FEB 24/ANOTHER RAID ON OUR PRECIOUS METALS AND THIS WILL CONTINUE UNTIL FIRST DAY NOTICE: GOLD CLOSED DOWN $9.10 TO $1810.45//SILVER CLOSED DOWN 46 CENTS TO $20.84//PLATINUM CLOSED DOWN $28.35 TO $912.65//PALLADIUM CLOSED DOWN $26.25 TO $1405.95//COVID UPDATES: DR PANDA/DR PAUL ALEXANDER//VACCINE IMPACT//SLAY NEWS//UKRAINE VS RUSSIA MAJOR UPDATES RE CHINA’S PEACE PLAN//UPDATES ON EAST PALESTINE DISASTER//SWAMP STORIES FOR YOU TONIGHT//

435 H SCOTIA CAPITAL 7 657 C MORGAN STANLEY 2 661 C JP MORGAN 12 737 C ADVANTAGE 17

TOTAL: 19 19 MONTH TO DATE: 15,055

JPMORGAN STOPPED 12/19

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR FEB/2023. CONTRACT: 19 NOTICES FOR 1900 OZ or 0.0590 TONNES

total notices so far: 15,055 contracts for 1,505,500 oz (46.827 tonnes)

SILVER NOTICES: 23 NOTICE(S) FILED FOR 115,000 OZ/

total number of notices filed so far this month :889 for 4,445,000 oz

END

GLD

WITH GOLD DOWN $9.10

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD////A WITHDRAWAL OF 2.60 TONNES OF GOLD FROM THE GLD//

INVENTORY RESTS AT 917.32TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 46 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ OUT OF THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 473.900. MILLION OZ (CORRECTED)

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GOOD SIZED 749 CONTRACTS TO 124,7276AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE GOOD SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.32 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. WE HAVE NOW COMING CLOSE TO OUR ALL TIME LOW OF 124,080 OI CONTRACTS RECORDED FEB 22/2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.32). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES 691 CONTRACTS. AS WELL, WE HAD 0 NOTICES FOR EXCHANGE FOR RISK TRANSFER ( AS THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 6.225 MILLION OZ. WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS( 1440 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 0.540. MILLION OZ FOLLOWED BY TODAY’S 15,000 OZ QUEUE JUMP// NEW TOTALS STANDING = 4.45 MILLION OZ + 6.225 MILLION OF EXCHANGE FOR RISK//TOTAL STANDING 10.675 MILLION OZ//// V) GOOD SIZED COMEX OI LOSS/ HUGE SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 163

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB:

TOTAL CONTRACTS for 17 days, total 16,218 contracts: OR 81.090 MILLION OZ . (954 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 81.090 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 81.090/ MILLION OZ/INITIAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 749 WITH OUR $0.32 LOSS IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1440 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 0.54 MILLION OZ FOLLOWED BY TODAY’S 15,000 OZ QUEUE JUMP = NEW STANDING: 4.45 MILLION OZ + 6.225 MILLION OZ EXCHANGE FOR RISK://NEW STANDING INCREASES TO 10.675 MILLION OZ .. WE HAVE A STRONG SIZED GAIN OF 854OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 23 NOTICE(S) FILED TODAY FOR 115,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1740 CONTRACTS TO 424,276 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 231 CONTRACTS.

.

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 1740 CONTRACTS) WITH OUR $13.05 LOSS IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 41.601 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 6800 OZ //NEW STANDING: 47.421 TONNES//(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). TONNES

YET ALL OF..THIS HAPPENED WITH OUR $13.05 LOSS IN PRICEWITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 1118 OI CONTRACTS (4.196 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2858 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 424,507

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1119 CONTRACTS WITH 1740CONTRACTS DECREASED AT THE COMEX AND 2858 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1118 CONTRACTS OR 4.196 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2858 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (1740) TOTAL GAIN IN THE TWO EXCHANGES 1349 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 41.601 TONNES FOLLOWED BY TODAY’S 6,800 OZ QUEUE JUMP // ///3) ZERO LONG LIQUIDATION //4) FAIR SIZED COMEX OPEN INTEREST LOSS// 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

43,592 CONTRACTS OR 4,359,200 OZ OR 135.58 TONNES 17 TRADING DAY(S) AND THUS AVERAGING: 2564 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES 135.58 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 135.58/3550 x 100% TONNES 3.83% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 135.58 TONNES/INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A GOOD SIZED 749 CONTRACTS OI TO 124,545 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A RECORD LOW OF 124,080 CONTRACTS FEB 22/2023.

EFP ISSUANCE 1440 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 1440 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1440 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 749 CONTRACTS AND ADD TO THE 1440 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG GAIN OF 691 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 3.477 MILLION OZ//

OCCURRED DESPITE OUR $0.32 LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED DOWN 20.32 PTS OR 0.62% //Hang Seng CLOSED DOWN 341.31 PTS OR 1.68% /The Nikkei closed UP 349.16 OR 1.29% //Australia’s all ordinaries CLOSED UO 0.27% /Chinese yuan (ONSHORE) closed DOWN 6.9438 //OFFSHORE CHINESE YUAN DOWN TO 6.9593// /Oil UP TO 76.04 dollars per barrel for WTI and BRENT AT 82.72 / Stocks in Europe OPENED MOSTLY RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1740 CONTRACTS DOWN TO 424,276 WITH OUR LOSS IN PRICE OF $13.05.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2858 EFP CONTRACTS WERE ISSUED: : APRIL 2858 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2858 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1118 CONTRACTS IN THAT 2858LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 1740 CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED (WITH OUR FALL IN PRICE OF $13.05). WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (47.421)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.421 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $13.05) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED GAIN OF 1118 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 4.196 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (41.219 TONNES) FOLLOWED BY TODAY’S QUEUE. JUMP OF 6800 OZ OR 0.2115 TONNES//NEW STANDING INCREASES TO 47.421 tonnes … ALL OF THIS WAS ACCOMPLISHED DESPITE OUR FALL IN PRICE TO THE TUNE OF $13.05.

WE HAD -231 CONTRACTS REMOVED FROM COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1118 CONTRACTS OR 111800 OZ OR 3.477 TONNES

Estimated gold comex today 162,153// //poor

final gold volumes/yesterday 187,014/// poor

INITIAL STANDINGS FOR FEB 2023 COMEX GOLD //FEB 24//

Total monthly oz gold served (contracts) so far this month

15,055 notices 1,505,500 46.827 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 3

i) out of Delaware 321.51 oz 10 kilobars

ii) Out of HSBC: 17,235.966 oz

iii) out of JPMorgan: 27,661,647.597 oz

total withdrawals: 41,169.523 oz real gold except the 10 kilobars from Delaware

in tonnes: 1.28 tonnes

Adjustments; 1

dealer to customer Brinks: 96,453.000 oz (3000 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEBRUARY.

For the front month of FEBRUARY we have an oi of 210 contracts having LOST 121 contracts. We had 189 notices

filed on Thursday so we gained 68 contracts or an additional 6800 oz will stand searching for metal at the comex

March gained 139 contracts to stand at 2168.

April lost 3652 contracts down to 328,692

We had 19 notice(s) filed today for 1900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 19 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer notice(s) was (were) stopped 12/ Received) by J.P.Morgan//customer account 3 and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB. /2023. contract month,

we take the total number of notices filed so far for the month (15,055 x 100 oz ), to which we add the difference between the open interest for the front month of (FEBRUARY 210 CONTRACTS) minus the number of notices served upon today 19 x 100 oz per contract equals 1,524,600 OZ OR 47.421 TONNES the number of TONNES standing in this active month of February.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (15,055 x 100 oz+ 210 OI for the front month minus the number of notices served upon today (19)x 100 oz} which equals 1,524,600 oz standing OR 47.421 TONNES in this active delivery month of FEBRUARY..

TOTAL COMEX GOLD STANDING: 47.421TONNES. SO JUST LIKE LAST MONTH WE START WITH A LOW INITIAL AMOUNT OF GOLD STANDING BUT THIS WILL GROW AS THE MONTH PROCEEDS TO ITS CONCLUSION.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,661.647.597 OZ

TOTAL REGISTERED GOLD: 10,879,594.431 (338,40 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 10,782,053.166 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,100,138 OZ (REG GOLD- PLEDGED GOLD) 283.05 tonnes//dropping like a stone

END

SILVER/COMEX

FEB 24/2023//INITIAL. SILVER CONTRACT FOR FEBRUARY

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

741,767.446 oz

CNT Delaware Manfra

Deposits to the Dealer Inventory

nil OZ

Deposits to the Customer Inventory

1,174,035.328 oz Loomis JPMorgan

No of oz served today (contracts)

23 CONTRACT(S) (115,000 OZ)

No of oz to be served (notices)

0 contracts (nil oz)

Total monthly oz silver served (contracts)

889 contracts (4,445,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i)Into JPMorgan: 574,461.408 oz

ii) Into Lomis: 599,533.92 oz

Total deposits: 1,174,035.328 oz

JPMorgan has a total silver weight: 147.741 million oz/288.392 million =51.22% of comex .//dropping fast

Comex withdrawals: 3

i) Out of Manfra 625,136.126 oz

ii) Out of CNT: 110,660.100 oz

iii) Out of Delaware: 5971.220 oz

Total withdrawals; 741,767.446 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 31.873MILLION OZ (declining rapidly).TOTAL REG + ELIG. 288.392 million o

CALCULATION OF SILVER OZ STANDING FOR FEB

silver open interest data:

FRONT MONTH OF FEB/2023 OI: 23 CONTRACTS HAVING LOST 3 CONTRACT(S.).

WE HAD 6 NOTICES FILED ON THURSDAY, SO WE GAINED 3 CONTRACTS OR AN ADDITIONAL 15,000 OZ OF SILVER WILL STAND AT THE COMEX

March LOST 11,533 CONTRACTS DOWN TO 17,487 contracts. WE HAD TWO MORE READING DAYS BEFORE FIRST DAY NOTICE FEB 28.

April GAINED 71 CONTRACTS TO STAND at 271.

TOTAL NUMBER OF NOTICES FILED FOR TODAY:23 for 115,000 oz

Comex volumes// est. volume today 102,765// excellent//rollovers

Comex volume: confirmed yesterday: 91,033 contracts ( very good//rollovers)

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 889 x 5,000 oz = 4,445,000 oz

to which we add the difference between the open interest for the front month of FEB(23) and the number of notices served upon today 23 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2023 contract month:889 (notices served so far) x 5000 oz + OI for the front month of FEB 23 – number of notices served upon today (23) x 500 oz of silver standing for the FEB. contract month equates 4.45 million oz + PREVIOUS 6.225 MILLION OZ ( EXCHANGE FOR RISK) = 10.675 MILLION OZ//(TOTAL OZ OF SILVER STANDING).

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917/32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

FEB 8/WITH GOLD UP $6.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 920.82 TONNES

FEB 7/WITH GOLD UP $5.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.92 TONNES

FEB 6/WITH GOLD UP $3.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.24 TONNES

FEB 3/WITH GOLD DOWN $52.55 TODAY: STRANGE: BIG CHANGES AGAIN IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 920.24 TONNES

FEB 2/WITH GOLD $10.95 TODAY: BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 918.50 TONNES

FEB 1/WITH GOLD DOWN $2.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 31/WITH GOLD UP $6.55 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 30/WITH GOLD DOWN $6.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 918.50 TONNES

JAN 27/WITH GOLD DOWN $0.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 919.37 TONNES

JAN 26/WITH GOLD DOWN $11.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 919.37 TONNES

JAN 25/WITH GOLD UP $7.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 917.34 TONNES

JAN 24/WITH GOLD UP $7.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 23/WITH GOLD UP $0.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.63 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 20/WITH GOLD UP $4.75 TODAY;BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 912.43 TONNES

JAN 19/WITH GOLD UP $16.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES INTO THE GLD///INVENTORY RESTS AT 910.98TONNES

JAN 18/WITH GOLD DOWN $1.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.9 TONNES FROM THE GLD////INVENTORY RESTS AT 909.24 TONNES

JAN 17/WITH GOLD DOWN $11.45 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.14 TONNES

JAN 13/WITH GOLD UP $22.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD///INVENTORY RESTS AT 912.14 TONNES

JAN 12/WITH GOLD UP $20.55 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 912.43 TONNES

JAN 11/WITH GOLD UP $1.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

GLD INVENTORY: 917.32 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 483.900 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Does Gold Really Preserve Purchasing Power? The Case Of The High-End Suit

One of the characteristics of gold is that it preserves wealth in a world of constantly devaluing fiat currency.

Put another way, it preserves your purchasing power over time.

If you hold onto dollars for several years, they will buy less stuff at the end of that time period than they did at the beginning. This is especially true when we have rapidly rising prices as we do today. But even when inflation is “under control,” Federal Reserve policy is to devalue the dollar by 2% every year.

It simply doesn’t make sense to hold onto dollars for any length of time.

We can demonstrate this in a tangible way by pricing a good or service in gold and examining the change in price over time.

As an example, let’s consider a high-end men’s suit.

In 1900, the average price of a high-end men’s suit was around $35.

At the time, the price of gold was set at $20.67 per ounce. That means a high-end suit priced in gold would have cost around 1.7 ounces of gold.

Today, the average price of a high-end suit is around $2,000.

Obviously, prices vary depending on the brand, region and other factors, but this provides a fair average. At the time I’m writing this, the price of gold is around $1,840 an ounce. I’ll use $1,800 for this calculation to keep it simple. That means a high-end suit priced in gold today costs a little over 1.1 ounces of gold.

As you can see, the price of a suit in gold has dropped a little over 35% since 1900. This is what you would expect given advances in technology and productivity. But priced in dollars, the price of a high-end men’s suit has increased by 5,614.3%.

Looking at it another way, if you had stuffed $41.34 under your mattress in 1900, today you might be able to buy a couple of Polo shirts if you find a deal. But if you had bought two 1-ounce gold coins and stuffed those under your mattress in 1900, today you’d be able to buy a fancy suit and have about $1,600 left over.

Of course, the price of gold fluctuates day to day, month to month, and year to year. In some years, the price of gold even falls. But over time, it has historically maintained its purchasing power even as fiat currencies lose buying power year after year.

Added to the fact that it carries no counterparty risk, gold is an excellent way to safely preserve wealth and mitigate risk in your portfolio.

end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

END

3. Chris Powell of GATA provides to us very important physical commentaries//

Agustin Carstens, head of the Bank for International Settlements (BIS), believes the battle between cryptocurrency and fiat currencies has come to an end, with the latter emerging as the winner. Fiat currency refers to money that has legal tender by government decree.

“That battle has been won … A technology doesn’t make for trusted money,” Carstens said in an interview with Bloomberg TV on Wednesday.

“Only the legal, historical infrastructure behind central banks can give great credibility” to money, he added.

Carstens is anticipating a “strong statement” from the G20 nations for stronger regulation on digital assets, pointing out that crypto as a financial activity can only exist “under certain conditions.”

Castens’ statements come after cryptocurrencies crashed over the past year, with Bitcoin – the most valuable cryptocurrency in the world – down by around 38 percent. After hitting a 2022 peak of around $47,450 in March, Bitcoin was trading at $23,700, as of Feb. 22, up around 60% from its Nov 2022 cycle lows.

The crash in cryptocurrencies is pegged on multiple factors. For one, rising interest rates made holding cash much more attractive than investing in risky and volatile assets like cryptocurrencies.

The crash of the LUNA coin in May added to the decline. At one point, LUNA was ranked as the seventh biggest cryptocurrency in the world. But following an unsustainable business model and other issues, LUNA declined by 96 percent in a single day in May 2022.

Confidence in the crypto market fell further in November when FTX, one of the largest crypto exchanges at the time, filed for bankruptcy after concerns about the company’s balance sheet and subsequent withdrawals triggered a liquidity crisis.

Flaws of Cryptocurrencies

A report published by the International Monetary Fund (IMF) in September 2022 that was co-authored by Carstens outlines three flaws that prevent cryptocurrencies from acting as a “sound basis for the monetary system.”

First is that cryptos lack a “sound nominal anchor.” Cryptocurrencies themselves are highly volatile.

Meanwhile, stablecoins, a type of crypto where its value is pegged to an asset like the U.S. dollar, “borrow credibility from real money issued by banks.”

Second, fiat money is anchored in a trusted institution like a central bank that guarantees the stability of the currency as well as the final settlement of transactions and their safety.

Crypto does not have such centralized government-level guarantees.

Third, the decentralized nature of cryptocurrencies means that it relies on incentives to anonymous validators to confirm transactions in the form of rents and fees.

This prevents scalability and results in congestion.

“For example, when the Ethereum network (a blockchain widely used for DeFi applications) nears its transaction limit, fees rise exponentially. As a result, over the past two years, users have moved to other blockchains, resulting in growing fragmentation of the DeFi landscape,” the report notes.

DeFi is short for decentralized finance.

National Risks

In October last year, the U.S. Financial Stability Oversight Council (FSOC) issued a warning that digital assets like cryptocurrencies could essentially undermine the financial stability of the country.

Despite the distributed nature of crypto asset systems, operational risks can arise due to the concentration of key services or from vulnerabilities linked to the distributed ledger technology on which the assets rely, the agency stated.

“Crypto-asset activities could pose risks to the stability of the U.S. financial system and emphasizes the importance of appropriate regulation, including enforcement of existing laws. It is vital that government stakeholders collectively work to make progress on these recommendations,” the report warned.

In a blog post on Jan. 27, the White House cited dangers from cryptocurrencies, including potential financial losses, fraud, and the empowerment of America’s rivals.

National security adviser Jake Sullivan had placed cryptocurrencies on the administration’s radar in June 2021 following the ransomware attack on Colonial Pipeline in May that year. Colonial was forced to pay the hackers 75 Bitcoins in ransom, which amounted to $4.4 million at the time.

In June 2021, former president Donald Trump had also indicated that he was not a fan of Bitcoin, pointing out that it was competing against the U.S. dollar as the reserve currency of the world.

* * *

[ZH: In response to all that projection, ignorance, and hyperbole, we paraphrase from the bard himself (for added credibility, of course): “the fat man whose salary depends on fiat’s dominion doth protest too much, wethinks”...]

end

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.9438

OFFSHORE YUAN: 6.9593

SHANGHAI CLOSED DOWN 20.32 PTS OR 0.62%

HANG SENG CLOSED DOWN 341.31 PTS OR 1.68%

2. Nikkei closed UP 349.16 PTS OR 1.29%

3. Europe stocks SO FAR: MOSTLY RED

USA dollar INDEX UP TO 104.91 Euro FALLS TO 1.0567 DOWN 31 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.4999!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 135.75/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.506%***/Italian 10 Yr bond yield FALLS to 4.381%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.545…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.322//(ITALY WORSE THAN GREECE?)

3j Gold at $1816.50//silver at: 21.02 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 05/100 roubles/dollar; ROUBLE AT 76.05//

3m oil into the 76 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 135.75/10 YEAR YIELD AFTER BREAKING .54%, REMAINS AT .4999% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9366–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9896well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

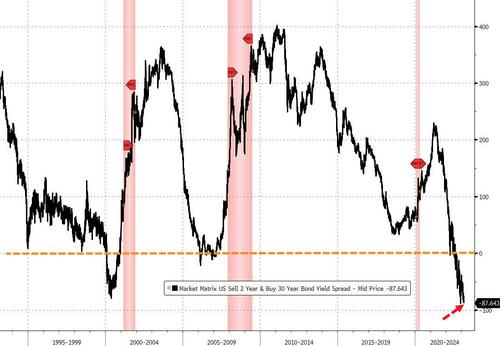

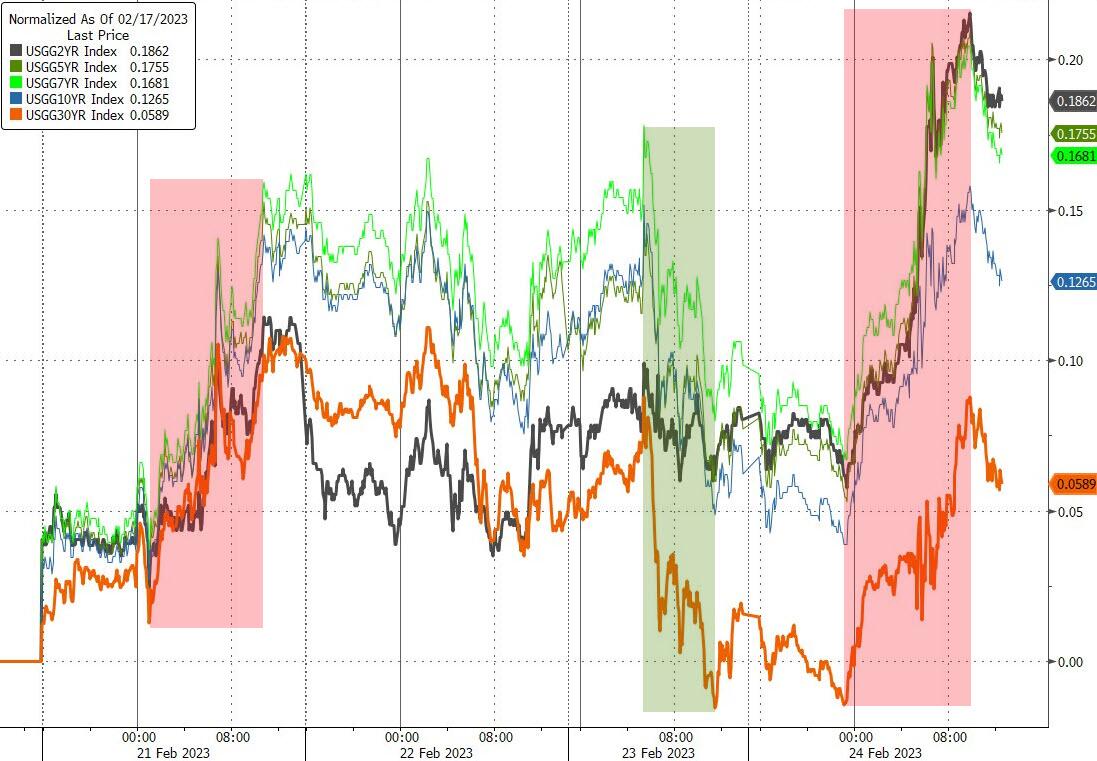

USA 10 YR BOND YIELD: 3.912% UP 3 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.9092 UP 3 BASIS PTS//INVERTED TO THE 10 YEAR!!

UK 2 YR BOND YIELD: 4.7306 UP 4 BASIS PT

USA DOLLAR VS TURKISH LIRA: 18,88…

GREAT BRITAIN/10 YEAR YIELD: 3.650% UP 6 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Slide With All Eyes On PCE Inflation

FRIDAY, FEB 24, 2023 – 08:04 AM

US index futures reversed Thursday’s rebound, and dropped as investors braced for data that may show accelerating inflation in the world’s largest economy. European stocks erased an earlier gain, while Asian equities fell on a quiet day for global markets. Contracts on the S&P 500 slipped 0.6% while those on the Nasdaq 100 fell 0.7% by 7:45a.m. ET. Friday sees the release of the personal consumption expenditures index, the Fed’s preferred price gauge, which is expected to show acceleration amid robust income and spending growth. The dollar rose amid concern over disappointing earnings and geopolitical tensions, and as the Yen tumbled after the confirmation hearing of Ueda’s proved to be far less hawkish than some expected.

In premarket trading, Beyond Meat jumped after its fourth-quarter net revenue topped analyst expectations, Boeing slipped after the planemaker paused deliveries of its 787 Dreamliner due to a documentation issue although analysts said they expect this to be a short-term issue, noting that it was due to non-compliance with paperwork. Warner Bros Discovery shares fell 5% in premarket trading on Friday after the parent of TNT, CNN and other TV networks reported quarterly sales that came in below analysts’ estimates. While the advertising market remains challenging, the worst of the merger integration period is behind them, analysts say.

Warner Bros Discovery fell after reporting quarterly sales that missed analysts’ estimates. Alibaba and NetEase lead a decline in US-listed Chinese stocks, with both internet companies’ results failing to offer a fresh boost as the rally spurred by China’s reopening wears off. Here are the other notable premarket movers:

Block rose as much as 8.2% in premarket trading on Friday after the digital payments company formerly known as Square reported fourth-quarter profit that beat estimates. Analysts noted that the company’s pledge to better manage its operating cost growth will be welcomed by investors.

Farfetch shares gain 8% in US premarket trading after the specialty online retailer reported fourth-quarter revenue that beat expectations. Analysts were broadly positive on the reiterated guidance for 2023, noting that partnerships with Ferragamo, Reebok and Neiman Marcus offered tailwinds for the financial year.

Opendoor Technologies fell 5% in premarket trading on Friday after KeyBanc Capital Markets said the data-driven home-flipper faces limits on how fast it can buy and sell homes.

Floor & Decor gained 5% in extended trading after reporting adjusted earnings per share for the fourth quarter that topped the average analyst estimate. The flooring retailer’s annual forecasts for sales and profit trailed analysts’ expectations.

Nektar Therapeutics plummeted 29% in extended trading after saying the Phase 2 study of rezpegaldesleukin in patients with active systemic lupus erythematosus did not meet the primary endpoint.

After hot prints on consumer and producer prices, a high reading in today’s PCE report could weigh on markets. The S&P 500 is headed for a third week of declines, with traders taming their optimism about the outlook for the economy as Fed officials promise further rate hikes to subdue soaring inflation.

“In the context of an inflation shock, a global energy crisis and the fastest rate-hike cycle in history, we have to assume that with a time lag there will be an economic consequence,” Sonja Laud, chief investment officer at Legal & General Investment Management, said on Bloomberg Television.

But central banks’ determination to take rates for higher for longer is not their only worry: decelerating growth, sluggish corporate performance, geopolitical tensions from Russia to North Korea, and centralization of power in China all complicate the investment landscape.

“Investors worry that this unexpected strength in the US economy, coupled with a steady reopening of the Chinese economy, will fuel further inflation which would lead the Fed to pursue a more aggressive tightening cycle,” said Geir Lode, the head of global equities at Federated Hermes. “Looking ahead, we see mixed signals: leading economic indicators continue to point to a recession, but lagging economic indicators show no signs of weakness, yet.”

European equity indexes faded earlier gains, with outperformance in the construction, utility and energy sectors while chemicals and travel lagged. The Stoxx 600 was down 0.1% after gaining 0.3%, but the DAX falls 0.6% after data showed the German economy contracted more than previously thought in the fourth quarter. BASF shares slide as much as 6% after the global chemicals giant halted share buybacks and gave an outlook that analysts deemed as muted. Here are the biggest European movers:

Saint-Gobain shares rise as much as 6.3%, the most since March 2022 with analysts saying the French building materials group’s results and margin guidance should provide some confidence

Embracer gains as much as 4.1% after the video-game maker said it plans to collaborate with New Line Cinema and Warner Bros. Pictures on feature films based on The Lord of the Rings

Jupiter Fund Management shares jump as much as 15%, the most since March 2020 after the UK investment manager’s results provided a rare batch of good news

Endesa gains 1.9% after the Spanish utility increased its 2022 dividend and reported full- year net income that beat the average analyst estimate

Elekta shares surge as much as 11% after the Swedish medical technology firm reported third-quarter earnings that strongly beat expectations

Accor shares jump as much as 4.5%, reaching the highest since May 5, after Stifel upgrades the French hospitality company to hold from sell, seeing a more attractive risk/reward

Sopra Steria shares rise as much as 4.7%, hitting levels unseen since 2018, in a second day of gains after the French IT services company reported profit for the full year that beat estimates

IAG falls as much as 4.1% after the parent of British Airways gave an outlook that failed to cheer investors after the stock’s 33% jump ahead of earnings

Valeo shares fell as much as 6.6% after the manufacturer of car parts published a free cash flow guidance which fell below analysts’ expectations

Earlier in the session, Asia’s stock benchmark dropped, heading for a fourth-straight weekly loss, as disappointing tech results dragged down China’s equity market and investors remained vigilant before the release of key US economic data. The MSCI Asia Pacific Index slipped as much as 0.7%, reversing earlier gains. Stocks in Hong Kong continued to drop after entering a technical correction Thursday; a gauge of Chinese technology stocks listed in Hong Kong tumbled 3.3%. NetEase Inc. slumped after a profit miss, while Alibaba Group Holding Ltd. fell as analysts remained cautious about its sales growth prospect. Meanwhile, Chinese President Xi Jinping was set to bring decision-making of the financial system further under his control with the revival of a powerful committee.

“A lot of the momentum in China has come in so it’s important to be discerning and look for the quality stocks that are more reasonably valued,” Julie Ho, an Asia ex-Japan equities portfolio manager at JPMorgan Asset Management, told Bloomberg Television. Japanese stocks advanced as Bank of Japan Governor nominee Kazuo Ueda said current policy easing was appropriate. He spoke at a parliamentary hearing in the approval process for his appointment. South Korean stocks slid as foreign investors turned net sellers for the first week this year amid concerns over the impact of tighter global monetary policy on the nation’s tech-heavy equity market. Malaysian stocks pared losses ahead of the annual budget presentation. Traders in Asia are awaiting US inflation numbers due today, after mixed data Thursday muddied the outlook for Federal Reserve policy. Gains in Asian stocks have stalled this month amid renewed worries of US policy tightening and a lack of positive catalysts for heavyweight Chinese shares. The MSCI Asia gauge is down almost 2% this week.

Japanese stocks rose as Bank of Japan governor nominee Kazuo Ueda backed continued easing in his confirmation hearing in parliament. Ueda said it will still take time to hit the central bank’s target for stable 2% inflation, adding that continuing with stimulus is appropriate for now. “Comments by Ueda came as no surprise — since he didn’t signal policy would change abruptly, the market is relieved,” said Ayako Sera, a market strategist at Sumitomo Mitsui Trust Bank Ltd. “Ueda is taking taking a very cautious stance, which is very positive for the stock market.” The Topix rose 0.7% to close at 1,988.40, while the Nikkei advanced 1.3% to 27,453.48. Banks dropped while real estate stocks rose. Tokyo Electron contributed the most to the Topix gain, gaining 7.1%. Out of 2,161 stocks in the index, 1,571 rose and 507 fell, while 83 were unchanged.

Australia’s S&P/ASX 200 index rose 0.3% to close at 7,307.00, as all sectors aside from mining advanced. Banks and industrials boosted the benchmark most. Still, the benchmark caped its third straight weekly loss, dropping 0.5%. In New Zealand, the S&P/NZX 50 index rose 0.2% to 11,905.

Key stock gauges in India posted their biggest weekly drop in eight months as investors continue to avoid riskier assets globally on the prospect of higher interest rates. Most stocks related to the Adani Group declined on Friday as the monthlong selloff in the conglomerate’s shares neared $150 billion. Selling in shares of the ports-to-power conglomerate has continued despite its efforts to reassure investors about its strategy and debt reduction plans. The S&P BSE Sensex fell 2.5% for the week, its biggest retreat since June 19, while the NSE Nifty 50 Index declined 2.7%. On Friday, the benchmark Sensex fell 0.2% to 59,463.93 in Mumbai, while the Nifty declined 0.3%.

In FX, the Dollar Index is up 0.1%, advancing for the third time in four days. The Australian dollar and Japanese yen are the weakest among the G-10’s.

Sweden’s krona was the only currency to advance against the dollar Friday and this week, as hawkish commentary from the central bank added to bets on further policy tightening.

The euro steadied below $1.06 and the bund curve twist-flattened very modestly. A surprisingly weak final reading of German GDP prompted traders to trim bets for ECB interest- rate rises in the coming months.

The pound was steady but was also among the best-performing major currencies this week after data showed UK household confidence rebounded by the most in almost two years. Gilts eased in early trade before Tenreyro, the BOE’s most dovish policy maker, speaks later in the day.

The yen fell and the volatility skew kept shifting lower after BOJ Governor nominee Kazuo Ueda warned against any magical solution to produce stable inflation and normalize policy as he largely stuck to the existing central bank script in the first parliamentary hearing to approve his appointment

In rates, treasuries are under pressure as US trading day begins, with yields inside Thursday’s rally ranges but near YTD highs reached this week. Yields are higher by 2bp-4bp, 10-year by 3bp at 3.91%; the 10-year yield is ~10bp higher on week and ~40bp higher over past five weeks. Thursday’s ranges included YTD highs for 5- and 10-year. The market is headed for its fifth straight weekly loss, having all but erased January’s gains amid hawkish repricing of Fed policy outlook. UK and German 10-year yields are little changed.

Fed swaps nearly fully price in a third 25bp rate increase in June, following expected moves in March and May. Next week brings a large quarterly month-end index rebalancing with the potential to drive buying, and Treasury coupon auctions resume March 7.

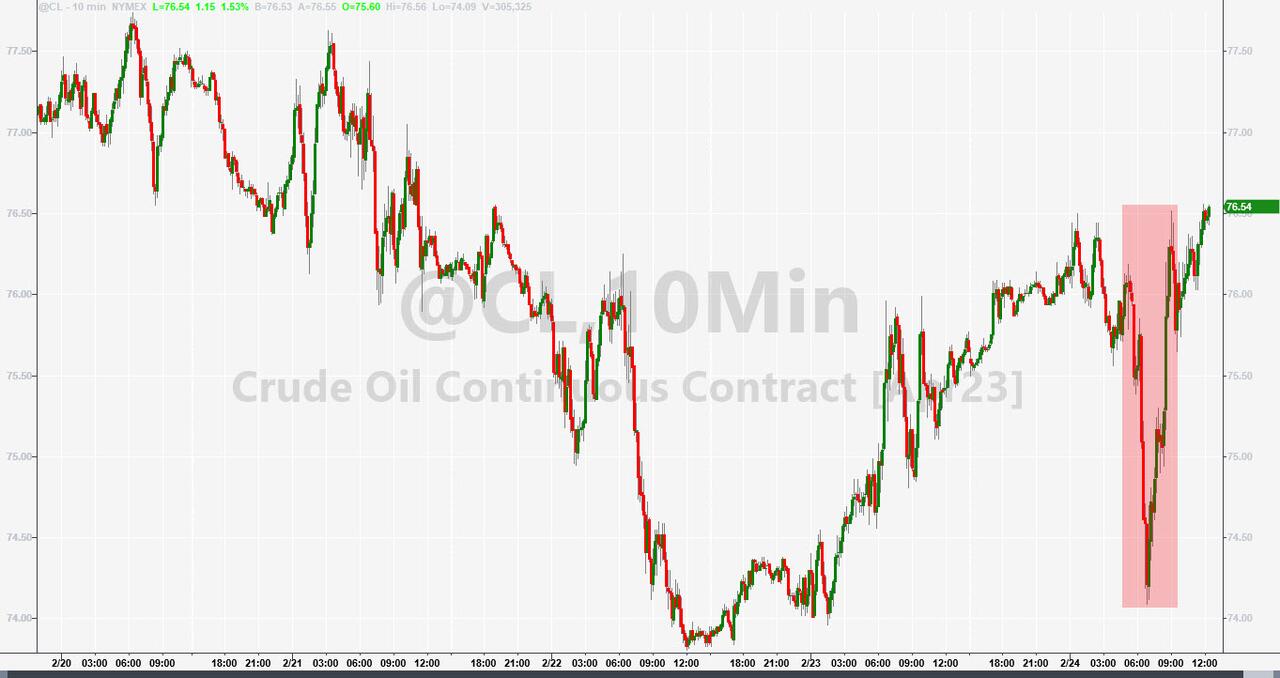

In commodities, oil extended Thursday’s advance amid strength in commodity currencies and optimism over China’s reopening. Crude futures advance with WTI rising 1.2% to trade near $76.30. Spot gold is little changed around $1,822.

Bitcoin was on pace for its second monthly advance, breaking with stocks and other riskier assets

Looking at the day ahead now, there’s a heavy data calendar in the US with personal income and spending data, along with the Federal Reserve’s preferred inflation measure, coming at 8:30 a.m. Later, there are reports on new home sales and sentiment as well as a number of Fed comments, including from Loretta Mester and James Bullard.

Market Snapshot

S&P 500 futures down 0.3% to 4,008.25

MXAP down 0.7% to 159.42

MXAPJ down 1.2% to 516.92

Nikkei up 1.3% to 27,453.48

Topix up 0.7% to 1,988.40

Hang Seng Index down 1.7% to 20,010.04

Shanghai Composite down 0.6% to 3,267.16

Sensex down 0.3% to 59,449.83

Australia S&P/ASX 200 up 0.3% to 7,307.03

Kospi down 0.6% to 2,423.61

STOXX Europe 600 up 0.3% to 463.97

German 10Y yield little changed at 2.47%

Euro little changed at $1.0588

Brent Futures up 0.9% to $82.91/bbl

Gold spot up 0.0% to $1,822.40

U.S. Dollar Index up 0.11% to 104.71

Top Overnight News from Bloomberg

China told the United Nations on Thursday that one year into the Ukraine war “brutal facts offer an ample proof that sending weapons will not bring peace,” just days after the United States and NATO warned Beijing against giving Russia military support. RTRS

Japan’s Jan CPI rose M/M, although not by as much as feared – the ex-food number was +4.2% (vs. +4% in Dec and below the St’s +4.3% forecast) while ex-food/energy came in at +3.2% (vs. +3% in Dec and below the St’s +3.3% forecast). BBG

BOJ governor nominee Kazuo Ueda said it was “appropriate” to continue easing and called Kuroda’s policies “unavoidable” while the joint statement w/the government didn’t require revision, but suggested YCC had negative side effects and warned normalization could occur once the 2% inflation target was in sight. Nikkei

China’s property market: in another sign the downturn is easing/ending, China Garden Holdings, one of the country’s largest developers, plans to buy land in local gov’t auctions for the first time in more than a year. WSJ

Chinese President Xi Jinping is set to bring decision-making of the financial system further under his control with the likely revival of a powerful committee to coordinate financial policy and the possible appointment of a key ally in a top position at the central bank. BBG

China’s overnight repurchase rate, a gauge of interbank funding costs, fell more than 80 basis points from Tuesday when it approached the highest level since 2021. That’s because the PBOC’s string of short-term cash injections that started last week, which included its biggest single-day boost on record, replenished the financial system with liquidity. BBG

The Adani Group will hold a fixed-income investor roadshow in Asia next week as the embattled Indian conglomerate seeks to repair the damage caused by a shock short-seller report. BBG

Credit Suisse cut payouts on a $3.5 billion real estate fund, as clients sought to pull their cash after rising interest rates hurt valuations. The fund’s net asset value is expected to drop as much as 10%. BBG

Inflation measured by the Fed’s favored gauges probably stayed robust last month, upending optimism that the peak has been passed. The headline PCE deflator probably rose 0.5% month on month, with the annual rate staying at 5%. More worrying, both core and supercore gauges may have accelerated too. The sources of the pickup – income and spending growth — probably remained healthy last month. BBG

Amazon founder Jeff Bezos hired an investment firm to evaluate a possible bid for the Washington Commanders, according to two people familiar with the situation. Wa Po

The DOJ wants to block Adobe’s $20 billion purchase of startup Figma, people familiar said. An antitrust lawsuit may be filed next month. The deal also faces antitrust reviews in the EU and UK. Adobe shares fell postmarket. BBG

A sharp rotation toward cyclical stocks has aided mutual fund performance this year. In contrast with 3Q, mutual funds rotated sharply toward cyclical stocks in 4Q, suggesting optimism around the economic outlook. Autos, Tech Hardware, and Banks were among the most added to industries. At a sector level, funds are overweight Financials, Industrials, Materials, and Consumer Discretionary. Mutual fund and ETF fund flow data have also flipped in favor of cyclical sectors in recent weeks. In contrast to increased cyclical exposure, mutual fund exposure to growth stocks is higher than at any point since 3Q14. (GIR)

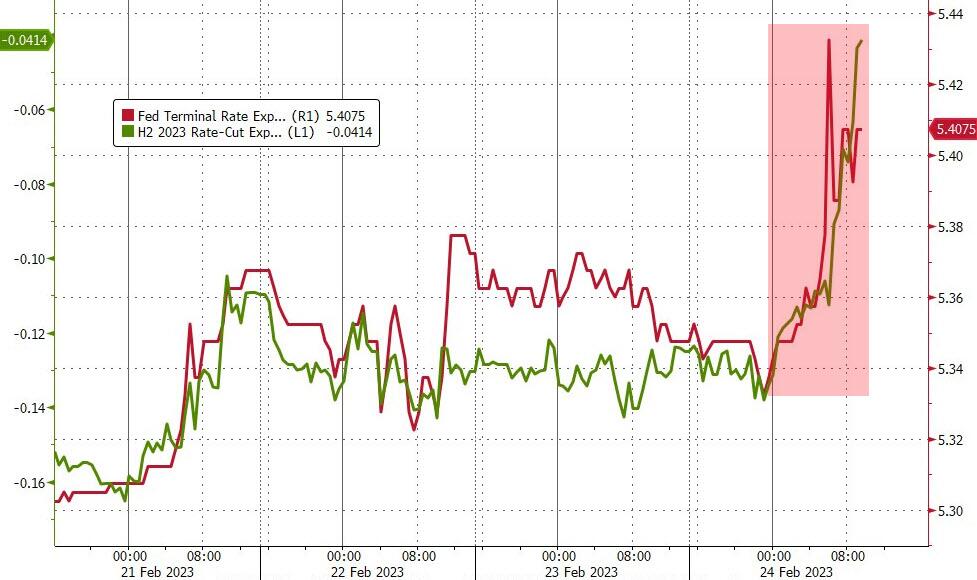

The market is no longer fighting the Fed’s higher-for-longer narrative as it used to. After back in January pricing in more than a half percentage point of easing by year-end, money markets now see around 18 basis points of cuts by December. BBG

The ECB may need to deliver significant interest-rate increases also in the second quarter, according to Bundesbank President Joachim Nagel. BBG

Europe should be closer to agreeing on a new set of fiscal rules in March, according to Economy Commissioner Paolo Gentiloni who expects diverging views on debt flexibility to be resolved shortly. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly rangebound after the choppy but positive performance on Wall St where markets spent most of the session recovering from the initial data-induced selling. ASX 200 was positive with the index led by outperformance in tech although gains are limited amid another batch of earnings releases and continued weakness in the mining industry. Nikkei 225 outperformed as the focus centred on comments from BoJ Governor nominee Ueda at the lower house confirmation hearing in which he noted that current monetary policy is appropriate and that Japan still needs more time for inflation to sustainably hit the 2% target. Hang Seng and Shanghai Comp. were lower after a substantial liquidity drain by the PBoC and as the US looks to include Chinese companies in a fresh round of Russian sanctions, while Hong Kong underperformed amid heavy losses in tech owing to weaker earnings from NetEase.

Top Asian News

BoJ Governor nominee Ueda said current monetary policy is appropriate and that Japan still needs more time for inflation to sustainably hit the 2% target, while he added it is appropriate to continue monetary easing from now on. Ueda stated that if trend inflation improves significantly, the BoJ needs to move toward monetary policy normalisation but if it does not improve, the BoJ must consider ways to maintain YCC while being mindful of market distortions. He also stated that the BoJ won’t conduct bond-selling operations and if it were to normalise policy, it would likely do so by raising interest paid to reserves parked with the central bank. Furthermore, he said must think about what to do with ETF holdings if the BoJ were to exit easy policy but now is not the time to do so and said the BoJ will stop massive bond buying if the 2% target is met.

BoJ Deputy Governor nominee Uchida said uncertainty regarding Japan’s economy is very high and BoJ must support Japan’s economy by maintaining ultra-easy policy, while he added it is wrong to tweak monetary policy just to address side effects and the right approach is to come up with ways to mitigate side-effects and effectively maintain current policy.

BoJ Deputy Governor nominee Himino said it is important to conduct economic policy flexibly and that current monetary policy is appropriate, while he added that they must aim for structural rises in wages. Furthermore, Himino said uncertainty over the global economy is very large and that they need to continue monetary easing for now.

European bourses are contained/slightly firmer, Euro Stoxx 50 +0.1%, with fresh drivers limited as the focus is on geopolitics and upcoming US data. Sectors are predominantly in the green, with Construction names bolstered post-Saint Gobain while Basic Resources lag slightly given recent commodity action. Stateside, futures are softer but with the ES still above 4k, the NQ -0.7% is the laggard following some recent pressure in the fixed income complex.

Top European News

Former UK PM Johnson has refused to support PM Sunak’s Brexit deal, which poses a major blow to Downing Street’s hopes of avoiding a Eurosceptic Conservative rebellion, according to The Telegraph.

ECB’s Nagel says the latest data shows core inflation is still too high, stopping tightening soon would be a cardinal sin. Cannot exclude more and significant hikes beyond March. Cannot rule out that headline inflation has plateaued, too speculative to say.

FX

The DXY remains firmer on the session though the upside has peaked at a 104.74 session high with Thursday’s high at 104.78 just above.

Action which comes to the modest detriment of peers, with the JPY lagging as nominee Ueda said the BoJ’s current policy is appropriate, with USD/JPY above 135.00 from a 134.07 base.

In close proximity to the JPY are the antipodeans, with the AUD affected by Yuan action and has slipped below 0.68 vs USD while the NZD remains just above 0.62, aided by RBNZ commentary.

EUR and GBP are the relative outperformers with catalysts light thus far and the EUR unreactive to German data or ECB’s Nagel while Sterling awaits BoE’s dove Tenreyro late-doors; holding around/above 1.06 and 1.20 respectively.

PBoC set USD/CNY mid-point at 6.8942 vs exp. 6.8948 (prev. 6.9028)

Fixed Income

Core benchmarks are little changed on the session, having seemingly faded after being unable to test Monday’s peak or Friday’s high, with some pre-PCE action perhaps factoring.

USTs are in-fitting directionally but are modestly negative on the session with yields elevated across the curve ahead of a busy afternoon agenda with the potential for month-end demand later also worth bearing in mind.

Specifically, Bunds, Gilts and USTs have peaked at 135.20, 102.67 and 111.19 respectively.

Commodities

WTI and Brent are firmer on the session with the April contracts residing around/just above Thursday’s peaks of USD 75.99/bbl and USD 82.77/bbl respectively.

Both TTF and Henry Hub gas contracts are firmer thus far, following a settlement in excess of 6% for Henry Hub on Thursday.

Spot gold is essentially unchanged on the session as while the USD remains firmer it is yet to advance significantly from early European morning levels; circa. USD 10/oz shy of Thursday’s USD 1833/oz peak which itself is just below the 10-DMA of USD 1836/oz.

Geopolitics

Ukrainian President Zelensky said the military situation in the south is quite dangerous in some places and is very difficult in the east, according to Reuters.

White House said the US will announce sanctions against Russian individuals and entities on Friday which will affect the banking, defence and tech sectors, while National Security Adviser Sullivan said G7 sanctions being announced on Friday will include countries that are trying to backfill products being denied to Russia.. Subsequently, US is to increase tariffs on 100 Russian metals, minerals and chemical products worth circa. USD 2.8bln; announces USD 2bn in security aid to Ukraine; announces export control measures against 90 Cos that support Russia’s defence sector..

China’s Foreign Ministry released a paper regarding China’s position on the political solution to the Ukraine crisis which noted respect for the sovereignty of all countries and that regional security cannot be guaranteed by strengthening or expanding military blocs, while it also called for a cease-fire (which would see Russian troops remaining in in Ukraine territory) to prevent Ukraine crisis from further aggravating or getting out of control. Furthermore, it stated that dialogue and negotiation are the only viable ways to resolve the crisis and that nuclear weapons should not be used in the Ukraine war. The proposal was quickly rebuffed by US National Security Advisor Jake Sullivan

EU delegation head in China said China should fulfil its responsibility to defend the UN Charter in the face of Russian aggression and that China’s position paper on Ukraine is not a peace proposal, while Ukraine’s Charge D’affaires said that they have a peace plan which they hope China supports and would like to see China do more to end the war.

French Finance Minister Le Maire said the G20 must condemn Russia’s aggression against Ukraine and must condemn Russia at the finance level, while he added Europe is thinking and working on new sanctions on Russia.

US Event Calendar

08:30: Jan. Personal Income, est. 1.0%, prior 0.2%

Personal Spending, est. 1.4%, prior -0.2%

Real Personal Spending, est. 1.1%, prior -0.3%

PCE Deflator MoM, est. 0.5%, prior 0.1%

PCE Deflator YoY, est. 5.0%, prior 5.0%

PCE Core Deflator MoM, est. 0.4%, prior 0.3%

PCE Core Deflator YoY, est. 4.3%, prior 4.4%

10:00: Jan. New Home Sales MoM, est. 0.7%, prior 2.3%

Jan. New Home Sales, est. 620,000, prior 616,000

10:00: Feb. U. of Mich. Sentiment, est. 66.4, prior 66.4

Feb. U. of Mich. Current Conditions, est. 72.7, prior 72.6

Feb. U. of Mich. Expectations, est. 62.5, prior 62.3

Feb. U. of Mich. 1 Yr Inflation, est. 4.2%, prior 4.2%

Feb. U. of Mich. 5-10 Yr Inflation, est. 2.9%, prior 2.9%

11:00: Feb. Kansas City Fed Services Activ, prior -11

Fed speakers

10:15: Fed’s Jefferson, Mester discuss paper on managing disinflation

10:15: Fed’s Mester Speaks on Panel at New York Conference

11:30: Fed’s Bullard Discusses Inflation

13:30: Fed’s Collins gives recorded remarks at US Monetary Policy For

13:30: Fed’s Waller discusses inflation

DB’s Jim Reid concludes the overnight wrap

It’s a sobering double anniversary today as it marks 1 year to the day that Russia invaded Ukraine and 3 years to the day that we saw the first big covid related sell-off after Italian cases spiked over the prior weekend. The world has been forever changed by those events with the full implications likely to reverberate for many years to come.

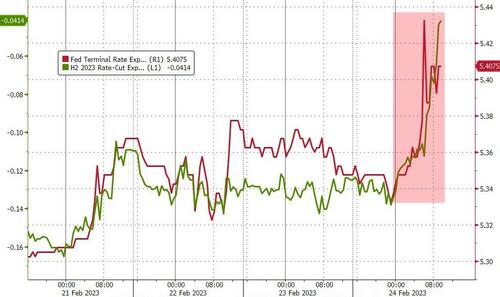

Indeed the aftershocks are still being felt every day in markets (good and bad). This has continued this week, with intraday volatility remaining high. Risk assets whipsawed yesterday, with the S&P 500 up nearly +1.0% in early trading before selling off -1.5% in the late US morning following further upward revisions to inflation data in the US and Europe. However that marked the high in yields for the day and a fixed income rally back lifted tech stocks, and in the end the S&P broke a 4-day losing streak to close up +0.53% with the NASDAQ at +0.72% ahead of today’s important PCE print.

There was some speculation that a portion of the post US midday rally was due to delta hedging effects as the S&P 500 traded through the 4000 level, with 0DTE (zero days to expiry) options being partially blamed. There is increasingly higher trading volumes of options on their expiry days than in the past. These options may have been listed at any point but trading activity has increased in options that are set to expire on the day recently. The uptick in interest of these contracts seems to be able to move markets considerably in both directions.

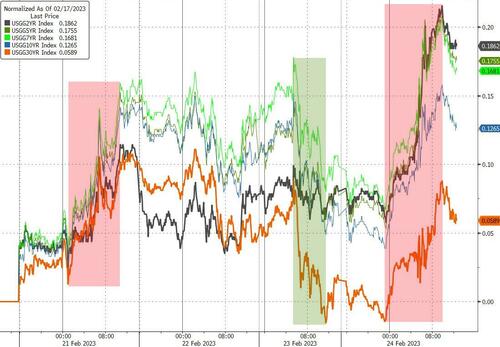

The rally also came as the terminal fed funds rate fell -2.0bps off its cycle highs to finish at 5.347 and US yields continued to fall lower after trading above 3.97% on an intraday basis for the first time since November. They then reversed course to end the day -3.9bps lower at 3.877%. And it was a similar story in Europe, with yields on 10yr bunds (-4.2bps), OATs (-4.5bps) and BTPs (-7.8bps) all moving lower.

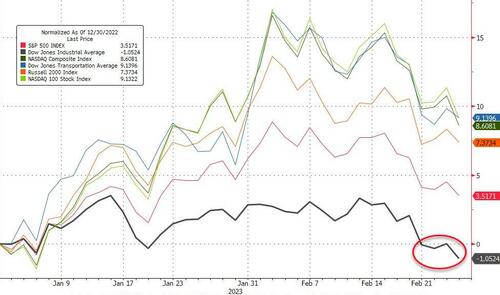

Back to equities and Nvidia (+14.02%) was the strongest performer in the entire S&P 500 following their revenue forecast the previous day that beat estimates. On the back of Nvidia’s results, Semiconductors (+5.13%) were the best performing S&P industry followed by cyclicals such as Transports (+1.46%) and Energy (+1.27%). In the meantime, European equities managed to post a small gain for the day, with the STOXX 600 up +0.06%.

In terms of the various data releases yesterday, the first was in the Euro Area, where the core inflation print for January was revised up to +5.3% (vs. +5.2% previously). That’s a new record since the Euro Area’s formation back in 1999, and offers further support for the ECB’s hawks as they look to take rates higher. Indeed, it also leans into our economists’ new ECB call from earlier in the week (link here), where they now see the terminal deposit rate going up to 3.75% at the June meeting.

Just as European inflation was being revised higher, there were also positive upward revisions to the Q4 numbers from the US. For instance, the PCE inflation measure targeted by the Fed rose by an annualised +3.7% in Q4, up from +3.2% previously. So just as with the CPI revisions, this is confirming that the inflation slowdown in Q4 was much smaller than previously thought. Likewise with the core PCE print, the Q4 number was revised up to an annualised +4.3% (vs. +3.9% before). The more important release on this front is today’s US core PCE deflator with DB and consensus at +0.5% m/m compared to a +0.3% reading last month. The accompanying personal income data sees a very a strong +1.0% m/m consensus expectation, while our economists are expecting growth of +0.6% m/m vs. +0.2% previously. DB’s economists expect a +1.3% monthly increase in consumption compared to a 1.4% consensus estimate and -0.2% reading last month.

Also yesterday we received the latest US initial jobless claims data with the week ending February 18 coming in at 192k (vs. 200k expected), while continuing claims was at 1654k (vs. 1700k expected). The rolling 3-month level of continuing claims is now back to rather benign levels, which puts further pressure on the Fed as the labour market continues to look robust through various lenses.

Gilts were a bit of an underperformer yesterday, with the 10yr yield ‘only’ down -1.3bps on the day after spending nearly the entire session in positive territory. That was after comments from the BoE’s Mann, one of the biggest hawks on the MPC, who said “I believe that more tightening is needed, and caution that a pivot is not imminent”. In addition, she said that “I don’t think we are in a restrictive stance particularly”. That led investors to almost fully price in a 25bp move at the next meeting in March, which would take the Bank Rate up to 4.25% if realised.

Asian equity markets are mostly struggling this morning even with the rally back in the US. As I type, the Hang Seng (-1.41%) is the biggest underperformer, dragged lower by declines in Chinese listed tech stocks while the CSI (-1.01%), the Shanghai Composite (-0.70%) and the KOSPI (-0.55%) are also edging lower. Elsewhere, the Nikkei (+1.10%) is bucking the regional negative trend after the incoming Bank of Japan (BOJ) head Kazuo Ueda, in his statement to lawmakers, lent his support for the current monetary policy stance while indicating that inflation is likely to rise gradually. Outside of Asia, US stock futures are indicating a slightly negative bias with those on the S&P 500 (-0.11%) and NASDAQ 100 (-0.24%) edging lower. Meanwhile, yields on the 10yr USTs (-1.16bps) are slightly lower, trading at 3.87%.

Coming back to Japan, data this morning showed that the core consumer inflation excluding food hit a 41-year high of +4.2% y/y in Japan (v/s +4.3% expected), rising from a +4.0% annual gain seen in December. It was the 9th consecutive month that core consumer inflation stayed above the BOJ’s 2% target. Headline came in as expected at 4.3%. So no surprises and an on message Kazuo Ueda probably reduces the near-term risk of an imminent surprise BoJ YCC move.

In other news yesterday, Bloomberg reported that the search for the Fed’s next Vice Chair was narrowing as the Biden administration looks to replace Lael Brainard, who’s now director of the National Economic Council. According to Bloomberg, the “top tier” candidates were Harvard professor Karen Dynan and Northwestern professor Janice Eberly, with an announcement “possible in the coming weeks.” Both have previous experience in government too, with each having served as Assistant Secretary of the Treasury for Economic Policy under President Obama. However, the article also mentioned that others were in “serious contention”, including the new Chicago Fed President, Austan Goolsbee, who previously served as Chair of the Council of Economic Advisers under President Obama.

On that theme of appointments, it was separately announced that the United States would be nominating Ajay Banga to be the next President of the World Bank. Banga previously served as CEO of Mastercard for a decade. The US has usually chosen the World Bank President and is the largest shareholder of the World Bank, but in practice they require support from other countries, so it could be some months before we officially know the next president.

To the day ahead now, and data releases from the US include January numbers on personal income, personal spending for January, the core PCE deflator and new home sales. We’ll also get the University of Michigan’s final consumer sentiment index for February. Otherwise from central banks, we’ll hear from the Fed’s Jefferson, Mester, Bullard, Collins and Waller, along with the BoE’s Tenreyro.

.

AND NOW NEWSQUAWK (EUROPE/REPORT)

DXY bid, USTs slightly softer and US equities edging lower pre-PCE/Fed speak – Newsquawk US Market Open

FRIDAY, FEB 24, 2023 – 06:30 AM

European bourses are contained/slightly firmer, with fresh drivers limited as the focus is on geopolitics and upcoming US data.

Stateside, futures are softer but with the ES just above 4k, the NQ is the laggard following some recent pressure in the fixed income complex.

DXY remains firmer on the session though is yet to meaningfully advance higher, to the mixed fortune of peers with JPY lagging post-Ueda while EUR & GBP are flat.

EGBs are little changed having faded from a failed test of recent peaks while USTs are slightly negative pre-PCE/Fed speak.

Crude continues to consolidate while metals are generally rangebound.

US has announced new Russian sanctions, affecting metals, minerals and chemicals alongside measures on Cos supporting their defence sector.

Looking ahead, highlights include US PCE Price Index, New Home Sales, US President Biden visiting Europe, Speeches from BoE’s Tenreyro, Fed’s Collins, Mester, Jefferson, Bullard & Waller.

Or why not try Newsquawk’s squawk box free for 7 days?

EUROPEAN TRADE

EQUITIES

European bourses are contained/slightly firmer, Euro Stoxx 50 +0.1%, with fresh drivers limited as the focus is on geopolitics and upcoming US data.

Sectors are predominantly in the green, with Construction names bolstered post-Saint Gobain while Basic Resources lag slightly given recent commodity action.

Stateside, futures are softer but with the ES still above 4k, the NQ -0.7% is the laggard following some recent pressure in the fixed income complex.

The DXY remains firmer on the session though the upside has peaked at a 104.74 session high with Thursday’s high at 104.78 just above.

Action which comes to the modest detriment of peers, with the JPY lagging as nominee Ueda said the BoJ’s current policy is appropriate, with USD/JPY above 135.00 from a 134.07 base.

In close proximity to the JPY are the antipodeans, with the AUD affected by Yuan action and has slipped below 0.68 vs USD while the NZD remains just above 0.62, aided by RBNZ commentary.

EUR and GBP are the relative outperformers with catalysts light thus far and the EUR unreactive to German data or ECB’s Nagel while Sterling awaits BoE’s dove Tenreyro late-doors; holding around/above 1.06 and 1.20 respectively.

PBoC set USD/CNY mid-point at 6.8942 vs exp. 6.8948 (prev. 6.9028)

Core benchmarks are little changed on the session, having seemingly faded after being unable to test Monday’s peak or Friday’s high, with some pre-PCE action perhaps factoring.

USTs are in-fitting directionally but are modestly negative on the session with yields elevated across the curve ahead of a busy afternoon agenda with the potential for month-end demand later also worth bearing in mind.

Specifically, Bunds, Gilts and USTs have peaked at 135.20, 102.67 and 111.19 respectively.

WTI and Brent are firmer on the session with the April contracts residing around/just above Thursday’s peaks of USD 75.99/bbl and USD 82.77/bbl respectively.

Both TTF and Henry Hub gas contracts are firmer thus far, following a settlement in excess of 6% for Henry Hub on Thursday.

Spot gold is essentially unchanged on the session as while the USD remains firmer it is yet to advance significantly from early European morning levels; circa. USD 10/oz shy of Thursday’s USD 1833/oz peak which itself is just below the 10-DMA of USD 1836/oz.

Former UK PM Johnson has refused to support PM Sunak’s Brexit deal, which poses a major blow to Downing Street’s hopes of avoiding a Eurosceptic Conservative rebellion, according to The Telegraph.

ECB’s Nagel says the latest data shows core inflation is still too high, stopping tightening soon would be a cardinal sin. Cannot exclude more and significant hikes beyond March. Cannot rule out that headline inflation has plateaued, too speculative to say.

DATA RECAP

UK GfK Consumer Confidence (Feb) -38 vs. Exp. -43.0 (Prev. -45.0)

German GfK Consumer Sentiment (Mar) -30.5 vs. Exp. -30.4 (Prev. -33.9, Rev. -33.8)

German GDP Detailed QQ SA (Q4) -0.4% vs. Exp. -0.2% (Prev. -0.2%); YY NSA (Q4) 0.3% vs. Exp. 0.5% (Prev. 0.5%)

NOTABLE US HEADLINES

US Assistant Secretary for Economic Policy Ben Harris is planning to leave, according to Axios.

US and China are to hold deputy-level bilateral discussions today on debt issues and sustainable finance, according to Reuters sources.

US Treasury Secretary Yellen says the Inflation Reduction Act is not a subsidy war with Europe, not trying to steal jobs. Soft landing for the US economy is possible.

Ukrainian President Zelensky said the military situation in the south is quite dangerous in some places and is very difficult in the east, according to Reuters.

White House said the US will announce sanctions against Russian individuals and entities on Friday which will affect the banking, defence and tech sectors, while National Security Adviser Sullivan said G7 sanctions being announced on Friday will include countries that are trying to backfill products being denied to Russia.. Subsequently, US is to increase tariffs on 100 Russian metals, minerals and chemical products worth circa. USD 2.8bln; announces USD 2bn in security aid to Ukraine; announces export control measures against 90 Cos that support Russia’s defence sector..