April 20/2023 · by harveyorgan · in Uncategorized · Leave a comment·Editi

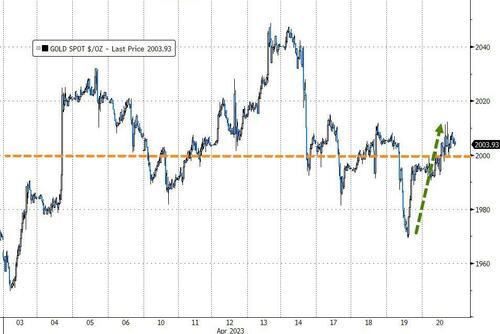

GOLD PRICE CLOSED: UP $12.70, TO $2007.80

SILVER PRICE CLOSED:UP 2 CENTS AT $25.30

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE $2004.95

Silver ACCESS CLOSE: 25.29

Bitcoin morning price:, $29,171 DOWN 1033 Dollars

Bitcoin: afternoon price: $28,311 DOWN 1893 dollars

Platinum price closing $1097.30 UP $4.10

Palladium price; $1594.15 DOWN $17.45

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2701.500 UP 16.29 CDN dollars per oz (ALL TIME HIGH 2732.50)

BRITISH GOLD: 1611.21 DOWN 2.10 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1827,68 UP 0.40 euros per oz //(ALL TIME HIGH//1860.82)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

COMEX DATA EXCHANGE:

COMEX//NOTICES

EXCHANGE: COMEX

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: APRIL 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,995.200000000 USD

INTENT DATE: 04/19/2023 DELIVERY DATE: 04/21/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 12

363 H WELLS FARGO SEC 25

435 H SCOTIA CAPITAL 13

661 C JP MORGAN 5

737 C ADVANTAGE 3 2

800 C MAREX SPEC 9 4

880 C CITIGROUP 1

TOTAL: 37 37

MONTH TO DATE: 23,445

JPMorgan stopped 5/37 contracts

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2023. CONTRACT: 37 NOTICES FOR 3700 OZ or 0.1150 TONNES

total notices so far: 23,445 contracts for 2,344,500 oz (72.923 tonnes)

SILVER NOTICES: 30 NOTICE(S) FILED FOR 150,000 OZ/

total number of notices filed so far this month : 374 for 1,870,000 oz

END

GLD

WITH GOLD UP $12.70

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD://////A DEPOSIT OF 0.70 TONNES OF GOLD INTO THE GLD

INVENTORY RESTS AT 926.57 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 2 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV.//: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 465.002 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 508 TO 158,879 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS STRONG SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG $0.11 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.11). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A MONSTER GAIN ON OUR TWO EXCHANGES 1009 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 25.83 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 501 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.055 MILLION OZ(FIRST DAY NOTICE)+ THE 25.83 MILLION OZ OF EXCHANGE FOR RISK/+ 1.975 MILLION OZ NORMAL SILVER STANDING FOR APRIL///THUS TOTAL NEW STANDING 27.805 MILLION OZ/ //// V) STRONG SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –71 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTRACTS for 13 days, total 17,976 contracts: OR 89.880 MILLION OZ . (1383 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 89.880 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE BUT BELOW LAST MONTH

APRIL 89.880 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 508 CONTRACTS WITH OUR $0.11 GAIN IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 501 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 1.055 MILLION OZ//FIRST DAY NOTICE// 150,000 OZ QUEUE JUMP (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //NEW EXCHANGE FOR RISK STANDING 25.83 MILLION OZ, THUS TOTAL SILVER OZ STANDING FOR DELIVERY IN APRIL TOTALS 27.805 MILLION .. WE HAVE A HUGE SIZED GAIN OF 1080 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 30 NOTICE(S) FILED TODAY FOR 150,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 7228 CONTRACTS TO 475,026 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED 646 CONTRACTS

this is the 7th day in a row where contracts on the comex were added!!

WE HAD A STRONG SIZED DECREASE IN COMEX OI ( 7228 CONTRACTS) WITH OUR $12.00 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR APR. AT 66.892 TONNES ON FIRST DAY NOTICE // PLUS A 500 OZ QUEUE. JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)YET ALL OF..THIS HAPPENED WITH OUR $12,00 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A GOOD SIZED LOSS OF 5313 OI CONTRACTS (16.525 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1915 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 475,076

IN ESSENCE WE HAVE A GOOD SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5313 CONTRACTS WITH 7228 CONTRACTS DECREASED AT THE COMEX AND 1915 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 5531 CONTRACTS OR 16.525 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1915 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (7228 //TOTAL LOSS IN THE TWO EXCHANGES 5959 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 66.892 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 500 OZ//NEW STANDING 74.02 TONNES // ///3) SOME LONG LIQUIDATION//4) STRONG SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 43,331 CONTRACTS OR 4,333,100 OZ OR 134.77 TONNES IN 13 TRADING DAY(S) AND THUS AVERAGING: 3333 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAY(S) IN TONNES 134.77 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 134.77/3550 x 100% TONNES 3.80% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 134.77 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A STRONG SIZED 508 CONTRACTS OI TO 158,879 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 501 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 501 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 501 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 508 CONTRACTS AND ADD TO THE 501 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE GAIN OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1009 CONTRACTS.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 5.045 MILLION OZ

OCCURRED WITH OUR $0.11 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 3.10 PTS OR 0.09% //Hang Seng CLOSED UP 29.21 POINTS OR 0.14% /The Nikkei closed UP 50.81 PTS OR 0.18% //Australia’s all ordinaries CLOSED DOWN 0.08 % /Chinese yuan (ONSHORE) closed UP TO 6.8803/OFFSHORE CHINESE YUAN UP TO 6.8861 /Oil DOWN TO 78.80 dollars per barrel for WTI and BRENT AT 81.86 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 7228 CONTRACTS DOWN TO 475,026 WITH OUR STRONG LOSS IN PRICE OF $12.00 ON WEDNESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1951 EFP CONTRACTS WERE ISSUED: : JUNE 1951 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1951 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 5959 CONTRACTS IN THAT 1915 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 7874 COMEX CONTRACTS..AND THIS GOOD SIZED LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $12.00. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (75.02) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 74.02 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $12.00) //// AND WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD OUR GOOD SIZED LOSS OF 5313 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE LOST A TOTAL OI OF 16.525 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (66.892 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 500 OZ… ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $12.00

WE HAD + ADDED 644 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 5313 CONTRACTS OR 531,300 OZ OR 16.525 TONNES.

Estimated gold comex today 155,752 poor

final gold volumes/yesterday 229,807 fair

//APRIL 20/ APRIL 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 803.770 oz 25 kilobars Brinks . |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | 160,855.000 Oz 5,000 kilobars jpmorgan |

| No of oz served (contracts) today | 37 notice(s) 3700 OZ 0.115 TONNES |

| No of oz to be served (notices) | 353 contracts 35300 oz 1.097 TONNES |

| Total monthly oz gold served (contracts) so far this month | 23,445 notices 2,344,500 OZ 72.923 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i)Into JPMorgan: 160,755.000 oz

5,000 kilobars

total deposits: 160,755.000 oz

customer withdrawals: 1

i) Out of Brinks: 803,77 oz (25 kilobars)

total withdrawals: 803.77 oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of APRIL we have an oi of 390 contracts having LOST 137 contracts. We had 142 contracts served ON WEDNESDAY so we GAINED 5 contracts or 500 oz will stand at the comex.

May GAINED 37 contracts up to 1794.

June LOST 9044 contracts DOWN to 393,485 contracts.

We had 37 contracts filed for today representing 3700 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 37 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 5 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2023. contract month,

we take the total number of notices filed so far for the month (23,445 x 100 oz ), to which we add the difference between the open interest for the front month of (APRIL. 390 CONTRACTS) minus the number of notices served upon today 37 x 100 oz per contract equals 2,379,800 OZ OR 74.02 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month: No of notices filed so far (23,445 x 100 oz)+ 390 OI for the front month minus the number of notices served upon today (37)x 100 oz} which equals 2,379,800 oz standing OR 74.02 TONNES in this active delivery month of APRIL..

TOTAL COMEX GOLD STANDING: 74.02 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,703,295.912 OZ 52,97 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,113,246.333 OZ

TOTAL REGISTERED GOLD: 12,292,837.996 (382.358 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 9,840,408.337 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,589,542 OZ (REG GOLD- PLEDGED GOLD) 329.379 tonnes//

END

SILVER/COMEX

APRIL 20//2023// THE APRIL 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 584,234.469 oz CNT Loomis . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 519,607.550 oz JPMorgan |

| No of oz served today (contracts) | 30 CONTRACT(S) (150,000 OZ) |

| No of oz to be served (notices) | 21 contracts (105,000 oz) |

| Total monthly oz silver served (contracts) | 374 Contracts (1,870,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i)Into JPMORGAN 519,607.550 oz

Total deposits: 519,607.550 oz

JPMorgan has a total silver weight: 141.674 million oz/273.640 million =51.90% of comex .//dropping fast

Comex withdrawals: 2

i) Out of CNT 566,743.369 oz

ii) Out of Loomis: 17,491.100 oz

Total withdrawals; 584,234.409 oz

adjustments: 1

JPMorgan: dealer to customer account:

3,418,935.160 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 30.629 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 273.680 million oz

CALCULATION OF SILVER OZ STANDING FOR MAR

silver open interest data:

FRONT MONTH OF APRIL /2023 OI: 51 CONTRACTS HAVING LOST 1 CONTRACT(S). WE HAD 31 NOTICES FILED ON TUESDAY SO WE GAINED 30 CONTRACTS OR AN ADDITIONAL 150,000 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF APRIL.

MAY SAW A LOSS OF 5307 CONTRACTS DOWN TO 60,957

JUNE HAD A 15 CONTRACTS GAIN TO 263

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 30 for 150,000 oz

Comex volumes// est. volume today 80,076 strong

Comex volume: confirmed yesterday: 95,621 very strong

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 374 x 5,000 oz = 1,870,000 oz

to which we add the difference between the open interest for the front month of APRIL(51) and the number of notices served upon today 30 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2023 contract month: 374 (notices served so far) x 5000 oz + OI for the front month of APRIL (51) – number of notices served upon today (30 )x 500 oz of silver standing for the APRIL. contract month equates to 1.975 million oz +/ NEW EXCHANGE FOR RISK TODAY: 0 MILLION OZ //NEW TOTALS EXCHANGE FOR RISK FOR MONTH OF APRIL: 25.83 MILLION OZ// THUS TOTAL SILVER OZ STANDING: 27.805 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

GLD INVENTORY: 926.57 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

CLOSING INVENTORY 465.002 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

A must read

Silver Demand Set Records In Every Category In 2022

THURSDAY, APR 20, 2023 – 03:20 PM

Silver demand set a record in every category last year based on final data released by the Silver Institute this week.

Total global silver demand in 2022 came in at a record $1.242 billion ounces. This represented an 18% increase in silver demand over 2021.

Net physical silver investment rose for a fifth consecutive year to a new high of 332.9 million ounces. Silver investment in India charted a staggering 188% increase over 2021 with lower prices and bargain hunting driving demand higher. There was modest demand growth in the US despite ongoing supply shortages that drove premiums exceptionally high – especially on American Silver Eagle coins.

Industrial demand posted a record of 556.5 million ounces in 2022. Green energy initiatives helped drive industrial offtake higher. Photovoltaics (PV) alone consumed 140.3 million ounces of silver.

Demand for silver in the solar energy sector is expected to continue to grow. According to a study by scientists at the University of New South Wales, solar manufacturers will likely require over 20% of the current annual silver supply by 2027. And by 2050, solar panel production will use approximately 85–98% of the current global silver reserves.

Electrification within the automotive segment, along with other power generation and distribution investments also supported industrial demand.

Silver jewelry fabrication increased by 29% year-on-year to a record 234.1 million ounces. India led the way, with demand doubling year on year.

Meanwhile, silverware demand in 2022 charted an even bigger spike of 80% to 73.5 million ounces, another record high.

While demand for silver soared, supply was flat last year.

Mine output dropped by 0.6% to 822.4 million ounces. Production from primary silver mines was almost flat year-on-year, rising by just 0.1% to 228.2 million ounces. Lower by-product output from lead and zinc mines, particularly in China and Peru, drove overall mine output down.

A modest increase in recycling offset the decrease in mine output.

Record global silver demand and a lack of supply upside contributed to last year’s 237.7 million ounce market deficit. It was the second consecutive annual deficit in a row. The Silver Institute called it “possibly the most significant deficit on record.” It also noted that “the combined shortfalls of the previous two years comfortably offset the cumulative surpluses of the last 11 years.”

Looking ahead to 2023, the Silver Institute projected “this year is expected to be another of solid silver demand. Industrial fabrication should reach an all-time high, boosted by continued gains in the PV market and healthy offtake from other industrial segments.”

The report noted that silver coin and silver bar demand, along with the demand for silver in jewelry fabrication would likely fall short of the 2022 record but they are all forecast to remain historically high.

Meanwhile, supply growth in 2023 will likely not exceed single digits.

As a result, this year will also see another large deficit for silver, amounting to a projected 142.1 Moz, which would be the second-largest deficit in more than 20 years. Adding up the supply shortfalls of 2021-2023, global silver inventories by the end of this year will have fallen by 430.9 Moz from their end-2020 peak. To put this into perspective, it is equivalent to more than half of this year’s forecasted annual mine production, and more than half of the inventories presently held in London vaults offering custodian services.”

You can download the Silver Institute’s full report HERE.

ernd

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//

END

3,Chris Powell of GATA provides to us very important physical commentaries

for sure!! Dollar hegemony is the cause of Africa (including South Africa’s) problems

(Global Times/Beijing)

Global Times: Dollar hegemony, not China, is the cause of Africa’s debt problems

Submitted by admin on Wed, 2023-04-19 20:07Section: Daily Dispatches

By Shi Qing

Global Times, Beijing

Wednesday, April 19, 2023

Not long ago U.S. Vice President Kamala Harris visited three African countries — Ghana, Tanzania, and Zambia. This is the fifth visit by a high-ranking Biden administration official to Africa this year.

During her visit, Harris repeatedly raised the issue of African debt, urging China to reduce debt owed by Ghana and Zambia, and announced the dispatching of a full-time resident adviser to Accra to assist the U.S. Ministry of Finance with debt restructuring issues from 2023 onwards.

While the U.S. is pointing its finger to African debt issue, its own domestic economy is on the verge of trouble. Washington’s monetary policy has shifted from extreme easing to radical interest rate hikes, triggering multiple U.S. banks to collapse as well as subsequent negative chain reaction around the world.

How can the U.S., whose financial policy is so irresponsible and self-serving, be so emboldened to lecture African countries how to deal with debt problems?

It is time for the U.S. to take a look in the mirror and examine its role in African debt issues.

The U.S.’ irresponsible monetary policy is the root of African debt problems. Relying on dollar hegemony, the U.S. has implemented three rounds of quantitative easing, cut interest rates to near zero, and flooded Africa and emerging markets with low-interest dollars.

It then arbitrarily and aggressively raised interest rates, boosted the U.S. dollar exchange rate, and attracted the return of dollars. As a result, African countries have to face liquidity shortages, broken funding chains, currency depreciation, skyrocketing debt repayment costs denominated in dollars, a surge in sovereign debt, and exacerbated debt problems. …

… For the remainder of the commentary:

https://www.globaltimes.cn/page/202304/1289429.shtm

end

Arkansas affirms gold and silver as legal tender as they eliminate taxes on them

(MMN)

Arkansas affirms gold and silver as legal tender and eliminates taxes on them

Submitted by admin on Wed, 2023-04-19 00:09Section: Daily Dispatches

From Money Metals News Service, Eagle, Idaho

Tuesday, April 18, 2023

LITTLE ROCK, Arkansas — Sound money advocates are rejoicing as House Bill 1718, the Arkansas Legal Tender Act, has become the law in the Natural State.

Backed by the Sound Money Defense League, Money Metals Exchange, and sound money advocates and supporters throughout the state, HB 1718 reaffirms gold and silver as legal tender, as well as ending all taxes on the purchase, sale, or exchange of specie, including state capital gains taxes.

The Arkansas Legal Tender Act, introduced by Rep. Robin Lundstrum (R-18) and Sen. Jonathan Dismang (R-18), passed overwhelmingly in the House by a vote of 82-8, unanimously out of the Senate with a 32-0 vote, and ultimately received Governor Sarah Huckabee Sanders’ signature on April 11. …

… For the remainder of the report:

END

I think Jan is correct: he guesses that Saudi Arabia is selling oil to China for gold

(Jan Nieuwenhuijs)

Jan Nieuwenhuijs: Is Saudi Arabia selling oil to China for gold?

Submitted by admin on Wed, 2023-04-19 00:00Section: Daily Dispatches

11:56p Tuesday, April 18, 2023

Dear Friend of GATA and Gold (and Silver):

Gold researcher Jan Nieuwenhuijs today addresses speculation, for which there is limited evidence, that Saudi Arabia is surreptitiously selling oil to China in exchange for gold from the Shanghai international exchange.

Nieuwenhuis’ analysis is headlined “Is Saudi Arabia Selling Oil to China for Gold?” and it’s posted at the Gainesville Coins internet site here:

https://www.gainesvillecoins.com/blog/is-saudi-arabia-selling-oil-to-china-for-gold

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

For your interest…

Craig Hemke at Sprott Money: Comex gold options sweet spot

Submitted by admin on Tue, 2023-04-18 23:48Section: Daily Dispatches

11:50p Tuesday, April 18, 2023

Dear Friend of GATA and Gold (and Silver):

Working from the assumption that the Comex gold and silver futures markets are largely rigged by the positioning of big options traders, the TF Metals Report’s Craig Hemke today tries predicting where that rigging will place gold and silver prices next Tuesday when options on the June contracts expire.

Hemke’s analysis is headlined “Comex Gold Options Sweet Spot” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/COMEX-gold-options-sweet-spot-April-18-2023

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/silver

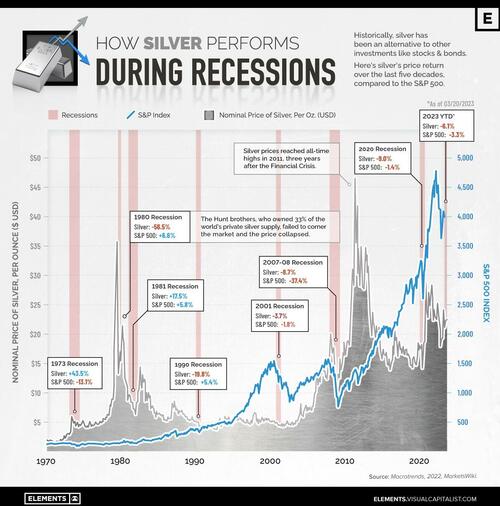

Silver Vs Stocks: Comparing Performance During Recessions

WEDNESDAY, APR 19, 2023 – 11:20 PM

Historically, silver has been an alternative to traditional investments like stocks and bonds.

Amid the recent wave of bank failures and rising interest rates, many investors sought the metal, making prices jump.

But has silver helped investors weather recessionary storms in the past?

The infographic below, via Visual Capitalist’s Bruno Venditti, uses data from Macrotrends to highlight silver’s price movements during recessions and compares it to changes in the S&P 500.

Silver Price During Recessions

Like gold, silver’s value comes from its scarcity as a precious metal. Silver, however, has a higher industrial use, from electronics and medical applications to batteries and solar panels.

Additionally, the silver market is much smaller than the gold market, making it a much more volatile asset.

The metal saw its biggest price drop in 1980 when it tumbled over 56% after the Hunt brothers, who controlled over half of the world’s privately owned silver, failed in an attempt to corner the market and were forced to sell after a rise in margin requirements.

Silver prices plummeted again during the 1990s recession before a steady recovery that culminated in an all-time high reached in 2011, three years after the 2007-2008 Financial Crisis.

Over the last five decades, silver has only outperformed the S&P 500 in three of eight recessions: 1973, 1981 and 2007.

As of March 2023, the silver nominal price was down 6.1% while the S&P500 was down 3.3%.

Silver Price in 2023

Over the next months, silver demand is expected to rise, supporting the price. Silver’s industrial market could be lifted from further gains in vehicle electrification and governments’ expanding commitment to green infrastructure, according to the Silver Institute.

However, if the economic scenario worsens and industrial users of silver reduce their output, the metal may face some headwinds.

END

5.IMPORTANT COMMENTARIES ON COMMODITIES:

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1.YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//,THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.8803

OFFSHORE YUAN: 6.8861

SHANGHAI CLOSED DOWN 3.10 POINTS OR 0.09%

HANG SENG CLOSED UP 29.21 PTS OR 0.14%

2. Nikkei closed UP 50.81 PTS OR 0.18%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 101.86 EURO FALLS TO 1.0934 DOWN 17 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.4670Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 134.77 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.480***/Italian 10 Yr bond yield RISES to 4.367*** /SPAIN 10 YR BOND YIELD RISES TO 3.522…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.303

3j Gold at $2007.00 silver at: 25.36 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 32 /100 roubles/dollar; ROUBLE AT 81.58//

3m oil into the 78 dollar handle for WTI and 81 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 134.77 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .4670% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8965 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9804 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.568 DOWN 3 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.767 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.2145 DOWN 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.41…

GREAT BRITAIN/10 YEAR YIELD: UP 1 BASIS PTS AT 3.8640

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

US Equity Futures Slide As Global Risk Sentiment Turns Sour

THURSDAY, APR 20, 2023 – 07:03 AM

US equity futures suffered their biggest overnight drop this week as a premarket slide in Tesla shares added to uncertainties surrounding the future of US monetary policy as well as the overall quality of the first-quarter earnings season. Contracts on the S&P 500 fell 0.7% as of 7:00 a.m. in New York while Nasdaq 100 futures took a 1% hit. Elsewhere, bond yields were lower, the USD was lower, and commodities were weaker on global demand fears.

In premarket trading, Tesla slid as much as 8.5% and were down -6% at last check, after the EV maker’s first-quarter results were hit by a slew of price cuts, denting profit margins and prompting at least six analysts – including Morgan Stanley’s Adam Jonas – to cut their price targets. MegaCap techs are also dragging indices lower with most names down 1%, or more. Bed Bath & Beyond shares tumbled 19% in premarket trading after Dow Jones reported that the retailer is preparing a bankruptcy filing for as early as this weekend. The stock had soared almost 100% in the three days prior. Here are some other premarket movers:

- Chip stocks decline in after Asian bellwether TSMC gave a disappointing revenue forecast for the current quarter amid a slump in demand for electronics.

- IBM rises as much as 2.2% after the IT services company reported first-quarter results that analysts say show positive growth trends.

- Las Vegas Sands rises as much as 4.8%, after the casino operator’s first-quarter earnings beat expectations and boosted hopes that a recovery in Macau and in Singapore is gaining momentum. Analysts hiked their price targets on the stock.

- Bath & Body Works drops 3.7% after Piper Sandler cuts its rating to neutral, with consensus estimates for the personal care products maker seen as “simply just too high.”

- Charles Schwab shares fall as much as 1.7% after Redburn downgraded the brokerage to sell from neutral, citing challenges from the Fed’s tightening cycle and the re-regulation of midsize banks.

- Cryptocurrency-exposed stocks fall and are poised to extend losses as Bitcoin dives further below the closely watched $30,000 level.

With better Bank earnings and a lackluster start from Tech earnings, the market seemingly remains stuck in near-term range of 3800 – 4200, with the SPX failing at 4150 level. Next week’s tech earnings will be the litmus test for bears and bulls.

Meanwhile, hawkish Fedspeak continues with some estimating 25bps – 50bps, or more, hikes remaining. Investors are seeking comfort whether policymakers will address growing recession worries, such as those flagged by the Federal Reserve’s monthly Beige Book survey which clearly noted that a credit crunch has arrived, or keep on fighting inflation as suggested by Fed Bank of New York President John Williams, who said price gains remained too high.

“We’re in a paradoxical situation,” said Alexandre Hezez, chief investment officer at Group Richelieu, a Paris-based asset manager. “If the Fed keeps on raising rates it’s not positive as it would mean we’re not done with inflation yet, but if it cuts, that would mean there are recessionary forces around.” The best path forward would be “a status quo” for the coming months, after a 25 basis-point hike in May, Hezez said, noting strong divergences on the matter among the Federal Open Market Committee.

European stocks are on course for their largest fall in almost four weeks amid tepid earnings and the prospect of additional monetary tightening. The Stoxx 600 is down 0.3% with autos, miners and tech the worst performing sectors while Renault and Nokia have fallen sharply after their respective quarterly updates. Here are the most notable European movers:

- Renault shares fall as much as 7.9% as pricing concerns offset positives from the first-quarter sales beat, with analysts questioning the sustainability of the French carmaker’s pricing

- Tryg shares rise as much as 4.7% with analysts saying the Danish insurer’s better-than-expected profit, dividend and combined operating ratio all make for a reassuring update

- Haleon shares rise as much as 3% in early trading to hit a record high. The consumer health group’s first-quarter update is strong and shows good momentum for the group, analysts say

- Bankinter jumps as much as 5%, kicking off 1Q earnings season for European banks with a strong set of numbers and analysts pointing to a net interest income beat

- Getlink shares gain as much as 2.8% after the French cross-channel transport operator reported a 1Q revenue beat and management maintained its Ebitda outlook

- Rexel shares rise as much as 3.8% after it reported a “strong beat” that should lead to consensus full-year estimates rising to the upper end of company’s guidance, Citi says

- ASML leads gains in shares of European semiconductor-equipment makers after TSMC — the industry bellwether and a major ASML customer — kept its full-year capex target unchanged

- Nordic Semiconductor shares fall as much as 17% to the lowest intraday level in more than two years after the chipmaker gave bleak 2Q guidance and scrapped a revenue outlook

- Sartorius AG falls as much as 7.8% after the German laboratory equipment group’s 1Q results, which Morgan Stanley analysts say was “significantly weaker than anticipated on all metrics”

- Stora Enso drops as much as 6.4% to lowest since August 2020 after the Finnish forestry group said operational Ebit for 2023 is now set to be “significantly lower” than in 2022

- Nokia shares fall as much as 2.9% to the lowest intraday level in more than a year, after the telecom equipment maker reported first-quarter margins well below estimates

Earlier in the session, Asian stocks edged lower as volatility across global markets remained subdued, with investors awaiting new catalysts and digesting recent corporate earnings. The MSCI Asia Pacific Index dropped as much as 0.4% before paring its loss. Most major benchmarks were up or down by less than 0.5%, with South Korea and mainland China leading the declines.

In key results Thursday, TSMC forecast worse-than-anticipated revenue for the current quarter, reflecting a persistent slump in global chip demand. Chinese EV battery maker CATL is expected to report strong revenue growth later in the day. China tech earnings so far have been in line, “could have been better but we stay more optimistic,” given positive initiatives from companies such as Alibaba, Xiaolin Chen, head of international at Kraneshares, told Bloomberg TV. “Overall you see very encouraging and constructive policies get introduced by policymakers or corporates themselves to become more market oriented.” The Kospi slipped after coming close to a bull market. The gauge is Asia’s best performer among major markets this year, climbing 19% from a September low amid frenzied gains in EV-battery related stocks and heavyweight Samsung Electronics.

Japanese stocks were mixed in thin trading as investors eye upcoming earnings from major domestic and overseas companies. The Topix closed little changed at 2,039.73, while the Nikkei advanced 0.2% to 28,657.57. Volume on both gauges was more than 20% below the 30-day averages. Out of 2,158 stocks in the Topix, 1,203 rose and 811 fell, while 144 were unchanged. “There is a lack of news, and investors are still waiting for corporate earnings results to come out and then further on, monetary policy,” said Naoki Fujiwara, chief fund manager at Shinkin Asset Management

In Australia, the S&P/ASX 200 index was little changed to close at 7,362.20, as gains in banks were offset by broad declines in mining shares. Asian shares were broadly lower as investors parsed mixed corporate earnings and the latest assessment on the US economy. Australia’s central bank should set up an expert policy board, hold fewer meetings and give press conferences explaining its decisions, according to recommendations from an independent review that would align it with many global peers. Read: RBA Review Calls for Expert Policy Panel, Fewer Meetings (3) In New Zealand, the S&P/NZX 50 index fell 0.3% to 11,879.68.

In FX, the Bloomberg Dollar Spot Index is flat. New Zealand dollar dropped to a month-low after data showed the nation’s inflation slowed down more than expected, spurring expectations for the central bank to ease policy tightening.

In rates, US two-year yields are lower after a five day rally, falling 3bps to 4.22% while 10-year yieldS fell as much as 5bps to 3.54%, the lowest since Monday; traders bet on 23bps of Fed tightening in May and 30bps by June, while pricing 50bps of cuts by year-end. German and UK two-year borrowing costs both fall by 1bps.

In commodities, crude futures extended their recent decline with WTI falling 1.8% to trade near $77.70. Will OPEC have to get involved again and cut production some more? Spot gold is little changed around $1,994.

Bitcoin continues to slip and has drifted more than 1% %to a fresh USD 28.56k WTD trough vs Monday’s USD 30.5k best, action which has come alongside the broader dip in sentiment with specific fundamentals somewhat limited.

To the day ahead now, and data releases from the US include the weekly initial jobless claims, existing home sales for March and the Conference Board’s leading index for March. From central banks, we’ll get the ECB’s account of their March meeting, and hear from ECB President Lagarde, the ECB’s Visco, Holzmann and Schnabel, the Fed’s Waller, Mester, Bowman and Bostic, the BoE’s Tenreyro and BoC Governor Macklem. Finally, earnings releases include AT&T, Union Pacific and American Express.

Market Snapshot

- S&P 500 futures down 0.7% to 4,147.50

- STOXX Europe 600 down 0.4% to 466.47

- MXAP little changed at 162.39

- MXAPJ down 0.1% to 523.29

- Nikkei up 0.2% to 28,657.57

- Topix little changed at 2,039.73

- Hang Seng Index up 0.1% to 20,396.97

- Shanghai Composite little changed at 3,367.03

- Sensex little changed at 59,513.37

- Australia S&P/ASX 200 little changed at 7,362.19

- Kospi down 0.5% to 2,563.11

- Brent Futures down 1.5% to $81.91/bbl

- Gold spot up 0.2% to $1,997.99

- U.S. Dollar Index down 0.12% to 101.84

- German 10Y yield little changed at 2.48%

- Euro up 0.1% to $1.0970

Top Overnight News

- Today Treasury Secretary Janet L. Yellen on Thursday will call for a “constructive” and “healthy” economic relationship between the United States and China, one in which the two nations work together to confront challenges like climate change, according to excerpts from prepared remarks. NYT

- The BOJ is “warming” to the idea of tweaking its policy in a hawkish direction this year, but probably won’t take any actions at next week’s meeting. RTRS

- TSMC, the leading chipmaker for the likes of Apple and Nvidia, has warned that a weaker than expected recovery in China has hit demand for its semiconductors. The Taiwanese chipmaker cut its forecast for the semiconductor market this year, excluding memory, to a mid-single-digit percentage decline. FT

- Germany’s PPI for March dramatically undershoots the Street consensus, coming in at +7.5% Y/Y (down from +15.8% in Feb and below the Street’s +9.8% forecast). RTRS

- Brussels is preparing emergency curbs on Ukrainian grain imports to five member states close to the war-torn country, bowing to pressure from Poland and Hungary after they took unilateral action to pacify local farmers. FT

- ECB minutes will be scoured today for any additional hints on the duration of the tightening cycle. It gave no guidance on its next moves after the March meeting, though Christine Lagarde, who speaks today, indicated more tightening is coming. Governing Council hawk Klaas Knot told the Irish Times that officials may need to raise interest rates in June and July following a hike next month. BBG

- NY Fed chief John Williams said that while the banking sector has stabilized following the second-largest bank collapse in US history, the recent stress may tighten credit conditions. Chicago’s Austan Goolsbee said he’s still waiting to see if the fallout causes the economy to slow more than expected. Loretta Mester and Raphael Bostic are among Fed speakers today. BBG

- Uncertainty continues to linger about whether or not the US will make it through to late summer without risking a debt-ceiling-related default after figures indicating the size of the Treasury’s tax day cash influx were somewhat lackluster. The amount of money that the US government has on hand to pay its bills jumped just $108.47 billion on Tuesday. BBG

- Tesla plunged as much as 8.5% premarket after Elon Musk signaled price cuts will continue at the expense of profit margins. Profit missed and the operating margin slumped to 11.4% from 19.2% a year ago. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded rangebound with the region indecisive following the flat handover from the US where earnings were under the spotlight and early headwinds were seen after firmer-than-expected UK CPI data. ASX 200 was indecisive as participants digested output updates and with the mining sector subdued despite the fresh record Q1 iron ore shipments by Rio Tinto, while Australian Treasurer Chalmers announced recommendations from the independent RBA review which included establishing separate boards for governance and monetary policy with fewer meetings and press conferences to be conducted after policy decisions. Nikkei 225 gradually pared opening losses following mixed trade data including better-than-expected exports growth and after a recent report that the BoJ is said to be wary of tweaking yield control this month. Hang Seng and Shanghai Comp were mixed following the lack of surprises by the PBoC which maintained its benchmark lending rates for the 8th consecutive month and as frictions lingered after the US Commerce Department imposed a USD 300mln civil penalty on Seagate for supplying hard disk drives to Huawei in violation of export controls.

Top Asian News

- PBoC 1-Year Loan Prime Rate (Apr) 3.65% vs Exp. 3.65% (Prev. 3.65%); 5-Year Loan Prime Rate (Apr) 4.30% vs Exp. 4.30% (Prev. 4.30%)

- PBoC official expects consumer inflation to pick up later this year; the impact on the Yuan from volatility in major currencies is limited, expects it to be basically stable with two-way swings.

- US Trade Representative Tai said they have seen supply chain fragility and that US trade restrictions on China are narrowly targeted, while she added the US doesn’t intend to decouple and intends a level trade playing field with China.

- US Commerce Department imposed a USD 300mln civil penalty on Seagate (STX) and said the Co. sold 7.4mln hard disk drives to Huawei between August 2020-September 2021 in violation of export controls, according to Reuters.

- RBA independent review recommended that the RBA should have dual objectives of price stability and full employment, while it should retain a flexible inflation target of 2%-3% and aim at the mid-point. It was also recommended that the government form a monetary policy board of experts which would comprise of the RBA Governor, Deputy Governor, Treasury Secretary and 6 external members with the Governor as Chair in which the policy board would conduct 8 meetings a year with a press conference after each meeting, while the government should establish a governance board with an external chair and legislate changes to commence from July 2024. Furthermore, the RBA should retain independence and the power of government to override decisions should be repealed.

- BoJ is reportedly open to tweaking Yield Curve Control (YCC) this year if wage momentum holds, according to Reuters sources; may engage is more lively debate in the June and July meetings; no current consensus on how soon to phase YCC out, July wage tally key.

European bourses are lower across the board, Euro Stoxx 50 -0.3%, as pressure emerged without a clear catalyst after a relatively contained open. Sectors are largely in the red, with Autos underperforming amid downside in Renault post-earnings and with attention on Tesla; elsewhere, Nokia slumps and L’Oreal trims upside after their latest updates. Stateside, futures are pressured to a larger extent than their European peers with downside occurring in tandem with the above move and exacerbated by marked pressure in Tesla, NQ -1.1%. TSMC (2330 TT/TSM) Q1 (TWD): Net Profit 206.9bln (exp. 192.8bln), Sales 508.6bln (exp. 517.9bln), Gross Profit 286.5bln (prev. 273.2bln). EPS 7.98 (exp. 7.41), Gross Margin 56.3% (exp. 54.5%). Q2 Guidance (USD): Revenue 15.2-16.0bn (exp. 17.3bln), Gross Margin 52-54% (exp. 52.5%), Operating Margin 39.5-41.5% (exp. 40%). TSM +0.4% in pre-market trade. Tesla (TSLA) – Q1 2023 (USD): Adj. EPS 0.85 (exp. 0.85), Revenue 23.33bln (exp. 23.29bln). Still sees FY production 1.80mln vehicles (exp. 1.84mln). Tesla did not release its automotive margins, but continues to believe that its operating margin will remain among the highest in the industry. CEO Musk has taken a view that pushing for higher volumes and a larger fleet is the right choice here vs lower volume and higher margins. -7.5% in pre-market trade.

Top European News

- Turkey Gas Field Launch Sets Up Pre-Election Giveaway

- European Gas Prices Swing With Signs of Weak Industrial Demand

- Melrose Spinoff Dowlais Slips in Rare London Trading Debut

- Nokia Misses Estimates as Clients Reduce Spending on 5G Gear

FX

- Kiwi deflated as NZ CPI metrics miss consensus, NZD/USD sub-0.6200 and AUD/NZD eyeing 1.0900.

- DXY drifting within 102.040-101.780 range after failing to close above the 21 DMA again.

- Aussie and Euro underpinned by option expiries between 0.6700-0.6695 and at 1.0925 vs the Buck.

- Franc firm and retesting 0.9850 vs Greenback as Treasury yields ease; Yen, Pound and Loonie rangy.

- PBoC set USD/CNY mid-point at 6.8987 vs exp. 6.8979 (prev. 6.8732)

Fixed Income

- Core benchmarks have pared back initial recovery momentum and are now in close proximity to the neutral mark on the session, though currently retain an incremental positive bias.

- Given the above, bonds are yet to mark new troughs though the waning momentum is notable but worth caveating with the particularly hefty upcoming US agenda.

- Specifically, the action has seen Bunds, Gilts and USTs move closer to their 133.42, 99.94 and 114-07 intraday lows vs initial recovery highs; stateside yields are lower, with curve action again most pronounced at the short-end.

Commodities

- Crude benchmarks remain under pressure, with specific fundamentals limited and the complex printing new multi-week lows. Though, the magnitude of today’s action has thus far been much less pronounced than the losses seen earlier in the week.

- Specifically, WTI and Brent June futures are under USD 78/bbl (vs high 79.07/bbl) and USD 82/bbl (vs high 82.92/bbl) respective highs.

- Spot gold has attempted to reclaim the USD 2k/oz mark but is yet to convincingly surmount the figure despite the softer USD and equity landscape, base metals are lower in fitting with the mentioned tone though the downside is perhaps capped as the Dollar dips.

- Pakistan’s first order for Russian discount oil has been placed, via Pakistan’s petroleum minister; intends to import 100k BPD of Russian oil.

Geopolitics

- China Hainan Maritime Bureau said it will ban passage during military drills in nearby waters in South China Sea amid military drills from Friday to Sunday, according to Kyodo.

- Iran says its navy has forced a US submarine to surface as it enters the Gulf, via State TV.

US Event Calendar

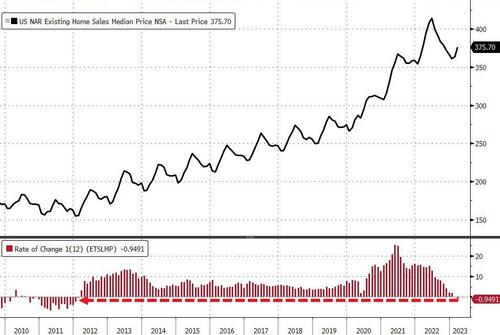

- 08:30: April Initial Jobless Claims, est. 240,000, prior 239,000

- 08:30: April Continuing Claims, est. 1.83m, prior 1.81m

- 08:30: April Philadelphia Fed Business Outl, est. -19.3, prior -23.2

- 10:00: March Existing Home Sales MoM, est. -1.8%, prior 14.5%

- 10:00: March Home Resales with Condos, est. 4.5m, prior 4.58m

- 10:00: March Leading Index, est. -0.7%, prior -0.3%

DB’s Jim Reid concludes the overnight wrap

Markets have struggled a bit over the last 24 hours, with bonds and equities selling off thanks to strong inflation data and a mixed batch of earnings releases. However by the close of business both Euro and US equities had broadly clawed their way back to flat (S&P -0.01%) but with yields on 10yr Treasuries (+1.5bps) ending just a shade under their one-month highs at of 3.59% and Bund yields at their highest close since March 9th.

The initial catalyst for the bond and equity weakness yesterday came from the UK inflation release shortly after we went to press yesterday. It showed CPI inflation had only fallen to +10.1% in March (vs. +9.8% expected), and core inflation was above expectations as well at +6.2% (vs. +6.0% expected), which disappointed hopes that we’d be in the midst of a broader trend lower by this point. At the same time, the print was also on the upside of the BoE’s own staff forecasts in February, which had looked for a +9.2% number yesterday. So with the previous day’s wage data surprising on the upside too, the picture is one of stronger inflationary pressures than previously thought.

With another inflation report surprising on the upside, that spurred a broader selloff among sovereign bonds, and investors continued to dial back the chances of rate cuts from central banks this year. UK gilts were at the forefront of that, with the 10yr yield up by +10.9bps, and investors moved to fully price in a 25bp rate hike from the BoE in May for the first time since late February. Our own UK economist at DB has also adjusted his expectations for the BoE (link here), and now sees them taking Bank Rate up by 25bps in both May and June. If realised, that would leave the terminal rate at 4.75%, and he argues the risks are now skewed to the upside of that as well.

Those moves in the UK were echoed in other countries, and investors priced in a growing chance that the ECB would deliver another 50bp hike in two weeks’ time. That led to a rise in yields across the continent, with those on 10yr bunds (+3.8bps), OATs (+3.7bps) and BTPs (+6.2bps) all moving higher on the day. Likewise in the US, the 10yr yield rose +1.5bps to 3.591%, which came as investors further downplayed the chance of rate cuts this year. What’s interesting is that investors are now increasingly considering whether the Fed will pursue further rate hikes after the next decision in May, and the odds of a 25bp hike in June hit a post-SVB high of 29.4% yesterday. That’s partly because of the inflation data of late, but they’ve also been propelled by the persistent easing of financial conditions over recent days, with Bloomberg’s index now at its most accommodative level since the SVB collapse. Whilst that might be welcome news after the recent turmoil, one consequence of easier financial conditions is it puts more of the onus on the Fed to tighten policy to get inflation back to target, rather than relying on tighter financial conditions.

On that topic, yesterday was the first Fed Beige Book since the SVB episode. The Beige Book is released two weeks prior to FOMC meetings and publishes anecdotal data/comments from the various districts. On credit conditions, five districts mentioned tighter conditions with a respondent from New York mentioning that “Credit standards tightened noticeably for all loan types, and loan spreads continued to narrow. Deposit rates moved higher.” A respondent from California, the epicentre for stress last month, said that “following recent volatility in deposit levels at regional and community banks, outflows have reportedly stabilized since late March.” Not all regions saw large disruptions with a respondent in Chicago saying there was “some movement in deposits but little change in credit availability following the collapse of Silicon Valley Bank”. Attention will turn to the senior loan officer survey early next month. It’s always been a huge favourite lead indicator of ours but the whole financial world will be watching this time around.

For equities, as discussed at the top, the main news came after the close as we heard from Tesla, which dropped more than -6% in after-market trading before recovering its losses. The EV-maker missed profit estimates with EPS coming in at $0.85 ($0.86 estimated) as margins were tighter than expected. The company also expects there to be “ongoing cost reduction” of their vehicles.IBM (+1.73% in after-market trading) rose after beating earning expectations and increased sales guidance for 2023.

Also after the close we learned that the US Treasury took in $129bn across corporate and individual income taxes, which means that the Treasury General Account is now up to $252bn, up from $144bn on Monday. Today is another big day to watch as it will capture a portion of Tuesday’s deadline day tax flows, yet to be reported. The overall total was softer than some initial assumptions and leaves an x-date of midsummer as the most likely. Also on the debt ceiling, House Speaker McCarthy released a plan yesterday to raise the debt ceiling by $1.5tr, which would push the “x-date” out into March 2024. The GOP hope to vote on the bill in the coming days as an opening salvo in talks with the White House. Moderate members of both parties also pushed forward an idea that would suspend the debt ceiling until December 31 and then possibly February 2025 if certain conditions were met. The plan is likely dead-on-arrival given the slim GOP majority and the weakened position of Speaker McCarthy, who would have to put the bill up to a vote.

Prior to this, and as mentioned at the top, the S&P 500 had another quiet day, ending just -0.01% lower and remaining in the very narrow band seen over recent sessions. There was a decent amount of dispersion once again though with rate-proxies such as utilities (+0.78%) and real estate (+0.55%) rising, while cyclicals fell back led by communications (-0.72%), materials (-0.31%), and energy (-0.25%). The VIX index of volatility declined a further -0.4pts to 16.4pts, which marked its lowest closing level since November 2021. Elsewhere the NASDAQ (0.03%) was similarly unchanged with the Dow Jones (-0.23%) seeing a marginal loss. In Europe there were modest declines as well, leaving the STOXX 600 down -0.10%.

Asian equity markets are broadly trading lower this morning following a tepid performance of US equities on Wall Street. As I type, the Chinese stocks are leading losses across the region with the Shanghai Composite (-0.69%) and the CSI (-0.63%) edging lower while the Hang Seng (+0.19%) is just above flat. Elsewhere, the KOSPI (-0.28%) is trading in negative territory while the Nikkei (+0.09%) held on to its minor gains. Outside of Asia, US stock futures tied to the S&P 500 (-0.18%) and NASDAQ 100 (-0.33%) are modestly lower as risk appetite remains downbeat following the latest batch of earnings.

In early morning data, exports in Japan rose +4.3% y/y in March (v/s +2.4% expected), down from growth of +6.5% in February mainly due to a drop in China-bound shipments. Imports outpaced exports, increasing 7.3% in the year to March (v/s a +11.6% expected increase), the smallest advance in two years and coming after the prior month’s 8.3% gain. Meanwhile, the nation’s trade deficit narrowed for the second consecutive month, contracting to 754.5 billion yen ($5.6 billion) from an upwardly revised deficit of 898.1 billion yen in February,

When it comes to the Bank of Japan’s decision next week, Bloomberg reported yesterday that officials were wary of adjusting their yield curve control policy this soon after last month’s market turmoil. The meeting isn’t until a week on Friday, but will be the first for new Governor Ueda, so will likely get more attention than usual anyway.

To the day ahead now, and data releases from the US include the weekly initial jobless claims, existing home sales for March and the Conference Board’s leading index for March. From central banks, we’ll get the ECB’s account of their March meeting, and hear from ECB President Lagarde, the ECB’s Visco, Holzmann and Schnabel, the Fed’s Waller, Mester, Bowman and Bostic, the BoE’s Tenreyro and BoC Governor Macklem. Finally, earnings releases include AT&T, Union Pacific and American Express.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

Earnings remain in focus, TSLA -6%, ahead of a packed Central Bank docket – Newsquawk Europe Market Open

THURSDAY, APR 20, 2023 – 01:46 AM

- APAC stocks traded rangebound with the region indecisive following the flat handover from the US. Tesla lower by 6.1% after hours post-earnings.

- European equity futures are indicative of a contained open with Euro Stoxx 50 future flat after the cash market closed flat yesterday.

- DXY lingers just below the 102 mark, FX markets overall contained, NZD the laggard across the majors post-CPI.

- Crude futures continued to retreat after slipping beneath post-OPEC voluntary cut lows.

- Looking ahead, highlights include German Producer Prices, US IJC, Existing Home Sales, EZ Consumer Confidence (Flash), ECB Minutes, Speeches from Fed’s Williams, Waller, Mester, Bowman & Bostic, ECB’s Lagarde & Schnabel, Supply from Japan, Spain & France.