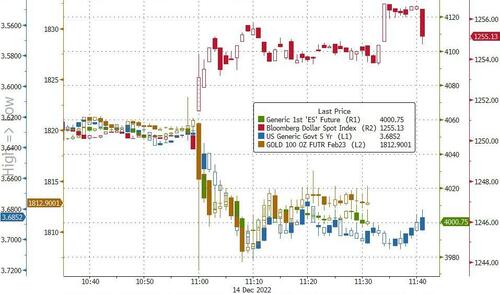

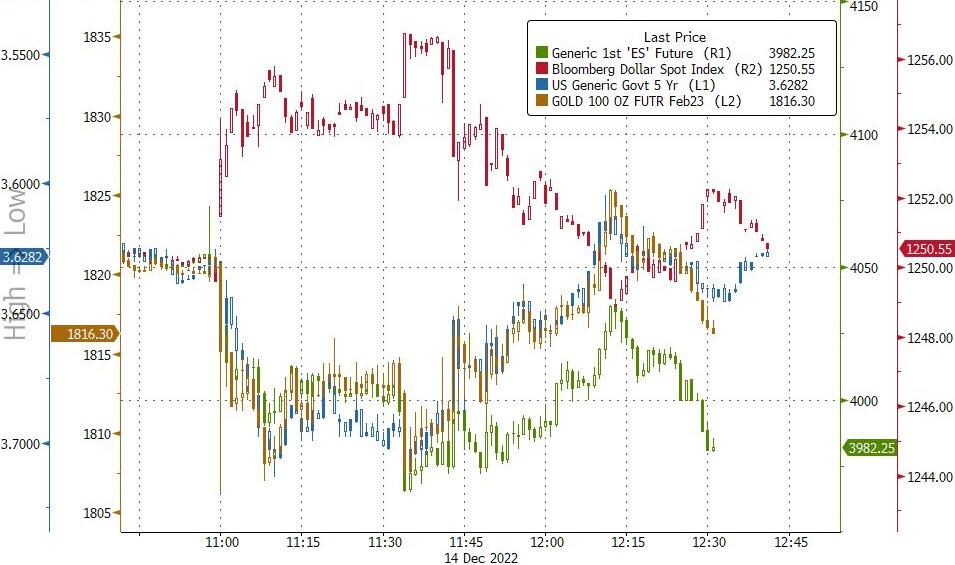

GOLD PRICE CLOSE: DOWN $6,20 at $1807.40

SILVER PRICE CLOSE: UP 0.07 to $23.85

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1807.90

Silver ACCESS CLOSE: 23.92

Bitcoin morning price:, 17,890 UP 119 DOLLARS

Bitcoin: afternoon price: $17,825 up 184

Platinum price closing $1031.85 DOWN $4.40

Palladium price; closing 1918,35 DOWN $17.05

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2448.07 DOWN $4.90 CDN dollars per oz

BRITISH GOLD: 1454.50 DOWN 9.95 pounds per oz

EURO GOLD: 1694.55 DOWN 10.25 euros per oz

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: DECEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,813.900000000 USD

INTENT DATE: 12/13/2022 DELIVERY DATE: 12/15/2022

FIRM ORG FIRM NAME ISSUED STOPPED

104 C MIZUHO 1

118 C MACQUARIE FUT 14

132 C SG AMERICAS 1

190 H BMO CAPITAL 85

435 H SCOTIA CAPITAL 41

624 H BOFA SECURITIES 19

657 C MORGAN STANLEY 1

661 C JP MORGAN 39

685 C RJ OBRIEN 5

700 C UBS 2

800 C MAREX SPEC 54 4

880 C CITIGROUP 21

905 C ADM 1

TOTAL: 144 144

COMEX//NOTICES FILED re JPMorgan 39/144

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR DEC. CONTRACT: 144 NOTICES FOR 14400 OZ or 0.4479 TONNES

total notices so far: 18,792 contracts for 1,879,200 oz (58.451 tonnes)

SILVER NOTICES: 133 NOTICE(S) FILED FOR 665,000 OZ/

total number of notices filed so far this month 3548 for 17,740,000 oz

END

GLD

WITH GOLD DOWN $6.20

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////HUGE CHANGES IN GLD INVENTORY:A DEPOSIT OF 2.31 TONNES INTO THE GLD

INVENTORY RESTS AT 912.72 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $0.07

AT THE SLV// :/HUGE CHANGES IN SILVER INVENTORY AT THE SLV THESE PAST 3 WEEKS! A LOSS OF 1.7 MILLION OZ FROM THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 512.000 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 3064 CONTRACTS TO 125,555 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR CONSIDERABLE $0.59 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR SHORTERS/HFT WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.59 AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD AN ATMOSPHERIC SIZED GAINED IN OUR TWO EXCHANGES OF 4309 CONTRACTS. AS WELL WE HAD EXCHANGE FOR RISK TRANSFER OF 0 CONTRACTS. WE HAD HUGE ATTEMPTED SPEC SHORT COVERINGS OF THEIR SHORTFALL. .WE PROBABLY HAD ZERO SHORT ADDITIONS WITH THE STRONG PRICE RISE OF THE SILVER. // OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. BUT THEY ALSO SUPPLIED THE NECESSARY SHORT CONTRACTS>>> HUGE NUMBER OF NEWBIE SPEC LONGS ADDED TO THEIR POSITIONS CAUSING ADDITIONAL MISERY TO OUR SHORTERS.

WE MUST HAVE HAD:

A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 23 .24. MILLION OZ FOLLOWED BY TODAY;S QUEUE JUMP TO LONDON of 165,000 OZ // V) HUGE SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL —329

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS DEC. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF DEC:

TOTAL CONTRACTS for 12 days, total 6568 contracts: OR 32.840 MILLION OZ PER DAY. (547 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 32.840 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 32.84 MILLION OZ INITIAL

RESULT: WE HAD AN ATMOSPHERIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4309 WITH OUR STRONG $0.59 GAIN IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC SIZED EFP ISSUANCE CONTRACTS: 1245 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 23.24 MILLION OZ FOLLOWED BY TODAY:S 165,000 QUEUE JUMP //NEW STANDING 23.930 MILLION OZ + EFR = 34.443 MILLION OZ. .. WE HAVE AN ATMOSPHERIC SIZED GAIN OF 4309 OI CONTRACTS ON THE TWO EXCHANGES FOR 7.3190 MILLION OZ.. THE SILVER SHORTS ARE NOW TRAPPED AS THEY ARE HAVING CONSIDERABLE DIFFICULTY IN COVERING THOSE SHORTS.

WE HAD 133 NOTICE(S) FILED TODAY FOR 665,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUGE SIZED 12,901 CONTRACTS TO 437,040 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 296 CONTRACTS.

.

THE HUGE SIZED INCREASE IN COMEX OI CAME WITH OUR STRONG GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR DEC. AT 58.86 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY:S QUEUE JUMP of 120 contracts or 12,000 oz//(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). NEW STANDING 59.539 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN PRICE OF $32.75 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A GIGANTIC SIZED GAIN OF 17,849 OI CONTRACTS (55.517 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4652 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 437,336

IN ESSENCE WE HAVE A GIGANTIC SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 17,553 CONTRACTS WITH 12,901 CONTRACTS INCREASED AT THE COMEX (SHORT SPECULATORS FAILING TO GET OUT OF THEIR MESS) AND 4652 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 17,553 CONTRACTS OR 54.59 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4652 CONTRACTS) ACCOMPANYING THE GIGANTIC SIZED GAIN IN COMEX OI (12,901) TOTAL GAIN IN THE TWO EXCHANGES 17,553 CONTRACTS. WE NO DOUBT HAD 1) ATTEMPTED SPECULATOR SHORT COVERINGS WITH SMALL SUCCESS// CONTINUED GOOD BANKER ADDITIONS BUT THEY ALSO SUPPLIED THE NECESSARY PAPER SHORT. WE HAD SOME SHORT SPEC ADDITIONS/// // HUGE NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR DEC. AT 58.86 TONNES FOLLOWED BY TODAY’S QUEUE JUMP of 12,000 oz// //NEW STANDING 59.885 TONNES///3) ZERO LONG LIQUIDATION //// //.,4) GIGANTIC SIZED COMEX OPEN INTEREST GAIN 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

DEC

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC :

27,800 CONTRACTS OR 2,780,000 OZ OR 86.465 TONNES 12 TRADING DAY(S) AND THUS AVERAGING: 2317 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES:86.465 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 86.465/3550 x 100% TONNES 2.43% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 86.465 tonnes Initial

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A HUGE SIZED 3064 CONTRACTS OI TO 125,555 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1245 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 1245 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1245 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3393 CONTRACTS AND ADD TO THE 1245 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF 4309 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 21.5435 MILLION OZ//

OCCURRED WITH OUR GAIN IN PRICE OF $0.59….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED UP 0.20 PTS OR 0.01% //Hang Sang CLOSED UP 77,25 OR 0.39% /The Nikkei closed UP 201.36 OR 0.72% //Australia’s all ordinaries CLOSED UP 0.67% /Chinese yuan (ONSHORE) closed UP TO 6.9499//OFFSHORE CHINESE YUAN UP TO 6.9554// /Oil UP TO 76.11 dollars per barrel for WTI and BRENT AT 81,25 / Stocks in Europe OPENED MOSTLY RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A VERY STRONG SIZED 12,901 CONTRACTS UP TO 437,040 WITH OUR THE GAIN IN PRICE..$32.75

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE -ACTIVE DELIVERY MONTH OF DEC… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4652 EFP CONTRACTS WERE ISSUED: ;: , . 0 FEB: 4652 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE:4652 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GIGANTIC SIZED TOTAL OF 17,553 CONTRACTS IN THAT 4652 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A HUGE SIZED COMEX OI GAIN OF 12,901 CONTRACTS..AND THIS GIGANTIC SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF GOLD $32.75. WE ARE WITNESSING SOME SPEC SHORTS ADDITIONS TO THEIR SHORTFALL. BANKERS CONTINUE AS NET BUYERS OF COMEX GOLD CONTRACTS AS THEY HAVE BEEN NET LONG FOR THE PAST FEW MONTHS. WE ALSO HAD HUGE NEWBIE SPECS ADDITIONS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING DEC (59.885)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL (TOTAL SO FAR THIS YEAR 591.535 TONNES)

Dec. 59.885 tonnes

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $32.75) //// ( AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A GIGANTIC GAIN OF 17,849 CONTRACTS ON OUR TWO EXCHANGES >. WE HAD SOME SPEC SHORT ADDITIONS AND ZERO SPEC SHORT COVERINGS.. // WE HAVE GAINED A TOTAL OI OF 55.517 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR GOLD TONNAGE STANDING FOR DEC. (54.57 TONNES), following our queue jump of 12,000 oz//new standing 59.885 tonnes…THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE OF $32.75

WE HAD – 296 CONTRACTS COMEX TRADES REMOVED FROM OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 17,553 CONTRACTS OR 1,755,300 OZ OR 54.59 TONNES

Estimated gold volume 98,742// poor//

final gold volumes/yesterday 242,313/ fair to good

INITIAL STANDINGS FOR DECEMBER 2022 COMEX GOLD //DEC 14

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 32.15 oz Brinks 1 kilobar . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | 4276.750 oz Brinks |

| No of oz served (contracts) today | 144 notice(s) 14400 OZ 0.4479 TONNES |

| No of oz to be served (notices) | 461 contracts 46,100 oz 1.433 TONNES |

| Total monthly oz gold served (contracts) so far this month | 18,792 notices 1,879,200 58.451 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i)Into Brinks 32.15 oz

i kilobar

total deposits 32.15 oz

customer withdrawals:1

i)Brinks: 4276.750 oz

Total withdrawals: 4276.75 oz

total in tonnes: .133 tonnes

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR DECEMBER.

For the front month of DECEMBER we have an oi of 605 contracts having LOST 1958 contracts

We had 2078 contracts served on Tuesday, so we gained 120 contracts or an additional 12,000 oz will stand for gold at the COMEX. We will gain in gold tonnage from this day forth.

The comex is running out of physical gold to serve our good friends over in London

JANUARY LOST 11 contracts to stand at 1315

February GAINED 12,043 contacts up to 373,351

We had 144 notice(s) filed today for 14,400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 144 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 39 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the DEC. /2022. contract month,

we take the total number of notices filed so far for the month (18,792 x 100 oz , to which we add the difference between the open interest for the front month of (DEC. 605 CONTRACTS) minus the number of notices served upon today 144 x 100 oz per contract equals 1,925,300 OZ OR 59.885 TONNES the number of TONNES standing in this active month of DEC.

thus the INITIAL standings for gold for the DEC contract month:

No of notices filed so far (18,792 x 100 oz+ (605 OI for the front month minus the number of notices served upon today (144} x 100 oz} which equals 1,925,300 oz standing OR 59.885 TONNES in this active delivery month of DEC..

TOTAL COMEX GOLD STANDING: 59.885 TONNES (A POOR STANDING//COMEX RUNNING OUT OF PHYSICAL TO SERVE UPON OUR LONGS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

we had one adjustment of 110,631.591 oz Brinks

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,091,091.771 OZ 65.04 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 23,300,853,953 OZ

TOTAL REGISTERED GOLD: 11,713,540.992 OZ (364.34 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 11,587,312,961 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,622,469 OZ (REG GOLD- PLEDGED GOLD) 299.29 tonnes//rapidly declining

END

SILVER/COMEX

DEC 14//INITIAL DEC. SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2,078,240.190 oz CNT Brinks |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 579,692.685 oz CNT |

| No of oz served today (contracts) | 133 CONTRACT(S) (655,000 OZ) |

| No of oz to be served (notices) | 1238 contracts (6,190,000 oz) |

| Total monthly oz silver served (contracts) | 3548 contracts (17,740,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into CNT: 579,692.685 oz

Total deposits: 579,692.685 oz

JPMorgan has a total silver weight: 150.778 million oz/297.980 million =50.62% of comex .//dropping fast

Comex withdrawals:2

i) Out of CNT: 599,904.790 oz

ii) Out of Brinks: 1,478,335.400 oz

Total withdrawals; 2,078,240.190 oz

adjustments: 3

ii) customer to dealer: Delaware 49,656,508 oz

and

HSBC 25,735.154 oz

dealer to customer: Loomis 4938.500 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 33,684 MILLION OZ (declining rapidly).TOTAL REG + ELIG. 297.980MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF DEC OI: 1371 CONTRACTS HAVING GAINED 11 CONTRACT(S.)

WE HAD 22 NOTICES FILED ON TUESDAY. SO WE GAINED A SMALL 33 CONTRACTS OR 165,000 oz

AS A QUEUE JUMP.

JANUARY SAW A GAIN OF 49 CONTRACTS UP TO 1615 CONTACTS.

FEB> GAINED 4 CONTRACTS TO 105 CONTRACTS

March GAINED 2672 contracts UP to 110,269 contracts

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 133 for 665,000 oz

Comex volumes:3,078// est. volume today// poor

Comex volume: confirmed yesterday: 56,435 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in DEC. we take the total number of notices filed for the month so far at 3648 x 5,000 oz = 17,740,000 oz

to which we add the difference between the open interest for the front month of DEC(1371) and the number of notices served upon today 133 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the DEC./2022 contract month: 3548 (notices served so far) x 5000 oz + OI for front month of DEC (1371 – number of notices served upon today (133) x 500 oz of silver standing for the DEC. contract month equates 23.930 million oz.. Also we have another criminal element to our silver oz standing, the use of Exchange for Risk/ Today an addition of 0 EFR contract transfers which are “Exchange for risk” settlements. I do not want to bore you but needless to say they are not physical transfers so are criminal in nature. There have been 2100 Exchange for Risk contracts settled these past 8 days for 10.500 million oz. Thus total delivery: 34.443 million oz.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:37,982// est. volume today// poor

Comex volume: confirmed yesterday: 77,222 contracts ( good)

END

GLD AND SLV INVENTORY LEVELS

DEC 14/WITH GOLD DOWN $6.20: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 912.72 TONNES

DEC 13/WITH GOLD UP $32.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD///INVENTORY RESTS AT 910.41

DEC 12/WITH GOLD DOWN $17.60: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

DEC 9/WITH GOLD UP $8.90//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

Dec 8/WITH GOLD UP $4.05, OVER THE PAST 3 WEEKS WE LOST 2.04 TONNES//INVENTORY RESTS AT 908.09 TONNES

NOV 14/WITH GOLD UP $7.30: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 910.12 TONNES

NOV 11/WITH GOLD UP $15.25//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD////INVENTORY RESTS AT 911.57 TONNES

NOV 10/WITH GOLD UP $40.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.38 TONNES

NOV 9/WITH GOLD DOWN $2.00: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES INTO THE GLD////INVENTORY RESTS AT 908.38 TONNES

NOV 8/WITH GOLD UP $34.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.47 TONNES FROM THE GLD//: INVENTORY RESTS AT 905.49 TONNES

NOV 7/WITH GOLD UP $2.95: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.63 TONNES FROM THE GLD//INVENTORY RESTS AT 906.96. TONNES

NOV 4/WITH GOLD UP $44.45 TO $1673.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.48 TONNES FROMTHE GLD////INVENTORY RESTS AT 911.59 TONNES.

NOV 3/WITH GOLD DOWN $18.30 TO $1628.85: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.05 TONNES FROM THE GLD////INVENTORY RESTS AT 915.07 TONNES

NOV 2/WITH GOLD UP 55 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 919.12 TONNES.

NOV 1/WITH GOLD UP $9.20 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES FORM THE GLD../INVENTORY RESTS AT 920.57 TONNES

OCT 31/WITH GOLD DOWN $4.00; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD//INVENTORY RESTS AT 922.59. TONNES//

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

GLD INVENTORY: 912.72 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

DEC 14/WITH SILVER UP 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 512.000 MILLION OZ//

DEC 13/WITH SILVER UP 59 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 600,000 OZ FROM THE SLV////INVENTORY RESTS AT 513.900 MILLION OZ//

DEC 12/WITH SILVER DOWN 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 514.500 MILLION OZ//

DEC 9/WITH SILVER RISING 77 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.2 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 514.500 MILLION OZ.

DEC 8/WITH SILVER RISING 34 CENTS TODAY: OVER THE PAST 3 WEEKS, WE HAVE GAINED A STRONG: 44.777 MILLION OZ/INVENTORY RESTS AT 516.700 MILION OZ.

NOV 14/WITH SILVER UP 41 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 11/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ FROM THE SLV///INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 10/WITH SILVER UP 39 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 368,000 OZ INTO THE SLV///INVENTORY RESTS AT 472.476 MILLION OZ//

NOV 9/WITH SILVER DOWN 10 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV/; A WITHDRAWAL OF 3.821 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 472.108 MILLION OZ//

NOV 8/WITH SILVER UP 48 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.751 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 475.929 MILLION OZ//

NOV 7/WITH SILVER UP 12 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 4/WITH SILVER UP $1.31 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.972 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 3.WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 566,000 OZ FROM THE SLV////INVENTORY RESTS AT 482.650 MILLION OZ//

NOV 2/WITH SILVER DOWN 9 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 92,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.216 MILLION OZ//

NOV 1/WITH SILVER UP 53 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 415,000 OZ FORM THE SLV////INVENTORY RESTS AT 483.308 MILLION OZ

OCT 31: WITH SILVER FLAT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .644 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 483.723 MILLION OZ//

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: A WITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

CLOSING INVENTORY 512.000 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

Pam and Russ Marten (WallStreet on Parade)

An Insider Blows the Whistle on How the Fed Has Allowed Crypto to Invade Federally-Insured Banks

By Pam Martens and Russ Martens: December 14, 2022 ~ Katie Cox worked for the Federal Reserve for 32 years, the last two decades of which were spent overseeing complex proposals for bank mergers. She left the Fed in 2020. Last Wednesday Katie Cox penned a shocker of a column for American Banker. She opened with this: “Suppose you’re a crypto company that wants to own a bank approved to engage in digital-asset activities. Here’s the fast-track way you might achieve that, while complying with rules in place since August: Go buy a bank, any bank. Convert your bank to a Federal Reserve member bank, meaning that your bank’s federal supervisor will now be the Fed, not the Office of the Comptroller of the Currency or the Federal Deposit Insurance Corp. Wait a little bit, maybe six months. Then send the Fed a letter notifying it that your bank is going … Continue reading →

FacebookTwitterWhatsAppLinkedInEmail

Sam Bankman-Fried Quietly Bought an SEC-Registered Stock Trading Operation; There Are Big Questions as to What’s Happening with Customer Accounts

By Pam Martens and Russ Martens: December 13, 2022 ~ Yesterday, just hours before Sam Bankman-Fried was arrested in the Bahamas at the request of Damian Williams, the U.S. Attorney for the Southern District of New York, Wall Street On Parade learned that Bankman-Fried had been allowed to purchase an SEC-registered retail brokerage firm in August of last year. The brokerage firm at that time was called RJL Capital Group and was based in Staten Island, New York. Bankman-Fried changed the firm’s name to FTX Capital Markets LLC and moved its headquarters to Broad Street in the financial district in lower Manhattan. According to Wall Street’s self-regulator, FINRA, FTX Capital Markets was licensed to conduct retail stock trading in 32 states. FINRA further notes that the firm’s SEC registration is “pending withdrawal” as of December 5 and all 32 state licenses are listed as “Termination Requested.” It is not clear if … Continue reading →

end

LAWRIE WILLIAMS:

12 Dec 2022

3. Chris Powell of GATA provides to us very important physical commentaries//

Waltzek interviews Bill Murphy of GATA

(GATA)

GoldSeek Radio’s Waltzek interviews GATA Chairman Murphy as metals rise

Submitted by admin on Tue, 2022-12-13 11:28Section: Daily Dispatches

11:25a ET Tuesday, December 13, 2022

Dear Friend of GATA and Gold:

GoldSeek Radio’s Chris Waltzek today interviews GATA Chairman Bill Murphy, who explains why he sees the monetary metals sector turning upward and cryptocurrency investors gaining interest in the metals. The interview is 11 minutes long and can be heard at GoldSeek’s companion site, SilverSeek, here:

https://silverseek.com/article/goldseek-radio-nugget-bill-murphy-and-away-gold-and-silver

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

END

GOLD/SILVER

/4. OTHER PHYSICAL SILVER/GOLD COMMENTARIES

end

5. Commodity commentaries//IRON ORE

END

6/CRYPTOCURRENCIES/BITCOIN ETC

Bankman denied bail and remains in custody in the Bahamas.

(zerohedge)

“Risk Of Flight Too Great” – Bankman-Fried Denied Bail, Remanded To Custody

TUESDAY, DEC 13, 2022 – 05:02 PM

Update (1700ET): Following his arrest last night, with its expectations of an imminent deportation, Sam Bankman-Fried told a Bahamian judge at an arraignment Tuesday that he wouldn’t waive his right to an extradition hearing.

A defense lawyer said Bankman-Fried planned to fight being sent to the US.

Counsel for SBF has requested bail be set at $250,000.

Manhattan US Attorney Damian Williams called the case “one of the biggest financial frauds in American history” and said the investigation of the alleged scheme is “very much ongoing.”

Which may explain why presiding judge JoyAnn Ferguson-Pratt denied SBF’s bail application, highlighting his “risk of flight” and ordered the crypto executive to be held in custody at the Bahamas Department of Corrections until Feb. 8.

The case has been adjourned to the said date.

* * *

The US Securities and Exchange Commission said it will file charges against FTX founder Sam Bankman-Fried on Tuesday relating to violations of securities law, accusing him of “orchestrating a scheme to defraud equity investors in FTX” and seeking to ban him from the cryptocurrency industry.

“We allege that Sam Bankman-Fried built a house of cards on a foundation of deception while telling investors that it was one of the safest buildings in crypto,” said SEC Chair Gary Gensler

The SEC made the announcement on Monday, shortly after Bahamian authorities arrest Bankman-Fried, the US Attorney’s Office Southern District of New York confirmed.

The SEC has charged Bankman-Fried with violating the anti-fraud provisions of the Securities Act of 1933 and the Securities Exchange Act of 1934. The SEC’s complaint seeks injunctions against future securities law violation that prohibits Bankman-Fried from participating in the issuance, purchase, offer, or sale of any securities except for his own personal account.

Here are some of the wildest accusations from the SEC’s 28-page filing:

SBF improperly diverted assets to his privately held crypto hedge fund:

Unbeknownst to those investors (and to FTX’s trading customers), Bankman-Fried was orchestrating a massive, years-long fraud, diverting billions of dollars of the trading platform’s customer funds for his own personal benefit and to help grow his crypto empire.

Throughout this period, Bankman-Fried portrayed himself as a responsible leader of the crypto community. He touted the importance of regulation and accountability. He told the public, including investors, that FTX was both innovative and responsible. Customers around the world believed his lies, and sent billions of dollars to FTX, believing their assets were secure on the FTX trading platform. But from the start, Bankman-Fried improperly diverted customer assets to his privately-held crypto hedge fund, Alameda Research LLC (“Alameda”), and then used those customer funds to make undisclosed venture investments, lavish real estate purchases, and large political donations.

Bankman-Fried then exempted his crypto hedge fund, Alameda, from risk mitigation procedures:

He told investors and prospective investors that FTX had top-notch, sophisticated automated risk measures in place to protect customer assets, that those assets were safe and secure, and that Alameda was just another platform customer with no special privileges. These statements were false and misleading. In truth, Bankman-Fried had exempted Alameda from the risk mitigation measures and had provided Alameda with significant special treatment on the FTX platform, including a virtually unlimited “line of credit” funded by the platform’s customers.

While he spent lavishly on office space and condominiums in The Bahamas, and sank billions of dollars of customer funds into speculative venture investments, Bankman-Fried’s house of cards began to crumble.

Here’s how he diverted funds:

Bankman-Fried diverted FTX customer funds to Alameda in essentially two ways: (1) by directing FTX customers to deposit fiat currency (e.g., U.S. Dollars) into bank accounts controlled by Alameda; and (2) by enabling Alameda to draw down from a virtually limitless “line of credit” at FTX, which was funded by FTX customer assets.

As a result, there was no meaningful distinction between FTX customer funds and Alameda’s own funds. Bankman-Fried thus gave Alameda carte blanche to use FTX customer assets for its own trading operations and for whatever other purposes Bankman-Fried saw fit.

SBF had a secret ‘fiat@ account with a negative $8 billion balance’:

Bankman-Fried directed FTX to have customers send funds to North Dimension in an effort to hide the fact that the funds were being sent to an account controlled by Alameda.

Alameda did not segregate these customer funds, but instead commingled them with its other assets, and used them indiscriminately to fund its trading operations and Bankman-Fried’s other ventures.

This multi-billion-dollar liability was reflected in an internal account in the FTX database that was not tied to Alameda but was instead called “fiat@ftx.com.” Characterizing the amount of customer funds sent to Alameda as an internal FTX account had the effect of concealing Alameda’s liability in FTX’s internal systems.

Here’s how ‘fiat@ftx.com‘ was ‘lost’ in the shuffle:

In 2022, FTX began trying to separate Alameda’s portion of the liability in the “fiat@ftx.com” account from the portion that was attributable to FTX (i.e., to separate out customer deposits sent to Alameda-controlled bank accounts from deposits sent to FTX-controlled bank accounts). Alameda’s portion — which amounted to more than $8 billion in FTX customer assets that had been deposited into Alameda-controlled bank accounts — was initially moved to a different account in the FTX database.

However, because this change caused FTX’s internal systems to automatically charge Alameda interest on the more than $8 billion liability, Bankman-Fried directed that the Alameda liability be moved to an account that would not be charged interest. This account was associated with an individual that had no apparent connection to Alameda. As a result, this change had the effect of further concealing Alameda’s liability in FTX’s internal systems.

SBF has claimed in interviews he ‘wasn’t aware’ of how illiquid Alameda’s collateral had become, yet according to the SEC:

Bankman-Fried was well aware of the impact of Alameda’s positions on FTX’s risk profile. On or about October 12, 2022, for example, Bankman-Fried, in a series of tweets, analyzed the manipulation of a digital asset on an unrelated crypto platform. In explaining what occurred, Bankman-Fried distinguished between an asset’s “current price” and its “fair price,” and recognized that “large positions – especially in illiquid tokens – can have a lot of impact.”

Bankman-Fried asserted that FTX’s risk engine required customers to “fully collateralize a position” when the customer’s position is “large and illiquid enough.” But Bankman-Fried knew, or was reckless in not knowing, that by not mitigating for the impact of large and illiquid tokens posted as collateral by Alameda, FTX was engaging in precisely the same conduct, and creating the same risk, that he was warning against.

SEC charged Bankman-Fried for orchestrating a scheme to defraud equity investors in FTX Trading Ltd. (FTX). The regulatory body noted that the former CEO concealed his “diversion of FTX customers’ funds to crypto trading firm Alameda Research while raising more than $1.8 billion from investors.”

UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK

Plaintiff: SECURITIES AND ) EXCHANGE COMMISSION,

Defendant: SAMUEL BANKMAN-FRIED Plaintiff Securities and Exchange Commission (the “Commission”), for its complaint against Defendant, Samuel Bankman-Fried (“Bankman-Fried”), alleges as follows:

SUMMARY

1. From at least May 2019 through November 2022, Bankman-Fried engaged in a scheme to defraud equity investors in FTX Trading Ltd. (“FTX”), the crypto asset trading platform of which he was CEO and co-founder, at the same time that he was also defrauding the platform’s customers. Bankman-Fried raised more than $1.8 billion from investors, including U.S. investors, who bought an equity stake in FTX believing that FTX had appropriate controls and risk management measures. Unbeknownst to those investors (and to FTX’s trading customers), Bankman-Fried was orchestrating a massive, years-long fraud, diverting billions of dollars of the trading platform’s customer funds for his own personal benefit and to help grow his crypto empire.

2. Throughout this period, Bankman-Fried portrayed himself as a responsible leader of the crypto community. He touted the importance of regulation and accountability. He told the public, including investors, that FTX was both innovative and responsible. Customers around the world believed his lies, and sent billions of dollars to FTX, believing their assets were secure on the FTX trading platform. But from the start, Bankman-Fried improperly diverted customer assets to his privately-held crypto hedge fund, Alameda Research LLC (“Alameda”), and then used those customer funds to make undisclosed venture investments, lavish real estate purchases, and large political donations.

3. Bankman-Fried hid all of this from FTX’s equity investors, including U.S. investors, from whom he sought to raise billions of dollars in additional funds. He repeatedly cast FTX as an innovative and conservative trailblazer in the crypto markets. He told investors and prospective investors that FTX had top-notch, sophisticated automated risk measures in place to protect customer assets, that those assets were safe and secure, and that Alameda was just another platform customer with no special privileges. These statements were false and misleading. In truth, Bankman-Fried had exempted Alameda from the risk mitigation measures and had provided Alameda with significant special treatment on the FTX platform, including a virtually unlimited “line of credit” funded by the platform’s customers.

4. While he spent lavishly on office space and condominiums in The Bahamas, and sank billions of dollars of customer funds into speculative venture investments, Bankman-Fried’s house of cards began to crumble. When prices of crypto assets plummeted in May 2022, Alameda’s lenders demanded repayment on billions of dollars of loans. Despite the fact that Alameda had, by this point, already taken billions of dollars of FTX customer assets, it was unable to satisfy its loan obligations. Bankman-Fried directed FTX to divert billions more in customer assets to Alameda to ensure that Alameda maintained its lending relationships, and that money could continue to flow in from lenders and other investors.

5. But Bankman-Fried did not stop there. Even as it was increasingly clear that Alameda and FTX could not make customers whole, Bankman-Fried continued to misappropriate FTX customer funds. Through the summer of 2022, he directed hundreds of millions more in FTX customer funds to Alameda, which he then used for additional venture investments and for “loans” to himself and other FTX executives. All the while, he continued to make misleading statements to investors about FTX’s financial condition and risk management. Even in November 2022, faced with billions of dollars in customer withdrawal demands that FTX could not fulfill, Bankman-Fried misled investors from whom he needed money to plug a multi-billion-dollar hole. His brazen, multi-year scheme finally came to an end when FTX, Alameda, and their tangled web of affiliated entities filed for bankruptcy on November 11, 2022.

The first thing to note in the rap sheet is the date, “From at least May 2019 . . .”, by which the SEC means FTX’s entire existence. It was around May 2019 that SBF bought the FTX.com domain and the first fundraising announcement didn’t drop until August of that year.

Additionally SEC Chair Gary Gensler, warned:

“The alleged fraud committed by Mr. Bankman-Fried is a clarion call to crypto platforms that they need to come into compliance with our laws.”

Grewal said the charges will be filed publicly “tomorrow” on Dec. 14 at the Southern District of New York.

end

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: UP TO 6.9499

OFFSHORE YUAN: 6.9554

SHANGHAI CLOSED UP 0.20 PTS OR 0.01%

HANG SANG CLOSED UP 77.25 OR 0.39%

2. Nikkei closed UP 201.36 PTS OR 0.72%

3. Europe stocks SO FAR: MOSTLY RED

USA dollar INDEX DOWN TO 103.48 Euro RISE TO 103.48 DOWN 9 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.248!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 135.09/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.9780%***/Italian 10 Yr bond yield RISES to 3.901%*** /SPAIN 10 YR BOND YIELD RISES TO 3.01…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.042//

3j Gold at $1807.65//silver at: 23.68 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 86/100 roubles/dollar; ROUBLE AT 63.71//

3m oil into the 76 dollar handle for WTI and 81 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 135.09 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9277– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9878 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.508% UP 1 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.556% UP 3 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,65…

GREAT BRITAIN/10 YEAR YIELD: 3.3410%

end

Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Gyrate Ahead Of Final Fed Decision Of 2022

WEDNESDAY, DEC 14, 2022 – 08:05 AM

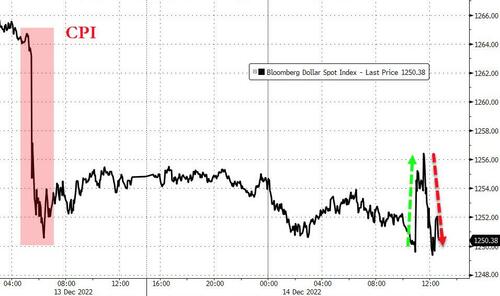

US equity futures were little changed ahead of the final Federal Reserve policy decision of 2022 as traders fretted whether cooler-than-expected inflation will justify smaller rate hikes. Contracts on the S&P 500 and Nasdaq 100 traded on either side of the unchanged line by 730am ET. The underlying benchmarks surged in early trading on Tuesday after the latest CPI data showed a US inflation posted the smallest monthly advance in more than a year, indicating the worst of inflation has likely passed; all gains were subsequently pared however with the S&P closing little changed (See “What Was Behind Today’s Drift Lower In Stocks“). Treasuries and bitcoin rallied, while the dollar slipped.

In premarket trading, Tesla shares fell as much as 1.5%, after Goldman Sachs slashed its price target on the electric-vehicle maker by almost a quarter, with the broker lowering estimates to reflect “softer” supply and demand. Charter Communications, the second-largest US cable TV provider, fell more than 7% in early trading after saying it will spend $5.5 billion to bring higher-speed broadband connections to customers, sparking concerns its capital-spending plan may crimp cash flow. Higher capital expenditure and lower cash flow create near-term uncertainty, yet expanding the footprint could fuel subscriber growth, Bloomberg Intelligence analysts said. Here are other notable premarket movers:

- Marriott International shares decline 1.3% on low volumes as Citi cut its recommendation on the stock to neutral from buy and downgraded a slew of other names in the REITs and Lodgings sectors

- Lennar rises 1.3% and PulteGroup climbs 1.5% as Barclays upgraded both stocks to overweight, turning positive on the US homebuilder sub-sector.

- KeyBanc recommends adding exposure to areas that offer secular growth, relatively stable demand drivers, and/or improving cyclical growth in REIT sector note in which it upgraded EastGroup Properties (EGP US) and Physicians Realty Trust (DOC US) and downgraded five stocks.

- Keep an eye on Stryker as its price target has been hoisted to a Wall Street-high at Cowen, which says there is positive underlying momentum heading into the fourth quarter.

- Apple analysts say that the iPhone maker will face minimal impact if it chooses to allow third-party app stores in Europe, as consumers like the current setup and the region accounts for a very small portion of total App Store revenue.

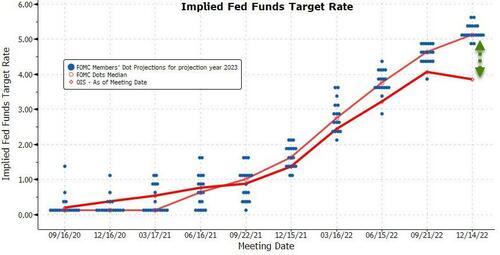

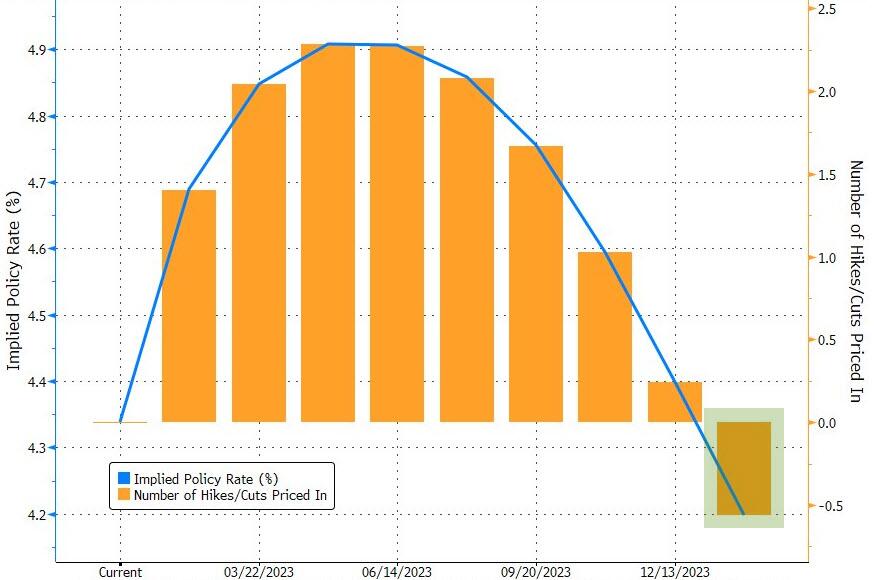

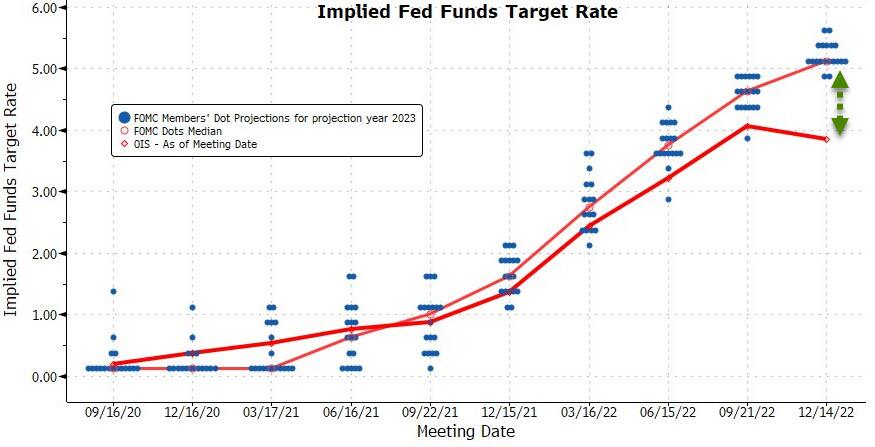

While the Federal Open Market Committee is widely expected to raise rates by 50 basis points, traders will be parsing Chair Jerome Powell’s comments for clues about future decisions, when hikes will stop and whether a rate cut is possible next year. As a reminder, Fed-dated OIS contracts are pricing in a 50bp move for the Fed policy decision and a peak policy rate around 4.83% in May; the dot plot is expected to indicate a 4.9% peak in 2023, corresponding to a 5% upper bound for fed funds rate target band (read our full preview here). The tricky part for Powell , according to Bloomberg, will be convincing investors that this isn’t a dovish pivot and that officials won’t prematurely end their assault against inflation. Stocks have partially erased last week’s slump on bets the Fed will moderate its aggressive tightening as prices cool.

“The question is, with inflation still at generational highs, will the Fed walk through that door?” Stephen Innes, managing partner at SPI Asset Management, wrote in a note. “After an initially high-spirited response, the relatively muted reaction for stocks is likely attributable to pre-risk event positioning, prevailing bearish growth sentiment, technical factors and the devil in the details.”

“The market is now pricing in an aggressive rate-cutting cycle right after we’ve reached the peak rate and I think that’s the unrealistic case,” Max Kettner, chief multi-asset strategist at HSBC Holdings Plc, said in an interview with Bloomberg Television. “What’s really unrealistic is we’ll get some kind of Goldilocks outcome where the Fed will be able to immediately cut rates after they’ve reached the peak rate without having to hold it there for really a sustained period of time.”

Meanwhile, Mark Haefele, chief investment officer at UBS Global Wealth Management, said investors should brace for challenges even as inflation eases: “The rally in the S&P 500 since mid-October has moved too quickly to price in good news,” Haefele wrote in a note. “We have preferred to hedge downside risk with options, rather than reducing our allocation to equities. We continue to favor a more defensive stance when adding exposure.”

After rising from 2019 to 2021, the S&P 500 and Nasdaq 100 are each poised for the worst year since 2008 as 2022 was marked by interest rate hikes, recession fears and the war in Ukraine. Next year is unlikely to bring relief, as strategists generally expect the S&P 500 to end 2023 relatively unchanged from current levels… which likely means the US economy will crater, the Fed will capitulate, and stocks will close double digits percent higher.

In European stocks, travel, miners and tech are the worst performers as all sectors fall, barring energy. Euro Stoxx 50 drops 0.7%. Here are the most notable European movers:

- Hensoldt rises as much as 4.5% before paring gains after the German sensor and radar maker raised its short and medium-term targets.

- Va-Q-tec shares rises as much as 4.5% to €25.35 after EQT Private Equity announced a voluntary public takeover offer for the German insulation company at an offer price of €26/share.

- Stadler Rail gains as much as 2.7% after the company signed a EU2.3b deal with Railways of Kazakhstan to supply 537 sleeper and couchette coaches, including a 20-year service contract.

- Volution Group rises as much as 3.6% after producing what Jefferies describes as an “encouraging” trading update with all geographies outperforming respective forecasts.

- AB Science shares fall as much as 34% after the company said Canada’s drug regulator is seeking additional information on AB Science’s application for approval of masitinib as a treatment for amyotrophic lateral sclerosis.

- Colruyt shares slump as much as 17%, to the lowest since July 2004, after the Belgian retailer reported results that missed estimates.

- Synlab falls as much as 9.7%, the most in a month, after Deutsche Bank downgraded the German laboratory diagnostic services company to hold from buy, due to uncertainties surrounding margin pressure going forward.

- Watches of Switzerland shares drop as much as 7.3%, the most since Sept. 29, after the watchmaker reported 1H results and maintained its guidance for the year.

Earlier in the session, Asian stocks gained as markets cheered a softer US inflation print ahead of the Federal Reserve’s policy decision, while Chinese shares eked out small gains amid Covid disruptions. The MSCI Asia Pacific Index rose as much as 0.9% Wednesday, led by technology shares. Most markets in the region were in the green, with Taiwan and South Korea leading the advance. Gauges in China and Hong Kong closed higher after a volatile trading session. The nation planned to proceed with a closely watched economic policy meeting in Beijing this week, opting not to postpone the gathering as Covid infections surge across the capital. The lower-than-expected readings in both US headline and core inflation bode well for a slowdown in the Federal Reserve’s monetary tightening. Investors will closely monitor the decision later Wednesday and Chair Jerome Powell’s comments for more clues on its future path.

“If the Fed does indeed pause in the months ahead — and with labor market still quite strong — there is some hope now that the US economy may manage to avoid a hard landing,” said Chetan Seth, Asia Pacific equity strategist at Nomura. “This optimism from US will be good news also for some parts of Asian equity space that are exposed to US/global growth such as tech-hardware/semi/memory areas.”

Japanese stocks climbed, following US peers higher, as US CPI data showed a deceleration in inflation. The Topix Index rose 0.6% to 1,977.42 as of market close in Tokyo, while the Nikkei advanced 0.7% to 28,156.21. Sony Group Corp. contributed the most to the Topix Index gain, increasing 1.5%. Out of 2,164 stocks in the index, 1,499 rose and 551 fell, while 114 were unchanged. “US inflation has weakened slightly, but Japanese equities are not moving as aggressively, considering that the easing of US monetary policy might also lead to a stronger yen,” said Tetsuo Seshimo, a portfolio manager at Saison Asset Management.

Australian stocks rose with the S&P/ASX 200 index higher 0.7% to close at 7,251.30, rising for a second session, boosted by strength in mining and energy shares. The advance comes as investors weighed a slowdown in US inflation ahead of the Federal Reserve’s policy decision. In New Zealand, the S&P/NZX 50 index fell 0.1% to

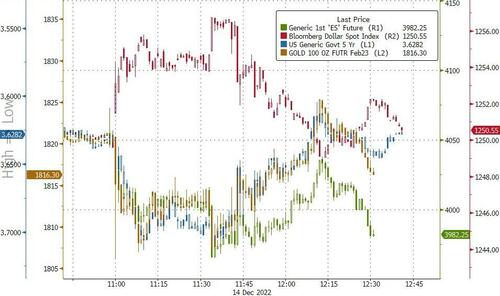

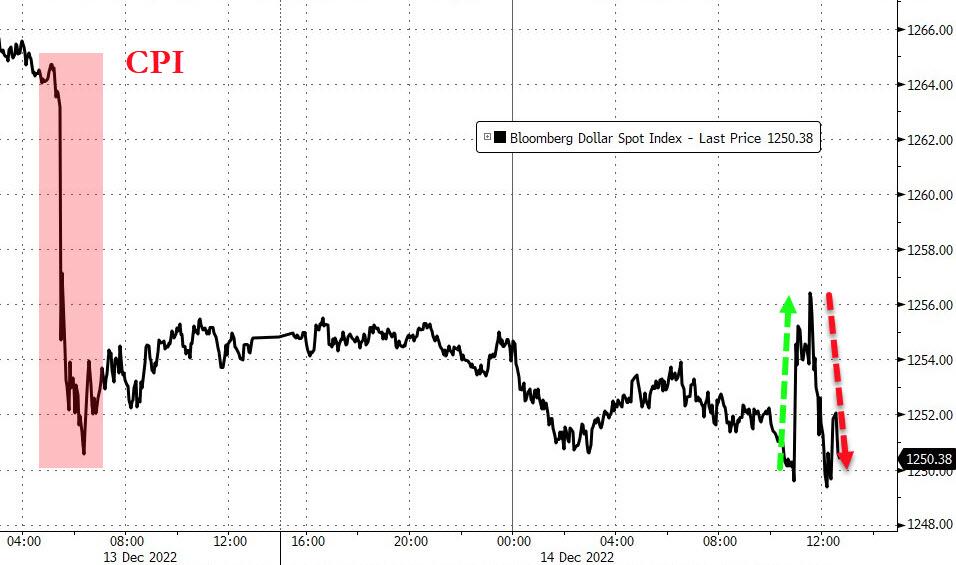

In FX, the Bloomberg Dollar Spot Index fell by 0.3% and the greenback weakened against most of its Group-of-10 peers.

- In the UK, the pound traded near the strongest level since June. Inflation in the country fell from a 41-year high in November, raising the possibility that the worst of the cost-of-living squeeze is over. Consumer prices rose 10.7% from a year earlier, the Office for National Statistics said Wednesday, down from 11.1% in October. Economists expected a rate of 10.9%.

- The euro rose to a day high of $1.0665 and euro-zone sovereign yield curves bear steepened after Germany’s federal government said it plans to issue a record €539 billion in federal debt next year to help fund generous aid for households and companies hit by the energy crisis

- Sweden’s krona was flatlined against the euro but rose against the dollar. Sweden’s inflation rate also came in lower than expected in November

- The yen outperformed all G-10 peers following a report that Bank of Japan officials see the possibility of having a policy review next year

- The New Zealand dollar was the worst performer. Reserve Bank of New Zealand Deputy Governor Christian Hawkesby said the central bank has “more work to do” to curb inflation. New Zealand faces a recession next year amid a global economic slowdown and as the central bank raises interest rates to curb inflation, the government said

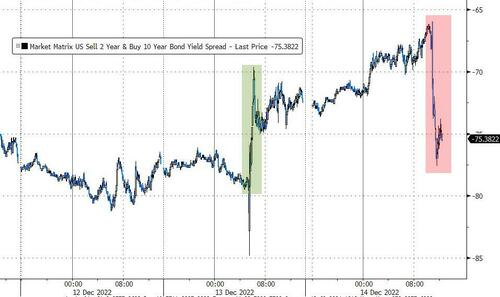

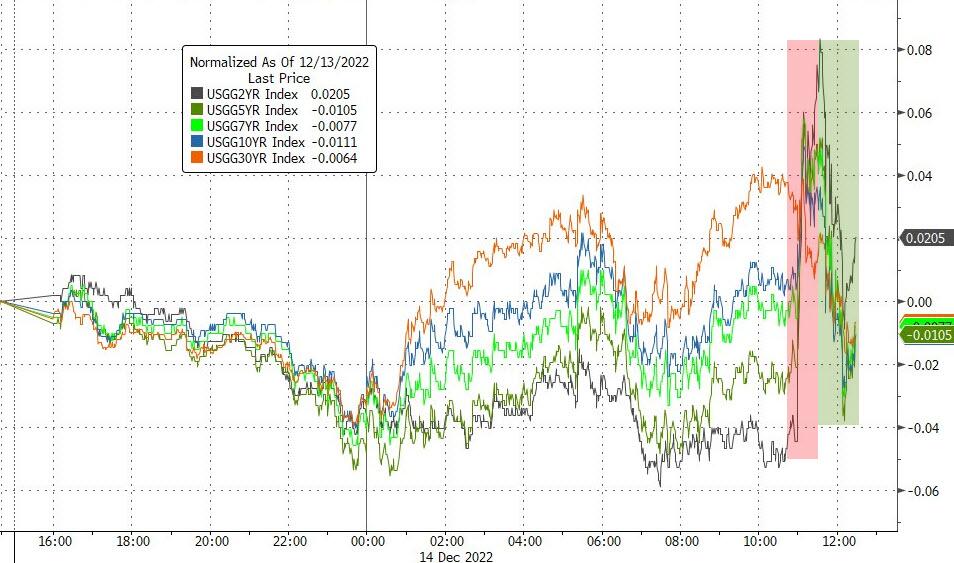

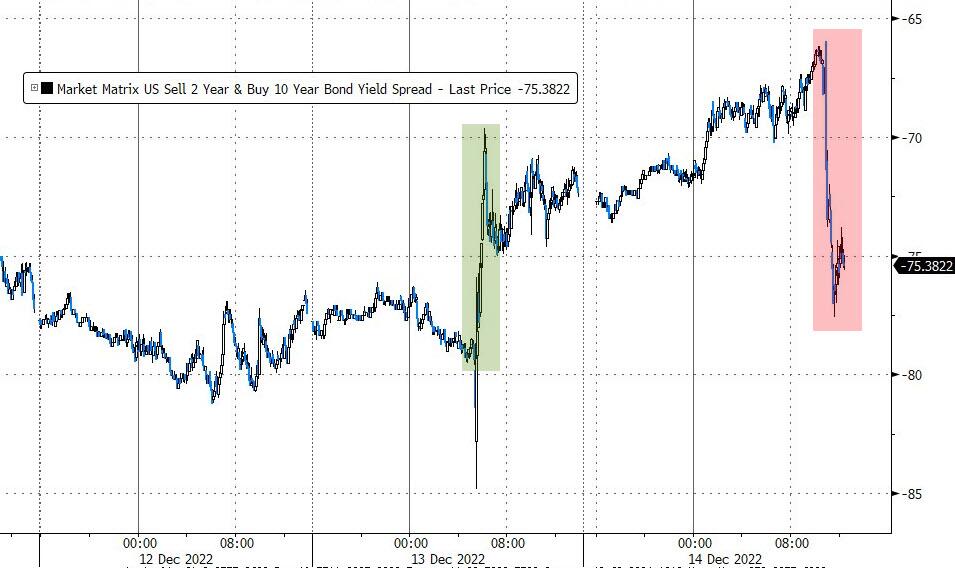

In rates, Treasuries curve extends Tuesday’s steepening move with 2s10s, 5s30s spreads wider by 3.5bp and 4.5bp on the day with the 2-year yield dropping 4bps to 4.180%. Front-end and belly yields are richer by 3bp-4bp as ahead of Fed rate decision, revised summary of economic projections and Chair Powell press conference. US 10-year around 3.50% is slightly richer vs Tuesday’s close, outperforming bunds and gilts by 7bp and 3bp in the sector following wider steepening moves across the German and UK curves. European bonds lag led by Italian debt after the EU said Italy’s progress on key fiscal reforms has been insufficient. Italian bonds lag Treasuries by 12bp in 10-year sector, leading losses across the European rates complex. Gilts twist-steepened, shaving 6bps off the 2-year yield to 3.402%, after UK inflation dipped from a 41-year high in November.

To the day ahead now, and the main highlight will be the Federal Reserve’s policy decision and Chair Powell’s subsequent press conference. We’ll also hear from the ECB’s Elderson. On the data side, we’ll get the UK CPI reading for November and Euro Area industrial production for October.

Market Snapshot

- S&P 500 futures little changed at 4,021.25

- STOXX Europe 600 down 0.5% to 440.28

- MXAP up 0.9% to 160.16

- MXAPJ up 1.0% to 520.22

- Nikkei up 0.7% to 28,156.21

- Topix up 0.6% to 1,977.42

- Hang Seng Index up 0.4% to 19,673.45

- Shanghai Composite little changed at 3,176.53

- Sensex up 0.3% to 62,729.76

- Australia S&P/ASX 200 up 0.7% to 7,251.30

- Kospi up 1.1% to 2,399.25

- German 10Y yield little changed at 1.96%

- Euro up 0.2% to $1.0652

- Brent Futures little changed at $80.70/bbl

- Brent Futures little changed at $80.71/bbl

- Gold spot down 0.1% to $1,809.07

- U.S. Dollar Index down 0.14% to 103.84

Top Overnight News from Bloomberg

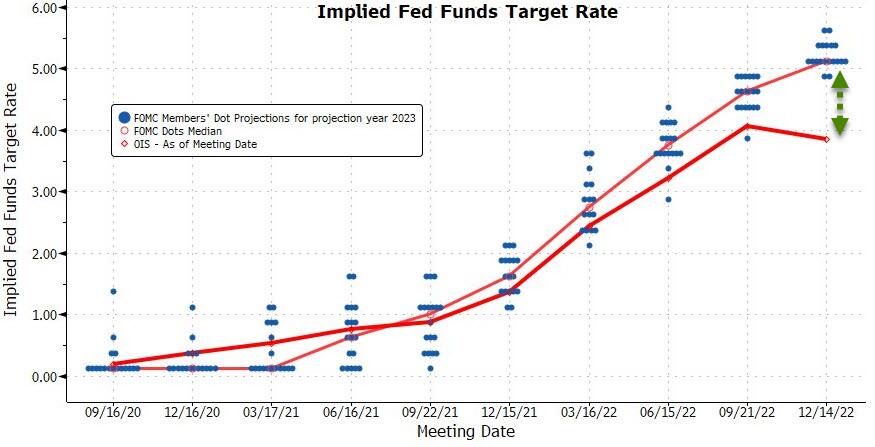

- The Federal Reserve is poised to moderate its aggressive tightening on Wednesday while signaling that interest rates will ultimately go higher than previously forecast

- The SNB will almost certainly raise interest rates this week, but economists are split three ways on how aggressively officials will act to tame inflation that’s the lowest in the OECD. While a large majority of forecasters anticipate a half-point hike on Thursday to reach 1%, Bloomberg’s survey also shows predictions for a larger or smaller step by the central bank led by President Thomas Jordan

- ECB policymakers’ primary lever to rein in soaring prices remains interest rates, with a half-point hike expected at Thursday’s Governing Council meeting. But President Christine Lagarde and her colleagues have also promised the “key principles” for so-called quantitative tightening, which is expected to kick off early next year

- New inflation forecasts to be presented by the ECB on Thursday are set to show readings above 2% through 2025, Reuters reported, citing one person familiar with the prediction

- The theme of selling volatility across the major currencies’ curves remains intact, and got another boost from the latest US CPI data, yet overnight volatility in the euro remains near the upper end of its range this year

- EU policymakers agreed to raise €20 billion ($21.3 billion) from the region’s carbon market to help finance the bloc’s strategy to wean itself off Russian natural gas, in a deal that is set to involve the use of some permits currently withdrawn from the system

- China will stop releasing comprehensive data on new Covid cases after the dropping of mandatory testing meant the numbers no longer reflected reality

- Chinese leaders are planning to proceed with a closely watched economic policy meeting in Beijing this week, opting not to postpone the gathering as Covid infections surge across the capital, according to people familiar with the matter

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks took impetus from the gains across global peers following the softer-than-expected US CPI data but with upside capped ahead of the slew of central bank decisions beginning with the FOMC later today. ASX 200 was led by strength in tech and commodity-related stocks amid the lower yields and a softer dollar. Nikkei 225 climbed back above the 28,000 level albeit with further upside limited after mixed BoJ Tankan and Machinery Orders data in which the large manufacturers’ sentiment index declined to its lowest since March 2021. Hang Seng and Shanghai Comp were mildly positive as China plans to allocate over CNY 1tln to bolster its semiconductor industry and amid further reopening headlines, although cases were said to be increasing rapidly in Beijing and China postponed its economic policy meeting that was set to begin on Thursday amid surging cases.

Top Asian News

- China is to offer a second booster and the National Health Commission said the second COVID vaccine booster dose can be given to high-risk groups and elderly people over 60 years old. It was also separately reported that China’s health authority said it will stop reporting asymptomatic cases from today, according to Reuters.

- China’s retreat from zero-COVID policy has reportedly sparked a wealth management product sell-off with fund managers forced to sell holdings amid a wave of redemptions, according to FT.

- China’s stats bureau cancelled the December 15th press conference on November economic data and will release the data online, according to Reuters.

- US is to add more than 30 Chinese companies to its trade blacklist as early as this week, according to Bloomberg citing a source familiar with the matter.

- Japan’s ruling LDP tax panel chief said senior officials agreed to raise corporate tax, tobacco tax and income tax as sources of funding the defence budget. It was later reported that Japan’s government is to tap the FX reserves special account for JPY 3.1tln in defence spending boost, according to a government draft cited by Reuters.

- China has decided against postponing its key economic policy meeting, via Bloomberg; subsequently, Reuters citing sources reports that this will occur between December 15th-16th.

- China is reportedly asking some large banks to purchase bonds after recent slump to stabilise the domestic bond market, Bloomberg reports.

- China’s NBS says domestic demand recovery is insufficient, via Bloomberg citing Radio; adds, the economic recovery can maintain momentum.

European bourses are under pressure across the board, Euro Stoxx 50 -0.7%, as the CPI-induced upside wanes ahead of the FOMC & Powell thereafter. Stateside, US futures are softer though comparably more contained, ES -0.1%, in a paring of the inflation move. A paring which has been attributed to various factors including it being a function of traders getting ahead of market pricing, while others cited valuations, technical factors and profit-taking.

Top European News

- New ECB forecasts will put inflation comfortably above 2% in 2024 and just above in 2025, according to a Reuters source. Reuters polling pencilled in 2023 inflation at 6%, 2024 at 2.3% and 2025 at 1.9%

- UK Chancellor Hunt said they will be announcing the details of further energy support for businesses very shortly, according to Reuters.

- 8/9 members of The Times’ Bank of England shadow MPC believe the BoE should raise rates by 75bps (vs. consensus of a 50bps move) with just one member opting for 50bps.

FX

- USD has continued to slip with the index down to 103.66 at worst, nearing Tuesday’s 103.57 trough to the benefit of most G10 peers.

- The JPY outperforms with USD/JPY dropping below 135.00 to a 134.61 low in wake of BoJ sources, while we are back to this level now the initial move pared given it seemingly echoes recent commentary from Tamura.

- EUR was already benefitting from the USD move but has derived further impetus from ECB sources indicating CPI to remain above target in 2024, with EUR/USD above 1.0670 at best.

- Sterling slipped in wake of softer CPI though Cable has more than recovered since to an, unsuccessful, test of 1.24 on multiple occasions.

- Kiwi fails to benefit from the USD action post-data, with AUD upside and unusually large NZD/USD OpEx perhaps factoring.

- BoJ sees the possibility of conducting a review in 2023, according to Bloomberg sources.

- Czech Central Bank vice governor Mora would support 25bps rate increase if a majority could be found, would be in favour of 50-75bps increase, according to fintag.cz.

- PBoC set USD/CNY mid-point at 6.9535 vs exp. 6.9556 (prev. 6.9746)

Fixed Income

- Bunds under marked pressure given a sizeable 2023 issuance remit and subsequent hawkish ECB source reports; with the benchmark sub-140.00 though above Tuesday’s 139.77 low.

- A sources piece which also sparked pressure in the periphery and, to a lesser extent, in USTs, though the benchmarks remains marginally firmer overall.

- Stateside, focus remains very much on the FOMC and as the session progresses we are seeing long-end yields begin to lift as the associated benchmarks slip further.

- German Debt Agency: intends to issue federal securities with a total volume of EUR 539bln in 2023. Total of EUR 274bln to be raised on capital markets in auctions. Further EUR 242bln to be issued on the money market.

Commodities

- Crude benchmarks are firmer on the session, with upside just shy of 1.0% at best, though both WTI and Brent remain shy of yesterday’s and by extension recent peaks.

- US Energy Inventory Data (bbls): Crude +7.8mln (exp. -3.6mln), Gasoline +0.9mln (exp. +2.7mln), Distillate +3.9mln (exp. +2.5mln), Cushing +0.6mln.

- EU gas price cap proposal put the price level at EUR 160-220MWh and EU states were reportedly considering delaying the decision on the gas price cap level.

- German Economy Minister said EU countries made progress on technical issues linked to gas price caps, but they are not through yet and it makes sense for EU countries to take some more time to finalise the gas price cap policy. Furthermore, discussions will continue on Monday and it was stated that it might be possible that they reach a solution via a majority vote, while they are said to have reached a 90-95% agreement on the gas price cap issue, but the big and symbolic issues have not yet been resolved.

- Czech Industry Minister said they proposed a revision in February to assess the gas price cap’s impact and proposed a gas price cap excluding OTC contracts, while the price level for triggering the gas price cap is the only open issue for next Monday.

- EU Energy Commissioner said Europe is not out of the danger zone regarding energy supplies.

- IEA Monthly Oil Market Report: raises 2022 oil demand growth estimate by 140k BPD to 2.3mln BPD, 2023 raised by 100k BPD to 1.7mln BPD.

- FT writes that “Traders are warning that thin volumes and erratic trading have disconnected the price of nickel on the London Metal Exchange from the rest of the global market”.

- Spot gold and silver are little changed overall, failing to derive any real traction from the general pullback in equity performance; holding steady above the USD 1800/oz mark and as such is well within Tuesday’s USD 1778-1824/oz range.

US Event calendar

- 07:00: Dec. MBA Mortgage Applications +3.2%, prior -1.9%

- 08:30: Nov. Import Price Index MoM, est. -0.5%, prior -0.2%; YoY, est. 3.2%, prior 4.2%

- 08:30: Nov. Export Price Index MoM, est. -0.5%, prior -0.3%; YoY, est. 5.7%, prior 6.9%

- 08:30: Nov. Import Price Index ex Petroleu, est. -0.5%, prior -0.2%

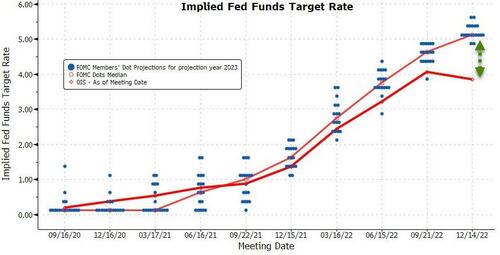

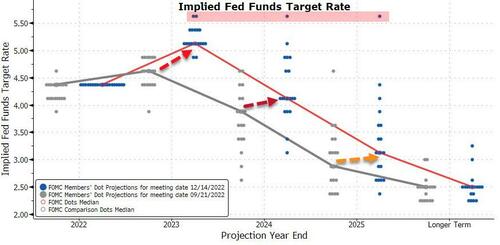

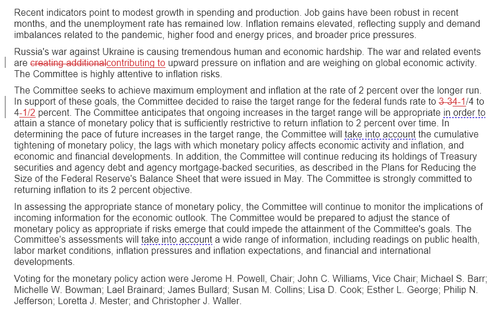

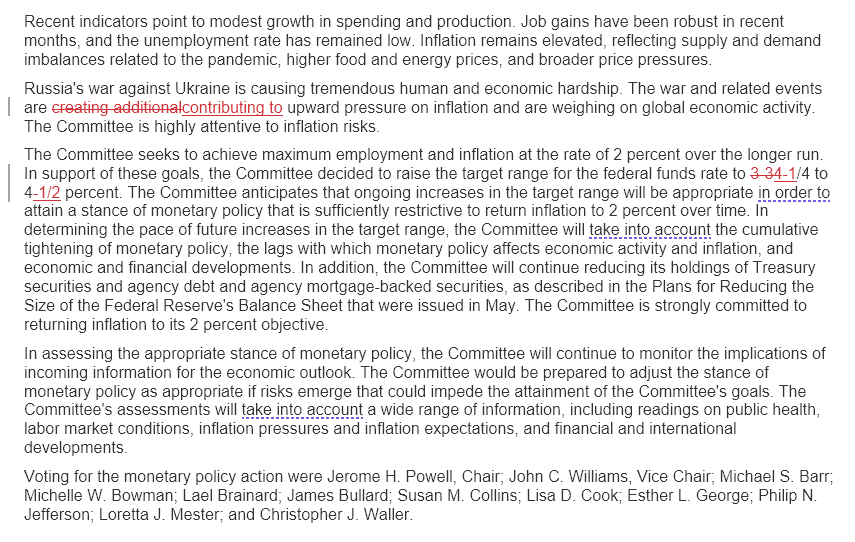

- 14:00: Dec. FOMC Rate Decision (Lower Bound, est. 4.25%, prior 3.75%; Upper Bound, est. 4.50%, prior 4.00%)

DB’s Jim Reid concludes the overnight wrap

A bit of personal news. I was honoured to be announced as DB’s Global Head of Macro Research yesterday to go along with my existing responsibilities. I will now have the regional economists reporting into me and I look forward to working with them all. My good friend Peter Hooper will become the Vice-Chair of DB Research and will continue to use his wealth of experience and connections to enhance DB research in this prestigious position. Congrats to Peter. Anyway, I may regret saying this but I’m very keen to hear from all our readers what you think works well and doesn’t work well in economic research. Not just at DB but across the street. Formats, style, content etc. etc. Any comments or suggestions will be gratefully received. My golf club jokes that any suggestions to the committee about how to run the club and course are very welcome and can be put in the member’s feedback box. The snag is that this box is kept on a small island in the middle of the big lake on the 10th hole.

The market playbook yesterday almost worked as perfectly as a slight draw into a tucked away pin at the back left of the green. However you would have had to get out of the position by 10am NY time to benefit most and avoid turning an eagle into a lowly birdie. That would have taken some discipline and luck. This week we’ve been highlighting the slightly below consensus DB CPI forecast, how big CPI/FOMC day moves have been all year, and how much S&P 500 single day maturity event risk hedging there has been ahead of the CPI and FOMC. This option hedging would have to be unwound with buying of the market as long as you didn’t get a much worse inflation print.

At just before 10am NY time the S&P 500 was +2.74%, and 2yr and 10yr yields had fallen -21.6bps and -18.8bps respectively, and all looked to be going to script. However, by the close this had mellowed to +0.73%, -15.7bps and -11.0bps respectively. Option hedging seems to be high again today around the FOMC so we could see another day of volatility as positions ultimately need to be squared post the event. Our equity strategists continue to be convinced that the set up is broadly bullish risk.

On the specifics of the report, there was plenty of good news, as monthly core CPI fell to its lowest in 15 months, and it also marked the first time in nearly 3 years that we’ve had two downside surprises on headline CPI in a row. In terms of the details, monthly CPI came in at +0.1% in November (vs. +0.3% expected), which in turn took the year-on-year reading down to +7.1% (vs. +7.3% expected). Now obviously 7.1% is still a very high number, but that’s the lowest print of 2022 so far and it’s also the 5th consecutive decline since its +9.1% peak back in June. At the same time, we had some positive news on core CPI, with the monthly print surprising on the downside as well at +0.2% (vs. +0.3% expected), which took the year-on-year measure down to +6.0% (vs. +6.1% expected).

If you were looking for points of caution, one is that the stickier prices in the consumer basket were still rising at a decent rate. They tend to change relatively slowly and are better correlated with future inflation. For instance, the Atlanta Fed break down the CPI report into a “flexible CPI” and “sticky CPI” print, and found that monthly sticky CPI was still running at +5.5% on an annualised basis in November. Another thing to remember is that for the same month as the CPI, wage pressures were still very strong, as we heard in the jobs report earlier in the month.