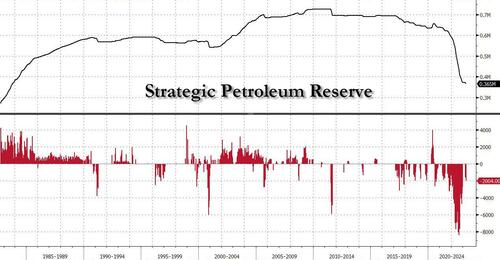

MAY 9/ALL PRECIOUS METALS HAVE A GREAT DAY TODAY: GOLD CLOSED UP $9.70 TO $2035.50, SILVER WAS UP 7 CENTS TO $25.64 AFTER BEING DOWN ALL DAY//PLATINUM WAS UP $29.00 TO $1108.25//PALLADIUM WAS UP $14.70 TO $1570.20//COVID UPDATES//DR PAUL ALEXANDER//VACCINE IMPACT//SLAY NEWS//VACCINE DEATHS AMONG YOUNG CHILDREN//DEBT CEILING MEETING IS TODAY BETWEEN BIDEN AND MCCARTHY//CRE CONTAGION SPREADS TO SWEDEN WITH ITS LARGEST REAL ESTATE CONGLOMERATE SHREDDED TO PIECES AS ITS BONDS GO TO JUNK AND ITS DIVIDEND SUSPENDED//BIDEN AGAIN DELAYS FILLING UP HIS SPR//TROUBLE IN PAKISTAN AS OPPOSITION LEADER KHAN ARRESTED AND THAT COULD LEAD TO CIVIL WAR IN THAT COUNTRY//SWAMP STORIES FOR YOU TONIGHT//

118 C MACQUARIE FUT 17 323 C HSBC 149 657 C MORGAN STANLEY 6 661 C JP MORGAN 93 737 C ADVANTAGE 1 4 905 C ADM 30

TOTAL: 150 150

JPMorgan stopped 93/150 contracts

FOR MAY:

GOLD: NUMBER OF NOTICES FILED FOR MAY/2023. CONTRACT: 150 NOTICES FOR 15000 OZ or 0.4665 TONNES

total notices so far: 5336 contracts for 533,600 oz (16.597 tonnes)

FOR MAY:

SILVER NOTICES: 88 NOTICE(S) FILED FOR 440,000 OZ/

total number of notices filed so far this month : 1951 for 9,755,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $9.70

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:///A DEPOSIT OF 5.66 TONNES INTO THE GLD//

INVENTORY RESTS AT 937,65 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 7 CENTS AT THE SLV//

SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF OF 0.08 MILLION OZ FROM THE SLV/: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 465.682 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 244 CONTRACTS TO 145,787 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS TINY SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.07 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.07). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A SMALL GAIN ON OUR TWO EXCHANGES OF 182 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 4.250MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS( 135CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.105 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE. JUMP OF 400,000 OZ(QUEUE JUMP RAISES THE AMOUNT OF SILVER STANDING)+0 EXCHANGE FOR RISK// TOTAL 4.25MILLION OZ OF EXCHANGE FOR RISK FOR THE MONTH(RAISES THE AMOUNT OF SILVER STANDING):THUS TOTAL OF 17.300 MILLION OZ OF STANDING FOR DELIVERY V) HUGE SIZED COMEX OI LOSS/ HUGE SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –1 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTRACTS for 7 days, total 5942 contracts: OR 29.710 MILLION OZ . (848 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 29.710 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 29.710 MILLION OZ/INITIAL

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 244CONTRACTS DESPITE OUR $0.07 LOSS IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 135 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 13.105 MILLION OZ//FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 400,000 OZ (INCREASES THE AMOUNT OF SILVER STANDING) +// + 0.0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //TOTAL EXCHANGE FOR RISK MONTH= 4.25 MILLION//NEW TOTALS 13.050 MILLION OZ + 4.25 MILLION = 17.300 MILLION OZ// .. WE HAVE A SMALL SIZED GAIN OF379 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 88 NOTICE(S) FILED TODAY FOR 440,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 5209 CONTRACTS TO 515,785 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: removed 989 CONTRACTS

WE HAD A STRONG SIZED INCREASE IN COMEX OI ( 5209 CONTRACTS) WITH OUR $8.70 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR MAY. AT 3.5085 TONNES ON FIRST DAY NOTICE // PLUS 300 OZ QUEUE. JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)////YET ALL OF..THIS HAPPENED WITH OUR $8.70 GAIN IN PRICEWITH RESPECT TO MONDAY’S TRADING.WE HAD A STRONG SIZED GAIN OF 5432 OI CONTRACTS (16.895 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 223 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 515,785

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5432 CONTRACTS WITH 5209 CONTRACTS INCREASED AT THE COMEX AND 223 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5,432CONTRACTS OR 16.895TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (223 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (5209 //TOTAL GAIN IN THE TWO EXCHANGES 5432 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 3.5085 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 300 OZ // NEW STANDING: 16.6718 TONNES // ///3) ZERO LONG LIQUIDATION//4) STRONG SIZED COMEX OPEN INTEREST GAIN/ 5) TINY ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 19,854 CONTRACTS OR 1,985,400 OZ OR 61.75 TONNES IN 7 TRADING DAY(S) AND THUS AVERAGING: 2836 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES 61.75 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 61.75/3550 x 100% TONNES 1.73% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES ( MUCH SMALLER THAN LAST MONTH)

MAY: 61.75 TONNES (HEADING FOR ANOTHER SMALLER MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A SMALL SIZED 244 CONTRACTS OI TO 145,787 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 135 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 135 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 135 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI RISE OF 244CONTRACTS AND ADD TO THE 135OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 379 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 1.895 MILLION OZ

OCCURRED WITH OUR $0.07 LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

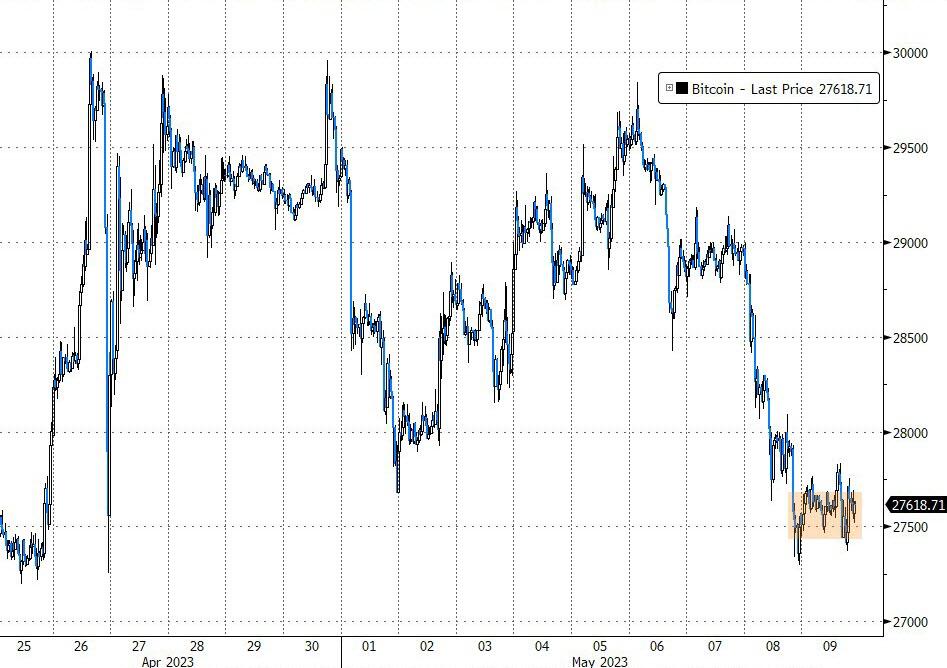

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED DOWN 37,33 PTS OR 0.40% //Hang Seng CLOSED UP 429,45 POINTS OR 2.12% /The Nikkei closed UP 292.94 OR 1.01% //Australia’s all ordinaries CLOSED DOWN 0.21 % /Chinese yuan (ONSHORE) closed DOWN 6.9215 /OFFSHORE CHINESE YUAN DOWN TO 6.9253 /Oil DOWN TO 72.55 dollars per barrel for WTI and BRENT AT 76.35 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 5209 CONTRACTS UP TO 515,785 WITH OUR STRONG GAIN IN PRICE OF $8.70 ON MONDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A TINY SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 223 EFP CONTRACTS WERE ISSUED: : JUNE 223 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 223 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 5,432 CONTRACTS IN THAT 223LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 5209COMEX CONTRACTS..AND THIS GOOD SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $8.70. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (16.6718) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 16.6718 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $8.70) //// AND WERE UNSUCCESSFUL IN KNOCKING CONSIDERABLE SPECULATOR LONGS AS WE HAD OUR STRONG SIZED GAIN OF 5432 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 16.895PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY. (3.5085 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 300 oz (0.00933 TONNES)//NEW STANDING 16.6718 TONNES ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $8.70

WE HAD –REMOVED 989 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 5432 CONTRACTS OR 543,200 OZ OR 16.895 TONNES.

Total monthly oz gold served (contracts) so far this month

5336 notices 533,600 OZ 16.597 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i)Into Manfra: 17,779.503 oz

(553 kilobars)

total deposits: 17,779.503 oz

customer withdrawals: 1

i) Out of Manfra

14,371.497 (447 kilobars)

total withdrawals: 14,371.497 oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 174 contracts having LOST 39 contracts. We had 42 contracts filed

on MONDAY, so we gained 3 contracts or an additional 300 oz (0.00933 tonnes) will stand for gold in this non active delivery month of May.

June LOST 17,486 contracts DOWN to 341,145 contracts.

July added 50 contracts to stand at 1404 contracts.

AUGUST GAINED 22,500 contracts up to 123,105 contracts

We had 150 contracts filed for today representing 15000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 150 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 93 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2023. contract month,

we take the total number of notices filed so far for the month (5,336 x 100 oz ), to which we add the difference between the open interest for the front month of MAY 174 CONTRACTS) minus the number of notices served upon today 150 x 100 oz per contract equals 536,000 OZ OR 16.6718 TONNES the number of TONNES standing in this NON- active month of May.

thus the INITIAL standings for gold for the MAYcontract month: No of notices filed so far (5,186 x 100 oz) 174 OI for the front month minus the number of notices served upon today (150)x 100 oz} which equals 536,000 oz standing OR 16.6718 TONNES

TOTAL COMEX GOLD STANDING: 16.6718 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH.

total pledged gold: 1,666,085.702 OZ 51.822 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,540,551.12 OZ

TOTAL REGISTERED GOLD: 12,400,059,885 (385,69 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,140,501.236 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,733,974 OZ (REG GOLD- PLEDGED GOLD) 333.87 tonnes//

END

SILVER/COMEX

MAY 9//2023// THE MAY 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

332,476,746 oz

Delaware HSBC Loomis

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

1,037,480.275 oz CNT Delaware Loomis

No of oz served today (contracts)

88 CONTRACT(S) (440,000 OZ)

No of oz to be served (notices)

659 contracts (3,295,000 oz)

Total monthly oz silver served (contracts)

1951 Contracts (9,755,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 3 deposits into the customer account

i) into CNT: 425,678.100 oz

ii) out of Delaware 10,951.525 oz

iii) Out of Loomis: 600,850.600 oz

Total deposits: 1,037,480.275 oz

JPMorgan has a total silver weight: 139,607 million oz/271.242 million =51.57% of comex .//dropping fast

Comex withdrawals 3

i) Out of Delaware: 999.300 oz

ii) Out of HSBC: 104,679.000 oz

iii) Out of Loomis: 226,798.446 oz

Total withdrawals; 322,476.746 oz

adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 31.624 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 271.242 million oz

CALCULATION OF SILVER OZ STANDING FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2023 OI: 747 CONTRACTS HAVING GAINED 47 CONTRACT(S). WE HAD 33 CONTRACTS FILED

ON MONDAY, SO WE FINALLY GAINED 80 CONTRACTS OR AN ADDITIONAL 400,000 OZ OF SILVER WILL STAND FOR DELIVERY IN THIS VERY

ACTIVE DELIVERY MONTH OF MAY.

JUNE HAD A 3 CONTRACT GAIN TO 936

JULY HAD A 62 CONTRACT GAIN TO 123,021 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 88 for 440,000 oz

Comex volumes// est. volume today 46,396 poor

Comex volume: confirmed yesterday: 38,598 poor

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 1951 x 5,000 oz = 9,755,000 oz

to which we add the difference between the open interest for the front month of MAY(747) and the number of notices served upon today 88 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2023 contract month: 1951 (notices served so far) x 5000 oz + OI for the front month of May (747) – number of notices served upon today (88 )x 500 oz of silver standing for the MAY contract month equates to 13.050 million oz + THE CRIMINAL 0 MILLION OZ EXCHANGE FOR RISK TODAY//NEW TOTAL EXCHANGE FOR RISK: 4.250//NEW TOTAL 17.300 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 437.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 431.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

GLD INVENTORY: 931.77 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

There’s a debate in the comments section here about whether Americans have gotten suddenly dumber, leading them to elect populist presidents and refuse vaccines. I started to weigh in but quickly realized that the story is broader and deeper than just vaccines and Donald Trump.

So here’s some context:

Starting in the 1960s, the US embraced a 3,000-year-old idea from Plato’s Republic, in which the ideal government would be run by the best possible person — a “philosopher king” who was both wise and good. In modern terms, an expert.

Starting with John Kennedy’s celebration of artistic and scientific excellence in the White House and continuing through the Vietnam War’s “best and brightest” leadership, we invented what later came to be called the “Ph.D. standard” in which people with advanced degrees from prestigious schools and records of success in a given field were put in charge of big parts of the government and economy — on the assumption that they were smart enough to actively manage things like financial markets and wars.

They failed miserably, screwing up everything they touched and leaving us with a corrupt, indebted world one itchy trigger finger away from nuclear armageddon. Or, seen through a different lens, they efficiently served their (Ivy League educated, highly credentialed) class by enriching the 99% while impoverishing what was once the middle class.

Specifically:

Monetary policy. Prior to 1971, the world was on a version of the gold standard that, without getting bogged down in the details, limited the amount of currency countries could create, thereby restraining governments’ more idiotically expensive impulses.

Then governments decided they could do a better job of managing their currencies than could an inert, arbitrary, barbarous rock. So they broke the link with gold and handed monetary policy to a generation of economists who, being brilliant and accomplished, would manage the world’s finances sagaciously, raising and lowering interest rates and the money supply just enough to produce steady non-inflationary growth, basically forever.

The result? The dollar’s purchasing power plunged while debt at every level of every major country soared. The amplitude of booms and busts increased to the point where the next bust might be fatal.

The Federal Reserve’s economists couldn’t have done worse if they were blind monkeys pulling random levers to get treats. Or, looking through that other lens, they served their class brilliantly by using artificially-low interest rates and various other forms of corruption to enrich banks and corporations, such that Wall Street now owns the world and the average person can’t afford to buy a house. Either way, they emphatically did not achieve the promised high-growth, low-inflation Nirvana.

Globalization. In the1980s and 1990s, we handed off trade policy to a different group of economists and other specialists who cut free trade deals with every country in sight, apparently unaware that American workers couldn’t compete with their $1-an-hour Chinese counterparts. The experts promised that free trade would benefit everyone by raising efficiency and lowering prices. What it actually did was crush millions of formerly unionized workers while enriching the multinationals that moved US factories to China for the (highly profitable) cheap labor.

The past two decades have seen a collapse in US living standards, political turmoil as a growing number of voters choose candidates who promise to tear the old system out by the roots, and the implosion of the old globalized world before anything concrete evolves to replace it. Expect a decade of inflation and supply chain chaos as the work of the globalist trade experts is swept away.

War and foreign policy. Instead of learning from the failure of the Vietnam War, U.S. foreign policy has become even more erratic and corrupt as each new generation of experts has blundered around the world (especially the Middle East) breaking things and killing innocents, making exponentially more enemies, and lying about all kindsof war crimes and management abuses.

Now the Pentagon/State Department Russia/China experts have decided that it’s time for a two-front World War III against those other two nuclear powers. Who gains from this? No one, except the arms makers and their affiliated politicians.

Public health. Three short years ago most Americans considered the Centers for Disease Control (CDC), the National Institutes of Health (NIH), and the rest of the public health establishment to be an exception to the growing sense that most experts were incompetent and/or corrupt.

But during the pandemic, the health establishment turned out to be if anything worse than the Fed’s economists or the Pentagon’s chicken hawks. They locked down schools unnecessarily, destroyed thousands of small businesses, and coerced young people into taking experimental vaccines that later turned out to be unnecessary. They contradicted each other in public and apparently lied about things like gain-of-function research and natural immunity. Some typical headlines:

Now people who once thought doctors could be trusted and vaccines were generally a good thing are questioning those beliefs. And until convinced otherwise, they’re not vaccinating their kids. Is that a public health problem? Maybe, but it’s also completely understandable after two years of pandemic chaos.

The (philosopher) king is dying

We can debate whether the people running America’s big systems are incompetent morons or brilliant soldiers in the war for super-rich supremacy. But either way, they’re not to be trusted.

It took five decades, thousands of lives, and trillions of dollars, but the idea of the philosopher king is finally dying. Americans did not get dumber. They learned from their experience and adjusted their attitudes accordingly. They’re buying gold because they don’t trust the Fed. They’re planting gardens because they don’t trust Big Food. They’re researching vaccines and accepting only those with proven (not experimental or fictitious) safety and efficacy. They’re voting for candidates who promise to control immigration, bring back factory jobs, avoid foreign wars, and eliminate medical coercion.

If only our experts had the same good sense and flexibility.

3,Chris Powell of GATA provides to us very important physical commentaries

(Ed Steer/GATA)

Ed Steer: Six consecutive withdrawals from SLV

Submitted by admin on Tue, 2023-05-09 03:37Section: Daily Dispatches

3:35p SGT Tuesday, May 9, 2023

Dear Friend of GATA and Gold (and Silver):

The weekend edition of Ed Steer’s Gold and Silver Digest, published by GATA board member Ed Steer, is headlined “Six Consecutive Withdrawals from SLV” and it’s posted in the clear at SilverSeek here:

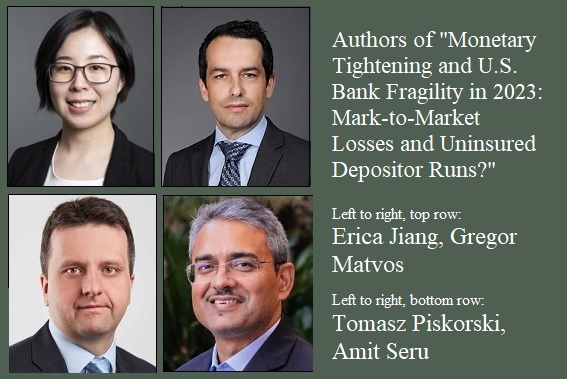

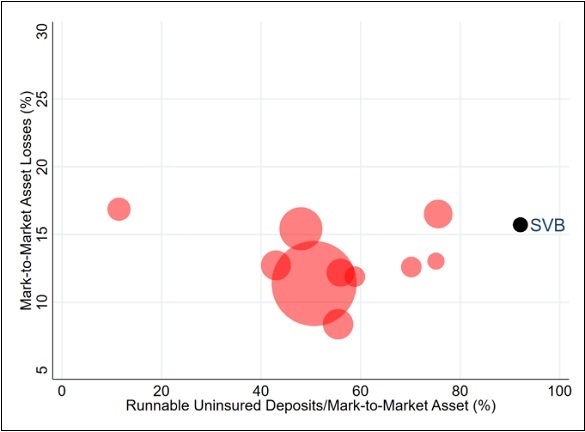

The systemic threats to the U.S. financial system were not remedied when Congress passed the watered-down Dodd-Frank financial reform legislation in 2010. While that has been evident with each Federal Reserve bailout of the mega banks and their derivative counterparties, the threat has now gained increased urgency for Congress to confront as a result of a new academic study. A team of four highly-credentialed academics at four separate universities present compelling evidence that one of the four largest U.S. banks, with “assets above $1 trillion,” could be at risk of a bank run.

The study is titled: “Monetary Tightening and U.S. Bank Fragility in 2023: Mark-to-Market Losses and Uninsured Depositor Runs?” Its authors are Erica Jiang, Assistant Professor of Finance and Business Economics at USC Marshall School of Business; Gregor Matvos, Chair in Finance at the Kellogg School of Management, Northwestern University, and Research Associate in the Corporate Finance group at the National Bureau of Economic Research (NBER); Tomasz Piskorski, Professor of Real Estate in the Finance Division at Columbia Business School and Research Associate at NBER; and Amit Seru, Professor of Finance at Stanford Graduate School of Business, a Senior Fellow at the Hoover Institution, and Research Associate at NBER.

The study focuses on unrealized losses on assets on the books of U.S. banks in a category called “held to maturity,” which under current accounting rules does not have to be marked to market, as well as unrealized losses on debt securities that also have not been marked to market, unless they are sold, for example, to raise cash to pay fleeing depositors. The professors find that “The U.S. banking system’s market value of those assets is $2.2 trillion lower than suggested by their book value of assets accounting for loan portfolios held to maturity.”

They then couple that finding with the threat posed to banks that hold large quantities of uninsured deposits – sums exceeding the federal deposit insurance cap of $250,000 per depositor, per bank. They then conduct various scenarios to see how different categories of banks would perform.

The most disturbing scenario is the following, which raises the issue of a bank with “assets above $1 trillion” potentially experiencing a bank run. (There are only four U.S. chartered banks that have assets above $1 trillion. According to the December 31, 2022 data from the Office of the Comptroller of the Currency, those are: JPMorgan Chase Bank N.A. with assets of $3.2 trillion; Bank of America N.A. with $2.4 trillion in assets; Citigroup’s Citibank N.A. with assets of $1.77 trillion; and Wells Fargo Bank N.A. with $1.71 trillion in assets.)

The scenario is explained as follows by the authors:

“To further assess the vulnerability of the US banking system to uninsured depositors run, we plot the 10 largest banks at the risk of a run, which we define as a negative insured deposit coverage ratio if all uninsured depositors run…Because of the caveats in our analysis as well as the potential of exacerbating their situation, we anonymize their names, but we also plot SVB [Silicon Valley Bank which failed on March 10] as comparison. We plot their mark-to-market asset losses (Y axis) against their uninsured deposits as a share of marked to market assets. Some of these banks have low uninsured deposits, but large losses, but the majority of these banks have over 50% of their assets funding with uninsured deposits. SVB stands out towards the top right corner, with both large losses, as well as large uninsured deposits funding. As Figure 5 shows [see below], the risk of run does not only apply to smaller banks. Out of the 10 largest insolvent banks, 1 has assets above $1 Trillion, 3 have assets between $200 Billion and $1 Trillion, 3 have assets between $100 Billion and $200 Billion and the remaining 3 have assets between $50 Billion and $100 Billion.”

We do not know which of the four mega banks the authors are referring to. We asked via email if they would identify the bank but they declined. Short sellers will, undoubtedly, drill down in the regulatory data filed by the four banks to determine the name of the bank in the study, so federal regulators and Congress need to move this issue immediately to the top of their banking crisis priority list.

Just 15 years ago, Citigroup/Citibank received the largest bailouts in U.S. banking history during and after the financial crisis of 2008. Its stock traded at 99 cents in early 2009. Sheila Bair, then the Chair of the Federal Deposit Insurance Corporation (FDIC), said this about Citigroup in her book, Bull by the Horns:

“By November, the supposedly solvent Citi was back on the ropes, in need of another government handout. The market didn’t buy the OCC’s and NY Fed’s strategy of making it look as though Citi was as healthy as the other commercial banks. Citi had not had a profitable quarter since the second quarter of 2007. Its losses were not attributable to uncontrollable ‘market conditions’; they were attributable to weak management, high levels of leverage, and excessive risk taking. It had major losses driven by their exposures to a virtual hit list of high-risk lending; subprime mortgages, ‘Alt-A’ mortgages, ‘designer’ credit cards, leveraged loans, and poorly underwritten commercial real estate. It had loaded up on exotic CDOs and auction-rate securities. It was taking losses on credit default swaps entered into with weak counterparties, and it had relied on unstable volatile funding – a lot of short-term loans and foreign deposits. If you wanted to make a definitive list of all the bad practices that had led to the crisis, all you had to do was look at Citi’s financial strategies…What’s more, virtually no meaningful supervisory measures had been taken against the bank by either the OCC or the NY Fed…Instead, the OCC and the NY Fed stood by as that sick bank continued to pay major dividends and pretended that it was healthy.”

Until Congress gets serious about breaking up these too-big-to-fail mega banks and restoring the banking system protections of the Glass-Steagall Act, which were repealed in 1999, every American is at risk of an unstable financial system.

Editor’s Note: The third paragraph has been updated to indicate that debt securities on the books of the banks were also included in the study.

END

END

5.IMPORTANT COMMENTARIES ON COMMODITIES:

end

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

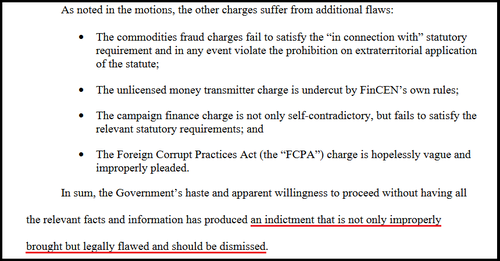

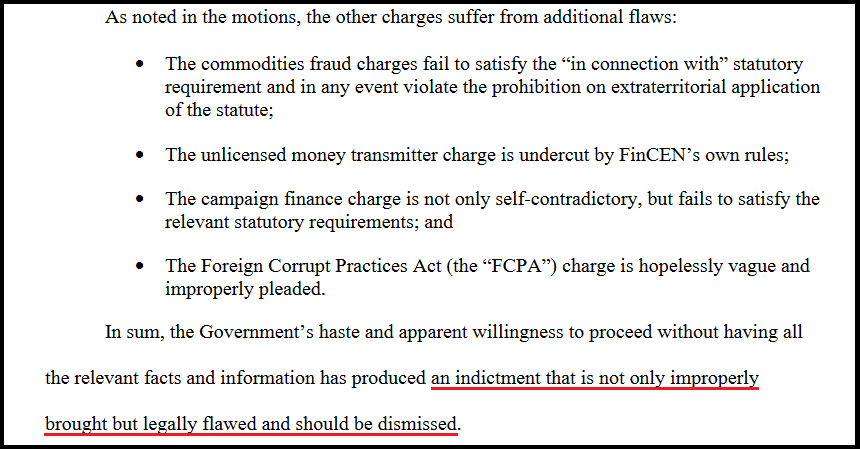

Disgraced FTX Founder Sam Bankman-Fried Tries To Dismiss Most Criminal Charges

TUESDAY, MAY 09, 2023 – 12:05 PM

FTX founder Sam Bankman-Fried asked a federal court in Manhattan Monday to dismiss 10 out of 13 criminal charges against him linked to the collapse of the failed crypto exchange. SBF has pleaded not guilty to fraud, conspiracy, campaign finance law violations and money laundering.

In a Monday filing, SBF’s lawyers argued that the US government had issued the original indictment against their client on Dec. 9 in a “classic rush to judgement” less than a month after the firm’s bankruptcy, and that several of the charges failed to properly state a crime.

“Rather than wait for traditional civil and regulatory processes following their ordinary course to address the situation, the government jumped in with both feet, improperly seeking to turn these civil and regulatory issues into federal crimes,” his lawyers wrote.

According to the letter, a campaign finance charge must be dismissed because it wasn’t included in the surrender warrant signed by the Bahamian government for his extradition.

SBF’s lawyers also attack the DOJ for bringing new charges against their client that alleged criminal conduct far beyond the Original Indictment and which are improperly brought.”

“Even if they are considered, the charges should be dismissed as legally flawed,” they added.

After Mr. Bankman-Fried properly consented to a simplified extradition procedure, the Bahamian government agreed to release him to U.S. authorities and issued a warrant of surrender specifying that he be tried on seven of the eight counts in the Original Indictment––but not the count relating to alleged campaign finance violations. Despite this clear direction from the Bahamian government, the Government now seeks to have Mr. Bankman-Fried tried on that charge as well.

The other charges they are attempting to have dismissed include those related to the unlicensed transmitting of money, bribery and bank fraud.

“The market crash took down many of the major players in this sector, not just FTX,” wrote the attorneys, noting that the broad market rout in 2022 hit many other cryptocurrency exchanges.

SBF’s trial is set for Oct 2. His right-hand(job) woman, former Alameda CEO Caroline Ellison and FTX co-founder Gary Wang both pleaded guilty in December to various federal wire fraud and conspiracy charges.

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS// MONDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.9215

OFFSHORE YUAN: 6.9253

SHANGHAI CLOSED DOWN 37.33 PTS OR 1.10%

HANG SENG CLOSED DOWN 429.45 PTS OR 2.12%

2. Nikkei closed UP 292,94 PTS OR 1.01%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 100.87 EURO RISES TO 1.1049 UP 40 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.421 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 134.77 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.30***/Italian 10 Yr bond yield FALLS to 4.235*** /SPAIN 10 YR BOND YIELD FALLS TO 3.396…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.072

3j Gold at $2032.20 silver at: 25.52 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 0 /100 roubles/dollar; ROUBLE AT 77.81//

3m oil into the 72 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 134.77 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .421% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8915 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9791 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.486 DOWN 3 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.802 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 3.9763 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.52…

GREAT BRITAIN/10 YEAR YIELD: UP 7 BASIS PTS AT 3.844

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Slide As Small Bank Selling Returns

TUESDAY, MAY 09, 2023 – 08:33 AM

US index futures retreated as the short squeeze that lifted distressed regional banks fizzled and went into reverse, dragging names such as PacWest as much as 20% lower in premarket trading, while the latest Chinese macro data spooked investors after imports dropped much more than expected; lastly investors braced for key US CPI data due tomorrow. Both S&P 500 and Nasdaq 100 contracts slipped 0.4% on Tuesday as of 8:00 a.m. ET. Meanwhile, the dollar is edging higher, set for a second day of muted gains. Oil prices have lost the momentum of the past two sessions, falling back in today’s trading. Gold is set for its third day of gains. Iron ore dropped in the wake of data that showed China’s imports of the steel-making ingredient fell to a 10-month low in April. Copper also slides.

In premarket trading, PacWest shares tumbled as much as 16% in premarket trading Tuesday, set to decline after two days of gains, while other US regional banks were also lower. Lucid Group fell 9.1% in premarket trading after the EV maker’s revenue and expected production disappointed investors. PayPal dropped 4.3% after the payment company warned that its adjusted operating margin won’t grow as quickly as it had anticipated earlier. By contrast, Palantir jumped 19% in premarket after the software firm published a surprise profit and a strong forecast, as well as reporting solid demand for its upcoming artificial intelligence tool. Some other notable premarket movers:

Skyworks shares fall 9.5% in US premarket trading after the update from the wireless semiconductor company showed continued headwinds for the Android ecosystem, weighing on its margin guidance and overshadowing an otherwise in-line quarterly print.

Coherus Bio slid 15% in low-volume premarket trading after the biopharma firm’s quarterly results showed a revenue miss driven by weakness at its Udenyca product, with analysts split on the quality of the outlook for the biopharma. Shares were down 8.4% in extended trading Monday.

Premier’s announcement of a strategic review is not a major surprise, analysts say, given a stagnant share-price and trading performance in recent times. Private equity buyers are seen as the most likely suitors, according to Credit Suisse, while SVB Securities sees significant value in a breakup of the business. Premier shares climbed 7.2% in after-hours trading on the news.

Shockwave Medical shares topped expectations and showed growth remains strong for the medical-devices company, though its shares will be put under pressure from a report that talks on a potential takeover offer for the firm by Boston Scientific have broken down. The shares declined 4.6% in after- hours trading.

International Flavors & Fragrances’ first-quarter results are mixed, with sales slightly above expectations but guidance below for the group. Shares fell 1.5% in after-hours trading.

McKesson’s quarterly earnings were solid but the pharmaceuticals distributor’s guidance is the highlight of its update, coming in well ahead of expectations. Analysts flagged continued growth in key areas for the group and that its guidance indicates it is executing successfully on its strategy. Shares in the group rose around 4% in after-hours trading.

Sentiment was also hit by a report showing a drop in Chinese imports last month, raising concerns about the country’s ability to boost the global economy. Investors also weighed signs that the world’s central banks may need to do more to fight sticky inflation.

Focus is now shifting to the US consumer-prices data due on Wednesday to gauge the interest-rate path, according to Michael Hewson, chief analyst at CMC Markets in London. “The US labor market remains tight and there is still inflationary pressure within the underlying economy,” he said. “For all the expectation that last week’s Federal Reserve rate hike might be the last, the strength of the US economy might mean that there may be one left to come.”

Separately, investors are also tracking efforts in Washington to end a standoff over the US debt ceiling, with President Joe Biden due to sit down with House Speaker Kevin McCarthy Tuesday for their first meeting in three months as the two face pressure to forge a deal. As we discussed previously, this game of chicken is unlikely to be resolved without a market panic first.

“Whilst we expect a last-minute resolution to the US debt-ceiling melodrama, anxiety is now starting to creep into markets,” said John Leiper, chief investment officer at Titan Asset Management.

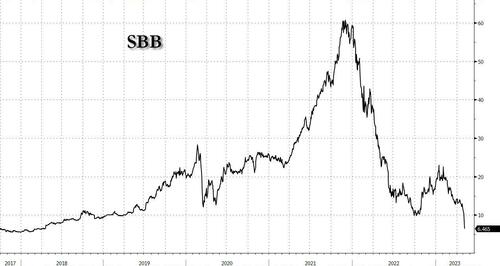

In Europe, the Stoxx 600 is down 0.6% with the consumer product and energy sectors also underperforming. Real estate stocks are leading the broader market lower in Europe as Swedish landlord SBB slumps after halting its dividend. Here are the biggest European movers:

SBB slumps as much as 13% to the lowest since April 2018, dragging the European real estate sector lower, after the Swedish landlord halted dividend payments and canceled a SEK2.6 billion rights issue

Fresenius SE shares gain as much as 7.4% on better-than-expected first quarter that Barclays says was boosted by its medicines and nutritions unit Kabi, as well as its separately listed dialysis unit

Grifols shares rise as much as 8.5%, the most since Feb. 16., with Jefferies saying the quarterly update from the Spanish blood-plasma firm beat on the top line and issued better margin guidance

Media stocks top all other Stoxx 600 sectors on Tuesday and buck weakness in the broader market, after Pearson said it’s working to embed generative AI technology across its product lineup

JD Sports shares rise as much as 3.2% after saying it’s in exclusive talks to buy French chain Courir for an enterprise value of €520m. Analysts say the deal fits with the company’s strategy

Banco BPM shares rise as much as 6%, with analysts saying the Italian lender’s quarterly results were strong, with the highlights being higher guidance and potentially greater shareholder returns

Amadeus shares rise as much as 1.7% with the travel IT services provider reported better-than-expected results across three main divisions as air traffic recovered across the globe

Marshalls slumps as much as 16% after the building materials group says trading this year has been weaker than expected. Analysts point to the weaker environment for housebuilding in 2023

Daimler Truck falls as much as 4.6% after 1Q results analysts say are consistent and in line with the pre-release last month, with the German truckmaker also confirming 2023 guidance

Evonik shares decline as much as 2.8% after it posted mixed results in 1Q. Analyst say the firm’s outlook will be a main focus after it said it now sees adjusted FY Ebitda “more likely” at the lower end

Victrex shares fall as much as 11%, hitting the lowest since April, as analysts said deteriorating volumes for the thermoplastics maker will put pressure on consensus estimates

JPMorgan strategists, who have been permabearish all year after cheering the 2022 collapse all year, are now calling for an end of European stock outperformance. Europe benefited from China’s reopening and a less-severe energy crisis than initially anticipated, but JPMorgan said these tailwinds are showing signs of fading, with economic surprises in the region now turning negative. After euro-zone stocks rose in the past seven months, investors “should be locking in these gains,” strategists led by Mislav Matejka wrote in a note on Tuesday.

Earlier in the session, Asian stocks edged lower as sentiment soured on China’s weak import data, while a recent rally in the nation’s state-owned enterprises fizzled. The MSCI Asia Pacific Index gave up earlier gains to fall as much as 0.2%, led lower by communication shares. Benchmarks in Hong Kong fell the most in two months, while Japanese shares outperformed the region as investors cheered latest corporate earnings. The Topix is approaching its highest level since August 1990. Chinese stocks slid in afternoon trading as a rally in state-owned firms reversed, dragging on the broader market. Meanwhile, fresh data showed imports slumped in April while export growth slowed, adding to pressures on an economic recovery that’s already been called into question.

“The imports miss could signal that Chinese household consumption still has a way to go,” said David Chao,global market strategist for Asia Pacific at Invesco Asset Management, adding that Chinese households are “not ready to pry open their purse strings to buy discretionary goods and products.” The reopening rally in China has stalled in recent months due to a lack of fresh catalysts. Still, market conditions are favorable for the country’s equities, said William Fong, head of Hong Kong China equities at Baring Asset Management Asia. “Recovering consumption and supportive government policies are driving improvement in Chinese corporate fundamentals.” Investors will be watching the US inflation data due Wednesday for more clues on the Federal Reserve’s next moves. A decline in the inflation reading and the recent banking turmoil have fueled expectations that the Fed will soon halt its monetary tightening or even begin cutting interest rates.

Japanese stocks rose as investors applauded results from major local firms and awaited key US inflation data. The Topix rose 1.3% to close at 2,097.55, while the Nikkei advanced 1% to 29,242.82. Steelmakers and trading houses were the biggest advancing industry groups after reports from companies including JFE and Sumitomo Corp. Toyota Motor contributed the most to the Topix gain, increasing 3.3%. Out of 2,160 stocks in the index, 1,720 rose and 360 fell, while 80 were unchanged. “US earnings and employment data were strong, and if monetary tightening continues, the dollar will strengthen and the yen will weaken, which is positive for Japanese equities.” said Tetsuo Seshimo, a portfolio manager at Saison Asset Management. “The market had low expectations for Japanese earnings, so the solid results should also be viewed positively.”

Stocks in India failed to hold initial gains and closed nearly flat, with banks among worst performers on profit-taking by investors. The S&P BSE Sensex was little changed at 61,761.33 in Mumbai, while the NSE Nifty 50 Index was flat at 18,265.95. The gauges surged more than 1% each on Monday, their biggest rally since March and are trading close to their highest levels since mid-December. India VIX, a gauge of volatility, has risen for three straight sessions through Tuesday amid selling in some sectors including banks after some lenders reported higher provisions for the March quarter. Out of 28 companies in the Nifty 50 guage that have so far reported quarterly earnings, 15 have either met or beaten consensus earnings estimates, while 10 have trailed. Construction major L&T and generic drug maker Dr Reddy’s will be reporting earnings on Wednesday.

In FX, the Bloomberg Dollar Spot Index inches up 0.1%; weakness in most global share markets spur light demand for the haven currency. The Norwegian krone is the weakest of the G-10 currencies while the Japanese yen is the strongest. Traders are also weighing “the outlook for interest rates alongside debt ceiling talks,” Jeff Ng, a senior currency analyst at MUFG Bank in Singapore, wrote in a note. “We anticipate more FX moves against the US dollar to materialize” as the US releases CPI numbers Wednesday, which may indicate that inflation stayed sticky. Investors are also bracing for US CPI figures due on Wednesday, as an expected steadying or slowdown in prices could bolster the view that Fed rate rises have ended after last week’s hike; further evidence of this could weigh on the dollar, strategists say. “While the short-term outlook for the dollar remains neutral in our view, thanks to positioning skewed to the short-side and unstable risk sentiment, markets remain ready to price in more Fed rate cuts, so downside risks are non- negligible,” ING strategists write in a note

In rates, Treasuries are slightly richer across the curve, erasing some of Monday’s losses, as stock futures retreat from Monday’s highs. Treasury yields richer by 2bp to 3bp across the curve with spreads slightly steeper, although broadly within a basis point of Monday’s closing levels; 10-year yields around 3.485%, richer by 2bp on the day with bunds lagging by 1.5bp in the sector; the two-year Treasury yield slips 2bps to 3.98%, pulling back form 4.01% hit on Monday, its highest in a week. Sentiment weakened slightly during Asia session when Chinese import data showed a steep drop. Focal points of US session include 3-year note auction, with critical April CPI data ahead Wednesday. Treasury auctions cycle begins with $40b 3-year note sale at 1pm, followed by 10- and 30-year sales Wednesday and Thursday. WI 3-year yield at ~3.655% is 15.5bp richer than April’s result, which stopped on the screws. In Europe, Bunds are little changed while Gilts have dropped, pushing UK 10-year yields up 4bps to 3.83% ahead of the Bank of England rate decision on Thursday.

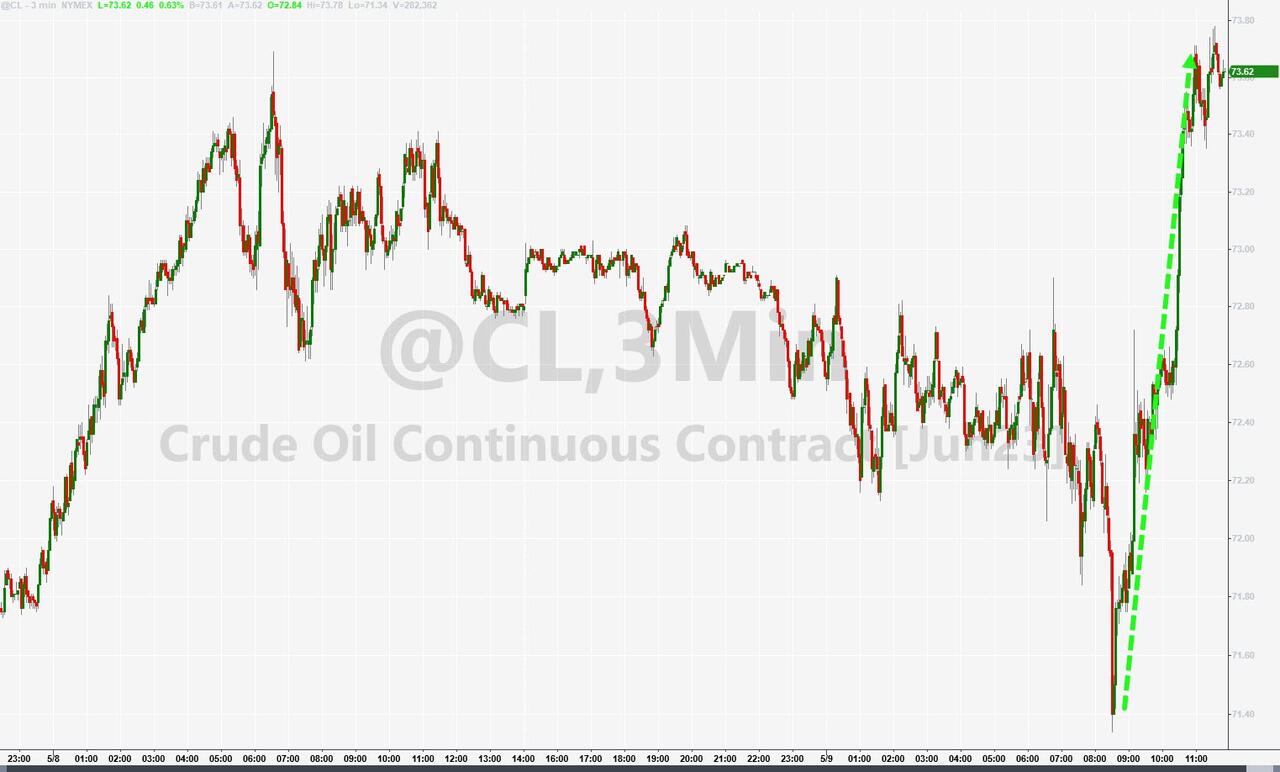

In commodities, crude futures decline with WTI falling 0.8% to trade near $72.60. Spot gold adds 0.3% to around $2,027.

Bitcoin is essentially unchanged within sub-USD 300 parameters and holding just above the USD 27.5k mark.

Looking at the day ahead, in the US we will get NFIB small business optimism, which will dovetail nicely with the SLOOS data that was released yesterday. Additionally, there is France’s March trade balance. From Central Banks, market participants will hear from the Fed’s Williams and Jefferson, as well as the ECB’s Lane, Vasle and Rehn. Lastly, while we are in the back-nine of earnings season there will be interest in reports from Saudi Aramco, Airbnb, Nintendo, Mitsubishi, Apollo, Electronic Arts, Daimler, and Wynn Resorts today.

Market Snapshot

S&P 500 futures down 0.4% to 4,137.50

STOXX Europe 600 down 0.5% to 464.49

MXAP down 0.2% to 162.34

MXAPJ down 0.9% to 517.13

Nikkei up 1.0% to 29,242.82

Topix up 1.3% to 2,097.55

Hang Seng Index down 2.1% to 19,867.58

Shanghai Composite down 1.1% to 3,357.67

Sensex down 0.1% to 61,688.29

Australia S&P/ASX 200 down 0.2% to 7,264.08

Kospi down 0.1% to 2,510.06

German 10Y yield little changed at 2.31%

Euro down 0.2% to $1.0977

Brent Futures down 1.2% to $76.07/bbl

Gold spot up 0.1% to $2,023.51

U.S. Dollar Index up 0.16% to 101.54

Top overnight news

China exports rise 8.5% Y/Y in April, above the Street’s +8% forecast, while imports sink 7.9% (significantly worse than the -0.2% consensus forecast). BBG

UBS appointed Ulrich Koerner to its top management body, giving the CEO of Credit Suisse a key role in overseeing the combination of the two firms. The announcement was part of a broader management shuffle that also saw Todd Tuckner, a veteran UBS banker, take over as CFO from Sarah Youngwood, who only joined the bank last year. BBG

Sweden’s Riksbank announced a half percentage-point hike to 3.50% on April 26 and said it would probably tighten policy again, by a quarter point this time, in either June or September before the hiking cycle comes to an end. RTRS

Investors shouldn’t count on the ECB’s unprecedented bout of interest-rate increases ending in July, as the majority of economists currently predicts, according to Governing Council member Martins Kazaks. “I don’t think it is that clear yet,” the hawkish Latvian official told Bloomberg on Monday by phone. “We still have quite some ground to cover and further rate increases will be necessary to tame inflation.” BBG

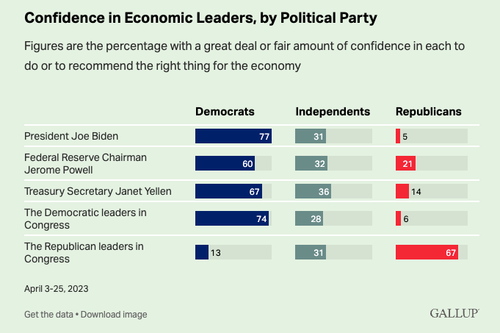

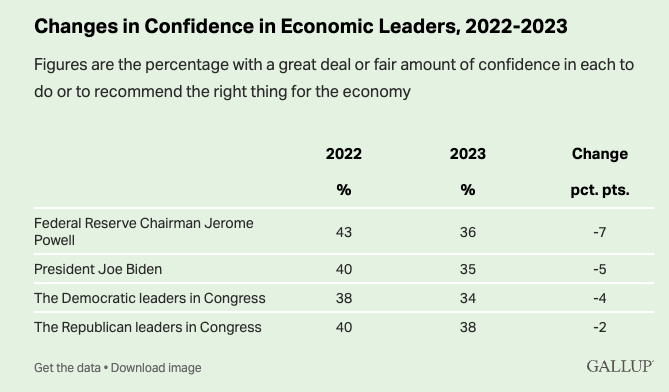

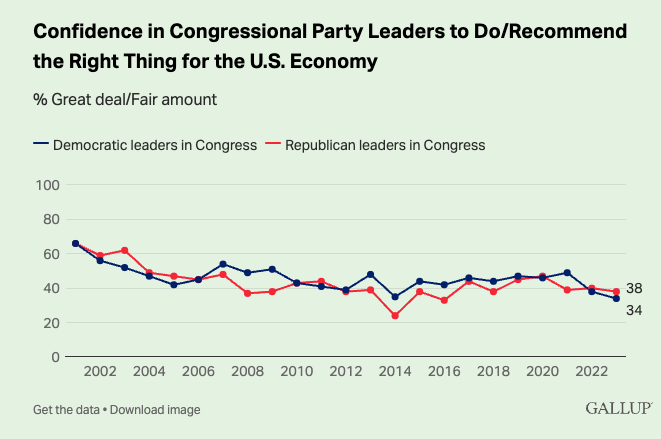

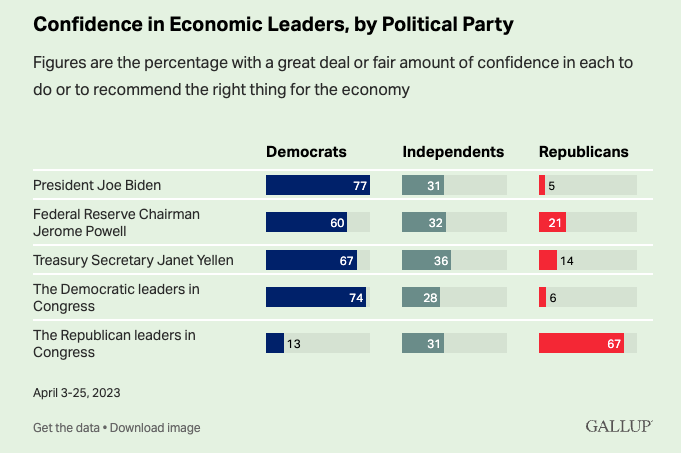

Americans have low confidence in Biden, Powell and Yellen on the economy according to a new Gallup poll (Biden’s economic polling numbers are nearly as low as they were for George W Bush during the heart of the ’08 financial crisis). CNN

Treasury Secretary Janet Yellen is reaching out to U.S. business and financial leaders to explain the “catastrophic” impact a U.S. default on its debt would have on the U.S. and global economies. RTRS

US lenders warned that commercial property is ‘next shoe to drop’. Executives and investors fret about impact of rising rates and empty buildings on $5.6tn market. FT

Fed steps up scrutiny of CRE risks at banks (“the Federal Reserve has increased monitoring of the performance of CRE loans and expanded examination procedures for banks with significant CRE concentration risk”). Fed

AMZN is offering certain Prime customers cash payments if they pick up their packages at various locations (including Whole Foods) instead of having them delivered to their home. RTRS

Stocks and bonds moved in lockstep for much of 2022, but that relationship has flipped this year. The two asset classes now display the largest negative correlation since August 2020…(WSJ)

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed following the indecisive performance from Wall St where the focus was on the Fed’s SLOOS which showed banks tightened credit terms and demand for loans declined, while the attention in the region shifted to earnings and data releases including mixed Chinese trade figures. ASX 200 was lower with early pressure seen across nearly all sectors and with the top-weighted financial industry choppy after earnings from Australia’s largest lender CBA which reported a slight increase in Q3 cash profit although NII was lower compared to the quarterly average in H1 and the Co. also noted that many customers are feeling the strain of higher interest rates and rising living costs. Nikkei 225 outperformed and reclaimed the 29,000 status, with the index unfazed by weak household spending data as participants digested earnings. Hang Seng and Shanghai Comp. were varied after the latest Chinese trade figures which showed stronger-than-expected export growth but imports disappointed with a surprise contraction.

Top Asian News

EU Ambassador to China thinks the comment by EU’s Borrell suggesting that EU navies patrol the Taiwan Strait has been grossly exaggerated, while he also commented regarding China’s anti-espionage law and consultancy crackdown in which he stated that this is not good news and expressed doubts regarding the compatibility of this policy with the opening up of China’s economy.

Chinese embassy said China strongly condemns and firmly opposes Canada’s decision to expel the Chinese diplomat and has lodged a protest with the Canadian government. China also claimed that Canada ‘sabotaged’ relations and vowed ‘resolute countermeasures’. Subsequently, China said it will expel a Canadian diplomat as a countermeasure.

BoJ Governor Ueda said their scheduled review won’t have any pre-set idea in mind on specific monetary policy moves and said they will take necessary policy action at each meeting with an eye on financial and price developments even while conducting the review. Ueda also commented that if the price target is met in a sustainable manner, the BoJ will end YCC and then shrink its balance sheet, while he added they are seeing some bright signs including on inflation expectations which have heightened and remain at elevated levels.

Australian Budget: Government forecasts 2022/23 budget surplus of AUD 4.2bln (exp. AUD 4bln), 2023/24 budget deficit at AUD 13.9bln (0.5% of GDP), 2024/25 budget AUD 35.1bln (1.3% of GDP). Click here for more detail.

European bourses are softer across the board, Euro Stoxx 50 -0.7%, as the region struggles to find a foothold in relatively quiet trade after a mixed APAC handover. Sectors are similarly softer with Real Estate lagging after soft Halifax data and SBB headwinds; individual movers dictated by earnings updates for Fresenius, Daimler Trucks & more. ES -0.4% dips with the region again lacking firm direction ahead of Fed speak and Biden’s debt ceiling meeting; NQ and RTY roughly in-fitting.

Top European News

ECB’s Kazaks says rate hiking may not be finished in July, via Bloomberg; bets on Spring 2024 ECB cuts are significantly premature. Doing too little remains the greater danger. Not impossible for the ECB to hike/pause in the scenario the Fed is cutting.

ECB’s Kazimir says based on current data, will need to keep raising rates for longer than anticipated; September projections are the earliest time to gauge the effectiveness of measures and see if inflation is heading to target.

Norges Bank Governor Bache says does not need additional policy tools, FX interventions to influence NOK are costly and not very efficient.

German Chancellor Schloz says the EU must reduce risks in China relations without cutting ties saying this is not decoupling, but smart de-risking is the way forward with China.

UK Barclaycard April consumer spending rose 4.3% Y/Y but was impacted by inflation squeeze on disposable incomes and higher food prices, according to Reuters.

FX

Buck finds its feet vs most majors bar the Yen as Treasury yields ease off Monday’s peaks and BoJ Governor Ueda notes higher Japanese inflation expectations.

DXY forms a firmer base around 101.500 and USD/JPY pivots 135.00 where 1bln option expiries roll off at the NY cut.

Aussie retreats as Chinese imports unexpectedly tumble and AUD/USD eyes support into 0.6750 from Monday’s high just over 0.6800.

Euro loses 1.1000+ status vs Dollar and Fib support against Pound as Cable retains underlying bid mostly above 1.2600.

PBoC set USD/CNY mid-point at 6.9255 vs exp. 6.9251 (prev. 6.9158)

Turkey raises the wages of some civil servants by 45%, according to Turkish President Erdogan.

Fixed Income

Choppy trade in bonds, but Bunds piggy-back bounce in Bobls after super-strong 5 year German auction, both holding near intraday highs within 118.34-06 and 135.90-33 ranges.

Gilts lag in catch-up trade after long UK weekend between 100.85-43 parameters.

US Treasuries regroup after Monday’s slump amidst a decline in NFIB business optimism and awaiting Fed commentary ahead of latest debt ceiling talks, T-note near 115-15+ peak vs 115-06+ trough.

Commodities

WTI and Brent are back on a modest downward trajectory after recent positive sessions and yesterday’s Alberta-driven upside; currently, the benchmarks are circa. USD 0.80/bbl lower.

Newsflow has been focused on UAE remarks and Aramco’s update after Chinese trade data was mixed with an unexpected contraction in imports potentially a signal towards weaker demand and a headwind for the complex.

Saudi Aramco Q1 – Saw lower crude oil prices. Major investments advance strategic downstream expansion in key global markets. Global downstream strategy is gaining momentum. 99.7% supply reliability. Believe oil and gas will remain critical components of the energy mix for the foreseeable future. Moving forward with the capacity expansion and long-term outlook remains unchanged.. “Based on the government budget figures the Saudi Government 2023 budgeted revenues are likely based on Brent of ~USD 81/bbl”, according to Al Rajhi Bank cited by Energy Intel’s Bakr.

Spot gold remains underpinned around the USD 2025/oz mark and surrounded by resistance/support marks in relatively close proximity. Base metals are broadly softer, given the mentioned Chinese trade data.

Geopolitics

Head of Russian Wagner Group Prigozhin said that they have not received the promised ammunition after earlier stating that shipments were preliminarily sent, according to Reuters.

US is to provide USD 1.2bln more in long-term military aid to Ukraine to further bolster its air defences, according to US officials cited by AP.

UK Foreign Secretary Cleverly is visiting the US and will hold talks with US Secretary of State Blinken on Tuesday to discuss support for Ukraine, according to Sky News.

US State Department said the US Ambassador to China told Chinese Foreign Minister Qin that there has been no change to US one-China policy, while US Secretary of State Blinken would like to visit China and intends to go when conditions allow.

US Event Calendar

06:00: April SMALL BUSINESS OPTIMISM, 89.0, est. 89.7, prior 90.1

08:30: Fed’s Jefferson Speaks to Atlanta Black Chamber

12:05: Fed’s Williams Speaks to Economic Club of New York

DB’s Jim Reid concludes the overnight wrap

We’re back from the King’s Coronation holiday today. I’ve had more quiche since I last sent the EMR than I’ve had in the previous decade. The weather over the three day weekend was in order; awful, quite nice, awful. Thankfully the big street party was on the sunny day. I’m looking forward to leaving the rain (and the leftover quiche) behind for a couple of days as I escape to Spain. DB is hosting a morning macro outlook event in our Madrid offices tomorrow, with a selection of research speakers, so please reach out to your DB sales coverage if you’d like to attend.

So London returns back to work today between the hotly anticipated US senior loan officers’ opinion survey (SLOOS) last night and US CPI tomorrow.

On the former, the headline numbers were weak but maybe not as bad as feared, but there were plenty of weakness in the report regardless. The headliner saw the net percentage of banks tightening lending standards on commercial and industrial (C&I) loans to medium/large businesses rise to 46% from 44.8% in Q4, and for small banks 46.7% from 44.8%. The medium/large businesses number is still below the peaks observed during the pandemic, GFC, early-2000s and early 1990s but is in recessionary territory. Meanwhile, the percentage of banks reporting stronger demand for C&I loans dropped to 55.6% in Q1 – the lowest level since 2009. Even as demand is lower, the willingness of banks to lend continues to fall. This dynamic was more apparent at smaller lenders, as one would expect.

There was a relatively muted market response to the SLOOS data, as the results were broadly in-line with expectations, or as a minimum didn’t bring any additional fear to the market. US 10yr Treasury yields were already around +6bps higher before the report and finished the day just off their highs to close +7.0bps higher at 3.507%. This morning in Asia, 10yr yields (-1.15bps) are slightly down as we go to press. 2yr yields similarly closed just off their highs, up +8.7bps on the day at 4.001% (-2bps in Asia). The rate selloff came despite minimal movements in Fed pricing. The chance of a rate cut in July fell from 40% to just under 37%, while fed futures are still implying two full 25bp rate cuts by year-end and a better-than-not chance of a third 25bp cut.