GOLD PRICE CLOSED: UP $0.75 TO $1960.15

SILVER PRICE CLOSED: UP $0.27 AT $24.99

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1954.85

Silver ACCESS CLOSE: 24.90

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $31,202 DOWN 91 Dollars

Bitcoin: afternoon price: $30,107 DOWN 1186 dollars

Platinum price closing $978.00 UP $2.50

Palladium price; $1285.25 DOWN $14.70

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,584.62 UP 14.34 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1493.36 UP 1.20 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1741.56 DOWN 4.80 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

CONTRACT: JULY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,959.200000000 USD

INTENT DATE: 07/13/2023 DELIVERY DATE: 07/17/2023

FIRM ORG FIRM NAME ISSUED STOPPED

190 H BMO CAPITAL 100

435 H SCOTIA CAPITAL 2

624 H BOFA SECURITIES 100

690 C ABN AMRO 1

737 C ADVANTAGE 8 4

905 C ADM 1

JPMorgan stopped 0/108 contracts.

FOR JULY:

GOLD: NUMBER OF NOTICES FILED FOR JULY/2023. CONTRACT: 108 NOTICES FOR 10,800 OZ or 0.3359 TONNES

total notices so far: 2494 contracts for 249,400 oz (7.757 tonnes)

FOR JULY:

SILVER NOTICES: 55 NOTICE(S) FILED FOR 275,000 OZ/

total number of notices filed so far this month : 4026 for 20,130,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $0.75

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 914.66 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP $0.27 AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.21 MILLION OZ OF SILVER FROM THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 460.731 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY AN UNBELIEVABLY HUGE AND RECORD SIZED 12,140 CONTRACTS TO 137,646 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR HUGE $0.64 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. TAS ISSUANCE WAS A FAIR SIZED 250 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH . CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 493 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.64). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A HUMONGOUS ATMOSPHERIC GAIN ON OUR TWO EXCHANGES OF 15,013 CONTRACTS. WE HAD 250 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 1.250 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1.25 MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS( 2873 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 16.110 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S HUGE 270,000 OZ QUEUE JUMP.+ 1.125 MILLION OZ EXCHANGE FOR RISK//NEW STANDING: 20.960 MILLION OZ + 1.125 EXCHANGE FOR RISK = 22.085 MILLION OZ/ // HUGE SIZED COMEX OI GAIN/ HUGE SIZED EFP ISSUANCE/VI) FAIR NUMBER OF T.A.S. CONTRACT ISSUANCE (493 CONTRACTS)/HUGE T.A.S. (250 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL – 298 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTRACTS for 8 days, total 7681 contracts: OR 38.405 MILLION OZ (960 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 38.405 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 38.405 MILLION OZ

RESULT: WE HAD A HUGE ATMOSPHERIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 12,140 CONTRACTS WITH OUR HUGE GAIN IN PRICE OF $0.64 IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 2873 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 16.110 MILLION OZ FOLLOWED BY TODAY’S HUGE 270,000 OZ QUEUE JUMP + 1.125 MILLION OZ EXCHANGE FOR RISK: TOTAL NOW STANDING 20.690 MILLION OZ + 1.125 MILLION OZ = 22.085 MILLION OZ.///// .. WE HAVE A HUGE ATMOSPHERIC SIZED GAIN OF 15,311 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A FAIR 493//ZERO FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION. THE NEW TAS ISSUANCE TODAY (250) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 55 NOTICE(S) FILED TODAY FOR 275,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 969 CONTRACTS TO 506,210 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED: 535 CONTRACTS

WE HAD A STRONG SIZED INCREASE IN COMEX OI ( 969 CONTRACTS) WITH OUR $3.35 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JULY. AT 5.1975 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0.3484 TONNE QUEUE JUMP: NEW TOTAL OF GOLD STANDING FOR JULY: 7.7916 TONNES// + /AN UNBELIEVABLY HUGE (AND CRIMINAL) ISSUANCE OF 29,832 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $3.35 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING.WE HAD A STRONG SIZED GAIN OF 5969 OI CONTRACTS (18.566 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 5000 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 506,210

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5969 CONTRACTS WITH 969 CONTRACTS INCREASED AT THE COMEX// AND A GOOD 5000 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5969 CONTRACTS OR 18.56 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A HUGE 29,832 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5000 CONTRACTS) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (969) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 5969 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 5.1975 TONNES FOLLOWED BY TODAY’S 0.3484 TONNE QUEUE JUMP//NEW TOTAL 7.7916 TONNES ///// /3) ZERO LONG LIQUIDATION//4) SMALL SIZED COMEX OPEN INTEREST GAIN/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: UNBELIEVABLY HUGE T.A.S. ISSUANCE: 29,832 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

TOTAL EFP CONTRACTS ISSUED: 19,390 CONTRACTS OR 1,939,000 OZ OR 60.311 TONNES IN 8 TRADING DAY(S) AND THUS AVERAGING: 2423 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES 60.311 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 60.311/3550 x 100% TONNES 1.69% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 60.311 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE ATMOSPHERIC SIZED GAIN OF 12,144 CONTRACTS OI TO 137,646 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 2873 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 2873 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2873 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 12,140 CONTRACTS AND ADD TO THE 2275 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 15,013 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 75.065 MILLION OZ

OCCURRED WITH OUR $0.64 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

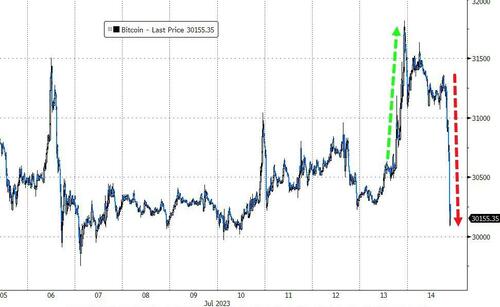

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED UP 1.22 PTS OR 0.04% //Hang Seng CLOSED UP 63.16 PTS OR 0.09% /The Nikkei CLOSED DOWN 28.07 OR 0.09% //Australia’s all ordinaries CLOSED UP 0.83 % /Chinese yuan (ONSHORE) closed UP 7.1359 /OFFSHORE CHINESE YUAN UP TO 7.1425 /Oil UP TO 76.89 dollars per barrel for WTI and BRENT UP AT 81.24 / Stocks in Europe OPENED ALMOST ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 969 CONTRACTS UP TO 506,210 WITH OUR GAIN IN PRICE OF $3.35 ON THURSDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5000 EFP CONTRACTS WERE ISSUED: : AUGUST 5000 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5000 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 5969 CONTRACTS IN THAT 5000 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 1504 COMEX CONTRACTS..AND THIS STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $3.35//THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS AN UNBELIEVABLY HUGE 29,832 CONTRACTS (4TH DAY IN A ROW/TAS GREATER THAN 20,000). THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (7.7916) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 7.7916 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $3.35) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED GAIN OF 5969 CONTRACTS ON OUR TWO EXCHANGES. WE HAD ZERO TAS LIQUIDATION THROUGHOUT THE THURSDAY COMEX SESSION. THE MASSIVE TAS ISSUED THURSDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 20.230 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY. (5.11974 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 0.3484 TONNES//TOTAL STANDING FOR JULY GOLD: 7.7916 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $3.35.

WE HAD – REMOVED 535 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 5969 CONTRACTS OR 595900 OZ OR 18.560 TONNES.

Estimated gold volume today:// 235,814 FAIR

final gold volumes/yesterday 298,096 GOOD

//JULY 14/ FOR THE JULY 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 6783.861 OZ BRINKS JPMorgan total 211 kilobars . |

| Deposit to the Dealer Inventory in oz | 97.65 oz BRINKS |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today | 108 notice(s) 10,800 OZ 0.3359 TONNES |

| No of oz to be served (notices) | 11 contracts 1100 oz 0.03421 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2494 notices 249,400 OZ 7.757 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

1 dealer deposit:

i)Into Brinks dealer: 97,65 oz

total dealer deposits: 97.65 oz

total customer deposits: 0 oz

we had 2 customer withdrawals:

i) Out of Brinks 321.910 oz (10 kilobars)

ii) out of JPMorgan: 6462.351 oz (201 kilobars)

total withdrawals: 6783.861 oz

Adjustments; 1//dealer to customer

from Loomis: 675.171 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 119 contracts having GAINED 60 contracts. We had 52 contracts served on Thursday. Thus we gained 112 contracts or an additional 11,200 oz of gold will stand at the comex.

AUGUST LOST 23,449 contracts DOWN to 282,369 contracts

SEPT gained 31 contracts to stand at 576

We had 108 contracts filed for today representing 10800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 108 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2023. contract month,

we take the total number of notices filed so far for the month (2494 x 100 oz ), to which we add the difference between the open interest for the front month of JULY (119 CONTRACT) minus the number of notices served upon today 108 x 100 oz per contract equals 250,500 OZ OR 7.7916 TONNES the number of TONNES standing in this NON active month of July.

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (2494) x 100 oz + (119) {OI for the front month} minus the number of notices served upon today (108) x 100 oz) which equals 250,500 oz standing OR 7.7916 TONNES

TOTAL COMEX GOLD STANDING: 7.7916 TONNES WHICH IS STRONG FOR A NON ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,879,274.546 OZ 58,45 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,275,815.652 OZ

TOTAL REGISTERED GOLD: 11,832,906.869 (368.05 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,442,908.783 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,953,632 OZ (REG GOLD- PLEDGED GOLD) 309.599 tonnes//

END

SILVER/COMEX

JULY 14

//2023// THE JULY 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 615,203.200 oz JPMorgan . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 2,456,640.265 oz Brinks CNT Loomis |

| No of oz served today (contracts) | 55 CONTRACT(S) (275,000 OZ) |

| No of oz to be served (notices) | 166 contracts (830,000 oz) |

| Total monthly oz silver served (contracts) | 4026 Contracts (20,130,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposits

total dealer deposit: 0 oz

total dealer deposits: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 3 deposits customer account:

i) Into Brinks 1,202,454.288 oz

ii) Into CNT: 624,109.907 oz

iii) Into Loomis: 630,076.070 oz

total customer deposits: 2456,640.265 oz

JPMorgan has a total silver weight: 139.367 million oz/278.856 million =50.35% of comex .//

Comex withdrawals 1

i) Out of JPMorgan 615,203.200 oz

adjustments: 0

TOTAL REGISTERED SILVER: 34.992 MILLION OZ//.TOTAL REG + ELIGIBLE. 278.886 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY /2023 OI: 221 CONTRACTS HAVING LOST 72 CONTRACT(S). WE HAD 126 NOTICES FILED ON THURSDAY SO WE GAINED A STRONG 54 CONTRACTS OR AN ADDITIONAL 270,000 OZ WILL STAND AT THE COMEX FOR DELIVERY IN JULY.

AUGUST GAINED 30 CONTRACTS TO STAND AT 674

SEPT HAS A GAIN OF 10,939 CONTRACTS UP TO 118,685

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 55 for 275,000 oz

Comex volumes// est. volume today 68,537 good /

Comex volume: confirmed yesterday: 94,049 STRONG

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 4026 x 5,000 oz = 20,130,000 oz

to which we add the difference between the open interest for the front month of JULY(221) and the number of notices served upon today 55 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2023 contract month: 4026 (notices served so far) x 5000 oz + OI for the front month of JULY (221) – number of notices served upon today (55 )x 500 oz of silver standing for the JULY contract month equates to 20.960 million oz + 1.125 MILLION OZ EXCHANGE FOR RISK /NEW TOTAL: 22.085 MILLION OZ..

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JULY 14/WITH GOLD UP $0.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 914.66 TONNES

JULY 13/WITH GOLD UP $3.30 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.66 TONNES

JULY 12/WITH GOLD UP $24.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.95 TONNES

JULY 11/WITH GOLD UP $6.15 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.0 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 915.26 TONNES

JULY 10 WITH GOLD DOWN $1.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.60 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 916.26 TONNES.

JULY 7 WITH GOLD UP $16.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.86 TONNES.

JULY 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 917.86 TONNES

JULY 5/WITH GOLD DOWN $2.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 2.6 TONNES FROM THE GLD///INVENTORY RESTS AT 921.90 TONNES

JULY 3/WITH GOLD UP $1.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.50 TONNES//

JUNE 30/WITH GOLD UP $10.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 924.50 TONNES

JUNE 29/WITH GOLD DOWN $3.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.81 TONNES

JUNE 28/WITH GOLD DOWN $1.15 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 925.65 TONNES

JUNE 27/WITH GOLD DOWN $9.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD./INVENTORY RESTS AT 925.65 TONNES

JUNE 26/WITH GOLD UP $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD/////INVENTORY RESTS AT 927.10 TONNES

JUNE 23/WITH GOLD UP $5.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: WITHDRAWALS OF 4.33 TONNES OF GOLD OVER THE PAST TWO DAYS. /INVENTORY RESTS AT 929.70 TONNES

JUNE 21/WITH GOLD DOWN $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 934.03 TONNES

JUNE 20/WITH GOLD DOWN $22.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.03 TONNES

JUNE 16/WITH GOLD UP $0.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.03 TONNES

JUNE 15/WITH GOLD UP $2.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 929.70 TONNES

JUNE 14/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 931.44 TONNES

JUNE 13/WITH GOLD DOWN $10.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.01 TONNES FORM THE GLD///INVENTORY RESTS AT 931.44

GLD INVENTORY: 914.66 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 14/WITH SILVER UP 27 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.21 MILLIONOZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 460.731 MILLION OZ/

JULY 13/WITH SILVER UP 64 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 12/WITH SILVER UP $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.881 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 11/WITH SILVER DOWN 5 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .020 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 464.822 MILLION OZ/

JULY 10/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.672 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 464.802 MILLION OZ

JULY 7/WITH SILVER UP 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.474 MILLION OZ

JULY 6/WITH SILVER DOWN 50 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.667 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.474 MILLION OZ//

JULY5/WITH SILVER UP 30 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JULY 3/WITH SILVER UP 7 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JUNE 30/WITH SILVER UP 19 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.377 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT468.141 MILLION OZ//

JUNE 29/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.763 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.764 MILLION OZ//

JUNE 28/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.527 MILLION OZ//

JUNE 27/WILVER SILVER UP 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 734,000 OZ INTO THE SLV////INVENTORY RESTS AT 470.527 MILLION OZ

JUNE 26/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 469.793 MILLION OZ.

JUNE 23/WITH SILVER DOWN 9 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A NET DEPOSIT OF 6.61 MILLION OZ INTO THE SLV OVER THESE PAST TWO DAYS//INVENTORY RESTS AT 469.793 MILLION OZ//

JUNE 21/WITH SILVER DOWN $.40 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.784 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 20/WITH SILVER DOWN 89 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 16/WITH SILVER UP 23 CENTS TODAY :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 463.183 MILLION OZ

JUNE 15/WITH SILVER DOWN 17 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.377 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 463.642 MILLION OZ//

JUNE 14/WITH SILVER UP 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 735,000 OZ FROM THE SLV///INVENTORY RESTS AT 465.019 MILLION OZ//

JUNE 13/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 465.754 MILLION OZ//

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

CLOSING INVENTORY 460.731 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

Could States Pave The Way For Currency Competition?

FRIDAY, JUL 14, 2023 – 07:20 AM

The US dollar is on shaky ground. There is a growing trend toward de-dollarization. Meanwhile, the Federal Reserve is tinkering with the idea of a digital dollar that could give the government unprecedented control over your spending.

Given the trajectory of the dollar, it might be a good idea to find some alternatives. In other words, we need currency competition.

Fortunately, there are options.

Gold and silver have served as money for thousands of years. Digital platforms make it easier than ever to transact business using either metal. This opens the door to creating an environment of currency competition, and the states are in a position to lead the way.

For instance, a bill introduced in Texas this year would have created a state-issued gold-backed digital currency. The bill didn’t advance, but it started the discussion and opened the door for future action.

As Allain L. de la Motte argues, “While the dollar won’t be displaced overnight, fostering a competitive environment where it needs to compete with sound money backed by gold is the best option for all 50 states.”

The following article was originally published by the Mises Wire. The opinions expressed are the author’s and do not necessarily reflect those of Peter Schiff or SchiffGold.

The US dollar has been the world reserve currency since 1944. At the Bretton Woods Conference, the dollar was pegged to gold and every other currency was pegged to the dollar. The fixed exchange rate system that emerged provided a stable environment for international trade and investment, as all countries had a currency value that was, directly or indirectly, tied to a fixed gold price.

The system began to unravel in the 1970s due to economic challenges faced by the United States, including the need to finance its war in Vietnam while simultaneously dealing with French president Charles de Gaulle’s demands that the US return France’s gold. His discontent may have been prophetic, foretelling a similar future sentiment. He said,

US imperialism leaves no field unoccupied. It takes every form, but the dollar is the most insidious. We pay the US to purchase us. So each time we have dollars, we will convert them into gold. Everyone should do the same. . . . Political pressures will no longer be used to manipulate money.

In August 1971, President Richard Nixon suspended the convertibility of the dollar into gold, effectively ending the gold standard and transforming the dollar into a total fiat currency. The value of fiat money is solely based on the faith and trust one has in its government. Interestingly, since 1913, the dollar has lost more than 97 percent of its purchasing power due to inflation.

Why Is the Dollar Still the Reserve Currency of the World?

Despite being a fiat currency, the dollar has managed to retain its privileges due to its extensive usage in international trade and financial markets and its association with one of the world’s largest economies. One of the primary drivers to attaining the status of the world’s reserve currency is the petrodollar, which refers to the role of the dollar as the primary currency used for international oil trade.

In the 1970s, following the oil crisis and the subsequent agreement between the Organization of Petroleum Exporting Countries and major oil-producing nations, oil was priced and traded in dollars, which meant that people purchasing oil had to use the dollar, creating a high demand for it.

The petrodollar system brought significant benefits to the United States. As global demand for its currency increased, this system allowed the US to maintain its economic influence and control over the international financial system. It also helped stabilize the dollar and supported its status as a global reserve currency.

However, with these privileges came great responsibilities toward all nations. Following the Golden Rule, the United States had a moral and ethical obligation to treat others as it would like to be treated. It failed on this crucial responsibility, and the consequences are now obvious.

In contracts, the language calls for “duty of good faith and fair dealing,” which prohibits one party from interfering with the other’s performance or undermining their expected benefits. A breach of this duty is a serious legal offense.

Similarly, in international relations, utilizing hegemony to shape international systems through coercive or noncoercive means violates this fundamental principle of law. It is a dangerous path, particularly when the global reserve currency is weaponized to achieve political, economic, or military dominance.

Unless the US practices what it preaches toward other nations, confidence will erode, and global trade and economic stability will be threatened worldwide. Given the interconnectedness of the world, pulling on one string of the spiderweb will shake the entire web. We are witnessing this phenomenon with the emergence of a global rebellion by nations that threaten to abandon the dollar as the world’s reserve currency to return to a more responsible form of money backed by gold.

Despite efforts by state regulators to find solutions, their actions have mostly been ineffective due to strong political opposition. Professor William Greene proposed an alternative approach in an article titled “Ending the Federal Reserve from the Bottom Up.” He suggested focusing on the negative mandate of Article I, Section 10 of the US Constitution, which states that “no State shall . . . make any Thing but gold and silver Coin a Tender in Payment of Debts.” He called this approach the “Constitutional Tender Act,” a template for a bill that can be introduced in every state.

His approach is intriguing, but it remains a risky proposition. At best, it would take months, if not years, to align the collective political will necessary to rectify the situation. Clearly, it is not the optimal choice.

It is imperative for all fifty US states to prepare for a potentially catastrophic collapse of the US dollar along with the ensuing worldwide aftermath. The resulting damage at the state level could be unimaginable.

What Is the Best Option?

Every surfer knows that there’s a precise moment to start paddling to catch a wave before it breaks. Start too early and it crashes upon you. Start too late, you miss it entirely. Timing is crucial if we want to harness the full power of the waves. Likewise, any state aiming to break free from the Federal Reserve must be prepared to seize that wave as soon as possible.

This new wave is the coalition of nations advocating for a sound monetary system backed by gold to replace the US dollar as the global reserve currency. The collective strength of this group allows them to fearlessly voice their dissatisfaction alongside other discontented national leaders. It’s a formidable pushback that is rapidly gaining traction. Beginning June 14, 2023, over one hundred countries have convened at the economic summit in St. Petersburg, Russia, to discuss the creation of such a gold-backed monetary system to replace the US dollar as the dominant currency.

What Is the Solution for a State?

Surprisingly, it is more simple than we might imagine. While the dollar won’t be displaced overnight, fostering a competitive environment where it needs to compete with sound money backed by gold is the best option for all fifty states. Citizens can decide which currency they trust, and the laws of supply and demand will determine the winner.

Currently, there are seven US states with existing laws granting legal tender status to foreign currencies that have legal tender status within their foreign borders. These states are Texas, Louisiana, Florida, Oklahoma, Tennessee, Alaska, and Arkansas.

Once a foreign country gives legal tender status to a secure, stable, functional, transparent, and legitimate gold-backed monetary system within its territory, it will have de facto legal tender status in these seven US states. Many friendly nations will soon have a solution to offer these seven states who are well-positioned to catch that wave when the opportunity presents itself.

Local governments should take proactive measures to prepare for the inevitable. While a governor’s executive order to supplement existing laws may not be necessary, such an order could help rally and focus statewide attention on the opportunity. One or more of these seven states could become a powerful magnet, attracting individuals who seek to move away from fiat currencies to money backed by gold. There is a significant first-mover advantage awaiting any state (or a group of states acting in unison) that takes the lead.

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

end

3,Chris Powell of GATA provides to us very important physical commentaries

Alasdair Macleod: The bell tolls for fiat

Submitted by admin on Thu, 2023-07-13 11:58Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, July 13, 2023

The importance of Russia’s announcement that a new gold-backed trade currency is on the BRICS meeting agenda for August 22—24 in Johannesburg seems to have gone completely over everyone’s heads, with mainstream media not even reporting it.

This is a mistake. China and Russia know that if they are to succeed in removing the dollar from their sphere of influence, they have to come up with a better alternative. They also know they have to consolidate their trade partners into a formidable bloc, so plans are afoot to consolidate BRICS, the Shanghai Cooperation Organisation, and the Eurasian Economic Union along with those nations that wish to join. It will be a super-group embracing most of Asia (including the Middle East), Africa, and Latin America.

The groundwork for the new currency has been laid by Sergei Glazyev and is considerably more advanced than generally realised.

This article explains why Russia and China are now prepared to fully back Glazyev’s expanded project.

For Russia, it is also now imperative to destabilise the dollar as a deliberate escalation of the financial war against America and NATO.

China’s priority is no longer to protect her export trade but to ensure that her African and Latin American suppliers are not destabilised by higher dollar interest rates. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/the-bell-tolls-for-fiat?gmrefcode=gata

end

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/

ANDREW MAGUIRE

LIVE FROM THE VAULT

August BRICS Summit hails death knell for the dollar – Live From the Vault Ep: 131

end

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//COCOA

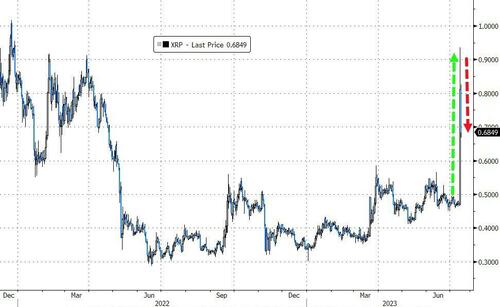

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1359

OFFSHORE YUAN: UP TO 7.1425

SHANGHAI CLOSED UP 1.22 PTS OR 0.04%

HANG SENG CLOSED UP 63.16 PTS OR 0.33%

2. Nikkei closed DOWN 28.08 PTS OR 0.09%

3. Europe stocks SO FAR: ALMOST ALL GREEN

USA dollar INDEX DOWN TO 99.46 EURO RISES TO 1.1229 UP 6 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.474 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 138.45/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ON SHORE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.4375***/Italian 10 Yr bond yield FALLS to 4.123*** /SPAIN 10 YR BOND YIELD RISES TO 3.490…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 3.907

3j Gold at $1959.45 silver at: 24.81 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 7 /100 roubles/dollar; ROUBLE AT 90.18//

3m oil into the 76 dollar handle for WTI and 81 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 138.45// 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO 0.461% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8589 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9646 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.7660 DOWN 0 BASIS PTS…

USA 30 YR BOND YIELD: 3.8940 DOWN 0 BASIS PTS/

USA 2 YR BOND YIELD: 4.639 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.20…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 2 BASIS PTS AT 4.4265

end

2. Overnight: Newsquawk and Zero hedge:

Futures Flat As Q2 Earnings Seasons Kicks Off

FRIDAY, JUL 14, 2023 – 07:11 AM

The week’s powerful rally which sent US stocks to a new 52-week high has faded, with futs down small after a quiet overnight session on the day JPM officially ushers in Q2 earnings season as the post-CPI market rally pauses for breath as investors contemplate how recent US inflation data will impact upcoming Fed policy decisions. As of 6:45am ET S&P futures are flat at 4,542 while Nasdaq futures are down 0.1%. Bond yields are 3-5bp higher, and the USD has reversed higher after dropping the lowest level in more than a year. Commodities are mixed with energy lagging and base metals such as iron ore extending gains from yesterday. Yesterday’s dovish PPI and lower-than-expected initial claims supports the soft-landing narrative. Key focus today will be banks earnings; JPM, C and WFC report pre-market. Keep an eye on banks’ commentary on consumer health, credit trends and loan growth. We will also get the latest UMich sentiment data (consensus sees 65.5 vs. 64.4 prior); 1yr inflation expectation is estimated to fell to its lowest in two years

In premarket trading, mega-cap tech stocks are mixed; Banks are mostly higher. Microsoft rose 1.6% in premarket trading as UBS raised the recommendation on the software giant’s stock to buy from neutral, saying cloud infrastructure spending is starting to stabilize after a significant deceleration over the past year. UnitedHealth Group Inc. gained after an earnings beat. Nikola soared as much as 25% set to extend Thursday’s 61% rally, after BayoTech agreed to buy up to 50 of its hydrogen-fuel-cell EVs over the next five years. If the gains hold until close, it will be the biggest weekly gain on record for the stock. Here are some other notable premarket movers:

- Acadia Pharmaceuticals (ACAD US) shares surged 20% in premarket trading after the biotech firm said it had expanded its licensing agreement with Neuren Pharmaceuticals to acquire the ex-North American rights for Daybue (trofinetide), which is used to treat Rett syndrome.

- Leslie’s (LESL US) shares drop 30% in premarket trading after the pool-supplies retailer cut its full-year adjusted earnings per share guidance. Analysts highlighted the sales weakness in the third quarter, with Piper Sandler downgrading their recommendation on the stock to neutral from overweight.

- Roivant Sciences (ROIV US) rose as much as 12% in premarket trading after a Wall Street Journal report the company is in talks to sell its treatment for inflammatory bowel disease to Roche Holding.

- Intuitive Machines (LUNR US) climbed as much as 32% in premarket trading, after the company said it successfully completed a spacecraft test run of its Nova-C lunar lander at the Houston Spaceport.

As Bloomberg notes, it’s been a week when almost everything rallied — from emerging markets to global bonds and the S&P 500 — all buoyed by faith that the Federal Reserve is finally winning the fight against inflation. While trading was subdued on Friday, investors are finishing the week with blockbuster gains across asset classes. MSCI’s global stock benchmark has leapt 3.5% in the past five days, the biggest advance since November.

“The market has been partying like it’s 1999 this week,” said DB’s Jim Reid. “It’s hard to stand in the way of that narrative at the moment regardless of what eventually happens.”

Bonds climbed too over the week with the US two-year rate, the most sensitive to short-term policy moves, dropping as much as 30 basis points.

The bullish trades reflect hope that the US is heading toward a “Goldilocks scenario” with inflation quickly easing while the economy avoids a recession. To be sure, the Fed is still likely to lift its benchmark rate later this month and central bankers continue to warn that more than one rate increase may still be necessary after that. The earnings season also kicks off in the US today with lenders JPMorgan Chase, Wells Fargo and Citigroup reporting.

“The Fed has already won the battle against inflation,” Raffaele Bertoni, head of debt capital markets at Gulf Investment Corp., said on Bloomberg Television. “If they want to be serious in maintaining inflation under control, the focus should be more on the reduction of the balance sheet or the quantitative tightening rather than increasing rates further.”

Fed Bank of San Francisco President Mary Daly, however, told CNBC Thursday that it’s too soon for policymakers to say they have done enough to return US inflation to their target. Fed Governor Christopher Waller also said he expects the US central bank will need to raise rates twice more this year to bring inflation down to its target.

Traders are now looking to earnings reports to reignite the rally. The focus is going to be mostly on the corporate outlooks given that beating profit expectations seems to be a low hurdle, even as some estimates have started to rise slowly. “Given that consensus expectations appear reasonable and valuations are already rich (not only in tech), only strong beats are likely to result in substantial price gains, while even small misses may lead to sharper drops,” said Wolf von Rotberg, an equity strategist at Bank J Safra Sarasin.

European stocks are also little changed with the Stoxx 600 coming off a five-session winning streak. Among individual stock movers in Europe, Nokia Oyj slumped more than 8% after the Finnish vendor of 5G equipment lowered its guidance. Ericsson dropped almost 8% as analysts pointed to a weak margin outlook for the Swedish telecom equipment maker. Swiss money manager Partners Group Holding AG gained more than 7% after assets under management rose in the first half. Here are the most notable European movers:

- Partners Group shares gain as much as 7.8%, most since May, after it posted a “positive” update on its assets under management, helping offset negative expectations for the firm ahead of the results

- Heineken rises as much as 2.7% after being raised to buy at Goldman Sachs as the broker expects the world’s second-largest brewer to “fully benefit” from raw material cost deflation

- Axfood shares rise as much as 8.2% to a two-month high after the Swedish food retailer’s second-quarter operating profit beat estimates, with analysts pointing to strength in its discount chain

- Brunello Cucinelli shares gain as much as 2.1% after the luxury clothier reported what analysts called a strong sales update, and increased full-year guidance

- Vallourec shares climb as much as 7.3%, the most since May, after French tube maker sees 2Q exceeding prior expectations, with Jefferies saying deleveraging plans are working

- Nokia falls as much as 10%, the most since January 2021, after an unscheduled profit warning and outlook cut, hinting an expected recovery in the sector is further away than earlier projected

- Ericsson shares dropped as much as 9.2%, as analysts pointed to a weak margin outlook for the Swedish telecom equipment maker in the third quarter and worries of poor US demand

- Brenntag shares dropped as much as 4.1% after the chemicals distributor was downgraded to underweight from neutral at JPMorgan, saying it struggles with “significant demand weakness”

- Ashmore shares fell as much as 8.3%, the most since November, after the emerging markets-focused asset manager’s AUM disappointed, with Nubis saying investment performance remains “poor”

- EMS-Chemie falls as much as 3.3%, the most since April. While the company’s first-half figures were in line with low expectations its full-year outlook was reduced further, ZKB notes

- Sixt slides as much as 6.7% in Frankfurt trading after being downgraded to hold from buy at Deutsche Bank, expecting the car-rental firm’s profit to drop in 2023

Earlier in the session, Asian stocks were on course for their best week since Nov. 2022, with Chinese equities rallying and peak-rate bets on the Federal Reserve boosting risk sentiment. The MSCI Asia Pacific Index rises as much as 0.8%, with gains for the week nearing 5%. Stocks in Korea, Taiwan and New Zealand led the advance on Friday. Chinese equities have been at the center of the risk rally in Asia, as traders increasingly see an end to years of regulatory crackdowns on technology firms. Other than gains in tech bellwethers such as Alibaba Group Holding Ltd., the broader market also advanced on hopes of more policy stimulus. An index of Chinese companies in Hong Kong is set for the biggest weekly gains since the first week of 2023. Risk appetite was also boosted as the US dollar and Treasury yields fell with softer inflation data in the US. Traders are now pricing in just one more rate hike this year from the Fed. Chinese tech stocks were volatile Friday, with Xiaomi and Meituan falling, after the Hang Seng Tech Index rose for four days in its longest rising streak since mid-June. The Hang Seng Tech Index erases losses of as much as 0.9% in the morning to trade 0.1% higher. Meituan, which was among the best performing stocks on the gauge in the past four days, drops as much as 1.4% on Friday; Xiaomi -1.4%. EV makers Nio down as much as 4.7% and XPeng -7.7%. Stocks fluctuated in Japan as the yen headed for a seven-day winning streak, which would mark its best performance since 2018.

“Risk on in emerging markets, especially, in China makes sense,” David Chao, global market strategist for Asia Pacific at Invesco Asset Management told Bloomberg television in an interview. Chao sees Chinese equities emerging among the best performers in second half of 2023. Stocks in Thailand rose even as a leading candidate for the prime ministerial post failed to win endorsement from the Parliament.

In FX, the Bloomberg Dollar Spot Index is flat although still on course for its largest weekly decline since November. USD/JPY climbed 0.2% to 138 in a reversal of the yen’s longest bull streak since 2018. GBP/USD held ground above 1.31, while EUR/USD wavered around 1.12. The offshore yuan ticked higher. China has ample foreign exchange reserves and will “resolutely” prevent wild swings in the yuan exchange rate, People’s Bank of China Deputy Governor Liu Guoqiang said at a briefing Friday. The currency’s short-term movement cannot be predicted accurately, but it hasn’t deviated from its fundamentals, Liu added.

In rates, treasuries fell, trimming their biggest two-day gain since early May as two-year and 10-year yields hover around their lowest levels in one month/ Two-year yields rose four basis points to 4.67% and 10- year yields climbed three basis points to 3.79%

In commodities, oil headed for a third weekly gain as supply disruptions in Africa and a reduction in shipments from Russia tightened the market; crude futures are flat with WTI trading near $76.85. Spot gold falls 0.2%. Gold was set for the best week since April.

Bitcoin is under modest pressure despite the USD continuing to languish with drivers thin and the docket ahead relatively spares aside from crucial banking updates.

To the day ahead now, and earnings season will step up a gear as we hear from JPMorgan, Citigroup Wells Fargo and BlackRock. Otherwise, data releases include the University of Michigan’s preliminary consumer sentiment index for July.

Market Snapshot

- S&P 500 futures little changed at 4,542.00

- MXAP up 0.6% to 168.93

- MXAPJ up 0.9% to 535.06

- Nikkei little changed at 32,391.26

- Topix down 0.2% to 2,239.10

- Hang Seng Index up 0.3% to 19,413.78

- Shanghai Composite little changed at 3,237.70

- Sensex up 0.5% to 65,888.13

- Australia S&P/ASX 200 up 0.8% to 7,303.08

- Kospi up 1.4% to 2,628.30

- STOXX Europe 600 little changed at 461.66

- German 10Y yield little changed at 2.50%

- Euro little changed at $1.1231

- Brent Futures little changed at $81.33/bbl

- Gold spot down 0.2% to $1,957.38

- U.S. Dollar Index little changed at 99.76

Top Overnight News

- The PBOC signaled more targeted support may be on the cards for the property market as it sought to assure investors that the risks banks face from the sector are controllable. BBG

- The US has launched a round of diplomacy with China to help soften the blow from new tech export restrictions that are expected to be announced soon. SCMP

- China loses its title as the top exporter of goods to the US for the first time in 15 years, falling behind Mexico and Canada. Nikkei

- BOJ is having internal discussions about tweaking the YCC policy as soon as this month, although no final decision has been made (any change would likely be very minor). RTRS

- Australia will promote deputy governor Michele Bullock to take over the RBA, deciding against giving Philip Lowe another term. FT

- Europe asks its metals suppliers to make semiconductor materials amid worries about China restrictions, but this may require state aid. FT

- Odds are growing that the Fed’s 25bp rate hike later this month will be the final one of the cycle, but officials want to see more evidence of disinflation before declaring victory. WSJ

- DeSantis is considering a course correction as his campaign struggles to gain traction. ABC News

- AMZN has created a new internal organization aimed at helping customers utilize generative AI tools on AWS. Insider

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly higher after the positive lead from Wall St where yields continued to decline as PPI data followed suit to the softer consumer inflation and supported the case for just one more Fed rate hike. ASX 200 was firmer with gains in the index led by the tech sector after similar outperformance of US counterparts amid a decline in yields, while the announcement that RBA Deputy Governor Bullock will take over from Governor Lowe in September had little effect on markets and was largely seen as policy continuation. Nikkei 225 swung between gains and losses with headwinds from JPY strength and speculation that the BoJ could raise its inflation forecast above the 2% target at its meeting this month, which could pave the way for policy normalisation, while former BoJ Director Hayakawa expects the BoJ to tweak yield curve control at the upcoming meeting by potentially raising the 10yr yield ceiling to 1.0%. Hang Seng and Shanghai Comp were positive albeit with gains capped despite the renewed support pledges by the PBoC to keep credit growth appropriate, as well as step up counter-cyclical adjustments and support for key sectors.

Top Asian News

- PBoC Deputy Governor Liu said China’s overall liquidity is ample and its credit structure improved in H1, while he also noted that financing costs stabilised and dropped in H1. Liu said the PBoC has ample policy tools and will step up counter-cyclical adjustments, as well as improve financial services for tech companies, guide banks to boost lending for tech companies and will increase support for SMEs and the green sector, according to Reuters.

- PBoC official said they will keep credit growth appropriate and step up support for key sectors, while the central bank will deepen interest rate reforms and will guide banks to increase lending to small firms and private firms. Furthermore, the official said there is ample room and various policy tools to cope with challenges, while they will use policy tools such as RRR and MLF, as well as innovate new policy tools if needed, according to Reuters.

- China’s top diplomat Wang Yi said US and China need to take practical actions to bring back ties onto the right track and that the US should adopt a rational and pragmatic attitude and meet China halfway. Wang also said the US must refrain from interfering in China’s internal affairs and stop suppressing China’s economy, trade, and technology, while the US must lift illegal and unreasonable sanctions against China, according to Xinhua.

- Australia named Deputy Governor Bullock as the next RBA Governor from September 18th, while Bullock said she is committed to ensuring that the Reserve Bank delivers on its policy and operational objectives.

- Chinese regulators are reportedly to meet with global investors in order to shore up economic confidence, via Reuters citing sources; focused on the current conditions of USD-denominated investment firms and the main challenges they face. Meeting will take place on Friday 21st July. Investors will be invited to provide suggestions on how to combat the challenges they are facing and to give their views on the Chinese economy.

European bourses are contained but remain on track to close the week out with marked gains, Stoxx 600 set for +3% WTD upside. Sectors are somewhat mixed with defensive names outperforming on the tentative tone while Telecom. lags after Nokia and Ericsson’s respective updates. Stateside, futures are near the unchanged mark as we await the final scheduled Fed speak before blackout commences alongside the formal commencement of Q2 earnings season. UnitedHealth Group Inc (UNH) Q2 2023 (USD): EPS 6.14 (exp. 6.01), Revenue 92.9bln (exp. 91.bln); FY23 adj. Net guidance 24.70-25.00/shr (exp. 24.76). +2.1% in pre-market trade. Nokia (NOKIA FH) – Q2 (EUR): Revenue 5.7bln (exp. 6.03bln), adj. EBIT Margin 11%. Cuts FY23 sales outlook to EUR 23.2-24.6bln (exp. 25.57bln, prev. 24.6-26.2bln). Weaker demand outlook in H2 is due to both the macro-economic environment and customers inventory digestion. UK CMA considers there is insufficient time remaining within the statutory period for a full and proper consideration of Microsoft’s (MSFT) submission re. the proposed Activision (ATVI) deal; revised period to end on 29th August 2023.

Top European News

- Nordic Mobile Equipment Makers Fall as Nokia Cuts Guidance

- Vallourec Jumps as Tube Maker Predicts Better-Than- Forecast 2

- Heineken Gains as Goldman Upgrades to Buy on Margin Outlook

- Sixt Drops; Deutsche Bank Downgrades on Weak Profit Momentum

- London Gatwick Airport Workers to Strike Over Pay, Union Says

- Nordic Banks Tested as Property Slumps: EMEA Earnings Week Ahead

FX

- DXY finds a base just above 99.500 after another heavy decline and approaching end of bleak week that started with the index peaking around 102.500.

- Aussie and Kiwi make way for Buck bounce as AUD/USD fades ahead of 0.6900 and NZD/USD from 0.6400+ at best.

- Yen retreats from 137.26 towards 138.50 as JGB-UST spreads re-widen.

- Euro and Pound pull up shy of 1.3150 and 1.1250 vs Dollar respectively, but EUR/USD evades 1bln option expiries at 1.1200, for now.

- BoJ to host the first long-term policy review workshop in December, to discuss monetary policy and financial systems. Second workshop in May 2024. To discuss analyses comprehensively until that point.

- PBoC set USD/CNY mid-point at 7.1318 vs exp. 7.1453 (prev. 7.1527)

Fixed Income

- Debt diverges towards the end of a hectic and mainly corrective bull-steepening week

- Bunds and Gilts above par between 133.18-132.69 and 95.02-94.53 respective bands, but T-note underwater within 113-01+/112-21 overnight range awaiting US import/export prices

- Fed’s Goolsbee and UoM sentiment with inflation expectation. JGBs volatile amidst contrasting BoJ vibes

Commodities

- A contained and catalyst-thin session thus far to conclude a busy week of macro developments before the Fed blackout begins and attention turns to the next round of Central Bank announcements.

- WTI Aug’23 and Brent Sep’23 are on track to conclude the week with gains of circa. USD 2.50/bbl and are currently at the upper-end of the week’s USD 72.67-77.33/bbl and USD 77.36-81.75/bbl respective parameters.

- Spot gold is a touch softer but holds above the USD 1950/oz handle around the USD 1954/oz 50-DMA; base metals more mixed as it stands.

- Qatar set September-loading Al-Shaheen crude term prices at USD 1.68/bbl above Dubai quotes.

Geopolitics

- Russian President Putin said new weapons supplies will further escalate the conflict in Ukraine and worsen the situation. It was separately reported that Putin also said he proposed to Wagner fighters at a meeting this month to continue serving in the military, while he added that Russia’s government and parliament must discuss the legal framework for private armies and said without a legal framework, ‘Wagner does not exist’, according to Kommersant.

US Event Calendar

- 08:30: June Import Price Index MoM, est. -0.1%, prior -0.6%; YoY, est. -6.1%, prior -5.9%

- June Export Price Index MoM, est. -0.1%, prior -1.9%; YoY, est. -11.0%, prior -10.1%

- 10:00: July U. of Mich. Sentiment, est. 65.5, prior 64.4

- U. of Mich. Expectations, est. 62.0, prior 61.5

- U. of Mich. Current Conditions, est. 70.5, prior 69.0

- U. of Mich. 1 Yr Inflation, est. 3.1%, prior 3.3%

- U. of Mich. 5-10 Yr Inflation, est. 3.0%, prior 3.0%

DB’s Jim Reid concludes the overnight wrap

After a hectic week, I’m playing a gig at a good friend’s 50th birthday party tomorrow night. I haven’t done any practise so I’m relying on a set list that worked 20 years ago. Given the nature of the event I’m assuming the audience won’t have heard much new music in that period so we should all be ok. If it all goes well I’ll be digging out research from 20 years ago as well to see if I can pull off the same trick.

The market has been partying like it’s 1999 this week, with the rally showing no sign of letting up over the last 24 hours, with bonds and equities surging thanks to growing hopes of a soft landing. It’s hard to stand in the way of that narrative at the moment regardless of what eventually happens. Much of that was propelled by the previous day’s CPI release, but investors then got a further dose of optimism from a weaker-than-expected PPI print, as well as the weekly jobless claims that were below consensus. That supported a fresh multi-asset advance, with the S&P 500 (+0.85%) and NASDAQ (+1.58%) closing at 15-month highs, yields on 10yr Treasuries falling -9.4bps to 3.77%, and Brent Crude oil prices closing at a 2-month high of $81.36/bbl. And that’s all before we start Q2 US earnings season today.

These moves over the last week have been part of an astonishing turnaround in the market narrative. After all, it was only on Thursday of last week that the bumper ADP report sent the 2yr Treasury yield up to 5.12% intraday, which is its highest level since 2007. But since then, we’ve had the smallest monthly jobs growth (+209k) since December 2020, along with the weakest core CPI (+0.16%) since February 2021, and investors are pricing in a growing chance of multiple rate cuts next year.

When it came to those developments yesterday, the main story was that monthly PPI came in at just +0.1%, and the previous month was revised down a tenth to -0.4%. So more positive news on the inflation side. In turn, that took the year-on-year PPI close to deflationary territory at +0.1% (vs. +0.4% expected), which is the lowest it’s been since August 2020. In addition, the core PPI measure excluding food and energy was at a monthly +0.1% (vs. +0.2% expected), with the year-on-year measure down to +2.4% (vs. +2.6% expected).

That downside surprise helped cement the message from the previous day’s CPI report. In particular, it meant investors became increasingly confident that the next meeting would mark the final rate hike of the current cycle, despite the Fed’s signal in their recent dot plot for two more. For example, the terminal rate priced in for November came down -1.5bps to 5.37%. And looking further out into 2024, the year-end rate came down a further -18.7bps to 3.725%. Bear in mind that after the ADP report, futures were briefly pricing in a 4.51% rate for December 2024, so the recent newsflow has led markets to price around three more 25bp rate cuts compared to a week ago.

The prospect of more rate cuts meant that sovereign bonds got a lift on both sides of the Atlantic. Yields on 10yr Treasuries were down -9.4bps to 3.77%, and those on 2yr Treasuries fell -11.2bps to 4.64%. In Europe it was a similar story, with yields on 10yr bunds (-8.9bps), OATs (-8.8bps) and BTPs (-12.1bps) all coming down as well.

The US rates move came in spite of comments from San Francisco Fed President Daly, who said it was “really too early to say that we’ve declared victory on inflation”. Later in the day, the generally hawkish Federal Reserve Governor Waller noted that he still saw two more hikes this year as necessary, though he added that if the next two inflation prints “look like the last two, the data would suggest maybe stopping” by September. So it seems that many FOMC members are still sceptical of the slowing inflation data but keeping an open mind. We won’t hear from many more Fed speakers now, since today is the last day before their blackout period ahead of the next meeting. In other Fed news yesterday, we heard that St Louis Fed President Bullard, another of the most hawkish FOMC members, was stepping down from this role. He wasn’t a voter this year, but his views held sway.

For equities, these hopes of a soft landing meant that the US indices hit fresh landmarks, with both the S&P 500 (+0.85%) and the NASDAQ (+1.58%) at a 15-month high. Tech stocks led the advance, with the FANG+ index (+2.70%) reaching a new all-time high, passing its previous peak from November 2021, having now risen by +80.86% on a YTD basis. Meanwhile in Europe, the STOXX 600 (+0.61%) advanced for a 5th consecutive session for the first time since April. There were some positive earnings releases as well, with PepsiCo (+2.38%) raising its outlook. Today will see further reports from the major US financials as well, including JPMorgan, Citigroup, Wells Fargo and BlackRock.

All this optimism over the economic outlook was bolstered again by the weekly jobless claims. They showed the initial claims down to 237k in the week ending July 8 (vs. 250k expected), which took the 4-week moving average down to a one-month low of 246.75k. Continuing claims did edge up from 1720k to 1729k but was largely brushed aside. There was also some better-than-expected data out of the UK, since monthly GDP in May only contracted by -0.1% (vs. -0.3% expected), despite the impact from the coronation bank holiday.

Asian equity markets are largely extending the global rally and are on course for their best week this year. The KOSPI (+1.14%) is leading gains with the Hang Seng (+0.44%), the Nikkei (+0.23%), the Shanghai Composite (+0.016%) and the CSI (+0.07%) also trading higher. Outside of Asia, US stock futures are pausing for breath with those on the S&P 500 (-0.06%) just below flat while those on the NASDAQ 100 (+0.08%) slightly higher ahead of the big bank earnings today. US treasuries are back up around a basis point across the curve after the huge rally this week.

In FX, the dollar index (which measures it against six major peers) is hovering around at a 15-month low of 99.59. Meanwhile, the Japanese yen is rallying for the seventh day, trading below 138 per dollar, its strongest level since May as we go to print.

On commodities, there was some interesting news as Bloomberg reported that India were considering banning exports of all non-Basmati rice, citing “people familiar with the matter.” That comes against the backdrop of significant rises in rice prices, following concerns that El Nino conditions will lead to a drought. Speaking of the El Nino, we also had the latest monthly update from the US’ Climate Prediction Center yesterday. Their forecasts are broadly similar to before, but they slightly downgraded the chances that the current El Nino would develop into a strong one, with the probability down to 52% at the peak (vs. 56% last month).

To the day ahead now, and earnings season will step up a gear as we hear from JPMorgan, Citigroup Wells Fargo and BlackRock. Otherwise, data releases include the University of Michigan’s preliminary consumer sentiment index for July.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

Tentative trade ahead of earnings & final pre-blackout Fed speak – Newsquawk US Market Open

FRIDAY, JUL 14, 2023 – 06:00 AM

- European bourses & US futures are relatively contained ahead of Fed speak and banking earnings

- Within Europe, Telecoms lag after updates from Ericsson and Nokia

- DXY struggles for direction just above 99.75 with peers mixed & JPY retreating

- Core fixed benchmarks diverge slightly as EGBs/Gilts extend while USTs slip ahead of data

- Commodities are generally contained with catalysts thin after a week of USD-driven upside

- Looking ahead, highlights include US Import & Export Prices, UoM Sentiment (Prelim), US Treasury Dealer Meeting Agenda. Earnings from JPMorgan, Wells Fargo, BlackRock & Citigroup. Fed’s Goolsbee.

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses are contained but remain on track to close the week out with marked gains, Stoxx 600 set for +3% WTD upside.

- Sectors are somewhat mixed with defensive names outperforming on the tentative tone while Telecom. lags after Nokia and Ericsson’s respective updates.

- Stateside, futures are near the unchanged mark as we await the final scheduled Fed speak before blackout commences alongside the formal commencement of Q2 earnings season.

- UnitedHealth Group Inc (UNH) Q2 2023 (USD): EPS 6.14 (exp. 6.01), Revenue 92.9bln (exp. 91.bln); FY23 adj. Net guidance 24.70-25.00/shr (exp. 24.76). +2.1% in pre-market trade

- Nokia (NOKIA FH) – Q2 (EUR): Revenue 5.7bln (exp. 6.03bln), adj. EBIT Margin 11%. Cuts FY23 sales outlook to EUR 23.2-24.6bln (exp. 25.57bln, prev. 24.6-26.2bln). Weaker demand outlook in H2 is due to both the macro-economic environment and customers inventory digestion.

- UK CMA considers there is insufficient time remaining within the statutory period for a full and proper consideration of Microsoft’s (MSFT) submission re. the proposed Activision (ATVI) deal; revised period to end on 29th August 2023.

- Click here for more detail.

- Click here and here for a recap of the main European equity updates.

FX

- DXY finds a base just above 99.500 after another heavy decline and approaching end of bleak week that started with the index peaking around 102.500.