the dollar, said Gerard Lyons, an external adviser to Prime Minister Liz Truss

- The UK’s foreign currency holdings are a fraction of the huge stockpiles built up by some of its peers, making unilateral intervention in the market to prop up the plunging pound a tall order for UK policymakers. The UK had $108 billion in foreign currency reserves at the end of August, according to data from the IMF

- Hedge funds ramped up bullish bets on the pound just days before the UK government’s unexpectedly large tax cuts sent the currency tumbling

- The ECB’s newest policy maker, Boris Vujcic, says “it’s clear that this is the right way to go,” backing this month’s 75-basis point interest-rate hike

- ECB Vice President Luis de Guindos said the biggest problem facing the continent’s economy is record inflation, which is becoming more broad-based, threatening investment and consumer spending

- ECB Governing Council member Yannis Stournaras says the central bank must maintain the main principles of gradualism and flexibility, since the problem it faces is different from the one that the US Fed faces

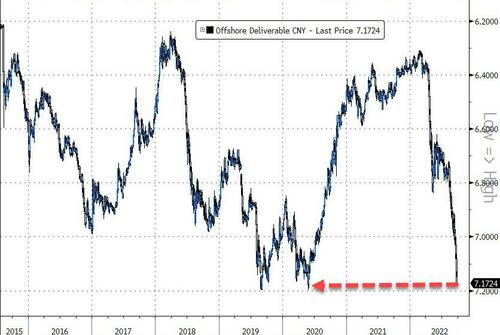

- China made it more expensive to bet against the yuan in the derivatives market, ramping up support for the currency as it slides toward the weakest level since the 2008 financial crisis

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mostly negative in a resumption of last week’s global stock rout amid the continued surge in the dollar and higher yields, while there was also FX volatility which saw a flash crash in GBP/USD to a record low. ASX 200 was dragged lower amid losses in the commodity-related sectors and with sentiment dampened by the collapse of potential M&A deals involving Ramsay Health-KKR and Link Administration-Dye & Durham. Nikkei 225 underperformed with Mazda Motors among the worst hit as it considers exiting Russian operations. Hang Seng and Shanghai Comp retraced most of their initial losses with Hong Kong underpinned following the scrapping of hotel quarantine policy and with casinos boosted as Macau is to resume tour groups from China, while the property industry benefits after China Construction Bank formed a CNY 30bln housing rental fund and some Twitter sources also circulated that some China state banks were reportedly ordered to buy stocks to contain selling.

Top Asian News

- PBoC injected CNY 42bln via 7-day reverse repos with the rate kept at 2.00% and CNY 93bln via 14-day reverse repos with the rate kept at 2.15% for a net CNY 133bln injection.

- There were rumours circulating on social media of a coup against Chinese President Xi, although experts and journalists in Beijing dismissed the rumours and said there was no evidence to support them, according to The Print.

- Philippines Stock Exchange announced a trading suspension for Monday amid a typhoon in the capital, according to Reuters.

European bourses are softer after a mixed cash open and despite a brief foray higher, Euro Stoxx 50 -0.5%, as sentiment remains subdued amid recession/inflation concerns. The breakdown features modest outperformance in the FTSE MIB as Italian election results are in-line with expectations. Stateside, futures are lower across the board in-fitting with peers going into a week of Fed speak and inflation data.

Top European News

- UK PM Truss said she is determined to make the special relationship with the US even more special and said she agreed with US President Biden that it is vital to protect the Northern Ireland Good Friday Agreement, while she wants to find a way forward with a negotiated solution with the EU, according to Reuters and a CNN interview.

- UK PM Truss is to review visa schemes in an attempt to ease UK labour shortages, according to FT.

- UK Chancellor Kwarteng hinted that more tax cuts are on the way and claimed his tax cuts “favour people right across the income scale” amid accusations they mainly help the rich, according to Evening Standard.

- UK Chancellor Kwarteng said he is focused on growing the economy and the longer term when asked about the market reaction to his statement on Friday. Kwarteng added that he shares ideas with BoE Governor Bailey but added that Bailey is completely independent and Kwarteng is confident the BoE is dealing with inflation, according to Reuters.

- UK opposition Labour Party leader Starmer said they would reintroduce the top rate of income tax at 45% which the government announced to scrap last week, while he added that they will support the government plan to lower the basic rate of income tax to 19%, according to Reuters.

- Italy’s right-wing bloc is seen winning the national election with 43.3% and centre-left bloc is seen winning 25.4%, according to the first projection by LA7 TV based on the actual vote count.. Click here for newsquawk snap analysis.

- Italy’s Meloni said Italians gave clear backing to a centre-right government led by the Brothers of Italy and said the situation is difficult and needs contribution from everyone. It was separately reported that Italy’s Democratic Party conceded in the election and said it will be the main opposition force, while Italy’s Meloni claimed leadership of the next Italian government, according to Reuters and AFP.

FX

- DXY climbed to a fresh YTD high of 114.58 before paring modestly, but remaining firmer, as GBP in particular lifts off worst levels.

- Cable succumbed to a flash crash overnight, with GBP/USD hitting an all-time-low around 1.0350 as participants confidence in the economy slips.

- EUR suffers amid the mentioned USD move but derives relative benefit from GBP, while ECB speakers thus far have added little.

- Antipodeans and CAD weighed on by broader risk and commodity pressure.

- Japanese Finance Minister Suzuki said the government and BoJ share views on concerns about a weak JPY, while he added that FX intervention had a certain effect and there is no change to the stance that they will respond to market moves as needed, according to Reuters.

- PBoC set USD/CNY mid-point at 7.0298 vs exp. 7.0019 (prev. 6.9920)

- PBoC imposed a 20% risk reserve requirement for FX forward sales from September 28th to rein in yuan weakness.

Fixed Income

- Gilts have retained some composure after slumping over 200ticks at the commencement of trade and have settled around halfway between intraday extremes.

- EGBs downbeat in sympathy while BTPs marginally lag core-EGB peers as Italian as-expected election results are digested with BTP-Bund only modestly wider as such.

- Stateside, USTs are pressured in-fitting with peers and also conscious of the week’s supply docket getting underway via a 43bln 2yr.

Central Banks

- Fed’s Bostic (2024 voter) said inflation is too high and that they need to do all they can to bring it down and said demand is beginning to shrink which will ultimately pay dividends in inflation levels. Bostic also stated that there are scenarios where they can avoid deep pain but there will likely be some job losses, according to Reuters.

- BoJ’s Kuroda says the BoJ will maintain accommodative monetary conditions to support companies, hopes to support a positive economic cycle, long-term inflation expectations have begun to heighten, via Reuters. Intervention from the MoF is an “appropriate” move, does not think gov’t intervention and BoJ policy are contradictory. Amamiya says the domestic economy is picking up, must carefully watch how FX moves affect the economy and prices.

- BoJ Governor Kuroda says when he stated that BoJ forward guidance will not change for 2-3yrs, did not refer to guidance on keeping short and long-term rates at present of lower levels via Reuters.

- ECB’s de Guindos says Q3 and Q4 point towards growth rates being close to zero within the EZ, the scenario is market by high uncertainty, lower growth and higher inflation.

- ECB’s Panetta says ECB is assessing the potential of distributed ledger technology (DLT) and “the extent to which it could improve our services.”.

- Capital Economics calls for the BoE to “get on the front foot with a big rate hike”. Allianz’s El-Erian says, on GBP, the fall is about extra tax cuts and Chancellor Kwarteng could recalibrate this. Alternative, would be for the BoE to hike at an emergency meeting. Adding, he would hike by 100bp.

- BoE publishes key elements of the 2022 annual cyclical scenario stress test; includes a scenario where the Bank Rate is assumed to rise rapidly to a peak of 6% in early 2023 before gradually reduced to sub-3.5%.

Commodities

- WTI and Brent November futures remain subdued in early European trade following last week’s recession-induced losses.

- Spot gold trades in tandem with the Buck and sees resistance at around USD 1,650/oz after falling to USD 1,627/oz as a casualty of the Sterling flash crash overnight.

- LME metals are softer across the board with 3M copper futures having a hard time reclaiming USD +7,500/t status with upside capped by the Buck.

- Iraq began trial operations at the Karabala oil refinery which has a production capacity of 140k bpd, according to a statement from the Oil Ministry.

- German Chancellor Scholz signed a strategic agreement with UAE’s President on accelerating energy security and industrial growth, while UAE’s ADNOC signed an agreement with Germany’s RWE which includes ADNOC exporting its first LNG cargo to RWE and will conduct trial shipments of low-carbon ammonia to Germany. Furthermore, Chancellor Scholz said while visiting Doha that he talked with the Emir about LNG deliveries and that they want to achieve further progress, according to Reuters.

- Germany is preparing a national electricity price cap to be implemented this fall in the scenario the EU falls to agree on a similar move for the entirety of the bloc, via WSJ citing officials.

- Vitol’s CEO said at the Asia Pacific Petroleum Conference that Russian gas supply cuts put enormous strain on supply-demand in Europe and that high gas prices are to impact 60%-80% of demand, while Ecopetrol’s CEO said they are increasing crude exports to Europe this year to replace Russian supplies and are drilling 600 oil wells this year.

- Anglo American (AAL LN) tightens copper production guidance for Chile to 560k-580k tonnes of copper (prev. 560k-600k tonnes) due to lower throughput at Los Bronces caused by a combination of water restrictions and a change in ore characteristics, via Reuters.

US Event Calendar

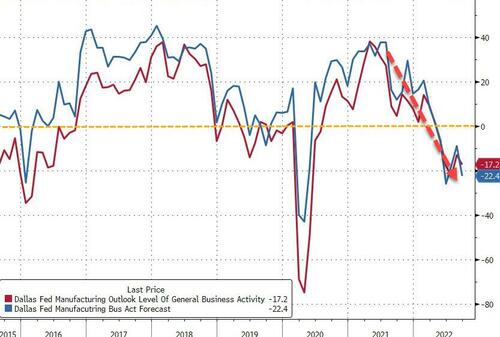

- 08:30: Aug. Chicago Fed Nat Activity Index, est. 0.23, prior 0.27

- 10:30: Sept. Dallas Fed Manf. Activity, est. -10.0, prior -12.9

Central Banks

- 10:00: Boston Fed’s Susan Collins Speaks to Boston Chamber of…

- 12:00: Fed’s Bostic Discusses Income Inequality

- 12:30: Fed’s Logan Speaks at Banking Conference

- 16:00: Fed’s Mester Discusses Economic Outlook

DB’s Jim Reid concludes the overnight wrap

I wonder whether any research report has ever been written whilst watching synchronised swimming? Well if not, then you’re reading the first ever as I’m getting a head start on the early morning news by starting this on Sunday evening watching my daughter Maisie do her second session after getting into the local club. Watching this sport is going to take some getting used to after years of watching football, cricket, golf, F1, athletics, rugby… actually…. virtually every sport bar synchronised swimming.

I think everyone felt they were swimming in a tsunami of newsflow last week after one of the most incredible macro weeks in recent memory in terms of breadth of events. Yes there have been more extreme weeks in crises but last week had a bit more variety and was outside of a crisis period. If over 500bps of global rate hikes wasn’t enough, you also had 2yr US yields moving higher for the 12th successive day on Friday (the longest steak since data begins in 1976), the BoJ intervening in FX markets for the first time since 1998, and what can only be termed as one of the darker days for sterling assets on record on Friday after a mammoth tax giveaway in what was a mini-budget in name and not by nature.

Henry and I put a note out on Friday night (link here) showing that it was the third worst day for Sterling (-3.57%) since Black Wednesday in 1992, with the worst two since being the day after the Brexit vote (-8.1%) and after the initial covid shock in 2020 (-3.71%) when there was a global flight to dollars. We also show a graph of daily Sterling moves back to 1862 and on that it was the 41st worst day in history spanning 47,000 trading days. Obviously in the long era of fixed FX rates there were the occasional big devaluations which were much bigger than Friday. This morning is Asia it fell around -4.5% at one point (1.0392) which was a record low against the Dollar. It’s around -2.78% as I type. This follows a weekend interview where Chancellor Kwarteng suggested that more tax cuts were to come so that certainly was a red rag to markets. Will we hear from the upper echelons of the BoE today? Watch out for any comments, especially at the market open. DB’s George Saravelos suggested on Friday that the Bank of England need to do an inter meeting hike to restore policy credibility.

There’s also a graph in our note mentioned above showing that Friday was the worst day for 5yr gilts (+50.3bps) since a +200bps hike in 1985 when sterling was also slumping. So maybe omens here.

I suppose the only slight mystery is the timing of the sell-off as the mini-budget in magnitude was broadly in-line with the recent elevated fiscal expectations that had been building. However perhaps it was the unabashed revival of trickle-down economics that had markets a little aghast. It goes against the current economic orthodoxy and the overall zeitgeist of our immediate times. As such there is likely to be concerns of a credibility issue.

We are publishing our long-term study today with the title “How we got here, and where we’re going?”. In it we try to put the current macro woes into historical context in an attempt to work out where we’re going. There are quite a few people who have proof-read it on my team and they were all thoroughly depressed at the end. I didn’t feel that way writing it but maybe it’s a case of starting point perceptions. Anyway, look out for it around the European lunchtime.