GOLD PRICE CLOSED: DOWN $10.70 TO $1945.20

SILVER PRICE CLOSED: DOWN $0.25 AT $23.73

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1943.10

Silver ACCESS CLOSE: 23.64

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

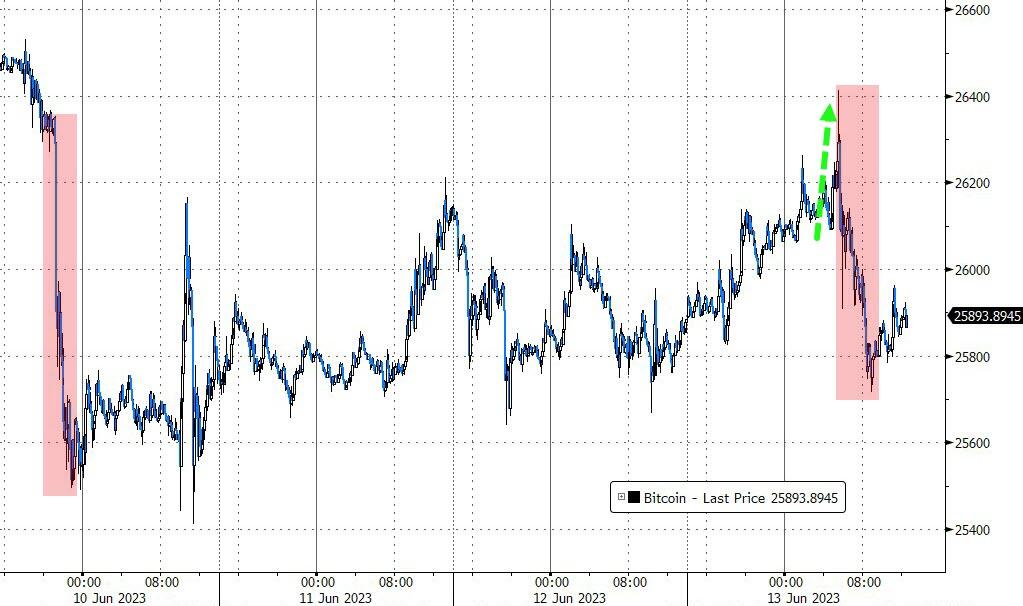

Bitcoin morning price:, $26,145 UP 329 Dollars

Bitcoin: afternoon price: $25,921 UP 104 dollars

Platinum price closing $980.75 DOWN $13.40

Palladium price; $1363,20 UP $16.35

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,587.72 DOWN 31.60 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1540,83 DOWN 25.33 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1800.40 DOWN 21.69 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JUNE 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,955.300000000 USD

INTENT DATE: 06/12/2023 DELIVERY DATE: 06/14/2023

FIRM ORG FIRM NAME ISSUED STOPPED

190 H BMO CAPITAL 8

323 C HSBC 30

323 H HSBC 9

363 H WELLS FARGO SEC 3

661 C JP MORGAN 16

661 H JP MORGAN 2

685 C RJ OBRIEN 1

686 C STONEX FINANCIA 1

690 C ABN AMRO 1

880 H CITIGROUP 9

TOTAL: 40 40

MONTH TO DATE: 18,062

JPMorgan stopped 18/40 contracts

FOR JUNE:

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2023. CONTRACT: 40 NOTICES FOR 4000 OZ or 0.1244 TONNES

total notices so far: 18,062 contracts for 1,806200 oz (56.180 tonnes)

FOR JUNE:

SILVER NOTICES: 0 NOTICE(S) FILED FOR NIL OZ/

total number of notices filed so far this month : 423 for 2,115,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $10.30

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:////A WITHDRAWAL OF 3.01 TONNES OF GOLD FROM THE GLD//

INVENTORY RESTS AT 931.44 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 25 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 465.754 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY AN ATMOSPHERIC SIZED 3508 CONTRACTS TO 149,471 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUMONGOUS SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.26 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. TAS ISSUANCE WAS AN ULTRA- HUMONGOUS SIZED 5487 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH . CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON FRIDAY NIGHT: A MONSTER SIZED 2772 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.26). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A HUGE GAIN ON OUR TWO EXCHANGES OF 3702 CONTRACTS. WE HAD 1000 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 5.0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 7.5 MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

A SMALL SIZED ISSUANCE OF EXCHANGE FOR PHYSICALS( 74 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.935 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S 10,000 OZ E.F.P. JUMP TO LONDON + 5.0 MILLION OZ EXCHANGE FOR RISK(ISSUED TODAY: TOTAL ISSUED SO FAR: 7.5 MILLION OZ)// TOTAL STANDING FOR THE MONTH 4.270 MILLION OZ + 7.5 MILLION EXCHANGE FOR RISK = 11.77 MILLION OZ// ) // HUMONGOUS SIZED COMEX OI GAIN/ SMALL SIZED EFP ISSUANCE/VI) UBER =HUMONGOUS NUMBER OF T.A.S. CONTRACT ISSUANCE (5487 CONTRACTS)//CONSIDERABLE T.A.S LIQUIDATION THROUGHOUT THE COMEX SESSION //MONDAY //

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL – CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTRACTS for 8 days, total 3983 contracts: OR 19.91 MILLION OZ (497 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 19.91 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 19.91 MILLION OZ//

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3508 CONTRACTS WITH OUR FALL IN PRICE OF $0.26 IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A TINY SIZED EFP ISSUANCE CONTRACTS: 74 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.935 MILLION OZ FOLLOWED BY TODAY’S 10,000 OZ E.F.P. JUMP+5.0 MILLION EXCHANGE FOR RISK TODAY + 2.5 MILLION EXCHANGE FOR RISK(PRIOR)//NEW TOTAL STANDING: 11.77 MILLION OZ////// .. WE HAVE A GIGANTIC SIZED GAIN OF 3582 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: AN EXTRA -TERRESTRIAL HUMONGOUS 5487//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY SESSION. THE NEW TAS ISSUANCE TODAY (5487) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 0 NOTICE(S) FILED TODAY FOR NIL OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2686 CONTRACTS TO 432,912 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED – 175 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 2686 CONTRACTS) WITH OUR $7.10 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JUNE. AT 70.79 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0.0124 TONNE E.F.P JUMP TO LONDON.: NEW TOTAL 62.843 TONNES STANDING SO FAR // + /A HUMONGOUS ISSUANCE OF 5487 T.A.S. CONTRACTS/SOME FRONT END OF TAS LIQUIDATION FRIDAY ////YET ALL OF..THIS HAPPENED WITH A $7.10 LOSS IN PRICE WITH RESPECT TO MONDAY’S TRADING.WE HAD A SMALL SIZED LOSS OF 1080 OI CONTRACTS (3.359 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1606 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 432,912

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1080 CONTRACTS WITH 2686 CONTRACTS DECREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): A HUGE 1882 CONTRACTS) AND 1606 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1080 CONTRACTS OR 3.359 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1606 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2686) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 905 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 70.79 TONNES FOLLOWED BY TODAY’S 400 OZ E.F.P. JUMP TO LONDON//// NEW STANDING FALLS TO 62.843 TONNES// /3) ZERO LONG LIQUIDATION//4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: HUMONGOUS T.A.S. ISSUANCE: 1882 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

TOTAL EFP CONTRACTS ISSUED: 17,292 CONTRACTS OR 1,729,200 OZ OR 53.78 TONNES IN 8 TRADING DAY(S) AND THUS AVERAGING: 2162 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES 53.78 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 53.78/3550 x 100% TONNES 1.520% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 53,78 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUMONGOUS SIZED 3508 CONTRACTS OI TO 149,591 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 74 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 74 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 74 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3508 CONTRACTS AND ADD TO THE 74 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 3582 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 17.91 MILLION OZ

OCCURRED DESPITE OUR $0.26 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 4.54 PTS OR 0.15% //Hang Seng CLOSED UP 32.61 PTS OR 0.50% /The Nikkei closed UP 584.65 OR 1.80% //Australia’s all ordinaries CLOSED UP 0.23 % /Chinese yuan (ONSHORE) closed DOWN 7.1503 /OFFSHORE CHINESE YUAN DOWN TO 7.1605 /Oil DOWN TO 68.32 dollars per barrel for WTI and BRENT DOWN AT 73.50 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2686 CONTRACTS DOWN TO 432,912 WITH OUR LOSS IN PRICE OF $7.10 ON MONDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1606 EFP CONTRACTS WERE ISSUED: : AUGUST 1606 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1606 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 1080 CONTRACTS IN THAT 1606 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 2686 COMEX CONTRACTS..AND THIS SMALL SIZED LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $7.10. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A HUGE 1882 CONTRACTS. THROUGHOUT LAST WEEK, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THIS SPELLS TROUBLE AHEAD AS ANOTHER RAID WILL SURELY BE UPON US!

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (62.843) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 62.843 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $7.10) //// AND WERE SUCCESSFUL IN KNOCKING A FEW SPECULATOR LONGS AS WE HAD OUR SMALL SIZED LOSS OF 1080 CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE TAS LIQUIDATION THROUGHOUT THE COMEX SESSION ON MONDAY . THE TAS ISSUED MONDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 3.359 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE. (70.709 TONNES) FOLLOWED BY TODAY’S 400 OZ EFP JUMP TO LONDON..NEW STANDING REMAINS AT 62.843 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $7.10

WE HAD – REMOVED 175 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 1080 CONTRACTS OR 108000 OZ OR 3.359 TONNES.

Estimated gold volume today:// 196,018 poor

final gold volumes/yesterday 129,496 extremely poor

//JUNE 13/ FOR THE JUNE 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 96.453 Loomis 3 kilobars . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 40 notice(s) 4000 OZ 0..1244 TONNES |

| No of oz to be served (notices) | 2142 contracts 214,200 oz 6.662 TONNES |

| Total monthly oz gold served (contracts) so far this month | 18,062 notices 1,806,200 OZ 56.180 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

Withdrawals: 1

i) Out of Loomis: 96.453 oz (3 kilobars)

Adjustments;2 all dealer to customer:

a) Out of HSBC: 10,706.283 oz

b) Out of Malca: 2411.325 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 2182 contracts having LOST 9 contracts. We had 5 contracts served on Monday so we lost 4 contracts or an additional 400 oz will not stand for gold at the comex. as these guys were EFP’d over to London where they will exercise these contracts on the T + 2 basis and take delivery over there.

The next front month after June is the non active delivery month of July. Here, July lost 6 contracts to stand at 2856 contracts.

AUGUST lost 3127 contracts down to 367,780 contracts

We had 40 contracts filed for today representing 4000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 40 contract(s) of which 2 notices were stopped (received) by j.P. Morgan dealer and 16 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2023. contract month,

we take the total number of notices filed so far for the month (18,062 x 100 oz ), to which we add the difference between the open interest for the front month of JUNE (2182 CONTRACT) minus the number of notices served upon today 40 x 100 oz per contract equals 2,020,400 OZ OR 62.843 TONNES the number of TONNES standing in this active month of June.

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (18,062) x 100 oz + (2182) [OI for the front month minus the number of notices served upon today (40)x 100 oz} which equals 2,020,400 oz standing OR 62.843 TONNES

TOTAL COMEX GOLD STANDING: 62.843 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,055,246.664 OZ 63.92 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,912,533.064 OZ

TOTAL REGISTERED GOLD: 11,654,123.196 (362.49 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 11,258,409.968 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,598,877 OZ (REG GOLD- PLEDGED GOLD) 298.565 tonnes//

END

SILVER/COMEX

JUNE 13//2023// THE JUNE 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 532,329.700 oz cnt Brinks Manfra . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 357,944.475 oz CNT Delaware HSBC |

| No of oz served today (contracts) | 0 CONTRACT(S) (NIL OZ) |

| No of oz to be served (notices) | 431 contracts (2,155,000 oz) |

| Total monthly oz silver served (contracts) | 423 Contracts (2,115,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposits

total dealer deposit: nil oz

total dealer deposits: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We had 3 deposits customer account:

i) Into CNT 1006.610 oz

ii) Into Delaware 10,192.010 oz

iii) Into HSBC: 346,745.855 oz

total customer deposits: 357,944.475 oz

JPMorgan has a total silver weight: 142,466 million oz/273.357 million =51.94% of comex .//dropping fast

Comex withdrawals 3

i) Out of Brinks: 6992.500 oz

ii) Out of CNT: 444,351.000 oz

iii) out of Manfra: 80, 986.200 oz

total withdrawals: 532,329.700 oz

adjustments: none

TOTAL REGISTERED SILVER: 27.117 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 273.353 million oz

DEALER SILVER DROPPING FAST. (moves into the 27 million oz column)

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE /2023 OI: 431 CONTRACTS HAVING LOST 2 CONTRACT(S).

WE HAD 0 NOTICES FILED ON MONDAY SO WE LOST 2 CONTRACTS OR AN ADDITIONAL 10,000 OZ WILL NOT STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF JUNE

JULY HAD A 4752 CONTRACT LOSS TO 81,411 CONTRACTS

AUGUST LOST 2 CONTRACTS TO STAND AT 28

SEPT HAS A GAIN OF 8094 CONTRACTS UP TO 56,491

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 82,197 very good /

Comex volume: confirmed yesterday:72,471 strong

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 423 x 5,000 oz = 2,115,000 oz

to which we add the difference between the open interest for the front month of JUNE(431) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2023 contract month: 423 (notices served so far) x 5000 oz + OI for the front month of JUNE (431) – number of notices served upon today (0 )x 500 oz of silver standing for the JUNE contract month equates to 4.270 million oz +7.5MILLION OZ EXCHANGE FOR RISK//NEW TOTAL: 11.77 MILLION OZ STANDING

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JUNE 13/WITH GOLD DOWN $10.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.01 TONNES FORM THE GLD///INVENTORY RESTS AT 931.44

JUNE 12/WITH GOLD DOWN $7.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.65 TONNES

JUNE 9/WITH GOLD DOWN $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.65 TONNES

JUNE 8/WITH GOLD UP $20.45 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.46 TONNES FROM THE GLD///INVENTORY RESTS AT 934.65 TONNES

JUNE 7 WITH GOLD DOWN $22.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 938.11 TONNES

JUNE 6/WITH GOLD UP $6.90 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 939.56 TONNES

JUNE 5/WITH GOLD UP $5.00 TODAY : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 938.11 TONNES

JUNE 2/WITH GOLD DOWN $24.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 938.11 TONNES

JUNE 1/WITH GOLD UP $14.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 939.56 TONNES

MAY 31/WITH GOLD UP $5.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 939.56 TONNES

MAY 30/WITH GOLD UP $14.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 26/WITH GOLD UP $.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 941.29 TONNES

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 937.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 931.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

GLD INVENTORY: 931.44 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 13/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 465.754 MILLION OZ//

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

JUNE 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF SILVER TO THE TUNE OF 550,000 OZ//INVENTORY RESTS AT 467.269 MILLION OZ

JUNE 8/WITH SILVER UP $0.63 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 7/WITH SILVER DOWN 17 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.01 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 6/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.809 MILLION OZ//

JUNE 5/WITH SILVER DOWN $.13 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 266,000 OZ FROM THE SLV////INVENTORY RESTS AT 466.809 MILLION OZ/

JUNE 2/WITH SILVER DOWN 23 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV./INVENTORY RESTS AT 467.015 MILLION OZ/

JUNE 1/WITH SILVER UP 49 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.933 MILLION OZ

MAY 31/WITH SILVER UP 37 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 367,000 OZ FROM THE SLV////INVENTORY RESTS AT 467.933 MILLION OZ//

MAY 30/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 26/WITH SILVER UP $0.44 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.306 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

CLOSING INVENTORY 465.754 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

Silver Is Significantly Underpriced Given The Looming Supply Shortage

TUESDAY, JUN 13, 2023 – 03:25 PM

Authored by Michael Maharrey via SchiffGold.com,

Given the current macroeconomic environment and the supply and demand dynamics, silver is significantly undervalued at $24 to $25 an ounce.

The bullish case for silver in the mainstream typically revolves around price inflation. There are certainly reasons to think inflation is stickier than the powers that be want to admit and that the Federal Reserve isn’t going to be able to win the inflation fight. That is bullish for both silver and gold.

But I don’t hear a lot of people in the mainstream talking about the looming supply shortage in the silver market.

In fact, the growing demand for silver in the solar power industry will likely put a significant squeeze on supply in the coming years, and the current price of silver does not reflect the likely shortages.

While the mainstream hasn’t talked much about this, people in the industry are aware of what’s going on. In an article published by Seeking Alpha, Silver Bullion Pte Ltd. CEO Gregor Gregersen mentioned that he “was intrigued by unofficial chatter about upcoming silver scarcities due to rapidly growing photovoltaic demands” during the Asia Pacific Precious Metals Conference.

We’re already seeing a squeeze on the supply of silver. While silver demand set records in every category in 2022, supply was flat with mine output falling by 0.6%. This resulted in a 237.7 million ounce market deficit in 2022.

It was the second consecutive annual deficit in a row. The Silver Institute called it “possibly the most significant deficit on record.” It also noted that “the combined shortfalls of the previous two years comfortably offset the cumulative surpluses of the last 11 years.”

This trend is not expected to reverse. As Gregersen noted, silver mine production has fallen due to a lack of investment.

Production cannot be materially increased over the short term as it can take over 10 years to commence new mining operations. Therefore, increased silver prices will not lead to increased mine production for a long time.”

Meanwhile, the demand for solar power is rising rapidly and that is going to drive the demand for silver significantly higher.

The International Energy Association (IEA) predicts that in 2023, investment in the solar power industry will exceed the amount of money flowing into oil production.

Due to its outstanding electrical conductivity, silver is an important element in the production of solar panels. It is used to conduct electrical charges out of the solar cell and into the system. Each solar panel only uses a small amount of silver, but with the demand for solar panels growing exponentially every year, those small amounts of silver add up.

According to a research paper by scientists at the University of New South Wales, solar manufacturers will likely require over 20% of the current annual silver supply by 2027. And by 2050, solar panel production will use approximately 85–98% of the current global silver reserves.

A few years ago, analysts projected that the amount of silver used in solar panels would fall. After all, silver is expensive and there is a strong incentive to find alternatives. In fact, the amount of silver used in the production of solar panels has been reduced by about 80%. But that trend is expected to reverse. The Australian paper noted that more efficient ‘N-type’ technologies now being developed require even more silver than current ‘PERC’ cells that make up more than 80%of the current market. TOPCon and SHJ panels require 30 to 80% more silver than the older technology.

Some argue demand for silver in solar energy production will eventually flatten as the industry develops cheaper alternatives to the white metal. But according to the paper, even if the industry reduces the use of silver, demand will still increase.

The results show that the current rate of reduction in silver consumption is not sufficient to avoid increasing silver demand from the PV industry and that the transition to high-efficiency technologies including TOPCon (a more advanced N-type silicon cell technology, first scaled in 2019) and SHJ (Silicon heterojunction solar cells, which are very efficient) could greatly increase silver demand, posing price and supply risks.”

Recession worries would typically dampen industrial demand for silver, but the photovoltaic industry is essentially recession-proof due to support from governments around the world. With battling climate change a priority, it is highly unlikely investment in solar power and other green energy technologies will fall, even in the midst of an economic downturn.

All of this signals a rapid increase in silver demand in an environment of constrained supply.

Economics 101 tells you that higher demand without a corresponding increase in supply will lead to increasing prices.

Silver isn’t currently priced for this dynamic.

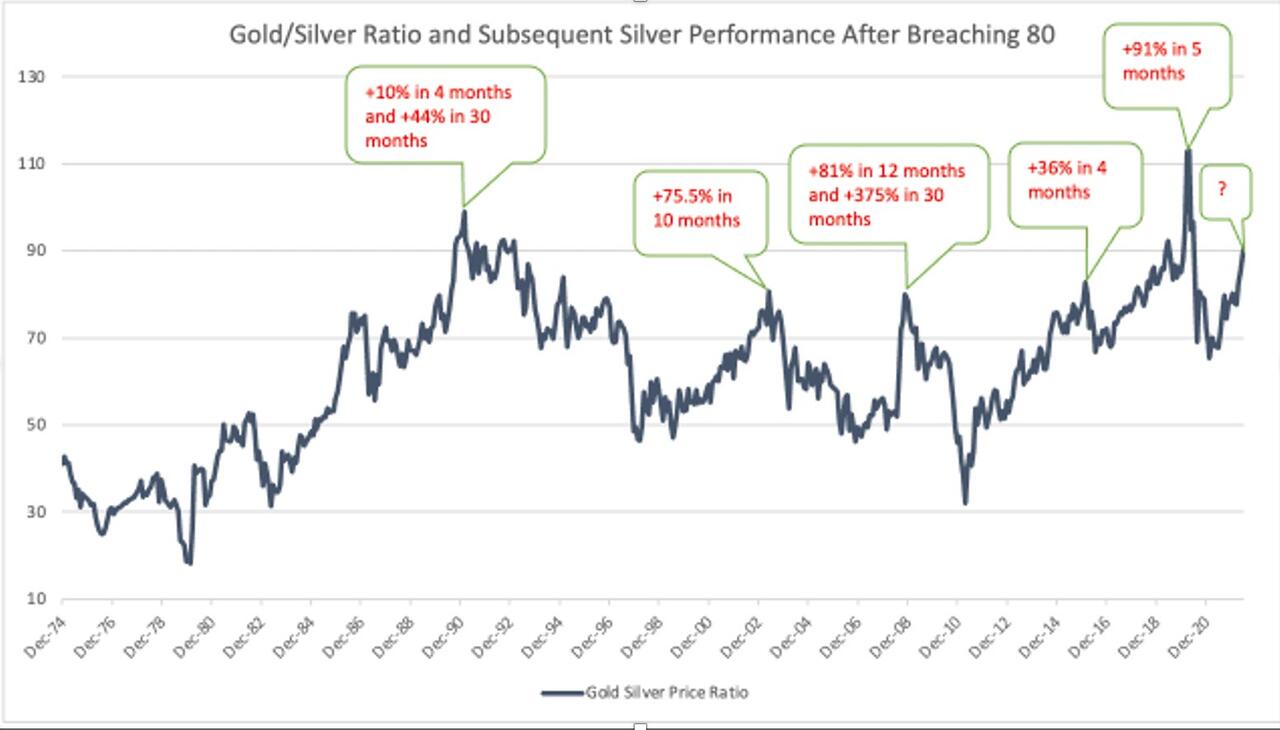

In fact, silver is significantly undervalued compared to gold.

The current silver-gold ratio is just over 81-1. That means it takes over 81 ounces of silver to buy an ounce of gold. To put that into perspective, the average in the modern era has been between 40:1 and 50:1. Historically, the ratio has always returned to that mean. And when it does, it does it with a vengeance. The ratio fell to 30-1 in 2011 and below 20-1 in 1979.

Historically, when the spread gets this wide, silver doesn’t just outperform gold, it goes on a massive run in a short period of time. Since January 2000, this has happened four times. As this chart shows, the snapback is swift and strong.

Gregersen wrote that it is only a matter of time before the mainstream picks up on the dynamics in the silver market.

In conclusion, the photovoltaic industry’s impending impact on silver pricing cannot be overlooked. As the silver shortages loom on the horizon, it is only a matter of time before mainstream media reports on these significant developments. Once the news spreads, we can anticipate substantial price surges in the silver market.”

Now is the time to buy while silver is effectively on sale.

END

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

3,Chris Powell of GATA provides to us very important physical commentaries

another decrease in SLV’s short position

(Ed Steer)

Ed Steer: Another decrease in SLV’s short position

Submitted by admin on Mon, 2023-06-12 19:31Section: Daily Dispatches

7:29p ET Monday, June 12, 2023

Dear Friend of GATA and Gold (and Silver):

The weekend edition of Ed Steer’s Gold and Silver Digest, published by GATA board member Ed Steer, is headlined “Another Decrease in SLV’s Short Position” and it’s posted in the clear at SilverSeek here:

https://silverseek.com/article/another-decrease-slvs-short-position

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4, OTHER IMPORTANT GOLD COMMENTARIES/

BRICS Gold-Backed Currency Coming in August

Tuesday, 6/13/2023 09:01

Or so this claim says…

On 22 AUGUST – about 2 months from today – the most significant development in international finance since 1971 will be unveiled, reckons Jim Rickards in The Daily Reckoning.

It involves the rollout of a major new currency that could weaken the role of the Dollar in global payments and ultimately displace the US Dollar as the leading payment currency and reserve currency.

It could happen in just a few years.

The process by which this will happen is unprecedented, and the world is unprepared for this geopolitical shock wave.

This monetary shock will be delivered by a group called the BRICS. The acronym BRICS stands for Brazil, Russia, India, China and South Africa.

This play for global reserve currency status by the BRICS will affect world trade, direct foreign investment and investor portfolios in dramatic and unforeseen ways.

The most important development in the BRICS system concerns the expansion of BRICS membership. This has led to the informal adoption of the name BRICS+ for the expanded organization.

There are currently eight nations that have formally applied for membership and 17 others that have expressed interest in joining. The eight formal applicants are: Algeria, Argentina, Bahrain, Egypt, Indonesia, Iran, Saudi Arabia and the United Arab Emirates.

The 17 countries that have expressed interest are: Afghanistan, Bangladesh, Belarus, Kazakhstan, Mexico, Nicaragua, Nigeria, Pakistan, Senegal, Sudan, Syria, Thailand, Tunisia, Turkey, Uruguay, Venezuela and Zimbabwe.

There’s more to this list than just increasing the headcount at future BRICS meetings.

If Saudi Arabia and Russia are both members, you have two of the three largest energy producers in the world under one tent (the US is the other member of the energy Big Three).

If Russia, China, Brazil and India are all members, you have four of the seven largest countries in the world measured by landmass possessing 30% of the Earth’s dry surface and related natural resources.

Almost 50% of the world’s wheat and rice production as well as 15% of the world’s gold reserves are in the BRICS. Meanwhile, China, India, Brazil and Russia are four of the nine highest-population countries on the planet with a combined population of 3.2 billion people or 40% of the Earth’s population.

China, India, Brazil, Russia and Saudi Arabia have a combined GDP of $29 trillion or 28% of nominal global GDP. If one uses purchasing power parity to measure GDP, then the BRICS share is over 54%. Russia and China also have two of the three largest nuclear arsenals in the world (the other leader is the United States).

By every measure – population, landmass, energy output, GDP, food output and nuclear weapons – BRICS is not just another multilateral debating society. They are a substantial and credible alternative to Western hegemony.

BRICS acting together is one pole of a new multipolar or even bipolar world.

When the new currency launch is announced in August, the currency will not fall on an empty field. It will fall into a sophisticated network of capital and communications. This network will greatly enhance its chances of success.

The BRICS are also developing an optical fiber submarine telecommunications system that would connect its members. It is being developed under the name BRICS Cable. Part of the motivation for BRICS Cable is to foil spying by the US National Security Agency on message traffic carried through existing cable networks.

What’s behind this quest to ditch the Dollar? In no small part the answer is US weaponization of the Dollar through the use of sanctions.

On numerous occasions from 2007-2014, I warned US officials from the Treasury, Pentagon and intelligence community that overuse or abuse of Dollar sanctions would lead adversaries to abandon the Dollar to avoid the impact of sanctions.

Such abandonment would lead to the diluted potency of sanctions, unforeseen costs imposed on the US and eventually to the collapse of confidence in the Dollar itself. These warnings were mostly ignored.

We have now reached the first and second stages of this forecast and are dangerously close to the third.

For years, the US has used sanctions to punish nations like Iran. But the sanctions the US and its allies imposed on Russia after it invaded Ukraine last year went far beyond previous sanctions regimes. They were unprecedented.

Many other nations began to conclude that they could be next if they run afoul of the US on certain issues. And that fear has greatly accelerated the push to opt out of the Dollar system entirely.

This desire is not limited to current targets such as Russia but is shared by potential targets including China, Iran, Turkey, Saudi Arabia, Argentina and many others.

The BRICS+ present a realistic effort to de-Dollarize global payments and eventually global reserves.

For years, I’ve argued that the Dollar would remain the world’s leading reserve currency for longer than most people think.

But below, I show you why a new BRICS+ currency could greatly accelerate the demise of the Dollar as the world’s leading reserve currency.

How could it happen so much faster than I previously thought?

The global desire to move away from the Dollar as a medium of exchange for international trade in goods and services is hardly new. The difference today is that it’s gone from a discussion point to a novelty to a looming reality in a remarkably short period of time.

Dubai and China have recently concluded an arrangement whereby Dubai will accept Chinese Yuan in payment for oil exports from Dubai. In turn, Dubai can use the Yuan to buy semiconductors or manufactured goods from China.

Saudi Arabia and China have been discussing similar oil- for-Yuan arrangements but nothing definitive has yet been put in place. These discussions are made complicated by Saudi Arabia’s long-standing petro-Dollar deal with the US Still, some progress along these lines is widely expected.

China and Brazil have recently reached a broad-based bilateral currency deal where each country accepts the currency of the other in trade. Meanwhile, there’s a growing strategic relationship between China and Russia as the two superpowers jointly confront the United States. In the trading relationship between the two nations, Russia can pay in Rubles for Chinese manufactured goods and other exports while China pays in Yuan for Russian energy, strategic metals and weapons systems.

Yet all these arrangements may soon be superseded by a new BRICS+ currency, which will be announced in Durban, South Africa, at the annual BRICS Leaders’ Summit Conference on Aug. 22-24.

The currency will be pegged to a basket of commodities for use in trade among members. Initially, the BRICS+ commodity basket would include oil, wheat, copper and other essential goods traded globally in specified quantities.

In all likelihood, the new BRICS+ currency would not be available in the form of paper notes for use in everyday transactions. It would be a digital currency on a permissioned ledger maintained by a new BRICS+ financial institution with encrypted message traffic to record payments due or owing by participating parties. (This is not a cryptocurrency because it is not decentralized, not maintained on a blockchain and not open to all parties without approval.)

The latest information from the BRICS working groups is that this basket valuation methodology is encountering the same problems that John Maynard Keynes encountered at the Bretton Woods meetings in 1944.

Keynes initially suggested a basket of commodities approach for a world currency he called the bancor. The difficulty is that global commodities included in any basket are not entirely fungible (there are over 70 grades of crude oil distinguished by viscosity and sulfur content among other attributes).

In the end, Keynes saw that a basket of commodities is not necessary and that a single commodity – gold – would better serve the purpose of anchoring a currency for reasons of convenience and uniformity.

Based on the impracticality of commodity baskets as uniform stores of value, it appears likely that the new BRICS+ currency will be linked to a weight of gold.

This plays to the strengths of BRICS members Russia and China, who are the two largest gold producers in the world and are ranked sixth and seventh respectively among the 100 nations with gold reserves.

These and related developments are frequently touted as the “end of the Dollar as a reserve currency.” Such comments reveal a lack of understanding as to how the international monetary and currency systems actually work.

The key mistake in almost all such analyses is a failure to distinguish between the respective roles of a payment currency and a reserve currency. Payment currencies are used in trade for goods and services. Nations can trade in whatever payment currency they want – it doesn’t have to be Dollars.

Reserve currencies (so-called) are different. They’re essentially the savings accounts of sovereign nations that have earned them through trade surpluses. These balances are not held in currency form but in the form of securities.

When analysts say the Dollar is the leading reserve currency, what they actually mean is that countries hold their reserves in securities denominated in a specific currency. For 60% of global reserves, those holdings are US Treasury securities denominated in Dollars. The reserves are not actually in Dollars; they’re in securities.

As a result, you cannot be a reserve currency without a large, well-developed sovereign bond market. No country in the world comes close to the US Treasury market in terms of size, variety of maturities, liquidity, settlement, derivatives and other necessary features.

So the real impediment to another currency as a reserve currency is the absence of a bond market where reserves are actually invested. That’s why it’s so difficult to displace Treasuries as reserve assets even if you wanted. Again, no country in the world can come close to the US in that regard.

But here’s where it gets interesting, and why the Dollar could lose its leading reserve status much faster than previously thought.

That’s because the BRICS+ currency offers the opportunity to leapfrog the Treasury market and create a deep, liquid bond market that could challenge Treasuries on the world stage almost from thin air.

The key is to create a BRICS+ currency bond market in 20 or more countries at once, relying on retail investors in each country to buy the bonds.

The BRICS+ bonds would be offered through banks and postal offices and other retail outlets. They would be denominated in BRICS+ currency but investors could purchase them in local currency at market-based exchange rates.

Since the currency is gold backed it would offer an attractive store of value compared with inflation- or default-prone local instruments in countries like Brazil or Argentina. The Chinese in particular would find such investments attractive since they are largely banned from foreign markets and are overinvested in real estate and domestic stocks.

It will take time for such a market to appeal to institutional investors, but the sheer volume of retail investing in BRICS+ instruments in India, China, Brazil and Russia and other countries at the same time could absorb surpluses generated through world trade in the BRICS+ currency.

In short, the way to create an instant reserve currency is to create an instant bond market using your own citizens as willing buyers.

The US did something similar in 1917. From 1790-1917, the US bond market was for professionals only. There was no retail market. That changed during World War I when Woodrow Wilson authorized Liberty Bonds to help finance the war.

There were bond rallies and Liberty Bond parades in every major city. It became a patriotic duty to buy Liberty Bonds. The effort worked, and it also transformed finance. It was the beginning of a world where everyday Americans began to buy stocks, bonds and securities as retail investors.

If the BRICS+ use a kind of Liberty Bond patriotic model, they may well be able to create international reserve assets denominated in the BRICS+ currency even in the absence of developed market support.

This entire turn of events – introduction of a new gold- backed currency, rapid adoption as a payment currency and gradual use as a reserve asset currency – will begin on Aug. 22, 2023, after years of development.

Except for direct participants, the world has mostly ignored this prospect. The result will be an upheaval of the international monetary system coming in a matter of weeks.

-END-

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES: CORN AND WHEAT

Wheat harvest in Kansas will be the smallest since 1957 along with corn

(zerohedge)

Kansas Wheat Harvest Will Be The Smallest Since 1957 And US Corn Is Being Absolutely Devastated By Drought

TUESDAY, JUN 13, 2023 – 08:20 AM

Authored by Michael Snyder via The Economic Collapse blog,

Significantly higher food prices are coming, because U.S. food production is going to be way below normal levels this year.

That is really bad news, because food prices are already absurdly high. In some cases, people are paying as much for a full shopping cart full of food as they did for a used vehicle in the old days. I wish that I was exaggerating, but I am not. Unfortunately, food prices are only going to go higher because farmers and ranchers are being hit extremely hard from coast to coast.

For example, it is being reported that wheat farmers in Kansas “will reap their smallest harvest in more than 60 years”…

Kansas has been called the country’s breadbasket. Now, wheat farmers in the state will reap their smallest harvest in more than 60 years.

This will go directly down the chain, from farmers to consumers at the grocery store.

Kansas normally produces more wheat than any other U.S. state by a wide margin.

But now the harvest in that state will be the smallest that we have seen since 1957…

For the last two years, a drought has withered a lot of the crop.

Now, this year’s wheat harvest in Kansas is shaping up to be the smallest since 1957. That year, the Eisenhower administration intentionally suppressed wheat production.

There were 166 million people living in the United States in 1957.

Today, there are 331 million people.

So who is going to volunteer to give up eating wheat this year so that others can consume what they normally do?

At this point, things are so bad that we are being told that flour mills in Kansas “will likely have to buy wheat grown in eastern Europe”…

Kansas flour mills will likely have to buy wheat grown in eastern Europe.

For decades, Kansas has led the nation in wheat production. The U.S. leads the world in in wheat exports, as well.

This is a major problem.

But can’t we all just eat more corn instead?

After all, corn is already in thousands upon thousands of different products that Americans consume on a regular basis.

Well, it turns out that corn production is being greatly affected by drought as well. The following comes from a Newsweek article entitled “Corn Prices Set to Soar After Midwest Hit by Worst Drought in 30 Years”…

An unusually dry May in the Midwest has raised concerns over this year’s corn crop in the Corn Belt, the region stretching from the panhandle of Texas up to North Dakota and east to Ohio which dominates the country’s corn production.

For a long time I have been warning that Dust Bowl conditions would return to the middle of the country, and now we are here.

Extremely dry conditions are being accompanied by unusually hot temperatures, and this combination is causing all sorts of havoc for corn farmers…

The USDA’s National Agricultural Statistics Service recently reported increasingly dry topsoil, poor pasture conditions in Missouri, and limited moisture for newly planted crops.

“We have very high temperatures all the way up through the northern plains of the Midwest, which impacts more than just corn and soybeans—it’s impacting other crops as well,” Curt Covington, senior director of partner relations at AgAmerica, America’s largest nonbank agricultural lender, told Newsweek.

We desperately need rain, and lots of it.

More than a third of all U.S. corn production is in areas that are currently experiencing drought, and the situation is especially dire in the “Corn Belt” states…

According to the US Drought Monitor, Illinois, Indiana, Iowa, Michigan, Minnesota, Missouri, Ohio, and Wisconsin, often called the “Corn Belt” states, are experiencing “exceptional drought” to “moderate drought.” The timing of the drought, this early in the season, could stress young plants.

Normally, if there is going to be serious drought in the middle of the country we see it later in the year.

So the fact that there is this much drought this early in 2023 is a really bad sign.

Of course it isn’t just wheat and corn farmers that are suffering…

-The size of the U.S. beef cow herd is “the smallest since 1962”.

-The orange harvest in Florida will be approximately 56 percent smaller than last year.

-Thanks to extremely bizarre weather, approximately 90 percent of Georgia’s peach crop for 2023 has been destroyed.

Most Americans don’t realize that things have gotten so bad.

If you do not know how to grow a garden, you might want to learn.

Food prices are already painfully high, and they are only going to go higher.

And this is all happening in the context of the worst global food crisis in modern history.

Hunger has been spreading around the world like wildfire, and Yahoo News is reporting that last year there was “a 33% spike in the number of people facing hunger globally”…

The 2023 Global Report on Food Crises, which published its findings last month, found that last year saw a 33% spike in the number of people facing hunger globally from the previous year, up from 193 million people in 53 countries and territories in 2021. It was also the fourth consecutive year that an increasing number of people experienced Phase 3, or above, food insecurity, which designates their situation as serious, according to the Integrated Food Security Phase Classification (IPC), a tool for improving food security analysis and decision making.

Sadly, this is just the beginning.

Due to multiple long-term trends which I discuss in my latest book, global famine has become inevitable.

No matter what decisions our leaders make now, they aren’t going to be able to keep global food production from collapsing in the years ahead.

They know this, but they don’t want everyone to freak out.

I would greatly encourage everyone to start becoming less dependent on the system and more self-sufficient.

Global food supplies are going to keep getting tighter and tighter, and once we get to a real crisis point you will want to be able to take care of yourself, your family and those that will be depending on you.

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS/TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1503

OFFSHORE YUAN: 7.1604

SHANGHAI CLOSED UP 4.54 PTS OR 0.15%

HANG SENG CLOSED UP 32.61 PTS OR 0.50%

2. Nikkei closed UP 584.65 PTS OR 1.80%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 102.88 EURO RISES TO 1.0794 UP 32 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.415 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 139.35 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN// OFF- SHORE:DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.365***/Italian 10 Yr bond yield FALLS to 4.023*** /SPAIN 10 YR BOND YIELD RISES TO 3.322…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.639

3j Gold at $1961.60 silver at: 24.17 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 40 /100 roubles/dollar; ROUBLE AT 83.68//

3m oil into the 68 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 139.55 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .415% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9064 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9784 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.722 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 3.867 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.583 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 23.67…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.434 UP 9 BASIS PTS (RATES RISING RAPIDLY)

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Hit 4400 And Reverse Ahead Of CPI Report

TUESDAY, JUN 13, 2023 – 08:08 AM

US equity futures traded sharply higher in early trading, with spoos (Sept futs contract) rising briefly above 4,400 before giving up much of their advance as traders awaited a crucial CPI print which will show pressures have cooled enough to allow the Fed to put tightening campaign on pause Wednesday and as traders assessed the impact of economic stimulus from China. As of 7:50am ET, S&P futures were flat at 4,390; Nasdaq futures were more buoyant, rising 0.3% on more positive tech news with Oracle’s earnings beat after surging 1.5% the day before to the highest level in over a year. 10Y Treasury yields are flat at 3.73% while a measure of the dollar weakens. Spot gold prices and oil are climbing, while iron ore is declining.

In premarket trading, Oracle shares rose 5% after the software company reported fourth-quarter results that beat expectations and gave a forecast for revenue growth that is ahead of the analyst consensus estimate. US-listed China stocks gained in premarket trading, with Alibaba Group Holding Ltd. rising 2% and Baidu Inc. up 4.7%, after China’s central bank unexpectedly lowered its seven-day reverse repurchase rate. Agribusiness Bunge dropped after reporting that it will buy Glencore Plc-backed Viterra in a stock-and-cash deal. Apple slipped after a downgrade from UBS Group AG. Here are some other notable premarket movers:

- Amazon.com rises 0.7% and has been at the forefront of this year’s rally in megacap technology stocks, but it’s also the furthest from regaining its record peak, suggesting to some that the shares still have room to run.

- Devon Energy is up as much as 2% after Goldman Sachs analyst Neil Mehta upgraded the energy company’s rating to buy from neutral on attractive valuation following months of underperformance.

- Manchester United shares rise as much as 31% as the bidding process for the Premier League football club heats up.

- Assurant rises 1.1% to overweight from neutral, seeing a number of near-term catalysts on the horizon for the business services company and finding the current stock price an attractive entry point for investors.

- Salesforce shares are up 0.7% following an event the software company hosted that was focused on AI. While analysts see long-term potential for Salesforce from AI, some noted the event may not have lived up to high expectations.

- Surmodics rises 3.3% as it is upgraded to buy from hold at Needham, which says the medical devices company’s SurVeil drug-coated balloon is likely to be approved sooner than expected by the US Food and Drug Administration following several positive developments.

Global stock markets are green across the globe amid talk of potential stimulus measures in China, with European stocks following their Asian counterparts higher after Wall Street closed firmly in the green on Monday.

Overnight China cut its 7-day reverse repo rates from 2% to 1.9%, the first such reduction in 10 months, raising speculation that it could trim the Loan Prime Rate next week. Separately, Bloomberg reported that China is (again) weighing broad stimulus with property support and rate cuts although this story has been floated so many times we doubt anyone actually believes it. Plans reportedly include at least a dozen measures to support domestic demand and the property sector. Interest rate reductions are also being mulled. State Council may discuss policies as soon as Friday, although may not be announced or implemented.

Meanwhile, as previewed yesterday, confidence is mounting that the latest reading of the US CPI due at 830am will show pressures have cooled enough to allow Federal Reserve policymakers to put their tightening campaign on pause Wednesday. It would mark the first time they forgo a rate hike after 10 consecutive moves in the key rate since March 2022 (read our full preview here).

Here is what the street expects the BLS will report, first the core May prints:

- Core CPI MoM is 0.4% (0.4% prior)

- Core CPI YoY 5.2% (5.5% prior).

And now the May headline CPIs:

- Headline MoM of 0.2% (prior 0.4%)

- Headline YoY 4.1% (prior 4.9%).

And here is JPM’s market reaction matrix.

“The market’s dovish expectations for the Fed’s decision later this week are closely tied to declining inflation, and any CPI figures that deviate from expectations could lead to significant repricing and impact sentiment towards riskier assets,” said Pierre Veyret, technical analyst at ActivTrades. Falling energy prices in May should offset increases in other categories to leave the headline index roughly unchanged, according to Anna Wong, Bloomberg’s chief US economist. Excluding food and energy, prices probably rose 0.3% — a deceleration from April’s 0.4% increase, she said.

That said, the market is still allowing for a possible Fed rate increase next month, with swaps showing an almost quarter-point of additional tightening priced in by the July meeting.

Interest rates in the UK, meanwhile, may still need to move higher. Figures showed that Britain’s labor market tightened unexpectedly in April, the latest evidence that the resilient economy continues to defy efforts to cool demand and inflationary pressures. The data spurred traders to ramp up bets that the Bank of England will keep raising rates. The pound strengthened.

In other news, Bank of America’s latest global survey of fund managers showed investors are “exclusively long” tech stocks amid the buzz around artificial intelligence. Long Big Tech was the most crowded trade, according to 55% of the participants, the strongest conviction since 2020.

European stocks erased their opening gains as initial optimism that China is considering a broad package of stimulus measures gave way to edginess ahead of the US inflation report due later in the day. The Stoxx 600 Index was little changed with mining and technology stocks gaining most, and real estate and utilities declining. Among individual movers, Finnish refiner Neste Oyj rose after being upgraded to outperform at RBC, while Polish e-commerce platform Allegro.eu SA fell after a group of shareholders offered a block of shares at a discount to the last close. Here are some of the most notable European movers:

- Neste gains as much as 4.9% after being raised to outperform at RBC following underperformance in the Finnish refiner’s shares and on a better growth outlook for its sustainable aviation fuel business

- Duerr shares gain as much as 4.8% after the engineering company agreed to buy BBS Automation Group from a group led by EQT at an enterprise value of €440m to €480m

- Hexagon rises as much as 6.4% after the Swedish software maker said a pact with US chipmaker Nvidia will allow its tools to be connected to Nvidia’s platform used for creating virtual spaces

- Embracer rises as much as 12%, the most since May 30, after the Swedish game- developer announced a restructuring program that will cut capital expenditure and overhead costs

- Kinepolis rises as much as 7.4%, the most since February 2022, after the movie theater operator announced after Monday’s close a share buyback program of up to €10 million

- DocMorris jumps as much as 20%, the most since February, after Germany’s Minister of Health Karl Lauterbach said digital e-prescriptions would be available nationwide starting July 1

- Allegro drops as much as 6.5%, the lowest in over a month, after a group of shareholders offered about 53m shares in the e-commerce platform to institutional buyers at PLN 32.25 apiece

- Almirall drops as much as 11% after the Spanish pharma firm said it has set the price of new shares to be issued in a capital increase at €8.2 each, representing ~5.7% discount to their last close

- Admiral drops as much as 7.4%, the most in more than three months, as Citi cuts the motor insurer to sell on an expected reset of earnings expectations and material downside risk in the 1H numbers

- CMC Markets shares drop as much as 7.3% at the open after the online trading platform’s FY results, with slower client activity weighing on its outlook and prompting PT cuts from brokers

Earlier in the session, Asian markets rose by more than 1% as China was said to consider broad stimulus measures, partially reported by Bloomberg News earlier this month. Investor speculation about looming cuts to China’s longer-term policy rates also intensified on Tuesday after the central bank unexpectedly lowered its seven-day reverse repurchase rate.

“The message is mixed: on the one hand, they surprised the market by announcing a cut in the short-term rate, but on the other, it also shows that the Chinese recovery is really weak,” said Charles-Henry Monchau, chief investment officer at Banque Syz.

- China’s Shanghai Comp. and the Hang Seng were both initially subdued despite the PBoC’s cut to its short-term interbank funding rate which raises the prospects of a cut to the MLF rate and benchmark LPR, with sentiment dampened by ongoing growth concerns and lingering frictions after the US added 43 entities to its export control list.

- Australia’s ASX 200 just about kept afloat but with upside capped after mixed data in which Westpac Consumer Confidence improved but remained near recession lows and NAB Business Confidence deteriorated.

- Japan’s Nikkei 225 resumed its outperformance and breached the 33,000 level for the first time in over three decades amid strength in automakers and with SoftBank spearheading the advances on news that Intel is to discuss being an anchor investor in the Arm IPO.