February 16+++a//2023 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSED: UP $6.80 at $1842.05

SILVER PRICE CLOSED: UP $0.08 to $21.69

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1836.50

Silver ACCESS CLOSE: 21.58

Bitcoin morning price:, 24,593 UP 543 Dollars

Bitcoin: afternoon price: $24,638 UP 588 dollars

Platinum price closing $929.70 UP $9.55

Palladium price; closing $1531.85 UP $57.95

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,471.68 UP $12.43 CDN dollars per oz

BRITISH GOLD: 1532.02 UP 6.32 pounds per oz

EURO GOLD: 1721.12 UP 3.02 euros per oz

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,834.200000000 USD

INTENT DATE: 02/15/2023 DELIVERY DATE: 02/17/2023

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 1

118 C MACQUARIE FUT 200

132 C SG AMERICAS 22 1

323 C HSBC 4

624 H BOFA SECURITIES 9

657 C MORGAN STANLEY 1

657 H MORGAN STANLEY 7

661 C JP MORGAN 3 42

686 C STONEX FINANCIA 26

800 C MAREX SPEC 13

880 C CITIGROUP 3

880 H CITIGROUP 172

905 C ADM 15 1

TOTAL: 260 260

MONTH TO DATE: 14,453

JPMORGAN STOPPED 42/260

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR FEB/2023. CONTRACT: 260 NOTICES FOR 26,000 OZ or 0.8087 TONNES

total notices so far: 14,453 contracts for 1,445,300 oz (44.955 tonnes)

SILVER NOTICES: 8 NOTICE(S) FILED FOR 40,000 OZ/

total number of notices filed so far this month :822 for 4,110,000 oz

END

GLD

WITH GOLD UP $6.80

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

//SMALL CHANGES IN GOLD INVENTORY AT THE GLD//// A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD

INVENTORY RESTS AT 921.08TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 8 CENTS

AT THE SLV// SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 483.992. MILLION OZ (CORRECTED

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1486 CONTRACTS TO 130,646 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.26 LOSS SILVER PRICING AT THE COMEX ON WEDNESDAY. FOR THE TWO MONTHS, OUR BANKERS HAVE RETURNED TO BEING NET SHORT AND THUS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.26. AND WERE SUCCESSFUL IN KNOCKING SOME SPEC LONGS, AS WE HAD A TINY SIZED LOSS ON OUR TWO EXCHANGES 179 CONTRACTS. AS WELL, WE HAD 0 NOTICES FOR EXCHANGE FOR RISK TRANSFER (0.0 MILLION OZ. ) AS THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1.775 MILLION OZ. WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS( 526 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 0.540. MILLION OZ FOLLOWED BY TODAY’S 50,000 OZ QUEUE JUMP OZ// NEW TOTALS STANDING = 4.225 MILLION OZ + 1.775 MILLION OF EXCHANGE FOR RISK//TOTAL STANDING 6.000 MILLION OZ//// V) HUGE SIZED COMEX OI LOSS/ GOOD SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -781

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB:

TOTAL CONTRACTS for 12 days, total 10,596 contracts: OR 52.980 MILLION OZ . (883 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 52.980 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 52.980/ MILLION OZ/INITIAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1486 WITH OUR STRONG $0.26 LOSS IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 526 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 0.54 MILLION OZ FOLLOWED BY TODAY’S 50,000 OZ QUEUE JUMP= NEW STANDING: 4.175 MILLION OZ + 1.775 MILLION OZ EXCHANGE FOR RISK://NEW STANDING INCREASES TO 6.00 MILLION OZ .. WE HAVE A STRONG SIZED LOSS OF 960 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 8 NOTICE(S) FILED TODAY FOR 40,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 3153 CONTRACTS TO 422,963 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 578 CONTRACTS.

.

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 3153 CONTRACTS) WITH OUR $19.65 LOSS IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 41.601 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE. JUMP OF 24,200 OZ //NEW STANDING: 46.566 TONNES//(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). TONNES

YET ALL OF..THIS HAPPENED WITH OUR $19.65 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A SMALL SIZED LOSS OF 1789 OI CONTRACTS (5.564 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 1364 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 422,963

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1789 CONTRACTS WITH 3153 CONTRACTS DECREASED AT THE COMEX AND 1364 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1211 CONTRACTS OR 3.766 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1364 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (3153) TOTAL LOSS IN THE TWO EXCHANGES 1211 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 41.601 TONNES FOLLOWED BY TODAY’S 40,000 OZ QUEUE JUMP // ///3) SOME LONG LIQUIDATION //4) FAIR SIZED COMEX OPEN INTEREST LOSS// 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

34,262 CONTRACTS OR 3,426,200 OZ OR 106.56 TONNES 12 TRADING DAY(S) AND THUS AVERAGING: 2855 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES 106.56 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 106.56/3550 x 100% TONNES 2.98% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 106.56 TONNES/INITIAL (HEADING FOR ANOTHER STRONG ISSUANCE)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A STRONG SIZED 1489 CONTRACTS OI TO 130,646 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 526 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 526 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 526 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1486 CONTRACTS AND ADD TO THE 526 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG LOSS OF 960 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 4.80MILLION OZ//

OCCURRED DESPITE OUR $0.26 LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 31.46 PTS OR 0.96% //Hang Seng CLOSED UP 175.50 PTS OR 0.84% /The Nikkei closed UP 194.58 PTS OR 0.71% //Australia’s all ordinaries CLOSED UP .82% /Chinese yuan (ONSHORE) closed DOWN 6.85555 //OFFSHORE CHINESE YUAN DOWN TO 6.86666// /Oil UP TO 78.78 dollars per barrel for WTI and BRENT AT 85.64 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 3153 CONTRACTS DOWN TO 422,963 DESPITE OUR HUGE LOSS IN PRICE OF $19.65

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB… THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1364 EFP CONTRACTS WERE ISSUED: : APRIL 1364 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1364 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 1789 CONTRACTS IN THAT 1364 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 3153 CONTRACTS..AND THIS SMALL SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR HUGE FALL IN PRICE OF $19.65. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG. TODAY THE SPEC LONGS WERE RINSED OUT!!

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (46.566)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 46.566 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $19.65) //// AND WERE UNSUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD A SMALL SIZED LOSS OF 1789 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE LOST A TOTAL OI OF 5.564 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (41.219 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 24,200 OZ OR 0,7527 TONNES//NEW STANDING INCREASES TO 46.566 tonnes … ALL OF THIS WAS ACCOMPLISHED DESPITE OUR FALL IN PRICE TO THE TUNE OF $19.65.

WE HAD -578 CONTRACTS COMEX TRADES ADDED TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 1789 CONTRACTS OR 178900 OZ OR 5.564 TONNES

Estimated gold comex today 155,765// poor//

final gold volumes/yesterday 180,008/// poor

INITIAL STANDINGS FOR FEB 2023 COMEX GOLD //FEB 16//

//

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 174,290.328 oz Delaware JPMorgan includes 10 kilobars from Delaware . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 260 notice(s) 26000 OZ 0.8987 TONNES |

| No of oz to be served (notices) | 518 contracts 51,800 oz 1.611 TONNES |

| Total monthly oz gold served (contracts) so far this month | 14,453 notices 1,445,300 44.955 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: NIL oz

customer withdrawals: 2

i) Out of Delaware 321.51 oz (10 kilobars)

ii) Out of JPMorgan: 173,968.518 oz (real gold leaving)

total withdrawals: 174,290.328 oz ..(5.421 tonnes)

Adjustments; 1

customer to dealer/

Delaware 701.994 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEBRUARY.

For the front month of FEBRUARY we have an oi of 778 contracts having lost 370 contracts. We had 612 notices

filed on Tuesday so we gained a huge 242 contract or an additional 24,200 oz will stand for metal at the comex

March gained 20 contracts to stand at 1795.

April lost 3605 contracts down to 339,527

We had 260 notice(s) filed today for 26,000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 3 notices were issued from their client or customer account. The total of all issuance by all participants equate to 260 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 42 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB. /2023. contract month,

we take the total number of notices filed so far for the month (14,453 x 100 oz ), to which we add the difference between the open interest for the front month of (FEBRUARY 778 CONTRACTS) minus the number of notices served upon today 260 x 100 oz per contract equals 1,497,100 OZ OR 46.566 TONNES the number of TONNES standing in this active month of February.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (14,453 x 100 oz+ 778 OI for the front month minus the number of notices served upon today (260)x 100 oz} which equals 1,497,100 oz standing OR 46.566 TONNES in this active delivery month of FEBRUARY..

TOTAL COMEX GOLD STANDING: 46.566 TONNES. SO JUST LIKE LAST MONTH WE START WITH A LOW INITIAL AMOUNT OF GOLD STANDING BUT THIS WILL GROW AS THE MONTH PROCEEDS TO ITS CONCLUSION.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

we had one adjustment of 110,631.591 oz Brinks

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,812,106.420 OZ 56.36 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,824,353.587 OZ

TOTAL REGISTERED GOLD: 10,989,283,391 (341.812 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 10,835,070.190 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,177,177 OZ (REG GOLD- PLEDGED GOLD) 285.44 tonnes//dropping like a stone

END

SILVER/COMEX

FEB 16/2023//INITIAL. SILVER CONTRACT FOR FEBRUARY

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 408,960.561 oz Brinks CNT Int Delaware Delaware Loomis Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 115,045.040 oz Manfra |

| No of oz served today (contracts) | 8 CONTRACT(S) (40,000 OZ) |

| No of oz to be served (notices) | 23 contracts (115,000 oz) |

| Total monthly oz silver served (contracts) | 822 contracts (4,110,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into Manfra: 15,045.040 oz

Total deposits: nil oz

JPMorgan has a total silver weight: 146.353 million oz/288.4171 million =50.73% of comex .//dropping fast

Comex withdrawals: 6

i)Out of CNT: 102,204.953 oz

ii) Out of Brinks: 2962,000 oz

iii) Out of Int Delaware 68,662.690 oz

iv) Out of Delaware 3022.138 oz

v) Out of Manfra: 212,290.081 oz

vi) Out of Loomis: 19,318.700 oz.

Total withdrawals; 1,977,554.829 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 31.784MILLION OZ (declining rapidly).TOTAL REG + ELIG. 288.171

MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR FEB

silver open interest data:

FRONT MONTH OF FEB/2023 OI: 31 CONTRACTS HAVING GAINED 5 CONTRACT(S.).

WE HAD 5 NOTICES FILED ON WEDNESDAY, SO WE GAINED 10 CONTRACTS OR AN ADDITIONAL 50,000 OZ OF SILVER WILL STAND AT THE COMEX

March LOST 2715 CONTRACTS DOWN TO 59,463 contracts

April GAINED 20 CONTRACTS TO STAND at 72.

TOTAL NUMBER OF NOTICES FILED FOR TODAY:8 for 40,000 oz

Comex volumes// est. volume today 61,491// fair to good

Comex volume: confirmed yesterday: 66,275 contracts (good)

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 822 x 5,000 oz = 4,110,000 oz

to which we add the difference between the open interest for the front month of FEB(31) and the number of notices served upon today 8 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2023 contract month:822 (notices served so far) x 5000 oz + OI for the front month of FEB (31 – number of notices served upon today 8) x 500 oz of silver standing for the FEB. contract month equates 4.225 million oz + PREVIOUS 1.775 MILLION OZ ( EXCHANGE FOR RISK) = 6.000MILLION OZ//(TOTAL OZ OF SILVER STANDING).

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

FEB 8/WITH GOLD UP $6.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 920.82 TONNES

FEB 7/WITH GOLD UP $5.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.92 TONNES

FEB 6/WITH GOLD UP $3.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.24 TONNES

FEB 3/WITH GOLD DOWN $52.55 TODAY: STRANGE: BIG CHANGES AGAIN IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 920.24 TONNES

FEB 2/WITH GOLD $10.95 TODAY: BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 918.50 TONNES

FEB 1/WITH GOLD DOWN $2.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 31/WITH GOLD UP $6.55 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 30/WITH GOLD DOWN $6.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 918.50 TONNES

JAN 27/WITH GOLD DOWN $0.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 919.37 TONNES

JAN 26/WITH GOLD DOWN $11.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 919.37 TONNES

JAN 25/WITH GOLD UP $7.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 917.34 TONNES

JAN 24/WITH GOLD UP $7.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 23/WITH GOLD UP $0.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.63 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 20/WITH GOLD UP $4.75 TODAY;BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 912.43 TONNES

JAN 19/WITH GOLD UP $16.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES INTO THE GLD///INVENTORY RESTS AT 910.98TONNES

JAN 18/WITH GOLD DOWN $1.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.9 TONNES FROM THE GLD////INVENTORY RESTS AT 909.24 TONNES

JAN 17/WITH GOLD DOWN $11.45 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.14 TONNES

JAN 13/WITH GOLD UP $22.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD///INVENTORY RESTS AT 912.14 TONNES

JAN 12/WITH GOLD UP $20.55 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 912.43 TONNES

JAN 11/WITH GOLD UP $1.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

GLD INVENTORY: 920.79 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 483.992 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Paulsen is nothing but a goofball.

(Peter Schiff)

Billionaire John Paulson: You Need Gold, Not Dollars

THURSDAY, FEB 16, 2023 – 07:45 AM

Billionaire hedge fund manager John Paulson said you’re better off owning gold than dollars.

Why?

Because he thinks the dollar is set up for long-term depreciation as the world drifts toward dedollarisation.

Paulson talked about the dedollarisation trend in an interview with journalist Alain Elkann.

Paulson said the trend is toward dedollarisation, but it will take a while to happen. While the US isn’t the economic powerhouse it once was, it remains dominant in terms of reserves and trade. But other countries, particularly China, have undercut America’s economic power. That is eroding the power of the once-mighty greenback.

Other countries do not want to rely on the dollar as much as they have in the past, and the US also has an enormous deficit with the rest of the world in terms of trade and investment balances that used to be very positive, but now it’s very negative. That points to the intermediate and long-term depreciation of the dollar versus other currencies.”

He also noted that the extraordinary amount of money printing by the Federal Reserve has also undercut faith in the US dollar.

A lot of our growth has been based on fiscal spending that has been financed by the Fed buying the debt of government. The Fed balance sheet has exploded due to ‘quantitative easing’, a polite way of saying ‘money printing’, and inflation resulted. If you had dollars and 9% inflation, this year you lost 9% of your money; interest rates were nowhere close to compensating for that loss.”

With this backdrop, a lot of investors and central banks are looking for an alternative to the dollar. As a result, Paulson said, “gold is rising again.”

I say again because it’s been the reserve currency of the world for thousands of years, a legitimate alternative to holding the dollar or other paper currencies. There has been a significant increase in demand from central banks to replace dollars with gold, and we’re just at the beginning of that trend. Gold will go up and the dollar will go down, so you’d be better off keeping your investment reserves in gold at this point.”

Paulson isn’t merely speculating. Central bank gold buying set a record in 2022.

But why gold and not some other currency, such as the Swiss franc or the euro?

The other currencies will likely rise in value against the dollar, but each has their own issues. The European Central Bank (ECB) has also printed a significant amount of money, and if you keep your money in fiat currencies you face the risk, due to geopolitical events, that your reserves can be seized. As the central banks did with Russia. China probably think that as they have so much of their reserves in dollars, if they get into a geopolitical spat with the Western world over Taiwan or something else there is a possibility these reserves will be frozen, like they did with Russia.”

You avoid that counterparty risk when you hold gold.

If you possess physical gold you don’t face that risk. You also have the potential for appreciation. We’re at the beginning of trends that are going to increase the demand for gold, and inflation and geopolitical tensions will determine the rate at which gold increases. This year gold will appreciate versus the dollar, and also over a three, five and 10-year basis.

end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

China’s Ensnared In The Middle-Income Trap

WEDNESDAY, FEB 15, 2023 – 10:25 PM

Authored by James Rickards via DailyReckoning.com,

China has fallen victim to what economists call the middle-income trap. Economists consider a low-income country to have around $5,000 annual income per capita. Middle-income countries have between $8,000 and $15,000 annual income per capita. High-income countries begin at around $20,000 annual income per capita.

China’s per capita annual income is $12,970 — solidly in the middle income category. By the way, in the U.S. it’s $75,180, among the highest in the world (second to Switzerland).

Due to China’s extreme income inequality, it is more useful to think of China as having two populations. One population of about 500 million urban workers has an annual per capita income of about $28,000, while a second population of about 900 million villagers has an annual per capita income of about $5,000.

That would put the 900 million villagers solidly in the lower income category, not even close to middle income. And there is extreme income inequality within the 500 million high-income groups such that most of those would have a middle income of about $12,000 per year, while a select few would be earning millions of dollars per year each.

China is predominately a low-income country with a significant middle-income cohort and a tiny slice of the super-rich. This income inequality makes China’s climb out of the middle-income ranks even more difficult. And the super-elite cohort is a potential source of social unrest among the less well-off.

The conventional wisdom is that the rise from low-income to middle-income status is fairly straightforward. You begin by moving tens of millions (or in China’s case, hundreds of millions) of people from rural villages to cities. You provide decent if spartan housing, public transportation, and attract foreign direct investment to build manufacturing plants.

With some training, the city residents become adept at assembly-style manufacturing. Low labor costs allow goods to be assembled cheaply and exported at attractive prices. The cycle feeds on itself with more migration, more direct foreign investment, and expanded manufacturing capacity. Per capita income rises from the low to middle-income range.

But to make it to the big leagues of high-income status, you need high technology applied to high-value-added innovation and manufacturing. China lacks this. China advocates seem impressed that 90% of our iPhones come from China. That’s true, but Chinese value-added is only about 6%. If an iPhone costs $1,000, only about $60 goes to China’s net of import costs and royalties.

In fact,very few countries (excluding OPEC members) have ever made this leap from middle-income to high-income. The only examples in Asia are Japan, South Korea, Hong Kong, Taiwan, and Singapore.

This list leaves many more countries (Malaysia, India, Turkey, Thailand, Brazil, Mexico, Argentina, Russia, Chile, and others) stuck in the middle-income trap with China.

High growth from a starting point of low-income to middle-income is not surprising and should be expected. It’s not a “miracle.” It’s just what happens when you clamp down on corruption, build enough infrastructure, and move millions from the country to the city. China’s done that.

The key variable in forecasting Chinese growth in the years ahead is therefore technology.

Can China not merely license foreign technology (at a high cost), but develop its own technology ahead of advanced-economy competitors?

The outlook here is not good for China.

They have shown little or no capacity to invent or produce in areas such as advanced semiconductors, high-capacity aircraft, medical diagnostics, nuclear reactors, 3D printing, AI, water purification, and virtual reality.

Projects that China has on display that are advanced (such as their bullet trains that run quietly at 310 kph) are done with technology licensed from Germany or France or are done with stolen technology. China has done little innovation on its own.

But the stolen technology channel is being shut down by bans on advanced semiconductor exports to China, and sanctions on the use of 5G systems from Huawei, for example.

On top of all that, China faces powerful economic headwinds in the form of excessive debt, adverse demographics, collapsing real estate markets, and a lack of oil and natural gas reserves. The country is also trying to reopen from its pandemic failures at a time when the world may be entering another global recession worse than 2008.

China also faces powerful geopolitical headwinds as a result of its genocide against the Uyghur minority, involuntary organ harvesting from political prisoners, concentration camps, female infanticide (over 20 million baby girls killed), suppression of religion, censorship, social credit scores, house arrests, and expropriation from entrepreneurs like Jack Ma of Alibaba Group.

Above all, China is handicapped by its return to Mao-style Communism under the leadership of the new Emperor for Life, Comrade Xi Jinping.

Xi has largely abandoned the relatively open economic policies of Deng Xiaoping, which prevailed from 1992 to 2007 under the leadership of Deng’s successors Jiang Zemin and Hu Jintao, with an updated version of Mao’s policies which place the Communist Party and its “core leader” at the center of all decision making and economic direction.

China’s economic headwinds can be summed up in three words — debt, demographics, and decoupling.

There is substantial empirical evidence that national debt to-GDP ratios in excess of 90% result in slower growth. It’s tough to precisely determine China’s, but its debt-to-GDP ratio is probably about 350%.

This problem is exacerbated in China by the fact that much of the debt is not spent productively. I have visited construction projects in the countryside of China where entire cities visible to the horizon were being built from the ground up.

Along with the cities were airports, highways, golf courses, convention centers, and other amenities. It was all empty. None of the buildings were occupied except by a handful of show tenants. Promises of future tenants rang hollow. The construction did create jobs and purchases of materials for a few years, but the debt-financed infrastructure was completely wasted.

The only ways out of a debt trap of the kind China has constructed are default, debt restructuring or inflation.

The last two are just different kinds of defaults. The situation does not necessarily resolve itself quickly. The debt burden can persist for years. Just don’t expect robust growth while it persists.

China’s birth rate is now below what is called the replacement rate. That rate is 2.1 children per couple. China’s current rate is reportedly about 1.6, but some analysts say that the actual rate is 1.0 or even lower. At that rate, China’s population will shrink from 1.4 billion to about 800 million in the next 70 years.

That’s a loss of 600 million people in a single lifetime.

If you assume productivity will remain constant (a reasonable assumption if China fails the high-tech transition), and the population drops by 40%, then it follows that the economy will shrink by 40% or more. That’s the greatest economic collapse in the history of the world.

In all, the pandemic, demographics, debt, decoupling, technology, and global recession should negatively impact Chinese growth in the years ahead.

This growth story inevitably bleeds into geopolitics in terms of a potential invasion of Taiwan and war in the South China Sea.

It is no doubt the greatest economic and geopolitical drama playing out in the world today with important implications for all investors.

end

3. Chris Powell of GATA provides to us very important physical commentaries//

Barrick eyes Nevada gold mines, won’t bid for Newcrest

Submitted by admin on Wed, 2023-02-15 11:55Section: Daily Dispatches

By Divya Rajagopal and Helen Reid

Reuters

Wednesday, February 15, 2023

Barrick Gold Corp. would be open to taking over Newmont’s stake in its Nevada Gold Mines joint venture, CEO Mark Bristow said today, after Newmont’s $16.9-billion bid for Newcrest ramped up pressure on gold miners to do deals.

The Newcrest acquisition by Newmont, if successful, could result in the enlarged company shedding some assets.

“I’ve always said that the best assets that we haven’t got are the other parts of our joint ventures,” Bristow told Reuters in an interview. “If there was a way of acquiring those assets, I think we would be desirous of acquiring them.”

Barrick beat analysts’ estimates for quarterly profit and announced a share buyback of up to $1 billion after record payouts to shareholders last year.

Bristow stuck to the company’s “build, not buy” approach and ruled out the possibility that Barrick would launch a counter bid for Newcrest. …

… For the remainder of the report:

end

Newcrest which was once upon a time owned by Newmont so far tells their former parent to take a hike. If they want them they must bid higher.

Sydney Morning Herald/GATA

Newcrest tells Newmont to raise its acquisition bid

Submitted by admin on Wed, 2023-02-15 21:42Section: Daily Dispatches

By Nick Toscano

Sydney Morning Herald

Thursday, February 16, 2023

Top Australian gold miner Newcrest has rejected a takeover proposal from U.S. mining giant Newmont, arguing that it undervalues the company, but has agreed to open its books to see if it can extract a higher offer from the suitor.

Newmont, the world’s largest listed gold miner, launched a bid this month to acquire all of Melbourne-based Newcrest’s shares at a 22% premium to their previous closing price in a deal that values the company at nearly $US17 billion (A$24.4 billion).

In an update to investors today, Newcrest said its board had considered the indicative offer but had unanimously determined to reject it as it “does not represent sufficient value for Newcrest shareholders.”

“To determine if Newmont can provide an improved proposal for consideration by the board that appropriately reflects the value of Newcrest, the board has indicated to Newmont that it is prepared to provide access to limited, non-public information on a non-exclusive basis,” it said. …

… For the remainder of the report:

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

5.IMPORTANT COMMENTARIES ON COMMODITIES: NICKEL +

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.8555

OFFSHORE YUAN: 6.8666

SHANGHAI CLOSED DOWN 31.46 PTS OR 0.96%

HANG SENG CLOSED UP 175.50 PTS OR 0.84%

2. Nikkei closed UP 194.58 PTS OR 0.71%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 103.62 Euro RISES TO 1.0700 UP 9 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.500!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 133.96/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.484%***/Italian 10 Yr bond yield RISES to 4.345%*** /SPAIN 10 YR BOND YIELD RISES TO 3.533…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.270//

3j Gold at $1834.00//silver at: 21.54 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 18/100 roubles/dollar; ROUBLE AT 74.76//

3m oil into the 78 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 133.96/10 YEAR YIELD AFTER BREAKING .54%, RISES TO .500% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9228– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9874 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.7990% DOWN 1 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.864 UP 1 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,85…

GREAT BRITAIN/10 YEAR YIELD: 3.535% UP 5 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Drop Ahead Of Data Barrage, More Fed Speakers

THURSDAY, FEB 16, 2023 – 08:10 AM

US stock-index futures dropped, reversing earlier gains before a barrage of economic data including jobless claims, housing starts and permits, and the Philly Fed as well as no less than four fed speakers, fading a two-day rally when investors welcomed buoyant US retail data and dismissed the risk of a hawkish response from the Federal Reserve trying to keep inflation in check.

S&P 500 futures traded near session lows, down 0.2% around 7.30am ET, while Nasdaq 100 futs drigted about 0.3% lower erasing an earlier gain. The tech-heavy Nasdaq 100 is up 16% this year and approaching a bull market as investors price in a growing likelihood of a soft landing for the economy. The Bloomberg Dollar Spot index retreated, lifting all Group-of-10 currencies. Treasuries advanced, mirroring gains in UK bond markets. Oil fell and gold edged higher, while Bitcoin climbed for a third day to approach $25,000 for the first time since August.

Among premarket movers, Cisco Systems Inc. jumped 4% after the communications equipment company raised its full-year forecast, a bullish sign for spending on tech infrastructure. More than a dozen analysts raised their price targets on the stock, with several noting that the company’s ability to clear the order backlog built during the pandemic is helping it combat a slowdown in tech demand. Cryptocurrency-exposed stocks also rose in premarket trading as Bitcoin inches closer to the $25,000 level, extending gains for a third consecutive session. Riot Platforms +4.5%, Marathon Digital +3.4%. Shopify wasn’t so lucky, and its shares tumbled as much as 9.7% in the premarket after the cloud-based commerce platform’s first-quarter revenue forecast was weaker than expected. Analysts said strong 4Q results were largely offset by the company’s “conservative” outlook. Here are the most notable premarket movers

- Roku shares rise as much as ~11% in premarket trading after the streaming-video platform reported fourth-quarter results that beat expectations and gave a revenue forecast that was ahead of consensus. Analysts were positive about the company’s move to check operating expenses and target to have Ebitda profitability in 2024.

- Seagen Inc. jumps as much as 7.5% in US premarket trading after the cancer-focused biotech posted a top- line beat for 4Q22 and 2023 guidance that fell in-line with estimates, prompting an upgrade at Raymond James and several other brokers to raise their price targets. Analysts note the positive outlook for the commercial expansion of the company’s cancer drugs, adding that while the biotech could start to turn a profit, management’s 2023 focus will be investing into the pipeline.

- RingCentral falls as much as ~13% in premarket trading on Thursday, after the software company forecast subscription revenue that was weaker than expected. Many analysts said the weak results should be offset by the company’s cost-cutting efforts.

- Shares in Emergent BioSolutions soar 16% in US premarket trading, after the life sciences company’s Narcan spray, used for treating opioid overdoses, got the nod from an FDA panel, which ruled the drug was safe for use without a doctor’s prescription.

- Twilio shares surge as much as ~15% in US premarket trading, set for their biggest gain in three months, after a forecast-beating profit outlook prompted analysts to raise their price targets on the software maker. While brokers said the macroeconomic backdrop could still hamper growth, they noted that Twilio’s focus on turning a profit showed it is prioritizing financial prudence. .

“A softer landing appears more likely given the strong consumer and the expectation that wages will keep heading up as labor markets remain tight,” said Louise Dudley, portfolio manager at Federated Hermes. “The positive retail sales numbers contribute to expectations that the US market can ride out the monetary tightening.”

“In light of the recent good US macro data, the market narrative is switching towards a ‘no-landing’ scenario where a recession could actually be avoided,” said Kevin Thozet, member of the investment committee at Carmignac Gestion in Paris.

“US long-term yields rising alongside risk assets suggest a recession isn’t expected in the second half of 2023,” he added.

At Swissquote, analyst Ipek Ozkardeskaya took a similar view. “The latest economic data clearly suggests that the US economy remains resilient to the interest rate hikes, and that soft landing is possible,” she said, adding that “the ‘Goldilocks’ scenario is reflected in US equity prices right now.”

European stocks rose for a fourth day, underpinned by positive corporate updates from Airbus SE, Standard Chartered Plc and Commerzbank AG. The Stoxx 600 rose 0.3 to its highest level in a year with media, telecoms and banks the best-performing sectors. Here are some of the most notable movers:

- Standard Chartered rises as much as 3.7% in early trading after announcing a buyback and higher returns guidance that offset an increase in impairments in the fourth quarter

- Pernod Ricard shares jump as much as 5% after the French spirits company’s first-half results comfortably beat the consensus and it announced a large stock buyback

- Orange shares rise as much as 5.5% after analysts said the telecom operator’s strategic direction and medium-term targets outlined by new CEO Christel Heydemann were reassuring

- Tenaris gains as much as 9.6%, the most intraday since July, after posting strong fourth-quarter results

- Centrica rises as much as 6.3% in early trading, with shares reaching their highest since May 2019, after the British Gas parent reported full-year operating profit that beat estimates

- Kerry shares rally as much as 5.1%, the most since Nov. 10, after the food company’s earnings, with Morgan Stanley highlighting a solid outlook against an uncertain macroeconomic backdrop

- Nestle shares fell as much as 1% after the food and beverage company reported full-year organic revenue growth that missed estimates

- Moneysupermarket shares fall as much as 9.6%, the most intraday since October, after the price comparison service’s revenue growth slowed in the fourth quarter and missed expectations

- Klepierre shares fall as much as 4.3%, the most since Jan. 10. The French mall landlord’s FY22 results are relatively solid yet analysts remain cautious on its outlook

- Heineken N.V. falls as much as 1.5% after Femsa’s board approved the sale of its stake in the brewer in the next 24 to 36 months after undertaking a strategic review

- Renault shares fall as much as 2.5% giving back initial gains, even after the French carmaker unveiled guidance for 2023 operating margin and free cash flow ahead of analyst expectations

- Sinch falls as much as 18%, the most since July, after the Swedish cloud communications firm reported fourth quarter results that missed estimates

Earlier in the session, equities advanced across Asia as traders awaited key US employment data, although initial gains in Chinese stocks evaporated on geopolitical worries. The MSCI Asia Pacific Index advanced as much as 1.4%, the most since Feb. 1. Samsung, Tencent and Alibaba were among the main contributors to the surge, also helping a rebound in the Hang Seng China Enterprises Index after it had fallen almost 10% from a January peak through Wednesday. Onshore Chinese shares closed lower as a joint communique between China and Iran on expanding cooperation acted as the negative trigger, coming weeks after the US said it would increase pressure on China to stop buying Iranian oil. The MSCI regional gauge is still down more than 3% from a Jan. 27 peak. In terms of the next near-term catalyst, traders expect to see an uptick in jobless claims in the US when the data is announced later Thursday, which could ease the pressure on the Federal Reserve for aggressive policy tightening. The bull-market run in Asian shares slipped this month as investors began to look for catalysts beyond China’s reopening with the jury still out on the pace of US interest rate hikes. Hong Kong benchmarks turned up again Thursday, however, as investors returned following the recent pullback. “I think the rebound is more likely driven by investors waiting on the sidelines looking for a good entry point into China tech,” said Vey-Sern Ling, managing director at Union Bancaire Privee. “Many have missed the sector’s rally from October, and the 10% decline in the past 3 weeks is a good opportunity.”

Japanese stocks rose, following US peers higher after strong economic data. The Topix Index rose 0.7% to 2,001.09 as of market close Tokyo time, while the Nikkei advanced 0.7% to 27,696.44. Toyota Motor Corp. contributed the most to the Topix Index gain, increasing 2.1%. Out of 2,163 stocks in the index, 1,546 rose and 534 fell, while 83 were unchanged. US retail sales in January rose by the most in two years, with cars, furniture and restaurants gaining the most. “Following the announcement of US retail sales, US stocks increased,” said Naoki Fujiwara, chief fund manager at Shinkin Asset Management. “It is favorable that consumer durables, which had been adjusted due to Covid special demands, was firm rather than in energy and food which were temporarily higher.”

Australian stocks gained, with the S&P/ASX 200 index rising 0.8% to close at 7,410.30, after Australian unemployment unexpectedly jumped as the economy shed jobs for a second straight month. The stock benchmark was boosted by gains in consumer discretionary and real estate stocks. In New Zealand, the S&P/NZX 50 index rose 0.6% to 12,157.75.

Indians stocks were mostly higher as investors sought cues from companies’ outlook for future earnings growth as the results season for the December quarter came to a close. The S&P BSE Sensex was little changed at 61,319.51 in Mumbai, while the NSE Nifty 50 Index advanced 0.1%. Sixteen of BSE Ltd.’s 20 sector gauges advanced, led by realty and metal firms. The Information technology gauge rose 1.3%, its third straight advance to the highest since Dec. 1 as most companies surprised analysts with a wider-than-expected expansion in profit and a robust outlook for clients’ spending on their services. Tech Mahindra contributed the most to the Sensex’s gain, increasing 5.6%. Out of 30 shares in the Sensex index, 14 rose and 15 fell, while 1 was steady.

In FX, the Dollar Index is down 0.1% while the Australian dollar is the strongest among the G-10 currencies. The euro climbed 0.2% to 1.0709 and one- month implied volatility in the currency rose as the tenor now captures the next ECB decision; although the relative premium remains below parity, options may soon turn overpriced. Bunds edged up as traders pared back bets slightly for further interest-rate rises by the ECB. The pound rose 0.2% to $1.2054 after closing 1.2% lower on the day on Wednesday following cooler-than-anticipated inflation data and hotter-than-expected US retail sales. Gilts advanced for the second day, led by the shorter end of the curve, as markets priced in the possibility of less monetary tightening by the BOE. Improved risk sentiment helped the Australian dollar erase an earlier loss after the nation’s jobless rate unexpectedly climbed

In rates, Treasuries are mostly higher, led by front-end following late Wednesday pricing of Amgen’s $24b jumbo deal. 10-year TSY yields were around 3.785%, richer by ~2bp vs Wednesday’s close and outperforming bunds and gilts by ~2bp in the sector. US yields are richer by 4bp-5bp across front-end of the curve with long-end slightly cheaper on the day, extending Wednesday’s steepening move; 2s10s, 5s30s spreads wider by 3bp and 5bp. Recent steepener stop-outs have left curve positioning cleaner, setting stage for re-steepening of spreads.Gains accumulated during Asia session and London morning, led by short-maturity gilts. In Europe, front-end bonds outperform and in particular the UK where traders pared back bets on additional rate hikes by the Bank of England. UK money markets trim BOE tightening premium by as much as 7bps, anticipating slowing inflation. The US has a $9b 30-year TIPS auction at 1pm

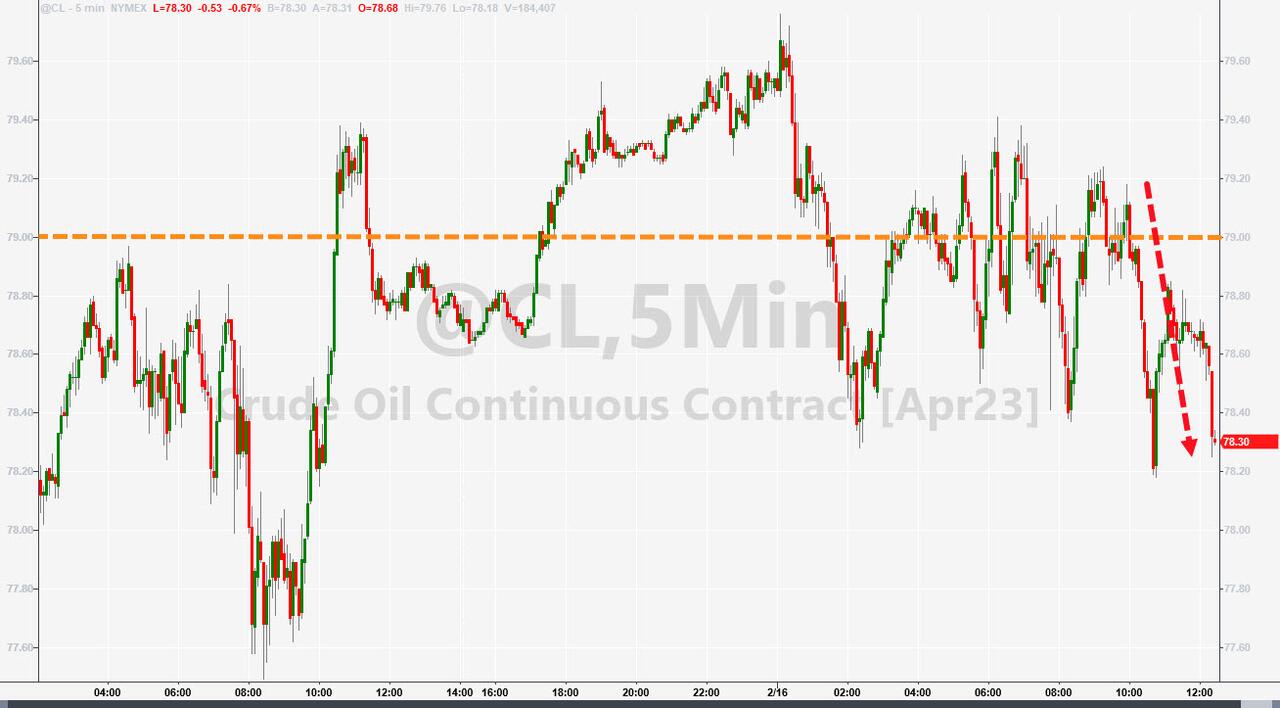

Crude futures decline with WTI down 0.4% to trade near $78.30. Spot gold is little changed near $1,838

Looking to the day ahead now, and data releases from the US include January’s PPI, housing starts and building permits, the weekly initial jobless claims, the February’s Philadelphia Fed business outlook. Otherwise from central banks, we’ll hear from the ECB’s Panetta, Nagel, Lane and Makhlouf, the Fed’s Mester, Bullard and Cook, BoE chief economist Pill and BoC Governor Macklem.Bitcoin is firmer on the session and at the top-end of parameters, though is yet to convincingly test the USD 25k mark to the upside.

Market Snapshot

- S&P 500 futures little changed at 4,160.00

- MXAP up 0.9% to 164.71

- MXAPJ up 0.8% to 537.38

- Nikkei up 0.7% to 27,696.44

- Topix up 0.7% to 2,001.09

- Hang Seng Index up 0.8% to 20,987.67

- Shanghai Composite down 1.0% to 3,249.03

- Sensex up 0.2% to 61,413.83

- Australia S&P/ASX 200 up 0.8% to 7,410.31

- Kospi up 2.0% to 2,475.48

- STOXX Europe 600 up 0.5% to 466.57

- German 10Y yield little changed at 2.46%

- Euro little changed at $1.0699

- Brent Futures little changed at $85.32/bbl

- Gold spot up 0.1% to $1,837.70

- U.S. Dollar Index down 0.19% to 103.72

Top Overnight News from Bloomberg

- China warned the US that rising tensions may jeopardize talks as both nations seek to repair ties in the aftermath of the balloon saga. Antony Blinken and Wang Yi are heading to a security summit in Germany where they may meet on the sidelines. Adding to the friction, China will impose hefty fines on Lockheed Martin and Raytheon over arms sales to Taiwan. BBG

- The Chinese Commerce Ministry said it blacklisted Lockheed Martin and an arm of Raytheon Technologies over the companies’ arms sales to Taiwan. Putting the companies on its “unreliable entities list” prohibits them from export and import activities related to China. WSJ

- Ukraine says the worst is probably over in terms of Russia’s attacks on its energy infrastructure thanks to improved defenses and Moscow’s exhausted military capabilities. BBG

- The ECB should start raising its interest rates in smaller increments and avoid committing to future moves as inflation in the euro zone falls, ECB board member Fabio Panetta said on Thursday.

- Blackstone’s Jonathan Gray expects the US Federal Reserve will raise interest rates to 5.25% to 5.5% and will then hold there an extended period of time, despite emerging signs of slowing inflation. The Federal Reserve is likely to take rates up to that level “for a while,” the president of the world’s biggest alternative asset manager said at an event in Hong Kong. The market is “too optimistic” over the economy weakening, he said. BBG

- Credit Suisse’s Michael Klein, who’ll run First Boston, told the unit’s staff they’ll be shareholders. He said the super boutique will be profitable and that should mean this year’s ugly bonus round won’t happen again. The bank is exiting distressed debt and special-situations trading. It also revealed it has paid $210 million to date in its long-running legal fight with Georgian tycoon Bidzina Ivanishvili. BBG

- Chip trouble. ASML data stolen by a China-based ex-employee were from internal software used to store technical information about machinery, people familiar said. Further afield, a US official said Russia is still procuring foreign chips and tech through intermediaries including Iran and North Korea. BBG

- The Pentagon is reviewing its weapons stockpiles and may need to boost military spending after seeing how quickly ammunition has been used during the war in Ukraine, the most senior US military official said. FT

- KPMG becomes the first of the “Big 4” accounting firms to cut its headcount following a sharp slowdown in its consulting business (KPMG will trim its workforce by ~2%, or 700 people). FT

- The S&P 500 risk premium is the lowest since 2007. Very low risk premiums can portend poor returns over the next few years…

A more detailed look at global markets courtesy of Newsquawk

APAC stocks gained as the region took impetus from the US where participants digested a slew of data releases including stronger-than-expected retail sales and better-than-feared NY Fed Manufacturing. ASX 200 was firmer after several key earnings releases although gains were capped by disappointing jobs data which showed a surprise contraction in Employment Change and a higher Unemployment Rate. Nikkei 225 was led by strength in auto manufacturers including Toyota which plans to boost output next month, while data releases were varied as machinery orders disappointed but trade data was mixed. Hang Seng and Shanghai Comp. conformed to the improved risk tone with tech front running the outperformance in Hong Kong and with the mainland also underpinned by China’s support pledges.

Top Asian News

- China’s NDRC said shortcomings and difficulties still exist in employment, education, medical care, childcare, elderly care, housing and ecological protection. NDRC added that it will boost the income of urban and rural residents, as well as improve the consumption capacity of low and middle-income residents. Furthermore, it will support improvement in spending on housing, NEVs and elderly care services, among other areas of consumption, according to Reuters.

- China’s Industry Minister said China’s industrial and information development is facing a more severe and complex external environment as the US escalates suppression of China’s advanced manufacturing industry, according to Reuters.

- China’s Politburo Standing Committee says the current COVID prevention situation in China is good overall, declares victory in COVID control.

- Japan’s Banking Lobby Chief expects the BoJ to steer an exit from massive monetary easing at some point in the future, if it can forsee sustained and stable CPI and wage growth. Policy adj. could increase volatility in capital/financial markets., prior 1.38m

European bourses are firmer across the board, Euro Stoxx 50 +0.6%, in a continuation of APAC trade with fresh developments somewhat limited ex-earnings. Sectors are mostly in the green with Media outperforming post-RELX, Telecoms bolstered by Orange & Vodafone, Banking by Commerzbank and Standard Chartered; for reference, heavyweight Nestle is lower as its headline metrics missed slightly. Stateside, futures are little changed overall after ending Wednesday’s session firmer after initial data-induced weakness, ES U/C, ahead of numerous Central Bank speakers. Sony (6758 JT) Chip unit head sees limited impact from chip export curbs to China by US, Japan, and the Netherlands, expects global smartphone demand to recover in H2 this year, inventory levels a concern.

Top European News

- ECB’s Panetta says the ECB should not unconditionally pre-commit to future policy moves, the extent and duration of monetary policy restriction matters now that rates are in restrictive territory. Headline inflation could fall below 3% towards the end of the year. Core inflation cannot turn on a dime and will eventually follow headline inflation. Wages are an upside risk and accelerating wage growth raises the spectre of a wage-price spiral.

- EU Top Court Advocate General in the Polish FX Mortgage case says Banks may not demand remuneration for use of capital in contracts rendered invalid; the possibility of demanding remuneration from banks by consumers should be based on Polish law and decision is up to Polish courts.

- UK PM Sunak and EU’s von der Leyen are to speak before the end of the week with the text of the Northern Ireland protocol deal to go before the DUP on Monday, according to The Times; the text will be presented to the DUP on Monday before the cabinet gets to view it on Tuesday. Government sources are confident the deal with satisfy unionist tests for backing a deal.

FX

- DXY has come under some modest pressure throughout the morning in what is more of a consolidation than any sustained bout of pressure, index to the lower-end of 103.52-103.89 session bounds.

- Amidst this, G10 peers are firmer across the board though again magnitudes are relatively slim with specific newsflow in-line with expectations and relatively incrementally.

- Though, this does come with the modest exception of GBP among G10s amid reports that the DUP could see the text of the N.Ireland Protocol deal on Monday, Cable at 1.2074 highs vs 1.2015 trough.

- Outside of G10s, the PLN has garnered interest after the ECJ opinion ruled in-favour of mortgage holders (i.e. against domestic banks), with EUR/PLN up to 4.7775 following the announcement.

- Elsewhere, peers are little changed/modestly firmer ex-USD, with the EUR and CAD await numerous Central Bank speakers.

- PBoC set USD/CNY mid-point at 6.8519 vs exp. 6.8524 (prev. 6.8183)

Commodities

- Crude benchmarks are softer/flat on the session and towards the lower-end of circa USD 1.50/bbl parameters with fresh developments somewhat limited for the complex.

- Gas markets diverge with US Henry Hub futures are firmer above USD 2.50/MMBtu whilst Dutch TTF sees losses but remains above EUR 50/MWh.

- Spot gold is essentially unchanged as participants await fresh catalysts while base metals are mixed overall and relatively rangebound themselves.

Fixed Income

- Gilts and Bunds have run out of recovery momentum and are now essentially unchanged as Bunds failed to breach the 135.12 Fib of Wednesday’s action with specific developments limited.

- In the periphery, a hefty amount of supply from France, Spain and Italian 2053 syndication have been digested with limited impact thus far, though BTPs are a handful of ticks lower than their core peers.

- Stateside, USTs are in the green though they are currently beneath their overnight peak in 112.11+ to 111.29+ parameters ahead of numerous data points and Fed speakers.

Geopolitics

- Russian embassy to the US said the destruction of Nord Stream pipelines was an act of international terrorism and the US should prove it was not involved, according to Reuters.

- US Senate passed a resolution condemning China over the spy balloon, according to Bloomberg. It was also reported that US officials said the downed Chinese spy balloon was aimed at US bases in Guam and Hawaii but was blown off course, according to NYT.

- Turkish Foreign Minister says will discuss bilateral relations, Ukraine war, Swedish and Finnish NATO with US Secretary of State Blinken next week; Turkey could evaluate Finland and Sweden’s NATO applications separately.

US Event Calendar

- 08:30: Jan. PPI Final Demand MoM, est. 0.4%, prior -0.5%, revised -0.4%

- PPI Final Demand YoY, est. 5.4%, prior 6.2%

- PPI Ex Food and Energy MoM, est. 0.3%, prior 0.1%

- PPI Ex Food and Energy YoY, est. 4.9%, prior 5.5%

- 08:30: Feb. Initial Jobless Claims, est. 200,000, prior 196,000

- Continuing Claims, est. 1.7m, prior 1.69m

- 08:30: Jan. Housing Starts, est. 1.36m, prior 1.38m

- Housing Starts MoM, est. -1.9%, prior -1.4%

- Building Permits, est. 1.35m, prior 1.33m, revised 1.34m

- Building Permits MoM, est. 1.0%, prior -1.6%, revised -1.0%

- 08:30: Feb. Philadelphia Fed Business Outl, est. -7.5, prior -8.9

- 08:30: Feb. New York Fed Services Business, est. -17.0, prior -21.4

Central bank speakers

- 08:45: Fed’s Mester Speaks at Global Interdependence Center Event

- 13:30: Fed’s Bullard Discusses the Economy and Monetary Policy

- 16:00: Fed’s Cook Gives Welcoming Remarks at Sadie Collective

- 18:15: Fed’s Mester Discusses the Economic Outlook

DB’s Jim Reid concludes the overnight wrap

So is good news, good news or bad news? Is bad news, bad news or good news? Are rising rates and yields a sign of normality or looming trouble again? Is US inflation hitting a glitch in its disinflationary journey? Is a soft, hard or no landing more likely now after what we’ve seen so far this year? Also are the seasonals causing havoc with the data? December’s US data was particularly weak and January’s particular strong.

These are the trillion dollar questions at the moment. At face value there is indeed growing evidence about the strength of the US economy, with the latest round of data releases still showing a very robust picture at the start of the year. This has helped to cement the market narrative of the last couple of weeks, which has seen investors reassess how high the Fed will need to raise rates in order to get a grip on inflation. Indeed only yesterday, 10yr Treasury yields rose a further +5.5bps, taking them up to their highest closing level of 2023 so far at 3.8%.

In terms of those different releases, first we had US retail sales for January, which posted its fastest monthly growth in nearly two years at +3.0% (vs. +2.0% expected). The components of the release also showed it to be a very broad-based gain, with not one of the major categories seeing a decline over the month either. Second, we had the New York Fed’s latest Empire State manufacturing survey, which surprised to the upside at -5.8 in February (vs. -18.0 expected). And interestingly, both the “prices paid” and “prices received” components rose on the month, so again a sign that inflationary pressures remain strong. Finally, we had the NAHB’s housing market index for February, which rebounded to 42 (vs. 37 expected), which marked the biggest monthly increase since July 2020. That’s coincided with a decline in mortgage rates since their peak in late-October/early November, and suggests that the Fed could need to tighten financial conditions even more if they want to get inflation under control.

When it comes to financial conditions, what’s striking is how accommodative they’ve remained over the last couple of weeks, even as estimates of the Fed’s terminal rate have risen to new highs. For instance, yesterday saw Bloomberg’s index of US financial conditions close at the loosest level in a year. In addition, they remain easier now than when the Fed began its hiking cycle in March, despite 450bps worth of hikes in that time. So for now at least, the economy has remained incredibly resilient in the face of the most rapid tightening cycle in a generation. A reminder here of DB’s Matt Luzzetti’s new 5.6% terminal call from Tuesday night which is probably the most aggressive on the Street as we have been for most of the last year.

For markets, the strong data led to a fresh push higher among longer-dated yields, with investors increasingly pondering whether rates will need to remain higher for longer given the recent releases. That meant that 10yr US Treasury yields ended the session up +5.5bps, although it was higher inflation breakevens that drove the move, with an increase of +4.5bps to 2.36%. Over at the front-end, the moves in inflation breakevens over recent weeks have been even more pronounced, which just shows how investors’ confidence has been dented in the hope that we’ll get a smooth inflation decline. In fact, the 2yr breakeven rose to 2.88% yesterday, which is up more than +80bps in less than a month, having closed at 2.04% on January 18.

This pattern was echoed in Europe too, with yields on 10yr bunds (+3.8bps), OATs (+4.4bps) and BTPs (+10.9bps) all rising on the day. The main exception to this pattern of sovereign bond losses came from UK gilts, with the 10yr yield down -3.4bps. That followed the latest CPI data for January, which showed inflation falling more than expected to +10.1% (vs. +10.3% expected). Core inflation also surprised on the downside at +5.8% (vs. +6.2% expected), raising the prospect that the BoE wouldn’t need to be as aggressive with rate hikes as some had thought.

Equities posted a decent performance on both sides of the Atlantic yesterday as the optimistic narrative prevailed. It was a tougher climb in the US right after the retail sales data, but the S&P 500 (+0.28%) was nevertheless propelled into the green in the last hour of trading after dropping c.-0.70% earlier in the session, with two-thirds of the members up for the day. Positive growth data lifted consumer discretionary (+1.16%) and industrials (+0.63%) sectors that raced ahead of the more defensive staples (+0.19%) and healthcare (-0.51%) stocks. Big tech left its mark too, as communications was the S&P 500’s top performing sector (+1.17%) and the NYSE FANG+ index rose by +0.56%. Such a backdrop naturally favoured the Nasdaq 100 (+0.77%), especially vis-à-vis the Dow Jones (+0.11%) index, but with strong growth data being the key narrative, the small cap Russell 2000 (+1.09%) was the relative outperformer for the day. On the flip side, energy (-1.78%) suffered the most amid another leg down in oil prices (WTI -0.71%), in part due to inventory headlines, and disappointing results from Devon Energy (-10.49%), which made the stock the worst performer in the index for the day.

Over in Europe, the relative outperformance of 2023 continued, with the broader STOXX 600 (+0.42%) hitting its highest level in just under a year. The broad-based rally, with roughly 75% of members in the green for the day, was underpinned by strong performance in economy-sensitive industrials (+1.52%) and consumer discretionary (+1.41%). Laggards were clustered in energy (-0.28%) and real estate (-0.80%).

Asian equity markets are making strong gains this morning. As I type, the Hang Seng (+2.31%) is leading gains in the region ending a four-day run of declines. This is followed by the KOSPI (+1.78%), the CSI (+0.97%), the Shanghai Composite (+0.77%) and the Nikkei (+0.67%). In overnight trading, US equity futures are printing fresh gains with those on the S&P 500 (+0.16%) and NASDAQ 100 (+0.38%) moving higher. Meanwhile, yields on the 10yr USTs (-2.31 bps) have pulled back overnight, trading at 3.78% as we go to press.

In early morning data, Australia’s unemployment rate unexpectedly rose from +3.5% to +3.7% in January, its highest level since the RBA started lifting interest rates from record lows. In January, the economy shed 11,500 jobs, lifting the number of unemployed by 21,900 people, indicating that the nation’s labour market might be starting to weaken after the central bank began hiking interest rates nine months ago.

Turning to the political sphere, in the UK we saw the surprise resignation of Scotland’s First Minister Nicola Sturgeon yesterday. Sturgeon has led the devolved government there since late-2014, shortly after the independence referendum that resulted in a 55-45% vote for Scotland to remain part of the UK. Her plan had been to make the next UK general election a de facto independence referendum, but has now said it will be up to the rest of the SNP to decide how best to win independence. That follows a Supreme Court ruling in November that said the devolved administration in Scotland wasn’t able to unilaterally call a referendum, and would require the consent of the UK government.

Looking at yesterday’s other data, US industrial production was unchanged in January (vs. +0.5% expected), and capacity utilisation unexpectedly fell to 78.3% (vs. 79.1% expected).