jan 26 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSED: DOWN $11.55 at $1930.00

SILVER PRICE CLOSED: UP $0.08 to $23.92

TODAY IS OPTIONS EXPIRY ON THE COMEX AND THUS THE REASON FOR THE RAID.

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1929.15

Silver ACCESS CLOSE: 23.90

Bitcoin morning price:, 23091 UP 179 DOLLARS

Bitcoin: afternoon price: $23,126 UP 144 dollars

Platinum price closing $1021.90 DOWN $21.00

Palladium price; closing 1676.20 DOWN $26.40

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,570.10 DOWN $36.91 CDN dollars per oz

BRITISH GOLD: 1553.83 DOWN 16.01 pounds per oz

EURO GOLD: 1771.14 DOWN 12.86 euros per oz

EXCHANGE: COMEX

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JANUARY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,941.200000000 USD

INTENT DATE: 01/25/2023 DELIVERY DATE: 01/27/2023

FIRM ORG FIRM NAME ISSUED STOPPED

624 H BOFA SECURITIES 1

737 C ADVANTAGE 1

TOTAL: 1 1

MONTH TO DATE: 6,328

JPMorgan stopped 10/243

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR JAN/2023. CONTRACT: 1 NOTICES FOR 100 OZ or 0.00311 TONNES

total notices so far: 6328 contracts for 632,800 oz (19.6827 tonnes)

SILVER NOTICES: 12 NOTICE(S) FILED FOR 60,000 OZ/

total number of notices filed so far this month : 1012 for 5060,000 oz

END

GLD

WITH GOLD DOWN $11.55

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

//HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD //

INVENTORY RESTS AT 919.37 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 8 CENTS

AT THE SLV// :/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE DEPOSIT OF 0.9 MILLION OZ INTO THE SLV//// WHAT A MASSIVE FRAUD!!!

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 521.9 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

IN THE LAST THREE DAYS: A GAIN OF 23.2 MILLION OZ (WHERE ON EARTH WERE THEY GOING TO GET THAT QUANTITY OF METAL)

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 168 CONTRACTS TO 135,090 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE FAIR GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.19 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. FOR THE PAST MONTH, OUR BANKERS HAVE RETURNED TO BEING NET SHORT AND THUS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.19. AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 639 CONTRACTS. AS WELL, WE HAD 0 NOTICES FOR EXCHANGE FOR RISK TRANSFER (0 OZ. ) AS THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 7.25 MILLION OZ. WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS( 329 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4,055. MILLION OZ FOLLOWED BY TODAY’S QUEUE. JUMP OF 60,000 OZ//NEW STANDING 5.065 MILLION OZ + 7.25 MILLION OF EXCHANGE FOR RISK//TOTAL STANDING 12.315 MILLION OZ//// V) FAIR SIZED COMEX OI GAIN/ FAIR EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –142

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTRACTS for 17 days, total 9669 contracts: OR 48.345 MILLION OZ PER DAY. (569 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 48.345 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 48.345 MILLION OZ

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 168 WITH OUR $0.19 GAIN IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 329 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN OF 4.055 MILLION OZ FOLLOWED BY TODAY’S 60,000 OZ. JUMP / //NEW STANDING RISES TO 5.065 MILLION OZ + EFR 7.25 MILLION = 12.315 MILLION OZ. .. WE HAVE A FAIR SIZED GAIN OF 497 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 12 NOTICE(S) FILED TODAY FOR 60,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 7141 CONTRACTS TO 507,068 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -4568 CONTRACTS.

.

WE HAD A STRONG SIZED INCREASE IN COMEX OI ( 7141 CONTRACTS) WITH OUR STRONG $7.55 GAIN IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR JAN. AT 2.1710 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 1 CONTRACTS OR 100 OZ //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). NEW STANDING 20.2301 TONNES

YET ALL OF..THIS HAPPENED WITH OUR $7.55 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A VERY STRONG SIZED GAIN OF 12,172 OI CONTRACTS (37.86 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5031 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 507,068

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,172 CONTRACTS WITH 7141 CONTRACTS INCREASED AT THE COMEX AND 5031 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 12,172 CONTRACTS OR 37.86 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5031 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (7141) TOTAL GAIN IN THE TWO EXCHANGES 12,172 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) SMALL INITIAL STANDING AT THE GOLD COMEX FOR JAN. AT 2.1710 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 100 OZ /NEW STANDING 20.2301 TONNES///3) ZERO LONG LIQUIDATION //4) VERY STRONG SIZED COMEX OPEN INTEREST GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN :

66,695 CONTRACTS OR 6,669,500 OZ OR 207.449 TONNES 17 TRADING DAY(S) AND THUS AVERAGING: 3923 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES:207.449 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 207.449/3550 x 100% TONNES 5.85% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 207.449 TONNES INITIAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A SMALL SIZED 168 CONTRACTS OI TO 135,090 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 329 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 329 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1219 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 168 CONTRACTS AND ADD TO THE 329 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GOOD SIZED GAIN OF 497 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 2.485 MILLION OZ//

OCCURRED WITH OUR 19 CENT GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//CORN

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)THURSDAY MORNING//WEDNESDAY NIGHT

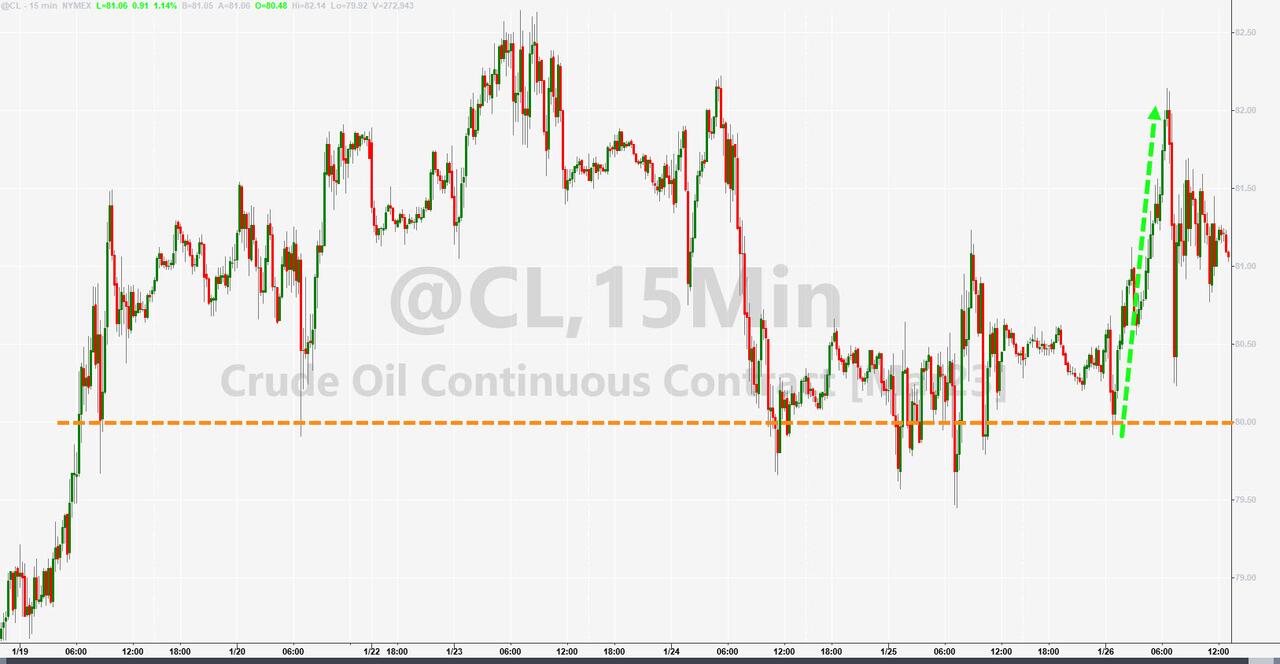

SHANGHAI CLOSED //Hang Seng CLOSED /The Nikkei closed UP 32.26 PTS OR 0.12% //Australia’s all ordinaries CLOSED DOWN 0.29% /Chinese yuan (ONSHORE) closed //OFFSHORE CHINESE YUAN UP TO 6.7408// /Oil UP TO 81.23 dollars per barrel for WTI and BRENT AT 87.34 / Stocks in Europe OPENED ALL GREEN ONSHORE YUAN TRADING XXXX LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING UP AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 7141 CONTRACTS UP TO 507,068 WITH OUR GAIN IN PRICE OF $7.55

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON-ACTIVE DELIVERY MONTH OF JAN… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5031 EFP CONTRACTS WERE ISSUED: ;: , . 0 FEB: 5031 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5031 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 12,172 CONTRACTS IN THAT 5031 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI GAIN OF 7141 CONTRACTS..AND THIS VERY STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR ADVANCE IN PRICE OF $7.55. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG .

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING Jan (20.2301)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes(TOTAL THIS YEAR 656.076 TONNES

JAN/2023: 20.2301 tonnes

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $7.55) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A VERY STRONG GAIN OF 12,172 CONTRACTS ON OUR TWO EXCHANGES // WE HAVE GAINED A TOTAL OI OF 52.068 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JAN. (2.1710 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 100 oz OR 0.00311 TONNES… ALL OF THIS WAS ACCOMPLISHED WITH OUR RISE IN PRICE TO THE TUNE OF $7.55.

WE HAD – 4568 CONTRACTS COMEX TRADES REMOVED FROM OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 12,172 CONTRACTS OR 1,217,200 OZ OR 37.86 TONNES

Estimated gold comex today 335,106//good//

final gold volumes/yesterday 286,498///good

INITIAL STANDINGS FOR JAN 2023 COMEX GOLD //JAN 26//

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1,800.456. oz Loomis Manfra 56 kilobars//both banks . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | 192.906 oz Brinks 6 kilobars |

| No of oz served (contracts) today | 1 notice(s) 100 OZ 0.00311 TONNES |

| No of oz to be served (notices) | 176 contracts 17,600 oz 0.5474 TONNES |

| Total monthly oz gold served (contracts) so far this month | 6328 notices 632,800 19.6827 TONNES* *new record for a January |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into Brinks 192.906 oz

(6 kilobars)

total deposits: 192.906 oz

customer withdrawals: 2

i) Out of Loomis: 1607.550 oz (50 kilobars)

ii) Out of Manfra 192.906 oz (6 kilobars)

Total withdrawals: 1800.456 oz

total in tonnes: 0.056607 tonnes

Adjustments:1

HSBC dealer to customer: 96.453 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of JANUARY we have an oi of 177 contracts having lost 244 contracts

We had 243 notices served on Tuesday, so we lost 1 contracts or an additional 100 oz(0.00311 tonnes) will stand for delivery in this

very non active delivery month of January. (queue jump)

February lost 25,202 contacts to 121,502 (looks like Feb. is going to be a huge delivery month

March gained 98 contracts to stand at 1280.

April gained 29,401 contracts up to 317,961

We had 1 notice(s) filed today for 100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN. /2023. contract month,

we take the total number of notices filed so far for the month (6328 x 100 oz , to which we add the difference between the open interest for the front month of (JANUARY 177 CONTRACTS) minus the number of notices served upon today 1 x 100 oz per contract equals 650,400 OZ OR 20.230 TONNES the number of TONNES standing in this non active month of January. This is a new record for gold standing in the month of January.

thus the INITIAL standings for gold for the JAN contract month:

No of notices filed so far (6328 x 100 oz+ (177 OI for the front month minus the number of notices served upon today (1)x 100 oz} which equals 650,400 oz standing OR 20.2301 TONNES in this NON active delivery month of JAN..

TOTAL COMEX GOLD STANDING: 20.2301 TONNES (A HUGE STANDING FOR METAL AND A NEW RECORD FOR ANY JANUARY MONTH )//COMEX RUNNING OUT OF PHYSICAL TO SERVE UPON OUR LONGS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

we had one adjustment of 110,631.591 oz Brinks

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,910,035.089 OZ 59.41 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,313,251.375 OZ

TOTAL REGISTERED GOLD: 11,020,384.584 OZ (342.78 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 11,292,866.891 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,110,349 OZ (REG GOLD- PLEDGED GOLD) 283.37 tonnes//rapidly declining

END

SILVER/COMEX

JAN 26/2023//INITIAL JAN. SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,472,699.220 oz Brinks CNT Delaware JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,055,788.769 oz CNT Delaware HSBC |

| No of oz served today (contracts) | 12 CONTRACT(S) (60,000 OZ) |

| No of oz to be served (notices) | 1 contracts (5,000 oz) |

| Total monthly oz silver served (contracts) | 1012 contracts (5,060,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 3 deposits into the customer account

i) Into CNT 599,229.410 oz

ii) Into Delaware: 17,815.134 oz

iii) Into HSBC: 438,744.225 oz

Total deposits: 1,055,788.769 oz

JPMorgan has a total silver weight: 149.388 million oz/292.767 million =50.99% of comex .//dropping fast

Comex withdrawals: 4

i) Out of Delaware: 2998.400 oz

ii) Out of Brinks 994.700 oz

iii) Out of CNT 277927.010 oz

iv) Out of JPMorgan: 1189,779.110 oz

Total withdrawals; 1,471,699.220 oz

adjustments: 3all dealer to customer

i) 101,150.000 JPMorgan

ii) 14,582.036 oz Loomis

iii) 4868.200 oz Manfra

the silver comex is in stress!

TOTAL REGISTERED SILVER: 33.060 MILLION OZ (declining rapidly).TOTAL REG + ELIG. 292,.767 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JAN

silver open interest data:

FRONT MONTH OF JAN/2023 OI: 13 CONTRACTS HAVING GAINED 5 CONTRACT(S.). WE HAD 7 NOTICES

FILED ON TUESDAY SO WE GAINED 12 CONTRACT(S) OR AN ADDITIONAL 60,000 OZ WILL STAND OVER HERE

FEB> LOST 65 CONTRACTS TO 129 CONTRACTS

March LOST 1521 CONTRACTS DOWN TO 108,015 contracts

TOTAL NUMBER OF NOTICES FILED FOR TODAY:12 for 60,000 oz

Comex volumes// est. volume today 86,496//strong

Comex volume: confirmed yesterday: 61,519 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 1012 x 5,000 oz = 5,060,000 oz

to which we add the difference between the open interest for the front month of JAN(13) and the number of notices served upon today 12 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JAN./2023 contract month: 1012 (notices served so far) x 5000 oz + OI for the front month of JAN (13 – number of notices served upon today (12) x 500 oz of silver standing for the JAN. contract month equates 5.065 million oz + 7.25 MILLION OZ ( EXCHANGE FOR RISK) = 12.315MILLION OZ//(TOTAL OZ OF SILVER STANDING).

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:52,938// est. volume today// fair

Comex volume: confirmed yesterday: 96,020 contracts ( very good/excellent)

END

GLD AND SLV INVENTORY LEVELS

JAN 26/WITH GOLD DOWN $11.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 919.37 TONNES

JAN 25/WITH GOLD UP $7.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 917.34 TONNES

JAN 24/WITH GOLD UP $7.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 23/WITH GOLD UP $0.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.63 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 20/WITH GOLD UP $4.75 TODAY;BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 912.43 TONNES

JAN 19/WITH GOLD UP $16.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES INTO THE GLD///INVENTORY RESTS AT 910.98TONNES

JAN 18/WITH GOLD DOWN $1.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.9 TONNES FROM THE GLD////INVENTORY RESTS AT 909.24 TONNES

JAN 17/WITH GOLD DOWN $11.45 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.14 TONNES

JAN 13/WITH GOLD UP $22.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD///INVENTORY RESTS AT 912.14 TONNES

JAN 12/WITH GOLD UP $20.55 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 912.43 TONNES

JAN 11/WITH GOLD UP $1.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

DEC 30/WITH GOLD UP $.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 29//WITH GOLD UP $8.35 TODAY:; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 28/WITH GOLD DOWN $6.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE DEPOSIT OF 5.50 TONNES INTO THE GLD..//INVENTORY REST S AT 918.51 TONNES

DEC 27/WITH GOLD UP $18.15 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 913.01 TONNES

DEC 23/WITH GOLD UP $19,15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES/

DEC 22/WITH GOLD DOWN $29.35 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 21/WITH GOLD FLAT TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 913.88 TONNES

DEC 20/WITH GOLD UP $27.05: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES INTO THE GLD////INVENTORY RESTS AT 912.14 TONNES

DEC 19/WITH GOLD DOWN $2.10: HUGE CHANGES IN GOLD INVENTORY AT THE GLD> A BIG WITHDRAWAL OF 3.47 TONNES FROM THE GLD//INVENTORY RESTS AT 910.41 TONNES

DEC 16/WITH GOLD UP $12.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 15//WITH GOLD DOWN $31.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 911.56 TONNES

DEC 14/WITH GOLD DOWN $6.20: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 912.72 TONNES

DEC 13/WITH GOLD UP $32.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD///INVENTORY RESTS AT 910.41

DEC 12/WITH GOLD DOWN $17.60: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

DEC 9/WITH GOLD UP $8.90//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

Dec 8/WITH GOLD UP $4.05, OVER THE PAST 3 WEEKS WE LOST 2.04 TONNES//INVENTORY RESTS AT 908.09 TONNES

GLD INVENTORY: 919.37 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JAN 26/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 900,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 521.900 MILLION OZ//

JAN 25/WITH SILVER UP 19 CENTS TO TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.3 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 521.000 MILLION OZ

JAN 24/WITH SILVER UP 21 CENTS TODAY: WHAT!! A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 20 MILLION OZ INTO THE SLV/( OCCURRED (LATE LAST NIGHT)//INVENTORY RESTS AT 518.70 MILLION OZ//

JAN 23/WITH SILVER DOWN 40 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.4 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 498.7 MILLION OZ//

JAN 20.WITH SILVER UP 9 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 750,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 497.300 MILLION OZ

JAN 19/WITH SILVER UP 24 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 498.05 MILLION OZ

JAN 18/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 8.15 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 498.05 MILLION OZ///

JAN 17/WITH SILVER DOWN 35 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 13/WITH SILVER UP 46 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.5 MILLION OZ FROM THE SLV..//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 12/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 508.700 MILLION OZ/

JAN 11/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 508.700MILLION OZ

JAN 10/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ

JAN 9/WITH SILVER DOWN 9 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 6/WITH SILVER UP 54 CENTS TODAY;BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.20 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 5/WITH SILVER DOWN 50 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.10 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 505.45 MILLION OZ//

JAN 4/WITH SILVER DOWN 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 506.55 MILLION OZ/

JAN 3/WITH SILVER UP 24 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: STRANGE: A WITHDRAWAL OF 1.2 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 507.85 MILLION OZ/

DEC 30/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 29/ WITH SILVER UP $0.63 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 28//WITH SILVER DOWN 46 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.715 MILLION OZ INTO THE SLV///..INVENTORY RESTS AT 509.050 MILLION OZ

DEC 27/WITH SILVER UP 34 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 507.350 MILLION OZ//

DEC 23/WITH SILVER UP 29 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT507.900 MILLION O//

DEC 22/WITH SILVER DOWN 53 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 21/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.0 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 20/WITH SILVER UP 105 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:: A DEPOSIT OF 700,000 OZ INTO THE SLV///INVENTORY RESTS AT 509.90 MILLION OZ//

DEC 19/WITH SILVER DOWN 13 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.05 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.20 MILLION OZ//

DEC 16/WITH SILVER UP 2 CENTS; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.85 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 508.15 MILLION OZ//

DEC 15/WITH SILVER DOWN 78 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF EXACTLY 2.00 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 510.000 MILLION OZ

DEC 14/WITH SILVER UP 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 512.000 MILLION OZ//

DEC 13/WITH SILVER UP 59 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 600,000 OZ FROM THE SLV////INVENTORY RESTS AT 513.900 MILLION OZ//

DEC 12/WITH SILVER DOWN 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 514.500 MILLION OZ//

DEC 9/WITH SILVER RISING 77 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.2 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 514.500 MILLION OZ.

DEC 8/WITH SILVER RISING 34 CENTS TODAY: OVER THE PAST 3 WEEKS, WE HAVE GAINED A STRONG: 44.777 MILLION OZ/INVENTORY RESTS AT 516.700 MILION OZ.

CLOSING INVENTORY 521.900 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

END

3. Chris Powell of GATA provides to us very important physical commentaries//

Craig Hemke explains why the Comex is a complete fraud. Do not except a gold bank run starting at the Comex. It will start elsewhere

Craig Hemke/Sprott/GATA)

Craig Hemke at Sprott Money: Gold bank run won’t start at the Comex

Submitted by admin on Wed, 2023-01-25 16:50Section: Daily Dispatches

4:50p ET Wednesday, January 25, 2023

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, writing today at Sprott Money, concludes that no serious gold action is taking place on the New York Commodities Exchange. Rather, Hemke writes, the same four big banks are just shuffling among themselves the contracts nominally being bought and sold.

When a run on the gold banking system develops, Hemke writes, it’s not likely to happen at the Comex.

Hemke’s analysis is headlined “Comex January Gold Deliveries” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/COMEX-January-Gold-Deliveries-January-25-2023

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4. Other gold/silver commentaries

Blain: Buy Gold To Fund Bottom-Fishing

THURSDAY, JAN 26, 2023 – 09:35 AM

Authored by Bill Blain via MorningPorridge.com,

“Gold is enough, Beautiful gold, Lovable gold, Spendable gold..….”

Gold – can’t eat it, can’t use it, but its everything crypto never was: tangible, exchangeable, a store of value, and a kitty for when things get tough. In uncertain markets…. Don’t forget the yellow stuff.

Writing the morning porridge after Burn’s Night, Scotland’s celebration of our acclaimed national poet, Robert Burns, following Whisky and Haggis is never easy… So in order to force my brain back into motion… let’s consider Gold!

Trying putting Gold in the context of today’s markets…. So foul and fair a market I have not seen. (Extra points if you know the reference from the Scottish Play – and what happens next!)

One hand we have a pandemic of optimism that inflation is broken, central banks are going to pivot and start cutting rates, thus its unbounded joy at the prospect of a minor downturn, recovery, growth and a swift rise in earnings pushing up stocks, while bonds rally into the ease. The China reopening will fuel global recovery. Put your buying boots on!

On the other hand are the ongoing portents of sticky inflation, central banks wanting to normalise positive interest rates around 2% inflation and 4% rates to promote functional capitalism (the end of the era of cheap money), and the shake-out in Zombie, over-levered companies and speculative hype that’s driven financial asset price inflation and now blocks growth and productivity gains. Stabilising the global economy will see rates and inflation higher for longer.

Then layer on the real-world challenges of War In Ukraine, Geopolitical threats, Energy Security, the consumer Cost of Living Crisis and Income Inequality, climate change, plus a host of immediate challenges emerging to the political order in the West; from failing services across health, housing, education to increased populist threats from Left and Right.

Pick yer poison and lay yer bets accordingly.

Markets work by reading the uncertain runes of unclear futures. There are threats out there – but outcomes probably fall into the middle. My classic mantra is: “Things are never as bad as you fear, but never as good as you hope.” I see markets as multi-dimensional and complex: a little bit of inflation here will have consequences way over there. Be aware of the complexity.

Many market participants tend to make the mistake of thinking price moves are determined by the linear cause and effect of events – this morning I read on Bloomberg: “High Equity Yields act as a better hedge against higher inflation than fixed income.” That is linearly true, but higher interest rates have consequential lateral effects; reducing consumption thus putting corporate earnings under stress and long-term less sustainable.

Nothing in markets is ever simple…. Think laterally. Which finally leads us to Gold and its place in uncertain markets.

According to the chart I was looking at, Gold prices peaked in 1980 at $2500 on an inflation adjusted basis. On a price basis the current price of Gild ($1945) is pretty close to the $1971 price seen during the depth of Covid.

My colleague Ashley Boolell, Shard’s head of commodities, reckons gold is going to a new record level this year, fuelled by a number of factors – not least being the ongoing market uncertainty. Each time we get another unexpected market number, or a corporate shock, it chips way confidence. In uncertain markets Gold is seen as the safe-haven investment – especially when there is the threat of the technical US default on the back of the debt-ceiling being blocked by the Alt-Right of the Republican Party.

Gold pays no interest. There is no return. It has no real use. Gold’s value is its scarcity.

It is formed in supernovas and neutron stars in Galaxies far, far away. All the gold on earth came arrived as space rubble and dust, absorbed as the planet coalesced in the clouds of material around the forming sun. All the gold that’s ever been mined would only just cover a football pitch to the depth of 1 meter. (205,238 tonnes over the entirety of human history according to the World Gold Council.) Aside from some very limited industrial catalyst applications, its not very useful, but because it does not react or tarnish – it’s been worshipped as a thing of value for millennia.

I was once told the prime driver of gold prices is the Monsoon. In wet years Indian farmers get rich on improved crop yields – meaning they buy their daughters more gold bangles for their wedding dowry. It’s a lovely thought – but apparently an exaggeration.

Unlike cryptocurrencies – which tried to push their way into finance as exchangeable stores of value despite their intangibility – gold’s tangibility as a store of value has made it the globally accepted token of wealth since year dot. Over the years it has morphed into a commodity in its own right – traded electronically and held as an investment because of its recognised store of value.

In times of uncertainty gold tends to rise. In times of market uncertainty it’s a very useful asset to hold. The trick to a market sell off is not being short equities when the stock crash comes, but being liquid enough to start buying after the crash or market correction. Analyse any great market tumble and its inevitably followed by a buying window – that delicious moment when the rest of the market is still panicked and fearful, but stock yields look cheap and bonds are selling for pennies because of weakness. That’s the moment to buy – but what with if your liquid bonds are in free-fall and offered only, and stocks are still in free-fall.

That’s when the liquidity of Gold is a marvellous thing. Going into market uncertainty with a nice little stash of gold to finance bottom fishing of distressed cheap assets is a marvellous thing!

Funny moment yesterday when I was chatting to Ashley about Gold y’day. Aside from being our commodities guru, he is also a published Science Fiction author. I asked him about the implications of space mining – which will be a very real thing in the next 50-years. What if a mission to the asteroid belt discovers a 10,000 tonne lump of orbiting gold? (I remember something like that from E Doc Smith’s Lensman series). Ashley told me that’s exactly what he’s writing about now!

END

5.IMPORTANT COMMENTARIES ON COMMODITIES:COPPER

.

end

6.CRYPTOCURRENCY COMMENTARIES/

Looks like they are going after Bankman Fried’s parents!

(zerohedge)

Lawyers Seek To Question Bankman-Fried’s Parents About Their Wealth; Goldman, JPM Revealed As FTX Creditors

THURSDAY, JAN 26, 2023 – 11:37 AM

With the public court of opinion having long ago convicted crypto fraudster Sam Bankman-Fried – even as several notable holdouts such as Bill Ackman and Andrew Ross-Sorkin remain – attention is now turning to his just as “effectively altruistic” parents. According to a court filing by bankrupt FTX, SBF’s parent should be forced to answer questions and provide financial documents about their personal wealth and any money they may have gotten from the 30-year-old scammer.

As Bloomberg notes, FTX asked a judge for permission to question under oath Bankman-Fried’s family and a handful of the company’s former top executives as part of a hunt for hidden assets that could be used to repay creditors owed billions of dollars. Or not so hidden: as a reminder in November it was revealed that SBF’s disgraced “progressive” parents – Stanford University law professors Joseph Bankman and Barbara Fried (who on her bio says she has “written extensively on questions of distributive justice, in the areas of tax policy, property theory and political theory” which apparently means using her son’s stolen money to buy herself beachfront mansions) – purchased at least one $16.4 million beachfront “vacation home” in the gated Bahamas community of Old Fort Bay.

The court filing shows “the aggressive approach that FTX advisers are taking to recover any money that Bankman-Fried may have inappropriately handed out.” The company was heavily involved in lobbying politicians and regulators and making campaign donations to Democrats and the White House. Federal prosecutors charged Bankman-Fried with fraud for his role in the collapse of FTX, which filed for bankruptcy in November.

Incidentally, when asked by Reuters in November why the couple decided to buy a vacation home in the Bahamas and how it was paid for, a spokesperson for the professors said only that Bankman and Fried had been trying to return the property to FTX. “Since before the bankruptcy proceedings, Mr. Bankman and Ms. Fried have been seeking to return the deed to the company and are awaiting further instructions,” the spokesperson said.

They’ll now get their chance.

According to the court filing, Joseph Bankman and his wife, Barbara Fried, were actively involved in their son’s company. Joseph Bankman, a law professor at Stanford Law School, offered tax advice to FTX employees and helped recruit the company’s first lawyers, the court filing said, citing media reports. Meanwhile, ultra-progressive liberal, Barbara Fried, founded a political action committee that got money from FTX and its top executives, according to the filing.

It gets better: the brother, Gabriel Bankman-Fried, founded an organization that lobbied members of the US Congress from a multimillion dollar property near the US Capitol, according to the filing.

Finally, for those wondering if the alleged criminal’s parents will be teaching at Stanford Law School next year (one really can’t make this up), the answer is no: apparently not even Stanford will sink that low.

Separately, FTX watchers will recall that early on, the now insolvent exchange asked the bankruptcy judge to keep the names of its thousands of creditors confidential and under seal. Well, we finally got a glimpse at some of the companies that provided money to fund Sam’s discretionary spending (i.e., theft of FTX funds). According to the latest bankruptcy court documents, FTX owes money to a dizzying assortment of firms including Goldman Sachs and JPMorgan.

The 116-page document filed on Wednesday detailing FTX’s creditors contains thousands of entries, and while the names of individuals are redacted, the list identifies heavyweights across Wall Street as holding some kind of claim against Sam Bankman-Fried’s once-giant exchange.

Oh well, time to crack down on the largest Wall Street banks for enabling the biggest fraud in history.

Joking aside – because everyone knows nothing will ever happen to Goldman and JPM – another interesting name in the creditor list stands out:

end

Arizona lawmakers are pushing a bill to make Bitcoin legal tender

(zerohedge)

Arizona Lawmakers Push Bill To Make Bitcoin Legal Tender

WEDNESDAY, JAN 25, 2023 – 06:40 PM

A bill introduced by Sen. Wendy Rogers reflects growing interest in bitcoin from U.S. states…

State Sen. Wendy Rogers (R-AZ) has introduced a set of bills aimed at making bitcoin legal tender in Arizona and allowing state agencies to accept bitcoin.

As Bitcoin Magazine’s ‘BTCCasey’ reports, the proposed legislation aims to recognize bitcoin as a legal form of currency in Arizona, allowing it to be used to pay for debts, taxes and other financial obligations.

This would mean that all transactions that are currently done in U.S. dollars could potentially be done with bitcoin, and individuals and businesses would have the option to use bitcoin as they see fit.

Specifically mentioning bitcoin alone, the legal tender bill defines bitcoin as, “the decentralized, peer-to-peer digital currency in which a record of transactions is maintained on the Bitcoin blockchain and new units of currency are generated by the computational solution of mathematical problems and that operates independently of a central bank.”

The acceptance bill is more broad, saying that, “A state agency may enter into an agreement with a cryptocurrency issuer to provide a method to accept cryptocurrency as a payment method of fines, civil penalties or other penalties, rent, rates, taxes, fees, charges, revenue, financial obligations and special assessments to pay any amount due to that agency or this state.”

Additionally, as CoinTelegraph reports, in legislation introduced in the first session of the Arizona State Senate in 2023, Senators Rogers, Borrelli, and Wadsack proposed having Arizona residents decide on amending the state’s constitution in regard to crypto and property taxes.

Should the measure pass the legislature, voters could choose in November 2024 to make virtual currency — specifically tokens that are not “a representation of the United States dollar or a foreign currency” – tax-exempt.

Under Arizona’s constitution, all federal, state, county and municipal property are tax exempt, as are public debts, many household goods, and certain “stocks of raw or finished materials, unassembled parts, works in process or finished products”.

Data from the Arizona Secretary of State indicates that there were more than 4 million registered voters in the November 2022 general election, with the state leaning slightly Republican.

This is the second time that Sen. Rogers has introduced a bill aimed at making bitcoin legal tender in her state. She introduced the same amendment in January 2022, which died by the second reading.

Although it may appear there are slim chances of the bill passing this time, El Salvador’s adoption of bitcoin as legal tender has proven to be a boon for growth and investment in the country.

Recent actions in states like Texas, New Hampshire, Missouri and Mississippi all indicate increasing U.S. state interest in bitcoin and its benefits.

As bitcoin adoption strengthens, the likelihood of such bills passing will only increase.

END

.

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//THURSDAY MORNING.7:30 AM

ONSHORE YUAN: XXX TO CLOSED

OFFSHORE YUAN: 6.7408

SHANGHAI CLOSED

HANG SENG CLOSED

2. Nikkei closed UP 32.26 PTS OR 0.12%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 101.59 Euro FALLS TO 1.0893 DOWN 28 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.475!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 129.78/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: XX-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.176%***/Italian 10 Yr bond yield RISES to 4.099%*** /SPAIN 10 YR BOND YIELD RISES TO 3.165…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.194//

3j Gold at $1936.25//silver at: 23.86 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 22/100 roubles/dollar; ROUBLE AT 69.05//

3m oil into the 81 dollar handle for WTI and 87 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 129.78/10 YEAR YIELD AFTER BREAKING .54% RISES TO .475% ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9187– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0027 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.482% UP 2 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.635 UP 1 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,81…

GREAT BRITAIN/10 YEAR YIELD: 3.320 % UP 8 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Rise Boosted By Solid Tesla Earnings, Chevron’s Giant Buyback

THURSDAY, JAN 26, 2023 – 08:06 AM

In a mirror image of Tuesday’s action, when MSFT earnings hammered stocks (after first headfaking them higher) only to see the selloff reverse completely during the course of Wednesday trading, on Thursday US equity futures and tech stocks were set to gain after an upbeat earnings report from Tesla reinforced optimism about the health of Corporate America. As of 7:30am, Nasdaq 100 futures were up 0.7% while S&P 500 futures rose 0.3%. Tesla jumped about 8% in premarket trading after the electric-car maker reported better-than-expected profit and said it was on track to deliver about 1.8 million vehicles this year. Risk sentiment was boosted by news that US energy giant Chevron had authorized a massive $75 billion stock buyback, representing 22% of its outstanding shares, helping elevate energy stocks around the globe. Asia stocks jumped to 9-month highs as Hong Kong returned from break and European stocks rose by 0.4%. Meanwhile, the dollar continued to weaken as speculation continued to mount that the Fed is drawing closer to the end of its rate-hiking cycle, and would follow in the footsteps of first Canada and then Indonesia, both of which have officially paused. Bonds and gold edged lower.

In premarket trading, all eyes were on Tesla which rose 7.3% after the electric-car maker reported better-than-expected profits and said it was on track to deliver about 1.8 million vehicles this year. Analysts noted that the EV market leader’s output target looks conservative as new factories in Berlin and Austin are set to add more capacity this year. Among peers: Rivian (RIVN US) +3.5%, Lucid (LCID US) +3.4%, Nikola (NKLA US) +1.9%, Nio (NIO US) +4.9%, Xpeng (XPEV US) +5.1%, Li Auto (LI US) +5%. Bank stocks traded higher in premarket trading Thursday, putting them on track to gain for a second straight day. In corporate news, a New York Stock Exchange employee failed to properly shut down a disaster-recovery system, leading to Tuesday’s chaotic opening session. Meanwhile, Cboe Global Markets wants to list more tokens on its crypto exchange, as established firms from traditional finance seek to capitalize on demand for reliable counterparties following the collapse of FTX. Here are some other notable premarket movers:

- Chevron (CVX US) gains 2.5% after it announced plans to buy back $75 billion of shares and increase dividend payouts after a year of record profits that evoked angry denunciations from politicians around the world as soaring energy prices squeezed consumers.

- Pfizer (PFE US) drops 1.8% in premarket trading as UBS downgrades the stock to neutral, saying estimates for the pharma giant’s Covid-19 franchise still look too high.

- IBM (IBM US) shares slip 2% after the tech infrastructure and IT services company’s free cash flow for 4Q fell short of estimates, which Morgan Stanley analysts say was a “significant blemish” in the quarter. That overshadowed IBM’s estimate-beating revenue and profit for the fourth- quarter.

- BuzzFeed (BZFD US) shares were indicated up about 35% following a Wall Street Journal report that the company reached a content creation deal with Meta. The deal was agreed last year and is worth nearly $10 million, WSJ cites people familiar with the matter as saying.

- Seagate (STX US) shares rise 7.6% as its quarterly update was better than expected and the computer- hardware firm’s guidance underpins a positive view on the stock, analysts say.

- Teradyne (TER US) falls 3% after its 1Q earnings forecast missed the average analyst expectation, on lower demand for semiconductors and storage tests. Fourth-quarter earnings beat analysts’ estimates.

- Las Vegas Sands (LVS US) shares gain 2.1% as analysts raise their price targets on the stock. They said better-than-expected results despite travel restrictions boded well for a recovery.

US stocks have kicked off 2023 with a rally that has set the S&P 500 on course for its best January since 2019, as investors bet that the Federal Reserve will slow the pace of rate hikes in time to avert a recession. Deutsche Bank AG strategists said this week they expect further gains in the first quarter as an economic contraction is “running late.”

Commenting on yesterday’s dramatic market reversal, Goldman trader John Flood writes that “when the market/stocks dont go down on bad news (MSFT guide) typically a bullish signal. I think we learned a lot from this price action today: this mkt is more resilient than most of us are giving it credit for (be very thoughtful/selective with your short positions as squeezes will be common this Q). Worth noting CVX raised the dividend by 6% and authorized a monster $75B buyback…energy complex will outperform on this tomorrow. Reminder buyback blackout period ends post close this Friday.“

Today all eyes will be on US GDP figures due later today, with economists expecting the data to show a slowdown in growth at the end of the year. Focus has also been on the fourth-quarter earnings season for signs of how companies plan to navigate slowing demand and elevated inflation. Analysts are projecting the first quarterly decline in US profits since 2020, but some market strategists have warned profit margin estimates for 2023 are still too high.

“Earnings have not been great but they are not disastrous either,’ said Rupert Thompson, chief economist at asset manager Kingswood Holdings Ltd. “Institutional investors have been short equities so you are seeing some of those positions being covered.” Thompson sees the January stock surge as overdone, given recession risks ahead, but did not discount further short-term gains because “if you do get a 5% pullback, people who missed the rally may think ‘shall we just bite the bullet now rather than wait for another 5% fall?”

“Sentiment remains fixated on the path of inflation, and where the Fed will go with interest-rate policy,” said Susannah Streeter, senior investment and markets analyst at Hargreaves Lansdown. Today’s economic data will be crucial to see “whether demand is being squeezed out of the economy and whether more storm clouds are gathering on the horizon,” she said.

Soft-landing bets for the US economy and expectations the Federal Reserve is nearing the end of its rate-hiking cycle have lifted stock markets and put the dollar on course for its worst monthly performance since last May. On Thursday, it held around flat against its Group-of-10 peers as investors awaited economic growth and jobs data as well as a core price index that could determine the Fed’s policy path.

In Europe, the Stoxx 600 was higher by 0.5% with outperformance in the tech sector after Nokia and STMicroelectronics posted better-than-expected numbers. Results from telecoms group Nokia Oyj and chipmaker STMicroelectronics NV were applauded by investors, helping to lift the Stoxx 600 index by half a percent. Here are some of the biggest European movers on Wednesday:

- Sabadell shares soar as much as 10% after the Spanish lender reported 4Q net profit that beat estimates and gave above- consensus estimates guidance

- Sartorius AG rises as much as 8.3% after the laboratory equipment firm reassured the market with an update to its financial targets; its subsidiary Sartorius Stedim Biotech rises, too

- STMicro jumps as much 9.3% after the chipmaker projected first-quarter and full-year sales ahead of consensus estimates, defying a slowdown in the broader semiconductor industry

- Nokia shares gain as much as 7.2%, the biggest intraday climb since July, after the telecom equipment maker outlined full-year outlook that met expectations

- Diageo falls as much as 7.4%, weighing on peers in the alcohol and beverages sector, after the Johnnie Walker maker’s results disappointed in North America and delivered an uncertain outlook

- Volvo shares slide as much as 4.9% in early trading after the Swedish truck producer reported 4Q22 earnings that came in below consensus

- SEB falls as much as 4.8%, the most since October, after the Swedish lender reported 4Q figures that beat expectations but were of a low quality, according to Citi

- Novartis falls as much as 2.4% on being cut to neutral from buy at Citi on a more cautious outlook for the Swiss pharma group’s cholesterol drug Leqvio and prostate cancer drug Pluvicto

- SAP shares fall as much as 4.1% after it’s free cash flow outlook for 2023 missed estimates, even though the firm still projected at least a double-digit growth for operating profits

Earlier in the session, stocks in Asia Pacific rose for a fifth straight day as investors in Hong Kong returned from Lunar New Year holidays that delivered a boost to consumption. The MSCI Asia Pacific Index climbed as much as 0.8% to the highest since April 22. Hong Kong-listed stocks rallied as data on spending and tourism during the three-day break signaled a recovery in demand is gaining traction in China. The Hang Seng Index closed at its highest since March. “Stocks in Hong Kong would probably remain on the stronger side,” Chetan Seth, an Asia Pacific equity strategist at Nomura, told Bloomberg Television. “What we might see in the months ahead is improvement in activity indicators.” Benchmarks in South Korea, Indonesia and Singapore also rose as traders assessed the global economy’s prospects.

China’s reopening has triggered a rebound across Asia, with investors now looking beyond Covid infection figures to evaluate how a recovery in the region’s largest economy will impact earnings. The MSCI Asia gauge is outperforming the S&P 500 by more than four percentage points so far in 2023

Japanese stocks fell, while markets in Australia, China, India, Taiwan and Vietnam were closed. Japanese stocks closed slightly lower, erasing early gains and halting a four-day winning streak, as investors assessed prospects for corporate earnings and the global economy. The Topix fell 0.1% to close at 1,978.40, while the Nikkei declined 0.1% to 27,362.75. Sony contributed the most to the Topix decline, decreasing 1.3%. Out of 2,161 stocks in the index, 893 rose and 1,116 fell, while 152 were unchanged. “There is a continued wait-and-see mood as there are two important indicators, the FOMC meeting and ISM employment reports coming up next week,” said Shogo Maekawa a global market strategist at JP Morgan Asset Management

In FX, the Bloomberg Dollar Index swung between moderate gains and losses. The Norwegian krone and Australian dollar led gains, while Sweden’s krona lagged. The euro retreated after six days of gains versus the greenback, though it is likely to enjoy continued monetary policy support, as several European Central Bank rate-setters spoke in favor of further hefty policy-tightening over coming months. Traders are likely to parse reports on US economic growth, initial jobless claims and a core price index due Thursday to gauge if the Fed will opt for a smaller rate hike on Feb. 1. Recent commentary from some central bank officials has backed the case for a quarter point increase

In rates, treasuries were lower after following gilts and, to a lesser extent, bunds during European morning. US yields cheaper by up to 4bp across long-end of the curve which leads losses on the day; 10-year yields back up to around 3.48% with gilts underperforming by additional 2bp in the sector and bunds trading broadly in line. UK and German 10-year yields rise by 4bps and 2bps respectively. A raft of US economic data is set to be released, and auction cycle concludes with 7-year notes following strong demand for 5- and 2-year sales. $35b 7-year notes at 1pm New York time is final coupon auction of the November-to-February financing quarter; all previous coupon auctions during January have stopped through. The WI 7-year around 3.525% is ~40bp richer than January’s stop-out and below auction stops since August.

Saira Malik, chief investment officer of Nuveen, said earnings risk in a consumer-led slowdown will act as a headwind to equities, with a shift into bonds underscoring the fragile sentiment. “You can start to increase your duration in fixed-income and get strong total returns in it without a lot of these heavy macro risks that are going to hit equities,” Malik said in an interview with Bloomberg TV. “Equities considering their valuation are less attractive.”

Elsewhere, oil prices rose for a second day, lifted by expectations of demand recovery in China. Crude future advance with WTI gaining 0.9% to trade near $80.90. Spot gold falls roughly 0.5% to trade near $1,937/oz.

Bitcoin fell more than 2%, reversing much of Wednesday’s gain.

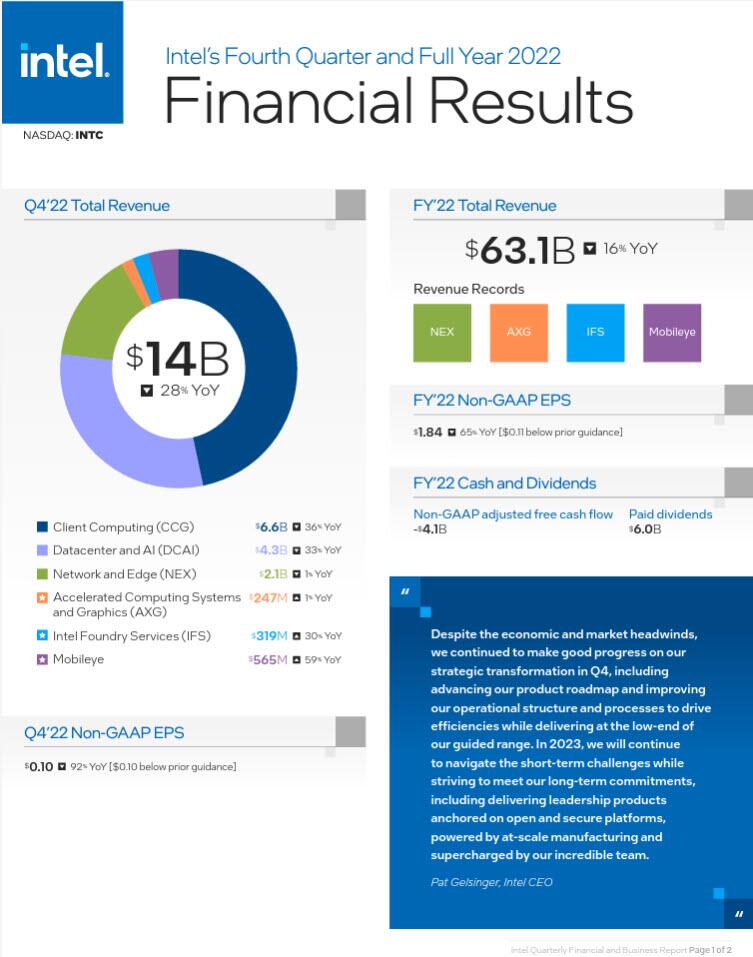

Looking to the busy day ahead now, data releases from the US include the advance estimate of Q4 GDP, preliminary durable goods orders for December, new home sales for December and the weekly initial jobless claims. Otherwise, earnings releases include Visa, Mastercard, Intel, American Airlines and Comcast.

Market Snapshot

- S&P 500 futures up 0.2% to 4,038.75

- MXAP up 0.6% to 170.22

- MXAPJ up 1.1% to 558.68

- Nikkei down 0.1% to 27,362.75

- Topix down 0.1% to 1,978.40

- Hang Seng Index up 2.4% to 22,566.78

- Shanghai Composite up 0.8% to 3,264.81

- Sensex down 1.3% to 60,205.06

- Australia S&P/ASX 200 down 0.3% to 7,468.30

- Kospi up 1.7% to 2,468.65

- STOXX Europe 600 up 0.5% to 454.33

- German 10Y yield little changed at 2.19%

- Euro down 0.1% to $1.0900

- Brent Futures up 0.4% to $86.50/bbl

- Gold spot down 0.5% to $1,937.17

- U.S. Dollar Index up 0.17% to 101.81

Top Overnight Stories

- BOJ members were divided over whether the 2% inflation goal could be sustainably achieved and felt the extreme level of accommodation should be sustained. Also, The IMF suggested that the BOJ could allow more flexibility in 10-year bond yields, a move that would involve policy changes for the central bank. RTRS / Nikkei

- China’s most scenic destinations have been inundated during the Spring Festival holiday, as Beijing’s shift away from Covid Zero spurred a travel frenzy despite the country’s ongoing omicron outbreak. BBG

- Bank of Indonesia has delivered enough interest-rate increases, according to Governor Perry Warjiyo, who signaled that this round of tightening is coming to an end as the Federal Reserve also winds down. This is the second central bank in as many days (after the Bank of Canada yesterday) to signal an end to rate hikes. BBG

- Pakistan’s economy is at risk of collapse, with rolling blackouts and a severe foreign currency shortage leaving businesses struggling to operate as authorities attempt to revive an IMF bailout to relieve the deepening crisis. FT

- Adani Group may take legal action against Hindenburg Research after the US short seller alleged “brazen” market manipulation and accounting fraud. Shares of Adani-related entities slumped yesterday, shaving $12 billion off the empire of Asia’s richest man, and a raft of its companies’ dollar bonds fell further today. BBG

- Eurozone officials start talks on creating a huge multibillion-euro fund to compete w/the US green energy subsidies. London Times

- The NYSE mayhem earlier this week was due to simple human error, people familiar said — an exchange employee didn’t correctly shut down a backup system running overnight so heading into Tuesday, the NYSE’s computers treated the 9:30 a.m. bell as a continuation of trading, skipping the opening auctions. No word yet on the cost of the chaos. BBG

- Donald Trump’s back. Meta will reinstate the former president’s social media accounts “in the coming weeks” following a two-year suspension. He had 34 million followers on Facebook and 23 million on Instagram back in 2021 but, more important, his re-election campaign will now be able to buy ads to raise money via direct appeals or by capturing users’ contact info to solicit them directly. BBG

- Tesla jumped as much as 8% premarket after profit beat, though there were mixed signals on the outlook. Elon Musk said production may top 1.8 million vehicles this year. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded somewhat mixed amid key holiday closures and after the flat handover from Wall St where the major indices recouped most of their initial losses after the BoC’s dovish hike. Nikkei 225 was subdued amid a firmer currency and upside in yields, while the government also lowered its overall economic assessment for the first time in 11 months. KOSPI gained despite the weaker-than-expected GDP data although the finance minister flagged the likelihood of a return to growth for the current quarter. Hang Seng outperformed as participants in Hong Kong returned from the Lunar New Year holiday and were greeted by strength in tech, property and autos, although trade across the rest of the region remained relatively quiet owing to the closures in Australia, China, Taiwan, India and Vietnam.

Top Asian News

- BoJ Summary of Opinions from the January meeting stated it is appropriate to maintain current monetary easing including YCC and that the BoJ must keep yields from rising across the curve while being mindful of the bond market function. Furthermore, they must spend more time to gauge the impact of the December decision and must conduct a review of policy at some point although it is appropriate to maintain easy policy for now, while they still see some distance in achieving the price goal and noted it will take some time to achieve sustained wage growth.

- IMF (policy proposal on Japan) says the BoJ should allow bond yields to move in a more flexible manner; If significant upside inflation risks materialise, BoJ needs to be ready to withdraw stimulus strong, e.g. by increasing interest rates; possible options for the BoJ include widening the yield bank, increasing the yield target, targeting shorter yields and shifting to a quantity target; BoJ policy is appropriate as inflation is likely to ease but risks are becoming more pronounced; FX intervention should be limited to special circumstances such as disorderly market conditions.

- Japan is to downgraded its COVID classification on May 8th, via NHK.

European bourses are firmer across the board, Euro Stoxx 50 +0.6%, with a busy morning for earnings dictating the state of play before Stoxx 600 heavyweight LVMH’s (MC FP) earnings, due after-market on Thursday. Stateside, futures are firmer across the board, ES Mar’23 +0.2% and comfortably above the 4k mark and as such the 10- and 200-DMAs which reside on either side of the figure. NDX +0.6% is the incremental outperformer after a well received update from Tesla (TSLA) +7% pre-market while IBM (IBM) slips -1.6% after its Q4 report.

Top European News

- US and EU are reportedly discussing a potential deal regarding critical raw materials and minerals, to enable the EU to benefit from the US’ Inflation Reduction Act/green investment plan, via Bloomberg citing sources.

- UK 2022 car production fell 9.8% Y/Y to 775k units, while car and light van production for 2023 is expected to increase 15% Y/Y to 984k units, according to SMMT.

- UK ONS says consumer behaviour indicators were broadly similar to the prior week.

- Irish Finance Minister McGrath says Brexit talks have reached a new level.

- Italian Economy Minister says before April they intend to extend relief measures to assist families and firms with energy costs, could alter regulations on capital gains tax.

- Denmark Calls for Mandatory Military Service for Women

- Europe Gas Prices Rebound After Slump With Asia Demand in Focus

- Diageo Drops as Sales Growth Slows in Crucial US Market

- Saipem Top Oil Services Pick at JPMorgan, Subsea 7 Cut

FX

- DXY slips to a minor new 101.500 y-t-d low, but holds in and pares some losses pre-US data raft.

- Aussie and Kiwi remain underpinned on inflation grounds, but AUD/USD heavy on 0.7100 handle and NZD/USD clipped around 0.6500.

- Yen recoils between 129.00-130.00 range vs Buck as Japan’s top currency diplomat warns that sharp moves will not be tolerated, CNH bid as HK markets return from holiday with COVID reopening optimism.

- Euro and Pound wobble above 1.0900 and 1.2400 vs Dollar and ahead of technical resistance.

- Morgan Stanley’s month-end USD rebalancing model: expects the USD to underperform in January, with weakness expected vs all G10 currencies ex-NOK.

- CBRT announced support for the conversion of firms’ foreign exchange obtained from abroad into Turkish liras to support ‘liraization’ in commercial activities, with firms to be provided with FX conversion support corresponding to 2% of the amount converted.

Fixed Income

- Core benchmarks have continued to ease from best levels with the IMF’s BoJ/Japan policy proposal adding to the pressure.

- Bunds holding just above 138.00 within 138.62-137.91 parameters while Gilts are just below 105.00 towards the mid-point of a 105.66-104.72 range.

- USTs are similarly contained around the 115.00 handle as participants await US data and a subsequent 7yr auction.

Commodities

- WTI and Brent March futures remain underpinned by the China-demand narrative, though are relatively rangebound overall and spent much of the morning trading with no firm direction with focus on geopols and French strike action.

- US and European gas futures are experiencing a modest divergence, with ING suggesting the US Nat Gas pressure is due to milder weather.

- TotalEnergies (TTE FP) says pension reforms strike action is interrupting shipments at French production sites, except for the Feyzin refinery (119k BPD). Continue to ensure petrol stations are supplied, no shortage.

- 24-hours strike declared at the 140k BPD Fos-Sur-Mer oil refinery in France, according to BFM TV citing an Esso Union official.

- German energy regulator says there is not enough gas saving in the third calendar week; household, business and industry consumption down 9%in total in that week (vs 20% target).

- Spot gold has been dipping from best levels amid seemingly yield-driven USD upside while LME copper is relatively resilient but has slipped from best levels.

Geopolitics

- Russian Kremlin says it sees the sending of Western tanks to Ukraine as direct and growing involvement in the conflict.

- Russian Security Council’s Secretary Patrushev says the US and NATO are participating in the Ukrainian conflict and want to prolong it.

US Event Calendar

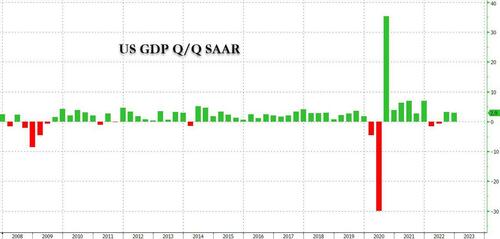

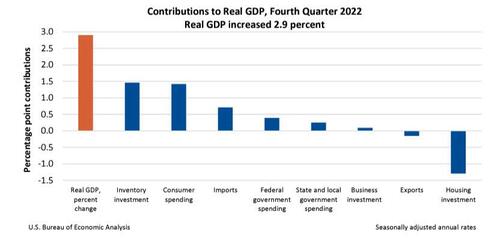

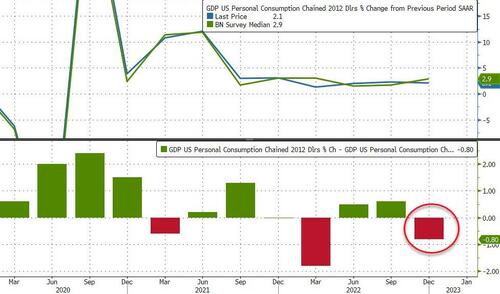

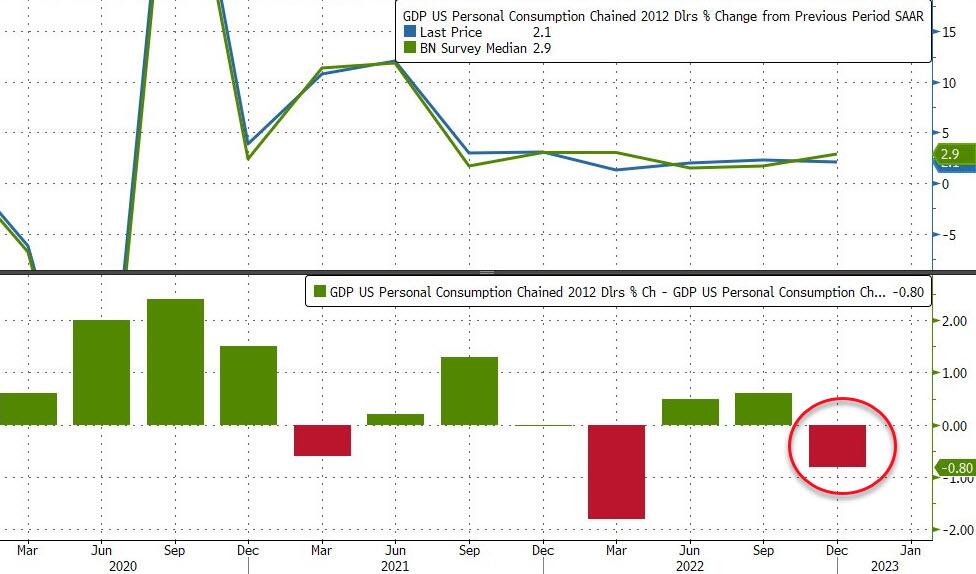

- 08:30: 4Q GDP Annualized QoQ, est. 2.6%, prior 3.2%

- 4Q GDP Price Index, est. 3.2%, prior 4.4%

- 4Q PCE Core QoQ, est. 3.9%, prior 4.7%

- 4Q Personal Consumption, est. 2.8%, prior 2.3%

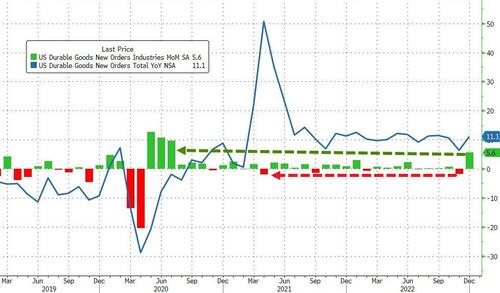

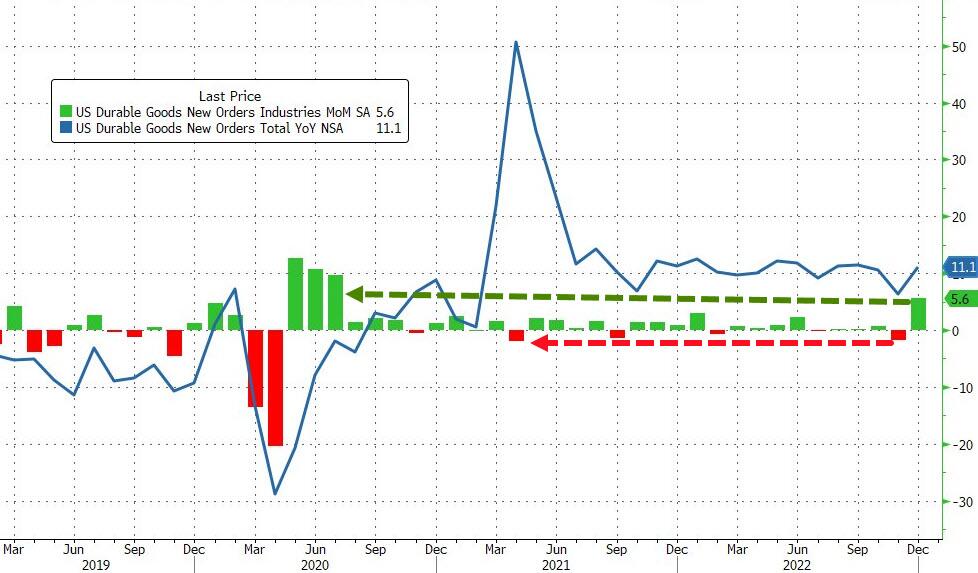

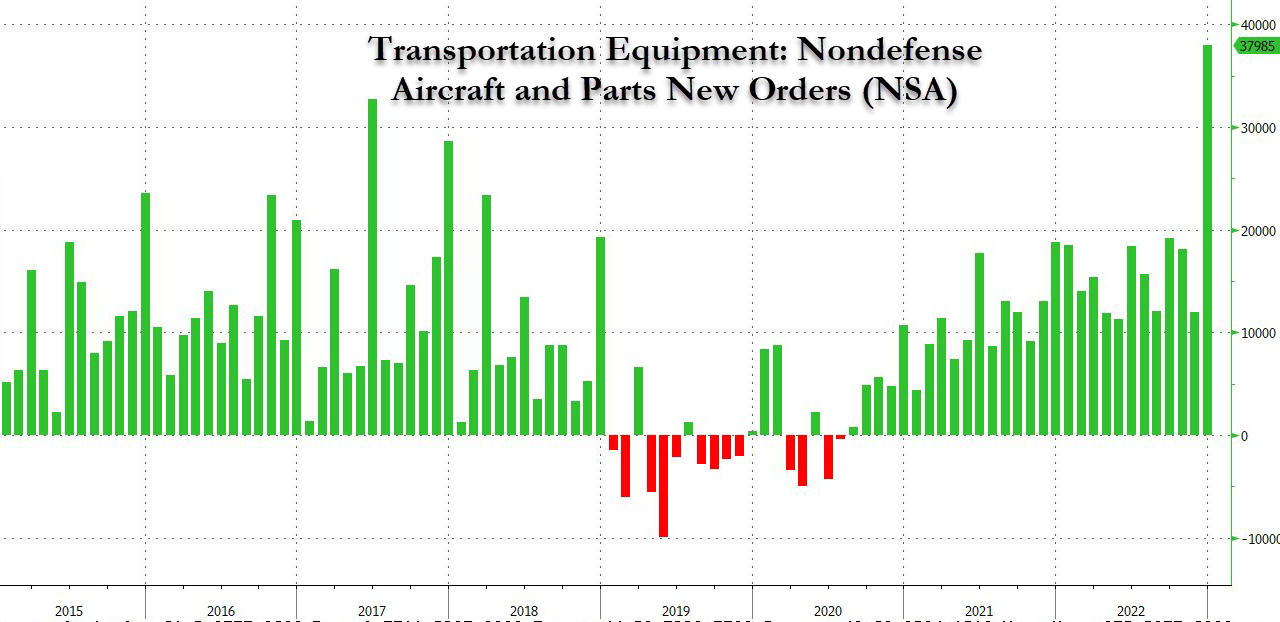

- 08:30: Dec. Durable Goods Orders, est. 2.5%, prior -2.1%

- Dec. -Less Transportation, est. -0.2%, prior 0.1%

- Dec. Cap Goods Orders Nondef Ex Air, est. -0.2%, prior 0.1%

- Dec. Cap Goods Ship Nondef Ex Air, est. -0.4%, prior -0.1%

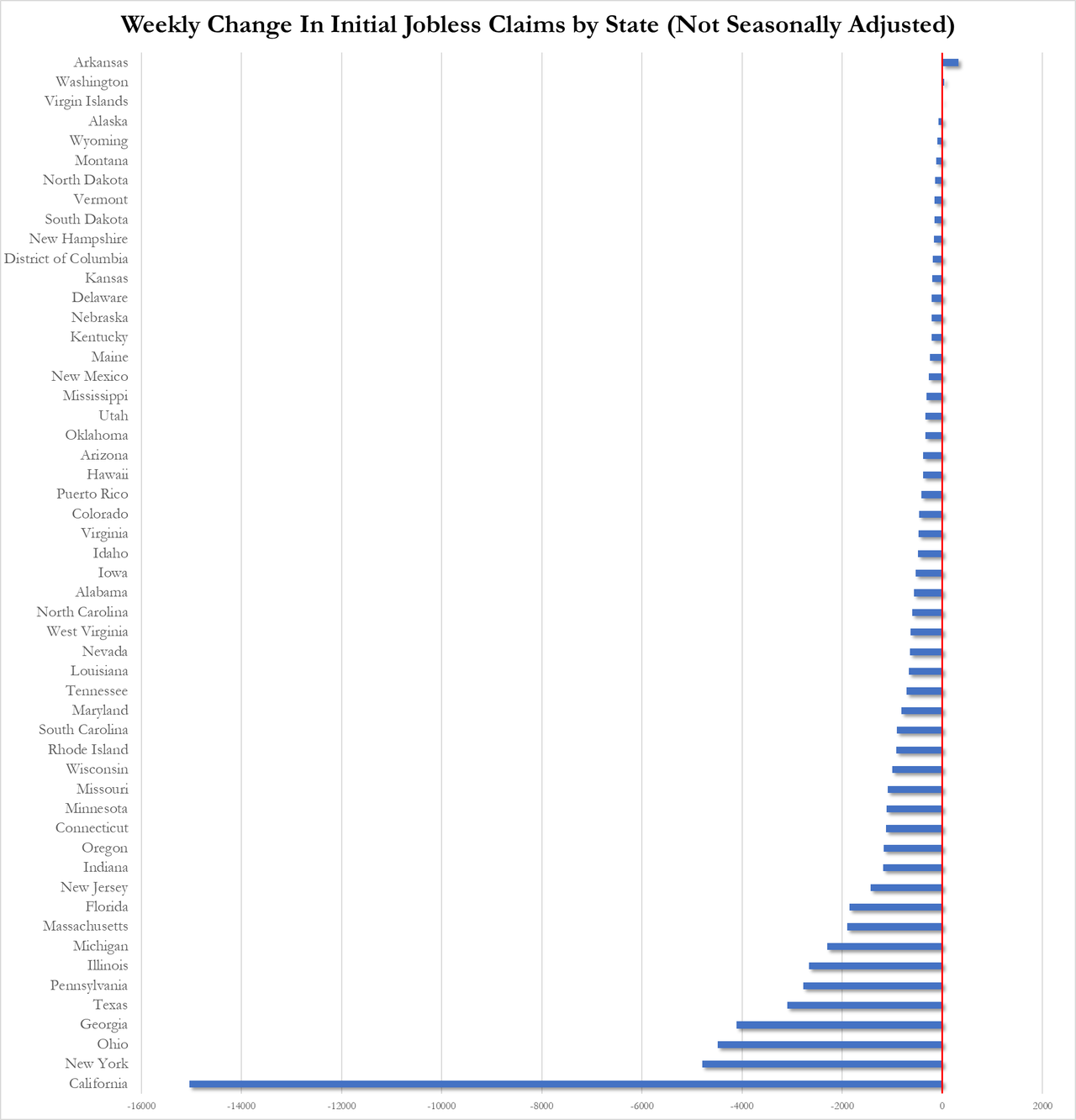

- 08:30: Jan. Initial Jobless Claims, est. 205,000, prior 190,000

- Continuing Claims, est. 1.66m, prior 1.65m

- 08:30: Dec. Advance Goods Trade Balance, est. -$88.1b, prior -$83.3b, revised -$82.9b

- 08:30: Dec. Retail Inventories MoM, est. 0.2%, prior 0.1%

- Wholesale Inventories MoM, est. 0.5%, prior 1.0%

- 08:30: Dec. Chicago Fed Nat Activity Index

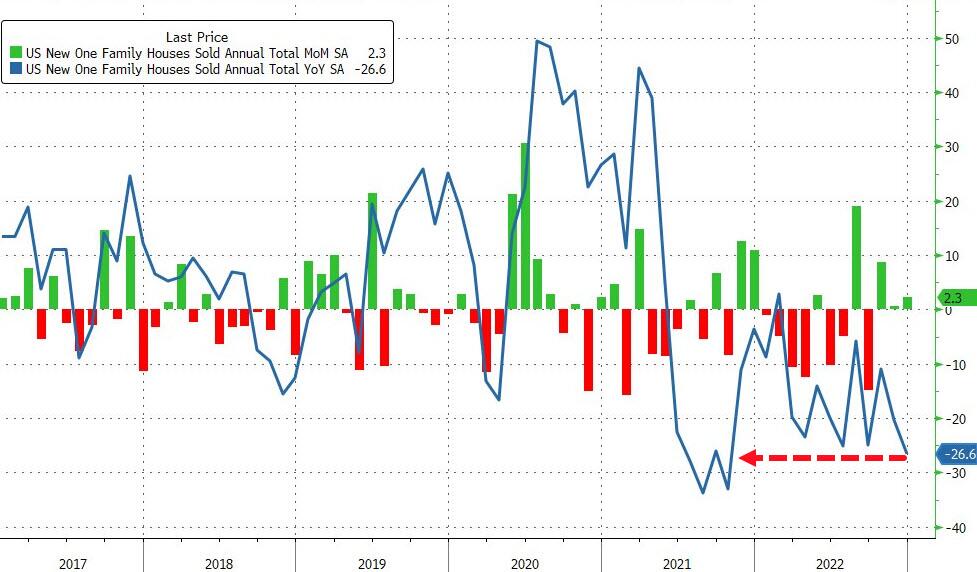

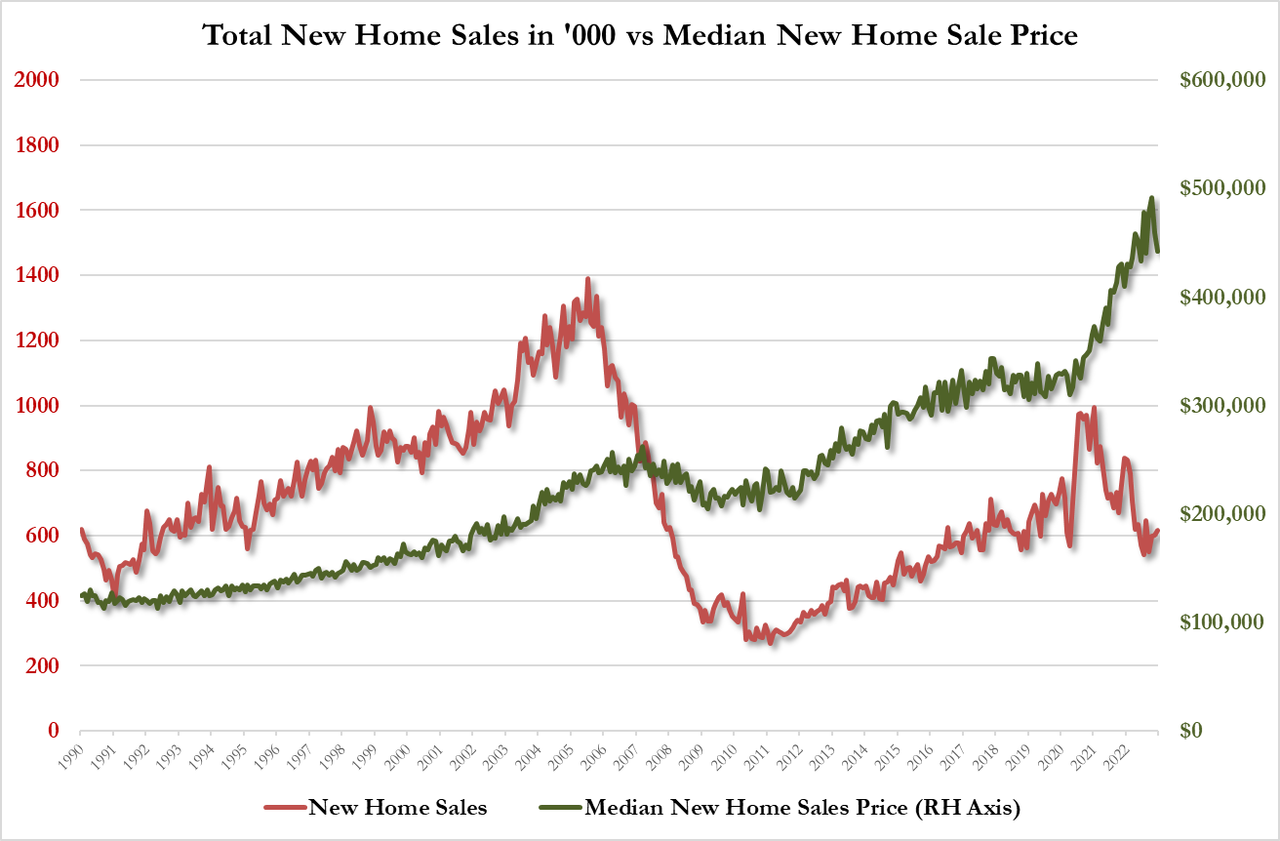

- 10:00: Dec. New Home Sales MoM, est. -4.4%, prior 5.8%

- New Home Sales, est. 612,000, prior 640,000

- 11:00: Jan. Kansas City Fed Manf. Activity, est. -8, prior -9

DB’s Jim Reid concludes the overnight wrap

Morning from Milan. Yet another first time since the pandemic started trip. Always nice to be back. I’d almost forgotten how good the food is here! It was a fairly positive macro dinner with clients generally constructive. It was unique to be in Italy and see no-one really too concerned about Italy credit quality which is testimony to the various EU/ECB packages both pre and post the pandemic and also impressive given how far the ECB has come on rates and how far it still has to go.

With markets overall on the calm side too at the moment we’re getting our mini vol from entering earnings crossfire season where a big name’s quarterly report can pick you off. Indeed, sentiment yesterday was heavily influenced at first by Microsoft’s disappointing cloud sales outlook from after the bell on Tuesday night. The company’s shares were down around -4.5% soon after the open, before sentiment steadily improved as the day progressed. By the end of the day, it had clawed its way back up to have only lost -0.59%. More broadly, the Nasdaq and S&P 500 hit intraday lows of -2.34% and -1.69%, respectively, before closing at -0.18% and -0.02%. So a decent recovery.

After the close, we then heard from Tesla and IBM. Tesla reported adjusted earnings of $1.19 EPS ($1.12 EPS expected) as it sought to boost output quickly to achieve its previous guidance of 1.8mn vehicles delivered this year. In after-market trading it then advanced +5.5%, especially after Elon Musk said that he expected demand would remain strong despite an expected contraction and that there was a new “next-generation” vehicle that would be announced in March. IBM (-2.0% after-market) also beat earning expectations at $3.60 EPS (consensus was $3.58), and increased its sales forecast whilst announcing they would be cutting headcount by 1.5%. Against this backdrop, US equity futures are looking more positive this morning, with those on the S&P 500 (+0.12%) and the NASDAQ 100 (+0.35%) both higher.

With the S&P 500 finishing the day largely unchanged, 12 of 24 industry groups were in positive territory for the day. Telecoms (+2.50%), banks (+1.17%), insurance (+0.78%), and food & beverage (+0.73%) outperformed, whereas transports (-1.43%) and utilities (-1.36%) were the biggest laggards. Europe closed before the last of the rally in the US, with the STOXX 600 finishing down -0.29%. The STOXX Technology index was similarly down -1.66% at the lows before staging a late recovery itself that only left it down -0.13%.