January 31, 2023 · by harveyorgan · in Uncategorized · Leave a comment·Edit

jan 31 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSED: UP $6.55 at $1929.70

SILVER PRICE CLOSED: UP $0.12 to $23.74

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1928.05

Silver ACCESS CLOSE: 23.72

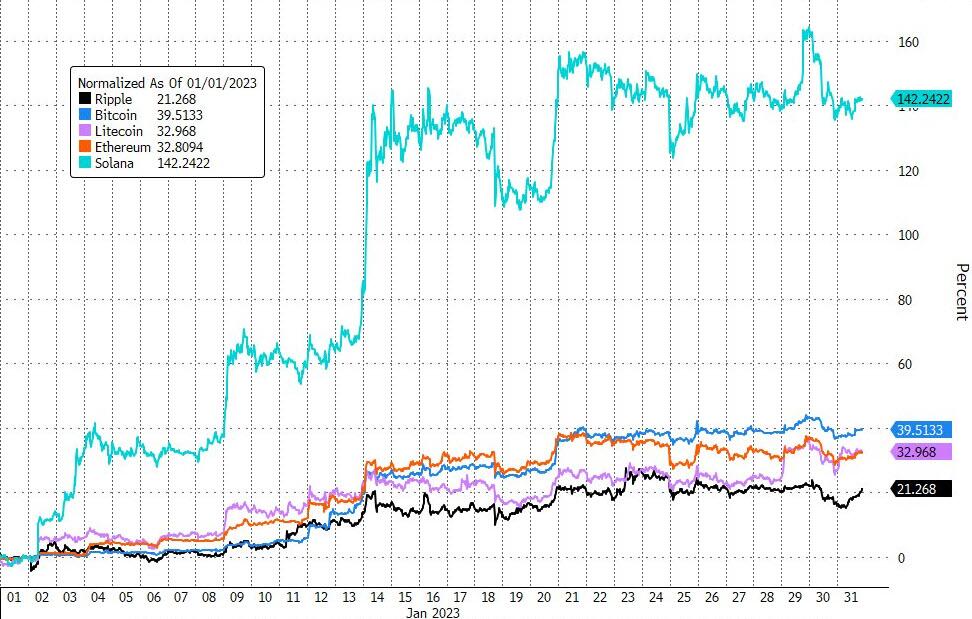

Bitcoin morning price:, 22,911 UP 229

DOLLARS

Bitcoin: afternoon price: $23,139 UP 457 dollars

Platinum price closing $1017.65 UP $2.00

Palladium price; closing 1659.05 UP $12.45

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,565.05 DOWN $1.35 CDN dollars per oz

BRITISH GOLD: 1565,17 UP 8.87 pounds per oz

EURO GOLD: 1774.70 UP 3.22 euros per oz

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,922.900000000 USD

INTENT DATE: 01/30/2023 DELIVERY DATE: 02/01/2023

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 448 153

104 C MIZUHO 47

118 C MACQUARIE FUT 342

132 C SG AMERICAS 255

132 H SG AMERICAS 72

167 H MAREX 3

323 H HSBC 500

363 H WELLS FARGO SEC 16

365 H MAREX CAPITAL M 1

407 C STRAITS FIN LLC 5

435 H SCOTIA CAPITAL 200

624 H BOFA SECURITIES 2432

657 C MORGAN STANLEY 30 431

661 C JP MORGAN 4981 968

685 C RJ OBRIEN 1

686 C STONEX FINANCIA 15

709 C BARCLAYS 24

726 C CUNNINGHAM COM 5

732 C RBC CAP MARKETS 20

737 C ADVANTAGE 21

800 C MAREX SPEC 55

880 C CITIGROUP 920

905 C ADM 24 41

TOTAL: 6,005 6,005

MONTH TO DATE: 6,005

JPMorgan stopped 968/6005

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR JAN/2023. CONTRACT: 6005 NOTICES FOR 600,500 OZ or 18.678 TONNES

total notices so far: 6005 contracts for 600,500 oz (18.678 tonnes)

SILVER NOTICES: 27 NOTICE(S) FILED FOR 135,000 OZ/

total number of notices filed so far this month : 135 for 135000 oz

END

GLD

WITH GOLD UP $6.55

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD

INVENTORY RESTS AT 917.06TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 12 CENTS

AT THE SLV// :/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.5 MILLION OZ OF SILVER FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 520.400 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GOOD SIZED 387 CONTRACTS TO 136,767 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE GOOD GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.12 GAIN SILVER PRICING AT THE COMEX ON MONDAY. FOR THE TWO MONTHS, OUR BANKERS HAVE RETURNED TO BEING NET SHORT AND THUS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.12. AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD A GOOD SIZED GAIN ON OUR TWO EXCHANGES OF 499 CONTRACTS. AS WELL, WE HAD 0 NOTICES FOR EXCHANGE FOR RISK TRANSFER (0 OZ. ) AS THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 0.0 MILLION OZ. WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS( 50 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 0.540. MILLION OZ FOLLOWED + 0.0 MILLION OF EXCHANGE FOR RISK//TOTAL STANDING 0.54 MILLION OZ//// V) GOOD SIZED COMEX OI GAIN/ SMALL EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –62

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTRACTS for 21 days, total 10,614 contracts: OR 53.070 MILLION OZ PER DAY. (505 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 53.070 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 387 WITH OUR $0.12 GAIN IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 50 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 0.54 MILLION OZ / /// 0 EXCHANGE FOR RISK://NEW STANDING RISES TO 0.54 MILLION OZ .. WE HAVE A GOOD SIZED GAIN OF 499 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 27 NOTICE(S) FILED TODAY FOR 135,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 6980 CONTRACTS TO 472,666 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: added + 14 CONTRACTS.

.

WE HAD A STRONG SIZED DECREASE IN COMEX OI ( 6994 CONTRACTS) WITH OUR $6.00 LOSS IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 41.576 TONNES ON FIRST DAY NOTICE //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). NEW STANDING 41.576 TONNES

YET ALL OF..THIS HAPPENED WITH OUR $6.00 LOSS IN PRICE WITH RESPECT TO MONDAY’S TRADING

WE HAD A STRONG SIZED LOSS OF 5511 OI CONTRACTS (17.145 PAPER TONNES) ON OUR TWO EXCHANGES WITH THE ALL OF THE LOSS DUE TO FINALIZATION OF SPREADER LIQUIDATION…..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1469 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 472,666

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5511 CONTRACTS WITH 6994 CONTRACTS DECREASED AT THE COMEX AND 1469 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 5511 CONTRACTS OR 17.14 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1469 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (6980) TOTAL LOSS IN THE TWO EXCHANGES 5511 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 41.576 TONNES ///3) ZERO LONG LIQUIDATION //4) HUGE SIZED COMEX OPEN INTEREST LOSS WITH ALL OF THAT LOSS DUE TO FINALIZATION OF SPREADER LIQUIDATION// 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN :

73,461 CONTRACTS OR 7,346,100 OZ OR 228.49 TONNES 21 TRADING DAY(S) AND THUS AVERAGING: 3398 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAY(S) IN TONNES:228.49 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 228.49/3550 x 100% TONNES 6.45% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES INITIAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A GOOD SIZED 387 CONTRACTS OI TO 136,767 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 50 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 50 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 50 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 387 CONTRACTS AND ADD TO THE 50 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GOOD SIZED GAIN OF 437 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 2.185 MILLION OZ//

OCCURRED DESPITE OUR 12 CENT GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//CORN

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED DOWN 13.65 PTS OR .42% //Hang Seng CLOSED DOWN 227.40 PTS OR 1.03% /The Nikkei closed DOWN 106.29 PTS OR 0.39% //Australia’s all ordinaries CLOSED DOWN .18% /Chinese yuan (ONSHORE) closed DOWN 6.7675 //OFFSHORE CHINESE YUAN DOWN TO 6.7666// /Oil DOWN TO 77.16 dollars per barrel for WTI and BRENT AT 83.66 / Stocks in Europe OPENED MOSTLY RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 6980 CONTRACTS DOWN TO 472,666 WITH OUR LOSS IN PRICE OF $6.00

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1469 EFP CONTRACTS WERE ISSUED: : APRIL 1469 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1469 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 5511 CONTRACTS IN THAT 1469 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 6980 CONTRACTS..AND THIS VERY STRONG SIZED LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $6.00. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG. TODAY ALL OF THE COMEX LOSS WAS DUE TO THE CONTINUATION OF SPREADER LIQUIDATION (A CRIMINAL EVENT BUT WHO IS WATCHING) .

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (41.601)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes(TOTAL THIS YEAR 656.076 TONNES

JAN/2023: 20.559 tonnes

FEB 2023: 41.576 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT fell $6.00) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG LOSS OF 5511 CONTRACTS ON OUR TWO EXCHANGES WITH ALL OF THE LOSS DUE TO THE CONCLUSION OF SPREADER LIQUIDATION // WE HAVE LOST A TOTAL OI OF 17.185 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (41.576 TONNES) … ALL OF THIS WAS ACCOMPLISHED WITH OUR FALL IN PRICE TO THE TUNE OF $6.00.

WE HAD +14 CONTRACTS COMEX TRADES REMOVED FROM OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 5511 CONTRACTS OR 551,100 OZ OR 17.14 TONNES

Estimated gold comex today 192,763//poor//

final gold volumes/yesterday 172,423/// poor

INITIAL STANDINGS FOR FEB 2023 COMEX GOLD //JAN 31//

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 96,453. oz 3 KILOBARS BRINKS . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | 192.906 oz Brinks 6 kilobars |

| No of oz served (contracts) today | 6005 notice(s) 600500 OZ 18.678 TONNES |

| No of oz to be served (notices) | 7370 contracts 737,000 oz 22.923 TONNES |

| Total monthly oz gold served (contracts) so far this month | 6005 notices 600,500 18.678 TONNES* |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 1

i) Out of Brinks 96.453 oz (3kilobars)

Total withdrawals: 96.453 oz

total in tonnes: 0.00299 tonnes

Adjustments:0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEBRUARY.

For the front month of FEBRUARY we have an oi of 13,375 contracts having lost 15,725 contracts

Thus by definition the initial amount of gold standing in February is as follows:

13,375 notices x 100 oz per notice =1,337,500 oz

or 41.601 tonnes

March gained 57 contracts to stand at 1921.

April gained 8,540 contracts up to 388,724

We had 6005 notice(s) filed today for 600500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 4981 notices were issued from their client or customer account. The total of all issuance by all participants equate to 6005 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 968 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN. /2023. contract month,

we take the total number of notices filed so far for the month (6005 x 100 oz , to which we add the difference between the open interest for the front month of (FEBRUARY 13,375 CONTRACTS) minus the number of notices served upon today 6005 x 100 oz per contract equals 1,336,700 OZ OR 41.601 TONNES the number of TONNES standing in this active month of January.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (6005 x 100 oz+ (13,375 OI for the front month minus the number of notices served upon today (6005)x 100 oz} which equals 1,336,700 oz standing OR 41.601 TONNES in this active delivery month of FEBRUARY..

TOTAL COMEX GOLD STANDING: 41.601 TONNES. SO JUST LIKE LAST MONTH WE START WITH A LOW INITIAL AMOUNT OF GOLD STANDING BUT THIS WILL GROW AS THE MONTH PROCEEDS TO ITS CONCLUSION.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

we had one adjustment of 110,631.591 oz Brinks

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,859,815.082 OZ 57.84 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,234,384.892 OZ

TOTAL REGISTERED GOLD: 11,020,384.584 OZ (342.78 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 11,214,000288 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,160,569 OZ (REG GOLD- PLEDGED GOLD) 284.93 tonnes//rapidly declining

END

SILVER/COMEX

JAN 31/2023//INITIAL. SILVER CONTRACT FOR FEBRUARY

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,505,324.205 oz Brinks Loomis |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 731,808.652 oz Delaware |

| No of oz served today (contracts) | 27 CONTRACT(S) (135,000 OZ) |

| No of oz to be served (notices) | 81 contracts (405,000 oz) |

| Total monthly oz silver served (contracts) | 27 contracts (135,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into Delaware: 731.808.652 oz

Total deposits: 731,808.652 oz

JPMorgan has a total silver weight: 149.338 million oz/292.082 million =51.13% of comex .//dropping fast

Comex withdrawals: 2

i) Out of Brinks 1,200,911.475 oz

ii) Out of Loomis: 304,462.700 oz

Total withdrawals; 1,505,324.203 oz

adjustments: 1l dealer to customer

i) 20,067.800 oz Brinks

the silver comex is in stress!

TOTAL REGISTERED SILVER: 32.399 MILLION OZ (declining rapidly).TOTAL REG + ELIG. 292.082 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JAN

silver open interest data:

FRONT MONTH OF FEB/2023 OI:108 CONTRACTS HAVING LOST 23 CONTRACT(S.).

THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER STANDING FOR DELIVERY IS AS FOLLOWS:

108 NOTICES X 5000 OZ PER NOTICE =540,000 OZ

March LOST 1404 CONTRACTS DOWN TO 106,027 contracts

TOTAL NUMBER OF NOTICES FILED FOR TODAY:27 for 135,000 oz

Comex volumes// est. volume today 64,787//fair

Comex volume: confirmed yesterday: 90,260 contracts ( very strong)

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 27 x 5,000 oz = 135,000 oz

to which we add the difference between the open interest for the front month of FEB(108) and the number of notices served upon today 27 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2023 contract month: 27 (notices served so far) x 5000 oz + OI for the front month of FEB (108 – number of notices served upon today (27) x 500 oz of silver standing for the FEB. contract month equates 0.540 million oz + 0 ( EXCHANGE FOR RISK) = 0.54MILLION OZ//(TOTAL OZ OF SILVER STANDING).

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:68,206// est. volume today// good

Comex volume: confirmed yesterday: 60,477 contracts ( good)

END

GLD AND SLV INVENTORY LEVELS

JAN 31/WITH GOLD UP $6.55 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 30/WITH GOLD DOWN $6.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 918.50 TONNES

JAN 27/WITH GOLD DOWN $0.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 919.37 TONNES

JAN 26/WITH GOLD DOWN $11.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 919.37 TONNES

JAN 25/WITH GOLD UP $7.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 917.34 TONNES

JAN 24/WITH GOLD UP $7.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 23/WITH GOLD UP $0.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.63 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 20/WITH GOLD UP $4.75 TODAY;BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 912.43 TONNES

JAN 19/WITH GOLD UP $16.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES INTO THE GLD///INVENTORY RESTS AT 910.98TONNES

JAN 18/WITH GOLD DOWN $1.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.9 TONNES FROM THE GLD////INVENTORY RESTS AT 909.24 TONNES

JAN 17/WITH GOLD DOWN $11.45 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.14 TONNES

JAN 13/WITH GOLD UP $22.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD///INVENTORY RESTS AT 912.14 TONNES

JAN 12/WITH GOLD UP $20.55 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 912.43 TONNES

JAN 11/WITH GOLD UP $1.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

DEC 30/WITH GOLD UP $.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 29//WITH GOLD UP $8.35 TODAY:; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 28/WITH GOLD DOWN $6.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE DEPOSIT OF 5.50 TONNES INTO THE GLD..//INVENTORY REST S AT 918.51 TONNES

DEC 27/WITH GOLD UP $18.15 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 913.01 TONNES

DEC 23/WITH GOLD UP $19,15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES/

DEC 22/WITH GOLD DOWN $29.35 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 21/WITH GOLD FLAT TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 913.88 TONNES

DEC 20/WITH GOLD UP $27.05: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES INTO THE GLD////INVENTORY RESTS AT 912.14 TONNES

DEC 19/WITH GOLD DOWN $2.10: HUGE CHANGES IN GOLD INVENTORY AT THE GLD> A BIG WITHDRAWAL OF 3.47 TONNES FROM THE GLD//INVENTORY RESTS AT 910.41 TONNES

DEC 16/WITH GOLD UP $12.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 15//WITH GOLD DOWN $31.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 911.56 TONNES

DEC 14/WITH GOLD DOWN $6.20: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 912.72 TONNES

DEC 13/WITH GOLD UP $32.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD///INVENTORY RESTS AT 910.41

DEC 12/WITH GOLD DOWN $17.60: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

DEC 9/WITH GOLD UP $8.90//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

Dec 8/WITH GOLD UP $4.05, OVER THE PAST 3 WEEKS WE LOST 2.04 TONNES//INVENTORY RESTS AT 908.09 TONNES

GLD INVENTORY: 917.06 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JAN 31/WITH SILVER UP 12 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.5 MILLLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 520.400 MILION OZ

JAN 30/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 521.900 MILLION OZ.

JAN 27/WITH SILVER DOWN 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 521.900 MILLION OZ//

JAN 26/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 900,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 521.900 MILLION OZ//

JAN 25/WITH SILVER UP 19 CENTS TO TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.3 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 521.000 MILLION OZ

JAN 24/WITH SILVER UP 21 CENTS TODAY: WHAT!! A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 20 MILLION OZ INTO THE SLV/( OCCURRED (LATE LAST NIGHT)//INVENTORY RESTS AT 518.70 MILLION OZ//

JAN 23/WITH SILVER DOWN 40 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.4 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 498.7 MILLION OZ//

JAN 20.WITH SILVER UP 9 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 750,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 497.300 MILLION OZ

JAN 19/WITH SILVER UP 24 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 498.05 MILLION OZ

JAN 18/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 8.15 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 498.05 MILLION OZ///

JAN 17/WITH SILVER DOWN 35 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 13/WITH SILVER UP 46 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.5 MILLION OZ FROM THE SLV..//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 12/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 508.700 MILLION OZ/

JAN 11/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 508.700MILLION OZ

JAN 10/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ

JAN 9/WITH SILVER DOWN 9 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 6/WITH SILVER UP 54 CENTS TODAY;BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.20 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 5/WITH SILVER DOWN 50 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.10 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 505.45 MILLION OZ//

JAN 4/WITH SILVER DOWN 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 506.55 MILLION OZ/

JAN 3/WITH SILVER UP 24 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: STRANGE: A WITHDRAWAL OF 1.2 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 507.85 MILLION OZ/

DEC 30/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 29/ WITH SILVER UP $0.63 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 28//WITH SILVER DOWN 46 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.715 MILLION OZ INTO THE SLV///..INVENTORY RESTS AT 509.050 MILLION OZ

DEC 27/WITH SILVER UP 34 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 507.350 MILLION OZ//

DEC 23/WITH SILVER UP 29 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT507.900 MILLION O//

DEC 22/WITH SILVER DOWN 53 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 21/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.0 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 20/WITH SILVER UP 105 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:: A DEPOSIT OF 700,000 OZ INTO THE SLV///INVENTORY RESTS AT 509.90 MILLION OZ//

DEC 19/WITH SILVER DOWN 13 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.05 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.20 MILLION OZ//

DEC 16/WITH SILVER UP 2 CENTS; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.85 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 508.15 MILLION OZ//

DEC 15/WITH SILVER DOWN 78 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF EXACTLY 2.00 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 510.000 MILLION OZ

DEC 14/WITH SILVER UP 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 512.000 MILLION OZ//

DEC 13/WITH SILVER UP 59 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 600,000 OZ FROM THE SLV////INVENTORY RESTS AT 513.900 MILLION OZ//

DEC 12/WITH SILVER DOWN 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 514.500 MILLION OZ//

DEC 9/WITH SILVER RISING 77 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.2 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 514.500 MILLION OZ.

DEC 8/WITH SILVER RISING 34 CENTS TODAY: OVER THE PAST 3 WEEKS, WE HAVE GAINED A STRONG: 44.777 MILLION OZ/INVENTORY RESTS AT 516.700 MILION OZ.

CLOSING INVENTORY 520.4 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Peter Schiff: The Federal Reserve Is Nowhere Near Victory

TUESDAY, JAN 31, 2023 – 07:20 AM

The mainstream is optimistic about both the economy and the Fed’s fight against inflation. In his podcast, Peter Schiff took apart the mainstream narrative, explaining that the economy is much weaker than most people realize and the Fed is nowhere near victory in the war on inflation.

We’re seeing a Santa Claus rally in stock in January, especially in the speculative momentum stocks. We’ve also seen a rally in the bond market. Peter called it a dead cat bounce.

What’s driving the move up in both stocks and bonds is the weakness in the economy. Because we continue to get more weak economic data. And not just weak economic data on the economy. There’s still hope that inflation has peaked, and the lower numbers that we’ve been seeing when it comes to month-over-month or year-over-year inflation rates — that this trend is permanent and therefore the inflation battle is over. The Fed can declare victory and start cutting rates and easing up on policy. All of this is what is creating the narrative that is driving this move up in both stocks and bonds. But I think as the year progresses, it’s going to be more obvious that inflation hasn’t peaked, that the Fed is nowhere near victorious in this fight, and the economy is actually going to be even weaker than the markets think.”

The mainstream narrative is that the economy will be weak enough to restrain the Fed, but not weak enough to put a big dent in corporate earnings.

They’re wrong. The economy is going to be much weaker than investors think, and it’s going to have an even bigger impact on earnings than investors think. But inflation is going to be much higher than anybody thinks, and that is really going to complicate the situation for both the Federal Reserve and the economy.”

We got the first look at Q4 GDP last week. The 2.9% increase was slightly better than projected.

The last two quarters of 2022 made up for the back-t0-back declines charted in the first and second quarters. That adds weight to the argument that we weren’t in a recession during the first half of the year. But Peter said he doesn’t think we had any real economic growth at all in 2022. He thinks the GDP deflator for the year was too low.

Just like with the CPI, the GDP deflator, I believe, dramatically understates what’s actually happening with consumer prices. I still think in 2022, the real increase in prices was north of 15%, which means if we accurately measured prices to determine the deflator for 2022 GDP, we would have in fact seen a massive contraction in the economy. That’s what’s actually happened. The government is covering it up by cooking the books. But in reality, the economy is shrinking.”

One of the prime reasons we saw an improvement in GDP during the last half of 2022 was an improvement in the trade deficit. The trade deficit was still huge, but not as huge as before.

One reason the trade deficit improved was the strength of the dollar. That lowered the cost of imports. But dollar strength began to unwind in the last half of Q4 and the dollar index is down about 1.5% in 2023.

The weakening dollar is now going to worsen the trade deficit.”

The release of oil from the strategic reserves last year also narrowed the trade deficit.

We’re not going to be doing that in 2023, so the trade deficits are going to be getting bigger and that is going to be subtracting from GDP.”

Peter said he thinks the US economy will get progressively weaker as the year goes on.

The Fed’s favorite inflation number – the Personal Consumption Expenditures Index (PCE) came in at 4.4% for 2022. That is more than double the Fed’s 2% target. But because it is closer to 2% than it has been in the recent past, the markets view it as a positive number. But Peter said in reality, PCE confirms that the Fed is nowhere near victory when it comes to the inflation fight.

That’s because it hasn’t nearly increased interest rates enough to put out this inflation fire. But more importantly, the federal government hasn’t cut spending at all. In fact, it has increased government spending. So, the inflationary forces that underlie the economy are actually getting stronger, not getting weaker. It’s just that investors haven’t been able to figure this out yet.”

Two things need to happen in order to beat inflation. We need positive real interest rates — an interest rate above the CPI. And we also need the US government to cut spending and stop running huge budget deficits. A Fed paper admitted that it can’t tame inflation with monetary policy alone, saying, “When the fiscal authority [the federal government] is not perceived as fully responsible for covering the existing fiscal imbalances, the private sector expects that inflation will rise to ensure sustainability of national debt.”

Neither of these things will likely happen. That means the Fed can’t possibly win this war. It might be able to brag about “progress,” but it is doomed to fail.

In this podcast, Peter Schiff also talks politics, including the government going after Google’s so-called monopoly and a plan in San Francisco to incentivize African-American drug use.”

His interview:

https://www.zerohedge.com/markets/peter-schiff-federal-reserve-nowhere-near-victory

end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

JOHN RUBINO

Gold And The Shrinking Trust Horizon

TUESDAY, JAN 31, 2023 – 11:41 AM

Last week I posted an article on the implosion of the official vaccine narrative.

That’s a controversial topic so not surprisingly it generated some heat on both sides. And a few readers expressed the wish that I’d stay in my lane (precious metals investing) and avoid venturing into unrelated and less well understood territory.

But believe it or not, the public health establishment losing its credibility is related to precious metals, via something called the trust horizon. It works like this: When things are good and the people in charge of big systems seem to be running them well, we’re content to trust the experts. We keep most of our money in banks, brokerage houses, and crypto wallets that exist for us only as websites. We buy produce that’s grown in a different hemisphere and shipped via boats, trains, and trucks to corporate chain grocery stores. We vaccinate ourselves and our kids according to the schedules set by the NIH or the CDC. We pop pills on our doctor’s orders without doing any research. We eat processed foods on the assumption that the FDA keeps them free of dangerous additives. And we believe what we see on cable news.

In other words, our trust horizon, defined as the distance from ourselves at which we’ll believe what we’re told, is global. We assume everything everywhere is working for our benefit and we’re thus willing to put our welfare in those distant hands.

But let some big systems fail to take proper care of us and we pull back, finding people and institutions closer to home that we can see and judge first-hand. We move our money out of distant banks and brokers and into local credit unions whose managers live down the street. We start buying groceries from farmers markets or directly from local farmers. Instead of popping whatever pill is standard for our ailments we look into “food as medicine” and other lifestyle remedies like exercise, supplements, and meditation. We homeschool our kids and join gun clubs. We buy homesteads and start raising chickens.

So where are today’s Americans on the trust horizon spectrum? Well, the military industrial complex is starting (potentially nuclear) wars all over the place. Government debt is growing exponentially. Wall Street has turned the markets into one big casino. Universities have become (very expensive) insane asylums. Congress is full of insider traders who amass fortunes while “serving the public.” And our presidents, well, insert your sarcastic phrase here.

It’s safe to say that for a growing number of disillusioned people, trust now extends to – maybe — the governor’s mansion, city hall, local farmers, their church and one or two community banks. And that’s about it.

Where does gold come in?

The biggest of the big systems that the experts have failed to manage is money. If we can’t trust the monetary authorities to maintain the value of the dollar (and in the past year we’ve learned that we emphatically cannot) then we need other forms of money to trust. And that would be gold and silver, the forms of money that disillusioned people have been running to since literally before the Roman Empire.

The advantage of precious metals lies with the concept of “counterparty risk.” Fiat currencies and pretty much everything else in today’s world require someone (the counterparty) to keep a promise for the thing in question to perform as advertised.

For your dollars to hold their value, the Fed must keep the money supply under control. For your bank account to work your bank has to stay solvent. Likewise your brokerage house. But gold and silver have no counterparty risk. No one must keep a promise for them to stay valuable. They are what they are, regardless of the behavior of the world’s experts. That’s why those experts hate precious metals and why regular people rediscover them every few generations.

Looked at this way, you can draw a direct line from the vaccine mess to gold and silver coins and bars stored in a safe place. And the line is getting thicker and stronger with every new scandal.

3. Chris Powell of GATA provides to us very important physical commentaries//

Biden continues to block Pebble gold mine from being developed in salmon rich Alaska

(Bloomberg/News)

Biden to block Pebble gold mine in salmon-rich area in Alaska

Submitted by admin on Mon, 2023-01-30 20:52 Section: Daily Dispatches

By Jennifer A. Dlouhy

Bloomberg News

Monday, January 30, 2023

The Biden administration is set to ban the dumping of mining waste near Bristol Bay, Alaska, by issuing a decree that thwarts longstanding plans to extract gold, copper, and molybdenum because of potential harm to the region’s thriving sockeye salmon industry.

The Environmental Protection Agency’s final determination, expected soon, would effectively block the mine planned by Pebble Limited Partnership as well as future mining of the same deposit in headwaters of Bristol Bay, home to the world’s largest sockeye harvest. The planned action was described by people familiar with the matter who asked not to be named because the decision hasn’t been announced.

Pebble, a subsidiary of publicly traded Northern Dynasty Minerals Ltd., has been seeking to mine in the area for more than two decades. The pending ban dovetails with a pledge President Joe Biden made while campaigning, when he said Bristol Bay “is no place for a mine.” …

… For the remainder of the report:

END

As expected BIS gold swamps ends at zero

(Robert Lambourne)

Robert Lambourne: After sharp rise in November, BIS gold swaps ended the year at zero

Submitted by admin on Tue, 2023-01-31 14:47Section: Daily Dispatches

By Robert Lambourne

Tuesday, January 31, 2023

Based on its December statement of account, published today —

— the Bank for International Settlements, the central bank of the central banks and their gold broker, appears to have closed its gold swap business as of the end of the year.

It has been a rather wild ride for the bank’s gold swap business since October, as the estimate for that month showed only 7 tonnes of gold swaps outstanding, and then In November the estimated volume of swaps rose dramatically to 105 tonnes.

t may be notable that the BIS has also recently published its guidance on how to complete the reports required under the revised Basel III reporting now being implemented.

The reduction in swaps more recently has been linked to the requirements of Basel III for more capital to be held in support of these transactions.

As is usually the case with the BIS, it seems unlikely that more information about the swaps will be released. It is also possible that the worsening outlook for the finances of Western nations, especially the United States, reduces the attraction of the gold swaps to the BIS and the central bank or banks for which the BIS seemingly has been acting.

As is clear from Table B below, the level of BIS swaps had been significantly higher in the first half of the year, and the October and December totals were easily the lowest in more than four years.

Table A below highlights the level of gold swaps reported in the annual reports of the BIS all the way back to 2010, when the bank’s use of gold swaps appears to have begun. At only one year-end since then, in March 2016, has the swap level been zero.

The BIS’ half-year report to September 30, 2022, has also just been published, and while it offers no direct comment on the use of gold swaps, its disclosures include confirmation that the BIS still holds 102 tonnes of its own gold and that very little of its activities in derivatives are with central banks.

An assumption that the gold held by the BIS remains at 102 tonnes has been used to make the estimate of the gold swap level for December. The low level of derivatives using central banks as counterparties disclosed in the last interim report is taken as a reason to assume that the swaps are almost certainly done with gold bullion banks rather than central banks. Historically, the first swaps described below were done with bullion banks.

While not necessarily related to the reduction in swaps sourced by the BIS, the recent strength of the gold price together with the conundrum facing the U.S. Federal Reserve about raising dollar interest rates must reduce the attraction of having to return swapped gold to bullion banks. Despite the rhetoric about pushing for higher interest rates, the Federal Reserve needs to avoid an erosion of confidence in the U.S. Treasuries market when the federal government’s rising debt is becoming more controversial.

Also, recent increases in interest rates are already hitting federal government finances. The recently published December Monthly Treasury Report focuses in its Highlights section on the federal government’s interest charge of $107 billion in the month. This is a higher interest charge than would arise on a full accruals basis, but is still rising sharply:

This appears to be the first month when the reported interest bill has exceeded $100 billion. An annual interest cost of maybe $800 billion in the current fiscal year seems possible even without further interest rate increases. In these circumstances the room for the Federal Reserve to raise interest rates seems really limited and hence it seems unwise for the BIS, probably acting as an agent for the Fed, to face future deliveries of gold via the use of swaps, since the parlous state of U.S. government finances is probably a significant boost for gold.

… Historical context

The BIS rarely comments publicly on its gold activities, but its first use of gold swaps was considered important enough to cause the bank to give some background information to the Financial Times for an article published July 29, 2010, coinciding with publication of the bank’s 2009-10 annual report.

The general manager of the BIS at the time, Jaime Caruana, said the gold swaps were “regular commercial activities” for the bank, and he confirmed that they were carried out with commercial banks and so did not involve central banks. It also seems highly likely that the BIS’ remaining swaps are still all made with commercial banks, because the BIS annual report has never disclosed a gold swap between the BIS and a major central bank.

The swap transactions potentially created a mismatch at the BIS, which may have ended up being long unallocated gold (the gold held in BIS sight accounts at major central banks) and short allocated gold (the gold required to be returned to swap counterparties). This possible mismatch has not been reported by the BIS.

The gold banking activities of the BIS have been a regular part of the services it offers to central banks since the bank’s establishment 90 years ago. The first annual report of the BIS explains these activities in some detail:

http://www.bis.org/publ/arpdf/archive/ar1931_en.pdf

A June 2008 presentation made by the BIS to potential central bank members at its headquarters in Basel, Switzerland, noted that the bank’s services to its members include secret interventions in the gold and foreign exchange markets:

https://www.gata.org/node/11012

The use of gold swaps to take gold held by commercial banks and then deposit it in gold sight accounts held in the name of the BIS at major central banks doesn’t appear ever to have been as large a part of the BIS’ gold banking business as it has been in recent years, although the recent declines suggest this is changing.

As of March 31, 2010, excluding gold owned by the BIS, there were 1,706 tonnes held in the name of the BIS in gold sight accounts at major central banks, of which 346 tonnes or 20% were sourced from gold swaps from commercial banks.

If the BIS was adopting the level of disclosures made by publicly held companies, such as commercial banks, some explanation of these changes probably would have been required by the accounting regulators. This irony may not be lost on those dealing with regulatory activities at the BIS. Presumably the shrinkage of the BIS’ gold banking business shows that even central banks now prefer to hold their own gold or hold it in earmarked form — that is, as allocated gold.

A review of Table B below highlights recent BIS activity with gold swaps, and despite the recent declines, the recent positions estimated from the BIS monthly statements have regularly been large, especially in early 2022, and the volume of trading has been significant.

No explanation for this continuing use of swaps has been published by the BIS. Indeed, no comment on the bank’s use of gold swaps has been offered since 2010.

This gold is supplied by bullion banks via the swaps to the BIS. The gold is then deposited in BIS gold sight accounts (unallocated gold accounts) at major central banks such as the Federal Reserve.

The reasons for this activity have never been fully explained by the BIS and various conjectures have been made as to why the BIS has facilitated it. One conjecture is that the swaps are a mechanism for the return of gold secretly supplied by central banks to cover shortfalls in the gold markets. The use of the BIS to facilitate this trade suggests of a desire to conceal the rationale for the transactions.

As can be seen in Table A below, the BIS has used gold swaps extensively since its financial year 2009-10. No use of swaps is reported in the bank’s annual reports for at least 10 years prior to the year ended March 2010.

The February 2021 estimate of the bank’s gold swaps (552 tonnes) was higher than any level of swaps reported by the BIS at its March year-end since March 2010. The swaps reported at March 2021 were at the highest year-end level reported, as is clear from Table A.

—–

Table A — Swaps reported in BIS annual reports

March 2010: 346 tonnes.

March 2011: 409 tonnes.

March 2012: 355 tonnes.

March 2013: 404 tonnes.

March 2014: 236 tonnes.

March 2015: 47 tonnes.

March 2016: 0 tonnes.

March 2017: 438 tonnes.

March 2018: 361 tonnes.

March 2019: 175 tonnes

March 2020: 326 tonnes

March 2021: 490 tonnes

March 2022: 358 tonnes

—–

The table below reports the estimated swap levels since August 2018. It can be seen that the BIS is actively involved in trading gold swaps and other gold derivatives with changes from month to month reported in excess of 100 tonnes in this period.

—–

Table B – Swaps estimated by GATA from BIS monthly statements of account

Month ….. Swaps

& year … in tonnes

Dec-22 … /0

Nov-22 … /105

Dec-22 … /0

Nov-22 … /105

Oct-22 ….. /7

Sep-22 …../57

Aug -22 ….. /75

Jul-22 ….. /56

Jun-22 ….. /202

May-22 ….. /270

Apr-22 ….. /315

Mar-22 …. /358

Feb-22 …. /472

Jan-22 ….. /501

Dec-21…. /414

Nov-21…. /451

Oct-21…. /414

Sep-21 …. /438

Aug-21 …. /464

Jul-21 …. /502

Jun-21 …./471

May-21 …./517

Apr-21 …. /472

Mar-21…. /490±

Feb-21 …../552

Jan-21 …. /523

Dec-20 …. /545

Nov-20 …. /520

Oct-20 …. /519

Sep-20…../ 520

Aug-20…../ 484

Jul-20 ….. / 474

Jun-20 …. / 391

May-20 …. / 412

Apr-20 …. / 328

Mar-20 …. / 326*

Feb-20 …. / 326

Jan-20 …. / 320

Dec-19 …. / 313

Nov-19 …. / 250

Oct-19 …. / 186

Sep-19 …. / 128

Aug-19 …. / 162

Jul-19 ….. / 95

Jun-19 …. / 126

May-19 …. / 78

Apr-19 ….. / 88

Mar-19 …. / 175

Feb-19 …. / 303

Jan-19 …. / 247

Dec-18 …. / 275

Nov-18 …. / 308

Oct-18 …. / 372

Sep-18 …. / 238

Aug-18 …. / 370

± The estimate originally reported by GATA was 487 tonnes, but the BIS annual report states 490 tonnes, It is believed that slightly different gold prices account for the difference.

* The estimate originally reported by GATA was 332 tonnes, but the BIS annual report states 326 tonnes. It is believed that slightly different gold prices account for the difference.

GATA uses gold prices quoted by USAGold.com to estimate the level of gold swaps held by the BIS at month-ends.

—–

As noted already, the BIS in recent times has refused to explain its activities in the gold market, nor for whom the bank is acting:

https://www.gata.org/node/17793

Despite this reticence the BIS has almost certainly acted on behalf of central banks in taking out these swaps, as they are the BIS’ owners and control its Board of Directors.

This refusal to explain prompts some observers to believe that the BIS acts as an agent for central banks intervening surreptitiously in the gold and currency markets, providing those central banks with access to gold as well as protection from exposure of their interventions.

As mentioned above, it is possible that the swaps provide a mechanism for bullion banks to return gold originally lent to them by central banks to cover bullion bank shortfalls of gold. Some commentators have suggested that a portion of the gold held by exchange-traded funds and managed by bullion banks is sourced directly from central banks.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the involvement of the Bank for International Settlements in the gold market.

* * *

end

Craig Hemke discusses gold/silver for the week ahead

(Craig Hemke)

Craig Hemke at Sprott Money: The busy week ahead for gold

Submitted by admin on Tue, 2023-01-31 13:44 Section: Daily Dispatches

By Craig Hemke

Sprott Money, Toronto

Tuesday, January 31, 2023

While there will be all sorts of economic and geopolitical headlines in the days ahead, two events that will drive precious metals stand out.

The first will be the conclusion of the January Federal Open Market Committee meeting on Wednesday. The second will be the release of the January U.S. jobs report on Friday.

If Comex gold and silver can successfully navigate both, the possibility of a February rally will grow

First of all, it’s not just those two events that will impact precious metal prices.

There will also be the updated manufacturing and service sector purchasing managers index as well as the latest updates on productivity and unit labor costs.

However, the most important scheduled events are the FOMC meeting on Wednesday and the U.S. jobs data on Friday. …

… For the remainder of the analysis:

https://www.sprottmoney.com/blog/The-Busy-Week-Ahead-January-31-2023

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

A MUST VIEW

FROM THE IMF:

Gold as International Reserves: A Barbarous Relic No More?

(SPECIAL THANKS TO KEVIN TO OBTAINING THIS FOR US:)

| Kevin Wallien | 9:24 AM (3 minutes ago) | ||

| to me | |||

Fyi

Gold as International Reserves: A Barbarous Relic No More?

end

No question about it: huge central bank buying of gold drove demand to 10 year highs

(London’s Financial Times)

(GATA) ‘Colossal’ central bank buying drives gold demand to decade high

By Harry Dempsey

Financial Times, London

Tuesday, January 31, 2023

Demand for gold surged to its highest in more than a decade in 2022, fueled by “colossal” central bank purchases that underscored the safe haven asset’s appeal during times of geopolitical upheaval.

Annual gold demand increased 18% last year to 4,741 tonnes, the largest amount since 2011, driven by a 55-year high in central bank purchases, according to the World Gold Council, an industry-backed group.

Central banks hoovered up gold at a historic rate in the second half of the year, a move many analysts attribute to a desire to diversify reserves away from the dollar after the U.S. froze Russia’s reserves denominated in the currency as part of its sanctions against Moscow.

Retail investors also piled into the yellow metal in a bid to protect themselves from high inflation.

Central bank purchases of gold hit 417 tonnes in the final three months of the year, roughly 12 times higher than the same quarter a year ago. It took the annual total to more than double of the previous year at 1,136 tonnes. …

… For the remainder of the report:

https://www.ft.com/content/ef6ed550-422a-4540-a8af- 41ff2ac30e67

end

from BullionVault:

Gold Price Rebounds from $1900 as ‘Unreported’ Central-Bank Buying Boosts Global Demand

Tuesday, 1/31/2023 14:45

The GOLD PRICE fell and then rebounded from 2-week lows against a rising Dollar in London trade Tuesday, heading into tomorrow’s much-anticipated US Federal Reserve decision on interest rates just shy of $1920 per ounce after the world’s largest gold ETF saw a small outflow overnight.

With the price of gold dipping within $1 of $1900 per ounce before rebounding, new data from the World Gold Council meantime made headlines by reporting the heaviest global gold demand since 2011 for last year as a whole.

“Colossal central bank purchases, aided by vigorous retail investor buying and slower ETF outflows, lifted annual demand to an 11-year high,” says the mining-industry- backed WGC, now marking 30 years of its regular and widely- respected Gold Demand Trends reports.

Despite that rise in total demand however, gold prices were dead flat in Dollar terms in 2022, rising just 0.08% on the previous year’s annual average for gold’s weakest price increase since the bottom of the bear market ending in 2015 thanks to large private investment flows to physical bullion turning negative, gold-backed ETF trust funds shrinking, and speculators cutting their bullish betting on futures and options contracts.

Chart of global gold demand in tonnes. Source: World Gold Council

Making a substantial estimate for unreported official- sector gold demand to put 2022 as the strongest such year since before the Bretton Woods gold-Dollar monetary system collapsed 5 decades ago, “Central bank buying [in 2023] is unlikely to match 2022 levels,” the WGC said today, launching its new report.

“Lower total [foreign-exchange] reserves may constrain the capacity to add to existing allocations. But lagged reporting by some central banks means that we need to apply a high degree of uncertainty to our expectations, predominantly to the upside.”

“There is chatter in the markets about the lack of reported increases in China’s central bank holdings,” says precious metals specialist Rhona O’Connell at brokerage StoneX.

Comparing Swiss export data for bullion shipped to Hong Kong against the city’s domestic consumer demand plus China’s wider jewelry-plus-retail-investment as well as the country’s world No.1 gold-mine output, “there is a shortfall of roughly 350 tonnes to make up,” O’Connell adds, saying that “these numbers are likely to increase” the view that the People’s Bank is under-reporting its gold reserves.

“While it is possible that some of [the over-supplied] metal may have come back out of the country…the extra would certainly account for the reported increase in [China’s] central bank reserves of more than 60 tonnes in the latter part of the year.”

Action in gold-backed ETFs was mixed on Monday, with the giant SPDR Gold Trust (NYSEArca: GLD) shrinking by 0.2% to its smallest in 5 sessions, while the smaller iShares gold trust (NYSEArca: IAU) was unchanged at its largest since mid- November, not seeing any net outflows of investment cash since Christmas Eve.

On the Chinese wholesale market’s 2nd day back from the Lunar New Year spring festival holidays, gold prices in Shanghai edged lower overnight from yesterday’s 28-month Yuan gold highs, trimming the city’s benchmark price ¥3 per gram to ¥419.

Betting on tomorrow’s US Fed decision meantime put a 99.8% certainty on a rise of 0.25 points – the smallest since the US central bank began ‘lift off’ from zero rates this time last year – after last week’s PCE data said inflation in the world’s largest economy continues to slip from 2022’s 4-decade highs.

Gold priced in the Euro also sank and rebounded, regaining its €15 down-spike to trade back at €1770 per ounce, while the UK gold price in Pounds per ounce rose back above £1560 – a new record high when first reached on Russia’s invasion of Ukraine 11 months ago – following a downgrade to the UK’s economic outlook from the International Monetary Fund.

With the IMF now saying UK GDP will shrink in 2023 while the rest of the developed world grows, “remember the UK outlook is just a couple of researchers in [Washington]” who work from external forecasts from the Bank of England and UK Treasury, says former Bank of England economist Tony Yates. “There is no gigantic seeing intelligence with independent insight.”

In contrast to the gold price – and enjoying no central- bank demand, official or unreported according to expert analysts – silver prices today dipped through $23 per ounce for the 2nd time in 6 weeks before rallying 50 cents in barely 2 hours.

end

5.IMPORTANT COMMENTARIES ON COMMODITIES:

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

END

.

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.7565

OFFSHORE YUAN: 6.7666

SHANGHAI CLOSED DOWN 13.65 PTS OR .42%

HANG SENG CLOSED DOWN 227.40 PTS OR 1.03%

2. Nikkei closed DOWN 106.29 PTS OR 0.39%

3. Europe stocks SO FAR: MOSTLY RED EXCEPT ITALY

USA dollar INDEX UP TO 102.29 Euro FALLS TO 1.0827 DOWN 23 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.488!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 130.43/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.289%***/Italian 10 Yr bond yield FALLS to 4.268%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.325…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.287//

3j Gold at $1914.20//silver at: 23.35 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 15/100 roubles/dollar; ROUBLE AT 70.55//

3m oil into the 77 dollar handle for WTI and 83 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 130.42/10 YEAR YIELD AFTER BREAKING .54% FALLS TO .488% ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9273– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0040 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.518% DOWN 3 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.639 DOWN 2 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,81…

GREAT BRITAIN/10 YEAR YIELD: 3.3554% DOWN 1 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

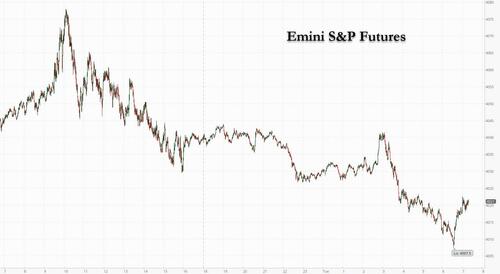

“Markets Are Tense”: Futures Slide As Central Bank Jitters Rise

TUESDAY, JAN 31, 2023 – 08:05 AM

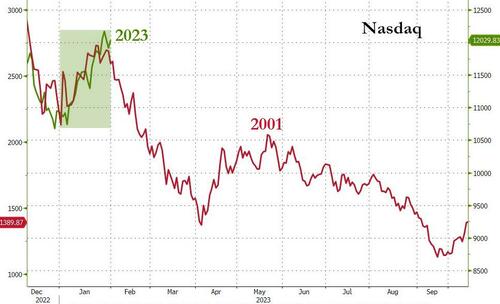

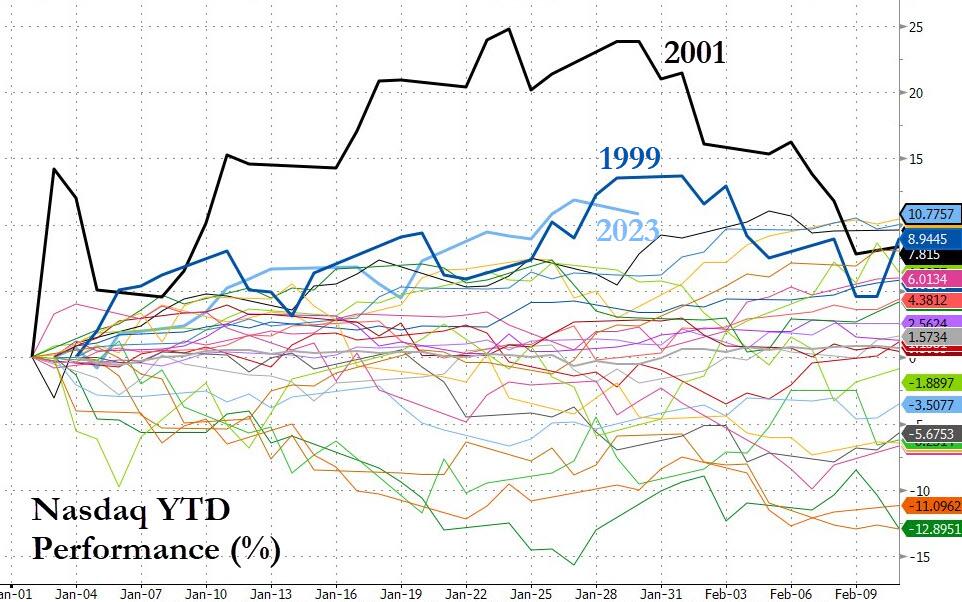

US equity futures showed no sign of rebounding on Tuesday from the Nasdaq’s worst single-day drubbing in over a month, with investors growing nervous ahead of this week’s barrage of central bank meetings which include the BOE and ECB Thursday and start tomorrow, when the Fed is expected to hike rates by 25bps; a barrage of earnings reports from some of the world’s biggest companies is also keeping investors busy.

Futures for the Nasdaq 100 and the S&P 500 indexes slipped 0.6% and 0.3%, recovering from even bigger losses earlier in the session as doubts continue to grow about the sustainability of a four-month old rally, which has accelerated further since the start of the year. The Nasdaq benchmark tumbled more than 2% on Monday, its largest decline since Dec. 22 . Despite the pre-Fed jitters, however, both the S&P 500 and the Nasdaq 100 are poised for their best start to a year since 2019 as optimism over slowing inflation and resilient economic growth fueled appetite for risk. However, the start of the earnings season with corporate warnings and reiteration of the Fed’s resolve to raise rates have put a damper on the recovery. Treasury yields dipped, the dollar edged higher and oil extended its recent losses.

In premarket trading, chipmaker stocks slumped with NXP Semiconductors NV dropping more than 4% after a disappointing first-quarter forecast. Exxon Mobil surpassed profit expectations for the ninth time in 10 quarters, but shares are down premarket as the company signaled investors won’t see any additional rewards. McDonald’s also fell as much as 1.8% after its operating margin for the fourth quarter misses the consensus estimate. Its 2023 forecast for the measure also trailed. Moderna and BioNTech are also dropping in US premarket trading after Pfizer’s 2023 outlook included softer revenue estimates for its Covid vaccine and pill than analysts expected (MRNA dips 2.4% and BNTX, which is partner on PFE’s shot, falls 2%). On the plus side, General Motors jumped more than 5% after posting forecasts that beat analysts’ estimates; its results lifted shares of automakers Ford and Stellantis. Here are some other notable premarket movers:

- Shares in NXP Semiconductors drop 4% in US premarket trading after the chipmaker gave a forecast for first-quarter revenue that missed estimates. The company saw weak demand in its mobile, industrial and smart home businesses, while its autos segment remained resilient.

- Shares of semiconductor companies are falling in US premarket trading on Tuesday, after Samsung Electronics said it expects the smartphone market to contract in 2023 and NXP Semiconductors (NXPI US) reported a sales decline in its mobile business.

- Micron leads chip stocks lower in US premarket trading after Samsung Electronics said it expects the smartphone market to contract in 2023 and NXP Semiconductors reported a sales decline in its mobile business.

- Comstock Resources (CRK US) shares rise as much as 6% in US premarket trading, ahead of the oil and gas company’s inclusion in the S&P SmallCap 600 index.

- Health insurance stocks and managed-care providers could come under pressure in the short term, analysts said, after a Medicare audit rule was finalized under which the agency will seek around $4.7 billion over 10 years in clawback payments. Shares in insurers including Humana (HUM US) and UnitedHealth (UNH US) declined in US postmarket trading on Monday.

- FibroGen Inc. (FGEN US) gained in postmarket trading Monday after William Blair raised the recommendation to outperform from market perform, joining at least two other analysts who have lifted their ratings this month.

- Integer Holdings Corp. (ITGR US) declined postmarket Monday after the medical device outsource manufacturer announced the launch of a $375m convertible senior notes offering.

- Harmonic (HLIT US) dropped in postmarket trading Monday after forecasting adjusted earnings per share for 2023 that missed the average analyst estimate.

“Markets are tense,” said Raphael Thuin, head of Capital Markets Strategies at Tikehau Capital. “They haven’t made up their minds about the ongoing earnings season,” he said, noting visibility also remains low on the outlook for inflation and how policy makers intend to keep price growth in check. He warned that a surprisingly hawkish tone from the Fed could trigger a backlash across markets. The US central bank will conclude its meeting on Wednesday and is widely expected to raise rates by 25 basis points.

Signs of earnings pressure are complicating the picture for investors hopeful that the Fed will ease off on its aggressive rate-hike cycle: According to data compiled by Bloomberg, earnings per share estimates for the S&P 500 have fallen since peaking in June 2022, while revenue projections have flatlined. Margins are coming under pressure as slowing inflation erodes pricing power.

“The prospect of a stabilization of interest rates at 5% after March is shifting the focus from the rate side to the growth side,” said Willem Sels, chief investment officer at HSBC Private Bank. “Mixed earnings will probably continue to lead to some volatility in coming weeks, so we are neutral on developed-market equities for now.”

European stocks extended a decline after data suggested the euro area will avoid a recession after unexpectedly expanding at the end of 2022, prompting traders to ramp up bets on monetary tightening by the ECB. The Stoxx 600 was down 0.7% with miners, financial services and energy the worst performing sectors. Gross domestic product edged up by 0.1% in the final quarter, Eurostat said Tuesday, defying economist estimates for a contraction of 0.1%. While German and Italian output shrank, France and Spain recorded expansion. There was also stronger-than-anticipated data on Monday from Ireland. Among individual stock movers in Europe on Tuesday, Swiss lender UBS Group AG dropped more than 3% after reporting a slump in revenue at its key wealth management business. Unicredit SpA surged after the Italian lender reported better-than-expected profit. Here are some of the biggest European movers on Tuesday:

- UniCredit shares rise as much as 9.6% after the Italian lender beat expectations across the board, including delivering what KBW says is a “monster” capital return

- Swedbank jumps as much as 5% after the lender’s 4Q net interest income (NII) fueled a strong profit beat. Analysts say they expect positive revisions to earnings estimates for 2023-2024

- Diageo gains as much as 2.1% after Investec upgraded the drinks giant to buy from hold, saying the shares are “a rare bargain” after their post-earnings decline

- SEB rises as much as 9.2%, their biggest jump since October 2021, after the French household-appliances maker reported 4Q sales that beat the average analyst estimate.

- UBS shares fall as much as 4.1% in early trading with analysts saying the Swiss banking and wealth management group’s results look mixed when delving into the details

- Tele2 shares fall as much as 5% after the telecom operator forecast low-single-digit growth in Ebitda after-leases for 2023, which analysts say was “soft” compared to consensus

- Rheinmetall shares fall as much as 7.2% after the defense company said it plans to offer of two series of unsubordinated, unsecured convertible bonds with an aggregate principal amount of €1 billion

- Wartsila shares fall as much as 5.8%. The power plant services company posted a “heavy” 50% miss on its fourth-quarter EPS, driven by legacy pricing and one-time items, RBC says

- AMS-Osram shares fall as much as 4.9% after the Swiss semiconductor company announced a CEO change, a move Vontobel described as “unexpected” and adding uncertainty

- Darktrace drops as much as 7.6% to a record low after Quintessential Capital Management issued a 70-page report explaining why it’s short the shares of the cybersecurity firm

- Trelleborg shares drop as much as 4.6%, retreating from yesterday’s record close, as Citi writes in note that it appears too early for a re-rating in the industrial firm’s stock

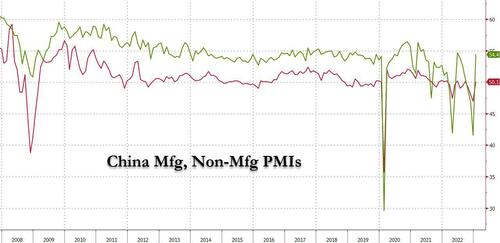

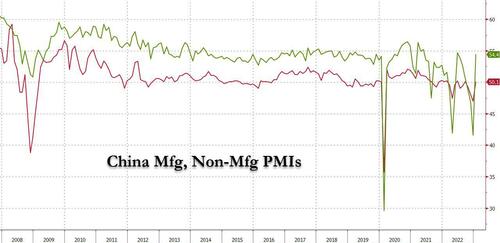

Asian stocks fell for a second day as mainland Chinese shares pulled back after Monday’s advance, with traders awaiting key decisions from major central banks this week. The MSCI Asia Pacific Index declined as much as 1.2%, dragged lower by technology shares after Samsung Electronics posted weaker-than-expected fourth-quarter results. Equity markets in Hong Kong, South Korea and Taiwan retreated. China’s CSI 300 Index fell even after the latest economic data showed manufacturing and services expanded for the first time in four months as the nation exited from Covid Zero.

The benchmark gauge shied away from a bull market after a recent rally fueled by the return of foreign investors took a breather. “Stocks generally have had a very good run recently despite concerns of a US recession and Fed hawkishness,” said Chetan Seth, an Asia Pacific equity strategist at Nomura. “So there is naturally a huge focus on US payrolls data this Friday and what Chair Powell has to say this coming Thursday early morning in Asia.” Interest-rate decisions are scheduled this week for the Federal Reserve, the European Central Bank and the Bank of England. The Fed is widely expected to raise rates by a quarter percentage point, with investors on the lookout for any changes in the future tightening path. The MSCI’s Asian benchmark was poised for a monthly gain of around 8%, its best January performance since 1994. The gauge has rallied 23% since Oct. 31 on China’s rebound, beating the S&P 500 by 19 percentage points