FEB 1/GOLD CLOSED DOWN $2.55 TO $1927.15//SILVER CLOSED DOWN 20 CENTS TO $23.54//PLATINUM WAS DOWN $17.80 TO $999.85//PALLADIUM WAS DOWN $17.20 TO $1642.05//COVID UPDATES: HUGE STUDY REVEALS LARGE HEART AND VEIN PROBLEMS/DEATHS FOR USA CITIZENS//GREAT STUDY ON IVERMECTIN, HOW IT WORKS AND HOW IT IS SAVING LIVES//FAKE VACCINE CARDS HANDED OUT TO DOCTORS IN HOUSTON SO THEY WOULD NOT BE FIRED..SHARYL ATTKINSON REPORTS ON THIS//BIG STUDY SUGGESTS THAT THE INCREASE PRODUCTION OF CATACHOLAMINES IS THE MAJOR CAUSE OF SUDDEN DEATH IN ATHLETES//IRAN AND RUSSIA SIGN A CO OPERATION BANKING AGREEMENT TO BY-PASS THE USA DOLLAR//CHINA-RUSSIA-INDIA-IRAN FORMULATES A TRADE ROUTE TO BYPASS EUROPE..A MUST READ//UKRAINE VS RUSSIA: USA OFFERS A FLIMSY PLAN TO END THE CONFLICT TO WHICH RUSSIA TOTALLY IGNORES (PEPE ESCOBAR)//LEBANON IN TURMOIL AS THE ECONOMY NOW ENTERS A HUGE HYPERINFLATION AS THEY JUST DEVALUED THE LIRA BY 90%/SOUTH AFRICA IN TURMOIL IN THEIR ENERGY SECTOR WITH CONTINUAL BLACKOUTS//POOR ADP PRIVATE JOBS REPORT//POOR USA MANUFACTURING SURVEY REPORT//FAKE JOLTS REPORT//HUGE WAVE OF USA BANKRUPTCIES//SWAMP REPORT FOR YOU TONIGHT//

072 C GOLDMAN 8 39 104 C MIZUHO 12 118 C MACQUARIE FUT 8 93 118 H MACQUARIE FUT 539 132 C SG AMERICAS 89 36 132 H SG AMERICAS 72 167 H MAREX 3 363 H WELLS FARGO SEC 1 407 C STRAITS FIN LLC 5 435 H SCOTIA CAPITAL 74 624 H BOFA SECURITIES 647 657 C MORGAN STANLEY 115 661 C JP MORGAN 259 685 C RJ OBRIEN 1 686 C STONEX FINANCIA 4 709 C BARCLAYS 6 726 C CUNNINGHAM COM 5 732 C RBC CAP MARKETS 20 5 800 C MAREX SPEC 52 23 880 C CITIGROUP 245

DLV615-T CME CLEARING BUSINESS DATE: 01/31/2023 DAILY DELIVERY NOTICES RUN DATE: 01/31/2023 PRODUCT GROUP: METALS RUN TIME: 21:43:45 880 H CITIGROUP 749 905 C ADM 18 10

TOTAL: 1,569 1,569

JPMorgan stopped 259/1569

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR JAN/2023. CONTRACT: 1569 NOTICES FOR 156,900 OZ or 4.880 TONNES

total notices so far: 7574 contracts for 757,400 oz (23.558 tonnes)

SILVER NOTICES: 4 NOTICE(S) FILED FOR 20,000 OZ/

total number of notices filed so far this month : 41 for 205,000 oz

END

GLD

WITH GOLD DOWN $2.55

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

//NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 917.06TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 20 CENTS

AT THE SLV// :/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.4 MILLION OZ OF SILVER FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 519.0 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 1496 CONTRACTS TO 138,263 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE GOOD GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.12 GAIN SILVER PRICING AT THE COMEX ON MONDAY. FOR THE TWO MONTHS, OUR BANKERS HAVE RETURNED TO BEING NET SHORT AND THUS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.12. AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD A GIGANTIC SIZED GAIN ON OUR TWO EXCHANGES OF 1984 CONTRACTS. AS WELL, WE HAD 0 NOTICES FOR EXCHANGE FOR RISK TRANSFER (0 OZ. ) AS THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 0.0 MILLION OZ. WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS( 396 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 0.540. MILLION OZ FOLLOWED BY TODAY’S SMALL QUEUE JUMP OF 5,000 OZ = .545 MILLION OZ + 0.0 MILLION OF EXCHANGE FOR RISK//TOTAL STANDING 0.545 MILLION OZ//// V) HUGE SIZED COMEX OI GAIN/ FAIR EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –92

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTRACTS for 1 days, total 396 contracts: OR 1.980 MILLION OZ PER DAY. (396 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 1.980 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 1.98 MILLION OZ/INITIAL

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1496 WITH OUR$0.12 GAIN IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 396 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 0.54 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUEUE + / /// 0 EXCHANGE FOR RISK://NEW STANDING RISES TO 0.545 MILLION OZ .. WE HAVE A GIGANTIC SIZED GAIN OF 1984OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 4 NOTICE(S) FILED TODAY FOR 20,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1024 CONTRACTS TO 471,642 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: removed – 157 CONTRACTS.

.

WE HAD A SMALL SIZED DECREASE IN COMEX OI ( 1024 CONTRACTS) WITH OUR $6.55 GAIN IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 41.601 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 12,300 OZ EFP TO LONDON//NEW STANDING: 41.219 //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). TONNES

YET ALL OF..THIS HAPPENED WITH OUR $6.55 GAIN IN PRICEWITH RESPECT TO TUESDAY’S TRADING

WE HAD A TINY SIZED GAIN OF 287 OI CONTRACTS (0,8926 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1311 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 471,642

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 287 CONTRACTS WITH 1024CONTRACTS DECREASED AT THE COMEX AND 1311 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 287 CONTRACTS OR 1.381 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1311 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (1024) TOTAL GAIN IN THE TWO EXCHANGES 444 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 41.601 TONNES FOLLOWED BY TODAY’S 12300 OZ Q.FP. JUMP TO LONDON// ///3) ZERO LONG LIQUIDATION //4) SMALL SIZED COMEX OPEN INTEREST LOSS// 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

1311 CONTRACTS OR 131,100 OZ OR 4.077 TONNES 1 TRADING DAY(S) AND THUS AVERAGING: 1311 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES:4.077 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 4.077/3550 x 100% TONNES 0.0116% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 4.077 TONNES/INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 1496 CONTRACTS OI TO 138,263 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 396 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 396 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 396 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1588 CONTRACTS AND ADD TO THE 396 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED GAIN OF 1892 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 9.460 MILLION OZ//

OCCURRED DESPITE OUR 12 CENT GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//CORN

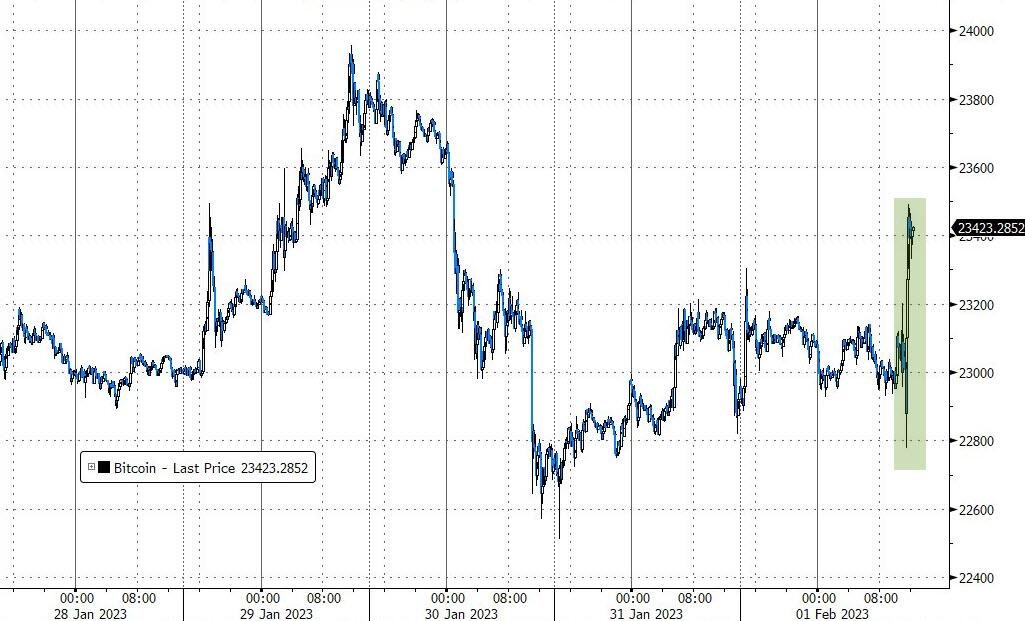

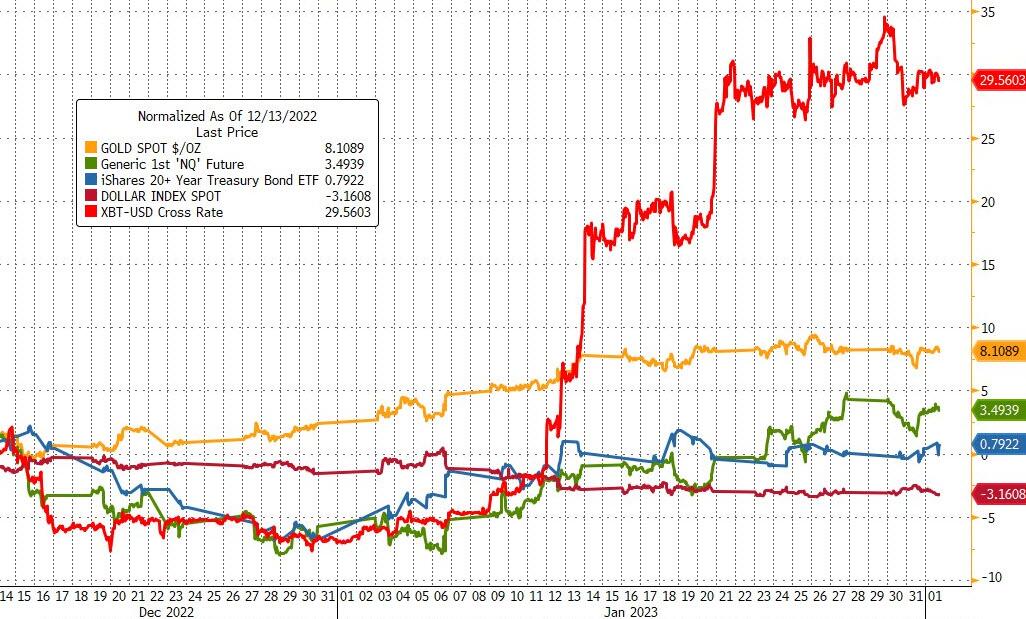

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 29.25 PTS OR .90% //Hang Seng CLOSED UP 229.485 PTS OR 1.05% /The Nikkei closed UP 19.77 PTS OR 0.07% //Australia’s all ordinaries CLOSED UP .31% /Chinese yuan (ONSHORE) closed UP 6.7423 //OFFSHORE CHINESE YUAN UP TO 6.7478// /Oil UP TO 79.40 dollars per barrel for WTI and BRENT AT 85.60 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

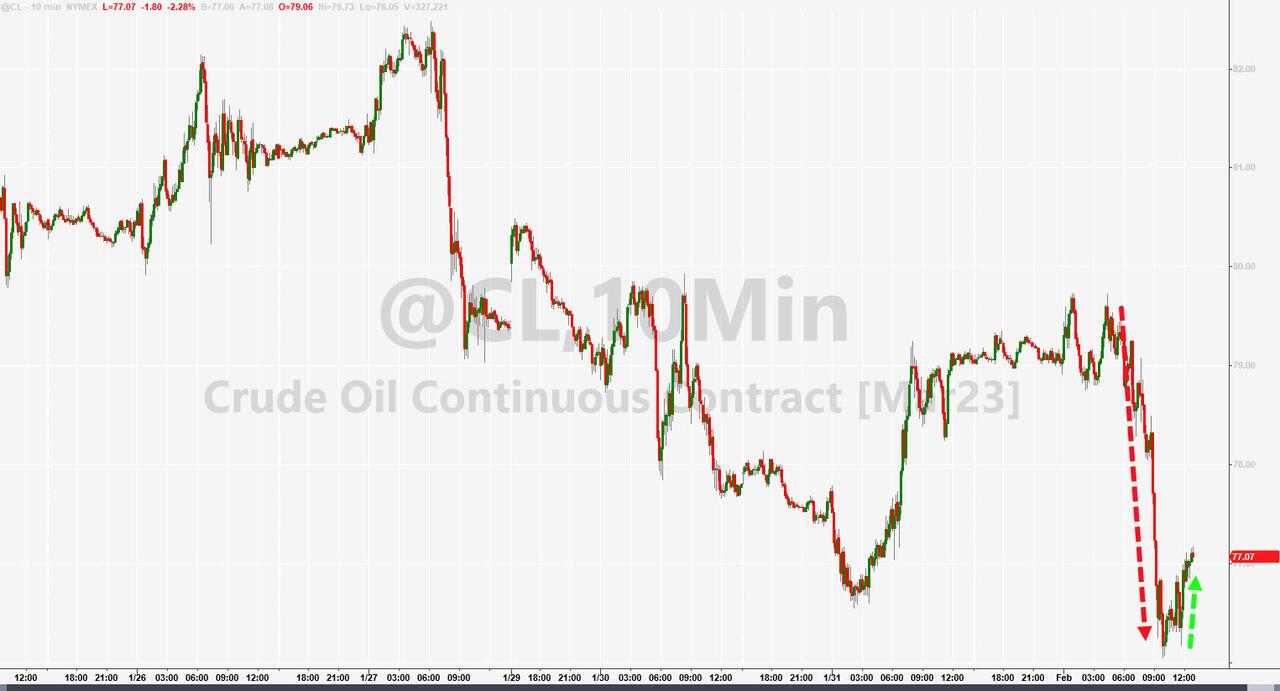

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 1024 CONTRACTS DOWN TO 471,642 DESPITE OUR GAIN IN PRICE OF $6.55

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1311 EFP CONTRACTS WERE ISSUED: : APRIL 1311 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1311 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A TINY SIZED TOTAL OF 287 CONTRACTS IN THAT 1311LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI LOSS OF 1024 CONTRACTS..AND THIS VERY TINY SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GAIN IN PRICE OF $6.55. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (41.219)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes(TOTAL THIS YEAR 656.076 TONNES

JAN/2023: 20.559 tonnes

FEB 2023: 41.219 tonnes

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $6.55) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A TINY GAIN OF 287 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 0.8926 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (41.219 TONNES) … ALL OF THIS WAS ACCOMPLISHED WITH OUR RISE IN PRICE TO THE TUNE OF $6.55.

WE HAD -157 CONTRACTS COMEX TRADES REMOVED FROM OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 287 CONTRACTS OR 28,700 OZ OR 0.8926 TONNES

Estimated gold comex today 192,763//poor//

final gold volumes/yesterday 172,423/// poor

INITIAL STANDINGS FOR FEB 2023 COMEX GOLD //FEB 1//

Total monthly oz gold served (contracts) so far this month

7574 notices 757400 23.558 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 1

i) Out of JPMorgan 12,781.796 oz (396kilobars)

Total withdrawals: 12,781.796 oz

total in tonnes: 0..3975 tonnes

Adjustments:0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEBRUARY.

For the front month of FEBRUARY we have an oi of 7242 contracts having lost 6133 contracts. We had 6005 notices

filed yesterday so we lost 128 contracts or an additional 12,800 oz were EFP’d by special delivery over to London for a future delivery

March gained 36 contracts to stand at 1957.

April gained 2930 contracts up to 391,554

We had 1569 notice(s) filed today for 156,900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1569 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 259 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB. /2023. contract month,

we take the total number of notices filed so far for the month (7574 x 100 oz ), to which we add the difference between the open interest for the front month of (FEBRUARY 7242 CONTRACTS) minus the number of notices served upon today 1569 x 100 oz per contract equals 1,325,200 OZ OR 41.219 TONNES the number of TONNES standing in this active month of January.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (7574 x 100 oz+ (7242 OI for the front month minus the number of notices served upon today (1569)x 100 oz} which equals 1,325200 oz standing OR 41.219 TONNES in this active delivery month of FEBRUARY..

TOTAL COMEX GOLD STANDING: 41.219TONNES. SO JUST LIKE LAST MONTH WE START WITH A LOW INITIAL AMOUNT OF GOLD STANDING BUT THIS WILL GROW AS THE MONTH PROCEEDS TO ITS CONCLUSION.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,221,653.076 OZ

TOTAL REGISTERED GOLD: 11,020,384.584 OZ (342.78 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 11,201,268.492 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,212,558 OZ (REG GOLD- PLEDGED GOLD) 286.54 tonnes//rapidly declining

END

SILVER/COMEX

FEB 1/2023//INITIAL. SILVER CONTRACT FOR FEBRUARY

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

554,174.446 oz Brinks Delaware JPMorgan

Deposits to the Dealer Inventory

nil OZ

Deposits to the Customer Inventory

30,059.350 oz Delaware

No of oz served today (contracts)

4 CONTRACT(S) (20,000 OZ)

No of oz to be served (notices)

68 contracts (340,000 oz)

Total monthly oz silver served (contracts)

41 contracts (205,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into Delaware: 30,059.350 oz

Total deposits: 30,059.350 oz

JPMorgan has a total silver weight: 148.877 million oz/291.558 million =51.11% of comex .//dropping fast

Comex withdrawals: 3

i) Out of Brinks 92,105.290 oz

ii) Out of Delaware: 969.956 oz

iii) Out of JPMorgan: 461,099.200 oz

Total withdrawals; 1,505,324.203 oz

adjustments: 1l dealer to customer

i) 154,055.390 oz Brinks

the silver comex is in stress!

TOTAL REGISTERED SILVER: 32.3215 MILLION OZ (declining rapidly).TOTAL REG + ELIG. 291.558 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JAN

silver open interest data:

FRONT MONTH OF FEB/2023 OI: 72 CONTRACTS HAVING LOST 36 CONTRACT(S.).

WE HAD 37 NOTICES FILED YESTERDAY, SO WE GAINED ONE CONTRACT OR AN ADDITIONAL 5,000 OZ OF SILVER WILL

STAND AT THE COMEX.

March LOST 18 CONTRACTS UP TO 106,009 contracts

TOTAL NUMBER OF NOTICES FILED FOR TODAY:4 for 20,000 oz

Comex volumes// est. volume today 64,787//fair

Comex volume: confirmed yesterday: 90,260 contracts ( very strong)

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 41 x 5,000 oz = 205,000 oz

to which we add the difference between the open interest for the front month of FEB(72) and the number of notices served upon today 4 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2023 contract month: 41 (notices served so far) x 5000 oz + OI for the front month of FEB (72 – number of notices served upon today (4) x 500 oz of silver standing for the FEB. contract month equates 0.545 million oz + 0 ( EXCHANGE FOR RISK) = 0.545MILLION OZ//(TOTAL OZ OF SILVER STANDING).

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

FEB 1/WITH GOLD DOWN $2.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 31/WITH GOLD UP $6.55 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 30/WITH GOLD DOWN $6.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 918.50 TONNES

JAN 27/WITH GOLD DOWN $0.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 919.37 TONNES

JAN 26/WITH GOLD DOWN $11.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 919.37 TONNES

JAN 25/WITH GOLD UP $7.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 917.34 TONNES

JAN 24/WITH GOLD UP $7.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 23/WITH GOLD UP $0.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.63 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 20/WITH GOLD UP $4.75 TODAY;BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 912.43 TONNES

JAN 19/WITH GOLD UP $16.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES INTO THE GLD///INVENTORY RESTS AT 910.98TONNES

JAN 18/WITH GOLD DOWN $1.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.9 TONNES FROM THE GLD////INVENTORY RESTS AT 909.24 TONNES

JAN 17/WITH GOLD DOWN $11.45 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.14 TONNES

JAN 13/WITH GOLD UP $22.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD///INVENTORY RESTS AT 912.14 TONNES

JAN 12/WITH GOLD UP $20.55 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 912.43 TONNES

JAN 11/WITH GOLD UP $1.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

DEC 30/WITH GOLD UP $.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 29//WITH GOLD UP $8.35 TODAY:; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 28/WITH GOLD DOWN $6.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE DEPOSIT OF 5.50 TONNES INTO THE GLD..//INVENTORY REST S AT 918.51 TONNES

DEC 27/WITH GOLD UP $18.15 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 913.01 TONNES

DEC 23/WITH GOLD UP $19,15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES/

DEC 22/WITH GOLD DOWN $29.35 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 21/WITH GOLD FLAT TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 913.88 TONNES

DEC 20/WITH GOLD UP $27.05: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES INTO THE GLD////INVENTORY RESTS AT 912.14 TONNES

DEC 19/WITH GOLD DOWN $2.10: HUGE CHANGES IN GOLD INVENTORY AT THE GLD> A BIG WITHDRAWAL OF 3.47 TONNES FROM THE GLD//INVENTORY RESTS AT 910.41 TONNES

DEC 16/WITH GOLD UP $12.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 15//WITH GOLD DOWN $31.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 911.56 TONNES

DEC 14/WITH GOLD DOWN $6.20: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 912.72 TONNES

DEC 13/WITH GOLD UP $32.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD///INVENTORY RESTS AT 910.41

DEC 12/WITH GOLD DOWN $17.60: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

DEC 9/WITH GOLD UP $8.90//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

Dec 8/WITH GOLD UP $4.05, OVER THE PAST 3 WEEKS WE LOST 2.04 TONNES//INVENTORY RESTS AT 908.09 TONNES

GLD INVENTORY: 917.06 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 1/WITH SILVER DOWN 20 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.4 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 519.000 MILLION OZ

JAN 31/WITH SILVER UP 12 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.5 MILLLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 520.400 MILION OZ

JAN 30/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 521.900 MILLION OZ.

JAN 27/WITH SILVER DOWN 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 521.900 MILLION OZ//

JAN 26/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 900,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 521.900 MILLION OZ//

JAN 25/WITH SILVER UP 19 CENTS TO TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.3 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 521.000 MILLION OZ

JAN 24/WITH SILVER UP 21 CENTS TODAY: WHAT!! A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 20 MILLION OZ INTO THE SLV/( OCCURRED (LATE LAST NIGHT)//INVENTORY RESTS AT 518.70 MILLION OZ//

JAN 23/WITH SILVER DOWN 40 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.4 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 498.7 MILLION OZ//

JAN 20.WITH SILVER UP 9 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 750,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 497.300 MILLION OZ

JAN 19/WITH SILVER UP 24 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 498.05 MILLION OZ

JAN 18/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 8.15 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 498.05 MILLION OZ///

JAN 17/WITH SILVER DOWN 35 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 13/WITH SILVER UP 46 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.5 MILLION OZ FROM THE SLV..//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 12/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 508.700 MILLION OZ/

JAN 11/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 508.700MILLION OZ

JAN 10/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ

JAN 9/WITH SILVER DOWN 9 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 6/WITH SILVER UP 54 CENTS TODAY;BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.20 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 5/WITH SILVER DOWN 50 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.10 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 505.45 MILLION OZ//

JAN 4/WITH SILVER DOWN 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 506.55 MILLION OZ/

JAN 3/WITH SILVER UP 24 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: STRANGE: A WITHDRAWAL OF 1.2 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 507.85 MILLION OZ/

DEC 30/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 29/ WITH SILVER UP $0.63 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 28//WITH SILVER DOWN 46 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.715 MILLION OZ INTO THE SLV///..INVENTORY RESTS AT 509.050 MILLION OZ

DEC 27/WITH SILVER UP 34 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 507.350 MILLION OZ//

DEC 23/WITH SILVER UP 29 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT507.900 MILLION O//

DEC 22/WITH SILVER DOWN 53 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 21/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.0 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 20/WITH SILVER UP 105 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:: A DEPOSIT OF 700,000 OZ INTO THE SLV///INVENTORY RESTS AT 509.90 MILLION OZ//

DEC 19/WITH SILVER DOWN 13 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.05 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.20 MILLION OZ//

DEC 16/WITH SILVER UP 2 CENTS; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.85 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 508.15 MILLION OZ//

DEC 15/WITH SILVER DOWN 78 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF EXACTLY 2.00 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 510.000 MILLION OZ

DEC 14/WITH SILVER UP 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 512.000 MILLION OZ//

DEC 13/WITH SILVER UP 59 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 600,000 OZ FROM THE SLV////INVENTORY RESTS AT 513.900 MILLION OZ//

DEC 12/WITH SILVER DOWN 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 514.500 MILLION OZ//

DEC 9/WITH SILVER RISING 77 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.2 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 514.500 MILLION OZ.

DEC 8/WITH SILVER RISING 34 CENTS TODAY: OVER THE PAST 3 WEEKS, WE HAVE GAINED A STRONG: 44.777 MILLION OZ/INVENTORY RESTS AT 516.700 MILION OZ.

CLOSING INVENTORY 519.00 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

3. Chris Powell of GATA provides to us very important physical commentaries//

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

end

5.IMPORTANT COMMENTARIES ON COMMODITIES: CARDBOARD BOXES

This is a strong indicator as to falling consumer demand /// uSA economy: cardboard boxes. Demand and output for boxes and other pkging material fell sharply in the 4th quarter of 2022

(Premack/FreightWaves)

Cardboard Box Demand Plunging At Rates Unseen Since The Great Recession

Demand and output for cardboard boxes and other packaging material fell sharply in the fourth quarter of 2022, according to data released by the American Forest & Paper Association and Fibre Box Association on Friday.

It’s the latest indicator that consumer demand is eroding following the pandemic. Dwindling savings, inflation, rising interest rates and fears of a recession may all be swaying consumers to spend less.

The American Forest & Paper Association reported that another type of packaging material called boxboard had its lowest operating rate in its five-year record during 2022’s final quarter. Boxboard is typically thinner than cardboard and lacks air pockets.

Box bloodbath? Cardboard crisis?

Box demand normally sees modest upticks of 1% to 2% each year. But government stimulus and the shift from service to goods demand through 2020 and 2021 shocked box demand into some of its fastest growth in history. Prices rose as much as 55% through this time, Josephson said.

A hangover after a yearslong cardboard carnival would be in order — and this one looks nasty.

“Inflationary pressures on the consumers have also added to the problem by reducing the consumers’ discretionary spending capabilities,” said Thomas Hassfurther, executive vice president of corrugated products at WestRock, in a Thursday call to investors. WestRock is the No. 2 largest packaging company in the U.S.

“In addition, consumer behavior changed very quickly as we exited the extreme COVID period, resulting in more of a preference towards travel, entertainment and experience versus that of tangible goods,” Hassfurther said. “Containerboard and box demand continues to be negatively impacted from the deterioration in U.S. and global economic conditions, rising interest rates and a cooler housing market.”

However, WestRock executives maintained that demand in 2023 still appeared “healthy” compared to pre-COVID times. On the Thursday call, they forecast shipments to be 6% higher in first-quarter 2023 compared to the same period in 2019, on a per-day basis.

A downturn after a wild upswing isn’t particularly shocking. What’s troublesome is that executives grew or made plans to grow in response to this unprecedented demand. An increase in supply will further drive down already-plummeting prices.

In the cardboard world, for example, more than 2 million tons per year of additional containerboard output is coming to the North American market. Ocean carriers expect to add a record-breaking number of new container ships through the next two years. And nearly 60 real estate firms, most of which expanded payrolls during the pandemic, have already had to lay off more than 13,000 workers through 2022 and 2023, according to Insider.

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.7423

OFFSHORE YUAN: 6.7478

SHANGHAI CLOSED UP 29.25 PTS OR .90%

HANG SENG CLOSED UP 229.85 PTS OR 1.05%

2. Nikkei closed UP 19.77 PTS OR 0.07%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 101.69 Euro RISES TO 1.0896 UP 35 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.476!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 129.75/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.282%***/Italian 10 Yr bond yield FALLS to 4.239%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.309…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.292//

3j Gold at $1930.00//silver at: 23.56 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 23/100 roubles/dollar; ROUBLE AT 70.04//

3m oil into the 79 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 129.75/10 YEAR YIELD AFTER BREAKING .54% FALLS TO .476% ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9158–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9978well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

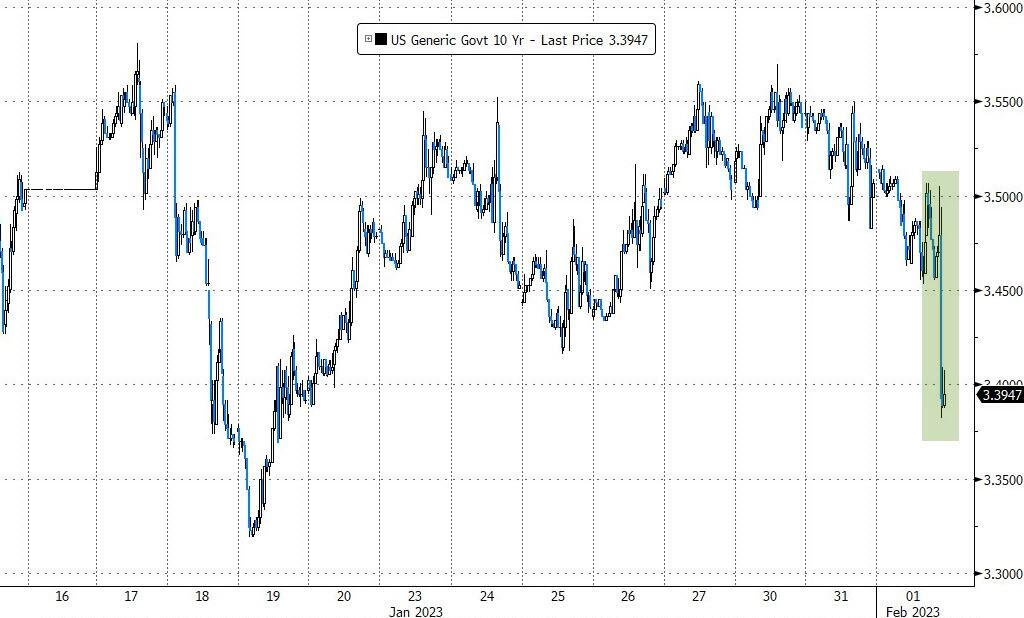

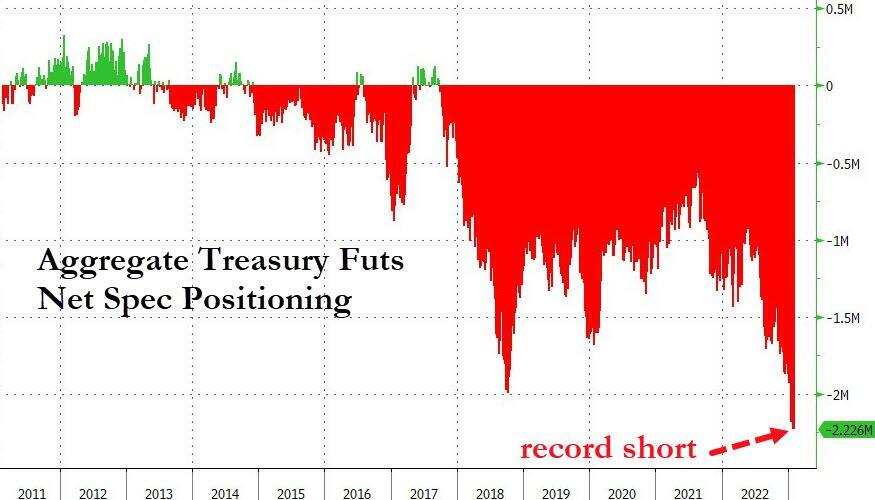

USA 10 YR BOND YIELD: 3.486% DOWN 4 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.61 DOWN 5 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,81…

GREAT BRITAIN/10 YEAR YIELD: 3.323% DOWN 3 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Dip As Markets Brace For Hawkish Fed Surprise

WEDNESDAY, FEB 01, 2023 – 08:05 AM

US stock index futures slipped on Wednesday – after a frenzied late rally into Tuesday’s month-end thanks to a monstrous, $6 billion in Market on Close buy orders – but were off session lows as investors awaited the Fed’s policy decision after a stellar start to the year for stocks amid speculation the central bank will signal a slowdown in the pace of rate hikes.

Futures on the S&P 500 were 0.2% lower, trading around 4083, while Nasdaq 100 futs popped into the green as of 745am ET, with both underlying indexes surging more than 1% on Tuesday. The Nasdaq soared more than 10% in January in a furious short-covering rebound unseen in more than two decades. An index of global stocks excluding the US is making history with a gain of 8.6% last month — the best start to a year on record. Elsewhere, European and Asian stocks rose, the 10-year Treasury yield fell about three basis points and the dollar index dipped before the Fed statement, where it’s forecast to unveil a 25 basis point rate increase.

Among notable movers in premarket trading, Electronic Arts Inc. after the video game maker cut its full-year forecast and announced a six-week delay in the release of its next Star Wars game. Chipmaker AMD rose after the chipmaker gave a sales forecast that was better than feared, helped by gains in the server market. Perennial loser Snap plunged as the social media company gave a weaker-than-expected forecast, saying changes to its advertising products may be “disruptive” to its business. Shares of other companies that get a bulk of their revenue from online advertising, including Meta and Pinterest also dropped. Bank stocks were also lower in premarket trading Wednesday as traders await the Federal Reserve’s interest rate decision. JPMorgan is planning to launch a digital bank in Germany as its second international consumer outpost. Meanwhile, some users of bankrupt crypto lender Celsius Network’s Custody program will be able to withdraw 94% of their eligible assets, according to a court filing. Here are some other notable premarket movers.

Peloton jumped 8% after it reported improved cash flow and a narrower net loss in the latest quarter, leading Chief Executive Officer Barry McCarthy to say that questions about the viability of the business have been “put to bed.”

Chinese stocks listed in the US rise in premarket trading, poised to end three days of declines, with Baidu and electric-vehicle stocks leading the way. Li Auto (LI US) +6%, XPeng (XPEV US) +4.1%, Baidu (BIDU US) +7.9%, Alibaba (BABA US) +1.5%, Pinduoduo (PDD US) +2.6%, Bilibili (BILI US) +3.1%

Western Digital shares slide 4.5% after its revenue forecast for the third quarter fell short of estimates. Analysts blamed weakness in the NAND flash market and PC demand, though some were hopeful that the data-storage device maker could weather the storm.

Electronic Arts shares fall 11% after the video-game company cut its full-year forecast and announced a six-week delay in the release of its next Star Wars game.

Match Group slides 8.7% after the dating services firm gave guidance for 1Q23 showing little fundamental business improvement is expected near-term.

Keep an eye on Rocket Pharmaceuticals (RCKT US) stock as Morgan Stanley initiates coverage with an overweight recommendation, saying the biotech is a leader in gene therapy with a robust cardiovascular pipeline and a hematology pipeline providing near-term revenue.

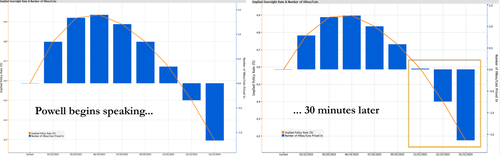

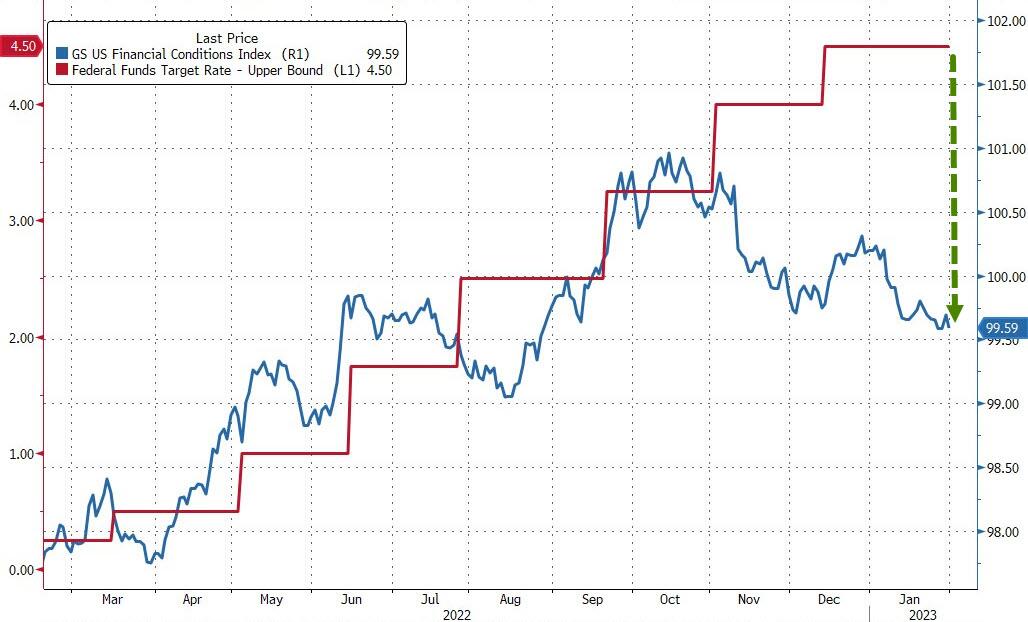

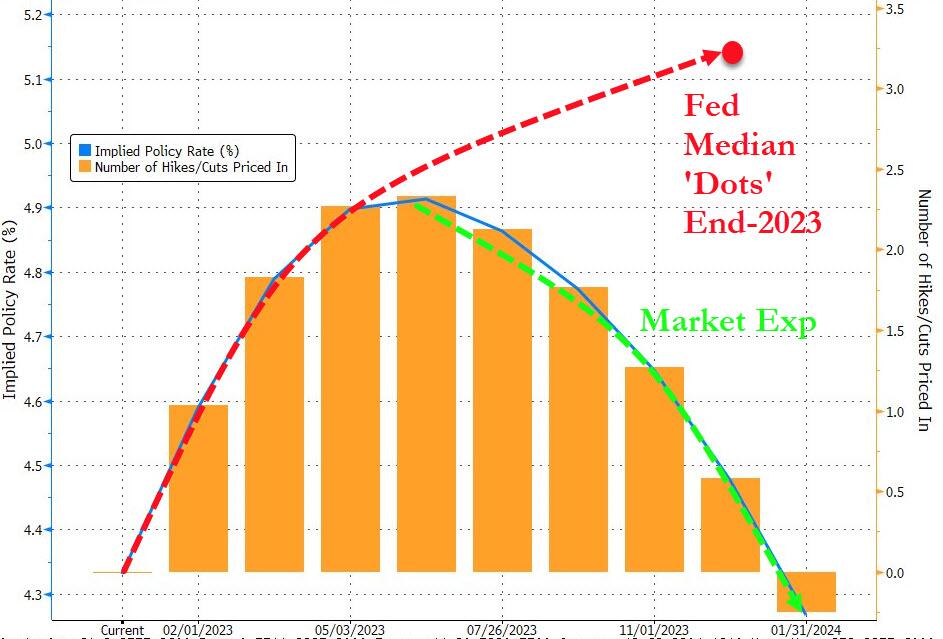

Today’s key event is the FOMC decision due at 2pm (preview here). Economists widely expect the central bank to raise rates by 25 basis points at the conclusion of its two-day meeting Wednesday. Chair Jerome Powell is likely to keep further hikes on the table while leaning against bets they will cut rates later this year.

“Powell will certainly sound satisfied about the falling inflation and slowing wages, but he will likely point out that inflation remains high, risks to inflation remain to the upside and that the job is not done yet,” said Ipek Ozkardeskaya, senior analyst at Swissquote Bank. “He will surely push back the expectation of any rate cut this year” and a hawkish statement could further weigh on stocks, she said.

Wage cost data that undershot forecasts, a cooling housing market dwindling consumer confidence suggest the Fed’s rate hikes over the past year have begun to curtail inflation, but still-loose financial conditions are complicating the central bank’s task.

“The question is will the Fed emphasize a pause or push back against the easing being priced in for this year and the next,” said Steve Donzé, deputy head of investment at Pictet Asset Management in Tokyo. “The market is worried about this, because a lot of this rally was helped by softer yields and the dollar and if the Fed starts to fight the easing that’s priced in it will have consequences for the yield curve and equities.”

Powell will also try to push back against easing financial conditions which are now as loose as they were in Jun 2022 when Fed Funds were 1.75%.

Focus is also on company earnings, with analysts expecting the first quarterly drop in US profits since 2020. Investors can no longer count on some crucial tailwinds that helped spur a remarkable two-decade stretch of earnings growth, according to Bank of America.

In Europe, the Stoxx Europe 600 index pared most of its early gain after a report showed inflation in the euro area slowed more than economists’ expectations in January. The the core measure remained sticky, however, suggesting heated debate to come at the European Central Bank over how much more interest rates must rise. The central bank is expected to lift its policy rate by 50 basis points on Thursday. Here are some of the biggest European movers:

GSK shares turned lower after gaining as much as 1.5% as its quarterly sales and profit both topped expectations, driven by a strong performance in the vaccines division and HIV drug portfolio

ABB shares rise as much as 1.3% after the Swiss automation company’s EV-charging business raised additional funds from minority investors

Husqvarna rises as much as 7% as the Swedish lawn care and outdoor equipment firm’s organic sales growth, particularly for its robotic products, led to an outperformance in 4Q

BBVA shares advance as much as 2.5% after it reported earnings which Jefferies described as solid. Analysts also noted the upbeat outlook for 2023

Virgin Money UK shares gain as much as 1.2% after the bank forecast net interest margin for the full year of 1.85% to 1.9%, in an update seen as “neutral” by Morgan Stanley

Darktrace shares rise as much as 6%, recovering from a two-day 17% slump, after the cybersecurity firm announced plans to buy back shares

Vodafone shares decline as much as 3.3% in early trading, after the telecom operator reported a further slowdown in service revenue growth in core markets including Germany and Spain

SEB falls as much as 4.4% after Trygg-Stiftelsen sold 75m shares in the bank at a price of SEK120 apiece, representing a 4.9% discount versus Tuesday’s close

Novartis dips as much as 1.9% after the Swiss drugmaker’s quarterly sales were a touch behind expectations due to a miss for psoriasis treatment Cosentyx

“Headline inflation continues to fall across the eurozone but core inflation, which strips out food and energy, flatlined,” said John Leiper, Chief Investment Officer at Titan Asset Management. “Price pressure, particularly in the services sector, will remain elevated for some time. Given the economy is holding up far better than predicted we expect the ECB to hike interest rates again on Thursday by a widely anticipated 50 basis points.”

Earlier in the session, Asian stocks rose ahead of the Federal Reserve’s interest-rate decision, as signs of cooling US inflation boosted risk appetite in the region. The MSCI Asia Pacific Index rose as much as 0.8%, driven by technology and consumer discretionary shares. Benchmarks in Hong Kong as well as the tech-heavy markets of South Korea and Taiwan all gained about 1%, while India declined. All eyes were on the Fed meeting later Wednesday, with markets expecting a 25-basis-point rate hike. Investors betting on a downshift in tightening were cheered by data showing slower growth in US employment costs, adding to signs of moderating inflation.

“Wall Street is slowly growing confident that this week’s Fed rate hike might end up being the last one in this tightening cycle,” said Edward Moya, senior market analyst at Oanda. “The economy is weakening and that is fueling Fed rate cut bets at the end of the year.” India’s benchmarks erased early gains driven by a budget boost, as a selloff among Adani group’s stocks accelerated in afternoon trading.

In India, Adani Group stocks resumed their selloff after the share sale by the Indian conglomerate’s flagship firm failed to turn sentiment from Hindenburg Research’s fraud allegations. In one bright spot for the group, nearly all dollar bonds issued by Adani companies extended gains into a second day.

Japanese stocks closed mixed ahead of the Federal Reserve meeting later Wednesday and as investors weighed domestic company results. The Topix fell 0.2% to close at 1,972.23, while the Nikkei advanced 0.1% to 27,346.88. Lasertec contributed the most to the Topix decline, falling 14% after the chip-equipment maker reported quarterly profit that missed analyst estimates and trimmed its order outlook. Out of 2,164 stocks in the index, 935 rose and 1,134 fell, while 95 were unchanged. “There is a consensus that the FOMC may end interest-rate hikes in March,” said Naoki Fujiwara, chief fund manager at Shinkin Asset Management. “After that, we would want to see the impact on the economy”.

Australian stocks rose with the S&P/ASX 200 index 0.3% higher to close at 7,501.70, boosted by gains in mining stocks and banks, as investors await the Federal Reserve’s policy meeting. Flight Centre was the top performer, surging 8% after the travel agency successfully completed a A$180 million placement to buy UK-based luxury travel brand Scott Dunn and provided a trading update. In New Zealand, the S&P/NZX 50 index rose 1% to 12,090.93.

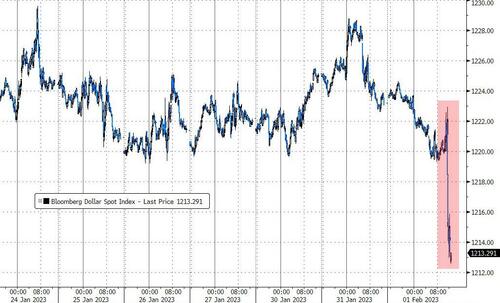

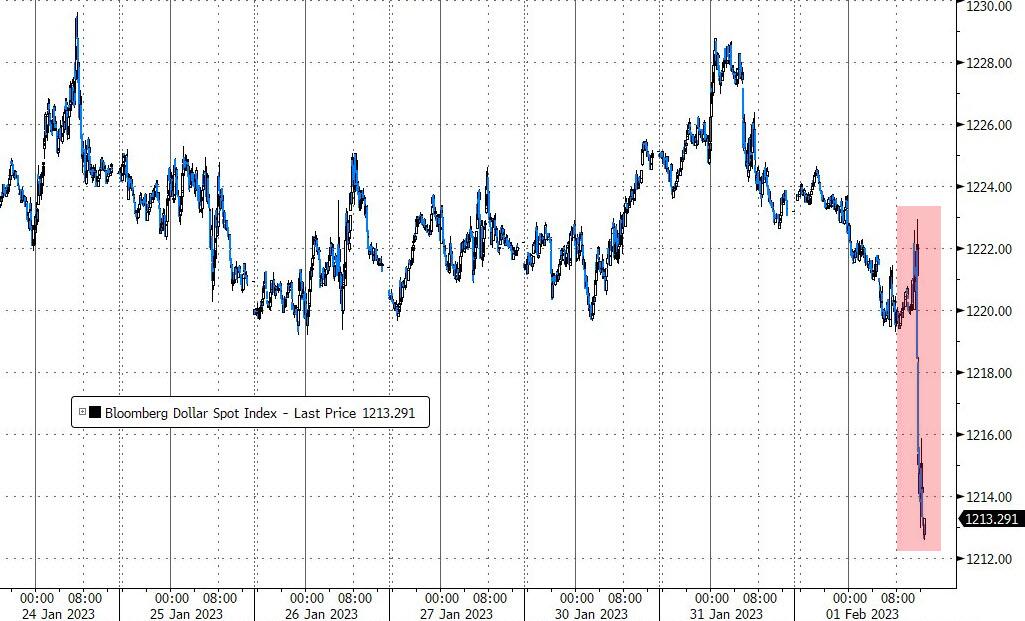

In FX, the Bloomberg Dollar Spot Index eased 0.1% ahead of the Fed policy decision later on Wednesday where it’s expected to raise rates by 25 basis points. The greenback was steady to weaker against its most Group-of-10 peers, with Scandinavian currencies topping the G-10 leaderboard. The Treasury curve bull flattened, with the 10-year yield dropping by about 4bps.

The euro inched up toward $1.09 though options suggest a move above $1.10 after the Fed and the ECB is unlikely. Euro-zone bonds pared an advance after core-CPI for the region came in higher than estimated in January, while the headline number eased more than forecast.

The pound underperformed most of its Group-of-10 peers, trading little changed against a the US dollar. Domestic focus remains on Thursday’s BOE decision.

New Zealand’s dollar was steady while short-maturity bonds gained and traders trimmed bets on a rate hike at the RBNZ’s February meeting after employment data missed estimates.

Treasury yields are slightly lower across the curve, with gilts outperforming over the early London session across the belly of the curve. US yields are richer by up to 2.5bp across the long end of the curve, which is outperforming slightly, flattening 2s10s, 5s30s spreads by 1.8bp and 0.5bp; 10-year yields around 3.485%, outperforming bunds by 3bp in the sector — the front end and belly of the UK curve is outperforming over the early London session. Fed-dated swaps market is pricing in around 27bp of rate hike premium for Wednesday’s decision and 47bp over the Feb. and March meetings; policy peak is priced at around 4.92% by the June meeting. The US session focus is on manufacturing data in the morning, before attention shifts to the Federal Reserve’s interest-rate decision at 2 p.m. in Washington and Chair Jerome Powell’s press conference 30 minutes later.

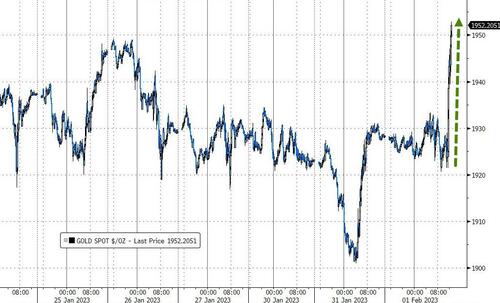

In commodities, crude futures are little changed, with WTI trading near $79.00. Spot gold falls roughly 0.1% to trade near $1,926

Looking to the day ahead now, and the main highlight will be the Fed’s latest policy decision as well as Chair Powell’s press conference. Otherwise, data releases include the flash CPI release for the Euro Area in January, as well as the unemployment rate for December. Alongside that, there’s the global manufacturing PMIs for January and in the US we’ve got the ISM manufacturing print for January, the ADP’s report of private payrolls, and the JOLTS job openings for December. Finally, earnings releases today include Meta.

Market snapshot

S&P 500 futures down 0.2% to 4,084

MXAP up 0.7% to 169.15

MXAPJ up 1.0% to 554.79

Nikkei little changed at 27,346.88

Topix down 0.2% to 1,972.23

Hang Seng Index up 1.1% to 22,072.18

Shanghai Composite up 0.9% to 3,284.92

Sensex little changed at 59,576.27

Australia S&P/ASX 200 up 0.3% to 7,501.66

Kospi up 1.0% to 2,449.80

STOXX Europe 600 up 0.2% to 454.03

Gold spot down 0.2% to $1,923.98

U.S. Dollar Index down 0.12% to 101.97

German 10Y yield little changed at 2.26%

Euro up 0.2% to $1.0880

Brent Futures little changed at $85.38/bbl

Top overnight News from Bloomberg

The EU risks missing a March target to agree on a reform of its debt-limit rules in the face of resistance from countries including Germany, a prospect that may force member states into abrupt and potentially painful budgetary adjustments

For bond investors looking to bet big on a rally this year, signs of distress in the world’s highly-leveraged housing markets are only adding to their conviction. Places like the UK, New Zealand and Sweden — where house prices are slumping and mortgage payments are rocketing — are high on their watchlist

Shaky property markets across much of the world pose another risk to the global economy as higher interest rates erode household finances and threaten to exacerbate falling prices

Swathes of office staff have been forced to work from home Wednesday as widespread industrial action closes schools and cripples Britain’s rail network. As many as 475,000 union members are on strike

Chinese President Xi Jinping called for enhanced efforts to boost consumption in order to realize a virtuous economic cycle, as the world’s second largest economy gradually recovers from Covid Zero

A surge in Chinese spending last month has spurred more optimism about the country’s economic rebound, though weakness among manufacturers and sales of cars and homes still suggest the recovery isn’t yet on sure footing

Asia’s manufacturers are improving at the start of the year as the region becomes more optimistic about the boost from China’s reopening, while activity in the euro area shows the downturn is softening as cost pressures ease

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded higher after the positive lead from Wall St where stocks advanced into month-end and which was facilitated by the softer Employment Cost growth in the US, although gains were capped by the approaching FOMC rate decision and after disappointing Chinese Caixin Manufacturing PMI data. ASX 200 was led higher by strength in the mining and materials sectors after a rebound in commodity prices and with an upgrade in the Final Australian Manufacturing PMI also conducive for risk appetite. Nikkei 225 briefly climbed above 27,500 but closed off its highs amid a deluge of earnings releases and after Japan’s manufacturing activity was confirmed to have declined for a 3rd consecutive month. Hang Seng and Shanghai Comp. were positive albeit with momentum restricted after Chinese Caixin Manufacturing PMI missed forecasts and printed a 6th consecutive month in contraction territory which was in contrast to the recent rebound seen in China’s official PMIs.

Top Asian News

US Defence Secretary Austin’s visit to Manila is expected to bring a deal on expanded US access to bases in the Philippines, according to a senior Philippines official cited by Reuters.

China’s President Xi says the need to coordinate expansion of domestic demand with deepening supply-side structural reforms, via State Media.

China securities regulator CSRC has released draft rules for IPO registration system reform for 1st February.

Tiny Radioactive Device Found in Australia After Desert Hunt

Modi Aims to Please All With $550 Billion India Budget

Gold Steadies as Traders Await Fed Meeting for Rate Outlook

China Lifts Southeast Asia Factories as Europe Downturn Softens

Insurers Top Losers as India Budget Seeks to Tighten Tax Rules

Adani Rout Passes $90 Billion as Stock Sale Fails to Stem Doubt

European bourses are little changed overall but with a modest positive bias, Euro Stoxx 50 +0.2%, ahead of data points and the FOMC. Sectors are predominantly in the green, but with the overall breadth narrow and no overarching theme in play despite numerous large cap earnings in the European morning; click here and here for details. Stateside, futures are a touch softer after yesterday’s strength, ES -0.4%, with after-market updates weighing ahead of data and the Fed’s policy announcement/press conference. Advanced Micro Devices, Inc. (AMD) – Q4 sales and profits topped expectations, but warns of revenue decline in Q1. +3.3% in pre-market trade Tesla (TSLA) intends to increase the Shanghai plant’s average weekly output to nearly 20k vehicles for Feb and March, according to an internal memo cited by Reuters.

Top European News

UK and EU reached a customs agreement which could pave the way for an end of post-Brexit wrangling over Northern Ireland, according to The Times.

Officials in Brussels have reportedly dismissed claims of a compromise deal on the ECJs role in the N. Ireland Protocol, via BBC’s Parker citing sources; Parker adds, “A precise timeline isn’t clear but one official says negotiators are in the “tunnel”.”.”Regardless any compromise of that kind would also represent a significant UK concession, as well as an EU one.” (re. the ECJ).

RTE’s Connelly, on reports of an EU/UK deal on the NI protocol, says there is “Nothing new. Talks ongoing. Progress (is) being made but no sign of anything imminent.”, citing a source.

FX

The DXY is subdued and holding modestly below the 102.00 mark with slightly softer US yields vs global peers and the pre-FOMC risk tone exerting modest pressure on the USD.

EUR and AUD are the current outperformers despite a fleeting dip in EUR/USD following EZ Flash CPI while AUD is benefiting from soft New Zealand labour data and a subsequent paring in RBNZ rate expectations; EUR/USD just shy of 1.09 while AUD/USD resides near 0.708.

CAD remains near 1.33 pre-data while Cable has extended above the 1.23 mark irrespective of a pushback on reporting of an EU/UK compromise.

SEK and NOK have benefitted somewhat from their respective PMIs, though EUR upside caps gains, while the INR has slipped post-budget.

PBoC set USD/CNY mid-point at 6.7492 vs exp. 6.7499 (prev. 6.7604)

Fixed Income

EGBs are firmer but well off initial best levels, with Bunds below 137.00 after more than paring a knee-jerk spike on the EZ Flash CPI release, where once again the headline cooled but core remains firmer.

Gilts are faring better than their German peer post-supply, with the 2033 Green Gilt better received than the 2033 Bund, which required a hefty retention.

USTs are marginally outperforming and towards the top-end of 114.17+ to 114.30 parameters with yields lower as such and action most pronounced at the long-end of the curve.

Commodities

Crude benchmarks have seen some modest two-way action throughout the morning, though the benchmarks are in relatively narrow ranges and near the unchanged mark overall.

Action which comes ahead of the OPEC+ JMMC event, which is not a decision-making meeting, and other risk events throughout the session.

US Energy Inventory Data (bbls): Crude +6.3mln (exp. +0.4mln), Cushing +2.7mln, Gasoline +2.7mln (exp. +1.4mln), Distillate +1.5mln (exp. -1.3mln).

OPEC+ JMMC has been pushed back one hour to 13:00GMT/08:00EST, according to Energy Intel.

Spot gold is little changed around the USD 1925/oz mark, given the broader tentative pre-FOMC price action. Base metals are softer following the miss in China’s Caixin PMI release.

Geopolitics

US is readying a USD 2.2bln weapons package for Ukraine which includes longer-range rockets for the first time, according to two officials cited by Reuters.

Russian Kremlin says that potential US supplies of long-range missiles to Ukraine would escalate tensions but would not stop Russia from achieving its goals; as bad as the present situation is, Russia believes the START treaty is very important; no current plans to hold talks between Russian President Putin and US President Biden, according to Sky News Arabia.

Belarusian servicemen have begun full independent operation of the Iskander missile system, according to the defence ministry.

US Event Calendar

07:00: Jan. MBA Mortgage Applications -9.0%, prior 7.0%

08:15: Jan. ADP Employment Change, est. 180,000, prior 235,000

09:45: Jan. S&P Global US Manufacturing PMI, est. 46.8, prior 46.8

10:00: Dec. Construction Spending MoM, est. 0%, prior 0.2%

10:00: Dec. JOLTs Job Openings, est. 10.3m, prior 10.5m

10:00: Jan. ISM Manufacturing, est. 48.0, prior 48.4

New Orders, prior 45.2, revised 45.1

Employment, prior 51.4, revised 50.8

Prices Paid, est. 40.4, prior 39.4

Central Banks

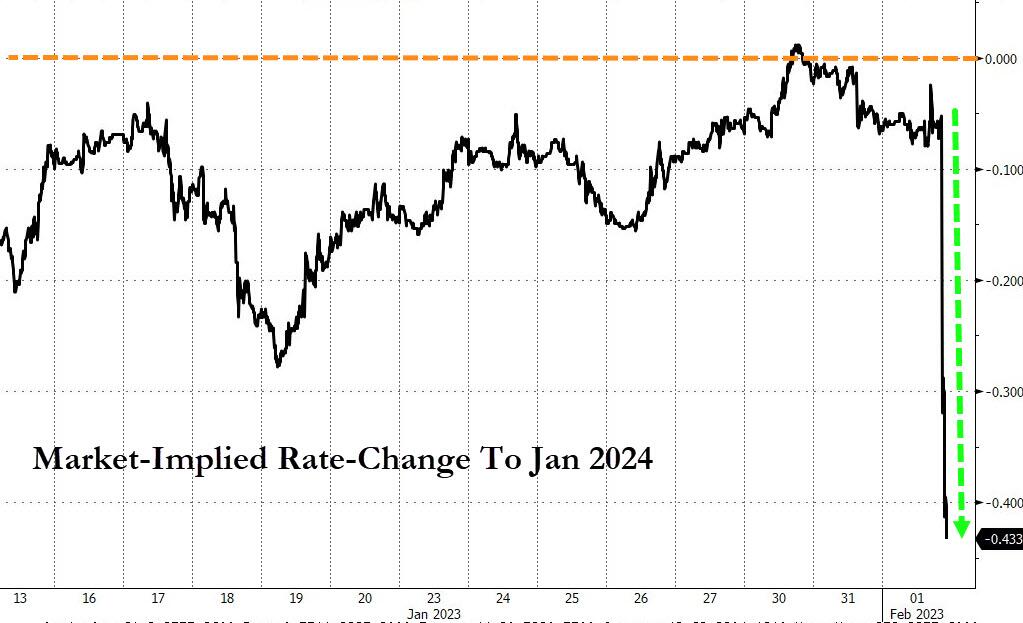

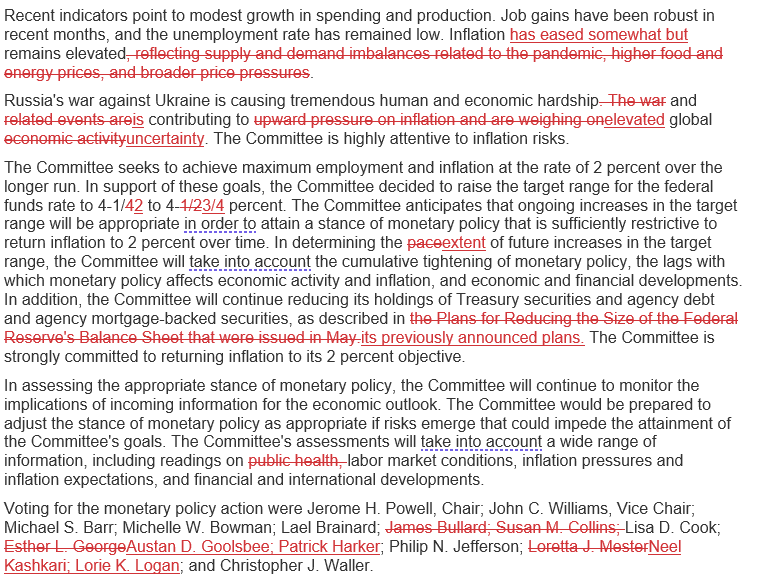

14:00: Feb. FOMC Rate Decision (Lower Bound est. 4.50%, prior 4.25%; Upper Bound est. 4.75%, prior 4.50%)

14:00: Feb. Interest on Reserve Balances R, est. 4.65%, prior 4.40%

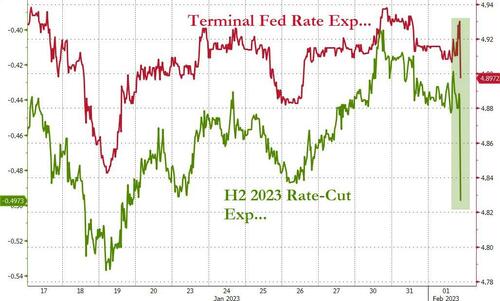

DB’s Jim Reid concludes the overnight wrap

After a very positive January, the start of February today marks a pivotal three days for markets that have the potential to decisively set the tone for the weeks ahead. That begins this morning with the flash CPI release from the Euro Area for January, before we have the Fed’s latest policy decision and Chair Powell’s press conference tonight. Then tomorrow we’ve got more policy decisions from the ECB and the BoE, an array of major earnings including Apple, Amazon and Alphabet, followed up by the US jobs report for January on Friday.

The last time we had a big round of central bank meetings like this in December, the rate hikes themselves were much as expected, but the hawkish rhetoric alongside them led to a big selloff. Nevertheless, the mood going into this round is much more optimistic, with the S&P 500 (+1.46%) closing at a 2-month high after the US Employment Cost Index numbers showed labour costs grew by less-than-expected, whilst the French CPI release also came in much as expected (unlike the Spanish print the previous day). So all eyes are now on the Fed to see whether they maintain their hawkish tone of recent meetings, or whether there might be any signals of a potential pause at future meetings.

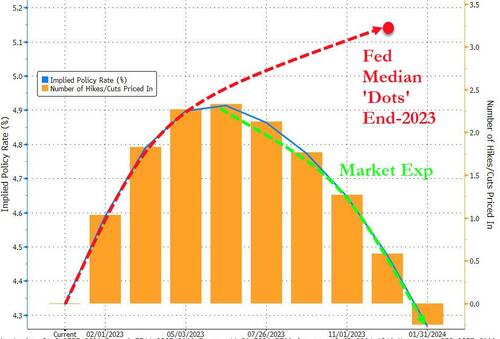

When it comes to the Fed’s decision today, a 25bps rate hike is now widely expected by both markets and economists, and anything other than that would be a massive shock. It would also mark the first “normal” sized hike since March 2022 when this hiking cycle began, before they embarked on a series of supersized hikes to swiftly get the policy rate into restrictive territory. Given that the 25bps move is anticipated, the main focus today will instead be on any changes to forward guidance, both in the statement and from Fed Chair Powell’s press conference.

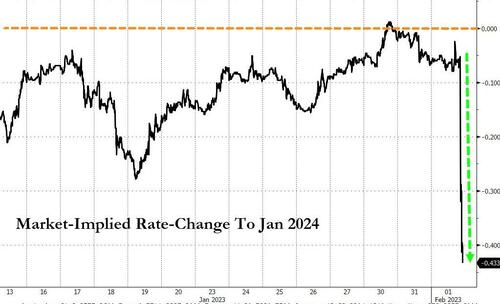

In their preview (link here), our US economists write that the statement is likely to keep the reference to “ongoing” rate hikes. Their view is that although the FOMC might be inclined to adjust this language as it moves closer to a pause, doing so now has little upside and risks widening the existing gap between market expectations and a more hawkish Fed. In terms of market expectations, futures are currently pricing in one more 25bps hike after today’s move, but only a one-in-three of another move after that. Indeed, terminal rate pricing points to just +58.3bps of further hikes, so closer to 50bps than 75bps. Futures are also indicating that the Fed will start cutting by year-end, which is contrary to the last FOMC minutes in December, where it said that “no participants” thought it would be appropriate to start cutting rates in 2023.

Ahead of the decision, there was some good news from their perspective in the latest ECI numbers for Q4. That’s closely followed by the Fed and showed an increase in employment costs of +1.0% (vs. +1.1% expected), which is the slowest quarterly increase in a year and added to the signs that wage growth is moderating. Nevertheless, if you wanted a more negative perspective, it’s still running above levels consistent with their target, and is above what we saw throughout the entirety of the 2010s. So as with the inflation figures, the Fed still have a way to travel before they can be comfortable about reaching their target, even if we’ve come off the highs from early 2022.

This optimism on the inflation side got added support from the French CPI numbers yesterday, with the EU-harmonised print at +7.0% as expected. That was a bit higher than the +6.7% in December, but the good news from an investor perspective was that it didn’t exceed expectations, unlike the Spanish print on Monday. All eyes will now be on the release for the Euro Area as a whole at 10:00 London time, and particularly on core inflation which hit a record 5.2% in December.

With all that to look forward to, markets staged a decent rally yesterday and the S&P 500 was up +1.46% to recover from its slump on Monday. The moves were part of a broad-based advance, with all 24 industry groups gaining on the day, led by autos (+4.32%), transports (+3.19%), retail (+2.24%), and materials (+2.22%). The worst performing industries were more defensive sectors, but even they advanced on the day as well. Meanwhile, the small-cap stocks in the Russell 2000 (+2.45%) were a particular outperformer as they closed at a 5-month high. The performance in Europe was rather weaker, with the STOXX 600 down -0.26%, but they hadn’t experienced the late selloff after the previous day’s close either.

Sovereign bonds also rallied ahead of the various meetings, with yields on 10yr Treasuries seeing a decline of -3.0bps decline to 3.507%, with yields remaining fairly stable overnight. That was echoed in Europe as well, where there were slightly larger moves in yields for 10yr bunds (-3.2bps), OATs (-3.4bps) and BTPs (-4.4bps). Those moves followed a small decline in terminal rate pricing for the Fed down -1.3bps on the day, while expectations for the ECB were basically unchanged (-0.6bps).

Overnight in Asia, that positive mood has continued with the major indices recovering after the previous day’s losses. Currently, the KOSPI (+0.72%) is leading gains with the Shanghai Comp (+0.29%), Hang Seng (+0.27%), CSI 300 (+0.25%) and the Nikkei (+0.09%), posting smaller advances. That’s also in spite of overnight data showing that Chinese manufacturing activity shrank more than expected in January, with the Caixin manufacturing PMI at 49.2 (vs. 49.8 expected), even if that was up from the 49.0 reading in December. Outside of Asia, the picture is a bit less positive as well, with futures on the S&P 500 (-0.28%) and the NASDAQ 100 (-0.39%) in negative territory ahead of the Fed’s decision today.

Looking at yesterday’s other data, the Euro Area economy unexpectedly grew by +0.1% in Q4 (vs. -0.1% expected), so avoiding a recession for the time being. That said, plenty of countries still saw a quarterly contraction, including Germany (-0.2%), Italy (-0.1%), Sweden (-0.6%) and Austria (-0.7%). Otherwise, UK mortgage approvals fell more than expected to 35.6k in December (vs. 45.0k expected), which is their lowest level since May 2020 when the economy was affected by the Covid-19 pandemic.

To the day ahead now, and the main highlight will be the Fed’s latest policy decision as well as Chair Powell’s press conference. Otherwise, data releases include the flash CPI release for the Euro Area in January, as well as the unemployment rate for December. Alongside that, there’s the global manufacturing PMIs for January and in the US we’ve got the ISM manufacturing print for January, the ADP’s report of private payrolls, and the JOLTS job openings for December. Finally, earnings releases today include Meta.

AND NOW NEWSQUAWK (EUROPE/REPORT)

Relatively contained trade ahead of key data, earnings & FOMC – Newsquawk US Market Open

WEDNESDAY, FEB 01, 2023 – 06:34 AM

European bourses are little changed overall but with a modest positive bias, Euro Stoxx 50 +0.2%, ahead of data points and the FOMC.

Stateside, futures are a touch softer after yesterday’s strength, ES -0.4%, with an after-market update from Snap weighing on peers

The DXY is subdued and holding modestly below the 102.00 mark with slightly softer US yields vs global peers exerting pressure

EGBs are firmer but well off initial best levels, with Bunds below 137.00 after more than paring a knee-jerk spike on the EZ Flash CPI release, where once again the headline cooled but core remains hot.

Crude benchmarks have seen some modest two-way action throughout the morning, though the benchmarks are in relatively narrow ranges and near the unchanged mark overall.

Looking ahead, highlights include US Final Manufacturing PMI, US ADP, ISM Manufacturing, JOLTS, Construction Spending, FOMC Policy Announcement & Press Conference, OPEC+ JMMC, US Quarterly Refunding Announcement, Earnings from McKesson, AmerisourceBergen, Meta, T-Mobile, Thermo Fisher, & Altria.

Or why not try Newsquawk’s squawk box free for 7 days?

EUROPEAN TRADE

EQUITIES

European bourses are little changed overall but with a modest positive bias, Euro Stoxx 50 +0.2%, ahead of data points and the FOMC.

Sectors are predominantly in the green, but with the overall breadth narrow and no overarching theme in play despite numerous large cap earnings in the European morning; click here and here for details.

Stateside, futures are a touch softer after yesterday’s strength, ES -0.4%, with after-market updates weighing ahead of data and the Fed’s policy announcement/press conference.

Advanced Micro Devices, Inc. (AMD) – Q4 sales and profits topped expectations, but warns of revenue decline in Q1. +3.3% in pre-market trade

Snap Inc (SNAP) – DAUs and DAUs guide was weak, while it does not provide revenue guidance and sees Q1 revenues falling. -15% in pre-market trade

Tesla (TSLA) intends to increase the Shanghai plant’s average weekly output to nearly 20k vehicles for Feb and March, according to an internal memo cited by Reuters.

The DXY is subdued and holding modestly below the 102.00 mark with slightly softer US yields vs global peers and the pre-FOMC risk tone exerting modest pressure on the USD.

EUR and AUD are the current outperformers despite a fleeting dip in EUR/USD following EZ Flash CPI while AUD is benefiting from soft New Zealand labour data and a subsequent paring in RBNZ rate expectations; EUR/USD just shy of 1.09 while AUD/USD resides near 0.708.

CAD remains near 1.33 pre-data while Cable has extended above the 1.23 mark irrespective of a pushback on reporting of an EU/UK compromise.

SEK and NOK have benefitted somewhat from their respective PMIs, though EUR upside caps gains, while the INR has slipped post-budget.

PBoC set USD/CNY mid-point at 6.7492 vs exp. 6.7499 (prev. 6.7604)

EGBs are firmer but well off initial best levels, with Bunds below 137.00 after more than paring a knee-jerk spike on the EZ Flash CPI release, where once again the headline cooled but core remains firmer.

Gilts are faring better than their German peer post-supply, with the 2033 Green Gilt better received than the 2033 Bund, which required a hefty retention.

USTs are marginally outperforming and towards the top-end of 114.17+ to 114.30 parameters with yields lower as such and action most pronounced at the long-end of the curve.

Crude benchmarks have seen some modest two-way action throughout the morning, though the benchmarks are in relatively narrow ranges and near the unchanged mark overall.

Action which comes ahead of the OPEC+ JMMC event, which is not a decision-making meeting, and other risk events throughout the session.

US Energy Inventory Data (bbls): Crude +6.3mln (exp. +0.4mln), Cushing +2.7mln, Gasoline +2.7mln (exp. +1.4mln), Distillate +1.5mln (exp. -1.3mln).

OPEC+ JMMC has been pushed back one hour to 13:00GMT/08:00EST, according to Energy Intel.

Spot gold is little changed around the USD 1925/oz mark, given the broader tentative pre-FOMC price action. Base metals are softer following the miss in China’s Caixin PMI release.

UK and EU reached a customs agreement which could pave the way for an end of post-Brexit wrangling over Northern Ireland, according to The Times.

Officials in Brussels have reportedly dismissed claims of a compromise deal on the ECJs role in the N. Ireland Protocol, via BBC’s Parker citing sources; Parker adds, “A precise timeline isn’t clear but one official says negotiators are in the “tunnel”.”.”Regardless any compromise of that kind would also represent a significant UK concession, as well as an EU one.” (re. the ECJ).

RTE’s Connelly, on reports of an EU/UK deal on the NI protocol, says there is “Nothing new. Talks ongoing. Progress (is) being made but no sign of anything imminent.”, citing a source.

NOTABLE DATA

EU HICP Flash YY (Jan) 8.5% vs. Exp. 9.0% (Prev. 9.2%); X Food & Energy Flash YY (Jan) 7.0% vs. Exp. 6.9% (Prev. 6.9%)

EU HICP-X Food, Energy, Alcohol & Tobacco Flash YY (Jan) 5.2% vs. Exp. 5.1% (Prev. 5.2%)

EU S&P Global Manufacturing Final PMI (Jan) 48.8 vs. Exp. 48.8 (Prev. 48.8)

German S&P Global/BME Manufacturing PMI (Jan) 47.3 vs. Exp. 47.0 (Prev. 47.0); French S&P Global Manufacturing PMI (Jan) 50.5 vs. Exp. 50.8 (Prev. 50.8)

UK S&P Global/CIPS Manufacturing PMI Final (Jan) 47.0 vs. Exp. 46.7 (Prev. 46.7)

UK BRC Shop Price Index YY (Jan) 8.0% (Prev. 7.3%)

NOTABLE US HEADLINES

US President Biden is to discuss the challenges posed by China and Russia during the State of the Union Address next week in the days after Secretary of State Blinken visits Beijing, according to SCMP citing a White House official.

US President Biden’s Administration is reportedly to propose today a rule that would limit late fees that credit card companies can charge, bringing the fee to USD 8 from as much as USD 41, according to WSJ citing the White House.

US is readying a USD 2.2bln weapons package for Ukraine which includes longer-range rockets for the first time, according to two officials cited by Reuters.

Russian Kremlin says that potential US supplies of long-range missiles to Ukraine would escalate tensions but would not stop Russia from achieving its goals; as bad as the present situation is, Russia believes the START treaty is very important; no current plans to hold talks between Russian President Putin and US President Biden, according to Sky News Arabia.

Belarusian servicemen have begun full independent operation of the Iskander missile system, according to the defence ministry.

CRYPTO

UK Treasury Crypto Proposals: incl. strengthening rules for crypto trading platforms and a robust world-fist regime for crypto lending.

APAC TRADE

APAC stocks traded higher after the positive lead from Wall St where stocks advanced into month-end and which was facilitated by the softer Employment Cost growth in the US, although gains were capped by the approaching FOMC rate decision and after disappointing Chinese Caixin Manufacturing PMI data.

ASX 200 was led higher by strength in the mining and materials sectors after a rebound in commodity prices and with an upgrade in the Final Australian Manufacturing PMI also conducive for risk appetite.

Nikkei 225 briefly climbed above 27,500 but closed off its highs amid a deluge of earnings releases and after Japan’s manufacturing activity was confirmed to have declined for a 3rd consecutive month.

Hang Seng and Shanghai Comp. were positive albeit with momentum restricted after Chinese Caixin Manufacturing PMI missed forecasts and printed a 6th consecutive month in contraction territory which was in contrast to the recent rebound seen in China’s official PMIs.

NOTABLE ASIA-PAC HEADLINES

US Defence Secretary Austin’s visit to Manila is expected to bring a deal on expanded US access to bases in the Philippines, according to a senior Philippines official cited by Reuters.

China’s President Xi says the need to coordinate expansion of domestic demand with deepening supply-side structural reforms, via State Media.

China securities regulator CSRC has released draft rules for IPO registration system reform for 1st February.

DATA RECAP

Chinese Caixin Manufacturing PMI Final (Jan) 49.2 vs. Exp. 49.5 (Prev. 49.0)

Australian Manufacturing PMI (Jan F) 50.0 (Prelim. 49.8)

New Zealand HLFS Job Growth QQ (Q4) 0.2% vs. Exp. 0.3% (Prev. 1.3%); Unemployment Rate (Q4) 3.4% vs. Exp. 3.3% (Prev. 3.3%)

New Zealand Labour Cost Index – QQ (Q4) 1.1% vs. Exp. 1.2% (Prev. 1.1%); YY (Q4) 4.3% vs. Exp. 4.3% (Prev. 3.8%)

1.c WEDNESDAY/ TUESDAY NIGHT

SHANGHAI CLOSED UP 29.25 PTS OR .90% //Hang Seng CLOSED UP 229.485 PTS OR 1.05% /The Nikkei closed UP 19.77 PTS OR 0.07% //Australia’s all ordinaries CLOSED UP .31% /Chinese yuan (ONSHORE) closed UP 6.7423 //OFFSHORE CHINESE YUAN UP TO 6.7478// /Oil UP TO 79.40 dollars per barrel for WTI and BRENT AT 85.60 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

2 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA

2B JAPAN

JAPAN/

3c CHINA /

CHINA/AFGHANISTAN

China plans to sell the lethal blowfish drones to the Taliban to protect their citizens in Kabul

(zerohedge)

China Plans To Sell Lethal Blowfish Drones To Taliban: Report

TUESDAY, JAN 31, 2023 – 08:40 PM

Following two major recent terrorist attacks which targeted Chinese nationals in Kabul, the Chinese government is desperately appealing to the Taliban to provide better security protection for its citizens in Afghanistan. The past week has seen multiple reports emerge saying that Beijing is even offering the Taliban advanced weaponry in order to bolster counter-terror efforts in the capital.