FEB 3/RAID CONTINUES WITH THE FAKE JOBS REPORT//GOLD CLOSED DOWN $52.55 TO $1863.65//SILVER CLOSED DOWN $1.23 TO $22.35//PLATINUM CLOSED DOWN $45.35 TO $1978.80//PALLADIUM CLOSED DOWN $25.30 TO $1629.75 TO $1629.75//COVID UPDATES: HUGE DEVELOPMENTS IN THAILAND WITH RESPECT TO THE COMA OF THE PRINCESS: BAJRAKRHYAHKA// DR S. BAKHDI PRESENTED DOCUMENTS TO THE ROYAL FAMILY/GOVERNMENT AND THEY ARE NOW TAKING ACTION AGAINST PFIZER//MORE PROJECT VERITAS TAPES RE PFIZER DIRECTOR DR. JORDAN//TAPES REVEAL PUNISHING DAMAGE TO THE FEMALE REPRODUCTIVE SYSTEM// GROWING NUMBER OF PHYSICIANS NOW REFUSE TO TAKE A BOOSTER SHOT//DR PAUL ALEXANDER//VACCINE IMPACT/SLAY NEWS//FRANCE CONTINUES TO HAVE PROTESTS ON THE ILL FATED NEW PENSION REFORM//RUSSIA MOBILIZES 500,000 SOLDIERS READY TO LAUNCH THEIR ATTACK IN THE DONBAS//INDIA CONTINUES ITS TURMOIL RE THE ADANI AFFAIR//USA PROVIDES A TOTAL PHONY JOBS REPORT WITH MASSIVE MADE UP ADJUSTMENTS: WITHOUT ADJUSTMENTS LOSS OF JOBS WOULD EQUAL 2.5 MILLION POOR SOULES AND NOW WITH THE ADJUSTMENTS THE BLS REPORTED A GAIN OF 500,000 A 8 TO 9 SIGMA ADVANCE (TOTALLY UNHEARD OF)//NEXT UP PHONY SERVICE ISM REPORT WHICH IS POLAR OPPOSITE TO THE SERVICE PMI REPORT// WE HAD 285,000 ILLINOIS RESIDENTS LOSE THEIR POWER BECAUSE OF NON PAYMENT OF ENERGY/SWAMP STORIES FOR YOU TONIGHT//

072 C GOLDMAN 9 104 C MIZUHO 2 118 C MACQUARIE FUT 96 13 132 C SG AMERICAS 6 363 H WELLS FARGO SEC 7 435 H SCOTIA CAPITAL 19 624 H BOFA SECURITIES 125 657 C MORGAN STANLEY 25 661 C JP MORGAN 111 55 686 C STONEX FINANCIA 1 690 C ABN AMRO 35 709 C BARCLAYS 1 732 C RBC CAP MARKETS 7 737 C ADVANTAGE 1 800 C MAREX SPEC 58 11 880 C CITIGROUP 48 905 C ADM 2 4

TOTAL: 318 318 MONTH TO DATE: 12,131

NO OF CONTRACTS STOPPED BY JPMORGAN: 55/318

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR FEB/2023. CONTRACT: 318 NOTICES FOR 31800 OZ or 0.9891 TONNES

total notices so far: 12,131 contracts for 1,213,100 oz (37.732 tonnes)

SILVER NOTICES: 81 NOTICE(S) FILED FOR 405,000 OZ/

total number of notices filed so far this month :167 for 835,000 oz

END

GLD

WITH GOLD DOWN $52.55

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

//BIG CHANGES IN GOLD INVENTORY AT THE GLD THIS IS VERY VERY STRANGE//TWO DAYS IN A ROW OF DEPOSITS EVEN THOUGH THE HUGE WHACKING IN PRICE DURING THE LAST TWO DAYS:: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 918.50 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $1.23

AT THE SLV// :/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.1 MILLION OZ OF SILVER FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 517.90 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 2484 CONTRACTS TO 141,471 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE HUGE GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY $0.04 GAIN SILVER PRICING AT THE COMEX ON THURSDAY. FOR THE TWO MONTHS, OUR BANKERS HAVE RETURNED TO BEING NET SHORT AND THUS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.04. AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD AN ATMOSPHERIC SIZED GAIN ON OUR TWO EXCHANGES OF 4084 CONTRACTS. AS WELL, WE HAD 355 NOTICES FOR EXCHANGE FOR RISK TRANSFER (1.775 MILLION OZ. ) AS THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1.775 MILLION OZ. WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A HUMONGOUS ISSUANCE OF EXCHANGE FOR PHYSICALS( 1600 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 0.540. MILLION OZ FOLLOWED BY TODAY’S GIGANTIC QUEUE JUMP OF 405,000 OZ// NEW TOTALS STANDING = .950 MILLION OZ + 1.775 MILLION OF EXCHANGE FOR RISK//TOTAL STANDING 2.725 MILLION OZ//// V) GIGANTIC SIZED COMEX OI GAIN/ GIGANTIC EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –344

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTRACTS for 3 days, total 2596 contracts: OR 12.980 MILLION OZ PER DAY. (865 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 12.98 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 12.98 MILLION OZ/INITIAL

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2484 DESPITE OUR TINY $0.04 GAIN IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1600 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 0.54 MILLION OZ FOLLOWED BY TODAY’S 405,000 OZ QUEUE JUMP= NEW STANDING: .950 MILLION OZ + 1.775 MILLION OZ EXCHANGE FOR RISK://NEW STANDING RISES TO 2.725 MILLION OZ .. WE HAVE AN ATMOSPHERIC SIZED GAIN OF 4084OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 81 NOTICE(S) FILED TODAY FOR 405,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 10,069 CONTRACTS TO 468,356AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: removed 48– CONTRACTS.

.

WE HAD A STRONG SIZED INCREASE IN COMEX OI ( 10,069 CONTRACTS) WITH OUR $10.95 LOSS IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 41.601 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 2100 OZ //NEW STANDING: 42.360 //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). TONNES

YET ALL OF..THIS HAPPENED WITH OUR $10.95 LOSS IN PRICEWITH RESPECT TO THURSDAY’S RAID

WE HAD A FAIR SIZED LOSS OF 2487 OI CONTRACTS (7.735 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7,582 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 468,404

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2487 CONTRACTS WITH 10,069CONTRACTS DECREASED AT THE COMEX AND 7582 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 2487 CONTRACTS OR 7.735 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7582 CONTRACTS) ACCOMPANYING THE VERY STRONG SIZED LOSS IN COMEX OI (10,069) TOTAL loss IN THE TWO EXCHANGES 2487 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 41.601 TONNES FOLLOWED BY TODAY’S 2100 OZ E.F.P. JUMP TO LONDON// ///3) CONSIDERABLE LONG LIQUIDATION //4) VERY STRONG SIZED COMEX OPEN INTEREST LOSS// 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

10,857 CONTRACTS OR 1,085,700 OZ OR 33.76 TONNES 3 TRADING DAY(S) AND THUS AVERAGING: 13619 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES:33.76 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 33.76/3550 x 100% TONNES 0.957% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 33.76 TONNES/INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 2884 CONTRACTS OI TO 141,471 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1600 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 1600 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1600 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2484 CONTRACTS AND ADD TO THE 1600 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF 4084 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 20.420 MILLION OZ//

OCCURRED DESPITE OUR 4 CENT GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED DOWN 22.34 PTS OR .68% //Hang Seng CLOSED DOWN 297.89 PTS OR 1.36% /The Nikkei closed UP 107.41 PTS OR 0.33% //Australia’s all ordinaries CLOSED UP .56% /Chinese yuan (ONSHORE) closed DOWN 6.7373 //OFFSHORE CHINESE YUAN DOWN TO 6.7431// /Oil UP TO 75.98 dollars per barrel for WTI and BRENT AT 82.31 / Stocks in Europe OPENED MOSTLY RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A VERY STRONG SIZED 10,069 CONTRACTS DOWN TO 468,356 WITH OUR LOSS IN PRICE OF $10.95

FROM THE HUGE RAID INITIATED BY OUR BANKER FRIENDS YESTERDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 7582 EFP CONTRACTS WERE ISSUED: : APRIL 7582 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 7582 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2487 CONTRACTS IN THAT 7582LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A VERY STRONG SIZED COMEX OI LOSS OF 10,069 CONTRACTS..AND THIS FAIR SIZED LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $10.95. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (42.360)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes(TOTAL THIS YEAR 656.076 TONNES

JAN/2023: 20.559 tonnes

FEB 2023: 42.360 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $10.95) //// AND WERE QUITE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD A FAIR SIZED LOSS OF 2439 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE LOST A TOTAL OI OF 7.735 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (41.219 TONNES) FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 2100 OZ OR 0.06 TONNES//new standing 42.360 tonnes … ALL OF THIS WAS ACCOMPLISHED WITH OUR FALL IN PRICE TO THE TUNE OF $10.95.

WE HAD -48 CONTRACTS COMEX TRADES ADDED TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 2487 CONTRACTS OR 248700 OZ OR 7.735 TONNES

Estimated gold comex today 298,947//good//

final gold volumes/yesterday 270,485/// fair

INITIAL STANDINGS FOR FEB 2023 COMEX GOLD //FEB 3//

Total monthly oz gold served (contracts) so far this month

12,131 notices 1,213,100 37.732 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 2

i) Out of Manfra 1350.342 (42 kilobars) oz

ii) Out of Brinks: 160.75 oz (5 kilobars)

Total withdrawals: 1511.092 oz (47 kilobars)

total in tonnes: 0.0469 tonnes

Adjustments:0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEBRUARY.

For the front month of FEBRUARY we have an oi of 1806 contracts having lost 4260 contracts. We had 4239 notices

filed yesterday so we lost 21 contracts or an additional 2100 oz were EFP jumped to London as the crooks could not find any metal over here.

March gained 119 contracts to stand to 2106.

April lost 6493 contracts up to 392,499

We had 318 notice(s) filed today for 31800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 318 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 55 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB. /2023. contract month,

we take the total number of notices filed so far for the month (11,813 x 100 oz ), to which we add the difference between the open interest for the front month of (FEBRUARY 1806 CONTRACTS) minus the number of notices served upon today 318 x 100 oz per contract equals 1,361,900 OZ OR 42.360 TONNES the number of TONNES standing in this active month of January.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (11,813 x 100 oz+ (1806 OI for the front month minus the number of notices served upon today (318)x 100 oz} which equals 1,361,900 oz standing OR 42.360 TONNES in this active delivery month of FEBRUARY..

TOTAL COMEX GOLD STANDING: 42.426TONNES. SO JUST LIKE LAST MONTH WE START WITH A LOW INITIAL AMOUNT OF GOLD STANDING BUT THIS WILL GROW AS THE MONTH PROCEEDS TO ITS CONCLUSION.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,217,232.653 OZ

TOTAL REGISTERED GOLD: 11,096,423,558 OZ (345.14 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 11,120,809.095 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,288,597 OZ (REG GOLD- PLEDGED GOLD) 288.91 tonnes//

END

SILVER/COMEX

FEB 3/2023//INITIAL. SILVER CONTRACT FOR FEBRUARY

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

87,040.710 oz

CNT

Loomis

Deposits to the Dealer Inventory

nil OZ

Deposits to the Customer Inventory

1,703,957.065 oz Delaware Loomis Manfra

No of oz served today (contracts)

81 CONTRACT(S) (405,000 OZ)

No of oz to be served (notices)

23 contracts (115,000 oz)

Total monthly oz silver served (contracts)

167 contracts (835,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 3 deposits into the customer account

i) Into Manfra: 502,212.846 oz

ii) Into Loomis: 600,968.060 oz

iii) Into Delaware: 600,776.159 oz

Total deposits: 1,703,957.065 oz

JPMorgan has a total silver weight: 148.279 million oz/292.926 million =50.52% of comex .//dropping fast

Comex withdrawals: 2

i) Out of CNT: 76,989.03 oz

ii) Out of Loomis: 10,051.680 oz

Total withdrawals; 87,040.710 oz

adjustments: 1

i) out of Manfra 297,916.600 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 32.513MILLION OZ (declining rapidly).TOTAL REG + ELIG. 292.926 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JAN

silver open interest data:

FRONT MONTH OF FEB/2023 OI: 104 CONTRACTS HAVING GAINED 36 CONTRACT(S.).

WE HAD 45 NOTICES FILED YESTERDAY, SO WE GAINED 81 CONTRACTS OR AN ADDITIONAL 405,000 OZ OF SILVER WILL

STAND AT THE COMEX.

March GAINED 585 CONTRACTS DOWN TO 105,863 contracts

April gained its first 14 contract OI to stand at 14.

TOTAL NUMBER OF NOTICES FILED FOR TODAY:81 for 405,000 oz

Comex volumes// est. volume today 64,787//fair

Comex volume: confirmed yesterday: 90,260 contracts ( very strong)

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 167 x 5,000 oz = 835,000 oz

to which we add the difference between the open interest for the front month of FEB(104) and the number of notices served upon today 81 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2023 contract month:167 (notices served so far) x 5000 oz + OI for the front month of FEB (104 – number of notices served upon today (81) x 500 oz of silver standing for the FEB. contract month equates 0.950 million oz + 1.775 MILLION OZ ( EXCHANGE FOR RISK) = 2.725MILLION OZ//(TOTAL OZ OF SILVER STANDING).

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:113,404// est. volume today// huge//crooks

FEB 3/WITH GOLD DOWN $52.55 TODAY: STRANGE: BIG CHANGES AGAIN IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 920.24 TONNES

FEB 2/WITH GOLD $10.95 TODAY: BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 918.50 TONNES

FEB 1/WITH GOLD DOWN $2.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 31/WITH GOLD UP $6.55 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 30/WITH GOLD DOWN $6.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 918.50 TONNES

JAN 27/WITH GOLD DOWN $0.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 919.37 TONNES

JAN 26/WITH GOLD DOWN $11.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 919.37 TONNES

JAN 25/WITH GOLD UP $7.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 917.34 TONNES

JAN 24/WITH GOLD UP $7.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 23/WITH GOLD UP $0.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.63 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 20/WITH GOLD UP $4.75 TODAY;BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 912.43 TONNES

JAN 19/WITH GOLD UP $16.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES INTO THE GLD///INVENTORY RESTS AT 910.98TONNES

JAN 18/WITH GOLD DOWN $1.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.9 TONNES FROM THE GLD////INVENTORY RESTS AT 909.24 TONNES

JAN 17/WITH GOLD DOWN $11.45 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.14 TONNES

JAN 13/WITH GOLD UP $22.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD///INVENTORY RESTS AT 912.14 TONNES

JAN 12/WITH GOLD UP $20.55 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 912.43 TONNES

JAN 11/WITH GOLD UP $1.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

DEC 30/WITH GOLD UP $.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 29//WITH GOLD UP $8.35 TODAY:; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 918.51 TONNES

DEC 28/WITH GOLD DOWN $6.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE DEPOSIT OF 5.50 TONNES INTO THE GLD..//INVENTORY REST S AT 918.51 TONNES

DEC 27/WITH GOLD UP $18.15 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 913.01 TONNES

DEC 23/WITH GOLD UP $19,15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES/

DEC 22/WITH GOLD DOWN $29.35 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 21/WITH GOLD FLAT TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 913.88 TONNES

DEC 20/WITH GOLD UP $27.05: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES INTO THE GLD////INVENTORY RESTS AT 912.14 TONNES

DEC 19/WITH GOLD DOWN $2.10: HUGE CHANGES IN GOLD INVENTORY AT THE GLD> A BIG WITHDRAWAL OF 3.47 TONNES FROM THE GLD//INVENTORY RESTS AT 910.41 TONNES

DEC 16/WITH GOLD UP $12.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 15//WITH GOLD DOWN $31.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 911.56 TONNES

DEC 14/WITH GOLD DOWN $6.20: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 912.72 TONNES

DEC 13/WITH GOLD UP $32.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD///INVENTORY RESTS AT 910.41

DEC 12/WITH GOLD DOWN $17.60: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

DEC 9/WITH GOLD UP $8.90//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

Dec 8/WITH GOLD UP $4.05, OVER THE PAST 3 WEEKS WE LOST 2.04 TONNES//INVENTORY RESTS AT 908.09 TONNES

GLD INVENTORY: 920.24 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 3/WITH SILVER $1.23 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 517.90 MILLION OZ//

FEB 2/WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.11 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 517.90 MILLION OZ

FEB 1/WITH SILVER DOWN 20 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.4 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 519.000 MILLION OZ

JAN 31/WITH SILVER UP 12 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.5 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 520.400 MILION OZ

JAN 30/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 521.900 MILLION OZ.

JAN 27/WITH SILVER DOWN 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 521.900 MILLION OZ//

JAN 26/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 900,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 521.900 MILLION OZ//

JAN 25/WITH SILVER UP 19 CENTS TO TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.3 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 521.000 MILLION OZ

JAN 24/WITH SILVER UP 21 CENTS TODAY: WHAT!! A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 20 MILLION OZ INTO THE SLV/( OCCURRED (LATE LAST NIGHT)//INVENTORY RESTS AT 518.70 MILLION OZ//

JAN 23/WITH SILVER DOWN 40 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.4 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 498.7 MILLION OZ//

JAN 20.WITH SILVER UP 9 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 750,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 497.300 MILLION OZ

JAN 19/WITH SILVER UP 24 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 498.05 MILLION OZ

JAN 18/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 8.15 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 498.05 MILLION OZ///

JAN 17/WITH SILVER DOWN 35 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 13/WITH SILVER UP 46 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.5 MILLION OZ FROM THE SLV..//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 12/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 508.700 MILLION OZ/

JAN 11/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 508.700MILLION OZ

JAN 10/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ

JAN 9/WITH SILVER DOWN 9 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 6/WITH SILVER UP 54 CENTS TODAY;BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.20 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 5/WITH SILVER DOWN 50 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.10 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 505.45 MILLION OZ//

JAN 4/WITH SILVER DOWN 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 506.55 MILLION OZ/

JAN 3/WITH SILVER UP 24 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: STRANGE: A WITHDRAWAL OF 1.2 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 507.85 MILLION OZ/

DEC 30/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 29/ WITH SILVER UP $0.63 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.050 MILLION OZ

DEC 28//WITH SILVER DOWN 46 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.715 MILLION OZ INTO THE SLV///..INVENTORY RESTS AT 509.050 MILLION OZ

DEC 27/WITH SILVER UP 34 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 507.350 MILLION OZ//

DEC 23/WITH SILVER UP 29 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT507.900 MILLION O//

DEC 22/WITH SILVER DOWN 53 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 21/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.0 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 20/WITH SILVER UP 105 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:: A DEPOSIT OF 700,000 OZ INTO THE SLV///INVENTORY RESTS AT 509.90 MILLION OZ//

DEC 19/WITH SILVER DOWN 13 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.05 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.20 MILLION OZ//

DEC 16/WITH SILVER UP 2 CENTS; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.85 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 508.15 MILLION OZ//

DEC 15/WITH SILVER DOWN 78 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF EXACTLY 2.00 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 510.000 MILLION OZ

DEC 14/WITH SILVER UP 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 512.000 MILLION OZ//

DEC 13/WITH SILVER UP 59 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 600,000 OZ FROM THE SLV////INVENTORY RESTS AT 513.900 MILLION OZ//

DEC 12/WITH SILVER DOWN 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 514.500 MILLION OZ//

DEC 9/WITH SILVER RISING 77 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.2 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 514.500 MILLION OZ.

DEC 8/WITH SILVER RISING 34 CENTS TODAY: OVER THE PAST 3 WEEKS, WE HAVE GAINED A STRONG: 44.777 MILLION OZ/INVENTORY RESTS AT 516.700 MILION OZ.

CLOSING INVENTORY 517.90 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

3. Chris Powell of GATA provides to us very important physical commentaries//

Russian mercenaries fight for gold mines in Central African Republic

Submitted by admin on Thu, 2023-02-02 11:21Section: Daily Dispatches

By Zeinab Mohammed Salih and Jason Burke The Guardian, London Thursday, February 2, 2023

Russian mercenaries from the Wagner Group have sustained heavy casualties in a new surge of fighting between government troops and rebels over the control of lucrative goldmines in Central African Republic.

The clashes come amid increasing instability in the anarchic, resource-rich country, which in recent years has become one of Russia’s main hubs of influence in sub-Saharan Africa.

The government offensive is led by some of the estimated 1,000 Wagner fighters stationed in the country since 2018.

Alasdair Macleod: The real war is in currencies, not Ukraine

Submitted by admin on Thu, 2023-02-02 11:31Section: Daily Dispatches

By Alasdair Macleod GoldMoney, Toronto Thursday, February 2, 2023

In the war between the Western alliance and the Asian axis, the media focus is on the Ukrainian battlefield. The real war is in currencies, with Russia capable of destroying the dollar.

So far, Russian President Vladimir Putin’s actions have been relatively passive. But already both Russia and China have accumulated enough gold to implement gold standards. It is now overwhelmingly in their interests to do so.

From Sergey Glazyev’s recent article in a Russian business newspaper, it is clear that settlement of trade balances between members, dialog partners, and associate members of the Shanghai Cooperation Organisation (SCO) optionally will be in gold. Furthermore, the Russian economy would benefit enormously from a decline in borrowing rates from current levels of more than 13% to a level more consistent with sound money.

To understand the consequences, in this article the comparison is made between the Western alliance’s fiat-currency and deficit-spending regime and the Russian-Chinese axis’ planned industrial revolution for some 3.8 billion people in the SCO family. China has a remarkable savings rate, which will underscore the investment capital for a rapid increase in Asian industrialisation without inflationary consequences.

With a new round of military action in Ukraine shortly to kick off, it will be in Putin’s interest to move from passivity to financial aggression. It will not take much for him to undermine the entire Western fiat-currency system — a danger barely recognised by a gung-ho NATO military complex. …

Wyoming Senate votes to hold invest and receive tax payments in gold and silver

(MMN)

Wyoming Senate votes to hold, invest, and receive tax payments in gold and silver

Submitted by admin on Thu, 2023-02-02 19:00Section: Daily Dispatches

By JP Cortez Money Metals News Service Eagle, Idaho Thursday, February 2, 2023

CHEYENNE, Wyoming — The Wyoming State Senate today voted 16-15, on a bipartisan basis, to pass a bill prompting the state treasurer to hold gold and silver “specie” to protect the state — as well as establish a process to receive certain tax payments in specie.

Introduced by Senator Bob Ide, R-Casper, SF 101 amends and further implements the Wyoming Legal Tender Act, a popular 2018 law that had removed all tax liability from gold and silver transactions and affirmed that the monetary metals are legal tender in Wyoming.

Senate File 101 prompts the Wyoming state treasurer to create a formal system to deal directly in constitutional money — a system that would also include holding gold as an asset to help the Cowboy State hedge against its high exposure to Federal Reserve note dollars and potentially invest in precious metals leases and bonds.

The Department of Revenue could receive mineral tax payments denominated in specie — that is, gold and silver. And in executing its duties, the state treasurer could hire precious metals firms that are experts in receiving, authenticating, exchanging, and storing gold and silver. …

The crypto bank hasn’t been accused of wrongdoing, but prosecutors want to see how deep the dealings between the crypto bank and FTX went…

Crypto bank Silvergate is reportedly being probed by the United States Department of Justice fraud unit over its involvement with the bankrupt FTX exchange and its affiliates.

The probe is investigating Silvergate’s hosting of accounts linked to former FTX CEO Sam Bankman-Fried’s businesses, according to a Feb. 3 report by Bloomberg, which cited “people familiar with the matter.”

The California-based crypto bank is not accused of any crime, but investigators are attempting to discover how deep the dealings with FTX and Alameda went.

Silvergate was heavily impacted by the collapse of FTX in November, reporting a $1 billion loss last quarter. The bank axed 40% of its staff and disclosed taking out billions of dollars in loans to prevent a liquidity crisis and bank run following the fall of the SBF empire.

The federal investigators are trying to ascertain whether Silvergate and any other companies working with FTX were aware of the situation.

According to Silvergate, Alameda opened an account with the bank in 2018, before the launch of FTX. It claims to have conducted due diligence and ongoing monitoring at the time, according to the report.

This week a bank representative said that the firm “has a comprehensive compliance and risk management program.”

Crypto trader Josh Rager commented on how this latest criminal investigation may impact crypto exchanges with ties to Silvergate.

On Jan. 27, Silvergate suspended its dividends, citing “recent volatility in the digital asset industry.” It maintained that it had a “cash position in excess of its digital asset customer-related deposits,” at the time.

Silvergate stock has lost 13% on the day tumbling to $17.14 in after-hours trading, according to MarketWatch. Furthermore, SI prices were currently 92% down from their all-time high of $220 in November 2021.

Cointelegraph reached out to Silvergate for comment but had not received a response at the time of publication.

END

.

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.7323

OFFSHORE YUAN: 6.7431

SHANGHAI CLOSED DOWN 22.34 PTS OR .68%

HANG SENG CLOSED DOWN 297.89 PTS OR 1.36%

2. Nikkei closed UP 107.41 PTS OR 0.39%

3. Europe stocks SO FAR: MOSTLY RED

USA dollar INDEX DOWN TO 101.44 Euro RISES TO 1.0935 UP 31 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.483!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 128.42/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.1425%***/Italian 10 Yr bond yield FALLS to 3.921%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.094…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.947//

3j Gold at $1915.50//silver at: 23.46 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 36/100 roubles/dollar; ROUBLE AT 70.41//

3m oil into the 75 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 128.42/10 YEAR YIELD AFTER BREAKING .54% FALLS TO .483% ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9130–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9984well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

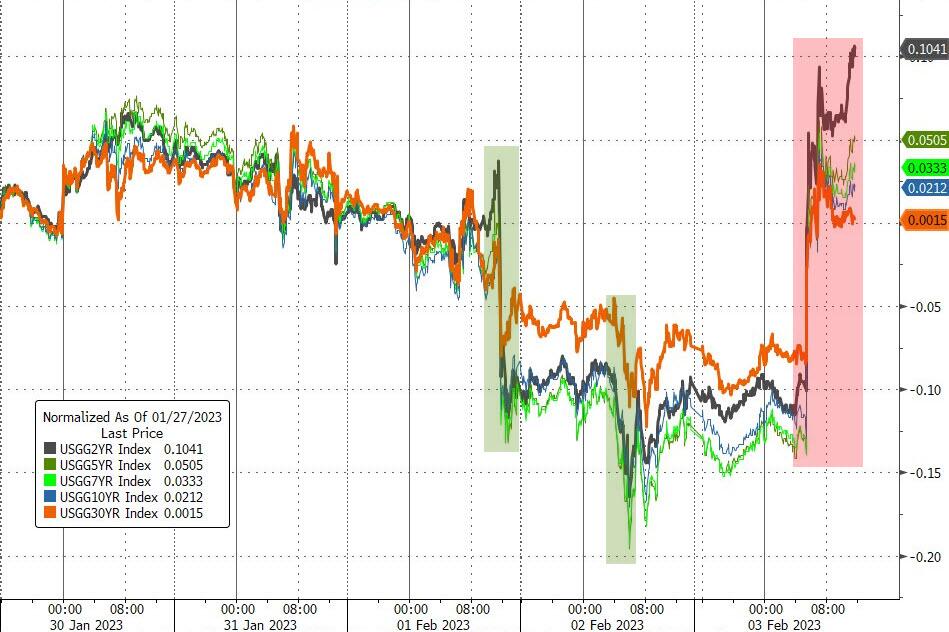

USA 10 YR BOND YIELD: 3.390% DOWN 1 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.541 DOWN 2 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,82…

GREAT BRITAIN/10 YEAR YIELD: 3.302% DOWN 12 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Drop As Tech Earnings Disappoint, Payrolls Loom

FRIDAY, FEB 03, 2023 – 08:12 AM

Thursday’s powerful rally reverse and Nasdaq futures slipped on Friday after the “Triple-A” tech giants Apple, Amazon and Alphabet poured cold water on sentiment after their reported earnings that largely missed expectations and showed an economic slowdown is choking demand for their businesses. APPL missed its 4Q revenue despite holiday season, stock -3.1%; AMZN’s Q1 guidance missed expectation, stock -5.4%; GOOGL signaled declines in searching demand, stock -4.0%. As a result, Nasdaq 100 futures fell 1% as of 7:45am ET after underlying benchmark soared 3.6% on Thursday, taking weekly gains to 5.2%. This would be the index’s fifth week of gains, marking the longest such winning streak since November 2021. S&P 500 futures also dropped, sliding 0.5% and off session lows. The risk off mood helped rates drop with the 10-year yield falling to about 3.38%; the dollar was flat, reversing earlier gains, while oil traded modestly in the red.

Today, the focal point will be the NFP data: consensus sees NFP to print 189k vs 223k prior; Unemployment to print 3.6% vs 3.5% prior. Further, keep an eye on the Hourly Earnings (4.6% survey vs. 4.3% prior) and Labor Force Participation Rate (62.3% survey vs. 62.3% prior) to further gauge the wage inflation.

As noted above, Apple, Amazon and Alphabet, which have a combined market value of almost $5 trillion, produced results that highlighted weaker demand for electronics, e-commerce, cloud computing and digital advertising. All three companies slumped in premarket trading. Together, they comprise about 27% of the Nasdaq 100. Here is a snapshot of their disappointing earnings:

Apple Inc (AAPL) Q1 2023 (USD): EPS 1.88 (exp. 1.94), Revenue 117.15bln (exp. 121.1bln), Products 96.39bln (exp. 98.98bln), iPhone 65.78bln (exp. 68.3bln), Mac 7.74bln (exp. 9.72bln), iPad 9.40bln (exp. 7.78bln). Co. said Q2 2023 revenue growth will be higher than the previous year and it sees a 5% impact from FX rates in Q2, while it expects iPhone revenue growth to accelerate in Q2 compared to Q1. Shares are lower by 3.3% pre-market.

Alphabet Inc (GOOGL) Q4 2022 (USD): EPS 1.05 (exp. 1.18), Revenue 76.05bln (exp. 76.53bln). Google advertising 59.04bln (exp. 60.64bln). Significant work underway to improve all aspects of cost structure, in support of investments in highest growth priorities. Shares are lower by 4.1% pre-market.

Amazon.com Inc (AMZN) Q4 2022 (USD): EPS 0.03 (exp. 0.18), Revenue 149.2bln (exp. 145.42bln).AWS net sales USD 21.38bln (exp. 21.76bln). Co. said in the short-term, it faces an uncertain economy but remain quite optimistic about the long-term opportunities for the Co. Shares are lower by 5.5% pre-market.

Elsewhere in premarket trading, bank stocks were mixed as investors awaited the release of economic data including monthly US payrolls. Here are some other notable premarket movers:

Nordstrom shares jump as much as 37% on news that meme-stock activist investor Ryan Cohen is building a large stake in the department store operator, a move that analysts said was positive, though they were looking to hear more regarding the activist’s intentions.

Gilead shares rose 3.9% on low volumes after the company reported 4Q results. Gilead’s core business performed well and complemented strong ongoing sales for the biopharma’s Covid treatment, which should bode well for investor sentiment into 2023, analysts say.

Qualcomm sank 3.6% after the semiconductor and telecommunication equipment provider gave worse-than-expected forecasts for the second quarter, saying it’s yet to see the benefits of China reopening in smartphone demand.

Starbucks shares fall 2.1% after the coffee chain delivered results that showed weakness in China that dragged on its overall performance.

Atlassian shares fall 12% as a second consecutive cloud guidance cut and weaker trends in its customer base are both causes for concern for analysts, though some say expectations for the software company have now been rebased to a beatable level.

Bill.com shares drop 20% as the back-office software firm’s quarterly results showed surprising levels of macro-driven weakness in its customer base, according to analysts.

Keep an eye on Boeing after the stock was cut to sector perform from outperform at RBC as the broker sees supply chain and production overhangs weighing on sentiment for the plane manufacturer.

Despite Friday’s weakness, US stock soared this week after Fed Chair Powell said the central bank has made progress in its fight to tamp down inflation, with investors brushing off fears of more rate hikes. Aside from further earnings, a slew of labor data will be in focus on Friday. Fed officials have made clear they want to see evidence that supply and demand imbalances in the labor market are starting to improve.

“The resilience of the labor market does appear to suggest that markets are underestimating how much further headroom the Federal Reserve might have when it comes to further rate hikes,” said Michael Hewson, chief market analyst at CMC Markets UK. “There continues to be a sense that the market is extraordinarily complacent about how quickly we might see the Federal Reserve pivot when it comes to interest rates.”

“Risk markets are buoyed by lower implied policy rates and expectations that the Fed will achieve a soft landing,” Alex Rohner, a fixed-income strategist at Bank J Safra Sarasin Ltd. wrote in a note. “This will be very hard to achieve. In fact, substantial tightening cycles such as the current one have historically led to a sharp rise in unemployment, and a recession.”

European stocks retreated after closing within a whisker of a bull market on Thursday. The Stoxx 600 is down 0.2% with real estate, construction and financial services the worst-performing sectors. French drugmaker Sanofi was the biggest decliner in index-points terms after forecasting a slowdown in profit growth this year. Carmakers also weighed on the index, following US peers lower after Ford’s disappointing earnings report. Here are the biggest European movers:

Sanofi shares drop as much as 5.2%, the most since November, after the French pharma giant reported fourth-quarter results that missed estimates on weak vaccine sales

IWG shares drop as much as 6.9% after Barclays cut the workspace provider to equalweight from overweight, saying that consensus looks too optimistic

Coloplast slides as much as 3.6%, before paring losses, after the Danish chronic and continence care firm’s in- line 1Q report was overshadowed by unchanged and somewhat cautious guidance

Volvo Car -3.4%, Ferrari -3%, Porsche -3.9%, Faurecia -2.3%, VW -1.6%, BMW -1.5%, Stellantis -1.5% after Ford posted fourth-quarter profit that fell short of Wall Street estimates

Cint falls as much as 41%, the most since its 2021 IPO after the Swedish data-insights firm pre-released weak 4Q results

Skanska falls as much as 4.2% after a weak performance for the Swedish construction group’s residential development arm proved a weak spot in an otherwise strong 4Q report

Zur Rose shares jumped as much as 92%, with trading halted multiple times over the course of the morning, after news the online pharmacy had sold its Swiss business to Migros subsidiary Medbase

CaixaBank shares rose as much as 3.9%, the most since December, after the Spanish lender reported fourth-quarter results that beat estimates and said it will consider additional extraordinary capital distributions

Earlier in the session, Asian stocks declined, with the regional benchmark on course for its first weekly drop of the year, as the rally in Chinese equities paused. The MSCI Asia Pacific Index declined as much as 0.6% on Friday, with declines in heavyweights Alibaba and BHP helping to offset gains in tech stocks in Japan and South Korea. Key gauges for Hong Kong and mainland China were major drags. Hopes for an energizing economic reopening and easing of corporate crackdowns have spurred a blistering rally in Chinese stocks — with the MSCI China Index up more than 50% from an October trough. But investors have started looking more deeply for new catalysts to extend the rally. Valuation of the MSCI measure of Chinese stocks may rise from the current level of around 11 times projected earnings, but to reach 13 times or more, “people need to have a very different view on geopolitical risks,” Wendy Liu, a strategist at JPMorgan Chase, said in an interview with Bloomberg TV. Still, “within that range, I think there are a lot of investment opportunities,” she said.

Japanese equities bucked the Asian trend and rose, as investors digested corporate earnings reports: Sony, Takeda Pharmaceutical and other companies that reported their latest quarterly results gained. The Topix Index rose 0.3% to 1,970.26 as of market close in Tokyo, while the Nikkei advanced 0.4% to 27,509.46. Sony contributed the most to the Topix Index’s gain, increasing 6.2% as the electronics and entertainment provider beat earnings expectations and lifted its outlook. Takeda and Murata also climbed after results. Still, among the 2,164 stocks in the index, decliners outpaced advancers 1,301 to 739, while 124 were unchanged. The latest flow data show foreign investors last week bought the most Japanese stocks and futures in more than four years.

Australian stocks posted a fifth week of gains: the S&P/ASX 200 index rose 0.6% to close at a nine-month high of 7,558.10, boosted by strength in banks and health care shares. The benchmark advanced for a fifth straight week, adding 0.9%. In New Zealand, the S&P/NZX 50 index rose 0.4% to 12,197.15.

India’s benchmark stocks gauge rallied to post its biggest weekly advance in more than six months as investors continued to overlook the selloff in shares of Adani Group, some of which rose on Friday after volatility-curbing measures from exchanges. The S&P BSE Sensex Index rose 1.5% to 60,841.88 in Mumbai, taking its weekly rally to 2.6%, the biggest since July 31. The NSE Nifty 50 Index advanced 1.4%, while its weekly gains trailed the benchmark at 1.4%, dragged by sharp plunge in shares of some Adani companies that are part of the broader index. Shares of Adani conglomerate were mixed as four out of ten companies, including Adani Enterprises, ended higher, led by 7.9% gain in ports and logistics unit while both cement units also advanced. The flagship gained 1.4%, overcoming an intraday plunge of as much as 35%. Local bourses placed six Adani Group companies, four of which also have derivative contracts traded, on a watchlist for additional trading scrutiny, a measure that analysts saw helping curb volatility in these stocks. However, the measure didn’t pacify selling in Adani Transmission and Adani Green Energy, which plunged by daily 10% limit. Excluding for the four gainers, rest six companies related to the group, closed at lower circuit level. “The equity markets witnessed an extremely high level of volatility all through the week, on account of external as well as domestic developments,” said Joseph Thomas, Head of Research, Emkay Wealth Management. “The Fed outcome as well as ECB, and also the selloff in the shares of a major business group added to the selling pressure.” Despite the selloff in Adani shares, investors have been focusing on sectors, such as consumer durables and technology, which have corrected sharply in recent weeks. Consumer durables index was the top gainer among BSE Ltd.’s 20 sector gauges while utilities, which have weight to Adani stocks, were the worst.

In FX, the Dollar Index is down 0.2% ahead of the US jobs report. The Canadian dollar and Australian dollar are the weakest among the G-10’s.

In rates, treasuries are slightly richer across the curve helped by a drop in S&P futures from Thursday’s peak as tech earnings from Apple, Amazon and Alphabet dented post-FOMC optimism. US 10-year yields around 3.39%, marginally richer vs. Thursday close with bunds lagging by 8bp in the sector, gilts by 2bp; US curve spreads slightly steeper, although within a basis point of Thursday close. Three-month dollar Libor +2.80bp at 4.83414%. European bonds also declined, paring some of the sizable gains seen after Thursday’s central bank decisions. German 10-year yields are up 6bps while the UK equivalent adds 2bps.

US economic data slate includes January jobs report (8:30am), S&P services PMI (9:45am) and ISM services index (10am): January jobs report estimate a headline print of 188k, down from prior 223k with whisper number at 197k.

In commodities, oil headed for a second weekly drop as optimism over a recovery in Chinese demand dimmed and US stockpiles kept rising. Crude futures are little changed with WTI trading near $75.85. Russia’s Kremlin said the EU embargo on Russian petroleum products will further unbalance energy market, according to Reuters. Base metals are mostly lower whilst copper bucks the trend; LME copper tested levels close to USD 9,050/t (vs high 9,091/t) before finding some support. Spot gold is down 0.1% at $1,910.

Bitcoin trades flat in European hours on either side of USD 23,500 awaitng the US NFP.

To the day ahead now, and the main highlight will be the US jobs report for January. Otherwise, in the US we’ve got the ISM services index for January, there’s the Euro Area PPI reading for December, and the final services and composite PMIs for January from around the world. From central banks, we’ll hear from the Fed’s Daly, the ECB’s Visco and BoE chief economist Pill.

Market Snapshot

S&P 500 futures down 0.7% to 4,161.00

STOXX Europe 600 down 0.3% to 457.99

MXAP down 0.2% to 169.86

MXAPJ down 0.3% to 555.25

Nikkei up 0.4% to 27,509.46

Topix up 0.3% to 1,970.26

Hang Seng Index down 1.4% to 21,660.47

Shanghai Composite down 0.7% to 3,263.41

Sensex up 1.6% to 60,865.73

Australia S&P/ASX 200 up 0.6% to 7,558.11

Kospi up 0.5% to 2,480.40

German 10Y yield little changed at 2.14%

Euro little changed at $1.0918

Brent Futures up 0.2% to $82.37/bbl

Gold spot up 0.1% to $1,914.44

U.S. Dollar Index little changed at 101.73

Top Overnight News

Bullish markets are increasingly pricing in a second-half reversal of the global monetary tightening wave, making it tougher for central bankers to vanquish inflation once and for all

Late to the global interest-rate hiking party, the ECB is trying to convince everyone that it will also be one of the last to leave; ECB Governing Council member Peter Kazimir said next month’s planned hike in borrowing costs probably won’t be the last, while Governing Council member Gediminas Simkus said a rate cut in 2023 is “not very likely”; Professional forecasters surveyed by the ECB expect inflation to average 2.1% in 2025

Russia will almost triple the amount of foreign currency it plans to sell through early March after a plunge in energy revenue brought it far below the target set in the budget

The BOJ’s unrealized losses from its bond holdings grew about 10 times last quarter due to the December policy adjustments that drove up yields

China’s policymakers plan to step up support for domestic demand this year but are likely to stop short of splashing out big on direct consumer subsidies, keeping their focus mainly on investment, three sources close to policy discussions said. RTRS

China said on Friday that cross border travel between the mainland, Hong Kong and Macau would fully resume from Feb. 6, dropping existing quotas and scrapping a mandatory COVID-19 test that was required before travelling. RTRS

CIA Director William Burns said on Thursday the intelligence agency assesses that China’s President Xi Jinping has been a little sobered by the war in Ukraine, but that it would be a mistake to underestimate Beijing and Moscow’s commitment to partnership. SCMP

BOE Chief Economist Huw Pill has said policy makers must “enguard against the possibility of doing too much” on interest rates, the latest sign that the quickest tightening cycle in three decades may be near an end. BBG

The ECB is likely to raise interest rates again in May after an already signalled hike in March, two policymakers said on Friday, with one arguing that the peak or “terminal” rate is at least starting to appear on the horizon.

The number of Russian troops killed and wounded in Ukraine is approaching 200,000, a stark symbol of just how badly President Vladimir V. Putin’s invasion has gone, according to American and other Western officials. NYT

The Kremlin on Friday rejected as a “hoax” media reports that U.S. CIA Director William Burns had travelled to Moscow with a secret peace proposal that involved Ukraine ceding a fifth of its territory to Russia. The Swiss newspaper Neue Zürcher Zeitung’s report, which said Burns had made a secret trip to Moscow last month to put forward the plan on behalf of the White House, has also been dismissed by Washington. RTRS

Big 3 Last Night: AAPL missed on EPS and revs on the call said the shortfall was driven by China supply disruptions (which have been resolved) while China demand improves (thanks to reopening) and gross margins were guided above the St (due in part to falling commodity costs); AMZN (worst of the 3) w/ the slowdown/miss in AWS (on the call said AWS is set to slow even more); GOOGL missed on EPS/op. income/revs (Google Search and YouTube advertising both were light). Into prints we saw L/O supply. Last night and pre open HFs buying the weakness. GS Securities

Turkey’s consumer inflation slowed less than forecast, even as months of deceleration are emboldening policymakers to consider interest- rate cuts ahead of approaching elections. Consumer prices rose an annual 57.7% last month, from 64.3% in December

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed as participants digested the latest bout of central bank rate hikes and a slew of earnings releases, while strong Chinese Caixin Services and Composite PMI data also failed to inspire. ASX 200 was led by healthcare and real estate, while the top-weighted financial sector also benefitted amid reports of early merger talks between regional lenders Bank of Queensland and Bendigo & Adelaide Bank. Nikkei 225 briefly breached the 27,500 level as earnings remained in focus with Sony among the best performers after it reported higher 9-month profits, as well as raised its FY net guidance and PS5 sales target. Hang Seng and Shanghai Comp. weakened despite the easing of border restrictions between mainland China, Hong Kong and Macau, while the rebound in Chinese Caixin PMI data also failed to spur risk appetite after the bout of global central bank policy tightening and with China’s Commerce Ministry warning that the nation’s imports and exports face an extremely severe environment on slowing external demand.

Top Asian News

Hong Kong Macau Affairs Office said will drop cross-border restrictions between the mainland, Hong Kong and Macau, as well as end pre-arrival PCR testing for some travellers and will resume group tours effective February 6th. Hong Kong Chief Executive Lee also announced that all border points between mainland China and Hong Kong are to resume without quotas on travel, according to Reuters.

Chinese policymakers are planning on supporting domestic demand in 2023 but are unlikely to “splash out” on direct consumer subsidies, keeping their focus on investment, according to Reuters sources.

China’s Cabinet stated that China’s economy still faces difficult and challenges, according to state media, adding that China’s economic operations are recovering, and will consolidate and expand economic recovery momentum, via Reuters.

European bourses trade mostly lower, with little in terms of news flow since the cash open as participants look ahead to the US jobs numbers. Sectors are now mixed with Energy, Basic Resources, and Healthcare as the top performers, with the former two aided by gains in underlying commodities, whilst healthcare is driven by gains in Roche (+3.0%) and AstraZeneca (+1.7%) whilst Sanofi (-2.9%) slips after poorly-received earnings. Sticking with sectors, the sectoral laggards comprise of Real Estate, Utilities, Construction and Financial Services. US futures are softer across the board with the NQ the underperformer amid disappointing earnings from highly concentrated mega-cap names (AAPL, AMZN, GOOG).

Top European News

BoE’s Chief Economics Pill said the UK has had some better times as of late, he is confident yesterday’s hike was necessary and appropriate, and there is still a lot of policy in the pipeline. Pill said the MPC has changed language quite substantially and the MPC’s job is to return inflation to the target and hold it over the medium term. He said he does not want to steer market rates on a day-to-day basis and they have to be prepared for shocks. He said it is important to guard against the possibility of doing too much. He has reasonably high confidence we will see inflation fall this year, focus is on whether inflation declined further ahead, and the notion of whether we are in a recession or not may vary throughout the year, via Times Radio.

ECB’s Simkus said inflation has probably peaked but core has yet to do so; 50bps hike in March may not be the last half-point move. He said a rate hike in May is possible, could be 25bps or 50bps but hardly 75bps. Rate reduction this year is unlikely but possible next year if the situation changes. Inflation trends are positive and approaching the terminal rate, according to Reuters and Bloomberg.

ECB’s Kazimir said March hike will not bring rates to peak. ECB will decide how many hikes take place beyond March, and fears that inflation could stay at levels too high. He said the fight against inflation is far from won.

ECB’s Rehn said the Governing Council intends to raise rates by 50bsp in March, via Twtter.

ECB’s Muller said core inflation is a cause for concern, via Bloomberg.

ECB’s Wunsch said a 25bps or 50bps rate hike is possible; will not go from 50bps in March to zero in May, and adds that 3.5% terminal rate is the minimum. He said core inflation remains persistent. He said Thursday’s decision was hawkish, market reaction was surprising.

ECB Survey of Professional Forecasters: 2023 inflation nudged higher to 5.9%, 2025 seen just above target at 2.1%.

FX

DXY has given up earlier gains after testing levels close to 102.00 before warning towards 101.50.

EUR and GBP reside as the current outperformers, with the former lifted by hawkish commentary from several ECB members, whilst both currencies benefit from upward revisions to January PMIs.

CAD is the lagged as USD/CAD continued its rebound from sub-1.3300 and y-t-d low, while the AUD suffers some contagion from a Yuan retreat.

Fixed Income

10yr USTs is nearer 115-13+ than 115-22+ extremes vs 116-00 at best in the previous session as eyes turn to the NFP.

Bunds have been down to 138.56 for a 137 tick retracement from Thursday peak following hawkish ECB commentary.

Gilts sub-107.00 at 106.89 having hit 107.78 yesterday, but downside is cushioned by dovishly-received remarks from BoE’s Pill.

Commodities

Crude benchmarks are choppy as the contracts trimmed their earlier modest gains, while complex-specific news flow has been rather light in the European morning.

Spot gold is flat intraday but with a downside bias despite the dollar waning throughout the European morning.

Base metals are mostly lower whilst copper bucks the trend; LME copper tested levels close to USD 9,050/t (vs high 9,091/t) before finding some support.

Russia’s Kremlin said the EU embargo on Russian petroleum products will further unbalance energy market, according to Reuters.

Geopolitics

US is tracking a suspected Chinese spy balloon which entered US airspace a couple of days ago which US military officials recommended to not shoot down because of safety risks, while President Biden was briefed regarding the spy balloon and asked the military to present options, according to a senior administration official cited by Reuters. It was later reported that Canada’s Department of National Defence was monitoring a possible 2nd balloon incident.

Chinese Foreign Ministry, on the US Pentagon suspecting a Chinese spy balloon over US, said speculation and hype are not conducive until the facts are clear, according to Reuters.

US CIA Director Burns said China is the biggest geopolitical challenge that the US faces and the CIA assessed that Chinese President Xi has been a little sobered by Ukraine but has serious focus and ambition on Taiwan, according to Reuters.

Chinese Foreign Ministry said there is no news to release at this time on US Secretary of State Blinken’s visit to China, according to Reuters.

Secretaries of Security Councils of Central Asia, Pakistan, India, China are to meet on Afghanistan in Moscow next week, according to Tass.

Reports of air raid sirens in Kyiv before EU-Ukraine summit started, according to AFP.

Russia’s Kremlin has rejected reports that the US offered Russia a secret peace plan on Ukraine, according to Reuters.

US Event Calendar

08:30: Jan. Change in Nonfarm Payrolls, est. 189,000, prior 223,000

Change in Private Payrolls, est. 190,000, prior 220,000

Change in Manufact. Payrolls, est. 7,000, prior 8,000

Unemployment Rate, est. 3.6%, prior 3.5%

Underemployment Rate, prior 6.5%

Labor Force Participation Rate, est. 62.3%, prior 62.3%

Average Hourly Earnings MoM, est. 0.3%, prior 0.3%

Average Hourly Earnings YoY, est. 4.3%, prior 4.6%

Average Weekly Hours est. 34.3, prior 34.3

09:45: Jan. S&P Global US Services PMI, est. 46.6, prior 46.6

ISM Services Prices Paid, prior 67.6, revised 68.1

ISM Services Employment, prior 49.8, revised 49.4

ISM Services New Orders, prior 45.2

ISM Services Index, est. 50.5, prior 49.6, revised 49.2

DB’s Jim Reid concludes the overnight wrap

After an action packed week, I’ve been press ganged into attending a fancy dress quiz night at our kids’ school this weekend. The theme is “back to the 90s”. My wife is going as Geri Halliwell and rather randomly I’m going as the late Keith Flint from the band The Prodigy as my wife found a supposedly good outfit for me. I’ve not seen it yet but I have a fake green Mohican, some fake nose studs, a studded collar and numerous fake ear piercings. My wife has her make up box ready as well. I can only hope it’s the 1990s and not the 1890s as we’ll look a bit racy next to Queen Victoria otherwise. For those that voted for us in II last year you’ll be spared pictures. For those that didn’t, you’ll get them when you least expect.

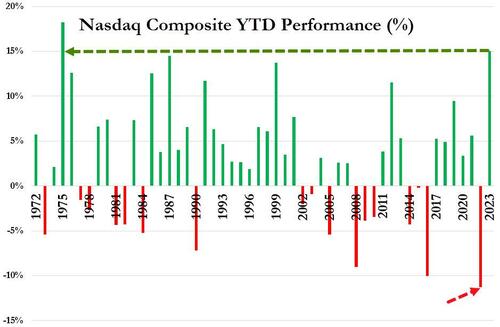

Ahead of that excitement, today we hit another payrolls Friday after an astonishing rally across the board over the last 36 hours. The highlight yesterday was one of the biggest rallies for European sovereigns in a decade as investors grew hopeful that central banks were nearing the end of their hiking cycles. Whilst plenty were questioning how sustainable this rally will prove given the actual decisions and central bank commentary, the results were undeniable. Yields on 10yr bunds (-20.4bps) saw their largest daily decline since November 2011, on the day that Mario Draghi became ECB President. That positivity was evident across the board, with the S&P 500 (+1.47%) hitting a 5-month high, and the NASDAQ (+3.25%) ending the day just shy of entering a bull market (+19.5% from the lows). However, entering that bull market might wait for another day as the big 3 tech earnings after the bell – Apple, Alphabet and Amazon – all disappointed in various ways. Their shares were down -3.2%, -4.6% and -5.1% in after-hours trading. However for some perspective they were up +3.7%, +7.3% and +7.4% respectively in normal trading.

Google’s parent company missed on Q4 revenues, particularly in YouTube ads, which are down year over year. Meanwhile Amazon reported their first annual loss since 2014, posting a net loss of -2.7bn, compared to $33bn in profit over the previous fiscal year. Apple had a poor holiday season that the company blamed in part on supply chain issues due to the Covid policies in China that led to a slower rollout of new products. Against that background, NASDAQ 100 futures are now -1.51% lower, with S&P futures down -0.53%.

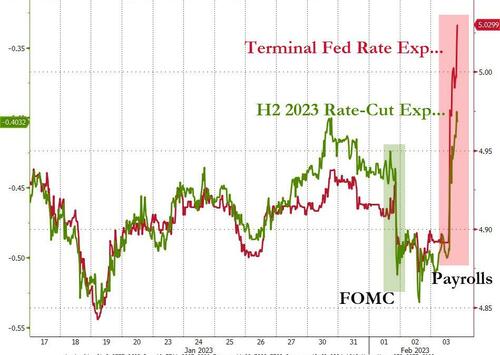

The normal hours rally got a big boost from what was at first glance a pretty hawkish ECB announcement before the nuances came through. The hike itself was 50bps as expected, taking the deposit rate up to a post-2008 high of 2.5%. And in a surprise move, they also pre-committed themselves to another 50bps hike in March, which only 2-3 weeks ago had been considered in the balance between 25 and 50. However, markets latched onto several other more dovish signals, in particular that after March they would “then evaluate the subsequent path of its monetary policy.” In addition, President Lagarde acknowledged that inflation risks were now “more balanced”, and that “the recent fall in energy prices, if it persists, may slow inflation more rapidly than expected.” What investors have liked about this week’s central bank commentary is that it will seemingly become more dependent on inflation data after March. The market thinks inflation is tamed and thus central banks will be able to, or will have to, cut rates before year-end. See our European economists’ views here, where they explain why they view yesterday’s decision as the ECB preparing for the third and final stage of the tightening cycle. They maintain their view of a 3.25% terminal rate following a 50bp hike in March and a final hike of 25bp in May.

Even as our view of terminal remained unchanged, investors moved to price in a move dovish back end to this year and beyond. For instance, even as investors moved to fully price in a 50bps move next month, the rate priced in for year-end came down by around 20bps. In turn, that triggered a massive rally for European sovereigns, with declines among 10yr bunds (-20.4bps), OATs (-23.7bps) and BTPs (-39.3bps) that we haven’t seen in years. On BTPs, it was the sixth best daily move since our daily data begins in 1993.

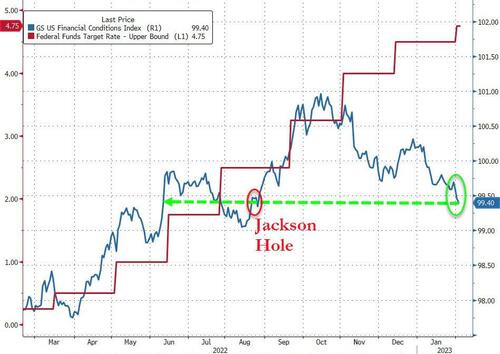

This rally initially wasn’t just confined to Europe though, since the ECB’s move added to pre-existing views that central banks are moving away from the forceful hikes of late-2022, and will instead adopt a more data-driven approach that could soon see a pause in the hiking cycle. This initially caused US Treasuries to rally along with Europe. However, in the NY afternoon, rates gave back some of their gains as expectations on the Fed’s terminal rate ultimately remained unchanged, leaving yields on 10yr Treasuries (-2.4bps) just slightly lower at 3.376%. The effects of that could be seen in financial conditions as well, with Bloomberg’s index for the US easing intraday to its most accommodative level since last February before tightening into the close as rates sold off. Regardless financial conditions remain nearly as loose as we have seen in nearly a year.

A major component of the looser financial conditions has been the rally in equities, with the S&P 500 (+1.47%) posting a third consecutive gain of more than +1% for the first time since October. The backdrop of lower rates meant that tech stocks saw a major outperformance, with the NASDAQ up +3.25%, and the FANG+ index seeing its best day since November with a +6.92% gain prior to the after-hours hiccup. It was much the same story in Europe too, with the STOXX 600 (+1.35%) at a 9-month high, along with advances for the DAX (+2.16%) and the CAC 40 (+1.26%) as well.

Asian equity markets are mixed this morning even as US equities closed on a positive note overnight. As I type, the KOSPI (+0.60%) and the Nikkei (+0.35%) are trading in the green. However, Chinese equities, led by the Hang Seng (-1.82%) and followed by the CSI (-1.67%) and the Shanghai Composite (-1.37%) are sharply lower in morning trading, taking some of the steam out of the strong rally since late October. The weak tech earnings from Wall Street overshadowed optimism about China’s economic recovery as the nation’s service sector expanded for the first time in 5 months in January. Data released showed that the services PMI rose to 52.9 from 48 in December as the sector got a boost from the lifting of strict Covid-19 curbs.

Elsewhere, the final estimate of Japan’s au Jibun Bank services PMI edged up to 52.3 in January, a 3-month high against the prior month’s reading of 51.1. The composite PMI advanced to 50.7 in January from 49.7 in December, moving above 50 for the first time in three months. Meanwhile, yields on Japanese 10yr government bonds fell (-0.9bps) to 0.48%, just below the ceiling of the Bank of Japan’s target range.

Looking forward, today’s main highlight will be the US jobs report for January, which will offer a firmer read on the state of the labour market entering 2023. Our US economists are expecting nonfarm payrolls to have grown by +175k, which would be the weakest since the December 2020 contraction, but would be consistent with a pattern that’s seen declines for 5 consecutive months now. If realised, they see the unemployment rate ticking up a tenth to 3.6%, and they think average hourly earnings will be up by +0.3%. Keep an eye out for the work week hours which was disappointing last month. Ahead of that, yesterday’s labour market data continued the theme of very strong readings, with the initial weekly jobless claims for the week ending January 28 at just 183k (vs. 195k expected). That’s their lowest level since last April, and this isn’t just a blip either, since the 4-week moving average fell to an 8-month low of 191.75k as well.

Finally, the other central bank decision yesterday came from the Bank of England, who hiked by 50bps as expected, thus taking Bank Rate up to 4%. The vote split was 7-2, with the minority preferring to leave rates unchanged. But the decision was seen as dovish, in part because the MPC dropped their previous guidance that they would “respond forcefully” if inflationary pressures were more persistent. Instead, there was a milder form of words that said if there were “more persistent pressures, then further tightening in monetary policy would be required.” Against that backdrop, sterling weakened by -1.18% against the US Dollar, and yields on 10yr gilts were down -30.1bps, which was a larger decline than in most other European countries. Our UK economist Sanjay Raja opines on the meeting here and has reduced his terminal forecast from 4.50% to 4.25%, with 25bps in March being the last hike. There are risks of modest rate hikes in H2. See his piece for more.