FEB 8/GOLD CLOSED UP $6.15 TO $1878.35//SILVER CLOSED UP 22 CENTS TO $22.37//PLATINUM CLOSED UP $6.10 TO $982.60//PALLADIUM CLOSED UP $3.30 TO $1654.25//COVID UPDATES//DR PAUL ALEXANDER//VACCINE IMPACT//DR PIERRE KORY INTERVIEWED BY GREG HUNTER A MUST VIEW//////UKRAINE VS RUSSIA UPDATES//SCOTT RITTER ON THE BACKGROUND TO THE USE OF TANKS//SWAMP STORIES//

072 C GOLDMAN 3 104 C MIZUHO 1 118 C MACQUARIE FUT 68 132 C SG AMERICAS 3 323 C HSBC 6 435 H SCOTIA CAPITAL 96 624 H BOFA SECURITIES 58 657 C MORGAN STANLEY 12 661 C JP MORGAN 55 800 C MAREX SPEC 2 4 880 C CITIGROUP 22 905 C ADM 2

TOTAL: 166 166

JPMORGAN STOPPED 55/166

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR FEB/2023. CONTRACT: 166 NOTICES FOR 16600 OZ or 0.5163 TONNES

total notices so far: 12,725 contracts for 1,272,500 oz (39.580 tonnes)

SILVER NOTICES: 0 NOTICE(S) FILED FOR NI OZ/

total number of notices filed so far this month :710 for 3,550,000 oz

END

GLD

WITH GOLD UP $6.15

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

///HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 2.90 TONNES FROM THE GLD//

INVENTORY RESTS AT 920.82 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $0.22

AT THE SLV// :/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.800 MILLION OZ OF SILVER INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 522.500 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 2062 CONTRACTS TO 133,601 AND FURTHER THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE HUGE LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR TINY $0.01 GAIN SILVER PRICING AT THE COMEX ON TUESDAY. FOR THE TWO MONTHS, OUR BANKERS HAVE RETURNED TO BEING NET SHORT AND THUS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.01. AND WERE SUCCESSFUL IN KNOCKING CONSIDERABLE SPEC LONGS, AS WE HAD A STRONG SIZED LOSS ON OUR TWO EXCHANGES OF 920 CONTRACTS. AS WELL, WE HAD 0 NOTICES FOR EXCHANGE FOR RISK TRANSFER (0.0 MILLION OZ. ) AS THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1.775 MILLION OZ. WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 793 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 0.540. MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP O// NEW TOTALS STANDING = 3.650 MILLION OZ + 1.775 MILLION OF EXCHANGE FOR RISK//TOTAL STANDING 5.425 MILLION OZ//// V) HUGE SIZED COMEX OI LOSS/ STRONG SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -349

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB:

TOTAL CONTRACTS for 6 days, total 7546 contracts: OR 37,730 MILLION OZ . (1257 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 37.73 MILLION OZ (HUGE)

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 37.73 MILLION OZ/INITIAL//HEADING FOR A RECORD MONTH OF ISSUANCE!!

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2062 DESPITE OUR TINY $0.01 GAIN IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 793 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 0.54 MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP= NEW STANDING: 3.650 MILLION OZ + 1.775 MILLION OZ EXCHANGE FOR RISK://NEW STANDING REMAINS AT 5.425 MILLION OZ .. WE HAVE AN STRONG SIZED LOSS OF 920OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE TINY GAIN IN PRICE//

WE HAD 0 NOTICE(S) FILED TODAY FOR NIL OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1557 CONTRACTS TO 439,755 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: removed –772 CONTRACTS.

.

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 1557 CONTRACTS) DESPITE OUR $5.25 GAIN IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 41.601 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 2900 OZ //NEW STANDING: 42.912 TONNES//(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). TONNES

YET ALL OF..THIS HAPPENED WITH OUR $5.25 IN PRICEWITH RESPECT TO TUESDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 1061 OI CONTRACTS (3.300 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2618 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 439,755

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1833 CONTRACTS WITH 785CONTRACTS DECREASED AT THE COMEX AND 2618 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1833 CONTRACTS OR 5.7013 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2618 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (1557) TOTAL LOSS IN THE TWO EXCHANGES 1061 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 41.601 TONNES FOLLOWED BY TODAY’S 2900 OZ QUEUE JUMP // ///3) ZERO LONG LIQUIDATION //4) SMALL SIZED COMEX OPEN INTEREST LOSS// 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

22,092 CONTRACTS OR 2,209,2000 OZ OR 68.715 TONNES 6 TRADING DAY(S) AND THUS AVERAGING: 3682 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAY(S) IN TONNES 68.715 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 68.715/3550 x 100% TONNES 1.94% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 68.715 TONNES/INITIAL (HEADING FOR ANOTHER STRONG ISSUANCE)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 2062 CONTRACTS OI TO 133,950 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 793 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 793 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 793 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2062 CONTRACTS AND ADD TO THE 793 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF 1269 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 6.3 MILLION OZ//

OCCURRED DESPITE OUR $0.01 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 15.99 PTS OR .49% //Hang Seng CLOSED DOWN 15.18 PTS OR 0.07% /The Nikkei closed DOWN 79.01 PTS OR 0.29% //Australia’s all ordinaries CLOSED UP .36% /Chinese yuan (ONSHORE) closed UP 6.7864 //OFFSHORE CHINESE YUAN UP TO 6.7937// /Oil UP TO 77.90 dollars per barrel for WTI and BRENT AT 84.21 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR 1557 CONTRACTS DOWN TO 439,755 DESPITE OUR GAIN IN PRICE OF $5.25

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2618 EFP CONTRACTS WERE ISSUED: : APRIL 2618 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2618 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1061 CONTRACTS IN THAT 2618LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 1557 CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $5.25. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG. TODAY THE SPEC LONGS WERE RINSED OUT!!

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (42.917)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes(TOTAL THIS YEAR 656.076 TONNES

JAN/2023: 20.559 tonnes

FEB 2023: 42.917 tonnes

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $5.25) //// AND WERE UNSUCCESSFUL IN KNOCKING MANY SPECULATOR LONGS AS WE HAD A FAIR SIZED GAIN OF 1061 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 5.7013 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (41.219 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 2800 OZ OR 0.087TONNES//new standing INCREASES TO 42.917 tonnes … ALL OF THIS WAS ACCOMPLISHED DESPITE OUR RISE IN PRICE TO THE TUNE OF $5.25.

WE HAD -772 CONTRACTS COMEX TRADES REMOVED TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1061 CONTRACTS OR 106100 OZ OR 3.300 TONNES

Estimated gold comex today 133,606//poor//

final gold volumes/yesterday 188,248/// poor

INITIAL STANDINGS FOR FEB 2023 COMEX GOLD //FEB 8//

Total monthly oz gold served (contracts) so far this month

12,725 notices 1,272,500 39.580 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits:

i) Into Delaware 546.567 oz 17 kilobars

ii) Into HSVC 80,377.500 oz 2500 kilobars

total deposits: 80,924.067 oz

customer withdrawals: 0

Adjustments; customer to dealer; 1020.972 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEBRUARY.

For the front month of FEBRUARY we have an oi of 1,239 contracts having lost 45 contracts. We had 73 notices

filed yesterday so we gained 28 contracts or an additional 2800 oz will stand for metal at the comex

March gained 203 contracts to stand to 2184.

April lost 2551 contracts down to 362,062

We had 166 notice(s) filed today for 16600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 166 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 55 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB. /2023. contract month,

we take the total number of notices filed so far for the month (12,725 x 100 oz ), to which we add the difference between the open interest for the front month of (FEBRUARY 1239 CONTRACTS) minus the number of notices served upon today 166 x 100 oz per contract equals 1,379,800 OZ OR 42.917 TONNES the number of TONNES standing in this active month of January.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (12,725 x 100 oz+ 1239 OI for the front month minus the number of notices served upon today (166)x 100 oz} which equals 1,379,800 oz standing OR 42.917 TONNES in this active delivery month of FEBRUARY..

TOTAL COMEX GOLD STANDING: 42.917TONNES. SO JUST LIKE LAST MONTH WE START WITH A LOW INITIAL AMOUNT OF GOLD STANDING BUT THIS WILL GROW AS THE MONTH PROCEEDS TO ITS CONCLUSION.

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 710 x 5,000 oz = 3,550,000 oz

to which we add the difference between the open interest for the front month of FEB(20) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2023 contract month:710 (notices served so far) x 5000 oz + OI for the front month of FEB (20 – number of notices served upon today (0) x 500 oz of silver standing for the FEB. contract month equates 3.650 million oz + PREVIOUS 1.775 MILLION OZ ( EXCHANGE FOR RISK) = 5.425MILLION OZ//(TOTAL OZ OF SILVER STANDING).

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

FEB 8/WITH GOLD UP $6.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 920.82 TONNES

FEB 7/WITH GOLD UP $5.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.92 TONNES

FEB 6/WITH GOLD UP $3.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.24 TONNES

FEB 3/WITH GOLD DOWN $52.55 TODAY: STRANGE: BIG CHANGES AGAIN IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 920.24 TONNES

FEB 2/WITH GOLD $10.95 TODAY: BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 918.50 TONNES

FEB 1/WITH GOLD DOWN $2.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 31/WITH GOLD UP $6.55 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 30/WITH GOLD DOWN $6.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 918.50 TONNES

JAN 27/WITH GOLD DOWN $0.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 919.37 TONNES

JAN 26/WITH GOLD DOWN $11.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 919.37 TONNES

JAN 25/WITH GOLD UP $7.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 917.34 TONNES

JAN 24/WITH GOLD UP $7.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 23/WITH GOLD UP $0.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.63 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 20/WITH GOLD UP $4.75 TODAY;BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 912.43 TONNES

JAN 19/WITH GOLD UP $16.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES INTO THE GLD///INVENTORY RESTS AT 910.98TONNES

JAN 18/WITH GOLD DOWN $1.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.9 TONNES FROM THE GLD////INVENTORY RESTS AT 909.24 TONNES

JAN 17/WITH GOLD DOWN $11.45 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.14 TONNES

JAN 13/WITH GOLD UP $22.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD///INVENTORY RESTS AT 912.14 TONNES

JAN 12/WITH GOLD UP $20.55 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 912.43 TONNES

JAN 11/WITH GOLD UP $1.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

GLD INVENTORY: 920.82 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 8/WITH SILVER UP 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 2.8 MILLION OZ OF SILVER INTO THE SLV///INVENTORY REST AT 522.5 MILLION OZ//

FEB 7/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.6 MILLION OZ OF SILVER INTO THE SLV///INVENTORY RESTS AT 519.700 MILLION OZ

FEB 6/WITH SILVER DOWN 14 CENTS: SMALL CHANGES SILVER INVENTORY AT THE SLV: A DEPOSIT OF .200 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 518.10 MILLION OZ.

FEB 3/WITH SILVER $1.23 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 517.90 MILLION OZ//

FEB 2/WITH SILVER UP 4 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.11 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 517.90 MILLION OZ

FEB 1/WITH SILVER DOWN 20 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.4 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 519.000 MILLION OZ

JAN 31/WITH SILVER UP 12 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.5 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 520.400 MILION OZ

JAN 30/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 521.900 MILLION OZ.

JAN 27/WITH SILVER DOWN 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 521.900 MILLION OZ//

JAN 26/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 900,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 521.900 MILLION OZ//

JAN 25/WITH SILVER UP 19 CENTS TO TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.3 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 521.000 MILLION OZ

JAN 24/WITH SILVER UP 21 CENTS TODAY: WHAT!! A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 20 MILLION OZ INTO THE SLV/( OCCURRED (LATE LAST NIGHT)//INVENTORY RESTS AT 518.70 MILLION OZ//

JAN 23/WITH SILVER DOWN 40 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.4 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 498.7 MILLION OZ//

JAN 20.WITH SILVER UP 9 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 750,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 497.300 MILLION OZ

JAN 19/WITH SILVER UP 24 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 498.05 MILLION OZ

JAN 18/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 8.15 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 498.05 MILLION OZ///

JAN 17/WITH SILVER DOWN 35 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 13/WITH SILVER UP 46 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.5 MILLION OZ FROM THE SLV..//INVENTORY RESTS AT 506.200 MILLION OZ//

JAN 12/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 508.700 MILLION OZ/

JAN 11/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 508.700MILLION OZ

JAN 10/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ

JAN 9/WITH SILVER DOWN 9 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 6/WITH SILVER UP 54 CENTS TODAY;BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.20 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.65 MILLION OZ//

JAN 5/WITH SILVER DOWN 50 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.10 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 505.45 MILLION OZ//

JAN 4/WITH SILVER DOWN 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 506.55 MILLION OZ/

JAN 3/WITH SILVER UP 24 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: STRANGE: A WITHDRAWAL OF 1.2 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 507.85 MILLION OZ/

CLOSING INVENTORY 522.5 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Huge Central bank gold purchases of 1,136 tonnes last year. The world produces around 3500 tonnes per year but only 2600 tonnes if you exclude China and Russia. Once physical gold enters reserves, the huge short positions of bullion banks becomes more pronounced.

a good read

(SchiffGold).

Central Bank Gold Reserves Chart Second-Highest Increase Since 1950 In 2022

Central banks closed out 2022 with reported net purchases of 28 tons of gold in December. Including large unreported purchases, this brought total central bank gold buying in 2022 to 1,136 tons. It was the second-highest level of net purchases on record dating back to 1950, and the 13th straight year of net central bank gold purchases.

China officially started buying gold again in November and made another large purchase of 30 tons in December. That raised China’s total gold reserves to over 2,000 tons for the first time.

The Chinese central bank accumulated 1,448 tons of gold between 2002 and 2019, and then suddenly went silent. Many speculate that the Chinese continued to add gold to its holdings off the books during those silent years.

There has always been speculation that China holds far more gold than it officially reveals. As Jim Rickards pointed out on Mises Daily back in 2015, many people speculate that China keeps several thousand tons of gold “off the books” in a separate entity called the State Administration for Foreign Exchange (SAFE).

The Central Bank of Türkiye (Turkey) continued its consistent buying in December, adding another 25 tons to its swelling gold reserves. Over the course of 2022, Turkey added about 150 tons of gold to its hoard.

Croatia bought 2 tons of gold after having not reported any changes in its gold reserves since 2001.

After a pause in November, the Reserve Bank of India resumed purchasing gold in December, with a modest 1-ton purchase. India ranks as the ninth largest gold-holding country in the world. Since resuming buying in late 2017, the Reserve Bank of India has purchased over 200 tons of gold. In August 2020, there were reports that the RBI was considering significantly raising its gold reserves.

These purchases were partially offset by large sales by Kazakhstan (29 tons) and Uzbekistan (1 ton). It is not uncommon for banks that buy from domestic production – such as Uzbekistan and Kazakhstan – to switch between buying and selling.

December purchases brought the total net increase in central bank gold reserves in Q4 to 417 tons. Through the second half of 2022, central banks bought 862 tons of gold.

The total increase in reserves was a combination of reported buying, along with an estimate for significant unreported buying. Central banks that often fail to report purchases include China and Russia. Many analysts believe China is the mystery buyer stockpiling gold to minimize exposure to the dollar. According to the World Gold Council, “Should more information about this unreported activity become available, these estimates may be revised.”

Total 2022 central bank purchases of 1,136 tons represented a 152% increase from 2021. It was the highest level of annual net central bank gold purchases since the suspension of dollar convertibility into gold in 1971, and the second-highest annual total on record. (The record was in 1967.)

According to the World Gold Council, there are two main drivers behind central bank gold buying — its performance during times of crisis and its role as a long-term store of value.

It’s hardly surprising then that in a year scarred by geopolitical uncertainty and rampant inflation, central banks opted to continue adding gold to their coffers and at an accelerated pace.”

World Gold Council global head of research Juan Carlos Artigas told Kitco News that the big purchases underscore the fact that gold remains an important asset in the global monetary system.

“Even though gold is not backing currencies anymore, it is still being utilized. Why? Because it is a real asset,” he said.

Globally, central banks have added to net reserves for 13 straight years. In that time, they bought over 6,800 tons of gold.

After record years in 2018 and 2019, central bank gold-buying slowed in 2020 with net purchases totaling about 273 tons. The lower rate of purchases in 2020 was expected given the strength of central bank buying both in 2018 and 2019. The economic chaos caused by the coronavirus pandemic has also impacted the market.

Central bank demand came in at 650.3 tons in 2019. At the time, that was the second-highest level of annual purchases for 50 years, just slightly below the 2018 net purchases of 656.2 tons.

end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

3. Chris Powell of GATA provides to us very important physical commentaries//

END

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

5.IMPORTANT COMMENTARIES ON COMMODITIES:

end

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.7864

OFFSHORE YUAN: 6.7937

SHANGHAI CLOSED DOWN 15.99 PTS OR .49%

HANG SENG CLOSED DOWN 15.18 PTS OR 0.07%

2. Nikkei closed DOWN 79.01 PTS OR 0.29%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 103.06 Euro RISES TO 1.0743 UP 12 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.4880!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 130.93/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.3515%***/Italian 10 Yr bond yield RISES to 4.226%*** /SPAIN 10 YR BOND YIELD RISES TO 3.368…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.214//

3j Gold at $1878.60//silver at: 22.39 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 88/100 roubles/dollar; ROUBLE AT 72.04//

3m oil into the 77 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 130/93/10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .488% ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9196–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9878well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.649% UP 1 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.700 UP 1 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,83…

GREAT BRITAIN/10 YEAR YIELD: 3.3275% UP 1 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Dip On Profit Taking After Post-Powell Delta Squeeze

WEDNESDAY, FEB 08, 2023 – 08:12 AM

US futures dipped after Tuesday’s furious last hour reversal rally sparked by Powell’s “disinflation” commentary which refrained from pushing back against investor optimism, even as stocks in Europe and Asia were still buoyant, with the FTSE 100 posting a new record high. S&P 500 eminis slipped 0.4% at 7:45 a.m. while Nasdaq futures were 0.2% lower. The underlying benchmarks jumped 1.3% and 2.1%, respectively, in the latest session as investors brushed off Fed chief Jerome Powell’s comments that borrowing costs may need to peak higher than previously expected, choosing to focus instead on his outlook that 2023 will be a year of significant declines in inflation. The dollar slid, Treasuries reversed some of Tuesday’s losses, and an index of commodities rose a second day.

In premarket trading, Chipotle dropped after its results missed estimates. Microsoft gained, with its market value poised to breach $2 trillion, as analysts raised price targets after it unveiled plans to use artificial intelligence tools to improve online search and browsing. Fortinet soared after the cybersecurity company gave a better-than-expected revenue forecast for 2023. Meanwhile, VF Corp. edged higher as it delivered some positives in its fiscal third-quarter earnings, though analysts say these are masking some weaker areas and a tough outlook for the Vans and North Face owner. Oak Street Health rose 30% to $33.68 after CVS agreed to acquire the elder-care provider for deal an enterprise value of about $10.6 billion. Alibaba surged premarket on news it too was developing a Chat GPT-like robot and currently conducting internal testing on the AI-tool. Here are some other notable premarket movers:

Prudential Financial (PRU US) shares decline 3.1% with analysts saying the insurer’s results missed expectations and citing ongoing concerns about the slowing pace at which it is returning capital.

Lumen Technologies (LUMN US) shares fall 13% with analysts seeing a difficult year of transition ahead for the fiber network provider after its Ebitda forecasts missed estimates.

Fortinet (FTNT US) rose 12% after the cybersecurity company gave a better-than-expected revenue forecast for 2023. Analysts noted that demand for its cyber security products remained resilient even as businesses clamp down on IT budgets.

NetEase (NTES US) rises 1.9% and its online education arm Youdao (DAO US) surges 22% in US premarket trading, after Youdao says it’s planning to roll out a demo product similar to ChatGPT soon.

Keep an eye on American Express (AXP US) as Morgan Stanley upgraded the shares to overweight from equal-weight as its consumer-finance analysts shift stock picks toward higher credit quality, sustainable revenue growth and positive operating leverage.

Watch United Rentals (URI US) as it was initiated with an outperform rating and $544 price target at Credit Suisse, which sees a strong outlook underpinned by a robust business model for the equipment-rental group.

Airline stocks may be in focus as Redburn turns more bullish on international airlines than domestic, despite expectations of compressed industry margins as costs rise. Becomes “more positive” on US network carriers given their discounted valuations.

US stocks extended their 2023 rally as traders turn more optimistic about the path of the economy and expect a Fed pivot soon. The rally has been boosted by the stubborn pessimism of noted sellside strategists such as JPM’s Marko Kolanovic, Goldman’s David J. Kostin and Morgan Stanley’s Mike Wilson who have been skeptical of the rally for the last 400 points and are warning of limited upside. At some point they will be right. The outperformance of tech stocks, specifically, is at risk as the Nasdaq 100 Index approaches a bull market and earnings estimates trend lower, with valuations swelling to expensive levels compared with real bond yields.

“I think we need to be careful with how we interpret the market rally we have been seeing,” said Madison Faller, global strategist at JPMorgan Private Bank. “To me it’s not a rally based upon incrementally dovish messaging — I think it’s actually more so that Powell’s message wasn’t incrementally hawkish,” she said in a Bloomberg TV interview. “In the short term, markets are perhaps running a little ahead of themselves in the sense that valuations are starting to look a little stretched.”

During his SOTU speech last night, Joe Biden said he is announcing new standards to require all construction materials used in federal infrastructure projects to be made in America and said the tax system is unfair, while he called for Congress to pass a minimum billionaire tax and proposed to quadruple the tax on corporate stock buybacks. Biden noted he is committed to working with China where it can advance American interests and benefit the world but if China threatens US sovereignty, the US will act to protect the country and also said the US is in the strongest position in decades to compete.

“Another hawkish speech goes unheard,” Ipek Ozkardeskaya, senior analyst at Swissquote Bank, said of Powell’s comments. “Investors focused on the fact that he appeared just as hawkish as he has always been, that he didn’t promise a 50bp hike at next meeting, and that he said that the Fed won’t actively shrink its balance sheet for at least a few years.”

European stocks rose to their highest level since April, tracking Tuesday’s rally on Wall Street as investors welcomed a balanced tone from Fed Chair Powell. The Stoxx 600 rose 0.8% as corporate earnings also provide support after positive updates from Equinor ASA, Akzo Nobel N.V and ABN AMRO Bank N.V. S&P and Nasdaq futures are both down 0.4%. Here are some of the most notable premarket movers:

ABN Amro shares rise as much as 6.1% after reporting 4Q results ahead of expectations. Analysts said it appears to be a high- quality beat for the Dutch bank

Equinor shares rise as much as 7.3% in early trading, the most in 11 months. The Norwegian energy group’s results are a beat and its shareholder returns appear to be well ahead of what was expected, analysts say

Pandora shares rise as much as 9.2% as the jewelry retailer’s quarterly earnings, organic growth and payouts topped estimates, analysts say

Tate & Lyle shares rise as much as 3% after the company announced stronger-than-expected 2028 performance targets in an update ahead of its capital markets event

Neste shares rise as much as 13%, the most since early March, after the refiner reported 4Q results that RBC said were “strong” amid higher-than-expected renewable products sales margin

Vestas shares gained as much as 3.7% after the world’s largest producer of wind turbines reported results that Jefferies said signaled the Danish company is “slowly turning the corner”

Maersk falls as much as 5.7% before paring losses after the shipping giant’s full-year forecast falls short of estimates, which Citi says will likely drive downgrades in consensus expectations

Societe Generale shares dropped as much as 2.7%, before paring losses, as its shareholder payout fell short of a previously pledged target even as quarterly profit beat estimates

Volkswagen falls as much as 2.7% to lead declines on the Stoxx 600 Automobiles & Parts Index on Wednesday after the German carmaker’s preliminary results showed cash flow below its target amid supply-chain and logistics disruptions

Handelsbanken shares fall as much as 6.9% after mixed results from the Swedish bank that failed to impress following stronger numbers from peers

TotalEnergies shares decline as much as 3% after the company published 4Q report that RBC viewed as neutral, and “broadly in line” with market expectations

Asian stocks edged higher as traders parsed comments by Federal Reserve Chair Jerome Powell that were seen as dovish, even after he reiterated that further interest rate hikes are needed to curb rising inflation. The MSCI Asia Pacific Index gained as much as 0.6%, driven by rate-sensitive technology shares. Benchmarks in Taiwan and South Korea advanced, while Japanese, Hong Kong and Chinese shares fluctuated. The Fed chair’s remarks at the Economic Club of Washington offered traders some relief, who were bracing for a more hawkish recalibration of rate expectations. While interest rates in the US will likely continue to rise, “in Asia, China’s recovery and reopening has just happened recently,” Ken Peng, head of Asia Pacific investment strategy at Citi Global Wealth Investments, said in a Bloomberg TV interview. “That momentum is there, it’s fairly strong.” Still, the stellar rally in Chinese shares over the past three months has stalled as traders take profit and await fresh catalysts. Meituan led Chinese technology stocks lower Wednesday after a report that short-form video service Douyin would make forays into the food-delivery business.

Japanese stocks fell, with investors assessing disappointing tech earnings and as the yen continued to strengthen. The Nikkei 225 declined 0.3% to 27,606.46 as of the market close in Tokyo, while the Topix Index was little changed at 1,983.97. Among the 2,163 stocks in the Topix, 1,138 rose, 886 fell and 139 were unchanged. SoftBank Group shares tumbled 5.1% after the company reported further steep losses in the latest quarter and CEO Masayoshi Son skipped the results call. Nintendo shares slid 7.5% after the electronics maker missed quarterly profit estimates and trimmed its full-year outlook as sales of its Switch game console missed targets. “The yen’s appreciation is offsetting the positive impact of higher U.S. stock prices,” said Tomo Kinoshita, global markets strategist at Invesco. “Earnings are also having a strong impact on the market, as the results seem to confirm that inventory and production adjustments are not completed yet.”

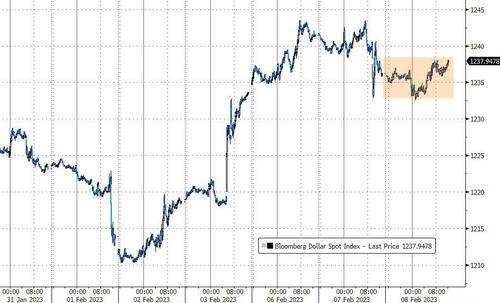

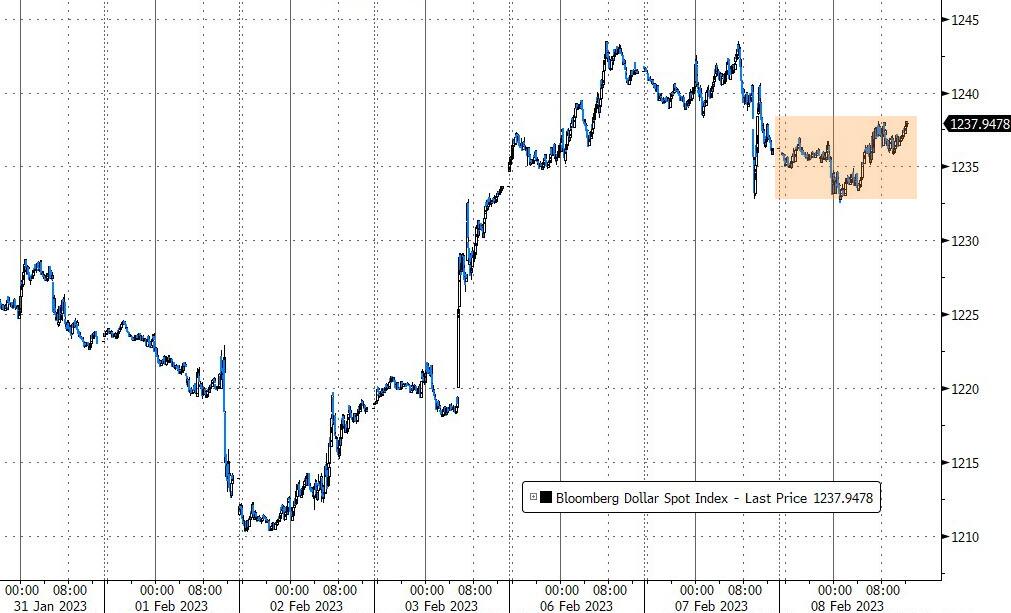

In FX, the Bloomberg Dollar Spot Index fell 0.2%, adding to Tuesday’s 0.4% drop, as the greenback weakened against all of its Group- of-10 peers. Scandinavian currencies and the pound were the best performers.

The euro rose to a day high of $1.0761 but remained within yesterday’s range. Bunds eased and the 2-10-year segment of the yield curve added around 2bps.

The pound continued to claw back some of the losses from the end of last week and briefly rose above $1.21. The gilt curve twist steepened modestly. The UK’s demand for workers accelerated for the first time in nine months in January, piling pressure on the Bank of England as it tries to tame inflation.

The Swedish krona rebounded a second day from a 14-year low versus the euro, while mixed data Wednesday could keep demand for straddles elevated in euro-krona ahead of the Riksbank monetary policy decision Thursday. Sweden’s housing market continued to seek a bottom at the start of the year, beset by falling activity after ten months of consecutive price declines

In rates, treasuries are richer across the curve, with gains led by intermediates, steepening the 5s30s spread by 1.5bp on the day and the US 10-year yield down 2bps. US 10-year yields are near middle of day’s range at 3.645% in the early US session, richer by 3bp on the day and outperforming bunds and gilts by 3.5bp and 1bp in the sector Core European markets are underperforming slightly as traders digest the European Central Bank decision Tuesday to introduce a new remuneration ceiling for deposits from May 1. The bund curve bear steepens with 2s10s widening 3.2bps. The US session focus is on the 10-year note auction, following Tuesday’s poor 3-year results. The treasury auction cycle resumes with a $35b 10-year sale at 1 p.m. in New York, and concludes with a $21b 30-year offering on Thursday; they follow a poor 3-year auction on Tuesday, which tailed by 4bp. WI 10-year at 3.625% is 5bp cheaper than January’s stop-out, which traded 0.5bp through the WI level.

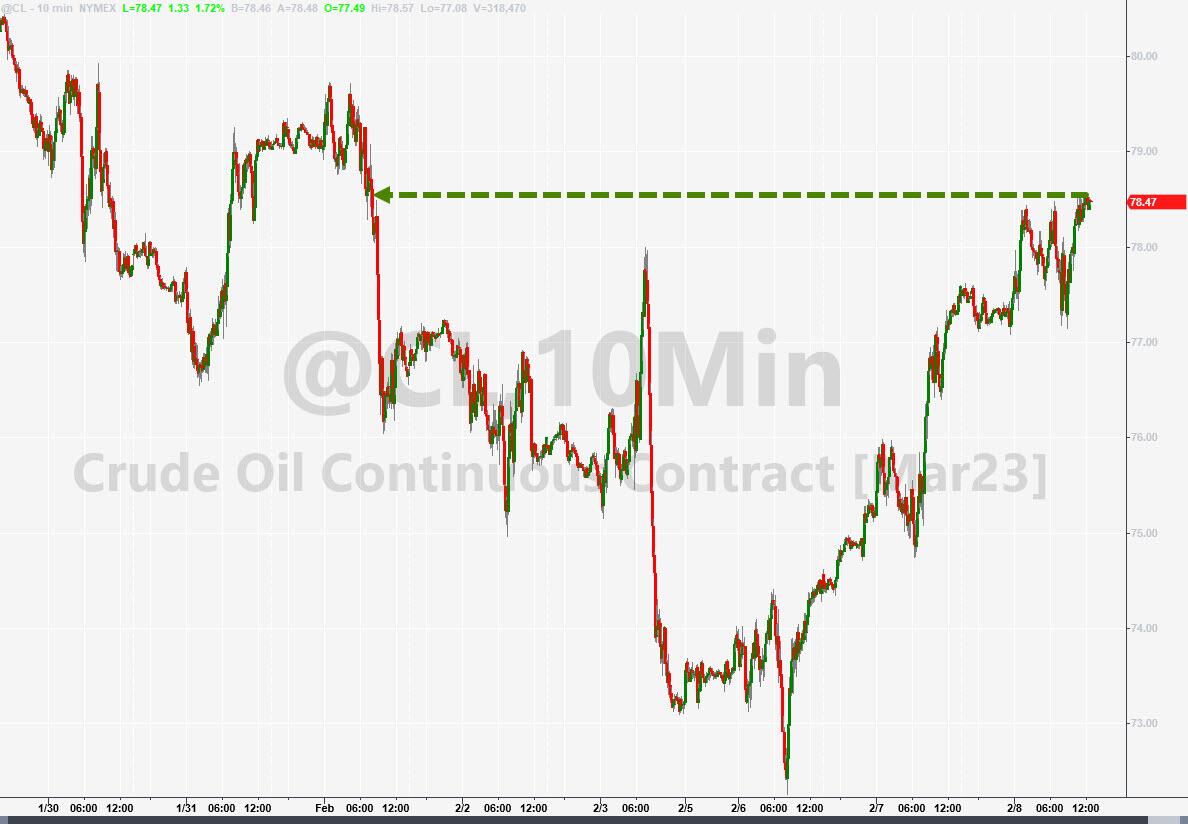

Crude futures advance with WTI adding 1.2% to trade near $78.10. Nat gas futures diverge once again while TotalEnergies writes that The tensions on European gas prices seen in 2022 are expected to continue into 2023, as the limited growth in global LNG production is supposed to meet both higher European LNG demand to replace Russian gas received in 2022 and higher Chinese LNG demand. Spot gold rises roughly 0.4% to trade near

Looking to the day ahead now, we’ll hear from several central bank speakers including the Fed’s Williams, Cook, Barr, Bostic, Kashkari and Waller, as well as the ECB’s Knot. Otherwise, data releases include Italian retail sales for December, and earnings releases include Disney and Uber.

Market Snapshot

S&P 500 futures down 0.3% to 4,164.75

STOXX Europe 600 up 0.8% to 461.83

MXAP up 0.6% to 167.43

MXAPJ up 0.7% to 546.28

Nikkei down 0.3% to 27,606.46

Topix little changed at 1,983.97

Hang Seng Index little changed at 21,283.52

Shanghai Composite down 0.5% to 3,232.11

Sensex up 0.6% to 60,663.61

Australia S&P/ASX 200 up 0.3% to 7,530.07

Kospi up 1.3% to 2,483.64

German 10Y yield little changed at 2.38%

Euro up 0.3% to $1.0755

Brent Futures up 1.1% to $84.64/bbl

Gold spot up 0.6% to $1,884.48

U.S. Dollar Index down 0.35% to 103.06

Top Overnight News from Bloomberg

High-frequency traders are often singled out as the culprits behind a lack of prices when markets get jumpy. But the activities of these controversial companies have gained a stamp of approval from the UK’s regulator, at least in currency markets

The BOJ’s negative-rate policy has kept short-term interest rates below zero since 2016, even as global peers shifted to hiking. But it also acts like a tax on yen funds, driving up local demand for foreign currencies to the point that there’s a premium on offer for what’s delivered via the foreign- exchange swap market

The BOJ Governor Haruhiko Kuroda is in the twilight of his 10-year tenure. His successor inherits a bond market that is larger than ever, but riddled with wild distortions. The lingering question for Japan is how the central bank can normalize policy

Romania may join Poland and other regional peers this week in holding interest rates steady as policy makers shift attention to risks posed by an economic slowdown even as inflation persists

China’s successful development shows there is another way to modernize, President Xi Jinping said, rejecting any need to “westernize” and doubling down on his goals of increased self reliance and improved social justice

China’s rapid reopening is having an unfortunate side effect for banks — a surge in funding costs to levels not seen in two years. A gauge of overnight borrowing costs climbed to the highest since 2021 on Wednesday, even as the People’s Bank of China pumped short-term cash into the financial system

India’s central bank slowed the pace of interest-rate increases while keeping the door open for further policy tightening to curb core inflation, an approach that aligns with the thinking of peers in the US and Australia. The central bank plans to allow lending and borrowing of government bonds as it seeks to deepen the nation’s $1 trillion debt market

Emerging-market investors were getting excited about a return to Egypt after last month’s devaluation of the pound. A surprise from the central bank has kept them away

Turkey President Recep Tayyip Erdogan is working on the assumption general elections will be held in Turkey three months from now despite twin earthquakes devastating much of the southeast this week

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were indecisive and failed to sustain the momentum from Wall St where markets whipsawed as attention centred on Fed Chair Powell before the major US indices eventually closed at session highs as Powell’s two-sided comments proved not to be as hawkish as some feared. ASX 200 was underpinned by strength in financials and with the mining-related industries benefitting from the rebound in underlying commodity prices. Nikkei 225 underperformed with sentiment in Japan pressured by weak earnings reports from the likes of SoftBank, Sharp and Nintendo. Hang Seng and Shanghai Comp. were indecisive amid lingering tensions from the spy balloon incident and after China denied a US request for a phone call between defence officials.

Top Asian News

Japan is arranging to relax border control measures for visitors from China as soon as this month and will end blanket testing for all travellers from China upon arrival, but will continue requiring a COVID test before departure from China, according to FNN.

New Zealand PM Hipkins said policy is to be focused on the cost of living and announced that the minimum wage will increase in line with CPI from April.

RBI hiked the Repurchase Rate by 25bps to 6.50% as expected through a 4-2 vote (prev. 5-1) and the MPC kept the policy stance of remaining focused on the withdrawal of accommodation through a 4-2 vote (prev. 4-2). RBI Governor Das stated further calibrated monetary policy action is warranted and that the situation remains fluid and uncertain, while he added that the stickiness of core inflation is a matter of concern and they need to see a decisive fall in inflation.

Beijing has asked students to wear masks at primary and middle schools, according to Bloomberg.

Japan may opt for milder chip-equipment curbs on China than the US despite agreeing on export curbs, according to a Japanese ruling party lawmaker cited by Reuters.

European bourses are firmer across the board, Euro Stoxx 50 +0.7%, taking advantage of the firmer Wall St. close and shrugging off indecisive APAC trade. Sectors are similarly bid with Energy outperforming given benchmark activity and post-Equinor, though upside is capped by TotalEnergies. Stateside, futures are in modest negative territory paring some of the post-Powell upside ahead of key speakers incl. Fed’s Williams. BIS’ Carstens says a re-think is needed on regulating big tech activities in the financial sector. Adding, it is time to consider tangible operations for direct regulation. Tesla (TSLA) China January deliveries 66.05k, +18% MM, via CPCA; adding, China sold 1.3mln passenger vehicles, -37.9% YY.

Top European News

NIESR cut 2023 UK GDP growth forecast to 0.2% from 0.7% and 2024 GDP to 1.0% from 1.7%, while it sees CPI averaging 8.3% in 2023 and 4.2% in 2024 vs. prev. forecast of 8.0% and 3.9%, respectively.

ECB says it will keep capital requirements steady this year. Click here for more detail. ECB’s Enria (supervisory board) says there is no generalised dissatisfaction with internal models, issues with some individual banks. Launched an initiative to simplify internal modes landscape

Vattenfall Operating Profit Rises Despite Big Trading Loss

Top Platinum Miner Says Payouts to Decline as Power Outages Hit

Ukraine Latest: Zelenskiy to Meet Sunak in London on Wednesday

Banco BPM Drops as Conservative Guidance Clouds Income Beat

Man United Surges After Daily Mail Report on Qatari Bid Plan

Fixed Income

EGBs remain underpressure but have lifted off of earlier 135.62 and 104.53 troughs in Bunds and Gilts, perhaps following the morning’s supply which was soft, though not as poor as the US 3yr.

Stateside, USTs have recuperated somewhat from Tuesday’s pressure ahead of numerous Fed speakers and a USD 35bln 10yr sale; yields are slightly softer with action much more pronounced at the short end.

Commodities

Crude benchmarks climb higher as Tuesday’s upside continues with multiple supportive factors for the complex; currently, the benchmarks are firmer by over 1.0%.

Nat gas futures diverge once again while TotalEnergies writes that “The tensions on European gas prices seen in 2022 are expected to continue into 2023, as the limited growth in global LNG production is supposed to meet both higher European LNG demand to replace Russian gas received in 2022 and higher Chinese LNG demand.”.

US Energy Inventory Data (bbls): Crude -2.2mln (exp. +2.5mln), Gasoline +5.3mln (exp. +1.3mln), Distillate +1.1mln (exp. +0.1mln), Cushing +0.2mln.

UK’s Unite union announced that a 48-hour strike is underway at BP (BP/ LN) Petrofac installations involving around 80 workers, according to Reuters.

Iranian official says OPEC is moving in the correct direction, sees oil prices increasing this year to circa. USD 100/bbl in H2 2023; OPEC+ likely to continue existing policy at the next gathering.

India’s Oil Minister says the OPEC SecGen has invited India to the next OPEC+ meeting.

Qatar set March Marine Crude OSP at +0.40/bbl vs Oman/Dubai; sets Land crude at +1.10/bbl vs Oman/Dubai, according to a document cited by Reuters; Iraq sets March Basrah Medium crude price to Asia at -1.10/bbl vs Oman/Dubai average; Europe OSP -6.95/bbl vs dated Brent, according to SOMO.

Activity at Peru’s major copper mines are at or near normal levels in spite of social unrest, according to data reviewed by Reuters; MMG’s Las Bambas mine elevated after last-minute supplies to avert the expected halt, but could still face production halt in the coming days as inputs are running out.

Spot gold is firmer, though off best levels as the DXY picks up from session lows below 103.00 and as such gold remains circa. USD 15/oz from USD 1900/oz at best.

LME aluminium lags and eyes USD 2,500/t to the downside following an exceptionally large warehouse build of 105.6k (vs prev. -2k).

FX

The USD continues to ease post-Powell though the DXY has lifted comfortably above 103.00 after briefly matching Tuesday’s 102.99 trough.

Amidst this, G10 peers are firmer across the board with GBP outperforming slightly and Cable incrementally above 1.21 courtesy of EUR/GBP action amid slightly tamer action for the single currency.

AUD is seemingly experiencing a modest second-wind post-RBA and ahead of Friday’s SOMP; AUD/USD tested 0.70 and NZD/USD at the upper-end of 0.6310-0.6348 parameters.

SEK is relatively contained despite mixed data ahead of the Riksbank while EUR/NOK has tested 11.00 to the downside at best.

PBoC set USD/CNY mid-point at 6.7752 vs exp. 6.7758 (prev. 6.7967)

BoC Governor Macklem flagged the debt load in explaining the early rate pause and said that rate hikes have hit homeowners hard, while the BoC needs time to gauge how households and businesses adapt to higher rates before making further moves. Macklem also commented that they cannot put it on a calendar and do not know how long the duration of the rate pause will be, according to Bloomberg.

Geopolitics

US Pentagon said China declined a US request for a phone call between the Pentagon chief and China’s defence minister, according to Reuters.

Russia says it is not satisfied with the progress of unblocking Russian exports as part of the Ukrainian grain deal and the EU is not fulfilling its promises on this, via Tass citing a diplomat.

Russian Deputy PM Novak says Russia will decide countermeasures to the EU sanctions by March 1; Russian oil output in February has been in line with January levels; January production stood at 9.8-9.9mln BPD.

Russia Foreign Ministry says US demands to restart nuclear arms treaty inspections are cynical because it is assisting Kyiv in striking Russian targets; adds, the US’ actions, in respect to Russia, are fraught with real risk of direct confrontation between the two nuclear states, according to Ria

UK PM Sunak says he will offer to provide Ukraine with longer-range capabilities. Note, Ukrainian President Zelensky is visiting the UK today and will be meeting with PM Sunak.

US Event Calendar

07:00: Feb. MBA Mortgage Applications, prior -9.0%

10:00: Dec. Wholesale Trade Sales MoM, est. -0.2%, prior -0.6%

10:00: Dec. Wholesale Inventories MoM, est. 0.1%, prior 0.1%

Fed speakers

09:15: Fed’s Williams Interviewed at WSJ Live Event

09:30: Fed’s Cook Takes Part in a Discussion in Washington

10:00: Fed’s Barr and Bostic Speak to Students in Mississippi

12:30: Fed’s Kashkari Speaks at Boston Economic Club

13:45: Fed’s Waller Discusses the Economic Outlook

DB’s Jim Reid concludes the overnight wrap

Morning from Paris where I’m staying at a hotel I last stayed in 3.5 years ago. All I can say is that the room service menu has soared in price since I was last here. As such after a cancelled dinner and a long day of no food I roamed the back streets of the Arc De Triomphe searching for something suitable. I gambled on a bagel shop. I got it back to my room and it was disgusting. The glamour of international business travel. I have a client breakfast, lunch and dinner today so I’m expecting much better!

Yesterday was all about the wait for Powell’s speech at the Economic Club of Washington, and then the interpretation of it. It’s a bit of a generalisation, and my views were scarred by 2 horrible bagels, but I would say the more the FOMC press conference went on last Wednesday the more dovish Powell sounded. However, last night’s speech was a little bit of the reverse. When all was said and done though, relative to pre-Powell levels terminal didn’t move much, rates moved a bit higher and equities saw an impressive climb (+1.29%). There was a fair bit of vol during the speech with the S&P trading in a wide 1.8pp range, while 10yr Treasuries traded in a 6bps range. The key market theme was that equities seemed to breathe a big sigh of relief that he didn’t choose this moment to notably change the script post payrolls. There was some fear that he would.

To review his comments, Powell continued to repeat last week’s FOMC mantra that further rate hikes were needed in order to rein in inflation and that policy would have to stay tight for some time. While directly addressing last week’s report he said it “shows you why we think this will be a process that takes a significant period of time … the labour market is extraordinarily strong”. He then spent a good deal of time referencing back to his comments from the FOMC press conference. These opening remarks caused the market to initially turn risk on with the S&P up 1.2% and 2yr yields moving -9bps lower after the first 30 minutes of the interview. However, Powell then pointed out that if the labour market remains strong “it may well be the case that we have to do more.” This seemed to signal to markets that a further 50bps of hikes is the floor for fed funds with risks to the upside on labour or inflation data coming out higher than expected. This caused a quick reversal with the S&P 500 dropping nearly -2% and 2yr yields climbing +8bps in the span of a half hour.

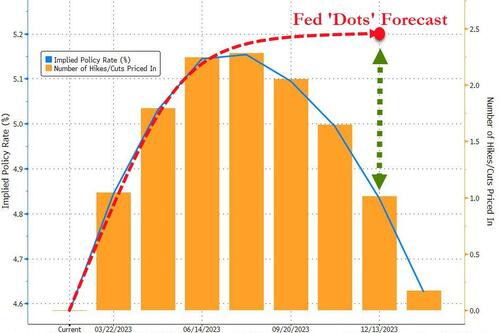

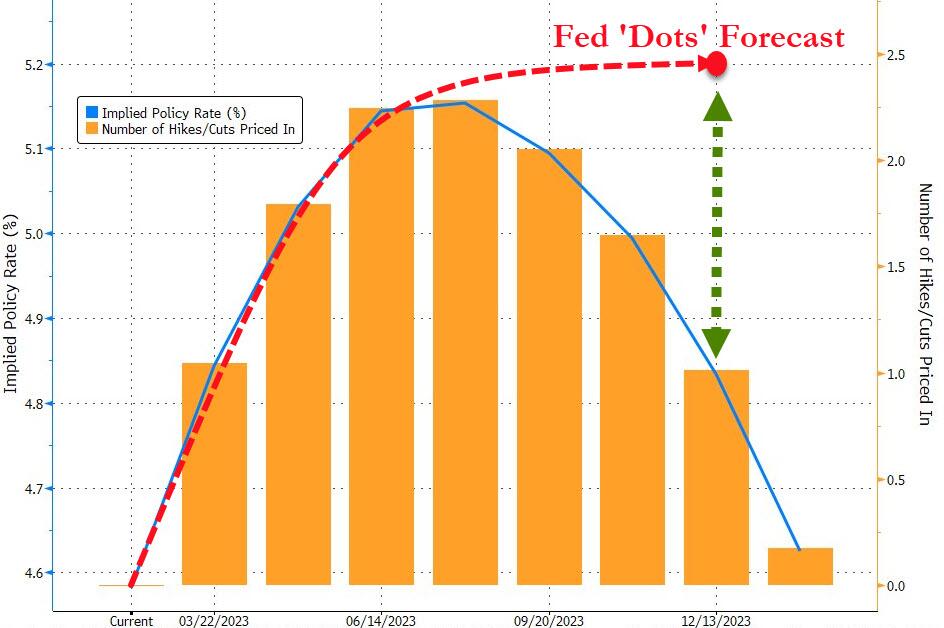

However, once Powell had wrapped up, both moves were retraced throughout the rest of the US afternoon with the S&P finishing near the highs of the day, and higher than during the peak of Powell’s interview, at +1.29%. Meanwhile the policy-sensitive 2yr yield sold off with yields finishing flat at 4.46% and 10yr yields +3.4bps higher at 3.67% (although -2.2bps lower this morning in Asia). Even with Powell raising the spectre of a higher terminal rate than the Fed had previously signalled, fed future pricing actually dropped ever so slightly with the July meeting closing at an implied fed funds rate of 5.153%, down 0.05bps. We’ve actually dipped -2.5bps this morning.

Digging into the market reaction more, it was a very risk-on rally with 70% of the S&P 500 higher on the day, with technology the leader once again. Semiconductors (+3.2%), Media (+3.1%), Energy (+3.1%) and Software (+2.6%) were the best performing sectors, while the only laggards were defensives like Telecoms (-1.2%), Household Goods (-0.7%) and Food & Beverage (-0.5%). The VIX volatility index finished near the lows of the day at 18.6pts.

There was also a larger risk on move in commodities with Brent crude oil up +3.33% to $83.69/bbl and WTI up +4.09% to $77.37/bbl following news that Saudi Aramco is increasing the prices of fuel shipments to Asia starting in March on the back of heightened demand. The move took another leg higher following the general risk-on sentiment following Powell’s remarks. The rise in oil and copper (+1.13%) due to China’s reopening meant that the Bloomberg Commodity index (+1.35%) rose by its largest amount since December 13.

Before Powell, markets had extended the hawkish shift seen since payrolls. First, the other central bankers we heard from continued to lean towards further rate hikes, with Minneapolis Fed President Kashkari saying that “right now I’m still at around 5.4%” on where rates needed to go. That would imply the Fed needs to do another 25bp move on top of current market pricing. Separately, Bundesbank President Nagel said that “more significant rate increases will be needed”, and pushed back on an imminent pause in saying that “I don’t see that our work is done with this rate hike in March.”

On top of those remarks, various pieces of data signalled that the battle against inflation was far from over. For instance, Manheim’s index of US used-vehicle prices was up by +2.5% in January, marking its strongest monthly increase since November 2021. Bear in mind that used cars and trucks make up over 4% of core CPI, and we’ve seen 6 consecutive monthly declines in that component, so any reversal there would help push up the overall numbers. Back in Europe, we also had the ECB’s latest Consumer Expectations Survey for December. That showed 12-month expectations for inflation remaining unchanged at 5.0%, and 3yr expectations moved back up a tenth to 3.0%, so still a full point above their target even at a medium-term horizon. And finally on the growth side, the recent strong data in the US saw the Atlanta Fed’s GDPNow tracker increase its Q1 growth estimate to an annualised +2.1%, up from +0.7% previously. A month ago many had a flat or negative quarter pencilled in for Q1.

Ahead of Powell, the more hawkish newsflow had led European sovereigns to lose ground for a 3rd consecutive day, with yields on 10yr bunds (+5.3bps), OATs (+4.7bps) and BTPs (+7.1bps) all moving higher. Those movements accelerated into the close after we heard that the ECB were adjusting the remuneration on government deposits, which would now have a ceiling of the euro short-term rate (€STR) minus 20bps. Previously, it had been whichever was lower of the deposit rate or the €STR. The aim is to encourage an orderly reduction in these deposits, which they said is “in order to minimise the risk of adverse effects on market functioning and ensure the smooth transmission of monetary policy”. Otherwise, European equities were pretty subdued yesterday, with the DAX (-0.16%) and the CAC 40 (-0.07%) posting small losses, whilst the STOXX 600 (+0.23%) saw a modest advance. This was all pre-Powell.

Asian equity markets are mixed overnight. As I type, the KOSPI (+1.39%) is leading gains with the Hang Seng also trading in positive territory. Meanwhile, the Nikkei (-0.43%) is lagging its peers following disappointing quarterly earnings from Nintendo, Softbank and Sharp Corp. Elsewhere, Chinese stocks are muted with the CSI (+0.01%) and the Shanghai Composite (-0.05%) fluctuating between gains and losses.

Outside of Asia, US stock futures are wavering with contracts tied the S&P 500 (-0.03%) fractionally lower and those on the NASDAQ 100 (+0.06%) just above flat.

President Biden delivered his State of the Union address last night, in which he promised that the US would not hit the debt ceiling and default on its debts. As expected President Biden called for increased taxes on stock buybacks as well as billionaires, while also touting efforts to near-shore American manufacturing that is aligned to critical supply chains. It probably wasn’t the most dramatic State of the Union address which might be partly due to US political gridlock.

Finally back to yesterday and it was another quiet day on the data front, but the US trade deficit came in at $67.4bn in December (vs. $68.5bn expected). Elsewhere, German industrial production for December underwhelmed with a -3.1% contraction (vs. -0.8% expected).

To the day ahead now, and we’ll hear from several central bank speakers including the Fed’s Williams, Cook, Barr, Bostic, Kashkari and Waller, as well as the ECB’s Knot. Otherwise, data releases include Italian retail sales for December, and earnings releases include Disney and Uber.

end

AND NOW NEWSQUAWK (EUROPE/REPORT)

US futures ease post-Powell and ahead of key speakers incl. Fed’s Williams – Newsquawk US Market Open

WEDNESDAY, FEB 08, 2023 – 06:26 AM

European bourses are firmer across the board, Euro Stoxx 50 +0.7%, taking advantage of the Wall St. close and shrugging off indecisive APAC trade.

Stateside, futures are in modest negative territory paring some of the post-Powell upside ahead of key speakers incl. Fed’s Williams.

The USD continues to ease post-Powell though the DXY has lifted comfortably above 103.00 after briefly matching Tuesday’s 102.99 trough.

EGBs remain under pressure but have lifted off of initial 135.62 and 104.53 lows in Bunds and Gilts, perhaps following the morning’s supply which was soft, though not as poor as the US 3yr.

Crude benchmarks climb higher as Tuesday’s upside continues with multiple supportive factors for the complex; currently, the benchmarks are firmer by over 1.0%.

Looking ahead, highlights include BoC Minutes, Speeches from Fed’s Williams, Cook, Barr, Bostic, Kashkari & Waller, Supply from the US, Earnings from CVS Health, Disney, Uber & Goodyear Tire.

Or why not try Newsquawk’s squawk box free for 7 days?

EUROPEAN TRADE

EQUITIES

European bourses are firmer across the board, Euro Stoxx 50 +0.7%, taking advantage of the firmer Wall St. close and shrugging off indecisive APAC trade.

Sectors are similarly bid with Energy outperforming given benchmark activity and post-Equinor, though upside is capped by TotalEnergies.

Stateside, futures are in modest negative territory paring some of the post-Powell upside ahead of key speakers incl. Fed’s Williams.

BIS’ Carstens says a re-think is needed on regulating big tech activities in the financial sector. Adding, it is time to consider tangible operations for direct regulation.

Tesla (TSLA) China January deliveries 66.05k, +18% MM, via CPCA; adding, China sold 1.3mln passenger vehicles, -37.9% YY.

The USD continues to ease post-Powell though the DXY has lifted comfortably above 103.00 after briefly matching Tuesday’s 102.99 trough.

Amidst this, G10 peers are firmer across the board with GBP outperforming slightly and Cable incrementally above 1.21 courtesy of EUR/GBP action amid slightly tamer action for the single currency.

AUD is seemingly experiencing a modest second-wind post-RBA and ahead of Friday’s SOMP; AUD/USD tested 0.70 and NZD/USD at the upper-end of 0.6310-0.6348 parameters.

SEK is relatively contained despite mixed data ahead of the Riksbank while EUR/NOK has tested 11.00 to the downside at best.

PBoC set USD/CNY mid-point at 6.7752 vs exp. 6.7758 (prev. 6.7967)

BoC Governor Macklem flagged the debt load in explaining the early rate pause and said that rate hikes have hit homeowners hard, while the BoC needs time to gauge how households and businesses adapt to higher rates before making further moves. Macklem also commented that they cannot put it on a calendar and do not know how long the duration of the rate pause will be, according to Bloomberg.

EGBs remain underpressure but have lifted off of earlier 135.62 and 104.53 troughs in Bunds and Gilts, perhaps following the morning’s supply which was soft, though not as poor as the US 3yr.

Stateside, USTs have recuperated somewhat from Tuesday’s pressure ahead of numerous Fed speakers and a USD 35bln 10yr sale; yields are slightly softer with action much more pronounced at the short end.

Crude benchmarks climb higher as Tuesday’s upside continues with multiple supportive factors for the complex; currently, the benchmarks are firmer by over 1.0%.

Nat gas futures diverge once again while TotalEnergies writes that “The tensions on European gas prices seen in 2022 are expected to continue into 2023, as the limited growth in global LNG production is supposed to meet both higher European LNG demand to replace Russian gas received in 2022 and higher Chinese LNG demand.”.

US Energy Inventory Data (bbls): Crude -2.2mln (exp. +2.5mln), Gasoline +5.3mln (exp. +1.3mln), Distillate +1.1mln (exp. +0.1mln), Cushing +0.2mln.

UK’s Unite union announced that a 48-hour strike is underway at BP (BP/ LN) Petrofac installations involving around 80 workers, according to Reuters.

Iranian official says OPEC is moving in the correct direction, sees oil prices increasing this year to circa. USD 100/bbl in H2 2023; OPEC+ likely to continue existing policy at the next gathering.

India’s Oil Minister says the OPEC SecGen has invited India to the next OPEC+ meeting.

Qatar set March Marine Crude OSP at +0.40/bbl vs Oman/Dubai; sets Land crude at +1.10/bbl vs Oman/Dubai, according to a document cited by Reuters; Iraq sets March Basrah Medium crude price to Asia at -1.10/bbl vs Oman/Dubai average; Europe OSP -6.95/bbl vs dated Brent, according to SOMO.

Activity at Peru’s major copper mines are at or near normal levels in spite of social unrest, according to data reviewed by Reuters; MMG’s Las Bambas mine elevated after last-minute supplies to avert the expected halt, but could still face production halt in the coming days as inputs are running out.

Spot gold is firmer, though off best levels as the DXY picks up from session lows below 103.00 and as such gold remains circa. USD 15/oz from USD 1900/oz at best.

LME aluminium lags and eyes USD 2,500/t to the downside following an exceptionally large warehouse build of 105.6k (vs prev. -2k).

NIESR cut 2023 UK GDP growth forecast to 0.2% from 0.7% and 2024 GDP to 1.0% from 1.7%, while it sees CPI averaging 8.3% in 2023 and 4.2% in 2024 vs. prev. forecast of 8.0% and 3.9%, respectively.

ECB says it will keep capital requirements steady this year. Click here for more detail. ECB’s Enria (supervisory board) says there is no generalised dissatisfaction with internal models, issues with some individual banks. Launched an initiative to simplify internal modes landscape

NOTABLE US HEADLINES

US President Biden said he is announcing new standards to require all construction materials used in federal infrastructure projects to be made in America and said the tax system is unfair, while he called for Congress to pass a minimum billionaire tax and proposed to quadruple the tax on corporate stock buybacks. President Biden noted he is committed to working with China where it can advance American interests and benefit the world but if China threatens US sovereignty, the US will act to protect the country and also said the US is in the strongest position in decades to compete.

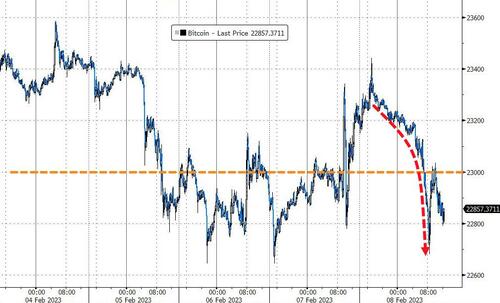

Bitcoin is little changed overall and resides towards the mid-point of a narrow sub-400 band with fresh developments limited.

GEOPOLITICS

US Pentagon said China declined a US request for a phone call between the Pentagon chief and China’s defence minister, according to Reuters.

Russia says it is not satisfied with the progress of unblocking Russian exports as part of the Ukrainian grain deal and the EU is not fulfilling its promises on this, via Tass citing a diplomat.

Russian Deputy PM Novak says Russia will decide countermeasures to the EU sanctions by March 1; Russian oil output in February has been in line with January levels; January production stood at 9.8-9.9mln BPD.

Russia Foreign Ministry says US demands to restart nuclear arms treaty inspections are cynical because it is assisting Kyiv in striking Russian targets; adds, the US’ actions, in respect to Russia, are fraught with real risk of direct confrontation between the two nuclear states, according to Ria

UK PM Sunak says he will offer to provide Ukraine with longer-range capabilities. Note, Ukrainian President Zelensky is visiting the UK today and will be meeting with PM Sunak.

APAC TRADE

APAC stocks were indecisive and failed to sustain the momentum from Wall St where markets whipsawed as attention centred on Fed Chair Powell before the major US indices eventually closed at session highs as Powell’s two-sided comments proved not to be as hawkish as some feared.

ASX 200 was underpinned by strength in financials and with the mining-related industries benefitting from the rebound in underlying commodity prices.

Nikkei 225 underperformed with sentiment in Japan pressured by weak earnings reports from the likes of SoftBank, Sharp and Nintendo.

Hang Seng and Shanghai Comp. were indecisive amid lingering tensions from the spy balloon incident and after China denied a US request for a phone call between defence officials.

NOTABLE ASIA-PAC HEADLINES

Japan is arranging to relax border control measures for visitors from China as soon as this month and will end blanket testing for all travellers from China upon arrival, but will continue requiring a COVID test before departure from China, according to FNN.

New Zealand PM Hipkins said policy is to be focused on the cost of living and announced that the minimum wage will increase in line with CPI from April.

RBI hiked the Repurchase Rate by 25bps to 6.50% as expected through a 4-2 vote (prev. 5-1) and the MPC kept the policy stance of remaining focused on the withdrawal of accommodation through a 4-2 vote (prev. 4-2). RBI Governor Das stated further calibrated monetary policy action is warranted and that the situation remains fluid and uncertain, while he added that the stickiness of core inflation is a matter of concern and they need to see a decisive fall in inflation.

Beijing has asked students to wear masks at primary and middle schools, according to Bloomberg.

Japan may opt for milder chip-equipment curbs on China than the US despite agreeing on export curbs, according to a Japanese ruling party lawmaker cited by Reuters.

1.c WEDNESDAY/ TUESDAY NIGHT

SHANGHAI CLOSED DOWN 15.99 PTS OR .49% //Hang Seng CLOSED DOWN 15.18 PTS OR 0.07% /The Nikkei closed DOWN 79.01 PTS OR 0.29% //Australia’s all ordinaries CLOSED UP .36% /Chinese yuan (ONSHORE) closed UP 6.7864 //OFFSHORE CHINESE YUAN UP TO 6.7937// /Oil UP TO 77.90 dollars per barrel for WTI and BRENT AT 84.21 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

2 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA

2B JAPAN

JAPAN/

Japan has a demographic problem as Japanese women are having 1.3 children instead of what is needed 2.1

This forces Japan to reach out to foreign workers and now this category reaches a record high!

(zerohedge)

Number Of Foreign Workers In Japan Reaches Record High

TUESDAY, FEB 07, 2023 – 09:30 PM

The number of foreigners working in Japan has reached a new high of almost 1.7 million.

As Statista’s Katharina Buchholz reports, after years of slow growth in the number of foreign workers admitted into the country, Japan has increased its efforts to attract them in the past couple of years.