by harveyorgan · in Uncategorized · Leave a comment·Edit

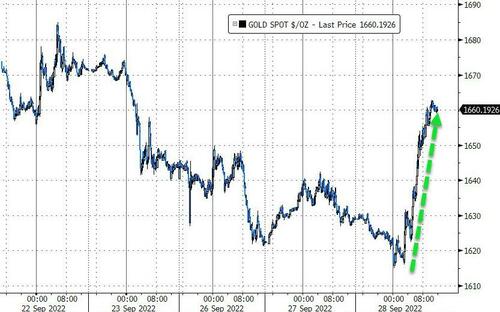

GOLD PRICE CLOSE: UP $32.30 to $1661.20

SILVER PRICE CLOSE: UP 32 cents to $18.91

Access prices: closes

Gold ACCESS CLOSE 1659.25

Silver ACCESS CLOSE: 18.89

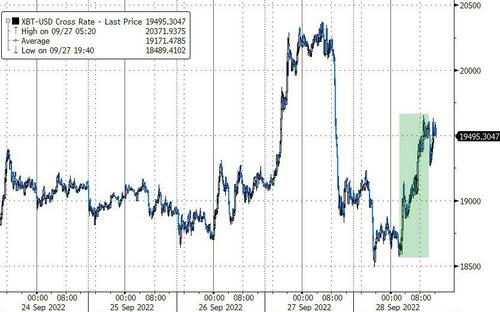

Bitcoin morning price: $18921 DOWN 134

Bitcoin: afternoon price: $19,492 up 358

Platinum price closing UP $13.80 AT $864.80

Palladium price; closing UP $13.80 at $2151,65

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,626.700000000 USD

INTENT DATE: 09/27/2022 DELIVERY DATE: 09/29/2022

FIRM ORG FIRM NAME ISSUED STOPPED

435 H SCOTIA CAPITAL 50

657 C MORGAN STANLEY 35

661 C JP MORGAN 598 533

690 C ABN AMRO 10

732 C RBC CAP MARKETS 141

880 H CITIGROUP 333

905 C ADM 32

TOTAL: 866 866

MONTH TO DATE: 12,013

GOLD: NUMBER OF NOTICES FILED FOR SEPT CONTRACT:

866 NOTICES FOR 86600 OZ //2.6936 TONNES

total notices so far: 12,013 contracts for 1,201,300 oz (37.365 tonnes)

SILVER NOTICES: 43 NOTICES FILED FOR 215,000 OZ/

total number of notices filed so far this month 6784 : for 33,920,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $32.30

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: //// A WITHDRAWAL OF 2.61 TONNES FROM THE GLD/

INVENTORY RESTS AT 940.86 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 32 CENTS

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF OF 0.645 MILLION OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 480.549 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 935 CONTRACTS TO 129,060 (ANOTHER ALL TIME RECORD LOW) AND FURTHER FROM THE NEW RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.07 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.07) AND WERE SUCCESSFUL IN KNOCKING OFF SOME SPEC SILVER LONGS AS WE HAD A STRONG LOSS OF 885 CONTRACTS ON OUR TWO EXCHANGES. WE DID HAVE CONTINUAL SHORT ADDITIONS WITH THE BANKERS ON THE BUY SIDE.

WE MUST HAVE HAD:

I) CONTINUAL SPECULATOR SHORT ADDITIONS ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 135,000 OZ QUEUE JUMP / // V) STRONG SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: –60

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 19 days, total 13,860 contracts: 69.300 million oz OR 3.647 MILLION OZ PER DAY. (729 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 69.300 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 69.300 MILLION OZ///

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 935 WITH OUR $0.07 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 50 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /GOOD BANKER ADDITIONS A// CONTINUAL NET SPEC SHORT ADDITIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 135,000 OZ QUEUE JUMP // .. WE HAD A STRONG SIZED LOSS OF 935 OI CONTRACTS ON THE TWO EXCHANGES FOR 4.425MILLION OZ..

WE HAD 43 NOTICE(S) FILED TODAY FOR 215,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

WE HAVE 2 MORE READING DAYS BEFORE FIRST DAY NOTICE

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A HUGE SIZED 9274 CONTRACTS TO 457,061 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED — -151 CONTRACTS.

.

THE HUGE SIZED DECREASE IN COMEX OI CAME DESPITE OUR GAIN IN PRICE OF $1.75//COMEX GOLD TRADING/TUESDAY / WE HAD INITIATION OF SPREADER LIQUIDATION// SOME SPECULATOR SHORT COVERINGS ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION AS ALL THE LOSS IN COMEX OI WAS DUE TO SPREADER LIQUIDATION //AND //CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 43,100 OZ //NEW STANDING 38.127 TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S)

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $1.75 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A STRONG SIZED LOSS OF 6552 OI CONTRACTS 19.922 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2722 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 457,061

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6552 CONTRACTS WITH 9274 CONTRACTS DECREASED AT THE COMEX AND 2722 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 6408 CONTRACTS OR 19.922 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2722) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (9274): TOTAL LOSS IN THE TWO EXCHANGES 6552 CONTRACTS. WE NO DOUBT HAD 1) SMALL SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS/// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.409 TONNES FOLLOWED BY TODAY’S MONSTROUS QUEUE JUMP OF 43,100 oz. 3) ZERO LONG LIQUIDATION (ALL THE LOST ARE SPREADERS)//// //.,4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/5/INITIATION OF SPREADER LIQUIDATION..TOTALLY FRAUDULENT BUT WHO IS WATCHING!!

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

57,299 CONTRACTS OR 5,729,900 OZ OR 178.22 TONNES 19 TRADING DAY(S) AND THUS AVERAGING: 3015 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAY(S) IN TONNES: 178.22 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 178.22/3550 x 100% TONNES .502% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 178.22 TONNES (SLIGHTLY RISING THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER,FELL BY A STRONG SIZED 935 CONTRACT OI TO RECORD LOW OF 129,000 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 50 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 50 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 50 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1875 CONTRACTS AND ADD TO THE 50 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 935 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 4.425 MILLION OZ

OCCURRED WITH OUR STRONG LOSS IN PRICE OF $0.07

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 48.79 PTS OR 1.58% //Hang Sang CLOSED DOWN 609.43 PTS OR 3.41% /The Nikkei closed DOWN 397.89 PTS OR 1.50-% //Australia’s all ordinaires CLOSED DOWN 0.55% /Chinese yuan (ONSHORE) closed DOWN AT 7.2354//OFFSHORE CHINESE YUAN DOWN 7.2411// /Oil UP TO 78.93 dollars per barrel for WTI and BRENT AT 86.57 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A HUGE SIZED 9274 CONTRACTS TO 457,061 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED DESPITE OUR RISE IN PRICE OF $1.75 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2722 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2722 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :2722 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5333 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED SIZED TOTAL OF 6552 CONTRACTS IN THAT 2722 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A HUGE SIZED COMEX OI LOSS OF 9274 CONTRACTS..AND THIS STRONG LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR RISE IN PRICE OF GOLD $1.75. ALL OF THE LOSS IN COMEX OI WILL NO DOUBT BE ATTRIBUTED TO INITIATION OF SPREADER LIQUIDATION//WE HAD CONTINUAL SHORT ADDITIONS WITH BANKERS TAKING THE BUY SIDE// WE ARE NOW WITNESSING THE SPECULATORS GOING MASSIVELY SHORT WHILE THE BANKERS WHO ARE HUGELY LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS ONCE THE SIGNAL HAS BEEN GIVEN TO ANNIHILATE THE SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (38.127),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.127 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $1.75) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED TOTAL LOSS ON OUR TWO EXCHANGES OF 6552 CONTRACTS // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS SOMEWHAT ADDED TO THEIR POSITIONS WITH SOME SUCCESS//INITIATION OF SPREADER LIQUIDATION// WE HAVE REGISTERED A STRONG LOSS OF 6408 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT. (38.127 TONNES)…

WE HAD -151 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 6552 CONTRACTS OR 655200 OZ OR 20.379 TONNES

Estimated gold volume 284,258/// fair//

final gold volumes/yesterday 218,762/ fair

INITIAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 28

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 32,794.012 oz BRINKS includes 1020 kilobars Brinks |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 866 notice(s) 86,600 OZ 2.6936 TONNES |

| No of oz to be served (notices) | 246 contracts 24,600 oz 0.7651 TONNES |

| Total monthly oz gold served (contracts) so far this month | 12,013 notices 1,201,300 OZ 37.365 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals: 1

i) Out of Brinks 32,794.012 oz or 1020 kilobars

total: 32,794.0123 oz

total in tonnes: 1.02 tonnes

Adjustments: 1

JPM: dealer to customer; 6655.257 0z

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 1112 contracts having GAINED 42 contracts .

We had 389 notices filed on TUESDAY so we gained a whopping 431 contracts or an additional 43,100 oz

will stand for gold in this very non active delivery month of September. This queue jump is actually the Londoners exercising efp’s and tendering them to the banks

for the physical!

October LOST a relatively small 9586 contracts LOWERING TO 31,458. Oct is generally a poor active delivery month. It WILL change…..probably around 75 85 tonnes will stand!!

WE HAVE 2 MORE READING DAYS BEFORE FIRST DAY NOTICE ( FRIDAY SEPT 30.2022)

November GAINED 96 contracts to stand at 928

December GAINED 54 contracts UP to 377,619

We had 866 notice(s) filed today for 86600 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 598 notices were issued from their client or customer account. The total of all issuance by all participants equate to 866 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 533 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (12,013) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 1112 CONTRACTS) minus the number of notices served upon today 866 x 100 oz per contract equals 1,225,800 OZ OR 38.127 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (12,013) x 100 oz+ (1112) OI for the front month minus the number of notices served upon today (866} x 100 oz} which equals 1,225,800 oz standing OR 38.127 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 38.127 TONNES (A HUMONGOUS STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,235,417.759 oz 69.534 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 26,524,450.883 OZ

TOTAL REGISTERED GOLD: 13,121,323.283 OZ (408.12 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 13,403,127.598 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,885,906 OZ (REG GOLD- PLEDGED GOLD) 338.97 tonnes//rapidly declining

END

SILVER/COMEX/SEPT 28

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,189,451.117 oz Brinks CNT Int. Delaware Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 4053.000 oz Delaware |

| No of oz served today (contracts) | 43 CONTRACT(S) 215,000 OZ) |

| No of oz to be served (notices) | 18 contracts (90,000 oz) |

| Total monthly oz silver served (contracts) | 6784 contracts 33,920,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into Delaware: 4053.000 oz

Total deposits: 4053.00 oz

JPMorgan has a total silver weight: 163.461 million oz/314.132million =52.02% of comex

Comex withdrawals: 4

i) Out of Brinks: 485,051.720 oz

ii)Out of CNT 23,378.170 oz

iii)Out of Int Delaware: 82,321.880 oz

iv) out of Manfra 598,699.347 oz

total withdrawals: 1,189,451.117 oz

adjustments: // 2

DEALER TO CUSTOMER:

i)JPMorgan: 195,119.310 oz

ii)out of Manfra 118,550.01 oz

iii) Out of Delaware: 76,552.692 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 42.686 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 314.173 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF SEPT OI: 61 CONTRACTS HAVING LOST 19 CONTRACTS. WE HAD

46 CONTRACTS SERVED ON TUESDAY SO WE GAINED 27 CONTRACTS OR AN ADDITIONAL

135,000 OZ WILL STAND FOR METAL IN THIS VERY ACTIVE MONTH OF SEPT.

WE WILL GAIN IN TOTAL SILVER STANDING EACH TRADING DAY UNTIL THE END OF THE MONTH

(CONTINUAL QUEUE JUMPING BY OUR BANKERS SEARCHING FOR SILVER METAL)

OCTOBER LOST 24 CONTRACTS TO STAND AT 341 CONTACTS.

NOVEMBER GAINED 19 CONTRACTS TO STAND AT 211

DECEMBER SAW A LOSS OF 932 CONTRACTS DOWN TO 113,356

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 43 for 215,000 oz

Comex volumes:81,613// est. volume today// good

Comex volume: confirmed yesterday: 65,273 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 6784 x 5,000 oz = 33,920,000 oz

to which we add the difference between the open interest for the front month of SEPT(61) and the number of notices served upon today 43 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT./2022 contract month: 6,784 (notices served so far) x 5000 oz + OI for front month of SEPT (61) – number of notices served upon today (43) x 5000 oz of silver standing for the SEPT contract month equates 34,010,000 oz. .

We have an inventory of 42.687 million oz of registered silver at the comex so Sept delivery of 34.010 MILLION OZ represents 79.67% of that category of silver.

If we add August’s final delivery (to Sept) for silver at 5.51 million oz, we have a total of 39.52 million oz delivered upon with a REGISTERED INVENTORY of 42.6876 million oz or 92.58% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:60,617// est. volume today// poor

Comex volume: confirmed yesterday: 83,937contracts ( poor)

END

GLD AND SLV INVENTORY LEVELS

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

GLD INVENTORY: 940.549 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

CLOSING INVENTORY 480.549 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Calling The Fed’s Bluff: They Are Holding A Losing Hand

WEDNESDAY, SEP 28, 2022 – 09:45 AM

The Fed has talked a big game lately. Many people (including me) assumed the Fed would fold a long time ago. There is a very good reason — the Fed will crush the economy and the US Treasury with higher interest rates.

In reality, the Fed is holding a losing hand and trying to bluff its way to victory.

The following analysis is by SchiffGold’s data analyst.

So far, the Fed has defied the skeptics, stuck to its guns, and pressed forward. Despite the hawkish stance, we can actually still be sure the Fed is bluffing.

Everyone knows that at some point the higher interest rates will prove catastrophic. Putting a precise timeline on it is difficult, but also not impossible. Someone can actually run the numbers and see when the Fed will be forced to show their cards. So that’s what I did.

How?

I started with data published by the Treasury that shows their entire debt schedule each month down to the Cusip level. It shows the maturity dates and the interest rates. First, I ran a mini-Monte-Carlo using different fixed rates to see the general impact. Next, I combined the Treasury data with the Fed’s own forecast. As debt rolls over, I replaced maturing debt with new debt at the Fed’s forecasted rate.

I made a few assumptions for simplicity:

- The calculation was only run on Marketable debt, specifically Bills, Notes, and Bonds

- I added $100B a month in new debt plus the additional interest expense

- I applied the same rate to all maturity levels (the yield curve is currently inverted but also pretty flat relative to history)

- When debt rolls off, I replace it with the same maturity schedule (e.g., 2-year notes roll back into 2-year notes)

Let’s start with the mini Monte Carlo using different interest rates.

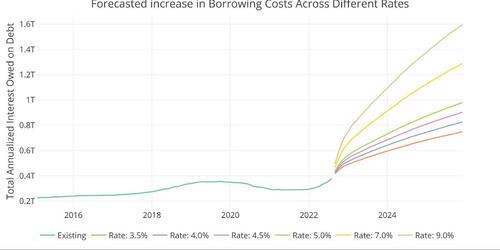

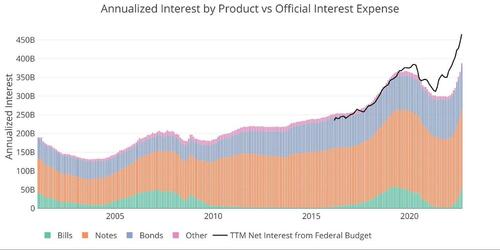

Figure: 1 Comparing Different Rates

Bam! Even the most conservative case (3.5%) shows that the debt gets unruly in a hurry. Under this scenario, the treasury is paying $600B a year in interest by January 2024. That is more than double the interest expense as recently as February 2022. Yes, double! And this is the scenario if the Fed were to freeze raising rates right now!

But, noooooo. The Fed needs to show they are serious. Powell is the new Volker and he has to prove it or the Fed could lose all credibility. So, last week they doubled down on their bluff. By the end of the year, they now anticipate rates at 4.4% rising to possibly 5% next year.

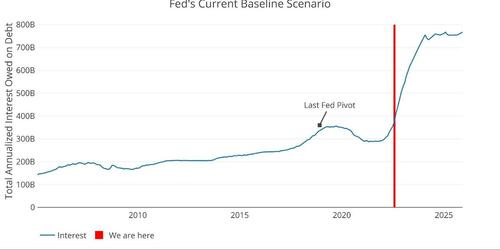

OK fine, let’s actually create this exact scenario. 4% in November, 4.4% in December, 5% in March 2023 for a full year, and then slowly lower rates in mid-2024 back to 3% by 2025. This is the Fed forecast.

Figure: 2 The Current Fed Scenario

Take a minute to digest the chart above. Note how the next few months look relative to the last 20 years. This is not just a little extra strain on the economy. By Jan 2024 the Treasury will be hemorrhaging $740B in interest! That is almost $500B more than the Treasury was paying in 2021. Half a trillion dollars a year more in interest… in 15 months!! Remember when people freaked out about sending Ukraine $40B? This is 12x higher!

These are not made-up numbers or a worst-case scenario. This is using actual Treasury data against the Fed’s actual base case scenario. This is what’s going to happen if the Fed sticks to its current plan. Remember in 2018 when the Fed had to fold cause the market threw a fit? It’s marked on the plot above in case you forgot. Well, we just blew past that level in June.

The Fed is moving much faster this time, but the data is still on a lag. It’s going to take time for the Fed to notice when they have actually broken something. I’ll let you in on a secret though, they have already broken something… they just don’t know it yet (or maybe they do – just look at the currency markets). They moved slower in 2018, they had time to watch the data and see when the market started to convulse. It then took time for the interest level to peak and come back down after the pivot.

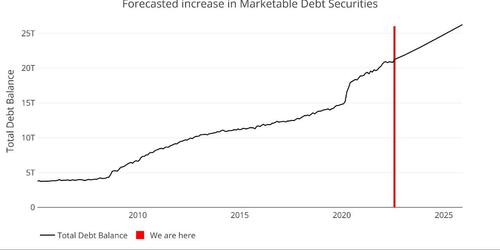

By the time they realize what they have done this time, it will probably be too late. Under this baseline scenario, debt will increase by a whopping $5T by the end of 2025. That is less than 40 months away.

Figure: 3 The Debt Forecast

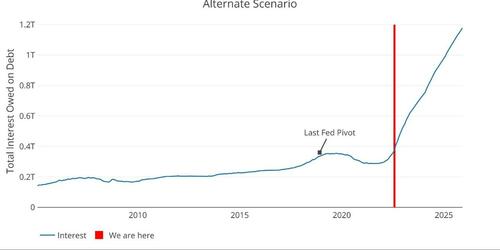

But wait. At every meeting, the Fed has gotten more hawkish. What if they dial things up again? They just went “all-in” at the September meeting. What if their next move is to pull out their car keys and drop them into the pot?

Let’s run this as an alternate scenario. Let’s assume that inflation is still high in 12 months and 5% rates are not enough. Instead of lowering rates back to 3%, they have to raise them up to 6% over the following year.

This is not a low-probability scenario. This is a very real risk. In this scenario, the Treasury is paying $1.17T per year just on interest by 2025. Yes, that is about $900B a year more than they were paying in 2021, or more than 4X higher!

This is a runaway freight train that will decimate the Federal budget, not to mention the entire economy. But don’t worry, the Fed is committed and “will do whatever it takes to get inflation back to 2%”. Yeah, okay – I will take one more look at the chart below and call that bluff ALL DAY LONG.

Figure: 4 The Interest Forecast – Alternate Scenario

I know what you’re thinking “Wow, that is one ugly chart!”

Oh, but wait, it gets worse.

Remember that this calculation is done on just Bills, Bonds, and Notes. This calculation had been a good proxy for total interest owed on the debt which also includes things like I-Bonds, Tips, Non-marketable debt, etc. This can be seen in the next chart below where the black line tracked nicely with the bar chart. The black line is pulled direct from the Treasury Monthly Statement. That is the actual interest paid as reported by the Treasury.

As you can see, the black line has pulled away from the calculated interest starting with Covid. The Treasury is paying a lot more interest across many different instruments. Unfortunately, the data provided via the treasury API is not good enough to run this calculation on the other instruments.

My point is that the above scenarios are underestimates. They only consider one portion of the debt, albeit the biggest portion, but actual interest is rising even faster!

Figure: 5 Net Interest Expense

So, what’s my point?

When you are deep in a hole and your cards are terrible, you have two choices. You can fold or bluff. If you bluff, you must do it effectively enough that you scare everyone out of the hand.

Unfortunately for the Fed, they played their hand wrong. This isn’t pre-Flop anymore. Pre-flop the Fed had horrendous cards but called. They went with “average inflation targeting”. Once that blew up in their face with a brutal flop, they checked again. This time with “inflation is transitory”. Whoops.

Then the Turn came and they realized they can’t just keep calling, they actually need to get everyone else out of the hand. So, they bluffed. They bluffed big! Unfortunately, it’s too late. Everyone is pot committed and The River is coming quickly! Just look at the charts above. Look at the red bars… this is not happening in 2-3 years. This is happening right now!

Not only is the debt spiral currently underway, but the economy now faces a slew of risks:

- What if falling liquidity in the bond market creates a spike in rates?

- What if the recession causes tax revenues to fall and borrowing to increase?

- What if the recession gets worse?

- What if China invades Taiwan?

- What if a corporate bankruptcy sets off a domino effect?

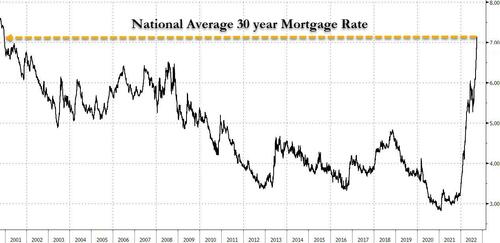

- What if the housing market falls due to spiking mortgage rates?

- What if the completely lopsided long-dollar trade unravels?

- What if the long-dollar trade continues and foreign currencies start to collapse?

- What if inflation doesn’t come down?

- What if the financial markets freeze because there is a credit event somewhere?

- What if the market cannot absorb all the new debt issuance and rates go up even more?

- What if Congress responds to any of these possibilities with more spending?

- What if new debt exceeds $1.2T a year?

None of these hypotheticals are far-fetched. I would argue each has a ~50% probability. That means the odds of none of these things happening is 0.02%. Said differently, there is a 99.98% chance that something besides the debt spiral also blows up. So, when one of these events does happen, the alternate scenario in Figure 4 becomes the best-case scenario. Remember that one? Where the Treasury is spending over $1T a year on interest? That’s called Game Over.

There is absolutely no way the Fed will sit by and continue raising rates, but somehow the Fed has the market convinced they are in control and will not pivot too early. The Fed has bluffed as hard as they possibly can. They have thrown the entire currency market into chaos. Even if they don’t care about foreign currencies or the economy, they cannot escape the laws of math. They have less than 6 months, 12 months tops. Either they pivot or the Treasury enters a debt spiral and the economy follows suit.

I get that Europe is a mess and China’s real estate market is falling apart. The Pound and Yen are both crashing. But just because all the boats around you are sinking faster than yours doesn’t mean you are safe. Get on board a real safe haven like gold or silver.

The physical gold and silver market can see what’s coming. That’s why deliveries are spiking and metal is flooding out of the vaults. The paper market looks depressed, but the physical market is a few steps ahead.

They don’t ring bells at the top or bottom, but right now the math is ringing the bell pretty darn loud. Are you paying attention?

US Debt interactive charts and graphs can always be found on the Exploring Finance dashboard: https://exploringfinance.shinyapps.io/USDebt/

END

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

Rickards: How Far Could Stocks Fall?

WEDNESDAY, SEP 28, 2022 – 09:06 AM

Authored by James Rickards via DailyReckoning.com,

The stock market was down again yesterday, the exchanges beginning where they left off last week. But it’s the larger trend that’s really disconcerting.

Investors don’t need to be told about the stock market collapse in recent months. The Dow Jones Industrial Average is down over 20% since January. The S&P 500 is down 23% since January. And the Nasdaq Composite is down 32% since its all-time high last November.

Those falls are not as bad as the crashes in March 2020 during the pandemic or late 2008 during the global financial crisis, but those comparisons offer little comfort since they were among the worst in history.

The real problem for stock investors today is not that the crash is bad so far, but that it might just be getting started.

We may be looking at losses that more closely resemble the over-80% collapse of the Dow Jones from 1929–1932 or the 80% collapse of the Nasdaq in 2000–2001 in the wake of the dot-com bubble.

Different Causes, Same Outcome

The culprit this time will not be reckless mortgage lending, Chinese viruses or sock puppet spokespersons. The danger is the much higher interest rates needed to squash global inflation.

Rates have been going up since last spring, but inflation continues at very high levels. The question for analysts and investors is how high will rates have to go before inflation falls to levels deemed acceptable by central bankers.

Most observers have connected the interest rate hikes with the fight against inflation, but relatively few have realized the full implications. The real key to fighting inflation is to do so by increasing unemployment.

Fed Chair Jay Powell had a lot to say at a press conference following last Wednesday’s decision to raise interest rates another 75 basis points (the Fed’s third consecutive 75-basis-point increase).

Job One

Powell began by emphasizing that stopping inflation was Job One. He said, “Without price stability the economy does not work for anyone.” He noted that “Growth in consumer spending has slowed.”

His key phrase was “The labor market has remained extremely tight… Job openings are incredibly high… They need… to come down.” That’s Powell’s way of saying higher unemployment is the key to lower inflation.

Powell also said, “We think that we’ll need to bring our funds rate to a restrictive level and to keep it there for some time.” Restrictive level means a level that will cause inflation to drop toward the desired target over time.

When asked when restrictive policy levels will be reached, Powell said “There’s a ways to go.” To emphasize the point, Powell also said, “We’re committed to getting to a restrictive level… and getting there pretty quickly.”

The Endgame

What is the Fed’s target exactly?

Powell said the target was “to bring inflation down to 2%,” the Fed’s desired rate. When asked about the 2% inflation target, Powell said “We can’t fail to do that.” He went on to say, “We have got to get inflation behind us. I wish there were a painless way to do that but there isn’t.”

You get the point.

Rates will have to go to 4.75% (from the current level of 3.0%) in the hope that inflation (as measured by core PCE year over year, the Fed’s favorite gauge) drops from 4.6% to 3.5%.

At that point, real rates will be over 1.0% and the Fed will wait as long as a year for inflation to drop from 3.5% to the Fed’s target of 2.0%.

The real takeaway here is that Powell is dead serious about hitting a 2% inflation target. It seems he’ll raise rates as long as it takes to get there. He’s in a hurry to do so. And he was completely candid about the fact that there would be economic pain in the process.

Unfortunately, the cost will be a severe recession and a rise of unemployment to 5% or higher with millions of job losses, massive business failures, billions of dollars in bad debts and a continued crash in stock prices.

Will Powell Back Down?

This suggests some critically important questions for markets. Will Powell actually have the stomach to force rates up to 4.75%, about where they need to go to slow inflation?

Based on his remarks, the answer is yes. But we’ll have to wait and see.

The Fed was raising rates and reducing its balance sheet when on Dec. 24, 2018, the stock market tanked and proceeded to fall 20% in 2½ months. Powell panicked and pivoted again to monetary easing. Maybe he’ll do it again.

But there’s an important difference between then and now. There was no inflation to speak of in 2018. The Fed could therefore afford to pivot to easing without any real concern about inflation.

That’s obviously not the case in late 2022. Inflation is the Fed’s biggest concern right now, and Powell is making it clear that he’s serious about getting control of it, even if it results in a lot of economic and financial pain.

All Pain, No Gain

The problem, which I’ve addressed many times, is that the Fed has misdiagnosed the nature of today’s inflation.

The Fed is trying to crush inflation by reducing demand in the economy. They’re focusing on “demand pull” inflation where consumers are buying in anticipation of even higher inflation to come.

But the inflation we’re seeing is called “cost push” inflation. This comes from the supply side, not the demand side. It comes from global supply chain disruptions and the war in Ukraine.

Since the Fed has misdiagnosed the disease, they are applying the wrong medicine. Tight money won’t solve a supply shock. Higher prices will continue. But tight money will hurt consumers, increase savings and raise mortgage interest rates, which hurts housing among other things.

So the question is how much damage will Powell’s quest do to the economy and markets? That’s the biggest issue for investors. The answer is that Powell will do far more damage than he expects.

History shows that the Fed will overshoot. There won’t be any “soft landing.”

That damage may help Powell get to his inflation target. But it will increase unemployment and destroy stock markets along the way.

That’s if all goes according to plan. The actual scenario could be worse. Market investors are not ready for this.

But you should be.

END

3.Chris Powell of GATA provides to us very important physical commentaries

GLOBAL FINANCIAL STORM OF EPIC PROPORTIONS

Egon von Greyerz

September 28, 2022

As the dark years are approaching, the world is now approaching survival mode. Admittedly, if you go to a high class restaurant in New York, London or Zurich, there are no signs of misery but instead of incredible affluence.

What is happening to middle America or England has not yet reached Wall Street or the City of London where exquisite food is plenty and excellent wines are flowing.

This is of course no different to the end of eras with major excesses and decadence. It was the same at the peak of the Roman Empire 2000 years ago or in 1929 just before the Dow crashed 90%.

Main Street is already in survival mode with cost of living increases of a magnitude that ordinary people can’t afford. Energy, fuel, food, mortgage rates, rents and most things have gone up by 10-20% or more in the last year.

MORE ABOUT EXTREME RISK AND GLOBAL WARNING AT THE END OF THIS ARTICLE

Everything has happened so quickly that people are in shock. But it is a fact that real MISERYhas now hit ordinary people.

As Charles Dickens wrote in David Copperfield:

Annual income twenty pounds,

annual expenditure nineteen six,

result happiness. Annual income

twenty pounds, annual

expenditure twenty pound

ought and six, result misery.

For Main Street it is no longer a question of making ends meet but of economic survival.

The Fed and other so called “independent” central banks are doing all they can to exacerbate the crisis. The Fed’s official two tasks are stable inflation and full employment.

Stable inflation the Fed has in latter years defined as 2%. How did they arrive at that? They probably don’t know themselves since there is nothing good about 2%. Because an annual inflation rate of 2% means that prices double every 36 years which is highly undesirable.

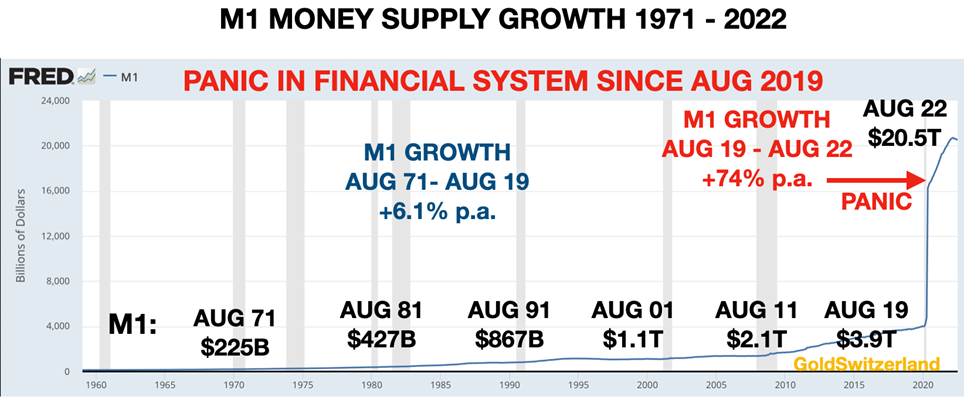

Anyway, even with pumping up M1 Money supply by $19 trillion between 2006 and December 2021 and keeping interest rates at 0% they still don’t have a clue why inflation is going up.

Many of us were laughing at Powell and Lagarde when they called the increase in inflation transitory!

Whilst clueless central bank heads are transitory, current inflation certainly isn’t.

HYPERINFLATIONARY ROCKET

It is absolutely incredible that the heads of the Fed and ECB, the world’s biggest central banks, didn’t have the basic knowledge to fathom that unlimited free money for over 10 years is like a matchstick to light the biggest inflationary rocket in history.

Yes, it seemed to take a long time before the inflation rocket was set alight. The explanation is self-evident. There were different compartments in the rocket. Before the consumer prices were set alight, the inflation flame reached all the financial assets such as stocks, bonds and property.

Between 2009 and January 2021, the Nasdaq for example went up 16X, the S&P 7X and house prices went up 2X.

But conveniently for the Fed, this Hyperinflation in asset prices doesn’t count as inflation.

So the Fed could continue to fulfil its main purpose which is to make the rich richer. As the Fed was conceived by private bankers in Jekyll Island in 1910 for the main purpose of enriching the bankers and their friends, it is clear that this Elite group must be looked after first.

ZERO INFLATION AND ZERO INTEREST RATES

In the autumn of 2021, as the inflation flame reached consumers, the Fed, ECB and other central banks were stuck in their zero inflation and zero interest rates lethargy.

But as 2022 progressed, central banks around the world woke up to the fact that inflation is here to stay. Since the wealthy probably have diversified into real assets by this stage, it was then time for the bankers to start tightening without hurting their wealthy friends.

Globally the Fed and their fellow banks, are without exception always behind the curve. So they flooded markets worldwide with worthless printed money at zero cost for much too long.

And now they are waking up to the fact that the accelerated money printing (debt creation) since 2019 is not just inflationary but hyperinflationary. So the inflation rocket is now fully ignited and has just started its journey.

Powell, Lagarde and at least 32 other central bankers in the world have gone from lethargy to panic mode and are thus coordinating a series of rate increases globally.

MONEY PRINTING TO INFINITY

Since ordinary people in the world are now suffering substantially due to massive inflation of everyday expenses, they no longer can make ends meet.

The next move we will see in many countries is the resumption of money printing or QE. In the UK, the new Chancellor Kwarteng (finance minister), decided to give major support to businesses and individuals with lower taxes and social charges, energy subsidies etc. The total cost will be in the hundreds of billions of pounds over coming years. The already weak pound fell another 5% and rates surged. The pound is now down 24% since May 2021.

So the consequences of this give-away UK budget will be higher inflation and higher cost of living for people. This is a vicious cycle that will be followed by most nations as they enter the race to perdition.

THIS TIME IS DIFFERENT!

Stock market investors have for decades been so uber-confident of their banker friends saving them from any major losses that any fall in the market is a buying opportunity.

Thus we have a whole generation of investors that have never seen a sustained bear market as they have always been saved by central banks.

But this time is different! Take my word for it. Central banks are now on a course to deflate all asset markets. As usual they will go on for longer than anyone expects.

And eventually it becomes a vicious cycle with higher rates, higher inflation, still higher rates and more inflation until both central banks and markets panic as the world enters a depressionary hyperinflation.

It might be difficult to fathom that we can have a depression and hyperinflation simultaneously. But as asset prices collapse (remember they are not measured in the inflation numbers), prices of consumer products will surge.

And that is exactly what we are seeing the beginning of now.

Stocks are down around 25% so far, bonds are down, property markets under pressure and food, energy, fuel, mortgage rates are doubling or trebling for many borrowers.

IT AIN’T OVER UNTIL THE FAT LADY SINGS

This is the perfect storm. But remember it has only just started and as I have stated in numerous articles and interviews, this won’t be over until the fat lady sings.

When will she sing? Well, if this is the end of a very major cycle as I believe it could be, it might be a decade or longer before she sings.

We must of course remember that nothing goes straight down and there will be violent corrections that initially will make investors euphoric. But most reactions will be short lived so buying the dips could be very dangerous.

We should first see hyperinflation taking hold properly and stock and property markets go down by at least 75% and possibly 95%. Bonds won’t stop going down until rates are 20%+. Many bonds will go to ZERO as borrowers default, including many sovereign states.

The US or EU won’t call it a default. They will just create a new currency like a CBDC (Central Bank Digital Currency) and with a magic wand make all the debt they have created disappear.

But you can’t make debt disappear without consequences. If debt is written off or swept under the carpet, the value of the assets that the debt supported will also implode. And that is how the world goes from a depressionary hyperinflation to a deflationary depression. At that point, much of the financial system will default.

The above scenario is the inevitable consequence of a world that has lived above its means for a century and especially since 1971. Few people realise for example that the US has increased its debt for 90 years with just a handful of years exception.

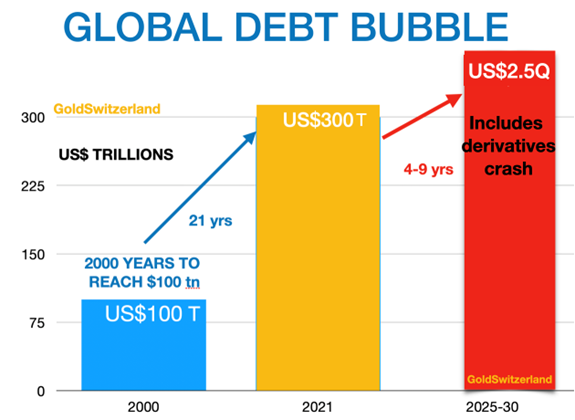

GLOBAL DEBT $2.5 QUADRILLION

With global debt, contingent liabilities and derivatives of around $2.5 quadrillion, there are a lot of assets/liabilities which need to implode before the world can show healthy and debt free growth again.

EPIC MONEY PRINTING BONANZA

Before the deflationary implosion, the world will experience the most epic money printing and debt creating bonanza in history. That will mark the last desperate attempt by central banks and governments to solve a debt problem with more worthless debt.

This bonanza will be a grand finale of the fireworks which will mark the end of another era of financial and economic failure.

Boom and busts are of course a feature of economic cycles and have always happened in history. What the world is experiencing for the first time is a global event with every country and every central bank involved. So the magnitude is so much greater this time and that by a massive margin.

Like with all forecasts, we are here talking about probabilities. As we all know, there are few certainties in life. But we do know that risk is higher than at any time in history. Never before has the world experienced epic bubbles of this magnitude on a global level.

As a friend of mine states, it might happen but not in my lifetime. This attitude is part of sound human optimism that “it won’t happen on my watch”. But now is not a time to be overconfident but to be humble and prepared.

Anyway, we are talking about risk and not certainties. And when risk is high we must be prepared and protect ourselves. Remember that no one will sell you fire insurance after the fire has started.

What we do know for certain is that future historians will tell the world what really happened and when. I would love to come back down to earth for a short while to experience future experts and historians say that this was the most obvious collapse in global history. And still virtually no one sees it today.

Well, as I often say: “Hindsight is the most exact of all sciences!”

WHEN RISK IS EXTREME EXTRAORDINARY CAUTION REQUIRED

Stocks

In my articles since mid August, I have warned about Epic Collapses of Stocks, Debts, Currencies etc and 30% Stock Crash.

Well the crash is here and now. The S&P is down 15% since mid August and another fall of the same magnitude is quite probable in the next couple of weeks. But even if that fall takes place and we see a temporary pause and correction, the secular bear market has only started.

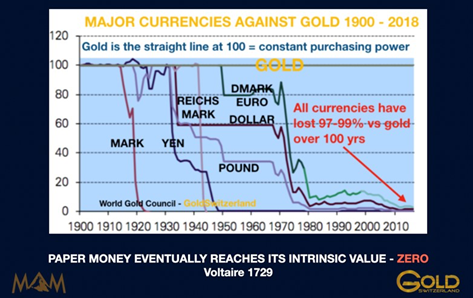

Currencies

Since 1971, the dollar and all other currencies have lost 97-99%. This is measured in real terms against the only currency which has survived in history – GOLD.

So currencies are in a race to the bottom and there is no prize for coming first in this race. All currencies can obviously not fall at the same time against each other and therefore they take turns. It has been a half century race and no currency has the stamina to be in the lead all the time.

Overall the Swiss franc has been the star performer due to probably the best managed economy in the world. When I started working in Geneva in 1969 one dollar cost me 4.30 Swiss francs. Today the same dollar costs me 0.98 Swiss francs. This means that the dollar has lost 77% against the Swiss.

To talk about a strong dollar in this case is clearly ridiculous. So for the moment the dollar is showing temporary strength. But that is likely to change relatively soon as it catches up on the downside.

When the current monetary era comes to an end within possibly 5-8 years all currencies will be worth ZERO. This is no different from any monetary era in history.

Gold

Out of laziness and convention gold is measured primarily in US dollars. Even in UK, Germany or media for example, it is always the dollar price of gold quoted.

But just as UK or German house prices are not quoted in dollars nor should gold. If the pound or euro is your base currency, you should measure gold in that currency.

The absolute correct way is of course to quote gold in grammes. What is the purpose to measure REAL money – GOLD – in a fiat currency when fiat currencies always go to ZERO over time. Yes, it might feel good to measure gold in a depreciating currency but it certainly doesn’t reflect the real value of gold.

Gold measured in dollars is temporarily weak. But has very little to do with gold but with the dollar which currently is overvalued.

If you measure gold in euros, pounds, yen, Australian dollars etc, gold is very near the highs. It will soon be in US dollars too.

The Wall Street Journal just had a major article with the title “Gold loses status as haven.”

Without exception, these articles always appear at the bottom of a market.

BANKING SYSTEM – GLOBAL WARNING

Investors’ financial health is now under serious attack.

If as I believe, stocks are entering a secular bear market and won’t stop until they are down 75-95%, most investors are in severe trouble. If also bonds and property will crash, there are few safe asset classes left.

Gold and silver stocks have major upside potential. But if held within the financial system they are subject to custodial risk. Better to hold these stocks with direct registration.

With the current problems in financial markets, combined with global debt levels, including derivatives, the heavily leveraged and fractured banking system is also extremely risky.

All banks globally are now under pressure as the debt crisis deteriorates and most debtors cannot service their debts at these higher interest rates. Next step will be that banks will experience a major increase in bad debts as well as accelerating defaults.

The strong dollar will also put a massive burden on dollar loans globally and especially emerging markets.

With the problems in Europe, most European banks are now extremely fragile.

If we add to that the $2 quadrillion derivative bubble, the world is now approaching a financial storm of historical proportions.

Personally I would not keep any major amounts of liquidity within the financial system.

WEALTH PRESERVATION

The ultimate form of wealth preservation is gold and silver.

But it serves no purpose to hold your wealth preservation assets within a risky banking system. Even worse of course to hold paper gold or silver in ETFs or other fund structures.

Substantial amounts of physical precious metals are held within the major Swiss banks. The two biggest Swiss banks are heavily leveraged and are running from one major credit or derivative loss to the next in the billions of Swiss francs. And they are changing top management almost as fast as ordinary people change their shirt. Definitely not a sign of health.

Gold and silver should be held in physical form in your own name with the facility to access it personally.

Precious metals held in banks are not insured.

Insurance companies are likely to incur major losses on their assets as their primary investments of stocks and bonds crash in value. Therefore it is essential to hold metals in vaults that are safe without insurance.

Remember that there will be shortages of many products including food and other essentials so keep some reserves.

Sadly the world is now entering the Dark Years as I have discussed in many articles.

But remember that after having prepared yourself, the most important things in life are family and friends. That is a support circle which will be the most critical in coming years.

END

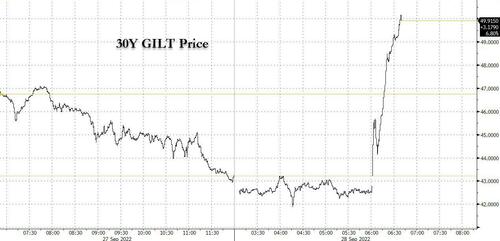

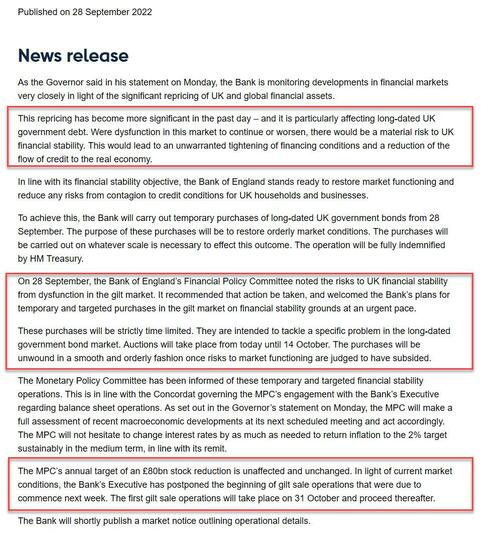

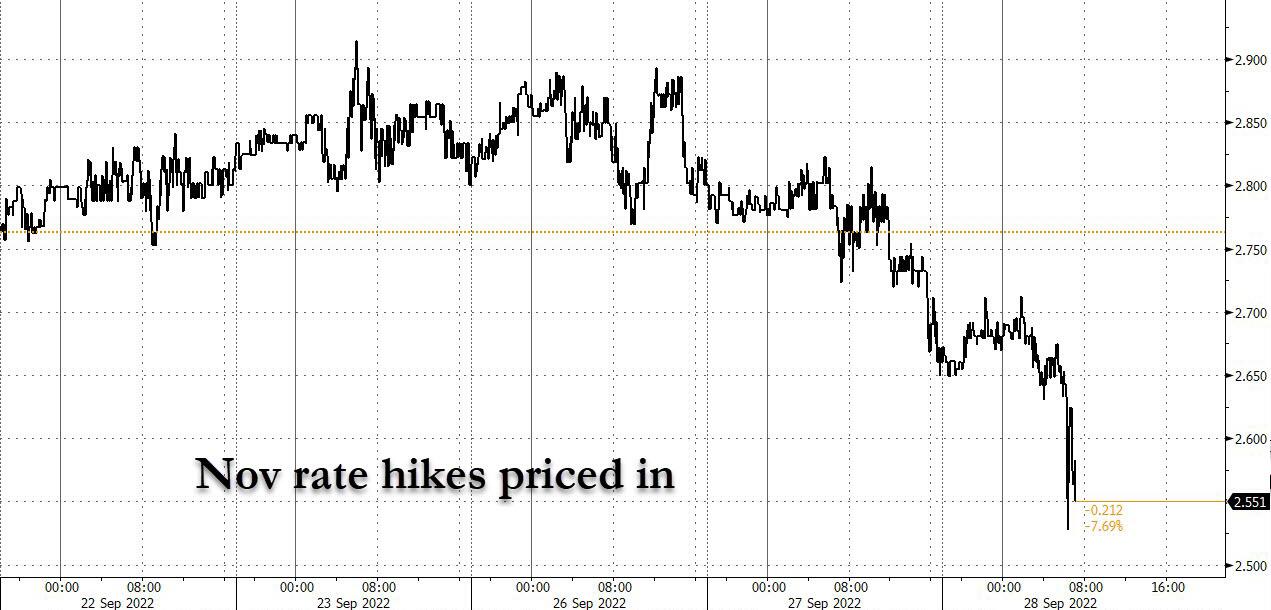

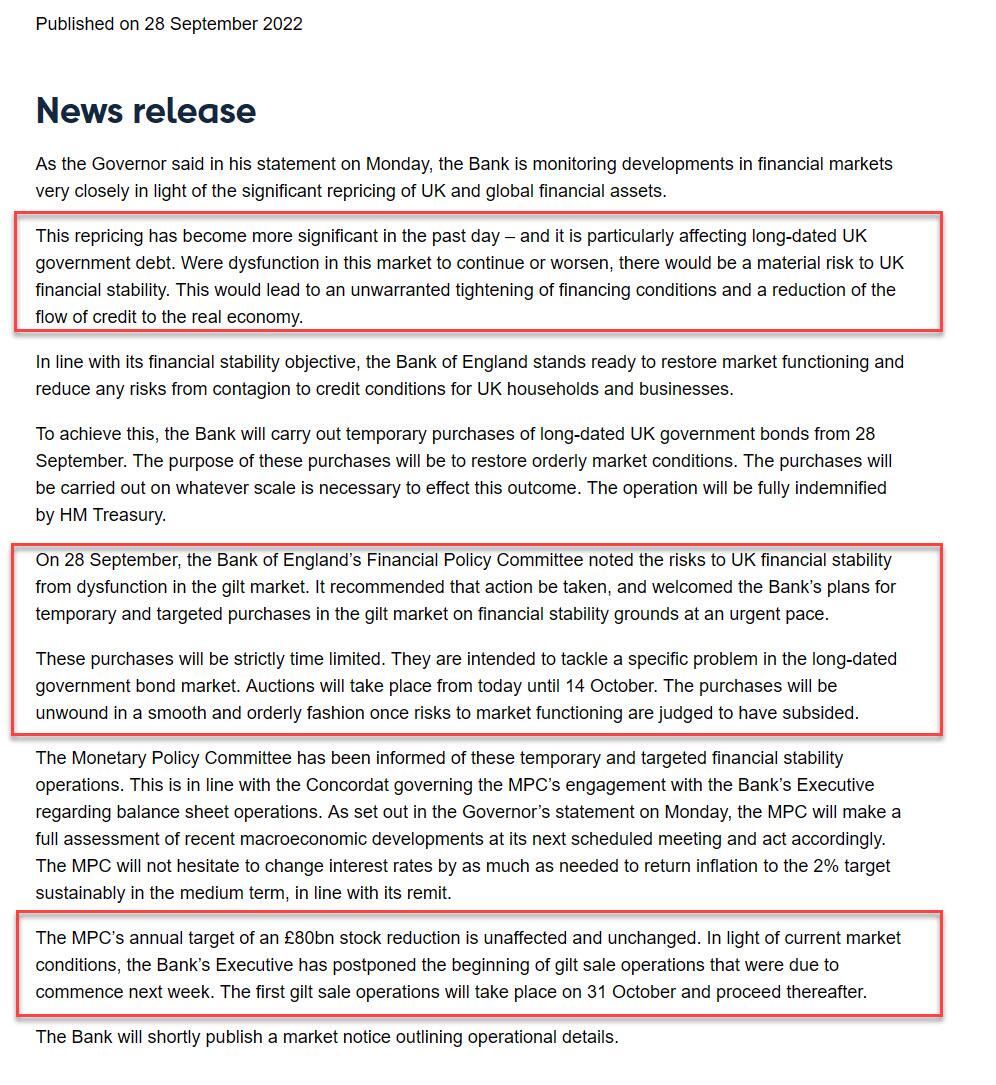

Gold in GBP Jumps as UK Deficit Crisis Sees BoE Tries to Suppress Gilt Yields

Adrian Ash – Wednesday, 9/28/2022 13:31

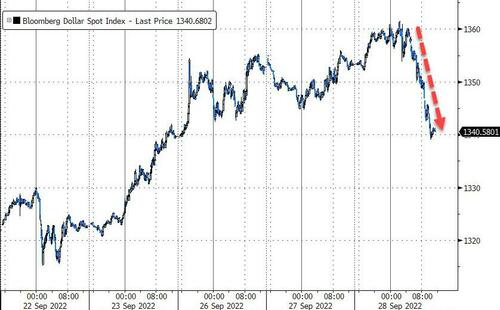

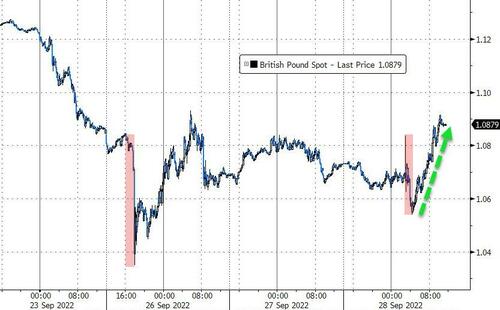

GOLD PRICES set new 2.5-year Dollar lows on Wednesday before rebounding in terms of all major currencies as the Bank of England stepped in and bought UK government debt in a surprise intervention, calling the slump in Sterling and Gilt prices a “dysfunction” while trying to suppress Gilt yields following new Chancellor Kwasi Kwarteng’s near-universally decried deficit-tax-cutting budget of last Friday.

Crude oil ticked higher and natural gas repeated yesterday’s 5% rise for European December contracts, but other commodities fell alongside global stock markets as the Dollar pushed the Euro below $0.95 to hit fresh 2-decade highs on its trade-weighted major currency index.

With the Dollar price of gold then bouncing $15 from a new 2.5-year low of $1615 before dropping back to $1625, the Euro price of gold rose back above €1700, some 13.4% higher from this time last year.

Gold for UK investors meanwhile jumped back to £1540 following the UK central bank’s sudden news, up 20.0% from this point in September 2021 but £40 below this week’s re-touch of gold’s all-time GBP high.

The UK gold price in Pounds per ounce has now touched that record £1580 level 3 times, first during the Covid Crisis of summer 2020, then during the Russian invasion of Ukraine crisis in March 2022, and then once again this Monday during the sudden UK government debt crisis.

Having failed to raise overnight UK rates by the 0.75 points widely expected at last Thursday’s regular policy meeting, “Were the significant repricing of…long-dated UK government debt…to continue or worsen, there would be a material risk to UK financial stability,” said the Bank of England today.

“This would lead to an unwarranted tightening of financing conditions and a reduction of the flow of credit to the real economy,” it went on, promising to detail the size of its intervention “shortly”.

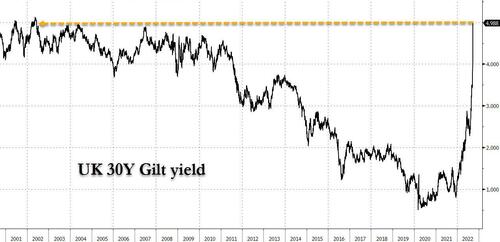

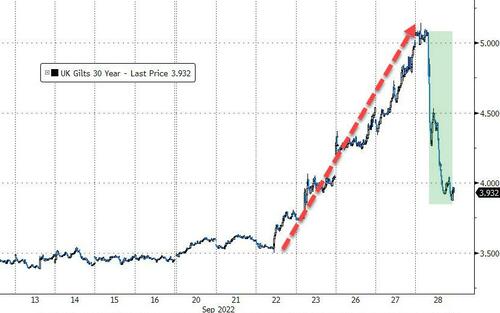

Prices for 30- year UK Gilts had fallen so hard overnight that the yield demanded by new buyers jumped above 5% per annum, up more than 2 whole percentage points to the highest since 2002.

Today’s BoE announcement saw that drop 75 basis points before rising back above 4.5% – itself a fresh 11- year high when reached in Monday’s Gilt crash.

This marks “a very successful and important intervention…the right thing to do,” according to former deputy governor of the Bank, now Professor Sir Charlie Bean.

“This is……bad,” says the Financial Times‘ economics editor, in contrast.

“It is actually incredible,” adds a Conservative MP quoted by a Sky News reporter.

“The UK central bank has had to step in to protect the UK from the actions of the UK’s own government!”

Having cut tax without cutting spending in Friday’s “mini budget” to need an additional £1 by April for every £7.65 already owed to Gilt market investors, Kwarteng himself meantime held talks with leading investment-bank and other financial-firm bosses in what the BBC calls a “crisis” meeting.

With lenders unable to price new home-loans amid the chaos in UK borrowing costs, almost 1-in-4 mortgage products were withdrawn by lenders on Tuesday according to MoneyFacts, slashing the total to just half the number available at the start of December, before the Bank of England finally raised its key overnight rate from 0% to reach 2.25% last week.

UK inflation in August ran just below 10% per year.

“Given elevated inflation pressures in many countries, including the UK, we do not recommend large and untargeted fiscal packages at this juncture,” the International Monetary Fund said overnight,, feeling it necessary to release what pundits called a “scorching” statement on Friday’s deficit announcement despite having “engaged with the [UK] authorities” on the matter and warning that household inequality will widen.

“This is the IMF self-declaring as a left-wing body,” said one pro-Government UK pundit on Wednesday.

“You really think this is about tax cuts?” said another.

“What the Sterling sell-off may have reflected…is the belief that this budget has made a Labour victory more likely.”

“[But] large unfunded tax cuts will lead to structurally higher deficits amid rising borrowing costs, a weaker growth outlook and acute public spending pressure stemming from the pandemic and a decade of austerity,” says ratings agency Moody’s, cutting its 2023 GDP growth forecast for the UK from 0.9% to 0.3% and warning it may downgrade the UK’s credit status.

“A sustained confidence shock arising from market concerns over the credibility of the government’s fiscal strategy…could more permanently weaken the UK’s debt affordability.”

With Wednesday’s rally in UK Gilt prices and the retreat in Gilt yields bucking another wide sell-off in European and other rich-world government bonds today, “Longer-dated sovereign notes in most developed markets are starting to look appealing,” Bloomberg says, quoting US investment giant J.P.Morgan and noting that “yields are at levels last seen in 2010.”

5.OTHER COMMODITIES: URANIUM

COMMODITIES IN GENERAL/EGGS

END

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.2354

OFFSHORE YUAN: 7.2411

SHANGHAI CLOSED: DOWN 48.79 PTS OR 1.58%

HANG SENG CLOSED DOWN 609.43 PTS OR 3.41%

2. Nikkei closed DOWN 397.89 PTS OR 1.50%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 114.47/Euro FALLS TO 0.95707

3b Japan 10 YR bond yield: FALLS TO. +.242/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 144.67/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.268%***/Italian 10 Yr bond yield RISES to 4.82%*** /SPAIN 10 YR BOND YIELD RISES TO 3.46%…** DANGEROUS

3i Greek 10 year bond yield RISES TO 4.97//

3j Gold at $1635.65silver at: 18.28 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 20/100 roubles/dollar; ROUBLE AT 58.25//

3m oil into the 78 dollar handle for WTI and 86 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 144.47DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9865– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9442well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.919 DOWN 4 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.844 UP 2 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

USA DOLLAR VS TURKISH LIRA: 18,54…GETTTING DANGEROUS

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Futures Rebound From 2022 Low After Bank Of England Panics, Restarts Unlimited QE

WEDNESDAY, SEP 28, 2022 – 07:53 AM

With everything biw breaking, including an explosive move in bond yields in the UK, 10Y yields rising above 4.00%, and Apple “suddenly” realizing there was not enough demand for the latest iteration of its iPhone 5, it was only a matter of time before some central bank somewhere capitulated and pivoted back to QE, and this morning that’s precisely what happened when the BOE delayed the launch of QT and restarted QE “on whatever scale is necessary” on a “temporary and targeted” (lol) basis to restore order, which sent UK bond surging (and yields tumbling the most on record going back to 1996 erasing an earlier jump to the the highest since 1998)…

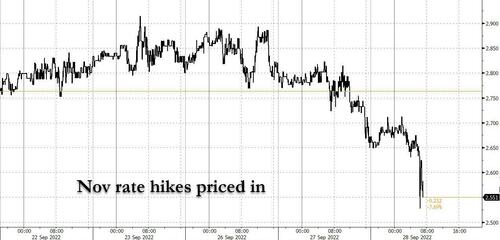

… the pound first surged before falling back as traders realized the UK now has both rate hikes and QE at the same time, the dollar sliding then spiking, the 10Y US TSY yield dipping from 4.00%, the highest level since 1998, and stock futures spiking from fresh 2022 lows, but then fizzling as traders now demand a similar end to QT/restart of QE from the Fed or else they will similarly break the market.

Needless to say, the BOE has opened up the tap on coming central bank pivots, and while the market may be slow to grasp it, risk is cheap here with a similar QE restarted by the Fed just weeks if not days away. Indeed, look no further than the tumbling odds of a November 75bps rate hike as confirmation.

As if the BOE’s pivot wasn’t enough, there was also a barrage of company specific news: in premarket trading, the world’s biggest company, Apple tumbled 3.9% after a Bloomberg report said the company was likely to ditch its iPhone production boost, citing people familiar with the matter. Shares of suppliers to Apple also fell in premarket trading after the report, with Micron Technology (MU US) down -1.9%, Qualcomm (QCOM US) -1.8%, Skyworks Solutions (SWKS US) -1.6%. Other notable premarket movers:

- Biogen shares surged as much as 71% in US premarket trading, with the drugmaker on track for its biggest gain since its 1991 IPO if the move holds, as analysts lauded results of an Alzheimer’s drug study with partner Eisai.

- Lockheed drops as much as 2.3% in premarket trading as it was downgraded to underweight at Wells Fargo, which is taking a more cautious view on the defense sector on a likely difficult US budget environment into 2023.

- Mind Medicine slid 35% in premarket trading after an offering of shares priced at $4.25 apiece, representing a 31% discount to last close.

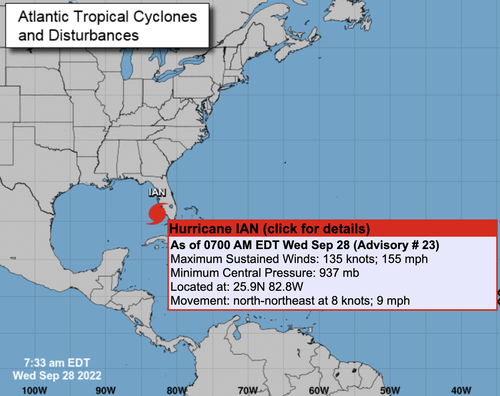

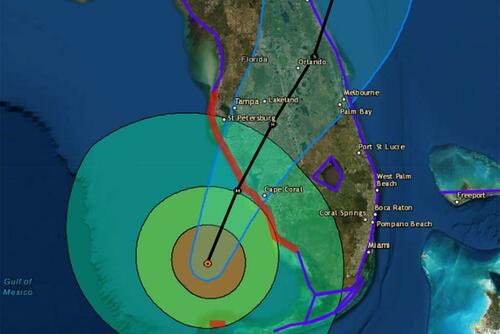

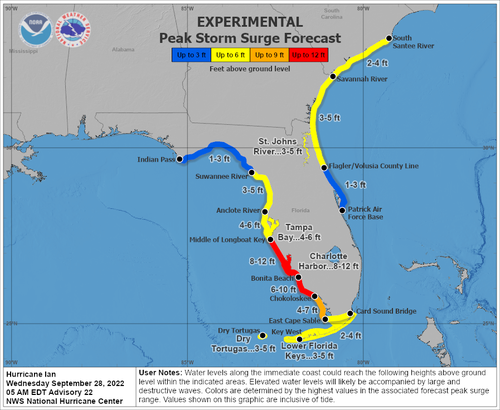

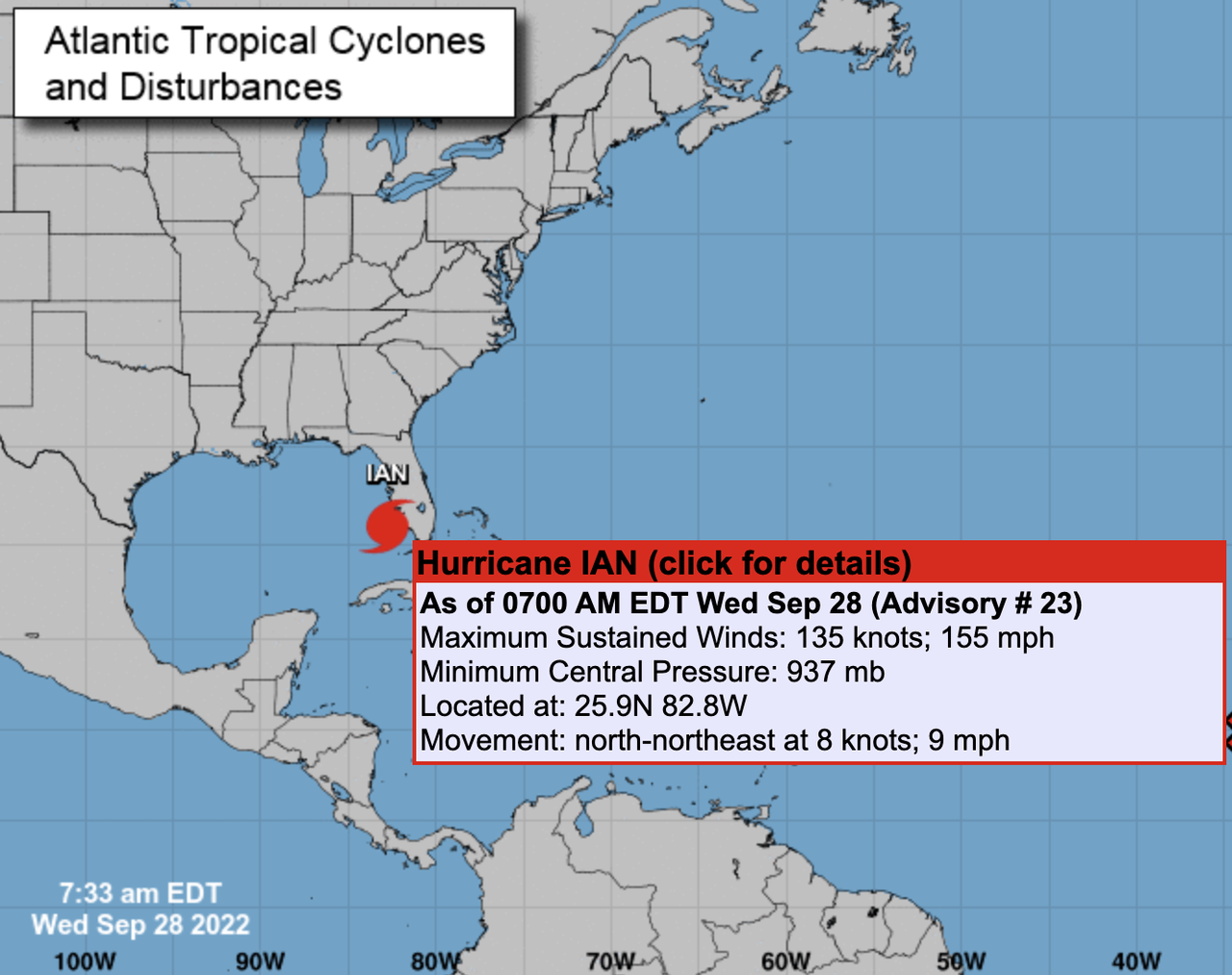

- Watch insurers, utilities and travel stocks as Hurricane Ian comes closer to making landfall on Florida’s Gulf coast.

- Keep an eye on southeastern US utilities including NextEra Energy (NEE US), Entergy (ETR US), Duke Energy (DUK US), insurers like AIG (AIG US), Chubb (CB US), as well as airline stocks

- Netflix (NFLX US) was raised to overweight from neutral at Atlantic Equities, the latest in a slew of brokers to turn bullish on the outlook for the streaming giant’s new ad- supported tier, though the stock was little changed in premarket trading

In other news, Hurricane Ian became a dangerous Category 4 storm as it roars toward Florida, threatening to batter the Gulf Coast with devastating wind gusts and floods.