April 13/2023 · by harveyorgan · in Uncategorized · Leave a comment·Editi

GOLD PRICE CLOSED: UP $31.70, TO $2041.00

SILVER PRICE CLOSED: UP 48 CENTS AT $25.83

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE $2040.25

Silver ACCESS CLOSE: 25.83

Bitcoin morning price:, $30,228 UP 318 Dollars

Bitcoin: afternoon price: $30,274 UP 364 dollars

Platinum price closing $1055.85 UP $35.45

Palladium price; closing $1520.35 UP $47.30

END

I am back to my usual routine.

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2720.30 UP 22.40 CDN dollars per oz (ALL TIME HIGH 2732.50)

BRITISH GOLD: 1628.30 UP 12.78 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1846.40UP 11.20 euros per oz //(ALL TIME HIGH//1860.82)

COMEX DATA EXCHANGE:

COMEX//NOTICES

EXCHANGE: COMEX

CONTRACT: APRIL 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,010.900000000 USD

INTENT DATE: 04/12/2023 DELIVERY DATE: 04/14/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 18

323 C HSBC 6

363 H WELLS FARGO SEC 29

435 H SCOTIA CAPITAL 6

624 H BOFA SECURITIES 9

657 C MORGAN STANLEY 6

661 C JP MORGAN 73 4

690 C ABN AMRO 1

732 C RBC CAP MARKETS 5

800 C MAREX SPEC 6 4

880 C CITIGROUP 1

880 H CITIGROUP 8

905 C ADM 6

TOTAL: 91 91

MONTH TO DATE: 21,770

JPMorgan stopped 4/91 contracts

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2023. CONTRACT: 91 NOTICES FOR 9,100 OZ or 0.28300 TONNES

total notices so far: 21,770 contracts for 2,177,000 oz (67.713 tonnes)

SILVER NOTICES: 5 NOTICE(S) FILED FOR 25,000 OZ/

total number of notices filed so far this month : 304 for 1,520,000 oz

END

GLD

WITH GOLD UP $31.70

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD://////A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD

INVENTORY RESTS AT 934.08 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 48 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV//: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 470.974 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 2996 TO 145,695 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS GIGANTIC SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG $0.30 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. WE HAVE NOW SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.30). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A MONSTER GAIN ON OUR TWO EXCHANGES 1586 CONTRACTS. WE HAD 425 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 13.330 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS( 1586 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.055 MILLION OZ(FIRST DAY NOTICE)+ THE 13.330 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 14.96 MILLION OZ/ //// V) HUGE SIZED COMEX OI GAIN/ HUGE SIZED EFP ISSUANCE/.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –378 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 8 days, total 13,050 contracts: OR 65.250 MILLION OZ . (1631 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR:62.250 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE BUT BELOW LAST MONTH

APRIL 62.25 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2996 CONTRACTS WITH OUR $0.30 GAIN IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1586 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 1.055 MILLION OZ//FIRST DAY NOTICE// 20,000 OZ QUEUE JUMP (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 4.75 MILLION NEW EXCHANGE FOR RISK ISSUED EARLY IN APRIL (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 14.96 MILLION OZ .. WE HAVE A GIGANTIC SIZED GAIN OF 4582 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 5 NOTICE(S) FILED TODAY FOR 25,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 6864 CONTRACTS TO 483,431 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED XX CONTRACTS

WE HAD A GOOD SIZED INCREASE IN COMEX OI ( 6864 CONTRACTS) WITH OUR $6.25 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR APR. AT 66.892 TONNES ON FIRST DAY NOTICE // PLUS A 5200 OZ QUEUE JUMP:(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)YET ALL OF..THIS HAPPENED WITH OUR $6.25 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A VERY STRONG SIZED GAIN OF 10,990 OI CONTRACTS (31. 374 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4126 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 483.431

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,087 CONTRACTS WITH 5961 CONTRACTS INCREASED AT THE COMEX AND 4126 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 10,990 CONTRACTS OR 34.183 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4126 CONTRACTS) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI (6864 //TOTAL GAIN IN THE TWO EXCHANGES 10,990 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 66.892 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 5200 OZ//NEW STANDING 69.576 TONNES // ///3) ZERO LONG LIQUIDATION//4) GOOD SIZED COMEX OPEN INTEREST GAIN/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 31,412 CONTRACTS OR 3,141,200 OZ OR 97.70 TONNES IN 8 TRADING DAY(S) AND THUS AVERAGING: 3926 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES 97.70 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 97.70/3550 x 100% TONNES 2.75% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 97.70 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 2990 CONTRACTS OI TO 145,695 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 243 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1586 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1586 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3374 CONTRACTS AND ADD TO THE 1586 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE GAIN OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 4582 CONTRACTS.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //22.910 MILLION OZ

OCCURRED DESPITE OUR $0.30 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

NORTH KOREA/SOUTH KOREA

i)THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 8.02 PTS OR .76% //Hang Seng CLOSED UP 34.62 POINTS OR .17% /The Nikkei closed UP 74.27 PTS OR 0.26% //Australia’s all ordinaries CLOSED DOWN 0.24 % /Chinese yuan (ONSHORE) closed UP TO 6.8777/OFFSHORE CHINESE YUAN UP TO 6.8835 /Oil UP TO 86.38 dollars per barrel for WTI and BRENT AT 83.03 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 6864 CONTRACTS UP TO 483,431 WITH OUR GAIN IN PRICE OF $6.25 ON WEDNESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF APRIL… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4126 EFP CONTRACTS WERE ISSUED: : JUNE 4126 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4126 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 10,990 CONTRACTS IN THAT 4126 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED GAIN OF 6864 COMEX CONTRACTS..AND THIS VERY STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $6.25. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (69.576) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 69.576 tonnes

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $6.25 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR VERY STRONG SIZED GAIN OF 10,990 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 34.183 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (66.892 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 5200 OZ… ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $6.25

WE HAD +903 CONTRACTS ADDED TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 10,990 CONTRACTS OR 1,099,000 OZ OR 34.183 TONNES.

Estimated gold comex today 189,246 poor

final gold volumes/yesterday 240,167 fair

//APRIL 13/ APRIL 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 643.02 oz 20 kilobars DELAWARE . |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | NIL OZ |

| No of oz served (contracts) today | 91 notice(s) 9100 OZ 0.2830 TONNES |

| No of oz to be served (notices) | 599 contracts 59,900 oz 1.863 TONNES |

| Total monthly oz gold served (contracts) so far this month | 21,770 notices 2,177,000 OZ 67.713 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: NIL oz

customer withdrawals: 1

i) Out of DELAWARE: 643.02 oz (20 kilobars)

total withdrawals: 643.02 oz

Adjustments; 1

I) OUT OF MANFRA: 6269.445 OZ DEALER TO CUSTOMER

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of APRIL we have an oi of 690 contracts having LOST 133 contracts. We had 185 contracts served upon yesterday so we GAINED 52 contracts or 5200 oz were QUEUE JUMPED.

May gained 30 contracts up to 1988.

June GAINED 5268 contracts UP to 408,539 contracts.

We had 91 contracts filed for today representing 9,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 73 notices were issued from their client or customer account. The total of all issuance by all participants equate to 91 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 4 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2023. contract month,

we take the total number of notices filed so far for the month (21,770 x 100 oz ), to which we add the difference between the open interest for the front month of (APRIL. 690 CONTRACTS) minus the number of notices served upon today 91 x 100 oz per contract equals 2,236,800 OZ OR 69.576 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:No of notices filed so far (21,770 x 100 oz)+ 690 OI for the front month minus the number of notices served upon today (91)x 100 oz} which equals 2,236,800 oz standing OR 69.576 TONNES in this active delivery month of APRIL..

TOTAL COMEX GOLD STANDING: 69.576 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,654,200.280 OZ 51.452 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,277,405.516 OZ

TOTAL REGISTERED GOLD: 12,277,405.516 (381.87 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 9,671,321.250 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,017,121 OZ (REG GOLD- PLEDGED GOLD) 249.366 tonnes//

END

SILVER/COMEX

APRIL 11//2023// THE APRIL 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,161,72..869 oz CNT BBRINKS DELAWARE JPMORGAN LOOMIS . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | NIL oz |

| No of oz served today (contracts) | 5 CONTRACT(S) (25,000 OZ) |

| No of oz to be served (notices) | 22 contracts (110,000 oz) |

| Total monthly oz silver served (contracts) | 304 Contracts (1,520,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

Total deposits: nil oz

JPMorgan has a total silver weight: 141.735 million oz/274.401 million =51.63% of comex .//dropping fast

Comex withdrawals: 5

i) Out of CNT: 14,773.800 oz

ii) Out of Brinks: 972.100 oz

iii) Out of Delaware: 6007.339 oz

iv) Out of JPMorgan: 539,818.020 oz

v) Out of Loomis 600,158.610 oz

Total withdrawals; 1,161,729.610 oz

adjustments: 1

dealer to customer JPMorgan: 676,075.200 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 34.117 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 274.401 million oz

CALCULATION OF SILVER OZ STANDING FOR MAR

silver open interest data:

FRONT MONTH OF APRIL /2023 OI: 27 CONTRACTS HAVING GAINED 2 CONTRACT(S. WE HAD 2 NOTICES FILED ON WEDNESDAY SO WE GAINED 4 CONTRACTS OR AN ADDITIONAL 20,000 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF APRIL.

MAY SAW A LOSS OF 3706 CONTRACTS DOWN TO 81,853

JUNE HAD A 36 CONTRACT GAIN TO 126

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 5 for 25,000 oz

Comex volumes// est. volume today 85,005 strong

Comex volume: confirmed yesterday: 108,880 huge

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 304 x 5,000 oz = 1,520,000 oz

to which we add the difference between the open interest for the front month of APRIL(27) and the number of notices served upon today 5 (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2023 contract month: 304 (notices served so far) x 5000 oz + OI for the front month of APRIL (27) – number of notices served upon today (5 )x 500 oz of silver standing for the APRIL. contract month equates 1.6300 million oz +/ EXCHANGE FOR RISK NOW TOTALS 13.330 MILLION OZ //new total standing 14/96 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

GLD INVENTORY: 934.08 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

CLOSING INVENTORY 470.974 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Peter Schiff: The World Is Starting To Divest Itself Of The Dollar

WEDNESDAY, APR 12, 2023 – 06:20 PM

In a surprise move earlier this month, OPEC announced further oil production cuts of about 1.16 million barrels per day. Analysts projected the cuts could raise the price of oil by $10 per barrel. Peter Schiff recently appeared on NewsMax’s Wake Up America and explained why these production cuts will further complicate the Federal Reserve’s efforts to fight price inflation, and more broadly, how global moves like this and others undermine the dollar.

Peter called the production cuts “a very big deal” and said it is clearly complicating efforts to bring down price inflation — especially given the fact that we’re in the midst of another financial crisis.

Not only is the supply of oil going to come down, but the supply of money – US dollars – used to buy oil is going up. The Fed has already gone back to quantitative easing to bail out the banks. So, we’re printing more money, but we’re not producing as much oil.”

Compounding the problem is the fact that the world is starting to divest itself from US dollars.

That will put more downward pressure on the value of the dollar, which of course will put more upward pressure on the price of oil.”

Wake Up America host Carl Higbie noted that President Trump made energy independence a priority. Peter said it’s not just energy independence that is necessary.

We need to be able to produce everything. We’re dependent on the rest of the world for everything that we consume because we no longer have the industrial capacity that we once enjoyed because of the policies that have been pursued for decades. We have too much regulation. We have too high taxes and too much government spending, and so we’re not producing what Americans consume. We rely on the rest of the world.”

Peter pointed out that the only way the US can rely on the world as it does is because the dollar is the reserve currency.

We may lose that privilege over the next several years, maybe even over the next few months. Who knows?”

The BRICS nations recently announced plans for a new currency. Higbie asked what impact that could have even if it only usurps a small percentage of global trade in dollars. Peter said he thinks it would hurt “substantially.”

And once they start moving in that direction, the pendulum is going to continue to swing. There are all sorts of reasons why the world should want to divest of dollars and no longer depend on the US dollar as a reserve currency, but we gave them another one. The Biden administration in slapping those economic sanctions on Russia really highlighted how dangerous it is to allow the United States to enjoy this privilege. And so, we have scared the world into divesting of dollars, something they should have done anyway because it was in their economic interest to do so.”

Peter emphasized that the dollar’s role as the world currency is a huge privilege for the US that the rest of the world pays for.

It enables Americans to live beyond our means. We’re able to consume all kinds of stuff that we did not produce. And the only reason we could do that is because we could print money that costs us nothing and our trading partners will accept that instead of actual goods. If we lose that privilege, our standard of living is going to implode.”

Higbie asked Peter what he would tell Joe Biden to do if he had 30 seconds with the president.

Well, he needs to resign. But he also needs to take Kamala Harris with him. But what we need is free market capitalism. We don’t need more government solutions to government-created problems. Government has to get out of the way so free market capitalism can clean up the mess government created.”

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//

“Lions Led by Donkeys:” The Irrevocable Decline in US Hegemony

Matthew Piepenburg

April 12, 2023

In his latest conversation with WTFinance’s Anthony Fatseas, Matterhorn Asset Management principal Matthew Piepenburg answers the question: Is the worst behind us?

The short answer is: No. The reasons, and signals, however, are many, which Piepenburg addresses from both a broad and market-specific perspective.

Piepenburg’s analysis begins and ends with a string cite of bond-market-driven signals and crises—from the repo disaster of 2019 to the latest US bank failures of 2023. Piepenburg distinguishes the bank failures of 2008 and 2023, but reminds that the Fed has its fingerprints on every crisis and every artificial “recovery.” The simple math of debt, inflation and monetary policy failures (akin to “credit cards and whiskey”) confirm that cornered central banks have no good options or scenarios left. It’s either tighten into economic depression (hangover) or loosen policy into a hyper-inflationary pain (hangover). The latter is most likely.

Piepenburg also addresses the added stressors of slow but steady de-dollarization and the waning petrodollar by unpacking their impact on desperate and increasingly ineffective Fed and currency options and the invisible tax of inflation. Trust in the experts (from markets, media and foreign policy) is falling because promise after promise has been broken in real-time.

Volatility in the two most important global assets—USDs and USTs–is a clear and present danger. Piepenburg explains how the QT policies of 2022 evolved into the current and predictable market headlines of 2023, including the rise of the BRICS and new trade alliances and alternative payment systems. By welching on the Bretton Woods gold-backed USD of 1944 in 1971, the US has created pent-up distrust of the US currency and IOU’s which means USD hegemony is slowly ending—though this does not mean the end of the USD as the world reserve currency.

Ultimately, Piepenburg advises more critical thinking, which is not the same as “anti-patriotic.” The facts and math of failed financial and military policies out of DC demand closer scrutiny and greater preparation for informed investors, which, as Piepenburg argues, involves a careful look at commodities in general and precious metals in particular.

end

A must view..

Mathew Piepenburg/Adam Taggart

“No Way Out” For Global Markets Trapped In A Doom-Loop Of Debt

https://www.zerohedge.com/markets/no-way-out-global-markets-trapped-doom-loop-debt

THURSDAY, APR 13, 2023 – 07:20 AM

In this compelling conversation with Wealthion founder, Adam Taggart, Matterhorn Asset Management principal, Matthew Piepenburg, addresses the current and vast range of headline market topics, signals and risks. Inflation, deflation, risk assets, bond stress, cryptos, war, bank failures, CBDC’s rise, trapped policy makers and, of course, the topic of precious metals are all carefully and plainly discussed.

Piepenburg’s broader views on current and future financial conditions are bluntly yet realistically presented as a “no way out” scenario for global economies distorted by cornered central bankers.

The bottom line is as simple as it is incontrovertible: The global economy is stuck in a doom loop of debt.

Either central banks raise rates to allegedly “kill inflation” by killing the economy and markets, or they resort to more mouse-click money and kill the currency in your wallet.

Historically, all debt-cornered nations spur collapsing markets followed by collapsing currencies and inflation-driven social unrest. Leaders of all eras and stripes (left or right) then address this unrest with tighter, more centralized controls over our economies and lives. CBDC is a classic and modern symptom of this timeless pattern. So is war. The current era will be no exception, as history (from ancient Rome to Chairman Mao, or Napoleon to the rise of fascist leaders of the 1930’s) offers no exception.

Piepenburg tracks the current evolution of this trend in a Federal Reserve that has tightened too fast and too high, breaking everything in its path in one dis-inflationary debt or banking crisis after the next, which are inevitably “solved” via more inflationary and mouse-clicked dollars. End result? Currency debasement, for which gold is one obvious and historical solution rather than “gold bug” apology.

Topic after topic, issue after issue, Piepenburg shows how there is now no easy or “soft” way out for policy makers who tricked the markets and themselves into believing that a debt crisis could be solved via more debt. In the end, the last bubble to burst is always the currency, and the USD, like every other currency, will be no exception.https://www.zerohedge.com/markets/no-way-out-global-markets-trapped-doom-loop-debt

END

Rickards: The Real Reason Gold Hasn’t Exploded

THURSDAY, APR 13, 2023 – 01:25 PM

Authored by James Rickards via DailyReckoning.com,

The world has changed radically in recent years. We’ve had the worst pandemic since 1918, and the third worst in world history. We’ve had a global supply chain breakdown. Inflation has been the worst since the early 1980s, despite the fact that it’s come down since peaking last June.

Meanwhile, Europe is experiencing its worst war since the end of World War II.

That kinetic war in Ukraine has been accompanied by a financial and economic war between the U.S., the U.K., the EU and Russia that involves extreme financial sanctions, including seizing the central bank reserves of the world’s 11th-largest economy.

That financial war and accompanying sanctions disrupted supply chains on top of the disruptions that were already present. They still persist.

And the world’s second-largest economy, China, locked down 50 million people in Shanghai and Beijing for months in a hopeless and misguided effort to suppress COVID. (China has finally seemed to learn that the virus goes where it wants). Meanwhile, tensions in the Taiwan Strait are high, with a lot of talk about a potential Chinese invasion or blockade of Taiwan. The list goes on.

If gold is the ultimate safe haven for investors and the world has been dangerously unsafe, then the price of gold must have been skyrocketing, right?

That’s not the case. Today gold is about $2,030 per ounce after gaining over $200 in the last month (that price fluctuates daily and intraday). That’s still lower than the $2,069 all-time high of Aug. 6, 2020.

The bottom line is, gold is lower today than it was three years ago. There have been some spills and thrills along the way including two peaks over $2,000 and several smashes down into the $1,680 range, but always followed by a reversion to a persistent central tendency that hasn’t moved much at all.

So, we’re back to the original question. With inflation, shortages, and war all around, why is gold not surging past $3,000 per ounce and making its way to $4,000, $5,000 and beyond?

Supply/demand conditions favor higher gold prices. Global production of gold has remained fairly constant for the past seven years. Over the same seven-year period, during a period when global output was flat, central banks increased their official holdings by over 6%.

China has added over 1,400 metric tonnes in the past thirteen years (that’s the official number; unofficially they probably own far more). Russia has acquired over 1,500 metric tonnes over that same period.

Other large buyers have included Poland, Turkey, Iran, Kazakhstan, Japan, Vietnam and Mexico. Central banks in the Visegard Group (Czech Republic, Hungary, Poland and Slovakia) have also bought gold.

What’s curious is that individual investors in the U.S. still seem indifferent to gold as a monetary asset. In theory, central banks are the most knowledgeable about the real condition of the global monetary system. If central banks are buying all the gold they can with hard currency (dollars or euros), it’s not clear what retail investors are waiting for.

Of course, central bank holdings are only about 17.5% of total above-ground gold and there is far more demand from bullion investors and for jewelry (a form of wearable wealth). Still, central banks are arguably the most knowledgeable market participants; and their steady increases in gold holdings is meaningful.

Interest rates also play a supporting role. Many of the directional moves in gold prices over the past three years have been tied to interest rate moves. The correlation is not perfect, but it is strong.

The rally in gold prices in late 2020 was tied to a fall in interest rates (yield-to-maturity) on the 10-year U.S. Treasury note from 1.930% on December 19, 2019 to 0.508% on July 31, 2020.

Similarly, the fall in gold prices after February 2021 was tied to an increase in interest rates on the 10-year Treasury note from 1.039% on January 2, 2021 to 3.130% on May 2, 2022. Rates are 3.44% as of today.

But I believe that interest rates on the 10-year Treasury note will fall again and will continue to fall as global growth weakens. That’s good news for gold investors. Short-term rates have gone up because of Fed policy, but long-term rates will go down because investors see that the Fed will cause a recession. That correlates with higher gold prices.

While market supply/demand conditions are favorable for gold, and the overall interest rate environment is also favorable for gold, neither has seemed to have the power needed to push gold sustainably past $2,000.

What’s the problem?

The real headwind for gold and the main reason gold has struggled to gain traction for the past three years has been the strong dollar.

After all, the dollar price of gold is really just the inverse of the strength of the dollar. A weaker dollar means a higher dollar price for gold. A stronger dollar means a lower dollar price for gold.

It may seem paradoxical to imagine a strong dollar in the midst of all the inflation we’ve been seeing. But that’s the case.

What’s extraordinary over the past three years isn’t that gold hasn’t soared; it’s that gold has held its own in the face of a persistently strong dollar. So that leads to the next question:

What’s been behind the strong dollar and what could cause the dollar to suddenly weaken and send gold prices into the stratosphere?

The strong dollar has been driven by a demand for dollar-denominated collateral, mostly U.S. Treasury bills, needed as collateral to support leverage on bank balance sheets and in hedge fund derivatives positions.

That high-quality collateral has been in short supply. As banks scramble for scarce collateral, they need dollars to pay for the Treasury bills. That fuels dollar demand.

The scramble for collateral also speaks to fears of a banking crisis in the wake of SVB’s collapse, weaker economic growth, fears of default, decreasing creditworthiness of borrowers and fear of a global liquidity crisis. We’re not there yet, but we’re getting close with no relief in sight.

As weak growth turns into a global recession, a new financial panic will be on the horizon. At that point, the dollar itself may cease to be a safe haven, especially given the aggressive use of sanctions by the U.S. and the desire of major economies such as China, Russia, Turkey, and India to avoid the U.S. dollar system if possible.

When this panic hits and the dollar is deemed no longer reliable, the world will turn to gold.

Frustration with the sideways movement of gold prices is understandable. But behind the curtain, a new liquidity crisis is brewing.

Investors should consider today’s prices a gift and perhaps a last chance to acquire gold at these prices before the real safe haven race begins.

Even above $2,000, gold is so cheap right now, it’s practically a steal.

3,Chris Powell of GATA provides to us very important physical commentaries

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

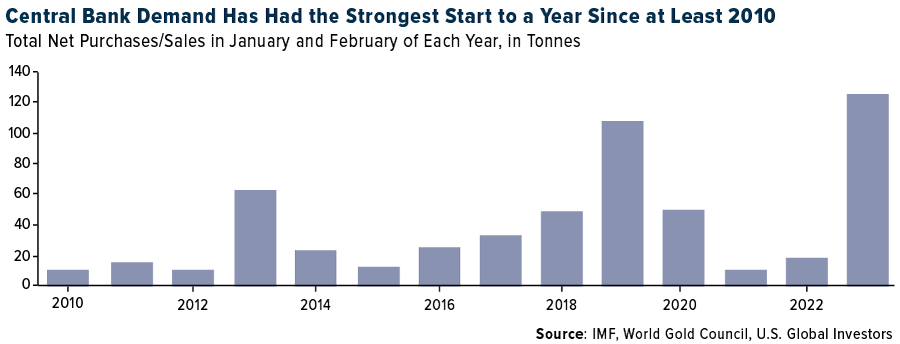

Record New Year for Central-Bank Gold

Frank Holmes – Thursday, 4/13/2023 09:01

Net buying set Jan + Feb record…

JANUARY and February saw central banks accumulate gold at the fastest New Year pace on record, says Frank Holmes at US Global Investors.

According to a report by the World Gold Council’s Krishan Gopaul, central banks collectively bought a net 125 tonnes of the metal in those two months, the highest amount for the year-to-date period since that group became net buyers in 2010.

The countries reporting the largest purchases in the first two months were Singapore (51.4 tonnes), Turkey (45.5 tonnes), China (39.8 tonnes), Russia (31.1 tonnes) and India (2.8 tonnes).

The Central Bank of Russia published an update on its gold reserves for the first time in about a year, so the 31.1 tonnes were likely accumulated over the course of several months instead of in January and February.

Meanwhile, very few countries’ central banks shrank their gold reserves. Net sellers were Kazakhstan, Uzbekistan, Croatia and the United Arab Emirates (UAE), though year-to-date purchases far outweighed sales.

If you look back at the list of net buyers, you’ll notice that three are members of the BRICS countries (Brazil, Russia, India, China and South Africa). I point this out because for the first time ever, BRICS countries’ share of the global economy has surpassed that of the G7 nations (Canada, France, Germany, Italy, Japan, the UK and US), on a purchasing parity basis. So we may be seeing the emergence of a multipolar world, with a US- centric world on one side and a China-centric world on the other.

Gold plays an important role in this multi- polarization. The BRICS need the precious metal to support their currencies and shift away from the US Dollar, which has served as the global foreign reserve currency for about a century. More and more global trade is now being conducted in the Chinese Yuan [Ed: Still barely 2%, way below China’s 18% share of global GDP] and there are reports that the BRICS – which could eventually include other important emerging economies such as Saudi Arabia, Iran and more – are developing their own medium for payments.

If this is indeed the case, the implication is clear to me that investors should be increasing their exposure to gold and gold miners. Gold is a finite resource. It’s expensive and time-consuming to produce more of it. At the same time, BRICS countries will continue to be net buyers as they seek to diversify away from the Dollar.

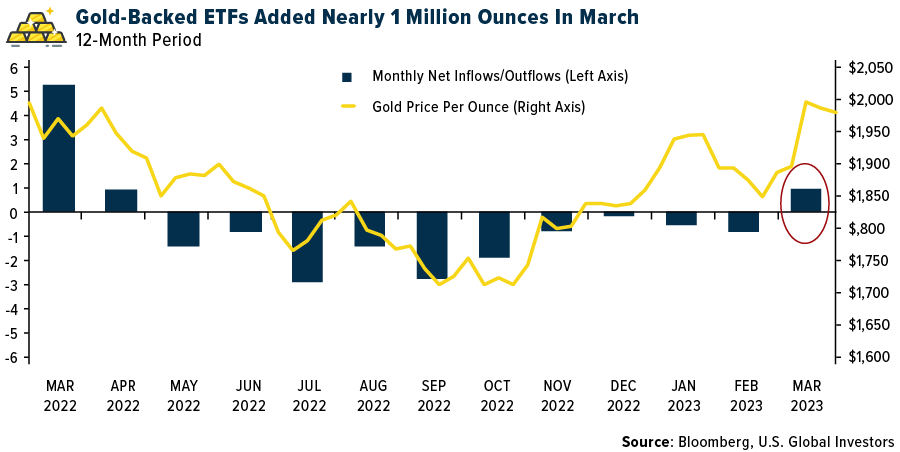

Net inflows into gold-backed ETFs turned positive in March after 10 straight months of outflows as the metal’s price flirts with a new record high.

Investors added nearly 1 million ounces to all known physical gold ETFs in March, the highest monthly increase since March 2022, when investors added 1.4 million ounces. As of March 31, total gold holdings stood at 93.2 million ounces, according to Bloomberg.

In light of weak economic news, ongoing inflation, rising rates, a shaky banking sector and geopolitical tension, gold is catching a strong bid as it seeks to make a new all-time high. On Thursday, the metal touched $2032 an ounce, just $43 off its record high, set in August 2020.

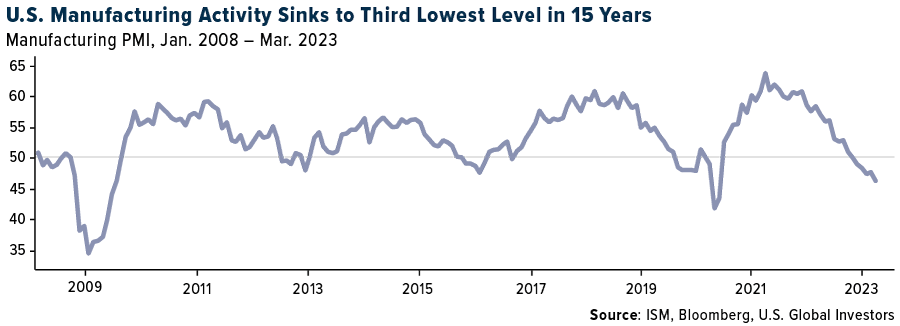

I believe accumulating gold and gold stocks is prudent and wise at this time, especially as recession signals are starting to flash. US manufacturing activity contracted at a faster rate for the fourth straight month, with ISM’s Manufacturing PMI sinking to 46.3 in March. That’s the third-lowest reading in 15 years, following the financial crisis and pandemic lockdowns. What’s more, every category – from new orders to production to inventories – was in contraction mode.

The Federal Reserve’s actions to slow economic growth appear to be having the desired effect. We may be looking at the end of the most aggressive rate hike cycle in two generations, and this carries risks that investors should be aware of.

Over the past 70 years, a Fed pause was followed by an economic recession 75% of the time, with an average lag of six months, according to CLSA’s Alexander Redman and Della Chen. The two analysts believe the Fed has just one more hike to go before it pauses and begins to reverse course. The cycle should be complete by July, Redman and Chen estimate.

If their estimates are correct, we may be looking at a recession late in the fourth quarter.

The time to buy equities, they say, is when the Manufacturing PMI bottoms after the start of the recession. Doing so resulted in positive 12-month returns seven out of eight times, for an average return of 26%.

Timing these things is always tricky, and we’re talking about events that could be months in the future. If a recession is in the cards, it may make sense to ride it out with the help of gold. As always, I recommend a 10% weighting, with 5% in physical gold and the other 5% in high-quality gold mining stocks, mutual funds and ETFs.

-END-

.

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: SUGAR

it appears that we have a sugar shortage as prices hit decade highs

(zerohedge)

Sugar Prices Hit Decade High On Global Shortage Fears

THURSDAY, APR 13, 2023 – 06:55 AM

The world is facing what appears to be a sugar shortage. A lack of deliverable sugar ahead of Friday’s expiry has sent the white-sugar futures contract for May to its highest level in over a decade.

John Stansfield, a senior sugar analyst at DNEXT Intelligence, told Bloomberg that the number of contracts to be closed, also known as open interest, implies a large delivery above 880,000 tons, adding those with short positions “don’t have the physical sugar to tender.”

White-sugar futures have surged nearly 20% in the last three weeks, hitting levels not seen since November 2011.

The price surge, which will increase costs for food producers of various items such as soda, candy, and baked goods, will maintain pressure on global food inflation.

Bloomberg explains the shortage of the sweetener is global:

Prices of the sweetener have jumped on prospects for limited exports out of key shipper India and lackluster supplies from Thailand, Europe, China, and Mexico.

India is one of the largest exporters of white sugar, but shipments are controlled by quotas that are almost exhausted with no real expectation of an increase, said Soren Jensen, a longtime market observer. India’s refining industry might soon have to shift from domestically produced raw sugar to imports — most likely from Brazil. The South American country just started its harvest, but transportation bottlenecks are an issue with sugar competing against a record soybean crop for space on railways and at ports.

And output estimates for the 2022-23 season will worsen the global shortage, according to Wilmar International Ltd. head of analysis Karim Salamon.

Salamon warned:

“Next year’s crop will probably not be better.

“The cane and beet acreage is likely to fall in most areas due to the effects of crop competition.”

A worsening global sugar shortage will be inconvenient for those addicted to candy and junk food. AddictionCenter has suggested that sugar is as addictive as Cocaine.

END

After many major mishaps, JPMorgan is shrinking is base meetals business as they fire dozens of traders along with with bonuses.

(zerohedge)

JPM Shrinks Base Metals Business, Fires Dozens Of Traders, Slashes Bonuses Following Series Of Nickel Scandals

THURSDAY, APR 13, 2023 – 12:10 PM

JPMorgan has fired dozens of base metals clients and slashed bankers’ bonuses, as the business “remains under harsh internal scrutiny in the wake of last year’s nickel crisis”, Bloomberg reported.

JPMorgan, Wall Street’s largest metals trader, has been reviewing its commodity exposure for over a year after it played a prominent role as the biggest counterparty of the Chinese company at the center of the nickel short squeeze on the London Metal Exchange which prompted a widespread backlash against what many viewed as market manipulation meant to bail out a prominent Chinese player. It was also a financier of the top Chinese copper trader whose business ground to a halt after a liquidity crisis last year.

While the review is ongoing, JPMorgan has already scaled back its base metals business substantially, according to Bloomberg sources, with the moves being felt across the industry: as part of the overhaul, the bank has cut numerous base metals clients in Asia, with particularly deep cuts among privately owned Chinese companies. It is continuing to work only with a few large, long-standing clients in the region, they said. Bloomberg last year reported that JPMorgan had stopped new inventory financing in China.

JPMorgan’s base metals team is under heightened internal scrutiny and bonuses for many have been cut, the people added. In the wake of the crisis last March, the bank’s nickel position was overseen by top management, including Chief Operating Officer Daniel Pinto, and its appetite for risk-taking in metals has been reined in.

The retreat by the longstanding market leader comes as the metals world has been grappling with wild price swings, high interest rates, and a series of scandals that have sapped market liquidity. Some other mainstay banks have also pared back their exposure, particularly in Asia, where ICBC Standard Bank had also halted new inventory financing deals for copper in China.

Meanwhile, others have sought to capitalize as JPMorgan pulls back, with several American and European banks seeking to expand in metals in recent months.

As a reminder, JPMorgan played a central role in the nickel crisis that brought the LME to its knees last March. It was the largest counterparty for Tsingshan Holding Group, the company whose huge short position was at the center of the squeeze. It reported a $120 million loss related to nickel in its first quarter results a year ago.

As the largest bank in the base metals industry, it was also involved in the saga in other ways. Court filings have shown that it was a broker for both Elliott Investment Management and Jane Street, which are suing the LME over the decision to cancel trades.

And when Maike Metals International ran into trouble later last year, JPMorgan was left with around 30,000 tons of copper it had been financing for the trading company in Shanghai. In the end, the bank was able to sell the metal without major losses, the people said, but the episode highlighted the risks of trading in China’s base metals industry. Maike has since filed a request for a court-led restructuring.

More recently, JPM was revealed as the owner of $1.3 million of LME nickel contracts that were invalidated after they turned out to be backed by bags of stones.

JPMorgan began monitoring its commodities exposure amid heightened market volatility even before the nickel short squeeze last March, but since then has been conducting a deeper review.

While the bank’s cuts have been focused on base metals, it has also been reviewing its activities across commodities. Several gold refineries have had their credit lines with the lender cut since the nickel crisis, according to people familiar with the matter.

And there have been a number of recent departures from JPMorgan’s commodities team, although they aren’t connected to the review, one of the people said. They include Jack Luo, a London-based banker who played a key role in handling the company’s relationship with Tsingshan and Maike, as well as Amar Singh, the head of commodities sales for Asia Pacific, according to people familiar with the matter.

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//,THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.8777

OFFSHORE YUAN: 6.8835

SHANGHAI CLOSED DOWN 8.02 POINTS OR .26%

HANG SENG CLOSED UP 34.62 PTS OR .26%

2. Nikkei closed UP 74.27 PTS OR 0.26%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 101.02 EURO RISES TO 1.1018 UP 21 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.456Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 133.27 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morninG

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.3778***/Italian 10 Yr bond yield RISES to 4.236*** /SPAIN 10 YR BOND YIELD RISES TO 3.427…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.239

3j Gold at $2026.00 silver at: 25.60 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 33 /100 roubles/dollar; ROUBLE AT 81.61//

3m oil into the 83 dollar handle for WTI and 86 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 133.27 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .456% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8908 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9811 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.4350 UP 2 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.664 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.9829 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.33…

GREAT BRITAIN/10 YEAR YIELD: UP 5 BASIS PTS AT 3.613

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Trade In Narrow Range As Attention Turns To PPI, Jobless Claims

THURSDAY, APR 13, 2023 – 08:06 AM

For the fourth day in a row, US equity futures are effectively unchanged in the overnight action, as the April doldrums continue, and as shown below spoos have traded in a narrow 80 points range all month.

Zooming in on today, we see that S&P futures edged fractionally higher as investors weighed the possibility of a pivot in Federal Reserve policy against increasing expectations of a recession. S&P 500 futures were up 0.2% as of 7:40 am ET while Nasdaq 100 futures gained 0.3%. On Wednesday The S&P 500 cash index dropped on Wednesday after minutes from the Fed’s last meeting showed policy makers expect a mild recession later this year. Both European and Asian stocks edged higher. Treasury yields stayed in a narrow range, with the rate-sensitive two-year holding below 4%. The Bloomberg dollar index dropped for a 3rd day and traded near the lowest level since the start of February.

Among notable movers in premarket trading, US-listed Chinese stocks gained after the Nasdaq Golden Dragon China Index posted its biggest single-day drop in a month. BigBear.ai Holdings Inc. dropped after the software company filed a shelf registration statement for the resale of up to about 113.3m shares of common stock from time to time. Cryptocurrency-exposed stocks climbed in US premarket trading on Thursday as Bitcoin hovers around the closely watched $30,000 level for a third session. Strategists at Bank of America said the rally may have room to run if flows between cryptocurrency exchanges and personal digital wallets are any guide. Riot Platforms +2.5%, Marathon Digital +3.1% and Coinbase +2.3%. Here are some other notable premarket movers:

- Delta Air Lines (DAL) gains as much as 4.1% in premarket trading after the company forecast adjusted earnings per share for the second quarter that beat the average analyst estimate.

- Exxon Mobil Corp. (XOM) shares are down 0.5% in premarket trading, after Scotiabank downgraded the energy giant to sector perform from sector outperform.

- Fastenal (FAST) falls 3.2% in premarket trading after reporting March daily sales growth of 6.8% that is “weaker than previous months”. Its 1Q EPS beats analysts’ expectation.

- LSB Industries (LXU) is cut to hold from buy and its PT halved at Jefferies, with the broker anticipating challenges facing the chemicals firm will continue for several quarters. Shares fall 2.5%.

- LyondellBasell Industries (LYB) is downgraded to hold from buy at Jefferies, with the broker flagging rising risks over US demand for the chemicals company amid growing pressure on consumers. Shares rise 2.7%.

- Precious metals miners rally in US premarket trading as the price of gold gains for a third day and holds above the $2,000/ounce level amid hopes over easier monetary policy by the end of the year.

- Rent the Runway (RENT) falls 4.1% in premarket trading after the fashion rental company’s annual revenue forecast disappointed. The company also said that Chief Financial Officer Scarlett O’Sullivan will transition out of her role.

- Sportsman’s Warehouse (SPWH) tumbles 20% in premarket trading after the sporting-goods retailer provided a weaker- than-expected net sales and profit outlook for the current period, calling out weather-related disruptions.

- Steven Madden (SHOO) is raised to buy from neutral at Citi on the expectation that executives at the shoe company will talk more optimistically about wholesale trends when it reports first- quarter results later this month. Shares rise 2.7% in light premarket trading.

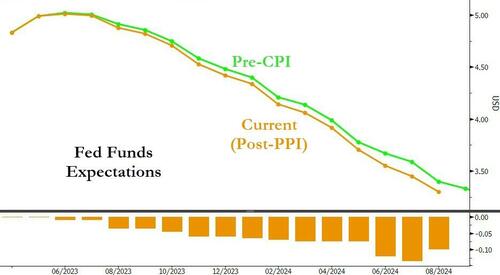

A rally in US stocks faltered this month as mixed economic data as well as the latest FOMC Minutes signaled a recession is inevitable this year, yet stubbornly strong (and manipulated) labor market data has thrown the bears for a loop. But with inflation continuing to cool, investors are now betting the central bank could cut rates before the end of the year.

The latest US inflation report offered evidence for both bond bulls and bears. While the year-on-year headline figure fell, core prices edged higher. Swaps markets still favor a quarter-point hike by the Federal Reserve in May, even as traders added to wagers that the Fed will cut interest rates before the end of this year at a faster pace than anticipated earlier in the week.

“There is sufficient uncertainty for most people to see what they want to see,” said James Athey, investment director at Abrdn. “Equities are taking comfort from the lack of outright ‘bad news’ from the CPI print and the fact that the Fed is still sounding dovish relative to” February, when Fed Chair Jerome Powell suggested borrowing costs may reach a higher peak than traders and policymakers anticipate.

March PPI data is expected by Bloomberg economists to pick up following February’s downside surprise, although a modest rise in the monthly print is viewed as unlikely to change Fed’s course where markets continue to expect a 25bp rate hike.

“US markets are struggling to find a place to settle amid conflicting concerns,” said Sophie Lund-Yates, lead equity analyst at Hargreaves Lansdown. “The Fed minutes show several members are concerned about recession risk. At the same time, we’ve seen recent market moves that seem to be in reaction to the idea that interest rates will be raised further than expected to bring inflation down. Ultimately, uncertainty is high and that will make it difficult for markets to land in any one given spot.”

Elsewhere, investors are set to get a first clue on the health of Corporate America when the big banks kick off the reporting season on Friday. Analysts expect S&P 500 earnings to have dropped 8% in the first quarter — the biggest year-over-year decline since 2020, according to data compiled by Bloomberg Intelligence. Strategists at UBS Global Wealth Management also said the outlook for stocks remains challenging in the absence of a Fed pivot and rising growth risks. They expect US corporate earnings to drop 4.5% in 2023.

European markets were solidly in the green; the Stoxx 600 rose 0.3% and on course for a fourth consecutive increase, with the DAX and FTSE 100 lagging. European luxury-goods stocks have rallied, led by LVMH whose shares rose to a record high after first-quarter sales topped estimates. Here are the biggest European movers:

- LVMH shares rallied to a record high after the luxury retailer reported better-than-expected first-quarter sales, led by Fashion & Leather Goods. The company, the first of the big luxury names to report sales for the period, has set a high bar for rivals, analysts said.

- Tesco shares gain as much as 2.6%, reaching the highest since May, after the UK’s biggest supermarket operator reported full-year adjusted operating profit that met estimates. Analysts liked the results overall, noting the firm’s strong free cash flow and safe-haven credentials.

- Enel slumped after Italian Prime Minister Giorgia Meloni cut an eleventh-hour deal with coalition partners to name industry veteran Flavio Cattaneo to replace Francesco Starace as chief executive officer of the state-controlled company.

- BayWa shares rise as much as 4.7% after M.M. Warburg Investment Research raised the recommendation on the stock to buy from hold on revised estimates from the trading and logistics company.

- EssilorLuxottica shares rise as much as 2.2% as the eye- care group is started with an overweight rating and €215 PT at JPMorgan, with the broker confident the company can continue to outperform the market.

Earlier, Asian stocks edged higher, helped by a rebound in Chinese shares after surprisingly strong exports data. The MSCI Asia Pacific Index was 0.1% higher as of 5:02 p.m. in Hong Kong. A gauge of Chinese shares listed in Hong Kong rose after sliding as much as 2% as data showed the nation’s exports jumped 14.8% in US dollar terms last month, and as investors downplayed concerns over shareholder stake sales in tech firms. Alibaba was among the biggest drags and weighed on a gauge of Hong Kong-listed tech stocks after a Financial Times report that SoftBank is trimming its stake in the Chinese internet firm. That came close on the heels of Wednesday’s selloff in Tencent on news of major shareholder selling. “Reported plans to lower exposure to Alibaba by SoftBank may reiterate the prevailing loss of confidence in Chinese tech firms by foreign investors, giving rise to concerns that more may do the same,” Jun Rong Yeap, market strategist at IG, wrote in a note. US data showed inflation is moderating, but not enough to dissuade the Fed from raising rates again next month. Defensive sectors including health care rose. South Korea led gains among key national equity gauges, while stocks rose in Singapore as well as Hong Kong. Japanese benchmarks also rose during afternoon trading hours amid data showing foreign investors made their largest-ever net purchase of the nation’s stocks last week.

Japanese equities closed slightly higher as data showing record foreign investment bolstered sentiment. Foreign investors bought a a net $18 billion worth of Japanese stocks last week, just before a media report that billionaire Warren Buffett is looking to increase his exposure to the nation’s equities. Foreign Buying of Japan’s Stocks Hits Record Amid Buffett Effect The Topix rose 0.1% to close at 2,007.93, while the Nikkei advanced 0.3% to 28,156.97. Keyence contributed the most to the Topix gain, increasing 2.5%. Out of 2,158 stocks in the index, 1,085 rose and 936 fell, while 137 were unchanged. The data on foreign investors “may have boosted appreciation of Japanese stocks and triggered domestic investors to buy,” said Ryuta Otsuka, strategist at Toyo Securities. “The news of Buffett’s investment in Japanese equities also continues to gain attention and it might encourage a reevaluation of the Japanese market.

In Australia, the S&P/ASX 200 index fell 0.3% to 7,324.10 as Australian employers added 53,000 jobs in March from the prior month, more than double economists’ forecasts, helping drive the Australian dollar higher. Australia’s employment growth surpassed expectations for a second straight month in March, underscoring the economy’s resilience and bolstering the case for the Reserve Bank to raise interest rates again. Read: Australia’s Surge in Employment Opens Door to Further Rate Hike In New Zealand, the S&P/NZX 50 index rose 0.1% to 11,930.86.

Indian markets extended their winning run to the ninth day on Thursday, the longest streak since January 2021, as retail inflation eases, while corporate earnings come into focus. The S&P BSE Sensex rose 0.1% to 60,431.00 in Mumbai, while the NSE Nifty 50 Index also rose by a similar margin to 17,828.00. Technology stocks were the biggest drag on the benchmarks. Tata Consultancy Services fell after missing street estimates for its 4Q earnings while Infosys slumped ahead of its results. ICICI Bank contributed the most to the Sensex’s gain, increasing 1%. Out of 30 shares in the Sensex index, 17 rose and 13 fell.

In FX, the Bloomberg Dollar Spot Index fell 0.3%, on track for a third straight day of losses while the Australian dollar and Swiss franc compete for top spot among the G-10 currencies. The euro approached its strongest level of the year against the dollar, which was weighed down by the growing conviction of investors that a 25 basis-point rate hike in May will be the last in the Fed’s current tightening cycle, and will be followed by cuts later this year; the pound rose to its highest level versus the US currency since June. Traders price in the possibility of roughly 65 basis point of cuts by year- end, little changed from Wednesday. The yen recovered from earlier losses versus the dollar after new Bank of Japan Governor Kazuo Ueda repeated plans to continue with monetary easing, pushing back against speculation that he’ll change the yield curve control policy.

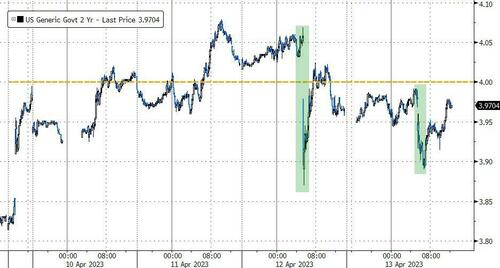

In rates, treasuries are under pressure in early US session with yields cheaper by 2bp to 4bp across the curve as stock futures pare a portion of Wednesday’s drop. Losses broadly led by belly of the curve. US 10-year yields trade around 3.42%, while US 2-year yields edge up 2.5 basis points to 3.97%, having fallen sharply Wednesday after data showed a slowdown in US CPI. Bunds and gild are also falling; the 10Y Bund was at 2.377%, marginally cheaper on the day. The latest Fed-dated OIS for the May meeting shows around 17bp of hike premium, unchanged on the day. US auction cycle concludes with $18b 30-year bond reopening at 1pm, following 2bp tail in Wednesday’s 10-year; WI 30-year yield around 3.65% is ~23bp richer than the March auction, which tailed by 0.7bp. IG issuance slate includes OMERS Finance Trust 5Y; Walmart was the only IG deal on Wednesday, pricing a 5-part $5b tranche, paying minimal new-issue concessions.

In commodities, crude futures are little changed with WTI trading near $83.30. Spot gold gains 0.6% to around $2,027. Bitcoin rises 1%.

Looking at the day ahead now, and data releases include UK GDP and Euro Area industrial production for February, and in the US there’s the March PPI reading and the weekly initial jobless claims. From central banks, we’ll hear from Bundesbank President Nagel and BoE Chief Economist Pill. Finally, earnings releases include Delta Air Lines.

Market Snapshot

- S&P 500 futures up 0.3% to 4130.25

- STOXX Europe 600 up 0.2% to 463.29

- MXAP up 0.2% to 162.63

- MXAPJ up 0.2% to 525.64

- Nikkei up 0.3% to 28,156.97

- Topix little changed at 2,007.93

- Hang Seng Index up 0.2% to 20,344.48

- Shanghai Composite down 0.3% to 3,318.36

- Sensex down 0.2% to 60,291.29

- Australia S&P/ASX 200 down 0.3% to 7,324.12

- Kospi up 0.4% to 2,561.66

- German 10Y yield little changed at 2.38%

- Euro up 0.2% to $1.1019

- Brent Futures little changed at $87.27/bbl

- Gold spot up 0.7% to $2,028.96

- U.S. Dollar Index down 0.21% to 101.28

Top Overnight News

- The export engine at the heart of the Chinese economy has roared back to life, defying expectations and bolstering hopes that Beijing will achieve its growth target this year. Customs data released on Thursday showed dollar-denominated exports expanded 14.8 percent compared with the same period a year earlier, after falling 6.8 per cent in January and February. Analysts polled by Reuters had forecast a contraction of 7 percent. FT

- SoftBank has moved to sell almost all of its remaining shareholding in Alibaba, limiting its exposure to China and raising cash. Softbank has sold about $7.2bn worth of Alibaba shares this year through prepaid forward contracts, after a record $29bn selldown last year. The forward sales will eventually cut SoftBank’s stake in the $262bn Chinese ecommerce group to just 3.8 percent. FT