GOLD PRICE CLOSE: UP $12.45 at $1790.65

SILVER PRICE CLOSE: UP 2 CENTS to $23.13

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1793.45

Silver ACCESS CLOSE: 23.22

Bitcoin morning price:, 17,016 DOWN 433 DOLLARS

Bitcoin: afternoon price: $17,019 DOWN 430 dollars

Platinum price closing $996.05 DOWN $11.45

Palladium price; closing 1728.80 DOWN $17.20

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2455.43 UP $29.56 CDN dollars per oz

BRITISH GOLD: 1474.65 UP 17.38 pounds per oz

EURO GOLD: 1693.93 UP 24.06 euros per oz

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: DECEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,777.200000000 USD

INTENT DATE: 12/15/2022 DELIVERY DATE: 12/19/2022

FIRM ORG FIRM NAME ISSUED STOPPED

104 C MIZUHO 1

132 C SG AMERICAS 1

190 H BMO CAPITAL 304

435 H SCOTIA CAPITAL 30

624 H BOFA SECURITIES 93

661 C JP MORGAN 255

800 C MAREX SPEC 17

880 C CITIGROUP 1

TOTAL: 351 351

MONTH TO DATE: 20,092

COMEX//NOTICES FILED re JPMorgan 253/351

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR DEC. CONTRACT: 351 NOTICES FOR 35,100 OZ or 1.0917 TONNES

total notices so far: 20,092 contracts for 2,009,200 oz (62.494 tonnes)

SILVER NOTICES: 1 NOTICE(S) FILED FOR 5,000 OZ/

total number of notices filed so far this month 3565 for 17,825,000 oz

END

GLD

WITH GOLD UP $12.45

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////HUGE CHANGES IN GLD INVENTORY:A DEPOSIT 2.32 TONNES TONNES OUT IF THE GLD

INVENTORY RESTS AT 913.88 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 2 CENTS

AT THE SLV// :/HUGE CHANGES IN SILVER INVENTORY AT THE SLV THESE PAST 3 WEEKS! A LOSS OF 1.85 MILLION OZ FROM THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 508.15 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 2344 CONTRACTS TO 123,124 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR HUGE $0.74 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR SHORTERS/HFT WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.74 AND WERE SUCCESSFUL IN KNOCKING CONSIDERABLE SPEC LONGS, AS WE HAD AN HUGE SIZED LOSS IN OUR TWO EXCHANGES OF 1591 CONTRACTS. AS WELL WE HAD EXCHANGE FOR RISK TRANSFER OF 0 CONTRACTS. WE HAD VERY LITTLE SPEC SHORT COVERINGS OF THEIR SHORTFALL. .WE PROBABLY HAD HUGE SHORT ADDITIONS WITH THE HUGE PRICE FALL OF THE SILVER. // OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. BUT THEY ALSO SUPPLIED THE NECESSARY SHORT CONTRACTS>>> SOME INCREASE OF NEWBIE SPEC LONGS ADDING TO THEIR POSITIONS CAUSING ADDITIONAL MISERY TO OUR SHORTERS.

WE MUST HAVE HAD:

A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 23 .24. MILLION OZ FOLLOWED BY TODAY;S E.F.P. JUMP TO LONDON of 110,000 OZ // V) GIGANTIC SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL —148

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS DEC. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF DEC:

TOTAL CONTRACTS for 14 days, total 7454 contracts: OR 37.27 MILLION OZ PER DAY. (532 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 37,27 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 37.27 MILLION OZ INITIAL( VERY SMALL)

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2344 WITH OUR $0.74 LOSS IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 605 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 23.24 MILLION OZ FOLLOWED BY TODAY:S 110,000 E,F,P. JUMP //NEW STANDING 23.480 MILLION OZ + EFR = 33.870 MILLION OZ. .. WE HAVE AN HUGE SIZED LOSS OF 1591 OI CONTRACTS ON THE TWO EXCHANGES FOR 8.695 MILLION OZ.. THE SILVER SHORTS ARE NOW TRAPPED AS THEY ARE HAVING CONSIDERABLE DIFFICULTY IN COVERING THOSE SHORTS.

WE HAD 1 NOTICE(S) FILED TODAY FOR 5,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A VERY STRONG SIZED 10,210 CONTRACTS TO 426,124 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: added 101 CONTRACTS.

.

THE HUGE SIZED DECREASE IN COMEX OI CAME WITH OUR STRONG LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR DEC. AT 58.86 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY:S HUGE QUEUE JUMP of 169 contracts or 16,900 oz//(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). NEW STANDING 62.659 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS PRICE OF $29.20 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A STRONG SIZED LOSS OF 7199 OI CONTRACTS (22.39 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3011 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 426,023

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7199 CONTRACTS WITH 10,210 CONTRACTS DECREASED AT THE COMEX AND 3011 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 7199 CONTRACTS OR 22.39 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3011 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (10,210) TOTAL LOSS IN THE TWO EXCHANGES 7199 CONTRACTS. WE NO DOUBT HAD 1) ZERO SPECULATOR SHORT COVERINGS // CONTINUED GOOD BANKER ADDITIONS BUT THEY ALSO SUPPLIED THE NECESSARY PAPER SHORT. WE HAD HUGE SHORT SPEC ADDITIONS/// // SMALL NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR DEC. AT 58.86 TONNES FOLLOWED BY TODAY’S QUEUE JUMP of 16900 oz// //NEW STANDING 63.676 TONNES///3) CONSIDERABLE LONG LIQUIDATION //.,4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

DEC

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC :

32,397 CONTRACTS OR 3,239,700 OZ OR 100.76 TONNES 14 TRADING DAY(S) AND THUS AVERAGING: 2314 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAY(S) IN TONNES:100.76 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 100.76/3550 x 100% TONNES 2.84% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 100.74 tonnes Initial//VERY SMALL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GIGANTIC SIZED 2344 CONTRACTS OI TO 123,733 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 605 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 605 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 605 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF2344 CONTRACTS AND ADD TO THE 605 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN HUGE SIZED LOSS OF 1739 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 8.695 MILLION OZ//

OCCURRED WITH OUR LOSS IN PRICE OF $0.74….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED DOWN 0.79 PTS OR 0,02% //Hang Sang CLOSED UP 82.08 OR 0.42% /The Nikkei closed DOWN 524.58 OR 1.87% //Australia’s all ordinaries CLOSED DOWN 0.73% /Chinese yuan (ONSHORE) closed DOWN TO 6.98721//OFFSHORE CHINESE YUAN DOWN TO 6.9813// /Oil DOWN TO 74,47 dollars per barrel for WTI and BRENT AT 79.54 / Stocks in Europe OPENED ALL RED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A VERY STRONG SIZED 10,210 CONTRACTS DOWN TO 426,124 WITH OUR THE HUGE LOSS IN PRICE..$29.20

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE -ACTIVE DELIVERY MONTH OF DEC… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3011 EFP CONTRACTS WERE ISSUED: ;: , . 0 FEB: 3011 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE:3011 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 7199 CONTRACTS IN THAT 3011 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 10,210 CONTRACTS..AND THIS STRONG SIZED LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF GOLD $29.20. WE ARE WITNESSING HUGE SPEC SHORTS ADDITIONS TO THEIR SHORTFALL. BANKERS CONTINUE AS NET BUYERS OF COMEX GOLD CONTRACTS AS THEY HAVE BEEN NET LONG FOR THE PAST FEW MONTHS. WE ALSO HAD SOME NEWBIE SPECS ADDITIONS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING DEC (63.626)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL (TOTAL SO FAR THIS YEAR 591.535 TONNES)

Dec. 63.626 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $29.20) //// ( AND WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD A STRONG LOSS OF 7199 CONTRACTS ON OUR TWO EXCHANGES >. WE HAD HUGE NUMBER OF NEW SPEC SHORT ADDITIONS AND NEGLIGIBLE SPEC SHORT COVERINGS.. // WE HAVE LOST A TOTAL OI OF 22.706 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR DEC. (54.57 TONNES), following our queue jump of 16900 oz//new standing 63.626 tonnes…THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE OF $29.20

WE HAD +101 CONTRACTS COMEX TRADES REMOVED FROM OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 7199 CONTRACTS OR 719,900 OZ OR 22.39 TONNES

Estimated gold volume 124,652// poor//

final gold volumes/yesterday 191,821/ poor

INITIAL STANDINGS FOR DECEMBER 2022 COMEX GOLD //DEC 16

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil oz . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 449 notice(s) 44,900 OZ 2.9519 TONNES |

| No of oz to be served (notices) | 384 contracts 38,400 oz 1.1944 TONNES |

| Total monthly oz gold served (contracts) so far this month | 20,072 notices 2,007,200 62.494 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

customer withdrawals: 9

Total withdrawals: nil oz

total in tonnes: .0 tonnes

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR DECEMBER.

For the front month of DECEMBER we have an oi of 735 contracts having LOST 618 contracts

We had 449 contracts served on Thursday, so we gained A STRONG 169 contracts or an additional 16,900 oz will stand for gold at the COMEX. We will gain in gold tonnage from this day forth.

The comex is running out of physical gold to serve our good friends over in London

JANUARY LOST 76 contracts to stand at 1222

February LOST 9018 contacts to 362,509

We had 351 notice(s) filed today for 35,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 351 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 255 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the DEC. /2022. contract month,

we take the total number of notices filed so far for the month (20,092 x 100 oz , to which we add the difference between the open interest for the front month of (DEC. 735 CONTRACTS) minus the number of notices served upon today 351 x 100 oz per contract equals 2,045,600 OZ OR 63.626 TONNES the number of TONNES standing in this active month of DEC.

thus the INITIAL standings for gold for the DEC contract month:

No of notices filed so far (20,092 x 100 oz+ (735 OI for the front month minus the number of notices served upon today (351} x 100 oz} which equals 2,045,600 oz standing OR 63.626 TONNES in this active delivery month of DEC..

TOTAL COMEX GOLD STANDING: 63.626 TONNES (A POOR STANDING//COMEX RUNNING OUT OF PHYSICAL TO SERVE UPON OUR LONGS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

we had one adjustment of 110,631.591 oz Brinks

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,091,091.771 OZ 65.04 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 23,296,383.403 OZ

TOTAL REGISTERED GOLD: 11,715,470.652 OZ (364.40 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 11,580,913.351 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,624,379 OZ (REG GOLD- PLEDGED GOLD) 299.35 tonnes//rapidly declining

END

SILVER/COMEX

DEC 16//INITIAL DEC. SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,313,296.020 oz Brinks Loomis JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,175,126.942 oz Brinks Delaware |

| No of oz served today (contracts) | 1 CONTRACT(S) (5,000 OZ) |

| No of oz to be served (notices) | 1109 contracts (5,545,000 oz) |

| Total monthly oz silver served (contracts) | 3565 contracts (17,850,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i) Into Delaware 569,755.202 oz

ii) into Brinks: 605,371.720 oz

Total deposits: 1,175,126.942 oz

JPMorgan has a total silver weight: 149.686 million oz/297.847 million =50.26% of comex .//dropping fast

Comex withdrawals:3

i) Out of Brinks 83,924.34 oz

i) Out of Loomis: 197,406.460 oz

ii) Out of JPMorgan: 1031,965.220 oz

Total withdrawals; 1,313,296.020 oz

adjustments: 2

dealer to customer: Brinks 10,051.680 oz

and

Manfra: 9795.400 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 33,672 MILLION OZ (declining rapidly).TOTAL REG + ELIG. 297.847MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF DEC OI: 1110 CONTRACTS HAVING LOST 38 CONTRACT(S.)

WE HAD 16 NOTICES FILED ON THURSDAY. SO WE LOST 22 CONTRACTS OR 110,000 oz

AS AN EFP JUMP TO LONDON

JANUARY SAW A LOSS OF 31 CONTRACTS LOWERING TO 1582 CONTACTS.

FEB> GAINED 4 CONTRACTS TO 114 CONTRACTS

March LOST 2370 contracts DOWN to 108,447 contracts

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 16 for 80,000 oz

Comex volumes// est. volume today 48,474// fair

Comex volume: confirmed yesterday: 64,120 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in DEC. we take the total number of notices filed for the month so far at 3565 x 5,000 oz = 17,825,000 oz

to which we add the difference between the open interest for the front month of DEC(1110) and the number of notices served upon today 1 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the DEC./2022 contract month: 3565 (notices served so far) x 5000 oz + OI for front month of DEC (1110 – number of notices served upon today (1) x 500 oz of silver standing for the DEC. contract month equates 23.370 million oz.. Also we have another criminal element to our silver oz standing, the use of Exchange for Risk/ Today an addition of 0 EFR contract transfers which are “Exchange for risk” settlements. I do not want to bore you but needless to say they are not physical transfers so are criminal in nature. There have been 2100 Exchange for Risk contracts settled these past 8 days for 10.500 million oz. Thus total delivery: 33.870 million oz.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:37,982// est. volume today// poor

Comex volume: confirmed yesterday: 77,222 contracts ( good)

END

GLD AND SLV INVENTORY LEVELS

DEC 16/WITH GOLD UP $12.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 15//WITH GOLD DOWN $31.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 911.56 TONNES

DEC 14/WITH GOLD DOWN $6.20: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 912.72 TONNES

DEC 13/WITH GOLD UP $32.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD///INVENTORY RESTS AT 910.41

DEC 12/WITH GOLD DOWN $17.60: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

DEC 9/WITH GOLD UP $8.90//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

Dec 8/WITH GOLD UP $4.05, OVER THE PAST 3 WEEKS WE LOST 2.04 TONNES//INVENTORY RESTS AT 908.09 TONNES

NOV 14/WITH GOLD UP $7.30: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 910.12 TONNES

NOV 11/WITH GOLD UP $15.25//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD////INVENTORY RESTS AT 911.57 TONNES

NOV 10/WITH GOLD UP $40.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.38 TONNES

NOV 9/WITH GOLD DOWN $2.00: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES INTO THE GLD////INVENTORY RESTS AT 908.38 TONNES

NOV 8/WITH GOLD UP $34.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.47 TONNES FROM THE GLD//: INVENTORY RESTS AT 905.49 TONNES

NOV 7/WITH GOLD UP $2.95: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.63 TONNES FROM THE GLD//INVENTORY RESTS AT 906.96. TONNES

NOV 4/WITH GOLD UP $44.45 TO $1673.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.48 TONNES FROMTHE GLD////INVENTORY RESTS AT 911.59 TONNES.

NOV 3/WITH GOLD DOWN $18.30 TO $1628.85: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.05 TONNES FROM THE GLD////INVENTORY RESTS AT 915.07 TONNES

NOV 2/WITH GOLD UP 55 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 919.12 TONNES.

NOV 1/WITH GOLD UP $9.20 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES FORM THE GLD../INVENTORY RESTS AT 920.57 TONNES

OCT 31/WITH GOLD DOWN $4.00; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD//INVENTORY RESTS AT 922.59. TONNES//

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

GLD INVENTORY: 913.88 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

DEC 16/WITH SILVER UP 2 CENTS; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.85 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 508.15 MILLION OZ//

DEC 15/WITH SILVER DOWN 78 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF EXACTLY 2.00 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 510.000 MILLION OZ

DEC 14/WITH SILVER UP 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 512.000 MILLION OZ//

DEC 13/WITH SILVER UP 59 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 600,000 OZ FROM THE SLV////INVENTORY RESTS AT 513.900 MILLION OZ//

DEC 12/WITH SILVER DOWN 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 514.500 MILLION OZ//

DEC 9/WITH SILVER RISING 77 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.2 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 514.500 MILLION OZ.

DEC 8/WITH SILVER RISING 34 CENTS TODAY: OVER THE PAST 3 WEEKS, WE HAVE GAINED A STRONG: 44.777 MILLION OZ/INVENTORY RESTS AT 516.700 MILION OZ.

NOV 14/WITH SILVER UP 41 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 11/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ FROM THE SLV///INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 10/WITH SILVER UP 39 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 368,000 OZ INTO THE SLV///INVENTORY RESTS AT 472.476 MILLION OZ//

NOV 9/WITH SILVER DOWN 10 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV/; A WITHDRAWAL OF 3.821 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 472.108 MILLION OZ//

NOV 8/WITH SILVER UP 48 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.751 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 475.929 MILLION OZ//

NOV 7/WITH SILVER UP 12 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 4/WITH SILVER UP $1.31 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.972 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 3.WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 566,000 OZ FROM THE SLV////INVENTORY RESTS AT 482.650 MILLION OZ//

NOV 2/WITH SILVER DOWN 9 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 92,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.216 MILLION OZ//

NOV 1/WITH SILVER UP 53 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 415,000 OZ FORM THE SLV////INVENTORY RESTS AT 483.308 MILLION OZ

OCT 31: WITH SILVER FLAT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .644 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 483.723 MILLION OZ//

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: A WITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

CLOSING INVENTORY 508.15 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

end

LAWRIE WILLIAMS:

3. Chris Powell of GATA provides to us very important physical commentaries//

Your weekend reading material

(Alasdair Macleod/GATA)

Alasdair Macleod: Rising rates lead to financial accidents

Submitted by admin on Thu, 2022-12-15 11:53Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, December 15, 2022

A recent Bank for International Settlements paper warning of unappreciated risks in foreign exchange markets echoes my earlier warning in an article for Goldmoney published over a month ago describing derivative risks in FX markets.

In this article I also show evidence that banks in both the U.S. and Eurozone are reducing the deposit side of their balance sheets by turning away big deposits that are ending up in central bank reverse repos, parking unwanted liquidity out of public circulation. The great unwind is well underway.

Credit contraction is not only driving a bear market in financial assets, but the exposure to malinvestments by rising interest rates is having negative consequences for the non-financial economy as well. Private equity, which has thrived on cheap finance used to leverage targeted businesses, is showing signs of unwinding with two major Blackrock funds suspending redemptions.

As we approach the season for year-end window dressing, we must hope that the volatility in thin markets that often accompanies it does not destabilise global financial markets.

… For the remainder of the analysis:

https://www.goldmoney.com/research/rising-rates-lead-to-financial-accidents?gmrefcode=gata

END

Very interesting: for the first time, India’s government is getting more favourable towards gold as money

(Reuters/GATA)

India’s government keeps getting more favorable toward gold as money

Submitted by admin on Thu, 2022-12-15 17:36Section: Daily Dispatches

India to Invite Bids for Extracting Gold from Dumps at Colonial-Era Mines

By Neha Arora and Mayank Bhardwaj

Reuters

Thursday, December 15, 2022

NEW DELHI — India plans to invite bids to extract gold from 50 million tonnes of processed ore in a cluster of colonial-era mines in the southern state of Karnataka, a senior government official with direct knowledge of the matter said today.

The Kolar fields, located about 65 kilometres (40 miles) northeast of India’s technology hub of Bengaluru, are among the country’s oldest gold mines

The Kolar mines, closed more than 20 years ago, held gold deposits worth around $2.1 billion, and India is now keen to take advantage of new technology that can extract gold from even the leftovers of ore that was processed in the past.

Other than gold, the government also aims to extract palladium from the processed ore, or dumps, said the official, who did not wish to be named, in line with official rules.

“We are looking at how to monetise these gold reserves trapped in the processed ore,” the official said. …

… For the remainder of the report:

end

GOLD/SILVER

/4. OTHER PHYSICAL SILVER/GOLD COMMENTARIES

Ep. 103 Live from the Vault

A MUST VIEW

Gold channelling East – How much does China really own? Feat. London Paul

In this week’s Live from the Vault, Andrew Maguire joins publisher and analyst London Paul to explore a multipolar metals market, following the reveal that China bolstered its gold reserves after offloading hundreds of billions of US Treasuries in recent months.

The precious metals expert dissects how the BIS is now squaring up 50 years of accrued leases and questions how the full implementation of NSFR regulation could affect investors into 2023 and beyond.

end

5. Commodity commentaries//IRON ORE

END

6/CRYPTOCURRENCIES/BITCOIN ETC

A huge story: Binance the largest exchange for cryptos witnesses their “proof of reserves” removed from Auditor’s site. Investors begin pulling their bitcoins etc

from them. All cyrptos will go to their instrinsic value and that value is zero!

(zerohedge)

Bitcoin Tumbles As Binance ‘Proof-Of-Reserves’ Removed From Auditor’s Site

FRIDAY, DEC 16, 2022 – 07:20 AM

Update (0720ET): Crypto exchange Binance has seen its proof-of-reserve audits removed from auditor Mazars’ website.

“Mazars has indicated that they will temporarily pause their work with all of their crypto clients globally, which include Crypto.com, KuCoin, and Binance. Unfortunately, this means that we will not be able to work with Mazars for the moment,” a spokesperson for the firm said in an emailed statement to Bloomberg News on Friday.

Binance CEO Changpeng “CZ” Zhao was quick to react to the news on Twitter with a retweet from a random commenter.

“Making a statement on why an auditing company decided to quit working with crypto? Ask them lol,” the tweet reads.

The news comes shortly after Mazars confirmed on Dec. 7 that Binance possessed control over 575,742 Bitcoin of its customers, worth around $9.7 billion at the time of writing.

The report has since been also removed from Mazars’ website.

CZ appeared on CNBC yesterday to ‘explain’…

Holy Sh*t!

Get your bitcoin OFF Binance.#bitcoinpic.twitter.com/xSxNoyARXH— Neil Jacobs (@NeilJacobs) December 15, 2022

Bitcoin puked right as the Mazars headlines hit, dropping back to $17,000…

* * *

As Bitcoin Magazine Pro’s Dylan LeClair and Sam Rule asked (and answered) earlier, is Binance facing FUD or legitimate questions?

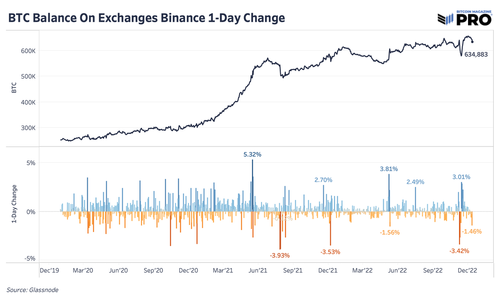

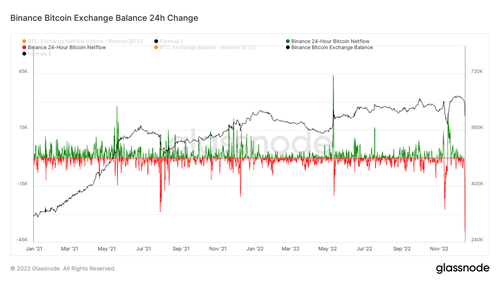

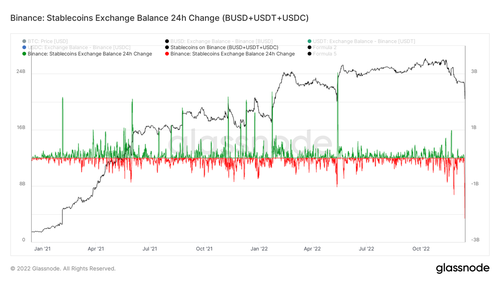

Binance’s bitcoin balance sees its largest one-day outflow ever. BUSD stablecoin experiences large redemptions and the price legitimacy for the exchange-native BNB token is called into question.

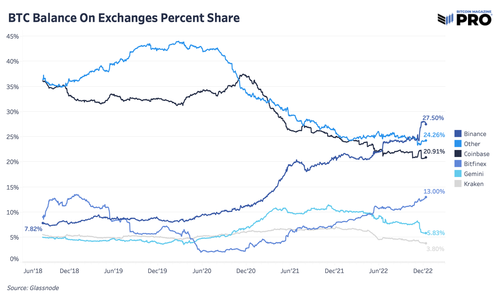

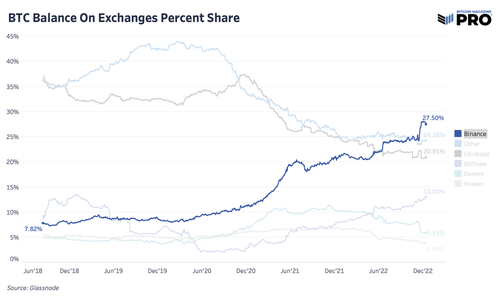

By far, one of the biggest winners in the aftermath of the FTX collapse has seemed — on the surface — to be Binance. After only having 7.82% market share of the bitcoin supply on exchanges in 2018, their share is now 27.50% despite a much broader trend of bitcoin supply leaving exchanges. The bitcoin balance on Binance now totals 595,864 BTC, which is 3.1% of outstanding supply, worth $10.58 billion. This bitcoin belongs to their customers and reflects a growing trend in market share over the last few years that has made Binance the largest bitcoin and cryptocurrency exchange in the world.

As highlighted previously in “The Exchange War: Binance Smells Blood As FTX/Alameda Rumors Mount,” Binance now controls approximately 60% of the spot and derivatives volume in the entire market as well. It’s hard to see how any exchange in the space can be a “winner” in the current market conditions, but one could make the case for Binance, with the exchange’s growing strength in a decimated industry. On top of that, Binance’s BNB token, the native currency of Binance’s own Ethereum-competing Layer 1 blockchain, is still one of the better performing tokens when valued in bitcoin terms this year.

Yet, is this recent “strength” everything that it seems or is it a facade? We’ve learned over the last month that no company is safe in this industry right now (especially exchanges) and questions are growing around Binance’s practices, solvency, BNB token value and the overall state of their business over the last few weeks. Is it FUD or legit? Let’s try to break some of it down, addressing the concerns through an objective and skeptical lens.

Binance Flows

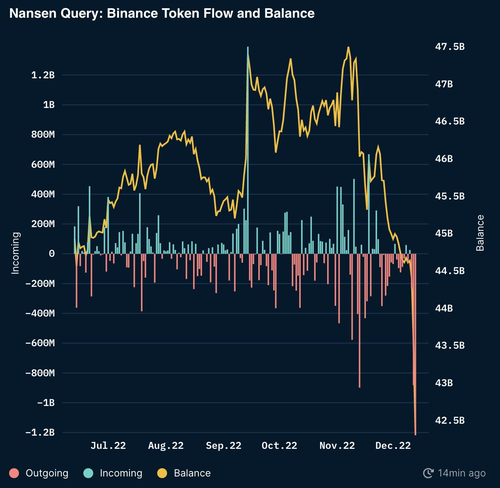

Over the last day, we’ve seen significant outflows from Binance across different various tokens and bitcoin when looking at both Nansen and Glassnode tracking. Across ETH and ERC20 tokens, Binance saw $3 billion leaving the exchange in its largest single-day outflow since June. Across Nansen total wallet tracking, all Binance balances are estimated at $62.5 billion with around 50% of those balances in stablecoins across BUSD and USDT.

Source: Nansen

Source: Nansen

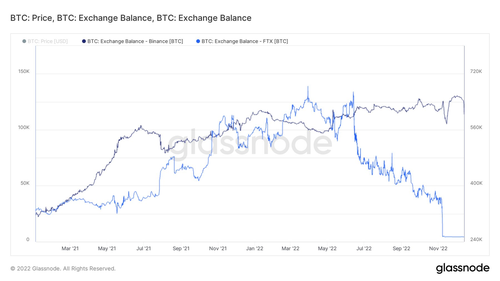

According to Glassnode, the total bitcoin exchange balance on Binance is down around 6-7% over the last day, after reaching a peak on December 1. Although balances remain above 500,000 bitcoin and Binance has shown a rising trend of bitcoin balances on the platform this year, this is a significant move for outflows in just 24 hours. The largest one-day change in bitcoin outflows was just shy of 4% back in July. As a general comparison, the trend of bitcoin exchange balances was a much different story for FTX, whose balance had been falling heavily since June.

Note that in some of the charts below, exchange balances are using daily data from Glassnode instead of 10-minute or 1-hour intervals where we can see more of the latest bitcoin exchange outflows. The numbers above reference the latest 1-hour interval data. Exchange balance data, especially intraday, can change and data is typically more reliable on a longer time horizon, especially given that we have little insight into Glassnode’s classification and data science techniques that are used to label different wallets and addresses. Yet, however you cut the data, Binance outflows over the last 24 hours are a bit alarming and raise questions: Is this a one-off event and just business as usual or is this the start of something more?

In absolute terms, the last 24 hours have brought about the largest ever flight away from Binance for both bitcoin and stablecoins — an extremely notable move.

In particular, in the case of BUSD, Binance’s native stablecoin that has its reserves custodied by U.S. financial firm Paxos, there has been a notable amount of redemptions as of late. Large holders of BUSD have been withdrawing from Binance and sending it to Paxos, redeeming the stablecoins for dollars. This shows up as BUSD being “burned” at the Paxos Treasury.

Readers can track the on-chain addresses provided by Binance for free here.

The main cause for concern is not whether Binance has any bitcoin/crypto or not. We can transparently see that the firm controls tens of billions worth of crypto assets. What isn’t exactly clear, similar to FTX, is whether the firm has commingled users funds or whether the firm has any outstanding liabilities against user assets.

Binance CEO Changpeng Zhao (CZ) has said that the firm has no liabilities with any other firms, but as recent months have shown, words don’t mean all that much. While we are not claiming that CZ is lying to the public about the state of Binance finances, we have no way to prove otherwise.

CZ’s response as to whether the company was going to audit liabilities against user assets was, “Yes, but liabilities are harder. We don’t owe any loans to anyone. You can ask around.”

Unfortunately, “ask around” isn’t a satisfactory enough answer for an ecosystem supposedly built around the ethos of don’t trust, verify.

While there is no doubt that Binance is an industry giant in the crypto derivatives industry, how do we know the firm isn’t doing similar things as past actors in regards to trading against clients using user funds and/or proprietary data. Things like the former Chief Legal Officer of Coinbase departing Binance U.S. last summer after just three months as the CEO leaves one with many questions.

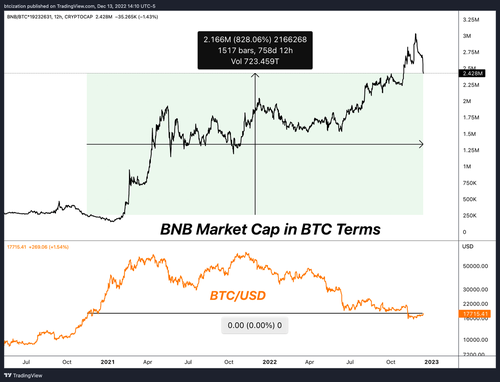

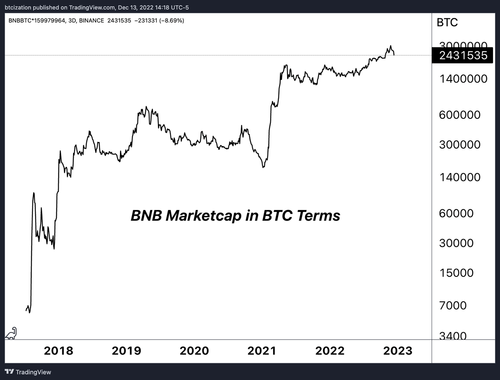

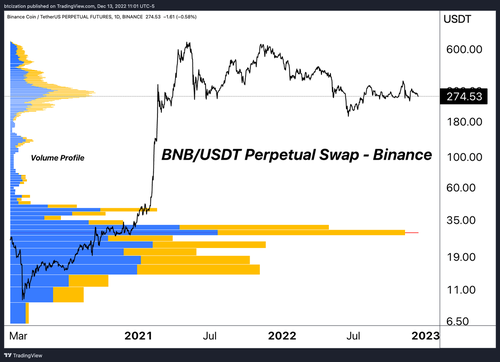

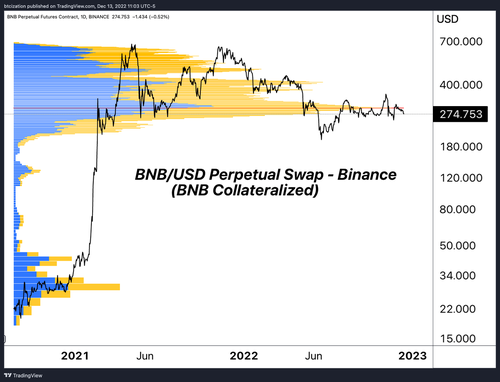

To add to our skepticism, the price of the Binance exchange token BNB is near all-time highs in bitcoin terms, appreciating an astounding 828% against bitcoin in the last 785 calendar days.

Is BNB, a more centralized cousin to Ethereum, really worth approximately 14% of all bitcoin that will ever exist? BNB is not equity in the Binance company. BNB is a crypto token spun up from nothing in 2017.

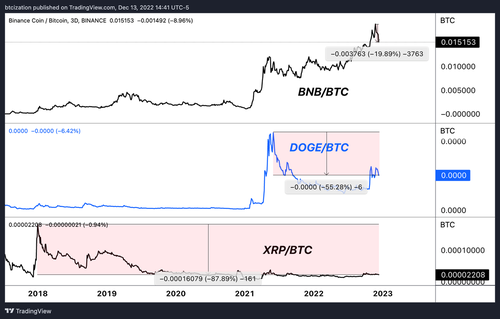

BNB is one of the few cryptocurrencies that is up year-to-date in bitcoin terms, with the others being illiquid alts well below their BTC-denominated all-time highs.

The only other two outperformers during 2022 have been the “meme” DOGE, which is 55% below its all time high in bitcoin terms, and quasi-security XRP, which has been delisted by major exchanges and is 87% below its all-time highs in bitcoin terms.

Why is the outperformance so notable? Why are we hammering this point so hard? Because financial markets aren’t magical machines tied to a fantasy-land reality. Financial markets — while appearing to be disconnected from reality at times — always come crashing down to reality, exposing those that were possibly perceived as giants once before.

For the most part, the crypto industry is an attempt at modern alchemy, and exchange tokens minted from nothing with centrally engineered “tokenomics” are no different.

In fact, they are part of the problem.

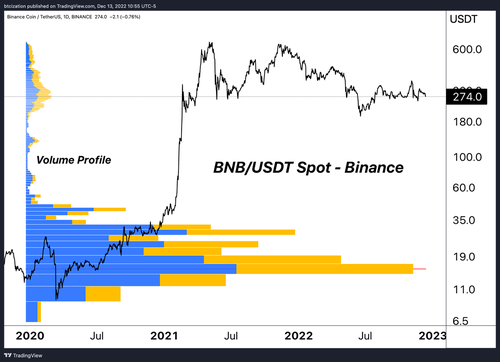

It could be possible that BNB was pushed up with the internal help of Binance or its unofficial affiliates during the bull run. Just look at the volume profile of where coins changed hands on its native exchange. While it would be a leap of faith to say this took place directly using customer funds à la FTX, the revenue of the company has been used to buy back the token, similar to a stock buyback.

While it remains to be seen whether the firm is levered against its own token in any sort of way, it would certainly be no surprise to us if the company supported the ascent of the token/chain, similarly to many other exchanges with token that outperformed bitcoin during the bull run. BNB is a “blockchain” that can be arbitrarily halted by the Binance team. It is not even attempting to be a decentralized application set.

That’s fine, but we remain extremely skeptical that its relative valuation against bitcoin — what we believe to be humanity’s best bet as decentralized digital cash — is tethered to reality.

How does something that traded with double the realized volatility of bitcoin during the bull market now have the same implied volatility in the bear market after it has appreciated by over an order of magnitude with a strong relative outperformance throughout 2022?

The entire “industry” is cross-collateralized, and all of the altcoins are merely riding on the beta of bitcoin with far less liquidity, thus having greater volatility and potential (fleeting) upside.

We think this attempt at modern alchemy is destined to fail, at worst. At best, the asset likely drastically underperforms global neutral money through its adoption phase. Said differently, the worst-case, paranoid-style take would be that the exchange rate of BNB is tied to the solvency status of Binance the exchange. We don’t think that there is an overly strong probability of this outcome per say, but it is certainly non-zero.

The coming weeks will be full of headlines around the state of global crypto regulation in a post-FTX world. In a 48-hour period, Reuters published news stating that the U.S. Justice Dept is split over charging Binance, Binance withdrawals for bitcoin and aggregate stablecoin pairs have hit all-time highs and the BNB exchange token has fallen 10% relative to bitcoin.

Out of an abundance of caution, we will continue to urge readers operating on any centralized exchange — of which Binance is most definitely included — to look into self custody solutions. There have been far too many instances of incompetence and/or misconduct from exchanges.

It’s not that we don’t trust CZ or Binance, it’s the fact that we don’t trust anyone.

The whole point of bitcoin is we now have an asset that is truly the liability of no one. Verify the ownership of an open distributed network with cryptography; don’t trust permissioned IOUs. With the mix of regulatory concerns about the global crypto derivatives industry, a questionable exchange token with unbelievable relative performance over the last two years and a shaky proof-of-reserves attestation — that was incorrectly claimed to be an audit and had industry CEOs raising eyebrows — we find the need to urge our readers to evaluate their counterparty risk.

We will update readers as the situation developers.

end

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS/FRIDAY MORNING.7:30 AM

ONSHORE YUAN: DOWN TO 6.98721

OFFSHORE YUAN: 6.98130

SHANGHAI CLOSED DOWN 0.79 PTS OR 0.02%

HANG SANG CLOSED UP 82.08 OR 0.42%

2. Nikkei closed DOWN 524.58 PTS OR 1.87%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 104.20 Euro FALLS TO 106.20 DOWN 18 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.249!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 137.08/JAPANESE YEN COLLAPSING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.1510%***/Italian 10 Yr bond yield RISES to 4.302%*** /SPAIN 10 YR BOND YIELD RISES TO 3.253…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.35//

3j Gold at $1776.90//silver at: 23.17 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 30/100 roubles/dollar; ROUBLE AT 64.65//

3m oil into the 74 dollar handle for WTI and 77 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 137.08 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9297– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9873 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.480% UP 5 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.540% UP 5 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,65…

GREAT BRITAIN/10 YEAR YIELD: 3.387 % UP 14 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Tumble Ahead Of $4 Trillion Quad Witch, 2nd Biggest Ever OpEx

FRIDAY, DEC 16, 2022 – 08:06 AM

A miserable week for global stocks – which wrongfooted traders as risk first soared after a weaker than expected CPI only to tumble more than 7% just two days later – was set to end with even more selling on Friday after hawkish signals from the Fed and the ECB sparked worries about higher-for-longer interest rates leading to a possible recession: the latest economic data signaled a slowdown in US growth; data from France showed that it faces a greater recession risk, with its PMI falling to its lowest level in two years. Similarly UK companies are steeling themselves for an economic contraction, with both the manufacturing and service sectors experiencing a slump in the fourth quarter. Economists now see a 60% probability of recession in the US and an 80% chance in Europe. Equity analysts have cut 12-month earnings estimates for the regions to the lowest levels since March and July, respectively.

Not helping matters is today’s massive, $4 trillion quad-witching option expiration, which as we previewed yesterday threatens to become a liquidity-draining vortex just as CTAs are forced to dump stocks. potentially leading to outsized price moves. With the S&P 500 stuck for weeks within 100 points of peak gamma at the 4,000 strike, the sheer volume provides a positioning reset that could turbocharge market moves. Given the backdrop of hawkish central banks and slowing growth, worries are mounting the expiration will act as an air pocket.

Finally, bitcoin plunged back under $17K following news that accounting firm Mazars has paused work for all crypto clients globally, according to Binance, which was a customer of the auditing firm.

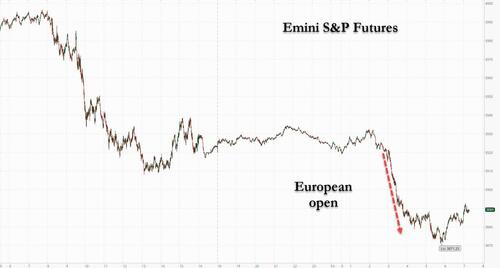

Between all that, it is perhaps surprising that S&P futures are down only 1% while contracts on the Nasdaq 100 dropped 0.62% by 6:56 a.m. in New York. The overnight selloff accelerated when Europe opened as European peripheral bonds blew out amid fears that the ECB’s aggressive tightening and QT will crash the European bond market. The dollar fluctuated and Treasuries dropped across the curve. Oil trimmed a weekly gain, sliding more than 2% amid renewed fears that the Fed is pushing the US into a crash-landing.

The S&P 500 index, already on track for its biggest annual slump since 2008, erased another $1.1 trillion in market capitalization in the past two days after both the Fed and the ECB took a more hawkish tone than expected about how much further rates will need to rise to tame inflation. The MSCI ACWI Index, the global equities gauge, headed for a 1.4% retreat this week.

“The worrying aspect for markets is the rate hike finishing lines are still unknown, and we have the two most dominant central banks in the world climbing the mountain into very restrictive territory,” Stephen Innes, managing partner at SPI Asset Management, wrote in a note. “Hiking interest rates into a dimming macro environment will undoubtedly trigger a recession. The question is just how profound.”

Ann-Katrin Petersen, senior investment strategist at BlackRock Investment Institute, said on Bloomberg Television that central banks were starting to acknowledge they will have to crush growth and will likely engineer recessions to tame inflation.

Among notable moves in US premarket trading, Adobe shares are up 3.7% in premarket trading, after the software company reported adjusted fourth-quarter earnings that beat expectations. Analysts said the report speaks to positive demand for creative design software despite economic uncertainties. Guardant Health shares sank after following disappointing results from a study of its blood test for detecting colorectal cancer in average-risk adults. Here are some other notable premarket movers:

- Amazon (AMZN US) falls 1.3% in premarket trading as JPMorgan cut its price target on the stock to $130 from $145 primarily due to AWS revenue deceleration and margin compression amid challenging macro conditions. .

- Meta Platforms (META US) rises 1.7% in premarket trading as JPMorgan raised the recommendation on the stock to overweight from neutral, citing increased cost discipline and a more favorable revenue outlook.

- Lanvin (LANV US) shares surge 56% in US premarket trading, following a volatile New York trading debut for the luxury group that saw its stock bounce between a gain of as much as 130% and declines of more than 50%.

- Stocks exposed to cryptocurencies drop in US premarket trading, as the price of Bitcoin fell below the $17,000 level after the Binance exchange said French auditor Mazars Group had paused work for all crypto clients globally. Hut 8 Mining (HUT CN) -4.6%, Block (SQ US) -2.1%.

“Recessionary fears raced back to the top of the agenda and any thoughts of a Santa rally have all but evaporated, with previous hopes of peak inflation and interest rates being soundly rejected,” said Richard Hunter, head of markets at Interactive Investor. “Comments from the ECB in particular that ‘we are not slowing down, we are in for the long game’ were in direct contrast to what markets had been pricing in over recent weeks.”

The slump this week also kept the S&P 500 from overcoming a technical downtrend in place since the start of the year, which has put an end to the past three bear-market rallies. The index didn’t convincingly break above its 200-day moving average, and is now close to testing its 50-day moving average, two other closely watched technical thresholds.

Europe’s equity benchmark fell for a third day, to a five-week low. European real-estate stocks were the biggest declinerss in Friday trading, with the subindex for the rate-sensitive sector the biggest laggard on the Stoxx 600, after the ECB on Thursday hit a more hawkish tone than expected alongside its latest rate decision. Stoxx 600 Real Estate sector declines 2.2% with the wider Stoxx 600 -1%. Telecoms and retailers also underperformed as all sectors fell barring autos, which are supported by recent data that showed auto sales in Europe rose for a fourth straight month. Here are some of the biggest European movers:

- Games Workshop shares jump as much as 15%, the most since September 2020, after the maker of the Warhammer series of games said it has reached an agreement in principle for Amazon to develop the company’s intellectual property into film and television productions.

- TeamViewer shares jump as much as 11% to touch their highest level in six months, after the remote- software provider said that it would eventually end its sponsorship partnership with Manchester United

- Hollywood Bowl rises as much as 6.8% to its highest level since June 8 after the bowling chain reported a strong set of FY22 results

- Suedzucker rises as much as 5.9%, adding to yesterday’s 3.3% gains, as Warburg says the German sugar producer’s latest financial update is a “blow-out guidance” for the coming fiscal year.

- OVS shares rise as much as 5.3% in Milan after 9-month results, with Banca Akros upgrading to buy from neutral, noting that the 4Q sales performance is “much higher of our expectation.”

- Rank falls as much as 9.1%, most in two months, after a trading update from the gambling firm.

- Wood shares fall as much as 8% as Barclays cuts the energy services firm to equal-weight

- National Express falls as much as 6.5% after being cut to hold from buy at Liberum, with the broker highlighting that growing headwinds point to a “deleveraging challenge,” according to note.

- Aalberts shares drop as much as 5.1% after the Dutch piping firm announced Wim Pelsma has notified its supervisory board that he wishes to step down as chief executive officer in the second half of 2023

- Tele2 shares drop as much as 4.7% after Redburn analyst Steve Malcolm cut the recommendation to sell from neutral, citing a potential 2023 guidance cut.

Asian equities fell Friday, extending the week’s decline, as hawkish views from global central banks offset the boost from easing delisting risk for Chinese stocks in the US. The MSCI Asia Pacific Index dropped as much as 0.9%, led by technology stocks. Shares in Japan and Taiwan were among the worst performers in the region; it posted the first weekly decline since October. Chinese shares eked out small gains after US officials said they got sufficient access to audit documents on companies in China and Hong Kong, removing the acute threat of delisting faced by those firms. Still, caution remained as the US government added dozens of Chinese tech companies to its blacklist. A risk-off mood extended into Friday’s trading after the Fed’s hawkish tone from its latest rate decision was echoed by the European Central Bank, squashing hopes for a pivot in monetary policies next year.

“As premature pivot bets collide with overly-exuberant China re-opening bets,” expectations will need to be “tempered for a bumpy path out of Zero-Covid amid winter/Lunar New Year travel and lingering confidence deficit,” said Vishnu Varathan, head of economics & strategy at Mizuho Bank. The Asian stock benchmark has fallen 1.8% this week, set to snap a six-week gaining streak as traders took profit following a recent rally, and as China’s surging Covid cases and the Fed’s tightening weighed on sentiment.

Japanese stocks declined for a second day, leading losses in the region, as investors assess the possibility of further tightening by global central banks and weak US retail sales data. The Topix Index fell 1.2% to close at 1,950.21, while the Nikkei declined 1.9% to 27,527.12. The MSCI Asia Pacific Index dropped 0.7%. Toyota Motor Corp. contributed the most to the Topix Index decline, decreasing 1.9%. Out of 2,163 stocks in the index, 343 rose and 1,737 fell, while 83 were unchanged. “Both the U.S. and Europe were down significantly yesterday, and Japanese stocks are also dragged by this,” said Ryuta Otsuka, a strategist at Toyo Securities Co

In FX, the greenback traded mixed versus its Group-of-10 peers; the yen was the best performer.

- The euro swung between modest gains and losses against the US dollar. The euro’s volatility skew steepened with the currency failing to tackle spot offers around $1.0750 after the hawkish ECB decision and as profit-taking took over.

- The pound climbed and UK bonds fell, in line with bunds.

- Australian dollar reversed an intraday gain after iron ore fell on news that China would be centralizing purchases of the commodity.

- Kiwi rose as data showed non-resident bond holdings hit a four-year high.

- In rates, Treasury yields added up to 4bps led by the long end.

In rates, treasury futures drifted lower over Asia and early European session, following wider losses seen across core European rates after several ECB policy members reinforced the bank’s hawkish stance. US session light, with focus including manufacturing data and Fed’s Daly talking on inflation. US yields were cheaper by up to 5bp across long-end of the curve, with 2s10s and 5s30s spread steeper by 3bp and 1bp on the day; 10-year yields near cheapest levels of the session at around 3.49% with bunds, gilts lagging by additional 6bp and 7bp in the sector. The German curve added 10-12 bps while Italian yields rose by 15-23bps after money markets bet the ECB will lift the deposit rate as high as 3.36% after a barrage of hawkish comments from ECB policy makers.

In commodities, crude benchmarks posted losses in excess of 2.0%; though, WTI still has around USD 4.0/bbl of downside required to bring it back to the WTD low of USD 70.25/bbl which printed on Monday. French President Macron said EU energy policy is likely to be finalized during the meeting on Monday, while it was separately reported that the Czech PM said EU leaders agreed the gas price cap deal must be done by Monday at the energy ministers’ meeting, according to Reuters. Spot gold and silver are experiencing some marked divergence with the yellow metal essentially unchanged, while silver has slipped by around 2% to the mid-USD 22/oz region.

Looking to the day ahead now, and data releases include the global flash PMIs for December. Central bank speakers include the Fed’s Daly, and the ECB’s Rehn, Holzmann and Centeno. Finally, earnings releases include Accenture.

Market Snapshot

- S&P 500 futures down 1.1% to 3,854.25

- STOXX Europe 600 down 0.8% to 426.66

- MXAP down 0.7% to 156.22

- MXAPJ down 0.6% to 508.56

- Nikkei down 1.9% to 27,527.12

- Topix down 1.2% to 1,950.21

- Hang Seng Index up 0.4% to 19,450.67

- Shanghai Composite little changed at 3,167.86

- Sensex down 0.8% to 61,333.94

- Australia S&P/ASX 200 down 0.8% to 7,148.68

- Kospi little changed at 2,360.02

- German 10Y yield little changed at 2.20%

- Euro little changed at $1.0625

- Brent Futures down 1.9% to $79.66/bbl

- Brent Futures down 1.8% to $79.72/bbl

- Gold spot down 0.0% to $1,776.18

- U.S. Dollar Index little changed at 104.59

Top Overnight News from Bloomberg

- An estimated $4 trillion of options is expected to expire Friday in a monthly event that tends to add turbulence to the trading day. This time, with the S&P 500 stuck for weeks within 100 points of 4,000, the sheer volume provides a positioning reset that could turbocharge market moves

- The Fed’s quarterly projections showed officials now expect so-called core inflation — which excludes food and energy — to end this year around 4.8%, up from the 4.5% figure they forecast in September. Yet that number looks much too high to Wall Street economists

- The ECB is likely to raise interest rates by 50 basis points at its meetings in both February and March, Governing Council member Olli Rehn said

- The ECB will likely accelerate the pace at which it offloads government debt accumulated during past crises from July next year as part of its fight against soaring inflation, Governing Council member Francois Villeroy de Galhau said

- Markets have understood the hawkish message sent by ECB rate setters, Governing Council member Robert Holzmann tells reporters in Vienna

- ECB Governing Council member Madis Muller said interest rates will likely rise above levels anticipated by markets as the economic slowdown isn’t enough to curb inflation as needed

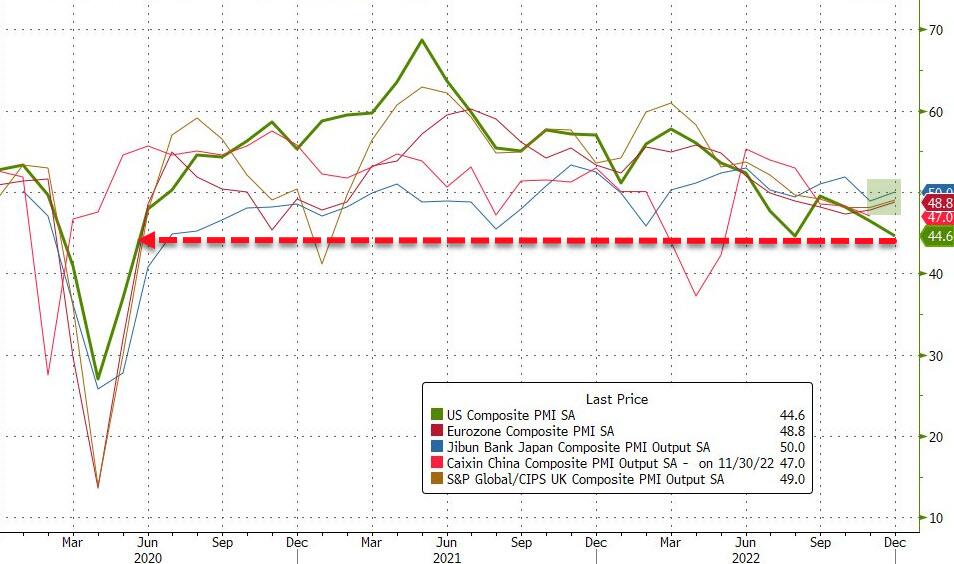

- Euro-zone composite PMI rose to 48.8 in December, from 47.8 in the prior month and versus an estimate 47.9

- Three senior Italian politicians criticized the ECB’s increase in borrowing costs, pointing to rising tensions between Giorgia Meloni’s government and Frankfurt officials

- UK Composite PMI was little changed at 49 in December, compared to last month’s reading of 48.2 and expectations for a drop to 48

- Britain is enduring the highest number of strikes since Margaret Thatcher was prime minister, according to estimates by a group of economists

- UK retail sales unexpectedly fell in November. The volume of goods sold in shops and online fell 0.4%, the Office for National Statistics said Friday. Sales excluding auto fuel fell 0.3%. Economists expected a 0.3% gain on both measures

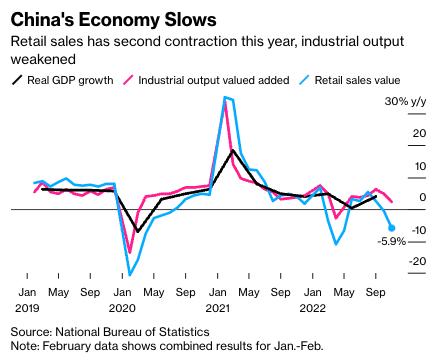

- China’s abrupt ending of its Covid Zero restrictions have forced economists to make sharp revisions to their growth projections for this year and next. UBS Group AG and Australia & New Zealand Banking Group Ltd. were the latest to adjust forecasts on Friday, cutting estimates for this year to 2.7% as Covid infections spread rapidly. Predictions for next year were raised sharply to close to 5% or higher, on the expectation that consumer and business activity will recover as Covid infections subside

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were pressured on spillover selling from global counterparts following the slew of central bank rate hikes and with markets also unnerved by a flurry of dismal US data releases. ASX 200 was lower with sentiment not helped by a deterioration in the latest Australian flash PMI data releases. Nikkei 225 underperformed after the ruling LDP tax panel agreed and provided details on the tax hike plan to boost the defence budget and with index-heavyweight Fast Retailing hit by the announcement of a 3-for-1 stock split. Hang Seng and Shanghai Comp lacked firm direction amid mixed headlines with some encouragement from reports related to US audits in which Chinese companies averted a delisting after the US was given full inspection access, while there was also a constructive tone in discussions between US Treasury Secretary Yellen and China’s Ambassador to the US in which they agreed to step up coordination on trade and policies.

Top Asian News

- China National Health Commission issued a plan to step up COVID control and prevention in rural areas where it will strengthen reserves of essential drugs and COVID home test kits. China will also accelerate COVID vaccination of the rural population, especially among the elderly and said that people returning to their hometowns in rural areas should monitor their health and reduce contact with the elderly at home, according to Reuters.

- China’s NDRC said the economy is facing more complex and grim external environments but added that the long-term positive trend hasn’t changed and it approved CNY 1.5tln of major projects as of end-November. NDRC said China’s economic growth is expected to continue picking up following the implementation of new COVID rules and that they will focus on stabilising growth, employment and prices, as well as speed up infrastructure project construction and expand effective investment, according to Reuters.

- China’s securities regulator said it welcomes the US PCAOB decision on auditing and will continue supervision work on auditing in the future, while it will create a more stable regulatory environment with the US, according to Reuters.

- China’s ambassador to the US met with US Treasury Secretary Yellen to discuss their views on global macroeconomic and financial developments, while it was reported that they agreed to step up coordination on trade and policies.

- Japan’s government is to implement defence tax hikes in stages over multiple years to secure more than JPY 1tln by fiscal 2027, while it is to adopt a new corporate surtax of 4.0%-4.5% and will introduce a surtax of 1% on incomes for the time being. Furthermore, it is to raise the tobacco tax in stages by JPY 3 a piece and said it will implement defence taxation at an appropriate time from 2024 onwards, according to a draft by the ruling LDP cited by Reuters.

European bourses remains on a downward trajectory as the post-ECB slump continues, Euro Stoxx 50 -1.0%. Sectors were initially mixed but are now all underwater with Real Estate lagging giving the detrimental rate environment. Stateside, US futures are pressured in-line with the above price action and ahead of a handful of Fed speakers, ES -1.1%.

Top European News

- UK Companies Brace for Recession as Manufacturing Slumps

- UK Dec. Flash Services PMI 50; Est 48.5

- Most Banks See More ECB Rate Hikes With Potentially Higher Peak

- Russian Missile Barrage Knocks Out Power to Ukrainian Cities

- UK Civil Aviation Regulator Raises Concerns With Wizz Air

- Bunzl Sinks as Barclays Cuts to Underweight, RS Group Upgraded

FX

- USD has whipsawed within a 104.20-73 range, well within yesterday’s bands, though an overall underlying bid has emerged, with the DXY climbing to incremental new peaks on multiple occasions.

- Though, this action is capped by marked JPY upside given its traditional haven allure and post-data; USD/JPY down to 136.83 at worst.

- GBP impaired further post-BoE dissent on the USD’s move and as the EUR proves comparably more resilient given the hawkish ECB; Cable to 1.2120 and EUR/USD holding above 1.06.

- Elsewhere, G10 peers are generally downbeat given the above narrative, though CAD has proven relatively resilient to the crude action.

- PBoC set USD/CNY mid-point at 6.9791 vs exp. 6.9844 (prev. 6.9343)

Fixed Income

- EGBs continue to slide. With Bunds lower by over 150 ticks and the associated 10yr yield above 2.2% post-ECB.

- Gilts are pressured in-turn, though to a slightly lesser extent given the BoE’s dovish dissenters.

- USTs are in the red, but with magnitudes much more contained and the curve steepening ahead of Fed speak and the region’s PMIs.

Commodities

- Currently, the crude benchmarks are posting losses in excess of 2.0%; though, WTI still has around USD 4.0/bbl of downside required to bring it back to the WTD low of USD 70.25/bbl which printed on Monday.

- Qatar Energy sells February Al-Shaheen crude at USD 1.30-1.50/bbl above Dubai quotes, according to sources.

- French President Macron said EU energy policy is likely to be finalised during the meeting on Monday, while it was separately reported that the Czech PM said EU leaders agreed the gas price cap deal must be done by Monday at the energy ministers’ meeting, according to Reuters.

- ICE warned it may pull the gas market from the EU over the Brussels price cap, according to FT.

- Currently, Dutch TTF Jan’23 is lower by around 8% on the session, though seemingly found a floor around EUR 120/MWh.

- Panama’s government ordered the suspension of operations at First Quantum Minerals’ copper project.

- Spot gold and silver are experiencing some marked divergence with the yellow metal essentially unchanged, while silver has slipped by around 2% to the mid-USD 22/oz region

Central Banks

- ECB’s Villeroy says must not speculate on the number of interest rate rises, too early to talk about the terminal rate.

- ECB’s Muller says rates are likely to increase by more than the market expects. Cannot rely on an economic slowdown to tame inflation.

- ECB’s Rehn says rates need to rise significantly. Interest rates will still have to rise significantly to reach levels that are sufficiently restrictive to ensure a timely return of inflation to the 2% medium-term target.

- ECB’s Holzmann says inflation still poses a challenge, does not want to say where the terminal rate is, the hawkish statement is equivalent to a 75bp hike.

- Bundesbank: German recession now expected in 2023, downturn not seen severe. Click here for more detail.

Geopolitics

- North Korean Leader Kim Jong Un guided a successful test of a ‘high-thrust solid-fuel motor’ at the satellite launching ground and the test was said to have provided a guarantee for the development of another new strategic weapon system, while Kim hopes the new-type strategic weapon would be made in the shortest span of time, according to KCNA.

- HKEX (388 HK) welcomed Asia’s first crypto assets ETFs after the listing of CSOP Bitcoin Futures ETF & CSOP Ether Futures ETF, according to Reuters.

- FTX is reportedly seeking permission to sell off LedgerX, Ember and its branches in Japan and Europe before they lose value and have their licences revoked, according to Cointelegraph.

- Kraken says “We are investigating reports from clients having difficulty connecting to the site and API as well as via mobile apps.”.

- Binance reports that Mazars is to pause work for crypto clients, via Bloomberg.

US Event Calendar

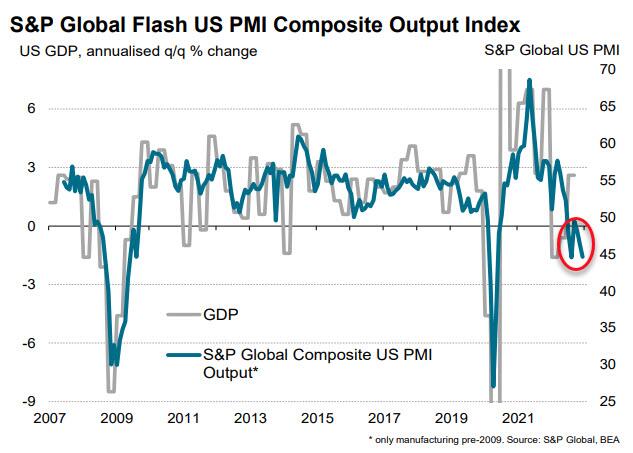

- 09:45: Dec. S&P Global US Composite PMI, est. 46.9, prior 46.4

- 09:45: Dec. S&P Global US Services PMI, est. 46.5, prior 46.2

- 09:45: Dec. S&P Global US Manufacturing PM, est. 47.8, prior 47.7

DB’s Jim Reid concludes the overnight wrap

At this age in life I generally have an idea of what I like and new experiences are rarer, for mostly good reasons. However, tomorrow I’ll attend my first ever artistic swimming (synchronised swimming in old parlance) Christmas performance. Maisie is the youngest in it but has taken to the sport very well in spite of her hip issues. I never thought in a million years I’d go to such an event but here goes.

Talking of year end performances, it would have been completely out of character for 2022 to go out with a whimper and with the last major act of the year, the ECB ensured that we didn’t. Following the hawkish message from the Fed, yesterday saw the ECB join in with a clear signal for markets to price in more aggressive rate hikes. Indeed, there could be no doubt about their message as they 1) pointed to further rate hikes ahead, 2) outlined their plans for quantitative tightening, and 3) upgraded their inflation forecasts significantly. Meanwhile, Bloomberg even reported afterwards that over a third of the Governing Council wanted a larger 75bps hike. That led to some massive market moves coming on the heels of the Fed, with yields on 2yr German debt (+22.1bps) seeing their largest daily increase since September 2008 if you use the generic 2yr series on Bloomberg and to the highest since that point too. And with the Fed and the ECB now pledging to take rates further into restrictive territory in 2023, risk assets took another major hit, with the S&P 500 (-2.49%) and the STOXX 600 (-2.85%) both seeing sizeable losses. The first punch from the Fed didn’t really land on markets but the second punch from the ECB did.