jan 25 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSED: UP $7.55 at $1941.55

SILVER PRICE CLOSED: UP $0.19 to $23.84

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1945.95

Silver ACCESS CLOSE: 23.90

Bitcoin morning price:, 22683 DOWN 290 DOLLARS

Bitcoin: afternoon price: $22912 DOWN 67 dollars

Platinum price closing $1042.90 DOWN $15.10

Palladium price; closing 1702.60 DOWN $40.15

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,605.03 UP $1591 CDN dollars per oz

BRITISH GOLD: 1569.98 DOWN 1.68 pounds per oz

EURO GOLD: 1782.34 UP 3.77 euros per oz

EXCHANGE: COMEX

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JANUARY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,933.900000000 USD

INTENT DATE: 01/24/2023 DELIVERY DATE: 01/26/2023

FIRM ORG FIRM NAME ISSUED STOPPED

435 H SCOTIA CAPITAL 52

624 H BOFA SECURITIES 178

661 C JP MORGAN 55 10

737 C ADVANTAGE 2 3

880 H CITIGROUP 186

TOTAL: 243 243

JPMorgan stopped 10/243

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR JAN/2023. CONTRACT: 243 NOTICES FOR 24,300 OZ or 0.7558 TONNES

total notices so far: 6327 contracts for 632,700 oz (19.679 tonnes)

SILVER NOTICES: 7 NOTICE(S) FILED FOR 35,000 OZ/

total number of notices filed so far this month 987 for 4,965,000 oz

END

GLD

WITH GOLD UP $7.55

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 0.28 TONNES INTO THE GLD //

INVENTORY RESTS AT 917.34 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 19 CENTS

AT THE SLV// :/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE DEPOSIT OF 2.3 MILLION OZ INTO THE SLV//// WHAT A MASSIVE FRAUD!!!

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 521 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

IN THE LAST TWO DAY: A GAIN OF 22.3 MILLION OZ (WHERE ON EARTH WERE THEY GOING TO GET THAT QUANTITY OF METAL)

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 253 CONTRACTS TO 134,922 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE GOOD GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.21 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. FOR THE PAST MONTH, OUR BANKERS HAVE RETURNED TO BEING NET SHORT AND THUS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.21. AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD A HUGE SIZED GAIN ON OUR TWO EXCHANGES OF 894 CONTRACTS. AS WELL, WE HAD 0 NOTICES FOR EXCHANGE FOR RISK TRANSFER (0 OZ. ) AS THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 7.25 MILLION OZ. WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS( 375 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4,055. MILLION OZ FOLLOWED BY TODAY’S QUEUE. JUMP OF 25,000 OZ//NEW STANDING 5.005 MILLION OZ + 7.25 MILLION OF EXCHANGE FOR RISK//TOTAL STANDING 12.255 MILLION OZ//// V) GOOD SIZED COMEX OI GAIN/ GOOD EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –257

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTRACTS for 16 days, total 9340 contracts: OR 46.700 MILLION OZ PER DAY. (583 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 46.700 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 46.700 MILLION OZ (CORRECTED)

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 253 WITH OUR $0.21 GAIN IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 375 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN OF 4.055 MILLION OZ FOLLOWED BY TODAY’S 25,000 OZ. JUMP / //NEW STANDING RISES TO 5.005 MILLION OZ + EFR 7.25 MILLION = 12.255 MILLION OZ. .. WE HAVE A VERY STRONG SIZED GAIN OF 894 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 7 NOTICE(S) FILED TODAY FOR 35,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2565 CONTRACTS TO 499,927 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED -684 CONTRACTS.

.

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 2565 CONTRACTS) DESPITE OUR STRONG $7.35 GAIN IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR JAN. AT 2.1710 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 198 CONTRACTS OR 19,800 OZ //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). NEW STANDING 20.227 TONNES

YET ALL OF..THIS HAPPENED WITH OUR $7.35 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING

WE HAD A SMALL SIZED LOSS OF 737 OI CONTRACTS (2.297 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1828 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 499,927

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 737 CONTRACTS WITH 2565 CONTRACTS DECREASED AT THE COMEX AND 1828 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 737 CONTRACTS OR 2.297 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1828 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2565) TOTAL LOSS IN THE TWO EXCHANGES 737 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) SMALL INITIAL STANDING AT THE GOLD COMEX FOR JAN. AT 2.1710 TONNES FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 19,800 OZ /NEW STANDING 20.227 TONNES///3) ZERO LONG LIQUIDATION //4) FAIR SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN :

61,664 CONTRACTS OR 6,166,400 OZ OR 191.800 TONNES 16 TRADING DAY(S) AND THUS AVERAGING: 3854 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES:191.800 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 191.800/3550 x 100% TONNES 5.40% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 191.800 TONNES INITIAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A SMALL SIZED 253 CONTRACTS OI TO 134,922 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 375 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 375 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1219 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 519 CONTRACTS AND ADD TO THE 375 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 628 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 3.14 MILLION OZ//

OCCURRED DESPITE OUR 21 CENT GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//CORN

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED //Hang Seng CLOSED /The Nikkei closed UP 95.82 PTS OR 0.35% //Australia’s all ordinaries CLOSED DOWN 0.29% /Chinese yuan (ONSHORE) closed //OFFSHORE CHINESE YUAN UP TO 6.7794// /Oil DOWN TO 80.84 dollars per barrel for WTI and BRENT AT 86.04 / Stocks in Europe OPENED ALL RED ONSHORE YUAN TRADING XXXX LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING XXX AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2565 CONTRACTS DOWN TO 499,927 DESPITE OUR GAIN IN PRICE OF $7.35

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON-ACTIVE DELIVERY MONTH OF JAN… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1828 EFP CONTRACTS WERE ISSUED: ;: , . 0 FEB: 1828 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1828 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 737 CONTRACTS IN THAT 1828 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 2565 CONTRACTS..AND THIS TINY SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR ADVANCE IN PRICE OF $7.35. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG .

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING Jan (20.227)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes(TOTAL THIS YEAR 656.076 TONNES

JAN/2023: 20.227 tonnes

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $7.35) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD ONLY A SMALL SIZED LOSS OF 737 CONTRACTS ON OUR TWO EXCHANGES // WE HAVE LOST A TOTAL OI OF .1648 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JAN. (2.1710 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 19,800 oz OR 0.5536 TONNES… ALL OF THIS WAS ACCOMPLISHED WITH OUR SMALL RISE IN PRICE TO THE TUNE OF $7.35.

WE HAD – 684 CONTRACTS COMEX TRADES REMOVED FROM OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 737 CONTRACTS OR 73700 OZ OR 2.297 TONNES

Estimated gold comex today 238,560//fair//

final gold volumes/yesterday 299,543///good

INITIAL STANDINGS FOR JAN 2023 COMEX GOLD //JAN 25//

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 12,024.474. oz HSBC 374 kilobars . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | 32.15 oz Brinks one kilobar |

| No of oz served (contracts) today | 243 notice(s) 24,300 OZ 0.7558 TONNES |

| No of oz to be served (notices) | 176 contracts 17,600 oz 0.5536 TONNES |

| Total monthly oz gold served (contracts) so far this month | 6327 notices 632700 19.679 TONNES* *new record for a January |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into Brinks 32.15 oz

(one kilobar)

total deposits: 32.15 oz

customer withdrawals: 1

i) Out of HSBC: 12,024.474. oz (374 kilobars)

Total withdrawals: 12024.474 oz

total in tonnes: 0.374 tonnes

Adjustments:0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of JANUARY we have an oi of 421 contracts having gained 95 contracts

We had 103 notices served on Tuesday, so we gained 198 contracts or an additional 19,800 oz(0.6158 tonnes) will stand for delivery in this

very non active delivery month of January. (queue jump).

February lost 34,445 contacts to 146,704 (looks like Feb. is going to be a huge delivery month

March gained 38 contracts to stand at 1182.

April gained 27,042 contracts up to 288,560

We had 243 notice(s) filed today for 133,757 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 55 notices were issued from their client or customer account. The total of all issuance by all participants equate to 243 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 10 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN. /2023. contract month,

we take the total number of notices filed so far for the month (6327 x 100 oz , to which we add the difference between the open interest for the front month of (JANUARY 421 CONTRACTS) minus the number of notices served upon today 243 x 100 oz per contract equals 650,300 OZ OR 20.227 TONNES the number of TONNES standing in this non active month of January. This is a new record for gold standing in the month of January.

thus the INITIAL standings for gold for the JAN contract month:

No of notices filed so far (6327 x 100 oz+ (421 OI for the front month minus the number of notices served upon today (243} x 100 oz} which equals 650,300 oz standing OR 20.227 TONNES in this NON active delivery month of JAN..

TOTAL COMEX GOLD STANDING: 20.227 TONNES (A HUGE STANDING FOR METAL AND A NEW RECORD FOR ANY JANUARY MONTH )//COMEX RUNNING OUT OF PHYSICAL TO SERVE UPON OUR LONGS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

we had one adjustment of 110,631.591 oz Brinks

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,910,035.089 OZ 59.41 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,314,858.672 OZ

TOTAL REGISTERED GOLD: 11,020,481.037 OZ (342.78 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 11,294,377.788 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,110446 OZ (REG GOLD- PLEDGED GOLD) 283.37 tonnes//rapidly declining

END

SILVER/COMEX

JAN 25/2023//INITIAL JAN. SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 586,499.848 oz Brinks CNT Delaware JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 979,124.672 oz CNT Delaware |

| No of oz served today (contracts) | 7 CONTRACT(S) (35,000 OZ) |

| No of oz to be served (notices) | 1 contracts (5,000 oz) |

| Total monthly oz silver served (contracts) | 1000 contracts (5,000,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i) Into CNT 599,916.022 oz

ii) Into Delaware: 379,208.650 oz

Total deposits: 979,124.672 oz

JPMorgan has a total silver weight: 150.528 million oz/293.182 million =51.23% of comex .//dropping fast

Comex withdrawals: 4

i) Out of Delaware: 480.498 oz

ii) Out of Brinks 114,616.570 oz

iii) Out of CNT 35,451.520 oz

iv) Out of JPMorgan: 431,481.160 oz

Total withdrawals; 586,499.748 oz

adjustments: 1/JPMorgan: dealer to customer//4,951.000 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 33.195 MILLION OZ (declining rapidly).TOTAL REG + ELIG. 292,.89 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JAN

silver open interest data:

FRONT MONTH OF JAN/2023 OI: 8 CONTRACTS HAVING LOST 2 CONTRACT(S.). WE HAD 7 NOTICES

FILED ON TUESDAY SO WE GAINED 5 CONTRACT(S) OR AN ADDITIONAL 25,000 OZ WILL STAND OVER HERE

FEB> LOST 23 CONTRACTS TO 194 CONTRACTS

March LOST 1488 CONTRACTS UP TO 109,536 contracts

TOTAL NUMBER OF NOTICES FILED FOR TODAY:7 for 35,000 oz

Comex volumes// est. volume today 56.523//fair

Comex volume: confirmed yesterday: 56,539 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 1000 x 5,000 oz = 5,000,000 oz

to which we add the difference between the open interest for the front month of JAN(8) and the number of notices served upon today 7 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JAN./2023 contract month: 1000 (notices served so far) x 5000 oz + OI for the front month of JAN (8 – number of notices served upon today (7) x 500 oz of silver standing for the JAN. contract month equates 5.005 million oz + 7.25 MILLION OZ ( EXCHANGE FOR RISK) = 12.255MILLION OZ//(TOTAL OZ OF SILVER STANDING).

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:52,938// est. volume today// fair

Comex volume: confirmed yesterday: 96,020 contracts ( very good/excellent)

END

GLD AND SLV INVENTORY LEVELS

JAN 25/WITH GOLD UP $7.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 917.34 TONNES

JAN 24/WITH GOLD UP $7.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 23/WITH GOLD UP $0.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.63 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 20/WITH GOLD UP $4.75 TODAY;BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 912.43 TONNES

JAN 19/WITH GOLD UP $16.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES INTO THE GLD///INVENTORY RESTS AT 910.98TONNES

JAN 18/WITH GOLD DOWN $1.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.9 TONNES FROM THE GLD////INVENTORY RESTS AT 909.24 TONNES

JAN 17/WITH GOLD DOWN $11.45 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.14 TONNES

JAN 13/WITH GOLD UP $22.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD///INVENTORY RESTS AT 912.14 TONNES

JAN 12/WITH GOLD UP $20.55 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 912.43 TONNES

JAN 11/WITH GOLD UP $1.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

DEC 30/WITH GOLD UP $.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 29//WITH GOLD UP $8.35 TODAY:; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 28/WITH GOLD DOWN $6.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE DEPOSIT OF 5.50 TONNES INTO THE GLD..//INVENTORY REST S AT 918.51 TONNES

DEC 27/WITH GOLD UP $18.15 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 913.01 TONNES

DEC 23/WITH GOLD UP $19,15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES/

DEC 22/WITH GOLD DOWN $29.35 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 21/WITH GOLD FLAT TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 913.88 TONNES

DEC 20/WITH GOLD UP $27.05: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES INTO THE GLD////INVENTORY RESTS AT 912.14 TONNES

DEC 19/WITH GOLD DOWN $2.10: HUGE CHANGES IN GOLD INVENTORY AT THE GLD> A BIG WITHDRAWAL OF 3.47 TONNES FROM THE GLD//INVENTORY RESTS AT 910.41 TONNES

DEC 16/WITH GOLD UP $12.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 15//WITH GOLD DOWN $31.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 911.56 TONNES

DEC 14/WITH GOLD DOWN $6.20: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 912.72 TONNES

DEC 13/WITH GOLD UP $32.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD///INVENTORY RESTS AT 910.41

DEC 12/WITH GOLD DOWN $17.60: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

DEC 9/WITH GOLD UP $8.90//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

Dec 8/WITH GOLD UP $4.05, OVER THE PAST 3 WEEKS WE LOST 2.04 TONNES//INVENTORY RESTS AT 908.09 TONNES

GLD INVENTORY: 917.34 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JAN 25/WITH SILVER UP 19 CENTS TO TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.3 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 521.000 MILLION OZ

JAN 24/WITH SILVER UP 21 CENTS TODAY: WHAT!! A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 20 MILLION OZ INTO THE SLV/( OCCURRED (LATE LAST NIGHT)//INVENTORY RESTS AT 518.70 MILLION OZ//

JAN 23/WITH SILVER DOWN 40 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.4 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 498.7 MILLION OZ//

JAN 20.WITH SILVER UP 9 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 750,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 497.300 MILLION OZ

JAN 19/WITH SILVER UP 24 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 498.05 MILLION OZ

JAN 18/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 8.15 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 498.05 MILLION OZ///

JAN 17/WITH SILVER DOWN 35 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 13/WITH SILVER UP 46 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.5 MILLION OZ FROM THE SLV..//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 12/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 508.700 MILLION OZ/

JAN 11/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 508.700MILLION OZ

JAN 10/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ

JAN 9/WITH SILVER DOWN 9 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 6/WITH SILVER UP 54 CENTS TODAY;BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.20 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 5/WITH SILVER DOWN 50 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.10 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 505.45 MILLION OZ//

JAN 4/WITH SILVER DOWN 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 506.55 MILLION OZ/

JAN 3/WITH SILVER UP 24 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: STRANGE: A WITHDRAWAL OF 1.2 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 507.85 MILLION OZ/

DEC 30/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 29/ WITH SILVER UP $0.63 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 28//WITH SILVER DOWN 46 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.715 MILLION OZ INTO THE SLV///..INVENTORY RESTS AT 509.050 MILLION OZ

DEC 27/WITH SILVER UP 34 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 507.350 MILLION OZ//

DEC 23/WITH SILVER UP 29 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT507.900 MILLION O//

DEC 22/WITH SILVER DOWN 53 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 21/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.0 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 20/WITH SILVER UP 105 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:: A DEPOSIT OF 700,000 OZ INTO THE SLV///INVENTORY RESTS AT 509.90 MILLION OZ//

DEC 19/WITH SILVER DOWN 13 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.05 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.20 MILLION OZ//

DEC 16/WITH SILVER UP 2 CENTS; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.85 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 508.15 MILLION OZ//

DEC 15/WITH SILVER DOWN 78 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF EXACTLY 2.00 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 510.000 MILLION OZ

DEC 14/WITH SILVER UP 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 512.000 MILLION OZ//

DEC 13/WITH SILVER UP 59 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 600,000 OZ FROM THE SLV////INVENTORY RESTS AT 513.900 MILLION OZ//

DEC 12/WITH SILVER DOWN 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 514.500 MILLION OZ//

DEC 9/WITH SILVER RISING 77 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.2 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 514.500 MILLION OZ.

DEC 8/WITH SILVER RISING 34 CENTS TODAY: OVER THE PAST 3 WEEKS, WE HAVE GAINED A STRONG: 44.777 MILLION OZ/INVENTORY RESTS AT 516.700 MILION OZ.

CLOSING INVENTORY 521.000 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

A must read:

Indians have always been a hoarder of gold; now they are settingh records for importing silver. They have imported more than 1/2 of annual production

(SchiffGold)

Indian Silver Imports Set Record In 2022

TUESDAY, JAN 24, 2023 – 05:45 PM

India’s love for gold is well-known. It is the second largest gold-consuming country in the world behind China. But Indians also have an affinity for silver.

Last year, silver imports into India hit a new record of 304 million ounces. That crushed the previous import high of 260 million ounces set in 2015.

More than half of the silver flowing into India is used in jewelry and silverware, and about one-third of India’s silver demand comes from investors in physical metal including silver bars and silver coins.

According to a report published by the Silver Institute, since 2010, Indian retail investors have bought around 730 million ounces of silver (22,700 tons). To put that into perspective, that represents about 90% of 2022’s total global silver mine production.

Over the last decade, the only years that silver investment demand fell in India were in 2016 and during the pandemic in 2020.

Silver investment in India was muted during the pandemic years but charted a healthy rebound in 2022. Investment in physical silver jumped to 79.4 million ounces last year, the highest level since 2015.

Indian silver demand is highest in rural and semi-urban areas. According to the Silver Institute report, this is a reflection of the relatively low entry price.

Furthermore, even fabricators and wholesalers buy silver as an investment during periods of low prices to be later converted into jewelry or silverware, or just to sell back when the price is high to take profits. Given the profile of investors, physical silver investment has so far been largely immune to competition from other asset classes, such as equities.”

The proliferation of silver exchange-traded products (ETP) in India has also spurred investment demand in the white metal.

The first Indian exchange-traded product was launched in September 2021. Currently, there are seven ETPs and five silver ETP Fund-of-Funds (FoFs, which invest in ETPs). As of the end of 2022, silver ETF holdings in India stood at an estimated 8 million ounces.

The Indian government’s crackdown on the gold market has boosted silver investment. According to the Silver Institute report, “The Indian government’s ongoing tough stance towards unaccounted money and the increased vigilance on gold transactions have benefited silver as investors have moved out of gold and in favor of silver.”

The Silver Institute report underscores the importance of India in the global silver market.

As the world’s sixth-largest economy and foremost silver fabricator, India also plays an essential role in silver and gold investment demand, historically recognized in that market as savings and investment assets, a reflection of the low penetration of banking and other financial products. Today, with new investment products available to Indian investors, India’s role in silver investment has the potential to grow even further.”

Increasing demand for silver in India is good news for the broader silver market.

Based on preliminary data, silver demand in 2022 is expected to chart a new all-time high of 1.21 billion ounces. That would be a 16% increase from 2021.

With mine production only projected to increase by 1%, the global silver market is forecast to record a second consecutive annual deficit in 2022. At 194 million ounces, this will be a multi-decade high and four times the level seen in 2021.

end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

END

3. Chris Powell of GATA provides to us very important physical commentaries//

Jim Rickards is correct: huge demand for physical gold coming from central banks

(Jim Rickards)

Jim Rickards: Gold’s breakout is central banking’s doing, not inflation’s

Submitted by admin on Tue, 2023-01-24 11:51Section: Daily Dispatches

By James G. Rickards

The Daily Reckoning, Baltimore

Monday, January 23, 2023

Most assets have a poor record over the past year. Gold is one of the few assets that posted a gain — not a major gain, but a gain.

Gold has really taken off since late October, from below $1,630 to almost $1,930 today. That’s a major move. What’s going on?

You might want to argue that it has to do with inflation. The trouble with that argument is that (official) inflation has been coming down for the past few months. Meanwhile, gold seemed to massively underperform with respect to the very serious inflation we saw earlier last year.

So again, why are we seeing a gold spike now? The most likely answer lies with central banks and geopolitics.

Central banks as a whole, led by Russia and China, purchased 399 metric tonnes of gold in the third quarter of 2022. (Fourth-quarter data are not yet available.)

That’s the most gold ever purchased by central banks in a single calendar quarter. It represents over 1% of all the gold held by all central banks combined.

If that pace continues or increases, it would amount to an increase of over 4% per year in central bank gold reserves. …

… For the remainder of the analysis:

Gold’s Breakout: It’s Not the Inflation

end

As we explained a few days ago China and Russia have been importing gold like crazy. Switzerland is the world’s greatest refiners of gold

We now know that China and Russia have accumulated 50,000 tonnes for the former and 10,000 tonnes for the latter

(Reuters)

Switzerland sent 524 tonnes of gold to China last year, most since 2018

Submitted by admin on Tue, 2023-01-24 14:55Section: Daily Dispatches

By Peter Hobson

Reuters

via Nasdaq.com, New York

Tuesday, January 24, 2023

LONDON — Swiss exports of gold to countries including China, Turkey, Singapore, and Thailand surged to multi-year highs last year, Swiss customs data showed today, as low prices boosted demand from consumers in Asia and the Middle East.

Rising interest rates caused many financial investors in Europe and North America to sell gold in 2022, releasing large amounts of metal from storage and pushing down prices.

This allowed bullion to flow to Asian markets, which are more focused on retail of jewellery and small gold bars to consumers who typically buy more when prices drop. Economic instability also spurred demand for gold, which many see as a safe investment, particularly in Turkey, where inflation has rocketed.

Switzerland is the world’s biggest gold refining and transit hub. It imports bullion from mines and storage centres around the world for processing and re-export. …

… For the remainder of the report:

end

4. Other gold/silver commentaries

END

5.IMPORTANT COMMENTARIES ON COMMODITIES:COPPER

.

end

6.CRYPTOCURRENCY COMMENTARIES/

END

.

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: XXX TO CLOSED

OFFSHORE YUAN: 6.7794

SHANGHAI CLOSED

HANG SENG CLOSED

2. Nikkei closed UP 95.82 PTS OR 0.35%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 101.77 Euro FALLS TO 1.0867 DOWN 4 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.4046!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 129.69/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: XX-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.086%***/Italian 10 Yr bond yield FALLS to 3.986%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.086…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.101//

3j Gold at $1925/35//silver at: 23.45 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 2/100 roubles/dollar; ROUBLE AT 68.98//

3m oil into the 80 dollar handle for WTI and 86 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 129.69/10 YEAR YIELD AFTER BREAKING .54% RISES TO .446% ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9215– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0015 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.425% DOWN 4 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.581 DOWN 4 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,82…

GREAT BRITAIN/10 YEAR YIELD: 3.3281 % DOWN 8 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Slide On Ugly Microsoft Outlook, Renewed War Escalation Fears

WEDNESDAY, JAN 25, 2023 – 07:55 AM

US equity futures slumped on Wednesday after Microsoft started off the tech giants’ earnings parade by pulling off the old pump and dump, first jumping on Azure/Cloud results which beat estimates, but then erasing all gains and slumping during the company’s conference call after the company’s guidance disappointed, forecasting slower earnings and weaker demand (separately, hours later customers reported difficulties across multiple regions in accessing Microsoft 365 services, which the company attributed to networking issues). Earnings reports from companies such 3M, Boeing and chipmaker Texas Instruments also reinforced concerns about the health of corporate America and added to investors’ jitters as they await updates from the likes of Tesla and IBM. Fears also grew that a decision to send German and US tanks to Ukraine would provoke an escalation in the war.

As a result, contracts on the tech-heavy Nasdaq fell 1.3% at 7:15 a.m. ET while S&P 500 futures dropped 0.8%, and traded right around 4,000. The Bloomberg Dollar Spot Index was little changed, leading to mixed trading in Group-of-10 currencies. Treasuries edged higher, mirroring gains in most UK and German government bonds. Brent crude was little changed, while gold and Bitcoin fell.

Southwest promises refunds over snow chaos

In premarket trading, all eyes were on Microsoft which fell after saying revenue growth in its Azure cloud-computing business will decelerate in the current period and warned of a further slowdown in corporate software sales. Amazon and Alphabet also fell in sympathy, dragging other cloud stocks lower (Amazon.com -1.6% and Alphabet -1.1%; Snowflake -3.1%, Datadog -4.0%, Adobe -1.4). Texas Instruments suffered its first sales decline since 2020 and gave a tepid forecast for the current quarter. Microsoft comprises about 12% of the Nasdaq 100, while Texas Instruments has a weighting of 1.4%. Here are other notable premarket movers:

- Enphase Energy (ENPH US) declines 4% after it was cut to neutral from overweight at Piper Sandler as demand for residential solar loans dipped more than the broker expected.

- Precigen (PGEN US) drops 16% after an offering of shares priced at $1.75 apiece, representing a 20% discount to the last close. Proceeds to be used to fund the development of product candidates and for other general corporate purposes.

- Block (SQ US) declines 4% as Oppenheimer cuts the stock to market perform from outperform, saying the firm looks less defensively-positioned than other payments names.

- Intuitive Surgical’s (ISRG US) falls 8.9% as the medical tech firm’s quarterly results are overshadowed by the company saying it won’t launch a new multiport robotic system in FY23, which analysts say removes a positive catalyst for the stock.

- Capital One’s (COF US) slumps 3.3% following the release of results. Its earnings slightly missed expectations and analysts flag a quicker-than-expected acceleration in net charge-offs for the company.

- Keep an eye on Stryker (SYK US) as it was initiated by KeyBanc at sector weight, which says the US med-tech firm’s valuation “reflects an above-average growth rate with some risk of mean reversion over time.”

A weak earnings outlook, fears of US recession as well as the potential escalation in the Ukraine-Russia war were all contributing to the market pullback, according to Kenneth Broux, a strategist at Societe Generale. “The market is definitely worried about slowing earnings growth especially on tech, so there has been a sense the market wants to keep selling tech and the dollar,” Broux said. “But a huge tail risk now is what happens in Ukraine, if there is an escalation in the conflict and Europe gets drawn into the conflict.”

While today’s drop will hurt, the Nasdaq 100 Index has surged 8.3% this year, on track for the best January since 2019. Expectations that the Federal Reserve will soon pivot away from its hawkish policy have aided the rally, though strategists are increasingly preferring non-US equities this year as they hunt for cheaper valuations and grow concerned about a US recession. Investors are now parsing earnings statements for the impact of the economic slowdown on results.

“The main focus is clearly on US big tech,” said Fabio Caldato, a partner at Olympia Wealth Management. “How can those bulls in a China shop reassure the financial community? Just showing growth. We remain very cautious on this aspect and prefer to underweight the whole sector.”

Next, all eyes will be on Tesla when the electric-car maker reports results after the market closes on Wednesday. Investors will focus on demand, profitability and 2023’s expected pace of deliveries. They are also keen to learn whether Chief Executive Officer Elon Musk will name a new CEO of Twitter.

In Europe, the Stoxx 600 was down 0.6% and on course for its first back-to-back declines of the year. Shares in major European software firms such as SAP SE and Sage Group Plc. feeling the heat from Microsoft and Dutch chip-tool maker ASML Holding NV falling after posting a profit miss. Here are the most notable European movers:

- EasyJet shares rise as much as 12% after the budget carrier reported 1Q revenue that was 8% ahead of consensus and projected strong trends will continue into the second quarter

- Aviva shares gain as much as 3.5%, the most since October, with JPMorgan saying the general insurance underwriting update from the group will provide some reassurance

- Caverion shares rise as much as 4.1% after the Bain-led consortium increased its offer for the Finnish building-maintenance-services firm following a rival bid from private equity firm Triton

- Hill & Smith rises as much as 2.2% after delivering an unscheduled trading update guiding to operating profit above expectations, which Jefferies describes as “pleasing to read”

- ASML shares fall as much as 2.3%, trimming a recent rally, after the Dutch chip-tool giant’s profitability target missed higher Street expectations despite its bullish sales growth forecast for 2023

- Netcompany shares plunge as much as 23%, the most on record, after the Danish IT consultant’s Ebitda margin guidance for 2023 missed expectations

- Aroundtown shares dropped as much as 7.4% after Societe Generale cut its recommendation to sell from buy as part of a more cautious view on REITs

- Gjensidige shares fall as much as 9.9% with analysts saying the Norwegian insurer’s results were weak across the board and that the lack of a special dividend will disappoint

Earlier in the session, Asian stocks headed for a fourth straight daily gain as tech stocks rose amid lighter trading volumes and holidays in China and Hong Kong. The MSCI Asia Pacific Index advanced as much as 0.4% to its highest since early June. Samsung Electronics and SK Hynix were among the biggest contributors to the gauge’s advance as Korea traders returned from the Lunar New Year holidays. “With the global growth outlook narrative shifting more toward a soft landing rather than recession, we are seeing the tech sector come back in favor for now,” said Charu Chanana, strategist at Saxo Capital Markets. “But caution is warranted as inflation risks are back on the horizon with China’s reopening.”

Tech investors also assessed Microsoft’s second-quarter earnings release, which showed profit beat estimates although the company gave a downbeat revenue forecast. Traders are now turning their attention to Tesla’s result announcement later Wednesday. Singapore stocks led gains in Asia Pacific alongside their South Korean peers.

Japanese stocks rose as investors continued to assess the overall economy and shifted their focus to upcoming earnings. The Topix rose 0.4% to 1,980.69 at the close in Tokyo, while the Nikkei advanced 0.4% to 27,395.01. The yen weakened 0.2% to 130.44 per dollar. Keyence contributed the most to the Topix’s gain, increasing 1.7%. Out of 2,161 stocks in the index, 1,342 rose and 699 fell, while 120 were unchanged. “Global economic recession risk has declined sharply as China and Europe demand is expected to improve this year,” said Daniel Yoo, head of global asset allocation at Yuanta Securities Korea. “Overall tech demand including capex investments of global corporations isn’t slowing down much.”

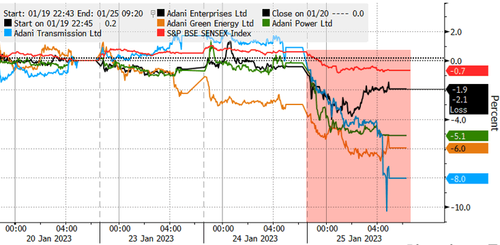

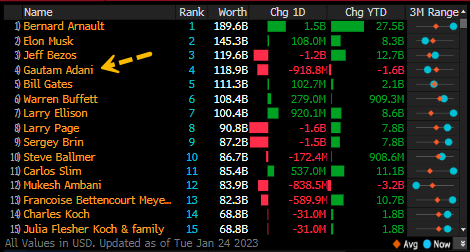

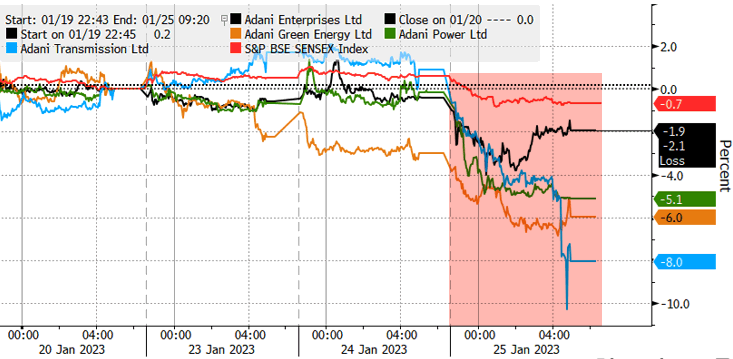

Stocks in India fell ahead of the expiry of monthly derivative contracts on Wednesday. Adani Group shares were among major decliners after activist investor Hindenburg Research shorted the group. The S&P BSE Sensex slid 0.9% to 60,404.47, as of 11:09 a.m. in Mumbai, while the NSE Nifty 50 Index declined 1%. All but one of BSE Ltd.’s 20 sector sub-indexes declined, led by a gauge of service industry stocks. HDFC Bank contributed the most to the Sensex’s decline, decreasing 1.8%. All but three of 30 shares in the Sensex dropped. All stocks controlled by Adani Group fell after Hindenburg Research accused firms owned by Asia’s richest man of “brazen” market manipulation and accounting fraud. Representatives for the Adani Group didn’t immediately respond to calls and emails seeking comment, saying the company would issue a statement in response later.

Meanwhile, Australian stocks dropped after data showed that domestic inflation accelerated to the fastest pace in 32 years in the final three months of 2022. Trading volumes have been light in Asia this week as markets in China, Hong Kong, Taiwan and Vietnam remain closed for the new-year break. A blackout period on communications ahead of the Federal Open Market Committee’s policy meeting next week has supported risk appetite, with the MSCI Asia gauge up about 25% from an October low

In FX, the Bloomberg Dollar Index was little changed even as the greenback advanced against most of its Group-of-10 peers, with notable outperformance in the Aussie dollar after CPI surprised to the upside. Kiwi dollar is the weakest among the G-10’s.

- The pound fell for a third day and gilts rose, led by the belly, after data showed UK factories’ fuel and raw material costs rose at the slowest pace in almost a year. Input prices rose 16.5% in December from a year ago, down from a peak of 24.6% in June. Money markets went to fully price in a 25-basis point rate cut by the Bank of England before the end of the year

- The euro fell a first day in six against the US dollar, though moves were limited to a narrow range. Bunds advanced, outperforming Italian notes.

- The Canadian dollar was little changed while overnight volatility in dollar- loonie rose to its highest level since Jan. 12 as traders position for the Bank of Canada policy decision. The implied breakeven of around 84 pips may be understating the possibility of outsized swings in the pair.

- Australian dollar rose against all of its G-10 peers, to trade at the highest level since August versus the greenback, and the nation’s bonds tumbled after 4Q inflation accelerated to the fastest pace in 32 years in the final three months of 2022. The outcome of 7.8% from a year earlier exceeded forecasts of 7.6% and prompted money markets to price in an interest-rate hike at next month’s central bank meeting.

- Kiwi dollar was the worst G-10 performer as New Zealand inflation held near three-decade high at 7.2% but undershoot RBNZ’s forecast.

In rates, the risk-averse tone benefited bonds, with UK and German 10-year yields falling by 8bps and 6bps respectively. Treasuries also rose as the Treasury curve bull-flattened modestly and as futures extending through Tuesday’s highs, following wider gains across gilts after soft UK factory price inflation data. Treasury yields richer by around 2bp from belly out to long-end with 10-year at 3.42%, lagging gilts by almost 4bp in the sector after sharp rally across UK bonds. The US auction cycle resumes at 1pm with $43b 5-year sale, before Thursday’s $35b 7-year notes; strong 2- year auction Tuesday traded through the WI by 1.3bp.

In commodities, oil prices are little changed with WTI hovering around $80.10. Spot gold falls roughly 0.6% to trade near $1,926/oz

Bitcoin is back below the USD 23k mark, though remains just above the WTD trough set on Monday at USD 22.3k.

On today’s calendar, we get data on US mortgage application (up 7.0%, vs up 27.9% last week). The EIA will release figures on oil inventories at 10:30 a.m. The US will sell $24 billion of two-year floating-rate notes and $36 billion of 17-week bills at 11:30 a.m., followed by $43 billion of five-year notes at 1 p.m. From central banks, the main highlight will be the Bank of Canada’s latest policy decision. Finally, earnings releases include Tesla, Boeing, IBM, AT&T and Abbott Laboratories.

Market Snapshot

- S&P 500 futures down 0.5% to 4,011.25

- MXAP up 0.3% to 169.09

- MXAPJ up 0.2% to 553.07

- Nikkei up 0.4% to 27,395.01

- Topix up 0.4% to 1,980.69

- Hang Seng Index up 1.8% to 22,044.65

- Shanghai Composite up 0.8% to 3,264.81

- Sensex down 1.3% to 60,174.06

- Australia S&P/ASX 200 down 0.3% to 7,468.30

- Kospi up 1.4% to 2,428.57

- STOXX Europe 600 down 0.3% to 451.94

- German 10Y yield little changed at 2.11%

- Euro little changed at $1.0884

- Brent Futures up 0.5% to $86.56/bbl

- Gold spot down 0.3% to $1,930.94

- U.S. Dollar Index little changed at 101.93

Top Overnight News from Bloomberg

- A gauge of German business expectations by the Ifo institute rose to 86.4 in January from 83.2 the previous month. That’s the fourth consecutive improvement and a bigger increase than economists had anticipated. A measure of current conditions slipped, however

- European natural gas headed for a third day of declines as ample supplies and reserves, along with the return of milder weather, help to ease the region’s energy crisis

- With the Federal Reserve’s Feb. 1 interest-rate decision a week away, traders in the options market are contemplating a scenario in which the rate hike it’s expected to deliver ends up being the last one of the tightening cycle

- Japan’s broken bond market continued to throw up anomalies with central bank ownership of some government debt exceeding the amount outstanding, according to its latest data

- Japan’s government cut its monthly view of the economy for the first time since February 2022, reflecting gathering concerns over the outlook for the global economy

A More detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed after the indecisive performance stateside owing to the varied data releases and geopolitical tensions, while the region also digested firmer-than-expected inflation data from Australia and New Zealand. ASX 200 failed to sustain an initial foray above 7,500 with the index subdued by hot CPI data which printed its highest since 1990 and boosted the market pricing for the RBA to continue with its hiking cycle next month. Nikkei 225 gradually edged higher with trade uneventful in the absence of any pertinent drivers although Dai Nippon Printing outperformed after Elliot Management built a stake in the Co. of slightly under 5%. KOSPI was among the biggest gainers on return from the Lunar New Year holiday with the index also driven by strength in top-weighted stock Samsung Electronics.

Top Asian News

- US Secretary of State Blinken is likely to warn China against aiding Russia when visiting Beijing, according to SCMP.

- Australian PM Albanese said there is increased engagement at different levels between Australian and Chinese agencies, according to Reuters.

- North Korea ordered a 5-day lockdown of its capital Pyongyang due to increasing cases of an unspecified respiratory illness, according to South Korean-based NK News.

- Japan lowers its overall economic view in January; first time in 11 months.

- Japanese Gov’t official, citing BoJ’s Kuroda, says the BoJ will resolutely keep monetary environment easy; BoJ aims to regain market functionality by tweaking YCC operations and maintaining an easy monetary environment.

European bourses are pressured across the board, Euro Stoxx 50 -0.6%, after a sluggish post-MSFT start to the session and thereafter a further waning in the general risk tone. Within Europe, a strong update from ASML has been overshadowed by the MSFT pressure, while the likes of Ryanair and IAG are buoyed by easyJet. Stateside, futures are all in the red with the NQ -1.2% lagging and the ES Mar’23 below 4k and its 200-DMA at 3999, to a 3996.5 session trough. NYSE said it is thoroughly examining the glitch and that the exchange ended Tuesday with a normal close, while a regular open is expected on Wednesday, according to Reuters.

Top European News

- German Economy Minister sees 2023 German GDP at 0.2% (vs -0.4% in Autumn forecast); 2023 inflation seen at 6% (vs prev. 7%); “we do not see signs of marked recession as feared by many observers”. In-fitting with earlier reports via the likes of Bloomberg and Reuters in recent sessions.

- French Regulator Set to Provisionally Close Government EDF Offer

- Traders Reverse Course to Bet BOE Will Cut Rates Before Year-End

- UK’s Growth Potential Falls, Reducing Hunt’s Room for Tax Cuts

- Renault Gets Two Upgrades, Shares Rise as Nissan Deal Nears

- Ukraine Latest: Allies to Send Tanks; Kishida Pressed to Visit

- UK Parliament Seeks Power to Scrutinize Finance Regulators

Notable US Headlines

- US House Speaker McCarthy said they need to have a responsible debt ceiling and called for eliminating wasteful spending, while he added debt is the greatest threat to the nation and that President Biden needs to stop playing politics on the debt ceiling.

- US President Biden is close to naming the next National Economic Council head, Fed Vice Chair Brainard has emerged as the top contender, according to Washington Post sources; current NEC Director Deese is expected to leave soon, no decision made yet.

- US Senator Manchin is to reportedly introduce a bill to delay EV tax credit due to disagreements over how to implement the programme, according to WSJ.

FX

- The DXY has spent the morning in close proximity to the 102.00 mark and has most recently extended to fresh session highs of 102.12 amid a general decline in the risk tone.

- AUD is the standout outperformer after much hotter-than-expected CPI while the NZD was only able to derive fleeting support from its own inflation data, at best AUD/USD and NZD/USD above 0.71 and 0.65 respectively.

- JPY has settled down somewhat after Tuesday’s pronounced action and was relatively resilient to Japan downgrading its economic assessment for the first time in almost a year.

- The aforementioned decline in sentiment that bolstered the USD did so at the expense of Cable and EUR/USD which moved below and further below 1.23 and 1.09 respectively.

Fixed Income

- Core EGBs have continued to extend with the Bund comfortably above 139.00, though the upside seemingly stalled after a brief breach of Fib resistance.

- An easing/pullback that was perhaps spurred by mixed German auction results; though, benchmarks remain elevated overall with Gilts once again outperforming and closer to 106.00 vs 105.08 low (current high 105.79).

- Stateside, USTs are firmer though lagging their EZ peers a touch ahead of a USD 43bln 5yr outing.

Commodities

- WTI and Brent front-month futures trade with no firm direction in early European hours, similar to yesterday’s price action, as market participants await the next catalyst for the complex.

- US Energy Inventory Data (bbls): Crude +3.4mln (exp. +1.0mln), Cushing +3.9mln, Gasoline +0.6mln (exp. +1.8mln), Distillate -1.9mln (exp. -1.1mln)

- US Treasury issued a license allowing Trinidad and Tobago to develop Venezuela’s Dragon offshore gas field.

- Spot gold and base metals have been impacted by the general risk tone with the yellow metal unable to glean any haven support as the USD remains firm.

Geopolitics

- Ukrainian President Zelensky said Russia is readying for new aggression and that Ukraine will prevent further Russian actions, while he added Russia is intensifying its offensive towards Ukraine’s Bakhmut.

- Russian Ambassador to the US said Washington’s possible deliveries of tanks to Ukraine would be a blatant provocation and it is clear Washington is trying to inflict a strategic defeat on us, according to Reuters.

- EU ambassadors have now formally given green light to roll over all the EU’s economic sanctions on Russia for an additional six months, via Radio Free Europe’s Jozwiak.

- German government is to send Leopard 2 tanks to Ukraine, Germany is to approve re-export of Leopard 2 tanks.

US Event Calendar

- 7am: U.S. MBA Mortgage Applications, 7.0%, prior 27.9%

DB’s Jim Reid concludes the overnight wrap

There’s been a little bit of a bias towards risk-off sentiment over the last 24 hours, thanks partly to some weaker-than-expected earnings releases that added to growing concerns about a potential US recession. The S&P 500 (-0.07%) came off its 7-week high from the previous day, oil prices took a sharp turn lower, and sovereign bonds rallied on both sides of the Atlantic. After the close, Microsoft did report better-than-expected earnings due to strength from their cloud-services business (Azure) even as their consumer businesses faltered. Their shares initially traded 4.5% higher before reverting late last night and are now down -1% in after-market trading after news came out during the earnings call that Azure sales could slow in Q1. S&P and NASDAQ futures are -0.46% and -0.78% down respectively as I type.

Those small equity losses in the normal trading session came as the flash PMIs for the US showed the economy still in contractionary territory at the start of the year. To be fair, the numbers were a bit better than expected, but even with the upside surprise the composite PMI was only at 46.6 (vs. 46.4 expected), which is its 7th consecutive month beneath the expansionary 50-mark. Looking at the details, the US PMIs also showed that input price rises had increased in January after 7 months of moderating, so that adds to some other indicators so far this quarter suggesting price pressures might be a bit more resilient than thought. The more negative tone from the data was then cemented by the Richmond Fed’s manufacturing index, which came in at a post-Covid low of -11 (vs. -5 expected).

Although the US numbers continued to point towards contraction, there was some better news from the Euro Area as the flash composite PMI came in at 50.2 (vs. 49.8 expected). That’s the first time it’s been above 50 since June, and came amidst upside surprises in both the services (50.7 vs. 50.1 expected) and manufacturing PMIs (48.8 vs. 48.5 expected) as well. The readings offer yet more evidence that the European economy has been faring better over recent months, echoing the rise in consumer confidence we saw the previous day.

With all this positive news out of Europe lately, our economists updated their forecasts yesterday (link here) and are no longer expecting a recession in 2023 as flagged in our German upgrade two weeks ago. That comes amidst falling gas prices, lower inflation, and declining uncertainty, which means our economists now expect the Euro Area to grow by +0.5% in 2023. They’ve also lowered their headline inflation outlook for 2023 to 5.8%, and now see 2024 at just 1.8%. Nevertheless, they don’t think the ECB can take their foot off the hawkish pedal just yet, since an improved growth outlook and stronger domestic demand raises the threat of more persistent underlying inflation.

Speaking of the ECB, yesterday saw a fresh round of commentary as the Governing Council debate how long to keep hiking rates by 50bps. On the one hand, Lithuania’s Simkus said that “there’s a strong case for staying on the course that’s been set for the coming meetings of 50 basis-point increases.” However the Executive Board’s Pannetta, one of the biggest doves on the council, said that beyond the next meeting in February “any unconditional guidance … would depart from our data-driven approach”. For now, investors are continuing to price in two 50bp moves as the most likely outcome, with +92.1bps worth of hikes priced over the next couple of meetings.

As this debate was ongoing, sovereign bonds rallied strongly on both sides of the Atlantic, with yields on 10yr Treasuries down -5.7bps to 3.45%. That was led by a sharp decline in real yields, which fell -7.6bps on the day. However, near-term policy expectations from the Fed were little changed ahead of their meeting a week from today, and the terminal rate priced for June was down just -0.1bps, whilst the 2yr Treasury yield fell -1.7bps to 4.21%. In Asia 10yr Treasury yields have moved back +1.29bps higher as we go to press. Back to yesterday, and there was a stronger rally in Europe, with yields on 10yr bunds (-5.1bps), OATs (-6.9bps) and BTPs (-11.1bps) all seeing a sharp decline.

As mentioned at the top, it was a bit of a battle for equities, with the major indices struggling to gain much traction after their recent rally. That left both the S&P 500 (-0.07%) and Europe’s STOXX 600 (-0.24%) with modest declines, although that was partly down to a drag from energy stocks after prices took a significant hit yesterday. For instance, Brent crude oil prices (-2.34%) had their worst day in nearly three weeks, falling to $86.13/bbl, whilst natural gas prices in Europe fell -11.71% to €58.27 per megawatt-hour as they closed in on the lows from last week. In the US, one of the worst performing industries for the S&P was Media & Entertainment (-1.02%), whose losses were partially due to the -2.09% pullback by Alphabet as the US Department of Justice did indeed sue the ad-giant under US anti-trust laws. This is the second such suit and a resolution could take years according to legal experts cited by Bloomberg.

Asian equity markets are continuing with their winning streak even with US futures lower. As I type, the KOSPI (+1.27%) is surging as trading has resumed after the Lunar New year holiday while the Nikkei (+0.43%) has rebounded after opening lower in morning trade. Markets in China and Hong Kong remain closed for the holidays. Elsewhere, the S&P/ASX 200 (-0.12%) is in negative territory following disappointing inflation data out from Australia.

Australian inflation rose to +8.4% y/y in December from +7.3% in November while surpassing market expectations for a rise of 7.7%. With inflation pressures broadening, its implication for policy rates pushed 10yr bond yields sharply higher (+5.2 bps) to settle at 3.52%, as we go to print. Meanwhile, the Australian dollar (+0.75%) is trading higher, hitting a 5-month high against the US dollar to trade at $0.7099.

Back to yesterday’s data, and the flash PMI releases were the main data highlight, but we did also get the UK’s public finance statistics for December. That showed public sector net borrowing (ex-banking groups) at £27.4bn (vs. £17.3bn expected), which was driven by more spending on energy support along with higher debt interest. Meanwhile, the latest flash PMIs from the UK weren’t as optimistic as their counterparts in the Euro Area, with the composite PMI falling to 47.8 (vs. 48.8 expected). That’s the lowest reading on that measure in two years, back when the economy went into lockdown again at the start of 2021.

To the day ahead now, and data releases include the Ifo’s business climate indicator for January from Germany. From central banks, the main highlight will be the Bank of Canada’s latest policy decision. Finally, earnings releases include Tesla, Boeing, IBM, AT&T and Abbott Laboratories.

AND NOW NEWSQUAWK (EUROPE/REPORT)

Sentiment slips with the ES Mar’23 below the 200-DMA, DXY bid but USTs off best – Newsquawk US Market Open

WEDNESDAY, JAN 25, 2023 – 06:40 AM

- European bourses are pressured across the board, Euro Stoxx 50 -0.6%, after a sluggish post-MSFT start to the session and thereafter a further waning in the general risk tone.

- Stateside, futures are all in the red with the NQ -1.2% lagging and the ES Mar’23 below 4k and its 200-DMA at 3999, to a 3996.5 session trough.

- DXY has benefitted from the decline in sentiment, to the detriment of GBP and EUR while AUD outperforms post-CPI.

- Core fixed benchmarks have continued to extend though with upside in Bunds capped by technicals/supply, USTs lagging in comparison pre-5yr supply.

- Crude benchmarks are little changed overall, relatively resilient to the above tone, while the USD has capped any haven allure for spot gold.

- Looking ahead, highlights include BoC Policy Announcement, BoJ SOO, Supply from the US. Earnings from AT&T, Tesla, Boeing, IBM & Abbott. Holiday in China (Lunar New Year).

View the full premarket movers and news report.

Or why not try Newsquawk’s squawk box free for 7 days?

EUROPEAN TRADE

EQUITIES

- European bourses are pressured across the board, Euro Stoxx 50 -0.6%, after a sluggish post-MSFT start to the session and thereafter a further waning in the general risk tone.

- Within Europe, a strong update from ASML has been overshadowed by the MSFT pressure, while the likes of Ryanair and IAG are buoyed by easyJet.

- Stateside, futures are all in the red with the NQ -1.2% lagging and the ES Mar’23 below 4k and its 200-DMA at 3999, to a 3996.5 session trough.

- Microsoft Corp (MSFT) Q2 2023 (USD): Adj. EPS 2.32 (exp. 2.30), Revenue 52.70bln (exp. 52.99bln), Co. Intelligent Cloud revenue USD 21.51bln (exp. 21.43bln), while it stated that Azure and other cloud revenue growth of 31% was driven by strong demand for consumption-based services. However, it noted growth is to slow in its commercial business for the rest of FY23 and that FY operating margins are expected to decrease around 2% Y/Y excluding Q2 charge and a favourable impact from the change in accounting method. -2.4% in the pre-market

- ASML (ASML NA) Q4 2022 (EUR): Revenue 6.43bln (exp. 6.38bln). Net 4.29bln (exp. 4.25bln). Sees Q1 2023 net sales 6.1-6.5bln (exp. 6.07bln); ASML intends to declare a total dividend for the year 2022 of EUR 5.80/shr. Click here for more detail. -1.5% in the pre-market

- NYSE said it is thoroughly examining the glitch and that the exchange ended Tuesday with a normal close, while a regular open is expected on Wednesday, according to Reuters.

- Click here for more detail.

FX

- The DXY has spent the morning in close proximity to the 102.00 mark and has most recently extended to fresh session highs of 102.12 amid a general decline in the risk tone.

- AUD is the standout outperformer after much hotter-than-expected CPI while the NZD was only able to derive fleeting support from its own inflation data, at best AUD/USD and NZD/USD above 0.71 and 0.65 respectively.

- JPY has settled down somewhat after Tuesday’s pronounced action and was relatively resilient to Japan downgrading its economic assessment for the first time in almost a year.

- The aforementioned decline in sentiment that bolstered the USD did so at the expense of Cable and EUR/USD which moved below and further below 1.23 and 1.09 respectively.

- Click here for more detail.

FIXED INCOME

- Core EGBs have continued to extend with the Bund comfortably above 139.00, though the upside seemingly stalled after a brief breach of Fib resistance.

- An easing/pullback that was perhaps spurred by mixed German auction results; though, benchmarks remain elevated overall with Gilts once again outperforming and closer to 106.00 vs 105.08 low (current high 105.79).

- Stateside, USTs are firmer though lagging their EZ peers a touch ahead of a USD 43bln 5yr outing.

- Click here for more detail.

COMMODITIES

- WTI and Brent front-month futures trade with no firm direction in early European hours, similar to yesterday’s price action, as market participants await the next catalyst for the complex.

- US Energy Inventory Data (bbls): Crude +3.4mln (exp. +1.0mln), Cushing +3.9mln, Gasoline +0.6mln (exp. +1.8mln), Distillate -1.9mln (exp. -1.1mln)

- US Treasury issued a licence allowing Trinidad and Tobago to develop Venezuela’s Dragon offshore gas field.

- Spot gold and base metals have been impacted by the general risk tone with the yellow metal unable to glean any haven support as the USD remains firm.

- Click here for more detail.

NOTABLE DATA

- German Ifo Business Climate New (Jan) 90.2 vs. Exp. 90.2 (Prev. 88.6); there probably will not be a recession but GDP will probably shrink slightly in Q1.

- Inflationary pressures are easing with the balance of companies wanting to increase prices falling to 35.4 from 40.1, companies export expectations have somewhat brightened and cautious optimism is spreading.

- German Ifo Expectations New (Jan) 86.4 vs. Exp. 85.0 (Prev. 83.2); Current Conditions New (Jan) 94.1 vs. Exp. 95.0 (Prev. 94.4)

NOTABLE HEADLINES

- German Economy Minister sees 2023 German GDP at 0.2% (vs -0.4% in Autumn forecast); 2023 inflation seen at 6% (vs prev. 7%); “we do not see signs of marked recession as feared by many observers”. In-fitting with earlier reports via the likes of Bloomberg and Reuters in recent sessions.

NOTABLE US HEADLINES

- US House Speaker McCarthy said they need to have a responsible debt ceiling and called for eliminating wasteful spending, while he added debt is the greatest threat to the nation and that President Biden needs to stop playing politics on the debt ceiling.

- US President Biden is close to naming the next National Economic Council head, Fed Vice Chair Brainard has emerged as the top contender, according to Washington Post sources; current NEC Director Deese is expected to leave soon, no decision made yet.

- US Senator Manchin is to reportedly introduce a bill to delay EV tax credit due to disagreements over how to implement the programme, according to WSJ.

- Click here for the US Early Morning note.

GEOPOLITICS

- Ukrainian President Zelensky said Russia is readying for new aggression and that Ukraine will prevent further Russian actions, while he added Russia is intensifying its offensive towards Ukraine’s Bakhmut.

- Russian Ambassador to the US said Washington’s possible deliveries of tanks to Ukraine would be a blatant provocation and it is clear Washington is trying to inflict a strategic defeat on us, according to Reuters.

- EU ambassadors have now formally given green light to roll over all the EU’s economic sanctions on Russia for an additional six months, via Radio Free Europe’s Jozwiak.

- German government is to send Leopard 2 tanks to Ukraine, Germany is to approve re-export of Leopard 2 tanks.

CRYPTO

- Bitcoin is back below the USD 23k mark, though remains just above the WTD trough set on Monday at USD 22.3k.

APAC TRADE