February 14+++a//2023 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSED: UP $1.40 at $1854.90

SILVER PRICE CLOSED: DOWN $0.01 to $21.87

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1864.20

Silver ACCESS CLOSE: 22.01

Bitcoin morning price:, 21,872 UP 127 Dollars

Bitcoin: afternoon price: $22,214 UP 342 dollars

Platinum price closing $938.40 DOWN $20.30

Palladium price; closing 1503.15 UP 68.00

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,474.61 UP $1.98 CDN dollars per oz

BRITISH GOLD: 1523,63 DOWN 2.51 pounds per oz

EURO GOLD: 1727.60 DOWN 3.63 euros per oz

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,851.900000000 USD

INTENT DATE: 02/13/2023 DELIVERY DATE: 02/15/2023

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 6

104 C MIZUHO 3

118 C MACQUARIE FUT 140

132 C SG AMERICAS 5

323 C HSBC 9

363 H WELLS FARGO SEC 273

435 H SCOTIA CAPITAL 101

624 H BOFA SECURITIES 90

657 C MORGAN STANLEY 18

661 C JP MORGAN 51 383

686 C STONEX FINANCIA 1

709 C BARCLAYS 2

737 C ADVANTAGE 1

800 C MAREX SPEC 3 13

880 C CITIGROUP 33

905 C ADM 4

TOTAL: 568 568

MONTH TO DATE: 13,581

JPMORGAN STOPPED 383/568

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR FEB/2023. CONTRACT: 568 NOTICES FOR 56,800 OZ or 1.7667 TONNES

total notices so far: 13,581 contracts for 1,358,100 oz (42.243 tonnes)

SILVER NOTICES: 53 NOTICE(S) FILED FOR 265,000 OZ/

total number of notices filed so far this month :809 for 4,045,000 oz

END

GLD

WITH GOLD UP $1.40

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

//NO CHANGES IN GOLD INVENTORY AT THE GLD////

INVENTORY RESTS AT 920.79TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 1 CENT

AT THE SLV// :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 460,000 OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 483.302. MILLION OZ (CORRECTED

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUMONGOUS SIZED 1807 CONTRACTS TO 133,089 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE HUGE GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.14 LOSS SILVER PRICING AT THE COMEX ON MONDAY. FOR THE TWO MONTHS, OUR BANKERS HAVE RETURNED TO BEING NET SHORT AND THUS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.14. BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD AN ATMOSPHERIC SIZED GAIN ON OUR TWO EXCHANGES OF 2729 CONTRACTS. AS WELL, WE HAD 0 NOTICES FOR EXCHANGE FOR RISK TRANSFER (0.0 MILLION OZ. ) AS THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1.775 MILLION OZ. WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 650 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 0.540. MILLION OZ FOLLOWED BY TODAY’S 265,000 OZ QUEUE JUMP OZ// NEW TOTALS STANDING = 4.155 MILLION OZ + 1.775 MILLION OF EXCHANGE FOR RISK//TOTAL STANDING 5.93 MILLION OZ//// V) HUGE SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -272

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB:

TOTAL CONTRACTS for 10 days, total 9319 contracts: OR 46.59 MILLION OZ . (932 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 46.59 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 46.59/ MILLION OZ/INITIAL//

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1807 DESPITE OUR $0.14 LOSS IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 650 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 0.54 MILLION OZ FOLLOWED BY TODAY’S 265,0000 OZ QUEUE JUMP= NEW STANDING: 4.115 MILLION OZ + 1.775 MILLION OZ EXCHANGE FOR RISK://NEW STANDING REMAINS AT 5.93 MILLION OZ .. WE HAVE AN ATMOSPHERIC SIZED GAIN OF 2079 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE LOSS IN PRICE//

WE HAD 53 NOTICE(S) FILED TODAY FOR 265,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2778 CONTRACTS TO 427,278 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 3153 CONTRACTS.

.

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 2778 CONTRACTS) WITH OUR $9.90 LOSS IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 41.601 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE. JUMP OF 49,200 OZ //NEW STANDING: 44.628 TONNES//(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). TONNES

YET ALL OF..THIS HAPPENED WITH OUR $9.90 LOSS IN PRICE WITH RESPECT TO MONDAY’S TRADING

WE HAD A FAIR SIZED LOSS OF 1428 OI CONTRACTS (4.4416 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1350 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 427,278

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1428 CONTRACTS WITH 2778 CONTRACTS DECREASED AT THE COMEX AND 1350 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1428 CONTRACTS OR 4.4416 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1350 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2778) TOTAL LOSS IN THE TWO EXCHANGES 1428 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 41.601 TONNES FOLLOWED BY TODAY’S 49,200 OZ QUEUE JUMP // ///3) SOME LONG LIQUIDATION //4) FAIR SIZED COMEX OPEN INTEREST LOSS// 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

29,384 CONTRACTS OR 2,938,400 OZ OR 91.396 TONNES 10 TRADING DAY(S) AND THUS AVERAGING: 2938 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAY(S) IN TONNES 91.396 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 93.396/3550 x 100% TONNES 2.62% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 93.396 TONNES/INITIAL (HEADING FOR ANOTHER STRONG ISSUANCE)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 1807 CONTRACTS OI TO 133,089 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 650 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 650 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 438 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2079 CONTRACTS AND ADD TO THE 650 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF 2457 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 12.283 MILLION OZ//

OCCURRED DESPITE OUR $0.14 LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 9.12 PTS OR 0.25% //Hang Seng CLOSED DOWN 50.66 PTS OR 0.24% /The Nikkei closed UP 175.48 PTS OR 0.64% //Australia’s all ordinaries CLOSED UP .18% /Chinese yuan (ONSHORE) closed UP 6.8182 //OFFSHORE CHINESE YUAN DOWN TO 6.8193// /Oil DOWN TO 79.05 dollars per barrel for WTI and BRENT AT 85.68 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2778 CONTRACTS UP TO 427,278 WITH OUR LOSS IN PRICE OF $9.90

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1350 EFP CONTRACTS WERE ISSUED: : APRIL 1350 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1350 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1428 CONTRACTS IN THAT 1350 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 2778 CONTRACTS..AND THIS FAIR SIZED LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR FALL IN PRICE OF $9.90. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG. TODAY THE SPEC LONGS WERE RINSED OUT!!

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (44.625)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes(TOTAL THIS YEAR 656.076 TONNES

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 44.625 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $9.90) //// AND WERE UNSUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD A FAIR SIZED LOSS OF 1428 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE LOST A TOTAL OI OF 4.4416 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (41.219 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 49,100 OZ OR 1.5272TONNES//NEW STANDING INCREASES TO 44.625 tonnes … ALL OF THIS WAS ACCOMPLISHED DESPITE OUR FALL IN PRICE TO THE TUNE OF $9.90.

WE HAD -3153 CONTRACTS COMEX TRADES ADDED TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 1428 CONTRACTS OR 142800 OZ OR 4.4416 TONNES

Estimated gold comex today 210,007// fair//

final gold volumes/yesterday 139,725/// poor

INITIAL STANDINGS FOR FEB 2023 COMEX GOLD //FEB 14//

//

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 86M128.797 oz JPMORGAN MANFRA Brinks Delaware 2600 kilobars JPM 42 KILOBARS Manfra 15 kilobars: Delaware . |

| Deposit to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 568 notice(s) 56800 OZ 1.7667 TONNES |

| No of oz to be served (notices) | 766 contracts 76,600 oz 2.3825 TONNES |

| Total monthly oz gold served (contracts) so far this month | 13,581 notices 1,358,100 42.243 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: NIL oz

customer withdrawals: 4

i) Out of Manfra 1350.342 oz (42 kilobar)

ii) Out of JPMorgan: 83,592.600oz (2600). kilobars

iii) out of Delaware; 482.265 oz (15kilobars)

iv) Out of Brinks 703.590 oz (real withdrawal/no kilobars)

total withdrawals: 86,128.797 oz

Adjustments; one

dealer to customer/JPMorgan: 8140.275 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEBRUARY.

For the front month of FEBRUARY we have an oi of 1334 contracts having gained 419 contracts. We had 81 notices

filed on Monday so we gained a huge 491 contract or an additional 49,100 oz will stand for metal at the comex

March LOST 221 contracts to stand at 1886.

April lost 4619 contracts down to 344,813

We had 568 notice(s) filed today for 56,800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 51 notices were issued from their client or customer account. The total of all issuance by all participants equate to 568 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 383 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB. /2023. contract month,

we take the total number of notices filed so far for the month (13,581 x 100 oz ), to which we add the difference between the open interest for the front month of (FEBRUARY 1334 CONTRACTS) minus the number of notices served upon today 568 x 100 oz per contract equals 1,434,700 OZ OR 44.625 TONNES the number of TONNES standing in this active month of January.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (13,581 x 100 oz+ 1334 OI for the front month minus the number of notices served upon today (568)x 100 oz} which equals 1,434,700 oz standing OR 44.625 TONNES in this active delivery month of FEBRUARY..

TOTAL COMEX GOLD STANDING: 44.625 TONNES. SO JUST LIKE LAST MONTH WE START WITH A LOW INITIAL AMOUNT OF GOLD STANDING BUT THIS WILL GROW AS THE MONTH PROCEEDS TO ITS CONCLUSION.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

we had one adjustment of 110,631.591 oz Brinks

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,812,504.867 OZ 56.37 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,026,034.754 OZ

TOTAL REGISTERED GOLD: 11,071,681.901 (344.37 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 10,944,353.253 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,259,177 OZ (REG GOLD- PLEDGED GOLD) 287.99 tonnes//

END

SILVER/COMEX

FEB 14/2023//INITIAL. SILVER CONTRACT FOR FEBRUARY

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,001,778.984 oz CNT HSBC Loomis Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 53 CONTRACT(S) (265,000 OZ) |

| No of oz to be served (notices) | 22 contracts (110,000 oz) |

| Total monthly oz silver served (contracts) | 809 contracts (4,045,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

Total deposits: nil oz

JPMorgan has a total silver weight: 146.939 million oz/290.143 million =50.65% of comex .//dropping fast

Comex withdrawals: 4

i)Out of CNT: 60,017.964 oz

iii) Out of HSBC 4994.700 oz

iii) Out of Loomis 236,627.210 oz

iv) Out of Manfra: 700,139.110 o

Total withdrawals; 1,001,778.984 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 31.784MILLION OZ (declining rapidly).TOTAL REG + ELIG. 290.143 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR FEB

silver open interest data:

FRONT MONTH OF FEB/2023 OI: 75 CONTRACTS HAVING GAINED 33 CONTRACT(S.).

WE HAD 20 NOTICES FILED ON MONDAY, SO WE GAINED 53 CONTRACTS OR AN ADDITIONAL 265,000 OZ OF SILVER WILL

STAND AT THE COMEX.

March LOST 3760 CONTRACTS DOWN TO 65,323 contracts

April GAINED 2 CONTRACTS TO STAND at 47.

TOTAL NUMBER OF NOTICES FILED FOR TODAY:53 for 265,000 oz

Comex volumes// est. volume today 81,564//strong

Comex volume: confirmed yesterday: 61,215 contracts ( fair)

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 809 x 5,000 oz = 4,045,000 oz

to which we add the difference between the open interest for the front month of FEB(75) and the number of notices served upon today 53 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2023 contract month:809 (notices served so far) x 5000 oz + OI for the front month of FEB (75 – number of notices served upon today 532) x 500 oz of silver standing for the FEB. contract month equates 4.155 million oz + PREVIOUS 1.775 MILLION OZ ( EXCHANGE FOR RISK) = 5.93MILLION OZ//(TOTAL OZ OF SILVER STANDING).

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 902.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

FEB 8/WITH GOLD UP $6.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 920.82 TONNES

FEB 7/WITH GOLD UP $5.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.92 TONNES

FEB 6/WITH GOLD UP $3.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.24 TONNES

FEB 3/WITH GOLD DOWN $52.55 TODAY: STRANGE: BIG CHANGES AGAIN IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 920.24 TONNES

FEB 2/WITH GOLD $10.95 TODAY: BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 918.50 TONNES

FEB 1/WITH GOLD DOWN $2.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 31/WITH GOLD UP $6.55 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 30/WITH GOLD DOWN $6.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 918.50 TONNES

JAN 27/WITH GOLD DOWN $0.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 919.37 TONNES

JAN 26/WITH GOLD DOWN $11.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 919.37 TONNES

JAN 25/WITH GOLD UP $7.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 917.34 TONNES

JAN 24/WITH GOLD UP $7.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 23/WITH GOLD UP $0.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.63 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 20/WITH GOLD UP $4.75 TODAY;BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 912.43 TONNES

JAN 19/WITH GOLD UP $16.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES INTO THE GLD///INVENTORY RESTS AT 910.98TONNES

JAN 18/WITH GOLD DOWN $1.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.9 TONNES FROM THE GLD////INVENTORY RESTS AT 909.24 TONNES

JAN 17/WITH GOLD DOWN $11.45 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.14 TONNES

JAN 13/WITH GOLD UP $22.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD///INVENTORY RESTS AT 912.14 TONNES

JAN 12/WITH GOLD UP $20.55 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 912.43 TONNES

JAN 11/WITH GOLD UP $1.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

GLD INVENTORY: 920.79 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 483.302 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

When They Say The US Government Has Never Defaulted, They’re Lying

MONDAY, FEB 13, 2023 – 08:35 PM

Authored by Michael Maharrey via SchiffGold.com,

The fake debt ceiling fight is on and the Biden administration has ratcheted up the scare tactics. One of its strategies is to make you think the world will collapse if the US defaults on its debt obligations. After all, the US always pays its bills on time — so we’re told.

A default would certainly be problematic. But despite what you’re being told, it’s not unprecedented. The US government has defaulted before.

I call this a fake debt ceiling fight because we all know how it will end. Congress will raise the debt ceiling. It may or may not come with some modest spending cuts. But we all know that any cuts will be superficial. Actual spending will keep going up. It always does.

But right now, we have to endure the dog and pony show as Republicans and Democrats haggle.

Republicans say they want spending cuts. (One has to wonder where this urgency was when the GOP controlled both houses of Congress and the White House, but that’s a discussion for another time.) Democrats say they won’t negotiate.

And here we are.

To fortify their position, the administration tells us that raising the debt ceiling is a matter of economic life and death. As I mentioned, the mantra is the US always pays its bills on time. As Mises Institute senior editor Ryan McMaken pointed out, as part of the strategy, Treasury Secretary Janet Yellen is parroting the oft-repeated claim that the US has never defaulted.

This sounds compelling. We all want our government to keep its word, right?

Of course, it doesn’t keep its word and this claim that the US has always paid its bills on time since 1789 is a lie. The US has defaulted more than once. And as McMaken points out, if you expand the idea of default to include inflating away the debt in real terms, default is even more common.

McMaken highlights the most notorious instance of US government defaults.

The following was originally published by the Mises Wire. Any opinions expressed are those of the author and do not necessarily reflect those of Peter Schiff or Schiff Gold.

In 1934, the United States defaulted on the fourth Liberty Bond. The contracts between debtor and creditor on these bonds was clear. The bonds were to be payable in gold. This presented a big problem for the US, which was facing big debts into the 1930s after the First World War. As described by John Chamberlain:

By the time Franklin Roosevelt entered office in 1933, the interest payments alone were draining the treasury of gold; and because the treasury had only $4.2 billion in gold it was obvious there would be no way to pay the principal when it became due in 1938, not to mention meet expenses and other debt obligations. These other debt obligations were substantial. Ever since the 1890s the Treasury had been gold short and had financed this deficit by making new bond issues to attract gold for paying the interest of previous issues. The result was that by 1933 the total debt was $22 billion and the amount of gold needed to pay even the interest on it was soon going to be insufficient.

So how did the US government deal with this? Chamberlain notes “Roosevelt decided to default on the whole of the domestically-held debt by refusing to redeem in gold to Americans.”

Moreover, with the Gold Reserve Act of 1934, Congress devalued the dollar from $20.67 per ounce to $35 per ounce—a reduction of 40 percent. Or, put another way, the amount of gold represented by a dollar was reduced to 59 percent of its former amount.

The US offered to pay its creditors in paper dollars, but only in new, devalued dollars.1 This constituted default on these Liberty Bonds, since, as the Supreme Court noted in Perry v. United States, Congress had “regulated the value of money so as to invalidate the obligations which the Government had theretofore issued in the exercise of the power to borrow money on the credit of the United States.”

This was clearly not a case of the US making good on its debt obligations, and to claim this is not default requires the sort of hairsplitting that only the most credulous Beltway insider could embrace.

Indeed, Carmen Reinhart and Kenneth Rogoff in their book This Time Is Different list this episode as a “default (by abrogation of the gold clause in 1933)” and as “de facto default.”

The Short Default of 1979

A second, less egregious case of default occurred in 1979. As Jason Zweig noted in 2011:

In April and May 1979, amid computer malfunctions, heavy demand from small investors and in the wake of Congressional debate over raising the debt ceiling, the U.S. failed to make timely payments on some $122 million in Treasury bills. The Treasury characterized the problem as a delay rather than as a default. While the error affected only a fraction of 1% of the U.S. debt, short-term interest rates—then around 9%—jumped 0.6 percentage point and the U.S. was promptly sued by bondholders for breach of contract.

Apparently, the United States sometimes does not pay its debts. While the 1979 default was relatively small, the 1934 default affected millions of Americans who had bought Liberty Bonds mistakenly thinking the government would make good on its promises. They were very wrong.

So, it is simply untrue that the US has never defaulted as Yellen claims. But this claim remains a useful tactic in sowing fear about “unprecedented” acts that would bring the entire US economy crashing down.

Default through Devaluation

But outright repudiation of contracts is only one way of defaulting on one’s obligations. Another is to deliberately devalue a nation’s currency—i.e., inflate it—so as to devalue the amount of debt a government owns in real terms.

And Zweig writes investors view this as a real form of avoiding one’s debt obligations:

Perhaps the biggest worry [among investors] isn’t default but … “financial repression.” In dozens of cases, governments have dug out from under burdensome debts not by refusing to pay interest but rather through other harsh means. For example, by keeping short-term interest rates below the level of inflation, a government can pay off its bondholders with cheapening money. Through regulations, it can compel banks and other financial firms to buy its own debt, much like geese being force-fed for foie gras. As a result, current yields and future inflation-adjusted returns on government bonds fall.

This strategy, Zweig concludes, “stiffs bond investors with negative returns after inflation.”

Zweig categorizes this as something separate from default, but Reinhart and Rogoff clearly consider it a form of de facto default. They write: “The combination of heightened financial repression with rises in inflation was an especially popular form of default from the 1960s to the early 1980s” (emphasis added).

(In the United States, a key event in this respect occurred in 1971 when Nixon closed the gold window. This was an explicit repudiation of the US’s obligation to repay dollars in gold to foreign states, and it also greatly enabled the US government in terms of financial repression and monetary inflation.)

Since the Great Recession, financial repression is popular again. This method of de facto default has enabled the federal government to take on massive amounts of new debt at rock-bottom interest rates. In real terms, the US government—or any government using this tactic—pays back its debts in devalued currency, essentially enabling the government to make good on the full extent of its debts. The cost to the public manifests in asset price inflation, goods price inflation, and a “hunt for yield” driven by a famine of income on safe assets. Americans of more modest means are those who suffer the most, and the result has been a widening gap of inequality in wealth.

It may very well be that a default could lead to significant economic and financial disruptions. But let’s stop pretending that a default is unprecedented or that the United States always pays its bills. It’s true that the US’s current debt machine, enabled through financial repression, is a form of slow-motion default. But that doesn’t make the US government any less of a deadbeat.

end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

No “North Star” for a Global Economy Drifting in Unsustainable Debt

Egon von Greyerz

February 14, 2023

In this latest conversation with Elijah Johnson of Liberty & Finance, Matterhorn Asset Management principal, Matthew Piepenburg, ties together the evolving themes of debt, credit market distress, currency failures and gold pricing.

Looking first at the UST market, Piepenburg argues that Treasuries matter simply because debt matters, and debt, by every metric, has passed the Rubicon of sustainability. The obvious distortions (and recessionary signposts) within the Treasury market are made clear by the inverted yield curve and the recent declines in the USD’s relative strength as measured by the DXY.

Piepenburg maintains that the West’s sanctions against Russia in general, and the US/Fed’s strong USD policy of 2022 in particular, have backfired with staggering panache. The net result has been a clear and steady process of de-dollarization as nations turn away from the USD and the UST for a host of described reasons.

The problem in US debt markets is only compounded by the hard fact that similar weaknesses exist globally. From the EU to Japan, the BRICS to DC, there is no “North Star” nation or economy to pull markets through what is in fact a simultaneous and global debt crisis.

As debt levels and yields rise, the only solution is now a familiar one: Monetizing those debts (and “controlling” those yields/rates) with inflationary mouse-click money from a local central bank. For now, however, the Fed is tightening rather than easing, and Piepenburg explains the ironic (and dis-inflationary) consequences (and eventual pivot) of an increasingly cornered Fed.

QT or QE, Piepenburg argues that the net result is either depression or inflation, and likely both: Stagflation. Stock markets, like the Fed, offer no place to hide, as current credit and equity markets are no longer supported by repressed rates and the old tailwinds of low-rate-driven stock buy-backs and debt roll-over tricks on Wall Street.

Piepenburg then turns to Gold’s out-performance in past, present and future contexts and gives special attention to objectively bogus inflation metrics and employment data as well as the true cost of allegedly “wining a war on inflation” with creative math while simultaneously seeking negative real rates.

Piepenburg carefully discusses gold price movements, OTC price manipulations, investor mindsets and the cases made for a strong and weak USD in 2023. In the end, Piepenburg argues that gold’s direction is heading North for the simple reason that global currencies, including the USD, are trending South.

please view:

3. Chris Powell of GATA provides to us very important physical commentaries//

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

5.IMPORTANT COMMENTARIES ON COMMODITIES: NICKEL +

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.8182

OFFSHORE YUAN: 6.8193

SHANGHAI CLOSED UP 9.12 PTS OR 0.28%

HANG SENG CLOSED UP 50.66 PTS OR 0.24%

2. Nikkei closed UP 175.48 PTS OR 0.64%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 102.83 Euro RISES TO 1.0759 UP 27 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.500!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 132.06/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.3735%***/Italian 10 Yr bond yield FALLS to 4.139%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.383…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.176//

3j Gold at $1859.25//silver at: 21.79 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 54/100 roubles/dollar; ROUBLE AT 73.30//

3m oil into the 79 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 132.42/10 YEAR YIELD AFTER BREAKING .54%, RISES TO .500% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9177– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9873 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.681% DOWN 4 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.758 DOWN 3 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,85…

GREAT BRITAIN/10 YEAR YIELD: 3.472% UP 7 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Rise Ahead Of Potential Valentine’s Day CPI Shocker

TUESDAY, FEB 14, 2023 – 08:00 AM

Happy Valentine’s day, which may end up being either a massacre or a happy ending, depending on what CPI numbers the BLS releases at 830am.

US stock futures were subdued in early Tuesday trading, creeping near session highs after moving higher in a narrow range as investors held off from making big bets ahead of inflation figures that will provide clues on the Federal Reserve’s policy outlook. Nasdaq 100 future rose 0.5% while S&P 500 futures edged 0.3% higher by 7:30 a.m. ET. Both underlying indexes surged more than 1% on Monday in the run up to the inflation data. Europe’s Stoxx50 advanced 0.5% in early European session. The yen jumped after Japan PM Kishida’s government confirmed that Kazuo Ueda would lead the BOJ, the pound climbed after UK jobs data and Treasuries rose a second day. Oil prices fell on a report that the Biden administration plans to sell more crude oil from the Strategic Petroleum Reserve. The dollar dropped and gold rose.

Among notable moves in premarket trading, ContextLogic surged as much as 24%, set to extend a jump on Monday following supportive comments from Citron Research about the ecommerce company. Palantir Technologies Inc. jumped after the data analysis company said it expects 2023 to be its first-ever profitable year. While analysts were positive about the profitability trend, they also noted the slowing pace of revenue growth. Here are some other notable premarket movers:

- Avis Budget shares gained as much as 3.3% in US premarket trading, after the vehicle rental company’s earnings exceeded analyst estimates, showing that demand for both commercial and leisure travel is holding up. Morgan Stanley analysts also pointed to a boost from lower vehicle depreciation costs.

- SolarEdge shares fall as much as 5.7% in US premarket trading, with analysts pointing to the solar equipment maker’s comments about a more cautious outlook for its US business. They expect the backlog of shipments to Europe to offset softening domestic demand.

- Fusion Pharmaceuticals climbed 39% in extended trading after the oncology company said it acquired a new drug application for an ongoing Phase 2 clinical trial evaluating 225Ac-PSMA I&T, which has the potential to treat prostate cancers.

- SkyWater Technology Inc. gained 9% in extended trading after the semiconductor manufacturer reported a narrower quarterly adjusted loss per share than analysts anticipated and revenue that topped expectations.

- Amkor Technology shares declined in extended trading on Monday after the semiconductor manufacturing company reported its fourth-quarter results and gave a forecast. The company reported earnings of 67 cents per share, compared with the consensus estimate of 70 cents.

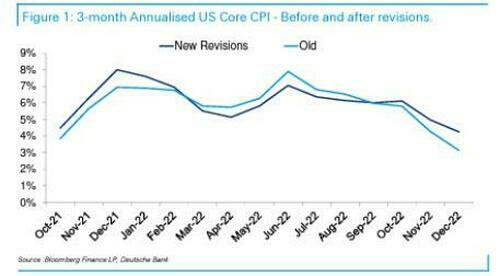

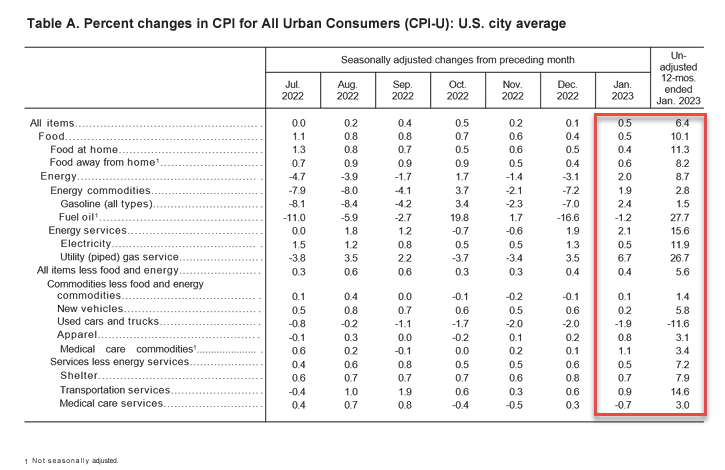

After sinking into a bear market last year, US stocks have rallied sharply in 2023 as investors bet that a cooling in inflation would prompt the Fed to slow the pace of rate hikes. Still, gains have wavered in recent days and data due later today is expected to show costs rising briskly from the prior month, suggesting the path to easing price pressures remains bumpy. That’s why, as discussed yesterday (see full preview here), all eyes will be on the crucial US inflation data at 8:30 am. Consumer prices probably rose 0.5%, the most in three months, while core prices may have advanced 0.4%. The annual rate may have slowed for a seventh month to 6.2%. Here is a quick recap of what to expect courtesy of DB’s Jim Reid:

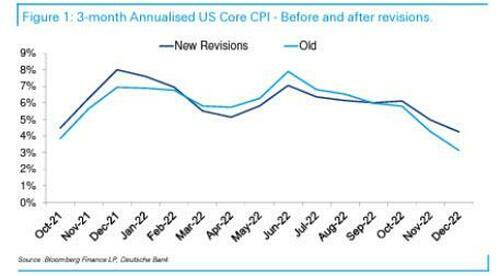

What better to get you in the mood for love than learning how quickly prices are rising in today’s highly anticipated US CPI print. Everything in the last few weeks has pointed to near-term upward pressure on US inflation in the early part of this year even if it eventually falls more sharply later in the year. Will markets and the Fed look through this if it happens? That’s the big question. The good news is that the market has been shaken out of its immaculate disinflation view in the last 7-8 business days with 10yr UST, Terminal (July) and Dec ’23 Fed Futures contracts up c.36bps, c.40bps and c.60bps, respectively, from its intra-day lows on February 2nd after what was interpreted as a dovish FOMC. Since then, we’ve had a very strong payrolls, the highest used car price growth for 14 months, and revisions to core CPI that showed a less aggressive disinflation path than originally reported. On the latter see more in my CoTD yesterday (link here) but 3 month annualised core CPI is now running at 4.25% rather than the 3.14% the market had imagined before Friday’s revisions.

Today’s number is also the first to see new expenditure weights that lifts OER’s importance. Given OER is expected to stay strong in the near-term before falling later in the year, this could push near-term inflation higher along with a few other things highlighted in the “The rise before the fall” chartbook from our economists last week. However, the market should be better prepared for this now that it’s more widely recognised.

In other words, expect fireworks in markets after that report as investors immediately asses what it means for the Fed’s future policy path. The stakes are even higher as, for the first time in a long time, stock and bond markets are flashing divergent signals on the economy and future Federal Reserve policy: bond markets have been cautious while stocks have been less worried. Today’s report will go a long way in determining which one is right. In addition to the inflation data, the US also reports real wages data for January. There’s also a run of Fed speakers to keep traders busy after the release, with Thomas Barkin, Lorie Logan, Patrick Harker and John Williams all appearing (more on the US calendar below).

“It feels like markets have been rather listless this week so far as we await the CPI number,” said James Athey, investment director at Abrdn. “Certainly in recent days the whisper has been getting higher and it’s rational to think that the reaction to a miss will be bigger – particularly given the recent rise in yields.”

Late on Monday, we got confirmation to another long-running rumor, namely that Joe Biden has decided to name Federal Reserve Vice Chair Lael Brainard as his top economic adviser, with an announcement coming as soon as Tuesday, people familiar with the matter said. The president’s selection of Brainard to replace outgoing NEC Director Brian Deese places her alongside another high-profile former Fed official, Treasury Secretary Janet Yellen, as a crucial player on economic policy amid the continuing battle with inflation and as Biden prepares for a likely reelection campaign.

Meanwhile, Japanese Prime Minister Fumio Kishida’s government nominated Kazuo Ueda to helm the Bank of Japan on Tuesday. Eisuke Sakakibara, nicknamed “Mr. Yen” for his ability to influence the currency during his tenure as Japan’s vice finance minister from 1997-1999, says that may pave the way for a rate hike by the fourth quarter.

The first quarterly decline in corporate earnings since 2020 has also hit risk demand this month. JPMorgan strategist Marko Kolanovic said on Monday he was “turning more defensive” on stocks as they don’t yet reflect a recession. A Bank of America survey also showed most investors still believe equities are seeing a bear market rally even as they turn more optimistic about global growth.

European stocks rose ahead of the CPI data. The Stoxx 600 added 0.5%, led by outperformance in the telecom, utility and financial service sectors. Here are the most notable European movers:

- EasyJet rose as much as 4.5% in early trading after being raised to buy from sell at Deutsche Bank as broker notes an improvement in the UK’s economic outlook

- Coca-Cola HBC shares jump as much as 4.5%, the most since Aug. 11, after reporting full-year net sales that beat analyst estimates

- Vodafone shares rose as much as 4.1% after Liberty Global’s move to acquire a 4.9% stake ramps up pressure for the company to appoint a permanent CEO and deliver a business revival

- Brenntag shares rise as much as 2.8% after activist investor Engine Capital took a 1% stake in the German chemicals distributor and urged it to prioritize the separation of its specialties unit

- Norma shares surge as much as 20%, the most on record, after Bloomberg reported that the German maker of hose and pipe components has had several takeover approaches recently

- Flutter shares rise as much as 4.1% before paring gains after the gambling company said it will consult shareholders on a secondary share listing in the US

- Michelin falls as much as 2.5% after the French tiremaker provided what Deutsche Bank calls “cautious” guidance

- Delivery Hero shares fall as much as 6.6% after the German food delivery company said it will issue about €1 billion in convertible bonds to buy back securities due in 2024 and 2025

- Norsk Hydro slumps as much as 4.6% in Oslo after the aluminum producer reported worse- than-expected adjusted Ebitda for the fourth quarter

- Rockwool drops 2.5% after guidance for 2023 was much weaker than expected, with volume and price outlook “blurry,” Handelsbanken writes in a note, downgrading its three-month view to hold

- Orkla falls as much as 7.7%, the most since October, after the Norwegian retail group’s 4Q results were held back by weakness in the firm’s Branded Consumer Goods (BCG) division

- MTU Aero shares fell as much as 3.7%, after the German aerospace company reported FY22 results which were “a little light on sales”

Earlier in the session, Asian stocks also advanced, rebounding from the lowest in about a month, as large tech shares rose ahead of crucial US inflation figures. The MSCI Asia Pacific Index climbed as much as 0.7%, with TSMC and SK Hynix among the biggest drivers. South Korea and Taiwan helped lead the charge while equities in Japan held gains as the government formally nominated Kazuo Ueda as Bank of Japan governor. Benchmarks in India also rallied close to the levels seen before the selloff in Adani Group stocks. Risk appetite in Asia was partly helped by a Federal Reserve survey showing US wage growth expectations slipped in January. The MSCI Asian stock benchmark had dipped as a months-long rebound on China reopening hopes peaked in late January and as investors tried to gauge how high US interest rates will go.

“Inflation peaked already but it’s likely to stay sticky, more sticky than perhaps what the market is pricing,” Thomas Poullaouec, head of APAC multi-asset solutions at T. Rowe Price, said in an interview with Bloomberg TV. “That’s why the market is getting disappointed when you see a more hawkish tone from central bankers.” US consumer-price data due later may provide the next clues on the Fed’s policy. Traders also continue to monitor the latest corporate earnings reports as well as developments in US and China relations following the recent balloon incident.

Japanese stocks advanced, following US peers higher, as investors await US CPI data later Tuesday for signs that inflation may be cooling and for clues on the direction of monetary policy. The Topix Index rose 0.8% to 1,993.09 as of market close Tokyo time, while the Nikkei advanced 0.6% to 27,602.77. Keyence Corp. contributed the most to the Topix Index gain, increasing 1.3%. Out of 2,163 stocks in the index, 1,667 rose and 420 fell, while 76 were unchanged. “Japanese stocks rose with the trend in US equities yesterday ahead of CPI data release,” said Hideyuki Suzuki, general manager at SBI Securities. “Investors are still cautious as the market might see volatility if the numbers are higher than expected.”

Australian stocks rose, the S&P/ASX 200 index higher 0.2% to close at 7,430.90, bolstered by gains in health stocks and banks. Investors await US inflation data after a drop in wage-growth expectations eased some of the concern over rising prices. In New Zealand, the S&P/NZX 50 index was little changed at 12,074.47

India’s benchmark stocks gauge rallied back to levels seen before a selloff in shares related to Adani Group, as investors remain bullish about earnings-growth potential in local companies despite worries over rising costs. The S&P BSE Sensex rose 1% to 61,032.26 in Mumbai, its highest level since Jan. 18, while the NSE Nifty 50 Index advanced 0.9%. The Sensex has now recouped the losses since the Adani-connected selloff began on Jan. 25, while the Nifty is about 1% away. Recent gains in the broader market are driven by rallies in technology and consumer-staples companies, most having reported better-than-expected earnings for the latest quarter. Tobacco and fast-moving consumer-goods maker ITC and software exporter Infosys are among biggest contributors to Sensex’s recovery, while banks have been the worst performers. Most Asian and European markets advanced on Tuesday ahead of crucial US inflation figures. Foreign investors have continued to take money out of Indian equities this month, though the pace of selling has moderated, with global funds turning buyers for three out of eight sessions. Adani Enterprises Ltd., the flagship firm of the diversified group, gained after reporting a profit for the December quarter. Most of the conglomerate’s other listed shares continued to trade lower. Reliance Industries contributed the most to the Sensex’s gain on Tuesday, increasing 2.4%. Out of 30 shares in the Sensex index, 19 rose and 11 fell.

In FX, the Bloomberg Dollar Spot Index declined 0.2%, adding to Monday’s 0.2% fall. The greenback traded mixed against its Group-of-10 peers, where the Swedish krona was the best performer followed by the British pound and the New Zealand dollar was the worst.

- The euro rose a second day to a high of $1.0767 but remained within recent ranges. The German yield curve bull-flattened a tad while the Italian curve twist- steepened amid positioning ahead of US inflation figures

- The pound advanced 0.5% to $1.2204, its highest in more than a week, following UK labor data that showed wages rose quicker than expected by economists at the end of 2022. UK average earnings excluding bonuses were 6.7% higher in the three months through December from the previous year. Economists surveyed by Bloomberg are anticipating the headline figure slowing to 6.2%

- The yen steadied, after paring an earlier advance. Japan’s bond futures gained following the government’s nomination of Kazuo Ueda to helm the BOJ on Tuesday in a move likely to pave the way for a gradual paring back of the central bank’s full-bore stimulus

- New Zealand’s dollar slumped and the nation’s bond yields declined as the nation’s falling inflation expectations prompted traders to pare rate-hike bets. The RBNZ’s two-year inflation expectations eased to 3.3% in 1Q, down from 3.62% in the three months to December, which was the highest since 1991

In rates, treasuries edged higher across the curve along with stocks as investors awaited January CPI report, with gains led by front-end of the curve as spreads unwind portion of Monday’s sharp flattening move. US yields richer by ~2bp across front-end of the curve with 2s10s, 5s30s spreads both steeper by ~1.5bp on the day; 10-year yields around 3.68%, outperforming bunds and gilts by 0.5bp and 4bp. Gilts underperform and bear-flatten following UK labor data that showed wages rose quicker than expected by economists at the end of 2022. US session also includes several Fed speakers. Fed-dated OIS currently price in around 28bp of rate hikes for the March meeting and a policy peak of approximately 5.20% for the July meeting. CPI data is expected to show price pressures building because of an upswing in activity; however late options activity Monday showed a large hedge on US 5-year yields dropping to around 3.70% by Wednesday’s close.

In commodities, crude futures decline with WTI down 1.5% to trade near $78.90. Spot gold rises roughly 0.4% to trade near $1,861.

Bitcoin is firmer on the session and at the top end of USD 21.61-21.88k boundaries which are by extension well within the week’s existing parameters.

Looking to the day ahead now, the main highlight will be the US CPI release for January. Other data releases include UK unemployment for December. From central banks, we’ll hear from the Fed’s Barkin, Logan, Harker and Williams, as well as the ECB’s Makhlouf. Lastly, earnings releases include Coca-Cola, Airbnb and Marriott.

Market Snapshot

- S&P 500 futures little changed at 4,148.50

- MXAP up 0.6% to 166.21

- MXAPJ up 0.3% to 541.87

- Nikkei up 0.6% to 27,602.77

- Topix up 0.8% to 1,993.09

- Hang Seng Index down 0.2% to 21,113.76

- Shanghai Composite up 0.3% to 3,293.28

- Sensex up 1.1% to 61,069.75

- Australia S&P/ASX 200 up 0.2% to 7,430.86

- Kospi up 0.5% to 2,465.64

- STOXX Europe 600 up 0.4% to 463.77

- German 10Y yield little changed at 2.35%

- Euro up 0.3% to $1.0760

- Brent Futures down 0.7% to $86.01/bbl

- Gold spot up 0.5% to $1,862.42

- U.S. Dollar Index down 0.39% to 102.95

Top Overnight News

- The world is counting on an economic bounceback from China to power global growth and help keep recession at bay. Don’t bank on it. China’s recovery after years of Covid-19 lockdowns will likely look a lot different from previous ones. And for many parts of the world, economists warn, it could be less potent than governments and businesses hope. WSJ

- Kazuo Ueda was nominated to head the BOJ, as expected, in a move that’ll probably pave the way for a gradual paring back of its full-bore stimulus. A rate hike may come by the fourth quarter, according to Eisuke Sakakibara, aka “Mr. Yen,” who sees the currency strengthening to about 120 per dollar this year. JGB traders price in an end to negative rates around mid-year. BBG

- UK posted mixed compensation performance in Dec, w/total average weekly earnings climbing 5.9% (down from +6.5% in Nov and below the St’s +6.2% forecast) although ex-bonus compensation jumped 6.7% (up from +6.5% in Nov and ahead of the St’s +6.5% forecast). RTRS

- CPI: street looking for headline YoY print of 6.2% (vs 6.5% prior, GIR +6.39%) and headline MoM .5% (vs .1% prior, GIR +.5%). In terms of Core YoY street expecting 5.5% (vs 5.7% prior, GIR +5.63%) and MoM of .4% (vs .4% prior, GIR .49%). Positioning has indeed turned more defensive into this print: last week the GS Prime book saw the largest net selling in 7 weeks, driven by Macro Products (index ETFs, futures, and baskets), which saw the largest short sales in nearly 5 months. In terms of S&P’s reaction function to headline YoY print I think risk is skewed to the upside as pain trade remains higher and this mkt continues to seek max pain whenever it gets a chance (yes some of this was pre traded yesterday). GS GBM

- President Joe Biden is set to name Lael Brainard, vice-chair of the US Federal Reserve, to be his top economic adviser, bringing the central bank’s second-in-command to the White House to serve as one of Washington’s top financial policymakers. FT

- Container shipping costs have plunged (in some cases, they’re down ~85% from their peak) thanks to a normalization of the global economy coupled w/inventory de-stocking and soft consumer demand for goods. FT

- Crypto is coming under attack from financial regulators with agencies such as the SEC keen to sever the asset’s ties to the banking system, pushing it far to the fringes of the financial world. WSJ

- Ford will cut 3,800 jobs across Europe, or 11 per cent of its workforce in the region, as it pares back its range of models and prepares to stop selling engine-driven cars later this decade. FT

- TikTok is designed to collect far more personal information from the phones of users compared to other social media apps (TikTok has 2x as many “trackers” in its source code than the industry average). London Times

- Share of companies reporting rising materials costs remains elevated but has fallen from its peak…

A More detailed look at global markets courtesy of Newsquawk

APAC stocks eventually traded mixed with a slight positive bias following the firm handover from Wall St where the major indices gained and the Treasury curve flattened ahead of US inflation data. ASX 200 was led by tech and telecoms after similar outperformance of their US counterparts but with gains capped as an improved business survey was offset by a deterioration in consumer confidence. Nikkei 225 was marginally firmer as participants digested GDP data which showed Japan’s economy returned to growth albeit at a slower-than-expected pace, while the government nominated academic Ueda as the next BoJ Governor, as expected. Hang Seng and Shanghai Comp. were indecisive after the PBoC’s liquidity drain and amid the current balloon-related frictions, although reports noted US Secretary of State Blinken is considering meeting with China’s Foreign Minister Wang which could provide an opportunity to diffuse the tensions.

Top Asian News

- Japan’s government nominated academic Kazuo Ueda as the next BoJ Governor, while it nominated BoJ Executive Director Shinichi Uchida and former FSA chief Ryozo Himino as Deputy Governors, as expected.

- China’s MOFCOM says China will take necessary measures to resolutely safeguard legitimate rights and interests of Chinese enterprises, with regards to US adding Chinese firms to the export control list.

- ‘Mr. Yen’ Says Ueda May Raise Rates by October, Currency to Gain

- Singapore to Set Effective Corporate Tax Rate at 15% From 2025

- Asia Stocks Rebound as Tech Shares Gain Before US Inflation Data

- Bitcoin Performance Tops Ether After SEC Swipe Against Staking

European bourses are modestly firmer, Euro Stoxx 50 +0.3%, in relatively limited newsflow following a mixed APAC handover ahead of US CPI. Stateside, futures are essentially flat with an incremental positive bias pre-CPI and Fed speak, newsquawk CPI preview available here. Within Europe, sectors are all in the green with Telecom’s outperforming on the back of Vodafone while *Travel & Leisure *benefits from a Tui update and easyJet broker move. Boeing (BA) has cut its outlook for India’s commercial aviation market to circa. 2.21k planes over the next decade (prev. forecast 2.240k), via APAC MD at Aero India. Tesla (TSLA) workers a New York are said to launch a union campaign, according to Bloomberg. TSMC (TSM/2330 TT) is to increase its investment at the Arizona plant by up to USD 3.5bln, according to Bloomberg. Turkey is reportedly planning to resume stock trading on Wednesday, via Bloomberg; Reuters sources add that authorities are taking steps to reduce the market impact of the earthquake.

Top European News

- UK and EU could announce a new customs deal within the next two weeks to resolve the dispute over post-Brexit trading rules in Northern Ireland, according to The Telegraph.

- “Negotiations over the Northern Ireland protocol are in the crucial final phase with a potential deal as early as next week””, according to UK government sources cited by The Guardian.

- A Reuters poll showed about three-quarters of respondents expect the BoE to hike rates by 25bps in March and then pause. Furthermore, the median view is for the UK economy to contract in Q1, Q2 and Q3, while the economy is expected to contract by 0.8% in 2023 (prev. forecast for 0.9% contraction) and expand by 0.8% in 2024 (prev. forecast 0.8%).

- German Finance Minister Lindner says cannot back current EU Commission fiscal-rule proposals.

- Turkey is reportedly to temporarily suspend some gold imports, according to Bloomberg; Wealth Fund is to support equities with a new mechanism.

FX

- The DXY has been pushed modestly below 103.00 and resides at the lower-end of 102.90-103.26 parameters pre-CPI.

- Action which initially saw JPY outperformance and NZD underperformance, in a reversal of Monday’s direction, as Ueda’s nomination was confirmed and New Zealand declared a post-cyclone state of emergency; NZD/USD below 0.6350.

- Though, the upside in JPY has dissipated with USD/JPY at the top-end of 132.46-131.79 boundaries.

- Most recently, GBP and EUR have taken pole position amid employment data and reports of Brexit/N. Ireland progress; with Cable above 1.22 and EUR/USD surpassing 1.0750.

- Amidst this, EUR/GBP is slightly softer as GBP outpaces its single currency peer, though the EUR is besting the CHF despite firmer Swiss PPI.

- Brazil’s President Lula and Finance Minister Haddad to meet at 13:00GMT/08:00EST to discuss the possible change in the inflation target, via Estadao; on Thursday, the National Monetary Council (CMN) may debate the issue if there is a decision by the president on the subject.

- PBoC set USD/CNY mid-point at 6.8136 vs exp. 6.8138 (prev. 6.8151)

Fixed Income

- EGBs remain firmer but well off initial best with core-pressure occurring amidst the morning’s UK & Italian sales, with Gilts lagging and BTPs slightly outperforming in the aftermath.

- Specifically, Bund are holding above 136.00 but are some 40 ticks shy of best while Gilts have been an equal margin below 104.00 at worst.

- Stateside, USTs are in-fitting with EGBs but with some slim relative outperformance and thus lie closer to the top-end of 112.26+ to 113.01+ ranges with yields lower across the curve pre-CPI.

Commodities

- Crude benchmarks are hampered following earlier reports that the Biden admin. intends to sell 26mln more from the SPR; as such, WTI Mar and Brent Apr are below USD 79.00/bbl and USD 86.00/bbl respectively.

- UAE Energy Minister says UAE is committed to the OPEC deal lasting until end-2023; more worried about supply than demand next year.

- Russian Urals crude supplies to China increased to a 7-month high of 230k BPD in January, according to Reuters sources; ports loaded 360k BPD of Urals to vessels heading to China over February 1-10th.

- Phillips (PSX) 66 Wood River refinery (380k BPD) reports flaring and a unit upset.

- Spot gold has been moving at the whim of the USD, with the yellow metal testing USD 1850/oz to the downside, though has recuperated somewhat as the DXY loses 103.00; 50-DMA resides at USD 1857/oz.

Geopolitics

- US State Department said the US stands with the Philippines in the face of the Chinese Coast Guard’s reported use of laser devices against the crew of a Philippines Coast Guard ship on February 6th in the South China Sea. US added that China’s conduct was provocative and unsafe which resulted in the temporary blindness of crew members and that China’s dangerous operational behaviour directly threatens regional peace and stability, while it reaffirmed any attack on Philippine armed forces, public vessels or aircraft would invoke mutual defence commitments under their treaty, according to Reuters.

- Russian Kremlin says that NATO is an organisation that is hostile to Russia and proves its hostility every day; NATO is trying to make its involvement in the conflict ever clearer.

US Event Calendar

- 06:00: Jan. SMALL BUSINESS OPTIMISM 90.3, est. 91.0, prior 89.8

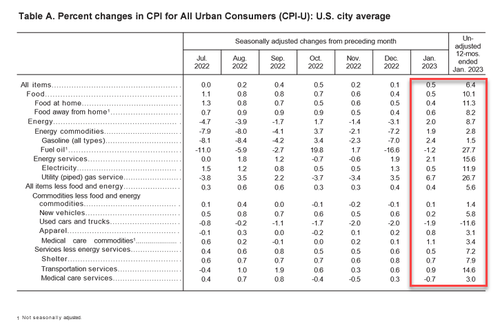

- 08:30: Jan. CPI MoM, est. 0.5%, prior -0.1%, revised 0.1%

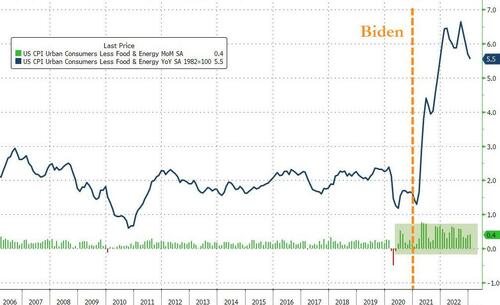

- 08:30: Jan. CPI YoY, est. 6.2%, prior 6.5%

- 08:30: Jan. CPI Ex Food and Energy MoM, est. 0.4%, prior 0.3%, revised 0.4%

- 08:30: Jan. CPI Ex Food and Energy YoY, est. 5.5%, prior 5.7%

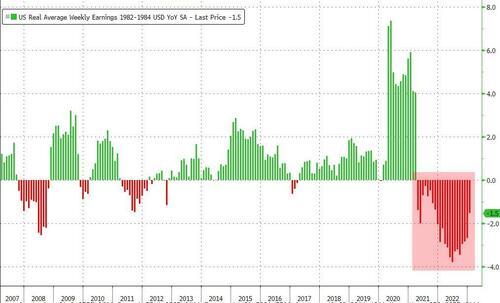

- 08:30: Jan. Real Avg Weekly Earnings YoY, prior -3.1%, revised -2.6%

- 08:30: Jan. Real Avg Hourly Earning YoY, prior -1.7%, revised -1.5%

Central Bank speakers

- 09:30: Fed’s Barkin Interviewed on Bloomberg TV

- 11:00: Fed’s Logan Takes Part in a Moderated Discussion

- 11:30: Fed’s Harker Discusses the Economic Outlook

- 14:05: Fed’s Williams Gives Speech at New York Bankers Conference

DB’s Jim Reid concludes the overnight wrap

A happy Valentine’s Day to all our readers. I hope you all have your highly personal words of love ready to express to your loved one(s). If not, you can do it in a few seconds on chatGPT. A lot less effort.

What better to get you in the mood for love than learning how quickly prices are rising in today’s highly anticipated US CPI print. Everything in the last few weeks has pointed to near-term upward pressure on US inflation in the early part of this year even if it eventually falls more sharply later in the year. Will markets and the Fed look through this if it happens? That’s the big question. The good news is that the market has been shaken out of its immaculate disinflation view in the last 7-8 business days with 10yr UST, Terminal (July) and Dec ’23 Fed Futures contracts up c.36bps, c.40bps and c.60bps, respectively, from its intra-day lows on February 2nd after what was interpreted as a dovish FOMC. Since then, we’ve had a very strong payrolls, the highest used car price growth for 14 months, and revisions to core CPI that showed a less aggressive disinflation path than originally reported. On the latter see more in my CoTD yesterday (link here) but 3 month annualised core CPI is now running at 4.25% rather than the 3.14% the market had imagined before Friday’s revisions.

Today’s number is also the first to see new expenditure weights that lifts OER’s importance. Given OER is expected to stay strong in the near-term before falling later in the year, this could push near-term inflation higher along with a few other things highlighted in the “The rise before the fall” chartbook (link here) from our economists last week. However, the market should be better prepared for this now that it’s more widely recognised.

In terms of what to expect from the CPI report, our US economists are looking for headline CPI to come in at +0.42% in January. On a monthly basis, it would be the fastest monthly pace since October, but given the very strong inflation in the first half of last year, that would still see the year-on-year measure fall to 6.2%, the slowest since October 2021. For core CPI, they think it will come in at +0.36%, which would take the year-on-year measure down to 5.5%, the slowest since December 2021. However, even though the year-on-year measures would still decline, that monthly trajectory would still be too fast for the Fed to be comfortable, as +0.36% monthly core CPI translates into an annualised pace of +4.4% if it happened every month. As usual, we’ll be poring over all the components of the report and our US economist Justin Weidner will be hosting a call 30 minutes after the release (2pm London time/9am NYT). To register see the details in his preview note here.

We’ve got four Fed speakers scheduled for today, so there should be some reaction after the release from policymakers. In the meantime, however, Governor Bowman said yesterday that she expected “it will be necessary to further tighten monetary policy to bring inflation down toward our goal”. Furthermore, she added that although “there are costs and risks to tightening monetary policy to lower inflation, I see the costs and risks of allowing inflation to persist as far greater.”

Ahead of this big day, yesterday saw futures map out their most aggressive path of rate hikes to date, with pricing for the Fed’s terminal rate trading above the 5.2% mark for most of the day before closing slightly higher at 5.1925%. 2yr US yields held at around 3-month highs while yields on 2yr German debt were up +2.3bps to their highest level since 2008, and it was the same story in France and the Netherlands too. As with the Fed, that came as expectations for future ECB policy rates hit their most aggressive to date, with over +100bps of hikes now priced in by the June meeting, which if realised would take their deposit rate above 3.5%. See Mark Wall’s blog from yesterday here where he reiterated his 3.25% ECB terminal rate forecast but continued to suggest the risks are on the upside with a likely 3.25-3.75% landing zone.

However, outside of that, markets were in more upbeat mode with the S&P 500 (+1.14%) advancing and 10yr Treasury yields (-2.7bps) falling as both asset classes clawed back some of last week’s declines. There was some talk about lower inflation expectations in the NY Fed’s latest Survey of Consumer Expectations. In reality, the important three-year horizon was down two-tenths to 2.7%, but five-year expectations were up a tenth to 2.5% and one-year unchanged at 5%. For three-year expectations, it’s actually their lowest since October 2020 before the current bout of high inflation began. But for five-year expectations, they’re at their highest in seven months. Markets seemed to like the report though and tech stocks were the biggest outperformers, and the NASDAQ (+1.48%) and the FANG+ index (+1.96%) saw even larger gains, aided by solid gains from Microsoft (+3.12%) and Meta (+3.03%). And over in Europe it was much the same story, with the STOXX 600 (+0.90%) leading a broad-based advance of its own.

The main exception to this pattern of equity gains were among energy stocks, which came amidst a fresh tumble in energy prices yesterday. For instance, natural gas futures in Europe were down -4.35% to a fresh 17-month low of €51.65 per megawatt-hour, so more positive news for European consumers, and we also saw the European Commission upgrade their Euro Area growth forecast for this year to +0.9% yesterday.

Asian equity markets are broadly positive overnight. As I type, the KOSPI (-0.87%) is leading gains across the region with the Nikkei (+0.52%) and the Hang Seng (+0.22%) also trading up. Elsewhere, Chinese stocks have reversed their opening gains with the CSI down -0.32% and the Shanghai Composite (-0.03%) trading fractionally lower. In overnight trading, US stock futures are indicating a negative start with those tied to the S&P 500 (-0.10%) and NASDAQ 100 (-0.15%) inching lower ahead of the US inflation data.

Early morning data from Japan showed that the economy comfortably avoided recession by expanding +0.6% on an annualised basis for the final quarter of 2022 but lower than market expectations of +2.0%. It followed a revised contraction of -1% recorded in 3Q compared with a year ago.

Staying on Japan, the government named Kazuo Ueda as its pick to become the next BOJ Governor. According to a government document, Ueda was nominated by Japan’s PM Fumio Kishida and would succeed incumbent Haruhiko Kuroda, whose term ends on April 8. Following the reported nomination, the Japanese yen strengthened +0.43% to trade at 131.85 against the dollar as we go to press.

To the day ahead now, and the main highlight will be the US CPI release for January. Other data releases include UK unemployment for December. From central banks, we’ll hear from the Fed’s Barkin, Logan, Harker and Williams, as well as the ECB’s Makhlouf. Lastly, earnings releases include Coca-Cola, Airbnb and Marriott.

end

AND NOW NEWSQUAWK (EUROPE/REPORT)

Mixed trade with Europe seen flat pre-US CPI; JPY leads G10 FX while NZD lags – Newsquawk Euro Market Open

TUESDAY, FEB 14, 2023 – 01:45 AM