GOLD PRICE CLOSED: UP $6.35 TO $1968.90

SILVER PRICE CLOSED: UP $0.15 AT $24.80

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1973.55

Silver ACCESS CLOSE: 24.95

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $29,247 UP 62 Dollars

Bitcoin: afternoon price: $29,310 UP 126 dollars

Platinum price closing $969.80 UP $6.05

Palladium price; $1295,00 UP $14.40

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,605.79 UP 17.23 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1524.85 UP 1.80 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1779.82 UP 2.90 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,962.100000000 USD

INTENT DATE: 07/25/2023 DELIVERY DATE: 07/27/2023

FIRM ORG FIRM NAME ISSUED STOPPED 132 C SG AMERICAS 7

435 H SCOTIA CAPITAL 4

624 H BOFA SECURITIES 3

JPMorgan stopped 0/7 contracts.

FOR JULY:

GOLD: NUMBER OF NOTICES FILED FOR JULY/2023. CONTRACT: 7 NOTICES FOR 700 OZ or 0.02177 TONNES

total notices so far: 3282 contracts for 328,200 oz (10.208 tonnes)

FOR JULY:

SILVER NOTICES: 26 NOTICE(S) FILED FOR 130,000 OZ/

total number of notices filed so far this month : 5095 for 25,475,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $6.35

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 919.00 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP $0.15 AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE SLV:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 452.480 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 273 CONTRACTS TO 147,084 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS GIGANTIC SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.24 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. TAS ISSUANCE WAS A STRONG SIZED 734 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH . CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 341 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.24). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A HUGE GAIN ON OUR TWO EXCHANGES OF 973 CONTRACTS. WE HAD A HUGE 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 5.25 MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 700 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 16.110 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S HUGE 135,000 QUEUE JUMP + 0 MILLION OZ EXCHANGE FOR RISK FOR TODAY//NEW STANDING: 25.605 MILLION OZ + 5.25 MILLION OZ EXCHANGE FOR RISK/PRIOR: NEW TOTAL 30.855 MILLION OZ// // GOOD SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/VI) GOOD NUMBER OF T.A.S. CONTRACT ISSUANCE (341 CONTRACTS)/ZERO EXCHANGE FOR RISK ISSUED/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –186 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTRACTS for 16 days, total 16,776 contracts: OR 83.880 MILLION OZ (1048 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 83.880 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 83.880 MILLION OZ (LARGER THAN LAST MONTH)

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 273 CONTRACTS WITH OUR GAIN IN PRICE OF $0.24 IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG EFP ISSUANCE CONTRACTS: 700 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 16.110 MILLION OZ FOLLOWED BY TODAY’S HUGE 135,000 OZ QUEUE. JUMP + 0 MILLION OZ EXCHANGE FOR RISK TODAY + (PRIOR EXCHANGE FOR RISK : 5.25 MILLION OZ): TOTAL NOW STANDING 25.605 MILLION OZ NORMAL STANDING + 5.25 MILLION EXCHANGE FOR RISK = 30.855 MILLION OZ.///// .. WE HAVE A HUGE SIZED GAIN OF 973 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GOOD 341//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION TO CONTAIN SILVER PRICE’S RISE. THE NEW TAS ISSUANCE TODAY (734) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE./

WE HAD 26 NOTICE(S) FILED TODAY FOR 130,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 11,056 CONTRACTS TO 476.758 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED: 582 CONTRACTS

WE HAD A GOOD SIZED DECREASE IN COMEX OI ( 10,474 CONTRACTS) DESPITE OUR $2.45 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JULY. AT 5.1975 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0.05287 TONNE QUEUE JUMP: NEW TOTAL OF GOLD STANDING FOR JULY: 10.386 TONNES// + /A FAIR (AND CRIMINAL) ISSUANCE OF 2487 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $2.45 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING.WE HAD A STRONG SIZED LOSS OF 6473 OI CONTRACTS (20.133 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4583 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 476,758

IN ESSENCE WE HAVE A GOOD SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6473 CONTRACTS WITH 11,056 CONTRACTS DECREASED AT THE COMEX// AND A GOOD 4583 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 6473 CONTRACTS OR 20.133 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 2487 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4583 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (10,474) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 6473 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 5.1975 TONNES FOLLOWED BY TODAY’S 0.05287 TONNE QUEUE JUMP//NEW TOTAL 10.386 TONNES ///// /3) SOME LONG LIQUIDATION WITH HUGE TAS LIQUIDATION AND SPREADER LIQUIDATION TO CONTAIN GOLD’S PRICE//4) STRONG SIZED COMEX OPEN INTEREST LOSS/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 2487 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

TOTAL EFP CONTRACTS ISSUED: 38,838 CONTRACTS OR 3,883,800 OZ OR 120.78 TONNES IN 16 TRADING DAY(S) AND THUS AVERAGING: 2283 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES 120.78 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 120.78/3550 x 100% TONNES 3.40% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 120.78 TONNES (WEAKER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A SMALL SIZED 273 CONTRACTS OI TO 147,084 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 700 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 570 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 700 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 273 CONTRACTS AND ADD TO THE 700 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 973 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 4.865 MILLION OZ

OCCURRED WITH OUR $0.24 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 8.49 PTS OR 0.26% //Hang Seng CLOSED DOWN 69.26 PTS OR 0.36% /The Nikkei CLOSED DOWN 14.17 PTS OR 0.04% //Australia’s all ordinaries CLOSED UP 0.84 % /Chinese yuan (ONSHORE) closed UP 7.1534 /OFFSHORE CHINESE YUAN UP TO 7.1538 /Oil UP TO 78.79 dollars per barrel for WTI and BRENT UP AT 82.75 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A VERY STRONG SIZED 11,056 CONTRACTS DOWN TO 476,176 DESPITE OUR GAIN IN PRICE OF $2.45 ON TUESDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4583 EFP CONTRACTS WERE ISSUED: : AUGUST 4583 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4583 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 6473 CONTRACTS IN THAT 4583 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 11,056 COMEX CONTRACTS..AND THIS GOOD SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GAIN IN PRICE OF $2.45//TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A FAIR 2487 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US TRYING TO CONTAIN OUR PRECIOUS METALS RISE IN PRICE. IT MAY BE TO NO AVAIL!!

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (10.386) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.386 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $2.45) //// BUT WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD A GOOD SIZED LOSS OF 6473 CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE TAS LIQUIDATION THROUGHOUT THE TUESDAY COMEX SESSION TRYING DESPERATELY TO CONTAIN GOLD’S RISE. THE TAS ISSUED TUESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. WE ALSO HAD SOME SPREADER COMEX LIQUIDATION TODAY AND TOGETHER WITH THE T.A.S. LIQUIDATION YOU NO DOUBT HAVE THE REASON FOR THE HIGH OI COMEX LOSS.

WE HAVE LOST A TOTAL OI OF 20.133 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY. (5.11974 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 0.05287 TONNES//TOTAL STANDING FOR JULY GOLD: 10.386 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $2.45.

WE HAD – REMOVED 582 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 6473 CONTRACTS OR 647,300 OZ OR 20.133 TONNES.

Estimated gold volume today:// 280,826 fair

final gold volumes/yesterday 294,376 fair

//JULY 26/ FOR THE JULY 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 385.812 OZ JPM 12 kilobars . |

| Deposit to the Dealer Inventory in oz | 32,009.849 oz ASAHAI |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today | 7 notice(s) 700 OZ 0.02177 TONNES |

| No of oz to be served (notices) | 57 contracts 5700 oz 0.1773 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3282 notices 328200 OZ 10.208 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

1 dealer deposit:

i) Into ASAHI: 32,009.849 oz

total dealer deposits: 32,009.849 oz

total customer deposits: 0 oz

we had 1 customer withdrawals:

i) Out of JPM: 385.812 oz (12kilobars)

total withdrawals: 385.812 oz

Adjustments; 0/

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 64 contracts having GAINED 17 contracts. We had 0 contracts served on Tuesday. Thus we gained 17 contracts or an additional 1700 oz of gold will stand at the comex.

AUGUST LOST 38,947 contracts DOWN to 90,552 contracts. We have 3 more reading days before the big August contract delivery month.

SEPT gained 135 contracts to stand at 1005

We had 7 contracts filed for today representing 700 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 7 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2023. contract month,

we take the total number of notices filed so far for the month (3282 x 100 oz ), to which we add the difference between the open interest for the front month of JULY (64 CONTRACT) minus the number of notices served upon today 7 x 100 oz per contract equals 333,900 OZ OR 10.386 TONNES the number of TONNES standing in this NON active month of July.

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (3282) x 100 oz + (64) {OI for the front month} minus the number of notices served upon today (7) x 100 oz) which equals 333,900 oz standing OR 10.386 TONNES

TOTAL COMEX GOLD STANDING: 10.386 TONNES WHICH IS STRONG FOR A NON ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,018,846.176 OZ 62,79 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,305,812.271 OZ

TOTAL REGISTERED GOLD: 11,705,166.767 (364,9787 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,600,645.504 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,686,320 OZ (REG GOLD- PLEDGED GOLD) 301.28 tonnes//

END

SILVER/COMEX

JULY 26

//2023// THE JULY 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 344,601.607 oz BRINKS Delaware . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 1,750,945.200 oz HSBC |

| No of oz served today (contracts) | 26 CONTRACT(S) (130,000 OZ) |

| No of oz to be served (notices) | 26 contracts (130,000 oz) |

| Total monthly oz silver served (contracts) | 5095 Contracts (25,475,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) Into HSBC: 1750,945.200 oz

total customer deposits: 1,750,945.200 oz

JPMorgan has a total silver weight: 139.331 million oz/278.575 million =49.91% of comex .//

Comex withdrawals 2

i) Out of Brinks 345,546.500 oz

ii) Out of Delaware 1055.107 oz

total: 344,601.607 oz

TOTAL REGISTERED SILVER: 35.369 MILLION OZ//.TOTAL REG + ELIGIBLE. 278.578 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY /2023 OI: 52 CONTRACTS HAVING GAINED 17 CONTRACT(S). WE HAD 10 NOTICES FILED ON TUESDAY SO WE GAINED 27 CONTRACTS OR AN ADDITIONAL 135,000 OZ WILL STAND AT THE COMEX FOR DELIVERY IN JULY,

AUGUST LOST 5 CONTRACTS TO STAND AT 826

SEPT HAS A LOSS OF 2396 CONTRACTS DOWN TO 120,106

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 26 for 130,000 oz

Comex volumes// est. volume today 50,175 fair /

Comex volume: confirmed yesterday: 54,656 fair

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 5095 x 5,000 oz = 25,475,000 oz

to which we add the difference between the open interest for the front month of JULY(52) and the number of notices served upon today 26 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2023 contract month: 5095 (notices served so far) x 5000 oz + OI for the front month of JULY (52) – number of notices served upon today (26 )x 500 oz of silver standing for the JULY contract month equates to 25.605 million oz + 0.0 MILLION OZ EXCHANGE FOR RISK TODAY//PRIOR EXCHANGE FOR RISK TOTALS 5.25 MILLION OZ /NEW TOTAL STANDING FOR DELIVERY: 30.855 MILLION OZ..WE HAVE 35 MILLION OZ OF REGISTERED SILVER AT THE COMEX//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

JULY 19/WITH GOLD UP $0.65 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 912.07 TONNES

JULY 18/WITH GOLD UP $23.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: .////INVENTORY RESTS AT 912.93 TONNES

JULY 17/WITH GOLD DOWN $6.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD.////INVENTORY RESTS AT 912.93 TONNES

JULY 14/WITH GOLD UP $0.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 914.66 TONNES

JULY 13/WITH GOLD UP $3.30 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.66 TONNES

JULY 12/WITH GOLD UP $24.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.95 TONNES

JULY 11/WITH GOLD UP $6.15 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.0 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 915.26 TONNES

JULY 10 WITH GOLD DOWN $1.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.60 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 916.26 TONNES.

JULY 7 WITH GOLD UP $16.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.86 TONNES.

JULY 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 917.86 TONNES

JULY 5/WITH GOLD DOWN $2.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 2.6 TONNES FROM THE GLD///INVENTORY RESTS AT 921.90 TONNES

JULY 3/WITH GOLD UP $1.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.50 TONNES//

JUNE 30/WITH GOLD UP $10.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 924.50 TONNES

JUNE 29/WITH GOLD DOWN $3.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.81 TONNES

JUNE 28/WITH GOLD DOWN $1.15 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 925.65 TONNES

JUNE 27/WITH GOLD DOWN $9.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD./INVENTORY RESTS AT 925.65 TONNES

JUNE 26/WITH GOLD UP $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD/////INVENTORY RESTS AT 927.10 TONNES

JUNE 23/WITH GOLD UP $5.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: WITHDRAWALS OF 4.33 TONNES OF GOLD OVER THE PAST TWO DAYS. /INVENTORY RESTS AT 929.70 TONNES

JUNE 21/WITH GOLD DOWN $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 934.03 TONNES

JUNE 20/WITH GOLD DOWN $22.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.03 TONNES

JUNE 16/WITH GOLD UP $0.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.03 TONNES

JUNE 15/WITH GOLD UP $2.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 929.70 TONNES

JUNE 14/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 931.44 TONNES

JUNE 13/WITH GOLD DOWN $10.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.01 TONNES FORM THE GLD///INVENTORY RESTS AT 931.44

GLD INVENTORY: 919.00 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

JULY 19/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 18/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 17/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 4.856 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 14/WITH SILVER UP 27 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.21 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 13/WITH SILVER UP 64 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 12/WITH SILVER UP $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.881 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 11/WITH SILVER DOWN 5 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .020 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 464.822 MILLION OZ/

JULY 10/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.672 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 464.802 MILLION OZ

JULY 7/WITH SILVER UP 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.474 MILLION OZ

JULY 6/WITH SILVER DOWN 50 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.667 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.474 MILLION OZ//

JULY5/WITH SILVER UP 30 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JULY 3/WITH SILVER UP 7 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JUNE 30/WITH SILVER UP 19 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.377 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT468.141 MILLION OZ//

JUNE 29/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.763 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.764 MILLION OZ//

JUNE 28/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.527 MILLION OZ//

JUNE 27/WILVER SILVER UP 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 734,000 OZ INTO THE SLV////INVENTORY RESTS AT 470.527 MILLION OZ

JUNE 26/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 469.793 MILLION OZ.

JUNE 23/WITH SILVER DOWN 9 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A NET DEPOSIT OF 6.61 MILLION OZ INTO THE SLV OVER THESE PAST TWO DAYS//INVENTORY RESTS AT 469.793 MILLION OZ//

JUNE 21/WITH SILVER DOWN $.40 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.784 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 20/WITH SILVER DOWN 89 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 16/WITH SILVER UP 23 CENTS TODAY :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 463.183 MILLION OZ

JUNE 15/WITH SILVER DOWN 17 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.377 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 463.642 MILLION OZ//

JUNE 14/WITH SILVER UP 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 735,000 OZ FROM THE SLV///INVENTORY RESTS AT 465.019 MILLION OZ//

JUNE 13/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 465.754 MILLION OZ//

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

CLOSING INVENTORY 452.480 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

END

3,Chris Powell of GATA provides to us very important physical commentaries

Pam and Russ Martens..

Pam and Russ Martens: Trillions in uninsured deposits are threat to Wall Street mega-banks

Submitted by admin on Tue, 2023-07-25 12:05Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Tuesday, July 25, 2023

In June, Reuters reported that JPMorgan Chase was expanding the reach of its commercial bank into two additional foreign countries — Israel and Singapore — bringing its foreign commercial bank presence to a total of 28 countries. Those plans could add billions of dollars more to its already problematic uninsured deposits.

Why federal regulators are allowing JPMorgan Chase to continue to expand, despite its admitting to five criminal felony counts since 2014 and currently facing three lawsuits in federal court for facilitating Jeffrey Epstein’s sex trafficking of underage girls, is drawing attention from watchdogs.

According to its regulatory filings, as of December 31, 2022, JPMorgan Chase Bank held $2.015 trillion in deposits in domestic offices, of which $1.058 trillion were uninsured. It also held another $418.9 billion in deposits in foreign offices, which were also not insured by the Federal Deposit Insurance Corp. (FDIC). That brought its uninsured deposits as of year-end to a total of $1.48 trillion or 60% of its total deposits.

Under federal statute, the deposits held by U.S. banks that are located on foreign soil are not insured by the FDIC. Depositors in the Cayman Islands branch of Silicon Valley Bank found that out the hard way when their deposits were seized by the FDIC after the bank failed in March.

Deposits in domestic bank offices in the U.S. that exceed $250,000 per depositor per bank are also not insured by the FDIC. …

… For the remainder of the commentary:

END

Chinese citizens are on a tear as they buy 555 tonnes of gold in the first half of this year

(zerohedge)

China’s gold consumption reaches 555 tons in first half of 2023, up 16.4%

Submitted by admin on Tue, 2023-07-25 21:12Section: Daily Dispatches

From Global Times, Beijing

Tuesday, July 25, 2023

China consumed 554.88 tons of gold in the first half of 2023, up 16.37% year-on-year, data from the China Gold Association showed today, as Chinese citizens’ income continues to rise steadily.

The “gold rush” is partly fueled by the investors’ growing risk aversion in buying equities and bonds, over concerns about volatile global financial environment, which is exacerbated by the U.S. bank financial crisis and the U.S. debt ceiling issue.

Among gold consumption, the purchase of gold bars jumped 30.12% year-on-year to 146 tons in the first six months, while that of gold jewelry reached 368 tons, up 14.82% from the same period last year. Gold used for industrial and other purposes declined 7.65% to 40 tons, the data showed.

“With the normalization and revival of the economy, China’s gold consumption shows an overall momentum of rapid recovery,” a statement on the website of the CGA said. Consumption of gold, silver, and jewelry led the gains of individual retail category in the first half this year, which continues to make contribution to fueling the economy, the statement noted. …

… For the remainder of the report:

https://www.globaltimes.cn/page/202307/1295007.shtml

END

China is now selling dollars to support the yuan value

(Reuters)

China state banks sell dollars to support yuan, sources tell Reuters

Submitted by admin on Tue, 2023-07-25 21:19Section: Daily Dispatches

From Reuters

Tuesday, July 25, 2023

China’s major state-owned banks were seen selling U.S. dollars to buy yuan in both onshore and offshore spot markets today in early Asian trade, three people with direct knowledge of the matter said, moves aimed at supporting the Chinese currency.

China’s state banks usually trade on behalf of the central bank in the country’s foreign exchange market, but they can also trade on their own behalf.

The dollar sales come after China’s top leaders pledged on Monday to step up policy support for the economy amid a tortuous post-COVID-19 recovery, focusing on boosting domestic demand and signalling more stimulus steps.

Policymakers also said China will keep the yuan exchange rate basically stable at reasonable and balanced levels, and vowed to invigorate the capital market and restore investor confidence.

“It is interesting that the Politburo mentioned FX stability in the statement, for the first time in recent years,” analysts at HSBC said in a note. …

… For the remainder of the report:

END

For your interest…

How right-wing news powers the ‘gold IRA’ industry

Submitted by admin on Tue, 2023-07-25 21:30Section: Daily Dispatches

Yes, the gold IRA business has some grifters, but not nearly as many as reside in central banking. The gold world awaits the Washington Post’s first critical question directed to a central banker. A few such questions might be suggested by the documents compiled and summarized here:

* * *

By Jeremy B. Merrill and Hanna Kozlowska

The Washington Post

Tuesday, July 26, 2023

Dedicated viewers of Fox News are likely familiar with Lear Capital, a Los Angeles company that sells gold and silver coins. In recent years the company’s ads have been a constant presence on Fox airwaves, warning viewers to protect their retirement savings from a looming “pension crisis” and “dollar collapse.”

One such ad caught the attention of Terry White, a disabled retiree from New York. In 2018 White invested $174,000 in the coins, according to a lawsuit by the New York attorney general — only to learn later that Lear charged a 33% commission.

Over several transactions, White, 70, lost nearly $80,000, putting an “enormous strain” on his finances, said his wife, Jeanne, who blames Fox for their predicament: “They’re negligent,” she said. A regretful White said he thought Fox “wouldn’t take a commercial like that unless it was legitimate.”

While the legitimacy of the gold retirement investment industry is the subject of numerous lawsuits — including allegations of fraud by federal and state regulators against Lear and other companies — its advertising has become a mainstay of right-wing media. …

… For the remainder of the report:

https://www.washingtonpost.com/business/2023/07/25/gold-ira-conservative-media/

END

In China’s bilateral trade, it exceeded trading in dollars for the first time ever

(Nikkei Asia/Toyko)

Yuan exceeds dollar in China’s bilateral trade for first time

Submitted by admin on Tue, 2023-07-25 22:23Section: Daily Dispatches

From Nikkei Asia, Tokyo

Tuesday, July 25, 2023

The yuan was used in 49% of China’s cross-border transactions last quarter, topping the dollar for the first time, a Nikkei analysis shows, mainly due to a more open capital market and more yuan-based trade with Russia.

Nikkei looked at international trade by companies, individuals, and investors based on currency, using statistical data from the State Administration of Foreign Exchange of China. Nikkei’s compilation does not include yuan-based settlements for trades and capital transactions that do not involve China as a counterparty.

The Society for Worldwide Interbank Financial Telecommunication, better known as SWIFT, reports that as of June the dollar’s share is the largest globally at 42.02%, including trades between countries other than China. The yuan represented 2.77% and ranked fifth overall after the euro, the U.K. pound, and the Japanese yen.

The yuan’s share of global payments remains small compared with the size of China’s economy, but is up from 1.81% about five years ago. Bilateral payments, backed by China’s economic influence, have gradually expanded its foothold. …

… For the remainder of the report:

END

Your most important read for the day. The bankers are massively short and to boot they cannot receive the much needed silver from Mexico as its largest mine is in a labour strike. That removes around 5 million oz per month from the equation

(Ted Butler//article in full)

Ted Butler: More on the silver Code Red

Submitted by admin on Tue, 2023-07-25 22:40Section: Daily Dispatches

By Ted Butler

Butler Research, Jupiter, Florida

via SilverSeek.com

Tuesday, July 25, 2023

Last week I made public an edited version of the more extensive weekly review sent to subscribers earlier. As previously stated, I believe there is an emergency in the Comex silver market based upon official data indicating a massive increase in futures positioning of more than 130 million ounces (26,000 contracts) as reported in the new commitment of traders report as of July 21.

While I tried my best to rely on the hard data and offer the most reasonable interpretation of that data, this is very complicated stuff, so it’s understandable that things may not seem as clear to others as they are to me

I’m sure many (if not most) are unclear on what I mean by a market emergency, the likes of which hasn’t existed in the Comex silver market since the Hunt Brothers emergency of 1980, 43 years ago.

So let me use instead a more recent market emergency — that of the London Metals Exchange nickel market of March 2022, as a contemporary example of what I’m talking about. …

… For the remainder of the analysis:

https://silverseek.com/article/more-silver-code-red

END

More on the Silver Code Red

July 25, 2023

Ted Butler

Butler Research

Last week, I made public an edited version of the more extensive weekly review sent to subscribers earlier. As previously stated, I believe there is a current market emergency in the COMEX silver market based upon official data indicating a massive increase in futures positioning of more than 130 million oz (26,000 contracts) as reported in the new COT report, as of July 21.

https://silverseek.com/article/code-red

While I tried my best to rely on the hard data and offer the most reasonable interpretation of that data, this is very complicated stuff, so it’s understandable that things may not seem as clear to others as they are to me. I’m sure many (if not most) are unclear on what I mean by a market emergency, the likes of which hasn’t existed in the COMEX silver market since the Hunt Bros emergency of 1980, 43 years ago. So, let me use instead a more recent market emergency – that of the LME nickel market of March 2022, as a contemporary example of what I’m talking about. Here’s a good run down of what transpired at the time.

https://www.ndtv.com/business/18-minutes-of-trading-chaos-which-broke-the-nickel-market-2824194

It is no exaggeration to claim that the LME nickel disaster is basically the same, in many respects, as to what I see ahead for the COMEX silver market. The nickel market was in a physical shortage condition at that time, same as the wholesale physical silver market is today. The long and short derivatives position in LME nickel grew to unreasonable levels, with a noted concentrated short position held by a large Chinese trader, identified as “Mr. Big Shot”. Just this past week, the COMEX silver futures market had a massive increase in total derivatives positions and the concentrated short position also grew massively as well.

In the end, the LME nickel shorts were no longer able to cap and contain prices and the price suddenly exploded – doubling and tripling in a matter of hours. This led to the LME busting trades, essentially, cancelling and reneging on contractual obligations, setting off an avalanche of lawsuits and instantly trashing the reputation of an exchange that existed for 150 years. Of course, I wrote about it at the time, making the clear analogy to what I saw coming in COMEX silver.

https://silverseek.com/article/real-lesson-lme-nickel

I know many think that I may be going overboard in describing what I see ahead for silver, but an objective review of what took place in LME nickel last year would seem to provide ample proof for what could happen in COMEX silver. While the basics in both markets seem identical – a physical shortage, coupled with a massive derivatives position (including extreme concentration on the short side) – there’s even more to be said about the coming COMEX silver emergency.

For one thing, I’m not aware of any prior warnings to the LME or the UK regulators about what turned out to be the nickel market emergency/debacle beforehand, whereas I know such warnings have been made in the coming COMEX silver market emergency (because I’ve made many such warnings). I send all my articles to all the commissioners at the CFTC, along with key officials at the Market Oversight and Enforcement Divisions, along with the CEO of the CME Group, Inc. (owner/operator of the COMEX). If the federal commodities regulator, as well as the designated industry self-regulator, are unconcerned about my warnings, it would appear reasonable that both should explain why or take immediate measures to try to head off the coming market emergency. The last thing I would want to do is cry “fire” in a crowded theater for no good reason.

Further, the LME nickel debacle affected very few market participants, whereas silver investors/participants everywhere, in the many millions worldwide, are affected by the ongoing COMEX silver manipulation and the market emergency I see dead ahead. This raises the stakes immeasurably for everyone, particularly the regulators.

Most concerning of all, in the LME nickel default and debacle, the principal player was the big Chinese speculative short seller, greatly assisted by the big banks, most notably, JPMorgan; whereas in the coming COMEX debacle, the banks appear to be directly positioned as the big silver short sellers. This has been the case for 40 years and despite billions of dollars of fines, settlements against too many banks to count and now jail time for bank employees – all for manipulating silver, gold and other precious metals prices on the COMEX and NYMEX – the banks still appear to be the big short sellers to this day.

As expected, the COT report for July 21 fully-confirmed extreme and even record commercial selling, particularly in terms of concentrated and collusive new shorting by the 4 and 8 largest COMEX commercial shorts. The 8 largest commercial shorts sold short more silver contracts, 12,100 (60 million oz), in one week than they had in years and maybe ever. I had made the case that the big commercials would not short big again (as a result of the big 4 not shorting on the $6 silver rally from March to May), but, clearly, those expectations were wrong.

Therefore, a reasonable observer would have to ask what was the motivation for the record one-week commercial selling. With silver so cheap in price in the face of a documented physical shortage and with strong technical buy signals (moving average penetrations) generated in the reporting week, the buyers, be they driven by supply/demand fundamentals or technical signals, need no explanation. It is the aggressive selling by the COMEX commercials (banks) that requires explanation and only one explanation is possible, namely, the commercials sold so aggressively to prevent an even larger run up in price that would have triggered massive new buying in silver away from the COMEX.

What I just described is nothing but in-your-face price manipulation – selling with the sole intent to prevent silver prices from increasing. There can be no other explanation. The fact that COMEX silver is supposed to be a regulated market, by not just the primary federal regulator, the CFTC, as well as the designated self-regulator, the CME Group, and both regulators sit by and do nothing but act as the three blind, deaf and dumb monkeys is nothing less than a national disgrace. The CFTC and CME Group can continue to disgrace themselves, but that’s their choice, as I do intend to press the issue to the best of my abilities.

Worst of all, the massive commercial selling this week is what creates the Code Red market emergency in COMEX silver, as there is no way that I can see that the massive positioning gets resolved without extreme price violence. The responsibility for the disorderly market conditions that I now see as being “baked” into COMEX silver as a result of the massive one-week surge in commercial selling, lies squarely on the CFTC and the CME Group.

I have been after both regulators for the better part of 40 years to address the ongoing COMEX silver manipulation and despite having to contend with their incompetence and malfeasance for all this time, I never thought both regulators would fail to act so irresponsibly as they are now. Neither would dare to openly debate the allegations of a market emergency, the avoidance of which couldn’t be of more significance to each.

What do I mean by a Code Red market emergency? A market condition that must resolve itself in disorderly prices. Those disorderly prices might include a blast to the downside, as the collusive commercials rig prices lower to induce the recent buyers to bail out, before the physical shortage conditions cause prices to soar. Or, the attempt to rig prices lower may fail and silver prices surge without a massive decline first.

In any event, the real blame for the disorderly prices ahead are the regulators, both the CFTC and the CME Group, which fail to address or even acknowledge the blatant manipulation in COMEX silver. I do intend to push both to do the right thing, but based upon their track records, they will be reluctant to address this serious issue. The one saving grace for higher silver prices is the physical shortage, which grows more pronounced daily. Surely, continued suppressed prices will not resolve the physical shortage, regardless of continued regulatory failure.

Ted Butler

July 24, 2023

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/SILVER

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//RICE

The rush is on to buy rise

(zerohedge)

“So It Begins”: US Supermarkets Hit With Buying Panic As India Bans Rice Exports

TUESDAY, JUL 25, 2023 – 07:45 PM

The decision by India to ban certain rice exports has sparked panic buying at supermarkets across the US. Videos circulating on social media show the staple food is flying off the shelves as high demand depletes supplies amid concerns of a global shortage. Some supermarkets have responded by implementing purchase limits, while others have hiked prices. The scenes below should remind readers of the panic buying days during Covid.

Indians being Indians, hoarding started. Big queue outside Patel Brothers, Dallas area after India banned exporting non Basmati rice… pic.twitter.com/8EgvwFWOKo— Aryabhata | ஆர்யபட்டா

(@Aryabhata99) July 21, 2023

Rice export stopped from India and massive panick hit the Indians in USA. Hoarding has started across the states. There has been multiple food shortages here, hoping rice shortage doesn’t get added to the list. pic.twitter.com/vdP6NBwrN6— The Thinking Hat

(@ThinkinHashtag) July 21, 2023

So it begins. India has banned some rice exports and now people are panic buying up rice. pic.twitter.com/ujpm66ER3n— Ian Miles Cheong (@stillgray) July 23, 2023

Apparently the ban is for non Basmati rice. So Tamil and Telugu community would be most impacted as they consume Sona Masoori rice. They started hoarding as if rice won’t be available anywhere else, ever. The fact is that Thai, Chinese, Japanese, Mexican and several immigrants in… pic.twitter.com/s8fRIeubMI— Mr B (@maddyb65) July 22, 2023

#MCTrends | The Indian government’s ban on the export of non-basmati rice has triggered panic buying in the US, with many departmental stores reporting empty shelves and putting limits on the number of rice bags customers can buy.@AnkitaSengupta_ reports

… pic.twitter.com/GgzonuW1tU— Moneycontrol (@moneycontrolcom) July 25, 2023

India’s export restriction applies to shipments of non-basmati white rice. The move is to contain food inflation by ensuring ample domestic supplies, as the El Niño weather pattern heavily impacts farm production. India is the largest exporter of rice.

We provided readers with enough understanding that rice, which is critical to the diets of billions of people worldwide, was headed for a shortage:

- Sept. 2022: The Stage Is Being Set For A Massive Global Rice Shortage

- May 2023: Global Rice Shortage Looms, Set To Be The Biggest In Decades

- May 2023: Thai Rice Crop In Crosshairs Of El Nino As Farmers Are Warned About Water Shortages

“India’s export ban needs to be seen in the light of this ominous setting,” Peter Timmer, Professor Emeritus at Harvard University, told Bloomberg. He has studied food security for decades and warned:

“There is considerably more reason for concern now that rice prices in Asia could spiral out of control pretty quickly.”

The president of the world’s largest rice shipper had this to say:

“In the short term, the price is definitely going up, it’s just a question of how high up it will go.

“And it will be a spike, it’s not going to be increasing incrementally,” said Chookiat Ophaswongse, honorary president of the Thai Rice Exporters Association.

Bloomberg data shows Thailand White Rice 5% is around $534 per ton, nearly a two-year high, and headed for a possible break above $579, which would mean prices would be back to 2012 highs.

India’s latest move has sparked panic buying of the grain.

end

ORANGE JUICE

Global shortage of orange juice. Florida supplies are low…

(zerohedge)

Orange Juice Squeezes To New Record High Amid Intensifying Fears Of Global Shortage

WEDNESDAY, JUL 26, 2023 – 06:55 AM

On Monday, orange juice futures rocketed to an all-time high due to global supply concerns among agricultural traders. The citrus greening disease continues to affect Florida and is spreading in Brazil — both regions are top producers, and a potential production loss from these areas could significantly tighten global supplies.

A new report from Bloomberg shows Brazil’s Citrosuco, one of the world’s top orange juice producers, has considered declaring a force majeure on supplies to clients after the crop disease and extensive rainfall damaged citrus groves.

In a July 17 letter sent to clients and seen by Bloomberg, the company said it was being “severely affected” by greening disease and rain that flooded farms. It added it won’t be able to ensure supplies at the volumes and prices previously agreed. Citrosuco confirmed the contents of the letter, which it said was sent as a warning to some clients who had contracts for delivery earlier this year. In a statement to Bloomberg on Monday, the company added the communication was part of specific commercial negotiations.

While the letter stated “supply performance is currently prevented by force majeure, until further notice,” the company said it had not taken the actual legal step associated with invoking force majeure, a clause companies usually enforce when an unforeseen event, such as a fire or natural disaster, prevents them from complying with a contract. –Bloomberg

Citrosuco’s warning was enough to send orange juice futures in New York above the $3 handle per pound, a new record high.

Data from the US Department of Agriculture and Citrosuco show Brazil exports 80% of its orange juice. Consumers who purchased OJ at US supermarkets have increasingly noticed labels on bottles that read: “Contains orange juice from US and Brazil.”

This is because Florida supplies are low and exports from Brazil have soared to new highs.

“The proliferation of disease continues to be great in Florida and the chance of a large comeback in production for the new season is limited,” Judy Ganes, president of J. Ganes Consulting, told Bloomberg.

Ganes said, “There are signs that disease is more prevalent in Brazil, too, which is also facing long-term problems with their crops.”

Even though egg prices have crashed, breakfast inflation remains elevated for yet another reason.

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

What an absolute mess! Bankman Fried is one strange dude

(zerohedge)

Bankman-Fried Agrees To Gag Order After “Star Witness” Ellison’s Diary Was Leaked To Press Last Week

TUESDAY, JUL 25, 2023 – 06:25 PM

It looks as though it may be time to re-up some of those Democratic donations for Sam Bankman-Fried, because there’s at least one judge out there that isn’t amused with his antics.

The former FTX founder has now agreed to a gag order that will “largely” prevent him from discussing his case publicly, Bloomberg wrote this week. Prosecutors in the case had accused Bankman-Fried of trying to discredit Caroline Ellison, who formerly lived with and worked with Bankman-Fried in the Bahamas.

US District Judge Lewis A. Kaplan said this week he was going to deal with the “adequacy and continuation” of SBF’s bail conditions. As Bloomberg wrote, this means SBF’s “current house arrest could be in jeopardy while he awaits trial on criminal fraud charges”.

Bankman-Fried will appear in court on Wednesday for a hearing.

Judge Kaplan has already concerned himself with Bankman-Fried’s bail restrictions, in the past warning that SBF needed to “rein in his use of encrypted messaging apps and VPN programs,” the report says.

The order was filed on Monday and and bans SBF and “other parties” from discussing anything with the press that “could interfere with a fair trial”. Specifically, Bloomberg writes that this could include “credibility of witnesses, information that isn’t admissible at trial and anything that could influence public opinion about the case”.

The “star witness” in the case has already pleaded guilty to fraud in a deal with prosecutors, the report says. Not only did she run Alameda Research, an offshoot of FTX, she also dated Bankman-Fried at one point.

The scrutiny this week came after a story broke last week in The New York Times about Ellison’s diary, detailing her “ambivalence” about her role at Alameda and her relationship with Bankman-Fried.

Prosecutors charged that SBF had leaked the material to “cast Ellison in a poor light, and advance his defense through the press.”

In a note filed Sunday, Bankman-Fried’s lawyers said that he had shared documents “in an effort to give his side of the story about topics that have already been reported in the media.” They argued that FTX’s new CEO “attacked” Bankman-Fried publicly while they “stood silent” and did nothing.

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1534

OFFSHORE YUAN: UP TO 7.1538

SHANGHAI CLOSED DOWN 8.49 PTS OR 0.26%

HANG SENG CLOSED DOWN 69.26 PTS OR 0.36%

2. Nikkei closed DOWN 14.17 PTS OR 0.04%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 100.87 EURO RISES TO 1.1073 UP 23 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.442 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 140.61/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ON SHORE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.4295***/Italian 10 Yr bond yield RISES to 4.081*** /SPAIN 10 YR BOND YIELD RISES TO 3.477…**

3i Greek 10 year bond yield FALLS TO 3.691

3j Gold at $1972.45 silver at: 24.74 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 11 /100 roubles/dollar; ROUBLE AT 90.02//

3m oil into the 78 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 141.48// 10 YEAR YIELD AFTER BREAKING .54%, RISES TO 0.466% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8619 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9547 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.890 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 3.947 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.864 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.95…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 1 BASIS PTS AT 4.3180

end

2.a Overnight: Newsquawk and Zero hedge:

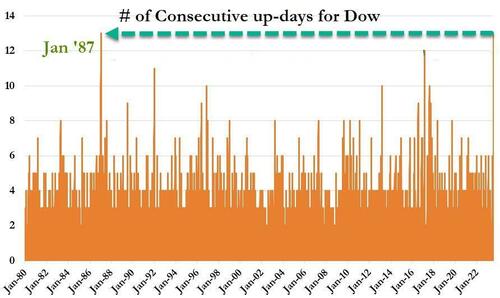

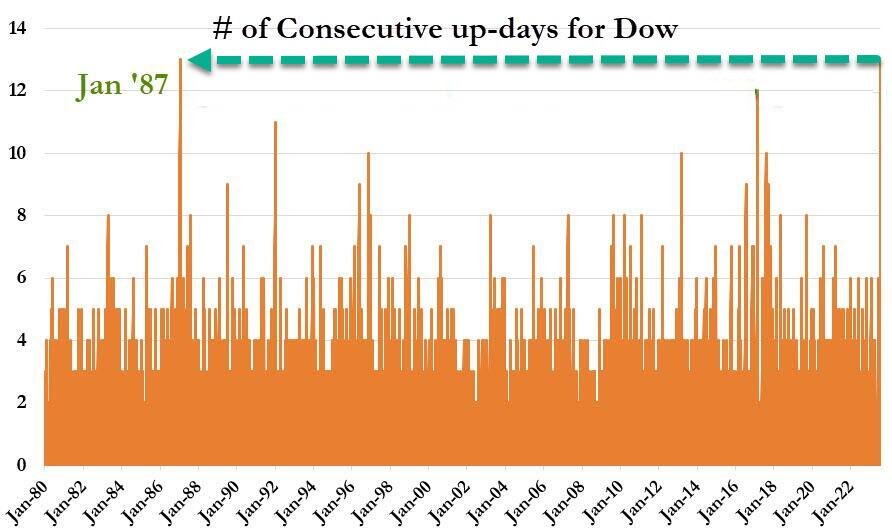

Futures Dip Ahead Of Fed’s “Last Rate Hike” As Dow Braces For 13 Straight Gains

WEDNESDAY, JUL 26, 2023 – 07:57 AM

US futures are lower as we enter the “last hike” day, with European stocks slumping after ugly results from LVMH (which tumbled 4.5%) and Asian markets also closing in the red as investors brace for more tightening from the Federal Reserve, even as results from some of the biggest European and American companies hinted at slowing economy and declining earnings. As of 7:30am ET, S&P eminis dropped 0.1% at 4,589 while Nasdaq futures were down 0.3%, pressured by disappointing results from some top constituents.

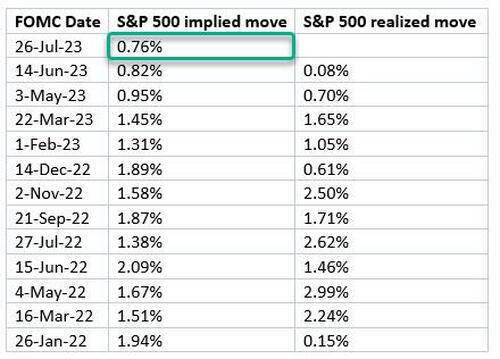

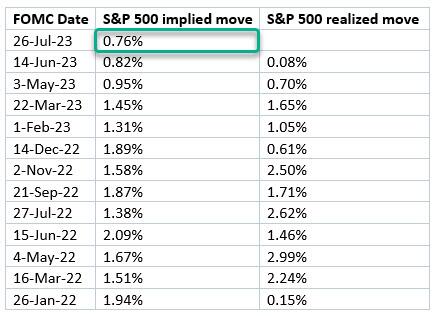

The market is pricing in just a 0.76% move after today’s FOMC, the lowest implied move on a Fed day since at least 2021.

Meanwhile, solid earnings from Boeing have propelled the Dow higher: the Dow Jones Industrial Average has risen 12 days straight — the longest winning run in over six years — and a 13th day of gains will extend the record to the longest since 1987.

Treasury yields were 1-2bps lower; the USD was weaker and commodities are mixed with base metals leading and Ags lagging. Today, focus will be Fed’s decision at 2pm ET and Powell’s Press Conference at 2.30pm ET. A 25bp hike is fully priced in, with consensus expecting (i) little meaningful changes to the post-meeting statement and (ii) Powell pointing to the June dots as the best guide as to the forward direction of policy (our full preview is here).

In premarket trading, Microsoft fell 4%, having posted tepid sales growth and amid missed Azure growth guidance while Snap sank 19%. Analysts, however, note that the unit’s deceleration is starting to moderate and they were positive about demand for the company’s new artificial intelligence-powered products and services. Chipmakers also mostly lost ground, after a subpar outlook from Texas Instruments, the biggest maker of analog semiconductors, indicated a demand slump for key types of electronics. On the other end, GOOGL jumped 7% after posting forecast-beating revenue. Meta rose ahead of its own report later Wednesday. Overall, tech earnings so far are still largely in line with expectation. Here are the most notable premarket movers:

- Boeing rose 3% after reporting $2.58 billion in free cash flow in the second quarter, surprising investors as a flurry of jet deliveries and customer deposits helped overcome the financial strain from supplier glitches.

- Dish Network jumps as much as 15% in premarket trading on Wednesday after Bloomberg News reported that the company said it will start selling its premium wireless service on Amazon.com later this week.

- PacWest jumped as much as 39% following news that it’s being bought by smaller rival Banc of California in a rescue deal aimed at boosting confidence in the lenders. Banc of California rose as much as 16%.

- Snap shares are sinking 19% after the social media company reported its second-quarter results and gave a revenue outlook that was weaker than expected. Analysts note that the company is still contending with weakness in its ads business as it looks to invest in new AI tools.

- Teladoc rises 6.1% after the virtual healthcare provider raised the bottom end of its revenue forecast range for the full year, with analysts saying that the firm’s control over costs is bearing fruit even as it faces a tough backdrop.

- Texas Instruments shares drop 3.5% after the chipmaker provided a forecast for the third quarter that left analysts disappointed, with some saying it overshadowed the second-quarter beat.

- Wells Fargo shares gain 2.6% in premarket trading after the lender announced plans to repurchase as much as $30 billion of its shares and boosted its dividend. Piper Sandler saw the authorization of the buyback as an “important show of strength” relating to the capital position of Wells Fargo, though Citi didn’t see any incremental information in the news.

Here is a summary of the most notable earnings reports:

- Alphabet Inc (GOOGL) Q2 2023 (USD): EPS 1.44 (exp. 1.34), Revenue 74.60bln (exp. 72.82bln). +6.9% in pre-market trade

- Microsoft Corp (MSFT) Q4 2023 (USD): EPS 2.69 (exp. 2.55), Revenue 56.2bln (exp. 55.47bln); soft Q1 guidance. -4.1% in pre-market trade

- Snap Inc (SNAP) Q2 2023 (USD): Adj. EPS -0.02 (exp. -0.04), Revenue 1.07bln (exp. 1.05bln) -18% in pre-market trade

- Texas Instruments Inc (TXN) Q2 2023 (USD): EPS 1.87 (exp. 1.76), Revenue 4.53bln (exp. 4.36bln) -3.8% in pre-market trade

- Visa Inc (V) Q3 2023 (USD): EPS 2.16 (exp. 2.12), Revenue 8.1bln (exp. 8.06bln) -0.3% in pre-market trade

- X Corp (formerly Twitter) is offering incentives on certain ad formats within the US and UK, via WSJ citing emails; additionally, has warned brands that verified status could be lost if certain spending thresholds are not met.

Fahad Kamal, chief investment officer at SG Kleinwort Hambros Bank, noted that Wednesday’s market pullback comes after a broad stretch of gains, with the S&P 500 less than 5% off record highs. “The bigger picture is that this quarter is probably the low point for earnings, this year will end up positive both in Europe and US,” he said, while cautioning of risks from “the effect of central bank policy tightening.”

“We are going to see some deceleration in corporate earnings, deceleration in economic growth, softening of demand, all of this will have a higher impact on equities,” Aarthi Chandrasekaran, director of investments at Shuaa Asset Management said on Bloomberg TV. Still, “the US economy is weakening but it’s not weakening enough to price in a full rate cut next year,” she said. Still, despite some disappointments, roughly 80% of US companies have thus far beaten profit estimates, as have half of European names. This is largely due to a steady trimming of expectations before the season kicked off.

Later on Wednesday, the Fed is expected to raise rates by 25 basis points, and swap contracts are factoring some additional rate increases by year-end as well. The expected Fed rate increase would be 11th since March 2022, cycle in which rates were raised at each scheduled meeting until last month’s, when policy makers said a pause was warranted to assess the impact of their cumulative actions on the economy and banking system. The European Central Bank should also deliver a quarter-point increase on Thursday. With those hikes baked in, investors will focus on signals on how much more policy tightening might be warranted (full preview here).

European stocks are lower and set to snap a six-session win streak after a flurry of corporate earnings dented investor sentiment. The Stoxx 600 is down 0.5%, led lower by the luxury-goods sector as LVMH tumbled as much as 4.5% after Europe’s biggest company provided further evidence of a slowdown in spending by US wealthy consumers. Miners are also under pressure after Rio Tinto cut its dividend following a fall in first-half profit. Here are the most notable European movers:

- Rolls-Royce shares rose as much as 25% to their highest level since March 2020 after the engine maker boosted its adjusted operating profit guidance for the year as its turnaround begins to bear fruit

- BAT shares gained as much as 3.4% after the tobacco company reaffirmed its forecast for the year, which was in line with last month’s update and reassured investors given the tough backdrop

- Stellantis shares rise as much as 2.9% after the carmaker reported first-half results that analysts say were strong and above consensus across the board

- RWE shares climbed as much as 3%, the most since April, after it boosted its adjusted Ebitda guidance for the full year. Morgan Stanley says the increase will likely trigger significant EPS upgrades

- Just EatTakeaway shares rally as much as 10% after the online food delivery company’s adjusted Ebitda for the first half beat estimates. Analysts praised the strong performance in its European markets

- Verallia gains as much as 11%, most in more than a year, after the French maker of glass bottles raised its earnings guidance. Citi says consensus earnings estimates should increase by double-digits

- Worldline shares rise as much as 6% after the payments company reported a second-quarter revenue and margins beat, with analysts noting the strength in the key Merchant Services business

- LVMH shares fell over 4.5% at the start of trading in Paris after the French luxury behemoth reported second-quarter revenue that provided further evidence of a slowdown in spending by wealthy US consumers

- Hexagon shares fall as much as 8.4% after the Swedish industrial software group’s free cash flow and Ebit came in below analyst expectations

- Lloyds falls as much as 5.2% after the UK lender booked additional loan-loss impairments. The bank’s upgraded loan margins were likely already in consensus estimates, analysts say

- Danone falls as much as 3.4%, most since May 9, after reporting like-for-like sales for the second quarter that beat the average estimate, with analysts saying more progress may be needed in 2H

- Porsche shares fell as much as 2.5% after the German luxury sports-car maker reported first-half sales that missed estimates. The results raise concerns about automotive pricing, according to Morgan Stanley

Earlier in the session, Asia’s key stock gauge snapped a two-day wining run as investors trimmed their positions ahead of the Federal Reserve’s monetary policy outcome, while Chinese stocks declined after Tuesday’s rally. The MSCI Asia Pacific Index declined as much as 0.3% with markets in Japan, South Korea and Hong Kong leading the losses. Stocks in Australia extended gains after consumer prices rose at a slower than expected pace for the three months ended June, fueling bets for a continued pause by the Reserve Bank next week.

The Fed is poised to hike interest rates by another 25 basis points, with investors keeping an eye on commentary by Chairman Jerome Powell. Asian stocks have, on average, reacted positively after a rate hike in 10 of the previous instances, data compiled by Bloomberg showed. Stocks in Asia have generally held their gains this month, buoyed by the receding odds of a recession in the US as well as China’s pivot toward a more friendly approach to the private sector and pledge of support for the economy.

Chinese stocks in Hong Kong fell after Tuesday’s surge as investors await more concrete policy decisions by Beijing following the politburo meeting. Policymakers have signaled that they intend to ease monetary policies and boost property markets. “It is really important that in the coming days and weeks, we see continued strong messages coming from different parts of the government,” Winnie Wu, China equity strategist at BofA Securities told Bloomberg Television in an interview.