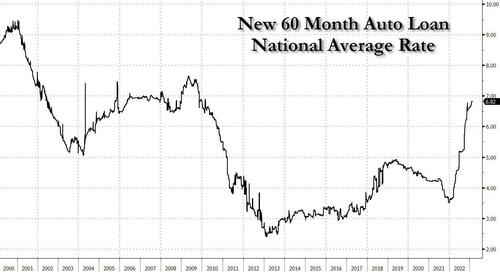

MARCH 3//GOLD CLOSED UP $14,10 TO $1848.50/SILVER CLOSED UP 67 CENTS TO $21.16//PLATINUM CLOSED UP $17.00 TO $979.00 WHILE PALLADIUM CLOSED UP $10.70 TO $1456.15/ COVID UPDATES//DR PAUL ALEXANDER//VACCINE IMPACT//SLAY NEWS//UKRAINE VS RUSSIA: BUKHMUT SURROUNDED AND MAY RETREAT//RIFT INSIDE OPEC MAY CAUSE OIL TO FALL//IN THE USA MORTGAGE READS CLIMB ABOVE 7%//USA SERVICE PMI INCREASES SIGNIFY STAGLATION COMING//TECH LAYOFFS CONTINUE//SUBPRIME AUTO LOANS INCREASE IN DEFAULTS//SWAMP STORIES FOR YOU TONIGHT//

Bitcoin: afternoon price: $22,345 DOWN 1121 dollars

Platinum price closing $979.00 UP $17.00

Palladium price; closing $1456.15 UP $10.70

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,520.74 UP $23.92 CDN dollars per oz

BRITISH GOLD: 1539.15 UP 1.27 pounds per oz

EURO GOLD: 1743.70 UP 9.73 euros per oz

COMEX DATA

EXCHANGE: COMEX

CONTRACT: MARCH 2023 COMEX 100 GOLD FUTURES SETTLEMENT: 1,833.500000000 USD INTENT DATE: 03/02/2023 DELIVERY DATE: 03/06/2023 FIRM ORG FIRM NAME ISSUED STOPPED323 C HSBC 133 363 H WELLS FARGO SEC 89 365 H MAREX CAPITAL M 2 435 H SCOTIA CAPITAL 5 624 C BOFA SECURITIES 19 624 H BOFA SECURITIES 84 657 C MORGAN STANLEY 17 657 H MORGAN STANLEY 280 661 C JP MORGAN 17 227 690 C ABN AMRO 6 726 C CUNNINGHAM COM 8 737 C ADVANTAGE 12 48 800 C MAREX SPEC 5 5 880 C CITIGROUP 24 880 H CITIGROUP 1 905 C ADM 33 1TOTAL: 508 508

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR MAR/2023. CONTRACT: 1508 NOTICES FOR 50,800 OZ or 1,6126 TONNES

total notices so far: 2110 contracts for 211,000 oz (6.5629 tonnes)

SILVER NOTICES: 146 NOTICE(S) FILED FOR 730,000 OZ/

total number of notices filed so far this month : 2684 for 15,420,000 oz

END

GLD

WITH GOLD UP $14.10

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD//// NO CHANGES TONNES OF GOLD OUT OF THE GLD/

INVENTORY RESTS AT 912.69TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 67 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 479.063. MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 2137 CONTRACTS TO 121,299 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE FAIR SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR SMALL $0.16 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. WE HAVE NOW SURPASSED OUR PREVIOUS ALL TIME LOW OF 124,080 OI CONTRACTS RECORDED FEB 22/2023. THUS NEW LOW COMEX OI SILVER IS NOW SET AT 121,299 MARCH 3/2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.16). AND WERE SUCCESSFUL IN KNOCKING SOME SPEC LONGS, AS WE HAD A HUGE LOSS ON OUR TWO EXCHANGES 1387 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 750 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.58 MILLION OZ FOLLOWED BY TODAY’S EFP TO LONDON OF 595,000 OZ//NEW STANDING: 14.275 MILLION OZ + THE 1.0 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 15.275 MILLION OZ/ //// V) FAIR SIZED COMEX OI LOSS/ SMALL SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL 82 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 3 days, total 1426 contracts: OR 7.130 MILLION OZ . (475 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 7.130 MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 7.130 MILLION OZ//INITIAL

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2137 WITH OUR $0.16 LOSS IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 750 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAR OF 15.58 MILLION OZ FOLLOWED BY TODAY’S 595,000 E.F.P. JUMP TO LONDON (WHICH REDUCES THE AMOUNT OF SILVER STANDING) + 1.0 MILLION OF EXCHANGE FOR RISK ISSUED (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 15.275 MILLION OZ .. WE HAVE A HUGE SIZED LOSS OF 1387 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 146 NOTICE(S) FILED TODAY FOR 730,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 5346CONTRACTS TO 436,462 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 279 CONTRACTS.

.

WE HAD A GOOD SIZED INCREASE IN COMEX OI ( 5346 CONTRACTS) DESPITE OUR $4.00 LOSS IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 4.9953 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 8,900 OZ (0.2468 TONNES) //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London).

YET ALL OF..THIS HAPPENED WITH OUR $4.00 LOSS IN PRICEWITH RESPECT TO THURSDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 7642 OI CONTRACTS (23,77 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2296 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 436,462

IN ESSENCE WE HAVE A STRONG INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7642 CONTRACTS WITH 5346CONTRACTS INCREASED AT THE COMEX AND 2296 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 7642 CONTRACTS OR 23.77 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2296 CONTRACTS) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI (5346) TOTAL GAIN IN THE TWO EXCHANGES 7642 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR MAR. AT 4.9953 TONNES FOLLOWED BY TODAY’S 8900 OZ QUEUE JUMP//NEW STANDING 6.8087 TONNES // ///3) ZERO LONG LIQUIDATION //4) GOOD SIZED COMEX OPEN INTEREST GAIN// 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

TOTAL EFP CONTRACTS ISSUED:8632 CONTRACTS OR 863,200 OZ OR 26.85 TONNES 3 TRADING DAY(S) AND THUS AVERAGING: 2877 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES 26.85 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 26.85/3550 x 100% TONNES 0.7563% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 26.85 TONNES/INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A GIGANTIC SIZED 2137 CONTRACTS OI TO 121,299 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A RECORD LOW OF 121,299 CONTRACTS MARCH 3/2023.

EFP ISSUANCE 750 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 750 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 750 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2055 CONTRACTS AND ADD TO THE 750 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE LOSS OF 1387 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES //6.935 MILLION OZ

OCCURRED WITH OUR $0.16 LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED UP 17,74 PTS OR 0.54% //Hang Seng CLOSED UP 138.08 PTS OR 0.68% /The Nikkei closed UP 428.60% PTS OR 1.56% //Australia’s all ordinaries CLOSED UP 0.32% /Chinese yuan (ONSHORE) closed UP 6.9067 //OFFSHORE CHINESE YUAN UP TO 6.9148// /Oil UP TO 77,85 dollars per barrel for WTI and BRENT AT 84.28 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 5346 CONTRACTS UP TO 436,462 DESPITE OUR LOSS IN PRICE OF $4.00.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAR… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2296 EFP CONTRACTS WERE ISSUED: : APRIL 2296 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2296 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 7642 CONTRACTS IN THAT 2296LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI GAIN OF 5346CONTRACTS..AND THIS VERY STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $4.00. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAR (6.8087) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 6.8087 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $4.00) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED GAIN OF 7642 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 23.77 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAR. (4.9953 TONNES) FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 8900 OZ (0.276 TONNES)… ALL OF THIS WAS ACCOMPLISHED WITH OUR FALL IN PRICE TO THE TUNE OF $4.00.

WE HAD -279 CONTRACTS REMOVED FROM COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 7642 CONTRACTS OR 764,200 OZ OR 23.77 TONNES

Total monthly oz gold served (contracts) so far this month

2110 notices 211,000 6.5629 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 1

i) Into Brinks: 28,141.38 oz

real gold entering

total dealer deposit: 28,141.38 oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 0

total withdrawals: nil oz

in tonnes: 0 tonnes

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 587 contracts having LOST 51 contracts. We had 140 notices filed yesterday so we

gained another 89 notices or an additional 8900 oz will stand for metal at the comex

April lost 675 contracts down to 322,863 contracts

May gained 10 contracts to stand at 55

We had 508 notice(s) filed today for 50,800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 7 notices were issued from their client or customer account. The total of all issuance by all participants equate to 508 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer notice(s) was (were) stopped 7127 Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR. /2023. contract month,

we take the total number of notices filed so far for the month (2110 x 100 oz ), to which we add the difference between the open interest for the front month of (MAR. 587 CONTRACTS) minus the number of notices served upon today 508 x 100 oz per contract equals 218,900 OZ OR 6.8047 TONNES the number of TONNES standing in this active month of MARCH.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (2110 x 100 oz+ 587 OI for the front month minus the number of notices served upon today (508)x 100 oz} which equals 218,900 oz standing OR 6.8047 TONNES in this active delivery month of MARCH..

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,630,976.622 OZ

TOTAL REGISTERED GOLD: 10,917,912.41 (339,59 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 10,713,064.511 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,128,183 OZ (REG GOLD- PLEDGED GOLD) 283.92 tonnes//dropping like a stone

END

SILVER/COMEX

MAR 3/2023// THE MARCH 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

600,140.580 oz

Deposits to the Dealer Inventory

nil

Deposits to the Customer Inventory

3095.152 oz Delaware

No of oz served today (contracts)

146 CONTRACT(S) (730,000 OZ)

No of oz to be served (notices)

171 contracts (855,000 oz)

Total monthly oz silver served (contracts)

2684 contracts (13,420,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into Delaware: 3095.152 oz

Total deposits: 3095.152 oz

JPMorgan has a total silver weight: 147.648 million oz/286.950 million =51.43% of comex .//dropping fast

Comex withdrawals: 1

i) Out of Loomis 600,140.580 oz

Total withdrawals; 600,140.58 oz

adjustments: 2

customer to dealer

Loomis: 5068.800 oz

and

dealer to customer

Brinks: 49,373.410 oz

oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 39.239MILLION OZ (declining rapidly).TOTAL REG + ELIG. 286.950 million oz

CALCULATION OF SILVER OZ STANDING FOR MAR

silver open interest data:

FRONT MONTH OF MAR/2023 OI: 317 CONTRACTS HAVING LOST 481 CONTRACT(S.) WE HAD 362 NOTICES FILED

YESTERDAY, SO WE LOST A HUGE 119 CONTRACTS OR AN ADDITIONAL 595,000 OZ WILL NOT STAND AND THESE GUYS DECIDED FOR AN E.F.P. JUMP TO LONDON AS OBVIOUSLY THEY COULD NOT SECURE ANY SILVER OVER HERE.

April LOST 15 CONTRACTS TO STAND at 405.

May LOST 1776 CONTRACTS DOWN TO 105,344.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 146 for 730,000 oz

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 2684 x 5,000 oz = 13,420,000 oz

to which we add the difference between the open interest for the front month of MAR(317) and the number of notices served upon today 146 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2023 contract month: 2684 (notices served so far) x 5000 oz + OI for the front month of MAR (317) – number of notices served upon today (146) x 500 oz of silver standing for the MAR. contract month equates 14.275 million oz +the 1.0 million oz of exchange for risk//new total standing 15.275 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

FEB 8/WITH GOLD UP $6.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 920.82 TONNES

FEB 7/WITH GOLD UP $5.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.92 TONNES

FEB 6/WITH GOLD UP $3.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.24 TONNES

FEB 3/WITH GOLD DOWN $52.55 TODAY: STRANGE: BIG CHANGES AGAIN IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 920.24 TONNES

FEB 2/WITH GOLD $10.95 TODAY: BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 918.50 TONNES

FEB 1/WITH GOLD DOWN $2.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 31/WITH GOLD UP $6.55 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 30/WITH GOLD DOWN $6.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 918.50 TONNES

JAN 27/WITH GOLD DOWN $0.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 919.37 TONNES

JAN 26/WITH GOLD DOWN $11.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 919.37 TONNES

JAN 25/WITH GOLD UP $7.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 917.34 TONNES

JAN 24/WITH GOLD UP $7.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 23/WITH GOLD UP $0.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.63 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 20/WITH GOLD UP $4.75 TODAY;BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 912.43 TONNES

JAN 19/WITH GOLD UP $16.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES INTO THE GLD///INVENTORY RESTS AT 910.98TONNES

JAN 18/WITH GOLD DOWN $1.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.9 TONNES FROM THE GLD////INVENTORY RESTS AT 909.24 TONNES

JAN 17/WITH GOLD DOWN $11.45 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.14 TONNES

JAN 13/WITH GOLD UP $22.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD///INVENTORY RESTS AT 912.14 TONNES

JAN 12/WITH GOLD UP $20.55 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 912.43 TONNES

JAN 11/WITH GOLD UP $1.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

GLD INVENTORY: 912.69 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 479.063 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

Rickards: One Of The Biggest Propaganda Campaigns Ever…

It’s extremely difficult to find the truth about the war in Ukraine.

The first reason for this is because… it’s a war.

Wars are always difficult to gauge in real-time.

The phrase “fog of war” was invented to convey the uncertainty and imprecision about the progress of any particular war.

Still, there’s another reason the war in Ukraine is confusing for so many.

It’s because the Ukrainian propaganda effort is one of the most astonishingly effective concoctions of lies ever seen.

From the “Ghost of Kyiv” fighter ace to the “Heroes of Snake Island” to wildly exaggerated claims of Russian casualties to the suppression of any news that reflects badly on Ukraine, the Ukrainian propaganda machine has been firing on all cylinders.

This might be expected given that President Zelenskyy is a former actor and comedian. He’s used to the media stage and making up scenes for the audience. Zelenskyy is backed up by a small army of media advisers and amplified by sympathizers including President Biden, U.K. Prime Minister Rishi Sunak and outlets like The New York Times.

Courage Under (Phony) Fire

The latest propaganda stunt was Joe Biden’s trip to Kyiv a few days before the first anniversary of the Russian invasion. Biden made a canned speech, authorized another $500 million in weapons and hopped back onto a train to Poland.

The propaganda pièce de résistance was when Biden and Zelenskyy walked into an open courtyard and the Kyiv air raid sirens began blaring. The Russians had been advised in advance that Biden would be there, and they agreed not to stage any raids during Biden’s visit.

In fact, there had been no raids for some time. No one saw any planes, drones or missiles. The sirens were just a stage effect intended to create a false sense of danger to be picked up as a soundtrack by global media.

Ukraine is losing the war badly but you can’t blame Westerners for believing otherwise. They’re all victims of the Zelenskyy-Ukraine propaganda machine.

What about the sanctions? How are they working out?

Sorry, but I Was Right

U.S. and EU sanctions on Russia because of Ukraine have been worse than a complete failure. They have failed to change Russia’s behavior, have failed to hurt Russia’s economy in a material way and have boomeranged to hurt the U.S., Europe and many Western financial institutions.

I wrote about this last year in March and April not long after the war began. My comments were greeted with skepticism (at best) and extreme criticism (at worse). No matter. I was right then and the evidence since has been overwhelming.

The Russian ruble is stronger today than before the war began. Russian oil and gas revenue is higher than it was before the war. Russian oil is being sold at a discount to India and China, but Russia is making up the discount in increased volume.

The Russian economy was only down about 3% in 2022 (earlier estimates expected it to fall around 20% or more), and the Russian economy is expected to show modest growth this year versus likely recessions in the U.S. and Europe. Russia and China are far along in developing an interoperative payments and settlement system for international transactions that will replace the SWIFT system that Russia was ejected from.

Actually damaging Russian institutions is extremely difficult because Russia has spent years preparing for just such a financial attack from the United States. Its banks are robust with good liquidity and access to interbank facilities, even without the benefit of SWIFT or Western correspondents.

Meanwhile, Russia continues to destroy the Ukrainian army with missiles from North Korea, drones from Iran and its own massive industrial capacity.

The Only Card the U.S. Can Play

So Ukraine is losing on the battlefield and the U.S.-led sanctions regime against Russia has failed. The only U.S. response is to escalate the conflict.

The escalation of U.S. weaponry provided to Ukraine is stunning. We started with Stinger surface-to-air missiles to shoot down Russian aircraft, and Javelin missiles, which are potent anti-tank weapons (although the British NLAW system being used in Ukraine is apparently better).

Next, we provided the HIMARS, which is a long-range heavy artillery piece with precision-guided shells. Ukraine has used it to good effect, although it seems the Russians have developed means to counter it.

Contrary to what the propaganda machine says, the Russians aren’t idiots. In fact, the very head of Ukraine’s military has said that “all military science is located in Russia.”

Anyway, since the delivery of HIMARS, the U.S., the U.K. and Germany have pledged to provide top-of-the-line tanks including the U.S. Abrams tank, the U.K. Challenger 2 and the German Leopard 2. Incidentally, there are unconfirmed reports that some Leopards are now appearing on the battlefield.

Then, without skipping a beat, Ukraine’s President Zelenskyy demanded F-16 fighter jets. Biden said no, but he also said no to tanks at first. It’s likely just a matter of time before he approves the F-16s.

All of this has been backed up with billions of dollars of intelligence, surveillance and communications systems designed to spot Russian targets and direct the application of U.S. weapons.

That’s to say nothing about the actual presence of NATO forces on the ground in Ukraine. Some sources indicate that as many as 20,000 Polish troops are on the front lines dressed in Ukrainian uniforms, making them foreign mercenaries. U.S. and U.K. forces are also on the ground there not in uniform, which is a violation of the Geneva Conventions.

Of course, this is no secret to the Russians. They recently warned us to withdraw all NATO personnel and equipment from Ukraine. If we don’t, the Russians renewed the warning that they could become legitimate targets.

Ukraine Is Losing

Still, none of this assistance has been particularly effective. Ukraine is losing the war badly as Russia slowly and methodically wears down Ukrainian forces along a broad front. Russia nearly has the strategically important city of Bakhmut encircled and will probably have it completely cut off before long, trapping 20,000–30,000 Ukrainian soldiers.

The loss of Bakhmut will be a significant defeat for Ukraine, as it will significantly weaken their defense line in the Donbas. They really only have one defense line to fall back to, and it’s notably weaker than the line they’re currently fighting to hold.

If Russia eventually manages to break through that last line, there’s very little between that line and the Dnieper River to stop them.

None of this is an indictment of the Ukrainian military, by the way. They’ve fought hard and bravely, and continue to do so. It’s just that they’re facing a superior force that significantly outnumbers them in tanks, aircraft, artillery and, importantly, ammunition. They’re simply outgunned.

Where’s the Cavalry?

Meanwhile, many of the weapons pledged (including the tanks) have not actually arrived and may not be ready for six months or more. Ukraine could sure use them now!

The F-16s in particular are a pipe dream because Ukrainian pilots don’t know how to fly them, and training can take almost a year. It’s possible that NATO pilots could secretly pilot them, but just think of the Russian propaganda victory if they shoot down and capture NATO pilots who aren’t supposed to be flying over Ukraine.

Still, apart from their effectiveness, another question arises. Can the U.S., the U.K. and Germany actually afford to provide these weapons without damaging their own readiness in the event of wars elsewhere?

The fact is Western arsenals have been badly depleted because of the weapons and ammunition provided to Ukraine. The European arsenals were not large to begin with, but even the U.S. supplies dropped into the danger zone. The situation is worse than that because the shortages cannot be made up quickly.

The U.S. has shut down many ammunition factories since the Cold War ended. These can be restarted but full wartime mobilization takes years, not weeks. World War II is a good example.

By 1943, the U.S. was producing wartime aircraft at a rate of almost 100,000 planes per year. But in 1941, that number was only 18,000. The Ford Motor Co. basically stopped automobile production and converted its huge River Rouge factory to aircraft production for the duration.

That fivefold increase in fighters and bombers took two years to achieve. It was not done in months. It’s fair to ask if this war is worth it in broad terms.

It’s even more pointed to ask if it’s worth jeopardizing U.S. national security by running down vital inventories of weapons to prop up a corrupt oligarchy in Eastern Europe.

The American people may discover the hard way that the answer to both questions is no.

END

3. Chris Powell of GATA provides to us very important physical commentaries//

Your weekend reading material

(courtesy Alasdair Macleod)

Alasdair Macleod: Interest rates are the silent killer

Submitted by admin on Thu, 2023-03-02 11:32Section: Daily Dispatches

By Alasdair Macleod GoldMoney, Toronto Thursday, March 2, 2023

This article is about why interest rates and bond yields are rising and why they will continue to rise, threatening to undermine the entire Western banking system.

Rising bond yields are deferring the prospect of a central bank pivot away from fighting inflation to tackling a widely expected recession. Anyway, these expectations wrongly assume that price inflation will fall in a recession, leading to lower interest rates.

History tells us that monetary debasement, rising prices, and a slump in business activity go together. Indeed, a slump in economic activity is almost certain, but interest rates will continue to rise, reflecting declining purchasing power for fiat currencies. There is nothing the monetary authorities can do to prevent it, and consequently a cyclical banking crisis, this time including both central and commercial banking systems, is bound to result.

In this article I point out the consequences of not understanding the true role of interest rates, the fallacies surrounding commodity price formation, and why a general glut cannot happen, which according to the Keynesians drives recessions.

Blaming inflation on Russia or other external forces cuts no ice. Our crisis is entirely of our own making. Rising interest rates are our silent killer. …

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.9067

OFFSHORE YUAN: 6.9148

SHANGHAI CLOSED UP 17.74 PTS OR 0.54%

HANG SENG CLOSED UP 138,08 PTS OR 0.68%

2. Nikkei closed UP 428.60 PTS OR 1.56%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 104.91 Euro RISES TO 1.0608 UP 8 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.500!!(Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 136.21/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.723%***/Italian 10 Yr bond yield RISES to 4.554%*** /SPAIN 10 YR BOND YIELD RISES TO 3.750…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.457//(ITALY WORSE THAN GREECE?)

3j Gold at $1845.95//silver at: 21.09 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 12/100 roubles/dollar; ROUBLE AT 75.44//

3m oil into the 77 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 136.21/10 YEAR YIELD AFTER BREAKING .54%, REMAINS AT .5000% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9394–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9964well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.016% DOWN 6 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.949 DOWN 7 BASIS PTS//INVERTED TO THE 10 YEAR!!

USA 2 YR BOND YIELD: 4.871 DOWN 3 BASIS PT

USA DOLLAR VS TURKISH LIRA: 18,90…

GREAT BRITAIN/10 YEAR YIELD: 3.918% UP 4 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

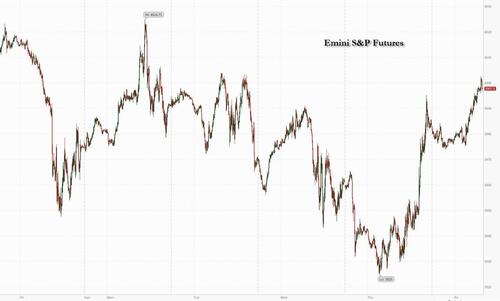

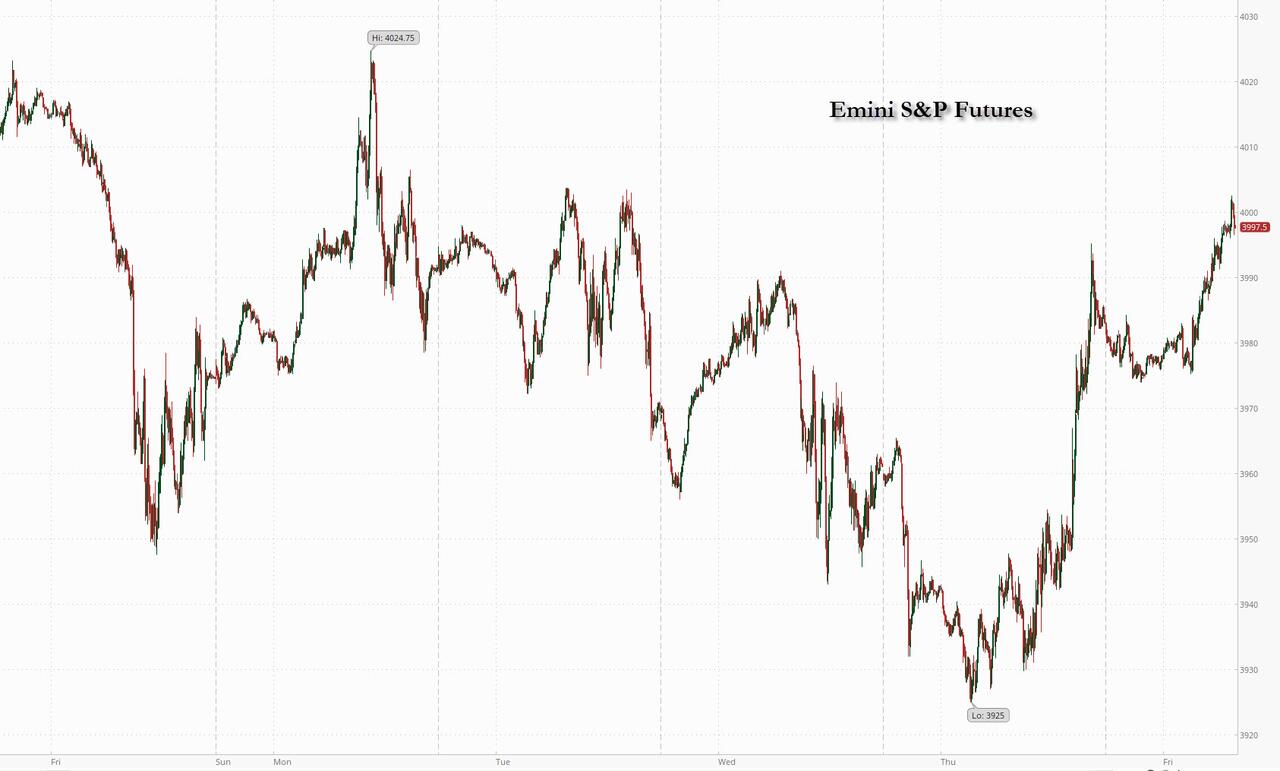

S&P Futures Rebound To 4,000 As Yields, Dollar Slide

FRIDAY, MAR 03, 2023 – 08:10 AM

Yesterday Goldman said that if stocks averted a Thursday slide they looked poised for a rebound as the selling pressure would slowly abate, and sure enough early Friday seems to validate that with US index futures extending yesterday’s rebound and set for the first weekly gain in four as Treasury yields slumped across the board with the benchmark 10-year rate briefly dipping below 4% after rising to 4.08% yesterday, and the dollar slid as traders assessed the outlook for the economy and path of Federal Reserve rate hikes. Contracts on the S&P 500 and Nasdaq 100 each edged about 0.3% higher at 7:30am in New York after the underlying benchmarks gained 0.8% and 0.9% respectively on Thursday, following a powerful intraday rebound sparked by borderline dovish comments from Fed’s Bostic (who just a day earlier slammed stocks with his hawkish words).

In premarket trading, Hewlett Packard and Tesla gained about 2%: the former boosted its forecast for the quarter, while data showed a rise in Tesla’s vehicle shipments from China last month. Marvell Technology slumped 8.5% after the chipmaker’s guidance fell short of expectations, though analysts think estimates are now bottoming out and remain positive on the longer-term outlook for the firm. Here are the other notable premarket movers:

Dell Technologies shares fell 3.7% in US premarket trading, with analysts cutting their price targets on the stock after the computer company’s outlook disappointed as demand for PCs falter against a difficult economic backdrop.

Zscaler shares declined 12% after the software company reported its second-quarter results and gave an outlook. While analysts are broadly positive on the report, they noted some signs of weakness in billings.

C3.ai shares jumped 16% after forecasting revenue for the fourth quarter that topped the average analyst estimate. CEO Thomas Siebel noted a “dramatic change” in business sentiment compared with mid-2022.

Elastic shares fall 3.2% after the software company reported third-quarter results that were seen as mixed, with higher-than-expected earnings, but a weaker outlook than the company previously guided for.

ChargePoint shares decline 11% after the electric-vehicle charging company gave a first-quarter revenue forecast that is much weaker than expected.

Keep an eye on Apple after Morgan Stanley said the stock has five under-appreciated catalysts that can drive a re-rating over the next 12 months, reiterating it as top pick and raising PT to $180 from $175.

US stocks climbed on Thursday, putting the S&P 500 on track for a small weekly gain, as investors focused on a comment by Atlanta Fed President Raphael Bostic that the central bank could be in a position to pause rate hikes sometime this summer. But other hawkish Fedspeak is keeping investors relatively cautious as they await ISM services date due later for further clues about the health of the economy. On Thursday Fed Governor Christopher Waller said he’d favor raising interest rates even more than his current outlook if economic indicators continue to come in hotter than expected.

“There is a cohort of investors who think the Fed may have to hike a lot more and that’s why interest rates are rising as much as they have recently,” Priya Misra, global head of rates strategy at TD Securities, said on Bloomberg Television. On Thursday, she recommended investors double down on buying 10Y TSYs (as covered here).

Data earlier this week showed continued labor market resilience in the world’s largest economy, supporting the case for the Federal Reserve to keep tightening policy, a theme that pushed almost every major asset into the red in February. However, stocks have managed to hold their own so far in March, despite a series of hot inflation readings and strong labor market prints that caused investors ramp up bets on where interest rates might peak. But while this lifted 10-year Treasury yields to three-month highs, analysts noted that the economic resilience is also propping up corporate balance sheets. Risk sentiment also received a boost on Friday from forecast-beating factory data from China.

“US stocks will be in a trading range squeezed between weakening growth and declining earnings,” said Rajeev De Mello, a global macro portfolio manager at GAMA Asset Management. “On the positive side, getting closer to the end of rate hikes, and only a moderate recession.” The end of “a necessary bear market” will coincide with an upsurge in stress in credit markets that could stem from private equity or the impact of slumping house prices in US, UK, Canada, Australia and New Zealand, Michael Hartnett wrote in a note (more in a follow-up post). Until then, cash is as good as bonds and stocks, he said.

“Short-term, equity markets seem to be more focused on a soft landing (for the economy) than they are on the cost pressures,” said Luke Hickmore, investment director at abrdn. While money markets now see US interest rates rising to about 5.5% by September, Hickmore reckons “markets are overpricing Fed and UK central bank policy-rate peaks, I think the policy peak comes earlier.”

European stocks are rising and on course for a weekly gain as investors focus on evidence of stronger economic output rather than the prospect of ongoing monetary tightening. The Stoxx 600 is up 0.6% with miners, tech and autos the strongest-performing sectors. Here are the most notable European movers:

European semiconductor stocks ASML, ASM International rise as much as 2.1% and 2.9% respectively, as Broadcom predicts a “soft landing” as companies spend on corporate networking infrastructure.

SAP shares rise as much as 2.4% as Morgan Stanley says the firm is its top European software-sector pick, following an analysis of subscription transition trends in the industry.

London Stock Exchange shares rise as much as 3.2% after JPMorgan analysts led by Enrico Bolzoni said their conviction in the overweight recommendation on the stock has increased following the exchange operator’s presentation.

Lufthansa shares climb as much as 6.2% to the highest since February 2020 after the German carrier guides for a “significant improvement” in adjusted Ebit in 2023, suggesting that consensus estimates will be raised, according to Bernstein.

Universal Music shares fall as much as 4.4%, the most since October, as a solid set of operating results for the record label is offset by one-offs related to share-based compensation and FX headwinds for its earnings outlook.

Admiral shares fall as much as 3% after Citi cut the recommendation to neutral from buy on the more cautious outlook for the UK motor space, with margin pressure building across the industry.

Pearson shares fall as much as 3.6%, as the education-publishing firm’s profit beat and predictions of continued sales growth for this year were likely tempered by expectations of revenue declines in its Higher Education unit. Citi also highlighted Pearson’s failure to announce a buyback.

Ferragamo shares fall as much as 3.1% after the Italian luxury company said 2023 will be a complex year of transition in a tougher macro environment. While turnaround stories in the luxury sector seem to be resonating with investors this year, Ferragamo is the outlier, analysts say.

Earlier in the session, Asian stocks headed for their first weekly gain in a month after a Federal Reserve official made dovish comments and traders stayed alert for any supportive measures that may come from China’s upcoming political meeting. The MSCI Asia Pacific Index rose as much as 1.1% on Friday, lifted by energy and industrial shares. Japanese stocks led gains in the region after a report showed the nation’s unemployment rate reached the lowest level in three years. Shares in India and Hong Kong also climbed.

Onshore Chinese stocks eked out a small gain before the National People’s Congress this weekend. Some investors have trimmed their expectations for further stimulus given China’s faster-than-expected economic recovery. “What we hope to see out of the NPC is further liberalization of market,” Julia Raiskin, Citigroup head of Asia Pacific markets, told Bloomberg Television. Most clients are still on the fence given the geopolitical concerns and uncertainty around US monetary policy, Raiskin added. Asia’s stock benchmark headed for a weekly gain of more than 1% after Atlanta Fed president Raphael Bostic said he’s “firmly” in favor of sticking with quarter-point interest rate hikes. Other central-bank officials in recent days have reinforced their hawkish rhetoric, keeping equity bulls in check.

Japanese equities rose with the benchmark Topix Index hitting its highest level since Jan. 2022 as investors assess dovish comments by a Fed official, suggesting a potential slowdown in US rate hikes. The Topix Index rose 1.3% to 2,019.52 as of market close Tokyo time, while the Nikkei advanced 1.6% to 27,927.47. Daiichi Sankyo Co. contributed the most to the Topix Index gain, increasing 5.1%. Out of 2,160 stocks in the index, 1,702 rose and 351 fell, while 107 were unchanged. Japanese benchmarks have been beating global peers this year, thanks in part to the high proportion of value stocks. The MSCI Japan Index has gained 6.9% versus a 3.5% advance for the index provider’s broadest regional benchmark. nvestors expect Tokyo Stock Exchange’s push for better corporate governance to lead to some big share price moves. In addition, higher interest rates are starting to be priced in and BOJ governor nominee Kazuo Ueda’s dovish stance are also becoming a tailwind for local companies, JPMorgan’s chief Japan equity analyst Rie Nishihara wrote in a note Thursday. “US market closed strong and Japanese value stocks are showing solid performance, lifting the index up,” said Hajime Sakai, chief fund manager at Mito Securities. “The TSE policy continues to be a positive influence on Japanese equities, and the market is awaiting BOJ’s meeting next week.”

Indian stocks rallied the most in more than three months as a rebound in Adani Group firms boosted investor sentiment. The S&P BSE Sensex rose 1.5% to 59,808.97 in Mumbai, while the NSE Nifty 50 Index advanced 1.6% as both measures rose most since Nov. 11. For the week, the gauges are up 0.6% and 0.7%, respectively. Adani Enterprises, the flagship firm of the ports-to-power conglomerate, led a rally in 10 group companies as US-based GQG Partners invested about $1.9 billion in four of its firms, a key signal that the embattled conglomerate’s efforts to win investor confidence is gaining traction. “We expect the markets to have a short-term bounce back due to increased optimism, but are still concerned about global interest rates and higher valuations, which can lead to increased medium-term volatility,” Axis Securities Chief Investment Officer Naveen Kulkarni said. All of BSE Ltd.’s 20 sector gauges rose on Friday, led by an index of services sector companies, while for the week realty firms were the top gainers. Banks were among prominent gainers on Friday as stake buys in Adani stocks tapered recent concerns over the sector’s exposure to the conglomerate. Reliance Industries contributed the most to the index gain on Friday, increasing 2.5%.

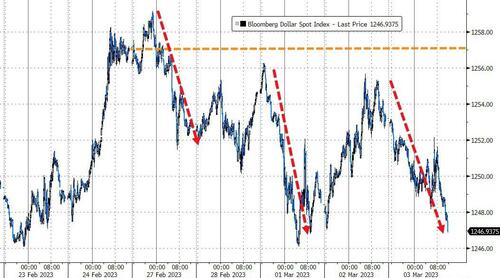

In FX, the Bloomberg Dollar Spot Index fell 0.3% as it continued a one day up and then next day down pattern. It’s set for a 0.6% drop this week, its first weekly decline since January. The greenback weakened against all of its Group-of-10 peers, with the Swiss franc and the Australian dollar as the top performers

The euro advanced to trade above the $1.06 handle. European bonds advanced with Treasuries, led by the long ends.

Gilt yields eased as much as 5 basis points across the curve, with money markets now seeing the BOE rate peaking at 4.76% in November, 4 basis points below Thursday’s close

Japan’s 10-year bond yield for some time rose above the central bank’s policy ceiling for the first time since Feb. 22 ahead of BOJ Governor Haruhiko Kuroda’s last policy meeting next week. The yen strengthened amid broad weakness in dollar after data suggested inflationary pressures remain strong in Tokyo. One-week implied volatility in dollar- yen rallied, in line with the roll, as the tenor now captures the BOJ meeting

Australia’s dollar rose as market sentiment was lifted by data showing a strong rebound in China’s services activity in February. Bonds trimmed losses. The Caixin China services PMI rose to 55 in February, from 52.9 the prior month, hitting the highest level since August 2022

In rates, Treasuries rallied across the curve, mostly unwinding Thursday’s selloff and matching similar gains in bunds during European morning. Long-end outperformance pushed inverted 5s30s spread to a new YTD low. Yields are richer by 2bp to 6bp across the curve with intermediates out to long-end outperforming, flattening 2s10s, 5s30s spreads by ~2bp on the day; 5s30s touched -34.2bp. 10-year yields hover around 4%, down ~5bp vs Thursday’s close and outperforming bunds by 2bp. No strong catalyst for Treasuries advance as selloff takes a breather; Thursday saw all yields top 4% for the first time since November, following an upward revision to the fourth-quarter unit-labor-costs growth rate. German 10-year yields snapped a five-day rising streak to slip three basis points. Focal points of US session include ISM services report and a handful of Fed speakers.

In commodities, crude futures decline with WTI falling roughly 0.4% to trade near $77.80. Spot gold rises roughly 0.6% to trade around $1,846. Bitcoin

Elsewhere, Bitcoin slumped 4.4% to the lowest level in more than two weeks on wider retreat in the crypto markets as investors assessed the fallout of crypto-friendly US bank Silvergate Capital Corp.

Looking to the day ahead now, and data releases include the global services and composite PMIs for February, and the ISM services index from the US. We’ll also get the Euro Area PPI reading for January. From central banks, we’ll hear from the Fed’s Logan, Bostic and Bowman, as well as ECB Vice President de Guindos, and the ECB’s Holzmann, Vasle, Muller and Wunsch. Finally in the political sphere, US President Biden and German Chancellor Scholz will be meeting at the White House.

Market Snapshot

S&P 500 futures up 0.1% to 3,988.75

MXAP up 1.1% to 161.28

MXAPJ up 0.8% to 523.68

Nikkei up 1.6% to 27,927.47

Topix up 1.3% to 2,019.52

Hang Seng Index up 0.7% to 20,567.54

Shanghai Composite up 0.5% to 3,328.39

Sensex up 1.5% to 59,816.36

Australia S&P/ASX 200 up 0.4% to 7,283.57

Kospi up 0.2% to 2,432.07

STOXX Europe 600 up 0.7% to 463.02

German 10Y yield little changed at 2.71%

Euro up 0.2% to $1.0619

Brent Futures little changed at $84.77/bbl

Gold spot up 0.6% to $1,846.59

U.S. Dollar Index down 0.32% to 104.69

Top Overnight News from Bloomberg

The ECB’s planned half-point increase in interest rates this month will probably be followed by more hikes, with borrowing costs to remain elevated for a while, according to Governing Council member Madis Muller

ECB Governing Council member Pierre Wunsch said market bets for interest rates to reach a 4% peak may prove accurate if underlying price pressures remain elevated

ECB Governing Council member Bostjan Vasle says he expects an interest-rate hike at this month’s policy meeting to be followed by “additional increases”

Sweden’s PMI services fell to 45.7 in February, led by the subindexes of orders received and employment, according to data published on Friday. That was the weakest showing since May 2020 and also the first time since the Covid-19 crisis that the index signals a contraction

Russia will reduce the amount of foreign currency it plans to sell through early April as energy revenues show signs of stabilizing despite restrictions imposed over its invasion of Ukraine

China’s central bank Governor Yi Gang signaled monetary policy will largely be stable this year, saying interest rates in the economy are appropriate, inflation will remain under control and the currency’s volatility wasn’t a concern

Turkey’s opposition is in crisis over a failure to agree on a joint candidate to contest President Recep Tayyip Erdogan, hampering a rare chance to unseat the country’s longest-serving leader at elections in less than three months

Traders in options on South Africa’s rand are starting to bet that King Dollar’s best days are over. The cost of hedging against rand declines, as measured by the premium of options to sell the currency over those to buy it, fell to about 190 basis points on Friday, according to data compiled by Bloomberg. That’s less than half the long-term average, and the lowest since early 2006, when the rand was buoyed by the commodities super-cycle that peaked two years later

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mostly higher amid tailwinds from the US where risk appetite was bolstered by comments from Fed’s Bostic that they could be in a position to pause by mid-to-late summer and as the region also digested further strong Chinese Caixin PMI data. ASX 200 was led by strength in telecoms, healthcare and financials albeit with gains limited ahead of next week’s RBA meeting where the central bank is widely expected to hike again. Nikkei 225 outperformed after recent data which showed Tokyo-area headline and core inflation began to soften and the Unemployment Rate edged lower, while a recent source report noted that the BoJ is to prefer watching how the impact of earlier policy tweaks works out for now. Hang Seng and Shanghai Comp. gained after strong Caixin Services and Composite PMI data which showed the fastest pick-up in activity since August. However, upside was capped heading into China’s ‘Two Sessions’ where participants will be eyeing a major overhaul of President Xi’s leadership team and the Government Work Report including this year’s official growth target, while US-China frictions continued to linger with the Biden administration adding 28 Chinese entities to the US trade blacklist.

Top Asian News

PBoC Governor Yi said they will keep the yuan exchange rate and prices stable, while he added that the yuan has become more flexible and helps stabilise the economy. Yi stated they will safeguard the bottom line for preventing systemic risks and will support the healthy development of platform companies. Yi also noted that China’s real interest rates are at an appropriate level now and using RRR to release long-term liquidity will still be an effective tool for the economy, according to Reuters.

PBoC Deputy Governor Liu said China’s economy is improving but there are still uncertainties and they will adjust policy in a timely way, but will not resort to flood-like stimulus and will steer monetary policy based on domestic conditions.

US President Biden’s administration added 28 Chinese entities to the US trade blacklist, according to a filing cited by Reuters. US Commerce Department later confirmed that it added 37 entities to the entities list with many of them from China, while the additions were due to nuclear and missile-related activities, supporting China’s military, human rights violations and support for the Russian military.

Japan’s Chief Cabinet Secretary Matsuno says they will consider taking necessary steps to curb inflation, incl. using the reserve budget.

China’s two-session will commence at 07:00GMT/02:00EST on March 4th and end on March 13th.

European bourses are firmer across the board, Euro Stoxx 50 +0.9%, in a continuation of the firmer Wall St./APAC handover. Sectors are predominantly in the green with Media lagging post-UMG while Basic Resources outperforms amid benchmark/overnight action while Tech recoups as yields ease. Stateside, futures are all in the green though only modestly so vs Europe, with the ES having eclipsed Thursday’s peak but is yet to convincingly test 4k.

Top European News

ECB’s Wunsch said the ECB could consider raising its key interest rate to as high as 4% if underlying inflation remains persistently high and noted if core inflation remains above 5% and there is no clear signal it is going down, they would have to do more, according to Reuters.

ECB’s Vasle expects March rate hike to be followed by additional hikes.

ECB’s de Guindos believes headline inflation will continue to decline, and around mid-year it could fall under 6%; says however core inflation could have a more stable performance.

ECB’s Muller says it is most likely that the March rate hike is not the last; rates will have to stay high for some time; core inflation is more worrisome than headline inflation.

UK Chancellor Hunt is set to extend GBP 2,500 energy price guarantee for an additional three months, according to The Times.

FX

The DXY is under pressure with G10 peers firmer across the board as UST yields ease across the curve following Thursday’s Fed commentary, DXY at the lower-end of 104.64-104.98 parameters.

Given the yield action, the CHF is the main beneficiary vs the USD and also against the EUR, with EUR/CHF pulling further back from parity to near-0.9950.

EUR is bid, though to a lesser extent than peers, following a mixed bag of final PMIs and in particular markedly softer January PPI, though hawkish ECB speak has helped to pare the PPI pullback; EUR/USD around 1.0628 high vs 1.0596 low.

GBP benefits from favourable PMI revisions and EUR/GBP action; currently, Cable is at 1.20 though is yet to convincingly test the figure.

USD/JPY is neared to 136.00 vs the 136.77 high after firmer-than-expected Tokyo CPI while the antipodeans are bolstered to a similar degree despite softer data prints.

PBoC set USD/CNY mid-point at 6.9117 vs exp. 6.9132 (prev. 6.8808)

Fixed Income

Benchmarks are firmer across the board as yields continue to pullback in an extension of APAC action with EZ PPI data assisting.

Specifically, Bunds have eclipsed Thursday’s 132.13 peak by a handful of ticks, though 2.70% in the 10yr yield is proving sticky; the periphery is bid to a slightly larger extent, though BTPs have pulled-back from best levels to 112.00.

Stateside, USTs are at the top-end of 110.15+ to 111.00 parameters with yields lower across the curve and action currently most pronounced at the long-end ahead of multiple Fed speakers and S&P Global & ISM PMIs.

Commodities

Crude benchmarks have been choppy, indecisive and rangebound throughout APAC and European hours, residing within sub-USD 1/bbl parameters.

Specific developments have been somewhat limited while we await a full readout from Putin’s Security Council meeting after limited Kremlin commentary.

PetroChina International executive said China gas demand is expected to pick up in 2023 from last year’s level but does not expect a quick rebound in China LNG imports this year if spot prices are as high as last year, while they expect business as usual in Russia-China gas trade, according to Reuters.

BoE on LME Clear: “Collectively, these reviews pointed to several shortcomings across LME Clear’s governance, management and risk management capabilities”. Click here for more detail.

China state planner NDRC says experts suggest strengthening regulation and supervision of the iron ore market to curb unreasonable price increases.

Nat Gas futures diverge between the US and Europe given the weekly inventory data and weather/reduced demand factoring respectively.

Spot gold is modestly firmer given the softer USD and as the yellow metal extends incrementally above its USD 1844/oz 21-DMA, while base metals are supported by the broader risk tone.

Geopolitics

US senior official said Ukraine will be a major topic in talks between US President Biden and German Chancellor Scholz, while the leaders are also expected to discuss challenges posed by China. Furthermore, the US has so far not seen that China has provided lethal aid to Russia and it is engaging with partners in Europe on sanctions against third countries aiding Russia, according to Reuters.

Russian Kremlin says that Russia will take measures to prevent a repeat of the border incursion on Thursday by Ukraine-backed nationalists.

US Event Calendar

09:45: Feb. S&P Global US Composite PMI, prior 50.2

09:45: Feb. S&P Global US Services PMI, est. 50.5, prior 50.5

10:00: Feb. ISM Services Index, est. 54.5, prior 55.2

ISM Services Employment, prior 50.0

ISM Services New Orders, prior 60.4

ISM Services Prices Paid, prior 67.8

Fed speakers:

11:00: Fed’s Logan Makes Opening Remarks at Event

12:00: Fed’s Bostic Discusses Racial Inequality Research

15:00: Fed’s Bowman Chairs Panel at Conference

DB’s Jim Reid concludes the overnight wrap

I hope the parents amongst you survived World Book Day yesterday where schools here in the UK make you send your child to school in a costume that reflects their favourite book. It seems to be getting more competitive each year and a parental arms race has developed. I tried to send my twins as “Irrational Exuberence” by Robert Shiller and “This time is different – Eight centuries of financial folly” by Reinhart and Rogoff. However my wife decided Harry Potter was more appropriate.

Back in muggle land it’s been more of the same for markets over the last 24 hours, as a fresh bond selloff took place after several data prints suggested that rate hikes still had further to go. Indeed, the day brought a number of new milestones, since 10yr Treasury yields closed above 4% for the first time since November, whilst Fed funds futures even priced a 5.5% terminal rate on an intraday basis, marking a new high for this cycle, before closing at c.5.45%. Meanwhile in Europe, sovereign bonds lost ground for a 5th day running, taking the 10yr bund yield up to its highest level since 2011. US equities did recover from early losses though with the S&P 500 ending up +0.76%.

Once again, the tone was set from the morning, with the Euro Area flash CPI release for February coming in above expectations. Headline CPI was at +8.5% (vs. +8.3% expected), but the more important point was that core CPI hit +5.6% (vs. +5.3% expected), which is the fastest core inflation on record since the formation of the single currency. This added to the growing evidence that Europe’s inflation problem has long since broadened out from just being an energy issue, and the reading will embolden the hawks on the Governing Council to keep taking rates higher. Our economists published a blog last night “An uncomfortable inflation surprise for the ECB” where they outline the problems for the council and how there is upside risk to our 3.75% terminal view. See here for more.

This narrative about higher inflation was then given further support from US data releases later in the session. In particular, unit labour costs in Q4 were revised up to show an annualised +3.2% increase, which is a substantial revision from the +1.1% rate that had been previously reported. And at the same time, the data on weekly initial jobless claims fell to 190k (vs. 195k expected) over the week ending February 25, suggesting that the labour market continued to remain in a very strong position.

Those data releases prompted a fresh round of losses for sovereign bonds, with Treasury yields seeing a noticeable increase after the US releases came out. By the close, the 10yr yield (+6.5bps) had risen to 4.06%, its highest level since November, just as the 2yr yield (+0.4bps) closed at 4.88%, its highest level since 2007, but lower than the 4.94% intra-day peak. 30yr yields breached 4% briefly again too. As in previous days, this increase in sovereign bond yields was driven by higher inflation expectations, with the 2yr breakeven (+6.7bps) at an 8-month high of 3.31%, and the 5yr breakeven (+6.5bps) at a 6-month high of 2.73%. This morning in Asia, 10yrs USTs are c.-1bps lower.

Back in Europe it was a very similar story, with yields on 10yr bunds (+4.0bps) hitting a post-2011 high of 2.75%. In light of the strong CPI print, the move was unsurprisingly driven by higher inflation breakevens, with the 10yr German breakeven up by +8.4bps to 2.63%, its highest level since early May. And that concern over inflation persistence was evident in Europe too, since the Euro 5y5y forward inflation swap hit its highest level in a decade at 2.56%. Elsewhere on the continent there was a sustained move higher in yields as well, with those on 10yr OATs (+4.5bps) at a post-2012 high, and those on 10yr gilts (+4.3bps) at their highest since Liz Truss was PM.

US equities were initially struggling against the twin headwinds of higher rates and the aftermath of Tesla’s investor day. However it seemed to turn when we heard from Atlanta Fed’s President Bostic post the European close. He favoured 25bps-sized hikes and saw a potential Fed pause some time in mid or late summer. Strangely this was seized on as being enough to propel stocks from declines to an S&P close of +0.76% on the day. The front end of rates markets came off their highs around the same time although the long end moved less. The Fed’s Waller later suggested that unless the next payrolls and CPI print showed some restraint, he would likely edge his terminal view up. So it was hard to see Fed speak as dovish whatever the market narrative.

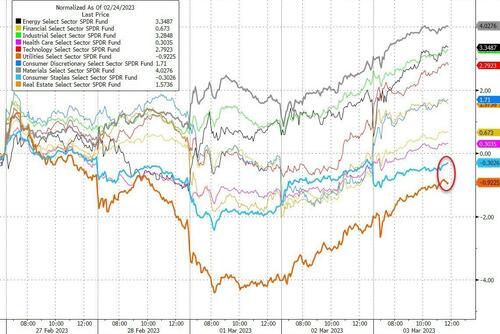

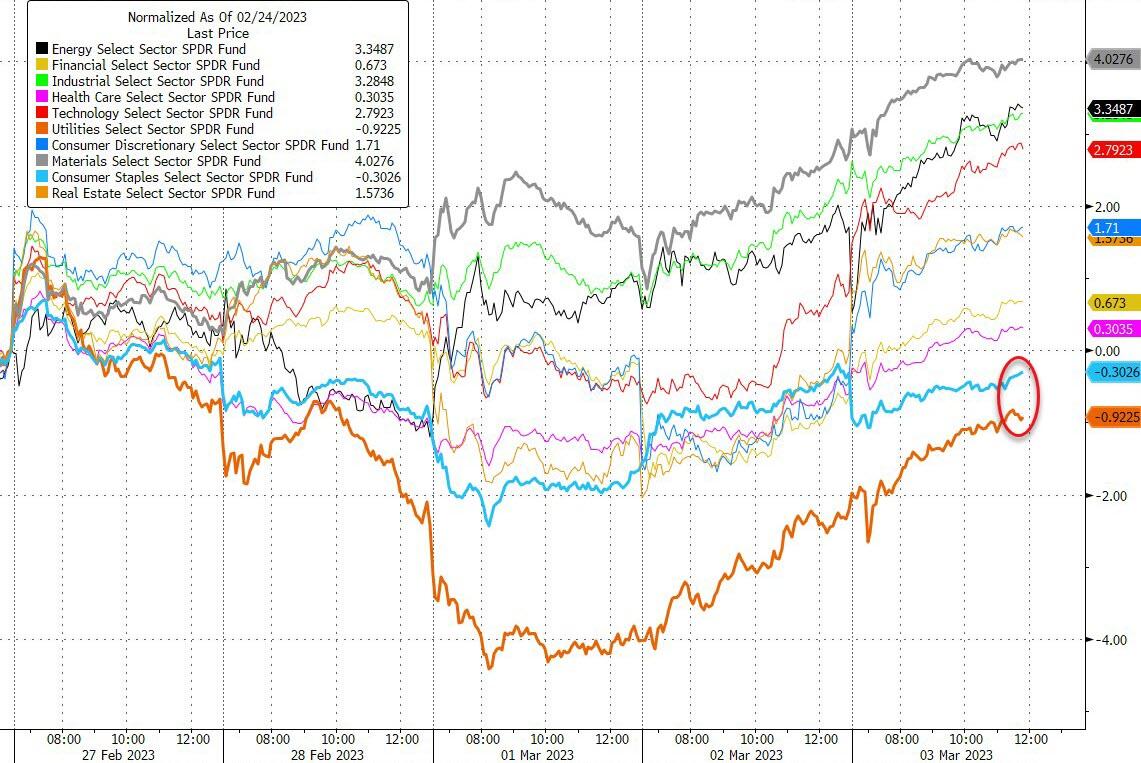

In terms of sectors, the more inflation-driven parts of the index like utilities (+1.82%), real estate (+1.22%) and staples (+1.21%) were the leading gainers, with only discretionary (-0.32%) and financials (-0.53%) in the red for the day as Tesla, the sixth largest S&P 500 stock by market cap, lost -5.85%, becoming the worst S&P 500 performer yesterday. Otherwise, more than three quarters of the index members finished in the green by the close. IT (+1.26%) was an outlier on this otherwise defensive leader board, primarily driven by Salesforce’s upbeat outlook and buyback plans that propelled the stock by +11.5% and the software index by +2.37%.

Europe also saw equity gains as the STOXX 600 (+0.51%) recovered some of the previous day’s declines, with energy (+1.69%) and more defensive staples (+1.39%) and utilities (+0.79%) lifted by higher inflation expectations. It also comes as oil prices posted further gains yesterday, with Brent crude up by +0.47% to $84.71/bbl, its highest level in two weeks.

Asian equity markets are higher this morning after a sharp recovery in China’s services sector activity (more below). As I type, the Nikkei (+1.48%) is leading gains followed by the Hang Seng (+0.71%) while the KOSPI (+0.13%), the Shanghai Composite (+0.17%) and the CSI (+0.03%) are modestly higher. In overnight trading, US equity futures are pointing to small losses with those on the S&P 500 (-0.18%) and NASDAQ 100 (-0.26%) ticking lower.

Coming back to China, we are seeing positive growth signs from the world’s second biggest economy after the services sector PMI rose sharply from 52.9 in January to a 6-month high of 55.0 in February (v/s 54.5 expected) as the removal of tough COVID-19 restrictions revived demand.

Elsewhere, Tokyo’s Core-CPI advanced +3.3% y/y in February as expected, albeit a lower print than the prior month’s +4.3% increase, indicating the effect of government subsidies which drove down soaring energy bills. Separate data showed that Japan’s jobless rate dropped to a three-year low of 2.4% in January from 2.5% in December while the jobs-to-applicants ratio fell to 1.35 from December’s 1.36, marking the first decline since August 2020. Meanwhile, Japan’s services sector in February expanded at its fastest pace since June 2022 as the final estimate of the services PMI came in at 54, higher than previous month’s reading of 52.3.

Returning back to yesterday, a more backward-looking piece of news came from the release of the ECB’s account of their February meeting. They showed that “it was generally felt that concerns of “overtightening” were premature”, and that policy rates were currently “barely consistent with the range of estimates for the neutral rate”. It also said there were “reservations” about the commitment to a 50bps move in March, but ultimately “it was seen as important to provide a firm signal of policy intentions”.

To the day ahead now, and data releases include the global services and composite PMIs for February, and the ISM services index from the US. We’ll also get the Euro Area PPI reading for January. From central banks, we’ll hear from the Fed’s Logan, Bostic and Bowman, as well as ECB Vice President de Guindos, and the ECB’s Holzmann, Vasle, Muller and Wunsch. Finally in the political sphere, US President Biden and German Chancellor Scholz will be meeting at the White House.

end

AND NOW NEWSQUAWK (EUROPE/REPORT)

Equities firmer across the board as the USD and yields ease with Fed speak/ISM ahead – Newsquawk US Market Open

FRIDAY, MAR 03, 2023 – 06:29 AM

European bourses are firmer across the board, Euro Stoxx 50 +0.9%, in a continuation of the firmer Wall St./APAC handover; US futures bid, though to a lesser extent.

DXY is under pressure with G10 peers firmer across the board as UST yields ease across the curve, CHF the main beneficiary.

Fixed income benchmarks are bid across the board as yields continue to pullback in an extension of APAC action with EZ PPI data assisting.

Crude benchmarks have been choppy, indecisive and rangebound throughout APAC and European hours, residing within sub-USD 1/bbl parameters.

Looking ahead, highlights include US Composite & Services PMIs, US ISM Services, Speeches from Fed’s Logan, Bostic, Bowman, Barkin.

Or why not try Newsquawk’s squawk box free for 7 days?

EUROPEAN TRADE

EQUITIES

European bourses are firmer across the board, Euro Stoxx 50 +0.9%, in a continuation of the firmer Wall St./APAC handover.