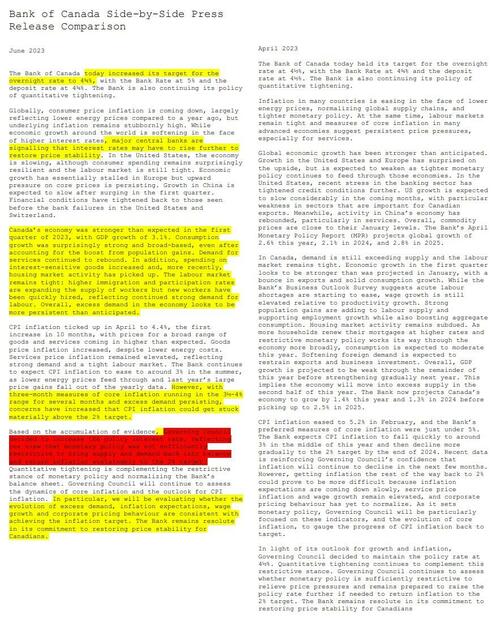

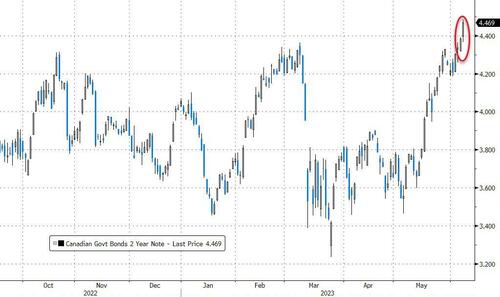

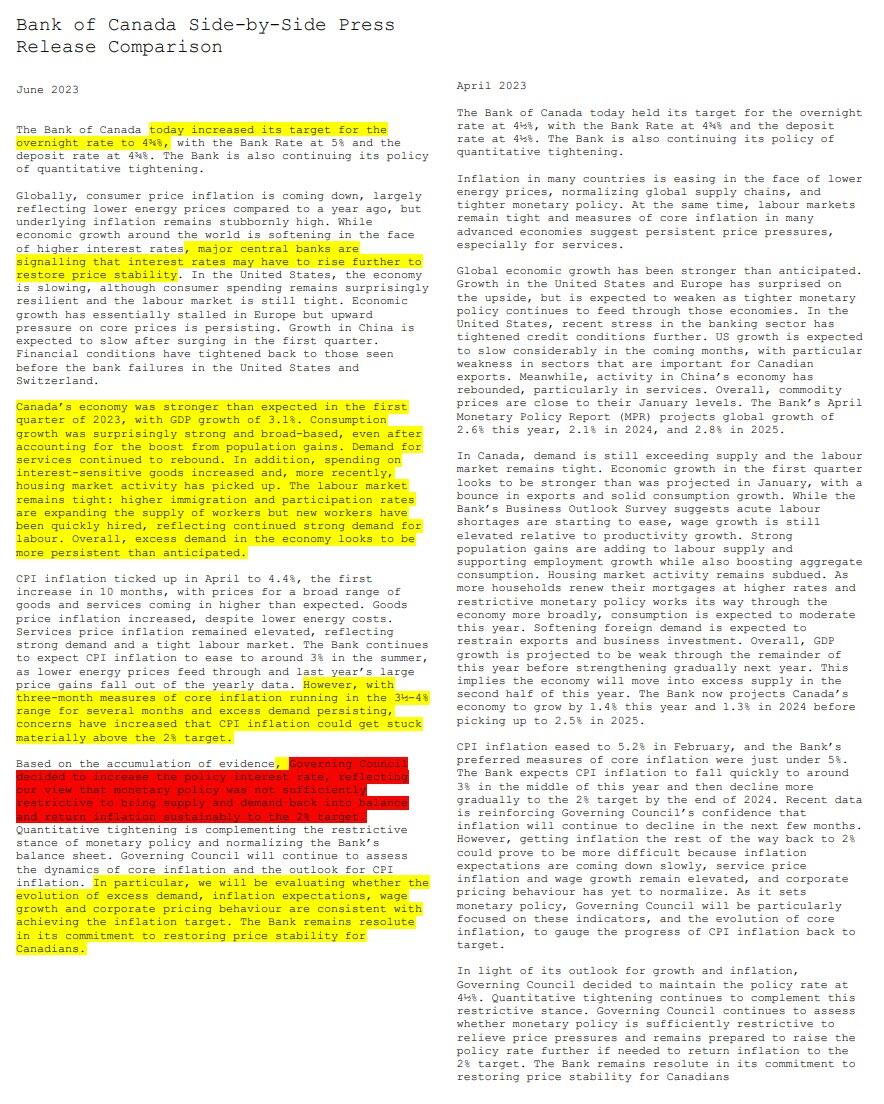

JUNE 7/GOLD CLOSED DOWN $22.15 TO $1943.15//SILVER CLOSED DOWN $.17 TO $23.44/PLATINUM CLOSED DOWN $13.60 TO $1022,90 WHILE PALLADIUM CLOSED DOWN $19.05 TO $1396.30/ANOTHER T.A.S.ORCHESTRATED RAID ON OUR PRECIOUS METALS//IMPORTANT READ FOR TODAY; TED BUTLER//BANK OF CANADA NO LONGER PAUSES AS IT RAISES INTEREST RATES BY .25%//UPDATES ON THE RUSSIAN DAM BLOW UP//COVID UPDATES//SWAMP STORIES FOR YOU TONIGHT..

132 C SG AMERICAS 2 190 H BMO CAPITAL 1 323 H HSBC 22 363 H WELLS FARGO SEC 8 435 H SCOTIA CAPITAL 101 661 C JP MORGAN 42 661 H JP MORGAN 4 690 C ABN AMRO 2 737 C ADVANTAGE 1 880 H CITIGROUP 21

TOTAL: 102 102

JPMorgan stopped 46/102 contracts

FOR JUNE:

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2023. CONTRACT: 102 NOTICES FOR 10,200 OZ or 0.3172 TONNES

total notices so far: 17,219 contracts for 1,721,900 oz (53.560 tonnes)

FOR JUNE:

SILVER NOTICES: 17 NOTICE(S) FILED FOR 85,000 OZ/

total number of notices filed so far this month : 421 for 2,105,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $22.15

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:////A WITHDRAWAL OF 1.45 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 938.11 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 17 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.01 MILLION OZ OF SILVER INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 467.819 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY AN ATMOSPHERIC SIZED 2626 CONTRACTS TO 137,871 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR SMALL $0.07 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. TAS ISSUANCE WAS A GOOD SIZED 525 CONTRACTS. THESE WILL BE USED FOR MANIPULATION THIS MONTH. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY: A GOOD SIZED 525 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.07). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A HUMONGOUS GAIN ON OUR TWO EXCHANGES OF 2773CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 2.5MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

A SMALL SIZED ISSUANCE OF EXCHANGE FOR PHYSICALS( 101 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.935 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S 85,000 OZ QUEUE JUMP + 2.5 MILLION OZ EXCHANGE FOR RISK(ISSUED PRIOR)// TOTAL STANDING FOR THE MONTH 4.76MILLION OZ ) // HUGE SIZED COMEX OI GAIN/ SMALL SIZED EFP ISSUANCE/VI) GOOD NUMBER OF T.A.S. CONTRACT INITIATION (525 CONTRACTS)//SOME T.A.S LIQUIDATION EARLY IN THE SESSION //

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -removed 46 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTRACTS for 5 days, total 1608 contracts: OR 8.040 MILLION OZ . (322 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 8.040 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 8.040 MILLION OZ//

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2626 CONTRACTS DESPITE OUR TINY RISE IN PRICE OF $0.07 IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 101 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.935 MILLION OZ FOLLOWED BY TODAY’S 85,000 OZ QUEUE JUMP+ 2.5 MILLION EXCHANGE FOR RISK(PRIOR)//NEW TOTAL STANDING: 6.76 MILLION OZ////// .. WE HAVE A GIGANTIC SIZED GAIN OF2700 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GOOD 525//SOME FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED EARLY DURING THE TUESDAY SESSION. THE NEW TAS ISSUANCE WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 17 NOTICE(S) FILED TODAY FOR 85,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2078 CONTRACTS TO 436,301 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED – 14 CONTRACTS

WE HAD A FAIR SIZED INCREASE IN COMEX OI ( 2078 CONTRACTS) WITH OUR $6.90 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JUNE. AT 70.79 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S .2830 TONNE QUEUE JUMP//0 E.F.P.: NEW TOTAL 63.107 TONNES STANDING SO FAR // + /A GOOD ISSUANCE OF 525 T.A.S. CONTRACTS/SOME FRONT END OF TAS LIQUIDATION TUESDAY ////YET ALL OF..THIS HAPPENED WITH A $6.90 GAIN IN PRICEWITH RESPECT TO TUESDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 2700 OI CONTRACTS (8.398 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 622 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 436,301

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2700 CONTRACTS WITH 2078 CONTRACTS INCREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): A GOOD 525 CONTRACTS) AND 622 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF2700CONTRACTS OR 8.398TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (622 CONTRACTS) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (2078) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 2700 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 70.79 TONNES FOLLOWED BY TODAY’S 9100 OZ QUEUE JUMP//0 OZ E.F.P. JUMP // NEW STANDING RISES TO 63.107 TONNES// /3) ZERO LONG LIQUIDATION//4) FAIR SIZED COMEX OPEN INTEREST GAIN/ 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: GOOD T.A.S. ISSUANCE: 525 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

TOTAL EFP CONTRACTS ISSUED: 11,404 CONTRACTS OR 1,140,400 OZ OR 35.49 TONNES IN 5 TRADING DAY(S) AND THUS AVERAGING: 2280 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY(S) IN TONNES 35.49 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 35.49/3550 x 100% TONNES 1.000% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 35.49 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUMONGOUS SIZED 2626 CONTRACTS OI TO 137,871 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 606 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 101 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 101 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2626 CONTRACTS AND ADD TO THE 101OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2727 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 13.635 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 2.42 PTS OR 0.08% //Hang Seng CLOSED UP 152.72 PTS OR 0.80% /The Nikkei closed DOWN 593.04 OR 1.82% //Australia’s all ordinaries CLOSED DOWN 0.13 % /Chinese yuan (ONSHORE) closed UP 7.1131 /OFFSHORE CHINESE YUAN UP TO 7.1242 /Oil DOWN TO 70.41 dollars per barrel for WTI and BRENT UP AT 75.06 / Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2078 CONTRACTS UP TO 436,301 WITH OUR GAIN IN PRICE OF $6.90 ON TUESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE… THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 622 EFP CONTRACTS WERE ISSUED: : AUGUST 622 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 622 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2700 CONTRACTS IN THAT 622LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 2078 COMEX CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $6.90. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY WAS A SMALLISH 525 CONTRACTS. THROUGHOUT LAST WEEK, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (63.107) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 63.107 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $6.90) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR FAIR SIZED GAIN OF 2700 CONTRACTS ON OUR TWO EXCHANGES. WE HAD MINOR TAS LIQUIDATION EARLY IN THE SESSION . THE TAS ISSUED TUESDAY, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 8.441PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE. (70.709 TONNES) FOLLOWED BY TODAY’S 9100 OZ QUEUE JUMP..NEW STANDING REMAINS AT 62.824 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $6.90

WE HAD – REMOVED 14 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 2700 CONTRACTS OR 270,000 OZ OR 8.398 TONNES.

Total monthly oz gold served (contracts) so far this month

17,219 notices 1,721900 OZ 53.560 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

No dealer withdrawals

Customer deposits: 1

i)Into Ashai: 48,157.530 oz

total deposits: 48,157.530 oz

Withdrawals: 0

total nil oz

Adjustments; 1 dealer to customer

a)Ashai: 13,106.320 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 3172 contracts having LOST 51 contracts. We had 142 contracts served on Monday so we gained 91 contracts or an additional 9100 oz will stand for gold at the comex.

The next front month after June is the non active delivery month of July. Here, July lost 277 contracts to stand at 2913 contracts.

AUGUST lost 1517 contracts down to 371,673 contracts

We had 102 contracts filed for today representing 10200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 102 contract(s) of which 4 notices were stopped (received) by j.P. Morgan dealer and 42 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2023. contract month,

we take the total number of notices filed so far for the month (17,219 x 100 oz ), to which we add the difference between the open interest for the front month of JUNE (3172 CONTRACT) minus the number of notices served upon today 102 x 100 oz per contract equals 2,019,800 OZ OR 62.824 TONNES the number of TONNES standing in this active month of June. (CME data corrected)

thus the INITIAL standings for gold for the JUNEcontract month: No of notices filed so far (17,219) x 100 oz + (3172) [OI for the front month minus the number of notices served upon today (102)x 100 oz} which equals 2,028,900 oz standing OR 63.107 TONNES

TOTAL COMEX GOLD STANDING: 63.107 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

total pledged gold: 2,045,150.099 OZ 63.612 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,920,988.717 OZ

TOTAL REGISTERED GOLD: 11,673,181,329 (363.31 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 11,247,807.448 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,631,031 OZ (REG GOLD- PLEDGED GOLD) 299.57 tonnes//

END

SILVER/COMEX

JUNE 7//2023// THE JUNE 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

320,436.024 oz CNT Delaware HSBC

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

991.100 oz Delaware

No of oz served today (contracts)

17 CONTRACT(S) (n85,000 OZ)

No of oz to be served (notices)

431 contracts (2,155,000 oz)

Total monthly oz silver served (contracts)

421 Contracts (2,105,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposits

total dealer deposit: nil oz

total dealer deposits: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We had 1 customer deposit

i) Into Delaware: 991.100 oz

Total deposits: 991.100 oz

JPMorgan has a total silver weight: 141.367 million oz/272.501 million =51.85% of comex .//dropping fast

Comex withdrawals 3

i) Out of CNT 20,238.390 oz

ii) Out of Delaware 984.134 oz

iii) Out of HSBC: 299,213.500 oz

total withdrawals: 320,436.024 oz

adjustments: 0

TOTAL REGISTERED SILVER: 27.121 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 272.501 million oz

DEALER SILVER DROPPING FAST. (moves into the 27 million oz column)

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE /2023 OI: 448 CONTRACTS HAVING GAINED 17 CONTRACT(S).

WE HAD 0 NOTICES FILED ON MONDAY SO WE GAINED 17 CONTRACTS OR AN ADDITIONAL 85,000 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF JUNE.

JULY HAD A 366 CONTRACT GAIN TO 95,542 CONTRACTS

AUGUST GAINED 1 CONTRACTS TO STAND AT 5

SEPT HAS A GAIN OF 2157 CONTRACTS UP TO 31,185

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 17 for 85,000 oz

Comex volumes// est. volume today 79,990 strong //raid/

Comex volume: confirmed yesterday:50,193 poor

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 421 x 5,000 oz = 2,105,000 oz

to which we add the difference between the open interest for the front month of JUNE(448) and the number of notices served upon today 17 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2023 contract month: 421 (notices served so far) x 5000 oz + OI for the front month of JUNE (448) – number of notices served upon today (17 )x 500 oz of silver standing for the JUNE contract month equates to 4.260 million oz +2.5MILLION OZ EXCHANGE FOR RISK//NEW TOTAL: 6.76 MILLION OZ STANDING

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JUNE 7 WITH GOLD DOWN $22.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 938.11 TONNES

JUNE 6/WITH GOLD UP $6.90 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 939.56 TONNES

JUNE 5/WITH GOLD UP $5.00 TODAY : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 938.11 TONNES

JUNE 2/WITH GOLD DOWN $24.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 938.11 TONNES

JUNE 1/WITH GOLD UP $14.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 939.56 TONNES

MAY 31/WITH GOLD UP $5.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 939.56 TONNES

MAY 30/WITH GOLD UP $14.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 26/WITH GOLD UP $.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 941.29 TONNES

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 937.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 931.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

GLD INVENTORY: 938.11 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 7/WITH SILVER DOWN 17 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.01 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 6/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.809 MILLION OZ//

JUNE 5/WITH SILVER DOWN $.13 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 266,000 OZ FROM THE SLV////INVENTORY RESTS AT 466.809 MILLION OZ/

JUNE 2/WITH SILVER DOWN 23 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV./INVENTORY RESTS AT 467.015 MILLION OZ/

JUNE 1/WITH SILVER UP 49 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.933 MILLION OZ

MAY 31/WITH SILVER UP 37 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 367,000 OZ FROM THE SLV////INVENTORY RESTS AT 467.933 MILLION OZ//

MAY 30/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 26/WITH SILVER UP $0.44 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.306 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

CLOSING INVENTORY 467.819 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

What Central Banks Giveth They Taketh Away; Wave Of Corporate Defaults On The Horizon

With a debt ceiling deal done, the threat of a US government default is off the table for the time being. But a wave of corporate defaults is on the horizon according to Deutsche Bank’s annual default study.

This is the inevitable consequence of central bank monetary policy and it was entirely predictable.

Deutsche Bank strategists Jim Reid and Steve Caprio say that corporate defaults will become “more normal” as we enter into a default cycle thanks to higher interest rates and a growing number of over-leveraged companies.

Our cycle indicators signal a default wave is imminent. The tightest Fed and ECB policy in 15 years is colliding with high leverage built upon stretched margins. And tactically, our US credit cycle gauge is producing its highest non-pandemic warning signal to investors, since before the GFC [Great Financial Crisis].”

The Deutsche Bank study projects defaults for US high-yield debt will peak at around 9% in late 2024. For comparison, the high-yield default rate was a mere 0.5% in 2021 and 1.3% in 2022.

The study predicts that the looming recession will create significant pain in the world’s credit markets, similar to the dot-com bust.

Corporate leverage is elevated. And global credit markets derive more of their revenue from manufacturing and the sale of physical goods than the real economy at large. Going forward, corporates will likely lose pricing power on their sale of physical goods, due to high inventory builds and a post-COVID demand shift from goods to services. But labor costs are likely to remain sticky, because of a shrinking working-age population and a desire for consumers to recoup nearly 2 years of negative real wage growth.”

Bank of America also forecasts a wave of defaults. According to its analysis, defaults could rise to $1 trillion if the US economy enters into a full-blown recession.

Meanwhile, Moody’s expects defaults on speculative-grade corporate debt globally will rise to 4.6% by the end of this year, up from 2.9% in March.

We’re already seeing a rise in corporate defaults. More companies globally defaulted in Q1 2023 than during any quarter since late 2020 at the peak of the government COVID lockdowns. Moody’s reported that 33 corporations it rates defaulted on their debts in the first quarter with 15 of those defaults coming in March.

What the Central Banks Giveth Central Banks Taketh Away

Central banks globally blew up this giant debt bubble with nearly two decades of artificially low interest rates. Central banks pushed rates to zero in the wake of the Great Recession and some banks, including the European Central Bank and the Bank of Japan took rates negative. Despite some efforts by the Federal Reserve to normalize rates in the mid to late 2010s, it never succeeded and had already started cutting rates due to shakiness in the economy before COVID. During the pandemic, central banks doubled down on their easy money policies.

The whole point of this monetary policy was to incentivize borrowing to “stimulate” the economy.

It worked.

Global debt hit a record $300 trillion at the end of 2022, according to data from S&P Global. That equals 349% leverage against global GDP and $37,500 of average debt for each person in the world.

Since 2000, non-financial corporate debt across America and Europe has grown from $12.7 trillion to $38.1 trillion, a 200% increase. Meanwhile, the percentage of US speculative-grade issuers of “B-” ratings and below doubled, to 36%, in September 2022 compared with September 2007.

Most people just assumed a low interest rate environment was the new normal. But in the wake of the COVID stimulus, price inflation finally caught up with the central banks, forcing them to raise interest rates.

Low-interest rates are the mother’s milk of a global economy built on easy money and debt. With interest rates rising, the bubbles are starting to pop.

What nobody seems willing to say out loud is that this problem falls squarely on the shoulders of governments and central banks. They implemented policies intended to incentivize the accumulation of debt. They created trillions of dollars out of thin air and showered the world with stimulus, unleashing the inflation monster. And now they’re trying to battle the dragon they set loose by raising interest rates. This will inevitably pop the bubble they intentionally blew up.

All of this was entirely predictable.

The US government is about to exacerbate the problem. With the debt ceiling out of the way, the US Treasury will have to go on a borrowing binge in order to replenish the cash reserves it spent while the government was up against the borrowing limit.

According to an analysis by Goldman Sachs, the US Treasury will likely need to sell around $700 billion in T-bills within six to eight weeks of a debt ceiling deal just to replenish cash reserves spent down while the government was up against the borrowing limit. On a net basis, the Treasury will likely have to sell more than $1 trillion in Treasuries this year.

The market may be able to absorb all of that paper, but it will almost certainly cause interest rates to rise even more as the sale drains liquidity out of the market.

This liquidity crunch will also spill over into the corporate bond market. The price of non-government debt instruments will have to fall as well in order to compete with Treasury bonds. That means the cost of borrowing will go up for everybody, making it harder for over-leveraged companies to refinance.

It’s likely that Deutsche Bank and other mainstream analysts are underestimating the extent of the default problem coming at us like a freight train.

It looks like the much-anticipated Ukrainian spring offensive may finally be getting underway. Yesterday, Russia repelled Ukrainian attacks in five places.

It’s very early — these were likely probing attacks looking to detect weak points in Russian defensive positions — but these attacks were much heavier than previous probing attacks.

We’ll have to see what happens.

When the main offensive comes, it’s very possible that Ukrainian forces will break through in certain areas. They might capture some territory (with plenty of U.S./NATO-supplied reconnaissance and intelligence to assist them), but it’s unlikely that their gains will be sustainable.

The offensive will probably peter out as Russian forces gradually grind it down.

Russia has several defensive lines in the region, fortified by minefields, anti-tank ditches, concrete obstacles known as dragon’s teeth, etc. These are formidable defenses that Russia has spent several months creating.

If Ukraine breaks through one line, it’ll have to confront another. And another. And another one after that.

It’s also important to realize that offensives on the scale envisioned require massive logistical support, and it’s far from clear that Ukraine has the resources to sustain a major offensive. It doesn’t help that Russia has been steadily targeting Ukrainian ammunition depots, transportation links, marshaling points, etc.

Meanwhile, Zelensky wants more Patriot missile systems. That’s because the Russians have already destroyed one-third of the systems we sent.

As I’ve argued before, Russia is winning the war. The West can’t afford to give Ukraine much more weaponry, and support for the war effort is declining.

Negotiation or Escalation

All that remains is negotiation or escalation toward nuclear war. Unfortunately, Biden will probably choose to escalate.

First he said no tanks, then he agreed to send tanks. Then he said no F-16s, now he’s agreed to send F-16s. There’s no reason to believe it’ll end there. Biden’s in way too deep to just walk away at this point.

And there’s certainly no reason to believe that Biden will relent on the anti-Russian economic sanctions. In fact, even more sanctions are being imposed.

Here’s the latest sanctions announcement from the U.S. as reported by Stratfor recently:

The United States enacted new sanctions on 69 Russian entities, one Armenian entity and one Kyrgyz entity, as well as halted the export of a wide range of up to 1,200 additional products and consumer goods to Russia, Reuters reported on May 19. The new sanctions and restrictions are part of the United States’ realization of the Group of Seven’s recent statement on Ukraine declaring the group’s intent to expand sanctions on Russia.

The measures suggest greater emphasis on blocking those who circumvent or facilitate the circumvention of sanctions, but the sanctions are unlikely to stop the emergence of new circumvention schemes or impede Russia’s ability to continue the war in Ukraine. Still, they will create new compliance risks for companies across a range of sectors from consumer goods to high technology that now must ensure that their business activities do not run afoul of the new measures.

In April, the International Monetary Fund further improved its forecast for Russia’s economy, which it sees growing by 0.7% this year, up 0.4 percentage points from the January forecast.

The Failure of Sanctions

The starting place for analysis is to realize that these anti-Russian sanctions are unprecedented as to the scope and the number of entities affected. The U.S. has frozen the bank accounts of the Russian Central Bank and a long list of Russian companies. It has kicked Russia out of the global interbank message traffic system called SWIFT.

It’s not too much to call SWIFT the central nervous system of the global financial system. Banning Russia greatly impedes the ability of their banks to make payments even if they are using currencies other than the U.S. dollar and transacting with non-U.S. banks.

U.S. companies by the thousands have closed up shop in Russia. They have either shut down their operations or temporarily suspended them. U.S. persons are prohibited from making new investments in Russia under pain of severe fines or imprisonment.

Strategic metals exports from Russia have been banned in many cases. Imports to Russia of semiconductors and other high-tech outputs and equipment have been banned. Russian oil exports by tankers have been prohibited.

This oil ban has been backed up by a separate ban on cargo and vessel insurance from major providers such as Lloyd’s of London. Without insurance, most parties won’t ship or purchase the oil.

The list goes on. New targets and sanctions are being announced continually. What has been the result of this global financial sanctions war?

It has been a complete failure. Russia is clearly winning the kinetic war on the ground in Ukraine, and it’s winning the financial war as well.

This Wasn’t in the Playbook

The Russian ruble is as strong as it was before the Russian invasion. Biden’s claim that sanctions would “destroy” the ruble was just hot air. The Russian economy declined about 3% in 2022 after critics claimed it would crash by 10% or more.

This year, Russia is projected to grow 0.7% by the IMF at a time when many analysts expect the U.S. economy to fall into a severe recession.

Russia has easily been able to evade sanctions on oil exports by using a “ghost fleet” of vessels that turn off transponders and engage in ship-to-ship oil transfers to mask the identity of the seller at the port of discharge.

There’s nothing surprising about this. Mastermind commodity trader Marc Rich did the same thing to evade oil export sanctions on Iran and Iraq in the 1990s and 2000s from his chateau in Zug, Switzerland.

The insurance bans have also proved ineffective. There are easy workarounds including self-insurance, captive insurance companies, and insurance from companies that are not participating in the boycott.

More recently, the U.S. has imposed further sanctions on two major gold mining companies in Russia. This is nonsense put on for show. Gold is an element, atomic number 79. Once it is melted and recast into generic bars it is untraceable. It can be moved secretly around the world by air and sold in markets from Shanghai to Singapore.

Gold is gold and it will go where it wants. The U.S. sanctions will have no impact except to increase costs in global trade.

The Desperation of Secondary Boycotts

Indeed, many of the most important countries in the world are maintaining a neutral stance and are not supporting U.S. sanctions. These neutral parties include India, China, South Africa, and Brazil, which collectively include almost 40% of the earth’s population.

India, China and Brazil are three of the ten largest economies in the world and collectively produce 24% of global GDP.

What’s new about the recent sanctions report quoted above is the U.S. is now getting desperate about the failure of sanctions to damage Russia or change Russian behavior in Ukraine.

The U.S. has begun imposing what are called secondary boycotts. This means that the sanctions do not target Russia directly, but target countries that do business with Russia and do not follow U.S. orders.

For example, China is reported to be selling semiconductors to Russia even as Brazil sells aircraft and India sells drones. China and India also purchase oil from Russia. It is also reported that South Africa has begun weapons sales to Russia.

All of these sales are in violation of U.S. sanctions. Reportedly, the U.S. will begin imposing separate sanctions on China, Brazil, India, and South Africa for not adhering to U.S. sanctions.

How Does This End Well?

These new secondary boycott sanctions will not be well-received. China, Brazil, India, and South Africa will not passively absorb the secondary boycotts.

They will retaliate in their own way. The tit-for-tax sanctions will not impede Russia at all, but they will lead to a further contraction of world trade, something last seen during the Great Depression.

Biden claims that the sanctions will not end until Russia withdraws entirely from Ukraine, including Crimea. Not only will Russia not withdraw, it continues to make major military and territorial gains. A Ukrainian offensive won’t fundamentally change that reality, unless it somehow manages to overcome very long odds.

This means the sanctions will continue indefinitely.

It also means Biden has created a major drag on world trade on top of the other headwinds already facing the global economy.

Investors will be well-served by allocating assets toward cash, gold, and other hard assets. These will be the real winners as the war in Ukraine drags on.

END

3,Chris Powell of GATA provides to us very important physical commentaries

Not surprising: Korea prefers dollars over gold. I guess they need the protection of the USA from North Korea.

(Reuters/GATA)

For the time being, Bank of Korea prefers dollars over gold

Submitted by admin on Tue, 2023-06-06 07:56Section: Daily Dispatches

By Jihoon Lee Reuters Monday, June 5, 2023

SEOUL, South Korea — The Bank of Korea assesses that it is more desirable to maintain its dollar liquidity than to increase gold holdings for foreign exchange reserves at this point, the central bank said.

“A cautious approach is necessary for determining whether to increase the ratio of gold in the foreign exchange reserves,” the bank’s Reserve Management Group said

Given the possibility of a global economic recession and underlying geopolitical risks, it a better to be ready to provide ample liquidity in dollars, the group said.

As reasons it also cited uncertainty of gold prices, which it said were near their latest peak, positive real interest rates, and difficulty of selling gold for liquidity purposes. …

Richard Mills: Gold revaluation and the hidden motive behind central banks’ gold buying

Submitted by admin on Tue, 2023-06-06 11:14Section: Daily Dispatches

11:15a ET Tuesday, June 6, 2023

Dear Friend of GATA and Gold:

The possibility of gold revaluation by central banks is examined this week by financial analyst Richard Mills of the Ahead of the Herd letter. Mills’ commentary is headlined “Gold Revaluation and the Hidden Motive Behind Central Banks’ Gold Buying” and its posted at his internet site here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

end

Good for him: Alex Mooney a sound money activist introduces a bill to block the Fed’s digital currency scheme

(Cortez)

Rep. Alex Mooney aims to block Fed’s digital currency scheme

Submitted by admin on Tue, 2023-06-06 16:01Section: Daily Dispatches

By JP Cortez Money Metals News Service, Eagle, Idaho Monday, June 5, 2023

A sound money champion, U.S. Rep. Alex Mooney, R-West Virginia, has introduced H.R. 3712, the Digital Dollar Pilot Prevention Act — legislation that would block the Federal Reserve from unilaterally pursuing any form of central bank digital currency scheme.

“Congress cannot give an inch when it comes to central bank digital currencies,” Mooney said. “They would threaten the liberties of law-abiding Americans and are being used by authoritarian countries right now to crack down on dissent.”

H.R. 3712 is the latest in a growing backlash to central planners’ designs to further centralize government control of currencies, including creating a greater ability to track all financial transactions, disallowing certain types of purchases, and even outright “turning off” a targeted individual’s access to money. …

H.R. 3712 is the latest in a growing backlash to central planners’ designs to further centralize government control of currencies, including creating a greater ability to track all financial transactions, disallowing certain types of purchases, and even outright “turning off” a targeted individual’s access to money. …

Submitted by admin on Tue, 2023-06-06 21:41Section: Daily Dispatches

By Ted Butler SilverSeek.com Tuesday, June 6, 2023

A set of readily-verifiable facts have combined to point to a stunning conclusion, namely, that thanks largely to enough people doing the right thing, the federal commodities regulator, the Commodity Futures Trading Commission, may have also finally done the right thing when it comes to the decades-old Comex silver price manipulation.

If my assessment is correct, the most logical conclusion is that we may be at the end of the long-running manipulation and set to rocket higher in silver prices.

Let me present the facts and leave it to you to decide for yourself. …

A set of readily-verifiable facts have combined to point to a stunning conclusion, namely, that thanks largely to enough people doing the right thing, that the federal commodities regulator, the Commodity Futures Trading Commission, may have also finally done the right thing when it comes to the decades-old COMEX silver price manipulation. If my assessment is correct, the most logical conclusion is that we may be at the end of the long-running manipulation and set to rocket higher in silver prices. Let me present the facts and leave it to you to decide for yourself.

A bit over two years ago, on March 5, 2021, I wrote an article in which I solicited public support in writing to the CFTC and to elected representatives concerning a letter I wrote to the agency about an issue I advanced for decades – the concentrated short position in COMEX silver futures (which I consistently maintained as a key to the manipulation). While there were many naysayers who countered that writing to the Commission was a waste of time, even more observers took the time to write in. Thanks to all who took the time to write in.

Fortunately, I took my own advice and also wrote to my elected officials and lucked out when through my local congressman and an extremely-competent staffer who diligently-followed up with the agency, received, two months later, an official response that shocked me. After always arguing with every single point, I raised with the CFTC about the concentrated short position in COMEX silver futures, its response this time indicated that it had shared my concerns with two of its critical divisions, Enforcement and Market Oversight.

If you take the time to read all the references and facts contained in the above two articles, I’m sure you will conclude that I have presented the case objectively to this point. But what’s this business about mission accomplished and the end of the long-running COMEX silver manipulation being at hand? It has to do with another easily-verifiable set of facts since the date of the Commission’s response (May 3, 2021) – the unprecedented decline in the concentrated short position in COMEX silver futures to this time, particularly concerning the commercial-only component of what I always considered at the core of the manipulation.

Thinking back on it, I was always intrigued by the way the Commission concluded its response to me in May 2021, namely, informing me that it could not offer further comment on what it might or might not do regarding the information I provided. This was the farthest cry possible from how it always treated my past complaints about the excessively-large concentrated short position in COMEX silver futures. But how could I possibly know whether the Commission was sincere in its response or whether it was just blowing smoke to bury the matter at hand?

Then, it dawned on me – it wasn’t words that would indicate whether the Commission was sincere or not – it was its actions; specifically, what would the concentrated short position actually do following its response? At this point, the record is quite compelling that there may have been strong action associated with the Commission’s words.

From the high-point of 65,262 contracts (326 million oz) on Feb 2, 2021 for the 4 largest COMEX shorts (which prompted me to write and encourage others to do the same in the first place), the short position of the 4 largest shorts has fallen to 36,478 contracts (183 million oz) as of the most recent COT report (May 30), and when adjusted to reflect the commercial-only component of this position, the concentrated position is down around close to 27,500 contracts (138 million oz), down close to a stunning 60% from Feb 2, 2021.

As I’ve been reporting recently (to subscribers), for the first time ever, on the recent $6 silver price rally from early March to the beginning of May, the 4 big commercial shorts on the COMEX failed to increase their concentrated short position, as they always had in the past. I took this to strongly suggest that they would not do so on the next silver rally, whenever that rally commenced. Now, that I’ve had a chance to think about the Commission’s response of May 3, 2021 and measure that response against the actual record of the sharp reduction in the concentrated short position since then, I can’t help but see the connection even stronger and I feel more assured that the days of concentrated short selling containing silver prices may be behind us.

It now seems to me that back in April-May of 2021, as the Commission was preparing to respond to my letter of March 5, it not only concluded that I was correct about the concentrated short position in COMEX silver futures being responsible for manipulating prices, it then informed the big commercial shorts to, essentially, knock it off.

Realistically speaking, had the Commission simply ordered the then-big silver shorts to cover their short positions immediately, all heck would have ensued, sending prices to the heavens. It would also have demonstrated that the Commission was negligent for decades. Instead, the Commission, most likely, gave the big commercial shorts some time (say two years) to work down their concentrated short positions. Can I certify that such a time-sensitive directive was given to the big COMEX silver shorts two years ago? Of course not, as how could I possibly be privy to such a directive? But I’ll be darned, that in hindsight, if all the facts don’t fit better than the glove in OJ’s trial.

Then why the question mark on the mission being accomplished? Because despite everything I’ve alleged (or speculated about) to this point being as real as rain and easily verified by the actual record; whether we are actually at the end of the silver manipulation is dependent on whether the former big commercials shorts add aggressively to new short positions on the next silver price rally. If they do add aggressively to shorts, that would suggest I am incorrect in what I have just written. In that case, there should be ample time to adjust my thinking and positioning, because a decent rally would have already occurred. If they don’t add aggressively to such short positions, then that rally should prove epic and we won’t have to sit around and wonder any longer about the silver manipulation.

I can’t rule out the possibility of a continued selloff, perhaps a sharp one, in the immediate period ahead; but neither is such a selloff guaranteed. Should we get yet another deliberate price rig to the downside, that will only enhance the prospects for the coming eventual rally being one for the ages.

US Corn Crop Deteriorates After Midwest Hit By Worst Drought In Decades

WEDNESDAY, JUN 07, 2023 – 06:55 AM

Farmers in Corn Belt states have been very concerned about their crops this spring as drought expands across the Heartland.

The latest weekly report from the US Department of Agriculture shows the US corn crop deteriorated by the most in nearly three years as drought conditions worsened in the Midwest.

About 64% of the nation’s corn crop was rated good-to-excellent in the weekly report, a five percentage-point plunge that was the most significant decline since August 2020. The drop was more than double of any analysts surveyed by Bloomberg.

According to the US Drought Monitor, Illinois, Indiana, Iowa, Michigan, Minnesota, Missouri, Ohio, and Wisconsin, often called the “Corn Belt” states, are experiencing “exceptional drought” to “moderate drought.” The timing of the drought, this early in the season, could stress young plants.

“Soil moisture levels decreased sharply,” the USDA’s Indiana field office noted in the report.

The drought, according to Newsweek, could be the worst in three decades “since the 1983–1985 North American drought.”

It’s still uncertain whether the report will be sufficient to stabilize Corn futures.

And maybe the drought in Corn Belt states is being exacerbated by El Nino.

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.1131

OFFSHORE YUAN: 7.1242

SHANGHAI CLOSED UP 2.42 PTS OR 0.08%

HANG SENG CLOSED UP 152.72 PTS OR 0.80-%

2. Nikkei closed DOWN 593.04 PTS OR 1.82%

3. Europe stocks SO FAR: MOSTLY GREEN

USA dollar INDEX DOWN TO 103.86 EURO RISES TO 1.0716 UP 17 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.417 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 139.61==37 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: UP// OFF- SHORE:UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.3745***/Italian 10 Yr bond yield RISES to 4.166*** /SPAIN 10 YR BOND YIELD RISES TO 3.385…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 3.693

3j Gold at $1960.45 silver at: 23.59 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 3 /100 roubles/dollar; ROUBLE AT 81.43//

3m oil into the 72 dollar handle for WTI and 77 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 139.37 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .417% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9057 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9705 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

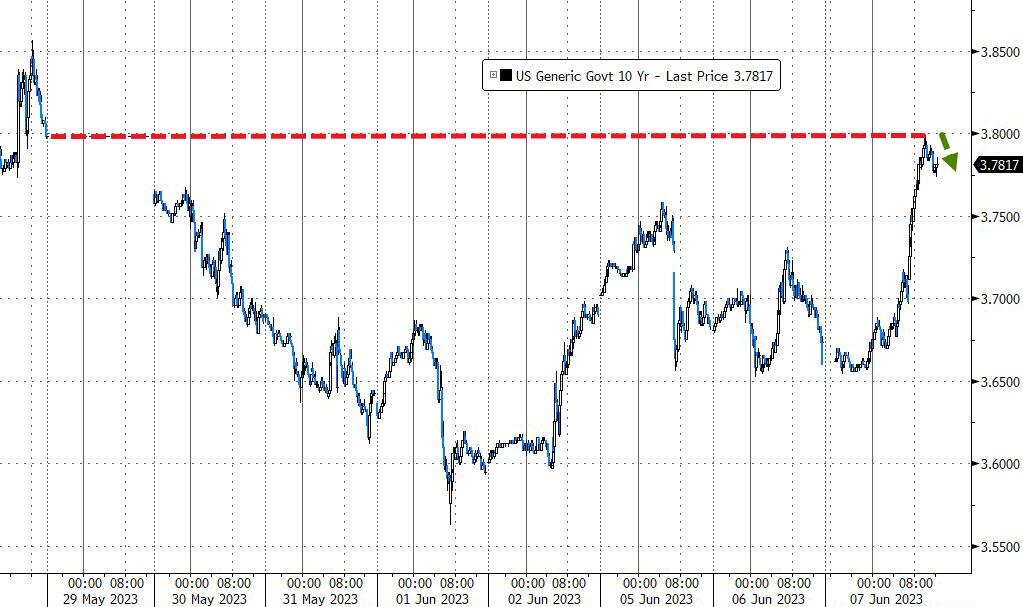

USA 10 YR BOND YIELD: 3.629 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 3.863 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.524 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 23.15…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.236 UP 3 BASIS PTS (RATES RISING RAPIDLY)

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Drift Higher Despite Sharp Drop In Chinese Exports

WEDNESDAY, JUN 07, 2023 – 08:11 AM

Futs are starting flat for a second consecutive day, having reversed earlier losses, after China reported a bigger-than-expected drop in exports and OECD warned of a weak global economic recovery. Shares are trying to build on Tuesday’s gains as a rally in megacap stocks that had propelled the S&P 500 to the edge of a bull market continued to fizzle. As of 8:00 am ET, S&P futures were modestly in the green at 4295 while Nasdaq 100 futs were up 0.2%The Bloomberg Dollar Spot Index traded near the day’s lows, boosting most Group-of-10 currencies. Treasury yields were little changed amid listless trading global bond markets. Oil and gold were flat, while Bitcoin retreats a day after climbing more than 5%. Today’s macro data includes mtge applications, trade balance, and consumer credit. Ultimately, the macro data prints are light for the balance of the week.

In premarket trading, Apple was set to extend Tuesday’s decline, falling in premarket trade along with Nvidia and Microsoft in a signal that more air is coming out of the rally in tech shares. Tech stocks continued to decline amid growing expectations that central banks will keep rates higher for longer (at least until the next big macro print), disappointing hopes they will pivot to rate cuts later this year. Here are some other notable premarket movers:

Amazon.com was upgraded to outperform from neutral at Edgewater Research, which sees a more positive outlook for the e-commerce and cloud-computing company. Shares are up as much as 0.7%.

Coinbase rises 2.2% after the crypto firm slumped 12% on Tuesday following the Securities and Exchange Commission’s lawsuit against the firm.

Dave & Buster’s rises 5.1% after the food and entertainment venue operator reported first-quarter earnings per share that beat estimates.

Herbalife slips 0.6% as Mizuho Securities initiates coverage with a neutral recommendation, saying the long-term targets of the nutrition company are achievable, but near-term visibility is limited.

Novocure Ltd. climbs as much as 5.1% as Wedbush analyst David Nierengarten raised his recommendation on the stock to neutral from underperform.

Petroleo Brasileiro SA’s US-traded shares are up 2.1% after Morgan Stanley upgraded the company to overweight from equal weight and raised the price target to $16.50 from $12.50, citing “further room for capital appreciation.”

Stitch Fix rises 7.3% as analysts note that the online clothing company’s better-than-expected revenue and cost-cutting measures could pave the way for better profitability.

Yext Inc. rallies 18% after the infrastructure-software company boosted its adjusted earnings per share guidance for the full year.

“One of the things I’m a little nervous about is that the rates market got a little too carried away about the central banks being able to quickly pre-emptively cut rates,” said Karen Ward, chief market strategist for EMEA at JPMorgan Asset Management, in an interview with Bloomberg TV. With rates markets pricing out some expected cuts, “that to me puts some of those growth, those megacap tech valuations, a little at risk,” she said.

European shares wavered, with sentiment damped by a bigger-than-expected drop in Chinese exports and an OECD warning that the global economy is set for a weak recovery, dogged by persistent inflation and restrictive central bank policies. Specifically, the OECD said a global recovery that will be weaker than expected, +2.7% for FY23 and +2.9% for FY24 vs. +3.4% average over the 7 years preceding COVID; this comes amid elevated global inflation

Euro Stoxx 50 falls 0.5%. FTSE MIB lags regionals, dropping 0.9%. Autos, insurance and chemicals are the worst-performing sectors. The FTSE 100 fluctuated after UK lender Halifax said the nation’s house prices posted their first annual decline since 2012. Hermes International was among the biggest drags on the benchmark, and was set to decline for the third straight session on Wednesday. Despite some hopes over potential stimulus, conviction on the China reopening trade has faltered, with sectors such as luxury goods among the hardest-hit. Here are some notable European movers:

Inditex shares rise as much as 6.2% to the highest since 2017 after the Zara owner reported a 1Q earnings beat and a strong start to 2Q. Analysts see potential consensus increases after the results.

Danske Bank gains as much as 5.9%, the most since October, after the Danish lender raised its key profitability target and said it will offer more than DKK50 billion in dividends by 2026.

Hugo Boss rises as much as 4.1% after UBS initiated coverage with buy and a Street-high price target, noting the firm’s turnaround story.

SBB climbs as much as 14%, extending the gains triggered after Friday’s surprise announcement that the beleaguered Swedish landlord would change its CEO.

DiscoverIE rises as much as 4.9% after the electronic components distributor reported results which analysts say demonstrate the strength of its business model, noting the firm’s positive outlook.

Assa Abloy gains as much as 4.9% after the Swedish lock and entrance systems manufacturer announced Mexican authorities gave a green light to its acquisition of hardware unit HHI.

888 Holdings rises as much as 22%, extending Tuesday’s gains, after a group of gambling-industry veterans built a stake in the owner of British betting chain William Hill.

Sectra drops as much as 10% after the Swedish medical imaging company was downgraded to sell at Carnegie, with the broker saying that the stock’s valuation has again become too high.

BE Semiconductor falls as much as 6.4%, extending a decline that started during Tuesday’s capital markets day, with analysts flagging a delay to a key product to 2027 from earlier 2025.

PGE drops as much as 3.4% after a court in Warsaw suspended the execution of the environmental decision for the company’s Turow open-pit lignite mine, allowing it to operate until 2044.

KBC dips as much as 0.7% after AlphaValue/Baader downgraded the Belgian bank to reduce as it expects margins to decline in 2024 due to rate cuts and lower loan volumes than anticipated.

“Weaker global trade is not a new story but it is surprising how quickly China’s reopening boost has faded,” said Craig Erlam, a senior market analyst at Oanda. “Pressure is set to intensify on the leadership to announce new stimulus measures in a bid to revitalize the economy again.”

Earlier in the session, Asian shares were mostly stronger following the positive handover from Wall St where the S&P 500 posted its highest close YTD and the Russell 2000 rallied amid strength in regional banks, although advances were capped as the attention in Asia turned to softer-than-expected Chinese trade data.

Hang Seng and Shanghai Comp. were positive after reports that China asked the largest banks to cut deposit rates to boost the economy and with Hong Kong led by tech strength, while price action was less decisive in the mainland after the latest Chinese trade data mostly disappointed including the wider-than-expected contraction in dollar-denominated exports.

Nikkei 225 wiped out its initial gains in an early 700-point swing and briefly dipped beneath the 32,000 level where it found some support.

ASX 200 was just about kept afloat but with the upside limited by the weaker-than-expected Australian GDP and hawkish adjustments to peak rate forecasts.

Indian stocks rallied for fourth consecutive day to hover around all-time high levels ahead of interest rate-setting panel’s decision on Thursday. The S&P BSE Sensex rose 0.6% to 63,142.96 in Mumbai, while the NSE Nifty 50 Index advanced 0.7% and both gauges closed a little short of their peak levels seen in December. Reliance Industries contributed the most to the Sensex’s gain, increasing 0.7%. Out of 30 shares in the Sensex index, 20 rose and 6 fell, while 4 were unchanged

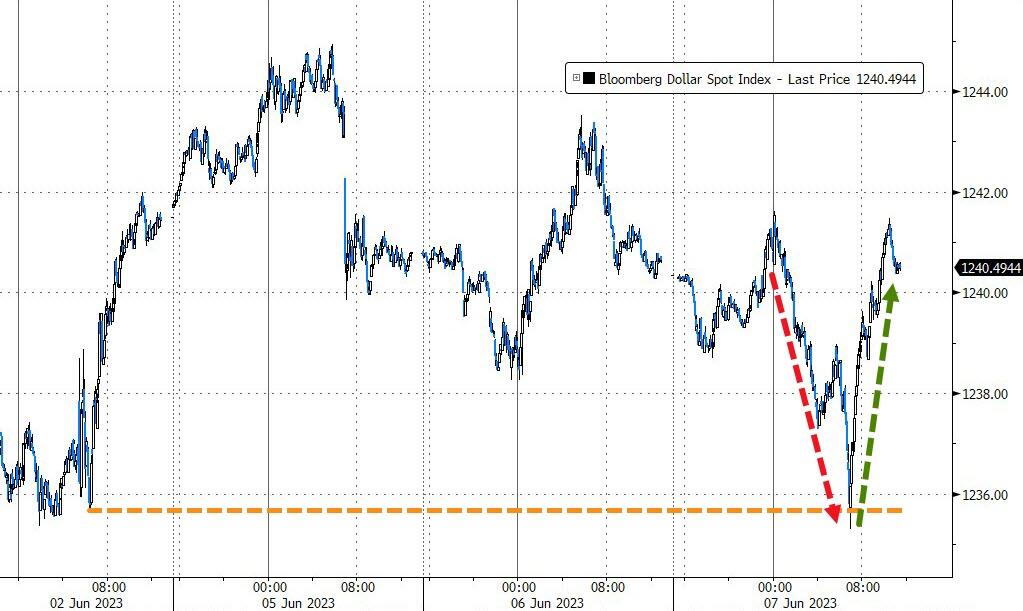

In FX, the Bloomberg dollar spot index gives up earlier gains. NZD and DKK are the weakest performers in G-10 FX, NOK and AUD outperform. the Turkey lira plunged to a record low, and is the worst-performing currency against the dollar versus expanded majors, as traders said state lenders had halted dollar sales to defend it.

In rates, treasuries are slightly cheaper across the curve with losses led by front-end and belly, flattening 2s10s, 5s30s spreads on the day. Stock futures remain inside Tuesday session range, while WTI crude oil futures advance over 1%. US session quiet for scheduled events, with minimal data, supply (except 17-week bills) and no Fed speakers expected. Yields cheaper by up to 3bp across front-end of the curve with 2s10s, 5s30s spreads flatter by 0.8bp and 2bp on the day; 10- year yields around 3.685%, cheaper by 2.5bp vs. Tuesday close with bunds and gilts outperforming by 1.5bp and 3bp in the sector

In commodities, WTI traded about 1% higher around $72.50 while ags appear to have caught a bid from the escalation of hostilities in Ukraine. Spot gold is little changed at $1,962/oz.

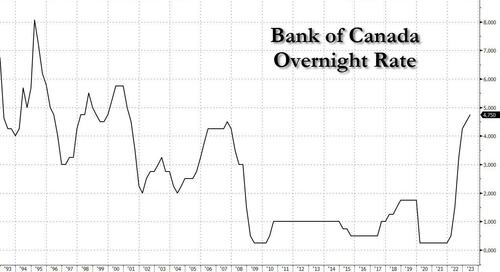

Looking at today’s calendar, at 7 a.m., we got the latest mortgage applications data (another drop, this time -1.4%), followed by April trade figures at 8:30 a.m and a consumer credit report at 3 p.m. The Bank of Canada will deliver a rate decision at 10 a.m. New York time. President Joe Biden will meet with his UK Prime Minister Rishi Sunak in Washington.

Market Snapshot

S&P 500 futures down 0.1% to 4,284.00

MXAP little changed at 163.82

MXAPJ up 0.5% to 517.07

Nikkei down 1.8% to 31,913.74

Topix down 1.3% to 2,206.30

Hang Seng Index up 0.8% to 19,252.00

Shanghai Composite little changed at 3,197.76

Sensex up 0.3% to 63,005.26

Australia S&P/ASX 200 down 0.2% to 7,117.99

Kospi little changed at 2,615.60

STOXX Europe 600 down 0.2% to 460.81

German 10Y yield little changed at 2.38%

Euro little changed at $1.0686

Brent Futures little changed at $76.30/bbl

Gold spot down 0.2% to $1,959.65

U.S. Dollar Index little changed at 104.16

Top Overnight News

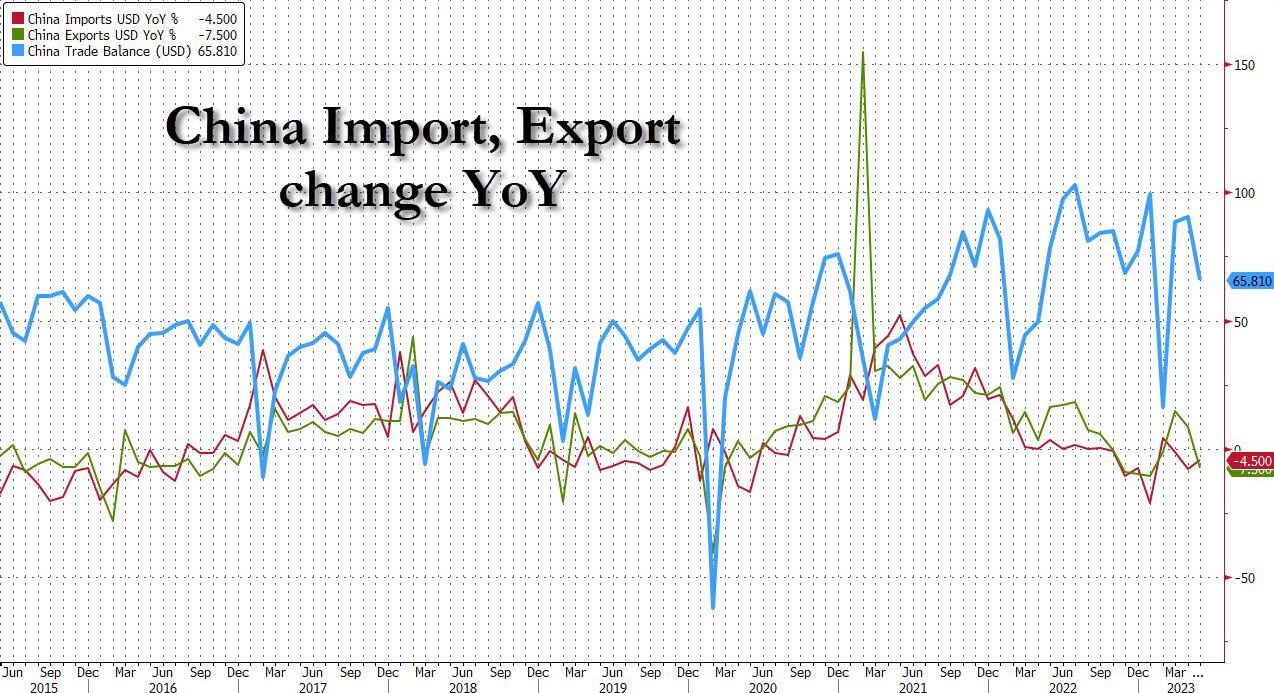

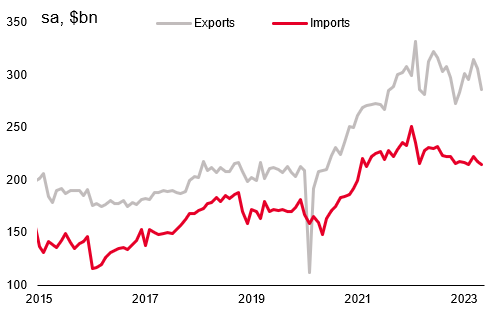

China’s May exports come in below plan, dropping 7.5% Y/Y in May (vs. the Street’s -1.8% forecast and much weaker than the +8.5% in April), although imports were a bit better (-4.5% vs. the Street’s -8%). China posts health commodity imports in May despite softer exports, with crude imports the third-highest monthly level on record. RTRS

US secretary of state Antony Blinken will travel to China this month, in the latest sign that Beijing and Washington are beginning to stabilize a turbulent bilateral relationship that had sunk to the lowest point in decades. FT

India expected to begin manufacturing GE jet-fighter engines in the country under a deal expected to be struck with Washington, part of New Delhi’s pivot away from Russian military equipment. WSJ

The Turkish lira plunged the most in more than a year as state lenders halted dollar sales to defend it, a sign the new economic administration is giving up on costly interventions. The currency fell as much as 7.2% per dollar, weakening for a 12th day. BBG

New York pushed past Hong Kong as the world’s most expensive city to live in as an expat, thanks to inflation and rising accommodation costs, while skyrocketing rents saw Singapore crash into the top five for the first time. Geneva and London remained in third and fourth places, according to the ECA International’s Cost of Living Rankings for 2023. BBG

Michael Dell’s family office plans to diversify its portfolio to absorb a payday of cash and stock worth more than $20 billion after Broadcom acquires VMware. BBG

Mike Pence kicks off his presidential campaign in Iowa, with the former VP saying “different times call for different leadership.” Pence is offering himself as the only traditional conservative who can win the nomination, defeat Biden and govern with more civility than Donald Trump. “Our party and our country need a leader that’ll appeal, as Lincoln said, to the better angels of our nature,” he said. BBG

Wells Fargo will sell an office building in San Francisco for $42.6-46MM, a steep discount to the $108MM paid for the property back in 2005. Real Deal

Reddit is cutting about 90 people, or 5% of its staff, and plans to slow hiring going forward, becoming the latest tech firm to reduce headcount. WSJ

AI: Equity investors are vigorously debating the influence generative artificial intelligence (AI) may have on the future revenue growth and profitability of companies, and the valuation of stocks. We believe further upside exists to the S&P 500 index level if investors price some potential productivity and profit boost from AI adoption. Based on a range of productivity scenarios, we estimate the benefit to S&P 500 fair value could be as small as +5% vs. current levels and as large as +14%. Read Ryan Hammond and team’s full report here.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly gained following the positive handover from Wall St where the S&P 500 posted its highest close YTD and the Russell 2000 rallied amid strength in regional banks, although advances were capped as the attention in Asia turned to softer-than-expected Chinese trade data. ASX 200 was just about kept afloat but with the upside limited by the weaker-than-expected Australian GDP and hawkish adjustments to peak rate forecasts. Nikkei 225 wiped out its initial gains in an early 700-point swing and briefly dipped beneath the 32,000 level where it found some support. Hang Seng and Shanghai Comp. were positive after reports that China asked the largest banks to cut deposit rates to boost the economy and with Hong Kong led by tech strength, while price action was less decisive in the mainland after the latest Chinese trade data mostly disappointed including the wider-than-expected contraction in dollar-denominated exports.

Top Asian News

China Stocks Woes Hamper Hong Kong IPO Recovery: ECM Watch

Blinken Plans Trip to Beijing in Bid to Stabilize US-China Ties

China Traders Are Leveraging Up The Most on Record on Flush Cash

Pakistan Bonds, Stocks Rise on Growing Optimism for IMF Loan

China’s Steel Slowdown Pushes Exports to Highest Since 2016

Air India Sends Relief Jet to Russia for Stranded Passengers