DEC 20/GOLD PRICE UP $27.05 TO $1815.60//SILVER IS UP A FULL $1.05 TO $24.05//PLATINUM IS UP 26.75 TO $1012.45/PALLADIUM IS UP $62.60 TO $1739.65//COVID UPDATES RE CHINA/DR PAUL ALEXANDER//VACCINE IMPACT//VACCINE INJURY//JAPAN FINALLY EXPANDS ITS YIELD CURVE AND WILL BUY UP TO 9 TRILLION YEN JAPANESE BONDS PER MONTH//THAT SET OF A FRENZY IN THE PRECIOUS METALS MARKET//RUSSIA VS UKRAINE UPDATES: UKRAINE SHELLS MAJOR TOWN INSIDE RUSSIAN TERRITORY AGAIN//TOM LUONGO A MUST READ//KARI LAKE WINS A COURT BATTLE AND NOW HER CASE WILL BE HEARD///SWAMP STORIES FOR YOU TONIGHT///

118 C MACQUARIE FUT 36 50 435 H SCOTIA CAPITAL 62 624 H BOFA SECURITIES 10 657 C MORGAN STANLEY 1 661 C JP MORGAN 28 686 C STONEX FINANCIA 1 800 C MAREX SPEC 8

TOTAL: 98 98 MONTH TO DATE: 20,271

COMEX//NOTICES FILED re JPMorgan 28/98

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR DEC. CONTRACT: 98 NOTICES FOR 9800 OZ or .3048 TONNES

total notices so far: 20,271 contracts for 2,027100 oz (63.049 tonnes)

SILVER NOTICES: 0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month 3609 for 18,045,000 oz

END

GLD

WITH GOLD UP $27.05

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////HUGE CHANGES IN GLD INVENTORY:A DEPOSIT OF 1.73 TONNES TONNES OUT OF THE GLD

INVENTORY RESTS AT 912.14 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $1.05

AT THE SLV// :/HUGE CHANGES IN SILVER INVENTORY AT THE SLV THESE PAST 3 WEEKS! A DEPOSIT OF 700,000 OZ FROM THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 509.90 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A SMALL SIZED 155 CONTRACTS TO 123,876 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.13 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. OUR SHORTERS/HFT WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.13 BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD A TINY SIZED LOSS IN OUR TWO EXCHANGES OF 5 CONTRACTS. AS WELL WE HAD EXCHANGE FOR RISK TRANSFER OF 0 CONTRACTS. WE HAD VERY LITTLE SPEC SHORT COVERINGS OF THEIR SHORTFALL. .WE PROBABLY HAD SMALL SHORT ADDITIONS WITH THE SMALL PRICE FALL OF THE SILVER. // OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. BUT THEY ALSO SUPPLIED THE NECESSARY SHORT CONTRACTS>>> SOME INCREASE OF NEWBIE SPEC LONGS ADDING TO THEIR POSITIONS CAUSING ADDITIONAL MISERY TO OUR SHORTERS.

WE MUST HAVE HAD: A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 23 .24. MILLION OZ FOLLOWED BY TODAY;S E.F.P.. JUMP TO LONDON of 5,000 OZ // V) SMALL SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL +4

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS DEC. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF DEC:

TOTAL CONTRACTS for 16 days, total 8503 contracts: OR 42.515 MILLION OZ PER DAY. (531 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 42.515 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 42.515 MILLION OZ INITIAL( VERY SMALL)

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 155 DESPITE OUR $0.13 LOSS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 150 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 23.24 MILLION OZ FOLLOWED BY TODAY:S 5,000 E.F.P.. JUMP TO LONDON //NEW STANDING 23.385 MILLION OZ + EFR = 33.885 MILLION OZ. .. WE HAVE A TINY SIZED LOSS OF 5 OI CONTRACTS ON THE TWO EXCHANGES FOR 0.025 MILLION OZ.. THE SILVER SHORTS ARE NOW TRAPPED AS THEY ARE HAVING CONSIDERABLE DIFFICULTY IN COVERING THOSE SHORTS.

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 176 CONTRACTS TO 424,801 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: removed 107 CONTRACTS.

.

THE SMALL SIZED INCREASE IN COMEX OI CAME WITH OUR SMALL LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR DEC. AT 58.86 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY:S HUGE QUEUE JUMP of 59 contracts or 5900 oz//(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). NEW STANDING 63.576 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS PRICE OF $2.10WITH RESPECT TO MONDAY’S TRADING

WE HAD A SMALL SIZED GAIN OF 280 OI CONTRACTS (0.8709 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 104 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 424,801

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 280 CONTRACTS WITH 176 CONTRACTS INCREASED AT THE COMEX AND 104 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 280 CONTRACTS OR 0.8709 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (104 CONTRACTS) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (176) TOTAL GAIN IN THE TWO EXCHANGES 280 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERINGS // CONTINUED GOOD BANKER ADDITIONS BUT THEY ALSO SUPPLIED THE NECESSARY PAPER SHORT. WE HAD FEW SHORT SPEC ADDITIONS/// // FEW NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR DEC. AT 58.86 TONNES FOLLOWED BY TODAY’S QUEUE. JUMP of 5900 oz// //NEW STANDING 63.757 TONNES///3) ZERO LONG LIQUIDATION //.,4) SMALL SIZED COMEX OPEN INTEREST GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

DEC

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC :

33,233 CONTRACTS OR 3,323,300 OZ OR 103.38 TONNES 16 TRADING DAY(S) AND THUS AVERAGING: 2077 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES:103.38 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 103.38/3550 x 100% TONNES 2.90% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 103.38 tonnes Initial//VERY SMALL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A SMALL SIZED 155 CONTRACTS OI TO 123,801 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 150 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 150 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 150 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 155 CONTRACTS AND ADD TO THE 150 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN TINY SIZED LOSS OF 5 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 0.025 MILLION OZ//

OCCURRED WITH OUR SMALL LOSS IN PRICE OF $0.13….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)MONDAY MORNING//SUNDAY NIGHT

SHANGHAI CLOSED DOWN 33.35 PTS OR 1.07% //Hang Sang CLOSED DOWN 258.01 OR 1.33% /The Nikkei closed DOWN 669.61 OR 2.46% //Australia’s all ordinaries CLOSED DOWN 1.66% /Chinese yuan (ONSHORE) closed UP TO 6.9689//OFFSHORE CHINESE YUAN UP TO 6.9722// /Oil UP TO 76.19 dollars per barrel for WTI and BRENT AT 80.10 / Stocks in Europe OPENED ALL MIXED. ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A VERY SMALL SIZED 176 CONTRACTS UP TO 424,801 DESPITE OUR THE LOSS IN PRICE $2.10

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE -ACTIVE DELIVERY MONTH OF DEC… THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 104 EFP CONTRACTS WERE ISSUED: ;: , . 0 FEB: 104 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 104 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 280 CONTRACTS IN THAT 104 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 176 CONTRACTS..AND THIS SMALL SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF GOLD $2.10. WE ARE WITNESSING FEW SPEC SHORTS ADDITIONS TO THEIR SHORTFALL. BANKERS CONTINUE AS NET BUYERS OF COMEX GOLD CONTRACTS AS THEY HAVE BEEN NET LONG FOR THE PAST FEW MONTHS. WE ALSO HAD SOME NEWBIE SPECS ADDITIONS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING DEC (63.757)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL (TOTAL SO FAR THIS YEAR 591.535 TONNES)

Dec. 63.757 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $2.10) //// AND WERE ALSO UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A SMALL GAIN OF 280 CONTRACTS ON OUR TWO EXCHANGES >. WE HAD A FEW NUMBER OF NEW SPEC SHORT ADDITIONS AND SOME SPEC SHORT COVERINGS.. // WE HAVE GAINED A TOTAL OI OF .8709 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR DEC. (54.57 TONNES), following our QUEUE jump of 5800 oz//new standing RISES to 63.757 tonnes…THIS WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE OF $2.10

WE HAD – 107 CONTRACTS COMEX TRADES REMOVED FROM OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 280 CONTRACTS OR 28000 OZ OR 0.8709 TONNES

Estimated gold volume 191,984// poor//

final gold volumes/yesterday 90,621/ awful

INITIAL STANDINGS FOR DECEMBER 2022 COMEX GOLD //DEC 20

39,625.783 oz Brinks Manfra HSBC includes 1011 kilobars

.

Deposit to the Dealer Inventory in oz

nil oz

Deposits to the Customer Inventory, in oz

211,457.127 oz BRINKS HSBC 1101 kilobars and 5476 kilobars

No of oz served (contracts) today

98 notice(s) 9800 OZ 0.3048 TONNES

No of oz to be served (notices)

227 contracts 22,700 oz 0.7060 TONNES

Total monthly oz gold served (contracts) so far this month

20,271 notices 2,027,100 63.048 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

customer withdrawals: 2

i) Out of Brinks: 8198.01 oz

ii) Out of Manfra: 6172.892 oz (192 kilobars)

Total withdrawals: 14,371.002 oz

total in tonnes: .446 tonnes

Adjustments: 2 dealer to customer account

a) Delaware; 1598.380 oz

b) Manfra 35,398.250 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR DECEMBER.

For the front month of DECEMBER we have an oi of 325 contracts having LOST 23 contracts

We had 81 contracts served on Monday, so we gained 58 contracts or an additional 5800 oz will stand for gold at the COMEX.

JANUARY LOST 15 contracts to stand at 1245

February LOST 3 contacts to 360,135

We had 98 notice(s) filed today for 9800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 98 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 28 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the DEC. /2022. contract month,

we take the total number of notices filed so far for the month (20,271 x 100 oz , to which we add the difference between the open interest for the front month of (DEC. 325 CONTRACTS) minus the number of notices served upon today 98 x 100 oz per contract equals 2,049,800 OZ OR 63.757 TONNES the number of TONNES standing in this active month of DEC.

thus the INITIAL standings for gold for the DEC contract month:

No of notices filed so far (20,271 x 100 oz+ (325 OI for the front month minus the number of notices served upon today (98} x 100 oz} which equals 2,049,800 oz standing OR 63.757 TONNES in this active delivery month of DEC..

TOTAL COMEX GOLD STANDING: 63.757 TONNES (A POOR STANDING//COMEX RUNNING OUT OF PHYSICAL TO SERVE UPON OUR LONGS.

To calculate the number of silver ounces that will stand for delivery in DEC. we take the total number of notices filed for the month so far at 3609 x 5,000 oz = 18,045,000 oz

to which we add the difference between the open interest for the front month of DEC(1068) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the DEC./2022 contract month: 3609 (notices served so far) x 5000 oz + OI for front month of DEC (1068 – number of notices served upon today (0) x 500 oz of silver standing for the DEC. contract month equates 23.385 million oz.. Also we have another criminal element to our silver oz standing, the use of Exchange for Risk/ Today an addition of 0 EFR contract transfers which are “Exchange for risk” settlements. I do not want to bore you but needless to say they are not physical transfers so are criminal in nature. There have been 2100 Exchange for Risk contracts settled during the first 3 days of the month for 10.500 million oz. Thus total delivery: 33.885 million oz.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

DEC 20/WITH GOLD UP $27.05: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES INTO THE GLD////INVENTORY RESTS AT 912.14 TONNES

DEC 19/WITH GOLD DOWN $2.10: HUGE CHANGES IN GOLD INVENTORY AT THE GLD> A BIG WITHDRAWAL OF 3.47 TONNES FROM THE GLD//INVENTORY RESTS AT 910.41 TONNES

DEC 16/WITH GOLD UP $12.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 15//WITH GOLD DOWN $31.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 911.56 TONNES

DEC 14/WITH GOLD DOWN $6.20: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 912.72 TONNES

DEC 13/WITH GOLD UP $32.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD///INVENTORY RESTS AT 910.41

DEC 12/WITH GOLD DOWN $17.60: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

DEC 9/WITH GOLD UP $8.90//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

Dec 8/WITH GOLD UP $4.05, OVER THE PAST 3 WEEKS WE LOST 2.04 TONNES//INVENTORY RESTS AT 908.09 TONNES

NOV 14/WITH GOLD UP $7.30: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 910.12 TONNES

NOV 11/WITH GOLD UP $15.25//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD////INVENTORY RESTS AT 911.57 TONNES

NOV 10/WITH GOLD UP $40.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.38 TONNES

NOV 9/WITH GOLD DOWN $2.00: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES INTO THE GLD////INVENTORY RESTS AT 908.38 TONNES

NOV 8/WITH GOLD UP $34.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.47 TONNES FROM THE GLD//: INVENTORY RESTS AT 905.49 TONNES

NOV 7/WITH GOLD UP $2.95: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.63 TONNES FROM THE GLD//INVENTORY RESTS AT 906.96. TONNES

NOV 4/WITH GOLD UP $44.45 TO $1673.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.48 TONNES FROMTHE GLD////INVENTORY RESTS AT 911.59 TONNES.

NOV 3/WITH GOLD DOWN $18.30 TO $1628.85: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.05 TONNES FROM THE GLD////INVENTORY RESTS AT 915.07 TONNES

NOV 2/WITH GOLD UP 55 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 919.12 TONNES.

NOV 1/WITH GOLD UP $9.20 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES FORM THE GLD../INVENTORY RESTS AT 920.57 TONNES

OCT 31/WITH GOLD DOWN $4.00; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD//INVENTORY RESTS AT 922.59. TONNES//

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

GLD INVENTORY: 912.14 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

DEC 20/WITH SILVER UP 105 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:: A DEPOSIT OF 700,000 OZ INTO THE SLV///INVENTORY RESTS AT 509.90 MILLION OZ//

DEC 19/WITH SILVER DOWN 13 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.05 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.20 MILLION OZ//

DEC 16/WITH SILVER UP 2 CENTS; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.85 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 508.15 MILLION OZ//

DEC 15/WITH SILVER DOWN 78 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF EXACTLY 2.00 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 510.000 MILLION OZ

DEC 14/WITH SILVER UP 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 512.000 MILLION OZ//

DEC 13/WITH SILVER UP 59 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 600,000 OZ FROM THE SLV////INVENTORY RESTS AT 513.900 MILLION OZ//

DEC 12/WITH SILVER DOWN 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 514.500 MILLION OZ//

DEC 9/WITH SILVER RISING 77 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.2 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 514.500 MILLION OZ.

DEC 8/WITH SILVER RISING 34 CENTS TODAY: OVER THE PAST 3 WEEKS, WE HAVE GAINED A STRONG: 44.777 MILLION OZ/INVENTORY RESTS AT 516.700 MILION OZ.

NOV 14/WITH SILVER UP 41 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 11/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ FROM THE SLV///INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 10/WITH SILVER UP 39 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 368,000 OZ INTO THE SLV///INVENTORY RESTS AT 472.476 MILLION OZ//

NOV 9/WITH SILVER DOWN 10 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV/; A WITHDRAWAL OF 3.821 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 472.108 MILLION OZ//

NOV 8/WITH SILVER UP 48 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.751 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 475.929 MILLION OZ//

NOV 7/WITH SILVER UP 12 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 4/WITH SILVER UP $1.31 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.972 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 3.WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 566,000 OZ FROM THE SLV////INVENTORY RESTS AT 482.650 MILLION OZ//

NOV 2/WITH SILVER DOWN 9 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 92,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.216 MILLION OZ//

NOV 1/WITH SILVER UP 53 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 415,000 OZ FORM THE SLV////INVENTORY RESTS AT 483.308 MILLION OZ

OCT 31: WITH SILVER FLAT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .644 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 483.723 MILLION OZ//

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: A WITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

CLOSING INVENTORY 509.90 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

end

LAWRIE WILLIAMS:

3. Chris Powell of GATA provides to us very important physical commentaries//

Jan is 100% correct: the west sets the price and gold moves west to east

(Jan Nieuwenhuis)

Jan Nieuwenhuijs: The West-East ebb and flow of gold revisited

Submitted by admin on Mon, 2022-12-19 20:24Section: Daily Dispatches

By Jan Nieuwenhuijs Gainesville Coins, Lutz, Florida Thursday, December 16, 2022

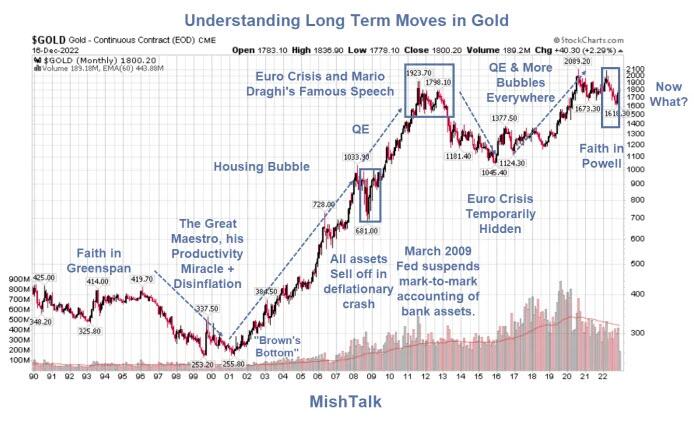

Gold trade between West and East still follows a 90-year-old pattern.

The price of gold is mainly set by Western institutional supply and demand, while countries in the East take the other side of the trade.

As a result, above-ground gold moves from West to East and back in sync with the price of gold decreasing and increasing. Knowledge of this pattern is imperative to understanding the gold market and the price of gold. …

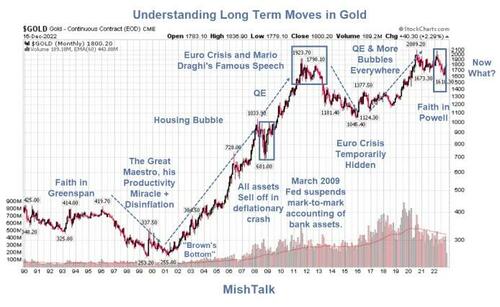

To understand what has happened and what is likely to happen, look at faith in the Fed and central banks in general…

A long-term chart suggests the real driver for gold is not inflation, not the dollar, not conspiracies, not China, and not oil, but rather faith in central banks.

Timeline Synopsis

Nixon closed the gold redemption window on August 15, 1971. The price of gold was $35 an ounce.

Faith in the dollar and central banks collapsed. Inflation soared.

Gold peaked at $850 per ounce on January 21 1980.

That’s when Fed Chair Paul Volcker jacked up interest rates to 20 percent to squash inflation.

Volcker was followed by Alan Greenspan, deemed the “Great Maestro”.

There was inflation every step of the way yet, gold fell from $850 an ounce to $250 an ounce proving gold is not an inflation hedge.

In the period between 1999 and 2002, Gordon Brown, UK Chancellor of the Exchequer (roughly the equivalent of the US Secretary of Treasury), sold off 395 tons of gold, showing great faith in fiat currencies over gold. This event is known as “Brown’s Bottom”.

To bail out banks that invested in worthless DotCom companies and also lost then huge amounts of money on bad loans to South American countries Greenspan recklessly lowered interest rates and held them too low too long.

Gold took off thanks to Fed stimulus that culminated in a housing bubble and bust.

Gold, like everything else sold off hard in that bust. In March of 2009, the Fed suspended mark-to-market accounting of bank assets. The stock market took off and so did gold.

The Fed launched QE and so did the ECB. Credit stress in the EMU was also brewing. There was a huge risk of the Eurozone would break apart. Greece was the weak link but fears were of a cascade if Greece left.

On 26 July 2012, the President of the European Central Bank, Mario Draghi, delivered a speech at a conference in London that brought a crucial turnaround in the euro crisis.

Mario Draghi said “Within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough.’

What did Mario Draghi do? The answer is amusing. Absolutely nothing. However, eurozone bond yield collapsed, temporarily saving the day.

In 2016 the Fed and ECB were both engaging in more QE and sovereign yields went negative in Europe and Japan. Gold blasted to a new high, double topping in 2021.

In 2022 the Fed finally got around to hiking. Gold started dropping hard in 2022 despite the fact that year-over-year inflation topped 9 percent. Once again this shows gold is a poor inflation hedge.

The Fed has kept up a steady stream of hawkish talk and here we are.

Fed’s Resolve

It was time to go to the gold sidelines when it was clear the Fed was about to go on a major hiking cycle.

I made a mistake in not believing the Fed’s resolve. By the time I did, I felt there was not much more downside.

Gold is up nearly $200 an ounce from the lows.

The Fed Projects Interest Rates Higher for Longer at Least Through 2023

Gold doesn’t seem to believe that although it did react poorly on the announcement.

Q: Can gold and Powell both be right? A: Yes, in a way.

Gold also reacts to credit stress. It soared following Nixon shock, in the housing bubble, and with QE.

It plunged under Greenspan disinflation and after Mario Draghi made his “Whatever it Takes Speech”

Meanwhile, the Fed seems hell bent on breaking something and I suspect they will.

Gold Weekly Support Levels

It’s possible gold is reacting to pending credit stress in the US, EU, China, or elsewhere. It’s possible that the $200 bounce is purely technical off strong support at $1650.

$1450 is also strong support. 1550 has moderate support. There is pretty strong resistance in a range $1850 to $1900.

If you believe the Fed will produce some uneventful soft landing with steady disinflation, gold may not be where you want to be.

Meanwhile, talk on Twitterland is of a new gold repricing model, of oil priced in gold, of yuan backed by gold, of 9 year cycles, and central bank buying gold was bearish then and bullish now, with price targets of $9,000. All that discussion seems more than a bit silly to me.

Finally, the lead chart shows gold is in a major 10-year cup and handle setup, normally a bullish formation. And typically, the longer the consolidation, the bigger the move when it happens.

The other side of the coin, as addressed in my previous post, is that bullish formations and support levels often fail in bear markets while resistance and bearish formations fail in bull markets.

That’s both sides of the gold case in one post without all the hype.

What About the Dollar?

Don’t fall into the trap of thinking gold always moves with the dollar. With the US dollar index at 90, gold has been at $250, $1,400, $1,200, and $600.

On a short term basis gold tends to move with the dollar, but sometimes, even for long periods of time, it doesn’t.

And while price correlation tends to be present, magnitude isn’t which is how you get $1,400 gold and $400 gold with the dollar index in the same place.

* * *

5. Commodity commentaries//IRON ORE

END

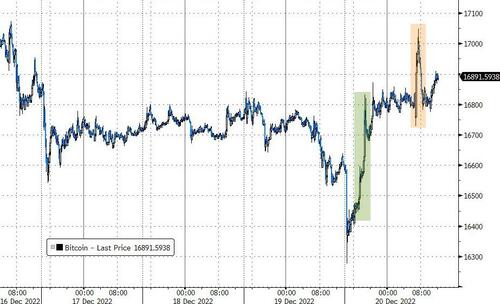

6/CRYPTOCURRENCIES/BITCOIN ETC

Special thanks to Robert H for sending this to us;

After weeks of speculation as to whether former billionaire, now hapless participant, Sam Bankman-Fried would be arrested for fraud surrounding FTX, the cryptocurrency exchange he ran into the ground, the mystery is over. The crypto exchange founder surrendered to Bahamian custody last week and is now awaiting extradition to the United States.

Following a grand jury indictment, Bankman-Fried was charged by the Southern District of New York, the Securities and Exchange Commission (SEC), and the Commodities and Futures Trading Commission (CFTC) on a variety of charges related to wire fraud, commodities fraud, securities fraud, money laundering, material misrepresentations, conspiracy to defraud the Federal Election Commission and to commit campaign finance violations.

The SEC alleges that Bankman-Fried orchestrated “a years-long fraud to conceal from FTX’s investors” the diversion of FTX customer funds to Alameda Research, a hedge fund owned by Bankman-Fried; the special treatment afforded to Alameda, such as unsecured and unlimited lines of credit; and FTX’s exposure to Alameda’s “significant holdings of overvalued, illiquid assets such as FTX-affiliated tokens.”

The SEC complaint also alleges that Bankman-Fried commingled FTX customers’ funds and used them to fund unrelated investments, purchase real estate, and make large political donations. The vast majority of these donations found their way into the coffers of the Democratic Party’s political machine, potentially impacting the outcome of 2022’s midterm elections. The CTFC filing further alleges that Bankman-Fried, FTX, and Alameda Research “caused the loss of over $8 billion in FTX customer deposits.”

The arrest brought to an ignoble end Bankman-Fried’s long-winded and pathetic apology tour, in which he claimed he had made mistakes of omission and negligence, for which he was deeply sorry, but had not committed fraud. The arrest came just one day before Bankman-Fried was to testify before the House Financial Services Committee, whose chair, Rep. Maxine Waters (D-Calif.), had deemed it “imperative” that Bankman-Fried appear. Shockingly, Rep. Waters had previously been seen offering Bankman-Fried a loving air kiss and wave of the hand following congressional testimony, in apparent gratitude for donations made to the cause.

The timing of the arrest—i.e., one languid month after the fraud had been revealed and FTX had collapsed, but then suddenly one day before his scheduled testimony—raised many eyebrows. Why wouldn’t the Department of Justice, the SEC, and the CFTC have been curious to hear what Bankman-Fried had to say? Most prosecuting attorneys would salivate at the prospect of Bankman-Fried tightening the noose around his own neck with the verbal rush that was sure to come forth in this public venue, especially considering what he’d already said in disdain of his lawyers’ and others’ advice to please quit talking and stop making it worse for himself and everyone he had harmed.

Some sober-minded legal commentators have speculated that the timing of the arrest was intended to prevent Bankman-Fried from doing just that, potentially including an alleged criminal and conspiratorial web that had been spun with leading members of the Democratic Party, to which Bankman-Fried fraudulently donated the vast majority of the $40 million in political contributions he made in this last election cycle. To be clear, this $40 million now appears to have been FTX customers’ money, not Bankman-Fried’s.

Eyes on the SEC

The SEC, or at least its chairman, Gary Gensler, may have also sought to avoid too much fuss being made over the several times that Gensler and his staff had met in consultation with Bankman-Fried to plot how to bring crypto regulation under SEC authority, in exchange for giving FTX special treatment which would put FTX ahead of its competitors.

In an apparent attempt to shift the narrative, Chairman Gensler said, “Sam Bankman-Fried built a house of cards on a foundation of deception while telling investors that it was one of the safest buildings in crypto.” He went on to warn all crypto platforms, wherever they may be domiciled, that they must come into compliance with U.S. laws. Fair enough. FTX was a fraud, and other crypto platforms should take notice.

Yet U.S. House Financial Services Committee member Rep. Tom Emmer (R-Minn.) lays much of the responsibility at Chairman Gensler’s feet, noting, “We need to get to the bottom of this. We need to understand why Gary Gensler and the SEC were not doing their job. We need to understand how this was allowed to get to the point where people and their savings are getting hurt. That’s exactly what the regulator’s supposed to be taking care of.”

The SEC has some explaining to do, true, but so do the numerous political actors within the Democratic Party who received and used stolen funds. A few have already sought to return the money or to donate it to charity. But these examples remain rare. Most recipients have remained silent amid the scandal, perhaps hoping it will all go away, forgotten amid some newer crisis or media’s and the public’s attention shifting elsewhere.

While we don’t yet have enough detailed information to run this to ground, the fraud which FTX appears to have perpetrated reaches into the highest orders of political power in this country. The scandal of FTX is an early domino to topple in what may be a long line of downfall, an exposure which likely is evidence of the vast corruption that may characterize the current political environment.

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//

TUESDAY MORNING.7:30 AM

ONSHORE YUAN: UP TO 6.9689

OFFSHORE YUAN: 6.9722

SHANGHAI CLOSED DOWN 33.35 PTS OR 1.07%

HANG SANG CLOSED DOWN 258.01 OR 1.33%

2. Nikkei closed DOWN 669.61 PTS OR 2.46%

3. Europe stocks SO FAR: MOSTLY MIXED

USA dollar INDEX DOWN TO 103.69 Euro RISES TO 106.33 UP 21 BASIS PTS

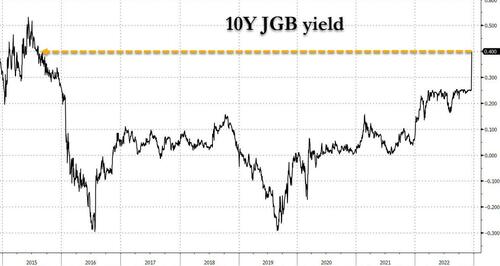

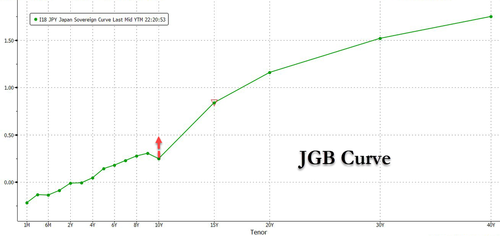

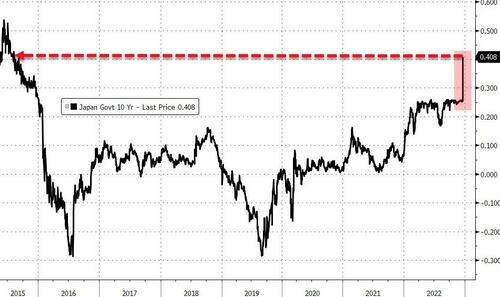

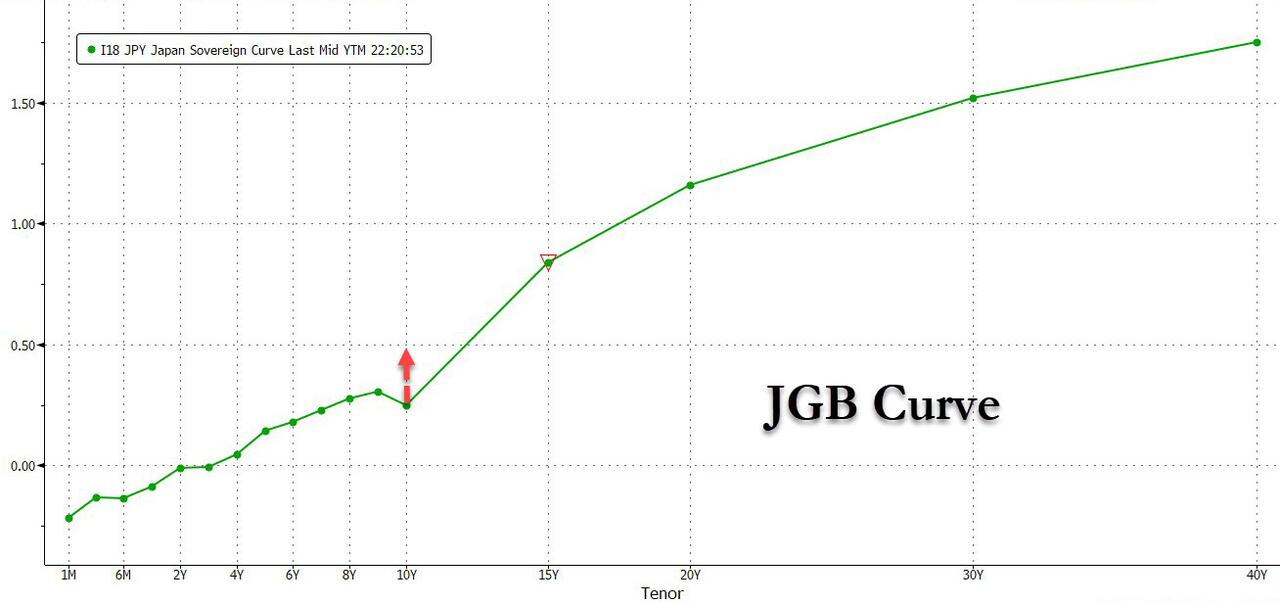

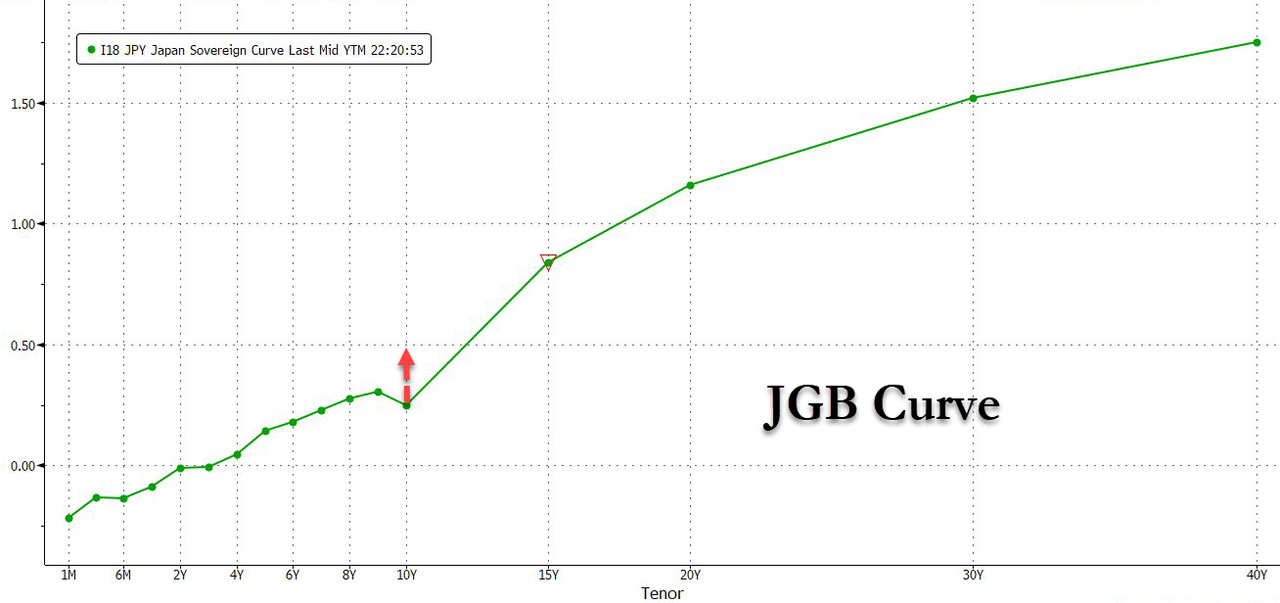

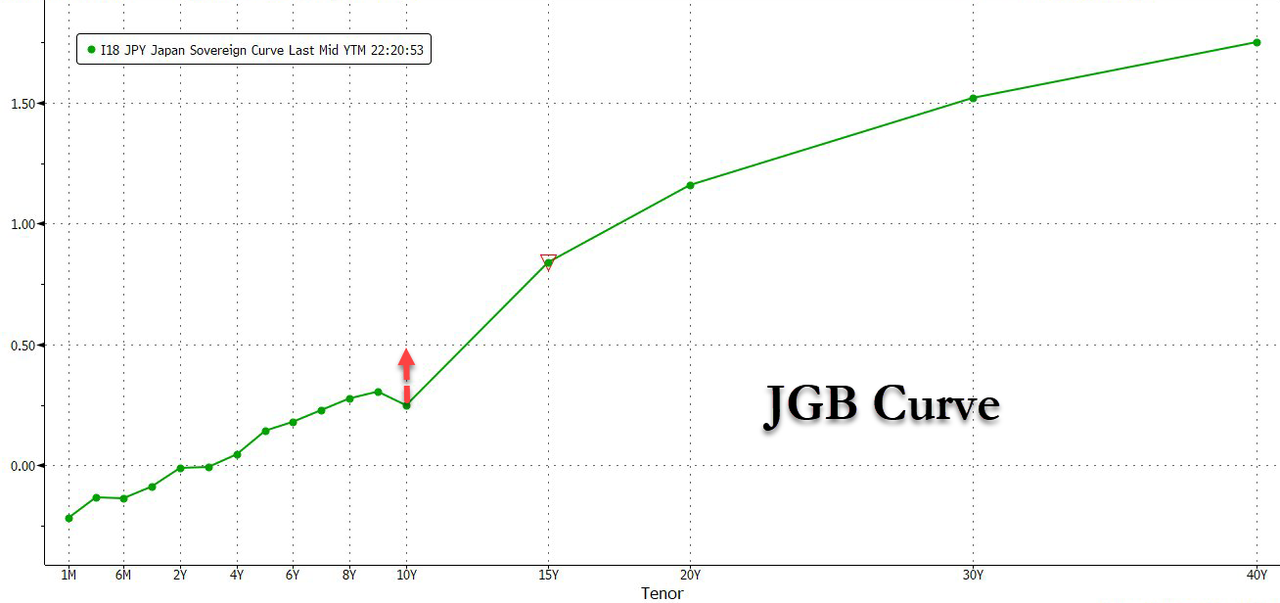

3b Japan 10 YR bond yield: RISES TO. +.395!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 132,53/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy the 9 TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.269%***/Italian 10 Yr bond yield RISES to 4.429%*** /SPAIN 10 YR BOND YIELD RISES TO 3.365…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.402//

3j Gold at $1801.60//silver at: 23.62 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 20/100 roubles/dollar; ROUBLE AT 68.92//

3m oil into the 76 dollar handle for WTI and 80 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 132.53

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9267–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9854 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

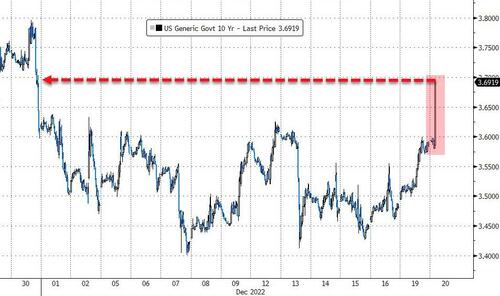

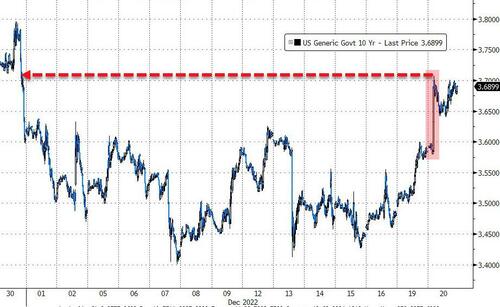

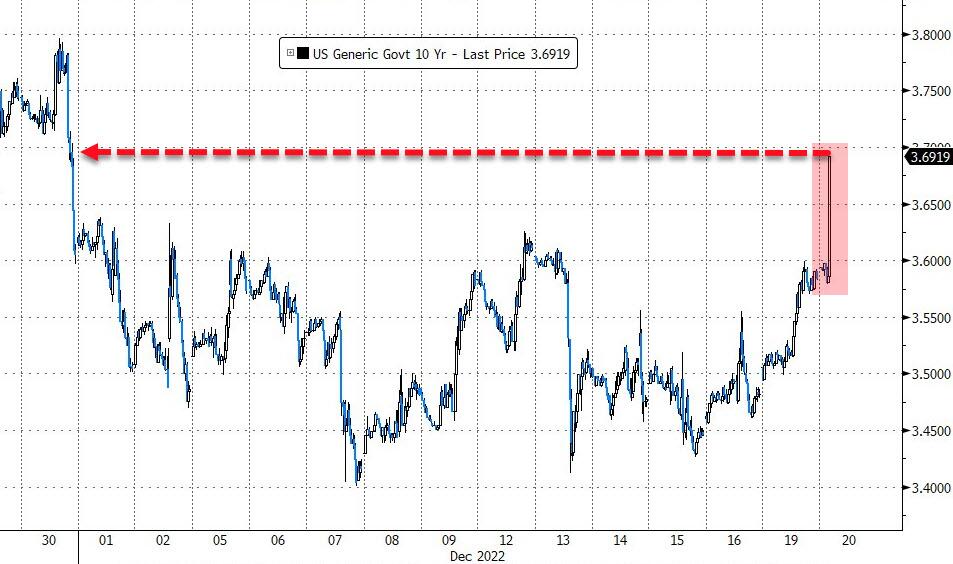

USA 10 YR BOND YIELD: 3.651% UP 7 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.708% UP 9 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,66…

GREAT BRITAIN/10 YEAR YIELD: 3.585 % UP 11 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

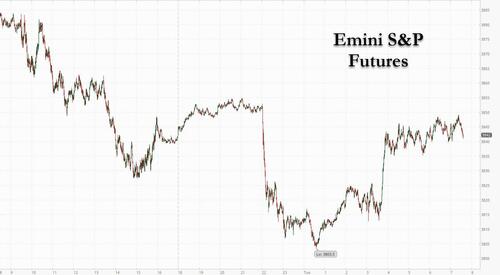

Futures Rebound From Post BOJ Shock As Dollar Tumbles

TUESDAY, DEC 20, 2022 – 08:08 AM

After last week’s CPI and FOMC decision, it was supposed to be smooth sailing into the illiquid, year-end waters as trading desks closed down for the year, and where among those few traders left some expected a Santa rally while others kept pressing their shorts. The BOJ – which was badly been lagging all of its central bank peers in tightening financial conditions – however had other plans, and on Tuesday morning Japan’s central bank shocked the world when it announced it would widen the Yield Control Curve band on the 10Y Treasury from 0.25% to 0.50% on either side, a move which had been viewed as a “when not if” – as markets knew the BoJ would eventually have to realign the “kinked” 10Y point with the rest of JGB curve and fundamentals…

… and begin a gradual policy alignment with rest of world’s already robust tightening, as they had instead continued to ease throughout ‘22 – but this was not seen as today’s business and virtually everyone expected this move to come after the Kuroda term ended in April ‘23, with most expecting a “phase-in” executed in smaller increments over time. So the news that the yield on Japan’s 10Y would be allowed to double from 0.25% to 0.50% came as a shock and sparked cross-asset contagion across the world, sending futures tumbling and bond yields soaring at least initially and briefly halted Japans’ treasury futures.

“Tighter BoJ policy would remove one of the last global anchors that’s helped to keep borrowing costs at low levels more broadly,”Deutsche Bank analysts told clients, noting the BOJ move had come as markets were “already reeling” from the ECB and Fed’s hawkishness last week.

BOJ governor Haruhiko Kuroda later reiterated at a press briefing that the widening of the yield band was aimed at improving market functioning and smoothing out a distorted yield curve. Still, the abrupt decision risks eroding confidence in the central bank’s messaging after the governor and other board members had repeatedly said a widening of the range would be tantamount to raising interest rates.

As attention turned away from the surge in yields -to the plunge in the dollar, US stock-index futures managed to recover most of their earlier losses, and as of 730am ET, contracts on the S&P 500 were flat while Nasdaq 100 futures slightly underperformed, falling 0.2% as the yield on 10-year Treasuries extended gains.

Contracts on the S&P 500 had slumped as much as 1.1% earlier after the BOJ’s move triggered concerns among investors already worried about the growing chorus of hawkish central banks: “There are some investors that are doing cross assets, and so if the yen moves — if the foreign exchange moves a lot — they automatically readjust” their equity futures positions, said Michael Makdad, an analyst at Morningstar Inc. in Tokyo.

But the move in stocks was actually relatively modest: the move in JGBs was more powerful, as the yield on 10Y bonds surged to the highest level since 2015…

… and dragged US TSYs along with it amid fears Japanese would be less willing to buy US paper (spoiler alert: the opposite will happen as local pensions start factoring in capital losses amid future YCC expansions) while the biggest fireworks took place in the world of FX, however, where the dollar tumbled as the yen rose: at one point the USDJPY plunged all the way down to 132.0 a 500+ pip move from where the pair was pre-BOJ, and the second biggest move in the past year, lagging only behind the shock US CPI miss repricing in November.

Among US premarket moves, Lucid Group advanced after the company said it has completed its stock sale program and successfully raised about $1.5 billion. Here are some of the biggest US movers today:

Verona Pharma (VRNA US) shares surge as much as 162% in US premarket trading after the drug developer achieved positive results in the Phase 3 ENHANCE-1 trial evaluating nebulized ensifentrine for the maintenance treatment of chronic obstructive pulmonary disease.

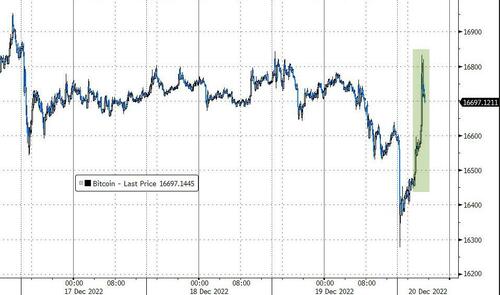

Cryptocurrency-exposed stocks rise as Bitcoin rebounds after falling to the lowest level this month as worries over the path of central bank policy damped moves across risky assets. Riot Blockchain (RIOT US) advances 1.6%, Marathon Digital (MARA US) +0.8%, Silvergate (SI US) +1.9%

MKS Instruments (MKSI US) stock rises 1.1% on low volumes after it was upgraded to overweight from sector weight at KeyBanc, with the broker saying the company’s strong competitive position should drive growth in semiconductor and advanced packaging.

Heico (HEI US) shares could be in focus as the aerospace parts manufacturer reported earnings per share for the fourth quarter that matched the average analyst estimate, but did not provide guidance for 2023.

Keep an eye on Conagra Brands (CAG US) stock as Morgan Stanley upgraded it to overweight, expecting the packaged-food sector to maintain its relative outperformance through 2023 and also raising J M Smucker (SJM US) to equal-weight.

Beam Therapeutics (BEAM US) is upgraded to outperform from market perform at BMO, which said that the risk/reward on the stock now seems skewed to the upside.

The insurance lead generation sector is JPMorgan’s favorite across small and mid-cap internet stocks for 2023, with analysts upgrading MediaAlpha (MAX US) to overweight from neutral, and EverQuote (EVER US) to overweight from underweight, while downgrading some advertising-exposed stocks.

Even before the BOJ, US stocks dropped for a fourth session on Monday as traders recoiled at the growing possibility that the Fed will push the US economy into a painful recession after central bank officials vowed to keep raising rates until they’re confident inflation is coming down meaningfully. The S&P 500 closed at its lowest level in more than a month, dragged by declines in big-tech firms including Apple, Microsoft and Amazon.com. As Bloomberg points out, US tech stocks are facing a big technical trial this week, with the Nasdaq 100 Index testing a long-term uptrend in place since 2008, based on a logarithmic scale and weekly data.

“The Fed now knows that the forward-looking indicators are starting to move in their favor,” Hugh Gimber, global market strategist at JPMorgan Asset Management, told Bloomberg Television. “They just want to see that coming through in hard data now and hence they want another few months just to get a clearer sense of the picture, but the direction of travel is much more positive.” Gimber expects a half-point hike when the Federal Open Market Committee meets in February, followed by a raise of 25 basis points in March.

European stocks also erased earlier losses, with the Stoxx 600 trading down -0.20% after tumbling more than 1% earlier. European real estate stocks underperformed; the Stoxx 600 Real Estate subindex drops 3.6% at 9:36 a.m. CET. Biggest laggards include Aroundtown -9.1%, Wihlborgs -4.5%, Balder -4.4%, LEG Immobilien -4.2%, Vonovia -4%, SBB -3.8%. Other notable European movers include:

Elior shares rise as much as 8.8% after the French caterer said it would buy Derichebourg Multiservices division by issuing new stock. The analysts noted that the equity-financed deal would add scale, boost margins and accelerate the company’s deleveraging.

Hugo Boss shares rise as much as 6% after Deutsche Bank analyst Michael Kuhn raised the recommendation to buy from hold.

Engie shares slumped as much as 6.9% after the French utility said it may take a hit of up to €5.7 billion ($6.1 billion) through next year from windfall taxes on soaring power sales and Belgium’s requirements for nuclear plant dismantling.

Credit Suisse shares decline as much as 3.9% as both Citi and RBC say the troubled lender needs to give greater visibility on its planned strategic overhaul for the stock to recover.

Petrofac shares drop as much as 10% to fresh record low as the energy infrastructure supplier predicts a full-year Ebit loss.

European real estate stocks underperformed on Tuesday after a hawkish move from the Bank of Japan, which adjusted its yield curve control program. Aroundtown is the sector’s biggest decliner, falling as much as 11%, after being downgraded to hold from buy at Berenberg.

Rheinmetall shares fall as much as 5.5% in Frankfurt, extending Monday’s losses, after German Defense Minister Christine Lambrecht set a deadline for the industry to fix defective infantry vehicles.

Kinepolis shares drop as much as 6.6%, the most in more than a month, after Berenberg lowers its price target and adopts a “more cautious” stance over its FY23/24 estimates.

Earlier in the session, Asian stocks fell as Japanese shares tumbled following a surprise policy tweak by the central bank, while China’s Covid disruptions also hurt sentiment. The MSCI Asia Pacific Index dropped as much as 1.1% before mostly trimming losses. The Nikkei 225 Index slumped 2.5% as the Bank of Japan raised the upper band limit of its yield curve control program, giving the yen a boost. Financial shares in the nation surged while tech and auto stocks slumped in Tokyo. “Usually the weak yen is good for the stock market earnings, and now if you have a stronger yen, it’s going to be a concern for the companies that were doing so well, mainly the exporters and maybe tourism,” said Peter Tasker, co-founder and strategist at Arcus Investment

“The whole Asian region is dragged down by BOJ’s new policy, which is triggering the short covering of yen,” said Steven Leung, executive director at UOB Kay Hian (Hong Kong) Ltd. “Those who borrow yen and invest in other securities” need to unwind positions, he added. Stocks in China and Hong Kong fell for the second day as the reopening rally continued to cool. China reported a pickup in Covid deaths, with analysts expecting the actual toll to be much worse than the official tally. Despite the dismantling of heavy Covid restrictions, activity in key cities has slowed as infections spike, diminishing the economic boost from a reopening. Investors are contending with slowdown risks in the region in 2023, with China’s path to reopening facing headwinds and doubts about the Fed’s ability to tackle inflation without pushing the US economy into a recession

In FX, the Bloomberg Dollar Spot Index was set a second day of losses as the greenback weakened against all of its Group-of-10 peers apart from the Australian and New Zealand dollars.

The yen rose by as much as 3.7%, to a four-month high of 132.06 per dollar, while the benchmark 10-year yield surged to 0.444%, the highest since 2015. The BOJ said it will now allow Japan’s 10-year bond yields to rise to around 0.5%, up from the previous limit of 0.25%; details here

Cross sales into yen hit the Aussie and kiwi with the latter already weakened after data showed business confidence in the nation slumped to a record low. Both Australia’s and New Zealand’s bonds also fell

The yuan flipped to a gain as the dollar weakened following the Bank of Japan’s hawkish shift. China’s loan prime rates were kept on hold, as expected.

In rates, Treasuries, bunds and gilts yields are off highs reached after BOJ’s yield pivot, though still up about 8 basis points each at the 10-year mark. Treasury futures off worst levels of the day, recouping a portion of losses into early US session after an aggressive cheapening move sparked by Bank of Japan widens the trading band on 10-year bond yields. Into peak selloff 10-year yields topped through 3.70% and onto cheapest levels since Nov. 30, before settling around 3.65% into the US session; the 2s10s spread remains wider by 5bp on the day after reaching steepest since Nov. 16. On outright basis Treasury yields remain cheaper by 1bp to 8.5bp across the curve in a bear steepening move, following wider selloff across JGBs where 10- year yields closed at 0.399% and 2s10s curve steepened 13bp on the day

In commodities, WTI trades within Monday’s range, adding 1.1% to near $75.98. Most base metals trade in the green. Spot gold rises roughly $19 to trade near $1,806/oz.

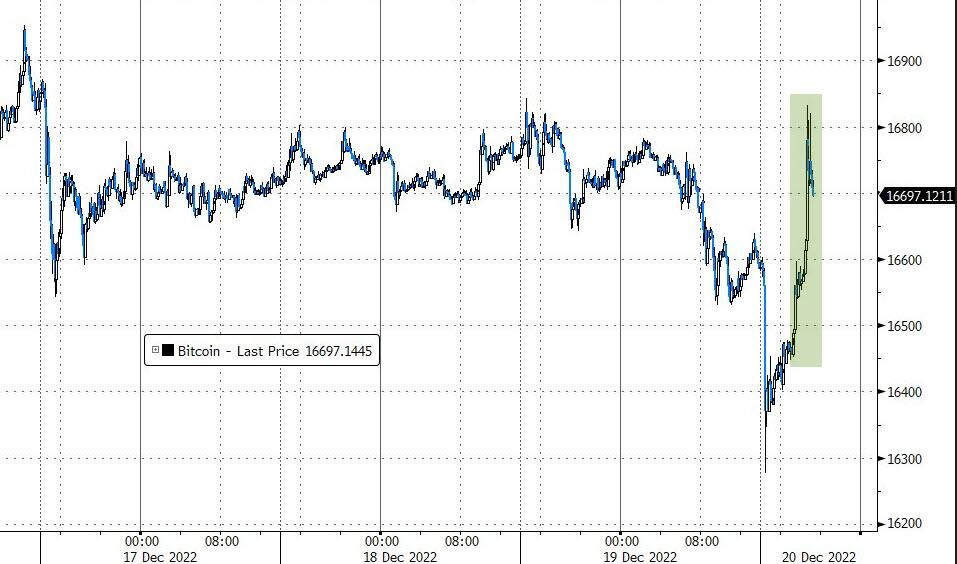

In crypto, Bitcoin is firmer to the tune of 1.0%, though once again remains within relatively narrow ranges.

To the day ahead now, and data releases include German PPI for November, US housing starts and building permits for November, and the European Commission’s advance December reading on consumer confidence for the Euro Area. Central bank speakers include the ECB’s Kazimir and Muller. Finally, earnings releases include Nike.

Market Snapshot

S&P 500 futures little changed at 3,842.50

STOXX Europe 600 down 0.4% to 424.16

MXAP little changed at 155.50

MXAPJ down 1.0% to 502.25

Nikkei down 2.5% to 26,568.03

Topix down 1.5% to 1,905.59

Hang Seng Index down 1.3% to 19,094.80

Shanghai Composite down 1.1% to 3,073.77

Sensex down 0.2% to 61,653.10

Australia S&P/ASX 200 down 1.5% to 7,024.27

Kospi down 0.8% to 2,333.29

German 10Y yield little changed at 2.27%

Euro up 0.2% to $1.0632

Brent Futures up 0.6% to $80.29/bbl

Gold spot up 0.9% to $1,804.50

U.S. Dollar Index down 0.73% to 103.96

Top Overnight News from Bloomberg

The BOJ’s surprise policy shift is sending shock waves through global markets that may just be getting started, as the developed world’s last holdout for rock-bottom interest rates inches toward policy normalization

The BOJ’s latest policy shock is cementing the central bank’s reputation for using the element of surprise to achieve its strategic goals

At least three funds stand to benefit from Japan’s policy move: UBS Asset Management, Schroders Plc and BlueBay Asset Management

ECB Governing Council member Francois Villeroy de Galhau said the euro-zone economy is unlikely to experience a deep slump as interest rates are lifted to tackle soaring inflation

The ECB remains “a long way” from achieving its goal of inflation of 2% over the medium term, according to Governing Council Member and Bundesbank President Joachim Nagel

South African President Cyril Ramaphosa emerged from a ruling party electoral conference with a stronger mandate, yet still has to overcome a series of political hurdles to tackle a daunting economic to-do list

Hong Kong will further ease social distancing measures, including rules on banquets, ahead of a trip by the city’s leader to Beijing

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks traded lower across the board with the broader risk profile hit by the BoJ’s unexpected tweak to its Yield Curve Control. Nikkei 225 fell over 2.5% as it reacted to the BoJ’s move, with the index briefly dipping under 26,500, although bank stocks soared. ASX 200 was dragged lower by its Tech and IT sectors whilst Banks and Utilities were the better performers. Hang Seng and Shanghai Comp conformed to the downbeat tone across the equity market, with the former seeing its housing stocks slip after the PBoC opted to maintain its 5yr LPR unchanged vs some expectations for a cut.

Top Asian News

RBA Minutes (Dec): Board considered several options for the cash rate decision at the December meeting: a 50bps increase; a 25bps increase; or no change in the cash; members also noted the importance of acting consistently. The Board did not rule out returning to larger increases if the situation warranted. Click here for the detailed headline

PBoC maintained the 1yr and 5yr Loan Prime Rates (LPRs) at 3.65% and 4.30% respectively, as expected, according to Bloomberg.

BoK Governor said the board believes it is premature to cut rates. BoK said consumer inflation is to gradually slow after hovering around 5% for some time; uncertainty is high over how swiftly consumer inflation will slow, according to Reuters. BoK Governor said the risk of USD/KRW rate surging at an unusual pace has decreased.

China reports five COVID-related deaths in the mainland on Dec 19 vs two a day earlier, according to Reuters.

Hong Kong Chief Executive Lee said Hong Kong will further ease social distancing measures, according to Bloomberg; subsequently, Hong Kong Health Authorities are to drop the rapid antigen COVID test requirement to enter bars/nightclubs from Thursday, no capacity limit on such venues.

Japan is reportedly mulling issuing JPY 500bln of green transformation economic transition bonds (GX bonds) in FY23, according to Japanese press Yomiuri.

Japanese government reportedly looking to issue around JPY 35.5tln of new JGBs for FY23/24, according to Reuters sources.

PBoC injected CNY 5bln via 7-day reverse repos with the rate maintained at 2.00%; injects CNY 141bln via 14-day reverse repos with the rate maintained at 2.15%; daily net injection CNY 144bln.

European bourses are under modest pressure, Euro Stoxx 50 -0.3%, as the complex lifts off post-BoJ lows in limited newsflow. US futures are moving in tandem with the above, ES -0.1%, ahead of a handful of stateside data prints. JPMorgan lowers its Apple (AAPL) iPhone volume forecasts for the December quarter to around 70mln (prev. forecast ~74mln).

Top European News

ECB’s Kazimir Says Stable Pace of Tightening Should Continue

Spain Court Foils Sánchez Bid to Name Judges in Power Clash

Engie Drops as Taxes, Nuclear Rules Take Multibillion Euro Bite

Swedish Property Stocks End Brutal 2022 With Tough Reset Ahead

Germany Cuts Russian Share in Gas Use by More Than Half in 2022

FX

JPY is the standout outperformer after the BoJ widened the 10yr yield band, sending USD/JPY to a test of 132.00 vs 137.00+ initial levels.

Amidst this, the DXY has been pushed below 104.00 to the modest benefit of G10 peers across the board.

Though, the read across from the USD’s downside to peers is being hampered somewhat by the pronounced action in JPY-crosses.

Elsewhere, antipodeans are the incremental laggards following the ANZ survey and post-RBA minutes, which has a dovish tilt.

PBoC sets USD/CNY mid-point at 6.9861 vs exp. 6.9862 (prev. 6.9746)

Fixed Income

Benchmarks have bounced from BoJ induced worst levels with modest assistance from German PPI and UK supply.

However, core debt is lower by around 100 ticks for Bunds and Gilts, with the German 10yr approaching 2.3% at best.

Stateside, USTs are directionally in-fitting though magnitudes are slightly more contained ahead of the US session, yields bid across the curve and bear-steepening.

Geopolitics

North Korea said Japan’s counterattack capabilities are effectively pre-emptive strike capabilities; said Japan’s new security strategy is bringing security crisis in the region. North Korea said it has the right to take “decisive” military measures to protect its rights in response to the changing security environment, via KCNA.

BOJ

STATEMENT

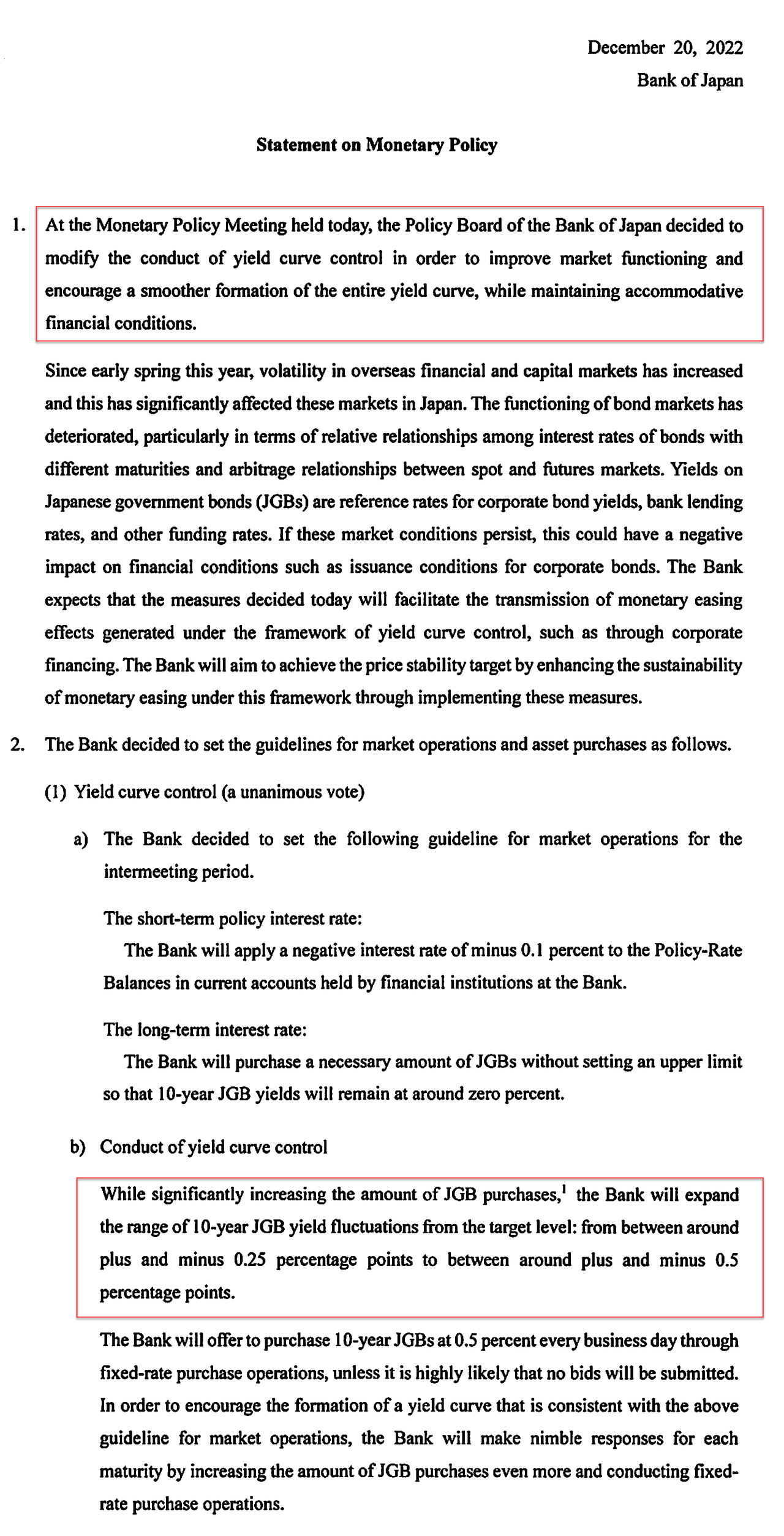

BoJ unexpectedly tweaked its Yield Curve Control (YCC) in which it widened the 10yr yield band to +/-0.5% (prev. +/-0.25%) and unexpectedly announced it is to increase bond purchases to JPY 9tln/m (prev. JPY 7.3tln/m) in Q1. The BoJ kept its rate unchanged at -0.10% and maintained 10yr JGB yield target of around 0% as expected. The decision on the YCC was unanimous. The adjustment is intended to “improve market functioning and encourage a smoother formation of the entire yield curve while maintaining accommodative financial conditions,” the central bank said. BoJ said it is to make nimble responses for each maturity by increasing the amount of purchases even more and conducting fixed-rate purchases operations when deemed necessary. BoJ maintained its rate guidance. Click here for the detailed headline

GOVERNOR KURODA

YCC:

Market functionality was decreasing. Domestic market has been hit by volatility abroad. Decision was made today as deteriorating market functions could threaten corporate financing.

Decision is not an exit of YCC or a change in policy, appropriate to continue easing policy.

There is no need to further expanding the allowance band, not likely that the market calls for another increase of the yield cap maximum limit.

Broader Policy:

It is too early to debate the exit to current monetary policy; today’s decision is not a rate hike.

Won’t hesitate to ease monetary policy further if necessary.

No intention to hike rates or tighten policy. Not thinking about revising the 2013 gov’t-BoJ joint statement.

OTHER

BoJ announced an unscheduled bond operation: BoJ offered to buy JPY 100bln in up to 1-3yr JGBs, JPY 100bln in 3-5yr JGBs, JPY 300bln in 5-10yr JGBs and JPY 100bln in 10-25yr, according to Reuters. BoJ to conduct unlimited bond buying in the 1-5yr tenors, according to Bloomberg.

Japanese Finance Minister Suzuki said it is not true that the government and the BoJ have decided on a policy to revise its joint statement, according to Reuters.

Japanese Economy, Trade, and Industry Ministry Nishimura said it is important to continue carrying out economic revitalisation based on the joint statement with the BoJ, according to Reuters.

Japan Securities Clearing Corporation has issued an emergency margin call re. JGB futures.

Commodities

Crude benchmarks slipping in tandem with broader sentiment initially and in the hours since have pared this pressure and are now posting upside just shy of USD 1.0/bbl.

Currently, Dutch TTF Jan’23 remains under modest pressure, but is yet to slip below the EUR 100/MWh mark.

Germany’s BDEW (energy industry association) says it is concerned about the EU gas price cap, it needs monitoring and adjusting if results in too little gas reaching Europe.

The yellow metal is a handful of ounces above the USD 1800/oz handle while base metals are firmer in action that is for the most part in-fitting with the above risk tone/dynamics.

US Event Calendar

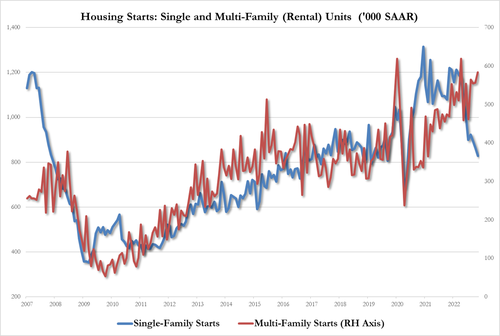

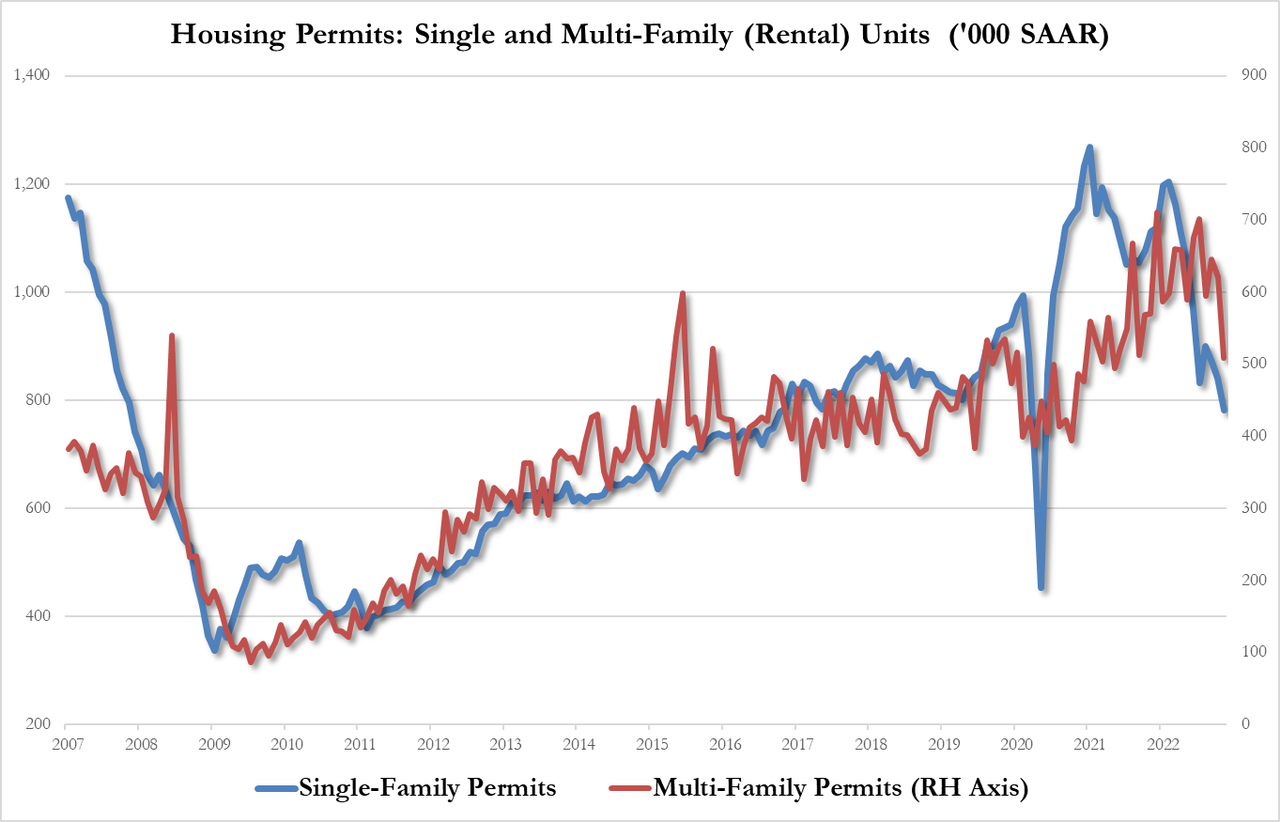

08:30: Nov. Building Permits MoM, est. -2.1%, prior -2.4%, revised -3.3%

08:30: Nov. Building Permits, est. 1.48m, prior 1.53m, revised 1.51m

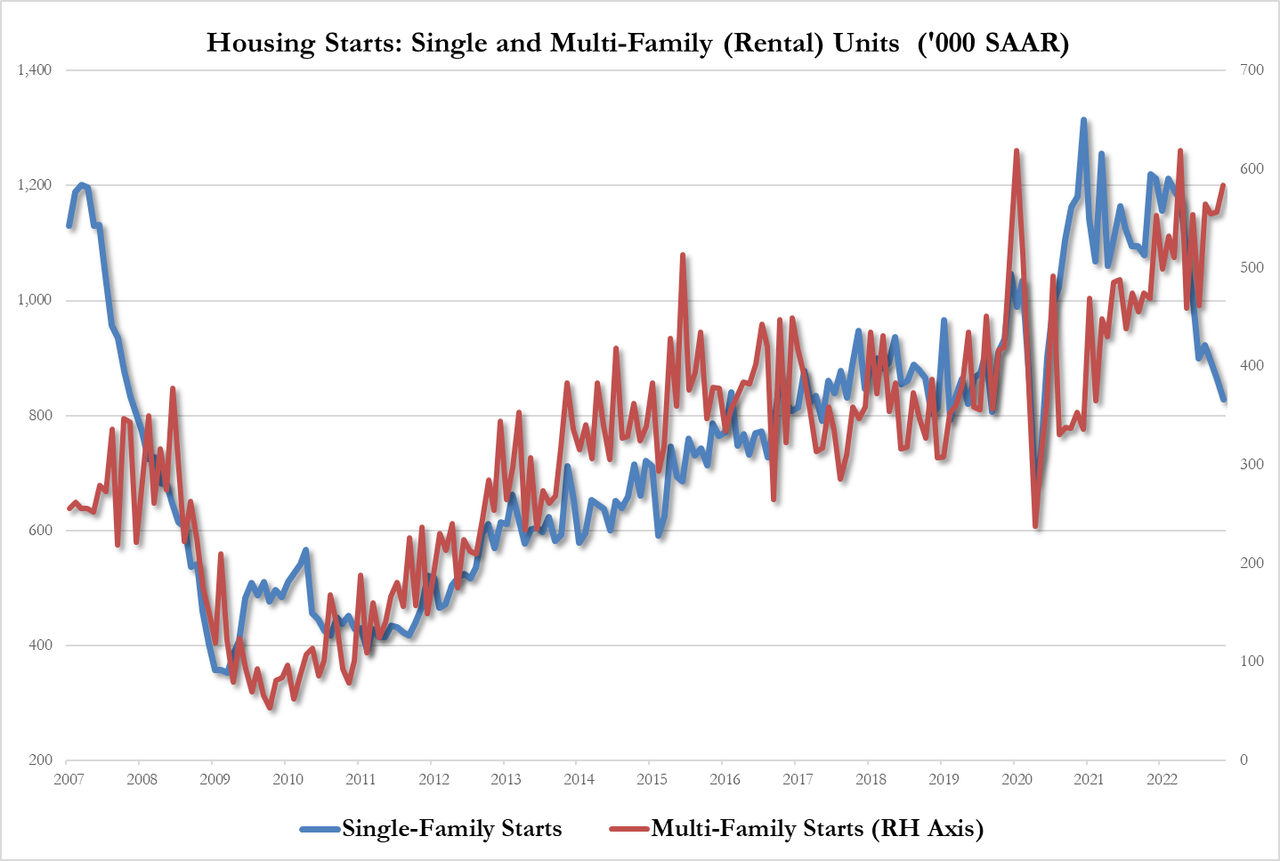

08:30: Nov. Housing Starts MoM, est. -1.8%, prior -4.2%

08:30: Nov. Housing Starts, est. 1.4m, prior 1.43m

DB’s Jim Reid concludes the overnight wrap

We go to press this morning amidst big moves in global markets overnight, since the Bank of Japan have decided to adjust their yield-curve-control policy, which is widely seen as the beginning of a potential end to their ultra-loose monetary policy. That policy has made them a big outlier compared to other central banks this year, having maintained rates at the zero lower bound whilst others embarked on their biggest tightening cycle in a generation. Indeed, it’s important not to underestimate the impact this could have, because tighter BoJ policy would remove one of the last global anchors that’s helped to keep borrowing costs at low levels more broadly.

In terms of the policy shift, the BoJ announced in a surprise move that Japan’s 10yr yield would now be able to rise to around 0.5%, having been limited to 0.25% previously. In turn, that led to a massive slump in Japanese equities, with the Nikkei down by -2.88% this morning, and those moves lower have been echoed more broadly. Indeed, not only are other indices in Asia pointing lower, including the CSI 300 (-1.64%), the Shanghai Comp (-1.03%), the Hang Seng (-2.19%) and the Kospi (-1.10%), but futures on the S&P 500 are currently down -1.07%, even after a run of 4 consecutive declines for the index already. The one big exception to this pattern of equity losses were bank stocks, with those in the Nikkei surging +4.96% this morning given the potential move away from ultra-low borrowing costs.

Unsurprisingly, Japanese government bond yields have surged on the back of the announcement, with the 10yr yield up +15.5bps this morning to 0.41% after trading around 0.25% for months. But the impact hasn’t been confined there either, with Australian 10yr yields up +19.5bps this morning, and those on US 10yr Treasuries up +8.1bps to 3.666%. In the meantime, the yen has strengthened massively, gaining +2.75% against the US Dollar this morning to 133.22 per dollar.

Even before the BoJ’s overnight announcement, markets had already got the week off to a rough start yesterday, with the bond selloff showing no sign of letting up whilst the S&P 500 (-0.90%) lost ground for a fourth day running. The moves were very similar to last week’s in many respects, with investors continuing to grapple with the prospect that central banks will keep hiking rates into 2023, not least after the hawkish tone from their recent meetings. That theme is only going to be bolstered by the BoJ’s move, which came as a big surprise to markets that were already reeling from the ECB and Fed’s hawkishness last week.

Whilst many investors are still expecting we could get a dovish pivot later in 2023, markets aren’t banking on that for now, with sovereign bonds seeing fresh losses on both sides of the Atlantic yesterday. In terms of the daily moves, yields did come off their highs by the end of the session in Europe, but those on 10yr bunds (+5.1bps), OATs (+4.4bps) and BTPs (+8.5bps) were still noticeably higher by the close. We also saw another round of milestones at the front-end of the curve as well, since yields on 2yr German and French debt both hit their highest levels since 2008. That followed further hawkish rhetoric from ECB speakers over the last 24 hours, with a nod to rate hikes continuing at a 50bps pace. For instance, Vice President de Guindos said that they had “to take additional measures to increase interest rates at a speed similar to that of this last 50 basis-point increase”. In the meantime, Lithuania’s Simkus said he had “no doubt” there’d be another 50bp move in February, and Slovakia’s Kazimir said that “we need to increase the base interest rate significantly higher than today.”

Whilst the continued bond selloff very much echoed last week, one key difference yesterday was that Eurozone bonds were no longer underperforming their international counterparts. For instance, yields on 10yr Treasuries saw a much larger increase on the day of +10.2bps to 3.585%, before their latest moves to 3.666% overnight. Higher real yields led that move yesterday, with the 10yr real yield up +7.2bps to 1.42%, followed by a further move to 1.45% this morning meaning that it’s now risen by over +40bps since its recent closing low earlier this month. And over in the UK, yields saw an even larger increase yesterday, with 10yr gilt yields up +17.3bps on the day to 3.50%. Those moves came as investors moved to price in a slightly more hawkish path for central bank policy rates, with pricing for the Fed’s rate by end-2023 up +5.5bps on the day to 4.413%.

This backdrop of growing concern about the rates outlook proved further bad news for equities, and the S&P 500 (-0.90%) fell to its lowest level in nearly 6 weeks. That’s its 4th consecutive decline, and means that in less than a week since the S&P briefly surged after the downside CPI surprise, the index has now lost -6.91% since its intraday peak. In terms of the drivers, tech stocks were a major contributor, with the NASDAQ (-1.49%) and the FANG+ index (-2.02%) seeing sizeable declines, although the Dow Jones didn’t fare so badly with a -0.49% decline. Europe was also a relative outperformer, with the STOXX 600 seeing a modest +0.27% gain after its -3.28% decline last week.

Elsewhere yesterday, we heard that EU member states had reached a deal to cap gas prices at €180 per megawatt-hour. It’ll apply for a year starting February 15, and follows lengthy negotiations on where the cap should be, with an earlier proposal from the Commission suggesting a €275/MWh level. The cap will also only apply if the difference with global liquefied natural gas prices is bigger than €35/MWh. Against this backdrop, European natural gas futures were down -5.98% yesterday to €109 per megawatt-hour.

On the data side yesterday, we got further evidence that the European economy was outperforming expectations this winter, with the Ifo’s business climate indicator from Germany rising to 88.6 (vs. 87.5 expected), marking its highest level in 4 months. However in the US, the NAHB’s latest housing market index showed that the housing market was continuing to struggle, with a decline in December to 31 (vs. 34 expected). With the exception of April 2020, that’s the index’s lowest reading in over a decade, and means that it’s fallen in every single month over 2022.

Finally, the US Congress are focusing on concluding their 2023 fiscal year omnibus budget package, ahead of the government funding deadline at the end of the week. Senate Minority Leader McConnell said that he expects to review the full text soon and signalled that there would be ample GOP support, indicating there would not be a period of protracted debate with the White House. The provisions are expected to total close to $1.7tr, and include funding for border security, state aid for natural disasters, a realigning of pandemic-era programs, and aid to Ukraine amongst a host of other initiatives and programs. Notably, it does not appear that there will be an increase to the debt ceiling in this agreement, so that’s another event that looks as though it could get some attention in 2023, particularly given the Republicans will control the House of Representatives next year.

To the day ahead now, and data releases include German PPI for November, US housing starts and building permits for November, and the European Commission’s advance December reading on consumer confidence for the Euro Area. Central bank speakers include the ECB’s Kazimir and Muller. Finally, earnings releases include Nike.

AND NOW NEWSQUAWK (EUROPE/REPORT)

JPY outperforms while core debt slumps post-BoJ’s unexpected action – Newsquawk US Market Open

TUESDAY, DEC 20, 2022 – 06:38 AM

European bourses are under modest pressure, Euro Stoxx 50 -0.3%, as the complex lifts off post-BoJ lows in limited newsflow.

JPY is the standout outperformer after the BoJ widened the 10yr yield band, sending USD/JPY to a test of 132.00 vs 137.00+ initial levels.

DXY has been pushed below 104.00 to the modest benefit of G10 peers across the board; though, JPY-cross action is limiting this.

Core debt has bounced from worst levels, though remains heavily hampered with yields bid and the curve steepening.

Crude has recovered from its initial downside, currently posting modest upside; Dutch TTF cools as we await ICE’s review

Looking ahead, highlights include Canadian Retail Sales, US Building Permits, EZ Consumer Confidence.

Benchmarks have bounced from BoJ induced worst levels with modest assistance from German PPI and UK supply.

However, core debt is lower by around 100 ticks for Bunds and Gilts, with the German 10yr approaching 2.3% at best.

Stateside, USTs are directionally in-fitting though magnitudes are slightly more contained ahead of the US session, yields bid across the curve and bear-steepening.

Crude benchmarks slipping in tandem with broader sentiment initially and in the hours since have pared this pressure and are now posting upside just shy of USD 1.0/bbl.

Currently, Dutch TTF Jan’23 remains under modest pressure, but is yet to slip below the EUR 100/MWh mark.

Germany’s BDEW (energy industry association) says it is concerned about the EU gas price cap, it needs monitoring and adjusting if results in too little gas reaching Europe.

The yellow metal is a handful of ounces above the USD 1800/oz handle while base metals are firmer in action that is for the most part in-fitting with the above risk tone/dynamics.

ECB’s Villeroy says France should be able to avoid a recession, any recession would be temporary.

ECB’s Vasle says the economic slowdown won’t notably ease inflation.

ECB’s Muller says rate hikes so far are not enough; hard to say what the terminal rate should be.

ECB’s Kazimir says monetary policy should tighten at a stable pace

NOTABLE DATA

German Producer Prices YY (Nov) 28.2% vs. Exp. 30.6% (Prev. 34.5%); MM (Nov) -3.9% vs. Exp. -2.5% (Prev. -4.2%)

NOTABLE US HEADLINES

Steel Dynamics (STLD) is to replace ABIOMED (ABMD) in the S&P 500 effective prior to the market open on December 22nd, according to S&P Dow Jones Indices.

US Congress’ USD 1.7tln FY23 funding bill has been introduced; 885bln for defense, 772bln for non-defense discretionary spending; lawmakers incl. Boeing (BA) 737 Max certification extension and USD 2bln for Taiwan weapons purchases within the proposed funding bill.

6.3 magnitude earthquake occurs in the northern California regions, via USGS.

GEOPOLITICS

North Korea said Japan’s counterattack capabilities are effectively pre-emptive strike capabilities; said Japan’s new security strategy is bringing security crisis in the region. North Korea said it has the right to take “decisive” military measures to protect its rights in response to the changing security environment, via KCNA.

CRYPTO

Bitcoin is firmer to the tune of 1.0%, though once again remains within relatively narrow ranges.

APAC TRADE

BOJ

STATEMENT