DEC 15//ANOTHER RAID ON GOLD/SILVER//GOLD CLOSED DOWN $29.20 TO $1778.20//SILVER CLOSED DOWN 74 CENTS TO $23.11//PLATINUM CLOSED DOWN $24.55 TO $1007.50//PALLADIUM CLOSED DOWN $121.85 TO $1796.55//COVID UPDATES//RON DESANTIS FORMS GRAND JURY ACCUSING PHARMACEUTICAL GIANTS OF CRIMES AGAINST HUMANITY//DR PAUL ALEXANDER//VACCINE IMPACT//VACCINE INJURY//USA, UK AND ECB ALL RAISE THEIR RATES BY 50 BASIS POINTS//UKRAINE VS RUSSIA WITH UK ADMITTING IT HAD BOOTS ON THE GROUND IN THE UKRAINE//USA RETAIL SALES PLUMMET/ALSO INDUSTRIAL PRODUCTION//SWAMP STORIES FOR YOU TONIGHT//

072 C GOLDMAN 1 118 C MACQUARIE FUT 13 190 H BMO CAPITAL 164 323 C HSBC 20 435 H SCOTIA CAPITAL 197 523 C INTERACTIVE BRO 1 624 H BOFA SECURITIES 893 661 C JP MORGAN 544 21 685 C RJ OBRIEN 1 686 C STONEX FINANCIA 1 700 C UBS 2 737 C ADVANTAGE 1 800 C MAREX SPEC 2 15 880 C CITIGROUP 21 905 C ADM 1

TOTAL: 949 949

COMEX//NOTICES FILED re JPMorgan 39/144

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR DEC. CONTRACT: 449 NOTICES FOR 44,900 OZ or 2.951 TONNES

total notices so far: 19,741 contracts for 1,974,100 oz (61.402 tonnes)

SILVER NOTICES: 16 NOTICE(S) FILED FOR 80,000 OZ/

total number of notices filed so far this month 3564 for 17,820,000 oz

END

GLD

WITH GOLD DOWN $29.20

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////HUGE CHANGES IN GLD INVENTORY:A WITHDRAWAL OF 1.16 TONNES TONNES OUT IF THE GLD

INVENTORY RESTS AT 911.56 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $.74

AT THE SLV// :/HUGE CHANGES IN SILVER INVENTORY AT THE SLV THESE PAST 3 WEEKS! A LOSS OF 2.0 MILLION OZ FROM THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 510.000 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

NOTE EXACT NUMBERS!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GOOD SIZED 522 CONTRACTS TO 126,077 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.07 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR SHORTERS/HFT WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.07 AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD AN STRONG SIZED GAINED IN OUR TWO EXCHANGES OF 888 CONTRACTS. AS WELL WE HAD EXCHANGE FOR RISK TRANSFER OF 0 CONTRACTS. WE HAD SOME ATTEMPTED SPEC SHORT COVERINGS OF THEIR SHORTFALL. .WE PROBABLY HAD ZERO SHORT ADDITIONS WITH THE PRICE RISE OF THE SILVER. // OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. BUT THEY ALSO SUPPLIED THE NECESSARY SHORT CONTRACTS>>> SOME INCREASE OF NEWBIE SPEC LONGS ADDED TO THEIR POSITIONS CAUSING ADDITIONAL MISERY TO OUR SHORTERS.

WE MUST HAVE HAD: A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 23 .24. MILLION OZ FOLLOWED BY TODAY;S E.F.P. JUMP TO LONDON of 500,000 OZ // V) GOOD SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL —46

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS DEC. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF DEC:

TOTAL CONTRACTS for 13 days, total 6849 contracts: OR 34.745 MILLION OZ PER DAY. (526 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 34.745 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 34.745 MILLION OZ INITIAL

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 522 WITH OUR $0.07 GAIN IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 381 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 23.24 MILLION OZ FOLLOWED BY TODAY:S 450,000 E,F,P. JUMP //NEW STANDING 23.480 MILLION OZ + EFR = 33.980 MILLION OZ. .. WE HAVE AN HUGE SIZED GAIN OF 949 OI CONTRACTS ON THE TWO EXCHANGES FOR 4.745 MILLION OZ.. THE SILVER SHORTS ARE NOW TRAPPED AS THEY ARE HAVING CONSIDERABLE DIFFICULTY IN COVERING THOSE SHORTS.

WE HAD 16 NOTICE(S) FILED TODAY FOR 80,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 706 CONTRACTS TO 436,334 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 279 CONTRACTS.

.

THE SMALL SIZED INCREASE IN COMEX OI CAME WITH OUR STRONG LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR DEC. AT 58.86 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY:S HUGE QUEUE JUMP of 892 contracts or 89,200 oz//(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). NEW STANDING 62.659 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS PRICE OF $6.20 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 888 OI CONTRACTS (2.737 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1586 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 436,334

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 888 CONTRACTS WITH 706 CONTRACTS DECREASED AT THE COMEX (SHORT SPECULATORS FAILING TO GET OUT OF THEIR MESS) AND 1586 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 888 CONTRACTS OR 2.737 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1586 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (706) TOTAL GAIN IN THE TWO EXCHANGES 888 CONTRACTS. WE NO DOUBT HAD 1) ATTEMPTED SPECULATOR SHORT COVERINGS WITH SMALL SUCCESS// CONTINUED GOOD BANKER ADDITIONS BUT THEY ALSO SUPPLIED THE NECESSARY PAPER SHORT. WE HAD SOME SHORT SPEC ADDITIONS/// // SMALL NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR DEC. AT 58.86 TONNES FOLLOWED BY TODAY’S QUEUE JUMP of 89,200 oz// //NEW STANDING 62,659 TONNES///3) ZERO LONG LIQUIDATION //// //.,4) SMALL SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

DEC

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC :

29,386 CONTRACTS OR 2,938,600 OZ OR 91.40 TONNES 13 TRADING DAY(S) AND THUS AVERAGING: 2260 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES:91.40 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 91.40/3550 x 100% TONNES 2.57% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 91.40 tonnes Initial

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GOOD SIZED 522 CONTRACTS OI TO 126,077 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 381 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 381 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 381 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 522 CONTRACTS AND ADD TO THE 381 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN HUGE SIZED GAIN OF 903 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 4.515 MILLION OZ//

OCCURRED WITH OUR SMALL GAIN IN PRICE OF $0.07….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 7.80 PTS OR 0.25% //Hang Sang CLOSED DOWN 304.88 OR 1.55% /The Nikkei closed DOWN 104.51 OR 0.37% //Australia’s all ordinaries CLOSED DOWN 0.65% /Chinese yuan (ONSHORE) closed DOWN TO 6.9680//OFFSHORE CHINESE YUAN DOWN TO 6.9673// /Oil UP TO 77,71 dollars per barrel for WTI and BRENT AT 82.63 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

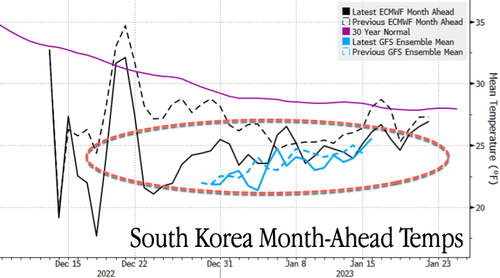

a)NORTH KOREA/SOUTH KOREA

outline

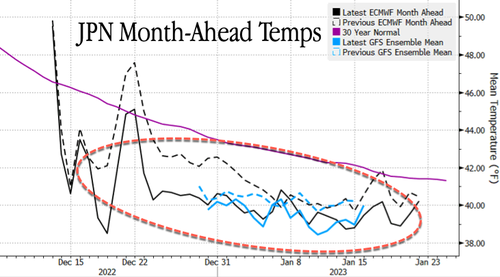

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A VERY SMALL SIZED 706 CONTRACTS DOWN TO 436,334 WITH OUR THE LOSS IN PRICE..$6.20

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE -ACTIVE DELIVERY MONTH OF DEC… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1586 EFP CONTRACTS WERE ISSUED: ;: , . 0 FEB: 1586 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE:1586 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 888 CONTRACTS IN THAT 1586 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI LOSS OF 706 CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF GOLD $6.20. WE ARE WITNESSING SOME SPEC SHORTS ADDITIONS TO THEIR SHORTFALL. BANKERS CONTINUE AS NET BUYERS OF COMEX GOLD CONTRACTS AS THEY HAVE BEEN NET LONG FOR THE PAST FEW MONTHS. WE ALSO HAD SOME NEWBIE SPECS ADDITIONS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING DEC (62.659)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL (TOTAL SO FAR THIS YEAR 591.535 TONNES)

Dec. 62.659 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $6.20) //// ( AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR GAIN OF 888 CONTRACTS ON OUR TWO EXCHANGES >. WE HAD SOME SPEC SHORT ADDITIONS AND ZERO SPEC SHORT COVERINGS.. // WE HAVE GAINED A TOTAL OI OF 2.737 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR DEC. (54.57 TONNES), following our queue jump of 89,200 oz//new standing 62.659 tonnes…THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE OF $6.20

WE HAD – 279 CONTRACTS COMEX TRADES REMOVED FROM OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 888 CONTRACTS OR 88,800 OZ OR 2.737 TONNES

Estimated gold volume 179,427// poor//

final gold volumes/yesterday 149,621/ poor

INITIAL STANDINGS FOR DECEMBER 2022 COMEX GOLD //DEC 15

Total monthly oz gold served (contracts) so far this month

19,741 notices 1,974,100 61.402 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i)Into Brinks 32.15 oz

i kilobar

total deposits 32.15 oz

customer withdrawals:1

i)Brinks: 4469.65 oz

Total withdrawals: 4469.65 oz

total in tonnes: .1390 tonnes

Adjustments: 1

i) Out of Manfra 1929.06 oz/customer to dealer

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR DECEMBER.

For the front month of DECEMBER we have an oi of 1353 contracts having GAINED 748 contracts

We had 144 contracts served on Wednesday, so we gained A HUGE 892 contracts or an additional 12,000 oz will stand for gold at the COMEX. We will gain in gold tonnage from this day forth.

The comex is running out of physical gold to serve our good friends over in London

JANUARY LOST 17 contracts to stand at 1298

February LOST 1426 contacts to 371,527

We had 449 notice(s) filed today for 44,900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 544 notices were issued from their client or customer account. The total of all issuance by all participants equate to 949 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 21 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the DEC. /2022. contract month,

we take the total number of notices filed so far for the month (19,741 x 100 oz , to which we add the difference between the open interest for the front month of (DEC. 1353 CONTRACTS) minus the number of notices served upon today 949 x 100 oz per contract equals 2,064,500 OZ OR 62.659 TONNES the number of TONNES standing in this active month of DEC.

thus the INITIAL standings for gold for the DEC contract month:

No of notices filed so far (19,741 x 100 oz+ (1353 OI for the front month minus the number of notices served upon today (949} x 100 oz} which equals 2,064,500 oz standing OR 62.659 TONNES in this active delivery month of DEC..

TOTAL COMEX GOLD STANDING: 64.214 TONNES (A POOR STANDING//COMEX RUNNING OUT OF PHYSICAL TO SERVE UPON OUR LONGS.

To calculate the number of silver ounces that will stand for delivery in DEC. we take the total number of notices filed for the month so far at 3564 x 5,000 oz = 17,820,000 oz

to which we add the difference between the open interest for the front month of DEC(1148) and the number of notices served upon today 16 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the DEC./2022 contract month: 3564 (notices served so far) x 5000 oz + OI for front month of DEC (1148 – number of notices served upon today (16) x 500 oz of silver standing for the DEC. contract month equates 23.480 million oz.. Also we have another criminal element to our silver oz standing, the use of Exchange for Risk/ Today an addition of 0 EFR contract transfers which are “Exchange for risk” settlements. I do not want to bore you but needless to say they are not physical transfers so are criminal in nature. There have been 2100 Exchange for Risk contracts settled these past 8 days for 10.500 million oz. Thus total delivery: 33.980 million oz.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

DEC 15//WITH GOLD DOWN $31.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 911.56 TONNES

DEC 14/WITH GOLD DOWN $6.20: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 912.72 TONNES

DEC 13/WITH GOLD UP $32.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD///INVENTORY RESTS AT 910.41

DEC 12/WITH GOLD DOWN $17.60: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

DEC 9/WITH GOLD UP $8.90//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

Dec 8/WITH GOLD UP $4.05, OVER THE PAST 3 WEEKS WE LOST 2.04 TONNES//INVENTORY RESTS AT 908.09 TONNES

NOV 14/WITH GOLD UP $7.30: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 910.12 TONNES

NOV 11/WITH GOLD UP $15.25//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD////INVENTORY RESTS AT 911.57 TONNES

NOV 10/WITH GOLD UP $40.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.38 TONNES

NOV 9/WITH GOLD DOWN $2.00: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES INTO THE GLD////INVENTORY RESTS AT 908.38 TONNES

NOV 8/WITH GOLD UP $34.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.47 TONNES FROM THE GLD//: INVENTORY RESTS AT 905.49 TONNES

NOV 7/WITH GOLD UP $2.95: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.63 TONNES FROM THE GLD//INVENTORY RESTS AT 906.96. TONNES

NOV 4/WITH GOLD UP $44.45 TO $1673.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.48 TONNES FROMTHE GLD////INVENTORY RESTS AT 911.59 TONNES.

NOV 3/WITH GOLD DOWN $18.30 TO $1628.85: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.05 TONNES FROM THE GLD////INVENTORY RESTS AT 915.07 TONNES

NOV 2/WITH GOLD UP 55 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 919.12 TONNES.

NOV 1/WITH GOLD UP $9.20 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES FORM THE GLD../INVENTORY RESTS AT 920.57 TONNES

OCT 31/WITH GOLD DOWN $4.00; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD//INVENTORY RESTS AT 922.59. TONNES//

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

GLD INVENTORY: 911.56 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

DEC 15/WITH SILVER DOWN 78 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF EXACTLY 2.00 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 510.000 MILLION OZ

DEC 14/WITH SILVER UP 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 512.000 MILLION OZ//

DEC 13/WITH SILVER UP 59 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 600,000 OZ FROM THE SLV////INVENTORY RESTS AT 513.900 MILLION OZ//

DEC 12/WITH SILVER DOWN 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 514.500 MILLION OZ//

DEC 9/WITH SILVER RISING 77 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.2 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 514.500 MILLION OZ.

DEC 8/WITH SILVER RISING 34 CENTS TODAY: OVER THE PAST 3 WEEKS, WE HAVE GAINED A STRONG: 44.777 MILLION OZ/INVENTORY RESTS AT 516.700 MILION OZ.

NOV 14/WITH SILVER UP 41 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 11/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ FROM THE SLV///INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 10/WITH SILVER UP 39 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 368,000 OZ INTO THE SLV///INVENTORY RESTS AT 472.476 MILLION OZ//

NOV 9/WITH SILVER DOWN 10 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV/; A WITHDRAWAL OF 3.821 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 472.108 MILLION OZ//

NOV 8/WITH SILVER UP 48 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.751 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 475.929 MILLION OZ//

NOV 7/WITH SILVER UP 12 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 4/WITH SILVER UP $1.31 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.972 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 3.WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 566,000 OZ FROM THE SLV////INVENTORY RESTS AT 482.650 MILLION OZ//

NOV 2/WITH SILVER DOWN 9 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 92,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.216 MILLION OZ//

NOV 1/WITH SILVER UP 53 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 415,000 OZ FORM THE SLV////INVENTORY RESTS AT 483.308 MILLION OZ

OCT 31: WITH SILVER FLAT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .644 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 483.723 MILLION OZ//

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: A WITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

CLOSING INVENTORY 510.000 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Schiff: The Fed Hikes Rates To Highest Level Since 2007; That’s A Big Problem

As expected, the Federal Reserve raised interest rates by 50 basis points at the December Federal Open Market Committee (FOMC) meeting. That pushed the federal funds rate to 4.5%. The last time rates were this high was in 2007. That’s bad news for an economy addicted to easy money.

While the pace of rate hikes slowed, the messaging coming out of the Fed was substantially the same as the November meeting.

The official FOMC statement was nearly identical to the November statement. The committee only made some slight changes to the verbiage describing the impact of the Russia-Ukraine war on the global economy.

The messaging relating to the future trajectory of monetary policy was unchanged. The statement said the committee “anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.” It also said the committee will continue to take into account “cumulative tightening” and “the lags with which monetary policy affects economic activity and inflation” as it makes future decisions.

As he did after the November meeting, Federal Reserve Chairman Jerome Powell sounded a hawkish tone. He said, “We have more work to do,” and emphasized that rates would move higher and stay higher longer than initially anticipated.

My view and my colleagues’ view is that this will take some time. We have a long ways to go to get back to price stability.”

Powell also dismissed the notion that the central bank might cut rates next year.

Powell claimed that the Fed has now pushed interest rates into “restrictive” territory. But it’s unclear how he arrived at this conclusion. With CPI still over 7%, real interest rates remain negative. That means the Fed continues to run an accommodative monetary policy. Yes, the Fed has tightened significantly, but it is still behind the inflation curve. In effect, it has slowed the flow of gasoline onto the inflationary fire, but it continues to pour gasoline on the inflationary fire.

When asked about the pain of inflation, Powell said Americans would suffer worse pain if the central bank failed to act and let inflation run out of control. In a tweet, Peter Schiff said that is a moot point.

Inflation is already out of control and the time for the Fed to have acted to prevent it without triggering a severe financial crisis has long since past.”

Nevertheless, Powell continued to hold out hope for a “soft landing,” meaning he thinks the Fed can defeat inflation without tipping the economy into a recession. But despite his optimism, he confessed he doesn’t really know the trajectory of the economy.

I don’t think anyone knows whether we’re going to have a recession or not, and if we do, whether it’s going to be a deep one or not. It’s not knowable.”

The Fed’s Problem

I disagree with Powell’s assertion about a recession. I think it’s a virtual certainty that the economy will spiral into a downturn. And I don’t think it will be short and shallow. I think it will be deep and prolonged.

My pessimism is rooted in the fact that the US economy is addicted to easy money. It is addicted to artificially low interest rates and quantitative easing. You can’t take an addict’s drug away without sending him into withdrawal.

As already noted, interest rates haven’t been this high since 2007. At that point, the Fed was cutting rates due to the housing bust. The economy couldn’t handle interest rates that high.

Rates peaked at 5.25% in 2006. That precipitated the housing bust and ultimately the financial crisis in 2008. Today, the Fed has pushed rates within 1% of that level. But there is a major difference between then and now. The bubbles are bigger. There is more debt. There is more malinvestment. If the extent of the bust is commensurate with the extent of the boom, we’re due for a doozy.

Powell and Company have backed themselves into a corner. They just don’t know it yet (or more likely, they haven’t admitted it).

Now, that doesn’t mean the Fed shouldn’t be raising rates. They should be. They should have raised them a lot more than they have. The problem is they never should have cut them. That was the mistake — it was cutting rates. Raising them back up is really just an acknowledgment of that mistake. But what happens is when the Fed raises rates, it uncovers all of the problems that it created when it reduced rates. Because when it slashed interest rates to zero, it inflated a bubble economy, and it inflated it with inflation. Quantitative easing was inflation.”

In a recent Bloomberg article, a group of economists voiced their fears that the Federal Reserve’s inflation fight may create an unnecessarily deep downturn. However, the Federal Reserve does not create a downturn due to rate hikes; it creates the foundations of a crisis by unnecessarily lowering rates to negative territory and aggressively increasing its balance sheet. It is the malinvestment and excessive risk-taking fuelled by cheap money that lead to a recession.”

In other words, the Fed sealed its fate when it cranked rates down to zero and ran some $5 trillion in QE.

The Fed is a pusher and it has been slowly cranking down the amount of drugs it’s giving to the addict. The addict is already feeling the pain. But the addict is hoping against hope it will get a bigger fix soon. That’s why the markets react with glee every time we get bad economic news or good news on the inflation front. The addict thinks that means the Fed will go back to the status quo – pushing the drugs.

But today, the Fed actually cranked down the drug level even lower. No matter what the pusher says, you can’t take away an addict’s drugs without causing pain. And at some point, the addict is going to go into full-blown withdrawal.

The question is what does the Fed do when this happens? How will it respond when it can no longer plausibly deny the economic chaos? Does it give the addict its drug? Or does it let the addict die?

Powell wants you to believe it will hold course and make the addict go through the pain necessary to get cleaned up. He claims the Fed won’t cut rates in 2023. But that tune can quickly change when the addict starts writing and screaming in pain. And history tells a different story. The Fed’s modus Operandi is to go right back to rate cuts and QE when the economy tanks.

Why should we believe it will be different this time?

Price inflation as measured by CPI has shown some signs of cooling. But a return to loose monetary policy is a return to inflationary policy.

So, the Fed is between a rock and a hard place. It can make the addict suffer a lot of pain and maybe even kill him. Or it can crank up the drugs again.

Neither scenario is particularly good.

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

end

LAWRIE WILLIAMS:

12 Dec 2022

3. Chris Powell of GATA provides to us very important physical commentaries//

Craig Hemke at Sprott Money: Same song, third verse

Submitted by admin on Wed, 2022-12-14 11:38Section: Daily Dispatches

11:35a ET Wednesday, December 14, 2022

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, writing today at Sprott Money, begins to outline his gold forecast for the new year, and he thinks gold’s performance will be like its performance in 2019 and 2010 — something gold owners probably won’t complain about. Hemke’s analysis is headlined “Same Song, Third Verse” and it’s posted at Sprott Money here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

END

Surging inflation is causing investors all over the world to buy Austrian gold coins

(Reuters/GATA)

Inflation, uncertainty fuel new gold rush at ancient Austrian Mint

Submitted by admin on Wed, 2022-12-14 19:33Section: Daily Dispatches

By Francois Murphy Reuters Wednesday, December 14, 2022

VIENNA, Austria — The Austrian Mint, one of the world’s oldest and biggest producers of gold bullion coins, is unable to keep up with demand as people rush to find a safe haven for their money amid surging inflation and economic fears caused by war in Ukraine.

“Demand for gold has never been as high as this year,” the Mint’s Chief Executive Gerhard Starsich, told Reuters in his ornate office in a Vienna building where coins have been struck since the 1830s. Behind its quiet facade lies a warren of workshops where modern machines melt metals and thump out money.

“At the moment, every gold coin that comes off the coining press has already been sold,” Starsich said. “Right now we could sell three times as many as we are able to produce.”

The Mint’s shop, a modern corner of the building, has had a long queue outside daily for months. Among those standing in line was pensioner Renate, one of the few willing to talk about her purchasing habits.

“I’m from an older generation. Whenever things get a bit uncertain, we come back to gold coins and tell ourselves we’ll always be able to sell them,” she said. “Gold has that safety factor.”

Starsich said customers were of all ages and from all walks of life. Around a third of the Mint’s sales are to foreign buyers.

The Mint was founded in 1194 to strike coins from the silver paid as a ransom for Richard the Lionheart, after he had been seized and held captive by enemies near Vienna. …

White House will not say whether Biden will return donations from FTX

(zerohedge)

“I Cannot Speak To This”: White House Won’t Say Whether Biden Will Return Donations From FTX’s Bankman-Fried

THURSDAY, DEC 15, 2022 – 08:50 AM

With Sam Bankman-Fried now officially in custody for allegedly swindling his investors out of “at least $1.8 billion”, questions have begun to swirl about whether or not campaign donations made by the former FTX CEO would be returned to the company, which is now trying to manage a bankruptcy.

In focus over the last few days has been campaign contributions that SBF made for President Biden’s 2020 campaign.

When asked about whether or not the Biden campaign would return 2020 contributions from Bankman-Fried, “White House press secretary Karine Jean-Pierre wouldn’t say Tuesday whether President Biden” would ask aides to return the cash, the NY Post reported.

Associated Press reporter Zeke Miller asked her: “The president received campaign donations [from Bankman-Fried]. Will the president return that donation? Does he call on all politicians … to return those funds?”

“So look, I’m covered here by the Hatch Act — [I’m] limited on what I can say and anything that’s connected to political contributions from here, I would have to refer you to the DNC,” press secretary Karine Jean-Pierre answered.

Miller followed up, stating: “I’m asking the president’s opinion, though.”

But the press secretary continued to dodge the question, stating: “You asked me two questions: You asked me about will he return donations and then you asked me about his opinion. I’m answering the first part, which is I’m covered by the Hatch Act from here. I’m limited on what I can say. And I just can’t talk to political contributions or anything related to that — I cannot speak to that from here.”

“I just cannot speak to this from here, even his thoughts,” she continued. “Even his opinion, even his thoughts about the contributions, donations, I cannot speak about that from here.”

Bankman-Fried is now well known to be one of the Democratic party’s largest donors, and the Post reports that he even had the chance to meet with Biden’s White House advisers prior to the collapse of his firm.

As Fox News notes, SBF sent $262,200 to Republicans throughout the 2021-2022 election cycle – a figure that pales compared to the $40 million he contributed to Democratic campaigns.

end

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS/THURSDAY MORNING.7:30 AM

ONSHORE YUAN: DOWN TO 6.9680

OFFSHORE YUAN: 6.9673

SHANGHAI CLOSED DOWN 7.80 PTS OR 0.25%

HANG SANG CLOSED DOWN 304.88 OR 1.55%

2. Nikkei closed UP 104.51 PTS OR 0.37%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 103.82 Euro FALLS TO 10642 DOWN 33 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.249!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 136.55/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.022%***/Italian 10 Yr bond yield RISES to 4.012%*** /SPAIN 10 YR BOND YIELD RISES TO 3.07…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.94//

3j Gold at $1776.90//silver at: 23.17 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 47/100 roubles/dollar; ROUBLE AT 64.46//

3m oil into the 77 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 136.55 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9282–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9878 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.484% DOWN 2 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.532% DOWN 1 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,65…

GREAT BRITAIN/10 YEAR YIELD: 3.2815%

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

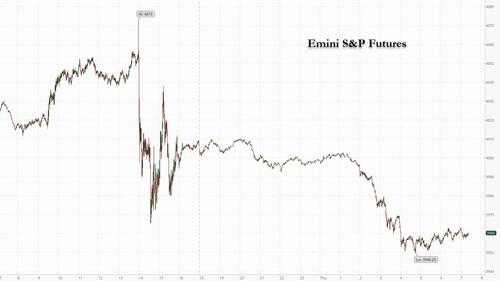

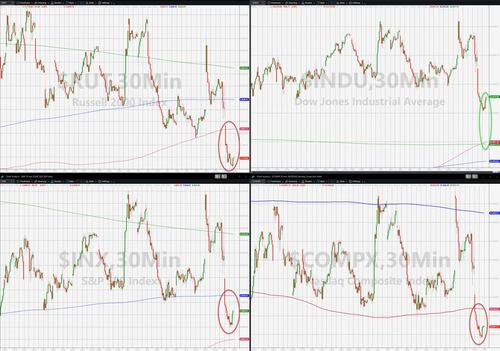

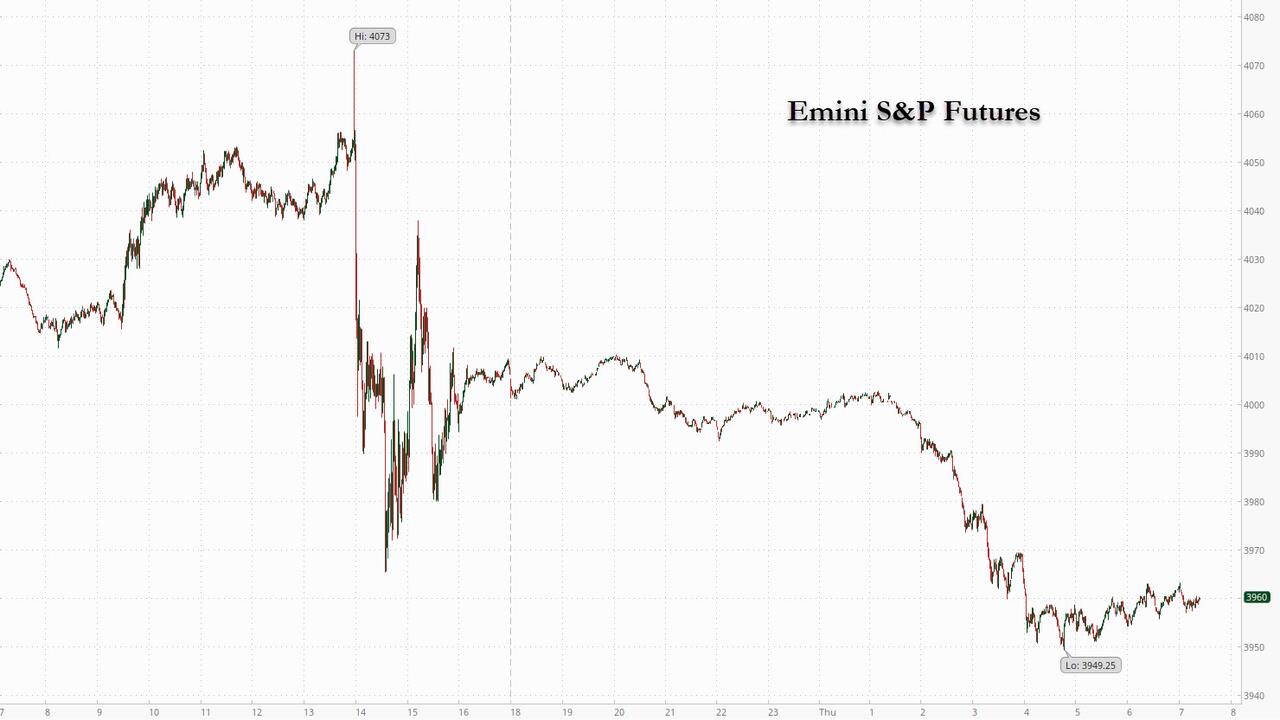

Futures Slide As Hawkish Fed Halts Global Risk Rally

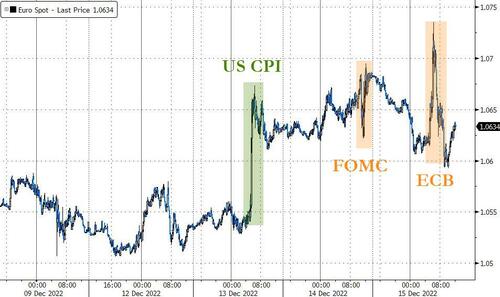

THURSDAY, DEC 15, 2022 – 07:56 AM

US futures extended declines on Thursday following hawkish signs from the Federal Reserve that it would keep rates higher for longer even as it pushed the US economy into a stagflationary recession. Contracts on the technology heavy Nasdaq 100 were down 1.3% by 7:45 a.m. in New York, while S&P 500 futures fell 0.9% after dropping as much as 1.1% earlier. Both underlying indexes dropped yesterday after Fed Chair Jerome Powell delivered a 50-basis-point rate hike, as expected, and said the central bank had more work to do – and will push the terminal rate to 5.1% or higher – in taming inflation despite ebbing price pressures and mounting fears of job losses.

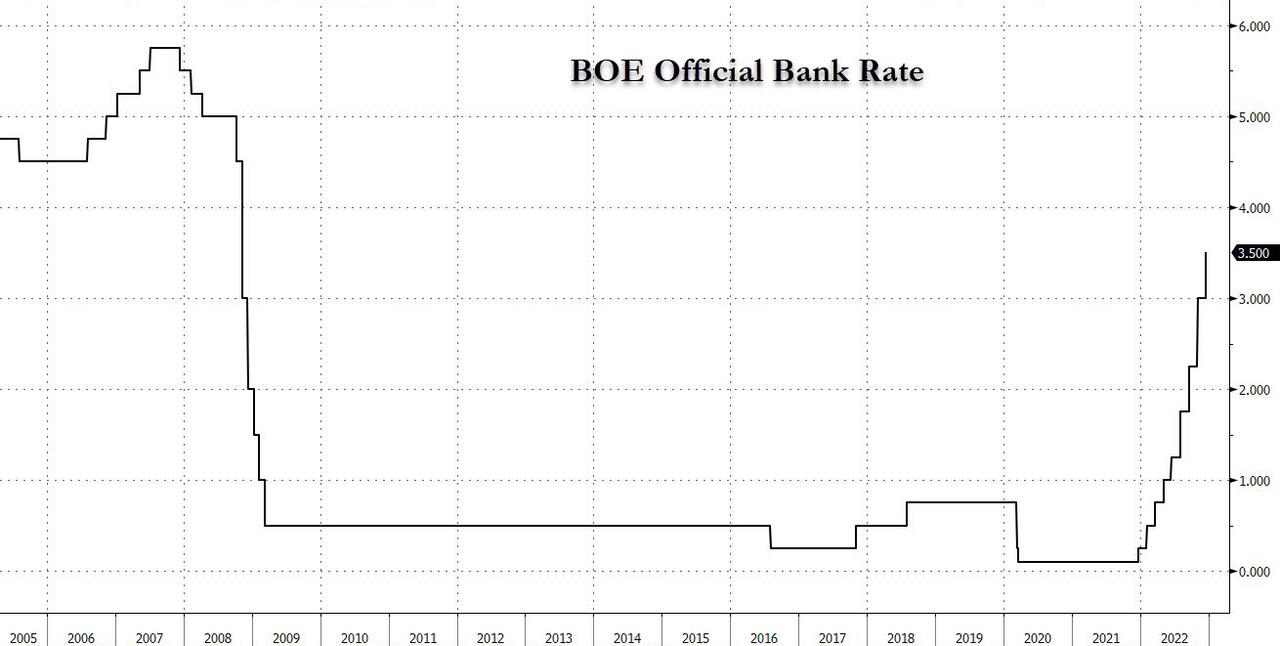

Demand for haven assets sent the dollar and Swiss franc higher amid a wave of rate hikes from Taiwan to Norway. Britain’s pound extended losses after an expected half-point rate hike by the Bank of England, while the euro fell before the European Central Bank’s decision.

A global rally sparked by softer-than-forecast US inflation came to a sudden end on Wednesday after policymakers signaled a peak rate that was far above market expectations and sought to dispel hopes for a rate cut next year. Chair Jerome Powell reaffirmed the central bank won’t back away from its fight against inflation despite mounting fears of job losses and a recession.

“The Fed was more hawkish than markets had expected,” Jack McIntyre, a money manager at Brandywine Global Investment Management, wrote in a note. “They seemingly still want financial markets to tighten further, which essentially means they want lower equity prices.”

Ronald Temple, chief market strategist at Lazard Asset Management, said that although the Fed has started to slow the pace of rate hikes, “that doesn’t mean smooth sailing ahead” for markets. “The effects of the tightening in 2022 will continue to be felt in 2023 through a weaker labor market, recession in Europe and potentially a recession in the US. The earnings hit from a recession is not priced into equity markets,” he said. And while prevailing post-FOMC sentiment among the skeleton crew of traders on Thursday was grim, Paul Kim, chief executive officer at Simplify ETFs, said a “vacuum of catalysts until the next Fed meeting in February” could also help markets continue their rebound over the next few weeks.

The Swiss franc held its gain after the nation’s central bank doubled the policy rate to 1% as forecast. China’s yuan fell as poor economic data and a surge in Covid cases weighed.

In premarket trading Tesla slumped again after CEO Elon Musk sold shares for the fourth time this year. Musk sold almost 22 million shares for $3.58 billion, according to filing late Wednesday. Bitcoin miner Core Scientific surged after one of its largest creditors B. Riley Financial issued an open letter Wednesday laying out a proposal for the company to avoid bankruptcy. Here are some other notable premarket movers:

Novavax shares drop 10% after the biotechnology firm offered $125m of shares and $125m of convertible bonds, and said its agreement to supply Covid vaccines to the UK had been halved.

Verizon stock rises 0.6% as Morgan Stanley upgrades it to overweight and downgrades AT&T (T US) to equal-weight, saying in a note that North American telecom services sector faces a balanced outlook heading into next year.

Keep an eye on Nvidia as it was initiated with a reduce recommendation at HSBC, which says the near-term chip inventory correction and demand uncertainty will overshadow the company’s potential in autos and artificial intelligence segments.

Watch Madison Square Garden Entertainment as Morgan Stanley upgrades the stock to equal-weight based on recent underperformance and proposed spin of traditional live entertainment business.

Defense stocks may be in focus after Morgan Stanley upgraded L3Harris (LHX US) to overweight, downgraded Lockheed Martin to equal-weight and maintained overweight and top pick status on Northrop Grumman (NOC US).

Across the Atlantic, investors were gearing up for another day of central bank meetings with the European Central Bank set to announce its rate decisions later on Thursday. Europe’s equity benchmark, the Stoxx 600, fell the most since Oct. 7 on a closing basis; the Stoxx 50 slumped 1.3%. FTSE 100 outperforms peers, dropping 0.5% ahead of a decision by the ECB which hiked rates by 50bps, to the highest since 2008; the BOE is also on deck. Consumer products, tech and retailers are the worst performing sectors. Here are some of the most notable European movers:

Juventus shares gain as much as 8.1% in Milan to lead gains on the FTSE Italia All-Share Index. Equita notes a report saying that Exor would be thinking of a delisting of the football club, adding that it doesn’t rule out this “could be a viable option.”

Ackermans & van Haaren rises as much as 4.2% after Kepler Cheuvreux analyst Andre Mulder raised the recommendation to buy from hold.

Zotefoams climbs as much as 7.7% after the UK foam-maker said pretax profit for 2022 is likely to come in ahead of market expectations.

European luxury stocks underperform as new economic data from China disappointed and Bryan Garnier cut its price target for Kering on an expected double-digit drop in fourth-quarter sales for key brand Gucci. Kering falls as much as 5.6%, LVMH as much as 2.4%

H&M drops as much as 4.7% after the apparel retailer reported quarterly sales which analysts said were in line with expectations, noting the lack of margin commentary. Focus has shifted to next month’s results, when there’ll be more clarity on margins.

Currys falls as much as 10% to the lowest since Oct. 13 after the UK electronics retailer cut its profit guidance for the year. The stock may see further short-term pressure, according to Liberum, which lowered its price target.

Ceconomy sinks as much as 11%, most since July, after the electronics retailer’s earnings. Analysts flag a vague outlook and potential margin pressure.

Earlier in the session, Asian stocks declined as the Federal Reserve signaled higher interest rates, while a disappointing set of economic data from China soured sentiment. The MSCI Asia Pacific Index dropped as much as 1.4%, led by consumer discretionary and technology shares. Most markets in the region were in the red, with Hong Kong and South Korea among the worst performers. A surprisingly hawkish tone by the Fed after an expected half-point hike fueled risk-off mood across Asia. Chair Jerome Powell said the Fed had a “ways to go” in its campaign to rein in inflation. Policymakers projected rates would end next year at 5.1%, higher than previously indicated.

Chinese benchmarks fell, with Hong Kong’s Hang Seng Index dropping more than 1%, as the nation’s economic activity worsened in November. There will likely be more disruption to growth as infections surge after the government abruptly dropped its Zero-Covid policy. “A broad-based miss in activity data could be attributed to the pre-Zero-Covid relaxation days, but challenges lie ahead as well with full reopening likely to be delayed by a large chunk of workers calling in sick as infections spread,” said Charu Chanana, market strategist at Saxo Capital Markets. The Asian stock benchmark may halt a six-week gaining streak if losses extend into Friday. The region’s shares had rallied since November following China’s Covid pivot and amid hopes of a more dovish Fed — with the latter getting a rude awakening from Wednesday’s meeting.

Japanese stocks followed US shares lower after the Federal Reserve signaled interest rates will climb higher than anticipated next year. The Topix Index fell 0.2% to 1,973.90 as of the market close in Tokyo, while the Nikkei declined 0.4% to 28,051.70. Keyence Corp. contributed the most to the Topix Index decline, decreasing 1.8%. Out of 2,163 stocks in the index, 1,082 rose and 935 fell, while 146 were unchanged. “Although it was hawkish, in a sense the content of the press conference gave the impression of a flexible stance,” said Hitoshi Asaoka, strategist at Asset Management One. “They would look to inflation data rather than just raising interest rates as they have done in the past.”

In FX, Bloomberg dollar spot index rose by as much as 0.7% as the greenback advanced versus all of its Group-of-10 peers. Risk- sensitive Antipodean and Scandinavian currencies were the worst performers.

The euro fell for the first day in three but held above the $1.06 handle. Bunds twist-flattened while Italian bonds bear flattened as money markets added somewhat to ECB peak-rate wagers after the Fed’s policy tightening yesterday

Norway’s krone held losses against the dollar and the euro after Norges Bank raised the deposit rate to 2.75%, in line with estimates, and kept its rate projection steady for next year

The Swiss franc swung to a loss against the dollar after the SNB hiked its interest rate by 50bps, to 1%, matching the median estimate

The pound slid amid broad-based dollar strength. The BOE hiked by the expected half-point; cable was generally flat after the decision.

Australian dollar declined amid poor Chinese data that showed economic activity worsened in November before the government abruptly dropped its Covid Zero policy. Bonds fell after data showed the economy added 64,000 roles, trumping a forecast 19,000 gain

New Zealand’s 10-year yield surged after GDP expanded more than twice as much as expected

Japan’s bonds fell after a 20-year debt auction met tepid investor demand. The yen weakened amid broad strength in the dollar

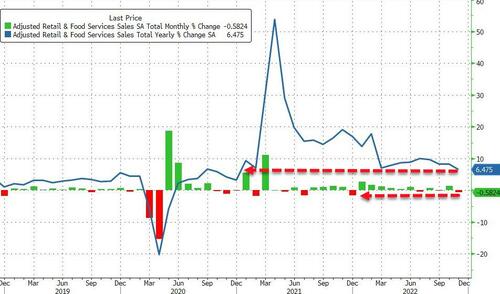

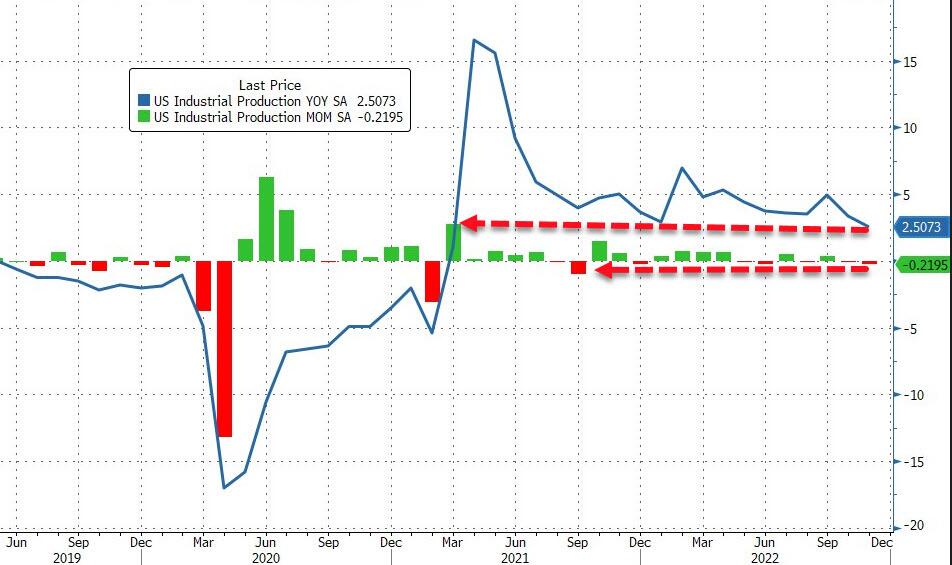

In rates, all 2s10s yield curves flatten as Treasury yields rose, led by the belly, with the exception of the 30-year segment. Bund curve bull flattens with 2s10s narrowing 3.2bps. Peripheral spreads widen to Germany with 10y BTP/Bund adding 3.0bps to 195.2bps. Elsewhere, Bank of England hiked rates 50bp as expected, in a three-way vote. US yields edge lower after Bank of England decision across long- end, following wider gains across gilts where 10-year UK outperforms Treasuries by 6bp on the day; 10-year yields around 3.47%, slightly richer on day on outright basis. Long-end outperformance in US curve sees 2s10s, 5s30s spreads extend flatter by 1.7bp and 2.2bp on the day. Dollar issuance slate remains light, with up to $5b expected for this week; Fed decision day saw a blank slate Wednesday. Packed data slate for the US session includes retail sales and industrial production.

In commodities, oil fluctuated between gains and losses after rallying almost 9% over the previous three sessions as TC Energy restarted a section of the Keystone pipeline, allowing for some flows to resume on the major conduit. Crude futures were steady, having pared a bulk of the Asian losses with the move coming in spite of the downside seen across the equity complex and a firmer USD. WTI trades within Wednesday’s range near $77.21. TC Energy announced it communicated with regulators and customers about the restart of the Keystone pipeline system sections unaffected by the leak but noted that the affected segment remains isolated and will not be restarted until it is safe and they receive approval to do so, according to Reuters. Spot gold falls roughly $29 to trade near $1,778/oz

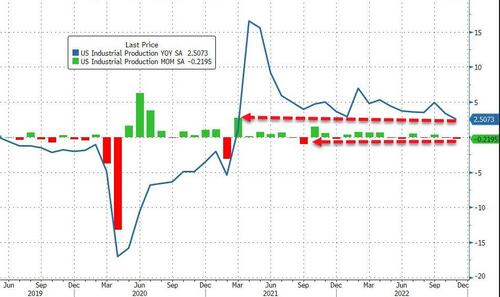

To the day ahead now, and the main highlight will be the monetary policy decisions from the ECB and the Bank of England. There are also a number of US data releases, including November’s retail sales and industrial production, December’s Empire state manufacturing survey and the Philadelphia Fed business outlook, as well as the weekly initial jobless claims. Finally, earnings releases today include Adobe.

Market Snapshot

S&P 500 futures down 1.0% to 3,957.25

STOXX Europe 600 down 1.2% to 437.27

MXAP down 1.6% to 157.70

MXAPJ down 1.6% to 511.73

Nikkei down 0.4% to 28,051.70

Topix down 0.2% to 1,973.90

Hang Seng Index down 1.5% to 19,368.59

Shanghai Composite down 0.2% to 3,168.65

Sensex down 1.3% to 61,888.02

Australia S&P/ASX 200 down 0.6% to 7,204.78

Kospi down 1.6% to 2,360.97

German 10Y yield little changed at 1.94%

Euro down 0.6% to $1.0613

Brent Futures down 0.8% to $82.02/bbl

Brent Futures down 0.8% to $82.06/bbl

Gold spot down 1.5% to $1,780.77

U.S. Dollar Index up 0.53% to 104.32

Top Overnight News from Bloomberg

The ECB is poised to slow the recent pace of interest-rate increases and outline plans to shrink its almost €5 trillion ($5.3 trillion) stash of bonds, broadening efforts to curb inflation that’s still five times the target

UK bond traders seeking shelter from this year’s turmoil are piling into 10-year securities, a section of the market that’s been relatively insulated from central bank action

Nurses have begun a round of historic strikes as Britain faces the prospect of heightened industrial action extending into next year

Almost 1 million people in China may die from Covid-19 as the government rapidly abandons pandemic curbs, according to a new study by researchers in Hong Kong

Expectations for long-term inflation rates in Sweden rose slightly in the latest Prospera survey, after a string of inflation outcomes that show price increases soaring far above the Riksbank’s 2% target

Turkish President Recep Tayyip Erdogan said he wants a three-way meeting with Syria’s Bashar Al-Assad and Russia’s Vladimir Putin, signaling a thaw with Damascus that could help end the war in Syria

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks were subdued in the aftermath of the FOMC. ASX 200 was dragged lower by weakness in nearly all sectors but with losses cushioned by strong jobs data. Nikkei 225 declined but just about remained above the 28K level following strong trade numbers in which the value of both exports and imports reached a record for the month of November. Hang Seng and Shanghai Comp were negative after disappointing Chinese Industrial Production and Retail Sales data, while property and tech stocks were driving the underperformance in Hong Kong after the HKMA raised rates in lockstep with the Fed, while attention was also on the PBoC which conducted a CNY 650bln 1-Year MLF operation vs. CNY 500bln maturing but maintained the rate at 2.75%.

Top Asian News

PBoC conducted CNY 650bln of 1-year MLF vs. CNY 500bln maturing with the rate kept at 2.75%.

HKMA raised its base rate by 50bps to 4.75%, as expected, following the Fed rate hike, while Macau’s Monetary Authority raised its base rate for the discount window by 50bps to 4.75%.

China’s stats bureau said China’s economy maintained its recovery trend in November despite multiple pressures but added that the foundation of the economic recovery is still not solid, according to Reuters.

US Senate passes bill to ban federal employees from using TikTok on government devices.

European bourses and US futures under pressure, seemingly in a second wave of the post-FOMC price action after action stabilised a touch overnight. Currently, Euro Stoxx 50 -1.3% and ES -1.0%, with non-Central Bank updates relatively thin ahead of key US data and more Policy Announcements. Foxconn (2317 TT) has ended most closed-loop restrictions in ‘iPhone city’ ( Zhengzhou) , via Bloomberg.

Top European News

UK PM Sunak eyes anti-strike laws which he vows would protect lives and livelihoods, according to Daily Mail.

European Gas Prices Rise With Focus on Cold Snap and LNG Supply

Norway Raises Key Rate and Signals It’s Nearing a Peak

Kering Leads European Luxury Lower on Disappointing China Data

Rebel European Soccer League Gets Setback in EU Court Opinion

VW Sees Growing Challenges Next Year on Inflation, Downturn

Hungary Says May Need to Amend Gazprom Contract on EU Price Cap

Central Banks

Swiss SNB Policy Rate (Q4) 1.00% vs. Exp. 1.00% (Prev. 0.50%); cannot be ruled out that further hikes will be necessary. Willing to intervene in FX as necessary. Inflation forecasts cut, implying Switzerland is at the peak level. Click here for full details & analysis.

SNB’s Jordan (press conference) says we have sold foreign currency in recent months to ensure appropriate monetary conditions. Willing to buy/sell foreign currency as necessary.

Norges Bank Policy Announcement (Dec): 2.75% vs. Exp. 2.75% (Prev. 2.50%); policy rate will most likely be raised further in Q1 2023. Inflation forecasts lifted, Repo Path forecasts tweaked but little changed, implying another 25bp move with some optionality for further tightening, if needed. Click here for full details & analysis.

FX

USD has continued to climb throughout the morning, DXY above 104.40 at best.

Action which has weighed on peers across the board, with EUR/USD and Cable testing 1.06 and 1.23 to the downside ahead of ECB & BoE.

Antipodeans are at the bottom of the G10 pile irrespective of upbeat macro news.

NOK undermined post-Norges Bank despite initial fleeting upside as the Bank guides towards further tightening, despite the domestic headwind.

CHF similarly dented in a ‘buy the rumour, sell the fact’ style following the as-expected SNB and as the inflation forecasts show the economy at the peak, perhaps limited the need for further tightening.

PBoC set USD/CNY mid-point at 6.9343 vs exp. 6.9325 (prev. 6.9535)

Fixed Income

Gilts continue to outperform and lead the complex’s revival, with Bunds and USTs lifting in turn though are comparably more contained and yet to make any real foray into positive territory.

USTs appear to be guided by the risk tone and ongoing curve flattening post-Fed, with Central Bank activity since essentially in-line with expectations.

Commodities

Crude benchmarks are flat, having pared a bulk of the APAC losses with the move coming in spite of the downside seen across the equity complex and a firmer USD.

TC Energy announced it communicated with regulators and customers about the restart of the Keystone pipeline system sections unaffected by the leak but noted that the affected segment remains isolated and will not be restarted until it is safe and they receive approval to do so, according to Reuters.

Canada said it decided to revoke the time-limited Nord Stream sanctions waiver that was granted to allow turbines to be repaired in Montreal for return to Germany with the decision made working closely with Ukrainian, German and other European allies, according to Reuters.

Spot gold and silver are unable to benefit from any traditional haven allure as the USD continues to ramp up; pressure in the yellow metal has brought it below the 10- & 200-DMAs to a test of the 21-DMA, at USD 1788/oz. 1787/oz and 1771/oz respectively.

Geopolitics

US is planning to send Ukraine advanced electronic equipment that converts unguided aerial munitions into “smart bombs”, according to officials cited by Washington Post.

US defence firms are in talks with Vietnam to sell helicopters and drones, while military deals with the US would signal a shift away from Vietnam’s reliance on Russia, according to Reuters.

Russia’s Washington embassy has warned that a transfer of the Patriot System to Ukraine would result in “unpredictable consequences”, via Walla News’ Elster.

US Event Calendar

08:30: Nov. Retail Sales Advance MoM, est. -0.2%, prior 1.3%

Nov. Retail Sales Ex Auto and Gas, est. 0%, prior 0.9%

Nov. Retail Sales Ex Auto MoM, est. 0.1%, prior 1.3%

Nov. Retail Sales Control Group, est. 0.1%, prior 0.7%

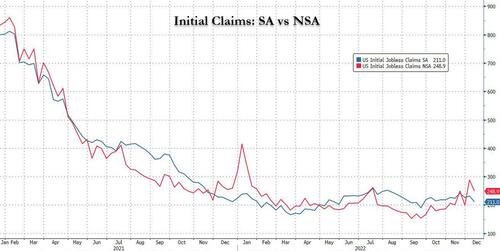

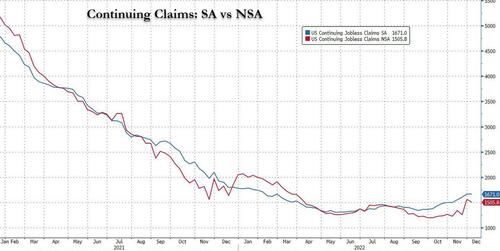

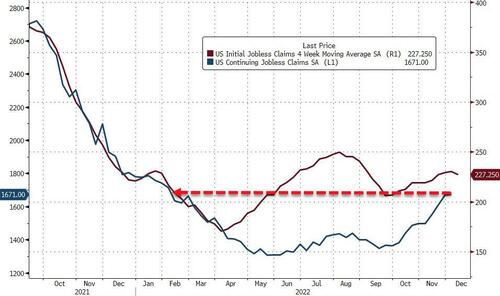

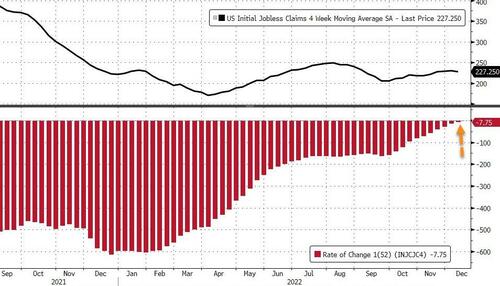

08:30: Dec. Initial Jobless Claims, est. 232,000, prior 230,000

Dec. Continuing Claims, est. 1.67m, prior 1.67m

08:30: Dec. Empire Manufacturing, est. -1.0, prior 4.5

08:30: Dec. Philadelphia Fed Business Outl, est. -10.0, prior -19.4

09:15: Nov. Industrial Production MoM, est. 0%, prior -0.1%

Nov. Capacity Utilization, est. 79.8%, prior 79.9%

Nov. Manufacturing (SIC) Production, est. -0.2%, prior 0.1%

10:00: Oct. Business Inventories, est. 0.4%, prior 0.4%

16:00: Oct. Total Net TIC Flows, prior $30.9b

Oct. Net Foreign Security Purchases, prior $118b

DB’s Jim Reid concludes the overnight wrap

If you wanted to briefly sum up the FOMC meeting last night you would probably say that the Fed were hawkish but that the market doesn’t believe they will be. Going through the details (our full US econ review, here), they did hike +50bps as expected, downshifting from four successive +75bps hikes. This brings the upper bound of the fed funds target range to 4.5%, around 360bps above where the markets thought it would be at this point last December. Last night’s meeting also brought a fresh round of projections from the Committee, where the median participant projected policy rates to rise to 5.1% by the end of next year, with core PCE expected to be 3.5%, still plenty above target. The distribution of dots was hawkish as well, as only 2 out of 19 participants pencilled in a policy rate below 5% by the end of 2023, so a strong rebuke to any investors expecting Fed cuts next year.

Indeed, that proved to be a key tenet of the press conference as well. After two optimistic CPI reports, Chair Powell tried to talk financial conditions back from getting too optimistic and easy, saying that even with today’s hikes the Fed still had a “ways to go” to make sure the fight against inflation was well and truly won. Much like the November FOMC, the Chair noted that the step down to smaller hiking increments makes sense as the Committee approaches terminal, and that the pace of rate increases was not nearly as important as the ultimate level of terminal or time spent there, pointing to the dots showing policy above 5% in a year’s time. In that vein, he also opened up the door for a 25bp hike at the Fed’s next meeting in February which may have helped markets reverse some of the immediate sell-off. Powell did note that core goods and housing services inflation was rolling over, in line with the Fed’s expectations, but that core services would remain above target so long as the labour market remained historically tight, as wages are a larger cost input in those sectors.

Markets sold off a touch in the hour following the hawkish dots and communications from the Chair, but the strong messaging was already anticipated by many following the last two CPI prints, as the Fed tries to avoid yet another counterproductive pricing pivot. Therefore, the net price action following the meeting was relatively modest, albeit with a decent sized range in the aftermath. 2yr Treasury yields ended the day -0.9bps lower having been -4.9bps lower heading into the meeting but +10bps 35mins after the decision. Meanwhile 10yr yields were -2.4bps lower after being roughly flat heading into the meeting, and c.+5bps 10 mins after the decision. The terminal rate priced for May increased a modest +1.2bps to 4.87%, still well below the Fed’s own projection of terminal. So something will have to give in the first few weeks of 2023. This morning in Asia, yields on 10yr USTs (+1.82 bps) have moved upwards, trading at 3.50%.

The S&P 500 was +0.71% higher immediately before the meeting but ended -0.61% lower after bouncing around between gains and losses throughout the press conference. So it seems the equity market took the hawkish bias more to heart than fixed income markets.

Asian equity markets are trading in negative territory this morning following the overnight negative lead from Wall Street. The KOSPI (-1.21%) and Hang Seng (-1.14%) are the biggest underperformers while the Nikkei (-0.33%), the Shanghai Composite (-0.28%) and the CSI (-0.23%) are also sliding in early trading. In overnight trading, US stock futures are rangebound with contracts on the S&P 500 (-0.01%) just below flat and the NASDAQ 100 (-0.11%) trading slightly lower.

The big news overnight was data from China showing the toll that widespread Covid restrictions took on growth last month before the government announced that it would ease its policy. Industrial production slowed to +2.2% y/y (v/s +3.5% expected) in November from the +5.0% rise recorded in October. This marked the slowest growth since May when Shanghai was put under a two-month lockdown. At the same time, retail sales (-5.9% y/y) had their biggest contraction since May, underperforming expectations for a decline of -4.0% and greater than a -0.5% drop recorded in October.

Other economic data showed that Australia’s unemployment rate for November remained at 3.4%, in line with market expectations.

Elsewhere in Asia, the Japanese Yen was pretty flat against the USD yesterday even following a Bloomberg report that officials at the Bank of Japan were considering a policy review next year. Historically, reviews have led to policy changes, so it’ll be interesting to see if this ends up happening and whether that might mark a shift away from the ultra-loose monetary policy of recent years, which has increasingly made the BoJ an outlier internationally. Japan reported that exports rose +20.0% y/y in November (v/s +19.7% expected) compared to an increase of +25.3% in October and were outpaced by imports (up +30.3%). The trade deficit swelled more than expected to -2.03 trillion yen in November versus a revised shortfall of -2.17 trillion yen in October. This morning the Yen (+0.13%) is slightly higher, trading at $135.65.

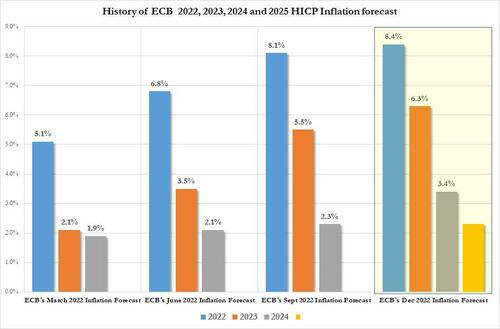

Now that the Fed is out of the way, attention will turn to central banks in Europe today, with the ECB’s decision coming up at 13:15 London time. As with the Fed yesterday, it’s widely expected that the ECB will shift away from the 75bp hikes at the last couple of meetings in favour of a 50bp move today, which would take the deposit rate up to 2%. But even as they slow down their hikes, Mark Wall and our European economists write in their preview (link here) that they’ll maintain a hawkish communications strategy, since the ECB doesn’t want the market to interpret smaller hikes as meaning a lower terminal rate or earlier rate cuts. This hawkishness is likely to come through a number of channels, including upwardly revised staff inflation forecasts, which our economists expect will show stronger inflation in 2023 and 2024 relative to September.

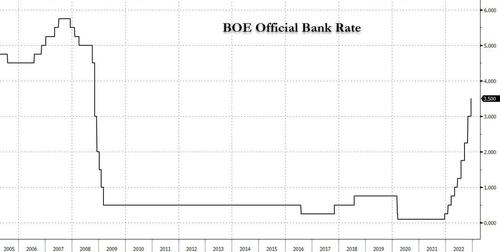

If the ECB wasn’t enough, today will also bring the Bank of England’s decision just over an hour beforehand at 12:00 London time. In terms of what to expect, investors and economists are widely anticipating that the BoE will echo the pattern elsewhere and slow their hikes from 75bps last time to 50bps today. That would take the Bank Rate up to 3.5%, but unlike the ECB, our UK economist expects the MPC to strike another dovish tone this month, and sound more cautious around the risks of over-tightening. The decision today also follows the latest CPI data for November yesterday, which fell back by more than expected to +10.7% (vs. +10.9% expected). See our economist’s full preview here.

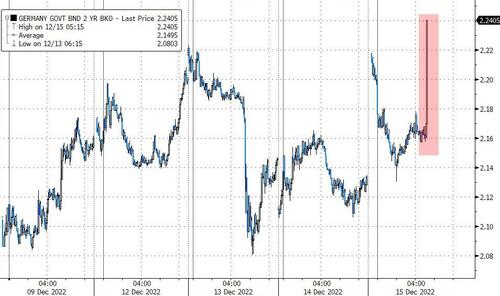

With all that to look forward to, European markets put in a pretty subdued performance yesterday, having closed ahead of the Fed decision. The main equity indices all lost modest ground, with the STOXX 600 (-0.02%), the DAX (-0.26%) and the FTSE 100 (-0.09%) posting declines. And for sovereign bonds it was a similar story, with yields on 10yr bunds (+1.7bps), OATs (+3.1bps) and BTPs (+6.7bps) all moving higher on the day. That said, some of the moves at the front-end were more positive, with the German 2yr yield actually falling -0.9bps on the day.

To the day ahead now, and the main highlight will be the monetary policy decisions from the ECB and the Bank of England. There are also a number of US data releases, including November’s retail sales and industrial production, December’s Empire state manufacturing survey and the Philadelphia Fed business outlook, as well as the weekly initial jobless claims. Finally, earnings releases today include Adobe.

AND NOW NEWSQUAWK (EUROPE/REPORT)

Post-FOMC action continues, SNB & Norges Bank in-line; BoE, ECB & US data ahead – Newsquawk US Market Open

THURSDAY, DEC 15, 2022 – 06:32 AM

European bourses and US futures are under pressure, seemingly in a second wave of the post-FOMC price action.

USD has continued to climb throughout the morning, DXY above 104.40 at best with peers dented across the board

SNB & Norges Bank were essentially in-line with expectations, hiking by 50bp & 25bp respectively.

Gilts continue to outperform and leading a relative ‘revival’ in the debt space, though USTs and Bunds are yet to make any real ground above neutral

Crude benchmarks are flat, having pared a bulk of the APAC losses with the move coming in spite of the above action

Looking ahead, highlights include US IJC, Retail Sales & Industrial Production, BoE, ECB, Banxico Policy Announcements, European Council Meeting (1/2), Press Conference from ECB’s Lagarde.

Or why not try Newsquawk’s squawk box free for 7 days?

EUROPEAN TRADE

CENTRAL BANKS

Swiss SNB Policy Rate (Q4) 1.00% vs. Exp. 1.00% (Prev. 0.50%); cannot be ruled out that further hikes will be necessary. Willing to intervene in FX as necessary. Inflation forecasts cut, implying Switzerland is at the peak level. Click here for full details & analysis.

SNB’s Jordan (press conference) says we have sold foreign currency in recent months to ensure appropriate monetary conditions. Willing to buy/sell foreign currency as necessary.

Norges Bank Policy Announcement (Dec): 2.75% vs. Exp. 2.75% (Prev. 2.50%); policy rate will most likely be raised further in Q1 2023. Inflation forecasts lifted, Repo Path forecasts tweaked but little changed, implying another 25bp move with some optionality for further tightening, if needed. Click here for full details & analysis.

EQUITIES

European bourses and US futures under pressure, seemingly in a second wave of the post-FOMC price action after action stabilised a touch overnight.

Currently, Euro Stoxx 50 -1.3% and ES -1.0%, with non-Central Bank updates relatively thin ahead of key US data and more Policy Announcements.

Foxconn (2317 TT) has ended most closed-loop restrictions in ‘iPhone city’ ( Zhengzhou) , via Bloomberg.

USD has continued to climb throughout the morning, DXY above 104.40 at best.

Action which has weighed on peers across the board, with EUR/USD and Cable testing 1.06 and 1.23 to the downside ahead of ECB & BoE.

Antipodeans are at the bottom of the G10 pile irrespective of upbeat macro news.

NOK undermined post-Norges Bank despite initial fleeting upside as the Bank guides towards further tightening, despite the domestic headwind.

CHF similarly dented in a ‘buy the rumour, sell the fact’ style following the as-expected SNB and as the inflation forecasts show the economy at the peak, perhaps limited the need for further tightening.

PBoC set USD/CNY mid-point at 6.9343 vs exp. 6.9325 (prev. 6.9535)

Gilts continue to outperform and lead the complex’s revival, with Bunds and USTs lifting in turn though are comparably more contained and yet to make any real foray into positive territory.

USTs appear to be guided by the risk tone and ongoing curve flattening post-Fed, with Central Bank activity since essentially in-line with expectations.

Crude benchmarks are flat, having pared a bulk of the APAC losses with the move coming in spite of the downside seen across the equity complex and a firmer USD.

TC Energy announced it communicated with regulators and customers about the restart of the Keystone pipeline system sections unaffected by the leak but noted that the affected segment remains isolated and will not be restarted until it is safe and they receive approval to do so, according to Reuters.

Canada said it decided to revoke the time-limited Nord Stream sanctions waiver that was granted to allow turbines to be repaired in Montreal for return to Germany with the decision made working closely with Ukrainian, German and other European allies, according to Reuters.

Spot gold and silver are unable to benefit from any traditional haven allure as the USD continues to ramp up; pressure in the yellow metal has brought it below the 10- & 200-DMAs to a test of the 21-DMA, at USD 1788/oz. 1787/oz and 1771/oz respectively.

US is planning to send Ukraine advanced electronic equipment that converts unguided aerial munitions into “smart bombs”, according to officials cited by Washington Post.

US defence firms are in talks with Vietnam to sell helicopters and drones, while military deals with the US would signal a shift away from Vietnam’s reliance on Russia, according to Reuters.

Russia’s Washington embassy has warned that a transfer of the Patriot System to Ukraine would result in “unpredictable consequences”, via Walla News’ Elster.

APAC TRADE

EQUITIES

APAC stocks were subdued in the aftermath of the FOMC.

ASX 200 was dragged lower by weakness in nearly all sectors but with losses cushioned by strong jobs data.

Nikkei 225 declined but just about remained above the 28K level following strong trade numbers in which the value of both exports and imports reached a record for the month of November.

Hang Seng and Shanghai Comp were negative after disappointing Chinese Industrial Production and Retail Sales data, while property and tech stocks were driving the underperformance in Hong Kong after the HKMA raised rates in lockstep with the Fed, while attention was also on the PBoC which conducted a CNY 650bln 1-Year MLF operation vs. CNY 500bln maturing but maintained the rate at 2.75%.

NOTABLE ASIA-PAC HEADLINES

PBoC conducted CNY 650bln of 1-year MLF vs. CNY 500bln maturing with the rate kept at 2.75%.

HKMA raised its base rate by 50bps to 4.75%, as expected, following the Fed rate hike, while Macau’s Monetary Authority raised its base rate for the discount window by 50bps to 4.75%.

China’s stats bureau said China’s economy maintained its recovery trend in November despite multiple pressures but added that the foundation of the economic recovery is still not solid, according to Reuters.

US Senate passes bill to ban federal employees from using TikTok on government devices.

DATA RECAP

Chinese Industrial Output YY (Nov) 2.2% vs. Exp. 3.6% (Prev. 5.0%); Retail Sales YY (Nov) -5.9% vs. Exp. -3.7% (Prev. -0.5%)

Chinese Urban Investment (YTD)YY (Nov) 5.3% vs. Exp. 5.6% (Prev. 5.8%); House Prices YY (Nov) -1.6% (Prev. -1.6%)