MARCH 29//GOLD CLOSED DOWN $4.85 TO $1967.35//SILVER HOWEVER ROSE BY 11 CENTS AS THERE ARE NO LONGER ANY SILVER LONGS TO FLEECE//PLATINUM CLOSED DOWN $10.50 TO $971.50//PALLADIUM IS UP $9.60 TO $1446.60//COVID UPDATES//GOOD COMMENTARIES FROM JOHN RUBINO AND DAVID SCHIFF//COVID UPDATES//VACCINE IMPACT//DR PAUL ALEXANDER//VACCINE IMPACT//SWAMP STORIES FOR YOU TONIGHT//VERY ABBREVIATED TODAY..

TODAY IS COMEX OPTIONS EXPIRY AND TRUE TO FORM THE CROOKS RAID SO THAT THE BANKS CAN MAKE THEIR PENNIES. THE BIGGER OTC/LONDON OPTIONS EXPIRY IS FRIDAY’

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1963.75

Silver ACCESS CLOSE: 23.33

Bitcoin morning price:, $27,261 UP 771 Dollars

Bitcoin: afternoon price: $27,120 DOWN 630 dollars

Platinum price closing $971.80 DOWN $10.50

Palladium price; closing $1446.60 UP $9.60

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2673.20 DOWN 17.63 CDN dollars per oz (ALL TIME HIGH 2732.50)

BRITISH GOLD: 1594,30 DOWN 4.900 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1811.15 DOWN 8.09 euros per oz //(ALL TIME HIGH//1860.82)

COMEX DATA EXCHANGE:

EXCHANGE: COMEX CONTRACT: MARCH 2023 COMEX 100 GOLD FUTURES SETTLEMENT:

1,972.400000000 USD INTENT DATE: 03/28/2023 DELIVERY DATE: 03/30/2023 FIRM ORG FIRM NAME ISSUED STOPPED ____________________________________________________________________________________________ 435 H SCOTIA CAPITAL 1 624 H BOFA SECURITIES 56 657 C MORGAN STANLEY 11 1 661 C JP MORGAN 43 737 C ADVANTAGE 4 ____________________________________________________________________________________________ TOTAL: 58 58 MONTH TO DATE: 6,128

END

COMEX DATA EXCHANGE:

: COMEX 868 CONTRACTS

:

JPMORGAN stopped 0/868 contracts

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR MAR/2023. CONTRACT: 58 NOTICES FOR 5800 OZ or 0.1804 TONNES

total notices so far: 6128 contracts for 612,800 oz (19.060 tonnes)

SILVER NOTICES: 21 NOTICE(S) FILED FOR 105,000 OZ/

total number of notices filed so far this month : 3181 for 15,905000 oz

END

GLD

WITH GOLD DOWN $4,85

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:////// A HUGE DEPOSIT OF 4,16 TONNES FROM THE GLD.

INVENTORY RESTS AT 927,23 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 11 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF OF 1.15 MILLION OZ FROM THE SLV: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 460,082 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A FAIR SIZED 447 TO 117,395AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS FAIR SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.28 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. WITH YESTERDAY’S READING AT THE COMEX, WE HAVE NOW SET ANOTHER RECORD LOW AT 117,395 CONTRACTS , MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.28). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A GOOD GAIN ON OUR TWO EXCHANGES 368 CONTRACTS. WE HAD 250 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 2.25 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS( 815 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.58 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S E.F.P.JUMP TO LONDON OF 10,000 OZ//NEW STANDING: 15.905 MILLION OZ + THE 2,25 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 18.155 MILLION OZ/ //// V) SMALL SIZED COMEX OI GAIN/ HUGE SIZED EFP ISSUANCE/. WE HAVE NOW REACHED THE POINT THAT THE CROOKS CANNOT LIQUIDATE ANY MORE SILVER SPEC LONGS.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –83 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 21 days, total 17,808 contracts: OR 89.040 MILLION OZ . (848 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 89.040 MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 89. 040 MILLION OZ//INITIAL//STRONG ISSUANCE BUT BELOW LAST MONTH

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 447 CONTRACTS DESPITE OUR $0.28 GAIN IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 815 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAR OF 15.58 MILLION OZ//FIRST DAY NOTICE// FOLLOWED BY TODAY’S 10,000 E.F.P. JUMP (WHICH DECREASES THE AMOUNT OF SILVER STANDING) + 2.25 MILLION OF EXCHANGE FOR RISK ISSUED EARLY IN MARCH (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 18.155 MILLION OZ .. WE HAVE A GOOD SIZED GAIN OF 368 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 21 NOTICE(S) FILED TODAY FOR 105,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 4563 CONTRACTS TO 478,611 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED-2286CONTRACTS.

WE HAD A GOOD SIZED DECREASE IN COMEX OI ( 4563 CONTRACTS) WITH OUR $19.70 GAIN IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR MAR. AT 4.9953 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 1600 OZ (0.04 TONNES) //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)YET ALL OF..THIS HAPPENED WITH OUR $19.70 GAIN IN PRICEWITH RESPECT TO MONDAY’S TRADING

WE HAD A FAIR SIZED LOSS OF 3134 OI CONTRACTS (9.748 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3066 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 478,611.

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4563 CONTRACTS WITH 4563 CONTRACTS DECREASED AT THE COMEX AND 1429 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 3134CONTRACTS OR 9.748 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1429 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (4563) //TOTAL LOSS IN THE TWO EXCHANGES 3134 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR MAR. AT 4.9953 TONNES FOLLOWED BY TODAY’S 1,600OZ QUEUE JUMP//NEW STANDING 19.0637TONNES // ///3) SOME LONG LIQUIDATION //4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

TOTAL EFP CONTRACTS ISSUED: 87,559 CONTRACTS OR 87,55,900OZ OR 272,34TONNES IN 21 TRADING DAY(S) AND THUS AVERAGING: 4169 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21TRADING DAY(S) IN TONNES 272.94 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 272.94/3550 x 100% TONNES 7.69% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 272.94 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A FAIR SIZED 447 CONTRACTS OI TO 117,395 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,685 CONTRACTS MARCH 27/2022

EFP ISSUANCE 1075 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 815 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 815 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 447 CONTRACTS AND ADD TO THE 815 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GOOD GAIN OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 368 CONTRACTS.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //2.255 MILLION OZ

OCCURRED DESPITE OUR $0.28 LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

i)WEDNESDAY MORNING//TUESSDAY NIGHT

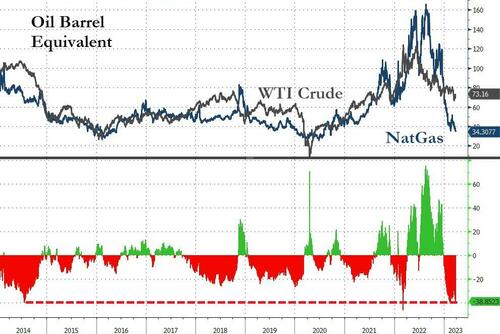

SHANGHAI CLOSED DOWN 5.32 PTS OR 0.16% //Hang Sang CLOSED UP 407.75 BPTS OR 2.06% /The Nikkei closed UP 365.53 PTS OR 1.33% //Australia’s all ordinaries CLOSED UP 0.23% /Chinese yuan (ONSHORE) closed DOWN TO 6.8875//OFFSHORE CHINESE YUAN DOWN TO 6.8963 /Oil DOWN TO 72.90 dollars per barrel for WTI and BRENT AT 78.26 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 4563 CONTRACTS DOWN TO 478,611 DESPITE OUR STRONG GAIN IN PRICE OF $19.70 ON WEDNESDAY

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAR… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1429 EFP CONTRACTS WERE ISSUED: : APRIL 1429 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1429 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR TOTAL OF 3134 CONTRACTS IN THAT 1429LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED LOSS OF 4563 COMEX CONTRACTS..AND THIS FAIR SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG GAIN IN PRICE OF $19.70 WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAR (19.0637) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $19.70 //// AND WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD OUR FAIR SIZED LOSS OF 3134 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE LOST A TOTAL OI OF 9.748 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAR. (4.9953 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 1600OZ (0.049 TONNES)… ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $19.70

WE HAD -2286 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 3134 CONTRACTS OR 313,400 OZ OR 9.748TONNES

TONNES

Estimated gold comex today 226,928/ //fair

final gold volumes/yesterday 310,938//FAIR TO GOOD

Total monthly oz gold served (contracts) so far this month

6128 notices 612800 OZ 19.060 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

I) Into Brinks: 782.370 oz

total deposits: 782.370 oz

customer withdrawals: 0

total withdrawals: NIL oz

in tonnes:

0

Adjustments; 1

i) From Manfra 32,794.02 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 59 contracts having LOST 852 contracts. We had 868 notices filed on TUESDAY so we

gained 16 contracts or an additional 1600 oz will stand for metal at the comex .

April LOST A CONSIDERABLE 26,357 contracts DOWN to 51,240 contracts. It is here that our banker friends have to worry as many will try and take delivery in this upcoming delivery month. WE HAVE 2 MORE READING DAYS BEFORE FIRST DAY NOTICE.

May GAINED 51 contracts to stand at 1273

We had 58 notice(s) filed today for 5800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 58 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR. /2023. contract month,

we take the total number of notices filed so far for the month (6128 x 100 oz ), to which we add the difference between the open interest for the front month of (MAR. 59 CONTRACTS) minus the number of notices served upon today 58x 100 oz per contract equals 612,900 OZ OR 19.0637 TONNES the number of TONNES standing in this active month of MARCH.

thus the INITIAL standings for gold for the MAR contract month:No of notices filed so far (6128 x 100 oz+ 911 OI for the front month minus the number of notices served upon today (58)x 100 oz} which equals 612,900 oz standing OR 19.0637 TONNES in this active delivery month of MARCH..

TOTAL COMEX GOLD STANDING: 19.0637 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 3181 x 5,000 oz = 15,905,000 oz

to which we add the difference between the open interest for the front month of MAR(21) and the number of notices served upon today 21 X (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2023 contract month: 3181(notices served so far) x 5000 oz + OI for the front month of MAR (21) – number of notices served upon today (21 x 500 oz of silver standing for the MAR. contract month equates 15.905 million oz +the 2.25 million oz of exchange for risk//new total standing 18.155 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 927,23 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 460.082 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Peter Schiff: Bank Regulations Aren’t The Solution; They Are The Problem

In the aftermath of the failure of Silicon Valley Bank and Signature Bank, everybody is trying to figure out what happened, who’s to blame, and what can be done to prevent it from happening again. One of the most popular “solutions” is more bank regulations. But in his podcast, Peter Schiff explained why regulations are the problem, not the solution.

During a congressional hearing on the bank failures, a common refrain from Democrats was that it was caused by “deregulation.”

Deregulation! Deregulation! Deregulation! Like the D in the regulation is the problem. The D is not the part that’s the problem. It’s the regulation that is the problem, and deregulation, to the extent that we actually had any, didn’t cause the problem. If we had any deregulation the problem is we didn’t deregulate enough.”

Politicians would have us believe that if we just had more bureaucrats overseeing banks, there wouldn’t be anything to worry about. They think that some politically connected people they appoint to a government job will somehow be so smart that they can figure out the problems and protect everybody.

They’re not. Chances are the regulators are dumber than the people that they’re regulating. Because, if the regulators were smarter, they wouldn’t be regulators. They could make a lot more money in the private sector.”

The best and the brightest aren’t the regulators. And competency isn’t generally the most important criterion in government hiring.

Also, the government sector has very little accountability.

Nobody cares. If you screw up in government, nobody loses any money. I mean, the public loses money. But the politicians don’t care about that. So, you’re never going to have the most competent people in government. That’s why you want the free market to regulate banks, as well as everything else.”

People often claim that advocates of the free market don’t want any regulation. But Peter said that’s not true. In fact, the free market is another way of regulating behavior and conduct.

You can have the government regulate, or you can have the market do it. When the market does it, it works a lot better than when the government does it. In fact, when the government basically usurps the job that would be better done by the market, they short-circuit the market safeguards. They basically prevent the markets from doing their job and regulating, and they substitute the judgment of these incompetent bureaucrats.”

So, how can the market regulate banks?

The same way the market regulates everything — competition and individual self-interest.”

In a truly free market, people wouldn’t just put their money in a bank without doing some homework.

That’s your hard-earned life savings. You’re not just going to throw it into any old bank. You’re going to do some research. And even if you’re not competent to do the research yourself, you’re going to make damn sure somebody else did the research, and you’re going to follow their lead and subscribe to that service.”

Meanwhile, banks would know this. They would value their reputation for safety and soundness. Bankers would be rewarded for sound, prudent stewardship of deposits.

I’m going to succeed as a banker by nurturing my reputation for sound, prudent banking. So, in a free market, the banks that are the most sound, the most prudent, take the fewest risks are going to be the ones that succeed because they’re going to gather the most deposits, and those riskier banks, well, they’re not going to make it. That’s the free market.”

But in a government market, the FDIC ensures all of the deposits. After the collapse of SVB and Signature Bank, the government made it clear that the insurance limits now go to infinity.

The result?

Who cares where you put your money? No bank is safer than any other bank. No matter what they do, no matter what hair-brained scheme they concoct, your money is safe.”

In effect, the government has eliminated competition based on safety and soundness. Bankers are no longer rewarded for playing it safe.

He’s not going to get any more customers by avoiding risk than he will by assuming risk because the government has taken that out of the equation. So, that is why there is so much risk. That is why the banks are so insolvent.”

The government has replaced free market regulation that would rein in risky behavior with government regulation that encourages risky behavior.

Of course, this system empowers government people. That’s why they don’t want a free market. They want to be able to appoint people of their choosing to “oversee” everything. This gives them power.

They don’t want a level playing field. They get power by tilting that playing field.”

In this podcast, Peter goes on to talk about a very interesting point that came out during the congressional hearing regarding bank “stress tests.”end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards/John Rubino

A multi-polar world is bad news for the American Empire but great news for gold…

Since the 1970s it’s been virtually impossible for a country to function without access to US dollars. And Washington maintained this highly-favorable status quo by putting various kinds of pressure — from sanctions to election theft to outright invasion — on anyone who stepped out of line.

This weaponization of the world’s reserve currency has, not surprisingly, created resentment in a lot of foreign capitals. And after a long gestation period, that resentment is now erupting into a rebellion against dollar hegemony. Among the big recent events:

The BRICS coalition has become the hottest ticket in geopolitics. Brazil, Russia, India, China, and South Africa (the BRICS) have been toying with the idea of forming a political/monetary counterweight to U.S. dominance since 2001. But beyond some aggressive gold buying by Russia and China, there was more talk than action.

Then the floodgates opened.Whether due to the pandemic’s supply chain disruptions, heavy-handed sanctions imposed by US-led NATO during the Russia-Ukraine war, or just the fact that de-dollarization was an idea whose time had finally come, the BRICS alliance has suddenly become the hottest ticket in town. In just the past year, Argentina, Indonesia, Saudi Arabia, Iran, Mexico, Turkey, the United Arab Emirates (UAE), and Egypt have either applied to join or expressed an interest in doing so. And new bilateral trade deals that bypass the dollar are being discussed all over the place.

Combine the land mass, population, and natural resources of the BRICS countries with those of the potential new members and the result is more or less half the world. And now things are getting real:

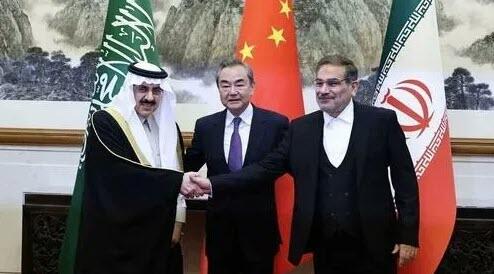

China brokers a peace deal between Saudia Arabie and Iran, two bitter historical enemies who want to join the BRICS alliance but can’t if they’re in an undeclared war. Should they stop competing and start cooperating they could dominate the Middle East and raise China’s clout in the region, at the petrodollar’s expense. An example of the press coverage:

Eurasia’s geo-economic integration took a great leap forward as a result of the Iranian–Saudirapprochement, which unlocks the Gulf Cooperation Council’s (GCC) trade potential with Russia and China. Its wealthy members can now tap into two series of Iranian-transiting megaprojects in one fell swoop through this deal, with the North-South Transport Corridor (NSTC) connecting them to Russia while the China-Central Asia-West Asia Economic Corridor (CCAWAEC) will do the same vis-à-vis China…

…Only two weeks after Saudi Arabia announced an effort to establish diplomatic ties to Iran in a deal mediated by China, more news surfaced that Saudi Arabia was also planning to reopen its embassy in Syria for the first time in over a decade. Rumors are swirling that Iran, Saudi Arabia and Syria are on the verge of geopolitical and economic agreements that sidestep the US.

Russia and India agree to trade oil for rupees. Russia is now India’s largest oil supplier, with 35% of that massive, growing country’s imports. The U.S. is not happy about this — but India doesn’t seem to care. From a recent article:

Even the US itself seems to have finally accepted that it can’t reverse this trend, which is evidenced by former Indian Ambassador to Russia Kanwal Sibal recently telling TASS that “Lately, the discourse from Washington has changed and India is no longer being asked to stop buying oil from Russia. In a recent visit to India, the US Treasury Secretary actually said that India can buy discounted oil from Russia as much as it wants so long as western tankers and insurance companies are not used.”

African leaders travel to Moscow. Representatives of 40 African nations traveled to Rissia for the Second International Parliamentary Conference “Russia – Africa in a Multipolar World.” According to the press release, the attendees:

… discussed the potential for collaboration across a range of sectors, their contribution to the African continent’s economy and security, and their work in the realms of science and education, politics, and techno-military area.

During the conference, the African continent was invited to work together to form a new multipolar world order. This is especially important given the significant human resources of Africa, which is home to more than 1.5 billion people and has enormous mineral reserves in its soil.

Brazil and Argentina announce a common currency. In February, the two dominant Latin American economies announced plans for a common currency called the “sur” for use in bilateral trade. South America is a big, resource-rich place with numerous grudges against its intrusive northern neighbor. So a de-dollarization movement there, while not as immediately consequential as what’s happening in the Middle East or Asia, is both plausible and potentially serious for the dollar.

Lower Dollar, Higher Gold

Even in an emerging multi-polar world, there’s no obvious replacement for the deep, liquid US capital markets. So the dollar won’t disappear from global trade. However:

If the BRICS have the commodities and the US and its allies are left with finance, pricing power for crucial things like oil and gold will shift to Russia, China, and the Middle East.

Falling demand for dollar-denominated bonds as reserve assets will send trillions of dollars now outside the US back home, raising domestic prices (which is to say lowering the dollar’s purchasing power and exchange rate).

The loss of its weaponized reserve currency will lessen the US’ ability to impose its will on the rest of the world (witness China as Middle-East peacemaker and India buying Russian oil with rupees).

To sum up, tomorrow’s world is multi-polar, and for the US and its allies, inflationary. That means a commodities bull market — at least in dollar terms — and extreme financial instability as the US Empire is forced to live within its means. It won’t be pretty but for gold bugs and commodity bulls, it might be extremely profitable.

I’ll leave you with this:

First CNN does a segment on de-dollarization, now Fox News also.

3,Chris Powell of GATA provides to us very important physical commentaries

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: LITHIUM

END

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.88753

OFFSHORE YUAN: 6.8963

SHANGHAI CLOSED DOWN 5.32 PTS OR 0.16%

HANG SANG CLOSED UP 407.75 PTS OR 2.06%

2. Nikkei closed UP 365,53 PTS OR 1.33%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 102.33 EURO RISES TO 1.08240UP 2 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.299 J apan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 132.83 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWNfor WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.327***/Italian 10 Yr bond yield RISES to 4,146*** /SPAIN 10 YR BOND YIELD RISES TO 3.350…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.160

3j Gold at $1968.00 silver at: 23.38 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 26/100 roubles/dollar; ROUBLE AT 77,15//

3m oil into the 72 dollar handle for WTI and 78 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 132.83 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .299% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9189as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9962 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

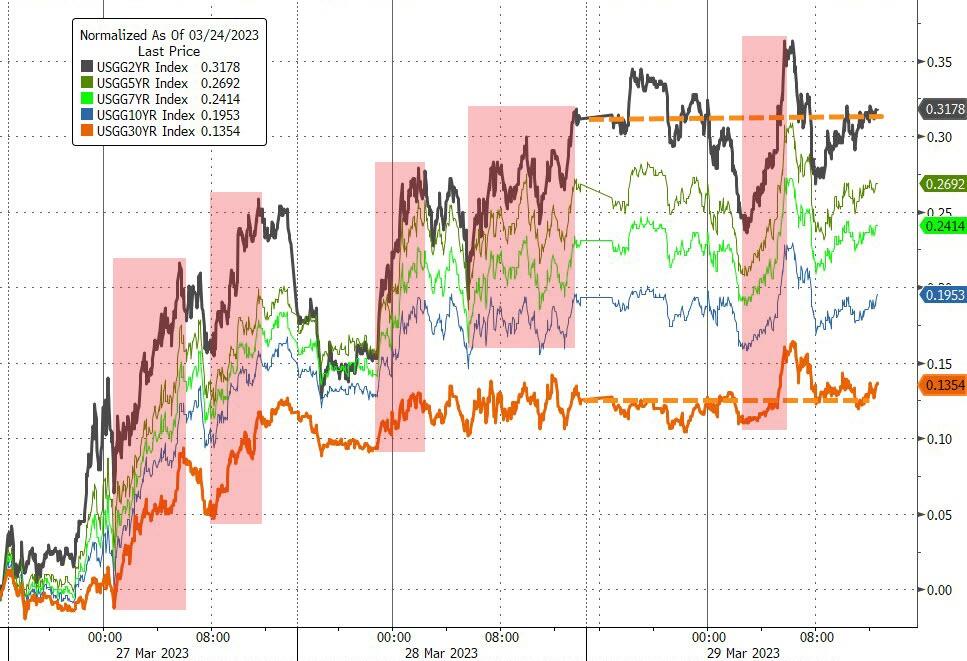

USA 10 YR BOND YIELD: 3.577UP 1 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.787 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.091 UP 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.15…

GREAT BRITAIN/10 YEAR YIELD: UP 1 BASIS PTS AT 3.4905

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

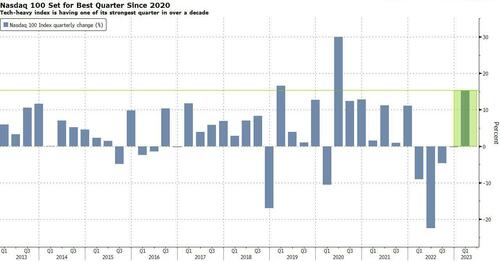

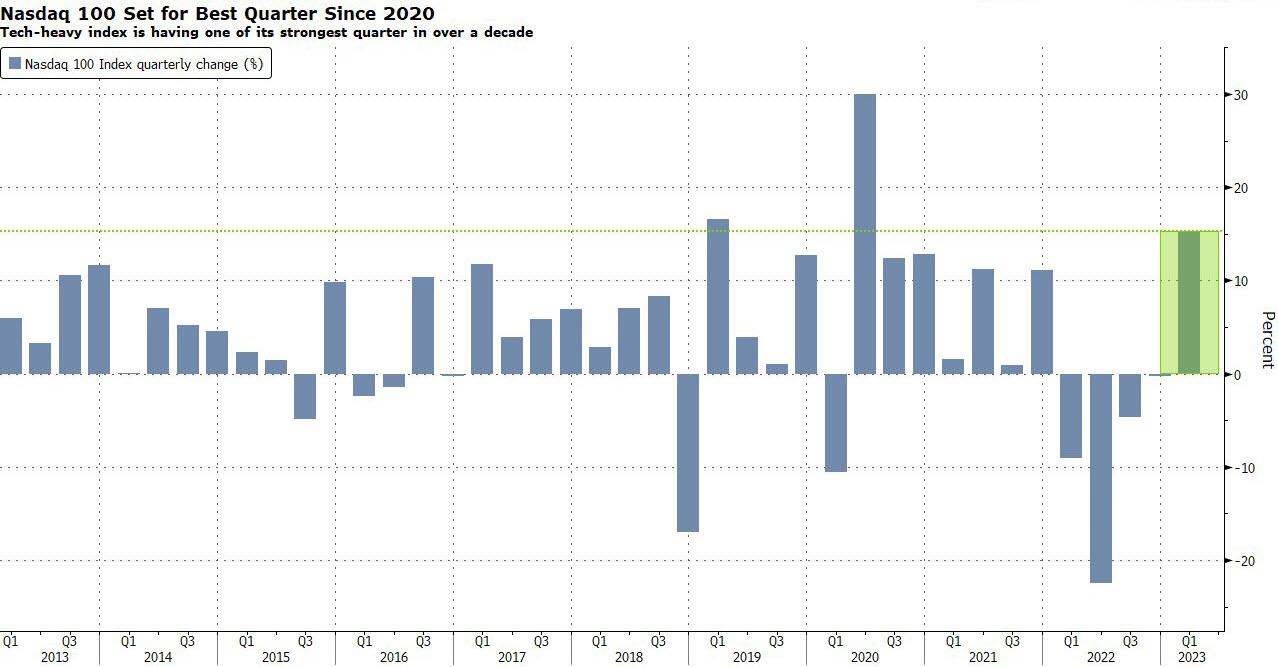

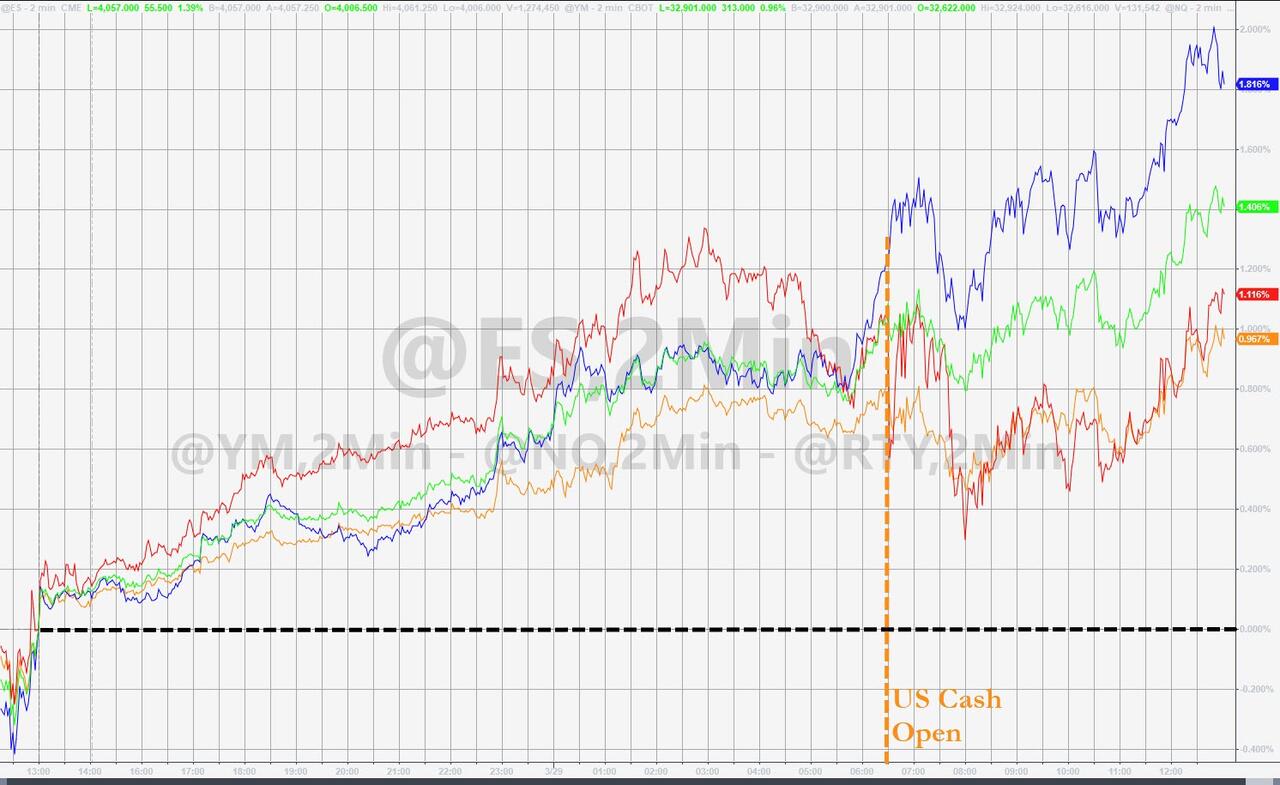

Futures Gain On China Tech Optimism, Easing Bank Fears; Nasdaq On Pace For Best Quarter In 3 Years

WEDNESDAY, MAR 29, 2023 – 03:09 PM

US futures extended gains for a second day on Wednesday as banking sector fears continued to ease, while Nasdaq futs got a boost from a rally in Asian tech stocks following the announced split of Chinese internet giant Alibaba which sent the Hang Seng up 2.1% and HSTECH +2.5%.

S&P 500 and Nasdaq 100 futures contracts were up 0.8% as of 7:30 a.m. in New York, trading at 4,034 and 12832 respectively.

The S&P 500 is set for a flat month, while the Nasdaq 100 has surged nearly 5% in March and more than 15% in Q1 – its best quarter in nearly three years and its first rise in 5 quarters – as tech stocks, especially megacaps, found renewed favor with investors.

Bond yields are lower following dovish comments by ECB’s Philip Lane on inflation which supported bunds over London session, and helping drive declines for front-end Treasury yields. The USD stronger, and commodities are flattish. WTI is up small, approaching the bottom-end of the recent $75 – $80 YTD range. Overnight, the WaPo reported that the government may move to strengthen capital/liquidity requirements for banks with assets larger than $100bn. Fed’s Bullard said that banking crisis can be contained with policy rather than by moves in interest rates; will the bond market remove any rate cut expectations? Doubtful.

In premarket trading, Alibaba Group ADRs fell in US premarket trading after surging Tuesday on plans to split. Its Hong Kong-listed shares were 12% higher, tracking overnight gains on Wall Street. That sparked a rally in Chinese tech shares as investors piled into the companies that were stung by a crackdown from Beijing over the past two years. UBS shares climbed as much as 3% after the Swiss lender said veteran UBS CEO Sergio Ermotti will return and replace Ralph Hamers as chief executive officer; Jefferies shares were little changed after the financial services firm’s profit plunged in its fiscal first quarter, as a bump in equities and fixed income trading failed to offset a slump in investment banking. Here are some other notable premarket movers:

Lululemon shares leap 15% in premarket trading after the athletic-apparel brand reported fourth-quarter adjusted earnings per share that beat analyst estimates and issued guidance that topped expectations. Analysts found the results to be strong overall, with most expecting the negative sentiment around the stock to be alleviated with the performance.

Micron rises 2.7% after the largest US maker of memory chips issued a forecast of adjusted revenue for the third quarter that was better than some had feared. Analysts were still cautious about the tough environment facing chipmakers, but see signs that the worst of the downturn may be behind the industry.

Shares of semiconductor companies are rising following Micron’s forecast and after Infineon raised its revenue outlook. Qualcomm gains 1%, Advanced Micro Devices (AMD US) +0.9%, Nvidia +0.8% and Intel +0.8%.

Alibaba and other US-listed Chinese internet stocks are poised for a pullback, after their shares surged on Tuesday following Alibaba’s plan to split into six units and seek separate listings. Alibaba slides 1.4% in premarket trading, Baidu -0.8%, JD.com -1.5%.

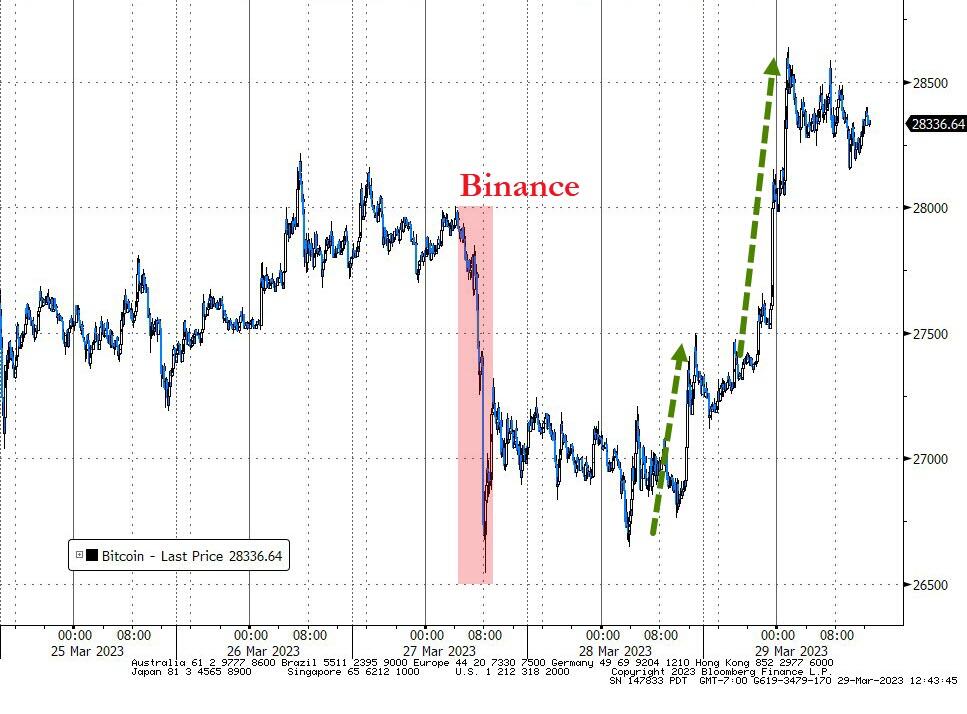

Cryptocurrency- related stocks rally as Bitcoin extends gains into a second day to breach the $28,000 level. Cipher Mining rises 15%, Riot Platforms +7.4%, Marathon Digital +6.3%, Coinbase +4%, MicroStrategy +3.9%.

Arcturus Therapeutics shares jump 25% after the biotech beat analysts’ earnings estimates for the fourth quarter and repaid debts that allow its “cash runway” to extend to 2026. Analysts were especially positive on the company’s update regarding its pipeline and its potential.

Lucid rose 1.9% after the electric vehicle-maker said it would cut 18% of its workforce, including employees and contractors. Morgan Stanley notes that fellow EV startups may need to consider similar cost cutting measures given increased competition and a challenging capital-raising environment.

US equities have traded in a narrow range over the past week, as investors digested the banking sector crisis, with contagion fears easing, while the Fed hinted that the rate-hiking cycle was near the end, but not ready for a pivot yet as inflation was still too high. Swaps traders currently price in more than a 50% probability the Fed will raise rates by a quarter point at its next meeting, with plans to ease thereafter, something with which several strategists, including those at BlackRock, disagree.

The bad news for markets “is that the Fed is very unlikely to cut rates until Q2 2024, unless US growth slows more markedly than we anticipate, leaving us with a ‘higher for longer’ scenario,” Willem Sels, global chief investment officer at HSBC Private Banking and Wealth, wrote in a note on the outlook for the next quarter. “Another key consideration for investors should be China’s reopening and the bounce in consumer activity, which markets are still completely underestimating,” he added, saying China’s renewed focus on growth will help reduce the risk of a recession in the rest of the world.

“We associate the current market pricing in terms of rate cuts not to be appropriate, we are not expecting any rate cuts in 2023 across different economies, especially in the US,” Giulio Renzi Ricci, investment strategist at Vanguard Asset Services, said on Bloomberg Television. “For that reason we don’t expect growth stocks, and tech in particular, still will need to be discounted back” once the market realizes a pause in rate cuts isn’t really happening.

At the same time, investors argue that the odds of a recession have risen after banking turmoil earlier this month sparked fears of wider contagion, and will lead to sharply tighter lending conditions. An index of dollar strength was steady after ending Tuesday near the lowest level in eight weeks. “The banking crisis and the new tighter standards for banks is equivalent to one to two rate hikes,” said Eva Ados, chief investment strategist for ERShares, in an interview with Bloomberg Television. “There is a big possibility here of a pricing mistake. We are pricing in the rate drop rather than the reason why rates are dropping, which is the banking crisis.”

Meanwhile, top US financial officials on Tuesday outlined what’s likely to be the biggest regulatory overhaul of the banking sector in years, addressing underlying issues that contributed to the collapse of Silicon Valley Bank and other US regional lenders.

There is a sea of green across the equity space with European stocks following their Asian counterparts higher and futures pointing to a positive open on Wall Street. Alibaba led the rally in Hong Kong after announcing plans to split into six business units, while tech stocks are also outperforming in Europe after upbeat forecasts from Micron and Infineon. here are the biggest European movers:

UBS shares climb as much as 3% after the Swiss lender said Sergio Ermotti will replace Ralph Hamers as chief executive officer

Coloplast rises as much as 2.6% after being upgraded to equal-weight at Barclays with the broker saying the ostomy products maker’s estimates now look more achievable

Infineon jumps as much as 7.9%, the biggest intraday advance since Feb. 2, after the chipmaker lifted revenue and margin estimates for the second quarter

Strix rises as much as 9.8%, the most in more than two months, after the kettle safety-control producer said in its full-year earnings report there are “green shoots” appearing

OCI gains as much as 13%, the most intraday since April 2020, after activist investor Jeff Ubben’s Inclusive Capital Partners urged the fertilizer maker to explore strategic options

WPP advances as much as 2.6% after Exane BNP upgraded to outperform from neutral, turning more positive on the ad agency sector

Next shares fall as much as 9.1%, with analysts viewing the clothing retailer’s maintained sales and profit guidance for 2024 as disappointing

Mercedes-Benz Group drops as much as 2.8% after Kuwait Investment Authority placed 20 million shares at a ~3.6% discount to the last close

Aroundtown falls as much as 12%, hitting another record low after Tuesday’s 10% drop, as in-line results and a dividend suspension did little to reassure traders

Atos drops as much as 11% after a report from BFM said Airbus wanted to renegotiate the price of Evidian, a unit of the embattled French digital services firm

Encavis sinks as much as 12%, the most intraday since January, as Jefferies notes the decision to waive its dividend to fund future growth marks a turning point

Asian stocks advanced as Chinese tech shares rallied on optimism Alibaba’s overhaul will pave the way for other tech giants to potentially unlock billions of dollars in shareholder value. The MSCI Asia Pacific Index rose as much as 0.8%, led by Hong Kong. Chinese technology stocks climbed 2.5% to a five-week high. Alibaba jumped 12%, while its biggest shareholder Softbank Group gained more than 6%. Alibaba surprised markets after the internet behemoth announced plans to split its $220 billion empire into six units that will individually raise funds and explore initial public offerings. The plan is positive for the sector and could signal further easing of regulatory constraints, according to analysts.

“The government needs to boost the economy this year, and the big tech platforms, which have been under pressure over the last couple of years and shedding staff, are key to help the government boost employment,” Vey-Sern Ling, managing director at Union Bancaire Privee, told Bloomberg TV. Elsewhere, Japanese stocks gained as easing concerns over the banking sector revived risk appetite following weeks of volatility. Shares in mainland China and South Korea eked out small gains as investors braced for a slew of data on the US economy this week

Japanese stocks rose as a revamp plan at Alibaba boosted SoftBank. Gains accelerated in the afternoon ahead of Thursday’s ex-dividend date for some 1,500 stocks. The Topix rose 1.5% to close at 1,995.48, while the Nikkei advanced 1.3% to 27,883.78. SoftBank Group surged 6.2%, the biggest boost to the Nikkei 225, after China’s Alibaba Group announced a six-way split of its businesses. The news fueled optimism for a recovery at one of the Japanese company’s most important holdings. Toyota contributed the most to the Topix gain, increasing 2.6%. Out of 2,159 stocks in the index, 2,013 rose and 101 fell, while 45 were unchanged. “Globally excessive concerns about the financial system have receded, and there is no new additional bad news,” said Shogo Maekawa, global market strategist at JPMorgan Asset Management Japan. “Domestically, the market was supported by buying for year-end dividends and dividend reinvestment.

Australian stocks also rose: the S&P/ASX 200 index gained 0.2% to close at 7,050.30, after Australian inflation decelerated more than expected in February, bolstering the case for the Reserve Bank to stand pat at next week’s policy meeting. Materials and energy stocks were the biggest gainers on the benchmark. Read: Australian Inflation Eases, Bolstering Case for Rate Pause “Markets were already quite convinced with the story of an April pause, given what’s happening globally. But this just adds to the story,” said Jessica Ren, a strategist at Westpac Banking Corp. in Sydney. Recent comments from RBA policymakers had been implying “get ready for a pause.” In New Zealand, the S&P/NZX 50 index fell 0.3% to 11,736.75

Finally, Indian stocks also ended higher on Wednesday with small-cap stocks registering their best performance in two months. Adani group stocks rebounded from the steep losses seen on Tuesday as company officials rebutted media reports that raised concerns about the group’s ability to repay debt. Flagship Adani Enterprises rallied 8.7%, while Adani Ports rose 7.3%. A late spurt in buying led by traders covering short positions ahead of monthly derivatives expiry saw India outperform most equity gauges in Asia. The S&P BSE Sensex rose 0.6% to 57,960.09 in Mumbai, while the NSE Nifty 50 Index advanced 0.8% to 17,080.70. The latter saw its best one-day gain since March 3. A gauge of small-cap stocks climbed 1.7% to mark its best day since January 31. “There was some short covering in the market toward the end of the session but it was not a sharp move,” Gaurav Bissa, vice president at InCred Capital. “That said, we are recommending clients to turn bullish on the Nifty as we see a bounceback in the near-term.” Hindustan Unilever contributed the most to the Sensex’s gains, increasing 1.9%. Out of 30 shares in the Sensex index, 26 rose while 4 stocks fell.

In FX, the dollar rose nearly 1% versus the yen to 132.09, its highest since March 22; the Bloomberg Dollar Spot Index edged up 0.1%. The US currency also benefited from Japanese financial year-end flows, which weighed on the yen in Asian trade. The Australian and New Zealand dollars struggled, while the euro and the pound were little changed against the US currency.

In rates, treasuries rose after a two-day selloff and erased a portion of the curve-flattening selloff of past two days as investors awaited remarks from Federal Reserve officials and economic releases this week for clues on monetary policy. In particular focus will be data on the central bank’s preferred inflation measure – the core PCE deflator – which is likely to factor into the Fed’s next policy decision. Dovish comments by ECB’s Philip Lane on inflation supported bunds over London session, helping drive declines for front-end Treasury yields. US yields, off session lows, remain richer by ~4bp on the day across front-end of the curve with inverted 2s10s spread steeper by ~2bp; 10-year around 3.55% is richer by ~2bp on the day with bunds lagging by 2.5bp in the sector. The US auction cycle concludes with $35BN 7-year note sale at 1pm, follows Tuesday’s decent 5-year note sale which stopped 1bp through the WI; WI 7-year yield around 3.590% is ~47bp richer than February’s result.

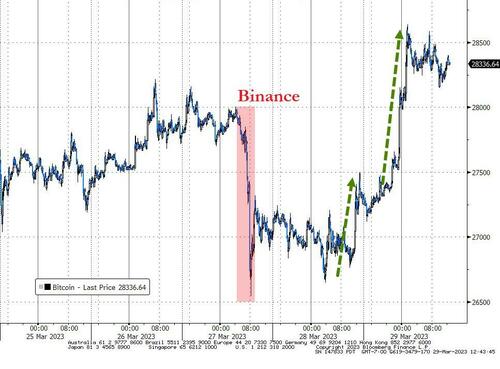

In commodities, crude futures advance with WTI rising 0.7% to trade near $73.70. Spot gold falls 0.4% to around $1,966. Bitcoin gains 4.1%.

Now to the day ahead. In terms of data releases, we have the US February pending home sales, in the UK February net consumer credit, mortgage approvals and M4, in Germany the April GfK consumer confidence and lastly in France March consumer confidence data. Finally, we will hear from ECB’s Kazimir as well the BoE’s Mann.

Market Snapshot

S&P 500 futures up 0.9% to 4,036.50

STOXX Europe 600 up 0.8% to 448.02

MXAP up 0.6% to 160.78

MXAPJ up 0.7% to 517.13

Nikkei up 1.3% to 27,883.78

Topix up 1.5% to 1,995.48

Hang Seng Index up 2.1% to 20,192.40

Shanghai Composite down 0.2% to 3,240.06

Sensex up 0.4% to 57,866.24

Australia S&P/ASX 200 up 0.2% to 7,050.33

Kospi up 0.4% to 2,443.92

German 10Y yield little changed at 2.32%

Euro down 0.1% to $1.0832

Brent Futures up 0.3% to $78.87/bbl

Gold spot down 0.6% to $1,962.15

U.S. Dollar Index up 0.24% to 102.68

Top Overnight News from Bloomberg

China warned the US and Taiwan President Tsai Ing-wen that any meeting with House Speaker Kevin McCarthy would be a serious provocation, raising the stakes for her trip to the US. Tsai left Taipei on Wednesday bound for New York on a plane that was guarded by F-16 fighters as it headed over the Pacific. She’ll later visit two Central American allies, and on the way home she’s planning to stop in Los Angeles, where she’s expected to meet with McCarthy. BBG

The BOJ’s Shinichi Uchida indicated that any yield curve control adjustment wouldn’t be communicated ahead of time. That’ll keep the market on its toes, with some concluding it’s the only way to avoid a bond selloff in advance. It comes as bets on policy normalization help the yen make a comeback as a haven. BBG

UBS said Sergio Ermotti will return as chief executive, as the Swiss giant moves into a new era with its takeover of Credit Suisse. Mr. Ermotti has been credited with repositioning the bank and focusing it on less risky businesses after UBS suffered big losses during the financial crisis. WSJ

UK mortgage approvals edged up in February but remained more than a third below their levels from a year ago as high borrowing costs squeezed household spending, the BOE has said. Lenders last month approved a total of 43,500 mortgages for house purchases, from 39,600 in January, the BoE said on Wednesday. Approvals in February 2022 came to 69,131. The figure was above analysts’ forecast of 42,000, and marked the first monthly increase since August 2022. FT

The UK competition regulator has launched an in-depth probe into US chipmaker Broadcom’s $69bn takeover of cloud software company VMware, after warning it could make computer servers more expensive. FT

More bullish oil momentum. US crude stockpiles slumped by 6.1 million barrels last week, API data is said to have shown, in what would be the biggest drop this year if confirmed by the EIA. Gasoline supplies also sank. In the Middle East, one of the top producers in Iraq’s Kurdistan region started cutting production as a spat that has halted 400,000 barrels a day of exports drags on. BBG

Jamie Dimon will be questioned in a civil lawsuit over JPMorgan Chase’s relationship with Jeffrey Epstein, people familiar with the matter said. The U.S. Virgin Islands sued JPMorgan last year, saying the bank facilitated Epstein’s alleged sex trafficking and abuse. WSJ

Top officials from the Federal Reserve and Federal Deposit Insurance Corporation will testify to the House Financial Services Committee on the collapse of Silicon Valley Bank and Signature Bank, a day after Tim Scott, a Republican senator, accused SVB of being “rife with mismanagement”. FT

Tesla’s move to slash prices in China has backfired as Elon Musk’s company loses market share to Warren Buffett-backed BYD, putting Chinese carmakers on track to sell more passenger vehicles than their foreign rivals for the first time in 2023. FT

The European Central Bank will need to increase interest rates further if recent stress in the financial system stays contained, Chief Economist Philip Lane told Zeit in an interview: BBG

The yen is making a comeback as a preferred foreign- exchange haven, after banking crises in the US and Switzerland hurt the dollar and franc’s standing as go-to assets for turbulent times: BBG

Traders are leaning toward further gains in the world’s biggest bond market, after a rally that got a major boost from short-covering by hedge funds this month: BBG

President Joe Biden responded to House Speaker Kevin McCarthy’s demands that he begin negotiations over the debt ceiling by challenging Republicans to produce a public budget plan before departing Thursday for a two-week Easter recess” BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly positive albeit with most major indices rangebound amid a lack of fresh macro drivers and heading into quarter-end, while Hong Kong markets outperformed as tech stocks surged on Alibaba’s plan for a six-way split. ASX 200 was kept afloat by strength in the commodity-related sectors and after softer-than-expected CPI data supported the case for the RBA to pause at next week’s meeting, although gains were limited by weakness in the top-weighted financial industry. Nikkei 225 traded higher after Japan’s parliament passed a record JPY 114tln budget for FY23 and with policymakers said to consider lowering mortgage rates for families with children, while BoJ officials also stuck to the dovish script. Hang Seng and Shanghai Comp. were varied with Alibaba front-running the advances in Hong Kong as its plan for a split is seen to unlock value for shareholders and has spurred some speculation that its large tech peers could follow suit, while the mainland lagged despite the PBoC’s liquidity injection as frictions lingered regarding Taiwan President Tsai’s planned transit through the US and after the Biden administration added five Chinese companies to the entity list for allegedly aiding China’s repression of Uyghurs.

Top Asian News

China NDRC Deputy Director General said China’s potential growth rate is the potential growth rate of the whole world and said they are optimistic for the growth situation for this year, according to Reuters.

US President Biden’s administration added five Chinese Co.s to the entity list for allegedly aiding China’s repression of Uyghurs.

Taiwan’s President Tsai comments before boarding a flight to New York in which she noted Democratic Taiwan defends democratic values and external pressure does not affect their determination to go out into the world, according to Reuters.

China’s Taiwan Affairs Office urged the US not to arrange a transit of Taiwan’s leader through the US and said any meeting between Taiwan President Tsai and US House Speaker McCarthy would be a severe provocation, while it added that China firmly opposes this and will definitely take measures to fight back, according to Reuters.

US senior administration official said Taiwan President Tsai’s planned transit is consistent with a long-standing US practice and the US sees no reason for Beijing to overreact to the transit which is consistent with the unofficial relationship and the One-China policy. The official added that every Taiwan president has transited through the US and President Tsai has met with members of Congress in all her previous six transits, as well as stated that China’s attempts to alter Taiwan’s status quo will not pressure the US to alter its practice of facilitating transits by Taiwan’s presidents, according to Reuters.

BoJ Deputy Governor Uchida said they will make a judgement on trend inflation by looking at various indicators, while he noted the BoJ would face an unrealised loss of JPY 50tln on its balance sheet if the 10yr bond yield rises to 2%, according to Reuters.

European bourses are firmer across the board, Euro Stoxx 50 +1.2%, as banking concerns continue to dissipate and focus turns to the sessions speakers. Sectors feature marked outperformance in Tech names after updates from Infineon and Micron; MU +2.5% pre-market. Stateside, futures are in the green, ES +0.9%, paring the downside from Tuesday which was a feature of underperformance in large-cap names; ahead, the US-specific docket is relatively light. Infineon raised Q2 revenue and segment margin guidance alongside lifting FY revenue guidance, primarily due to resilient business dynamics in its core automotive and industrial segments. Micron: Q2 adj. EPS -1.91 (exp. -0.86); it made inventory write-downs of USD 1.43bln in the quarter, which had an impact of USD 1.34/shr. Q2 revenue USD 3.69bln (exp. 3.702bln). Expects profitability to remain extremely challenged in the near-term and said profitability levels in the industry are currently not sustainable.

Top European News

EU’s Dombrovskis said the situation in the EU banking sector is stable and banks are prepared to withstand shocks.

ECB’s Lane says to ensure that inflation falls to 2%, further interest rate hikes are required under the scenario expected by the ECB, according to Die Zeit; rates must increase if banking tensions have no or a “fairly limited” impact, bank sector tensions are seen as settling down and there is no reason to expects major problems.

ECB’s Kazimir agreed not to give guidance on the May ECB meeting, Kazimir thinks inflation is too high for too long; ECB should continue increasing rates, possibly at a slower pace; will take into account financial market situation.

BoE FPC Minutes: All UK banks are resilient to risks from rising interest rates, including from bond positions; maintains countercyclical capital buffer rate at 2%; UK firms are resilient from higher debt costs.

FX

The DXY is erring lower and has dipped below the 102.50 mark within 102.41-102.75 boundaries despite marked AUD & JPY pressure.

Pressure which stems from cooler-than-expected inflation and a myriad of factors sparking a pullback from recent peaks respectively; AUD/USD at 0.6662 low and USD/JPY above 132.00.

In contrast, the DXY remains softer given the resilience of the EUR and GBP with ECB’s Lane and BoE data respectively perhaps assisting with EUR/USD above 1.0850 though Cable is yet to breach 1.2350 convincingly.

CAD fails to derive any lasting support from oil benchmarks and as such is struggling to retain the 1.36 handle while the SEK is impaired by softer retail data despite favourable sentiment indicators.

Swedish NIER expects the Riksbank to continue on its set path re. rate increases, with the cycle deemed to be over in July when the rate will be 3.75%.

PBoC set USD/CNY mid-point at 6.8771vs exp. 6.8780 (prev. 6.8749)

Fixed Income

Debt futures rebound relatively firmly to defy month end rebalancing flows tilted towards stocks over bonds.

Bunds reclaim more than half of Tuesday’s losses within a 135.47-136.28 range, Gilts towards the top of 104.18-103.56 parameters and T-note nearer 114-28 than 114-14+ ahead of US housing data, House hearing on bank failures and USD 35bln 7-year auction.

Greece has commenced the sale of a new 5yr bond with price guidance at circa 95bps over mid-swaps, according to Reuters sources.

Commodities

WTI and Brent are firmer but reside in relatively narrow sub-USD 1/bbl parameters which specifics light aside from weekly inventory data yesterday and ahead alongside ongoing focus re. Iraqi flows through Turkey.

Specifically, WTI trades around USD 74/bbl (in a 73.51-74.00/bbl range) while its Brent counterpart trades on either side of USD 79/bbl (in a 78.73-79.32/bbl parameter).

Spot gold remains softer and in Tuesday’s parameters while base metals are generally softer despite the tone but again in narrow ranges, with the exception of iron ore which is bolstered on steel consumption expectations.

US Private Energy Inventory (bbls): Crude -6.1mln (exp. +0.1mln), Cushing -2.4mln, Distillate +0.5mln (exp. -1.5mln), Gasoline -5.9mln (exp. -1.6mln).

US Energy Secretary Granholm said Strategic Petroleum Reserve buybacks could begin late this year and that work on two of four oil reserve sites are to go ‘into the fall’ which has delayed the buybacks, according to Reuters.

Russian Gazprom says “We are approaching the limit of gas supplies to China”, via Sky News Arabia.

Cargill informed the Russian Agriculture Ministry that it will stop the export of Russian grain from the next exporting season (July), according to the Russian ministry which adds it will not affect the volume of domestic grain shipments abroad.

Geopolitics

Ukrainian military officials said Russian forces remain relentless in their attempts to take full control of Bakhmut and Avdiivka in eastern Ukraine but were not making progress, according to Reuters.

Ukrainian President Zelensky extended an invitation to Chinese President Xi to visit Ukraine, according to AP; Kremlin says it is not up to Russia to advise China’s leader when to visit Ukraine, adds that Russia’s wider war with hostile states will last for a long time

US President Biden responded that he hasn’t seen that but is concerned when asked if he was concerned about Russia sending tactical nuclear weapons to Belarus, according to Reuters.

Russia has started drills with Yars Intercontinental Ballistic Missiles, according to its Defence Ministry

US Event Calendar

07:00: March MBA Mortgage Applications 2.9%, prior 3.0%

10:00: Feb. Pending Home Sales YoY, prior -22.4%

10:00: Feb. Pending Home Sales (MoM), est. -3.0%, prior 8.1%

Central Banks

08:05: NY Fed Head of Supervision Dianne Dobbeck Speaks to Bankers

10:00: Fed’s Barr Appears Before the House Financial Services Panel

DB’s Jim Reid concludes the overnight wrap

Two days of relative calm has helped encourage a quieter week and encourages me that I can go on holiday after tomorrow without too much disturbances. If anything spectacular happens for an hour this afternoon I’ll be oblivious to it as I’m having another back injection under general anaesthetic as the sciatica is flaring up again. So my recent operation hasn’t helped. I went for a nerve conduction test last Friday and I have 4 trapped nerves. 2 in my leg and 2 in my neck/arm. I can’t ask for too much sympathy as its all golf and weight training related. If I accepted that I wasn’t 25 anymore I suspect I’d be in decent shape. However I still have an ambition to get down to become a scratch golfer and without exciting goals and targets life is a duller affair. Anyway, I’ll be doing the EMR tomorrow before heading off skiing, where I’ll also be trying to protect my knees. So we’ll save our emotional goodbyes for two weeks until tomorrow.

Anyway the relative calm continues to be most felt in bond market repricing, 2yr USTs rose +13.4bps yesterday (unchanged in Asia). They are around +50bps above where they were last Friday lunchtime but still down about -100bps from where they were on March 9th, around Powell’s testimonies. Improving sentiment was also evident in the fed futures market which further trimmed expectations of rate cuts. Fed futures are pricing in -70bps of rate cuts to year-end, with the implied rate for the Fed’s December meeting rising +11.2bps yesterday to 4.318%. This is up from 3.57% at the lows on Friday. So a big but steady and fairly quiet move over the last 48-72 business hours.

Longer-dated Treasury yields were more subdued yesterday, with 10yr yields just +3.9bps higher at 3.564%. This is the second smallest move in either direction since the SVB news broke. European sovereign debt yields also rose as the banking sector further stabilised and regional economic survey data improved (more on that below). 10yr bund yields were +6.3bps higher at 2.29%, while the more policy sensitive 2yr rate was +7.1bps higher to 2.59%. Other sovereign 10yr European yields rose more than German yields, with Gilts (+9.0bps), BTPs (+7.4bps), and OATs (+6.5bps) all higher.

In equities, the S&P 500 fell back -0.16%. On a sector-by-sector level there was a significant amount of dispersion, as energy (+1.45%) and other cyclicals such as transports (+0.78%) and capital goods (+0.55%) outperformed but media (-1.10 %) and healthcare equipment (-1.04%) fell back. The tech-heavy NASDAQ traded down -0.45%.

Briefly looking at the US regional banking sector, the FDIC’s Gruenberg stated yesterday that regional bank liquidity has remained stable. Against this backdrop, the regional banks KBW index traded up +0.32% with most of the smaller regional banks gaining on the day, while a couple of heavier weighted banks (BofA -1.3% & Wells Fargo -0.8%) were a drag on the KBW index. The embattled First Republic also finished -2.32% lower.

European equity markets traded flat, with the STOXX 600 down -0.06%. We heard the ECB’s Enria emphasise that bank oversight needs to be more efficient in Europe, and that changes to supervision should reduce the burden on banks. In particular, Enria stated that a closer look at the European CDS market is in order, calling for an improvement in the degree of information available on the market, as opposed to implementing prohibitions or new rules. He also spoke on the recent banking turmoil, stating that the “direct exposure to Credit Suisse is relevant but manageable”, but that he was “concerned by nervousness among investors on banks”.

This morning in Asia, equity markets are seeing decent gains. The Hang Seng (+1.80%) is outperforming amid a rally in Chinese technology shares on Alibaba’s reorganisation news that will see the company split into six independent business groups seeking separate IPOs. Their shares are up around +13%. This rally bolstered other Asian equities with the Nikkei (+0.46%) and the CSI (+0.24%) edging higher while the Shanghai Composite (-0.04%) is just above flat. Elsewhere, the KOSPI (-0.16%) is losing ground after opening slightly higher in early trade. In overnight trading, US stock futures are indicating a positive start with contracts tied to the S&P 500 (+0.39%) and NASDAQ 100 (+0.30%) both higher.

Moving on, Australia’s CPI slowed to an eight-month low of +6.8% y/y in February (v/s +7.2% expected), down from the prior month’s +7.4% annual increase. This was down to a smaller rise in housing and fuel costs. This will further support the pause narrative at next month’s RBA meeting.

In terms of yesterday’s data, the US March Conference Board consumer confidence index results came in firmly above expectations at 104.2 (vs 101 expected and 103.4 last month) as confidence in future business and labour market conditions rose. Looking into the details, the expectations index, the short-term outlook for income, business and labour market conditions, rose to 73 from 69.7 in February, however, the present situation index, which reflects consumer assessment of current business and labour market conditions, fell from 152.8 to 151. The survey was for the 4 week period up to March 20, which puts just about half the response time after SVB first showed signs of stress and only really covered the first few days of the CS news flow.