by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSE: DOWN $0.85 to $1660.35

SILVER PRICE CLOSE: DOWN 15 cents to $18.76

Access prices: closes

Gold ACCESS CLOSE 1660.60

Silver ACCESS CLOSE: 18.91

OPTIONS EXPIRY TOMORROW

THEN GOLD AND SILVER WILL EXPLODE

Bitcoin morning price: $19479 DOWN 13

Bitcoin: afternoon price: $19,432 DOWN 60

Platinum price closing UP $2.10 AT $866,90

Palladium price; closing UP $62,55 at $2215,20

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,660.400000000 USD

INTENT DATE: 09/28/2022 DELIVERY DATE: 09/30/2022

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 12

435 H SCOTIA CAPITAL 10

624 H BOFA SECURITIES 234

657 C MORGAN STANLEY 2

661 C JP MORGAN 151

880 H CITIGROUP 95

905 C ADM 8

TOTAL: 256 256

MONTH TO DATE: 12,269

JPMORGAN STOPPED

GOLD: NUMBER OF NOTICES FILED FOR SEPT CONTRACT:

256 NOTICES FOR 25600 OZ //0.7962 TONNES

total notices so far: 12,269 contracts for 1,226,900 oz (38.162 tonnes)

SILVER NOTICES: 21 NOTICES FILED FOR 105,000 OZ/

total number of notices filed so far this month 6805 : for 34,025,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $.85

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: //// A DEPOSIT OF 3.30

TONNES FROM THE GLD/

INVENTORY RESTS AT 940.86 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 15 CENTS

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF OF 0.645 MILLION OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 479.904 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 709 CONTRACTS TO 129,709 AND CLOSER TO THE NEW RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.32 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.32) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SOME SPEC SILVER LONGS AS WE HAD A GIGANTIC GAIN OF1538 CONTRACTS ON OUR TWO EXCHANGES. WE DID HAVE ATTEMPTED SPEC SHORT COVERINGS WITH THE BANKERS CONTINUALLY ON THE BUY SIDE.

WE MUST HAVE HAD:

I) CONTINUAL SPECULATOR SHORT COVERINGS ////CONTINUED BANKER OI COMEX ADDITIONS /. II) WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.855 MILLION OZ FOLLOWED BY TODAY’S 15,000 OZ QUEUE JUMP / // V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: –59

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 20 days, total 14,630 contracts: 73.150 million oz OR 3.670 MILLION OZ PER DAY. (732 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 73.150 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 73.150 MILLION OZ///

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 709 WITH OUR $0.32 GAIN IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 770 CONTRACTS ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /GOOD BANKER ADDITIONS A// NET SPEC SHORT LIQUIDATIONS /// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST. OF 3.855 MILLION OZ FOLLOWED BY TODAY’S 15,000 OZ QUEUE JUMP // .. WE HAD A GIGANTIC SIZED GAIN OF 1479 OI CONTRACTS ON THE TWO EXCHANGES FOR 7.395MILLION OZ..

WE HAD 21 NOTICE(S) FILED TODAY FOR 105,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

WE HAVE 1 MORE READING DAY BEFORE FIRST DAY NOTICE

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 175 CONTRACTS TO 457,236 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE WILL PROBABLY SEE THE COMEX OI FALL TO AROUND 380,000 AS OUR SPECS GET ANNIHILATED.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED — -402 CONTRACTS.

.

THE SMALL SIZED INCREASE IN COMEX OI CAME DESPITE OUR STRONG GAIN IN PRICE OF $32.30//COMEX GOLD TRADING/WEDNESDAY / WE HAD SMALL SPREADER LIQUIDATION// SOME SPECULATOR SHORT COVERINGS ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE./. WE HAD ZERO LONG LIQUIDATION //AND CONTINUED ADDITIONS TO OUR BANKER LONGS!! THE COMEX WILL BLOW UP AS THE SPECS CANNOT DELIVER GOLD TO OUR BANKER LONGS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 8.401 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 1000 OZ //NEW STANDING 38.158 TONNES (QUEUE JUMPING = EXERCISING LONDON BASED EFP’S)

YET ALL OF..THIS HAPPENED WITH OUR STRONG GAIN IN PRICE OF $32.30 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 4967 OI CONTRACTS 15.483 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4803 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 457,236

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4978 CONTRACTS WITH 175 CONTRACTS INCREASED AT THE COMEX AND 4803 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI gain ON THE TWO EXCHANGES OF 4978 CONTRACTS OR 15.483 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4803) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (175): TOTAL GAIN IN THE TWO EXCHANGES 4978 CONTRACTS. WE NO DOUBT HAD 1) SMALL ATTEMPTED SPECULATOR SHORT COVERINGS// CONTINUED GOOD BANKER ADDITIONS/// ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 8.409 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 1000 oz. 3) ZERO LONG LIQUIDATION //// //.,4) SMALL SIZED COMEX OPEN INTEREST GAIN 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL/5/SMALL SPREADER LIQUIDATION.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

62,102 CONTRACTS OR 6,210,200 OZ OR 193,16 TONNES 20 TRADING DAY(S) AND THUS AVERAGING: 3105 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAY(S) IN TONNES: 193.16 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 193.16/3550 x 100% TONNES 5.43% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES (SLIGHTLY RISING THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT., FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER,ROSE BY A STRONG SIZED 709 CONTRACT OI TO 129,709 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 770 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 770 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 770 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 709 CONTRACTS AND ADD TO THE 770 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 15479 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 7.395 MILLION OZ

OCCURRED WITH OUR STRONG GAIN IN PRICE OF $0.32

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 3.86 PTS OR 0.13% //Hang Seng CLOSED DOWN 85.01 PTS OR 0.48% /The Nikkei closed UP 248.07PTS OR 0.95% //Australia’s all ordinaires CLOSED DOWN 1.51% /Chinese yuan (ONSHORE) closed UP AT 7.1252//OFFSHORE CHINESE YUAN UP 7.1199// /Oil UP TO 82.35 dollars per barrel for WTI and BRENT AT 89.44 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 175 CONTRACTS TO 457,236 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS SMALL COMEX INCREASE OCCURRED DESPITE OUR HUGE RISE IN PRICE OF $32.30 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (4803 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO MASSIVELY SHORT AND NOW THEY ARE DESPERATELY TRYING TO COVER THEIR FOLLY.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.. THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4803 EFP CONTRACTS WERE ISSUED: ;: , . 0 DEC :4803 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4803 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED SIZED TOTAL OF 4978 CONTRACTS IN THAT 4803 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 175 CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR VERY STRONG RISE IN PRICE OF GOLD $32.30. WE HAD SMALL SPREADER LIQUIDATION//WE HAD SPEC SHORT DESPERATELY TRYING TO COVER BUT WITH BANKERS TAKING THE BUY SIDE, IT IS BECOMING DIFFICULT FOR OUR SHORTERS. THUS, WE ARE NOW WITNESSING THE SPECULATORS GOING MASSIVELY SHORT WHILE THE BANKERS WHO ARE HUGELY LONG CONTINUE TO ADD TO THEIR PURCHASES. THIS WILL NOT END WELL FOR OUR SPECS ONCE THE SIGNAL HAS BEEN GIVEN TO ANNIHILATE THE SPECS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING SEPT (38.158),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $32.30) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED TOTAL GAIN ON OUR TWO EXCHANGES OF 4978 CONTRACTS // COMMERCIAL LONGS ADDED TO THE POSITIONS, AND SPECULATOR SHORTS TRIED TO COVER FROM THEIR SHORT POSITIONS WITH MINIMAL SUCCESS AS THE PRICE SKYROCKETED//WE HAD CONTINUING OF SPREADER LIQUIDATION// WE HAVE REGISTERED A STRONG GAIN OF 4978 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR SEPT. (38.158 TONNES)…

WE HAD -402 CONTRACTS COMEX TRADES REMOVED. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 4978 CONTRACTS OR 497,800 OZ OR 15.483 TONNES

Estimated gold volume 202,082/// fair//

final gold volumes/yesterday 307,702/ fair

FINAL STANDINGS FOR SEPT ’22 COMEX GOLD //SEPT 29

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 23,245.180 oz BRINKS |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 256 notice(s) 25,600 OZ 0.7962 TONNES |

| No of oz to be served (notices) | 0 contracts 00oz 0.00 TONNES |

| Total monthly oz gold served (contracts) so far this month | 12,269 notices 1,226,900OZ 38.162 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits nil oz

customer withdrawals: 1

i) Out of Brinks 23,245.180 oz

total: 23,245.180 oz

total in tonnes: 0.7230 tonnes

Adjustments: 1

JPM: dealer to customer; 30,479.124 0z

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPT.

For the front month of SEPT we have an oi of 256 contracts having LOST 856 contracts .

We had 866 notices filed on WEDNESDAY so we gained 10 contracts or an additional 1000 oz

will stand for gold in this very non active delivery month of September. This queue jump is actually the Londoners exercising efp’s and tendering them to the banks

for the physical!

October LOST a large 8582 contracts LOWERING TO 22,876. Oct is generally a poor active delivery month. We will probably have around 55 to 60 tonnes of gold initially stand for delivery but that will grow as the month of October comes to an end.

WE HAVE 1 MORE READING DAYS BEFORE FIRST DAY NOTICE ( FRIDAY SEPT 30.2022)

November GAINED 520 contracts to stand at 1448

December GAINED a huge 8183 contracts UP to 385,802

We had 256 notice(s) filed today for 25600 oz FOR THE SEPT. 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 256 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 151 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2022. contract month,

we take the total number of notices filed so far for the month (12,269) x 100 oz , to which we add the difference between the open interest for the front month of (SEPT 256 CONTRACTS) minus the number of notices served upon today 256 x 100 oz per contract equals 1,226,800 OZ OR 38.158 TONNES the number of TONNES standing in this NON active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month:

No of notices filed so far (12,269) x 100 oz+ (256) OI for the front month minus the number of notices served upon today (256} x 100 oz} which equals 1,226,800 oz standing OR 38.158 TONNES in this NON active delivery month of SEPTEMBER.

TOTAL COMEX GOLD STANDING: 38.158 TONNES (A HUMONGOUS STANDING FOR A SEPT ( NON ACTIVE) DELIVERY MONTH)

WE WILL INCREASE IN GOLD TONNAGE STANDING FROM THIS DAY FORTH UNTIL THE END OF THE MONTH.

SOMEBODY IS AFTER A HUGE AMOUNT OF GOLD. THE EFPS ARE NOW BEING USED TO TAKE GOLD FROM THE COMEX. THUS THE AMOUNT OF GOLD STANDING FOR SEPT. WILL RISE EXPONENTIALLY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,218,731.290 oz 69.01 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 26,501,205.703 OZ

TOTAL REGISTERED GOLD: 13,090,844.141 OZ (407.18 tonnes)

TOTAL OF ALL ELIGIBLE GOLD: 13,410,361,542 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,872,113 OZ (REG GOLD- PLEDGED GOLD) 338.16 tonnes//rapidly declining

END

SILVER/COMEX/SEPT 29//FINAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 524,610 oz CNT JPM |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1994.100 oz Delaware |

| No of oz served today (contracts) | 21 CONTRACT(S) 105,000 OZ) |

| No of oz to be served (notices) | 00 contracts (NIL oz) |

| Total monthly oz silver served (contracts) | 6805 contracts 34,025,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into Delaware: 1994.100 oz

Total deposits: 199.100 oz

JPMorgan has a total silver weight: 162.946 million oz/313.609million =51.97% of comex

Comex withdrawals: 2

i)Out of CNT 2,078.100 oz

ii)Out of JPMorgan: 522,877.510

total withdrawals: 524,610.62 oz

adjustments: // 2

DEALER TO CUSTOMER:

i)HSBC 30,468.980 oz

ii) Delaware 10,329.47 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 42.645 MILLION OZ (declining rapidly)

TOTAL REG + ELIG. 313.609 MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF SEPT OI: 21 CONTRACTS HAVING LOST409 CONTRACTS. WE HAD

43 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED 3 CONTRACTS OR AN ADDITIONAL

15,000 OZ WILL STAND FOR METAL IN THIS VERY ACTIVE MONTH OF SEPT.

WE WILL GAIN IN TOTAL SILVER STANDING EACH TRADING DAY UNTIL THE END OF THE MONTH

(CONTINUAL QUEUE JUMPING BY OUR BANKERS SEARCHING FOR SILVER METAL)

OCTOBER LOST 28 CONTRACTS TO STAND AT 313 CONTACTS.

NOVEMBER GAINED 16 CONTRACTS TO STAND AT 227

DECEMBER SAW A GAIN OF 828 CONTRACTS DOWN TO 114,184

.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 21 for 105,000 oz

Comex volumes:81,613// est. volume today// good

Comex volume: confirmed yesterday: 65,273 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 6805 x 5,000 oz = 34,025,000 oz

to which we add the difference between the open interest for the front month of SEPT(21) and the number of notices served upon today 21 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT./2022 contract month: 6,805 (notices served so far) x 5000 oz + OI for front month of SEPT (21) – number of notices served upon today (21) x 5000 oz of silver standing for the SEPT contract month equates 34,025,000 oz. .

We have an inventory of 42.645 million oz of registered silver at the comex so Sept delivery of 34.025 MILLION OZ represents 79.78% of that category of silver.

If we add August’s final delivery (to Sept) for silver at 5.51 million oz, we have a total of 39.535 million oz delivered upon with a REGISTERED INVENTORY of 42.645 million oz or 92.70% of that category of silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:57,835// est. volume today// poor

Comex volume: confirmed yesterday: 86,100contracts ( good)

END

GLD AND SLV INVENTORY LEVELS

SEPT 29/WITH GOLD DOWN $.85 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: ADEPOSIT OF 3.3 TONNES INTO THE GLD//INVENTORY RESTS AT 943.16 TONNES

SEPT 28/WITH GOLD UP $32.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FORM THE GLD////INVENTORY RESTS AT 940.549 TONNES

SEPT 27/WITH GOLD UP $1.75: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FROM THE GLD////INVENTORY RESTS AT 943.47 TONNES

SEPT 26/WITH GOLD DOWN $17.15: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 947.23 TONNES

SEPT 23/WITH GOLD DOWN $24.60: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWALOF 2.03 TONNES FORM THE GLD//INVENTORY RESTS AT 950.13 TONNES

SEPT 22/WITH GOLD UP $5.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 952.16 TONNES

SEPT 21/WITH GOLD UP $4.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.79 TONNES FROM THE GLD///INVENTORY RESTS AT 952.16 TONNES

SEPT 20/WITH GOLD DOWN $6.65; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 TONNES FROM THE GLD////INVENTORY RESTS AT 957.95 TONNES

SEPT 19/WITH GOLD DOWN $4.80: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONES FROM THE GLD//INVENTORY RESTS AT 960.85 TONNES

SEPT 16.WITH GOLD UP $5.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT 1,45 TONNES INTO THE GLD//INVENTORY RESTS AT 962.01 TONNES

SEPT 15/WITH GOLD DOWN $30.20: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.35 TONNES FROM THE GLD.//INVENTORY RESTS AT 960.56 TONNES

SEPT 14/WITH GOLD DOWN $7.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY REST AT 962.88 TONNES

SEPT 13/WITH GOLD DOWN $22.85 : BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73ONNES FROM THE GLD////INVENTORY RESTS AT 964.91 TONNES

SEPT 12/WITH GOLD UP $12.30: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 966.64 TONNES

SEPT 9/WITH GOLD UP $7.85: 2 BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.90 AND ANOTHER 1.51 TONNES FROM THE GLD////INVENTORY RESTS AT 966.64 TONNES

SEPT 8/WITH GOLD DOWN $6.10:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 971.05 TONNES

SEPT 7/WITH GOLD UP $13.70: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 971.05 TONNES

SEPT 6 WITH GOLD DOWN $9.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.08 TONNES//

SEPT 2/WITH GOLD UP $7.00// SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD/ //INVENTORY RESTS AT 973.08 TONNES

SEPT 1/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.37 TONNES

AUGUST 31.WITH GOLD DOWN $10.20:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.24 TONNES FROM THE GLD////INVENTORY RESTS AT 973.37 TONNES

AUGUST 30.WITH GOLD DOWN $12.00:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 980.61 TONNES

AUGUST 29/WITH GOLD DOWN $.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FORM THE GLD/////INVENTORY RESTS AT 982.64 TONNES

AUGUST 26/WITH GOLD DOWN $26.60; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 25/WITH GOLD UP $9.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 24/WITH GOLD UP $.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD//INVENTORY RESTS AT 984.38 TONNES

AUGUST 23/WITH GOLD UP $12.25 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.83 TONNES INTO THE GLD///INVENTORY RESTS AT: 987.66

AUGUST 22/WITH GOLD DOWN $14.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

AUGUST 19/WITH GOLD DOWN $8.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 985.83 TONNES

GLD INVENTORY: 943.16 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 29/WITH SILVER DOWN 15 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 645,000 OZ FROM THE SLV//INVENTORY RESTS AT 479.904 MILLION OZ//

SEPT 28/WITH SILVER UP $.52 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 645,000 OZ FROM THE SLV.//INVENTORY RESTS AT 480.549 MILLION OZ//

SEPT 27/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 481.194 MILLION OZ

SEPT 26/WITH SILVER DOWN 43 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 737.000 OZ FROM THE SLV////INVENTORY RESTS AT 481.194 MILLION OZ//

SEPT 23/WITH SILVER DOWN 68 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .507 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 481.931 MILLION

SEPT 22/WITH SILVER UP 10 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .691 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.424 MILLION OZ/

SEPT 21/WITH SILVER UP 33 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.902 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 482.115 MILLION OZ//

SEPT 20/WITH SILVER DOWN 18 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.475 MILLION OZ//INVENTORY RESTS AT 479.213 MILLION OZ//

SEPT 19/WITH SILVER DOWN 2 CENTS TODAY: GIGANTIC CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.108 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 477.738 MILLION OZ

SEPT 16/WITH SILVER UP 8 CENTS TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.58 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 469.63 MILLION OZ//

SEPT 15/WITH SILVER DOWN $.25 TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 467.050 MILLION OZ//

SEPT 14/WITH SILVER UP $0.06 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.899 MILLION OZ/

SEPT 13/WITH SILVER DOWN $.31 TODAY:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.672 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.899 MILLION OZ//

SEPT 12/WITH SILVER UP 1.04 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSIT OF 553,000 OZ AND 464,000 OZ INTO THE SLV////INVENTORY REST AT 468.571 MILLION OZ///

SEPT 9/WITH SILVER UP 31 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 138,000 OZ INTO THE SLV////INVENTORY RESTS AT 467.557 MILLION OZ/

SEPT 8/WITH SILVER UP 16 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 7/WITH SILVER UP 34 CENTS : BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 830,000 OZINTO THE SLV////INVENTORY RESTS AT 467.419 MILLION OZ//

SEPT 6/WITH SILVER UP ONE CENT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 533,000 OZ FROM THE SLV//INVENTORY RESTS AT 466.589 MILLION OZ//

SEPT 2/WITH SILVER UP 13 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.567 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 467.140 MILLION OZ//

SEPT 1/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.573 MILLION OZ//

AUGUST 31/WITH SILVER DOWN 36 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 3.087 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 465.573 MILLION OZ//

AUGUST 30/WITH SILVER DOWN 34 CENTS TODAY: BIG CHANGES:A WITHDRAWAL OF 1.478 MILLION OZ FROM THE SLV. //INVENTORY RETS AT 470.135 MILLION OZ//

AUGUST 29/WITH SILVER DOWN 7 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY A THE SLV: A WITHDRAWAL OF 2.765 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 470.135 MILLION OZ//

AUGUST 26/WITH SILVER DOWN 39 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 25/WITH SILVER UP 21 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.160 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 472.900 MILLION OZ//

AUGUST 24/WITH SILVER DOWN 12 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 475.066 MILLION OZ/

AUGUST 23/WITH SILVER UP 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.194 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 479.490 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 483.684 MILLION OZ

AUGUST 19/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.798 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.684 MILLION OZ.

CLOSING INVENTORY 479 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

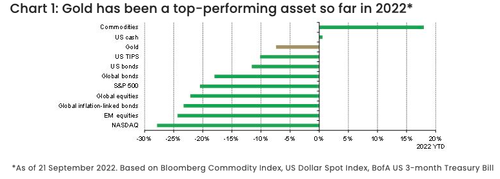

Gold Is One Of The Best Performing Assets Of 2022

THURSDAY, SEP 29, 2022 – 09:25 AM

Authored by Michael Maharrey via SchiffGold.com,

Given historically high inflation, why haven’t we seen a big rally in gold and silver?

There are a number of factors that have weighed on precious metals, but as the World Gold Council points out, it’s important to put gold and silver’s recent price movements in a broader perspective.

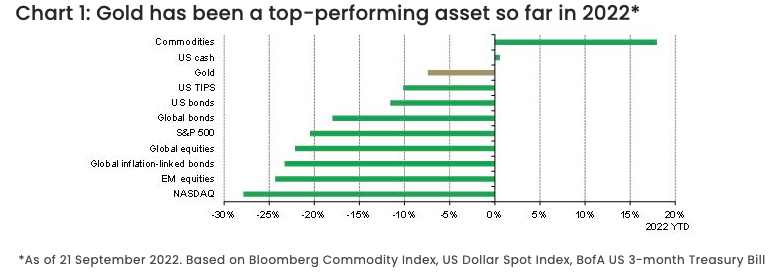

In fact, gold has been one of the better-performing asset classes in 2022.

Gold has outperformed US bonds, foreign bonds, the S&P 500, foreign stocks, the NASDAQ, and US Treasury Inflation-Protected Securities (TIPS). The only things that have outperformed gold are commodities, especially oil and agricultural goods, and the US dollar.

So, while gold has fallen more than 5% over the year, it has fallen far less than most other assets, and if you hold gold in your portfolio, it has helped hedge some of those other losses.

The Mighty Dollar

Dollar strength has been the story of 2022. As the World Gold Council put it, “Rising rates and a strong dollar have had a significant negative effect on gold’s performance despite support from geopolitics and inflation.”

We’ve seen the dollar index at 20-plus-year highs. This seems kind of crazy given the level of inflation. After all, high inflation means the dollar is devaluing, right?

Yes.

And it has.

Your purchasing power has decreased precipitously. In June, we reported that the average US household will spend about $5,200 more this year than they did last year on the same consumption basket. That breaks down to $433 extra in expenditures every single month. So, your dollar is worth considerably less.

But when we talk about dollar strength, we’re talking about the greenback compared to other fiat currencies. And over the last year, the dollar has been the cleanest dirty shirt in the laundry. Other fiat currencies have devalued even more. As Mike Maloney put it, “The US dollar has strengthened so much and so quickly this year that it has become a juggernaut, trampling pretty much every other asset.

The question is how long can this last?

In a nutshell, it will last as long as the mainstream thinks the Fed can win this inflation fight.

Peter Schiff recently said Jerome Powell still thinks he can pull off the impossible. A lot of people agree. You can see this in the bond market. Yields indicate investors think the Fed will do whatever is necessary to bring inflation down, it will do so effectively, and it won’t crash the economy. Peter said the markets are wrong on all counts.

They’re wrong about the economy and they’re wrong about the inflation. The economy is going to be much weaker than investors think. But at the same time, inflation is going to be much stronger than investors think.”

And Peter said once the Fed can no longer deny this reality, it will go back to loose monetary policy.

I think when Powell is really confronted with how ugly this is going to be, then we’re finally going to get that pivot. But this is a giant game of chicken, and I think Powell is going to keep up this pretense as long as he possibly can.”

In the meantime, other central banks are playing catch up. The ECB has gotten much more aggressive in its inflation fight. Other central banks are tightening. Japan is the only country still dragging its heels. The World Gold Council argues that this will begin to curb dollar strength.

The fact the other central banks are being more resolute in their policy decisions – partly to curb inflation, partly to defend their currencies – should weigh on the US dollar.”

Looking at the longer term, dollar dominance continues to erode. Some analysts think we are rapidly approaching a post-dollar world.

Gold’s Underlying Strength

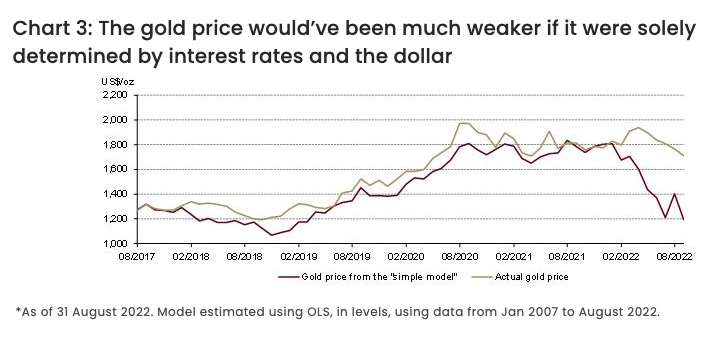

Despite the headwinds, gold has performed better than might be expected.

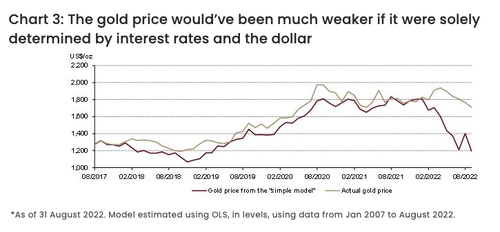

Based solely on interest rates and dollar strength, gold should have fallen about 30%, according to a WGC model.

Meanwhile, negative investor sentiment drove heavy gold ETF outflows and weak positioning in the futures market. This put additional pressure on gold. The World Gold Council argues that gold has held up remarkably well given these headwinds.

The fact that gold has performed as well as it has, all things considered, is a testament to its global appeal and more nuanced reaction to a wider set of variables.”

The World Gold Council highlights some of the underlying support for gold beyond a likely softening of the dollar in the near future.

Positioning in gold futures has turned net short again and this, historically, has not lasted long – often mean-reverting in subsequent weeks. At the same time, central bank demand for gold remains quite strong. Finally, as recessionary and geopolitical risks increase, investors may shift to more defensive strategies, looking for high-quality liquid assets such as gold to reduce portfolio losses.

Given these factors, the World Gold Council said it is optimistic that gold’s headwinds may start to subside, but that supportive factors will remain, “thus encouraging demand for gold as a long-term investment hedge.”

END

another good read from Peter Schiff..

Schiff gold

This Looks A Lot Like the Dot-Com Bust With One Big Difference – Inflation

THURSDAY, SEP 29, 2022 – 01:45 PM

This is starting to look a lot like the popping of the dot-com bubble with one big difference — inflation.

Beginning in mid-June, we saw a significant bear market rally in stocks. But the recent declines have wiped out those gains and more. For instance, the Dow jumped 14% during the 2-month rally. By the close on Friday, Sept. 23, it was once again down 20% from its all-time high. That same day, the NASDAQ closed just 2% off its June low after a 23% rally.

As WolfStreet points out, the collapse of this bear market rally was predicated on the fantasy of a Federal Reserve pivot.

The bear-market rally happened because markets – meaning folks and algos playing in them – had this fabulous reaction to the Fed’s aggressive rate-hike scenario: They began fantasizing about a Fed “pivot” and about rate cuts and some even about QE all over again. Asset prices began to jump and yields began to fall.”

WolfStreet points out that this bear market rally is reminiscent of the dot-com era. During a similar two-month rally from May 27 through July 17, 2000, the NASDAQ jumped by 33% without ever getting back to its old high. Ultimately, the NASDAQ collapsed by 78%.

That bear-market rally in the summer of 2000 suckered a lot of people back into the market, thinking that stocks would be going to the moon again, and they got crushed.”

The difference between then and now is we have a CPI over 8%.

The Fed has inflated an everything bubble. Since 2008, the central bank has pumped over $8 trillion into the economy. It got away with this inflation for a long time because most of that money wasn’t getting to consumers. Instead, we saw asset prices spike – particularly the stock market and real estate.

The Fed tried to normalize rates in 2018 and the air started coming out of those bubbles. It had already pivoted back to rate cuts and QE long before COVID. In a sense, the pandemic saved the Fed’s bacon. It gave the central bank an excuse to pump trillions of dollars in new liquidity into the economy and reinflate the bubbles. But the extent of the quantitative easing and the fact that the government handed out trillions to consumers changed the dynamics. Suddenly, the inflation started showing up in the CPI.

The Fed denied it for months, calling inflation “transitory.” But once it became impossible to deny, it launched its inflation fight. Predictably, the markets tanked until they decided the Fed was about finished tightening. Now, reality has set in again and we’re back to the bear market.

WolfStreet sums it up.

These artificially inflated markets cannot even maintain their level amid rate hikes and QT. Even little-bitty rate hikes, just four in a year, and small amounts of QT caused markets to tank, just like interest rate repression and QE had caused them to soar. It was becoming clear to everyone: QT was having the opposite effect of QE.”

The question remains: what will the Fed do. Will it hold the course? Or will it do what it has done in the past — pivot back to inflationary, loose monetary policy to rescue the economy, as it did after the dot-com bust (setting up the 2008 financial crisis).

WolfStreet argues that there will be no Fed pivot. He thinks the central bankers will be willing to tank the economy to get inflation back to 2%, just as Jerome Powell promises.

There have been lots of people who said that the Fed will keep doing QT “until something breaks.” Last time it did QT until the repo market broke. That was when the banks stopped lending to the repo market, which then blew out, which cause the Fed to bail it out in September 2019.

“But this time, the biggest thing that the Fed is in charge of has already broken: price stability. Inflation is the worst it has been in 40 years. And the Fed is tightening in order to fix this huge thing that has broken – to bring this inflation back under control and down to 2% (as per core PCE). This could be a long and tough slog. And other things that might break along the way are by comparison just minor inconveniences.”

This is where I part ways with WolfStreet’s analysis. I think the things that break will be far more and “minor inconveniences.”

Just consider the impact on the national debt. When you run the numbers, it becomes clear the US government can’t operate in a high interest rate environment. And the US government isn’t alone under a big pile of debt. Corporations are overleveraged and consumer debt is at record levels.

So far, the Fed has stayed resolute to follow through with its inflation fight. Peter Schiff said the Fed still thinks it can do the impossible, and it will ultimately pivot. But not until it can no longer deny the impacts of its tighter monetary policy.

I think when Powell is really confronted with how ugly this is going to be, then we’re finally going to get that pivot. But this is a giant game of chicken, and I think Powell is going to keep up this pretense as long as he possibly can.”

The mainstream has conceded a recession looms, although most people say it will be short and shallow. But as Peter Schiff said, the bust needs to be proportional to the boom.

We’ve never had a boom this big. We’ve never had interest rates this low for this long. We’ve never had an economy more screwed up than the one we have right now. We’ve never had bigger asset bubbles, bigger debt bubbles, more misallocations of capital and resources. So, we have more mistakes that we need to fix now than ever before. So, how are we going to do that with a short shallow recession? We’re not. It’s going to be a massive recession. And again, the Fed has no stomach for that, and that’s why the Fed is going to pivot.”

Alan Greenspan was able to engineer a recovery after the dot-com bust with some rate cuts. Ben Bernanke was able to engineer a recovery after 2008 with rate cuts and QE. (And by recovery, I mean reinflate the bubbles.) But they didn’t have to contend with 8.3% CPI. Jerome Powell does. And that changes everything.

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz

Lawrie Williams: Gold fulfills expectations in the U.K. and elsewhere if not the U.S.

Submitted by admin on Wed, 2022-09-28 13:52Section: Daily Dispatches

By Lawrie Williams

SharpsPixley.com, London

Tuesday, September 27, 2022

If one reads all the headlines about gold, one could be forgiven for thinking that 2022 has been a pretty disastrous year for those banking on the yellow metal to preserve their wealth.

This is indeed the case for gold holders in the United States, here the gold price has declined around 9%, although that is less than half that seen in most U.S. equities since the beginning of the year — even more in the NASDAQ stocks. But in the case of UK gold holders and holdings valued in pounds sterling, it has been a very different story altogether due to the fall in value of the pound against the dollar so far this year.

This has been a similar experience in other areas of the world where local currencies have been in strong decline against their U.S. counterpart.

In pound sterling terms, the gold price has actually appreciated by no less than 13% while the FTSE all-share index for comparison has declined by around 10% over the same period.

With the Bank of England following the U.S. Federal Reserve with an aggressive interest rate raising policy to fight inflation, and commenting that the UK economy is probably already in at least a mild recession, one can anticipate further equity price slippage, while the gold price can probably still hold its own, making it a continuingly good wealth protection choice for investors.

Of course the UK is not the only country where the gold price has been appreciating in the local currency due to the U.S. dollar’s strength. There are many others.

We have already reported on the resultant strength of the Australian gold mining sector during the most recent quarter due to the almost A$42 per ounce gold price rise during Q2 resulting from a 6-cent movement in the exchange rate between the U.S. and Australian dollars. With producer costs mostly in Australian dollars the miners mostly saw some good cost benefits. Although these would inevitably close over time, the short term advantages will have been beneficial. …

… For the remainder of the commentary:

end

END

3.Chris Powell of GATA provides to us very important physical commentaries

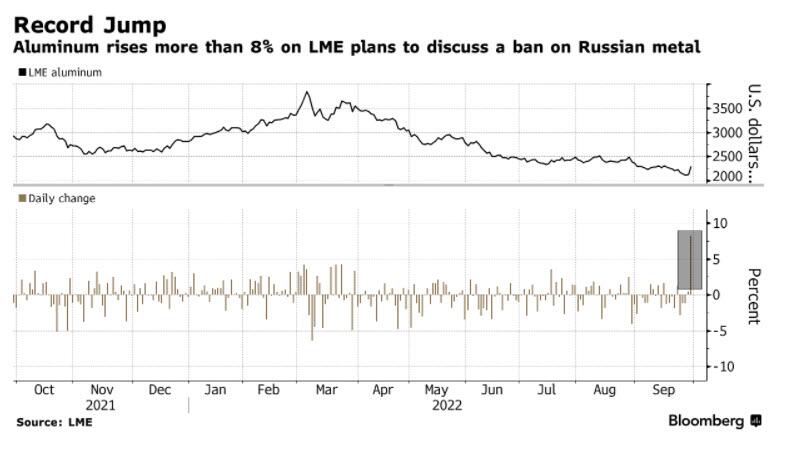

5.OTHER COMMODITIES: ALUMINUM

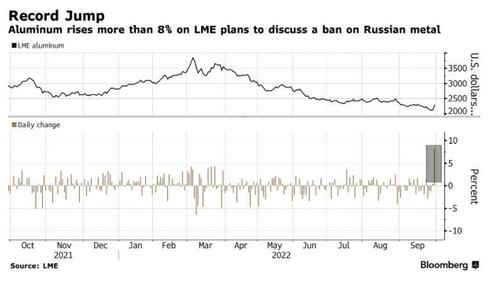

Aluminum surges the most on record. The crazy and corrupt LME considers a ban on Russian supply

(zerohedge)

Aluminum Surges Most On Record As LME Considers Russia Ban

THURSDAY, SEP 29, 2022 – 08:21 AM

The closer we get to year end, the more we are reminded of the turbulent days of February and March when commodity prices soared to record highs on fears Russian supplies would be permanently taken off the market. And while commodities as a whole are sharply below those levels, and in many cases are even down on the year, every now and then we get a reminder just how complacent the market has become when it comes to continued Russian commodity supplies.

Today was such a day for aluminum, which soared by a record 8.5% on the London Metal Exchange after Bloomberg reported the exchange plans to discuss a potential ban on new Russian metal supplies. Prices for the most widely used base metal spiked to $2,305 a ton in the biggest intraday gain on record. Nickel rallied 5% and zinc more than 4%, paring sharp losses for industrial metals so far this month, sparked by market fears that an imminent recession will collapse demand.

Citing sources, Bloomberg reports that “the LME plans to launch a discussion paper on whether and under what circumstances it should block new supplies of Russian metal from being delivered to its network of warehouses.”

The reason for the resulting spike in prices is that any move by the LME to block Russian supplies could have significant ramifications for the global metals markets, as the country is a major producer of aluminum, nickel and copper. Fears that sanctions could disrupt Russian nickel exports helped trigger a massive short squeeze on the LME in March.

While launching a discussion paper doesn’t mean the LME has made any decisions about what it will do, the move marks a shift in approach. The exchange had previously said it did not plan to take any action outside the scope of sanctions, which have for the most part left large Russian metal producers like Rusal and Norilsk Nickel untouched.

“The LME continues to take the required action to ensure market stability in response to sanctions,” the bourse said in a statement Thursday. It will keep the situation under review as it prioritizes an “orderly market,” the LME said.

COMMODITIES IN GENERAL/

END

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 7.1252

OFFSHORE YUAN: 7.1199

SHANGHAI CLOSED: DOWN 48.79 PTS OR 1.58%

HANG SENG CLOSED DOWN 3.86 PTS OR 0.13%

2. Nikkei closed UP 248.07 PTS OR 0.95%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 112.78/Euro RISES TO 0.9738

3b Japan 10 YR bond yield: RISES TO. +.249/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 144.65/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN -// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.285%***/Italian 10 Yr bond yield FALLS to 4.65%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.44%…** DANGEROUS

3i Greek 10 year bond yield FALLS TO 4.90//

3j Gold at $1651.25//silver at: 18.66 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 89/100 roubles/dollar; ROUBLE AT 56.68//

3m oil into the 82 dollar handle for WTI and 89 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 144.65DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this .9796– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9538well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.830 UP 12 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.775 UP 9 BASIS PTS//(USA 30 YR INVERTED TO THE USA 10)

USA DOLLAR VS TURKISH LIRA: 18,54…GETTTING DANGEROUS

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE

Stocks Slide, Ugly Mood Returns As Traders Ask ‘Did Anything Change’

THURSDAY, SEP 29, 2022 – 08:08 AM

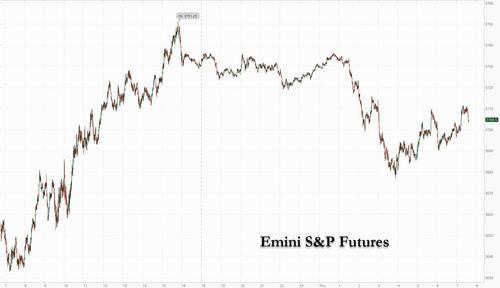

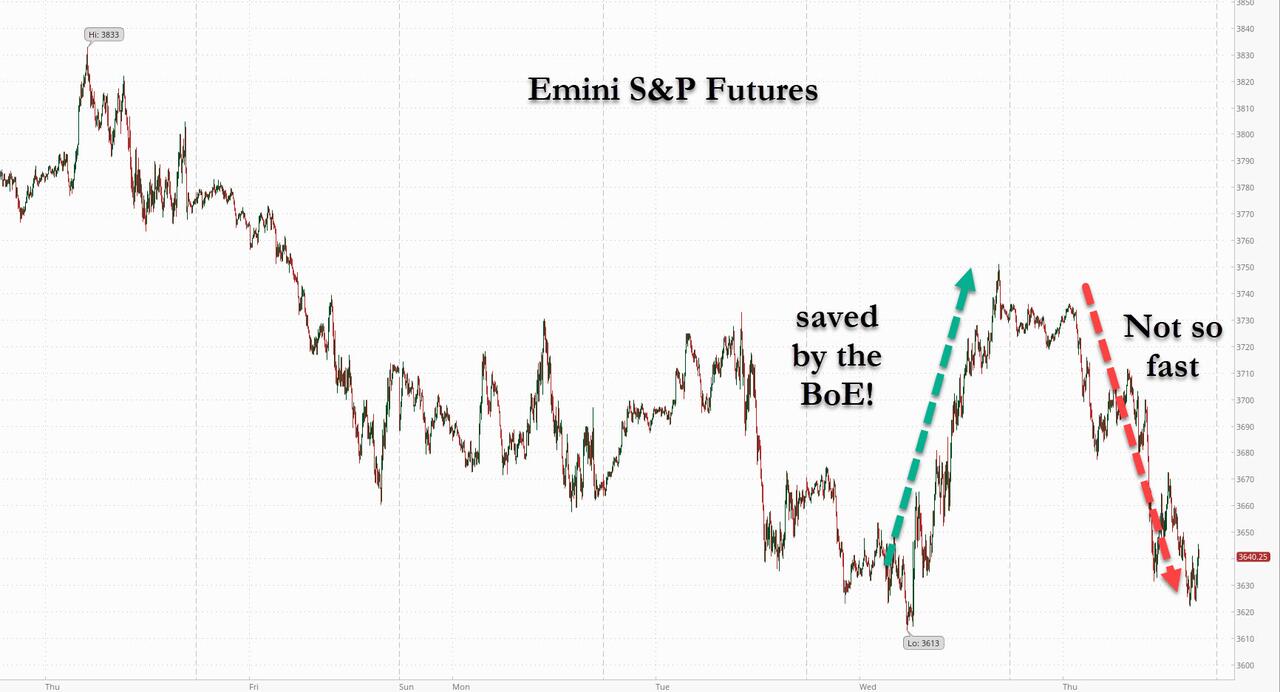

The brief post-BOE euphoria has worn off, and risk-off sentiment returned to markets as concern about inflation and the global economy overshadowed the Bank of England’s desperate attempt to restore calm by restarting QE, exacerbated by more hawkish central bank talk and defiance by British PM Liz Truss’s tax plan (which has been slammed from the IMF all the way to the White House). Treasuries resumed their slide with UK gilts, while US equity futures fell as European stocks extended a selloff that’s caused valuations to drop to their lowest since 2012. As of 730am, emini S&P futures slid 0.7% to 3704, recovering from losses as big as 1.5% earlier.

The dollar rose and Treasuries resumed their slump as investors focused on expectations the Federal Reserve will continue to deliver aggressive interest-rate hikes. The pound snapped a two-day gain and UK gilt yields rose as Prime Minister Liz Truss defended a giant package of unfunded tax cuts that sent markets into turmoil.

“Other than the dollar, there are not many assets that are trading constructively,” said Julia Raiskin, Asia-Pacific head of markets for Citigroup Inc. “The markets are very pessimistic. Investors are fairly on the sidelines.”

In premarket trading, US-listed Chinese stocks drop in premarket trading, following in the footsteps of Hong Kong- listed peers as the Hang Seng Tech Index erased almost all gains since a March nadir. Alibaba (BABA US) -3%, Nio (NIO US) -2.9%, Baidu (BIDU US) -2.4%, Pinduoduo (PDD US) -2.6%, JD.com (JD US) -2.4%. Bank stocks also slumped after snapping a six-day losing streak the day earlier. Here are other notable premarket movers:

- Coinbase falls 2.5% in premarket trading after Wells Fargo starts coverage at underweight, with operating results set to remain under pressure. Bakkt (BKKT US) and Riot Blockchain (RIOT US) are both initiated at equal-weight, with Riot declining 3% in premarket trading.

- Altus Power (AMPS US) slumped 16% in premarket trading after the company’s secondary offering priced at $11.50 per share, below Wednesday’s record close of $14.23.

- First Solar (FSLR US) gained 1.3% in premarket trading after Evercore ISI analyst Sean Morgan raised the recommendation to outperform from inline, saying the company is poised to benefit from the Inflation Reduction Act.

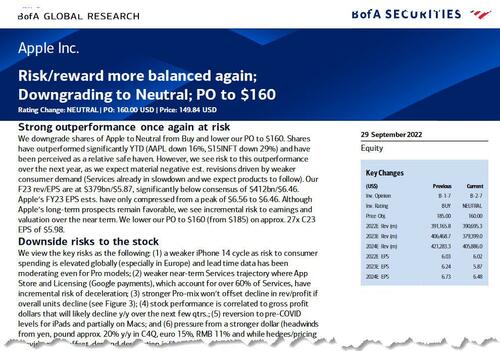

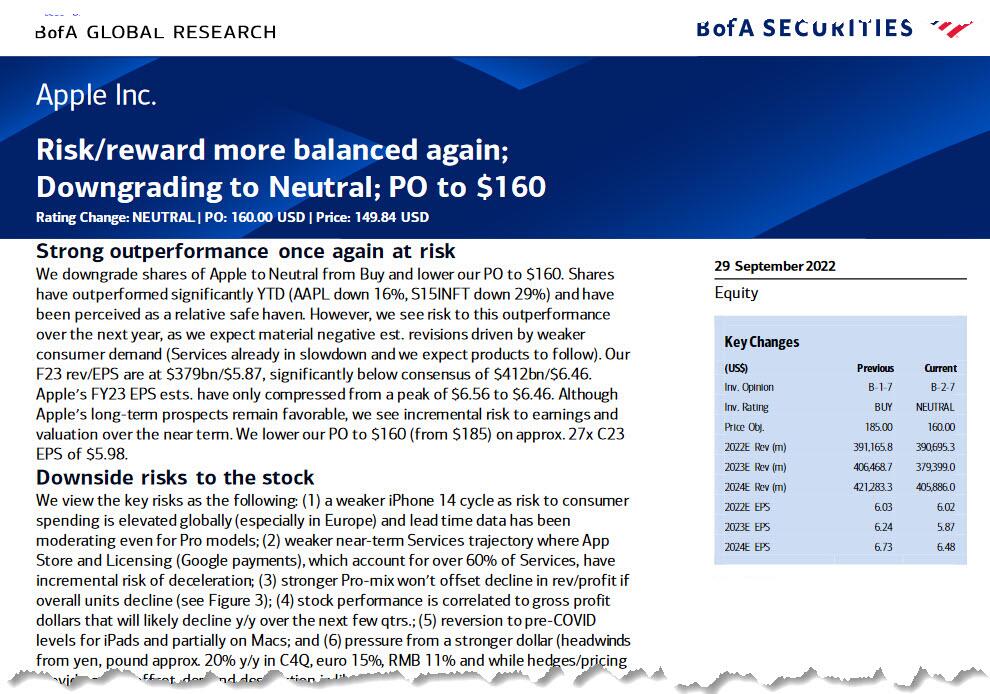

- Apple (AAPL US) shares were down 2.6% in premarket trading, set to extend Wednesday’s decline, as BofA Global Research cut the recommendation on the stock to neutral from buy.

European stocks bounced off session lows amid heightened risk-off mood. Euro Stoxx 50 slumped as much as 1.2%. Autos, retailers and real estate are the worst performing sectors as all slump. European miners rose after news that the London Metal Exchange is launching a discussion paper that marks the first step toward a potential ban on new supplies of Russian metal. Porsche AG rose as much as 5.2% as its shares started trading in Frankfurt after parent Volkswagen AG set the final listing price for the sports-car maker at the upper limit of its offer range. Here are some other notable European movers:

- Accor shares jumped as much as 8.1%, before paring gains, after the French hospitality company raised FY22 Ebitda guidance to a level which analysts said was above consensus estimates.

- Rational rose as much as 16% after the German kitchen appliances manufacturer raised its sales and Ebit guidance, citing improvements in the supply chain picture.

- Capricorn Energy shares rose as much as 8.9% to 261p amid a proposed merger with NewMed Energy that’s expected to deliver total value to Capricorn shareholders of 271 pence per share.

- H&M shares dropped as much as 7.2%, heading for the lowest close since September 2004, after it reported 3Q results that missed estimates and highlighted “very negative” market conditions.

- Next fell as much as 10% after the UK high street retailer cut its FY guidance, citing the cost of living crisis and saying the devaluation of the pound is set to prolong inflationary pressures.

- Colruyt shares plunged 24%, the most intraday on record, after it said the consolidated net result for FY22/23, ex. one-offs, is expected to decrease considerably compared with last year.

- Ubisoft shares fell after the video-game company pushed back its Skull & Bones title to March 2023 from November, despite maintaining FY guidance. Analysts say the decision raises concern.

- Wacker Chemie shares dropped as much as 7.8% after Stifel cut its price target, saying lower silicone and polysilicon prices hit sentiment.

- Hornbach shares dropped as much as 7% after it published its latest 2Q report. The home improvement retailer posted a worse-than expected Ebit decline y/y, Warburg said.

- European auto stocks fell and were among the worst performing subgroups on the wider market, with Volkswagen and its parent Porsche Automobil Holding SE leading declines.

European bond yields also rose as investors digested the latest inflation data and commentary from European Central Bank officials. Euro-area economic confidence dropped to the lowest since 2020.

Investors are contending with threats posed by discordant moves from central banks over the past few days, with Fed officials adamant on further monetary tightening, the BOE unveiling a £65 billion ($71 billion) plan to support government debt and authorities in Asia trying to prop up weakening currencies.

“The central bank is in a very difficult position right now,” Julie Biel, Kayne Anderson Rudnick portfolio manager and senior research analyst, said of the BOE in an interview with Bloomberg TV. “Everyone has been a little bit backed into a corner in seeing the volatility and market reaction.”

Former Bank of England Governor Mark Carney accused the UK government of “undercutting” the nation’s economic institutions, and said that its fiscal plans were to blame for the drop in the pound and bonds. Simon Wolfson, the boss of Next Plc and a Conservative peer, also appeared to blame the Tory government for a crash in the currency and a worsening outlook for UK inflation, which the company cited as it lowered guidance for sales and profits.

Separately, the European Commission announced an eighth package of sanctions that would include a price cap on Russia’s oil exports as Russia vowed to go ahead with the annexation of the parts of Ukraine that its troops currently control after UN-condemned votes, putting the Kremlin on a fresh collision course with the US and its allies.

Earlier in the session, Asian stocks pared earlier gains spurred by the Bank of England’s unlimited bond-buying plan, as sentiment again turned cautious with fears over a global recession. The MSCI Asia Pacific Index was up 0.2%, having earlier gained as much as 1.2%. Benchmarks in Australia and Japan outperformed, while South Korea’s market closed almost flat. Gauges in Hong Kong and China ended in the red with tech stocks sliding near the lowest since to a sector index was introduced in 2020. Hang Seng Tech Index Slides Toward Lowest Since 2020 Inception The key Asian equity benchmark slumped Wednesday to its lowest since April 2020 on concerns over the Federal Reserve’s ongoing rate hikes. While the the UK central bank’s intervention to avert a crash in the gilt market helped calm investor nerves briefly, few saw the rally as a signal for a full-fledged rebound.

“We remain very cautious on the markets and would exercise a degree of patience,” Kerry Craig, a global market strategist at JPMorgan Asset Management, said in an interview with Bloomberg TV. Central bank moves, inflation and “the looming risk of recession” need to be monitored, he said. Down almost 12% in September, the MSCI Asian benchmark is set to post its worst monthly performance since the pandemic-triggered crash in March 2020. An index of Asia Pacific stocks excluding Japan is on course for its fifth-straight quarterly loss, its longest losing streak in 21 years.

Japanese equities rose, rebounding along with global peers as investors assessed the Bank of England’s move to buy government bonds. More than 1,100 Topix stocks traded without rights to the next dividend. The Topix rose 0.7% to close at 1,868.80, while the Nikkei advanced 0.9% to 26,422.05. Out of 2,169 stocks in the Topix, 1,854 rose and 271 fell, while 44 were unchanged. “Though there is still a strong uncertainty in the US and UK markets over the rise in long-term interest rates, for now there is a sense of relief in the markets as government bond yields in the UK settled down due to the unlimited purchase plan,” said Tomo Kinoshita, a global market strategist at Invesco Asset Management.

In Australia, the S&P/ASX 200 index rose 1.4% to close at 6,555.00, boosted by gains in mining shares and banks. In New Zealand, the S&P/NZX 50 index rose 0.7% to 11,200.04

Stocks in India declined for a seventh straight day in the longest losing streak since February, tracking a selloff across global markets amid worries over possible recession. The S&P BSE Sensex gave up an advance of as much as 1% to end 0.3% lower at 56,409.96 in Mumbai. The NSE Nifty 50 Index slipped 0.2% as both indexes posted their longest stretch of declines in seven months. The key gauges have dropped more than 5% each this month and are on track to record their worst monthly performance since the pandemic led crash of March 2020. Ten of the 19 sector sub-indexes compiled by BSE Ltd. declined Thursday led by the utilities gauge which has lost 11% for the month, making it the worst sectoral performer.

In FX, the Bloomberg Dollar Spot Index first rose then fell, as Treasuries slumped to unwind some of the previous day’s swift rally. The euro fell as much as 1% to $0.9636, before paring losses. It’s significantly more costly to hedge against euro price swings compared to a week ago, as traders bet on wider ranges with risks skewed to the downside. The pound erased losses amid month-end flows, after earlier falling by as much 1.2% to $1.0763. UK bonds extended losses after Prime Minister Liz Truss defended her new government’s giant fiscal package of unfunded tax cuts, which have tipped markets into chaos. Commodity currencies led declines among G-10 peers. Onshore yuan eked out the first gain in nine days following a stern PBOC warning against “one-sided” speculation, but offshore yuan weakened 0.4%

In rates, Treasuries pared Wednesday’s gains with yields cheaper by up to 11bp across the 5-year tenor into early US session, with the belly’s underperformance helped by a large block sale in 5-year note futures. Treasury 10-year yields near highs of the day at around 3.83%, outperforming bunds and gilts by 3.5bp and 4.5bp in the sector; belly-led losses cheapens 2s5s30s Treasuries fly by 7bp on the day. Moves follow a more aggressive bear flattening move in gilts, wit front-end yields are cheaper by 20bp on the day. US session focus on GDP and Fed speakers throughout the day. Bunds, Italian bonds dropped and money markets raised ECB tightening bets after German state CPIs rose in September while euro-area economic confidence dropped to 93.7 in September, the lowest since 2020. UK 10-year bonds decline after Truss doubled down on her economic package;

In commodities, Brent rebounded from earlier lows, to trade near $89.50 following reports of OPEC+ considering production cuts. Spot gold falls roughly $12 to trade near $1,648/oz. Bitcoin is under modest pressure but lies within narrow ranges of less than USD 500 at present and well within recent parameters as such.

Looking to the day ahead now, and data releases include German CPI for September, Italian PPI for August, and UK mortgage approvals for August (the calm before the storm). We’ll also get the weekly initial jobless claims from the US, as well as the third estimate of Q2 GDP. From central banks, we’ll also hear from an array of speakers, including ECB Vice President de Guindos, and the ECB’s Simkus, Panetta, Centeno, Villeroy, Knot, Elderson, Rehn, Vasle, Kazaks, Muller and Lane. In addition, there’ll be remarks from the Fed’s Bullard, Mester and Daly, as well as BoE Deputy Governor Ramsden and the BoE’s Tenreyro.

Market Snapshot

- S&P 500 futures down 1.1% to 3,692.25

- MXAP up 0.2% to 139.97

- MXAPJ little changed at 453.71

- Nikkei up 0.9% to 26,422.05

- Topix up 0.7% to 1,868.80

- Hang Seng Index down 0.5% to 17,165.87

- Shanghai Composite down 0.1% to 3,041.21

- Sensex down 0.3% to 56,446.56

- Australia S&P/ASX 200 up 1.4% to 6,554.97

- Kospi little changed at 2,170.93

- STOXX Europe 600 down 1.6% to 383.23

- German 10Y yield little changed at 2.23%

- Euro down 0.9% to $0.9650

- Brent Futures down 1.2% to $88.23/bbl

- Brent Futures down 1.2% to $88.23/bbl

- Gold spot down 0.9% to $1,644.68

- U.S. Dollar Index up 0.92% to 113.64

Top Overnight News from Bloomberg

- Britain is in a self-inflicted financial crisis that threatens to accelerate the economy’s dive into recession — and the country’s new prime minister is coming under intense pressure to blink

- The ECB should opt for a “big” increase in interest rates in October, according to Governing Council member Martins Kazaks, who said in an interview that subsequent hikes are likely to be smaller. His Baltic counterparts Gediminas Simkus and Madis Muller also indicated they’d back significant moves, while Mario Centeno of Portugal called for a “measured and balanced” approach

- The ECB must ensure pay pressures don’t get out of control in its efforts to keep expectations stable, according to Governing Council member Olli Rehn

- The Riksbank believes it is very important that monetary policy continues to act for inflation to fall back and stabilize at the target of 2% within a reasonable time perspective, the Swedish central bank says in minutes from its latest monetary policy meeting

- Japan’s capital markets suffered the biggest foreign outflow in three months last week as growing fears of a global downturn fueled a search for liquidity

- China’s economy stabilized in the current quarter, and the final three months of the year will be key to the nation’s economic recovery, Premier Li Keqiang said

- As doubts grow over whether Xi Jinping still prioritizes expanding China’s economy over other goals, he’s tipped to appoint a new economic adviser who’s vowed to put growth first

- OPEC+ has begun discussions about making an oil-output cut when it meets next week, a delegate said

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks traded higher as the region took impetus from the rally on Wall St where risk sentiment was buoyed and yields retreated following the BoE’s announcement to resume Gilt purchases. ASX 200 outperformed in which the commodity-related sectors led the broad advances across industries following the recent upside in energy and metal prices, while firm monthly CPI data did little to dent risk sentiment. Nikkei 225 was also positive but with gains initially capped as more than half of the stocks traded ex-dividend. Hang Seng and Shanghai Comp were also firmer with the Hong Kong benchmark spearheaded by tech and energy stocks, while the mainland also digested reports that the PBoC is setting up a more than CNY 200bln re-lending facility quota for equipment upgrades which aims to expand market demand in the manufacturing sector.

Top Asian News

- PBoC injected CNY 105bln via 7-day reverse repos with the rate kept at 2.00% and injects CNY 77bln via 14-day reverse repos with the rate kept at 2.15% for a CNY 180bln net injection.

- Chinese President Xi told Japanese PM Kishida that they attach great importance to the development of China-Japan relations and he is willing to work with Kishida to build relations, while Kishida told Xi that bilateral relations are currently facing many issues and challenges but he hopes to build constructive and stable relations to boost peace and prosperity, in messages to mark 50 years of diplomatic relations.

- Hong Kong’s Worst Trading Debut in 2022 Sends EV Maker Down 34%

- US’s Harris Goes to DMZ Hours After North Korea Missile Launch

- Japan’s First Bond to Help Ocean Planned by Major Seafood Firm

- Best HK IPO Quarter in Year Ends With Disaster Debut: ECM Watch

- Yuan Bears Bet China Is Powerless to Fight the Mighty Dollar

- China Vows to Speed Up Delayed Homes With Special Loans

European stocks are experiencing another bleak session thus far as the overnight gains in futures dissipated heading into the cash open. Sectors are in a sea of red with no clear theme. Autos kicked off the day as the outperformer as the Porsche AG IPO occurred at a premium to the guided price of EUR 82.50/shr. US equity futures are also trading with losses across the board, with relatively broad-based downside of 1.3-1.5% seen across the front-month contracts.

Top European News

- UK PM Truss says the fiscal statement (i.e. mini-Budget) is the correct plan.

- UK Chief Secretary to the Treasury says the growth plan will get the economy growing, one of the reasons growth plans included tax cuts was to alleviate the household burden. BoE intervention has had the desired effect. Disagrees with the IMF’s remarks.

- US President Biden’s administration was reportedly alarmed by the market turmoil caused by the UK’s economic program and is seeking ways to encourage PM Truss’s team to dial back its tax cuts, according to Bloomberg.

- France is reportedly considering proposals for up to two hour power cuts for parts of the country on a rotating basis, via Reuters sources; additionally, telecom names have highlighted power issues with the German and Swedish gov’ts.

- German Network Regulator says recent gas consumption by households is too high to remain sustainable, via Reuters; gas savings of 20% are required to avoid an emergency.

- German gov’t could make a “low three-digit billion amount” available for the gas price break, discussion of EUR 150-200bln, via Handelsblatt citing gov’t circles; will reportedly be announced today.

- Europe Gas Eases With Traders Weighing Impact of Pipeline Blasts

- Rational Jumps After Boosting Sales Guidance Above Consensus

- Truss Says UK Tax Cuts Are the ‘Right Plan’ Amid Market Rout

- German Economy Seen Shrinking Next Year Due to Energy Crisis

- Profligate Government to Blame for Pound Drop, Says Wolfson

FX

- USD has regained some poise after a mid-week pullback; though, the DXY remains off earlier 113.79 highs and thus shy of the YTD/WTD peak at 114.78.

- Yuan has derived pronounced support from Reuters reports that China’s state banks have been told to stock up for intervention offshore, sending USD/CNH to 7.1437 from circa. 7.20 pre-release.

- Cable managed to ‘recover’ to a test of 1.09 but failed to breach the level with multiple BoE speakers in focus later.

- EUR/USD moving at the whim of broader USD action and failing to glean any real traction from multiple speakers and German state/Spanish mainland CPI data.

Fixed Income

- Core benchmarks are pressured across the board in a modest pullback of the pronounced BoE-induced ‘recovery’ seen yesterday, with numerous speakers due and the second BoE operation.

- Specifically, Bund lies towards the bottom of a 200 tick range while Gilts are holding onto the 95.00 handle with the associated yield lifting further above 4.0%.

- Stateside, USTs are similarly at the lower-end of parameters ahead of data and numerous speakers while the curve flattens further

Central Banks

- ECB’s Simkus says his choice of hike for October is 75bp, says 50bp would be the minimum, via Bloomberg. A 100bp hike would be too much at this point.

- ECB’s Centeno says decisions must be measured and balanced, still far from the neutral rate, via Bloomberg.

- ECB’s Rehn says prospect of recession in Euro Area is likely.

- ECB’s Vasle says current hike pace is “appropriate” response to inflation; expects to raise rates at the next several meetings.

- ECB’s de Cos says so far there is no clear evidence of de-anchoring of inflation expectations. Based on current models, median terminal rate value is at 2.25-2.5% (significant uncertainty).

- ECB’s Kazaks says 75bp will likely be appropriate for October, via Bloomberg.

- PBoC says they are to add more loans to ensure property delivery when required, via Reuters.

- China’s state banks have reportedly been told to stock up for Yuan intervention offshore, according to Reuters sources, in a bid to defend the weakening Yuan.. State banks were asked to asked offshore branches, such as those in Hong Kong, New York and London, to review holding of the CNH to ensure dollar reserves are ready to be deployed.

- RBI likely selling USD via state-run banks around 81.92-81.93 levels, according to traders cited by Reuters

- NBH hikes one-week deposit rate by 125bp, to 13.00%.

- Turkish President Erdogan says interest rates need to come down further; CBRT needs to lower rates at the next meeting, via Reuters.

Geopolitics

- Japanese Chief Cabinet Secretary Matsuno said North Korea’s multiple missile launches are unacceptable and Japan will maintain close contact with allies including the US to monitor and deal with North Korea, according to Reuters.

- Turkish President Erdogan said Turkey will increase its military presence in northern Cyprus, according to Sky News Arabia.

- EU Official expects an agreement on the next Russian sanctions package, or at least major parts of this, before the EU Summit next week. Expects the discussion to focus on referendums, possible annexation, nuclear threat and Nord Stream.

- Russian State Duma representatives have received invitations to the Kremlin for Friday, September 30th at 13:00BST, via Ria.

- Russian Kremlin says the ceremony on incorporating new territories will occur on Friday, September 30th – President Putin will speak.

US Event Calendar

- 08:30: Sept. Initial Jobless Claims, est. 215,000, prior 213,000

- 08:30: Sept. Continuing Claims, est. 1.39m, prior 1.38m

- 08:30: 2Q GDP Annualized QoQ, est. -0.6%, prior -0.6%

- 08:30: 2Q PCE Core QoQ, est. 4.4%, prior 4.4%

- 08:30: 2Q Personal Consumption, est. 1.5%, prior 1.5%

- 08:30: 2Q GDP Price Index, est. 8.9%, prior 8.9%

Central Bank Speakers

- 09:30: Fed’s Bullard Discusses Economic Outlook

- 13:00: Fed’s Mester and ECB’s Lane Take Part in Policy Panel

- 16:45: Fed’s Mary Daly Speaks at Boise State University

DB’s Jim Reid concludes the overnight wrap

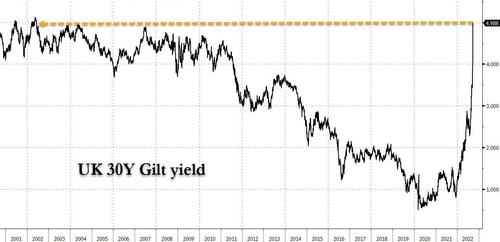

How could you have earned a 42% return yesterday from a AA-rated investment? Simple. At anytime between 8-11am all you had to do was buy 40yr Gilts before the BoE effectively restarted QE only days before QT was suppose to start (it’s been postponed until October 31st – ironically Halloween). The buying operation is aimed at restoring liquidity to a broken long end market and is temporary but it’s another stunning development to a stunning year. I’ve always felt that this debt supercycle would end up with central banks doing QE even if interest rates were positive. The reason being is that the economy can be growing and seeing inflation at a point when investors baulk at funding all the debt. I appreciate this BoE operation is slightly different and I would have never have guessed the series of events that got us here but it might not be the last time a central bank buys government bonds when not at the zero bound given how much debt there is and how much there’s likely to be going forward.

It’s becoming clearer the extent to which Tuesday’s rout at the long-end was exacerbated by collateral calls on LDIs (liability driven investments) that pension funds have typically used in some size in recent years. With these swaps moving so far out of the money, the risk was that investors would have to sell liquid assets to meet margin calls. If they didn’t have this (which a lot don’t), then obviously there would have been huge liquidity events. To understand the fears that were around over the last 48 hours, Sky News’ economics editor Ed Conway said yesterday that “I am told there were a swathe of pension funds that … would have essentially collapsed by this afternoon”. Whether that’s true, we’ll never know but it shows the level of fear.