FEB 7/GOLD PRICE ROSE $5.25 TO $1872.20//SILVER CLOSED UP ONE CENT TO $22.15//PLATINUM CLOSED UP $3.70 WHILE PALLADIUM ROSE $52.35 TO $1650.95//COVID UPDATES: USA COVID COMMENTARY//VACCINE IMPACT//DR PAUL ALEXANDER//UKRAINE VS RUSSIA UPDATE//UPDATE ON THE EARTHQUAKE WHACKING TURKEY/SYRIA//USA TRADE DEFICIT RISES AGAIN/SWAMP STORIES TONIGHT//

072 C GOLDMAN 1 132 C SG AMERICAS 1 323 C HSBC 3 435 H SCOTIA CAPITAL 65 5 624 H BOFA SECURITIES 25 657 C MORGAN STANLEY 5 661 C JP MORGAN 21 800 C MAREX SPEC 8 2 880 C CITIGROUP 10

TOTAL: 73 73

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR FEB/2023. CONTRACT: 73 NOTICES FOR 7300 OZ or 0.2270 TONNES

total notices so far: 12,559 contracts for 1,255,900 oz (39.063 tonnes)

SILVER NOTICES: 540 NOTICE(S) FILED FOR 2,700,000 OZ/

total number of notices filed so far this month :710 for 3,550,000 oz

END

GLD

WITH GOLD UP $5.25

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

///HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 2.32 TONNES FROM THE GLD//

INVENTORY RESTS AT 917.92 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $0.01

AT THE SLV// :/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.600 MILLION OZ OF SILVER INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 519.7 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 4116 CONTRACTS TO 135,663 AND FURTHER THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE HUGE LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR TINY $0.14 LOSS SILVER PRICING AT THE COMEX ON MONDAY. FOR THE TWO MONTHS, OUR BANKERS HAVE RETURNED TO BEING NET SHORT AND THUS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.14. AND WERE SUCCESSFUL IN KNOCKING CONSIDERABLE SPEC LONGS, AS WE HAD AN ATMOSPHERIC SIZED LOSS ON OUR TWO EXCHANGES OF 3289 CONTRACTS. AS WELL, WE HAD 0 NOTICES FOR EXCHANGE FOR RISK TRANSFER (0.0 MILLION OZ. ) AS THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1.775 MILLION OZ. WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS( 827 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 0.540. MILLION OZ FOLLOWED BY TODAY’S MASSIVE 2.7 MILLION OS QUEUE JUMP O// NEW TOTALS STANDING = 3.650 MILLION OZ + 1.775 MILLION OF EXCHANGE FOR RISK//TOTAL STANDING 5.425 MILLION OZ//// V) GIGANTIC SIZED COMEX OI LOSS/ ATMOSPHERIC SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -489

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB:

TOTAL CONTRACTS for 5 days, total 6753 contracts: OR 33.765 MILLION OZ . (1351 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 33.765 MILLION OZ (HUGE)

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 33.765 MILLION OZ/INITIAL//HEADING FOR A RECORD MONTH OF ISSUANCE!!

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4116 DESPITE OUR TINY $0.14 LOSS IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 827 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 0.54 MILLION OZ FOLLOWED BY TODAY’S 2,700,000 OZ QUEUE JUMP= NEW STANDING: 3.650 MILLION OZ + 1.775 MILLION OZ EXCHANGE FOR RISK://NEW STANDING ESCALATES TO 5.425 MILLION OZ .. WE HAVE AN ATMOSPHERIC SIZED LOSS OF 2800OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE TINY FALL IN PRICE//AND THE MASSIVE QUEUE JUMP

WE HAD 540 NOTICE(S) FILED TODAY FOR 2,700,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 7778 CONTRACTS TO 441,312 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: removed –320 CONTRACTS.

.

WE HAD A STRONG SIZED DECREASE IN COMEX OI ( 7778 CONTRACTS) DESPITE OUR $3.30 GAIN IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 41.601 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S E.F.P JUMP TO LONDON OF 6,000 OZ //NEW STANDING: 42.967 TONNES//(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). TONNES

YET ALL OF..THIS HAPPENED WITH OUR $3.30 IN PRICEWITH RESPECT TO MONDAY’S TRADING

WE HAD A STRONG SIZED LOSS OF 5365 OI CONTRACTS (16.687 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2413 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 441,312

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5365 CONTRACTS WITH 7778CONTRACTS DECREASED AT THE COMEX AND 2413 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 5365 CONTRACTS OR 15.692 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2413 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (7778) TOTAL LOSS IN THE TWO EXCHANGES 5365 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 41.601 TONNES FOLLOWED BY TODAY’S 6000 OZ E.F.P. JUMP TO LONDON // ///3) CONSIDERABLE LONG LIQUIDATION //4) STRONG SIZED COMEX OPEN INTEREST LOSS// 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

21,299 CONTRACTS OR 2,129,900 OZ OR 66.24 TONNES 5 TRADING DAY(S) AND THUS AVERAGING: 4259 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY(S) IN TONNES 66.24 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 66.24/3550 x 100% TONNES 1.85% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 66.24 TONNES/INITIAL (HEADING FOR ANOTHER RECORD ISSUANCE)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 4116 CONTRACTS OI TO 135,663 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 827 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 827 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 827 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 4116 CONTRACTS AND ADD TO THE 827 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED LOSS OF 3289 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 16.445 MILLION OZ//

OCCURRED DESPITE OUR $0.14 LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 9.48 PTS OR .29% //Hang Seng CLOSED UP 76.54 PTS OR 0.36% /The Nikkei closed DOWN 8,28 PTS OR 0.03% //Australia’s all ordinaries CLOSED DOWN .72% /Chinese yuan (ONSHORE) closed DOWN 6.7856 //OFFSHORE CHINESE YUAN DOWN TO 6.7948// /Oil UP TO 75.10 dollars per barrel for WTI and BRENT AT 81.78 / Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG 7778 CONTRACTS DOWN TO 441,312 DESPITE OUR GAIN IN PRICE OF $3.30

FROM THE HUGE RAID INITIATED BY OUR BANKER FRIENDS FRIDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2413 EFP CONTRACTS WERE ISSUED: : APRIL 2413 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2413 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 5365 CONTRACTS IN THAT 2413LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 7778 CONTRACTS..AND THIS STRONG SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GAIN IN PRICE OF $3.30. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG. TODAY THE SPEC LONGS WERE RINSED OUT!!

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (42.839)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes(TOTAL THIS YEAR 656.076 TONNES

JAN/2023: 20.559 tonnes

FEB 2023: 42.839 tonnes

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $3.30) //// BUT WERE QUITE SUCCESSFUL IN KNOCKING MANY SPECULATOR LONGS AS WE HAD A VERY STRONG SIZED LOSS OF 5365 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE LOST A TOTAL OI OF 16.687 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (41.219 TONNES) FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 10,400 OZ OR 0..3235TONNES//new standing REDUCES TO 42.839 tonnes … ALL OF THIS WAS ACCOMPLISHED DESPITE OUR RISE IN PRICE TO THE TUNE OF $3.30.

WE HAD -320 CONTRACTS COMEX TRADES ADDED TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 5365 CONTRACTS OR 536500 OZ OR 16.687 TONNES

Estimated gold comex today169,218//poor//

final gold volumes/yesterday 172,032/// poor

INITIAL STANDINGS FOR FEB 2023 COMEX GOLD //FEB 7//

Total monthly oz gold served (contracts) so far this month

12,559 notices 1,255,900 39.063 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into Brinks: 2700.01 oz

total deposits: 2700.01 oz

customer withdrawals: 1

i) Out of JPMorgan: 96,453.000 tonnes or 3,000 kilobars

total withdrawals: 96,453.000 oz

total in tonnes: 3.000 tonnes

Adjustments:0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEBRUARY.

For the front month of FEBRUARY we have an oi of 1,284 contracts having lost 422 contracts. We had 318 notices

filed yesterday so we lost 104 contracts or an additional 10,400 oz will not stand for metal at the comex and thus were EFP’d over to London. I guess there is no gold over here for the crooks to great their grubby hands on.

March lost 197 contracts to stand to 1981.

April lost 7650 contracts down to 364,613

We had 73 notice(s) filed today for 7300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 73 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 21 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB. /2023. contract month,

we take the total number of notices filed so far for the month (12,559 x 100 oz ), to which we add the difference between the open interest for the front month of (FEBRUARY 1284 CONTRACTS) minus the number of notices served upon today 73 x 100 oz per contract equals 1,377,000 OZ OR 42.839 TONNES the number of TONNES standing in this active month of January.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (12,559 x 100 oz+ 1284 OI for the front month minus the number of notices served upon today (73)x 100 oz} which equals 1,377,000 oz standing OR 42.839 TONNES in this active delivery month of FEBRUARY..

TOTAL COMEX GOLD STANDING: 42.770TONNES. SO JUST LIKE LAST MONTH WE START WITH A LOW INITIAL AMOUNT OF GOLD STANDING BUT THIS WILL GROW AS THE MONTH PROCEEDS TO ITS CONCLUSION.

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 710 x 5,000 oz = 3,550,000 oz

to which we add the difference between the open interest for the front month of FEB(560) and the number of notices served upon today 540 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2023 contract month:710 (notices served so far) x 5000 oz + OI for the front month of FEB (560 – number of notices served upon today (540) x 500 oz of silver standing for the FEB. contract month equates 3.650 million oz + PREVIOUS 1.775 MILLION OZ ( EXCHANGE FOR RISK) = 5.425MILLION OZ//(TOTAL OZ OF SILVER STANDING).

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

FEB 7/WITH GOLD UP $5.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.92 TONNES

FEB 6/WITH GOLD UP $3.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.24 TONNES

FEB 3/WITH GOLD DOWN $52.55 TODAY: STRANGE: BIG CHANGES AGAIN IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 920.24 TONNES

FEB 2/WITH GOLD $10.95 TODAY: BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 918.50 TONNES

FEB 1/WITH GOLD DOWN $2.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 31/WITH GOLD UP $6.55 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 30/WITH GOLD DOWN $6.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 918.50 TONNES

JAN 27/WITH GOLD DOWN $0.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 919.37 TONNES

JAN 26/WITH GOLD DOWN $11.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 919.37 TONNES

JAN 25/WITH GOLD UP $7.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 917.34 TONNES

JAN 24/WITH GOLD UP $7.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 23/WITH GOLD UP $0.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.63 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 20/WITH GOLD UP $4.75 TODAY;BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 912.43 TONNES

JAN 19/WITH GOLD UP $16.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES INTO THE GLD///INVENTORY RESTS AT 910.98TONNES

JAN 18/WITH GOLD DOWN $1.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.9 TONNES FROM THE GLD////INVENTORY RESTS AT 909.24 TONNES

JAN 17/WITH GOLD DOWN $11.45 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.14 TONNES

JAN 13/WITH GOLD UP $22.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD///INVENTORY RESTS AT 912.14 TONNES

JAN 12/WITH GOLD UP $20.55 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 912.43 TONNES

JAN 11/WITH GOLD UP $1.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

GLD INVENTORY: 917.92 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 7/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.6 MILLION OZ OF SILVER INTO THE SLV///INVENTORY RESTS AT 519.700 MILLION OZ

FEB 6/WITH SILVER DOWN 14 CENTS: SMALL CHANGES SILVER INVENTORY AT THE SLV: A DEPOSIT OF .200 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 518.10 MILLION OZ.

FEB 3/WITH SILVER $1.23 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 517.90 MILLION OZ//

FEB 2/WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.11 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 517.90 MILLION OZ

FEB 1/WITH SILVER DOWN 20 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.4 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 519.000 MILLION OZ

JAN 31/WITH SILVER UP 12 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.5 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 520.400 MILION OZ

JAN 30/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 521.900 MILLION OZ.

JAN 27/WITH SILVER DOWN 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 521.900 MILLION OZ//

JAN 26/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 900,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 521.900 MILLION OZ//

JAN 25/WITH SILVER UP 19 CENTS TO TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.3 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 521.000 MILLION OZ

JAN 24/WITH SILVER UP 21 CENTS TODAY: WHAT!! A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 20 MILLION OZ INTO THE SLV/( OCCURRED (LATE LAST NIGHT)//INVENTORY RESTS AT 518.70 MILLION OZ//

JAN 23/WITH SILVER DOWN 40 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.4 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 498.7 MILLION OZ//

JAN 20.WITH SILVER UP 9 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 750,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 497.300 MILLION OZ

JAN 19/WITH SILVER UP 24 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 498.05 MILLION OZ

JAN 18/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 8.15 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 498.05 MILLION OZ///

JAN 17/WITH SILVER DOWN 35 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 13/WITH SILVER UP 46 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.5 MILLION OZ FROM THE SLV..//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 12/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 508.700 MILLION OZ/

JAN 11/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 508.700MILLION OZ

JAN 10/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ

JAN 9/WITH SILVER DOWN 9 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 6/WITH SILVER UP 54 CENTS TODAY;BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.20 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 5/WITH SILVER DOWN 50 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.10 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 505.45 MILLION OZ//

JAN 4/WITH SILVER DOWN 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 506.55 MILLION OZ/

JAN 3/WITH SILVER UP 24 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: STRANGE: A WITHDRAWAL OF 1.2 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 507.85 MILLION OZ/

CLOSING INVENTORY 519.7 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Peter Schiff: The Fed Can’t Fight What It Doesn’t Understand

With the Federal Reserve delivering a smaller 25 basis point rate hike at its February meeting, there is a perception that the central bank is nearing victory in the inflation fight. But as Peter Schiff pointed out during his podcast, Jerome Powell made several statements that indicate he doesn’t really understand inflation. That raises a question. How can the Fed fight what it doesn’t understand?

The markets are certainly behaving as if the tightening cycle is finished.

I think traders are looking at the softening economic data and a pullback in some of the inflation measures that we’ve had in recent months, and they think that the Fed is done hiking now even though Powell indicated that a couple more hikes are coming.”

Peter said the markets also seem to believe that inflation is going to be coming down faster.

But the reality is inflation is not going to weaken. It’s going to strengthen. The economy is not only going to weaken, but weaken much more than the markets expect. So, the markets may in fact be right that the Fed stops hiking. But not because inflation comes down, but because the economy comes down, or because employment comes down and unemployment goes up. But as of now, everybody thinks everything is great. It’s a Goldilocks scenario. People are looking for a soft landing where the economy weakens just enough to bring down inflation but not enough to bring down corporate earnings.”

Peter said the weakness in the dollar is going to be the catalyst for another explosive move up in commodity prices.

And it’s the decline in commodity prices that is helping to keep down goods prices, which is why everybody is so convinced that we’ve seen the worst of inflation and it’s headed lower. But as commodities start to make new highs when the dollar makes new lows, that’s going to throw cold water on that theory, and people are once again going to be afraid of higher inflation. But I think the Fed is going to be afraid to fight it because it’s afraid of what that fight might do to a much weaker economy and much weaker labor market than what the Fed now expects.”

During his press conference, Jerome Powell acknowledged that pain inflation causes Americans.

Because the real cause of inflation is the US government and the Federal Reserve acting in concert with one another, where the US government spends money it doesn’t have, and then the Fed prints the money for the government to spend — that is why we have inflation. So, if inflation is causing an economic hardship, and if the government and the Fed cause inflation, then it’s the government and the Federal Reserve that are responsible for that hardship.”

Powell said in order to get inflation back to 2%, it will require below-trend economic growth for some time and a softening of labor market conditions. Peter said this is one of many economic concepts Powell got wrong.

In order to bring down inflation, you don’t need to restrain economic growth. You need to restrain the growth of the money supply. You need to restrain spending that results from money printing or excess credit.”

And we don’t need to put people out of work to bring down prices.

We need to put more people to work. That’s what we need. People working means we produce more stuff. The more stuff we have, the lower the price of that stuff.”

Peter pointed out that the large deficit spending going on in Washington D.C. is exacerbating the situation by flooding the economy with fiscal stimulus.

That is interfering with the Fed’s fight against inflation. If the Fed was really serious about fighting inflation, Powell would be demanding that the federal government cut spending. Instead he’s doing the opposite [by urging Congress to raise the debt ceiling].”

A reporter asked Powell if there is any evidence of a “wage-price spiral.” Peter noted that there can’t be any evidence of such a thing because it doesn’t exist.

The whole concept of a wage-price spiral was dreamed up by a bunch of Keynsian economists during the 1970s that were looking for a scapegoat to blame inflation on.”

Prices don’t go up because wages go up.

Wages are, in fact, prices. They’re just the price of labor. And prices don’t go up because prices go up. Wages go up and other prices go up because the government creates inflation. But Powell wants people to think that inflation is created by the private sector, that the Fed is just some innocent bystander — and the government.”

Peter said the fact Powell doesn’t understand this is more evidence that Powell doesn’t understand inflation.

Along those same lines, Powell said the Fed has a bedrock belief that consumer expectations play a large part in creating inflation. In other words, consumer perception of what might happen actually causes it to happen. Inflation becomes a self-fulfilling prophecy.

This is just another way for the Federal Reserve to point the blame for inflation at the private sector, at consumers, or maybe at businesses. But the reality is consumers are not causing inflation to go up because they expect it. Inflation is going up because the Fed is creating inflation, because the government is creating inflation. Consumers are simply reacting to the inflation that has already been created.”

If consumers suddenly decide there is no more inflation but the Fed keeps creating money out of thin air — creating inflation — it doesn’t matter. Consumers will still get higher prices no matter what they think.

This all raises an important question: if Jerome Powell and other central bankers at the Fed don’t understand inflation, how will they successfully fight it?

Short answer: they won’t.

In this podcast, Peter also talks about the market reaction to the FOMC meeting, economic data, and fraud surrounding PPP loans.

end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

looks like trouble is brewing at Goldman Sachs

(courtesy Pam and Russ Martens)

There Are Very Strange Things Going On at Goldman Sachs

By Pam Martens and Russ Martens: February 7, 2023 ~

Goldman Sachs’ online bank, Marcus, is offering an interest rate on its savings accounts that is 350 times the interest rate being offered by its competitors, JPMorgan Chase and Bank of America. That’s not normal. Not normal at all. (Above screen shots were taken this morning. Chase and Bank of America screen shots come from BankRate; Marcus screen shot comes from Marcus.)

Marcus is the online banking platform offered by Goldman Sachs Bank USA – a federally-insured bank backstopped by the U.S. taxpayer. But what 99 percent of Americans don’t know about Goldman Sachs Bank USA is that it is the unit of Goldman Sachs that holds trillions of dollars in derivatives, including the kind of credit derivatives that blew up the U.S. economy in 2008 and would have taken down Goldman Sachs were it not for sneaky bailouts.

According to the most recent report from the Office of the Comptroller of the Currency (OCC), Goldman Sachs Bank USA has $513.9 billion in assets and $50.97 trillion in derivatives as of September 30, 2022. Yes, you read that correctly. (See Table 24 of the OCC report.) The most dangerous of the derivatives, credit derivatives, tally up to $623.6 billion, which is $110 billion more than the bank has in assets.

This might help to explain why Goldman Sachs is offering 350 times the going interest rate of its competitors to attract deposits and shore up its capital base.

Other noteworthy things are happening at Goldman Sachs. On January 9, Reuters ran this headline: “Goldman Sachs readies biggest layoffs since the financial crisis,” noting that “over 3,000 employees will be let go….”

Eight days after the ax fell on more than 3,000 workers’ jobs, Goldman announced that its quarterly profit had plunged by 66 percent versus the prior year and that it was taking a $972 million provision for credit losses in the quarter. That credit loss provision compared to $344 million taken a year earlier.

Ten days later, the firm announced in a regulatory filing that its Chairman and CEO, David Solomon, would be getting a compensation package that was 29 percent less than the prior year – still an obscene $25 million for one year’s toils.

Goldman is also being negatively portrayed in the business press. On Saturday, Bill Cohan reported at the Financial Times that “Goldman Sachs has lost its swagger. The market value of the venerable 154-year-old investment bank, at $121bn, is now $42bn less than its longtime arch-rival Morgan Stanley. It used to be that Goldman was the more valuable bank for many years.” (“Venerable” is an interesting choice of words for Cohan to use to describe Goldman Sachs. See our report: Goldman Sachs Says Its Dark Pools Are Under Investigation – Along with About Everything Else the Firm Does.)

One day after Cohan’s article ran, Emily Flitter and Katherine Rosman reported at the New York Times that Goldman’s Solomon, who is pulling down a cool $25 mill at his day job, has a side hustle of DJ-ing at tiki bars and owns his own record label. (You can’t make this stuff up.)

Goldman is also dealing with a big problem with its Apple credit card. On August 4 of last year, Goldman Sachs provided the following disclosure when it filed its quarterly report (10-Q) with the Securities and Exchange Commission:

“The firm is cooperating with the Consumer Financial Protection Bureau in connection with an investigation of GS Bank USA’s credit card account management practices, including with respect to the application of refunds, crediting of nonconforming payments, billing error resolution, advertisements, and reporting to credit bureaus.”

As it turns out, there are hundreds of complaints filed with the Consumer Financial Protection Bureau by consumers using the Apple credit card that is provided by Goldman Sachs. The Apple credit card holders allege being put through a living hell by Goldman Sachs when fraudulent charges are made on their Apple credit card, along with a host of other problems. In typical Goldman Sachs style, it has managed to earn the hostility of everyday consumers, airline pilots, and even a police officer with its handling of credit card complaints.

The Apple credit card via Goldman Sachs was launched three years ago in August of 2019. Goldman wrote at the time: “Goldman Sachs is the issuer of the card and is responsible for underwriting, customer service, the underlying platform and all matters related to regulatory compliance through Goldman Sachs Bank USA.”

On January 13, Sridhar Natarajan at Bloomberg News reported how the Apple credit card was racking up losses at Goldman Sachs’ Platform Solutions division:

“The division’s $1 billion pretax loss reported for 2021 was mostly tied to the Apple Card, people with knowledge of the numbers said. And about $2 billion [in losses] in 2022 mainly stems from the Apple card and installment-lending platform GreenSky, the people said.”

Is it possible that Goldman Sachs needs a CEO with no side hustles?

3. Chris Powell of GATA provides to us very important physical commentaries//

Newmont will probably have to bid higher to gain back Newcrest which was once theirs. Newcrest was once Newmont’s Australian subsidiary

(Reuters)

Newmont bids for Australia’s Newcrest but it may not be enough

Submitted by admin on Mon, 2023-02-06 08:31Section: Daily Dispatches

By Melanie Burton and Scott Murdoch Reuters Monday, February 6, 2023

MELBOURNE, Australia — Top gold producer Newmont Corp said it had made a $16.9 billion offer for Australian peer Newcrest Mining Ltd. to build a global gold behemoth, although investors and analysts said it undervalued the target amid a leadership change.

Newcrest is seeking a new boss, with previous chief executive Sandeep Biswas having stepped down in December, while global interest rates are expected to peak this year and turn down, improving the outlook for gold prices.

If successful, the all-share deal would be the largest mining takeover and the third largest corporate buyout in Australian history, according to Refinitiv data.

The Australian gold miner said that it was considering the proposal. Newmont, the world’s biggest gold producer by market value and ounces produced, described the combination as “a powerful value proposition.”

However, the initial feedback from shareholders is that they want a higher price, according to a person familiar with Newcrest’s deliberations. …

Submitted by admin on Mon, 2023-02-06 09:41Section: Daily Dispatches

By John Stonestreet Reuters Monday, February 6, 2023

Swiss citizens will get the chance to try to ensure that their economy never becomes cashless, a pressure group said, after collecting enough signatures to trigger a popular vote on the issue.

The Free Switzerland Movement says cash is playing a shrinking role in many economies, as electronic payments become the default for transactions in increasingly digitised societies, making it easier for the state to monitor its citizens’ actions.

It wants a clause added to Switzerland’s currency law, which governs how the central bank and government manage the money supply, stipulating that a “sufficient quantity” of banknotes or coins must always remain in circulation. …

Digital Currency Group (DCG) plans to hand its equity stake in Genesis’ trading arm to Genesis Global, which will then be sold, pending court approval…

A Genesis creditor has revealed the new proposed restructuring plan between Genesis, Digital Currency Group and creditors will see creditors getting back at least 80% of their funds.

On Feb. 6, Genesis Global announced it reached an “agreement in principle” with Digital Currency Group (DCG) and its creditors, which will eventually see its crypto trading and market-making arm sold as part of restructuring efforts.

DCG would contribute its share of equity in Genesis Global Trading — Genesis’ brokerage subsidiary business — to Genesis Global Holdco, the holding entity for Genesis.

The transaction would bring all Genesis-related entities under the same holding company.

It will also refinance its existing 2023 term loans with an aggregate value of $526 million and make them payable to creditors.

The agreement will also see crypto exchange Gemini contribute $100 million for its Gemini Earn users who have funds frozen with the bankrupt firm.

Pending the close of these transactions, which need the necessary court approval, Genesis will seek to put its then-owned Genesis Global Trading entity up for sale.

A Feb. 6 user update from the Genesis creditor and crypto yield platform Donut said the plan “has a recovery rate of approximately $0.80 per dollar deposited, with a path to $1.00” for Genesis creditors.

It added the recoverable amount depends on the “equity note, realized liquidation prices and considers the unknown costs associated with the remainder of this bankruptcy.”

Genesis is currently restructuring as part of its Chapter 11 bankruptcy proceedings stemming from a liquidity crisis in November brought on by the bankruptcy of crypto exchange FTX.

Genesis Global Trading was not included in the company’s Chapter 11 filing at the time, with Genesis Global Holdco saying the business would “continue client trading operations.“

At an initial bankruptcy hearing in January, Genesis lawyers said that the firm was looking for a quick resolution to its creditor disputes and expressed optimistic that the company would come out of Chapter 11 proceedings by late May.

.

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.7856

OFFSHORE YUAN: 6.7948

SHANGHAI CLOSED UP 9.40 PTS OR .29%

HANG SENG CLOSED UP 76.54 PTS OR 0.36%

2. Nikkei closed DOWN 8.28 PTS OR 0.03%

3. Europe stocks SO FAR: MOSTLY GREEN

USA dollar INDEX UP TO 103.61 Euro FALLS TO 1.0702 DOWN 27 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.490!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 132.03/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.3235%***/Italian 10 Yr bond yield RISES to 4.193%*** /SPAIN 10 YR BOND YIELD RISES TO 3.341…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.154//

3j Gold at $1866.10//silver at: 22.14 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 8/100 roubles/dollar; ROUBLE AT 71.03//

3m oil into the 75 dollar handle for WTI and 81 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 132.03/10 YEAR YIELD AFTER BREAKING .54%, RISES TO .490% ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9253–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9902well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.642% UP 1 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.690 UP 2 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,83…

GREAT BRITAIN/10 YEAR YIELD: 3.3415% UP 10 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Rise Ahead Of Key Powell Speech

TUESDAY, FEB 07, 2023 – 08:06 AM

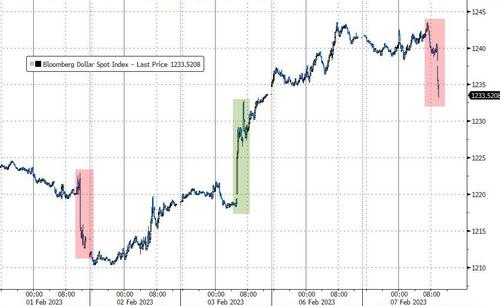

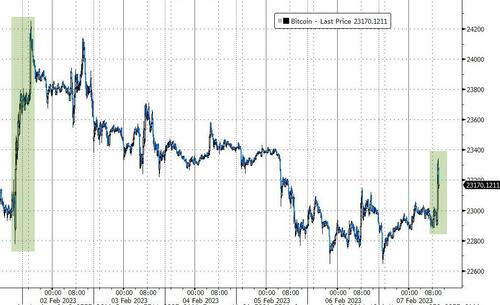

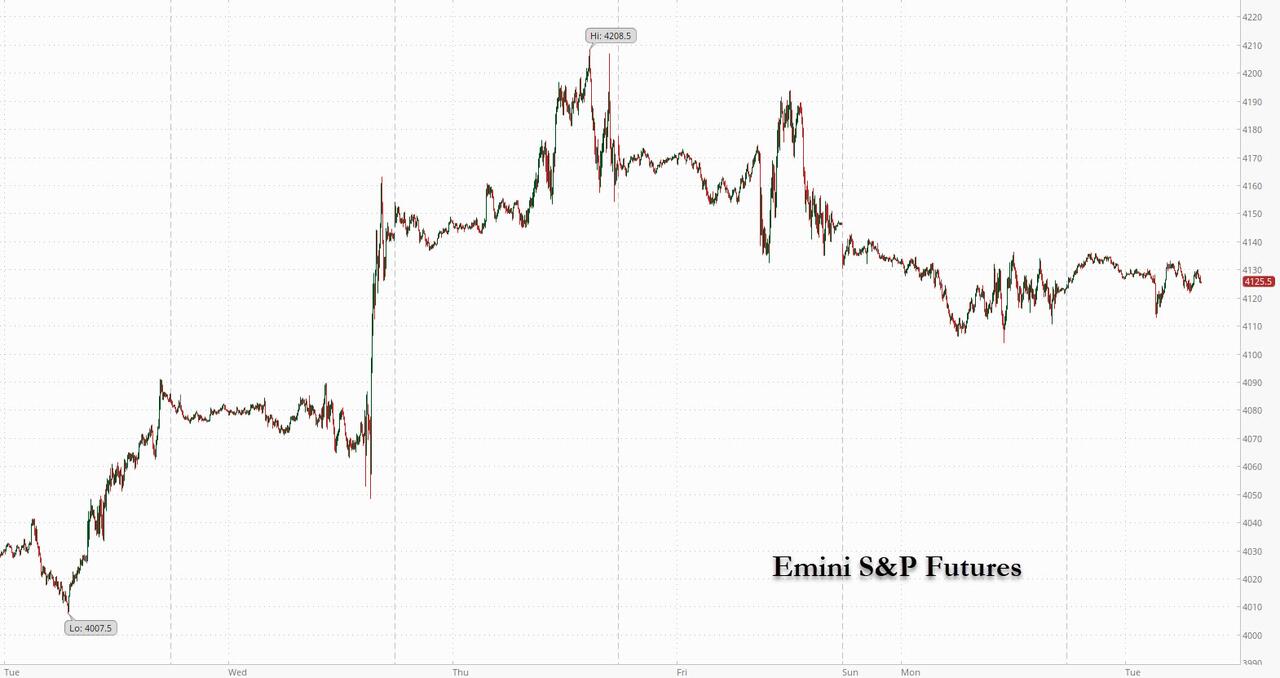

US equity futures rose, led by Nasdaq 100 contracts, setting up the tech-heavy index for a rebound as investors brace for Powell 2nd press conference in less than a week, in which he is widely expected to be more hawkish than he was during last week’s FOMC. S&P 500 futures climbed 0.1% as of 7:45 a.m. ET while Nasdaq 100 contracts added 0.3%. The Bloomberg Dollar Spot Index retreated from the day’s highs, boosting most Group-of-1o currencies. Treasury yields pulled back after two days of outsized gains. Oil climbed with gold, while Bitcoin advanced for a second day.

Among notable moves in premarket trading, Activision gained after the video game publisher’s results beat expectations thanks to the performance of its big game titles. Bed Bath & Beyond sank 33% and was set for its biggest one-day drop in nearly six months (which in turn followed a record surge the day prior) after the troubled home-furnishings retailer said it’s planning to issue convertible preferred securities and warrants that would raise more than $1 billion. Bank stocks were lower in premarket trading Tuesday, putting them on track to fall for a third straight session. Nu Holdings Ltd/Cayman Islands and Block Inc. are among the most active financials stocks in early premarket trading, gaining 1% and 0.3% respectively. Here are some of the biggest US movers today:

Activision Blizzard shares rise 2.6% to $73.47, still well below Microsoft’s offer to buy the company at $95 per share, after the video game publisher’s results beat expectations thanks to the performance of its big game titles.

Oak Street Health shares surge 36% after a Wall Street Journal report that the company is close to an agreement to be acquired by CVS Health for about $10.5 billion, including debt. Peer Cano Health (CANO US) gains 11%.

Baidu ADRs soared 15% in US premarket trading on growing hopes over the Chinese search giant’s ChatGPT-like service, which the company said is on track to roll out in March. Artificial intelligence- related stocks gained amid Baidu’s progress: SoundHound AI +15%, BigBear.ai +3.3%, C3.ai +4%

Pinterest shares slip 3.2% after the social network reported fourth-quarter revenue that was weaker than expected. While analysts were positive about the platform’s improving engagement trends, they noted that the ad market remains tough.

ZoomInfo Technologies fell 10% after the sales and marketing software company gave guidance for 2023 EPS and revenue that missed estimates. Analysts noted that cost cuts and layoffs among software firms have hurt ZoomInfo’s ability to up-sell on deals, while the macroeconomic environment is also a challenge.

Bed Bath & Beyond shares slump 31% after the troubled home-furnishings retailer said that it’s planning to issue convertible preferred securities and warrants that would raise more than $1 billion.

Chegg tumbles 24% after the US online education provider issued weaker-than-expected 2023 guidance. Expectations for a second year of shrinking sales prompted a downgrade at KeyBanc, while other brokers slash their price targets, adding the company could face future challenges from emerging AI technologies.

Adecoagro the US-listed agricultural firm with operations in South America, drops 5.9% after Morgan Stanley downgrades it to underweight from equal- weight, saying soy and corn yields will be impacted by severe drought in Argentina.

The sharp rally in US stocks had cooled in the past two days amid mounting fears that resilient economic growth would keep the Fed hawkish for longer. Fallout from the flight over the US of an alleged Chinese spy balloon has also kept risk demand subdued. Fed Chair Jerome Powell is set to speak later today and investors are keen for clues on whether the central bank could further slow the pace of rate hikes over the next few months.

“There is little to cheer as the Fed hawks are returning to the playground, mixed with escalating geopolitical tensions with China,” said Ipek Ozkardeskaya, senior analyst at Swissquote Bank. Investor confidence about the outlook for technology stocks also appears to be fizzling out. Just as the Nasdaq 100 is getting close to entering a bull market, bearish bets on the index are piling up, signaling that the outperformance isn’t expected to last, according to Citi’s Chris Montagu.

Heading into today’s 12pm speech by Powell, Investors are assessing whether the Fed Chair will dampen market optimism for interest-rate cuts later in 2023, following January’s strong payrolls report and comments from other Fed officials about the possibility of a higher peak than policy makers had previously expected. Treasuries steadied after a two-day rout sparked by traders ramping up bets on future Fed tightening.

“I expect that Powell will drive home that point that they’ve done a lot and there’ll be a tightening that is going to impact the economy later on this year,” Jack McIntyre, a portfolio manager at Brandywine Global Investment Management LLC, said on Bloomberg Television. As discussed last night, market positioning is vulnerable for another delta squeeze should Powell prove to be more dovish than expected.

Meanwhile, Bloomberg notes that the fourth-quarter reporting season has done little to support optimism about corporate fundamentals. Earnings in sectors from energy to consumer discretionary have been coming in below pre-season estimates and companies are dialing back outlooks based on expectations growth will slow. Still, in a seemingly contrarian move, analysts have boosted stock-price targets, signaling how equity prices are being driven more by the Fed’s outlook than profits.

Geopolitical concerns are also back on the radar. As the US attempts to recover the sunken remains of a huge Chinese balloon it blasted out of the sky with a missile, Beijing acknowledged ownership of a second balloon spotted drifting over several Latin American countries.

In Europe, the Stoxx 600 advances 0.3% as investors focus on positive corporate earnings rather than the prospect of additional monetary tightening. Energy and banks are among the best performing sectors, boosted by BP Plc and BNP Paribas SA after their respective updates exceeded expectations. Turkish assets extended declines as the country continued to grapple with earthquakes that killed at least 4,000 people in Turkey and Syria. Here are some of the biggest European movers:

BP shares gain as much as 4.3% after the oil major raised its dividend and extended share buybacks after reporting record full-year profits

BNP Paribas rises as much as 2.1% after the euro zone’s largest bank announced a 5-billion-euro buyback and upgraded its 2025 financial targets

Demant climbs as much as 12%, the most since February 2021, after the Danish hearing-aid maker presented a stronger-than-expected outlook for 2023

Paradox Interactive jumps as much as 13% with analysts saying the Swedish video-game developer’s results look strong on the bottom line

Lotus Bakeries advances as much as 7.3%, the most since August 2021, as analysts said the biscuit maker’s results topped expectations on all metrics

TeamViewer jumps as much as 18% after the German software maker projected 2023 revenue ahead of analyst expectations and announced a buyback program of as much as €150m

Carlsberg falls as much as 3.7%, the most since October, as analysts said guidance from the Danish brewer was disappointing

Siemens Energy drops as much as 4.8% after its results confirmed pre-released figures that had disappointed investors

Synlab slides as much as 25%, the most since the German laboratory and diagnostics firm’s May 2021 IPO, after it cut its 2022 margin guidance

AMS-Osram tumbles as much as 20% after the company issued a first-quarter outlook that missed estimates, suspended cash dividends and guided 2024 targets to the lower end of prior ranges

Morgan Advanced falls as much as 8.2% after providing a trading update in which the specialty chemicals company said a recent cyber attack will reduce FY23 Ebita by 10%-15%

Nordic Semiconductor drops as much as 19%, the biggest intraday slide since 2018, after the chipmaker said it no longer expects to meet its 2023 revenue target

In FX, the Bloomberg Dollar Spot Index eased as the greenback was little changed or weaker against its Group-of-10 peers. The Australian dollar led gains after the RBA raised the Cash Rate by 25bps to 3.35%, as expected, while it stated that the Board expects further increases in interest rates and is resolute in its determination to return inflation to the target. RBA said inflation is expected to decline this year due to both global factors and slower growth in domestic demand, as well as noted that the path to achieving a soft landing remains a narrow one. Furthermore, it stated there is uncertainty around the timing and extent of the expected slowdown in household spending and that another source of uncertainty is how the global economy responds to the large and rapid increase in interest rates around the world, while these uncertainties mean that there are a range of potential scenarios for the Australian economy. Elsewhere, the Norwegian krone was the worst performer.

The euro fell as much as 0.3% to touch $1.0697, before paring losses. The currency is set for its fourth day of declines, the longest losing streak since November. Bunds and Italian bonds were little changed ahead of scheduled policymaker speeches. Germany’s industrial production fell 3.1% m/m (estimate -0.8%) in December versus revised +0.4% in November

The pound slid to a day-low of $1.1987 before paring. Gilts were steady after Monday’s sharp drop

The Australian dollar rebounded from a one-month low to rally by as much as 1% while sovereign yields jumped after the Reserve Bank raised its key rate by 25bps to 3.35% and signaled that more tightening is needed to crush stubbornly-high inflation

The yen also bounced from a one-month low after Japanese workers’ nominal wages in December rose at the fastest pace since 1997, an acceleration in gains that may fuel speculation the central bank will consider shifting policy after Governor Haruhiko Kuroda steps down in April

In rates, treasuries clawed back some of Monday’s heavy declines with two-year yields eased as much as 5bps ahead of comments from Powell. At 730am ET, Treasuries were mixed with the curve steeper as front-end unwinds portion of Monday’s selloff. Long-end is steady, leaving 2s10s, 5s30s spreads both steeper by 3bp-4bp on the day. Bunds lag over early London session amid debt sales. Focal points of US session include 3-year note auction at 1pm New York time, an hour after Fed Chair Powell is slated to make unscripted comments at an event. US yields little changed across long-end of the curve while front-end trades richer by ~3bp on the day; US 10-year yields around 3.64%, richer by ~1bp vs Monday’s close with bunds and gilts lagging by 4bp and 6bp in the sector. Treasury auction cycle begins with $40b 3-year note sale; $35b 10-year and $21b 30-year new issue auctions are ahead Wednesday and Thursday. WI 3-year yield at 4.09% is around 11bp cheaper than January’s, which stopped 2.3bp through the WI level.

In commodities, crude benchmarks rose for a second session, after Saudi Arabia signaled it was optimistic about oil demand by unexpectedly raising prices for customers in its main market of Asia, while also lifting those for Europe and the US. WTI added 2.4% to trade near $75.90. Pumping has begun on the Kirkuk-Ceyhan oil pipeline from Iraq; exports from Ceyhan expected to being on Tuesday, according to an energy official. TotalEnergies SE is being forced to cut production of fuels like gasoline and diesel at its French oil refineries for 48 hours, according to the CGT union. US official later confirmed the US is considering raising the tariff on Russian aluminium to 200% but stated no decision was made and no announcement is expected this week, according to Reuters. Spot gold is modestly firmer and at the top-end of the session’s ranges, rising roughly 0.4% to trade near $1,874 while base metals are mixed overall with LME Copper moving back towards the USD 9k/t mark.

Looking at today’s events, at 8:30 a.m. ET we’ll get US trade balance data. Fed Chair Jerome Powell will speak at 12 p.m., followed by comments from Fed Vice Chair for Supervision Michael Barr due at 2 p.m. At 1 p.m., the US will sell $40 billion in three-year notes. Earnings today include KKR, DuPont, Prudential, Chipotle and Carlyle.

To the day ahead now, and we’ll hear from an array of central bank speakers, including Fed Chair Powell at 12pm, followed by comments from Fed Vice Chair for Supervision Michael Barr due at 2 p.m. Other central bank speakers include the ECB’s Schnabel and Villeroy, BoE Deputy Governor Ramsden, Deputy Governor Cunliffe and Chief Economist Pill, and Bank of Canada Governor Macklem. Data releases include the US trade balance at 8:30am ET. At 1 p.m., the US will sell $40 billion in three-year notes. Earnings today include KKR, DuPont, Prudential, Chipotle and Carlyle. Finally, tonight will see US President Biden deliver the State of the Union address.

Market Snapshot

S&P 500 futures up 0.2% to 4,131.00

MXAP up 0.4% to 166.13

MXAPJ up 0.2% to 542.05

Nikkei little changed at 27,685.47

Topix up 0.2% to 1,983.40

Hang Seng Index up 0.4% to 21,298.70

Shanghai Composite up 0.3% to 3,248.09

Sensex down 0.3% to 60,335.03

Australia S&P/ASX 200 down 0.5% to 7,504.14

Kospi up 0.6% to 2,451.71

STOXX Europe 600 up 0.3% to 458.44

German 10Y yield little changed at 2.30%

Euro little changed at $1.0718

Brent Futures up 1.6% to $82.26/bbl

Gold spot up 0.4% to $1,875.19

U.S. Dollar Index little changed at 103.55

Top Overnight News from Bloomberg

Japan’s Finance Ministry hasn’t approached BOJ Deputy Governor Masayoshi Amamiya about becoming the next governor, says Finance Minister Shunichi Suzuki

French labor unions are holding a third day of mass strikes and protests against raising the retirement age, keeping up pressure on the government as parliament debates the proposed reform

London house prices flatlined in December, recording their worst performance in more than three years, one of the UK’s biggest mortgage lenders said

Rescue teams from overseas began deploying in Turkey on Tuesday after a pair of powerful earthquakes a day earlier killed at least 4,000 people in the country and neighboring Syria, leaving millions to suffer without power or heat throughout a snowy night

A $5 trillion investor coalition wants to change how markets assess government bonds to help unlock climate finance to emerging markets by proposing a framework it says focuses on fairness between richer and poorer countries

A More detailed look at global markets courtesy of Newsquawk

APAC stocks eventually traded mixed after the weak lead from global counterparts as markets continued to ramp up hawkish Fed pricing, while the region also digested the RBA rate decision. ASX 200 was initially kept afloat amid strength in the energy sector after a rebound in oil prices although the index was later pressured after the RBA lifted the Cash Rate by 25bps to a fresh decade-high and signalled further rate increases ahead. Nikkei 225 was indecisive after mixed data in which household spending disappointed but wages topped forecasts, while the earnings deluge also continued. Hang Seng and Shanghai Comp. were varied with Hong Kong led by a rebound in the tech, healthcare and property sectors following yesterday’s underperformance although the mood in the mainland was less decisive owing to the recent spy balloon frictions and with a lack of fresh drivers aside from Wuhan relaxing property buying restrictions.

Top Asian News

US President Biden said the US made it clear to China what it would do regarding the balloon and it was always his view that the balloon should be shot down, while he added the balloon incident doesn’t weaken US-China relations, according to Reuters.

RBA raised the Cash Rate by 25bps to 3.35%, as expected, while it stated that the Board expects further increases in interest rates and is resolute in its determination to return inflation to the target. RBA said inflation is expected to decline this year due to both global factors and slower growth in domestic demand, as well as noted that the path to achieving a soft landing remains a narrow one. Furthermore, it stated there is uncertainty around the timing and extent of the expected slowdown in household spending and that another source of uncertainty is how the global economy responds to the large and rapid increase in interest rates around the world, while these uncertainties mean that there are a range of potential scenarios for the Australian economy.

Chinese President Xi says will strive to achieve overall improvement in economic operations, via state media; Premier Li says China’s economy still faces many challenges.

European bourses are modestly firmer, Euro Stoxx 50 +0.2%, after yesterday’s pronounced pressure and ahead of key Central Bank speak. Within Europe, sectors are mixed with Energy the clear outperformer post-BP, with the FTSE 100 bid, while Banking names are bolstered on yields/BNP Paribas. Stateside, the picture is very similar to the above though the NQ +0.3% is the incremental outperformer with US yields ever so slightly softer. BP (BP/ LN) Q4 2022 (USD): Adj. Net 4.81bln (exp. 5.11bln), Revenue 69.3bln (exp. 59.5bln). Adj. EPS 0.2644 (exp. 0.2713); Co. plans a further USD 2.75bln share buyback; Co. increases dividend by 10% Nintendo (7974 JT) 9-month (JPY): Net Profit 346mln, -5.8%; Operating Profit 410mln, -13%; Recurring Profit 482mln, -6%; Switch unit sales 14.91mln (prev. 18.95mln). FY22/23: Switch unit sales 18mln (prev. guided 19mln), Op. Income 480bln (exp. 500bln)

Top European News

ECB’s Villeroy says we are not very far from the peak in inflation, does not think the ECB needs to choose between fighting inflation and avoiding a recession; better economic environment does make the monetary task easier.

HS2 faces more delays and cuts as the UK looks to rein in the costs of the project, according to FT.

Ion Markets began bringing clients back onto the clearer derivatives platform overnight following the ransomware attack, according to a Reuters source.

UK Cabinet Reshuffle: Grant Shapps expected to be new energy security secretary, Kemi Badenoch expected to be new business and trade secretary, according to Times’ Swinford; Greg Hands will be the new Conservative Party Chairman.

FX

DXY solid around 103.500 in advance of Fed chair Powell, Aussie boosted by hawkish RBA hike and guidance overnight, as AUD/USD rebounds firmly from sub-0.6900 lows to probe 0.6950 and AUD/NZD from 1.0908 to 1.0985.

Yen rebounds circa 100 pips vs Dollar between 131.70-132.71 bounds as strong Japanese wages more than offset weak household consumption.

Franc, Kiwi and Loonie claw back some heavy post-NFP losses vs Buck, but Euro and Sterling lag on 1.0700 and 1.2000 handles.

PBoC set USD/CNY mid-point at 6.7967 vs exp. 6.7962 (prev. 6.7737)

Russian Government is said to be pushing the CBR to hint at looser policy; Bank of Russia is unwilling to signal that easing is imminent; CBR is under pressure from the government to improve forecasts, according to Bloomberg.

Fixed Income

Core EGBs are softer, though off worst levels, with pressure emanating from hawkish remarks from ECB’s Villeroy; Bunds down to 136.49 at worst.

Gilts are similarly lower by just under 20 ticks ahead of BoE’s Pill and despite a well received 2027 sale.

Stateside, USTs are little changed overall with yields slightly lower though very much at the top-end of Monday’s parameters ahead of Chair Powell and a 3yr sale.

Commodities

Crude benchmarks continue to climb as the momentum from APAC trade remains in play, with fresh developments somewhat limited after Monday’s OSP updates; WTI and Brent are firmer by over 2.0%.

BP alongside earnings remarked that it expects oil prices to remain supported in Q1 by recovering Chinese demand, ongoing uncertainty around the level of Russian exports and low inventory levels.

Pumping has begun on the Kirkuk-Ceyhan oil pipeline from Iraq; exports from Ceyhan expected to being on Tuesday, according to an energy official.

Fire at the Norsi Nizhny Novgorod (340k BPD) oil refinery in Russia has been extinguished, site is operating normally, via Lukoil.

US official later confirmed the US is considering raising the tariff on Russian aluminium to 200% but stated no decision was made and no announcement is expected this week, according to Reuters.

Spot gold is modestly firmer and at the top-end of the session’s ranges, while base metals are mixed overall with LME Copper moving back towards the USD 9k/t mark.

Geopolitics

North Korean leader Kim presided over a military meeting and vowed to expand drills and bolster war readiness posture, according to Yonhap.

US Event Calendar

8:30 am: Dec. Trade Balance, est. -$68.5b, prior -$61.5b

12:00 pm: Fed Chair Powell Speaks in Washington

2:00 pm: Fed’s Barr Discusses Financial Inclusion

2:00 pm.: US Secretary of State Antony Blinken will meet German Vice Chancellor Robert Habeck

3:00 pm: Dec. Consumer Credit, est. $25b, prior $28b

DB’s Jim Reid concludes the overnight wrap

Off to Brussels this morning so for those attending the DB Outlook lunch see you later. A few people asked me yesterday how our 1990s fancy dress quiz went at our kid’s school on Saturday. What I can say is that there are few benefits of being an older parent other than when there is a 1990s music round. There were many blank faces in the room but a mispent youth (rather not being born then) meant I aced that round and our team won overall. I can’t say I added a huge amount outside of music and sport though. There unfortunately wasn’t a round on 800 years of financial market data. For those that want to see how close I looked to Keith Flint of the Prodigy and how much my wife looked like Geri from the Spice Girls please let me know and I’ll send.

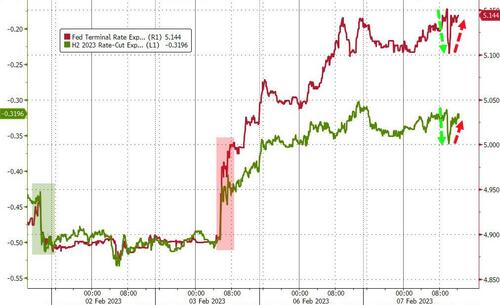

Markets got the week off to a “scary spice” start yesterday, with bonds and equities both soft, especially bonds. That was driven by growing doubts among investors about whether inflation would come down as hoped over the coming months, which in turn saw them price in a much more aggressive pace of rate hikes from central banks. Indeed, expectations of the Fed’s terminal rate for this cycle hit the first new high of the cycle since early November with the July contract ending yesterday with an implied rate of 5.157%, up from 4.81% at the recent lows last Wednesday. Indeed we’ve seen a full 25bps rate hike added to market pricing (and a bit more) since the jobs report came out on Friday. December 2023 contracts were up another 20bps yesterday and are now +48.5bps since just before the payroll report.

If investors are questioning the terminal rate once again, then this could have some big implications for markets. We wrote in our Sweet Spot note from January how a big driver of the post-October rally has been the fact that expectations of the Fed’s terminal rate stabilised around 5% and stopped rising after that point. But if we see expectations of the terminal rate take another leg higher, then clearly that would knock out a key pillar of support from the recent rally.

There was an inkling of this trend yesterday as Federal Reserve Bank of Atlanta President Bostic (non-voter this year) said that the strong Payroll report from last Friday increases the possibility that the Fed would have to increase rates further than previously forecast. President Bostic also echoed Chair Powell when referencing how inflation in core services ex-shelter has not improved as much as other sectors of the economy and sees that there is a lot of work left to do.

With investors pricing in a significantly more hawkish policy response, all eyes will be on Fed Chair Powell’s interview today at the Economic Club of Washington, DC. That’s taking place from 5pm London time, and will be the first chance he’s had to publicly respond to the bumper jobs report on Friday, which came out after his post-FOMC press conference last week. Clearly any implication that there are upside risks to the Fed’s rate outlook would validate the shift in market pricing over the last couple of days.

Ahead of that, US Treasuries lost ground across the board, with the 10yr yield up by +11.5bps on the day to 3.64% (although -2.2bps this morning in Asia). Bear in mind that on Thursday the 10yr yield hit an intraday low of 3.331%, so this is a significant bounceback. In the meantime, European sovereigns saw some sizeable shifts of their own, with yields on 10yr bunds (+10.3bps), OATs (+10.6bps) and BTPs (+13.3bps) rising significantly. The biggest underperformer were UK gilts though, where the 10yr yield rose by a massive +18.9bps on the day. That followed comments from the BoE’s Mann, who has recently been one of the most hawkish members on the MPC, but said that “in my view the next step in bank rate is still more likely to be another hike than a cut or hold.” She also struck some other hawkish tones, saying that “the consequences of under tightening far outweigh, in my opinion, the alternative.”

Equities didn’t react that well to the prospect of higher rates either, and the S&P 500 (-0.61%) lost ground for a second day running. Given the move in rates the sector skew was in favour of defensives with insurance (+1.0%), utilities (+0.9%), and food & beverage (+0.6%) outperforming while apparel (-2.0%), tech hardware (-1.7%), and media (-1.3%) all were the biggest laggards. With tech and communication stocks selling off the NASDAQ (-1.00%) and NYFANG index (-0.99%) underperformed. The one thing that made both indices look slightly better than otherwise was the fact that Tesla (+2.5%) rallied on news that Elon Musk was cleared by a federal jury and also that prices on the company’s model Y would be increasing.

Meanwhile Europe’s STOXX 600 was down -0.78%. Several negative geopolitical noises didn’t help either, and the NASDAQ Golden Dragon China index (-2.22%) that’s made up of US-listed Chinese companies struggled following the downing of the Chinese balloon by the US over the weekend. Later in the session, Bloomberg also reported from sources that the US was planning to place a 200% tariff on Russian aluminium.

While the speech is usually light on foreign policy, President Biden might address both of these issues in his State of the Union address to a joint session of Congress tonight. In a preview released by the White House yesterday, Biden will be calling for a quadrupling of the 1% tax on stock buyback that was part of the Inflation Reduction Act passed last year, as well as a new minimum tax on billionaires. We should note that given a Republican majority in the House of Representatives, neither is likely to become law. Other speaking points released include capping the price of insulin, using US-made products for the projects funded by the Administration’s infrastructure law, and aiming to reduce the deficit.

Elsewhere, the devastating earthquake that hit Turkey and Syria yesterday morning has had some ramifications across markets more broadly. In particular, oil prices were supported by the decision to stop oil flows to the Ceyhan export terminal, which exported around 1% of global oil supplies in January. That helped Brent crude close +0.49% higher at $80.99/bbl, although prices were knocked back later in the session amidst the global risk-off tone. Otherwise, Turkish assets saw significant losses yesterday, with the BIST 100 index down -1.35%, but only after recovering late in the session from an intraday low of -4.99%. In the meantime, yields on Turkey’s 2yr USD yield were up +43.2bps on the day.

Asian equity markets have somewhat stabilised this morning shrugging off the overnight losses on Wall Street. Across the region, the Hang Seng (+0.84%) is leading gains with the KOSPI (+0.48%), the CSI (+0.34%) and the Shanghai Composite (+0.33%) all reversing their previous session losses so far. Elsewhere, the Nikkei (-0.04%) is fractionally lower while the S&P/ASX 200 (-0.57%) is losing ground after the Reserve Bank of Australia (RBA) increased its cash rate for the ninth consecutive month (more on this below). Outside of Asia, US stock futures tied to the S&P 500 (+0.10%) and NASDAQ 100 (+0.13%) are inching higher.

In its latest monetary policy decision, the RBA raised its official cash rate by 25bps (as expected), taking it to 3.35%, its highest since September 2012, while warning of more rate hikes this year to dampen stubbornly high inflation. It was a pretty hawkish meeting. The Australian dollar has reacted positively, rallying + 0.67% to trade at 0.6929 against the US dollar at the time of writing.

Earlier data showed that real wages in Japan (+0.1% y/y) in December rose for the first time in nine months (v/s -1.5% expected) due to robust temporary bonuses to ease the impact of inflation. It followed a downwardly revised -2.5% drop recorded previously. Meanwhile, nominal cash earnings advanced more than anticipated to +4.8% y/y in December, notching the fastest growth since January 1997’s +6.6%. There are some likely distortions but this was still much higher than the +2.5% expected. See our economists’ note on it here. On the contrary, household spending (-1.3% y/y) dropped for the second consecutive month in December (v/s -0.4% expected) as people spent less on food.

There wasn’t much data of note yesterday, although German factory orders were up by a stronger-than-expected +3.2% in December (vs. +2.0% expected). Otherwise, Euro Area retail sales were down -2.7% that same month (vs -2.5% expected).

To the day ahead now, and we’ll hear from an array of central bank speakers, including Fed Chair Powell, Fed Vice Chair for Supervision Barr, the ECB’s Schnabel and Villeroy, BoE Deputy Governor Ramsden, Deputy Governor Cunliffe and Chief Economist Pill, and Bank of Canada Governor Macklem. Data releases include the US trade balance and German industrial production for December. Earnings releases include BP and Linde. Finally, tonight will see US President Biden deliver the State of the Union address.

end

AND NOW NEWSQUAWK (EUROPE/REPORT)

Equities modestly firmer after Monday’s pronounced pressure, Powell ahead – Newsquawk US Market Open

TUESDAY, FEB 07, 2023 – 06:22 AM

European bourses are modestly firmer, Euro Stoxx 50 +0.2%, after yesterday’s pronounced pressure and ahead of key Central Bank speak.

Stateside, the picture is very similar to the above though the NQ +0.3% is the incremental outperformer with US yields ever so slightly softer.

DXY steady around 103.500 in advance of Fed chair Powell, Aussie boosted by hawkish RBA hike and guidance overnight

Core EGBs are softer, though off worst levels, with pressure emanating from hawkish remarks from ECB’s Villeroy with Gilts similarly softer

Crude benchmarks continue to climb as the momentum from APAC trade remains in play, with fresh developments somewhat limited after Monday’s OSP updates; WTI and Brent are firmer by over 2.0%.

Looking ahead, highlights include Fed’s Powell & Barr, ECB’s Schnabel, BoE’s Cunliffe, BoC’s Macklem, Supply from the US, and Earnings from Centene, DuPont and Royal Caribbean.

Or why not try Newsquawk’s squawk box free for 7 days?

EUROPEAN TRADE

EQUITIES

European bourses are modestly firmer, Euro Stoxx 50 +0.2%, after yesterday’s pronounced pressure and ahead of key Central Bank speak.

Within Europe, sectors are mixed with Energy the clear outperformer post-BP, with the FTSE 100 bid, while Banking names are bolstered on yields/BNP Paribas.

Stateside, the picture is very similar to the above though the NQ +0.3% is the incremental outperformer with US yields ever so slightly softer.

BP (BP/ LN) Q4 2022 (USD): Adj. Net 4.81bln (exp. 5.11bln), Revenue 69.3bln (exp. 59.5bln). Adj. EPS 0.2644 (exp. 0.2713); Co. plans a further USD 2.75bln share buyback; Co. increases dividend by 10%

Nintendo (7974 JT) 9-month (JPY): Net Profit 346mln, -5.8%; Operating Profit 410mln, -13%; Recurring Profit 482mln, -6%; Switch unit sales 14.91mln (prev. 18.95mln). FY22/23: Switch unit sales 18mln (prev. guided 19mln), Op. Income 480bln (exp. 500bln)

DXY solid around 103.500 in advance of Fed chair Powell, Aussie boosted by hawkish RBA hike and guidance overnight, as AUD/USD rebounds firmly from sub-0.6900 lows to probe 0.6950 and AUD/NZD from 1.0908 to 1.0985.

Yen rebounds circa 100 pips vs Dollar between 131.70-132.71 bounds as strong Japanese wages more than offset weak household consumption.