Mar 30.2023 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSED: UP $12.25 T0 $1979.60

SILVER PRICE CLOSED: UP $0.46 AT $23.84

FRIDAY: OTC/LONDON OPTIONS EXPIRY EXPECT GOLD AND SILVER TO BE DOWN UNTIL THIS CROOKED SCHEME IS FINISHED/FIRST DAY NOTICE

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1980.95

Silver ACCESS CLOSE: 23.90

Bitcoin morning price:, $27,261 UP 771 Dollars

Bitcoin: afternoon price: $27,874 DOWN 1360 dollars

Platinum price closing $989.00 UP $17.20

Palladium price; closing $1474.45 UP $27.45

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2680.95 UP 7.63 CDN dollars per oz (ALL TIME HIGH 2732.50)

BRITISH GOLD: 1598.98 UP 4.23 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1816.90 UP 6.34 euros per oz //(ALL TIME HIGH//1860.82)

COMEX DATA EXCHANGE:

EXCHANGE: COMEX

CONTRACT: MARCH 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,966.100000000 USD

INTENT DATE: 03/29/2023 DELIVERY DATE: 03/31/2023

FIRM ORG FIRM NAME ISSUED STOPPED

435 H SCOTIA CAPITAL 1

624 H BOFA SECURITIES 2

657 C MORGAN STANLEY 2

661 C JP MORGAN 1

905 C ADM 2

TOTAL: 4 4

MONTH TO DATE: 6,132

END

COMEX DATA EXCHANGE:

: COMEX 868 CONTRACTS

:

JPMORGAN stopped 0/868 contracts

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR MAR/2023. CONTRACT: 4 NOTICES FOR 400 OZ or 0.11244 TONNES

total notices so far: 6132 contracts for 613,200 oz (19.073 tonnes)

SILVER NOTICES: 15 NOTICE(S) FILED FOR 75,000 OZ/

total number of notices filed so far this month : 3196 for 15,980,000 oz

END

GLD

WITH GOLD DOWN $4,85

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:////// A HUGE DEPOSIT OF 2.24 TONNES FROM THE GLD.

INVENTORY RESTS AT 929.46 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 11 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF OF 0.551 MILLION OZ FROM THE SLV: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 460,633 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 987 TO 118,382 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS STRONG SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.11 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. WITH THIS WEEK’S READING AT THE COMEX, WE HAVE NOW SET ANOTHER RECORD LOW AT 117,395 CONTRACTS , MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.11). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A HUGE GAIN ON OUR TWO EXCHANGES 3867 CONTRACTS. WE HAD ANOTHER 200 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 5.0 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS( 2008 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.58 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP TO LONDON OF 75,000 OZ//NEW STANDING: 15.980 MILLION OZ + THE 5.0 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 20.980 MILLION OZ/ //// V) HUGE SIZED COMEX OI GAIN/ HUGE SIZED EFP ISSUANCE/. WE HAVE NOW REACHED THE POINT THAT THE CROOKS CANNOT LIQUIDATE ANY MORE SILVER SPEC LONGS.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –100 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 22 days, total 19,816 contracts: OR 99.080 MILLION OZ . (900 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 99.07 MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 99.07 MILLION OZ//INITIAL//STRONG ISSUANCE BUT BELOW LAST MONTH

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 987 CONTRACTS WITH OUR $0.11 GAIN IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 2008 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAR OF 15.58 MILLION OZ//FIRST DAY NOTICE// FOLLOWED BY TODAY’S 75,000 QUEUE JUMP (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 5.0 MILLION OF EXCHANGE FOR RISK ISSUED EARLY IN MARCH (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 20.980 MILLION OZ .. WE HAVE A GOOD SIZED GAIN OF 2987 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 15 NOTICE(S) FILED TODAY FOR 75,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 4746 CONTRACTS TO 473,865 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED- 737 CONTRACTS.

WE HAD A GOOD SIZED DECREASE IN COMEX OI ( 4009 CONTRACTS) WITH OUR $4,85 LOSS IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR MAR. AT 4.9953 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 300 OZ (0.009 TONNES) //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)YET ALL OF..THIS HAPPENED WITH OUR $4.85 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A FAIR SIZED LOSS OF 3867 OI CONTRACTS (9.735 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 879 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 473,865

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3867 CONTRACTS WITH 4746 CONTRACTS DECREASED AT THE COMEX AND 879 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 3867 CONTRACTS OR 12.027 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (879 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (4746) //TOTAL LOSS IN THE TWO EXCHANGES 3867 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR MAR. AT 4.9953 TONNES FOLLOWED BY TODAY’S 300 OZ QUEUE JUMP//NEW STANDING 19.073 TONNES // ///3) SOME LONG LIQUIDATION //4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

TOTAL EFP CONTRACTS ISSUED: 88,438 CONTRACTS OR 8,843,800OZ OR 275.07TONNES IN 22TRADING DAY(S) AND THUS AVERAGING: 4019 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 22 TRADING DAY(S) IN TONNES 275.07TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 275.07/3550 x 100% TONNES 7.75% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 275.07 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 987 CONTRACTS OI TO 117,395 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 2008 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 2008 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2008 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 987 CONTRACTS AND ADD TO THE 2008 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC GAIN OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2987 CONTRACTS.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //14.935 MILLION OZ

OCCURRED DESPITE OUR $0.11 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

NORTH KOREA/SOUTH KOREA

i)THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED UP 21.19 PTS OR 0.65% //Hang Sang CLOSED UP 116.73 PTS OR 0.58% /The Nikkei closed DOWN 100.85 PTS OR 0.38 % //Australia’s all ordinaries CLOSED UP 1.06% /Chinese yuan (ONSHORE) closed UP TO 6.8719/OFFSHORE CHINESE YUAN DOWN TO 6.8745 /Oil UP TO 74.22 dollars per barrel for WTI and BRENT AT 79.14 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 4746 CONTRACTS DOWN TO 473,865 WITH OUR LOSS IN PRICE OF $4.85 ON WEDNESDAY

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAR… THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 879 EFP CONTRACTS WERE ISSUED: : APRIL 879 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 879 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR TOTAL OF 3867 CONTRACTS IN THAT 879 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED LOSS OF 4746 COMEX CONTRACTS..AND THIS FAIR SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $4.85 WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAR (19.073) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $4.85 //// AND WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD OUR FAIR SIZED LOSS OF 3134 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE LOST A TOTAL OI OF 12.027 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAR. (4.9953 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 300 OZ (0.009TONNES)… ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $4.85

WE HAD -737 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 3867 CONTRACTS OR 386,700OZ OR 12.027TONNES

TONNES

Estimated gold comex today 174,848/ //poor

final gold volumes/yesterday 241,374//FAIR

//MARCH 29/ MARCH 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1993.36oz INT DELAWARE 62 KILOBARS . |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | n782.370oz |

| No of oz served (contracts) today | 4 notice(s) 400 OZ 0.1804TONNES |

| No of oz to be served (notices) | 0 contracts NIL oz 0 TONNES |

| Total monthly oz gold served (contracts) so far this month | 6132 notices 613200 OZ 19.073 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: NIL oz

customer withdrawals: 1

i) Out of Int Delaware: 1993.36 oz

(62 kilobars)

total withdrawals: NIL oz

in tonnes:0.0619

0

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 4 contracts having LOST 55 contracts. We had 58 notices filed on WEDNESDAY so we

gained 3 contracts or an additional 300 oz will stand for metal at the comex .

April LOST A CONSIDERABLE 26,915 contracts DOWN to 26,915 contracts. It is here that our banker friends have to worry as many will try and take delivery in this upcoming delivery month. WE HAVE 1 MORE READING DAY BEFORE FIRST DAY NOTICE.

May GAINED 320 contracts to stand at 1593

We had 4 notice(s) filed today for 400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 4 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR. /2023. contract month,

we take the total number of notices filed so far for the month (6132 x 100 oz ), to which we add the difference between the open interest for the front month of (MAR. 4 CONTRACTS) minus the number of notices served upon today 4 x 100 oz per contract equals 613,200 OZ OR 19.073 TONNES the number of TONNES standing in this active month of MARCH.

thus the INITIAL standings for gold for the MAR contract month:No of notices filed so far (6132 x 100 oz+ 4 OI for the front month minus the number of notices served upon today (4)x 100 oz} which equals 612,900 oz standing OR 19.073 TONNES in this active delivery month of MARCH..

TOTAL COMEX GOLD STANDING: 19.073 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,643,341.368 OZ 51.114tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,291,699.603 OZ

TOTAL REGISTERED GOLD: 11,518,645.240 (358.27 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 9,773,054.363 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,8753,04 OZ (REG GOLD- PLEDGED GOLD) 307,16 tonnes//

END

SILVER/COMEX

MAR 29/2023// THE MARCH 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 857,149.301oz CNT Delaware JPMorgan . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 1045.400oz JPMorgan |

| No of oz served today (contracts) | 15 CONTRACT(S) (75,000 OZ) |

| No of oz to be served (notices) | 0 contracts (NILoz) |

| Total monthly oz silver served (contracts) | 3196 Contracts (15,980,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

I)) Into JPMorgan 1045.400 oz

Total deposits: 1045.400 oz

JPMorgan has a total silver weight: 144.383million oz/279.086million =51.61% of comex .//dropping fast

Comex withdrawals: 3

i)Out of CNT 20,176.180 oz

ii) out of Delaware 233,538.521 oz

iii) Out of JPMorgan: 603,434.600 oz

Total withdrawals; 857,149.301 oz

adjustments: 1

i) Out of Manfra: 205,830.610 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 35.809 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 279.086 million oz

CALCULATION OF SILVER OZ STANDING FOR MAR

silver open interest data:

FRONT MONTH OF MAR/2023 OI: 15 CONTRACTS HAVING LOST 6 CONTRACT(S.) WE HAD 21 NOTICES FILED

WEDNESDAY, SO WE GAINED 15 CONTRACTS OR AN ADDITIONAL 75,000 OZ WILL STAND FOR METAL ON THIS SIDE OF THE POND

April LOST 101 CONTRACTS TO STAND at 237

May LOST 153 CONTRACTS DOWN TO 89,797

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 15 for 75,000 oz

Comex volumes// est. volume today 61,084 very good/

Comex volume: confirmed yesterday: 46,291 Contracts ( FAIR)

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 3196 x 5,000 oz = 15,980,000 oz

to which we add the difference between the open interest for the front month of MAR(15) and the number of notices served upon today 15 X (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2023 contract month: 3196(notices served so far) x 5000 oz + OI for the front month of MAR (15) – number of notices served upon today (15)x 500 oz of silver standing for the MAR. contract month equates 15.980 million oz +the 5.0million oz of exchange for risk//new total standing 20.980 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 929.46 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 460.633 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

nd

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards/John Rubino

3,Chris Powell of GATA provides to us very important physical commentaries

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: LITHIUM

END

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.8719

OFFSHORE YUAN: 6.8745

SHANGHAI CLOSED UP 21.19PTS OR 0.65%

HANG SANG CLOSED UP 21.19 PTS OR 0.65%

2. Nikkei closed DOWN 100.85 PTS OR 0.38%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 101.82 EURO RISES TO 1.0905 UP 63BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.320 J apan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 132.83 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.3465***/Italian 10 Yr bond yield RISES to 4,212*** /SPAIN 10 YR BOND YIELD RISES TO 3.382…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.279

3j Gold at $1982.00 silver at: 23.381am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 8/100 roubles/dollar; ROUBLE AT 77,08//

3m oil into the 74 dollar handle for WTI and 79 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 132.40 10 YEAR YIELD AFTER BREAKING .54%, RISESTO .321% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9138 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.99625 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

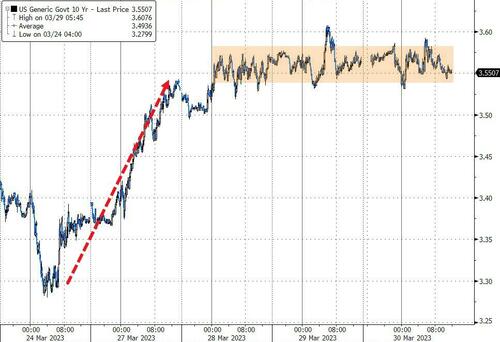

USA 10 YR BOND YIELD: 3.555 DOWN1 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.751 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.103 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.17…

GREAT BRITAIN/10 YEAR YIELD: UP 3BASIS PTS AT 3.534

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Storm Higher On Easing Bank Stress, Looming Quarter-End

BY TYLER DURDEN

THURSDAY, MAR 30, 2023 – 03:15 PM

US index futures extended their gains for a third day, approaching 4,100 – the highest level in over a month – amid easing concerns around the banking crisis and as investors weighed the likelihood that a peak in interest rates is nearing. As of 730am ET, S&P 500 futures were up 0.5% near session highs of 4,080 while the Nasdaq rose 0.6%. The tech-heavy index is set for its best quarter since 2020, pushing into a bull market Wednesday and closing at the highest level since August in a sign investors are preparing for the Fed to end its interest rate hiking cycle and potentially pivot to looser policy later this year. On Wednesday, the gauge entered a new bull market, rising more than 20% from December lows. The yield curve steepened as the 10Y yield dipped 2bps to 3.54%, while the DXY has resumed its selloff and remains below its 50, 100, and 200dma. Commodities are stronger with all 3 complexes stronger.

Among premarket movers, Philip Morris rose after being raised to overweight from neutral at JPMorgan, becoming the broker’s top tobacco sector pick. Meanwhile, Viking Therapeutics fell as the biopharmaceuticals company offered $250m of shares at a discount. Here are other notable premarket movers:

- Sprinklr shares gain 14% in US premarket trading after the software company gave a full-year forecast for both revenue and subscription revenue that is stronger than expected.

- RH shares drop 6.8% after the upscale home furnishings company issued weaker-than-expected full-year guidance for FY23. Analysts were disappointed with the outlook, flagging management’s comments on challenging business conditions being set to continue.

- Semtech falls 13% after the chipmaker forecast a first-quarter loss, against analysts’ estimates of a profit, while its fourth-quarter adjusted EPS fell short of projections by a penny. Cowen analysts cut their target on the stock, noting a “very difficult” start for the company following the closure of its Sierra Wireless deal.

- Charles Schwab stock declines 1.9% as Morgan Stanley cut it to equal-weight from overweight, saying that Schwab’s clients are pulling cash out of the firm’s low- interest-rate bank accounts at twice the rate that MS expected.

- Viking Therapeutics is down 4.3% after launching a $250m share offering at $14.50 each via William Blair, Raymond James.

- Watch Southern Copper as it was downgraded to equal-weight from overweight at Morgan Stanley, which cited a more balanced risk-reward, with the stock adequately reflecting company’s strong cash generation and consistent returns to shareholders.

The US stocks rally comes after a week of treading water as investors weigh the likelihood of further banking turmoil alongside a slew of economic data and clues from central banks on the path for interest rates. The market is now pricing a dovish pivot by the Federal Reserve, compounded by remarks from Chair Jerome Powell yesterday saying policymakers’ forecasts anticipate one more interest-rate hike, which he subsequently clarified is in reference to the Fed’s most recent dot plot and not an actual preview of what the Fed will do. Markets now await core PCE data later today for further clues around the Fed’s next move, even as they expected US rates to drop to 4.3% by the end of the year, around 70 basis points lower than the current level.

“Some investors may be jumping the gun, I would be quite cautious about these signals,” said Gilles Guibout, head of European equity strategies at AXA Investment Managers SA. “Yes the Nasdaq may be up 20%, but that does not necessarily mean that we are in a new cycle or that the same risks which weighed just recently have waned.” The current rally is built more on expectations than actions, leaving the market vulnerable should central banks disappoint investors, Veyret added.

“Market sentiment remains relatively positive, and investor confidence remains high despite the recent turmoil brought by the financial sector, as appetite for risk gets supported by the prospect of dovish pivots from central banks, providing a good excuse to push stock indices higher just before the end of the quarter,” said Pierre Veyret, a technical analyst at ActivTrades.

Citigroup strategists also say markets are being complacent, having ignored recession risks and rallied from October lows on “soft” or even “no-landing” narrative. Based on their model, quantitative strategists including Alex Saunders see recession risks remaining high, with economists still having that eventuality penciled in for the second half.

On the other end, Goldman strategists said investors should buy US growth stocks with high margins, while avoiding low-margin ones even as equity and rates markets are at odds over the likelihood of a recession. If the economy avoids recession, real yields are likely to rise and valuations for growth stocks with low margins are more sensitive to higher yields, strategists including Ryan Hammond and David Kostin wrote in a note.

Meanwhile, global stocks and bonds are moving more closely in line with each other than they have in nearly three decades, providing a headache for fund managers seeking to spread their risk. On a brighter note, correlation among stocks globally is low which should be a good environment for stock pickers, according to Bernstein strategists Sarah McCarthy and Mark Diver.

European stocks rose to their highest level in almost three weeks as financial-stability concerns continue to recede. The Stoxx 600 is up 1% with retail, real estate and banks the strongest-performing sectors. Major EMEA markets are higher, led by Spain with the UK lagging. Preliminary CPI data is printing lower MoM and coming in below expectations. Recent IPOs/Hyper Growth are the best performing single baskets, +2.5%+. Vol is leading, Quality is lagging; Value over Growth; Cyclicals over Defensives. UKX +0.7%, SX5E +1.1%, SXXP +0.9%, DAX +1.0%. Real estate stocks lead European equity gains Thursday, extending the previous session’s rebound, as bond yields slipped and markets trimmed peak interest-rate bets. The Stoxx 600 Real Estate Index was 3.1% higher, with all 34 members of the gauge in the green; the index had risen 2.6% on Wednesday. Here are the biggest European movers today:

- H&M shares jump as much as 13% after the clothing retailer reported profits that beat consensus estimates, driven by what Jefferies defines as “over-delivery”

- SSE shares climb as much as 3% after it increased its forecast for full-year earnings, citing the strong performance of its “balanced” business model in a volatile year

- Petrofac rises as much as 73%, the most on record, triggering volatility halts on the stock in London trading after winning a contract to design and install an offshore wind project

- Allegro gains as much as 7.7% after Poland’s biggest e-commerce platform’s 2022 results matched guidance seen previously as ambitious

- Vestas shares jump as much as 6.7%, after the world’s largest producer of wind turbines won its biggest ever onshore order

- SMA Solar shares rise as much as 18%, the most in more than a year, after the German solar equipment maker increased its Ebit guidance for this year by 30%

- JDE Peet’s shares fall as much as 4.3% after Mondelez completed the sale of about 7.7m shares in coffee and tea company at a ~6% discount to last close

- Drax shares drop as much as 12%, the most since May 2022, after the UK power firm’s biomass project was rejected for the nation’s carbon capture and storage program

- S4 Capital shares drop as much as 10% in early trading with analysts saying its mixed results and guidance point to a slower year ahead

- BioMerieux falls as much as 3.4% after holder Sitam Belgique offers shares representing about 0.8% of the biotechnology company via Natixis

- Basler shares slump as much as 18% after the consumer electronics firm released FY23 guidance, which Jefferies said was disappointing on both the top and bottom line

- Paradox Interactive falls as much as 8.4% after the Swedish game developer was downgraded to a short-term hold from buy at Handelsbanken

Earlier in the session, Asian stocks eked out small gains after a rally in US shares overnight, as investors adjusted their positions ahead of quarter-end and markets continued to digest Chinese e-commerce giant Alibaba’s break-up plans. The MSCI Asia Pacific Index reversed earlier losses to rise as much as 0.2%, led by energy and consumer discretionary shares. Australia advanced on the back of strength in US tech shares, while Japanese stocks dropped as a majority of shares traded ex-dividend. India was closed for a holiday. Chinese tech shares gained, lifting the broader market, as investors turned more positive on the sector. In a conference call Thursday, Alibaba’s chief executive Daniel Zhang said the company would gradually give up control of some of its main businesses.

“Alibaba’s spinoffs announced spark thumping revival of Chinese tech optimism and hopes,” Vishnu Varathan, Asia head of economics and strategy at Mizuho Bank, wrote in a note. “This builds on ‘risk on’-type price action,” he said, while “banking fears are relegated for now.” In a busy day of Chinese earnings, major banks including Bank of Communications and the nation’s largest developer Country Garden reported full-year results. The current earnings season is offering investors clues on China’s recovery path as the world’s second-largest economy emerges from Covid Zero. The Asian regional stock gauge was poised to rise about 3% this quarter, extending the momentum seen in the previous quarter, as China’s reopening and easing bets on the Federal Reserve’s interest rate hikes helped sentiment in the region

Japanese equities fell, halting a three-day rally, as 1,500 Topix stocks traded without rights to the next dividend, shaving 23.5 points off the benchmark. The Topix fell 0.6% to close at 1,983.32, while the Nikkei declined 0.4% to 27,782.93. Out of 2,159 stocks in the Topix, 1,330 rose and 748 fell, while 81 were unchanged. “Japanese stocks are down mainly due to the ex-dividend trading,” said Hirokazu Kabeya, chief global strategist at Daiwa Securities. “Otherwise, the receding concerns around banking situation in the US and Europe, and the slight weakening of yen are actually decent conditions for buying Japanese stocks.”

In FX, the greenback gave up an earlier advance after strengthening as investors digested the latest remarks by Fed officials. The Bloomberg Dollar Index is down 0.2% while the Swiss franc is the best performer among the G-10s, closely followed by the British pound and Australian dollar.

In rates, Treasury yields were steady, following muted trading on Wednesday when the 10-year benchmark moved by the smallest margin in more than a month. Treasuries were mixed with the curve steeper as front-end and belly sectors richen vs Wednesday’s close while long-end cheapens slightly. Outperformance by front-end Treasuries steepens 2s10s spread by more than 1bp; 10-year yields little changed around 3.56% narrowly underperforms bunds and gilts. Bund futures rallied after the the German state of North Rhine-Westphalia reported a notable slowdown in CPI, and then extended gains after Spanish inflation came in lower than forecast. Gains proved short-lived, however, with German bonds now lower on the day.

In commodities, oil rebounded amid the continued disruption to shipments from Turkey; WTI rose 0.8% to trade near $73.60. Gold steadied and Bitcoin rose, trading briefly above $29,000. Spot gold adds 0.2% to around $1,968.

Looking to the day ahead, we get initial jobless claims and the final Q4 GDP revision, from Europe we have the Eurozone March economic, industrial and services confidence data, as well as the German March PPI and the Italian February PPI and unemployment rate. We will also be hearing from the Fed’s Barkin as well as Collins.

Market Snapshot

- S&P 500 futures up 0.6% to 4,080

- MXAP up 0.2% to 161.05

- MXAPJ up 0.6% to 520.59

- Nikkei down 0.4% to 27,782.93

- Topix down 0.6% to 1,983.32

- Hang Seng Index up 0.6% to 20,309.13

- Shanghai Composite up 0.7% to 3,261.25

- Sensex up 0.6% to 57,960.09

- Australia S&P/ASX 200 up 1.0% to 7,122.34

- Kospi up 0.4% to 2,453.16

- STOXX Europe 600 up 1.0% to 454.56

- German 10Y yield little changed at 2.31%

- Euro up 0.3% to $1.0872

- Brent Futures up 0.8% to $78.92/bbl

- Gold spot up 0.2% to $1,967.88

- U.S. Dollar Index down 0.23% to 102.40

Top Overnight News

- China’s largest oil producer just had its best-ever year. PetroChina made a profit equivalent to around $22 billion in 2022, around two-thirds higher than it earned the year before. That was in part due to the rise in the average oil price despite a fall in the second half. PetroChina’s bumper earnings led to a jump in its Hong Kong-listed shares, which closed up 7.8% on Thursday. The shares are now trading at their highest level since October 2018. WSJ

- Taiwan President Tsai Ing-wen arrived in New York for a two-night stop in the US amid simmering tensions between Washington and Beijing. Tsai said the security of the world hinges on the self-ruled island’s fate. China warned the trip will have a severe impact on ties with the US. BBG

- Spain’s inflation almost halved in a month to 3.1 per cent in March as energy costs dropped, in a possible early sign of a sharp fall in European headline inflation this year. The year-on-year rise in harmonized Spanish consumer prices compared with the previous month’s rate of 6 per cent and was lower than the 4 per cent forecast by economists polled by Reuters. FT

- Russia’s Federal Security Service said it had detained Wall Street Journal reporter Evan Gershkovich in the Russian city of Yekaterinburg on suspicion of spying, according to reports by the Interfax and RIA Novosti news agencies. NYT

- The EU’s member states and parliament have clinched a deal on higher renewable energy targets after lengthy negotiations, including carve-outs on nuclear energy following pressure from France. FT

- The UK is to allow investors to count nuclear energy as a “green” investment. In an announcement on Thursday, the government said it would include nuclear in the UK’s green taxonomy — a system used by investors to determine whether an investment is counted as sustainable or not. FT

- The White House is planning as soon as this week to recommend tougher rules for midsize banks, according to people familiar with the matter, after the collapse of two lenders earlier this month sent tremors through the banking system. The recommendations are expected to call for new rules from the Federal Reserve and other agencies, including for banks with $100 billion to $250 billion in assets. WSJ

- Dated Brent — which sets the price for about two-thirds of global supply — is about to be transformed for good as Platts will soon use West Texas crude to help determine prices. The switch, which has been fraught with controversy, comes as the existing benchmark is slowly running out of tradable oil. BBG

- Blackstone’s Steve Schwarzman said the banking turmoil was “caused by people on iPhones and other devices” rather than a wave of bad loans. People heard on social media that a bank might be in trouble and “responded with huge withdrawals in a very short period of time,” he said in an interview. Most US banks can withstand the current crisis, which is simply an interim issue, he added. BBG

- Bank of Japan Governor Haruhiko Kuroda changed the course of global markets when he unleashed a $3.4 trillion firehose of Japanese cash on the investment world. Now Kazuo Ueda is likely to dismantle his legacy, setting the stage for a flow reversal that risks sending shockwaves through the global economy: BBG

- After the fall of Credit Suisse and its hastily arranged merger with its rival — and the return of former UBS chiefSergio Ermotti — Switzerland sees just one big winner and a lot of losers: BBG

- Investors are betting one major central bank will successfully navigate the policy tightening required to cool inflation without sending its economy into reverse: the Reserve Bank of Australia: BBG

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks traded mixed as the region only partially sustained the momentum from the US where the Nasdaq 100 entered a bull market after the recent bond selling slowed and as banking sector fears continued to subside. ASX 200 was higher with strength in tech, mining and financials leading the broad optimism across sectors and amid an adjustment in rate expectations with NAB lowering its peak rate forecast to 3.85% from 4.10%. Nikkei 225 was pressured heading closer to fiscal year-end amid mild upside in Japanese yields and with notable weakness across large transportation/logistics companies. Hang Seng and Shanghai Comp. were indecisive and ultimately faltered despite another substantial liquidity effort by the PBoC with participants digesting a slew of earnings releases and as US-China frictions lingered.

Top Asian News

- Chinese Premier Li said at the Boao Forum that to achieve greater success, chaos and conflicts must not happen in Asia otherwise the future of Asia will be lost and they oppose taking sides, forming new blocs and a new Cold War. Premier Li also commented that the economic situation in March is even better than in January and February, while they will consolidate the recovering trend of China’s economy and promote a continued recovery, as well as roll out new measures to increase market access and improve the business environment, according to Reuters.

- Spanish PM Sanchez said at the Boao Forum that relations between Europe and China, and by extension between Spain and China, do not need to be confrontational, while he added there is ample room for win-win cooperation and that they must remain partners economically and beyond, according to Reuters.

- China and Brazil reached an agreement to trade in their own currencies, ditching the US dollar as an intermediary.

European bourses are in the green, Euro Stoxx 50 +1.2%, following soft inflation prints via Spain and the German state’s ahead of the mainland figure. Sectors are similarly bolstered with defensives lagging while Retail and Real Estate outperform given H&M and (initially) lower yields respectively. Stateside, futures are firmer though the magnitude is more modest and sees the region holding onto their recent upside ahead of data/Fed speak. Blackstone (BX) CEO Schwarzman says their property investment is in good shape. Google (GOOG) Cloud VP says Microsoft (MSFT) is selectively buying out complainants and “definitely” has a very anti-competitive posture in cloud; criticised imminent deals with EU cloud rivals.

Top European News

- UK Chancellor Hunt is on course for a clash with BoE Governor Bailey after Hunt refused to rule out watering down post-financial crisis banking rules despite the BoE warning against weakening banking regulation, according to The Telegraph.

- UK Chancellor Hunt said Britain will not go toe-to-toe with the US and EU by offering billions in green subsidies, according to The Times.

- ECB’s Schnabel said a rise in unit labour costs indicates possible second-round effects on inflation and her suspicion is that the energy impact won’t drop out of core inflation quickly, while she also noted that they have not seen general outflow from Eurozone bank deposits, according to Reuters.

- ECB’s Elderson says if the baseline scenario is met, there will be more ground to cover and rates will have to be increased further, adds we are not seeing any movements in the bond markets that give us cause for concern.

FX

- Dollar broadly softer on the eve of PCE data, as Fed Chair Powell points to dot plots showing one more hike in the cycle, DXY dips below midweek low. between 102.780-340 parameters as month-end positioning persists.

- Euro wobbles in wake of soft EZ inflation metrics before recovering ground vs Buck on a 1.0800 handle.

- Pound underpinned by firm UK implied rates and yields, with Cable hovering around 1.2350 and EUR/GBP eyeing 100 DMA just under 0.8800.

- Franc shrugs off sub-forecast Swiss Kof ahead of speeches from SNB, as USD/CHF approaches 0.9150 from around 0.9200 at one stage.

- PBoC set USD/CNY mid-point at 6.8886 vs exp. 6.8901 (prev. 6.8771).

- Brazil’s proposed new fiscal rules would target zero primary deficit next year, a primary surplus of 0.5% of GDP in 2025 and 1.0% of GDP in 2026, according to sources cited by Reuters.

Fixed Income

- Bunds led an initial rally in fixed following the cooler North Rhine-Westphalia inflation reading and thereafter peaked at 136.77 following a similarly ‘cool’ Spanish figure.

- Action which lifted USTs and Gilts in tandem to 114.23+ and 1014.47 respective peaks.

- However, this has since seen a marked reversal which was possibly Gilt/Sonia-led, irrespective of obvious catalyst; as such, core benchmarks are now essentially unchanged on the session ahead of the German mainland and US data points/speakers.

Commodities

- Crude benchmarks are bolstered by the softer USD and supportive risk tone following Wednesday’s slightly lower settlement; WTI and Brent at the top-end of circa. USD 1/bbl parameters.

- Specifics have been light for crude and also gas markets, with the latter subdued and featuring Dutch TTF in relative proximity to the unch. mark.

- Metals are marginally firmer, in-line with the magnitude of US equity futures, deriving support from the USD/sentiment; Citi cuts its 2023 Palladium view to USD 1500/oz (prev. 2025/oz).

- Specifically, spot gold is at the mid-point of USD 1955-1971/oz boundaries, with the 10-DMA at USD 1970.80/oz capping action thus far.

Geopolitics

- Explosions were heard in the vicinity of Syria’s capital of Damascus amid Israeli ‘aggression’, according to the state news agency.

- China’s Defence Ministry says China’s military is willing to work with Russia’s military to strengthen strategic communication and coordination.

- Russia’s Federal Security Service (FSB) says a WSJ reporter has been detained for espionage, according to Interfax; WSJ reporter Gershkovich detained in Russia, according to Bloomberg.

US Event Calendar

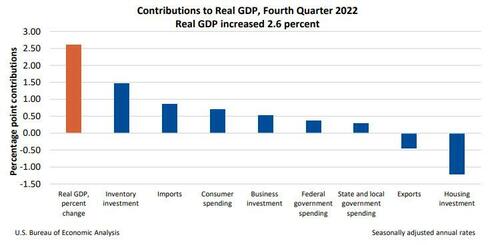

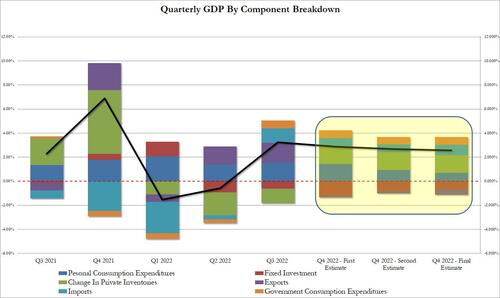

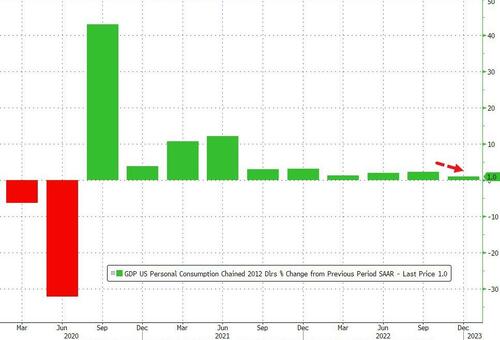

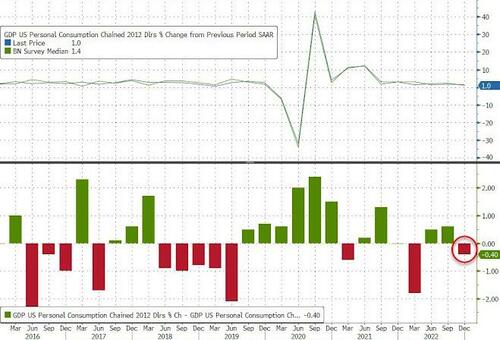

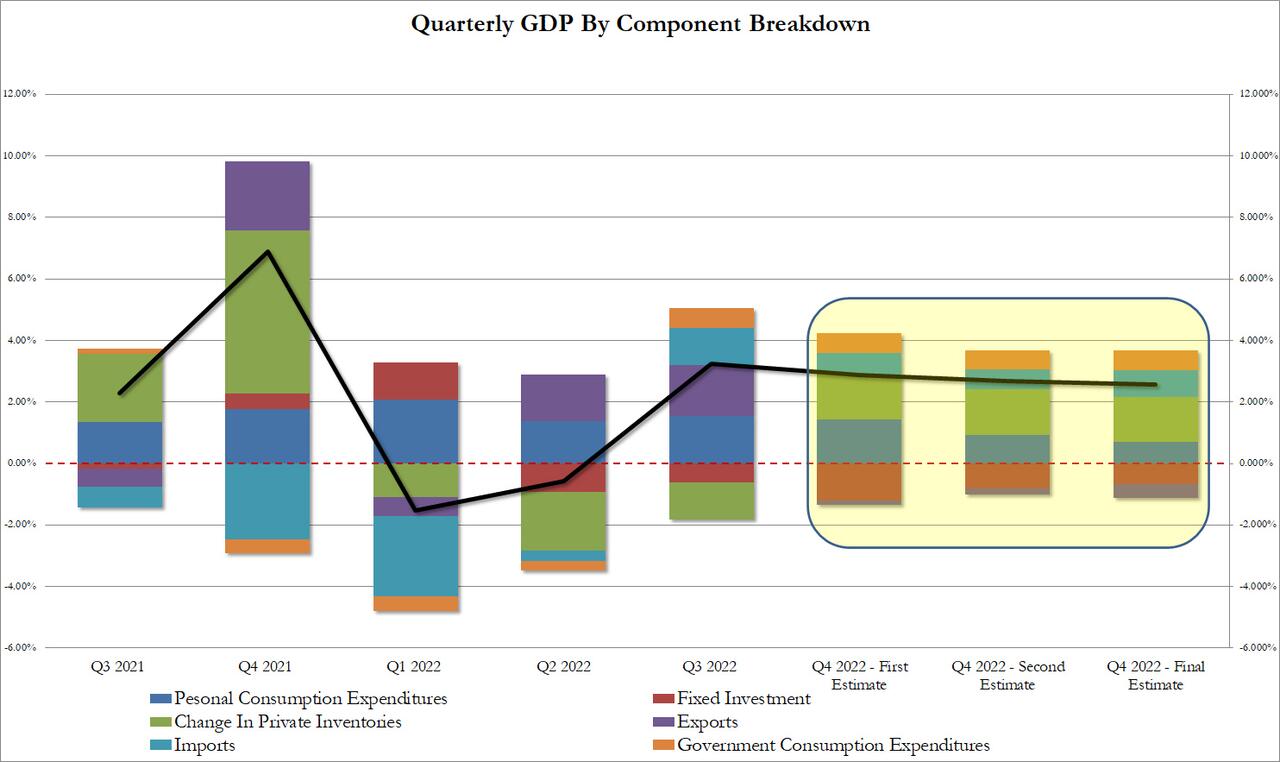

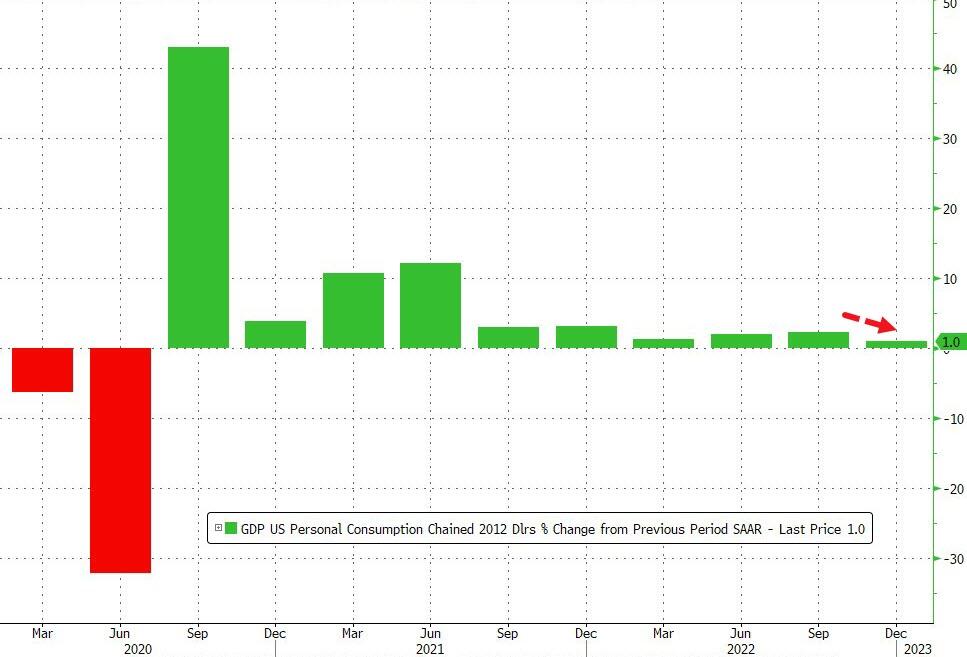

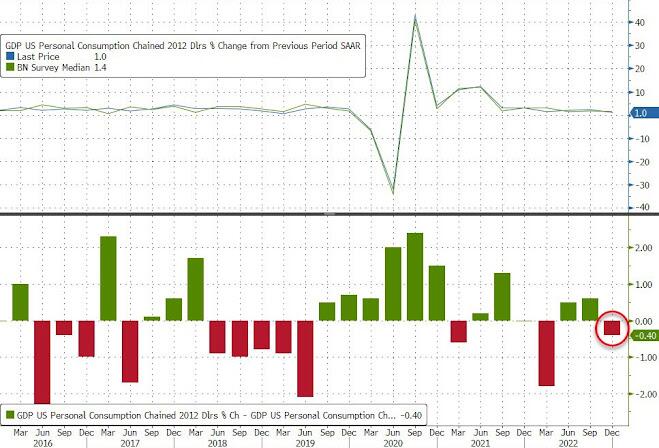

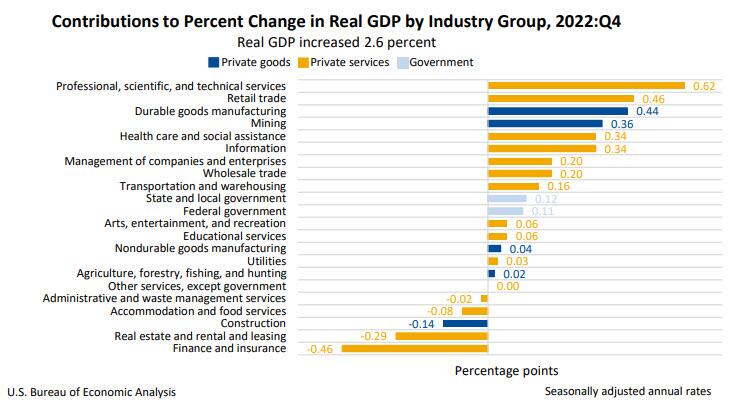

- 08:30: 4Q GDP Annualized QoQ, est. 2.7%, prior 2.7%

- 4Q Personal Consumption, est. 1.4%, prior 1.4%

- 4Q GDP Price Index, est. 3.9%, prior 3.9%

- 4Q PCE Core QoQ, est. 4.3%, prior 4.3%

- 08:30: March Initial Jobless Claims, est. 195,000, prior 191,000

- March Continuing Claims, est. 1.7m, prior 1.69m

DB’s Jim Reid concludes the overnight wrap

Right. I’m off skiing for the first time in nearly 3.5 years tomorrow. Wish me luck for the 14-hour drive. The good news is that Maisie is returning to ski school as her recovery from being in a wheelchair for 14 months continues well. The twins are also doing ski school for the first time. Hopefully learning this early will prevent them having the injuries I’ve had skiing (5 knee and one shoulder op in last 8 years) after taking it up when I was 30 and thinking I was of Olympic standard. Talking of injuries, I had another back injection under general anaesthetic yesterday and in the theatre, there were about 15 nurses and medical staff for a relatively simple, short procedure. I joked to the consultant that there were far less people in the room when my wife had a complicated, high risk twin birth! So hopefully my body will hold up. See you in a couple of weeks. You’ll be in good hands when I’m away.

As I pack my bags, that’s three days in a row now where not much has happened. If this carries on for much longer we’ll soon start to worry about tomorrow’s US core PCE inflation print again and maybe a Fed that will have to keep on raising rates. We also have German inflation today so it’s perhaps a good sign that we’re starting to focus on these type of things again. By the time you read this the first regional number will be out from North Rhine Westphalia. ECB Chief Economist Lane even discussed yesterday how from a macroeconomic perspective recent events were a non-event. He expects the recent turmoil in the financial sector to “settle down”, and that rather than rate cuts “more hikes will be needed” instead.

The worry I have is that policy is still not tight enough to completely tame inflation organically, but starting to get too tight to avoid accidents. Clearly if the accident is bad it can easily cause a big enough economic shock to make a big dent in lowering inflation. Has the last three weeks been a bad enough accident? Well it will almost certainly tighten bank lending standards relative to what would have happened (we think they would have tightened anyway). If that’s the worst of it, this could translate to a slow weakening for the economy over several months rather than an immediate shock. If so inflation could stay on the high side for a few months, and it will take a brave Fed/ECB to decide to ignore it and instead focus on the financial stability risks instead if we have a period of calm.

For now we’re back to risk-on. The S&P 500 (+1.42%) closed at above the levels seen before a pretty high percentage of us had ever heard of Silicon Valley Bank 3 weeks ago. At the same time US Treasury yields plateaued across the curve yesterday after climbing steadily, but substantially, since last Friday lunchtime.

In US equity markets, all industry groups were up on the day, driven by strong performance in semiconductor (+2.82%), autos (+2.64%), real estate (+2.34%) and technology hardware (+1.95%). The last of which helped the NASDAQ, which was up +1.79% and set for its best quarter since 2020 if nothing goes wrong in the next couple of days. Toward the end of the US trading session, there was a Bloomberg report that the FDIC was planning on having the biggest US banks shoulder a “larger-than-usual” share of the $23bn cost from the SVB and Signature bank failures. This news saw the S&P Banks index fall -0.8% as the news broke an hour before the US close, but bank stocks fully retraced this move and finished up +1.40% on the day.

Over the pond, the European STOXX 600 climbed +1.30%, driven by similar outperformance in the tech sector which rose by +2.67%, which tied with real estate for the best sector in Europe yesterday. Bank shares in Europe remained resilient as the index rose +1.92% on the day. Looking more closely, UBS rose +3.72% after news that the former CEO was being bought back to manage the recent acquisition of Credit Suisse.

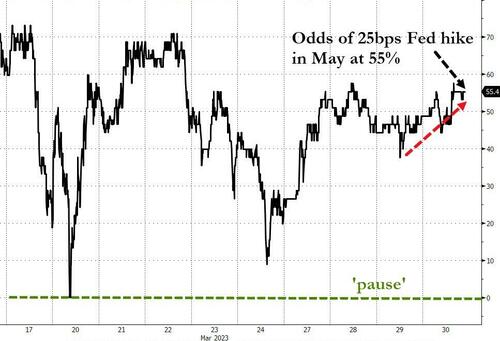

We heard from Fed’s Barr yesterday, who highlighted that the Fed intends to maintain its “meeting-by-meeting judgement on rates” and that “incoming data” will continue to be analysed. With Barr’s comments consistent with the previous messaging coming from Chairman Powell, the expected rate for May’s meeting remained little changed, rising by +0.6bps. For December’s meeting, the implied rate rose +2.9bps, pricing in 58bps of cuts into year-end from the terminal rate priced for May. 10yr Treasury yields traded largely flat on the day, moving between small gains and losses before yields finished down -0.5bps at 3.564%, their smallest move in either direction since the news on SVB broke mid-March. There was a similar story for US 2yr yield, which traded in a 13bp range before finishing up +1.9bps to 4.10%.

Back to Europe and apart from Lane we heard from the ECB’s Kazmir yesterday who emphasised that the members of the governing council had “agreed we will not give guidance about May ECB policy meeting.” Kazmir also stated that the “ECB shouldn’t back down on rates but maybe slow the pace.”

Against this backdrop, the ECB rate priced in by overnight index swaps for the December meeting rose +3.7bps, bringing the expected rate to 3.334% so pricing in just 5bps of cuts by year-end, given the current terminal rate is priced at 3.39% in October. 10yr bund yields rose +3.8bps, while the more interest rate sensitive 2yr yield climbed +6.3bps.

Markets are a little softer in Asia overnight. As I check my screens for one last time for a couple of weeks, the Nikkei (-0.73%) is leading losses with the Hang Seng (-0.50%) also slipping even though Alibaba (c.+1%) is extending its gains after jumping +12% yesterday on news of its major shakeup. In mainland China, the Shanghai Composite (-0.24%) and the CSI (-0.21%) are also lower. Elsewhere, the KOSPI (+0.51%) is bucking the negative trend in early trade. US stock futures tied to the S&P 500 (-0.05%) and NASDAQ 100 (-0.17%) are drifting lower. Yields on the 10yr as well as 2yr Treasury are both up +1bps, trading at 3.57% and 4.11% respectively as we go to press.

Early morning data showed that Australia’s quarterly job vacancies dipped -1.5% in Feb quarter (v/s -4.6% in the November quarter), marking the third consecutive quarter of decline even as it remains above pre-pandemic levels.

We had several data releases yesterday, with pending home sales for February beating expectations to come in at 0.8% (vs -3.0% expected) month-on-month. Pending home sales year-on-year rose to -21.1% from -22.4%. We saw the US MBA purchase index continue its modest pick-up off very weak levels, coming in at +2.9%, although this is down slightly from +3% last week.

We also had the German GfK consumer confidence come in slightly above expectations at -29.5 (vs -30 expected), although still far below average. In France, the consumer confidence index was in line with expectations at 81, down from 82 in February. Data in the UK yesterday spoke to a stronger real economy, as both February UK consumer credit data (£1.41 billion vs £1.2 billion expected) and mortgage approvals (43.5k vs. 41.3k expected) beat expectations. After the data release, we heard from BoE’s Mann who emphasised that the outlook for the UK economy had improved with the lower energy costs, and for the first time called for minimum buffers for LDI funds.

Moving to commodities markets, the deadlock between Iraq and the Kurdish region was on its third day. One of the biggest oil producers in Iraqi Kurdistan, the Norwegian owned DNO ASA, has decided to lower production as the dispute continues and storage space for inventory begins to diminish. This initially led to rally for oil prices with WTI and Brent crude futures over +1.1% midday before the US stockpiles data showed weaker demand. In all, WTI crude futures fell back -0.31% to $72.97/bbl, while Brent crude also fell short of a 3-day winning streak, down by -0.37% to $78.28/bbl. Finally, off the back of the improved risk sentiment, Bitcoin rallied strongly, up +3.96% on Wednesday to break above $28,000 at $28,392.

Now to the day ahead. From the US we have initial jobless claims, from Europe we have the Eurozone March economic, industrial and services confidence data, as well as the German March PPI and the Italian February PPI and unemployment rate. We will also be hearing from the Fed’s Barkin as well as Collins.

AND 2 b) NOW NEWSQUAWK (EUROPE/REPORT)

Cooler German-state/Spanish inflation metrics supports sentiment; Fed speak ahead – Newsquawk US Market Open

THURSDAY, MAR 30, 2023 – 01:12 PM

- European bourses are higher following cooler German-state/Spanish inflation metrics

- US futures hang onto Wednesday’s upside with current gains more contained vs European peers

- USD softer with Fed speak ahead to the modest benefit of G10 peers, GBP leads with Cable above 1.2350

- Bunds led an initial rally on the inflation figures, though this has since dissipated with benchmarks now near unchanged

- Commodities benefit from the above tone and softer USD with specific newsflow light

- Looking ahead, highlights include German CPI (Prelim.), US Q4 GDP & PCE Prices (Final), Banxico & SARB Policy Announcement, CBRT Minutes, Speeches from Fed’s Barkin, Collins, Kashkari, Treasury Secretary Yellen and SNB’s Maechler & Moser.

View the full premarket movers and news report.

Or why not try Newsquawk’s squawk box free for 7 days?

EUROPEAN TRADE

EQUITIES

- European bourses are in the green, Euro Stoxx 50 +1.2%, following soft inflation prints via Spain and the German state’s ahead of the mainland figure.

- Sectors are similarly bolstered with defensives lagging while Retail and Real Estate outperform given H&M and (initially) lower yields respectively.

- Stateside, futures are firmer though the magnitude is more modest and sees the region holding onto their recent upside ahead of data/Fed speak.

- Blackstone (BX) CEO Schwarzman says their property investment is in good shape.

- Google (GOOG) Cloud VP says Microsoft (MSFT) is selectively buying out complainants and “definitely” has a very anti-competitive posture in cloud; criticised imminent deals with EU cloud rivals.

- Click here for more detail.

FX

- Dollar broadly softer on the eve of PCE data, as Fed Chair Powell points to dot plots showing one more hike in the cycle, DXY dips below midweek low. between 102.780-340 parameters as month-end positioning persists.

- Euro wobbles in wake of soft EZ inflation metrics before recovering ground vs Buck on a 1.0800 handle.

- Pound underpinned by firm UK implied rates and yields, with Cable hovering around 1.2350 and EUR/GBP eyeing 100 DMA just under 0.8800.

- Franc shrugs off sub-forecast Swiss Kof ahead of speeches from SNB, as USD/CHF approaches 0.9150 from around 0.9200 at one stage.

- PBoC set USD/CNY mid-point at 6.8886 vs exp. 6.8901 (prev. 6.8771).

- Brazil’s proposed new fiscal rules would target zero primary deficit next year, a primary surplus of 0.5% of GDP in 2025 and 1.0% of GDP in 2026, according to sources cited by Reuters.

- Click here for more detail.

FIXED INCOME

- Bunds led an initial rally in fixed following the cooler North Rhine-Westphalia inflation reading and thereafter peaked at 136.77 following a similarly ‘cool’ Spanish figure.

- Action which lifted USTs and Gilts in tandem to 114.23+ and 1014.47 respective peaks.

- However, this has since seen a marked reversal which was possibly Gilt/Sonia-led, irrespective of obvious catalyst; as such, core benchmarks are now essentially unchanged on the session ahead of the German mainland and US data points/speakers.

- Click here for more detail.

COMMODITIES

- Crude benchmarks are bolstered by the softer USD and supportive risk tone following Wednesday’s slightly lower settlement; WTI and Brent at the top-end of circa. USD 1/bbl parameters.

- Specifics have been light for crude and also gas markets, with the latter subdued and featuring Dutch TTF in relative proximity to the unch. mark.

- Metals are marginally firmer, in-line with the magnitude of US equity futures, deriving support from the USD/sentiment; Citi cuts its 2023 Palladium view to USD 1500/oz (prev. 2025/oz).

- Specifically, spot gold is at the mid-point of USD 1955-1971/oz boundaries, with the 10-DMA at USD 1970.80/oz capping action thus far.

- Click here for more detail.

NOTABLE HEADLINES

- UK Chancellor Hunt is on course for a clash with BoE Governor Bailey after Hunt refused to rule out watering down post-financial crisis banking rules despite the BoE warning against weakening banking regulation, according to The Telegraph.

- UK Chancellor Hunt said Britain will not go toe-to-toe with the US and EU by offering billions in green subsidies, according to The Times.

- ECB’s Schnabel said a rise in unit labour costs indicates possible second-round effects on inflation and her suspicion is that the energy impact won’t drop out of core inflation quickly, while she also noted that they have not seen general outflow from Eurozone bank deposits, according to Reuters.

- ECB’s Elderson says if the baseline scenario is met, there will be more ground to cover and rates will have to be increased further, adds we are not seeing any movements in the bond markets that give us cause for concern.

DATA RECAP

- German North Rhine-Westphalia State CPI YY (Mar) 6.9% (Prev. 8.5%); MM (Mar) 0.6% (Prev. 1.0%)

- German Saxony State CPI YY (Mar) 8.3% (Prev. 9.2%); MM (Mar) 0.9% (Prev. 0.8%)

- Reminder, the mainland figure is due at 13:00BST; German Nationwide CPI YY is expected at 7.3% (prev. 8.7%) with a forecast range of 6.7-8.1%.

- Spanish CPI Flash NSA YY (Mar): 3.3% vs exp. 3.8% (prev. 6.0%); Core YY 7.5% (prev. 7.6%)

- EU Consumer Inflation Expectations (Mar) 18.9 (Prev. 17.7); Selling Price Expectations (Mar) 18.7 (Prev. 23.8)

- Swiss KOF Indicator (Mar) 98.2 vs. Exp. 100.5 (Prev. 100.0, Rev. 98.9).

NOTABLE US HEADLINES

- Click here for the US Early Morning Note.

GEOPOLITICS

- Explosions were heard in the vicinity of Syria’s capital of Damascus amid Israeli ‘aggression’, according to the state news agency.

- China’s Defence Ministry says China’s military is willing to work with Russia’s military to strengthen strategic communication and coordination.

- Russia’s Federal Security Service (FSB) says a WSJ reporter has been detained for espionage, according to Interfax; WSJ reporter Gershkovich detained in Russia, according to Bloomberg.

CRYPTO

- Coinbase (COIN) is reportedly in ongoing talks about remaining in Canada after a key deadline after Canada’s tightened regulations passed, although its larger rival Binance looks set to close up shop, according to CoinDesk.

APAC TRADE

- APAC stocks traded mixed as the region only partially sustained the momentum from the US where the Nasdaq 100 entered a bull market after the recent bond selling slowed and as banking sector fears continued to subside.

- ASX 200 was higher with strength in tech, mining and financials leading the broad optimism across sectors and amid an adjustment in rate expectations with NAB lowering its peak rate forecast to 3.85% from 4.10%.

- Nikkei 225 was pressured heading closer to fiscal year-end amid mild upside in Japanese yields and with notable weakness across large transportation/logistics companies.

- Hang Seng and Shanghai Comp. were indecisive and ultimately faltered despite another substantial liquidity effort by the PBoC with participants digesting a slew of earnings releases and as US-China frictions lingered.

NOTABLE ASIA-PAC HEADLINES

- Chinese Premier Li said at the Boao Forum that to achieve greater success, chaos and conflicts must not happen in Asia otherwise the future of Asia will be lost and they oppose taking sides, forming new blocs and a new Cold War. Premier Li also commented that the economic situation in March is even better than in January and February, while they will consolidate the recovering trend of China’s economy and promote a continued recovery, as well as roll out new measures to increase market access and improve the business environment, according to Reuters.

- Spanish PM Sanchez said at the Boao Forum that relations between Europe and China, and by extension between Spain and China, do not need to be confrontational, while he added there is ample room for win-win cooperation and that they must remain partners economically and beyond, according to Reuters.

- China and Brazil reached an agreement to trade in their own currencies, ditching the US dollar as an intermediary.

DATA RECAP

- New Zealand ANZ Business Confidence (Mar) -43.4% (Prev. -43.3%); Activity Outlook (Mar) -8.5% (Prev. -9.2%)

2 c. ASIAN AFFAIRS

ASIAN AND AUSTRALIAN CLOSINGS//EUROPE OPENING TRADING:

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED UP 21.19 PTS OR 0.65% //Hang Sang CLOSED UP 116.73 PTS OR 0.58% /The Nikkei closed DOWN 100.85 PTS OR 0.38 % //Australia’s all ordinaries CLOSED UP 1.06% /Chinese yuan (ONSHORE) closed UP TO 6.8719/OFFSHORE CHINESE YUAN DOWN TO 6.8745 /Oil UP TO 74.22 dollars per barrel for WTI and BRENT AT 79.14 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

2 d./NORTH KOREA/ SOUTH KOREA/