by harveyorgan · in Uncategorized · Leave a comment·Editi

GOLD PRICE CLOSED: UP $6.90 TO $1965.30

SILVER PRICE CLOSED: UP $0.07 AT $23.61

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1963/05

Silver ACCESS CLOSE: 23.60

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

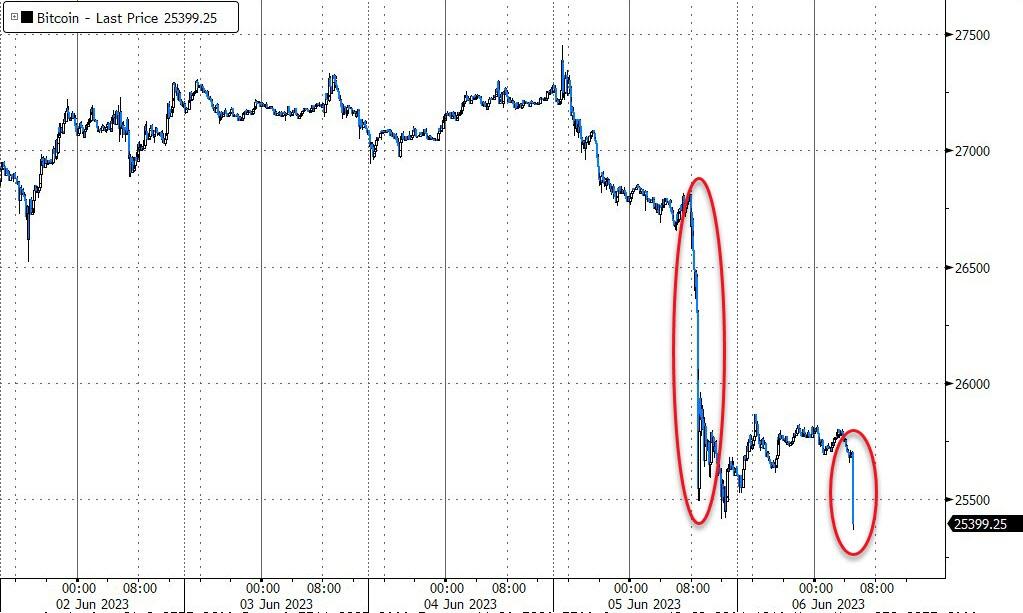

Bitcoin morning price:, $25,678 UP 176 Dollars

Bitcoin: afternoon price: $26,775 UP 1273 dollars

Platinum price closing $1036.50 UP $2.30

Palladium price; $1414.35 DOWN $0.60

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,631.30 DOWN 5.75 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1579.96 UP 2.60 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1836.13 UP 5.20 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JUNE 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,958.000000000 USD

INTENT DATE: 06/05/2023 DELIVERY DATE: 06/07/2023

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 5 3

190 H BMO CAPITAL 2

323 C HSBC 1

323 H HSBC 32

363 H WELLS FARGO SEC 5

435 H SCOTIA CAPITAL 127

661 C JP MORGAN 60

661 H JP MORGAN 5

690 C ABN AMRO 7 3

737 C ADVANTAGE 1

880 H CITIGROUP 30

905 C ADM 3

TOTAL: 142

JPMorgan stopped 60/142 contracts

FOR JUNE:

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2023. CONTRACT: 142 NOTICES FOR 14,200 OZ or 0.4416 TONNES

total notices so far: 17,117 contracts for 1,711,700 oz (53.241 tonnes)

FOR JUNE:

SILVER NOTICES: 00 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 404 for 2,020,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $6.90

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:////A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 939.56 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 7 CENTS AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 466.809 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 1439 CONTRACTS TO 135,345 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.13 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. TAS ISSUANCE WAS A GOOD SIZED 623 CONTRACTS. THESE WILL BE USED FOR MANIPULATION THIS MONTH. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY: A GOOD SIZED 623 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.13). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A HUGE GAIN ON OUR TWO EXCHANGES OF 2225 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 2.5 MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

A STRONG SIZED ISSUANCE OF EXCHANGE FOR PHYSICALS( 606 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.935 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP + 2.5 MILLION OZ EXCHANGE FOR RISK(ISSUED PRIOR)// TOTAL STANDING FOR THE MONTH 4.675 MILLION OZ ) // HUGE SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/VI) STRONG NUMBER OF T.A.S. CONTRACT INITIATION (623 CONTRACTS)//SOME T.A.S LIQUIDATION //MONDAY EARLY IN THE SESSION.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -removed 180 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTRACTS for 4 days, total 1507 contracts: OR 7.535 MILLION OZ . (376 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 7.535 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 7.535 MILLION OZ//

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1439 CONTRACTS DESPITE OUR FALL IN PRICE OF $0.13 IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 606 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.935 MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP+ 2.5 MILLION EXCHANGE FOR RISK(PRIOR)//NEW TOTAL STANDING: 6.675 MILLION OZ////// .. WE HAVE A GIGANTIC SIZED GAIN OF 2225 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG 623//SOME FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED MONDAY. THE NEW TAS ISSUANCE WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1742 CONTRACTS TO 434,743 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED – 520 CONTRACTS

WE HAD A SMALL SIZED DECREASE IN COMEX OI ( 1222 CONTRACTS) DESPITE OUR $5.00 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JUNE. AT 70.79 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S .1617 TONNE QUEUE JUMP//0 E.F.P.: NEW TOTAL 62.824 TONNES STANDING SO FAR // + /A GOOD ISSUANCE OF 778 T.A.S. CONTRACTS/SOME FRONT END OF TAS LIQUIDATION MONDAY ////YET ALL OF..THIS HAPPENED WITH A $5.00 GAIN IN PRICE WITH RESPECT TO MONDAY’S TRADING.WE HAD A SMALL SIZED GAIN OF 862 OI CONTRACTS (2.68 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2604 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 434,223

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 862 CONTRACTS WITH 1742 CONTRACTS DECREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): A GOOD 778 CONTRACTS) AND 2604 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 862 CONTRACTS OR 2.681TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2604 CONTRACTS) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (1742) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 862 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 70.79 TONNES FOLLOWED BY TODAY’S 5,200 OZ QUEUE JUMP//0 OZ E.F.P. JUMP // NEW STANDING RISES TO 62.824 TONNES// /3) ZERO LONG LIQUIDATION//4) SMALL SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: GOOD T.A.S. ISSUANCE: 778 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

TOTAL EFP CONTRACTS ISSUED: 10,782 CONTRACTS OR 1,078,200 OZ OR 33.54 TONNES IN 4 TRADING DAY(S) AND THUS AVERAGING: 2878 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY(S) IN TONNES 33.54 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 33.54/3550 x 100% TONNES 0.957% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 33.54 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 1439 CONTRACTS OI TO 133,806 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 606 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 606 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 606 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1439 CONTRACTS AND ADD TO THE 606 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2045 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 10.23 MILLION OZ

OCCURRED DESPITE OUR $0.13 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED DOWN 37.10 PTS OR 1.15% //Hang Seng CLOSED DOWN 9.22 PTS OR 0.05% /The Nikkei closed UP 289.35 OR 0.900% //Australia’s all ordinaries CLOSED DOWN 1.10 % /Chinese yuan (ONSHORE) closed DOWN 7.1168 /OFFSHORE CHINESE YUAN DOWN TO 7.1302 /Oil DOWN TO 70.41 dollars per barrel for WTI and BRENT UP AT 75.06 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1742 CONTRACTS DOWN TO 434,223 DESPITE OUR GAIN IN PRICE OF $5.00 ON MONDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2604 EFP CONTRACTS WERE ISSUED: : AUGUST 2604 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2604 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 862 CONTRACTS IN THAT 2604 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED LOSS OF 1742 COMEX CONTRACTS..AND THIS SMALL SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GAIN IN PRICE OF $5.00. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY WAS A FAIR 778 CONTRACTS. DURING THROUGHOUT LAST WEEK, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (62.824) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 62.824 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $5.00) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR SMALL SIZED GAIN OF 1382 CONTRACTS ON OUR TWO EXCHANGES. WE HAD MINOR TAS LIQUIDATION EARLY IN THE SESSION . THE TAS ISSUED MONDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 4.298 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE. (70.709 TONNES) FOLLOWED BY TODAY’S 5,200 OZ QUEUE JUMP..NEW STANDING REMAINS AT 62.824 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $5.00

WE HAD – REMOVED 520 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 862 CONTRACTS OR 86,200 OZ OR 2.681 TONNES.

Estimated gold volume today:// 133,630 poor-awful

final gold volumes/yesterday 187,600 poor

//JUNE 6/ FOR THE JUNE 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil . nil |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 142 notice(s) 14,200 OZ .4416 TONNES |

| No of oz to be served (notices) | 3081 contracts 308100 oz 9.583 TONNES |

| Total monthly oz gold served (contracts) so far this month | 17,117 notices 1,711,700 OZ 53.241 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

No dealer withdrawals

Customer deposits: 0

total deposits: NIL oz

Withdrawals: 0

total nil oz

Adjustments; 2 customer to dealer

a) JPMorgan: 11,574.333 oz

b) Brinks 99.62 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 3223 contracts having LOST 506 contracts. We had 558 contracts served on Monday so we gained 52 contracts or an additional 5200 oz will stand for gold at the comex.

The next front month after June is the non active delivery month of July. Here, July gained 204 contracts to stand at 2990 contracts.

AUGUST lost 1348 contracts down to 370,156 contracts

We had 142 contracts filed for today representing 14200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 142 contract(s) of which 60 notices were stopped (received) by j.P. Morgan dealer and 241 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2023. contract month,

we take the total number of notices filed so far for the month (17,117 x 100 oz ), to which we add the difference between the open interest for the front month of JUNE (3223 CONTRACT) minus the number of notices served upon today 142 x 100 oz per contract equals 2,019,800 OZ OR 62.824 TONNES the number of TONNES standing in this active month of June. (CME data corrected)

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (17,117) x 100 oz + (3223) [OI for the front month minus the number of notices served upon today (142)x 100 oz} which equals 2,019,800 oz standing OR 62.824 TONNES

TOTAL COMEX GOLD STANDING: 62.824 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,716,303.965 OZ 53.38 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,872,831.247 OZ

TOTAL REGISTERED GOLD: 11,686,287.649 (363.49 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 11,186,543.598 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,969,984 OZ (REG GOLD- PLEDGED GOLD) 310.10 tonnes//

END

SILVER/COMEX

JUNE 6//2023// THE JUNE 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 554,043.058 oz CNT Loomis . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 601,094.460 oz CNT |

| No of oz served today (contracts) | 00 CONTRACT(S) (nil OZ) |

| No of oz to be served (notices) | 431 contracts (2,155,000 oz) |

| Total monthly oz silver served (contracts) | 404 Contracts (2,020,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposits

total dealer deposit: nil oz

total dealer deposits: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We had 1 customer deposit

i) Into CNT: 601,094.460 oz

Total deposits: 601,094.460 oz

JPMorgan has a total silver weight: 141.367 million oz/272.820 million =51.79% of comex .//dropping fast

Comex withdrawals 2

i) Out of CNT 10,192.010 oz

ii) Out of Loomis 543,851.048 oz

total withdrawals: 554,043.058 oz

adjustments: 1 dealer to customer

i) Ashai: 214,665.200 oz

TOTAL REGISTERED SILVER: 27.121 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 272.820 million oz

DEALER SILVER DROPPING FAST. (moves into the 27 million oz column)

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE /2023 OI: 431 CONTRACTS HAVING LOST 0 CONTRACT(S).

WE HAD 0 NOTICES FILED ON MONDAY SO WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF JUNE.

JULY HAD A 1799 CONTRACT LOSS TO 95,176 CONTRACTS

AUGUST GAINED 0 CONTRACTS TO STAND AT 4

SEPT HAS A GAIN OF 3116 CONTRACTS UP TO 29,028

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 47,939 poor/

Comex volume: confirmed yesterday:54,347 poor to fair

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 404 x 5,000 oz = 2,020,000 oz

to which we add the difference between the open interest for the front month of JUNE(431) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2023 contract month: 404 (notices served so far) x 5000 oz + OI for the front month of JUNE (431) – number of notices served upon today (0 )x 500 oz of silver standing for the JUNE contract month equates to 4.175 million oz +2.5MILLION OZ EXCHANGE FOR RISK//NEW TOTAL: 6.675 MILLION OZ STANDING

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

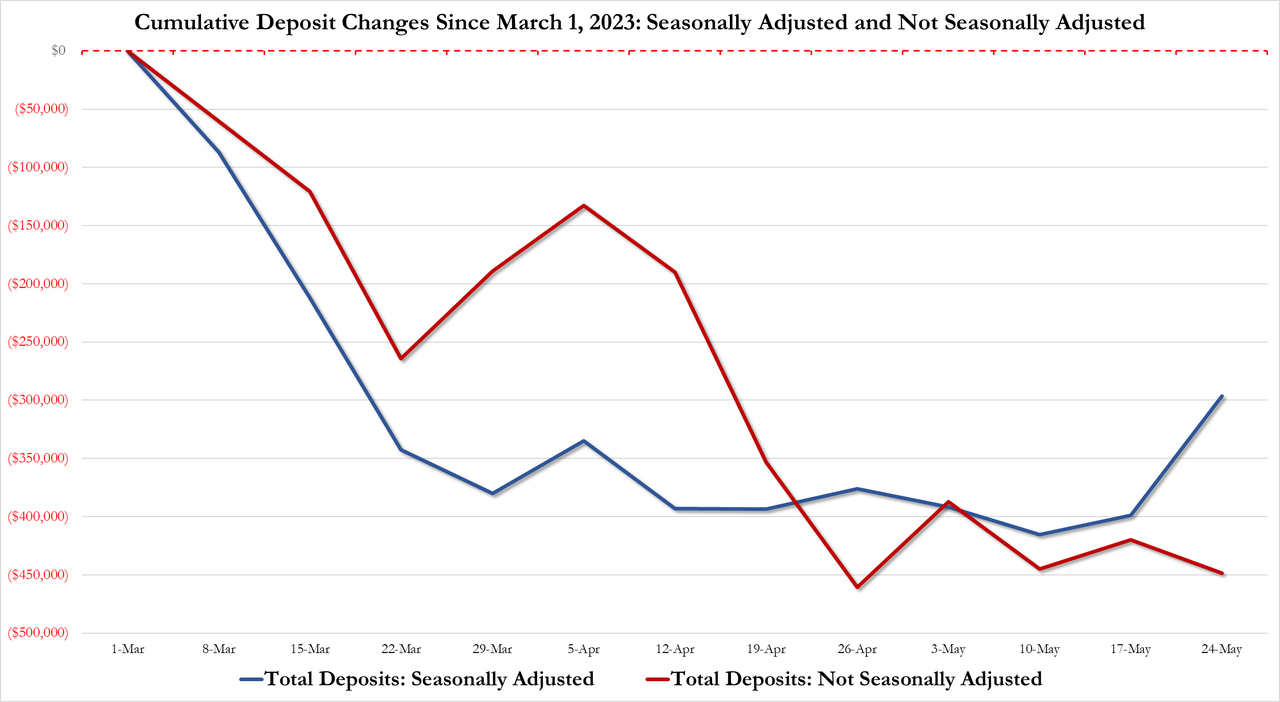

GLD AND SLV INVENTORY LEVELS

JUNE 6/WITH GOLD UP $6.90 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 939.56 TONNES

JUNE 5/WITH GOLD UP $5.00 TODAY : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 938.11 TONNES

JUNE 2/WITH GOLD DOWN $24.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 938.11 TONNES

JUNE 1/WITH GOLD UP $14.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 939.56 TONNES

MAY 31/WITH GOLD UP $5.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 939.56 TONNES

MAY 30/WITH GOLD UP $14.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 26/WITH GOLD UP $.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 941.29 TONNES

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 937.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 931.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

GLD INVENTORY: 939.56 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 6/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.809 MILLION OZ//

JUNE 5/WITH SILVER DOWN $.13 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 266,000 OZ FROM THE SLV////INVENTORY RESTS AT 466.809 MILLION OZ/

JUNE 2/WITH SILVER DOWN 23 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV./INVENTORY RESTS AT 467.015 MILLION OZ/

JUNE 1/WITH SILVER UP 49 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.933 MILLION OZ

MAY 31/WITH SILVER UP 37 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 367,000 OZ FROM THE SLV////INVENTORY RESTS AT 467.933 MILLION OZ//

MAY 30/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 26/WITH SILVER UP $0.44 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.306 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

CLOSING INVENTORY 466.809 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff/Mike Maharrey

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

Russ and Pam Martens;

JPMorgan and Citigroup Are Using the Same Accounting Maneuver as Silicon Valley Bank on Hundreds of Billions of Underwater Debt Securities

By Pam Martens and Russ Martens: June 6, 2023

As we reported yesterday, Silicon Valley Bank was not even on the “Problem Bank List” maintained by the Federal Deposit Insurance Corporation (FDIC) when it imploded in a span of 48 hours in March. According to testimony by the Federal Reserve’s Vice Chairman for Supervision, Michael Barr, on March 28 before the Senate Banking Committee, depositors had yanked $42 billion of their deposits from the bank on March 9 and had queued up to grab another $100 billion on March 10 when it was abruptly put into FDIC receivership. Had the FDIC not stepped in, Silicon Valley Bank would have lost 85 percent of its deposits in a two-day stretch.

Two of the key internal problems at Silicon Valley Bank were its large amount of uninsured deposits (which pose a flight risk in times of banking turmoil) and Silicon Valley Bank’s decision to classify 43 percent of its assets to the Held- to-Maturity (HTM) category. Under a highly controversial accounting rule, HTM debt instruments are not marked to market or shown on the balance sheet at fair value, but are instead listed at amortized cost – effectively what was paid for the debt instrument at the time of its purchase.

The HTM accounting treatment is allowing banks to create an illusion on their balance sheet as to what their assets are worth during the fastest rate increases by the Federal Reserve in 40 years. The bigger the dollar amounts held as HTM investment securities, the bigger the illusion. (While fair value for HTM securities and unrealized losses are provided in supplemental charts in SEC filings, the fair value is not reflected in the asset value on the balance sheet itself – leaving the average shareholder clueless as to what the bank’s assets are actually valued at by the market.)

Because a large portion of the debt instruments held as HTM were purchased with a fixed rate of interest when interest rates were much lower, the current market prices of these debt instruments may have declined anywhere from 10 to 25 percent.

It now turns out that two of the largest federally-insured banks in the U.S. – and potentially others that we have yet to explore – are holding hundreds of billions of dollars of debt securities in the HTM category.

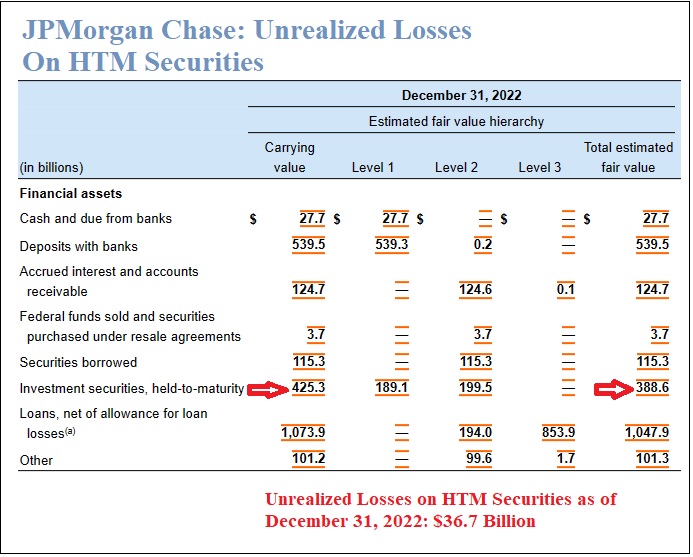

As the charts below from the 2022 10-K (Annual Report) filings with the Securities and Exchange Commission indicate, JPMorgan Chase is holding $425.3 billion in HTM securities, which actually have a fair market value of just $388.6 billion or an unrealized loss of $36.7 billion.

Making the situation even more questionable for JPMorgan Chase, as we reported on May 30, most of these debt instruments were not designated as HTM at time of purchase, but were transferred to that category in 2020, 2021, and 2022. (See our report: JPMorgan Chase Transferred $347 Billion in Debt Securities Over the Last 3 Years to Inflate Its Capital Using a Controversial Maneuver.)

JPMorgan Chase has admitted to five felony counts since 2014, including two for its dicey handling of the business bank account of the biggest Ponzi schemer in U.S. history (Bernie Madoff); and three separate counts for rigging the foreign exchange, precious metals and U.S. Treasury market. (Not to put too fine a point on it, but the U.S. Treasury market is how the United States pays its bills.) The deeply conflicted Board at JPMorgan Chase has kept Jamie Dimon as its Chairman and CEO throughout this crime wave.

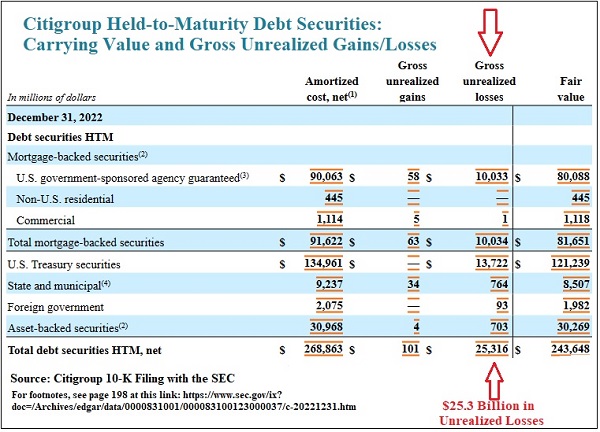

Citigroup’s 10-K for 2022 shows $268.9 billion in HTM securities, which have a fair market value of just $243.6 billion, or an unrealized loss of $25.3 billion.

Citigroup teetered near collapse in 2008; its stock price went to 99 cents in the spring of 2009; and it received over $2.5 trillion in secret, cumulative loans from the Federal Reserve from December 2007 to at least July of 2010 to keep it from total collapse, according to the audit released in 2011 by the Government Accountability Office (GAO). (See page 131 of the GAO report.) For additional insights into the role that accounting played in Citigroup losing almost all of its market value in 2008 and 2009, see accounting expert and Citigroup whistleblower Richard Bowen’s May 15 report.

After the financial crisis of 2008 to 2010 and the exposure of accounting maneuvers that played a role in enabling it, the Financial Accounting Standards Board (FASB) attempted to require fair value accounting for most financial instruments. The proposal had wide support but was shot down as a result of heavy pressure from the banking industry.

The CFA Institute, the not-for-profit association of investment professionals that awards the CFA (Certified Financial Analyst) and CIPM (Certificate in Investment Performance Measurement) designations, submitted an exhaustive written response to the FASB’s proposal, including a 29-page Appendix that provided an in-depth analysis of why fair value reporting was necessary for both transparency and the integrity of financial reports.

An argument in the CFA Institute’s letter was as follows:

“Based upon the market experience of our members and the relevant academic research, there is strong evidence that financial institution share prices incorporate the fair value of their financial instruments. The question for standard setters is whether the financial statements should likewise reflect financial instrument values in an attempt to mitigate the economic disconnect between book value and share price. We believe this is important to ensure financial statements are relevant for all investors in making investment decisions. What standard setters need to consider is whether all investors, not just some professional analysts or investors, can perform such analysis and valuation themselves and whether financial statements should assist all users and investors in the determination of the value of the enterprise. Decision- useful financial information such as the fair value of financial instruments, which represent nearly all assets and liabilities of a financial institution, should not bypass the basic financial statements.”

JPMorgan Chase and Citigroup also have exposure to large amounts of uninsured deposits. (See our report: At Year End, 4,127 U.S. Banks Held $7.7 Trillion in Uninsured Deposits; JPMorgan Chase, BofA, Wells Fargo and Citi Accounted for 43 Percent of That.)

3,Chris Powell of GATA provides to us very important physical commentaries

JPMorgan sees signs of de-dollarization

(Reuters)

Signs of de-dollarization emerging, Wall Street giant JPMorgan says

Submitted by admin on Mon, 2023-06-05 13:36Section: Daily Dispatches

By Marc Jones

Reuters

Monday, June 5, 2023

LONDON — Signs of de-dollarisation are unfolding in the global economy, strategists at the biggest U.S. bank JPMorgan said today, although the currency should maintain its long-held dominance for the foreseeable future.

The impact of steep U.S. interest rate rises and the use of sanctions that have frozen the likes of Russia out of the global banking system are driving the so-called BRICs nations — Brazil, Russia, India, China and South Africa — to challenge the dollar’s hegemony.

JPMorgan’s strategists Meera Chandan and Octavia Popescu at the Wall Street bank laid out that while overall dollar usage remains within its historical range, its usage was more “bifurcated under the hood.”

The dollar’s share of traded currency volumes is just shy of record highs, at 88%, while the euro’s share has shrunk by 8 percentage points in the last decade to a record low of 31%. The share of the Chinese yuan, meanwhile, has risen to a record high of 7%.

“De-dollarisation is evident in FX reserves where (the dollar’s) share has declined to a record as share in exports declined, but is still emerging in commodities,” the strategists said.

JPMorgan’s assessment is the most high profile of any large U.S. bank although heavyweight asset managers such as Goldman Sachs Asset Management have also voiced views on the trend.

JPMorgan’s note estimated that for global exports, the U.S. share is now down to a record low 9%, whereas China was at a record high of 13%.

In global central bank FX reserves too, the dollar’s share is down to a record low of 58%, albeit a level that is still by far the largest globally. …

… For the remainder of the report:

END

In GoldSeek Radio interview, GATA’s Murphy asks: So where are the silver bulls?

Submitted by admin on Mon, 2023-06-05 20:30Section: Daily Dispatches

8:27p ET Monday, June 5, 2023

Dear Friend of GATA and Gold:

Interviewed by GoldSeek Radio’s Chris Waltzek, GATA Chairman Bill Murphy acknowledges the much-touted bullish fundamentals for silver but says those fundamentals have been touted for years, and he asks: “Where are the silver bulls?”

Waltzek said the bulls are on the way.

The interview is 10 minutes long and can be heard at GoldSeek’s companion site, SilverSeek, here:

https://silverseek.com/article/goldseek-radio-nugget-bill-murphy-has-moved-all-his-chips-silver

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

This is good: gold is gaining in popularity among American investors

(Ronan Manly)

Ronan Manly: Gold gains hugely in popularity among American investors

Submitted by admin on Mon, 2023-06-05 21:11Section: Daily Dispatches

By Ronan Manly

Bullion Star, Singapore

Monday, June 5, 2023

Gallup, the Washington analytics and surveying firm, recently released the findings of its annual “Economy And Personal Finance” survey that asks the U.S. public the simple question” “Which investment asset class do you think is the best long-term investment?”

And they are extremely encouraging for gold, with 26% of survey respondents saying that they perceive gold to be the best long-term investment

This 26% score for gold in 2023 is nearly double the 15% of respondents who opted for gold as the best long-term investment in the 2022 survey, and reinforces evidence seen elsewhere that there is an ongoing massive shift in gold’s favor among the U.S. public right now.

Not only that, but the percentage of Americans opting for gold as the best long-term investment was also the highest result for gold in the annual poll since 2012, when 28% of the U.S. public opted for gold. This means that the percentage of the U.S. public who think gold is the best long-term investment is now at its highest for 11 years. …

… For the remainder of the analysis:

end

4, OTHER IMPORTANT GOLD COMMENTARIES/

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

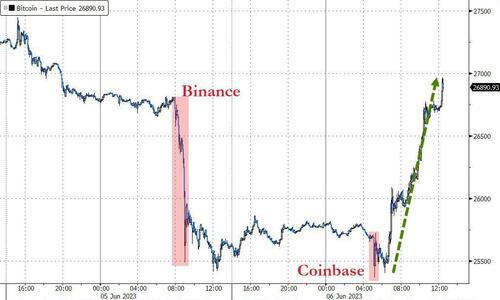

SEC sues Coinbase and that stock crashes

(zerohedge)

Coinbase Crashes After SEC Sues Crypto Exchange

TUESDAY, JUN 06, 2023 – 08:20 AM

A day after the SEC sued Binance – the world’s largest crypto exchange – Bloomberg reports that Gensler and his anti-crypto goons have now sued Coinbase in federal court in New York on Tuesday, alleging the crypto firm broke US securities rules.

Developing…

COIN shares are plunging in the pre-market on the news, extending losses from Binance headlines yesterday…

And Bitcoin (and the rest of the crypto-verse) are also lower…

It appears the war on crypto just turned ‘hot’.

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1168

OFFSHORE YUAN: 7.1302

SHANGHAI CLOSED DOWN 37.10 PTS OR 1.15%

HANG SENG CLOSED DOWN 9.22 PTS OR 0.05%

2. Nikkei closed UP 289.35 PTS OR 0.90%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 104.17 EURO FALLS TO 1.0686 DOWN 26 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.419 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 139.61 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE:DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.3329***/Italian 10 Yr bond yield RISES to 4.104*** /SPAIN 10 YR BOND YIELD FALLS TO 3.329…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.668

3j Gold at $1964.40 silver at: 23.74 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 35 /100 roubles/dollar; ROUBLE AT 81.30//

3m oil into the 70 dollar handle for WTI and 75 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 139.61 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .419% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9077 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9699 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.675 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 3.870 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.467 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 21.506…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.239 UP 3 BASIS PTS (RATES RISING RAPIDLY)

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Drift Amid Global Risk-Off Sentiment

TUESDAY, JUN 06, 2023 – 08:03 AM

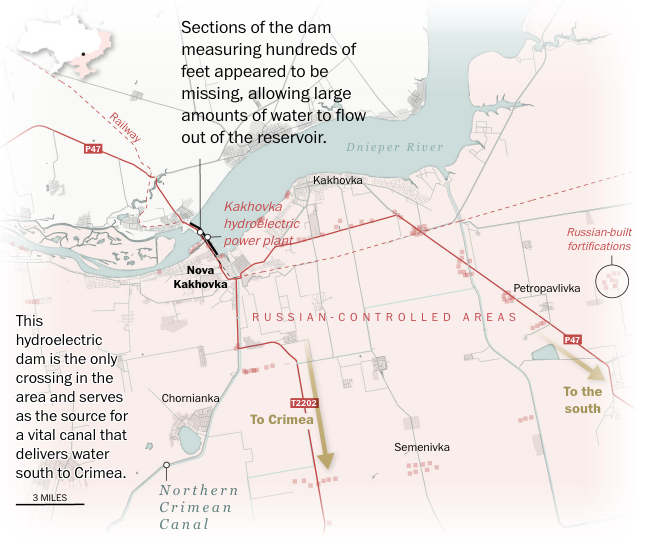

US equity futures are flat, bond yields are lower, the dollar is higher, and commodities (ex-Ags) are weaker as the excitement over the Saudi 1mmb/d production cut fizzles and as hedge fund shorts once again take the upper hand. Ags are higher led by wheat on headlines from Ukraine, where a dam was damaged in an explosion.

As of 7:45am ET, S&P futures were unchanged with the Nasdaq fractionally in the red as well, with Apple down 0.4% in premarket trading on concern the ludicrous price ($3500) of its much-anticipated mixed-reality headset will crater demand. European semiconductor firms slid after Taiwan Semiconductor — the main chipmaker to Apple — said capital spending will be at the lower end of its guidance range. Overall, there appears to be a mild risk-off tone pre-market, With the S&P 500 on the edge of a new bull market, there’s a sense among traders that markets have run up too fast on the hype for artificial intelligence. The balance of the week is light on macro data points so markets may trade in a tight range into CPI/Fed next week.

In premarket trading, tech Mega caps were mixed pre-mkt as investors digest AAPL’s developer day. AAPL is down 0.7% in early trading after the iPhone maker launched its much- anticipated mixed-reality headset at an eye-popping price of $3,499. While analysts were optimistic about the product and technology, they acknowledged that the price point was high and that it would limit the number of shipments in the near- term. Chevron fell 1%, while declines in Shell and BP weighed on Europe’s main stock benchmark after crude gave up all its gains spurred by news of Saudi Arabia’s supply cut. Other notable premarket movers:

- Mobileye shares declined 5.2% in premarket trading after chipmaker Intel said it will sell part of its holdings in the Israeli automated driving technology maker.

- Unity Software shares jump as much as 5.7% in premarket trading, extending Monday’s 17% gain after Apple said it’s working with the video-game engine maker for its new Vision Pro headset.

- Blue Bird dropped 8.5% in postmarket trading Monday after holders Coliseum Capital and American Securities offered 5 million shares in the school-bus maker via BofA Securities, Barclays, Jefferies, BMO Capital Markets and Piper Sandler.

- HealthEquity Inc. (HQY US) gained 6% postmarket after the healthcare savings account provider boosted its year profit and revenue forecast. First quarter profit and sales topped estimates.

“Our stance towards equities is a cautious one,” said Steven Bell, chief economist for EMEA at Columbia Threadneedle Investments, noting the asset class doesn’t look cheap and earnings growth forecasts look too optimistic. “We don’t expect a dramatic decline, but bonds look more attractive on a relative basis.”

European stocks slipped into the session as energy, telecom and autos underperform. Euro Stoxx 50 falls 0.4%. Stoxx 600 drops 0.1%, FTSE MIB lags regionals, sliding 0.6%. Meanwhile, the euro weakened and German bonds gained Tuesday after the European Central Bank said euro-area consumer inflation expectations eased significantly in April. Here are the most notable premarket movers:

- Idorsia shares soared as much as 21%, the most on record, before paring the gain. The Swiss biotech started exclusive negotiations with an undisclosed party regarding its Asia Pacific businesses.

- Banca Monte dei Paschi gained as much as 3.6% after la Repubblica reported that BPER Banca could be a possible suitor for the lender, citing unidentified sources.

- BAT shares fluctuated before trading up 0.3% after the company reaffirmed its full-year revenue forecast in constant currency. The unchanged outlook is “broadly reassuring” given the disappointing US performance, according to Investec.

- Chemring shares rose as much as 10.6% after the defense company reported half-year results and kept its forecasts for 2023 unchanged. Jefferies said that the update was strong and shows more organic revenue growth potential.

- ASML shares slumped as much as 1.8% after TSMC said its capex budget this year will be near the lower end of its guidance range, denting hopes that a recent boom in demand for artificial intelligence computing chips would encourage chipmakers to boost capacity. Other European semiconductor equipment makers also fell.

- Boohoo shares dropped as much as 2.7% after the online fast-fashion retailer was downgraded to neutral from outperform at Davy. The broker said Boohoo is better placed to “survive” Shein than Asos, but now has a smaller comparative advantage.

- Shares of Swiss utility BKW fell as much as 12%, the most on record, after UBS cut its recommendation to sell from buy, citing falling energy prices and the stock’s recent rally.

- Deutsche Pfandbriefbank fell as much as 5.5% after Citi downgraded the stock to sell and moved its price target to a Street-low of €6.1, based on the German lender’s real estate exposure.

Earlier in the session, Asian stocks rose to a three-month high, helped by a rally in Chinese developers. There are signs that Beijing is taking steps to bolster the economy, with authorities asking some of the biggest banks to lower their deposit rates. Elsewhere, stocks traded mixed with price action rangebound following on from the subdued performance stateside where participants ‘sold the news’ following Apple’s headset announcement and with sentiment clouded by weak data releases.

- Hang Seng and Shanghai Comp. were somewhat varied with the former boosted by strength in property names, although the mainland was less decisive and lagged amid mixed US-China rhetoric.

- Nikkei 225 was initially pressured after disappointing Household Spending and Labour Earnings data which briefly dragged the index beneath the psychological 32,000 level where it then found support and staged a recovery amid dip buying.

- Australia’s ASX 200 was led lower by underperformance in the consumer-related sectors and top-weighted financial industry, with losses later exacerbated after the RBA delivered a surprise 25bps rate hike to lift the Cash Rate Target to 4.10% and it also kept the door open for further policy tightening.

- Indian stocks ended little changed on Tuesday, while gauges of small- and mid-sized companies extended their record runs as investors looked to rotate allocations following the end of the earnings season. The S&P BSE Sensex Index was little changed as was the NSE Nifty 50 Index. BSE’s small and midcap indexes rallied for the 12th consecutive session and scaled new records despite momentum being overbought based on the 14-day RSI. The key gauges traded lower for a large part of the session on Tuesday before erasing losses in the final 30 minutes of trade, helped by a recovery in banking stocks. The benchmark Sensex has traded close to its previous peak over the last few sessions but so far has failed to climb to a new record. The Sensex and Nifty have risen about 3.2% and 2.7% this year but trail the 8% rally in small and mid-cap gauges.

Elsewhere, Australia unexpectedly hiked on Tuesday and kept the door open to further increases, sparking a rally in the country’s currency.

In FX, the Bloomberg Dollar Spot Index was up near session highs, recovering from early weakness; AUD and JPY are the strongest performers in G-10 FX, NOK and GBP underperform. The EUR/USD dropped -0.2% after after the latest ECB survey shows consumers’ inflation expectations fell significantly in April. AUD/USD leads gains, rallying as much as 1% after the RBA increased its cash rate by a quarter percentage point and said further tightening may be needed. Only 10 of 30 economists surveyed by Bloomberg predicted the rate hike

In rates, German bonds outperform Treasuries and gilts across the curve as yields drop, led by short-end bunds. Treasuries are slightly richer across the curve, following wider gains in bunds after an ECB survey shows consumers’ inflation expectations fell significantly in April. Yields are richer by 1bp-2bp across the curve with intermediates outperforming slightly, steepening 5s30s by 1bp on the day; 10- year yields around 3.66%, richer by 2bp vs Monday’s close with bunds outperforming by 3.5bp in the sector. The two-year Treasury yield slips 1bps to 4.45%, 10-year yield down 2bps to 3.66%, slightly steepening the 2-year/10-year curve. German curve sharply bull-steepens over early London session following consumer inflation expectations data — Germany 2-year yields remain richer by 8bp on the day with 2s10s spread steeper by 2.5bp, 5s30s by 4bp. Dollar IG issuance slate includes NAB 2Y/5Y and ADB 2Y/10Y; twelve companies priced $20.1b Monday, surpassing weekly volume projection in a single day; desks project around $80b for the month of June.

In commodity markets, wheat surged after Ukraine said Russian forces blew up a giant dam in the country’s south, unleashing a torrent of floodwater that threatens thousands of people and poses a potential threat to Black Sea grain supplies. Meanwhile, crude drifted 2.2% lower to trade near $70.58. Most base metals trade in the green; LME nickel rises 1.4%, outperforming peers. LME aluminum lags, dropping 1.1%. Spot gold is little changed at $1,962/oz

Looking ahead, the US session has no economic data releases or Fed speakers scheduled, amid quiet period ahead of June FOMC meeting.

Market Snapshot

- S&P 500 futures little changed at 4,277.50

- MXAP up 0.3% to 164.13

- MXAPJ down 0.2% to 514.04

- Nikkei up 0.9% to 32,506.78

- Topix up 0.7% to 2,236.28

- Hang Seng Index little changed at 19,099.28

- Shanghai Composite down 1.1% to 3,195.34

- Sensex down 0.3% to 62,586.79

- Australia S&P/ASX 200 down 1.2% to 7,129.64

- Kospi up 0.5% to 2,615.41

- STOXX Europe 600 little changed at 459.93

- German 10Y yield little changed at 2.34%

- Euro down 0.1% to $1.0702

- Brent Futures down 2.1% to $75.12/bbl

- Gold spot down 0.2% to $1,958.11

- U.S. Dollar Index little changed at 104.02

Top Overnight News

- Australia’s central bank surprised the mkt and raised interest rates by a quarter-point to an 11-year high, and warned that further tightening may be required to ensure that inflation returns to target. RTRS

- Chinese authorities asked the nation’s biggest banks to lower their deposit rates for at least the second time in less than a year, according to people familiar with the matter, marking an escalated effort to boost the world’s second-largest economy. BBG

- China will likely further cut banks’ reserve ratio and interest rates in the second half of this year to support the economy, the China Securities Journal reported on Tuesday, citing policy advisors and economists. RTRS

- Underlying price pressures in the euro zone may prove more difficult to tame but monetary policy is showing signs of effectiveness and further rate hikes must be done step by step, Dutch central bank chief Klaas Knot said on Tuesday. RTRS

- Eurozone inflation expectations decreased significantly according to the latest ECB survey, reversing most of the increases seen in the previous month. ECB

- Something unusual has happened to the price of butter in Germany this year — it has fallen sharply even as the cost of many other foods kept rising at double-digit rates. Following a dip in energy prices, surging food costs have become the main source of inflation for the eurozone consumers. They are up 20% since the start of last year, causing alarm among politicians and central bankers. But economists and industry executives increasingly believe the factors behind a fall in the price of German butter — down almost 30% since in December as dairy producers’ costs have fallen — will soon begin to have a broader impact. FT

- A major dam and power station in a Russian-occupied part of Ukraine were destroyed Tuesday, with both sides accusing each other of being responsible for an incident that has caused serious flooding, put thousands of homes at risk and potentially threatened the safety of Europe’s largest nuclear power plant. WSJ

- Eight years after he first announced he was running for president, Chris Christie is readying for a return to the national stage. The brash former governor of New Jersey is expected to launch his second presidential run on Tuesday with a town hall-style event in Manchester, New Hampshire, some 300 miles north of his home state. FT

- Citadel brought back retired portfolio manager Drew Gillanders to expand the fund’s equities trading in Europe. The 51-year-old, who worked at Citadel between 2019 and 2022, will report to co-CIO Pablo Salame. BBG

- Recession risk has receded as the debt ceiling crisis fades and the banking sector stabilizes. Although labor market rebalancing and inflation progress have been encouraging, a firmer growth outlook will likely prompt the Fed to hike again in July (and push several other DM central banks in a more hawkish direction too). GIR

A more detailed summary of global markets courtesy of Newsquawk

APAC stocks traded mixed with price action mostly rangebound following on from the subdued performance stateside where participants ‘sold the news’ following Apple’s headset announcement and with sentiment clouded by weak data releases. ASX 200 was led lower by underperformance in the consumer-related sectors and top-weighted financial industry, with losses later exacerbated after the RBA delivered a surprise 25bps rate hike to lift the Cash Rate Target to 4.10% and it also kept the door open for further policy tightening. Nikkei 225 was initially pressured after disappointing Household Spending and Labour Earnings data which briefly dragged the index beneath the psychological 32,000 level where it then found support and staged a recovery amid dip buying. Hang Seng and Shanghai Comp. were somewhat varied with the former boosted by strength in property names, although the mainland was less decisive and lagged amid mixed US-China rhetoric.

Top Asian News

- RBA surprisingly raised the Cash Rate Target by 25bps to 4.10% (exp. 3.85%), while it reiterated that the Board remains resolute in its determination to return inflation to the target and some further tightening of monetary policy may be required. It also repeated that inflation in Australia has passed its peak, but at 7% is still too high and it will be some time yet before it is back in the target range. RBA stated that this further increase in interest rates is to provide greater confidence that inflation will return to target within a reasonable timeframe, as well as noted that recent data indicates that the upside risks to the inflation outlook have increased and the Board has responded to this.

- China has reportedly asked the largest banks to cut deposit rates to boost the economy, according to Bloomberg sources. State-owned lenders including Bank of China, ICBC, and Bank of Communications were advised to cut rates on a range of products, including demand deposits by 5bps and 3yr and 5yr time deposits by at least 10bps.

- Former ByteDance executive claimed the Chinese Communist Party accessed TikTok’s Hong Kong user data, according to WSJ. It was separately reported that Vietnam’s ministry found TikTok violations during its inspection.

- BoJ Governor Ueda said BoJ is to continue QQE until the inflation target is achieved, and added inflation and inflation expectations are heightening, according to Reuters.

European equities trade with little in the way of firm direction as incremental catalysts for the region remain light. Equity sectors in Europe are mixed with Health Care top of the leaderboard whilst Energy lags to the downside with WTI and Brent both below Friday’s closing levels despite efforts by OPEC+. US equity futures are hugging the unchanged mark with the ES around 20 points shy of the 4300 mark after venturing as high as 4305.75 yesterday.

Top European News

- ECB’s Knot said inflation is still way too high but the worst is behind us; underlying pressures will prove more difficult to bring down. He said they are seeing first signs that monetary policy tightening is being transmitted to the real economy, and will keep tightening policy until we see inflation return to 2% target, but this will be done step by step.

- ECB Consumer Expectations Survey (Apr): Inflation Expectations: 4.1% 12-months ahead (Mar 5.0%), 3yr ahead 2.5% (Mar 2.9%). Nominal Income: 1.1% over the next 12-months (Mar 1.3%). Nominal Spending: 3.8% over the next 12-months (Mar 4.1%)

- Barclaycard said UK May consumer spending rose 3.6% Y/Y and noted that higher food prices limited discretionary spending, according to Reuters.

FX

- DXY edged higher throughout the European morning and currently resides near session highs above 104.00.

- JPY is continues to claw back losses at the expense of its US counterpart as yields softened.

- Aussie remains the clear G10 outperformer in wake of another largely unexpected 25 bp rate rise from the RBA overnight.

- Euro eased back from circa 1.0732 against the Dollar to sub-1.0700 and the base of 1bln option expiries between the round number and 1.0695.

- PBoC set USD/CNY mid-point at 7.1075 vs exp. 7.1080 (prev. 7.0904)

Fixed Income

- Debt futures have racked up bigger and longer-lasting gains on a combination of bullish or supportive factors ranging from geopolitical developments, disinflationary vibes and a deeper reversal in oil that should have dovish implications for price pressures ahead.

- Bunds have been up to 135.57 for a 100+ tick flip from Eurex trough to peak.

- Gilts probed 97.00 within a 97.06-96.35 range in wake of a well received 2053 DMO tap

- US Treasuries are above 114-00 between 114-06+/113-24 overnight parameters.

- UK sells GBP 2.5bln 3.75% 2053 Gilt: b/c 2.58x (Prev. 2.50x), average yield 4.478% (Prev. 4.083%) & tail 0.5bps (Prev. 0.2bps)

Commodities

- WTI and Brent futures continue trundling lower as the post-OPEC pop faded, with prices now back at levels seen in the run-up to last weekend’s confab.

- Asian refiners are likely to take less oil from Saudi Arabia for July and buy more spot cargoes such as those from the UAE after the surprise price hike and output cut, according to Reuters citing traders.

- Kazakhstan Energy Minister said the country will go ahead with the USD 16.5bln claim against international oil giants over costs, no plans for out-of-court settlement, according to Reuters.

- Spot gold is relatively steady around the USD 1,950/oz mark and within recent ranges, with some potential haven support underpinning prices.

- Base are mostly softer with LME copper still hovering above USD 8,250/t following the recent gains as China looks to bolster its property sector. On that note, iron ore continued to benefit from these tailwinds and printed higher levels in around seven weeks.

- Shanghai futures exchange says trading of alumina futures will begin on June 9th.

Geopolitics

RUSSIA-UKRAINE

- Russia’s Federal Security Service (FSB) says Ukraine planning a “dirty bomb” attack in Russia, via RIA.

- Twitter sources reported that the Nova Kakhovka Dam was blown up in southern Ukraine, while Ukraine’s south military command later confirmed that the dam was blown up by Russian forces. Furthermore, a Moscow-backed official said there was no critical danger to the Zaporizhzhia nuclear plant yet from the destruction of the dam, according to Reuters.

- Russia’s Defence Ministry said they destroyed 8 leopard tanks in the Donetsk region and that Ukraine continues with its offensive in Donetsk, while it also noted huge losses were inflicted on Ukrainian forces in Donetsk and that Ukrainian forces are deploying fresh troops in the eastern combat zone, according to Reuters.

- Ukraine’s State Atomic Agency said the destruction of the Kakhova dam poses a risk to the Zaporizhzhia nuclear power plant, but the situation is under control, according to Reuters.

- Ukraine’s Foreign Minister said Ukraine will “probably” only be able to join NATO after the end of the war and said Ukraine has enough weapons to begin its counter-offensive, according to Reuters.

OTHER

- White House said the US is seeing an increasing level of aggressiveness by China’s military and the US is prepared to address growing aggressiveness. White House stated the US wants to see Beijing justify what it is doing with increased military and said both recent Chinese intercepts occurred in international space, while it added that it won’t be long before someone gets hurt and that unsafe intercepts can lead to miscalculations.

- South Korea has scrambled air force jets after Russian and Chinese military planes entered its air defence zone, according to joint chiefs; did not violate South Korean air space.

US Event Calendar

- Nothing scheduled

DB’s Jim Reid concludes the overnight wrap

DB Research has just released our latest World Outlook featuring our updated views on economics and markets. We’ve called this edition “The Waiting Game…” because we maintain our call for a US recession in Q4 as the lags from tighter monetary policy really start to hit. As we’ve felt for a while, you have to respect the lag and be patient. Markets on the other hand are anything but and want instant gratification. That’s what makes it an interesting time now and for the next few months ahead.

To recap we think this hard landing is the logical next step in a succession of all-too foreseeable events since the pandemic: the biggest increase in the money supply in decades, followed by the highest inflation in decades, and then the most aggressive series of rate hikes in decades. A hard landing is just the next phase of this. If you’re looking for hope we are optimistic about the prospects of AI changing the nature of our economies in the years ahead. We desperately need a new source of growth given weak productivity and poor demographics. And although AI is unlikely to help us out of this cycle, its promise is a hope we cling onto as we move deeper into the 2020s after a very challenging start to the decade.

Finally in terms of adverts, Steve Caprio on my credit team has an update to our view this morning (link here). He posits that while the consensus view among clients is for a summer squeeze, we see little reason to chase the market and so we retain our defensive positioning across ratings and tenors.

Markets certainly stopped chasing and squeezing yesterday, in part thanks to a weak ISM services print that helped to ramp up fears about a recession. Earlier in the day it had looked rather different, and at one point the S&P 500 was even on track to close in bull market territory, having risen by over 20% since its closing low last October. But the negative data surprise ultimately dominated, and that led to a decent risk-off move that meant the index fell short of that milestone by the close.

In terms of the release, the ISM services for May came in at 50.3 (vs. 52.4 expected), so just above the 50-mark that separates expansion from contraction and the second lowest since the pandemic, only beating a strange out of the blue plunge in December. The sub-components didn’t look too promising either, with new orders down to 52.9, whilst employment at 49.2 was in contractionary territory for the first time since December. Other releases out yesterday were a bit weaker-than-expected too, with April’s factory orders only up by +0.4% (vs. +0.8% expected), alongside downward revisions to the previous month.

Treasuries rallied on the back of the ISM, and the 10yr yield gave up its initial rise to fall by almost -8bps intraday straight after the release, before closing -0.1bps down on the day at 3.683%. Another contributing factor was that the weak data led to growing expectations that the Fed would pause their rate hikes at their meeting next week, with only a 24.5% chance of a hike now priced in down from 30.5% at the end of last week. Ultimately, markets are increasingly coalescing around the idea that the Fed will skip a meeting in June before delivering another hike in July, which is in line with the updated call from our US economists in the World Outlook. This morning in Asia, yields on 10yr USTs (+1.73 bps) are slightly higher again as we go to print.

Sovereign bonds in Europe lost ground more consistently yesterday after ECB President Lagarde continued to signal more rate hikes ahead at the European Parliament. Among others, Lagarde said that the ECB’s “future decisions will ensure that the policy rates will be brought to levels sufficiently restrictive”. And in turn, that helped to cement investors in their conviction that the ECB would proceed with another 25bp hike next week. As a result, yields on 10yr bunds (+6.9bps), OATs (+6.3bps) and BTPs (+6.8bps) all moved higher on the day.

For equities, it was an up-and-down day, and in the end the S&P 500 (-0.20%) closed lower, after being +0.40% at the day’s highs. In addition to the weaker US data, specific factors appeared to weigh during the day. Oil majors reversed their initial gains from the OPEC+ news over the weekend, while Apple closed -0.76% lower, after being up over 2% intra-day at one point. This comes as the world’s largest technology company unveiled their new “mixed reality” headset with a sticker price of $3499. With tech stocks slipping, the NASDAQ (-0.09%) was largely flat on the day, though its YTD gains still stand at +26.40%.

Back in Europe, the more negative tone continued to take hold, with the STOXX 600 (-0.48%) getting the week off to a rough start. In part, that reflected a surge in European natural gas prices (+24.9%) following their recent declines. And that occurred alongside a broader spike in energy prices, following the decision from Saudi Arabia to cut its oil output by 1 million barrels per day. However a late drop in risk sentiment near the US close meant Brent crude (+0.76%) ended the day at $76.71/bbl, whilst WTI (+0.57%) closed at $71.89/bbl with both contracts trading comfortably off their intraday highs.