JULY 13//GOLD CLOSED UP $3.35 TO $1959.40//SILVER AGAIN HAS A STELLAR DAY UP $.64 TO $24.72//PLATINUM ROSE BY $23.30 TO $975.50 WHILE PALLADIUM WAS UP $18.30 TO $1299.95//RUSSIA VS UKRAINE UPDATES//COVID-VACCINE UPDATES/DR PAUL ALEXANDER//VACCINE IMPACT//SLAY NEWS/EVOL NEWS/NEWS ADDICTS//USA DATA: PPI TUMBLES//UNADJUSTED JOBLESS CLAIMS RISE TO 6 MONTH HIGHS//SWAMP STORIES FOR YOU TONIGHT//

190 H BMO CAPITAL 10 435 H SCOTIA CAPITAL 27 624 H BOFA SECURITIES 3 690 C ABN AMRO 30 14 737 C ADVANTAGE 12 8

JPMorgan stopped 0/52 contracts.

FOR JULY:

GOLD: NUMBER OF NOTICES FILED FOR JULY/2023. CONTRACT: 52 NOTICES FOR 5200 OZ or 0.1462 TONNES

total notices so far: 2386 contracts for 238,600 oz (7.4214 tonnes)

FOR JULY:

SILVER NOTICES: 126 NOTICE(S) FILED FOR 630,000 OZ/

total number of notices filed so far this month : 3971 for 19,855,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $3.35

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES OF GOLD FROM THE GLD/

INVENTORY RESTS AT 914.66 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP $0.64 AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 462.941 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY AN UNBELIEVABLY HUGE SIZED 5224 CONTRACTS TO 125,506 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR HUGE $1.00 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. TAS ISSUANCE WAS A GIGANTIC SIZED 1166 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH . CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 1166 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $1.00). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A HUMONGOUS ATMOSPHERIC GAIN ON OUR TWO EXCHANGES OF 7499CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 0MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS( 2275 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 16.110 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S HUGE 545,000 OZ QUEUE JUMP.//NEW STANDING: 20.690 MILLION OZ/ // HUGE SIZED COMEX OI GAIN/ HUGE SIZED EFP ISSUANCE/VI) HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE (1166CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL – 940 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTRACTS for 7 days, total 4808 contracts: OR 24.040 MILLION OZ (686 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 24.040 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 24.040 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5224 CONTRACTS WITH OUR HUGE GAIN IN PRICE OF $1.00 IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 2275 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 16.110 MILLION OZ FOLLOWED BY TODAY’S HUGE 545,000 OZ QUEUE JUMP: TOTAL NOW STANDING 20.690 MILLION OZ///// .. WE HAVE A HUGE ATMOSPHERIC SIZED GAIN OF7499 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 1166//ZERO FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION. THE NEW TAS ISSUANCE TODAY (1166) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 126 NOTICE(S) FILED TODAY FOR 630,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUGE ATMOSPHERIC SIZED 22,071 CONTRACTS TO 505,241 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED: 1435 CONTRACTS

WE HAD A HUGE SIZED INCREASE IN COMEX OI ( 22,071 CONTRACTS) WITH OUR $24.50 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JULY. AT 5.1975 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0.1462 TONNE QUEUE JUMP: NEW TOTAL OF GOLD STANDING FOR JULY: 7.4401 TONNES// + /AN UNBELIEVABLY HUGE (AND CRIMINAL) ISSUANCE OF 29,245 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $24.50 GAIN IN PRICEWITH RESPECT TO WEDNESDAY’S TRADING.WE HAD AN ATMOSPHERIC SIZED GAIN OF 24,749 OI CONTRACTS (72.979 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2678CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 505,241

IN ESSENCE WE HAVE A HUGE SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 24,749 CONTRACTS WITH 22,071 CONTRACTS INCREASED AT THE COMEX// AND A FAIR 2678 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 24,749CONTRACTS OR 76.979 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A HUGE 29,245 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2678 CONTRACTS) ACCOMPANYING THE HUGE ATMOSPHERIC SIZED GAIN IN COMEX OI (22,071) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 24,749 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 5.1975 TONNES FOLLOWED BY TODAY’S 0.1462 TONNE QUEUE JUMP//NEW TOTAL 7.4401 TONNES ///// /3) ZERO LONG LIQUIDATION//4) HUGE SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: UNBELIEVABLY HUGE T.A.S. ISSUANCE: 29,245 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

TOTAL EFP CONTRACTS ISSUED: 14,390 CONTRACTS OR 1,439,000 OZ OR 44.76 TONNES IN 7 TRADING DAY(S) AND THUS AVERAGING: 2055 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES 44.76 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 44.76/3550 x 100% TONNES 1.26% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 44.76 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED GAIN OF 5524 CONTRACTS OI TO 125,606 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 2275 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 2275and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2275 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 5224 CONTRACTS AND ADD TO THE 2275 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 7499 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 37.495 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED UP 40.34 PTS OR 1.26% //Hang Seng CLOSED UP 489.69 PTS OR 2.60% /The Nikkei CLOSED UP 475.40 OR 1.49% //Australia’s all ordinaries CLOSED UP 1.55 % /Chinese yuan (ONSHORE) closed UP 7.1632 /OFFSHORE CHINESE YUAN UP TO 7.1705 /Oil UP TO 75.84 dollars per barrel for WTI and BRENT UP AT 80.12 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY AN UNBELIEVABLY HUGE SIZED 22,041CONTRACTS UP TO 505,241 WITH OUR GAIN IN PRICE OF $24.50 ON WEDNESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2678 EFP CONTRACTS WERE ISSUED: : AUGUST 2678 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2678 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: AN ATMOSPHERIC SIZED TOTAL OF 24,749 CONTRACTS IN THAT 2678LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GIGANTIC SIZED GAIN OF 22,041 COMEX CONTRACTS..AND THIS HUGE SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $24.50//WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS AN UNBELIEVABLY HUGE 29,245 CONTRACTS (THIRD DAY IN A ROW). THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (7.4401) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 7.4401 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $24.50) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD AN ATMOSPHERIC SIZED GAIN OF 24,749 CONTRACTS ON OUR TWO EXCHANGES. WE HAD ZERO TAS LIQUIDATION THROUGHOUT THE WEDNESDAY COMEX SESSION. THE MASSIVE TAS ISSUED WEDNESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 81.44PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY. (5.11974 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 0.1462 TONNES//TOTAL STANDING FOR JULY GOLD: 7.4401 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $24.50.

WE HAD – REMOVED 1435 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 24,749 CONTRACTS OR 2,474,900 OZ OR 76.979 TONNES.

Total monthly oz gold served (contracts) so far this month

2386 notices 238,600 OZ 7.421 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

1 dealer deposit:

i)Into Brinks dealer: 99.400 oz

total dealer deposits: 99.400 oz

total customer deposits: 0 oz

we had 1 customer withdrawals:

i) Out of Brinks 419,11 oz

total withdrawals: 419,16 oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 59 contracts having LOST 0 contracts. We had 47 contracts served on Wednesday. Thus we gained 47 contracts or an additional 4700 oz of gold will stand at the comex.

AUGUST LOST 4718 contracts DOWN to 305,818 contracts

SEPT gained 92 contracts to stand at 545

We had 52 contracts filed for today representing 5200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 52 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2023. contract month,

we take the total number of notices filed so far for the month (2386 x 100 oz ), to which we add the difference between the open interest for the front month of JULY (59 CONTRACT) minus the number of notices served upon today 52 x 100 oz per contract equals 239,200 OZ OR 7.4401 TONNES the number of TONNES standing in this NON active month of July.

thus the INITIAL standings for gold for the JULYcontract month: No of notices filed so far (2386) x 100 oz + (59) {OI for the front month} minus the number of notices served upon today (53) x 100 oz) which equals 239,200oz standing OR 7.4401 TONNES

TOTAL COMEX GOLD STANDING: 7.4401 TONNES WHICH IS STRONG FOR A NON ACTIVE DELIVERY MONTH.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,282,501.863 OZ

TOTAL REGISTERED GOLD: 11,833,484.390 (368.07 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,449,017.473 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,954,210 OZ (REG GOLD- PLEDGED GOLD) 309.617 tonnes//

END

SILVER/COMEX

JULY 13

//2023// THE JULY 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

824,228.228 oz LOOMIS MANFRA

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

NIL oz

No of oz served today (contracts)

126 CONTRACT(S) (630,000 OZ)

No of oz to be served (notices)

167 contracts (835,000 oz)

Total monthly oz silver served (contracts)

3971 Contracts (19,855,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposits

total dealer deposit: 0 oz

total dealer deposits: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 deposits customer account:

total customer deposits: nil oz

JPMorgan has a total silver weight: 139.982 million oz/277.015 million =50.39% of comex .//dropping fast

Comex withdrawals 2

i) Out of Loomis: 720,884.900 oz

ii)Out of Manfra: 103,343.328 oz

adjustments: 1..customer to dealer Manfra

i) 558,124.400 oz

TOTAL REGISTERED SILVER: 34.992 MILLION OZ//.TOTAL REG + ELIGIBLE. 277.015 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY /2023 OI: 293 CONTRACTS HAVING LOST 198 CONTRACT(S). WE HAD 307 NOTICES FILED ON WEDNESDAY SO WE GAINED A STRONG 109 CONTRACTS OR AN ADDITIONAL 545,000 OZ WILL STAND AT THE COMEX FOR DELIVERY IN JULY.

AUGUST GAINED 33 CONTRACTS TO STAND AT 644

SEPT HAS A GAIN OF 4753 CONTRACTS UP TO 107,746

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 126 for 630,000 oz

Comex volumes// est. volume today 85,421 strong /

Comex volume: confirmed yesterday: 85,460 STRONG

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 3971 x 5,000 oz = 19,855,000 oz

to which we add the difference between the open interest for the front month of JULY(293) and the number of notices served upon today 126 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2023 contract month: 3971 (notices served so far) x 5000 oz + OI for the front month of JULY (293) – number of notices served upon today (126 )x 500 oz of silver standing for the JULY contract month equates to 20.690 million oz +

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JULY 13/WITH GOLD UP $3.30 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.66 TONNES

JULY 12/WITH GOLD UP $24.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.95 TONNES

JULY 11/WITH GOLD UP $6.15 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.0 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 915.26 TONNES

JULY 10 WITH GOLD DOWN $1.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.60 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 916.26 TONNES.

JULY 7 WITH GOLD UP $16.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.86 TONNES.

JULY 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 917.86 TONNES

JULY 5/WITH GOLD DOWN $2.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 2.6 TONNES FROM THE GLD///INVENTORY RESTS AT 921.90 TONNES

JULY 3/WITH GOLD UP $1.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.50 TONNES//

JUNE 30/WITH GOLD UP $10.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 924.50 TONNES

JUNE 29/WITH GOLD DOWN $3.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.81 TONNES

JUNE 28/WITH GOLD DOWN $1.15 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 925.65 TONNES

JUNE 27/WITH GOLD DOWN $9.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD./INVENTORY RESTS AT 925.65 TONNES

JUNE 26/WITH GOLD UP $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD/////INVENTORY RESTS AT 927.10 TONNES

JUNE 23/WITH GOLD UP $5.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: WITHDRAWALS OF 4.33 TONNES OF GOLD OVER THE PAST TWO DAYS. /INVENTORY RESTS AT 929.70 TONNES

JUNE 21/WITH GOLD DOWN $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 934.03 TONNES

JUNE 20/WITH GOLD DOWN $22.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.03 TONNES

JUNE 16/WITH GOLD UP $0.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.03 TONNES

JUNE 15/WITH GOLD UP $2.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 929.70 TONNES

JUNE 14/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 931.44 TONNES

JUNE 13/WITH GOLD DOWN $10.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.01 TONNES FORM THE GLD///INVENTORY RESTS AT 931.44

GLD INVENTORY: 914.66 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 13/WITH SILVER UP 64 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 12/WITH SILVER UP $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.881 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 11/WITH SILVER DOWN 5 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .020 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 464.822 MILLION OZ/

JULY 10/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.672 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 464.802 MILLION OZ

JULY 7/WITH SILVER UP 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.474 MILLION OZ

JULY 6/WITH SILVER DOWN 50 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.667 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.474 MILLION OZ//

JULY5/WITH SILVER UP 30 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JULY 3/WITH SILVER UP 7 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JUNE 30/WITH SILVER UP 19 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.377 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT468.141 MILLION OZ//

JUNE 29/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.763 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.764 MILLION OZ//

JUNE 28/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.527 MILLION OZ//

JUNE 27/WILVER SILVER UP 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 734,000 OZ INTO THE SLV////INVENTORY RESTS AT 470.527 MILLION OZ

JUNE 26/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 469.793 MILLION OZ.

JUNE 23/WITH SILVER DOWN 9 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A NET DEPOSIT OF 6.61 MILLION OZ INTO THE SLV OVER THESE PAST TWO DAYS//INVENTORY RESTS AT 469.793 MILLION OZ//

JUNE 21/WITH SILVER DOWN $.40 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.784 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 20/WITH SILVER DOWN 89 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 16/WITH SILVER UP 23 CENTS TODAY :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 463.183 MILLION OZ

JUNE 15/WITH SILVER DOWN 17 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.377 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 463.642 MILLION OZ//

JUNE 14/WITH SILVER UP 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 735,000 OZ FROM THE SLV///INVENTORY RESTS AT 465.019 MILLION OZ//

JUNE 13/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 465.754 MILLION OZ//

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

CLOSING INVENTORY 462.941 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

Jim Grant: We Could Be Heading Toward A Generational Bear Market In Bonds

Financial commentator and investment guru Jim Grant has similar concerns. In a recent interview on Odd Lots Podcast, Grant said he thinks we’re at the beginning of a long-term trend of a weak bond market with higher interest rates that could last decades.

The Federal Reserve has pushed its fund rate to over 5% to fight inflation, but Grant called the central bank “dogmatic” and its inflation-fighting toolbox “rusty.”

There’s a bureaucratic dogmatism in the Fed. They’ve got these algebraic models, my goodness, how formidable they look on a blackboard, but they don’t actually function very well so far as the future’s concerned. And the Fed was in fact, dogmatic through 2021 into 2022 buying mortgages recently, I think up to March 2022. So you asked about their inflation-fighting tools? They’re rusty.”

Grant was asked why we haven’t seen interest rate hikes have more impact on the economy. Housing prices have dropped, but not substantially. Americans are still piling up credit card debt. The economy appears to be limping along just fine.

Grant said that he thinks something is going to break — it’s just a matter of time.

I was of the view that try as Jay Powell might to emulate Paul Volcker, Mr. Powell is not working with Paul Volcker’s economy. There is much more debt, therefore much more fragility.”

Grant cited the big increase in private credit as an example.

People are head over heels over private credit. They contend that this is a not quite Nvidia-quality breakthrough in the history of finance. But it’s up there. And, but you know, private credit is a manifestation of the imperative to build leverage — whether it’s on the federal level or the corporate level, not quite so much, in recent years, on the individual level. So there’s a lot of leverage. And I would say Tracy with respect to the paradox of nothing breaking much yet, just be patient. I expected it might.”

Grant pointed out that what is inevitable is always certain. But it’s not always punctual.

I look back on some of my work there and I was rather impatient for the inevitable difficulties and crises attending upon this credit creation jag. I thought certainly it was gonna happen like Tuesday or so. So it’s like the elapsed time between the first signs of house prices going way above trend on the one hand and the onset of the housing-related credit difficulties of 2007, 2008 and 2009. That period of six years was approximately 20 years in journalistic time if you were a little bit too insistent upon.”

Jim was asked when we hit a tipping point when financial solutions to financial problems are no longer viable. He said, “A tipping point was six years ago.”

It was a long time ago, but it did not tip. So why can’t it go on forever, I don’t know? They’re always these excesses that do crop up. They are met with additional stimulus intervention, manipulation. And still we go on. Who was it who said there is a deal of ruin in a country? I guess it was Adam Smith. And there’s a great deal of ruin, so to speak, in finance and manipulated finance. And one of the singularities of the present time is the American position in international finance. You know, this country emits the reserve currency, which means that we consume much more than we produce. We finance the difference with dollar bills that only we can lawfully print at a most reasonable price of like nothing. And we remit the dollars to our creditors, mainly in Asia, say, and those dollars don’t leave the country because they come back in the shape of Treasuries and mortgages purchased for the portfolio interests of our accreditors. So that is kind of a new thing in the long historical sweep. It’s not so new in terms of years, but in terms of phenomena, the reserve currency country being a chronic big debtor, that’s kind of a different thing. Reserve currency country living on the kindness of strangers, so to speak. That’s not exactly writ. The more one learns, the less dogmatic one becomes about timing, certainly.”

Grant addressed the recent run-up in stocks despite the high-interest rate environment and hawkish Fed rhetoric. He said it’s due to “the muscle memory of a generation of 0% interest rates and all-you-can-eat credit.”

The great all-you-can-eat credit buffet table was open for business for 10 years. Interest rates fell from 1981 until a couple of, actually a couple of weeks ago. It’s called 40 years. So that’s a lot of muscle memory. Central banks have intervened predictably until fairly recently when markets shuttered. Look what happened in 2019. You know, the repo market, this obscure recondite thing caught a head cold in September and the Fed resumes QE and said it’s not QE. Yeah, it was QE. So naturally people assume that the upside is the side to be on. It takes a true contrarian, almost a bloody-minded contrarianiess to butt one’s head against that. But it’s a living. So why do people do it? Because A) because cyclical memories are short and cycles are recurrent, and B) because it has ‘worked’ — that phrase ought to be in quotes.”

Grant said he thinks we’re about to enter “a long cycle of rising interest rates” and a “generational” bear market in bonds.

The great question of whether rates are mean or reverting? So what characterizes interest rate movements is their generation length phasing, not necessarily cycles, but there are phases.

Interest rates fell for the last quarter of the 19th century, rose for the first 20 years of the 20th, fell from 1920, ‘46 rose in ‘46 to ‘81, fell from ‘81 to, call it, 2021. So at each juncture there was some mark of excess, some mark of speculative excess blow-off. Certainly in 1981, you know, a 20%+ funds rate seemed excessive. A 14% yield in 1984 in long bond when the CPI was printing at four or five, that seemed excessive. 10 percentage points of real yield — that seemed a lot.

So I speculate that we are embarked on a long cycle of rising rates. And I say that first of all, for reasons of pattern recognition, there’s no theory behind it. But I observe that in 2020 and ‘21, some unimaginably large number of debt securities were priced to yield less than nothing. Bloomberg keeps this particular figure. And I bet still, perhaps you could check me on this, I bet still there’s like a hundred billion of bonds priced to yield less than nothing worldwide. But there were $18 trillion, I think at the peak.

The most extraordinary expression of unqualified bullishness on an asset class because it had the name of “bonds” which had been falling in yield, rising in price. So no, it would not surprise me at all if we were embarked on something resembling a generation length bear market in bonds, meaning rising yields and falling prices that would fit the form.

3,Chris Powell of GATA provides to us very important physical commentaries

Brien Lundin: Central banking’s end game is here, so join us in New Orleans

Submitted by admin on Wed, 2023-07-12 18:19Section: Daily Dispatches

You’ll join GATA’s Bill Murphy and Chris Powell.

* * *

6:23p ET Wednesday, July 12, 2023

Dear Friend:

I’m writing you today with excitement and urgency — because we’ve just opened registration for this year’s New Orleans Investment Conference, to be held Wednesday through Saturday, November 1-4, and it may be the most eagerly awaited event in our 49-year history.

Here’s why: The end game Is here.

If you have been reading my newsletters and posts over the past year, you know I’ve been tracking the four-decade-plus trend of ever-easier money from the Federal Reserve and other central banks.

Ever since Paul Volcker raised rates and killed off inflation in the early 1980s, every economic hiccup, from mere slowdowns to all-out crises, has been met by monetary easing. But this is important: In each instance, interest rates were lowered but the central bankers were never able to raise them back to near the previous range.

The result was that the markets and the economy became addicted to ever-easier money.

Thus, they needed so much more as the Great Financial Crisis erupted in 2008 — and they got it: The Fed drove rates to zero and began printing money through quantitative easing, sending the Fed’s balance sheet up to $4.5 trillion over the next five years.

Then came Covid — and the Fed duplicated everything it did after 2008, but instead of five years, the Fed did it all in about five days!

So with the next crisis — which we all know is coming — the Fed is going to absolutely blow the doors off.

Here’s why I’m writing you now: The next big event that forces the Fed to open the monetary floodgates lies ahead, and likely much sooner than most expect.

Whether it’s simply the expected recession that so many indicators are pointing toward, or something breaking in the stock market, the bond market, or the banking sector, we know it’s coming.

And when it arrives, the Fed will be forced to do much more easing than it ever did before — catapulting gold, silver, commodities, and mining stocks to dizzying heights.

This is why I’m assembling the perfect roster of experts to not only analyze what’s going on, but also predict what’s about to happen and give you specific, actionable advice to profit.

Consider those who have told us they’re coming to talk to you so far:

Jim Rickards, Danielle DiMartino Booth. Lyn Alden. George Gammon. Rick Rule. Dominic Frisby. Brent Johnson. Dave Collum. Peter Boockvar. James Stack. Peter Schiff. Jim Iuorio. Tavi Costa. Adrian Day. Adam Taggart. The Real Estate Guys. Gwen Preston. Brent Cook.

Also, Mark Skousen. Nick Hodge. Bob Prechter. Chris Powel. Economic Ninja. Albert Lu. Gary Alexander. Dana Samuelson. Jeff Hirsch. Steve Hochberg. Mary Anne and Pamela Aden. Bill Murphy. Gerardo Del Real. Omar Ayales. Rich Checkan. Keith Weiner. …

… and, of course, yours truly!

We’ll also have a special in-person briefing by none other than Matt Taibbi, the renowned journalist who broke open the Twitter files and Russian collusion scandals.

If you want to know how the Deep State is trampling your liberties, and their next steps, you won’t want to miss this exclusive report from Taibbi, just for New Orleans Conference attendees.

Again, there’s much more to come, since we’’e still in the early stages of planning this year’s event, and I’ve got some more big surprises in store.

But even at this early date, one thing seems certain: New Orleans 2023 is going to be a blockbuster.

We are now opening registration for New Orleans 2023 — and I urge you to be among the first to secure your place.

You see, I don’t think I remember an investment event as eagerly awaited as this one.

Everything is pointing toward a major new bull run in metals and commodities. Interest rates are peaking and gold and bonds are beginning to look past the pause toward the next inevitable turn downward in the rate cycle.

When that happens, the metals are going to soar, and the strategies and picks you’ll get at New Orleans ’23 should multiply those gains.

I fully expect our entire hotel room block to sell out this year, so you’ll have to act soon to make sure you’ll get in.

Now consider this: By registering now, you’ll not only guarantee your place at New Orleans ’23, but you’ll also save up to $500 from the full registration fee.

Delaying will only cost you money. Just click on the link below to learn more and join us in New Orleans:

The U.S. SEC filed a lawsuit against the bankrupt crypto lender on July 13 followed by news reports about the arrest of the former CEO Alex Mashinsky.

The SEC alleges that Celsius and Mashinsky “misrepresented Celsius’s central business model and the risks to investors by claiming that Celsius did not make uncollateralized loans, the company did not engage in risky trading, and the interest paid to investors represented 80% of the company’s revenue.”

The SEC is demanding that Mashinsky be prohibited from buying, offering, or selling cryptocurrencies, to be disgorged of “all ill-gotten gains in the form of any benefits of any kind derived from the illegal conduct alleged” in the complaint, and for the former CEO pay civil penalties to be determined by the court.

The former CEO was reportedly arrested after a probe into the company’s collapse, reported Bloomberg citing people familiar with the matter.

Mashinsky was found guilty by investigators at the Commodity Futures Trading Commission, which concluded that the former CEO broke numerous U.S. regulations before the company’s implosion in 2022.

The investigation against the troubled crypto lender began after New York Attorney General sued Mashinsky on Jan. 5.

The NYAG alleged that the former CEO misled investors and caused billions of dollars in losses.

The trouble for Celsius and its former CEO began in June last year when the crypto lender abruptly suspended withdrawals on the platform.

On June 16, 2022, securities regulators from five different U.S. states opened an investigation into Celsius, and within a month, the platform filed for bankruptcy.

The arrest of Mashinsky and the lawsuit against Celsius comes within months of the SEC’s lawsuits against crypto exchanges Binance and Coinbase.

Celsius network didn’t immediately respond to Cointelegraph’s requests for comments.

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1632

OFFSHORE YUAN: UP TO 7.1705

SHANGHAI CLOSED UP 40.34 PTS OR 1.26%

HANG SENG CLOSED UP 48.69 PTS OR 2.60%

2. Nikkei closed UP 475.40 PTS OR 1.49%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 99.87 EURO RISES TO 1.1176 UP 35 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.461 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 138.45/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ON SHORE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.4475***/Italian 10 Yr bond yield FALLS to 4.126*** /SPAIN 10 YR BOND YIELD FALLS TO 3.484…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.856

3j Gold at $1959.75 silver at: 24.27 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 96 /100 roubles/dollar; ROUBLE AT 89.91//

3m oil into the 75 dollar handle for WTI and 80 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 138.45// 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO 0.461% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8627 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9642 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.825 DOWN 4 BASIS PTS…

USA 30 YR BOND YIELD: 3.932 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.664 DOWN 8 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.16…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 15 BASIS PTS AT 4.5005

end

2. Overnight: Newsquawk and Zero hedge:

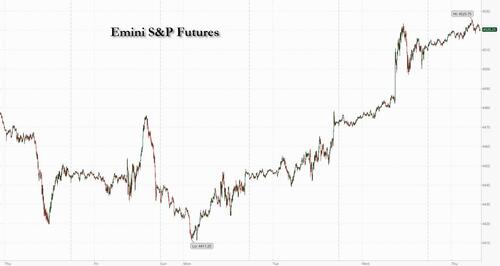

Futures Hit Fresh 52 Week High, Dollar Sinks In Global Post-CPI Rally

THURSDAY, JUL 13, 2023 – 08:12 AM

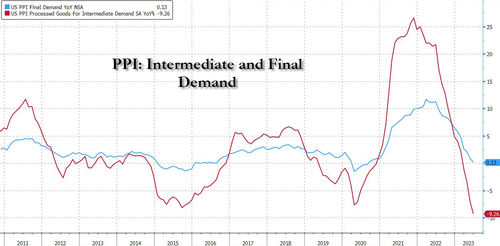

For the second day in a row, US equity futures are higher as part of a global risk-on move one which has sent spoos to fresh 52 weeks highs, and fast approaching the Jan 2022 all time high. Tech is again outperforming led by the “magnificent 7″ megacaps following the unexpectedly soft CPI print which sparked expectations that after the July hike the Fed is done, and has accelerated the dollar tumble. As of 7:45am ET, S&P futures were 0.3% higher to 4,522 while Nasdaq futures rose 0.6%. Bond yields and the USD continue their move lower, with steepening in the belly of the curve. The DXY has made a 52-wk low today. The plunge in the dollar means that commodities are bid with strength across all 3 segments; keep an eye on Ags as India may move to restrict rice exports and the Black Sea Grain Initiative expires next week. Today’s macro data focus is on PPI, which will boost confidence that yesterday’s CPI print was not a fluke. Keep an eye on PPI in the future as China’s negative PPI and the lack of money supply growth may put accelerating downward pressure on input costs. Bank earnings kick off tomorrow.

In premarket trading, airline stocks rose after Delta Air Lines increased its adjusted earnings per share outlook for the year and reported stronger-than-expected second-quarter results; Delta shares jumped as much as 4.2% premarket. Walt Disney shares rose 1.3% in premarket trading after the entertainment company extended the contract of Chief Executive Officer Bob Iger for another two years. US-listed Chinese stocks also rose as Beijing urged Washington to immediately end unilateral sanctions on Chinese companies to help bilateral economic and trade cooperation. Alibaba (BABA) +1.4%, Baidu (BIDU) +2.5%, JD.com (JD) +2.8%, Bilibili (BILI) +3.0%. Here are some other notable premarket movers:

SoFi Technologies Inc. drops 4.5% after the US online lender was cut to underweight from equal-weight at Morgan Stanley.

Viasat Inc. plunges 22% as the company said an unexpected event occurred during reflector deployment that may materially impact the performance of the ViaSat-3 Americas satellite.

Trade Desk shares rise 3.8% in premarket trading, after Nasdaq said the stock would replace Activision Blizzard in the Nasdaq 100.

Ess Tech and MillerKnoll Inc. are among the most active industrials stocks in early premarket trading, gaining 8.6% and falling 5.9% respectively

Delta Air Lines is up 4.4% after increasing its adjusted earnings per share outlook for the year and reporting stronger- than-expected second-quarter results.

Axonics gains 0.9% after shares were initiated with an overweight rating at KeyBanc Capital Markets, which sees opportunity for improved investor sentiment as the medtech company addresses some near-term pressures.

BioCryst Pharmaceuticals rises 7% after BofA Global Research raised the recommendation to buy from neutral.

Carvana falls 5.8% as JPMorgan cut its recommendation on the used-car retailer to underweight from neutral, saying shares have again disconnected from fundamentals.

Coinbase fell as much as 2.1% as Barclays cut its recommendation on the biggest US crypto exchange to underweight from equal-weight, saying the regulatory overhang on the stock is likely to last for some time.

Cryoport shares plummet 29% after the cryogenic storage firm reported preliminary second-quarter revenue that missed estimates. Analysts saw the update as disappointing, with Stephens noting that it raised a “variety of questions.”

Intercept Pharmaceuticals gains 9.6% after HC Wainwright & Co. double-upgraded the company’s recommendation to buy from sell saying that strong interim results from a mid-stage trial “look to breathe new, longer life to the franchise.”

LL Flooring tumbles 4.9% as Loop Capital downgrades to sell from hold, writing that the company faces a tough macroeconomic environment, with declining home sales and interest rates likely to rise.

Meta Platforms rises 1.4% as Cowen upgrades its rating to outperform from market perform, citing factors including Threads monetization optionality. Meanwhile, Morgan Stanley boosts its price target.

Snowflake Inc. shares are up 2% after Scotiabank upgrades the software company to sector outperform from sector perform.

In case it wasn’t clear yet, investors are piling back into equities as concerns over higher interest rates and a potential recession ease. Data Wednesday showed the US inflation rate slid to a two-year low, while today’s PPI report is expected to show a decline from a year ago.

“The question now is whether the market continues to trade off the easing inflation narrative,” ING Bank NV strategists led by Antoine Bouvet wrote in a note. “There is an excuse to do so as today’s PPI report is also expected to be friendly.”

One driver for the surge in risk assets is a rout in the dollar; some top money managers said the dollar is poised for further losses as US exceptionalism wanes. Hedge funds turned net sellers of the dollar for the first time since March, according to data from the CFTC. “The recent USD underperformance reflects a qualitative shift in market comfort with being short USD as the terminal Fed policy rate looks increasingly capped,” Steven Englander, head of global G-10 FX research and North America strategy for Standard Chartered Bank, wrote in a note.

Back to stocks, European shares extended Wednesday’s rally, which saw the Stoxx 600 Index surge 1.5%. The European benchmark is in the midst of its longest rising streak since mid-April and has almost erased its second-half losses. Swatch Group AG, the maker of Omega and Longines watches, jumped more than 6% as China’s reopening fueled a rise in profits. Watches of Switzerland Group Plc, the biggest retailer of Rolex watches in the UK, soared 10%. US equity futures rose after solid gains on Wall Street. Here are some of the more notable European movers:

Swatch shares jump as much as 6.9% after the Swiss watchmaker reported earnings that beat estimates.

Watches of Switzerland soars as much as 12%, the most since January 2022, after the UK retailer of Rolex watches reported results and kept its guidance unchanged for the year

Aker BP climbs as much as 2.3% after Norway’s second-biggest oil and gas producer increased its production guidance for the year

Valeo gains as much as 4% after Stifel raised the French automotive supplier to buy from hold

Experian shares rise as much as 0.9% after the consumer credit reporting company reaffirmed its full-year organic revenue forecast

Barratt Developments drops as much as 5.4%, after the UK homebuilder noted a “significant deterioration” in demand during the second quarter. Peers also fell

Schneider Electric falls as much as 3.7%, the most since May, after BofA double downgraded the French maker of electrical products to underperform from buy

BASF shares decline as much as 2.3%, before paring the drop, as its new lower Ebit guidance for the full year implies a cut to consensus at the mid-point of about 14%

Bufab drops as much as 13%, the most since March 2020, after the Swedish bolt and fastener maker reported 2Q results which DNB said fell short of expectations in terms of revenue and organic growth

Barry Callebaut shares dip as much as 2% after reporting volume growth that Vontobel said is lower than expected, partly as a result of inflationary conditions

Orpea shares fall as much as 1.7% after the French retirement-home operator cut its FY23 EbitdaR outlook, citing low occupancy rates in France, an “adverse reputational context” and high staff costs

Earlier in the session, the MSCI Asia Pacific Index headed for the highest close in more than three weeks, with stocks in Hong Kong recording some of the biggest gains. Chinese Premier Li Qiang met with senior executives from firms including Alibaba Group Holding Ltd. and ByteDance Ltd., a sign that the government is ending its crackdown on the technology industry.

In FX, the Bloomberg Dollar Index fell 0.3%, taking losses this week to 1.8% and a fresh 52-week low after Wednesday’s CPI print gave momentum to the bearish greenback trend. NZD/USD and AUD/USD led gains, both climbing around 1%, while the British pound extended its rally to a sixth day, staying above the $1.30 level that it hit Thursday for the first time since April 2022, after data showed the UK economy shrank less than expected in May.

“A further decline in PPI and a rise in claims could see dollar losses extend,” wrote Chris Turner head of FX strategy at ING, who sees the selloff potentially marking the start of the dollar’s long-awaited cyclical decline. “DXY should press big psychological support at 100.00, the next target would be 99.00 on a breakout”

In rates, yields were broadly lower as investors unwound bets that the Fed would raise rates again following an expected hike this month; treasuries continued their bull-steepening streak as yields on the two-year slumped as much as 12 basis points to 4.63%, the lowest level in four weeks; as odds of another Federal Reserve hike after July are receding. The 5s30s spread is wider by ~5bp; 10-year around 3.82%, lower by 3bp on the day, with bunds and gilts outperforming by 6bp and 2bp in the sector. European bonds also rallied, led by Italy; traders are no long fully pricing another 50 basis points of hikes for the European Central Bank and erased bets on the Bank of England taking the key rate to 6.5%, seeing a peak of 6.25% instead. Germany’s 10-year yield dropped eight basis points to 2.49%. Yields are richer across the curve with front-end outperforming. The week’s auction cycle concludes with $18 billion 30-year reopening at 1pm New York time, which follows strong demand for 3- and 10- year sales that drew minimal market reaction. The WI 30-year yield at ~3.935% is ~3bp cheaper than last month’s, which stopped 1.1bp through. As investors globally continue to digest Wednesday’s benign US CPI data, Thursday brings PPI and 30-year bond auction, adding to steepening pressure on the curve.

In commodities, crude oil was steady even after the International Energy Agency said cut its forecast for demand growth. Iron ore rose as hopes increased that Beijing will deliver more economic aid for the beleaguered property sector and as investors shrugged off disappointing Chinese trade data.

Bitcoin is comfortably above the USD 30k mark but yet to make much traction above the USD 30.5k figure with catalysts light and price action broadly still a function of Wednesday’s inflation update.

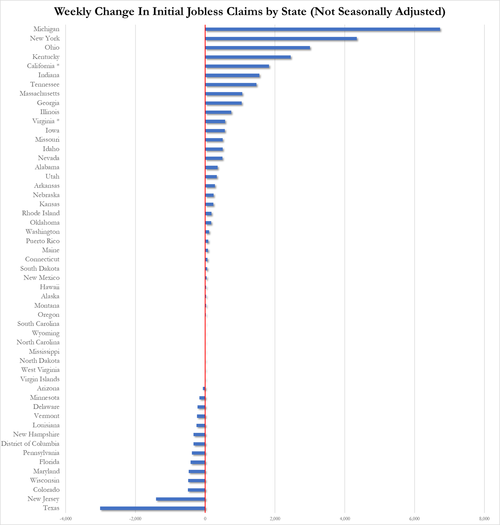

Looking to the day ahead now, and data releases include the US PPI reading for June, the weekly initial jobless claims, as well as UK GDP and Euro Area industrial production for May. From central banks, we’ll hear from the Fed’s Daly and Waller, whilst the ECB will be publishing the accounts of their June meeting. Lastly, earnings releases include PepsiCo and Delta Air Lines.

Market Snapshot

S&P 500 futures up 0.3% to 4,522.25

MXAP up 1.7% to 167.86

MXAPJ up 1.9% to 529.98

Nikkei up 1.5% to 32,419.33

Topix up 1.0% to 2,242.99

Hang Seng Index up 2.6% to 19,350.62

Shanghai Composite up 1.3% to 3,236.48

Sensex up 0.6% to 65,806.88

Australia S&P/ASX 200 up 1.6% to 7,246.91

Kospi up 0.6% to 2,591.23

STOXX Europe 600 up 0.4% to 460.49

German 10Y yield little changed at 2.49%

Euro up 0.3% to $1.1164

Brent Futures up 0.5% to $80.52/bbl

Gold spot up 0.2% to $1,961.03

U.S. Dollar Index down 0.24% to 100.28

Top Overnight News

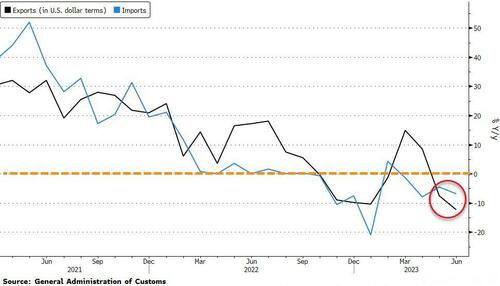

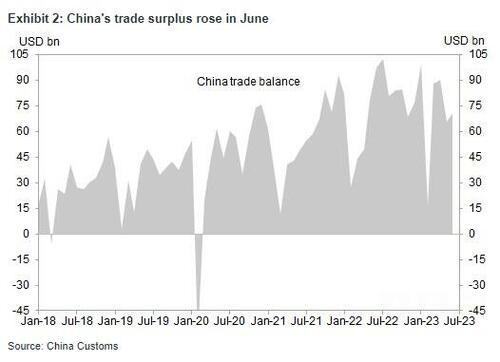

China’s trade data for June undershoots the Street, with exports -12.4% Y/Y (vs. the Street -10%) and imports -6.8% (vs. the Street -4.1%). BBG

Washington-Beijing relationship will be tested (again) as the White House proceeds with plans to impose restrictions on American investment in China (the US Treasury has sought to narrow the scope of the restrictions). NYT

China is sending its strongest signal yet that it supports the development of platform companies, putting an end to years of probes into tech firms at a time when Beijing is going all-out to prevent economic growth from sputtering. SCMP

Global energy demand forecast is trimmed by 220K BPD by the IEA given mounting economic headwinds (although demand overall will hit a fresh record this year). IEA

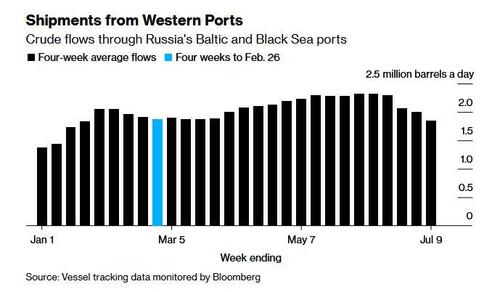

Russia offered a deal to extend the grain export agreement in exchange for the country’s agricultural bank could see a subsidiary connected to the SWIFT int’l payment system. RTRS

Junk market shrinks by nearly ~$200B since its peak in 2021, helping to prop up prices despite a softer growth backdrop. FT

The Federal Trade Commission has opened an expansive investigation into OpenAI, probing whether the maker of the popular ChatGPT bot has run afoul of consumer protection laws by putting personal reputations and data at risk. WaPo

PEP kicked off earnings season on an upbeat note, posting organic revenue growth of +13% (the Street was modeling +9.8%) with EPS of 2.09 (more than 10c ahead of the Street’s 1.96 forecast). The EPS beat was driven by better revenue, GMs, and op. margins (and the tax rate was actually a bit higher than anticipated, which means underlying earnings power was even stronger than it seems). RTRS

DAL reported strong Q2 earnings, with EPS of 2.68 (vs. the Street’s 2.41), and they raise guidance for the year. They now see EPS of $6-7 for 2023 (vs. previously pointing to the high-end of $5-6) with Q3 EPS targeted at 2.20-2.50 (vs. the Street’s 2.06 forecast). RTRS

Remote work risks wiping $800 billion from the value of office buildings in major cities by 2030, McKinsey said. That would represent a 26% drop compared to levels in 2019, and an even worse decline of 42% is possible. The trend is set to continue as employers downsize space as soon as long-term leases come to an end. Only 37% of people are back at the office every day. (BBG)

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded higher as the region reacted to the softer-than-expected US inflation data which underpinned the global risk appetite, while weaker-than-expected Chinese trade data failed to dampen the spirit. ASX 200 was firmer with all sectors lifted by the constructive mood and as yields continued to decline. Nikkei 225 reclaimed the 32,000 level at the open after the US CPI data provided a rising tide for stocks. Hang Seng and Shanghai Comp were positive with outperformance in the Hong Kong benchmark due to tech strength after Chinese Premier Li met with several HK-listed tech giants, endorsed the platform economy and pledged more support for the sector, while gains in the mainland were somewhat capped alongside the latest Chinese trade data which missed forecasts. Credit Suisse upgrades Chinese equities to Overweight.

Top Asian News

China’s Customs said the nation’s exports showed strong resilience in H1 but also noted that sluggish global economic growth, slowing global trade and investment, geopolitical risks and weakening external demand continue to impact China’s trade. Furthermore, it stated that China’s trade growth faces relatively big pressure but China is confident it can consolidate its market share in global trade this year, while a Customs official noted feelings of pressure and optimism for China trade in H2, according to Reuters.

US Secretary of State Blinken will meet with China’s top diplomat Wang Yi at the ASEAN meetings.

Chinese hackers reportedly breached the email of US Commerce Secretary Raimondo and State Department officials, according to WSJ.

Bank of Korea kept its base rate unchanged at 3.50%, as expected, with the rate decision made unanimously and 6 members wanted to keep the door open for one more rate hike. BoK said domestic economic growth is expected to recover gradually, while GDP growth and consumer price inflation this year are expected to be consistent with forecasts. Furthermore, BoK Governor Rhee said several board members expressed concern about the rise in household debt, while he added that inflation will rebound to around 3% by year-end and fall again to the 2% level next year.

Fast Retailing (9983 JT) 9-month(JPY): PBT 359bln, +2.8%; Operating Profit 330.6bln, +21.9%; Net Profit 238bln, +0.3%. CFO says Chinese consumption appears to be recovering strongly.

Japan Top FX Diplomat Kanda says closely watching FX market moves; there is a view that speculative Yen short positions are unwinding rapidly; there is a view that deflationary norm may be changing.

European bourses are modestly firmer across the board in a continuation of the post US CPI trade, Euro Stoxx 50 +0.6%. Sectors are primarily in the green with Retail names outperforming after Fast Retailing while Homebuilders lag following Barratt Developments earnings commentary. Stateside, futures are also firmer ahead of IJC and Fed speak ES +0.3%; NQ +0.6% outperforms as yields continue to pullback. PepsiCo Inc (PEP) Q2 2023 (USD): Core EPS 2.09 (exp. 1.96), Revenue 22.32bln (exp. 21.73bln); raises annual revenue and profit forecasts after price hikes and steady demand. FY EPS view 7.47 (exp. 7.32). +3.1% in pre-market trade. US FTC investigating whether ChatGPT harms consumers, WaPo reports.

Top European News

UK PM Sunak is set to be presented a plan on Thursday to give a million public sector workers a pay rise of around 6%, according to The Telegraph.

ECB’s Visco says we are not very far from a peak in interest rates, somewhat disagrees with the preference for tightening.

ECB’s Stournaras says we said a July hike was likely, but data since has become weaker, via Econostream; September hike is not a given, particularly since data points to a Q3 stagnation. Emphasises data-dependence.

FX

DXY extends post-CPI decline towards 100.000 as Treasury yields retreat further and markets position for less aggressive Fed.

Kiwi and Aussie outperform due to high beta properties, with NZD/USD probing 0.6350 and AUD/USD touching 0.6850.

Pound encouraged by less weak than feared UK GDP data and Euro gains at the expense of soft Dollar, as Cable tops 1.3050 and EUR/USD approaches 1.11-75-85 resistance zone.

Yen lags after stalling near 138.00 and takes note of verbal intervention from Japan’s top currency diplomat Kanda.

PBoC set USD/CNY mid-point at 7.1527 vs exp. 7.1623 (prev. 7.1765)

Fixed Income

Bonds bounce further in follow-on reaction to soft US inflation data.

Bunds breach several resistance levels and trip stops on the way to 133.13 from 131.92.

Gilts more contained within 94.91-33 range post-better than forecast UK GDP and OBR warning on Government’s debt recovery strategy.

T-note nearer 112-24+ peak than 112-07 trough after big block trade in 5 year futures that looked like a buy given price action at the time.

Commodities

Crude benchmarks are incrementally firmer but well within earlier ranges as Brent loses a little bit of its upward momentum after surpassing USD 80/bbl.

Meanwhile, spot gold is inching higher as the USD remains downbeat but with upside once again capped by the broader tone; base metals firmer, given the aforementioned factors are both supportive.

Russian Urals oil price has moved USD 2-3/bbl above the price cap on Thursday, via Reuters’ calculations.

IEA Monthly Oil Market Report: oil demand is set to increase by 2.2mln BPD in 2023 to reach a record 102.1mln BPD (vs. June view of 102.3mln BPD). China is to account for 70% of global oil demand gains. China’s widely anticipated reopening has so far failed to extend beyond travel and services.

EU’s VP Sefcovic says the EU has gathered 16BCM of demand in the second round of joint gas purchases, results which exceed expectations.

Geopolitics

North Korea said it test-launched a Hwasong-18 ICBM on Wednesday and leader Kim guided the missile test, while Kim said they will continue military offensive measures until the US abandons its hostile policy against Pyongyang.

UN Security Council is to meet publicly on Thursday regarding North Korea’s missile launch, according to Reuters.

US Event Calendar

08:30: June PPI Final Demand MoM, est. 0.2%, prior -0.3%

08:30: June PPI Final Demand YoY, est. 0.4%, prior 1.1%

08:30: June PPI Ex Food and Energy MoM, est. 0.2%, prior 0.2%

08:30: June PPI Ex Food and Energy YoY, est. 2.6%, prior 2.8%

08:30: July Initial Jobless Claims, est. 250,000, prior 248,000

08:30: July Continuing Claims, est. 1.72m, prior 1.72m

14:00: June Monthly Budget Statement, est. -$184b, prior -$88.8b

DB’s Jim Reid concludes the overnight wrap

Markets have put in a very strong performance over the last 24 hours, thanks to a promising US CPI report that boosted hopes of a soft landing in the markets’ eyes. There were several details that investors liked, but a key one was that it marked the first time in 29 months that the monthly core inflation print had been beneath 2% on an annualised basis. So the Fed would be very happy if we got some more reports like yesterday’s, and markets moved to price in more rate cuts for next year as a result. In turn, that led to a significant rally, with the S&P 500 (+0.74%) closing at a 15-month high, whilst yields on 10yr Treasuries came down -11.2bps to 3.86%.

What the financial world and the Fed will have to weigh up is whether the improvement in inflation is coming just in time or too late to change the direction of travel. Monetary policy operates with a lag and we still have several hundred basis points of hikes to fully work through the system. Ironically, if inflation is falling back to trend but the Fed takes some time to move to an easing bias, then policy will become more restrictive in real terms. However, it’s fair to say that this print gives them the ability to move to an easing bias earlier. So you can see why markets would get excited.

When it came to the specifics of the CPI release, the main news was that inflation continued to soften, with monthly headline CPI at just +0.18% in June. That was beneath the consensus expectation for a +0.3% reading, and it took the year-on-year measure down to just +3.0%, which is the lowest it’s been since March 2021. On core CPI there was even better news, as the monthly print came in at +0.16%, which is the weakest since February 2021 before the current inflation spike really got going. Similarly, that took the year-on-year core CPI print down to +4.8%.

To be honest, it was difficult to find any negative spin from yesterday’s release. At worst, you could highlight the outsized contribution of airfares (-8.1%) to the core CPI slowdown and say some of the stickier factors were a bit stronger, but even those were still coming down from their levels over recent months. For instance, the Atlanta Fed breaks down the CPI into a sticky and flexible CPI series, and their sticky CPI print hit a 24-month low of +0.24% in June. On top of that, it was clear the declines were broad-based, as the Cleveland Fed’s trimmed mean that excludes the biggest outliers in either direction came in at +0.22%, which is the lowest since February 2021.

Although the CPI report was a downside surprise, it doesn’t look like it’d be enough to dissuade the Fed from hiking in a couple of weeks’ time. They’ve been consistent that they want to see a succession of lower numbers before they ease policy, particularly after summer 2021 when some weaker numbers led to false hope that inflation would prove transitory. This cautious message was supported by comments from Richmond Fed President Barkin, who said that backing off too soon would require the Fed to do even more. Market pricing has been reflective of that too, with expectations for a July hike unchanged yesterday at 89%. But even as a July hike looks almost-locked in, the CPI print led investors to lower the rate path further out. For example, terminal rate pricing for November came down by -4.8bps to 5.38%. And when it comes to next year, pricing for the December 2024 came down by -18.6bps on the day to 3.91%, and is down another -5.3bps overnight to 3.86%.

With investors pricing in more rate cuts, sovereign bonds rallied strongly across the world. The 10yr US Treasury yield was down -11.2bps to 3.86%, whilst the 2yr yield was down by an even larger -12.9bps to 4.75%. Bear in mind it was less than a week ago after the bumper ADP print that the 2yr yield went as high as 5.12%, so we’ve seen a pretty big turnaround since then. The rates rally was led by real yields, with 10yr real Treasury yield down -15.5bps on the day, its sharpest daily decline since March. Treasury yields have extended their decline overnight, with 2yr yields down another -4.4bps to 4.70%, whilst the 10yr yield has also fallen another -0.8bps to 3.85%. In Europe yesterday it was much the same story, with yields on 10yr gilts (-14.9bps), OATs (-11.6bps) and BTPs (-15.8bps) all plummeting.

The CPI report also led to some pretty seismic movements in FX markets, with the dollar index (-1.19%) posting its worst day in 8 months and falling to a 14-month low. That led to several milestones elsewhere, with the euro closing above $1.11 for the first time since March 2022 and this morning it’s up further to another 2023 high of $1.115. In the meantime, the pound surpassed the $1.30 mark for the first time since April 2022.

This backdrop was favourable for equities, and both the S&P 500 (+0.74%) and the NASDAQ (+1.15%) closed at 15-month highs. Over in Europe there were even larger advances, with the STOXX 600 (+1.51%) surging, and the DAX (+1.47%) posting its strongest daily performance since the financial turmoil in March.

Elsewhere yesterday, the Bank of Canada delivered a 25bp hike as expected, taking their overnight rate to a 22-year high of 5%. There were hawkish elements to the decision as well, as their latest Monetary Policy Report is now projecting a slower return to the 2% target relative to April, with a return to 2% in the middle of 2025. The statement said that the Governing Council “remains concerned that progress towards the 2% target could stall, jeopardizing the return to price stability.” Looking forward, overnight index swaps are currently pricing 7.9bps of hikes at the September meeting, so a roughly one-in-three likelihood of another 25bp hike.

Asian equity markets have followed up with further gains overnight, with a strong rally amidst the prospect of the Fed moving less aggressively. That’s led to major gains across the board, with the Hang Seng (+2.49%), the Nikkei (+1.67%), the CSI 300 (+1.12%), the Shanghai Composite (+0.86%) and the KOSPI (+0.82%) all advancing. US equity futures are similarly pointing to a positive start later, with those on the S&P 500 up +0.26%, whilst NASDAQ 100 futures are up +0.44%.

Lastly overnight, the Bank of Korea left its key interest rate unchanged at 3.5% as expected. That’s the 4th consecutive meeting that rates have been on hold now, but the statement said that the Board would “maintain a restrictive policy stance for a considerable time with an emphasis on ensuring price stability.”

To the day ahead now, and data releases include the US PPI reading for June, the weekly initial jobless claims, as well as UK GDP and Euro Area industrial production for May. From central banks, we’ll hear from the Fed’s Daly and Waller, whilst the ECB will be publishing the accounts of their June meeting. Lastly, earnings releases include PepsiCo and Delta Air Lines.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

Constructive risk tone as post-CPI action continues, DXY & yields retreat further – Newsquawk US Market Open

THURSDAY, JUL 13, 2023 – 06:34 AM

European bourses & US futures are firmer as the post-inflation action continues ahead of IJC

DXY extends the post-inflation decline towards 100.00 amid a further retreat in yields

Antipodeans outperform, EUR & GBP also bid; as above, fixed benchmarks continue to climb

Crude inches higher with attention on Urals while spot gold is more contained but base metals extend

Looking ahead, highlights include US IJC, ECB Minutes, OPEC OMR, Supply from the US.

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

European bourses are modestly firmer across the board in a continuation of the post US CPI trade, Euro Stoxx 50 +0.6%.

Sectors are primarily in the green with Retail names outperforming after Fast Retailing while Homebuilders lag following Barratt Developments earnings commentary.

Stateside, futures are also firmer ahead of IJC and Fed speak ES +0.3%; NQ +0.6% outperforms as yields continue to pullback.

PepsiCo Inc (PEP) Q2 2023 (USD): Core EPS 2.09 (exp. 1.96), Revenue 22.32bln (exp. 21.73bln); raises annual revenue and profit forecasts after price hikes and steady demand. FY EPS view 7.47 (exp. 7.32). +3.1% in pre-market trade

US FTC investigating whether ChatGPT harms consumers, WaPo reports.

Click here and here for a recap of the main European equity updates.

FX

DXY extends post-CPI decline towards 100.000 as Treasury yields retreat further and markets position for less aggressive Fed.

Kiwi and Aussie outperform due to high beta properties, with NZD/USD probing 0.6350 and AUD/USD touching 0.6850.

Pound encouraged by less weak than feared UK GDP data and Euro gains at the expense of soft Dollar, as Cable tops 1.3050 and EUR/USD approaches 1.11-75-85 resistance zone.

Yen lags after stalling near 138.00 and takes note of verbal intervention from Japan’s top currency diplomat Kanda.

PBoC set USD/CNY mid-point at 7.1527 vs exp. 7.1623 (prev. 7.1765)

Crude benchmarks are incrementally firmer but well within earlier ranges as Brent loses a little bit of its upward momentum after surpassing USD 80/bbl.

Meanwhile, spot gold is inching higher as the USD remains downbeat but with upside once again capped by the broader tone; base metals firmer, given the aforementioned factors are both supportive.

Russian Urals oil price has moved USD 2-3/bbl above the price cap on Thursday, via Reuters’ calculations.

IEA Monthly Oil Market Report: oil demand is set to increase by 2.2mln BPD in 2023 to reach a record 102.1mln BPD (vs. June view of 102.3mln BPD). China is to account for 70% of global oil demand gains. China’s widely anticipated reopening has so far failed to extend beyond travel and services.

EU’s VP Sefcovic says the EU has gathered 16BCM of demand in the second round of joint gas purchases, results which exceed expectations.

US Senator Warren said Fed Chair Powell should halt the rate hikes, while she added that the banking industry is still overly concentrated and anything that causes the demise of small banks is a bad idea, according to Bloomberg.

UK GDP Estimate MM (May) -0.1% vs. Exp. -0.3% (Prev. 0.2%); YY (May) -0.4% vs. Exp. -0.7% (Prev. 0.5%); 3M/3M (May) 0.0% vs. Exp. -0.1% (Prev. 0.1%)

UK RICS Housing Survey (Jun) -46.0 vs. Exp. -34.0 (Prev. -30.0)

EU Industrial Production MM (May) 0.2% vs. Exp. 0.3% (Prev. 1.0%); YY (May) -2.2% vs. Exp. -1.2% (Prev. 0.2%)

NOTABLE EUROPEAN HEADLINES

UK PM Sunak is set to be presented a plan on Thursday to give a million public sector workers a pay rise of around 6%, according to The Telegraph.

ECB’s Visco says we are not very far from a peak in interest rates, somewhat disagrees with the preference for tightening.

ECB’s Stournaras says we said a July hike was likely, but data since has become weaker, via Econostream; September hike is not a given, particularly since data points to a Q3 stagnation. Emphasises data-dependence.

CRYPTO

Bitcoin is comfortably above the USD 30k mark but yet to make much traction above the USD 30.5k figure with catalysts light and price action broadly still a function of Wednesday’s inflation update.

GEOPOLITICS