FEB 1 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSED: DOWN $10.95 at $1916,20

SILVER PRICE CLOSED: UP $0.04 to $23.58

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1912.35

Silver ACCESS CLOSE: 23.45

Bitcoin morning price:, 23,794 UP 392 Dollars

Bitcoin: afternoon price: $23,792 UP 390 dollars

Platinum price closing $1024.05 UP $24.20

Palladium price; closing 1655.05 UP $13.60

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,547.15 DOWN $45.12 CDN dollars per oz

BRITISH GOLD: 1563.73 DOWN 12.90 pounds per oz

EURO GOLD: 1752.52 DOWN 20.80 euros per oz

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,927.800000000 USD

INTENT DATE: 02/01/2023 DELIVERY DATE: 02/03/2023

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 98

104 C MIZUHO 31

118 C MACQUARIE FUT 412

132 C SG AMERICAS 89

435 H SCOTIA CAPITAL 241

624 H BOFA SECURITIES 1638

657 C MORGAN STANLEY 10 289

661 C JP MORGAN 4189 654

686 C STONEX FINANCIA 11

690 C ABN AMRO 37

709 C BARCLAYS 16

732 C RBC CAP MARKETS 5 14

737 C ADVANTAGE 1

800 C MAREX SPEC 23 55

880 C CITIGROUP 619

905 C ADM 12 34

TOTAL: 4,239 4,239

MONTH TO DATE: 11,813

JPMorgan stopped 654/4239

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR JAN/2023. CONTRACT: 4239 NOTICES FOR 423900 OZ or 13.185 TONNES

total notices so far: 11,813 contracts for 1,181,300 oz (36.743 tonnes)

SILVER NOTICES: 45 NOTICE(S) FILED FOR 225,000 OZ/

total number of notices filed so far this month : 86 for 420,000 oz

END

GLD

WITH GOLD DOWN $10.95

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 918/50TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 4 CENTS

AT THE SLV// :/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.1 MILLION OZ OF SILVER FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 517.90 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 724 CONTRACTS TO 138,987 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.20 LOSS SILVER PRICING AT THE COMEX ON WEDNESDAY. FOR THE TWO MONTHS, OUR BANKERS HAVE RETURNED TO BEING NET SHORT AND THUS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.20. BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD A GIGANTIC SIZED GAIN ON OUR TWO EXCHANGES OF 1558 CONTRACTS. AS WELL, WE HAD 0 NOTICES FOR EXCHANGE FOR RISK TRANSFER (0 OZ. ) AS THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 0.0 MILLION OZ. WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS( 600 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 0.540. MILLION OZ FOLLOWED BY TODAY’S SMALL QUEUE JUMP OF 0 OZ = .545 MILLION OZ + 0.0 MILLION OF EXCHANGE FOR RISK//TOTAL STANDING 0.545 MILLION OZ//// V) HUGE SIZED COMEX OI GAIN/ GOOD EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –234

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTRACTS for 2 days, total 996 contracts: OR 4.980 MILLION OZ PER DAY. (498 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 4.980 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 4.98 MILLION OZ/INITIAL

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 724 DESPITE OUR $0.20 LOSS IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 600 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 0.54 MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE + / /// 0 EXCHANGE FOR RISK://NEW STANDING RISES TO 0.545 MILLION OZ .. WE HAVE A GIGANTIC SIZED GAIN OF 1558 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 45 NOTICE(S) FILED TODAY FOR 225,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 6788 CONTRACTS TO 478,425 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: added + 495 CONTRACTS.

.

WE HAD A GOOD SIZED INCREASE IN COMEX OI ( 6783 CONTRACTS) DESPITE OUR $2.55 LOSS IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 41.601 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 39,300 OZ //NEW STANDING: 42.426 //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). TONNES

YET ALL OF..THIS HAPPENED WITH OUR $2.55 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 8747 OI CONTRACTS (27.20 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1964 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 478,425

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8747 CONTRACTS WITH 6783 CONTRACTS INCREASED AT THE COMEX AND 1964 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 8747 CONTRACTS OR 125.667 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1964 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (6783) TOTAL GAIN IN THE TWO EXCHANGES 8747 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 41.601 TONNES FOLLOWED BY TODAY’S 39,300 OZ QUEUE. JUMP// ///3) ZERO LONG LIQUIDATION //4) GOOD SIZED COMEX OPEN INTEREST LOSS// 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

3275 CONTRACTS OR 327,500 OZ OR 10.186 TONNES 2 TRADING DAY(S) AND THUS AVERAGING: 1638 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES:10.186 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 10.186/3550 x 100% TONNES 0.0287% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 10.186 TONNES/INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A VERY STRONG SIZED 724 CONTRACTS OI TO 138,987 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 600 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 600 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 600 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 724 CONTRACTS AND ADD TO THE 600 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED GAIN OF 1324 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 6.620 MILLION OZ//

OCCURRED DESPITE OUR 20 CENT LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED UP 0.75 PTS OR .02% //Hang Seng CLOSED DOWN 113.82 PTS OR 0.52% /The Nikkei closed UP 55.17 PTS OR 0.20% //Australia’s all ordinaries CLOSED UP .24% /Chinese yuan (ONSHORE) closed UP 6.7233 //OFFSHORE CHINESE YUAN UP TO 6.7279// /Oil DOWN TO 75.91 dollars per barrel for WTI and BRENT AT 82.15 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 6783 CONTRACTS UP TO 477,930 DESPITE OUR LOSS IN PRICE OF $2.55

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1964 EFP CONTRACTS WERE ISSUED: : APRIL 1964 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1964 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 8747 CONTRACTS IN THAT 1964 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI GAIN OF 6783 CONTRACTS..AND THIS VERY STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $2.55. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (42.426)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes(TOTAL THIS YEAR 656.076 TONNES

JAN/2023: 20.559 tonnes

FEB 2023: 42.426 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $2.55) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A VERY STRONG GAIN OF 8747 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 27.20 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (41.219 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 39,300 OZ OR 1.22 TONNES//new standing 42.426 tonnes … ALL OF THIS WAS ACCOMPLISHED WITH OUR FALL IN PRICE TO THE TUNE OF $2.55.

WE HAD +495 CONTRACTS COMEX TRADES ADDED TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 8747 CONTRACTS OR 874700 OZ OR 27.20 TONNES

Estimated gold comex today 240,633//fair//

final gold volumes/yesterday 221,572/// fair

INITIAL STANDINGS FOR FEB 2023 COMEX GOLD //FEB 2//

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 2909.311 oz Manfra . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 4239 notice(s) 423,900 OZ 13.185 TONNES |

| No of oz to be served (notices) | 1827 contracts 182,700 oz 5,683 TONNES |

| Total monthly oz gold served (contracts) so far this month | 11,813 notices 1,181,300 36.743 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 1

i) Out of Manfra 2909.311 oz

Total withdrawals: 2909.311 oz

total in tonnes: 0.0904 tonnes

Adjustments:1 customer to dealer /HSBC 76,039.974 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEBRUARY.

For the front month of FEBRUARY we have an oi of 6066 contracts having lost 1176 contracts. We had 1569 notices

filed yesterday so we gained393 contracts or an additional 39300 oz were queue jumped as these oz will stand for metal at the comex. We will now gain

in oz standing from this day forth until the conclusion of February.

March gained 30 contracts to stand at 1987.

April gained 7438 contracts up to 398,992

We had 4239 notice(s) filed today for 423,900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 4189 notices were issued from their client or customer account. The total of all issuance by all participants equate to 4239 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 654 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB. /2023. contract month,

we take the total number of notices filed so far for the month (11,813 x 100 oz ), to which we add the difference between the open interest for the front month of (FEBRUARY 6006 CONTRACTS) minus the number of notices served upon today 4239 x 100 oz per contract equals 1,364,000 OZ OR 42.426 TONNES the number of TONNES standing in this active month of January.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (11,813 x 100 oz+ (6066 OI for the front month minus the number of notices served upon today (4239)x 100 oz} which equals 1,364,000 oz standing OR 42.426 TONNES in this active delivery month of FEBRUARY..

TOTAL COMEX GOLD STANDING: 42.426 TONNES. SO JUST LIKE LAST MONTH WE START WITH A LOW INITIAL AMOUNT OF GOLD STANDING BUT THIS WILL GROW AS THE MONTH PROCEEDS TO ITS CONCLUSION.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

we had one adjustment of 110,631.591 oz Brinks

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,807,826.915 OZ 56.23 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,218,743.745 OZ

TOTAL REGISTERED GOLD: 11,096,423,558 OZ (345.14 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 11,122,320.187 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,288,597 OZ (REG GOLD- PLEDGED GOLD) 288.91 tonnes//

END

SILVER/COMEX

FEB 2/2023//INITIAL. SILVER CONTRACT FOR FEBRUARY

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,144,953.200 oz Brinks CNT JPMorgan Loomis |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 598,699.347 oz Manfra |

| No of oz served today (contracts) | 45 CONTRACT(S) (225,000 OZ) |

| No of oz to be served (notices) | 23 contracts (115,000 oz) |

| Total monthly oz silver served (contracts) | 86 contracts (430,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into Manfra: 598,699.347 oz

Total deposits: 598,699.3470 oz

JPMorgan has a total silver weight: 148.279 million oz/291.012 million =50.92% of comex .//dropping fast

Comex withdrawals: 4

i) Out of Brinks 233,123.04 oz

ii) Out of CNT: 303,996.760 oz

iii) Out of JPMorgan: 597,934.300 oz

iv) Out of Loomis 9899.100 oz

Total withdrawals; 1,144,953.200 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 32.215 MILLION OZ (declining rapidly).TOTAL REG + ELIG. 291.012 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JAN

silver open interest data:

FRONT MONTH OF FEB/2023 OI: 68 CONTRACTS HAVING LOST 4 CONTRACT(S.).

WE HAD 4 NOTICES FILED YESTERDAY, SO WE GAINED ZERO CONTRACTS OR AN ADDITIONAL NIL OZ OF SILVER WILL

STAND AT THE COMEX.

March LOST 731 CONTRACTS DOWN TO 105,270 contracts

TOTAL NUMBER OF NOTICES FILED FOR TODAY:45 for 225,000 oz

Comex volumes// est. volume today 64,787//fair

Comex volume: confirmed yesterday: 90,260 contracts ( very strong)

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 86 x 5,000 oz = 420,000 oz

to which we add the difference between the open interest for the front month of FEB(68) and the number of notices served upon today 45 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2023 contract month: 86 (notices served so far) x 5000 oz + OI for the front month of FEB (68 – number of notices served upon today (45) x 500 oz of silver standing for the FEB. contract month equates 0.545 million oz + 0 ( EXCHANGE FOR RISK) = 0.545MILLION OZ//(TOTAL OZ OF SILVER STANDING).

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:114,156// est. volume today// huge//crooks

Comex volume: confirmed yesterday: 71,338 contracts ( good)

END

GLD AND SLV INVENTORY LEVELS

FEB 2/WITH GOLD $10.95 TODAY: BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNEES OF GOLD INTO THE GLD////INVENTORY RESTS AT 918.50 TONNES

FEB 1/WITH GOLD DOWN $2.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 31/WITH GOLD UP $6.55 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 30/WITH GOLD DOWN $6.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 918.50 TONNES

JAN 27/WITH GOLD DOWN $0.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 919.37 TONNES

JAN 26/WITH GOLD DOWN $11.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 919.37 TONNES

JAN 25/WITH GOLD UP $7.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 917.34 TONNES

JAN 24/WITH GOLD UP $7.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 23/WITH GOLD UP $0.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.63 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 20/WITH GOLD UP $4.75 TODAY;BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 912.43 TONNES

JAN 19/WITH GOLD UP $16.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES INTO THE GLD///INVENTORY RESTS AT 910.98TONNES

JAN 18/WITH GOLD DOWN $1.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.9 TONNES FROM THE GLD////INVENTORY RESTS AT 909.24 TONNES

JAN 17/WITH GOLD DOWN $11.45 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.14 TONNES

JAN 13/WITH GOLD UP $22.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD///INVENTORY RESTS AT 912.14 TONNES

JAN 12/WITH GOLD UP $20.55 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 912.43 TONNES

JAN 11/WITH GOLD UP $1.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

DEC 30/WITH GOLD UP $.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 29//WITH GOLD UP $8.35 TODAY:; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 28/WITH GOLD DOWN $6.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE DEPOSIT OF 5.50 TONNES INTO THE GLD..//INVENTORY REST S AT 918.51 TONNES

DEC 27/WITH GOLD UP $18.15 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 913.01 TONNES

DEC 23/WITH GOLD UP $19,15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES/

DEC 22/WITH GOLD DOWN $29.35 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 21/WITH GOLD FLAT TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 913.88 TONNES

DEC 20/WITH GOLD UP $27.05: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES INTO THE GLD////INVENTORY RESTS AT 912.14 TONNES

DEC 19/WITH GOLD DOWN $2.10: HUGE CHANGES IN GOLD INVENTORY AT THE GLD> A BIG WITHDRAWAL OF 3.47 TONNES FROM THE GLD//INVENTORY RESTS AT 910.41 TONNES

DEC 16/WITH GOLD UP $12.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 15//WITH GOLD DOWN $31.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 911.56 TONNES

DEC 14/WITH GOLD DOWN $6.20: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 912.72 TONNES

DEC 13/WITH GOLD UP $32.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD///INVENTORY RESTS AT 910.41

DEC 12/WITH GOLD DOWN $17.60: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

DEC 9/WITH GOLD UP $8.90//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

Dec 8/WITH GOLD UP $4.05, OVER THE PAST 3 WEEKS WE LOST 2.04 TONNES//INVENTORY RESTS AT 908.09 TONNES

GLD INVENTORY: 918.50 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 2/WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.11 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 517.90 MILLION OZ

FEB 1/WITH SILVER DOWN 20 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.4 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 519.000 MILLION OZ

JAN 31/WITH SILVER UP 12 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.5 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 520.400 MILION OZ

JAN 30/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 521.900 MILLION OZ.

JAN 27/WITH SILVER DOWN 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 521.900 MILLION OZ//

JAN 26/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 900,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 521.900 MILLION OZ//

JAN 25/WITH SILVER UP 19 CENTS TO TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.3 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 521.000 MILLION OZ

JAN 24/WITH SILVER UP 21 CENTS TODAY: WHAT!! A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 20 MILLION OZ INTO THE SLV/( OCCURRED (LATE LAST NIGHT)//INVENTORY RESTS AT 518.70 MILLION OZ//

JAN 23/WITH SILVER DOWN 40 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.4 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 498.7 MILLION OZ//

JAN 20.WITH SILVER UP 9 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 750,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 497.300 MILLION OZ

JAN 19/WITH SILVER UP 24 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 498.05 MILLION OZ

JAN 18/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 8.15 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 498.05 MILLION OZ///

JAN 17/WITH SILVER DOWN 35 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 13/WITH SILVER UP 46 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.5 MILLION OZ FROM THE SLV..//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 12/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 508.700 MILLION OZ/

JAN 11/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 508.700MILLION OZ

JAN 10/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ

JAN 9/WITH SILVER DOWN 9 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 6/WITH SILVER UP 54 CENTS TODAY;BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.20 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 5/WITH SILVER DOWN 50 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.10 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 505.45 MILLION OZ//

JAN 4/WITH SILVER DOWN 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 506.55 MILLION OZ/

JAN 3/WITH SILVER UP 24 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: STRANGE: A WITHDRAWAL OF 1.2 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 507.85 MILLION OZ/

DEC 30/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 29/ WITH SILVER UP $0.63 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 28//WITH SILVER DOWN 46 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.715 MILLION OZ INTO THE SLV///..INVENTORY RESTS AT 509.050 MILLION OZ

DEC 27/WITH SILVER UP 34 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 507.350 MILLION OZ//

DEC 23/WITH SILVER UP 29 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT507.900 MILLION O//

DEC 22/WITH SILVER DOWN 53 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 21/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.0 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 20/WITH SILVER UP 105 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:: A DEPOSIT OF 700,000 OZ INTO THE SLV///INVENTORY RESTS AT 509.90 MILLION OZ//

DEC 19/WITH SILVER DOWN 13 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.05 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.20 MILLION OZ//

DEC 16/WITH SILVER UP 2 CENTS; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.85 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 508.15 MILLION OZ//

DEC 15/WITH SILVER DOWN 78 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF EXACTLY 2.00 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 510.000 MILLION OZ

DEC 14/WITH SILVER UP 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 512.000 MILLION OZ//

DEC 13/WITH SILVER UP 59 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 600,000 OZ FROM THE SLV////INVENTORY RESTS AT 513.900 MILLION OZ//

DEC 12/WITH SILVER DOWN 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 514.500 MILLION OZ//

DEC 9/WITH SILVER RISING 77 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.2 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 514.500 MILLION OZ.

DEC 8/WITH SILVER RISING 34 CENTS TODAY: OVER THE PAST 3 WEEKS, WE HAVE GAINED A STRONG: 44.777 MILLION OZ/INVENTORY RESTS AT 516.700 MILION OZ.

CLOSING INVENTORY 517.90 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Schiff: Is The Fed Easing Up On The Inflation Fight?

THURSDAY, FEB 02, 2023 – 09:45 AM

Is the Federal Reserve easing off the accelerator on its inflation fight?

The answer depends on whether you believe your eyes or your ears.

Our eyes tell us the Fed is slowing down on rate hikes.

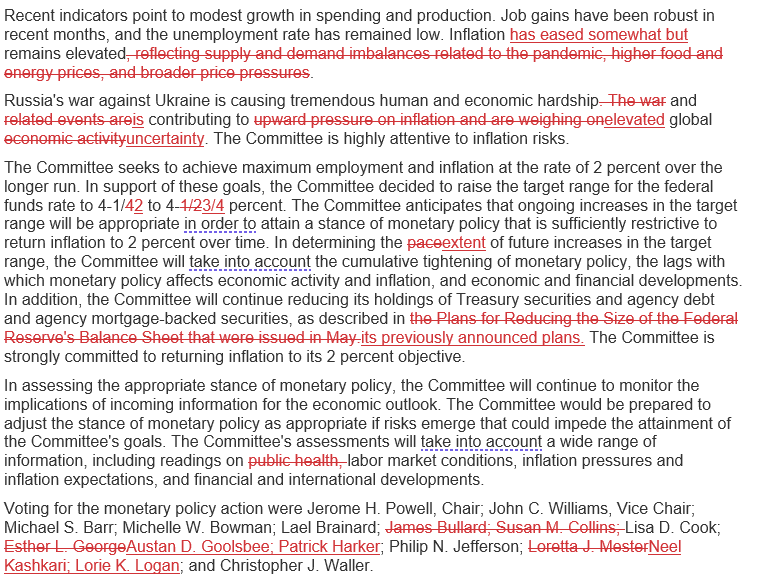

After easing back from a 75 basis point hike in November to a 50 basis point hike in December, the Federal Open Market Committee (FOMC) delivered an even smaller 25 basis point hike at its February meeting. With the most recent rate increase, the target range for the federal funds rate is between 4.5 and 4.75%.

A quarter-percent rate hike was widely anticipated. The mainstream narrative is that inflation has peaked and the central bank is now easing its foot off the accelerator.

But if our eyes tell us the Fed is winding down the inflation fight, the messaging coming from the central bank says the opposite. The FOMC statement said, “Inflation has eased somewhat but remains elevated,” and it signaled additional rate hikes in the future.

The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.”

As it did in the last two meetings, the FOMC left wiggle room to pivot, saying the committee will continue to take into account “cumulative tightening” and “the lags with which monetary policy affects economic activity and inflation” as it makes future decisions.

During his press conference, Powell repeatedly said “the job is not done,” and emphasized that “It would be very premature to declare victory, or to think that we’ve really got this.” He indicated that the central bank could raise rates a couple more times.

We’ve raised rates four and a half percentage points, and we’re talking about a couple of more rate hikes to get to that level we think is appropriately restrictive. Why do we think that’s probably necessary? We think because inflation is still running very hot.”

Answering another question, Powell said, “It’s our judgment that we’re not yet at a sufficiently restrictive policy stance, which is why we say that we expect ongoing hikes.”

On the other hand, Powell also gave himself some wiggle room, saying that he does see inflation easing.

We can now say I think for the first time that the disinflationary process has started. We can see that and we see it really in goods prices so far.”

Powell continues to insist there is a path for the central bank to bring price inflation down to 2% without causing a significant economic slowdown. He brought up the “strong” labor market several times during his press conference.

Reaction

The markets appear to believe what they’re seeing, not what they’re hearing.

Despite what Powell actually said, the mainstream seemed to read between the lines and initially took the outcome of the FOMC meeting as confirmation that the tightening cycle is nearly over.

Stocks see-sawed after the announcement. The Dow initially sold off before swinging some 170 points to the upside after Powell’s press conference ended. The Dow slid into the close, finishing up 8 points. But the NASDAQ with its more speculative stocks closed up 2% on the day, and the S&P 500 finished up just over 1%.

Gold surged by over $20 and pushed over $1,950 an ounce. The dollar fell, along with bond yields.

All of this indicates that the initial market take was that the Fed is nearly finished raising rates.

Allianz Investment Management senior investment strategist Charlie Ripley told CNBC that the messaging leaned “slightly dovish,” adding that a lack of clarity on future interest rate moves signals the Fed is nearing the end of its rate tightening cycle

The Fed is essentially speaking out of both sides of the mouth as they signaled further increases are appropriate, but also acknowledged they will consider the cumulative amount of tightening in future policy decisions.”

In an interview on Fox Business, Peter Schiff said he heard a lot of economic ignorance coming out of Powell’s mouth. He said the “disinflation” that Powell mentions is “transitory.”

Schiff zeroed in on a comment Powell made claiming consumer expectations cause inflation.

“Inflation is caused by the government,” he said. “It’s caused by the Federal Reserve printing money and Congress spending it.”

Schiff said even if the Fed delivers a couple more 25 basis point hikes, it’s still not enough to slay inflation. He noted that even with the rate hikes, Americans continue to borrow money in order to keep up spending and saving has fallen into the basement.

Peter said he believes we are heading toward a major economic downturn, but even that won’t slay the inflation dragon.

Looking Ahead

No matter what’s going on in the Fed members’ heads, right now, I think the inflation fight will end the moment something breaks in the economy.

And I’m convinced something will break in the economy.

Powell insists there is a path forward that brings inflation down while avoiding a recession. I think that’s wishful thinking or bureaucratic spin. I think it’s a virtual certainty that the economy will spiral into a downturn. And I don’t think it will be short and shallow. I think it will be deep and prolonged.

My pessimism is rooted in the fact that the US economy is addicted to easy money. It is addicted to artificially low interest rates and quantitative easing. You can’t take an addict’s drug away without sending him into withdrawal. The economy can only limp along so long with tighter monetary policy.

Interest rates haven’t been this high since 2007. At that point, the Fed was cutting rates due to the housing bust. The economy couldn’t handle interest rates that high.

Powell and Company have backed themselves into a corner. They just don’t know it yet (or more likely, they haven’t admitted it).

end

Is Gold The Last Freedom Train?

BY TYLER DURDEN

THURSDAY, FEB 02, 2023 – 04:37 PM

Most people believe the Federal Reserve stabilizes the economy and our money. In reality, the central bank incentivized debt and destroys wealth.

Is there a way to sidestep the destructive forces of central banking and fiat money?

T.W. Thiltgen believes there is a freedom train we can escape on – gold.

The following guest post was written by T.W. Thiltgen. The opinions expressed are his and don’t necessarily reflect those of Peter Schiff or SchiffGold.

I pose this question to you so that you can begin to consider that there is currently a macroeconomic problem that is more important than all other problems this country faces.

That macro condition is the relentless destruction of capital throughout the world and the US in particular.

Merriam-Webster Dictionary defines capital as “accumulated possessions to bring in income.”

For our purposes here, I will just call it SAVINGS.

In economics, one of the important identities is S=I or Savings = Investment.

You cannot invest if you have not saved, and you will be able to invest less if your savings fall. This may seem obvious but bear with me.

Your savings can be destroyed by other than your own bad investment decisions. Negative real interest rates (interest rates adjusted for inflation) are the central driver in the destruction of capital for at least the last 14 years from the start of the 2008-2009 collapse.

By keeping interest rates below the rate of inflation, the Federal Reserve has destroyed saving on an unimaginable scale. Even today, US Treasury interest rates are still 3% points below the rate of inflation. And that’s using the government’s numbers. The real inflation rate using the methodology of the 1980s would put today’s inflation rate near 15%. Either of these numbers is disastrous, but taking the average of the number between 7% and 15% or 11 ½ % means that the value (purchasing power) of your savings is being destroyed in a very short number of years. Even if inflation falls back to 3 – 4%, your real inflation-adjusted saving will decline at a rate that will ultimately lower your standard of living.

Forgetting savings for a moment, the reason is because real wages never keep up with inflation. This is why that real disposable income is less today than in the early 1970s. We are now living on capital generated by past generations. We are destroying the seed corn left to us by those previous generations. Unless going forward you as an individual can maintain your inflation-adjusted purchasing power, you are destined to suffer a serious decline in your standard of living, as is the rest of the country.

It will be very difficult to maintain purchasing power because you have to pay taxes on any interest income received even when the purchasing power of the principal and interest you receive back has lower purchasing power than when you bought the CD or Treasury Securities. You are actually paying taxes on phantom profits that you got in return. Are you starting to ask if the title of this article is possibly true?

As negative real interest rates continue, bank deposits and currency are becoming less valuable as a claim on goods and services. There are currently $18 trillion in bank deposits and $2 trillion in fiscal notes (cash). If negative rates continue, it is only a matter of time before holders of these deposits and currency begin to convert them to something else (anything else), rental property, land, gold, art, etc. Nobody will let those $20 trillion lose purchasing power at the rate that is occurring now.

As deposits are withdrawn, the foundation of bank lending will be reduced, causing loans to be called in. This will accelerate the collapse of the economy. If the Federal Reserve tries to stop this loss of deposits by continuing to raise interest rates and thereby giving depositors a real rate of return, then the high interest rates coupled with the massive debt load will make many debt obligations unpayable and a financial disaster much worse than 2008-2009 will occur. And if they give in and print more money when the economy turns down, inflation will explode again.

As you can see from the choices above, the possibilities of a soft landing in the economy, from this situation are VERY LOW.

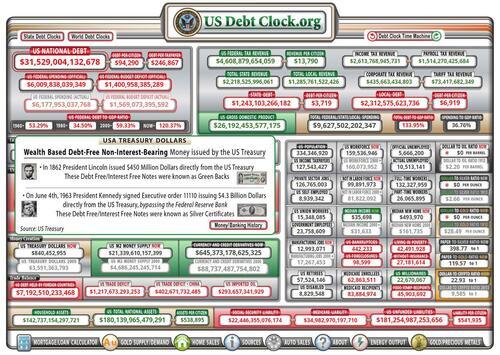

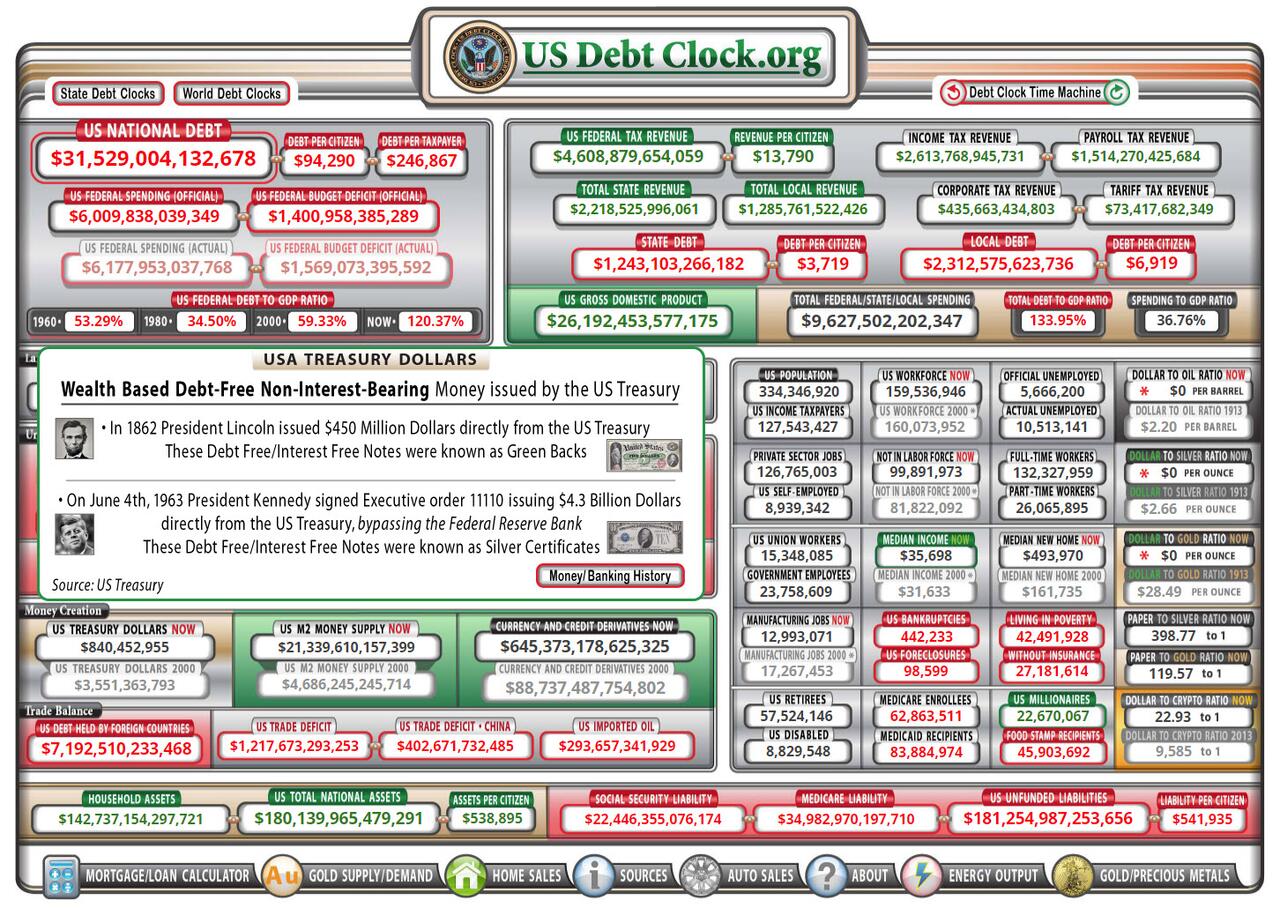

I would call your attention to a website called usdebtclock.org. I recommend that you go to the site and just stare at the debt clock as it clicks away the solvency of our government, as well as the solvency of corporations, municipalities, and individuals — in REAL TIME.

The entire fabric of our society is being ripped apart because of the rapid increase in debt of all types. In particular, the unfunded liabilities of the US government now total $181 TRILLION (bottom right). Now, look at the upper left at the US national debt of $31 TRILLION. If we were able to keep deficit spending to the same level as growth in GDP, the debt of $31 trillion would be manageable.

The problem for everyone is the unfunded liabilities.

The annual deficit is nearly $1.5 trillion each year now, but unfunded liabilities are rising by over $5 trillion each year. These unfunded liabilities consist of Medicare, Medicaid, prescription drug benefits, military and civilian retirement, and other programs. These unfunded liabilities used to show up in the annual deficit, but the law was changed to accrue them in a separate category so people would not see them.

Why? you may ask.

The justification was that they were not REAL LIABILITIES because they never actually have to be paid. Only interest on the national debt has to be paid. Because the total amount of the US debt plus US unfunded liabilities is so great that what can’t be paid, won’t be paid and the people writing the law KNEW IT.

After you have spent a few hours over a week’s time looking at each item in the debt clock and looking at the speed of increase, you decide what the end result will be. Then start to envision the value of our US fiat money, whether it be a currency, bank deposits or government bills, notes, or bonds.

If interest rates in the US continue to stay higher than those of other countries, as is the case now, the US dollar will continue to strengthen over time relative to other fiat currencies. (But all fiat currencies are falling versus gold.) What a wonderful opportunity this presents to holders of fiat US dollars. It allows them to convert them to “real money” — gold and also silver. This is an opportunity that citizens of other countries do not have as gold has already risen in terms of their currencies, as their values relative to the US dollar have fallen.

Gold is now one of the best-performing assets, as bonds, as well as stocks, are down substantially in 2022. When this conversion occurs, not if, not only will gold outperform other asset classes but the derivatives of gold such as gold mining shares will also.

Most investors and traders are moving in and out of stocks and bonds in order to garner a profit. Over time, most never realize a real return over inflation, brokerage fees, management fees, and taxes. Those who do not believe me simply have not looked at the data. Most investors look at nominal dollars and don’t factor in inflation and the opportunity costs of not considering other investments such as a business, farmland, or a host of others.

In my opinion, the goal of anyone who has “savings” is to have those savings retain purchasing power over time. You have earned it and paid income tax on it. Now you need to make sure those savings retain purchasing power.

I believe that everyone who has savings should convert some of those savings to real money — gold.

As J.P. Morgan said, “Gold is money, everything else is credit.”

What he was saying is that gold is money that is no one else’s liability. Gold is money par excellence. Gold is the best money because it has the highest stocks to flow of any commodity. Gold is not an investment, it is MONEY.

Once you have an allocation to REAL MONEY, you can now invest (i.e. speculate) in other areas, comfortable that in an inflationary or deflationary crash, you will survive financially. Gold is the only money that has retained its purchasing power over the last 5,000 years.

By converting part of your savings to gold at least you will have some portion of your savings that will not lose purchasing power. In addition, you will be able to survive a complete collapse in the monetary system.

If you have studied the debt clock at length and have come to the conclusion that, “everything is going to work out OK,” then you probably have the “Normalcy Bias”.

Normalcy bias is what keeps people from leaving their homes when a hurricane is coming or a fire is close to their property. What they are thinking is it has never hit here or burned near here, therefore it will be OK this time.

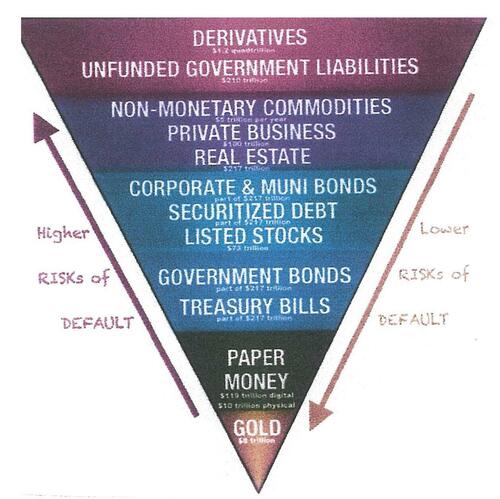

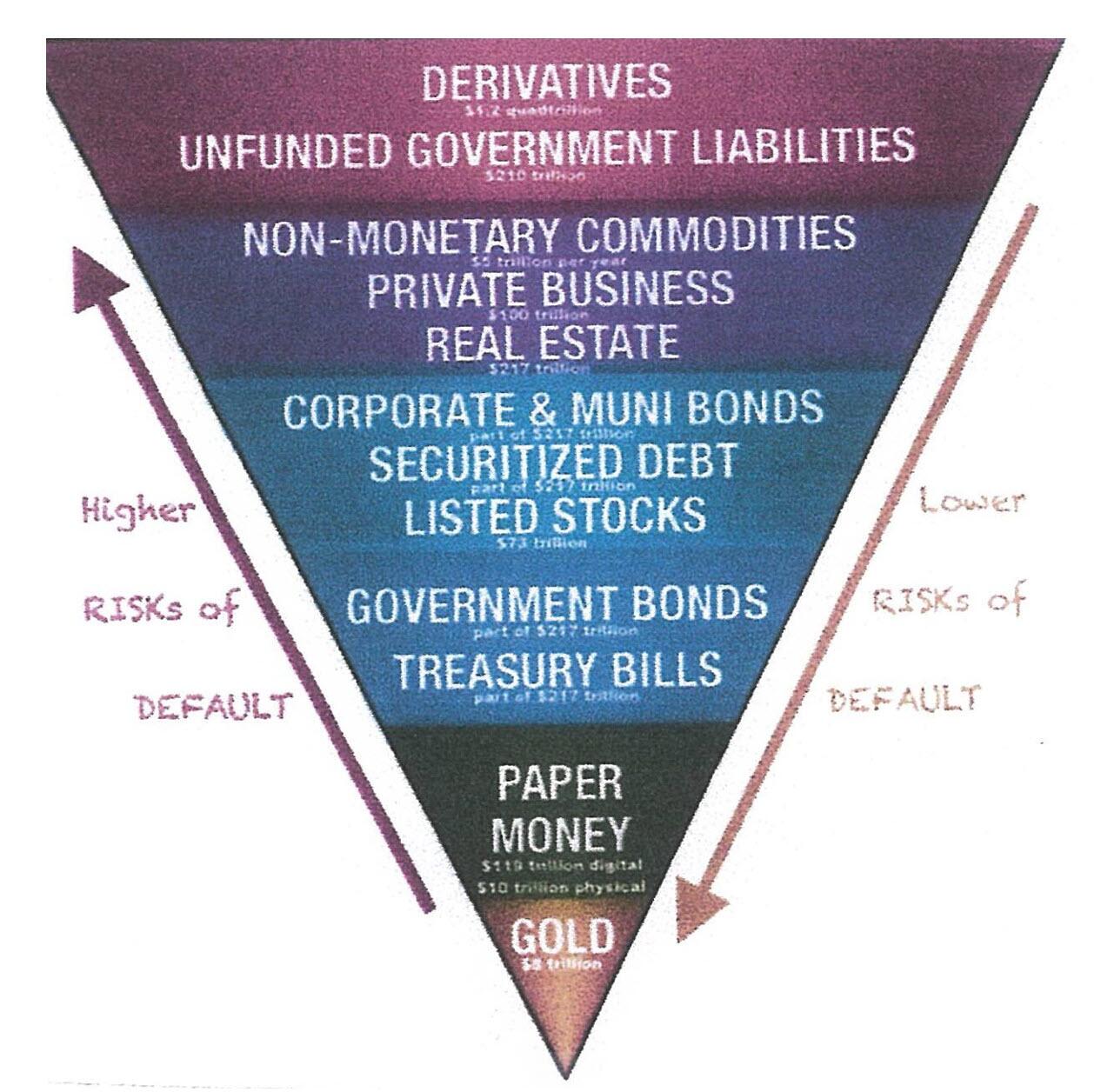

I will leave you with what Alan Greenspan the past Chairman of the Federal Reserve, said about deficit spending and gold. After reading you can see John Exter’s pyramid that shows what dies first as everything eventually flows to Real Money — gold.

In the absence of the gold standard, there is no way to protect savings from confiscation through inflation. There is no safe store of value. If there were, the government would have to make its holding illegal, as was done in the case of gold. If everyone decided, for example, to convert all his bank deposits to silver or copper or any other goods and thereafter declined to accept checks as payments for goods bank deposits would lose their purchasing power and government-created bank credit would be worthless as a claim on goods. The financial policy of the welfare state requires that there be no way for the owners of wealth to protect themselves. This is the shabby secret of the welfare statists’ tirades against gold. Deficit spending is simply a scheme for the confiscation of wealth. Gold stands in the way of this insidious process. It stands as a protector of property rights. If one grasps this, one has no difficulty in understanding the statists’ antagonism toward the gold standard.”

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

3. Chris Powell of GATA provides to us very important physical commentaries//

USAGold’s February ‘News & Views’ notes gold’s return as a reserve currency

Submitted by admin on Wed, 2023-02-01 09:56Section: Daily Dispatches

10a ET Wednesday, February 1, 2023

Dear Friend of GATA and Gold:

USAGold’s “News & Views” letter for February is published today and among its many short and sweet observations, maybe the most important one is that gold is returning as an international reserve currency, making it a compelling option for ordinary investors.

The February edition of “News & Views” is posted at USAGold here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

As Turkey witnesses a huge inflation in their country, its citizens are buying gold hand over fist

(Bloomberg News)

Amid soaring inflation, Turkey’s government and people hurl themselves into gold

Submitted by admin on Wed, 2023-02-01 10:05Section: Daily Dispatches

Gold as Inflationary Hedge Makes Turkey World’s Biggest Buyer

ByKerim Karakaya and Beril Akman

Bloomberg News

Tuesday, January 31, 2023

Turkey was the biggest buyer of gold among central banks last year, with households also rushing to buy the commodity to shield from geopolitical uncertainty and rampant inflation.

The central bank’s gold reserves were at the highest level on record, the World Gold Council said in a report today. The official figure was 542 tonnes, up by 148 tonnes

Demand for jewelery in the country also increased and jumped 32% year-on-year in the last quarter of 2022. “Despite the rise in the local gold price during 4Q, soaring consumer inflation brought the investment motive to the fore,” the gold council said.

Turkey has stepped up its ambitions to produce more gold than the existing average of 35 tonnes annually over the last five years, President Recep Tayyip Erdogan said last week. “Together with oil, gold is one of the most imported items,” he said during the opening of a new gold mine facility in the country’s west.

“We have the reserves to meet at least half of the demand in this area.” …

… For the remainder of the report:

END

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

State Department Engages with Gold Industry to Discuss Sanctions

FEBRUARY 1, 2023

Yesterday, Ambassador James O’Brien, Head of the Office of Sanctions Coordination, led an interagency discussion with leading companies and associations across the gold sector. The meeting focused on the importance of the gold industry’s robust implementation of Russia-focused sanctions and of applying broader due diligence standards, including to Russia-backed actors, such as the Wagner Group, around the globe. The United States remains committed to imposing economic consequences on Russia for its unprovoked war in Ukraine and destabilizing activities across Africa. The meeting also focused on the role gold plays in supporting other regimes of concern, including in Latin America and Africa, and illicit networks, as well as how the industry can mitigate the role of malign actors while also supporting economic development programs, with a focus on labor and human rights.

-END-

end

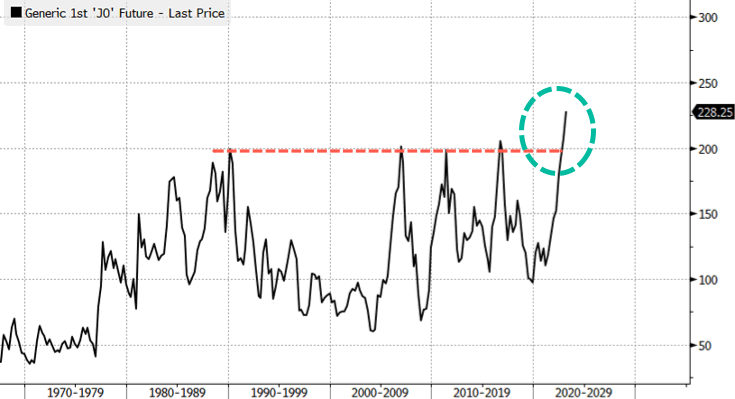

5.IMPORTANT COMMENTARIES ON COMMODITIES: orange juice

ORANGE JUICE

Orange juice prices rise amid a supply squeeze

(zerohedge)

Orange Juice Futures Hit New Record High Amid Supply Squeeze

WEDNESDAY, FEB 01, 2023 – 06:25 PM

OJ futures have hit a new high, surging 10 cents or 4.56% to $2.292/lb, surpassing the 2016 record of $2.2585, due to limited supply.

The USDA predicts Florida’s citrus production will reach 44.5 million boxes this year, which could result in the state’s smallest orange harvest since 1945. This is due to “greening disease” and hurricane damage in Florida’s citrus groves.

Recall we have closely followed the squeeze in supplies:

- Orange Juice Prices Could “Increase Substantially” As Hurricane Pummels Florida’s Top Citrus Grow Region

- Orange Juice Futures Limit Up On Global Supply Squeeze

The domestic shortage has led domestic companies to seek out new supplies in Mexico and Brazil. WSJ reported a gallon of orange juice has risen above $6 in some US supermarkets.

Besides orange juice, egg prices are also soaring. People aren’t thrilled about rapid food inflation.

I almost put the Orange Juice back at Walmart today. These prices are out of hand. #DoBestByEveryBody #Inflation— Darryl R Ware II (@DarrylRWareII) January 31, 2023

It’s 5.00 for orange juice, 3.50 for eggs. Let’s focus on the important issues, not the fantasy that America will be “all electric” anywhere in our lifetimes. But good job on other stuff you’re doing. Keep up the support for Ukraine and reducing gas prices.— Corey (@elbrynncanticle) January 30, 2023

Maybe is a Republican strategy to put you down let’s say there is around 10 people dead at day because weapons rights

prices of food eggs $10:00

Bread $6:00

Coffee cream $9:00

Milk $$7:00

Frozen orange juice $ $8:00

Please we don’t want to mention the prince of chicken,fish,Beef— ALICIA M Blay Casal Franco Rivero (@ALICIAMBlayCas1) January 29, 2023

end

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

END

.

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.7235

OFFSHORE YUAN: 6.7279

SHANGHAI CLOSED UP 0.75 PTS OR .02%

HANG SENG CLOSED DOWN 113.82 PTS OR 0.52%

2. Nikkei closed UP 55.17 PTS OR 0.20%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 101.00Euro FALLS TO 1.0988 DOWN 25 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.492!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 128.43/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

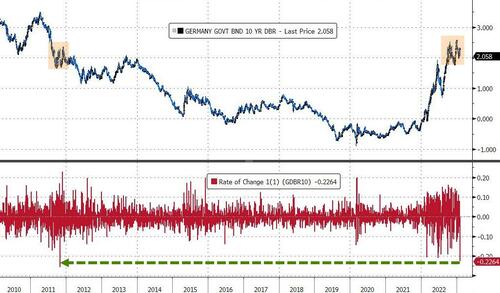

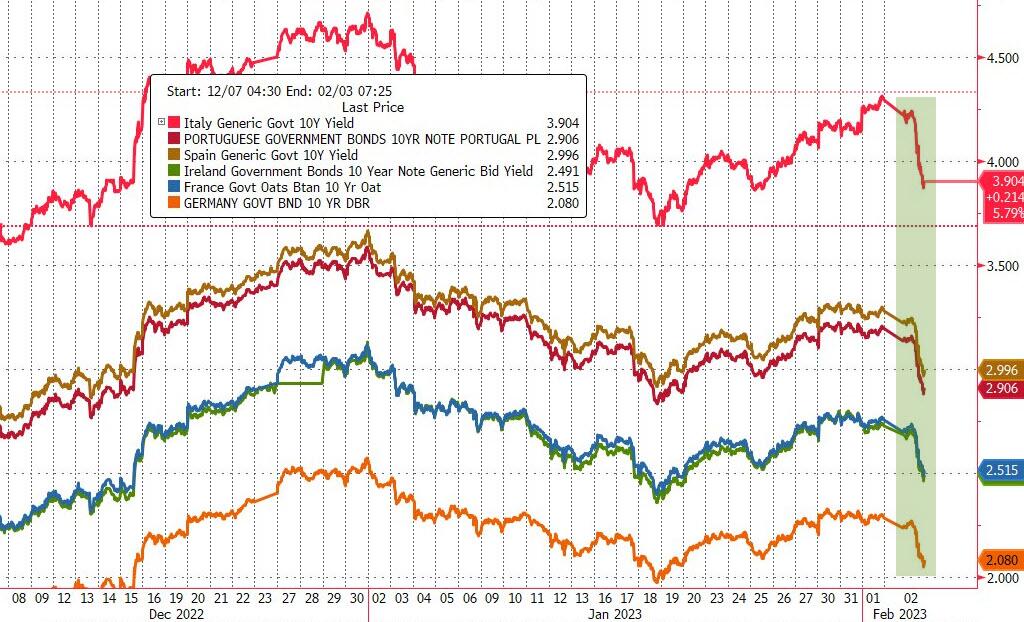

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.208%***/Italian 10 Yr bond yield FALLS to 4.111%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.217…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.204//

3j Gold at $1954.60//silver at: 24.41 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 16/100 roubles/dollar; ROUBLE AT 70.04//

3m oil into the 75 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 128.43/10 YEAR YIELD AFTER BREAKING .54% FALLS TO .492% ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9095– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9992 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.382% DOWN 2 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.549 DOWN 0 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,82…

GREAT BRITAIN/10 YEAR YIELD: 3.31415% DOWN 16 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

“The More He Talked, The More Dovish He Was”: Futures, Global Stocks Surge As Powell Steamrolls Bears

THURSDAY, FEB 02, 2023 – 08:15 AM

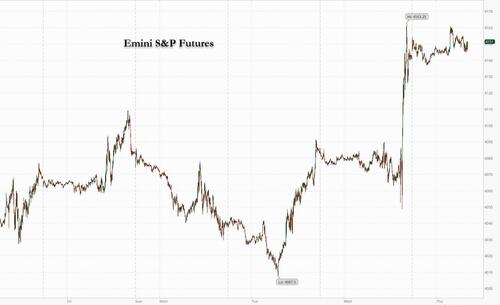

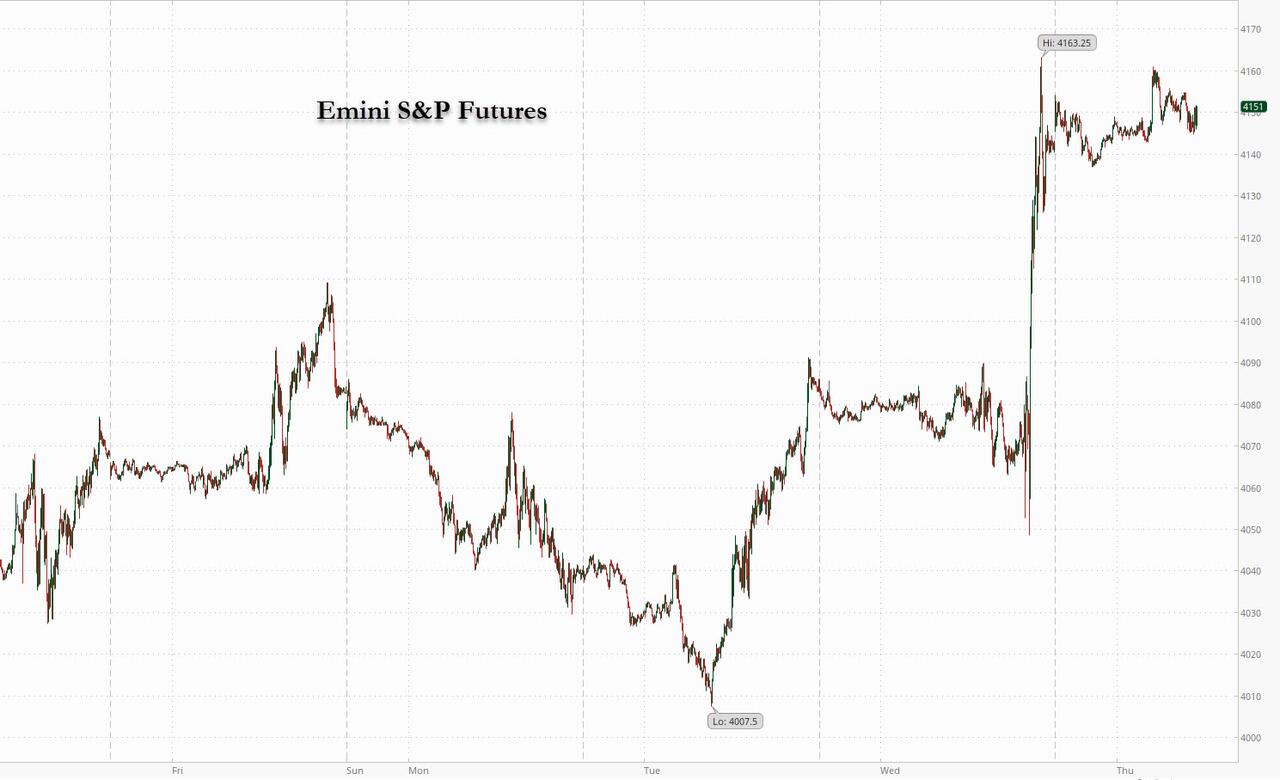

Global markets rose, with US futures solidly in the green as tech stocks were set to extend their rally on Thursday, lifted by Powell’s comments on inflation and Meta surging 20% in US premarket trading after the social-media giant’s earnings and buyback news. Summarizing yesterday’s market moving FOMC decision and presser, Goldman said that even though the “FOMC Statement was Hawkish: kept ‘ongoing’ and ‘appropriate’, however “more importantly presser was dovish: 1) Powell’s disinflation language (“we can say the disinflation process has started”, something that’s “welcome, encouraging, and gratifying”) and 2) the fact Powell didn’t warn markets RE easing financial conditions in the last few weeks.” In kneejerk reaction bears everywhere were steamrolled as Powell triggered a marketwide short squeeze.

Nasdaq futures were up 1.3% at 7:45 a.m. ET after the tech-heavy index jumped 2% during the previous session and closed at its highest level since September; the Nasdaq 100 is up 13% this year, having posted the best monthly gain since July in January. The recovery follows last year’s 33% slump, which was the worst since the 2008 global financial crisis. S&P futures added another 0.4% to yesterday’s surge, which pushed spoos to 4152, the highest since August as the consensus bearish trade (JPM, MS, GS, BofA are all bearish) gets steamrolled.

In premarket trading, it was all about Meta, whose gain of about 20% – the biggest one-day surge in the stock since 2013 – represents about 75 points in Nasdaq 100 futures’ advance, or about three quarters of the rise as the social media giant posted quarterly sales that topped estimates and boosted its stock-buyback authorization. If the gains hold, Meta will more than double its market value since a Nov. 3 low. The owner of Facebook is the best performer in the S&P 500 Index since the stock’s recent November 3 closing low of $88.91, and is poised to more than double in value since then. Shares of social-media companies such as Snap Inc. and other tech companies such as Alphabet Inc. gained in US premarket today. The Google parent, Apple and Amazon.com Inc. are among tech giants reporting results today. Here are some other premarket movers:

- Bank stocks are higher in premarket trading Thursday amid a broader rally by risk assets following the Federal Reserve’s interest-rate decision. In corporate news, Citigroup’s wealth arm has stopped accepting securities of Gautam Adani’s group of firms as collateral for margin loans. Meanwhile, Bank of America’s global mining head Omar Davis, one of the most senior bankers covering the sector, is retiring

- Carvana jumped as much as ~31%, putting the used car dealer on course for its sixth session of straight gains amid the rally in riskier assets.

- Shares in companies exposed to cryptocurrencies gained as Bitcoin held at its highest level since last August.

The euphoric mood was set by Powell’s comment Wednesday that the “disinflation process has started” suggesting that the aggressive tightening cycle is starting to reduce the pace of price growth, even as he warned of a “couple” more hikes to come. Positioning in US swaps markets assumes the Fed is getting closer to cutting rates as traders bet that economic conditions are likely to keep it from the additional rate increases that policy makers still anticipate.

“The more he talked, the more dovish he was,” Charles-Henry Monchau, chief investment officer at Banque Syz, said of Powell’s briefing. “It’s possible we’ll continue to see a series of volatility, but definitely the conditions seems to be more risk-on than last year,” he said on Bloomberg Television.

That said, some bears were stuck in denial: “Markets heard what they wanted to hear from the Fed,” said Veronique Riches-Flores, economist and founder of RichesFlores Research. “Markets will likely surf on this wave in the short term and it’s a good environment for risk assets.”

“Moving forward though there will likely be a lot of volatility around key indicators, such as the jobs data on Friday,” she said. “At one stage, if the data shows the economy is really resilient, investors will need to anticipate that Powell will need to take back control and that can lead to even more volatility.”

European stock also rose, tracking Wednesday’s gains on Wall Street after the Fed downshifted to a 25bps rate increase and noted inflation had eased somewhat. The Stoxx 600 was up 0.8% with tech, real estate and retail the best performing sectors. Here are some of the biggest European movers:

- Shell shares rise as much as 2.2% in London after the oil major launched a $4 billion share buyback, and posted full-year results that showed a record performance in 2022

- Banco Santander shares jump as much as 4.3% after the Spanish lender beat estimates, and offered positive guidance that analysts said could lead to further consensus upgrades

- Telecom Italia shares jump as much as 14%, the most intraday since November 2021, after KKR made a non-binding offer for a stake in the phone company’s multi-billion-euro network

- Dassault Systemes shares gain as much as 5.4%, the biggest intraday climb since November, after the software company’s FY constant-currency sales growth forecast topped estimates

- Siemens Healthineers gains as much as 6.8% as analysts flag solid order book momentum at the medtech group, offsetting a miss to first-quarter Ebit

- Telenor shares gain as much as 6.8%, the biggest intraday climb since March 2020, after the telecom operator’s guidance for Ebitda growth in Nordic markets beat analyst expectations

- Infineon shares jump as much as 8.8%, the most since March, after the chipmaker lifted its full-year margin forecast and kept its revenue outlook while factoring in a weaker dollar

- ING shares drop as much as 8.2% in early trading as analysts said the lack of a new buyback announcement and some areas of weakness in the Dutch lender’s results offset a profit beat

- Electrolux shares drop as much as 11% with analysts saying the appliances manufacturer’s update was much worse than anticipated

- Roche falls as much as 1.4% after a cautious outlook weighed on an overall weak quarterly report from the Swiss pharmaceutical giant

- Deutsche Bank shares drop 5.3%, most in four months, after the German lender’s earnings missed estimates. JPMorgan analysts say lack of buyback guidance also weighed

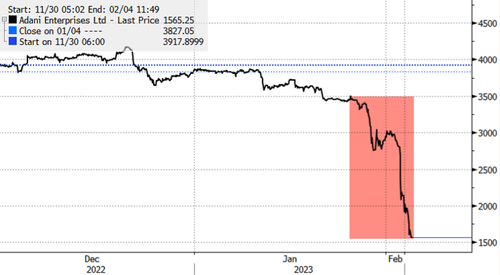

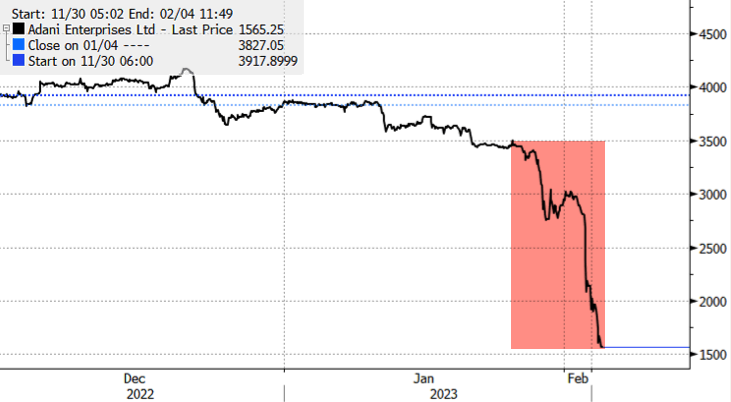

Asian stocks advanced as the Federal Reserve chair said efforts to quell inflation are making progress, supporting risk sentiment. The MSCI Asia Pacific Index climbed as much as 1% before paring more than half of the advance. Interest-rate sensitive tech stocks led gains, with TSMC, Samsung and Baidu giving among the biggest boost to the gauge. Tech-heavy benchmarks including Taiwan and South Korea led a rally in the region, while measures in Japan were mixed as the yen strengthened against the dollar. Key gauges in Hong Kong and Singapore fell, while Adani Group shares dragged on Indian benchmarks.

Investors cheered remarks by Jerome Powell that price pressures have started to ease, even as the Fed chair also said more interest-rate hikes are in store after delivering a quarter percentage-point rate increase. The dollar extended its fall following the Fed’s decision, helping boost foreign inflows to Asian equities. “Markets are really charting out their own path right now, looking at what inflation has been doing,” Charu Chanana, a senior markets strategist at SAXO Capital Markets, said in an interview with Bloomberg TV, adding that she would be more careful about risks ahead. “Even though Chair Powell highlighted dis-inflationary pressures that are there, we are potentially looking at inflation really being a monster,” she said. The key Asian stock index briefly touched its highest level since April after climbing some 27% from its October trough amid euphoria over China’s reopening and growing bullish calls on Asia. The gauge has outperformed the S&P 500 Index by about two percentage points so far this year.

Japanese equities ended mixed, bucking a broader rally in global stocks, as the Federal Reserve’s slower pace of rate hike strengthened the yen. The Topix Index fell 0.4% to 1,965.17 as of market close, while the Nikkei advanced 0.2% to 27,402.05. Toyota Motor Corp. contributed the most to the Topix Index decline, decreasing 1.2%. Out of 2,164 stocks in the index, 608 rose and 1,462 fell, while 94 were unchanged. “Powell’s acknowledgment of a slowdown in inflation while mentioning that the labor market is strong were well received,” said Takashi Ito, a senior strategist at Nomura Securities. Still, Japanese stocks are unlikely to rise as much as US peers as the yen strengthened.

Stocks in India were mostly higher on Thursday as investors looked beyond the rout in Adani Group shares, while companies continued to report strong earnings performance. All but one of the 10 companies related to the Adani Group declined as a week-long selloff in the diversified conglomerate’s shares stretched to $108 billion. On Wednesday, the group’s flagship firm Adani Enterprises, abruptly scrapped its fully-subscribed $2.4 billion follow-on stock sale plan amid carnage in its shares. It was the worst performer on Thursday, falling 27%, while three firms extended slide by 10% each. The S&P BSE Sensex rose 0.4% to 59,932.24 in Mumbai, while the NSE Nifty 50 Index was little changed. For the week, the Sensex is up 1% while the Nifty is steady, dragged by some of Adani companies and insurers, which have come under pressure following changes to India’s tax rules for the sector. Even as the carnage in Adani shares has dampened sentiment, investors are starting to focus on companies’ earnings performance and growth outlook. Tata Consumer was the latest to report higher-than-expected profit for the December quarter while mortgage lender HDFC and jewelry maker Titan’s earnings met the consensus view

The Dollar Index fell 0.1% following the Fed rate decision and after Chairman Jerome Powell said the central bank has made progress in its battle against inflation, while the Norwegian krone and British pound are the weakest among the G-10 currencies. “The slowdown in the pace of Fed tightening to 25bps underlines the fact that the risk reward balance for central banks fighting the inflation threat is changing and after the aggressive action last year and the signs of easing inflation, greater caution in tightening policy is feasible,” MUFG analysts write in a note, adding that policy announcements from the ECB could highlight a policy divergence between the central banks. “The greater caution by the ECB last year means it has more work to do and that should be on show today with a 50bp hike coupled with still a hawkish message of more work to do to reach a level of policy consistent with price stability,” they add

- EUR/USD rose as much as 0.4% to 1.1033, extending gains for the third day before the ECB is expected to hike rates and warn that it will maintain its position that more aggressive rate rises are in store. A more hawkish policy stance by the ECB compared with the Fed suggest that investors are likely to focus on rate differentials, which could push EUR/USD towards 1.15 in the coming months

- USD/JPY slips 0.1%, after falling around after the Fed announcement

- EUR/SEK hovers near 11.4 hit earlier in the week, its strongest since March 2020. The Swedish krona has come under selling pressure over the past two weeks amid growing concerns about Sweden’s sluggish growth and a deteriorating housing market due to higher inflation.

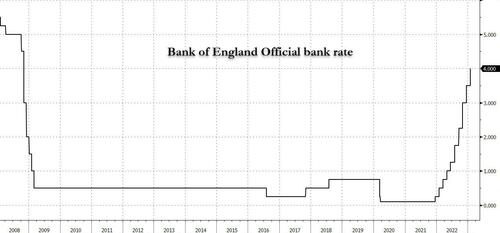

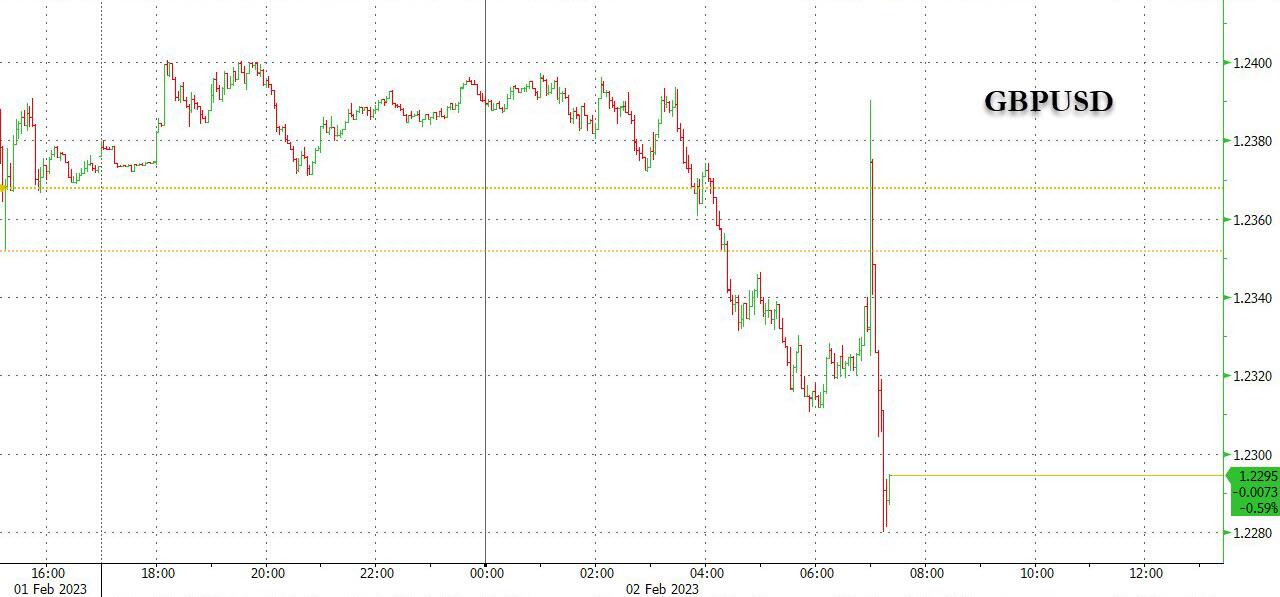

In rates, Treasuries were richer across belly of the curve, broadly holding Wednesday’s post-Fed move along with stocks. US yields richer on the day by up to 1.5bp across belly of the curve, the 10Y trading at 3.38% after closing around 3.42%; gilts had brief setback after Bank of England decision, followed by new yield lows for 10-year sector, richer by 16bp on the day (as reported earlier, Bank of England delivered a 50bp rate hike as expected with a vote split of 7-2 for a hike to 4%; statement said that inflation risks were skewed significantly to the upside). In Europe, focus now shifts to ECB rate decision at 8:15am New York time and President Christine Lagarde’s press conference. Three-month dollar Libor +0.99bp at 4.80614%. US economic data slate includes January Challenger job cuts (7:30am), 4Q nonfarm productivity, initial jobless claims (8:30am) and December factory orders (10am)

In commodities, WTI trades around session lows under USD 76.50/bbl (vs a USD 77.24/bbl high) while its Brent counterpart sits under USD 82.75/bbl (vs a USD 83.61/bbl high). Shell CEO sees continued appetite for gas in China, too early to say if the European energy crisis over. Adds, gas business can keep growing next year. Spot gold is holding onto gains above the $1950/oz mark with the 19th April peak at USD 1981/oz ahead while LME Copper reclaimed USD 9.1k/T after slipping below the mark on Wednesday.

Looking to the day ahead now, and the main highlights will be the ECB and BoE policy decisions, along with the subsequent press conferences from President Lagarde and Governor Bailey. Otherwise, US data releases include the weekly initial jobless claims, December’s factory orders, and the preliminary reading of nonfarm productivity in Q4. Lastly, earnings releases include Apple, Amazon and Alphabet.

Market Snapshot

- S&P 500 futures up 0.4% to 4,150.25

- STOXX Europe 600 up 0.6% to 456.03

- MXAP up 0.2% to 169.87

- MXAPJ up 0.3% to 557.20

- Nikkei up 0.2% to 27,402.05

- Topix down 0.4% to 1,965.17

- Hang Seng Index down 0.5% to 21,958.36

- Shanghai Composite little changed at 3,285.67

- Sensex up 0.4% to 59,945.83

- Australia S&P/ASX 200 up 0.1% to 7,511.65

- Kospi up 0.8% to 2,468.88

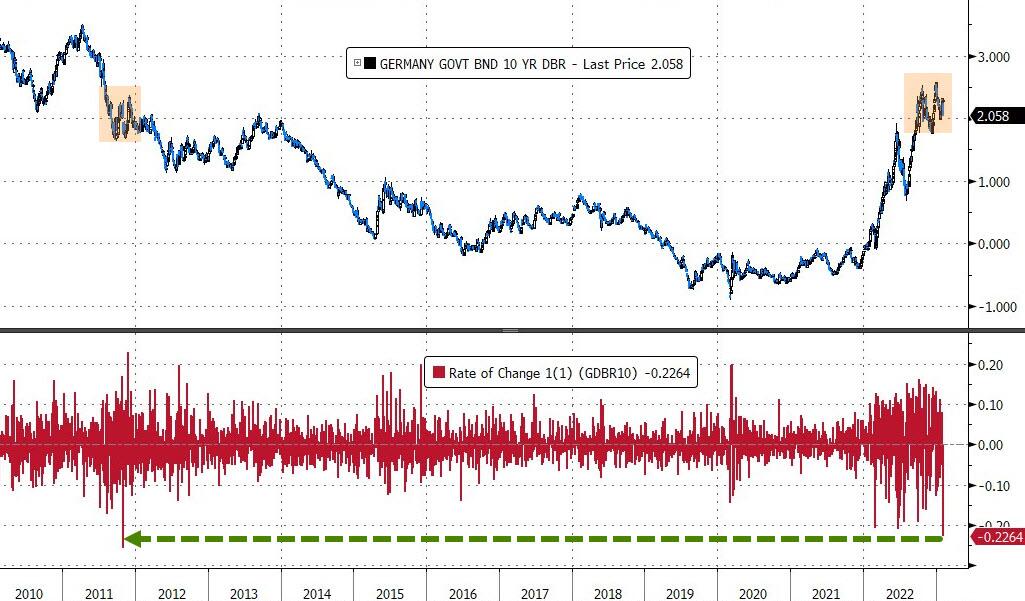

- German 10Y yield little changed at 2.26%

- Euro little changed at $1.0994

- Brent Futures little changed at $82.82/bbl

- Gold spot up 0.2% to $1,954.63

- U.S. Dollar Index little changed at 101.17

Top Overnight News from Bloomberg

- The dollar has had its worst start to the year since 2018, and chances are the losses may deepen with some help from the European Central Bank on Thursday.

- Currency option investors are looking for the Bank of England’s rate decision to have a bigger near-term impact on the pound than European Central Bank’s move later Thursday will have on the euro.

- Traders who’ve shrugged off Federal Reserve Chair Jerome Powell’s repeated warnings that interest rates will remain elevated this year will have their wagers tested again within weeks by key economic data.

- European stocks climbed with US equity futures, building on Wall Street’s advance after Federal Reserve Chair Jerome Powell said the central bank had made progress in its battle against inflation.

- Bank of Japan Deputy Governor Masazumi Wakatabe signaled there will be no policy change next month shortly before the end of his term and warned against further adjustments to the central bank’s yield curve control program.

- The Bank of Japan may be able to step toward normalizing policy this year by achieving its sustainable inflation target, according to Takatoshi Ito, an ally of Haruhiko Kuroda and a contender to replace him in April.

- Investors are readying for the final stretch in the race to replace Bank of Japan Governor Haruhiko Kuroda, a decision that could whipsaw markets from the yen to Treasuries.

- North Korea’s Foreign Ministry said the door remains shut for talks with the US on winding down its atomic arsenal, setting the stage for renewed provocations by pledging to respond to what it saw as threats from Washington.

More detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly higher in the aftermath of the FOMC meeting where the Fed slowed the pace of rate increases and Fed Chair Powell provided a slew of two-sided remarks in which he pointed to a couple more rate hikes to get to an appropriately restrictive stance but noted they are not very far from that level and acknowledged that the disinflationary process had begun. ASX 200 was led by outperformance in gold miners and tech but with gains limited by weakness in other commodity-related sectors and after mixed data. Nikkei 225 notched marginal gains with earnings releases driving the best and worst performing stocks and the 27,500 level continued to elude the index. Hang Seng and Shanghai Comp. initially gained although price action was then choppy after the HKMA raised rates in lockstep with the Fed and the PBoC continued its substantial post-holiday liquidity drain.

Top Asian News

- Hong Kong Monetary Authority raised its base rate by 25bps to 5.00%, which was as expected and in lockstep with the Fed.

- Australia-China trade discussions have the Australian PM Albanese “anticipating” a Beijing visit in 2023, via SCMP citing sources; adding, next steps amid the easing of tensions will see Trade Minister Farrell visiting Beijing prior to the PM. Subsequently, Chinese Commerce Minister Wentao and Australian Trade Minister Farrell will hold talks next week via video link, via Global Times.

- Maker of $555,000 Flying Motorbikes to Begin Trading on Nasdaq

- StanChart, HSBC Slip as Goldman Says Rates Boost Played Out

- Kuroda Ally Ito Sees Chance of BOJ Starting Unwinding in 2023

- Ex-BOJ Deputy Gov Nakaso Says to Serve on APEC Advisory Body

- Gold Rises to Nine-Month High as Fed Signals End to Rate Hikes

European bourses are benefitting from post-FOMC tailwinds with heavyweight earnings reports bolstering performance in the Tech, Telecoms and Energy sectors, Euro Stoxx 50 +1.1%. Stateside, futures are firmer across the board with action more contained vs European peers, ES +0.4%, with the exception of the NQ +1.3% which outperforms post-META. Meta Platforms Inc (META) – The social media bellwether surged over 20% afterhours after Q4 results, where although EPS missed expectations, revenue topped estimates, as did DAUs for the group, while advertising revenue was also above the consensus view, and it boosted its buyback by USD 40bln. +19% in pre-market trade

Top European News

- France’s Le Maire Expects Lawmaker Majority for Pension Reform