April 28/2023 · by harveyorgan · in Uncategorized · Leave a comment·Editi

GOLD PRICE CLOSED: UP $1.45 TO $1990.35

SILVER PRICE CLOSED: UP 1 CENT AT $24.95

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE $1989.25

Silver ACCESS CLOSE: 25.05

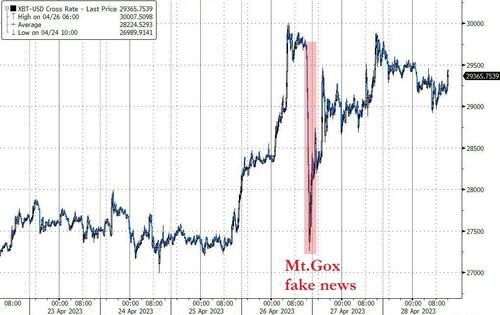

Bitcoin morning price:, $29,293 down 355 Dollars

Bitcoin: afternoon price: $29,386 DOWN 262 dollars

Platinum price closing $1078.80 DOWN $3.80

Palladium price; $1505.70 UP $1.95

“Our government… teaches the whole people by its example. If the government becomes the lawbreaker, it breeds contempt for law; it invites every man to become a law unto himself; it invites anarchy.” … Louis D Brandeis (former Supreme Court Justice)

GO GATA!

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2695.15 DOWN 6.95 CDN dollars per oz (ALL TIME HIGH 2732.50)

BRITISH GOLD: 1583,17 DOWN 6.71 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1805.60 UP 3.50 euros per oz //(ALL TIME HIGH//1860.82)

DONATE

FOR APRIL

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2023. CONTRACT: 106 NOTICES FOR 10600 OZ or 0.3297 TONNES

total notices at conclusion of April: 24,330 contracts for 2,433,000 oz (75.676 tonnes)

and that completes April as final standing 75.676 tonnes of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

FOR MAY:

GOLD: NUMBER OF NOTICES FILED FOR MAY/2023. CONTRACT: 1057 NOTICES FOR 105,700 OZ or 3.2877 TONNES

total notices so far: 1057 contracts for 105,700 oz (3.2877 tonnes)

FOR MAY:

SILVER NOTICES: 1015 NOTICE(S) FILED FOR 5,075,000 OZ/

total number of notices filed so far this month : 1015 for 5,075,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

FOR THE MAY GOLD CONTRACT:

EXCHANGE: COMEX

CONTRACT: MAY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,989.900000000 USD

INTENT DATE: 04/27/2023 DELIVERY DATE: 05/01/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 400

323 C HSBC 111

DLV615-T CME CLEARING

BUSINESS DATE: 04/27/2023 DAILY DELIVERY NOTICES RUN DATE: 04/27/2023

PRODUCT GROUP: METALS RUN TIME: 20:27:39

363 H WELLS FARGO SEC 254

435 H SCOTIA CAPITAL 419

523 C INTERACTIVE BRO 13

657 C MORGAN STANLEY 14

657 H MORGAN STANLEY 226

661 C JP MORGAN 297 240

686 C STONEX FINANCIA 4

690 C ABN AMRO 11

726 C CUNNINGHAM COM 17

732 C RBC CAP MARKETS 27

737 C ADVANTAGE 3 35

800 C MAREX SPEC 33

905 C ADM 6 4

TOTAL: 1,057 1,057

MONTH TO DATE: 1,057

JPMorgan stopped 240/1057 contracts

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $1.45

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD://////A MASSIVE WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD.

INVENTORY RESTS AT 926.28 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 1 CENT AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV.//: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 469.182 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS SIZED 3169 CONTRACTS TO 140,794 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.16 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.16). AND WERE SUCCESSFUL IN KNOCKING A FEW SPEC LONGS AS WE HAD A HUGE LOSS ON OUR TWO EXCHANGES OF 2,157 CONTRACTS WITH MOST OF THAT LOSS DUE TO FINALIZATION OF SPREADER LIQUIDATION IN THE SILVER ARENA.. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 0 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS( 1012 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.105 MILLION OZ(FIRST DAY NOTICE)+ 0 MILLION OZ OF EXCHANGE FOR RISK// //// V) GIGANTIC SIZED COMEX OI LOSS/ HUGE SIZED EFP ISSUANCE/.VI) FINALIZATION OF SPREADER LIQUIDATION

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –81 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTRACTS for 19 days, total 23,600 contracts: OR 118.035 MILLION OZ . (1242 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 118.035 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3169 CONTRACTS DESPITE OUR $0.16 GAIN IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC SIZED EFP ISSUANCE CONTRACTS: 1012 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 13.105 MILLION OZ//FIRST DAY NOTICE// 0 OZ E.F.P. JUMP TO LONDON (WHICH DECREASES THE AMOUNT OF SILVER STANDING) AND ZERO QUEUE JUMP + 0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //TOTAL STANDING 13.105 MILLION OZ// .. WE HAVE A GIGANTIC SIZED LOSS OF 2076 OI CONTRACTS ON THE TWO EXCHANGES ALTHOUGH MOST OF THE LOSS WAS DUE TO FINALIZATION OF SPREADER LIQUIDATION

WE HAD 1057 NOTICE(S) FILED TODAY FOR 5,075,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 3,519 CONTRACTS TO 475,737 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: added 337 CONTRACTS

this is the third straight day of additions to comex volume//total insanity. We have had 8 additions out of the last 10 trading days.

WE HAD A GOOD SIZED DECREASE IN COMEX OI ( 3519 CONTRACTS) DESPITE OUR $4.00 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR MAY. AT 3.5085 TONNES ON FIRST DAY NOTICE // PLUS A 0 OZ QUEUE. JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)////YET ALL OF..THIS HAPPENED WITH OUR $4.00 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING.WE HAD A SMALL SIZED LOSS OF 22 OI CONTRACTS (0.6843 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3497 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 475,400

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 22 CONTRACTS WITH 3519 CONTRACTS DECREASED AT THE COMEX AND 3487 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 22 CONTRACTS OR 0.6843 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3497 CONTRACTS) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (3519 //TOTAL LOSS IN THE TWO EXCHANGES 22 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 3.5085 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 0 OZ / // ///3) FEW LONG LIQUIDATION//4) GOOD SIZED COMEX OPEN INTEREST LOSS/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 63,473 CONTRACTS OR 6,347,300 OZ OR 197,42 TONNES IN 19 TRADING DAY(S) AND THUS AVERAGING: 3340 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAY(S) IN TONNES 197.42 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 197.42/3550 x 100% TONNES 5.57% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES ( MUCH SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A GIGANTIC SIZED 3169 CONTRACTS OI TO 140,797 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 1012 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1012 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1012 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3169 CONTRACTS AND ADD TO THE 1012 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2157 CONTRACTS WITH MOST OF THE LOSS DUE TO CONTINUATION OF SPREADER LIQUIDATION

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 10.785 MILLION OZ

OCCURRED WITH OUR $0.16 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED UP 27,21 PTS OR 1.14% //Hang Seng CLOSED UP 54,29 POINTS OR 0.27% /The Nikkei closed UP 398.76 PTS OR 1.40% //Australia’s all ordinaries CLOSED UP 0.25 % /Chinese yuan (ONSHORE) closed UP TO 6.9190/OFFSHORE CHINESE YUAN UP TO 6.9316 /Oil DOWN TO 75.04 dollars per barrel for WTI and BRENT AT 78.65 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 3519 CONTRACTS DOWN TO 475,737 DESPITE OUR GAIN IN PRICE OF $4.00 ON THURSDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3497 EFP CONTRACTS WERE ISSUED: : JUNE 3497 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3497 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 22 CONTRACTS IN THAT 3497 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED LOSS OF 3519 COMEX CONTRACTS..AND THIS SMALL SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GAIN IN PRICE OF $4.00. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (3.5075) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 3.5085 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $4.00) //// BUT WERE SUCCESSFUL IN KNOCKING A FEW SPECULATOR LONGS AS WE HAD OUR SMALL SIZED LOSS OF 22 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE LOST A TOTAL OI OF 1.116 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY. (3.5085 TONNES) ALL OF THIS WAS ACCOMPLISHED WITH OUR RISE IN PRICE TO THE TUNE OF $4.00

WE HAD +ADDED 337 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 22 CONTRACTS OR 2200 OZ OR 0.6843 TONNES.

Estimated gold comex today 175,769 poor//

final gold volumes/yesterday 216,756 fair

//APRIL 28/ MAY 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 578,718 oz HSBC JPMorgan 18 kilobars for both . |

| Deposit to the Dealer Inventory in oz | 21,798.378 OZ Brinks 678 kilobars |

| Deposits to the Customer Inventory, in oz | 160,755.000 Oz JPM 5,000 kilobars |

| No of oz served (contracts) today | 1057 notice(s) 105,700 OZ 3.2877 TONNES |

| No of oz to be served (notices) | 71 contracts 7100 oz 0.2208 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1057 notices 105,700 OZ 3.2877 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 1

i) Into Brinks: 21,798.378 oz

total dealer deposit: 21,798.378 oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 2

i) Our of JPMorgan: 96,453 oz (2 kilobars)

ii) Out of HSBC: 482.265 oz (15 kilobars)

total withdrawals: 578.718 oz

Adjustments;

i) dealer to customer Brinks: 4244.226oz

ii) customer to dealer: 39,352.82 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 1128 contracts having LOST 66 contracts.

Thus by definition, the initial amount of gold standing in this non active month of May is as follows:

1128 contracts x 100 oz per contract = 112800 oz or 3.5085 tonnes

June LOST 5067 contracts DOWN to 378,406 contracts.

AUGUST GAINED 1764 contracts up to 52,952 contracts

We had 1015 contracts filed for today representing 101,500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 297 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1057 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 240 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2023. contract month,

we take the total number of notices filed so far for the month (1,057 x 100 oz ), to which we add the difference between the open interest for the front month of MAY 1128 CONTRACTS) minus the number of notices served upon today 1057 x 100 oz per contract equals 112,800 OZ OR 3.5085 TONNES the number of TONNES standing in this NON- active month of May.

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (1057 x 100 oz)+1128 OI for the front month minus the number of notices served upon today (1057)x 100 oz} which equals 112,800 oz standing OR 3.5085 TONNES

TOTAL COMEX GOLD STANDING: 3.5085 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,713,349.037 OZ 53.29 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,362,216.911 OZ

TOTAL REGISTERED GOLD: 12,356,047.766 (384.32 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,006,169.145 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,642,698 OZ (REG GOLD- PLEDGED GOLD) 331,932 tonnes//

END

SILVER/COMEX

APRIL 28//2023// THE MAY 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,025,644.204 oz JPMorgan Brinks CNT HSBC . |

| Deposits to the Dealer Inventory | 4760.200 oz Brinks |

| Deposits to the Customer Inventory | 681,152.176 oz CNT |

| No of oz served today (contracts) | 1015 CONTRACT(S) (5,075,000 OZ) |

| No of oz to be served (notices) | 1605 contracts (8,025,000 oz) |

| Total monthly oz silver served (contracts) | 1015 Contracts (5,075,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: 1

i) Into Brinks 4760.200 oz

total: 4760.200 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i)Into CNT: 681.152,176 oz

Total deposits: 681,152.176 oz

JPMorgan has a total silver weight: 139,600 million oz/270.974 million =51.53% of comex .//dropping fast

Comex withdrawals: 4

i) Out of JPMorgan; 591,769.520. oz

ii) Out of Brinks 104,418.700 oz

iii) Out of HSBC: 258,707.488 oz

iv) Out of CNT 70,748.516 oz

Total withdrawals; 1,025,644.204 oz

adjustments: 2

i) customer to dealer Manfra: 905,173.200 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 33.204 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 270.974 million oz

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY /2023 OI: 2621 CONTRACTS HAVING LOST 5099 CONTRACT(S).

THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER STANDING IN THIS VERY ACTIVE DELIVERY MONTH OF MAY IS AS FOLLOWS:

2621 CONTRACTS X 5000 OZ PER CONTRACT = 13,105,000 OZ

.JUNE HAD A 205 CONTRACTS GAIN TO 819

JULY HAD A 1067 CONTRACT GAIN TO 118,475 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1015 for 5,075,000 oz

Comex volumes// est. volume today 44,871 fair

Comex volume: confirmed yesterday: 83,324 good

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 1015 x 5,000 oz = 15,075,000 oz

to which we add the difference between the open interest for the front month of MAY(2621) and the number of notices served upon today 1015 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2023 contract month: 1015 (notices served so far) x 5000 oz + OI for the front month of APRIL (2621) – number of notices served upon today (1015 )x 500 oz of silver standing for the MAY contract month equates to 13.105 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

GLD INVENTORY: 926.28 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

CLOSING INVENTORY 469.182 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//

John Rubino….

Rubino: You Can’t Taper A Ponzi Scheme

FRIDAY, APR 28, 2023 – 01:27 PM

Authored by John Rubino via substack,

Why a shrinking money supply risks a massive, uncontrolled crash…

You probably hear the term “Ponzi scheme” tossed around frequently out there, but you may not know what it is and why it matters. So here’s a little background from Wikipedia:

A Ponzi scheme (/ˈpɒnzi/, Italian: [ˈpontsi]) is a form of fraud that lures investors and pays profits to earlier investors with funds from more recent investors.[1] Named after Italian businessman Charles Ponzi, the scheme leads victims to believe that profits are coming from legitimate business activity (e.g., product sales or successful investments), and they remain unaware that other investors are the source of funds. A Ponzi scheme can maintain the illusion of a sustainable business as long as new investors contribute new funds, and as long as most of the investors do not demand full repayment and still believe in the non-existent assets they are purported to own.

In the 1920s, Charles Ponzi carried out this scheme and became well known throughout the United States because of the huge amount of money that he took in.[4] His original scheme was based on the legitimate arbitrage of international reply coupons for postage stamps, but he soon began diverting new investors’ money to make payments to earlier investors and to himself.[5] Unlike earlier similar schemes, Ponzi’s gained considerable press coverage both within the United States and internationally both while it was being perpetrated and after it collapsed – this notoriety eventually led to the type of scheme being named after him.[6]

The key takeaway is that a Ponzi scheme dies when the inflow of new money is insufficient to pay off existing investors victims. To understand why this matters today, let’s do a thought experiment. Say that in the coming year, the US has to pay out 5% more for Medicare and Social Security, and 7% more for its global military empire. Meanwhile, businesses with debts coming due have to roll them over at higher interest rates, while homeowners with adjustable-rate mortgages see their monthly payments rise.

In the aggregate, that’s a lot of new dollars — let’s say half a trillion — that didn’t exist a year ago but are needed now. And they have to come from somewhere. In a normal fiat currency system, the central bank simply creates the needed currency out of thin air, everyone gets paid, and the resulting decline in the value of the currency is small enough that few are bothered.

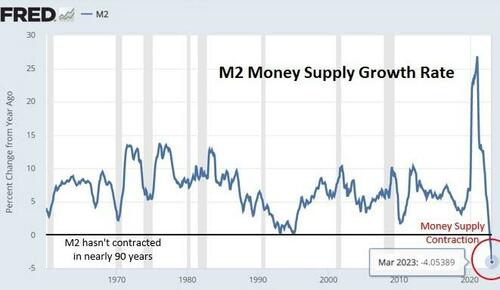

But that’s not what’s happening today. As the above obligations come due, the amount of available money is … shrinking. The following chart of the M2 money supply growth rate shows a massive spike from all the covid lockdown stimmy checks (which partially accounts for last year’s surge in consumer prices) and a correspondingly dramatic plunge this year. Note that during the entire fiat currency era, M2 has never before gone down.

This means some debts won’t be paid. Creditors thus stiffed will fail to pay their debts and so on until sectors start blowing up. Think back to last month’s local and regional bank near-death experience for a relatively benign example of what this unraveling will look like.

To sum up, the current global financial system is a Ponzi scheme and the new money spigot has been turned off. Excitement is about to ensue.

Here’s where it gets even more interesting

During the pandemic, central banks discovered how easy it is to flood an economy with newly-conjured cash. The US, for instance, simply mailed checks to citizens and gifted “loans” to small businesses while tossing trillions in loan guarantees and direct aid at favored large corporations. Easy peasy.

When today’s Ponzi scheme starts to unravel, those same governments will be faced with a choice between letting virtually everything grind to a halt as trouble at the collapsing periphery starts heading for the core (that is, as small players die in ways that threaten JP Morgan Chase), or restarting the stimmy check machine, but on a much bigger scale and with a major twist:

Instead of sending out paper or electronic checks to individual bank accounts, the Fed will roll out its much-discussed central bank digital currency and fund “free” account balances for everyone who it deems worthy of such a gift. The vast majority, traumatized by the disappearance of their jobs and stock portfolios, will willingly accept the free money. And just like that, the next financial system is born.

Which, as always, takes us back to gold and silver. History says the first phase of this process will feature an equities bear market that takes precious metals down for the ride. But in the second phase (i.e., the CBDC introduction), people who prefer not to own “programable” currency that’s monitored 24/7 by the NSA will convert their Fed bucks to real assets. Shortages of gold and silver will ensue and prices will respond accordingly.

end

3,Chris Powell of GATA provides to us very important physical commentaries

We reported on this during the week: Argentina is to settle Chinese imports in yuan bypassing the dollar

(Wong/SCMP)

Argentina to settle Chinese imports in yuan as China marches into South America to dethrone dollar

Submitted by admin on Fri, 2023-04-28 02:28Section: Daily Dispatches

By Kandy Wong

South China Morning Post, Hong Kong

Thursday, April 27, 2023

China’s push for greater use of its currency in bilateral trade settlements has made further inroads in South America, with Argentina set to follow Brazil and start to pay for Chinese imports in yuan rather than U.S. dollars.

Economy Minister Sergio Massa confirmed on Wednesday that Argentina, following a meeting with Chinese ambassador Zou Xiaoli and companies from various sectors, had “activated the swap with China.

Argentina will, Massa added, pay for US$1.04 billion of Chinese imports in April in yuan instead of US dollars and then US$790 million per month from May.

The second-largest country in South America is attempting to maintain its reserves of US dollars after a historic drought reduced exports by US$15 billion, including from its key agricultural sector. …

… For the remainder of the report:

end

We have a huge 25 million share reduction in the short position on SLV. The vehicle itself is a fraud

Ted Butler…

Ted Butler: The SEC and Black Rock blink on SLV

Submitted by admin on Fri, 2023-04-28 03:14Section: Daily Dispatches

By Ted Butler

SilverSeek.com

Thursday, April 27, 2023

The big news is last night’s release of the new short report on stocks, which indicated a massive 25 million share reduction in the short position on SLV, the big silver ETF, as of the close of business April 14. The short position on SLV fell from 41.5 million shares to 16.3 million shares, the largest by-monthly drop (60%) in history, to the lowest short position on SLV in more than two years — back to the time in Feb 2021 when BlackRock (the trust’s sponsor) amended the trust’s prospectus to include new risk factors warning short sellers to beware of shorting shares due to serious concerns of the availability of physical silver bullion.

https://www.wsj.com/market-data/quotes/etf/SLV

So, the immediate issue is what was behind the sudden large reduction in the short position on SLV (after all, 20 to 25 million ounces of silver is a big deal) and why would I conclude it involved any “blinking” by the Securities & Exchange Commission (the nation’s securities regulator) and BlackRock (the largest asset manager in the world)? …

… For the remainder of the analysis:

https://silverseek.com/article/sec-and-blackrock-blink-slv

end

A good interview to see

(Eric Sprott/GATA)

Eric Sprott details his investment outlook in interview with Craig Hemke

Submitted by admin on Fri, 2023-04-28 03:46Section: Daily Dispatches

2:45p ICT Friday, April 28, 2023

Dear Friend of GATA and Gold (and Silver):

Craig Hemke’s monthly wrapup on the monetary metals markets for Sprott Money is an interview with mining entrepreneur Eric Sprott, who says he is investing on the assumption of an economic recession, stock market decline, continued crisis in banking worsened by the collapse of commercial real estate, and strength in the monetary metals.

Silver has been manipulated so long, Sprott says, that one day it could explode seemingly out of the blue.

Sprott mentions a few mining companies whose prospects strike him as especially good.

The interview is 35 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Your weekend reading material

Alasdair Macleod….

Alasdair Macleod: The consequences of statist intervention

Submitted by admin on Fri, 2023-04-28 01:07Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, April 27, 2023

This article looks at our current economic condition from the viewpoint of classical economics. It is now 87 years since classical economics were dismissed by John Maynard Keynes in his “General Theory of Employment, Interest, and Money.”

Central to Keynes’ opus was a desire to create a role for the state, intervening in economic affairs. In searching for this objective, he had to traduce the law of the markets — Say’s Law. We show why this was mistaken. The error has been at the root of the accumulated errors of monetary policies ever since.

It has led to the destruction of the dollar’s purchasing power, reflected in a gold price that has risen from $35 to $2,000 — a depreciation of the dollar’s value as a medium of exchange relative to legal, sound money of over 98%. Furthermore, it has weakened America and her allies relative to the rising hegemons who may or may not have a cohesive understanding of economics but at least are not in thrall to the failed statist policies of the West. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/statist-intervention-the-consequences?gmrefcode=gata

end

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

Agnico eagle is probably the best of the majors: They reported strong first quarter results.

(Agnico eagle)

AGNICO EAGLE REPORTS FIRST QUARTER 2023 RESULTS – STRONG OPERATIONAL RESULTS WITH RECORD SAFETY PERFORMANCE; OPTIMIZATION ACTIVITIES PROGRESSING WELL IN THE ABITIBI GOLD BELT; 2022 SUSTAINABILITY REPORT RELEASED; YAMANA TRANSACTION AND SAN NICOLAS JOINT VENTURE TRANSACTION CLOSED

April 27, 2023

Download this Press ReleasePDF Format (opens in new window)

Stock Symbol: AEM (NYSE and TSX)

(All amounts expressed in U.S. dollars unless otherwise noted)

TORONTO, April 27, 2023 /CNW/ – Agnico Eagle Mines Limited (NYSE: AEM) (TSX: AEM) (“Agnico Eagle” or the “Company”) today reported financial and operating results for the first quarter of 2023.

“The year is off to a good start with strong operational results and the best quarterly safety performance in the Company’s over 65-year history, which positions us well to meet our full year guidance projections. Costs were better than expected, primarily due to the strong operating results, favourable currency movements and a slight easing of inflationary pressures,” said Ammar Al-Joundi, Agnico Eagle’s President and Chief Executive Officer. “With the completion of the acquisition of Yamana’s Canadian assets on March 31st, our focus in 2023 continues to be on the optimization of our strategic positions in the Abitibi gold belt, with an aim of increasing annual gold production from this region by approximately 500,000 ounces by the end of the decade. Efforts are ongoing to evaluate several opportunities to leverage existing infrastructure which has the potential to significantly increase future gold production at lower capital intensity and with a reduced environmental footprint. If realized, these opportunities have the potential to deliver increased returns to our shareholders with reduced execution and operating risk,” added Mr. Al-Joundi.

First quarter 2023 highlights – Solid operational performance and important strategic consolidations

- Strong quarterly production and costs with record safety performance – Payable gold production1 in the first quarter of 2023 was 812,813 ounces at production costs per ounce of $804, total cash costs per ounce2 of $832 and all-in sustaining costs (“AISC”) per ounce3 of $1,125. These results include only the Company’s 50% of the production from the Canadian Malartic mine up to March 30, 2023, and 100% thereafter

- Solid quarterly financial results – The Company reported quarterly net income of $3.87 per share in the first quarter of 2023, with adjusted net income4 of $0.58 per share. Operating cash flow was $1.30 per share. The quarterly net income of $3.87 per share includes a remeasurement gain of approximately $1.5 billion arising from the acquisition of 50% of the Canadian Malartic complex not previously owned by the Company

- Gold production, cost and capital expenditure guidance reiterated for 2023 – Expected payable gold production in 2023 remains unchanged at approximately 3.24 to 3.44 million ounces with total cash costs per ounce expected to be between $840 and $890 and AISC per ounce expected to be between $1,140 and $1,190. Total capital expenditures (excluding capitalized exploration) for 2023 are still estimated to be approximately $1.42 billion. The Company’s 2023 production, costs and capital expenditure guidance assumes 50% ownership of Canadian Malartic for the first three months of 2023 and 100% ownership for the last nine months of the year

- Update on key value drivers and pipeline projects

- Odyssey project – Good progress was made on underground development and surface construction activities in the first quarter of 2023. Underground development via ramp access has now passed the bottom of the Odyssey South deposit and has reached the level of the first shaft access point. Shaft sinking activities have also commenced. The first production blast occurred at the Odyssey South deposit in late March 2023. Drilling activities were focused on infilling the internal zones at the Odyssey South deposit and mineral resource expansion of the East Gouldie deposit to the east and west

- Detour Lake – In the first quarter of 2023, the mill set a record for first quarter throughput and activities continued to focus on mill process optimization and improving availability with the goal of achieving and potentially exceeding throughput of 28.0 million tonnes per annum (“Mtpa”). Step out drilling continued to the west of the resource pit shells and the Company is integrating additional drill data into a revised mineral resource model that will be used to evaluate potential underground mining scenarios

- Optimization of assets and capital infrastructure in the Abitibi region – With the Company now owning of 100% of Canadian Malartic complex, the Company expects to have up to 40,000 tonnes per day (“tpd”) of excess mill capacity at Canadian Malartic Complex starting in 2028. By maximizing the mill throughput in the region, the Company believes there is potential to increase future gold production at lower capital costs and with a reduced environmental footprint. Internal evaluations are underway to assess potential production opportunities at the Macassa near surface deposits and the Amalgamated Kirkland (“AK”) deposit, Upper Beaver and the Wasamac project. These evaluations are expected to be completed by year-end 2023

- Continued exploration success at Meliadine, Kittila, LaRonde Zone 5 (“LZ5”) and Goldex expected to drive future mineral reserve and mineral resource additions

- Meliadine – Drilling has targeted the vertical extensions of the mineralized zones in the central part of the Tiriganiaq and Wesmeg deposits. At Tiriganiaq, a recent intercept yielded 17.2 grams per tonne (“g/t”) gold over 4.9 metres at 770 metres depth. At Wesmeg, drilling in the eastern part of the deposit continues to return wide, high-grade intersections, with recent results including 8.9 g/t gold over 7.0 metres at 532 metres depth

- Kittila – Drilling has extended the Rimpi Main Zone to the north, outside of the current mineral resources, with highlights of up to 5.0 g/t gold over 9.2 metres at 1,141 metres depth. In addition, drilling has extended the Rimpi Zone mineralization down-plunge from the Roura area within the Parallel / Sisar zones, with intercepts of up to 5.0 g/t gold over 4.9 metres at 1,199 metres depth

- LZ5 – Drilling continues to expand the mineral resource envelope which now extends to a depth of 950 metres, with highlights including 3.0 g/t gold over 30.0 metres at 671 metres depth and 3.7 g/t gold over 10.1 metres at 840 metres depth. Inferred mineral resources are expected to be added at depths between 770 and 950 metres by year-end 2023

- Goldex – Infill drilling in the South Zone Sector 3 has returned high-grade results, including 9.8 g/t gold over 15.5 metres at 1,246 metres depth and 6.0 g/t gold over 12.0 metres at 1,274 metres depth. Initial drilling in the W Zone (approximately 200 metres west of the main Goldex deposit) has returned 1.8 g/t gold over 35.0 metres at 480 metres depth in an area with historical mineralized inventory

- Acquisition of Yamana’s Canadian assets and 50/50 San Nicolás copper-zinc joint venture with Teck completed

- Yamana Transaction – The previously announced transaction to acquire the Canadian assets of Yamana Gold Inc. (“Yamana”) closed on March 31, 2023 (the “Yamana Transaction”), and the Company now owns 100% of the Canadian Malartic Complex, the Wasamac project located in the Abitibi region of Quebec and several other exploration properties located in Ontario and Manitoba. The closing of the Yamana Transaction further solidifies the Company’s presence in the Abitibi gold belt, a region of low political risk and high geological potential, where the Company has a strong competitive advantage from having operated in the region for over 50 years

- San Nicolás – The previously announced 50/50 joint venture agreement between Teck Resources Limited (“Teck”) and Agnico Eagle in respect of the San Nicolás copper-zinc development project located in Zacatecas, Mexico was entered into on April 6, 2023. Minera San Nicolás S.A.P.I de C.V., the joint venture company that holds the project, is now working to advance permitting and development of the project and is planning to submit an Environmental Impact Assessment and permit application for San Nicolás in 2023 and is targeting completion of a feasibility study in 2024

- 2022 sustainability report published, illustrating continued commitment to strong ESG performance and implementation of a climate strategy action plan – In 2022, Agnico Eagle maintained or improved performance across many key ESG indicators, including safety performance, efficient management of water resources and increased Indigenous employment. In addition, efforts were accelerated in 2022 to maintain a climate resilient business by setting an interim reduction target of 30% of absolute Scope 1 and 2 emissions by 2030, and publication of the Company’s first Climate Action Report

- A quarterly dividend of $0.40 per share has been declared

ENend

Live from the Vault

Andrew Maguire and Robert Kientz

BlogCompany NewsCryptocurrencyPrecious MetalsUser GuidesLive from the Vault

The tyrannical side of digital currency: Is our freedom under threat…..

Robert Kientz

5.IMPORTANT COMMENTARIES ON COMMODITIES:

end

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1.YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS// FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.9190

OFFSHORE YUAN: 6.9316

SHANGHAI CLOSED UP 37.29 POINTS OR 1.40%

HANG SENG CLOSED UP 54.29 PTS OR 0.27%

2. Nikkei closed UP 398.76 PTS OR 1.40%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 101.78 EURO FALLS TO 1.0982 DOWN 49 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.390Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 136.07 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.3598***/Italian 10 Yr bond yield FALLS to 4.261*** /SPAIN 10 YR BOND YIELD FALLS TO 3.415…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.191

3j Gold at $1983.25 silver at: 24.85 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1 AND 75 /100 roubles/dollar; ROUBLE AT 79,58//

3m oil into the 75 dollar handle for WTI and 78 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 136.07 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .390% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8961 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9842 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.473 DOWN 5 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.706 DOWN 5 BASIS PTS/

USA 2 YR BOND YIELD: 4.0476 DOWN 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.45…

GREAT BRITAIN/10 YEAR YIELD: DOWN 3 BASIS PTS AT 3.7660

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

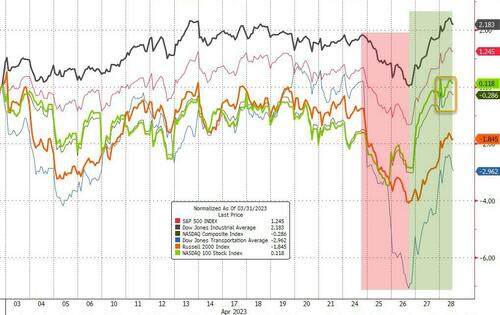

Stocks Slide As Tech Rally Goes Into Reverse After Amazon AWS Shocker

FRIDAY, APR 28, 2023 – 08:02 AM

A rally in US tech stocks was set to reverse on Friday as investors punted on a surprisingly downbeat comment by Amazon about the rapid slowdown in AWS sales growth in April, as well as the prospect of more interest-rate hikes, elevated inflation, signs of slowing economic growth and so on. Contracts on the Nasdaq 100 were down 0.3% by 730 a.m. ET after the underlying index soared 2.8% in its best day since Feb. 2 on Thursday following upbeat results this week from a slate of technology heavyweights. S&P 500 futures were also down 0.3% following the benchmark index’s sharpest gain since January. Treasuries bounced, while gold prices edged lower. Oil prices were also set to end the week lower. The dollar, meanwhile, rose while bitcoin was flat.

Amazon.com shares fell in premarket trading after the e-commerce company’s cautious comments on its AWS cloud computing business offset the otherwise strong first-quarter results. Shares had surged as much as 12% in extended trading Thursday, before reversing course as the comments highlighted weakness in Amazon Web Services, its most profitable division, where sales growth had slowed dramatically in April. Cloud stocks dropped in sympathy amid worries that demand for technology is cooling. Microsoft (MSFT US) -0.3%, Snowflake (SNOW US) -3.3%, Datadog (DDOG US) -3%.

In other notable moves in premarket trading, Snap Inc. tumbled after reporting revenue for the first quarter that missed the average analyst estimate. Cloudflare Inc. sank after the cybersecurity-focused software company issued a weaker-than-expected revenue forecast for the current period. Intel Corp. rallied as the chipmaker reported first-quarter results and projected a return to free cash flow in the second half of the year.

Here are the most notable premarket movers:

- Amazon.com slipped 1% in premarket trading after the e-commerce company’s cautious comments on its cloud computing business offset the otherwise strong first-quarter results. Shares had surged as much as 12% in extended trading Thursday, before reversing course after the comments highlighting weakness in Amazon Web Services, its most profitable division

- Intel shares gained 4% in premarket trading, after the chipmaker reported first-quarter results and projected a return to free cash flow in the second half of the year. Analysts noted that the worst might be over for the struggling chipmaker, with some of them saying that its revenues might have found a bottom.

- Snap fell 19% in premarket trading, after reporting revenue for the first quarter that missed the average analyst estimate. Analysts noted that the outlook for the stock has weakened as the social-media company continues to make adjustments to its platform in a tough macro environment.

- Cloudflare fell 24% in premarket trading, poised for its biggest drop ever if its losses hold, after the cybersecurity-focused software company issued a weaker-than- expected revenue forecast for the current period and lowered its full-year revenue outlook. Analysts noted that the company was forced to cut guidance as sales cycles materially lengthened in the aftermath of the SVB collapse and the subsequent banking crisis.

- Pinterest falls 13% in premarket trading after the social-media company gave a forecast that was seen as weak. While analysts noted that the macro backdrop remains tough, some were optimistic that the firm is on track to expand its margins this year.

- Shares of US-listed Hong Kong online brokerage firm Top Financial (TOP US) post a sixfold increase in premarket trading. More than 150,000 shares have been traded as of 4:42 a.m. in New York.

- First Solar shares plunge 9% in US premarket trading, set for their worst day since July 2022, after the solar module manufacturer’s first quarter net sales disappointed, with analysts pointing to sluggish momentum in bookings. Still, brokers noted that the company reiterated its guidance for the year, spurring hopes it will be able to meet forecasts.

- Amgen declined in postmarket trading, as analysts highlight that first quarter revenues for Enbrel and Otezla missed consensus estimates. The company boosted its adjusted earnings per share forecast for the full year.

- Capital One shares dropped in postmarket trading after the company reported adjusted earnings per share for the first quarter that fell short of analyst estimates. The firm reported total deposits for the first quarter that beat the average analyst estimate.

- Alteryx declined in extended trading on Thursday, after the software company gave a second-quarter forecast that was weaker than expected.

While the quarterly reporting season has been far better than many – especially Mike Wilson – feared so far, US stocks have struggled to extend a first-quarter rally amid worries of a recession and a staunchly hawkish Federal Reserve.

CMC Markets chief market strategist, Michael Hewson, said that while the unexpected strength in first-quarter earnings from the technology sector was “no doubt a relief for investors,” it also comes against “very low expectations.” “When the penny finally drops with respect to” an expected weakening in consumer demand, “perhaps the gains this week might start to run out of steam,” he said.

Focus today will be on the Fed’s preferred inflation gauge — the core PCE deflator. Bloomberg Economics expects the reading for March to show core services inflation accelerating from the previous month.

Meanwhile, Bank of America Corp. strategist Michael Hartnett said he expects a drop in earnings and a softening labor market to derail the equity rally further. In a note citing data from EPFR Global, the strategist said US stock funds saw outflows for a second straight week at $2.7 billion.

Markets remain on edge, as data showing a surprise increase in US inflation pressures reinforced expectations of a Federal Reserve interest rate hike next week, and possibly in June. A growth rebound in France and a forecast-beating expansion in Spain have fanned hopes Europe can avert a recession, but an uptick in consumer-price gains points to more rate increases by the European

In Europe, traders firmed up bets on the ECB slowing to a 25bps rate hike next week after digesting a raft of growth and inflation figures from the region. The euro-area economy grew slightly less than expected in the first quarter after German economic growth stagnated while regional CPI prints from the bloc’s largest economy suggest the national print will slow later today.

Stocks are also in the red with the Stoxx 600 lower by 0.2% with utilities and travel among the worst performers, but it was banks that were the worst-performing sector in Europe Friday, with the Stoxx 600 Banks Index falling as much as 2.8%, its biggest drop in a month, on worries of resurgent inflation. The subindex was 1.7% lower as vs the Stoxx 600 Index’s 0.2% decline. Spanish and Italian banks were among the worst performers with Sabadell -6.9%, CaixaBank -4.7%, FinecoBank -3.8%, Banco BPM -3.8%. NatWest fell 5.6% after a miss on net interest income and softer guidance on deposit growth offset a profit beat for the UK lender. Here are the most notable European movers:

- Electrolux gains as much as 9.8%, the most in three years, after the Swedish white-goods manufacturer reported better-than-feared 1Q results that pave the way for estimate upgrades

- Numis shares rise as much as 68% to 343p after Deutsche Bank agreed to buy the boutique investment bank, a City household name, in a £410 million-deal

- SCA shares gain as much as 8.5% after the Swedish forestry group’s first-quarter earnings blew past estimates which had been under pressure into the print after weaker results from its peers

- Prudential shares rise as much as 4.7% in early trading, as analysts say the insurer’s new business update looks solid and shows encouraging recoveries in Hong Kong and Indonesia

- Hikma Pharmaceuticals rises as much as 4.9% after the UK firm raised guidance for its generic drugs in a trading update. Barclays says the upgrade will be “taken well” by the market

- Covestro surges by as much as 6.3% after it forecast better-than-expected 2Q Ebitda and resumed buybacks.

- Kingspan shares jump as much as 6.2% after the Irish insulation and building-products maker said it sees first-half trading profit of more than €400m and announced plans to delist from the LSE

- SBB shares fall as much as 14% after the Swedish landlord posted a pretax loss of SEK4 billion in 1Q and announced plans to raise SEK2.6 billion in new class D shares

- Remy Cointreau dropped as much as 9.5%, the most since the Covid market crash of March 2020, after the distiller announced quarterly sales and an outlook that Citi called “very concerning”

- NatWest shares fall as much as 7.1% after a net interest income miss and softer guidance on deposit growth offset a profit beat for the UK lender. Analysts also noted the lack of a guidance upgrade

- Unicaja dropped as much as 10% after the lender reported net income for the first quarter that missed the average analyst estimate, with Morgan Stanley saying these are “disappointing” results

“What looks like sticky contemporaneous inflation remains an issue, preventing the market from getting too carried away on the rate-cutting phase to come in subsequent quarters,”’ wrote Padhraic Garvey, head of global debt and rates strategy at ING Financial Markets.

Earlier in the session, Asian stocks advanced, helping pare their month-to-date loss, as strong corporate earnings boosted optimism for a global economic recovery. Japanese equities extended gains after the results of the Bank of Japan policy meeting (more below). The MSCI Asia Pacific Index climbed as much as 0.8% before paring more than half of those gains, charged higher by TSMC and Samsung after tech earnings bolstered Wall Street overnight. Markets were mostly higher in the region with benchmarks in Japan, Hong Kong and Taiwan among the biggest winners.

Japanese stocks extended gains as the Bank of Japan maintained policy, including stimulus measures, in its first decision under Governor Kazuo Ueda. The Topix rose 1.2% to close at 2,057.48. The Nikkei advanced 1.4% to 28,856.44, its highest close since Aug. 19. The yen weakened 0.8% to around 135 per dollar. The BOJ scrapped its guidance on future interest-rate levels and called for a long-term review of its policies. The central bank also ditched the reference in its guidance to Covid-19 and its expectation that interest rates will stay at current or lower levels. This decision suggests “maintaining status quo,” said Rina Oshimo, a senior strategist at Okasan Securities adding that “the BOJ’s continued monetary easing stance has probably been factored in to some extent beforehand. Investors’ attention is shifting to corporate earnings, and it is difficult to take aggressive positions ahead of the major holidays and important events such as the FOMC meeting in the U.S.” BYD, ANA and China Life Insurance were among the major Asian companies that climbed after reporting better-than-expected quarterly results during Asia’s busiest earnings weak.

Chinese equities advanced as the nation’s top leaders reiterated support for the economy, while warning that domestic demand is still insufficient. The main Asian stock benchmark is still on course for a monthly loss of about 1% in April. The gauge is down roughly 6% from its late-January high amid a rout in Chinese equity market.

Australian stocks gained, with the S&P/ASX 200 index rising 0.2% to close at 7,309.20, supported by banks and mining shares. The gain comes after technology earnings bolstered Wall Street stocks. Still, the Australian benchmark edged 0.3% lower for the week, posting a second straight weekly loss. For the month, the index advanced the most since January. In New Zealand, the S&P/NZX 50 index rose 0.9% to 12,019.84

Indian stocks posted their biggest monthly gain in five to outperform Asian peers, supported by strong foreign inflows and as corporate earnings continue to meet investors’ expectations. The S&P BSE Sensex rose 0.8% on Friday to 61,112.44 in Mumbai, while the NSE Nifty 50 Index advanced by the same magnitude. For the month, the Nifty 50 and BSE-Sensex climbed 4.1% and 3.6%, respectively with shares of automobile, banks and metal companies leading the winners. The MSCI Asia-Pacific index fell 1.1% this month. “Our bottom up model supported by market internals suggests further legs in the ongoing rally,” ICICI Securities’ Dharmesh Shah said in a note on Friday. Stocks of Adani Group saw a sharp rally ahead of the submission of Indian capital market regulator’s report to the Supreme Court-appointed panel on Wednesday. Flagship Adani Enterprises jumped 3.9% while Adani Ports gained 3.3%. Reliance Industries contributed the most to the Sensex’s gain, increasing 1.8%. Out of 30 shares in the Sensex index, 24 rose and six fell

In FX, the Bloomberg US dollar index advanced 0.5%, rising against all its peers Friday, sending the Bloomberg Dollar Spot Index for its biggest weekly advance since early March and its second consecutive weekly gain for the first time since Feb, as the yen plummets after the Bank of Japan policy decision which scrapped their existing rate guidance. The yen led major currency losses Friday, with USD/JPY up as much as 1.7% to 136.18, after the BOJ stuck with stimulus, disappointing those naive souls who think that Japan will ever be able to normalize (it won’t). European data showed the euro zone dodged a winter recession by growing at the start of 2023, despite inflation remaining a menace. The 20-nation economy expanded by 0.1% in the first quarter, falling short of the 0.2% median estimate in a Bloomberg survey of analysts, even as the German’s GDP Chain Linked GDP contracted. As a result, traders firmed up bets on the ECB slowing to a 25 basis-point rate hike in May.

In rates, treasuries gained following wider gains in core European rates as traders priced out some ECB rate-hike premium after a raft of growth and inflation figures from the region. US session features data including employment cost index and PCE deflator. US yields are richer by nearly 5bp across intermediates with 10-year yields around 3.48%, lagging bunds by around 3bp in the sector; US 2s10s spread is flatter by over 1bp on the day with front-end lagging gains further out the curve. German two-year yields are down 9bps at 2.74% while US two-year yields drop 4bps to 4.03%.

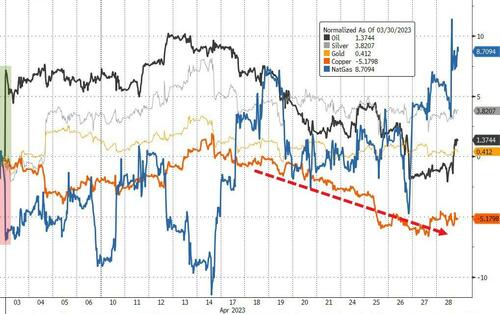

In commodities, crude futures are little changed with WTI trading near $74.80. Spot gold falls 0.2% to around $1,983.

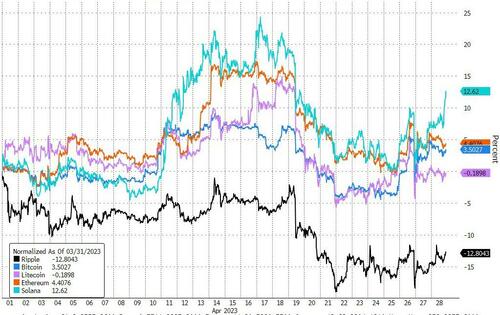

Bitcoin has eased further away from the USD 30k mark after failing to convincingly challenge it overnight or in Thursday’s session.

Looking at today’s calendar, we have crucial PCE data coming up at 8:30 a.m. today, accompanied by personal income figures for March that will indicate the pace of wage growth. At 10 a.m., we’ll get the latest reading on the University of Michigan consumer sentiment gauge. On the corporate earnings front, we have Chevron, Exxon, Colgate-Palmolive, Aon, and PetroChina all reporting.

US Market Snapshot

- S&P 500 futures down 0.4% to 4,137.25

- STOXX Europe 600 down 0.3% to 462.57

- MXAP up 0.2% to 160.26

- MXAPJ up 0.3% to 513.43

- Nikkei up 1.4% to 28,856.44

- Topix up 1.2% to 2,057.48

- Hang Seng Index up 0.3% to 19,894.57

- Shanghai Composite up 1.1% to 3,323.28

- Sensex up 0.3% to 60,841.97

- Australia S&P/ASX 200 up 0.2% to 7,309.15

- Kospi up 0.2% to 2,501.53

- German 10Y yield little changed at 2.36%

- Euro down 0.4% to $1.0983

- Brent Futures down 0.4% to $78.05/bbl

- Gold spot down 0.3% to $1,982.30

- U.S. Dollar Index up 0.50% to 102.01

Top Overnight News

- The BOJ has scrapped a key part of its forward guidance on interest rates in Kazuo Ueda’s first board meeting as governor, signaling the first step towards unwinding its ultra-loose monetary policy. The yen fell sharply on Friday as the 71-year-old economist played it safe during his debut, announcing a comprehensive review of the BoJ’s policies while holding off from revising its longstanding yield curve control measures. FT

- Japan’s Tokyo CPI overshot the Street consensus for April, coming in at +3.5% on the headline (vs. the Street’s +3.3% forecast and up from +3.3% in March) and +3.8% core (vs. the Street +3.5% and up from +3.4% in March). BBG

- Chinese leaders kept their economic policy stance largely unchanged, signaling it’s too early to pivot toward tighter monetary and fiscal measures or push contentious economic reforms as growth rebounds. BBG

- Russia hurled missiles at cities across Ukraine as people slept early on Friday, killing at least 12 people in the first large-scale air strikes in nearly two months. RTRS

- Inflation in the euro-area muddied the rate debate there too. CPI accelerated in France and Spain and traders and policymakers are braced for the German figure later. GDP data showed the bloc expanded by 0.1% in the first quarter, falling short of the 0.2% consensus. France and Italy bounced back from negative readings in the prior quarter, while Spain gathered momentum and Germany stagnated. BBG

- Chanel rules out an IPO, insisting it will stay a private company, and expresses optimism about Asia but caution in the US. FT

- The repossession industry is seeing an uptick in demand as more Americans struggle to afford their car payments. And companies that specialize in seizing vehicles are having trouble hiring enough agents, after many decamped for other jobs during the pandemic when business largely dried up due to stimulus measures. BBG

- Amazon fell premarket after jolting investors with a warning that cloud sales growth is slowing. The stock had jumped earlier on a profit and revenue beat. Snap is set for its biggest intraday share drop in more than six months after reporting a decline in quarterly revenue. BBG

- First Republic’s advisers are working on a private-sector solution they hope can overcome skepticism in Washington and keep the embattled California bank from being shut down by the Federal Deposit Insurance Corporation. FT

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were positive after taking impetus from the rally on Wall St where the S&P 500 and DJIA posted their best daily performance since January as sentiment was fuelled by strong earnings results, while the region also digested a slew of earnings, month-end data releases and the BoJ policy decision. ASX 200 was initially led higher by outperformance in financials and tech, but then faded most of the gains. Nikkei 225 was lifted after Industrial Production and Retail Sales topped forecasts, while the BoJ kept also policy settings unchanged, tweaked its forward guidance which remained dovish and announced it is to conduct a policy review. Hang Seng and Shanghai Comp were firmer amid tech strength and an abundance of earnings releases, with sentiment also supported by the PBoC’s liquidity efforts ahead of the 5-day closure in the mainland.

Top Asian News

- Chinese Commerce Minister Wang Wengtao met German Vice Chancellor Habeck in Berlin to discuss the implementation of economic and trade consensus between both countries, while they also discussed deepening bilateral practical cooperation, creating a fair and just business environment for Chinese and German companies, as well as green cooperation, according to MOFCOM.

- China’s Politburo says China economic expansion is under recovery, but internal momentum is weak; economic transformation faces new constraints. Should prioritise attracting foreign investment and stabilise the basic market for foreign trade/investment.

- BoJ kept policy steady with rates at -0.10% and parameters of QQE with YCC maintained, but tweaked its forward guidance whereby it stated that it will take additional easing steps without hesitation as needed while striving for market stability in which the central bank dropped its reference to COVID-19 pandemic and dropped forward guidance that pledged to keep interest rates at current or lower levels. BoJ also announced to conduct a broad-perspective review of monetary policy with a planned time-frame of one to one and a half years and noted that it will patiently continue with monetary easing as uncertainty over Japan’s economy is extremely high.

- Governor Ueda: Will make changes to monetary policy as needed during the review period.; decided to maintain policy easing including YCC, will conduct a review of policy of past 25 years; Japanese CPI is likely to slow below 2% in H2 2023. Review is differentiated from examination/assessment as it does not intend near-term policy changes. Won’t hesitate to ease policy further if necessary.