MAY 17/2023 · by harveyorgan · in Uncategorized · Leave a comment·Editi

GOLD PRICE CLOSED: DOWN $8.25 TO $1981.30

SILVER PRICE CLOSED: DOWN $0.02 AT $23.74

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1982.90

Silver ACCESS CLOSE: 23.76

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $26,656 DOWN 378 Dollars

Bitcoin: afternoon price: $27,324 UP 290 dollars

Platinum price closing $1075.25 UP $11.05

Palladium price; $1492.00 DOWN $9.05

“Our system is so stinkin’ corrupt that we owe Sodom and Gomorrah an apology.” … Trader Dan Norcini in 2009

GO GATA!

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,666.40 DOWN 12.00 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1587/80 DOWN 5.90 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1829.39 DOWN 1.79 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MAY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,988.400000000 USD

INTENT DATE: 05/16/2023 DELIVERY DATE: 05/18/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 2

363 H WELLS FARGO SEC 1

737 C ADVANTAGE 3

TOTAL: 3 3

JPMorgan stopped 0/3 contracts

FOR MAY:

GOLD: NUMBER OF NOTICES FILED FOR MAY/2023. CONTRACT: 3 NOTICES FOR 300 OZ or 0.009331 TONNES

total notices so far: 5873 contracts for 587,300 oz (18.2674 tonnes)

FOR MAY:

SILVER NOTICES: 0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 2163 for 10,815,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $8.25..

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:///A DEPOSIT OF 0.87 TONNES OF GOLD FROM THE GLD//

INVENTORY RESTS AT 934.94 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 2 CENTS AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV; : INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 469.448 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A VERY STRONG SIZED 992 CONTRACTS TO 140,139 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS STRONG SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.34 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. THIS HAS ALL THE HALLMARKS OF TRADE AT SETTLEMENT (TAS) MANIPULATION WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS IN FULL FORCE DURING MID CYCLE IN THE DELIVERY MONTH. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY: A STRONG 538 CONTRACTS. THE CROOKS LIQUIDATED SOME OF THEIR SHORT END OF THE SPREAD TRADE MANIPULATING THE PRICE OF SILVER SOUTHBOUND!!

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.34). AND WERE SUCCESSFUL IN KNOCKING SOME SPEC LONGS AS WE HAD A SMALL LOSS ON OUR TWO EXCHANGES OF 364 CONTRACTS (SOME OF THIS LOSS WITH HIGH PROBABILITY IS DUE TO TAS LIQUIDATION). WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 4.250 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS( 570 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.105 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 105,000 OZ (E.F.P. JUMP LOWERS THE AMOUNT OF SILVER STANDING)+0 EXCHANGE FOR RISK// TOTAL 4.25 MILLION OZ OF EXCHANGE FOR RISK FOR THE MONTH(RAISES THE AMOUNT OF SILVER STANDING):THUS TOTAL OF 17.135 MILLION OZ OF STANDING FOR DELIVERY V) HUGE SIZED COMEX OI LOSS/ GOOD SIZED EFP ISSUANCE/VI) PROBABLE: SMALL NUMBER OF SHORT T.A.S. CONTRACT LIQUIDATION MANIPULATING THE PRICE DOWN

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -removed 58 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTRACTS for 13 days, total 9914 contracts: OR 49.570 MILLION OZ . (762 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 49.57 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 49.57 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 992 CONTRACTS WITH OUR $0.34 LOSS IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 570 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 13.105 MILLION OZ//FIRST DAY NOTICE FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 105,000 OZ (DECREASES THE AMOUNT OF SILVER STANDING) +// + 0.0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //TOTAL EXCHANGE FOR RISK MONTH= 4.25 MILLION//NEW TOTALS 12.885 MILLION OZ + 4.25 MILLION = 17.135 MILLION OZ// .. WE HAVE A FAIR SIZED LOSS OF 422 OI CONTRACTS ON THE TWO EXCHANGES AS WE HAD SOME TAS LIQUIDATION. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG 570!!

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A HUGE SIZED 14,189 CONTRACTS TO 521,832 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED + 35 CONTRACTS

WE HAD A HUGE SIZED DECREASE IN COMEX OI ( 14,189 CONTRACTS) WITH OUR HUGE $28.05 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR MAY. AT 3.5085 TONNES ON FIRST DAY NOTICE // PLUS 4800 OZ QUEUE. JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)/+ /A HUGE ISSUANCE OF 1000 T.A.S. CONTRACTS//CONSIDERABLE LIQUIDATION OF TAS TODAY////YET ALL OF..THIS HAPPENED WITH OUR HUGE $28.05 LOSS IN PRICE WITH RESPECT TO TUESDAY’S TRADING.WE HAD A VERY STRONG SIZED LOSS OF 10,692 OI CONTRACTS (33.286 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3497 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 521,832

IN ESSENCE WE HAVE A VERY STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,692 CONTRACTS WITH 14,189 CONTRACTS DECREASED AT THE COMEX//TAS CONTRACTS INITIATED: 1000 CONTRACTS) AND 3497 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 10,692 CONTRACTS OR 33.256 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3497 CONTRACTS) ACCOMPANYING THE HUGE SIZED LOSS IN COMEX OI (14,189) //TOTAL LOSS IN THE TWO EXCHANGES 10,692 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 3.5085 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 4800 OZ // NEW STANDING: 18.7713 TONNES // ///3) ZERO LONG LIQUIDATION//4) HUGE SIZED COMEX OPEN INTEREST LOSS/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6/ T.A.S. ISSUANCE: 1000 CONTRACTS AFTER WHICH THEY UNLOADED CONSIDERABLE CONTRACTS.)

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 37,097 CONTRACTS OR 3,709,700 OZ OR 115.38 TONNES IN 13 TRADING DAY(S) AND THUS AVERAGING: 2853 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAY(S) IN TONNES 115.38 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 115.38/3550 x 100% TONNES 3.22% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES ( MUCH SMALLER THAN LAST MONTH)

MAY: 115.38 TONNES (HEADING FOR ANOTHER SMALLER MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A VERY STRONG SIZED 992 CONTRACTS OI TO 140,139 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 570 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 570 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 570 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 992 CONTRACTS AND ADD TO THE 570 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GOOD SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 422 CONTRACTS

THUS IN OUNCES, THE GOOD LOSS ON THE TWO EXCHANGES TOTAL 2.110 MILLION OZ

OCCURRED DESPITE OUR $0.34 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 6.75 PTS OR 0.21% //Hang Seng CLOSED DOWN 417.68 POINTS OR 2.09% /The Nikkei closed UP 250.60 OR 0.84% //Australia’s all ordinaries CLOSED DOWN 0.49 % /Chinese yuan (ONSHORE) closed DOWN 6.9960 /OFFSHORE CHINESE YUAN DOWN TO 7.0140 /Oil UP TO 71.07 dollars per barrel for WTI and BRENT AT 75.01 / Stocks in Europe OPENED MOSTLY RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A HUGE SIZED 14,189 CONTRACTS DOWN TO 521,832 WITH OUR HUGE LOSS IN PRICE OF $28.05 ON TUESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF MAY… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3497 EFP CONTRACTS WERE ISSUED: : JUNE 3497 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3497 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 10,692 CONTRACTS IN THAT 3497 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A HUGE SIZED LOSS OF 14,224 COMEX CONTRACTS..AND THIS GIGANTIC SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE LOSS IN PRICE OF $28.05. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY MONTH, THE TOTAL T.A.S. ISSUANCE: A STRONG 1000 CONTRACTS. THE SHORT SIDE WAS LIQUIDATED TUESDAY AND AGAIN TODAY.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (18.733) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 18.733 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $28.05) //// AND WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD OUR VERY STRONG SIZED LOSS OF 10,692 CONTRACTS ON OUR TWO EXCHANGES BUT I SUSPECT THAT MOST OF THAT LOSS WAS DUE TO LIQUIDATION OF THE TAS.

WE HAVE LOST A TOTAL OI OF 33.256 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY. (3.5085 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 4800 oz (0.1493 TONNES)//NEW STANDING 18.7713 TONNES ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $28.05

WE HAD +added 35 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 10,692 CONTRACTS OR 1,069,200 OZ OR 33.256 TONNES.

Estimated gold comex today 232,467// fair

final gold volumes/yesterday 261,211// FAIR

//MAY 17/ MAY 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil OZ . |

| Deposit to the Dealer Inventory in oz | NIL |

| Deposits to the Customer Inventory, in oz | 10,165.388 oz Delaware |

| No of oz served (contracts) today | 3 notice(s) 300 OZ 0.009331 TONNES |

| No of oz to be served (notices) | 162 contracts 16200 oz 0.538 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5873 notices 587,300 OZ 18.2674 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: NIL oz

customer withdrawals: 0

total withdrawals: nil oz

Adjustments; 0/

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 165 contracts having GAINED 46 contracts. We had 2 contracts filed

on TUESDAY, so we gained 48 contracts or an additional 4800 oz (0.14933 tonnes) will stand for gold in this non active delivery month of May.

June LOST A HUGE 20,710 contracts DOWN to 226,358 contracts. (FROM WHICH A CONSIDERABLE AMOUNT WAS DUE TO TAS LIQUIDATION)

July added 25 contracts to stand at 1770 contracts.

AUGUST GAINED 6210 contracts up to 239,418 contracts (SMALLER ROLL //CONFIRMS TAS LIQUIDATION)

We had 3 contracts filed for today representing 300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 3 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2023. contract month,

we take the total number of notices filed so far for the month (5,873 x 100 oz ), to which we add the difference between the open interest for the front month of MAY (165 CONTRACTS) minus the number of notices served upon today 3 x 100 oz per contract equals 603,500 OZ OR 18.7713 TONNES the number of TONNES standing in this NON- active month of May.

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (5,873 x 100 oz) x 165 OI for the front month minus the number of notices served upon today (3)x 100 oz} which equals 603,500 oz standing OR 18.7713 TONNES

TOTAL COMEX GOLD STANDING: 18.7713 TONNES WHICH IS HUGE FOR A NON ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,666,085.702 OZ 51.822 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,592,643.413 OZ

TOTAL REGISTERED GOLD: 12,401,304.774 (385,73 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,191,336.639 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,735,219 OZ (REG GOLD- PLEDGED GOLD) 333.91 tonnes//

END

SILVER/COMEX

MAY 17//2023// THE MAY 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 169,194.180 oz CNT Delaware Int Delaware JPMorgan . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 600,155.500 oz JPMorgan |

| No of oz served today (contracts) | 0 CONTRACT(S) (nil OZ) |

| No of oz to be served (notices) | 414 contracts (2,070,000 oz) |

| Total monthly oz silver served (contracts) | 2163 Contracts (10,815,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

ii) Into JPMorgan: 600,155.500 oz

Total deposits: 600,155.500 oz

JPMorgan has a total silver weight: 140.724 million oz/271.911 million =51.74% of comex .//dropping fast

Comex withdrawals 4

i) Out of CNT: 5028.280 oz

ii) Out of Delaware 4930.400 oz

iii) Out of int. Delaware: 60,212.850 oz

iv) Out of JPMorgan: 99,022.650 oz

Total withdrawal: 169,194.180 oz

adjustments: 0

TOTAL REGISTERED SILVER: 29.747 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 271.911 million oz

we have now seen the movement of the registered silver comex into the 29 million column:

CALCULATION OF SILVER OZ STANDING FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2023 OI: 413 CONTRACTS HAVING LOST 26 CONTRACT(S). WE HAD 4 CONTRACTS FILED

ON TUESDAY, SO WE LOST 22 CONTRACTS OR AN ADDITIONAL 110,000 OZ WILL NOT STAND FOR DELIVERY ON THIS SIDE OF THE POND AS OUR BANKERS COULD NOT FIND ANY METAL OVER HERE SO THEY WERE E.F.P.d TO LONDON FOR FUTURE DELIVERY.

JUNE HAD A 18 CONTRACT GAIN TO 1060

JULY HAD A 1335 CONTRACT LOSS TO 115,507 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 48,782 poor

Comex volume: confirmed yesterday: 65,994 fair

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 2163 x 5,000 oz = 10,815,000 oz

to which we add the difference between the open interest for the front month of MAY(414) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2023 contract month: 2163 (notices served so far) x 5000 oz + OI for the front month of May (414) – number of notices served upon today (0 )x 500 oz of silver standing for the MAY contract month equates to 12.885 million oz + THE CRIMINAL 0 MILLION OZ EXCHANGE FOR RISK TODAY//NEW TOTAL EXCHANGE FOR RISK: 4.250//NEW TOTAL 17.135 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 937.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 931.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

GLD INVENTORY: 934.94 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

CLOSING INVENTORY 469.448 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

end

end

3,Chris Powell of GATA provides to us very important physical commentaries

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

This is good to watch:

Von Greyerz & Macleod: Insights On The Rotten State Of The Banking System

TUESDAY, MAY 16, 2023 – 08:25 PM

In this discussion between Egon von Greyerz and Alasdair Macleod, on the state of the current banking system and the importance of gold, the speakers express concerns about the system’s eventual collapse due to the excessive creation of “funny money.”

They suggest that gold is the only currency to have survived throughout history and is thus essential for long-term wealth preservation.

Egon and Alasdair also discuss the role of gold in the currency crisis and predict an eventual panic into gold.

Moreover, they stress that the value of gold should not be measured in worthless, fiat money and that higher gold prices are necessary to meet future demand.

Finally, they caution against wishing for the gold price to go up, as it would decrease the quality of life.

Watch the full interview below: https://www.zerohedge.com/markets/von-greyerz-macleod-insights-rotten-state-banking-system

Timestamps:

- 0:00 Introductions

- 0:42 This weeks news – Banking collapse

- 2:32 Derivatives

- 3:07 What’s keeping the gold price high?

- 12:10 Property rights

- 13:30 What role does gold play

- 19:57 Gold price

- 22:44 Influx of wealth preservation

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: PLATINUM

END

end

5 B GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS// WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.9960

OFFSHORE YUAN: 7.0140

SHANGHAI CLOSED DOWN 6.75 PTS OR 0.21%

HANG SENG CLOSED DOWN 417.68 PTS OR 2.09%

2. Nikkei closed UP 250.60 PTS OR 0.84%

3. Europe stocks SO FAR: MOSTLY RED

USA dollar INDEX UP TO 102.11 EURO RISES TO 1.0827 DOWN 39 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.362 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 137.00 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.23000***/Italian 10 Yr bond yield RISES to 4.158*** /SPAIN 10 YR BOND YIELD RISES TO 3.361…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.936

3j Gold at $1985.20 silver at: 23.66 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 46 /100 roubles/dollar; ROUBLE AT 80.856//

3m oil into the 71 dollar handle for WTI and 75 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 137.00 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .362% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8998 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9745 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.522 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 3.836 DOWN 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.0626 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.76…

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 3.817 DOWN 1 BASIS PTS

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

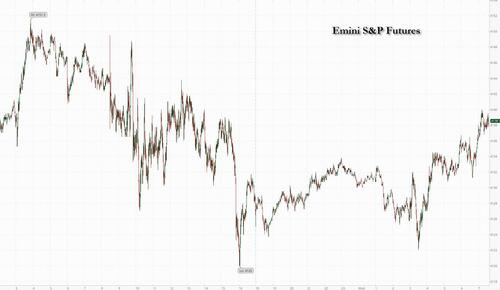

Futures Rise Amid Renewed Hope For Debt Ceiling Breakthrough

WEDNESDAY, MAY 17, 2023 – 08:13 AM

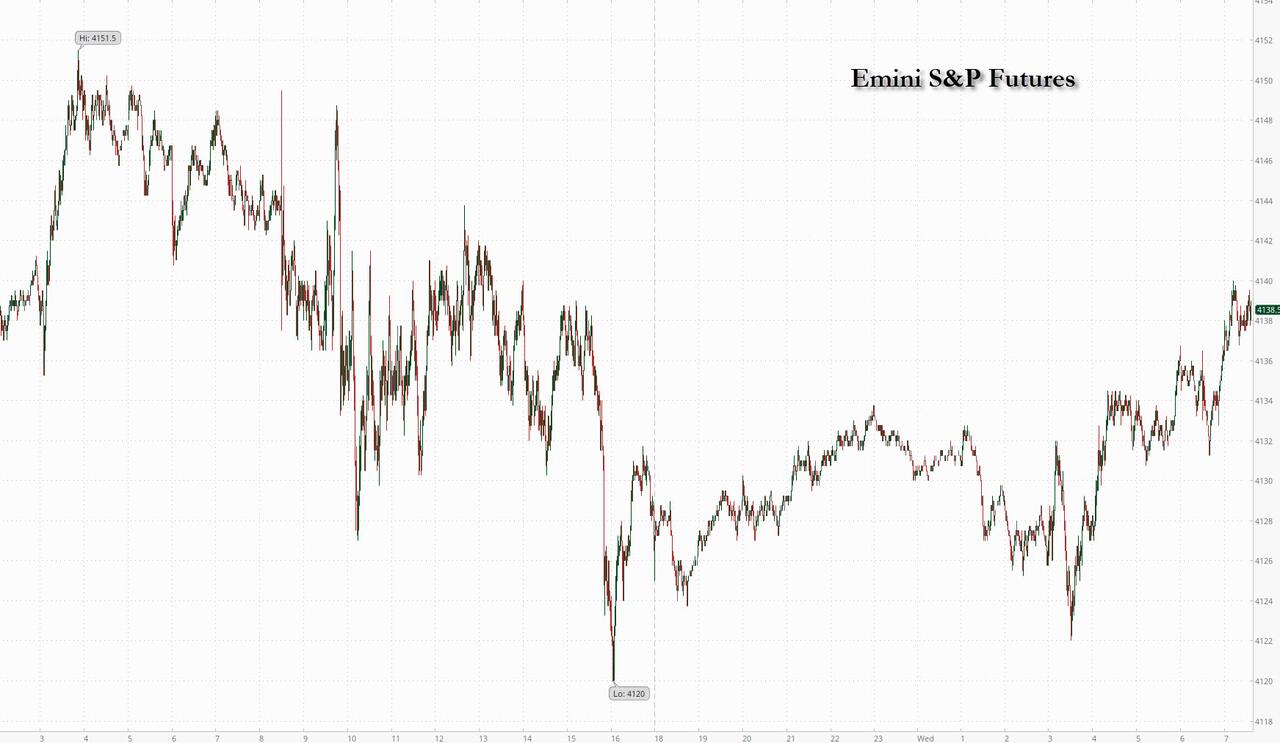

US stock futures crept higher on Wednesday and traded near the best levels of the session, as investors remained focused on debt ceiling talks while negotiators seek a framework agreement for Joe Biden and Kevin McCarthy to review upon the president’s return from a truncated trip to Asia. Contracts on the S&P 500 were up 0.3% as 7:45am ET a.m. while Nasdaq 100 futures added 0.2%. Europe’s Estoxx50 little changed on the day; while Japan’s Nikkei 225 closed above the 30,000 for the first time since September 2021 a day after the Topix closed at its highest level in more than three decades. Treasuries are slightly richer across the curve with spreads broadly within 1bp-2bps of Tuesday’s close while the dollar is flat. Oil rebounded from an earlier drop concerns over demand in China and expectations of rising stockpiles in the US. Iron ore continues its week in the green, while gold and bitcoin declines.

In premarket trading, Western Alliance Bancorp jumped as much as 9.8% after the regional lender reported growth in deposits this quarter, soothing concerns after it was caught up in the turmoil engulfing the US regional banking sector. Tesla rose as much as 1.7% in premarket trading on Wednesday, as CEO Elon Musk said the electric-car maker will “try a little advertising and see how it goes.” This is a major shift for the company that’s largely avoided traditional marketing to sell its vehicles. Manchester United gained after Bloomberg reported that Sheikh Jassim Bin Hamad J.J. Al-Thani submitted an improved offer for the football club. Here are some other notable premarket movers:

- Doximity drops as much as 11% in premarket trading on Wednesday, after the health-care software company gave a weaker-than-expected 1Q forecast due to delayed product launches. Analysts note that the outlook puts a lot of pressure on the company to ramp in the second half of the year.

- Gates Industrial Corp. declined 1.4% postmarket after leading holder Blackstone offered 22.5 million shares via Citigroup, Evercore ISI, Goldman Sachs.

- Maxeon Solar Technologies dropped 6% postmarket after the solar-panel maker offered 5.1 million shares and leading holder TotalEnergies offered an additional 1.7 million via BofA Securities, Morgan Stanley.

- Intapp Inc. fell 5.2% postmarket after the software company offered 2 million shares and selling stockholders offered 4.25 million via BofA Securities, Barclays.

- Container Store tumbled 17% in post-market trading Tuesday after its full- year net sales forecast fell short of the average of analysts’ estimates.

- Vivid Seats dropped 12% postmarket as selling stockholder Hoya Topco LLC offers 16m Class A shares via Citigroup, Morgan Stanley.

A rally that lifted global stocks by almost 9% this year through the end of April reversed this month as the debt-ceiling standoff compounded fears about an economic slowdown and outweighed a better-than-feared corporate earnings season. “That is leading to the reason why equity markets have stalled over the last couple of weeks because you are not really paid now to make big bets ahead of this event,” Grace Peters, JPMorgan Private Bank’s head of investment strategy, said in an interview with Bloomberg TV.

Still, the calm in equity indexes “hides a lot of movement under the surface,” said Marija Veitmane, senior multi-asset strategist for State Street Global Markets.“Our favorite trade is preference for growth stocks over value as we believe that recession is inevitable so earnings are likely to falter, while growth should get some support from falling rates.”

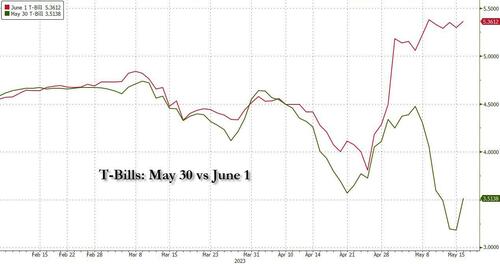

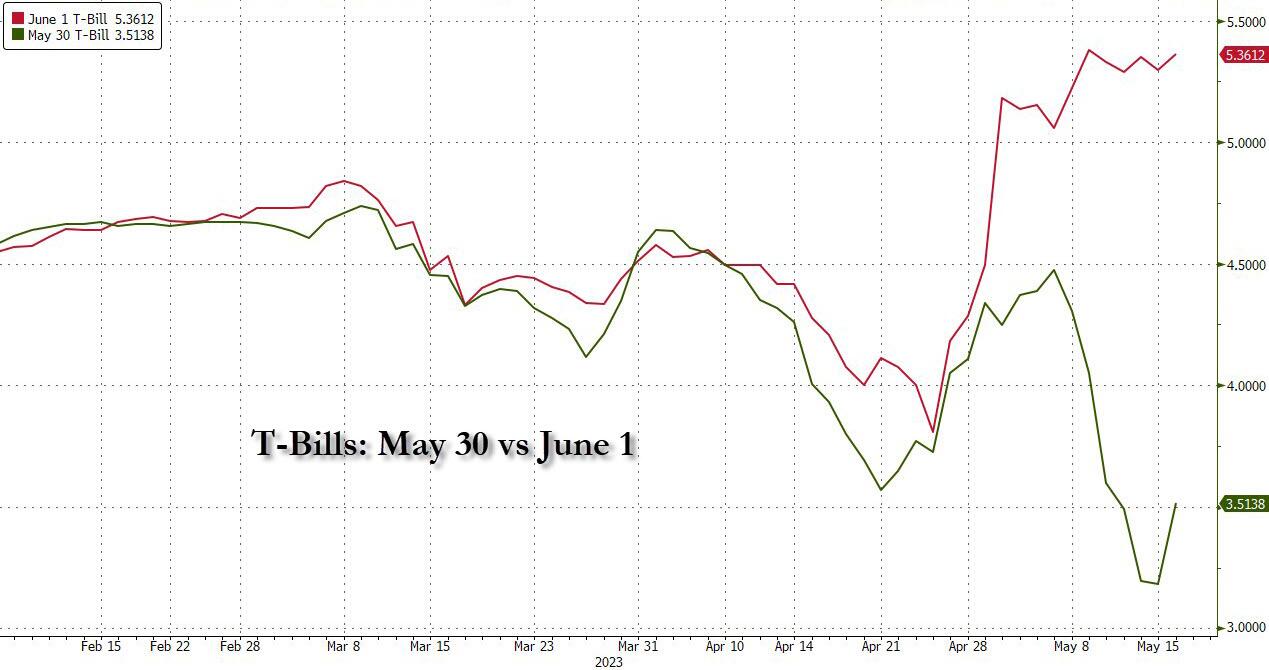

Negotiators are seeking a framework agreement to review upon President Joe Biden’s return from a truncated trip to Asia. Any breakthrough in the talks would give markets cause to rally, dissipating one of the biggest tail risks weighing on sentiment. “Longer term, that would be a dip that we would buy if that were to come to pass,” Peters said. “The market does ultimately I think assume this will get resolved.” In the meantime, Treasury bills maturing after June 1 are under pressure, as costs to insure Treasuries in the credit-default swap market surge.

Meanwhile, strategists at Goldman Sachs Group said artificial intelligence offers the biggest potential long-term support for US profit margins, although they warned there’s high uncertainty around AI’s impact. AI can boost net margins by nearly 400 basis points over a decade, strategists led by Ben Snider wrote in a note.

European stocks are slightly lower as risk sentiment struggles to gain any real traction with US debt ceiling negotiations making only glacial progress. The Stoxx 600 is down 0.1% with real estate, financial services and retail the worst performing sectors while miners and travel stocks rise. Here are the most notable European movers:

- Argenx shares rise as much as 5.8% after Bloomberg reported several major drugmakers keen to expand in immunology have been studying the biotech and have it at the top of their wish lists

- Aegon shares climb as much as 5.6% after the Dutch insurance company’s 1Q capital generation before holdco costs beat consensus expectations, suggesting modest consensus upgrades, Citi says

- SAP shares rise as much as 1.9% after the software giant projected sales growth to accelerate beyond 2025, a bullish ambition as the firm’s transition to cloud bears fruit, according to analysts

- Watches of Switzerland shares fall as much as 12%, to the lowest since September 30, after the top seller of Rolex timepieces in the UK said it expects a decline in first-quarter sales

- Commerzbank declines as much as 7.9%, worst performer on the Stoxx 600 Banks Index, as analysts say an increase in guidance for FY net interest income is not enough, as it only matches consensus

- Experian shares decline as much as 5.7%, reaching the lowest since March, after the consumer credit reporting company’s organic revenue forecast for the year failed to match expectations

- British Land declines as much as 5.1% after the landlord’s FY results showed net asset values for the group fell more than expected. Jefferies noted the decline was worse than for rival Land Securities

- Ubisoft shares sink as much as 11% after the French video-game company’s quarterly bookings and outlook for the current quarter came in well below expectations

- Euronext shares decline as much as 5.5% as analysts point to limited room for consensus change after the French stock-market operator offered no adjustment to 2023 cost guidance

- JD Sports drops as much as 5.2% after the sports retailer reported a FY gross profit margin that missed estimates. RBC flagged the gross profit margin being below their expectations

- Zurich falls as much as 3.6% after the insurer’s presented “relatively solid” quarterly figures, with Jefferies flagging some weakness in its Farmers division and Vontobel notes a miss on Solvency

Elsewhere, the greenback remains on the front foot with the Bloomberg Dollar Spot Index rising 0.3% to its highest in over five weeks. Bunds and gilts are on the front foot with German and UK 10-year yields falling by 4bps and 3bps respectively.

Earlier in the session, Asian stocks retreated as weaker-than-expected data from China continued to weigh on sentiment concerning the country’s economic growth outlook. The MSCI Asia Pacific Index fell as much as 0.5%, with AIA Group, Meituan and Ping An Insurance Group the biggest drags. Shares in Hong Kong were the region’s worst performers after disappointing factory output and jobless data yesterday. Key gauges in Japan, Taiwan and South Korea rose. The Hang Seng Index declined 2.1%, the most in a week, dragged lower by property and technology stocks. Tencent, which ended down 0.6%, saw large fund net outflow before its earnings report came after the market closed.

Japanese stocks gained for a fourth day after a better-than-expected GDP report, with the Nikkei 225 closing above the 30,000 for the first time since September 2021 a day after the Topix closed at its highest level in more than three decades. The Topix Index rose 0.3% to 2,133.61, while the Nikkei advanced 0.8% to 30,093.59. Mitsubishi UFJ Financial Group Inc. contributed the most to the Topix Index gain, increasing 2.2%. Out of 2,159 stocks in the index, 900 rose and 1,161 fell, while 98 were unchanged. “It’s fascinating time to be looking at the Japanese equity market at the moment,” said Bruce Kirk, Chief Japan Equity Strategist at Goldman Sachs, on Bloomberg TV. “What we are seeing is a perfect alignment between the interests of the government, the regulator, the exchange, and also the investors, both foreign and domestic.”

Meanwhile commodity-heavy Australian stocks continued their decline, as the S&P/ASX 200 index fell 0.5% to close at 7,199.20, weighed by mining shares and banks. Australian salaries rose at around half the pace of inflation in the first three months of 2023, suggesting the economy will avoid a wage-price spiral and bolstering the case for the central bank to stand pat in June. Read: Australia Pay Gains Suggest Economy to Avoid Wage Breakout In New Zealand, the S&P/NZX 50 index was little changed at 11,951.66

Stocks in India also dropped for a second session as investors continued to book profits after a recent rally in the key gauges. The S&P BSE Sensex fell 0.6% to 61,560.64 in Mumbai, while the NSE Nifty 50 Index posted a similar decline to close at 18,181.75. Stocks in the benchmark gauges are trading at 19.2 times their estimated earnings for the next 12 months, close to the 5-year average of 19.8x. Infosys contributed the most to the index’s decline, decreasing 1.3%. Out of 30 shares in the Sensex index, 7 rose and 23 fell

In FX, the Bloomberg Dollar Spot Index rose 0.3% to 1234.32 as the greenback rallied to a two-week high of 137.17 yen. In quiet trade, the dollar gained against all G10 currencies bar the New Zealand dollar, which rose as much as 0.4% to 0.6253. The yuan slid past the key level of 7 per dollar for the first time this year in a further sign the recovery of the world’s second- largest economy from its Covid restrictions is grinding to a halt; the offshore yuan slipped as much as 0.3% to 7.0201 per dollar, while the onshore currency dropped as much as 0.4% to 7.0026.

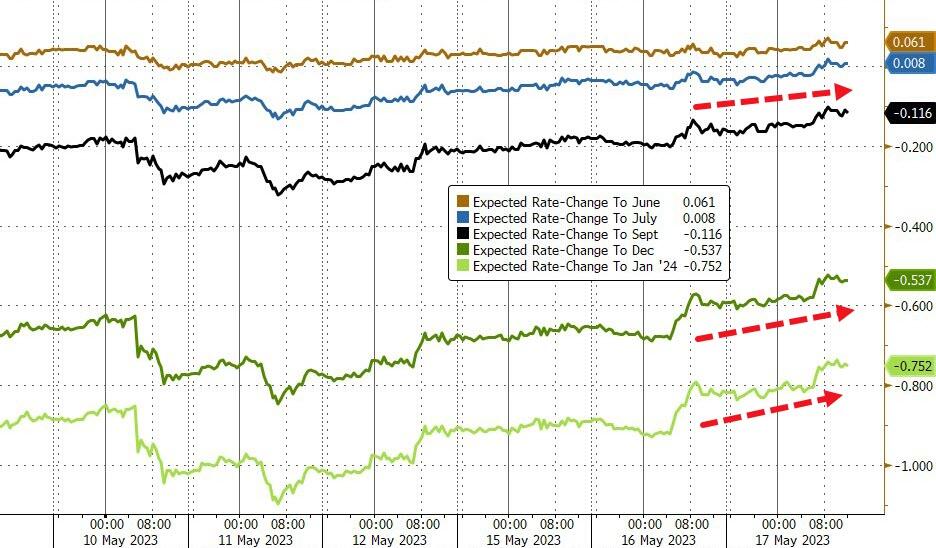

In rates, treasuries are slightly richer across the curve with spreads broadly within 1bp-2bps of Tuesday’s close. 10-year yields are around 3.515%, richer by ~2bp on the day, with bunds and gilts outperforming by 3bp and 1.5bp in the sector. The two-year Treasury yield rose 2 basis points to 4.10%, after climbing as high as 4.12% on Tuesday; Treasuries remained pressured after Fed officials appeared divided on whether to raise rates or pause its tightening cycle. Traders are betting on the possibility that the Fed will keep rates on hold at 5.25% at its June meeting; they are pricing around 19 basis points in cuts in September, and a total of around 60 basis points of cuts by year-end.

Bigger gains remain in core European rates after a strong 10-year German bond auction, which produced highest demand since August 2020. US session features 20-year bond sale at 1pm New York time. For $15b 20- year bond auction, WI yield ~3.945% is 2.5bp cheaper than April’s stop-out, which tailed the WI by 0.2bp. IG issuance slate empty so far; Pfizer priced a $31b deal Tuesday, the 4th largest on record, while energy producer Ovintiv issued a $2.3b offering; Pfizer offered investors upwards of 20bps in new-issue concessions

In commodities, crude futures decline with WTI down 0.2% to trade near $70.70. Spot gold falls 0.2% to around $1,985. Bitcoin drops 0.4%.

UK MPs have warned that trading in Bitcoin and other speculative crypto assets should be regulated to prevent consumers from being lulled into a false sense of security about the risks posed, according to The Times.

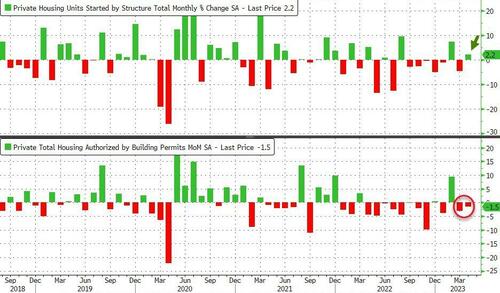

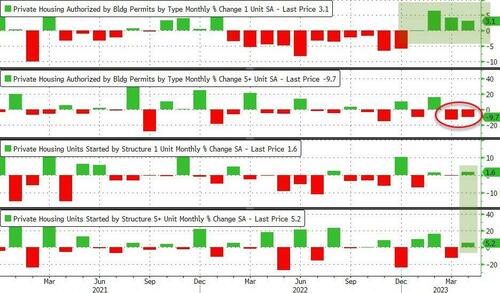

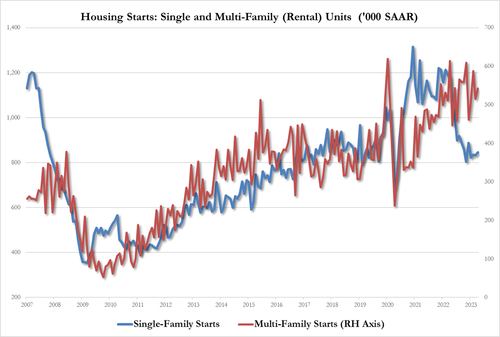

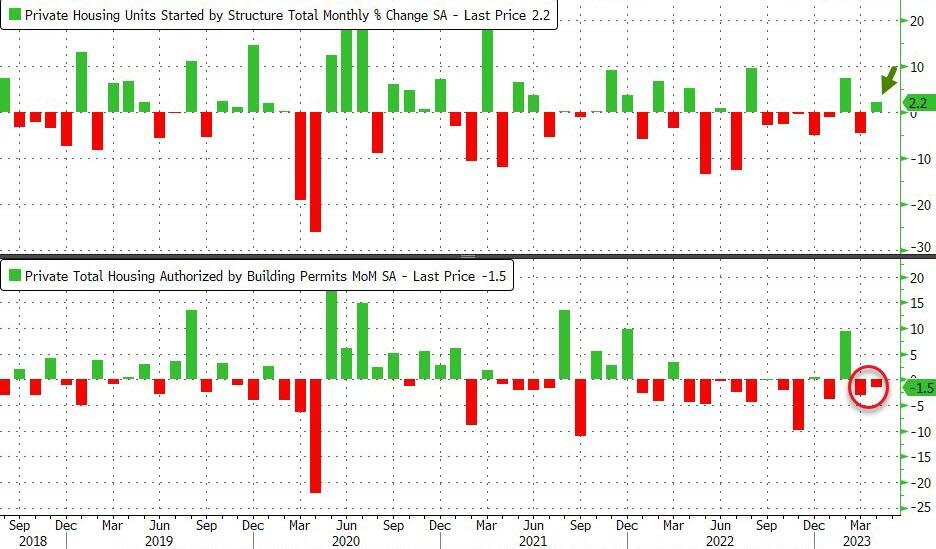

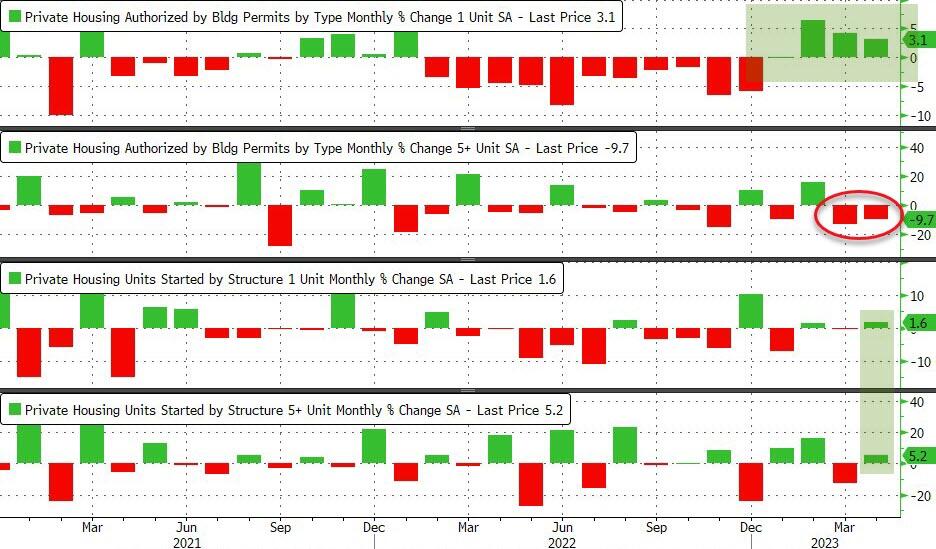

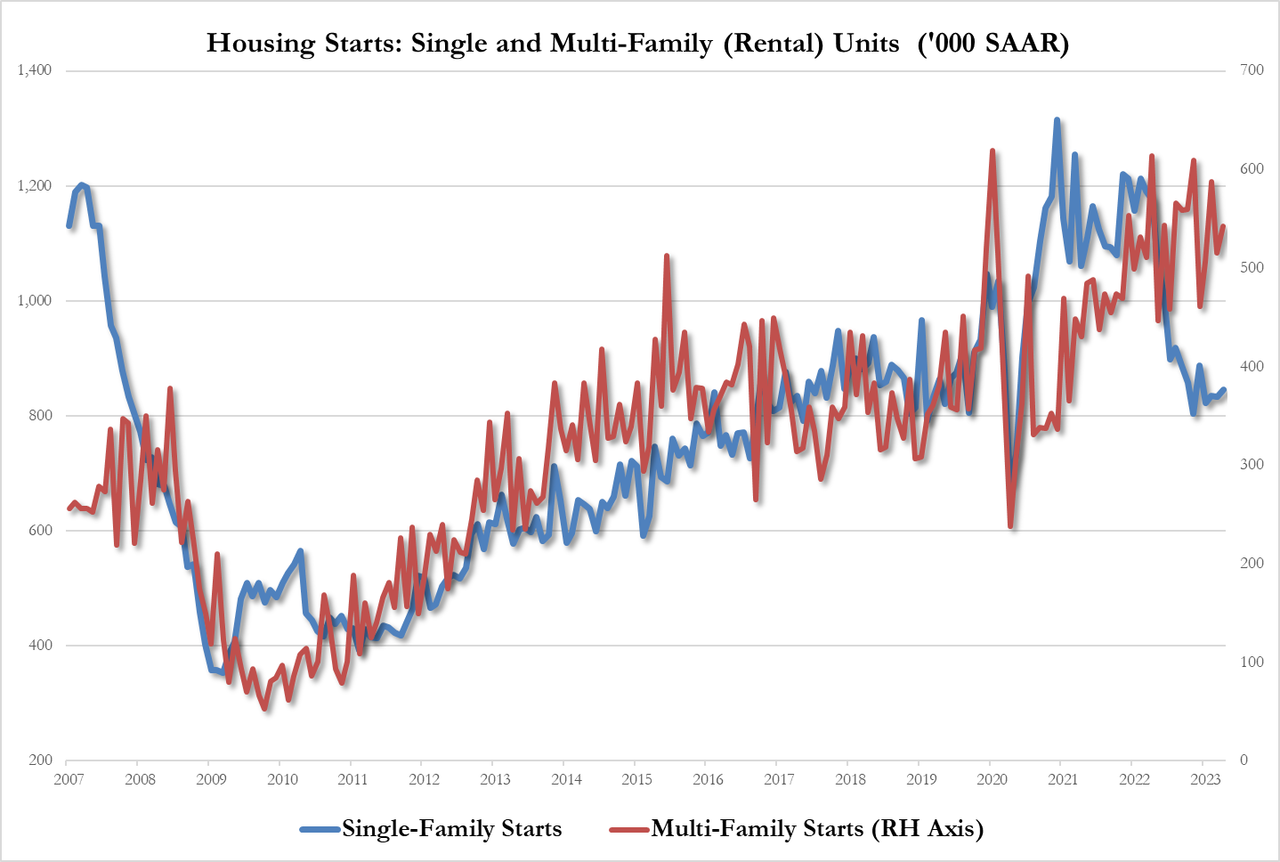

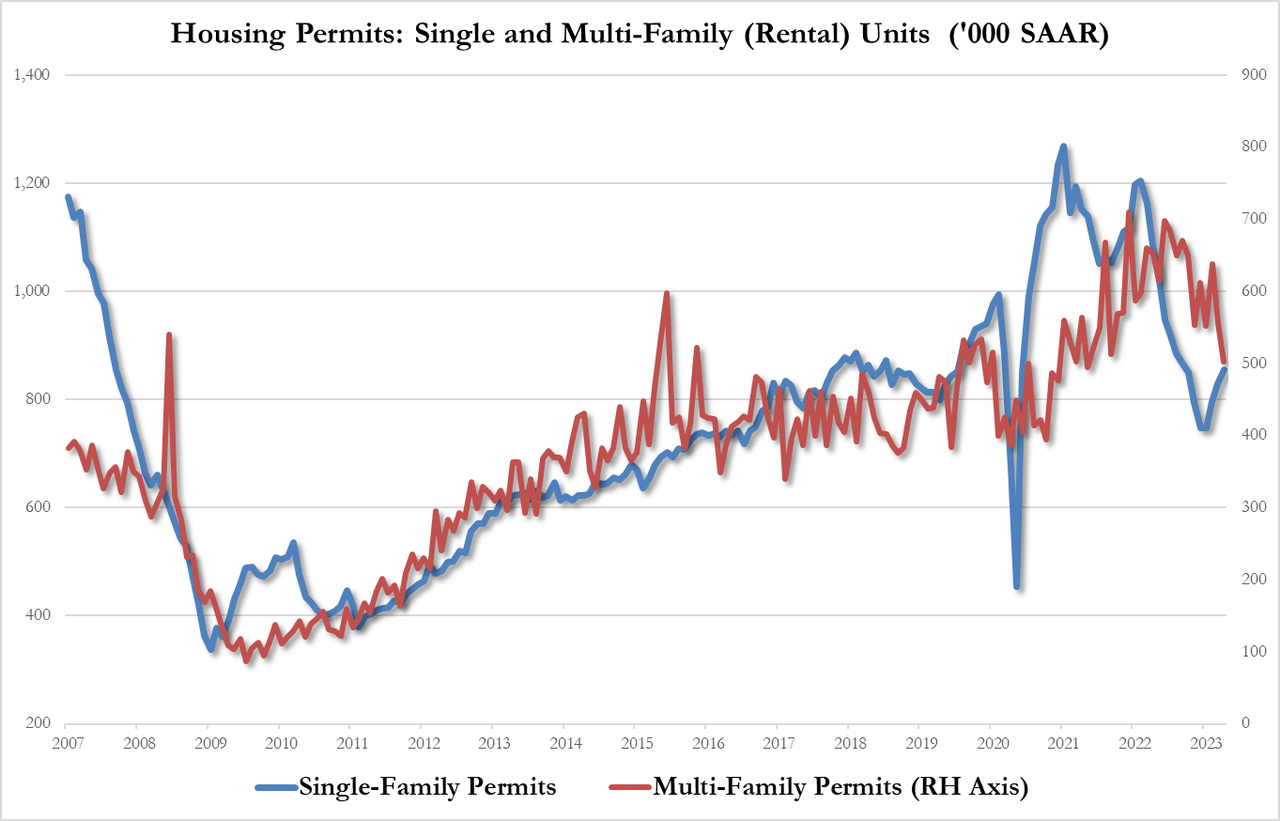

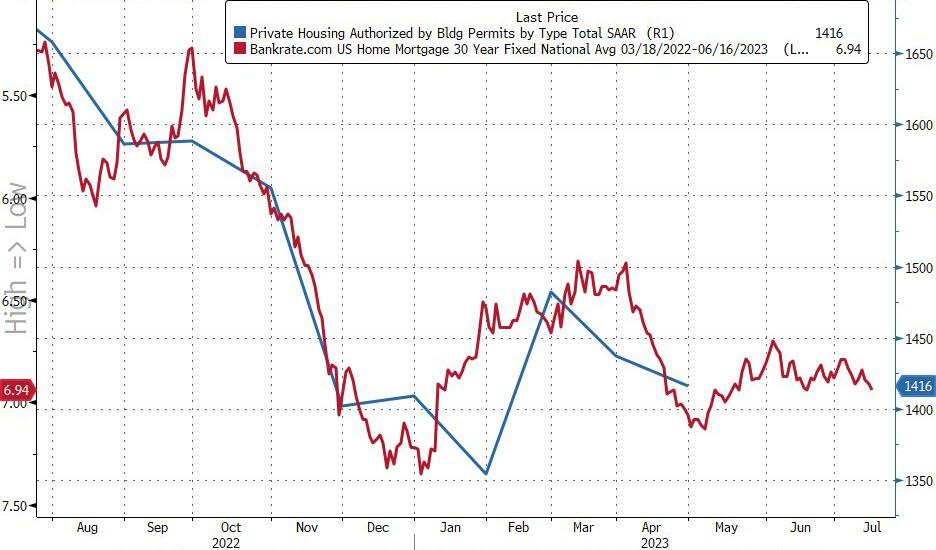

Looking to the day ahead now, data releases include US housing starts and building permits for April, along with the final CPI print for April from the Euro Area. From central banks, we’ll hear from BoE Governor Bailey, ECB Vice President de Guindos, along with the ECB’s de Cos, Elderson, Centeno and Rehn. Finally, earnings releases include Target and Cisco.

Market Snapshot

- S&P 500 futures up 0.3% to 4,133.50

- MXAP down 0.4% to 161.25

- MXAPJ down 0.6% to 510.86

- Nikkei up 0.8% to 30,093.59

- Topix up 0.3% to 2,133.61

- Hang Seng Index down 2.1% to 19,560.57

- Shanghai Composite down 0.2% to 3,284.23

- Sensex down 0.8% to 61,445.80

- Australia S&P/ASX 200 down 0.5% to 7,199.24

- Kospi up 0.6% to 2,494.66

- STOXX Europe 600 down 0.1% to 464.11

- German 10Y yield little changed at 2.33%

- Euro down 0.2% to $1.0843

- Brent Futures down 0.3% to $74.67/bbl

- Gold spot down 0.1% to $1,986.63

- U.S. Dollar Index up 0.28% to 102.85

Top Overnight News from Bloomberg

- Japan’s Q1 GDP comes in solidly above the Street consensus at +1.6% (the Street was modeling +0.8%) thanks to strong consumer spending. WSJ

- China’s new home prices for April comes in +0.32% M/M, down from the +0.44% number posted in March. WSJ

- UBS projects a massive accounting gain from its takeover of Credit Suisse, with the combined firms’ “negative goodwill” seen boosting reported profit by $34.8 billion. On the downside, UBS estimates litigation, regulatory matters and related liabilities may take $4 billion out of capital over 12 months. BBG

- House Democrats plan to begin collecting signatures Wednesday for a discharge petition to raise the debt ceiling, a long-shot parliamentary maneuver designed to circumvent House Republican leadership and force a vote. WSJ

- US oil/gas drilling is starting to dip amid subdued prices, creating headwinds for the equipment industry (and potentially leading to higher energy prices down the board). FT

- The FTC’s lawsuit to block AMGN-HZNP is the first time in more than 10 years that the gov’t has tried to stop a drug merger (the FTC warned on Tues that “rampant consolidation” in the industry was pushing up prices). FT

- Western Alliance provided some encouraging statistics around deposit dynamics. Overall deposits stabilized during the final days of March and have resumed a growth trajectory since. QTD deposit growth is north of $2B as of May 12. In addition, insured deposits are now nearly 80% of the total, while the company is making progress repositioning its balance sheet. RTRS

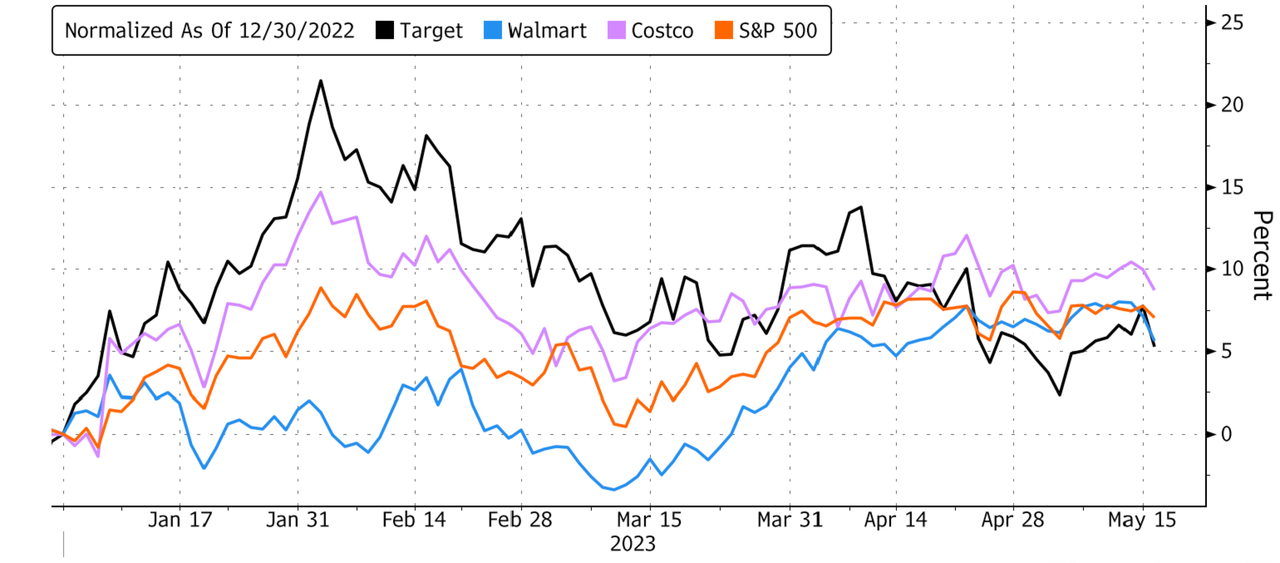

- TGT: Stock is down in the pre-market on the 2Q guide but our desk thinks they did what they needed to do with 1Q good enough and 2Q possible conservative (we’ll see more on that from the call). 2Q EPS of $2.05 vs Consensus $1.77 and EBITDA 12% better. Total sales were in-line, with comps of 0% (traffic was +0.9% vs Consensus +1% (bogey was for around a 0% to +0.5%, so this was about in-line and while nothing special, is no worse than feared). Gross margins missed by 40 bps but SG&A beat by a sizeable 150 bps. Guided 2Q EPS below at $1.30-$1.70 (Consensus $1.91) and comps of down low-singles (Consensus +0.2%). Encouragingly, inventory down 17% y/t vs -3% last quarter, reaffirming the FY guide, which could be considered a bit conservative after today’s beat (but early to say). H/T Scott Feiler

- Tesla’s CEO Elon Musk said the electric-car maker will dabble in advertisements, a major shift for the company that’s largely avoided traditional marketing. “We’ll try a little advertising and see how it goes,” Musk said Tuesday at Tesla’s annual shareholder meeting, in response to an investor’s question. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed with the region cautious after the weak handover from the US where risk appetite was clouded amid debt ceiling concerns, while the meeting between US President Biden and congressional leaders achieved no major breakthroughs although was said to be productive and has set the stage to carry on further conversations. ASX 200 was subdued amid losses across nearly all sectors and following mixed wage price index data. Nikkei 225 outperformed and climbed above the 30,000 level for the first time since September 2021 with sentiment also underpinned by stronger-than-expected Japanese GDP data. Hang Seng and Shanghai Comp. were lower with price action contained amid a lack of fresh macro catalysts to detract from the recent streak of disappointing data releases from China.

Top Asian News

- Chinese embassy spokesman said the visit to Taiwan by former UK PM Truss this week is a dangerous political show which will do nothing but harm to the UK, according to The Guardian.

European bourses are in close proximity to the unchanged mark, Euro Stoxx 50 +0.1%, with fresh drivers somewhat limited and following a mixed APAC session though one that feature marked Nikkei 225 outperformance, above 30k. Within Europe, the DAX 40 +0.3% outperforms after heavyweight Siemens’ (+2.0%) Q2 update alongside strength in SAP (+1.6%) following a guidance update and buyback announcement; in contrast, Financial Services are pressured by LSE and Euronext while Commerzbank is the Banking sector laggard. Stateside, futures are modestly firmer in generally horizontal trade with the ES +0.1% around 4130 ahead of debt ceiling updates with the overnight developments slightly constructive but the impasse ultimately remains. Tencent (700 HK): Q1 2023 (CNY): Revenue 149.99bln (exp. 146.29nlm). Net 32.5bln (exp. 33.2bln), Operating 40.43bln (exp. 40.7bln); Weixin and Wechat MAUs 1.32bln (exp. 1.32bln).

Top European News

- The Royal United Services Institute think tank warned that UK PM Sunak will have to find USD 42bln in tax hikes and spending cuts to pay for his pledge to boost defence spending to 2.5% of GDP, according to The Mirror.

- The Resolution Foundation has warned that the BoE’s decision to hike interest rates could limit Chancellor Hunt’s room to lower taxes in the Autumn, according to The Times.

- UK Labour opposition leader Keir Starmer calls for the UK’s current Brexit deal to be renegotiated, but declares the UK must not re-join the EU or single market, according to Sky News.

- ECB’s de Cos says the ECB is getting near the end of its tightening cycle; transmission remains strong.

- ECB’s Rehn says need to see core CPI slow substantially.

- BoE Governor Bailey says “If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required.”. MPC pays particular attention to indicators of inflation persistence, including labour market tightness and wage growth, and services price inflation. There are signs that the labour market is loosening a little.

FX

- DXY tops 103.000 amidst broad gains mainly forged at the expense of the Yuan.

- USD/CNY probes 7.0000 and USD/CNH approaches Fib at 7.0364 after a spate of disappointing Chinese data.

- Yen under 137.00 vs Dollar and relying on 200 DMA for a reprieve, Sterling sub-1.2450 and relatively unaffected by BoE’s Bailey.

- Euro teeters above Fib in the low 1.0800 zone.

- PBoC set USD/CNY mid-point at 6.9748 vs exp. 6.9750 (prev. 6.9506).

Fixed Income

- Firm bounce in core EU bonds and strong demand for supply along the way.

- Bunds and Gilts are both towards the top of ranges extending to 135.82 and 100.83 from 135.28 and 100.41 respectively.

- USTs relatively restrained with T-note tethered to 115-00 ahead of US housing data and USD 15bln 20-year sale.

Commodities

- Crude benchmarks are essentially unchanged after drifting in the first half of the session as the USD picked up and sentiment slipped; a narrative that has eased/lifted from respective session peaks since.

- Currently, WTI and Brent are incrementally firmer within circa. USD 1/bbl parameters with specific newsflow light and focus on geopols. amid reports that Iran’s Economy Minister discussed oil and gas projects with Saudi Arabia, according to Bloomberg.

- Spot gold is drifting with the USD firmer and sentiment improving throughout the morning, yellow metal below USD 2k/oz and approaching the USD 1981/oz 50-DMA.

- Base metals are more mixed, with the region attempting to recoup some of the recent China-induced pressures but with action capped on USD strength.

- US Energy Inventory Data (bbls): Crude +3.7mln (exp. -0.9mln), Gasoline -2.5mln (exp. -1.1mln), Distillate -0.9mln (exp. +0.1mln), Cushing +2.9mln.

- UBS lowers Year-End Brent forecast by USD 10/bbl to USD 95/bbl amid greater-than-expected supply.

Debt Ceiling latest

- US President Biden said they had a good, productive meeting on the debt ceiling and there is still more work to do, while he made it clear to House Speaker McCarthy that they will talk regularly over the next several days. Biden is confident they will continue to make progress on avoiding default and said that defaulting on debt is not an option, while he also noted it is disappointing Republicans refuse to consider raising revenue, according to Reuters.

- White House said President Biden directed staff to meet daily on outstanding issues and said he would like to check in with leaders later this week by phone and meet with them upon return from overseas. Biden also emphasised that while more work remains on a range of difficult issues, he is optimistic that there is a path to a budget agreement, according to Reuters.

- President Biden will no longer visit Australia or Papua New Guinea and will return to the US on Sunday to focus on the debt ceiling talks, according to NBC.

- US House Speaker McCarthy said they have set the stage to carry on conversations in debt talks and that President Biden agreed to appoint a couple of people from the administration to negotiate directly with his team. McCarthy also said there is a lot of work to do in a short amount of time and that they are still very far apart but added it is possible to get a deal by the end of the week and it is not that difficult to reach an agreement. However, McCarthy later said he is not more optimistic about getting a deal by the end of the week.

- US Senate Majority Leader Schumer said the debt meeting was good and productive, while he added that they all agreed a default is a horrible option, according to Reuters.

- US Senate Republican Leader McConnell earlier told Senate Republicans there had not been much progress on debt ceilings talks with POTUS and other leaders.

- House Democrats are to reportedly begin collecting signatures for effort to raise debt ceiling, according to WSJ.

- Punchbowl on the US debt limit, says “Initial discussions began Tuesday night, with full-scale negotiations set to kick off this morning, we’re told”, “Sources close to the talks expect any debt-limit boost to run well into 2025.”

Geopolitics

- Russia’s Kremlin says it will not enter a hypothetical discussion on what Russia will do if the grain deal lapses.

DB’s Jim Reid concludes the overnight wrap

Yesterday Henry and I published a chartbook entitled “A Time Capsule for the Future”. It imagines how those in the distant future might look at what the macro signals were telling us now in May 2023. Would it be obvious in hindsight as to what happened next? For us, this has been the most predictable US cycle of our careers from the moment the US money supply exploded. From then it wasn’t difficult to predict we’d get very high inflation, and from then that central banks would have to hike rates aggressively. The next stage continues to look clear to us: given aggressive rate hikes and curve inversions, we think there’ll be a US recession rather than a soft landing. Indeed, just about every leading indicator is now pointing to one. Does it look as obvious to you? Will future historians digging up this time capsule say the same thing? Or what are we not seeing that might prove us wrong? We’d be interested in hearing your views, especially those of you from the future! The presentation is here and tomorrow we’ll be hosting a webinar on it at 2:30pm London time. Please Register Here if you want to view.

Markets had a slightly tough session yesterday, as robust data and hawkish comments from Fed officials helped drive a selloff across bonds (mostly) and equities (a bit). Having said that the market was really waiting for the results of the latest meeting on the debt ceiling between President Biden and congressional leaders starting an hour before the US close. House Speaker McCarthy continues to say the two sides remain far apart. However, he acknowledged that “it is possible to get a deal by the end of the week” despite there being a lot of work to do. He also noted that the talks were “more productive” than previous meetings and that a smaller group of staffers from both sides are working toward a deal, with talks commencing as soon as tonight. President Biden announced that there was “consensus, I think, among the congressional leaders that defaulting on the debt is simply not an option.” Senate leadership from both parties exhibited optimism that a deal could be reached as well. Before the meeting even started there was news that President Biden was going to shorten his upcoming trip to Asia and return to Washington on Sunday after the G-7 meeting in Japan. This highlights the seriousness around Treasury Secretary Yellen’s June 1st deadline.

Ahead of the meeting, Treasuries had already been hurt by a collection of strong data releases, which knocked hopes among investors that rates would be cut later this year. For instance, retail sales (excluding auto and gas) were up by +0.6% in April (vs. +0.2% expected) following two consecutive monthly declines. Then industrial production grew by +0.5% in April (vs. unch expected), whilst the NAHB’s housing market index rose for a 5th month running to 50 (vs. 45 expected).

With those releases in hand and the hawkish Fed-speak discussed below, investors grew more doubtful that the Fed would pivot towards rate cuts this year, and the rate priced in for the December meeting was up +7.4bps on the day to 4.484%. In turn, that helped spur a rise in Treasury yields across the curve, with the 10yr yield up +3.2bps to 3.534% and 2yr yields +7.2bps higher. Meanwhile the 30yr yield was up +1.2bps at 3.854%, marking its highest level since March 8, just before SVB’s collapse led to market turmoil. Having said that yields are 1-2bps lower across the curve in Asia.

Before the slight rally back in Asia, the losses for Treasuries were given added support from various Fed speakers, whose tone was generally on the hawkish side. First, we had Cleveland Fed President Mester, who said that rates weren’t sufficiently restrictive just yet, and that “given how stubborn inflation has been, I can’t say that I’m at a level of the fed funds rate where it’s equally probably that the next move could be an increase or a decrease”. Later on, Richmond Fed President Barkin said that “if more increases are what’s necessary” to reduce inflation then he was “comfortable doing that.”

New York Fed President Williams said the committee was still waiting for the long lags of monetary policy while also noting that inflation is still “too high”. He did say that he sees supply-demand imbalances improving throughout the economy. Chicago Fed President Goolsbee reminded the market that service inflation remains too high and that “its far too premature to be talking about rate cuts.” Lastly, Dallas Fed President Logan tried to walk the line between the hawks and doves saying that gradual policy adjustment can help mitigate stability risks and that justifies the Fed slowing the pace of hikes or outright pausing.

This combination of news meant that equities struggled yesterday, with the S&P 500 (-0.64%) reversing its gains from the previous session and close near its lows on the day. The declines were generally broad-based (88% of the index lower), but tech stocks were the exception and saw the NASDAQ outperform slightly (-0.18%) . That was aided by a strong advance from the megacap stocks, with the FANG+ index rising +0.97% yesterday in a big outperformance. The latest moves further showcase just show top-heavy the equity gains have been this year. Indeed, the S&P 500 is up by +7.04% on a YTD basis, but the equal-weighted S&P 500 is now down -0.80% since the start of the year.

Back in Europe, markets followed a broadly similar pattern to the US, with the STOXX 600 down -0.42%, whilst yields on 10yr bunds (+4.4bps), OATs (+5.1bps) and BTPs (+3.5bps) all moved higher. Sentiment wasn’t helped by the latest ZEW survey from Germany, where the expectations component fell for a 3rd consecutive month in May to -10.7 (vs. -5.0 expected), so further reversing the more positive sentiment we saw around the turn of the year. On the other hand, there was some further good news from natural gas prices, which fell -1.53% to another 22-month low of €31.82/MWh.

Elsewhere, UK gilts were an outperformer yesterday following signs that the labour market might be softening. In particular, the number of payrolled employees unexpectedly fell by -136k in April (vs. +25k expected), which marked the first monthly decline in that measure since February 2021. Furthermore, the unemployment rate over the three months to March rose a tenth to 3.9% (vs. 3.8% expected). See our economist’s view on the data here. The release meant investors slightly downgraded the likelihood of a rate hike at the BoE’s next meeting in June, with the chances down to 78%, having been at 85% the previous day.

It was the reverse story in Canada, with 10yr yields up by +17bps after the country’s CPI reading unexpectedly rose in April. That showed inflation rising to +4.4% (vs. +4.1% expected), which ended a run of 5 consecutive monthly declines in headline inflation. In turn, investors dialled up the chances that the Bank of Canada might hike rates at the next meeting following their recent pause, with overnight index swaps now seeing a 35% chance of another 25bp move in June.

Asian equity markets are mixed this morning as US debt negotiations continue. Across the region, the Nikkei (+0.66%) is topping gains, moving beyond the 30,000 level for the first time since September 2021, as Japan’s Q1 GDP beat estimates (more below) while the KOSPI (+0.56%) is also trading up. Elsewhere, Chinese stocks are losing ground this morning with the Hang Seng (-0.48%), the CSI (-0.35%) and the Shanghai Composite (-0.24%) all edging lower. Outside of Asia, US stock futures are printing mild gains with those on the S&P 500 (+0.19%) and NASDAQ 100 (+0.25%) retracing some of yesterday’s losses.

Coming back to Japan, data showed that the economy grew +1.6% in the first quarter this year on an annualized basis (v/s +0.8% expected), recording the first increase in three quarters and following a revised -0.1% fall in Q4 last year (initially +0.1%). A strong rebound in service activity after reopening post pandemic was the main driver of growth.

To the day ahead now, and data releases include US housing starts and building permits for April, along with the final CPI print for April from the Euro Area. From central banks, we’ll hear from BoE Governor Bailey, ECB Vice President de Guindos, along with the ECB’s de Cos, Elderson, Centeno and Rehn. Finally, earnings releases include Target and Cisco.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

Debt ceiling impasse remains, DXY bid & equities contained; TGT due – Newsquawk US Market Open

WEDNESDAY, MAY 17, 2023 – 06:20 AM

- European bourses & US futures are incrementally firmer in somewhat limited trade with corporate updates factoring and the focus on debt talks

- DAX 40 outperforms amid strength in Siemens & SAP; region follows mixed APAC trade, though Nikkei 225 surpassed 30k

- Overall, debt ceiling updates were slightly constructive, but the impasse does ultimately remain

- DXY briefly topped 103.00 as the Yuan continues to slip on soft data to the detriment of peers with JPY and GBP lagging

- Core benchmarks have experienced a bounce on firm EGB/UK supply, while USTs are slightly more restrained pre-20yr

- Crude is essentially unchanged with specific drivers limited while base metals are mixed as the USD firms and after recent Chinese data

- Looking ahead, highlights include US Building Permits/Housing Starts. ECB’s de Guindos. Supply from the US. Earnings from Target, Cisco & TJX

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses are in close proximity to the unchanged mark, Euro Stoxx 50 +0.1%, with fresh drivers somewhat limited and following a mixed APAC session though one that feature marked Nikkei 225 outperformance, above 30k.

- Within Europe, the DAX 40 +0.3% outperforms after heavyweight Siemens’ (+2.0%) Q2 update alongside strength in SAP (+1.6%) following a guidance update and buyback announcement; in contrast, Financial Services are pressured by LSE and Euronext while Commerzbank is the Banking sector laggard.

- Stateside, futures are modestly firmer in generally horizontal trade with the ES +0.1% around 4130 ahead of debt ceiling updates with the overnight developments slightly constructive but the impasse ultimately remains.

- Tencent (700 HK): Q1 2023 (CNY): Revenue 149.99bln (exp. 146.29nlm). Net 32.5bln (exp. 33.2bln), Operating 40.43bln (exp. 40.7bln); Weixin and Wechat MAUs 1.32bln (exp. 1.32bln).

- Click here and here for a recap of the main European updates.

- Click here for more detail.

FX

- DXY tops 103.000 amidst broad gains mainly forged at the expense of the Yuan.

- USD/CNY probes 7.0000 and USD/CNH approaches Fib at 7.0364 after a spate of disappointing Chinese data.

- Yen under 137.00 vs Dollar and relying on 200 DMA for a reprieve, Sterling sub-1.2450 and relatively unaffected by BoE’s Bailey.

- Euro teeters above Fib in the low 1.0800 zone.

- PBoC set USD/CNY mid-point at 6.9748 vs exp. 6.9750 (prev. 6.9506).

- Click here for more detail.

- Click here for the notable FX expiries for today’s NY cut.

FIXED INCOME

- Firm bounce in core EU bonds and strong demand for supply along the way.

- Bunds and Gilts are both towards the top of ranges extending to 135.82 and 100.83 from 135.28 and 100.41 respectively.

- USTs relatively restrained with T-note tethered to 115-00 ahead of US housing data and USD 15bln 20-year sale.

- Click here for more detail.

COMMODITIES

- Crude benchmarks are essentially unchanged after drifting in the first half of the session as the USD picked up and sentiment slipped; a narrative that has eased/lifted from respective session peaks since.

- Currently, WTI and Brent are incrementally firmer within circa. USD 1/bbl parameters with specific newsflow light and focus on geopols. amid reports that Iran’s Economy Minister discussed oil and gas projects with Saudi Arabia, according to Bloomberg.

- Spot gold is drifting with the USD firmer and sentiment improving throughout the morning, yellow metal below USD 2k/oz and approaching the USD 1981/oz 50-DMA.

- Base metals are more mixed, with the region attempting to recoup some of the recent China-induced pressures but with action capped on USD strength.

- US Energy Inventory Data (bbls): Crude +3.7mln (exp. -0.9mln), Gasoline -2.5mln (exp. -1.1mln), Distillate -0.9mln (exp. +0.1mln), Cushing +2.9mln.

- UBS lowers Year-End Brent forecast by USD 10/bbl to USD 95/bbl amid greater-than-expected supply.

- Click here for more detail.

NOTABLE HEADLINES

- The Royal United Services Institute think tank warned that UK PM Sunak will have to find USD 42bln in tax hikes and spending cuts to pay for his pledge to boost defence spending to 2.5% of GDP, according to The Mirror.

- The Resolution Foundation has warned that the BoE’s decision to hike interest rates could limit Chancellor Hunt’s room to lower taxes in the Autumn, according to The Times.

- UK Labour opposition leader Keir Starmer calls for the UK’s current Brexit deal to be renegotiated, but declares the UK must not re-join the EU or single market, according to Sky News.

- ECB’s de Cos says the ECB is getting near the end of its tightening cycle; transmission remains strong.

- ECB’s Rehn says need to see core CPI slow substantially.

- BoE Governor Bailey says “If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required.”. MPC pays particular attention to indicators of inflation persistence, including labour market tightness and wage growth, and services price inflation. There are signs that the labour market is loosening a little.

DATA RECAP

- EU HICP Final YY (Apr) 7.0% vs. Exp. 7.0% (Prev. 7.0%); X F&E Final YY (Apr) 7.3% vs. Exp. 7.3% (Prev. 7.3%); X F, E, A & T Final YY (Apr) 5.6% vs. Exp. 5.6% (Prev. 5.6%)

DEBT CEILING

- US President Biden said they had a good, productive meeting on the debt ceiling and there is still more work to do, while he made it clear to House Speaker McCarthy that they will talk regularly over the next several days. Biden is confident they will continue to make progress on avoiding default and said that defaulting on debt is not an option, while he also noted it is disappointing Republicans refuse to consider raising revenue, according to Reuters.