GOLD PRICE CLOSED: DOWN $5.20 TO $1939.70

SILVER PRICE CLOSED: DOWN $0.26 AT $24.43

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1940.00

Silver ACCESS CLOSE: 24.43

Shanghai Gold Benchmark Price

USD oz  AM1971.34

AM1971.34

PM1969.78

Historical SGE Fix

New York price at the time: $1944.00

premium $27.00

xxxxxxxxxxxxxxxxxx

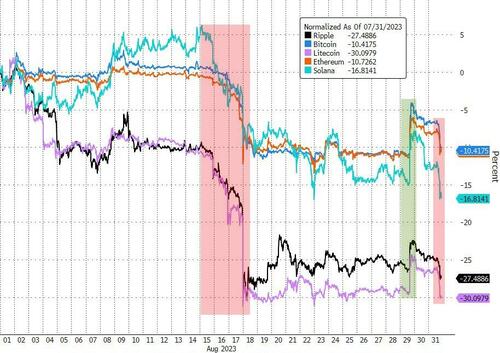

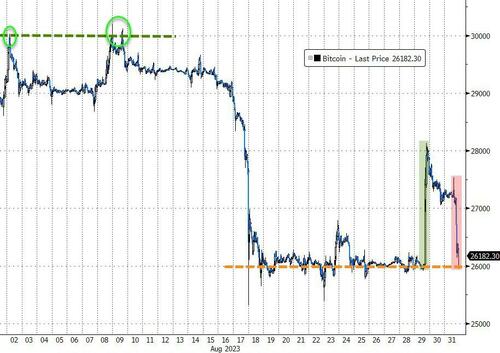

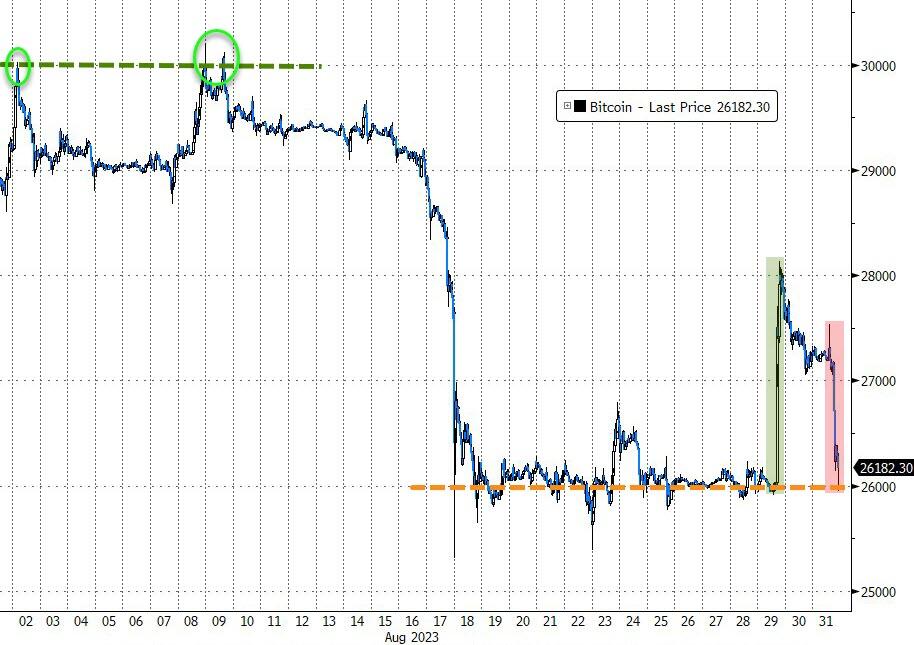

Bitcoin morning price:, $27,244 DOWN 6 Dollars

Bitcoin: afternoon price: $27,250 DOWN 702 dollars

Platinum price closing $980,45 DOWN $2.95

Palladium price; $1227.60 DOWN $30.19

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,622.56 DOWN 7.25 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1531.75 UP 4.35 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1789.14 UP 10.32 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,944.300000000 USD

INTENT DATE: 08/30/2023 DELIVERY DATE: 09/01/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 820

132 C SG AMERICAS 197

323 H HSBC 822

363 H WELLS FARGO SEC 545

365 H MAREX CAPITAL M 2

435 H SCOTIA CAPITAL 252

624 H BOFA SECURITIES 931

657 C MORGAN STANLEY 41

661 C JP MORGAN 1037 52

686 C STONEX FINANCIA 36

690 C ABN AMRO 25 44

709 C BARCLAYS 500

726 C CUNNINGHAM COM 5

732 C RBC CAP MARKETS 85 7

737 C ADVANTAGE 38

905 C ADM 29

TOTAL: 2,734 2,734

MONTH TO DATE: 2,734

JPMorgan stopped 52 /2754 contracts.

FOR SEPT.:

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2023. CONTRACT: 2754 NOTICES FOR 275,400 OZ or 8.503 TONNES

total notices so far: 2754 contracts for 275,400 oz (8.503 tonnes)

FOR SEPT:

SILVER NOTICES: 1863 NOTICE(S) FILED FOR 9,315,000 OZ/

total number of notices filed so far this month : 1863 for 9,315,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN 5.20

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/HUGE CHANGES IN GOLD INVENTORY AT THE GLD: /A DEPOSIT OF 87 TONNES OF GOLD INTO THE GLD.

INVENTORY RESTS AT 890.10 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 2 CENTS AT THE SLV// SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.21 MILLION OZ OZ SILVER OUT OF THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 440.000 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 3180 CONTRACTS TO 131,813 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY $0.02 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. TAS ISSUANCE WAS A STRONG SIZED 751 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 751 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.02). BUT WERE SUCCESSFUL IN KNOCKING SOME SILVER CONTRACTS AS WE HAD A STRONG SIZED LOSS OF 700 CONTRACTS ON BOTH EXCHANGES ALONG WITH HUGE T.A.S.LIQUIDATION THROUGHOUT THE COMEX SESSION.

WE MUST HAVE HAD:

A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS( 2145 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 14.875 MILLION OZ (FIRST DAY NOTICE) / // HUGE SIZED COMEX OI LOSS/ GIGANTIC SIZED EFP ISSUANCE/VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE (751 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL 335 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTRACTS for 23 days, total 34,286 contracts: OR 171.430 MILLION OZ (1490 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 171.43 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3180 CONTRACTS WITH OUR LOSS IN PRICE OF $0.02 IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC EFP ISSUANCE CONTRACTS: 2145 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR SEPT OF 14.875 MILLION OZ /// WE HAVE A STRONG LOSS OF 700 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG 751 CONTRACTS//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED//ALONG WITH COMEX SPREADER LIQUIDATION, DURING THE WEDNESDAY COMEX SESSION . THE NEW TAS ISSUANCE WEDNESDAY NIGHT (751) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 1863 NOTICE(S) FILED TODAY FOR 9,315,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 5100 CONTRACTS TO 447,906 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: 349 CONTRACTS

WE HAD A STRONG SIZED INCREASE IN COMEX OI ( 5449 CONTRACTS) WITH OUR $8.15 GAIN IN PRICE//WEDNESDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 12.656 TONNES ON FIRST DAY NOTICE + /A FAIR (AND CRIMINAL) ISSUANCE OF 1239 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR $8.15 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A VERY STRONG SIZED GAIN OF 7195 OI CONTRACTS (23.46 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2095 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 447,906

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7195 CONTRACTS WITH 5100 CONTRACTS INCREASED AT THE COMEX// AND A FAIR 2095 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 7195 CONTRACTS OR 22.38 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1239 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2095 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (5100) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 7195 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 12.656 TONNES F/// 3) ZERO LONG LIQUIDATION WITH CONSIDERABLE TAS LIQUIDATION DURING THE COMEX SESSION //4) STRONG SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1239 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUG :

TOTAL EFP CONTRACTS ISSUED: 62,783 CONTRACTS OR 6,278,300 OZ OR 195.28 TONNES IN 23 TRADING DAY(S) AND THUS AVERAGING: 2727 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 23 TRADING DAY(S) IN TONNES 195.28 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 195.28/3550 x 100% TONNES 5.44% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT:

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 3180 CONTRACTS OI TO 131,813 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A GIGANTIC 2145 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 2145 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2145 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2845 CONTRACTS AND ADD TO THE 2145 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1035 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 5.175 MILLION OZ

OCCURRED DESPITE OUR $0.02 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

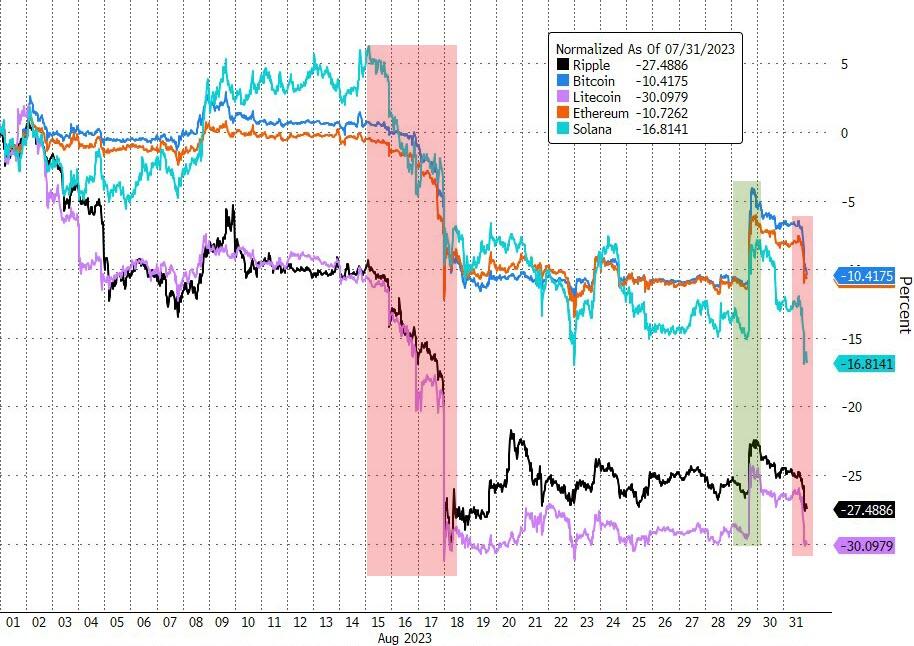

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 17.91 PTS OR 0.54% //Hang Seng CLOSED DOWN 100.80 PTS OR 0.55% /The Nikkei CLOSED UP 285.80 PTS OR 0.88% //Australia’s all ordinaries CLOSED UP 0.15 % /Chinese yuan (ONSHORE) closed UP 7.2870 /OFFSHORE CHINESE YUAN UP TO 7.2952 /Oil UP TO 82.34 dollars per barrel for WTI and BRENT UP AT 85.81 / Stocks in Europe OPENED ALL MOSTLY GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

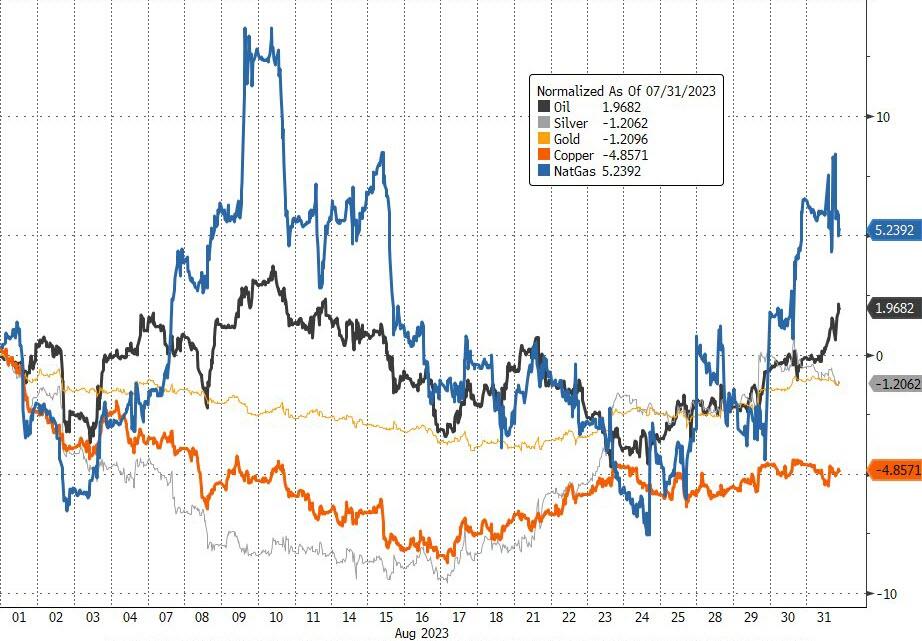

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 5100 CONTRACTS TO 447,906 WITH OUR GAIN IN PRICE OF $8.15 ON WEDNESDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF AUGUST… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2095 EFP CONTRACTS WERE ISSUED: : DEC 2095 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2095 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG TOTAL OF 7195 CONTRACTS IN THAT 2095 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 5100 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR ADVANCE IN PRICE OF $8.15//WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A FAIR 1239 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (12.656) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 12.656 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $8.15) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG GAIN OF 7195 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD LITTLE T.A.S. LIQUIDATION ON THE FRONT END OF WEDNESDAY’S TRADING. THE T.A.S. ISSUED ON WEDNESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 22.38 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST. (12.656 TONNES) ON FIRST DAY NOTICE // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $8.15.

WE HAD – REMOVED 349 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 7195 CONTRACTS OR 719,500 OZ OR 22.38 TONNES.

Estimated gold volume today:// 140,596 really awful

final gold volumes/yesterday 186,088 awful//speculators have left the gold arena

//AUGUST 31/ FOR THE SEPT. 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 32.151 OZ BRINKS 1 KILOBARS . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 2734 notice(s) 273,400 OZ 8.503 TONNES |

| No of oz to be served (notices) | 1325 contracts 132,500 oz 4.1213 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2734 notices 273400 OZ 8.503 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: nil oz

we had 1 customer withdrawals

i) Out of bRINKS: 32.151 ONE KILOBAR

total withdrawals 32.151 oz

Adjustments; 1 dealer TO CUSTOMER

1)outof JPMorgan 13,503.402 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER.

For the front month of SEPTEMBER we have an oi of 4069 contracts having GAINED 120 contracts.

So my definition, the initial amount of gold standing for Sept is as follows:

4069 contracts x 100 oz per contract = 406900 oz or 12.656 tonnes

This is huge for a non active delivery month.

Oct GAINED 611 contracts to 29,402 contracts.

We had 2734 contracts filed for today representing 273,400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 1037 notices were issued from their client or customer account. The total of all issuance by all participants equate to 2754 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 52 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2023. contract month,

we take the total number of notices filed so far for the month (2,734 x 100 oz ), to which we add the difference between the open interest for the front month of SEPT (4069 CONTRACT) minus the number of notices served upon today 2734 x 100 oz per contract equals 406.900 OZ OR 12.656 TONNES the number of TONNES standing in this non active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month: No of notices filed so far (2734) x 100 oz + (4069) {OI for the front month} minus the number of notices served upon today (2734) x 100 oz) which equals 406,900 oz standing OR 12.656 TONNES

TOTAL COMEX GOLD STANDING: 12.656 TONNES WHICH IS SMALL FOR AN INACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,011,076.496 OZ 62.55 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,389,738,459 OZ

TOTAL REGISTERED GOLD 10 ,854.431 (337.61 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,535,307.318 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,843355 OZ (REG GOLD- PLEDGED GOLD) 275.06 tonnes//dropping like a stone

END

SILVER/COMEX

AUGUST 31

//2023// THE SEPT 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,064,524,00 oz Brinks JPMorgan . |

| Deposits to the Dealer Inventory | 586,113.500 oz ASAHI |

| Deposits to the Customer Inventory | 607,700.840oz CNT |

| No of oz served today (contracts) | 1863 CONTRACT(S) (9,315,000 OZ) |

| No of oz to be served (notices) | 1051 contracts (5,255,000 oz) |

| Total monthly oz silver served (contracts) | 1863 Contracts (9,315,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 1

i)Into ASAHI 586,113.500 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposit customer account:

i) Into CNT 607,706.840 oz

total customer deposits: 607,706.840 oz

JPMorgan has a total silver weight: 138,660 million oz/277.734 million = 49,96% of comex .//

Comex withdrawals 2

i) Out of Brinks 455,110.410 oz

ii) Out of JPMorgan: 609,413.966 oz

total 1,064,524.00

adjustments: 2 : customer to dealer

i) CNT 488,260.300 oz

ii) Manfra: 581,263.743

TOTAL REGISTERED SILVER: 44.350 MILLION OZ//.TOTAL REG + ELIGIBLE. 277,734 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF SEPT /2023 OI: 2914 CONTRACTS HAVING LOST 3233 CONTRACT(S).

THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER STANDING IN THIS ACTIVE DELIVERY MONTH IS AS FOLLOWS:

2914 CONTRACTS X 5000 OZ PER CONTRACT = 14,570,000 OZ WHICH IS QUITE LOW FOR SEPT.

OCT GAINED 144 CONTRACT TO STAND AT 1147.

DEC. LOST 319 CONTRACTS TO STAND AT 117,421 .

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1863 for 9,315,000 oz

Comex volumes// est. volume today 71,696 strong

Comex volume: confirmed yesterday 106,407 huge

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 1862 x 5,000 oz = 9,315,000 oz

to which we add the difference between the open interest for the front month of SEPT (2914) and the number of notices served upon today 1863x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2023 contract month: 1863 (notices served so far) x 5000 oz + OI for the front month of SEPT (2914) – number of notices served upon today (1863 )x 500 oz of silver standing for the SEPT contract month equates to 14.570 million oz.

There are 44.350 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 31/WITH GOLD DOWN $5.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 30/WITH GOLD UP $8.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.59 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.23 TONNES

AUGUST 29/WITH GOLD UP 17.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.6 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.64 TONNES

AUGUST 28/WITH GOLD UP $6.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / //INVENTORY RESTS AT 884.04 TONNES

AUGUST 25/WITH GOLD DOWN $6.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 884.04 TONNES

AUGUST 24/WITH GOLD UP $0.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //INVENTORY RESTS AT 884.91 TONNES

AUGUST 23/WITH GOLD UP $21.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 4.32 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 884.91 TONNES

AUGUST 22/WITH GOLD UP $2.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.87 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 889.23 TONNES

AUGUST 21/WITH GOLD UP $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.60 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 890.10 TONNES

AUGUST 18/WITH GOLD UP $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 887.50 TONNES

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 16/WITH GOLD DOWN $7.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 15/WITH GOLD DOWN $7,45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 895.87 TONNES

AUGUST 14/WITH GOLD DOWN $2.10 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.75 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 899.63 TONNES

AUGUST 11/WITH GOLD DOWN $2.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 903.31 TONNES

AUGUST 10/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 9/WITH GOLD DOWN $8.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 8/WITH GOLD DOWN $9.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES FORM THE GLD /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 7/WITH GOLD DOWN $5.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///INVENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 31/WITH GOLD UP $9.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 28/WITH GOLD UP $14.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 915,82 TONNES

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

GLD INVENTORY: 890.10 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 31/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.834 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 443.210 MILLION OZ

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.834 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 443.210 MILLION OZ

AUGUST 29/WITH SILVER UP 49 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 183,000 OF SILVER INTO THE THE SLV// /.////INVENTORY RESTS AT 445.044 MILLION OZ

AUGUST 28/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.281 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 444.861 MILLION OZ

AUGUST 25/WITH SILVER UP ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 446.145 MILLION OZ

AUGUST 24/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.651 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 448.896 MILLION OZ

AUGUST 23/WITH SILVER UP 94 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FROM THE SLV// /.////INVENTORY RESTS AT 450.547 MILLION OZ

AUGUST 22/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: /.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 21/WITH SILVER UP 59 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 917,0000 OZ FROM THE SLV//.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 18/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 16/WITH SILVER DOWN 13 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 15/WITH SILVER DOWN 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 14/WITH SILVER DOWN 3 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.459 MILLION OZ INTOTHE SLV/: //////INVENTORY RESTS AT 452.565 MILLION OZ

AUGUST 11/WITH SILVER DOWN 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.926 MILLION OZ INTOTHE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 452.106 MILLION OZ

AUGUST 10/WITH SILVER UP 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 9/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 8/WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 7/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 31/WITH SILVER UP 45 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 28/WITH SILVER UP 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.930 MILLION OZ

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

CLOSING INVENTORY 440.000 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

END

3,Chris Powell of GATA provides to us very important physical commentaries

My goodness, these guys are good! They are already at 2.4 miles deep (12,672 feet) and they are going deeper?

It must be soooo hot at that level

(Reuters)

South Africa’s Harmony plans to take world’s deepest gold mine deeper

Submitted by admin on Wed, 2023-08-30 18:14Section: Daily Dispatches

By Felix Njini

Reuters

Wednesday, August 30, 2023

NAIROBI, Kenya — Harmony Gold Mining, South Africa’s biggest gold producer by volume, said it will seek board approvals on deepening its flagship Mponeng mine, which buoyed a rebound to profit in the year through June.

The Johannesburg-based firm aims to extend the life of the world’s deepest gold mine and will seek board approvals when studies are completed this year, CEO Peter Steenkamp said.

Harmony said Mponeng delivered a “stellar” performance with output up 22% as the miner rebounded to an annual profit of $275 million from a net loss of $48 million a year earlier. …

… For the remainder of the report:

END

END

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES

ALERT! US Mint Panics Making 3M Silver Eagles in AUGUST! Too Late…Us Mint Trust is GONE!(Bix Weir)

Inbox

Search for all messages with label Inbox

Remove label Inbox from this conversation

| Bix Weir via aweber.com | 12:56 PM (2 minutes ago) | ||

| to me | |||

| Wow! US Mint Director, Ventris Gibson, must have gotten the message that “We the People” are NOT HAPPY with the performance of the US Mint. After years of NOT making Silver Eagles to meet demand there has been an explosion in SAE production at the MINT! 3M ounces in August alone and now premiums are coming back from their trip to the moon. Knowing that the Mint was making 4-5M per month under the previous Mint Director, David Ryder, I expect that will be the target for Ventris going forward. Now let’s stop the US Mint from using their silver derivative hedge book from assisting the COMEX Silver Price Riggers! ALERT! US Mint Panics Making 3M Silver Eagles in AUGUST! Too Late…Us Mint Trust is GONE!(Bix Weir)https://youtu.be/DAD0rgPhsSA |

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2870

OFFSHORE YUAN: UP TO 7.2952

SHANGHAI CLOSED DOWN 17.91 PTS OR 0.54%

HANG SENG CLOSED DOWN 100.80 PTS OR 0.55%

2. Nikkei closed UP 285.80 OR 0.88%

3. Europe stocks SO FAR: ALL MOSTLY GREEN

USA dollar INDEX UP TO 103.55 EURO FALLS TO 1.0858 DOWN 71 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.638 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 145.90/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ON SHORE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.4915***/Italian 10 Yr bond yield DOWN to 4.129*** /SPAIN 10 YR BOND YIELD FALLS TO 3.503…**

3i Greek 10 year bond yield FALLS TO 3.735

3j Gold at $1945.65 silver at: 24.56 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 13 /100 roubles/dollar; ROUBLE AT 96.35//

3m oil into the 82 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 146.35// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.638% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8822 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9579well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

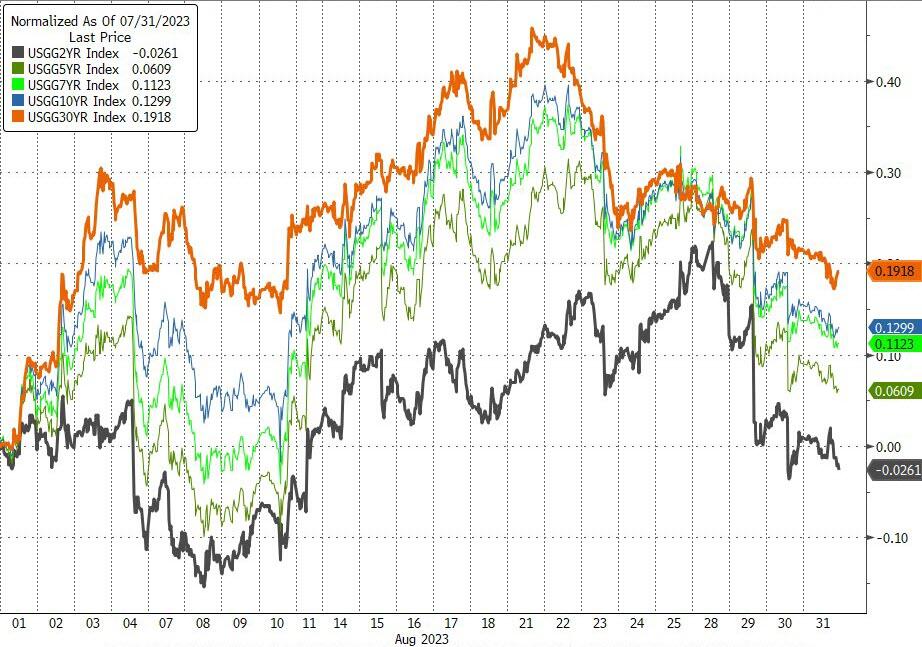

USA 10 YR BOND YIELD: 4.095 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.213 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.863 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.68…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 8 BASIS PTS AT 4.4015

end

2.a Overnight: Newsquawk and Zero hedge:

USA EARLY MORNING REPORT

Futures, Global Markets Rise As Yields Drops Ahead Of PCE Data

THURSDAY, AUG 31, 2023 – 08:14 AM

US stock futures, European bourses and Asian markets all rose, while the 10-year Treasury yield traded near a three-week low and the USD eeked out its first gain of the week as traders reacted to a modest improvement in China’s mfg PMI and looked ahead to Thursday’s PCE data and Friday’s jobs report. At 7:45am ET, S&P futures rose 0.25% to 4,535 while Nasdaq 100 futures reversed earlier losses. Europe’s Stoxx 600 benchmark stayed in the green, buoyed by record profits at UBS as a result of its emergency takeover of Credit Suisse. Commodities are stronger led by oil and metals with natgas and wheat the biggest laggards. Today’s macro data focus includes jobless claims, income/spending and the PCE Deflator. Chicago PMI, expected to rise to 44.2, may point to a stabilization in mfg. Tomorrow we cap off the week with NFP.

In premarket trading, the retail rout continued with Dollar General plunging more than 13% after the company cut its 2024 net sales and profit forecast; Chewy also fell 5.3% as analysts say the pet products company’s customer growth disappointed in the second quarter amid macro uncertainties. Evercore ISI downgraded its rating. Okta jumped 11% after it reported second-quarter results that beat expectations and raised full-year forecast. Analysts highlight improvement in margins and the company’s sales strategy. Here are some other notable premarket movers:

- Arista Networks gains 2.3% after Citi upgraded the communications-equipment company to buy from neutral, citing an expected 400G cloud spend recovery into next year.

- CrowdStrike climbed 1.4% as it again delivered strong results with consistent execution and outperformance across metrics, analyst Matthew Hedberg says he likes the continued momentum and the opportunity to consolidate security spend, seeing this as a building tailwind.

- Palantir declines 4% after Morgan Stanley cut its rating, saying that near-term optimism about the AI product cycle and valuation premium make for an “unfavorable risk-reward.”

- Salesforce rises 5.6% after the software firm reported second-quarter results that beat expectations and gave an outlook that is seen as strong.

- Shopify’s US shares rise 5.6% after Amazon announced an app integration to allow merchants to offer Buy with Prime on Shopify stores.

- UGI jumps 7.3% after the natural gas and electric power distribution company said its board is reviewing strategic alternatives to unlock shareholder value.

- Victoria’s Secret falls 5.3% after the lingerie retailer’s second-quarter results fell shy of estimates and it forecast a sales decline ahead.

Sentiment was modestly boosted after China’s NBS PMIs showed that Manufacturing came in at 49.7 (up from 49.3 in Jul and ahead of the Street’s 49.2 forecast) and Manufacturing new orders back in expansion mode for the first time in 5 months; on the other hand, Non-Manufacturing ticked down to 51 (down from 51.5 in Jul and below the Street’s 51.2 forecast).

The S&P 500 was headed for the worst month since February, while the Nasdaq 100 is set for the largest decline this year. Asian and global stocks are also on pace for the biggest monthly losses since February.

Traders are closing out the month with economic data and China’s bruised markets center stage. Thursday’s mixed moves come after stocks and bonds pared their August losses in the past week. US jobless numbers picked up slightly to 235,000 according to economists polled by Bloomberg ahead of initial claims data due Thursday. Friday’s non-farm payrolls are seen at 170,000 in August versus 187,000 in July, while hourly wage growth is predicted to slow slightly. Weaker-than-expected economic numbers supported predictions for the Fed to ease back on interest-rate hikes on Wednesday.

“The big market catalyst we’re looking for in September is the Fed meeting,” Hugh Gimber, global market strategist at JPMorgan Asset Management, said by phone. “Tomorrow’s payrolls data will be hugely relevant for that meeting. Without a slowdown in wages, a soft landing is impossible.”

European stocks were higher with the Stoxx 600 rising 0.4%. The financial services, retail and real estate sectors are leading gains. The euro dropped 0.5% versus the dollar as euro-zone inflation stopped slowing in August, according to data on Thursday. That presents European Central Bank officials with a quandary as they weigh the possibility of tighter policy against signs of flagging growth. Here are the biggest European movers:

- UBS shares climb as much as 7.2% to their highest level since October 2008 after the bank posts 2Q net income of $29 billion, bolstered by negative goodwill from Credit Suisse acquisition

- Rockwool rises as much as 6.5%, making it the biggest gainer on Europe’s Stoxx 600 index, after the Danish insulation firm increased its guidance for the second time in two months

- Dormakaba shares soar as much as 13%, most since April 2015, after the Swiss access and security company reported Ebitda for the full year that beat average estimates

- Grafton shares rise as much as 3.5% as analysts highlight optionality from the UK construction and materials company’s strong balance sheet, as evidenced by a new share buyback

- Pernod Ricard falls as much as 5.3%, the most in more than a year, after the maker of Absolut Vodka reported results that were hit by negative FX effects and said it expected a “soft” quarter ahead

- Eiffage drops as much as 2.6% after the construction and concessions company delivered 1H results which Jefferies describes as “soft,” highlighting an increase in net debt and a miss on profit

- Adevinta shares fall as much as 2.7%. The Norwegian classifieds company said on an earnings call its German vehicle marketplace may merely see “more normal” growth rates going forward

- Recticel shares slumped as much as 15% after the Belgian company’s first-half earnings missed estimates due to challenging conditions in the European construction markets

- Ion Beam Applications plunged 15%, the most since March 2020, after the Belgian medical technology company reported first-half earnings that analysts say were below expectations

Earlier in the session, Asian stocks were mixed, heading for their worst monthly drop since February, as the rally in Chinese equities faltered amid worries about growth and the property crisis in Asia’s largest economy.

The MSCI Asia Pacific Index erased earlier gains of as much as 0.4% to trade little changed. Benchmarks in Japan and Singapore rose, while those in South Korea, Taiwan and Australia were lower. Equities in mainland China were set to extended their losses for another session after factory output contracted again, with the onshore stock benchmark poised for its biggest monthly decline since October. Gauges in Hong Kong fluctuated.

After suffering most of August on China’s growth concerns, the main Asian stock benchmark was on course for about a 5% drop this month, even after the recent recovery in Chinese stock markets helped narrow the loss. Equities rebounded earlier this week on the mainland following Beijing’s latest steps to shore up investor confidence in capital markets on Sunday but the rally lost steam after mid-week.

- Japan’s Nikkei 225 saw mild gains although the machinery sectors were in the red following the dire Japanese industrial output data, with a Japanese government official highlighting a decline in demand both domestically and abroad, with output falling in several areas including production machinery.

- Australia’s ASX 200 was flat on either side of 7,300 as the gains in the Telecoms and Financial sectors were offset by losses in Energy and Consumer Staples.

- Stocks in India posted their biggest decline this week, weighed by a regional selloff. Investors will look forward to release of quarterly GDP data due after close of markets. The S&P BSE Sensex fell 0.4% to 64,831.41 in Mumbai, while the NSE Nifty 50 Index declined 0.5%, their biggest single-day declines since Aug. 25. For the month, the gauges fell more than 2.5% each, their first retreat since February. The selloff in India has come on the back of rising worries over inflation and insufficient rains in many regions.

Asian stocks have been driven by “a combination of what’s happening in the US macro cycle and what’s happening in the Chinese macro cycle,” as well as the “ongoing AI bubble,” Mixo Das, Asia equity strategist at JPMorgan Securities, said in an interview with Bloomberg TV.

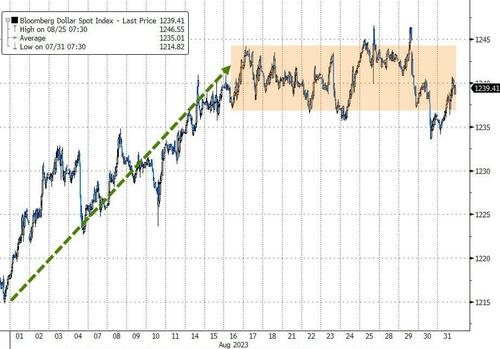

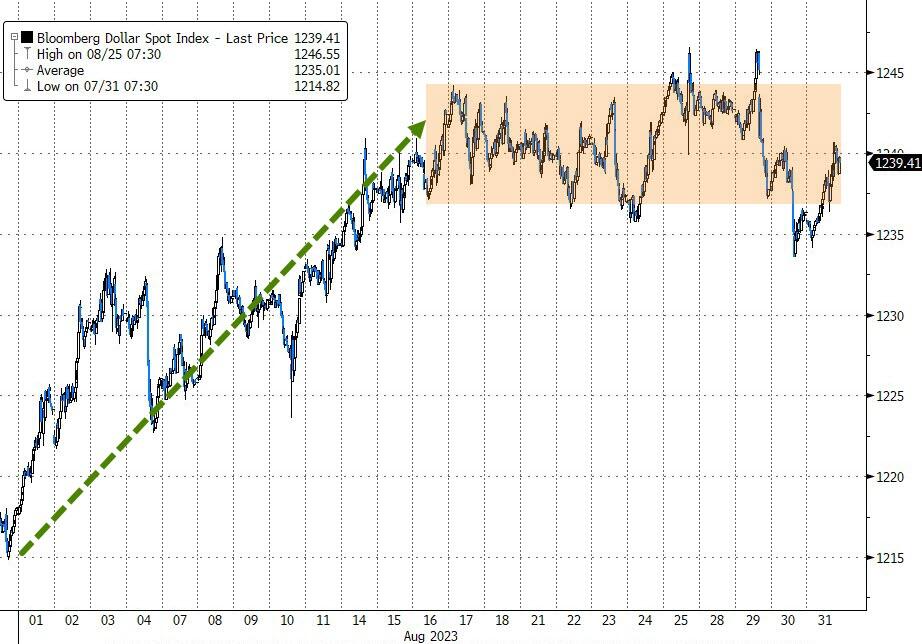

In FX, the Bloomberg Dollar Spot Index rose to session highs and after falling as much as 0.2% earlier. The yen rose the most among the Group-of-10 currencies. The greenback is likely to be “somewhat” volatile over the data release as PCE is the Fed’s preferred inflation measure, said Richard Grace, a senior currency analyst at InTouch Capital Markets Pte. “The market appears to still trying to work out the recent pattern of stronger-than-expected US economic data for a number of weeks, and now a pattern of weaker-than-expected US economic data for a number of days”

The euro fell as traders bet the ECB will hold off on raising rates next month, even as recent data shows inflation is still running above target. The repricing in ECB rates comes after policymaker Isabel Schnabel highlighted the mounting risks to growth and said she can’t say how long rates will remain in restrictive territory. “If the weakness we have seen so far is not enough to bring inflation down, the economy needs to weaken even more,” said Athanasios Vamvakidis, head of G-10 FX strategy at Bank of America. “That’s the main concern for the euro.” AUD/USD rose 0.2% to 0.6488, paring an earlier rise of as much as 0.5%.

In rates, treasuries held small gains in early US trading, paced by UK and euro-zone bond markets, with yields mostly inside Wednesday’s ranges. TSY yields are lower across the curve by 1bp-3bp; Wednesday’s ranges included lowest levels in more than two weeks for all benchmarks except the 30-year. Month-end index rebalancing at 4pm will extend its duration by an estimated 0.12 year as Treasuries issued during the month are added. Bunds are higher while the euro has extended declines as traders seem to focus on the slowdown in euro-area core inflation rather than the headline rate which held steady. Market pricing now suggests a less than 30% chance the ECB raises rates in September, down from ~40% before the data. German 10-year yields are down 5bps at 2.49% while two-year yields drops 9bps. The US economic calendar includes weekly jobless claims and July personal income and spending at 8:30am New York time and August MNI Chicago PMI at 9:45am. Focal points of US session include personal income and spending data that includes PCE deflator, Fed’s preferred inflation gauge, and month-end index rebalancing.

In commodities, Brent crude oil advanced for a third day with WTI rising 0.5% to trade around $82. Spot gold rises 0.1%.

Bitcoin was under modest pressure holding around the USD 27k mark within fairly narrow ranges above the figure. Pressure which eminates from the firmer USD in European trade.

Looking to the day ahead now, and data releases include the Euro Area flash CPI print for August, as well as the unemployment rate for July. In the US we’ve got the weekly initial jobless claims, PCE inflation for July, and the MNI Chicago PMI for August. From central banks, we’ll hear from the Fed’s Bostic and Collins, ECB Vice President de Guindos and the ECB’s Schnabel, and the BoE’S Pill. We’ll also get the ECB’s accounts of their June meeting. Finally, earnings releases include Lululemon, Dollar General and Broadcom.

Market Snapshot

- S&P 500 futures up 0.1% to 4,529.00

- MXAP little changed at 161.98

- MXAPJ down 0.4% to 507.25

- Nikkei up 0.9% to 32,619.34

- Topix up 0.8% to 2,332.00

- Hang Seng Index down 0.5% to 18,382.06

- Shanghai Composite down 0.6% to 3,119.88

- Sensex down 0.2% to 64,966.59

- Australia S&P/ASX 200 up 0.1% to 7,305.27

- Kospi down 0.2% to 2,556.27

- STOXX Europe 600 up 0.3% to 460.38

- German 10Y yield little changed at 2.52%

- Euro down 0.3% to $1.0886

- Brent Futures up 0.2% to $85.99/bbl

- Gold spot up 0.2% to $1,945.26

- US Dollar Index up 0.23% to 103.39

Top Overnight News

- China’s NBS PMIs are mixed for Aug, with Manufacturing coming in at 49.7 (up from 49.3 in Jul and ahead of the Street’s 49.2 forecast) and Manufacturing new orders back in expansion mode for the first time in 5 months, but Non-Manufacturing ticked down to 51 (down from 51.5 in Jul and below the Street’s 51.2 forecast). RTRS

- Chinese president Xi Jinping is not planning to attend the G20 leaders’ summit in New Delhi next weekend and is expected to be replaced by the country’s premier, according to western officials briefed on the situation. FT

- Toyota Motor seeks to shatter its production record this year, aiming to manufacture 10.2 million vehicles globally, the Nikkei has learned, and cross the eight-figure milestone for the first time. Nikkei

- Europe’s CPI in Aug szx mixed, with headline running hot at +5.3% Y/Y (unchanged vs. Jul and above the Street’s +5.1% forecast) while core was +5.3% (down from +5.5% in Jul and inline w/the Street). BBG

- UBS soared to the highest since 2008 after it posted the biggest-ever quarterly profit for a bank and CEO Sergio Ermotti said inflows are climbing across the board. The bank sees positive underlying pretax profit in the second half and will cut about 3,000 jobs as it targets cost savings of $10 billion by end-2026 from its takeover of Credit Suisse. BBG

- The EU’s agriculture chief has proposed that the EU subsidize the cost of transiting Ukrainian grain through the bloc after Russia pulled out of an initiative to allow exports via the Black Sea. FT

- Fed’s Bostic warns that US monetary policy should avoid overtightening (“I think we should be cautious and patient and let the restrictive policy continue to influence the economy, lest we risk tightening too much and inflicting unnecessary economic pain”). BBG

- Facing the prospect of a politically damaging government shutdown within weeks, House Speaker Kevin McCarthy is offering a new argument to conservatives reluctant to vote to keep funding flowing: A shutdown would make it more difficult for Republicans to pursue an impeachment inquiry against President Biden, or to push forward with investigations of him and his family that could yield evidence for one. NYT

- Visa and Mastercard are planning to increase credit-card fees. The changes could result in merchants paying an additional $502 million annually in fees, according to a consulting company. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks eventually traded mostly negatively following a marginally positive handover from Wall Street, which saw an equity bid underpinned by dovish US economic data. ASX 200 was flat on either side of 7,300 as the gains in the Telecoms and Financial sectors were offset by losses in Energy and Consumer Staples. Nikkei 225 saw mild gains although the machinery sectors were in the red following the dire Japanese industrial output data, with a Japanese government official highlighting a decline in demand both domestically and abroad, with output falling in several areas including production machinery. Hang Seng and Shanghai Comp varied at the open but later succumbed to losses, whilst Baidu soared 4.6% after winning Chinese approval for its AI model. The Mainland was more cautious from the start following mixed PMI data which saw Manufacturing topping expectations but remaining in contraction.

Top Asian News

- Baidu (BIDU/9888 HK) is reportedly among the first firms to win China approval for AI models, according to Bloomberg. Baidu rolled out its Chat GPT-rival AI app to the public, according to a statement cited by AFP

- PBoC said it will continue to step up loans to private firms and will use stocks and bonds to deal with risks of private property developers in a prudent way, according to Reuters. PBoC added it will encourage and guide institutional investors to buy bonds of private firms and will support IPO and refinancing of private firms.

- PBoC injected CNY 209bln via 7-day reverse repos with the rate at 1.80% for a CNY

- The Japanese government cut its assessment of industrial production and noted industrial output is seesawing, according to Reuters.

- Japanese government official on industrial output said demand fell both domestically and abroad in July, and noted that output fell in many areas including production machinery. The official said the decrease in chip manufacturing machinery is due to weak demand abroad, the outlook appears to be severe; chip shortage is easing in autos, which is on a steady recovery, according to Reuters.

- Japanese government official said the electronics device market in China is in a severe state; Domestic material industries are partially affected by China’s real estate concerns, according to Reuters.

- BoJ Board Member Nakamura said the BoJ must patiently maintain easy policy for the time being, and need more time to shift to monetary tightening; Japan’s economy is no longer in deflation; tweaks to policy must be cautious. Was not against making YCC flexible, opposition was re. timing. July decision was not part of any exit from ultra-loose policy. BoJ will closely watch impact on Yen moves on economy and prices. FX is not driven by interest rate differentials alone.

- Japanese PM Kishida said to be considering lifting the minimum wage to JPY 1500/hr by mid 2030s, via NHK.

- Japan’s major five banks are to increase housing loan interest rates by 0.1% to 0.2%, according to Jiji News.

- Fitch affirms China at A+, outlook stable; revises lower 2023 China GDP Growth forecast to 4.8% (prev. 5.6%).

European bourses are modestly firmer, Euro Stoxx 50 +0.1%, having trimmed initial upside throughout a session of significant Central Bank updates. Downside which has occurred despite a dovish-shift to pricing for the ECB post-HICP & Schnabel; within Europe, Real Estate leads the sectors while Banking names lag as both areas of the economy take impetus from yield action. Though, the Banking pressure is offset somewhat by marked upside in UBS +4.5% post-earnings; SAP modestly firmer after CRM earnings, CRM +5.5% in pre-market. Stateside, futures are mixed around the unchanged mark with some slight underperformance in the NQ -0.1% ahead of key data and despite the broader European-driven yield action.

Top European News

- ECB’s Schnabel says outlook for the Euro Area remains highly uncertain, activity has moderated visibly, and forward-looking indicators signal weakness ahead. Cannot predict where the peak rate is going to be, or for how long rates will have to be held at restrictive levels, cannot commit to future actions. Within the remarks, Schnabel is very balanced and holds open the door for a hike or a skip at the September gathering. For reference, the remarks were published pre-HICP

- ECB’s Holzmann says August inflation data is a conundrum for the ECB; we are not yet at the highest level for rates, another hike or two is possible. ECB should consider needing PEPP reinvestments before the end of next year. Based on current data, would not exclude a rate hike in September but hasn’t made mind up yet. Much closer to terminal rate but likely not there yet. Remarks published after the HICP data

- BoE’s Pill says the UK faces second-round inflation effects and inflation is too high, cases for caution on inflation despite the declines in the headline. There is a lot of policy in the pipeline to come through. There is the possibility of doing too much when it comes to the fight against inflation. Policy needs to be sufficiently restrictive for long enough.. Adds, one option for policy is to hold rates steady for longer; tends to favour that approach.

- UK PM Sunak is expected to announce a new Defence Secretary to replace Ben Wallace on Thursday, according to government officials cited by the FT. Grant Shapps is a surprise frontrunner for the role, according to insiders.

FX

- DXY rebounds firmly from 103.000 to 103.550, while Euro reels from 1.0939 to 1.0865 vs the Buck after mixed EZ data and less hawkish remarks from ECB’s Schnabel.

- Yen relishes softer yields as it continues consolidation against Greenback either side of 146.00 irrespective of mixed Japanese macro releases.

- Sterling buffeted as BoE’s Pill warns against complacency on inflation given second round effects, but backs a steady for longer strategy rather than overtightening.

- Cable wanes around 1.2700 pivot, EUR/GBP eases from 0.8598 towards 0.8560.

- PBoC sets USD/CNY mid-point at 7.1811 vs exp. 7.2765 (prev. 7.1816)

- China’s major state-owned banks seen selling USD in onshore spot foreign exchange market; Banks spotted swapping CNY for USD in onshore forwards market, via Reuters citing sources.

- Brazil’s 2024 Budget Law revenue measures will reportedly reach BRL 168bln, according to Estadao sources. The revenue package will consider ending the deductibility of Interest on Equity for all sectors.

Fixed Income

- Bonds approaching month end on the up, but not before overcoming several wobbles.

- Bunds towards top of 132.87-131.83 range and perhaps latching on to soft EZ core inflation and less hawkish vibes from ECB’s Schnabel.

- Gilts also bid between 95.28-94.66 parameters as BoE’s Pill states preference for a longer period of steady rates rather than overtightening.

- T-note more restrained within 111-00/110-24+ confines awaiting PCE, IJC, Fed’s Collins and Chicago PMI.

- Following the European data and ECB speakers, pricing for a 25bp hike at the September meeting has dropped to a 30% probability from over 60% in recent sessions.

- UK DMO intends to hold 15 Gilt auctions between October-December, and a syndicated sale of a new long-dated conventional in November.

Commodities

- Crude benchmarks are a touch firmer on the session with specific details light as we await an update from the BSEE on how much, if any, production has been lost due to Hurricane Idalia.

- Gas markets are bid but off highs while spot gold is little changed and torn between the softer risk tone and stronger USD.

- For Ags., Reuters citing Turkish sources reported that President Erdogan is to meet Russia President Putin in Sochi on September 4th to discuss Ukraine and the grain deal. As a reminder, earlier in the week reports indicated that the nation’s Foreign Ministers are to speak in today’s session as Turkey looks to bring Russia back to the Black Sea grain deal.

Geopolitics

- US approves first arms to Taiwan under foreign aid program, according to AFP citing an official.

- US reportedly restricts the export of some AMD (AMD) chips to Middle Eastern countries, according to Reuters sources.

- North Korea conducted full-force command training in response to the SK-US joint exercise, according to Yonhap.

- Japanese PM Kishida has requested top LDP lawmaker Nikai to visit China to resolve the Fukushima water issue, according to local press.

- Australia and EU to resume free-trade deal talks on Thursday via teleconference, a month after the sides failed to reach a deal, according to Reuters.

US Event Calendar

- 07:30: Aug. Challenger Job Cuts 266.9%; YoY, prior -8.2%

- 08:30: Aug. Initial Jobless Claims, est. 235,000, prior 230,000

- Continuing Claims, est. 1.71m, prior 1.7m

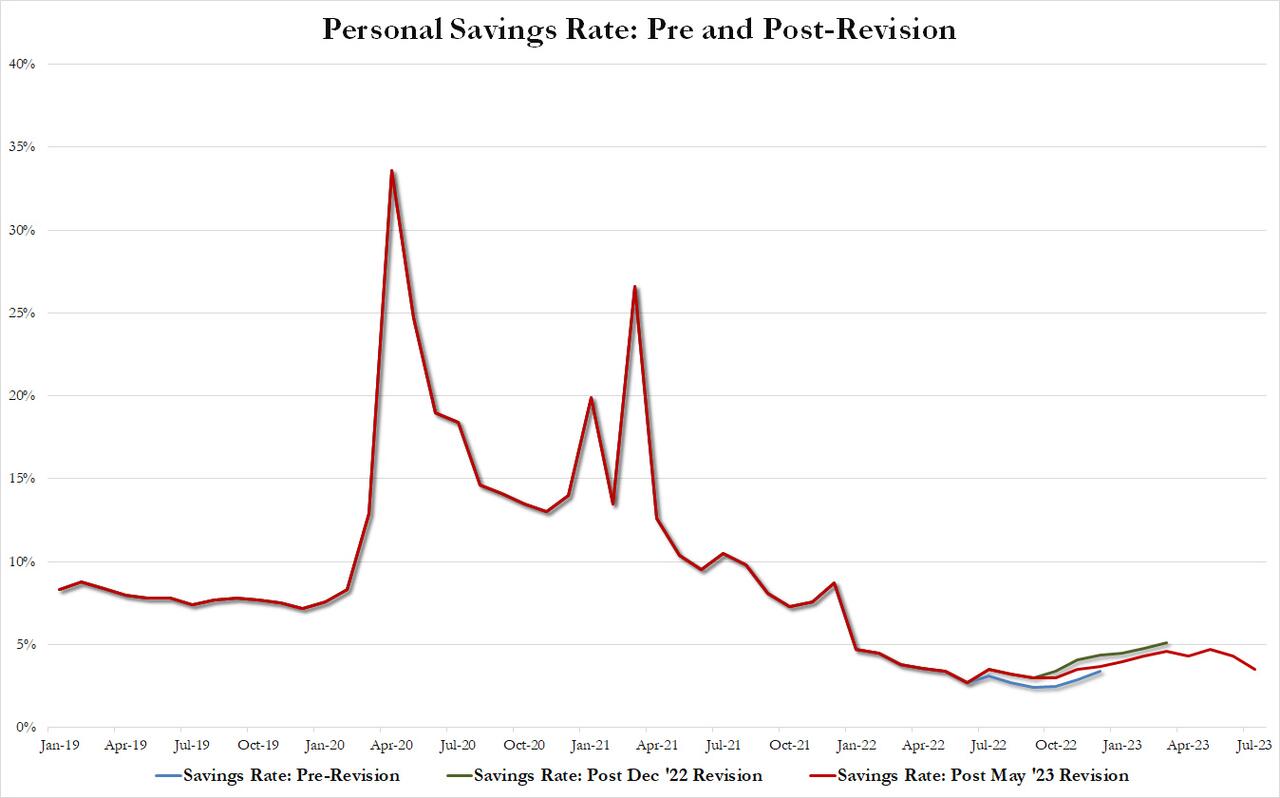

- 08:30: July Personal Income, est. 0.3%, prior 0.3%

- Personal Spending, est. 0.7%, prior 0.5%

- Real Personal Spending, est. 0.5%, prior 0.4%

- 08:30: July PCE Deflator MoM, est. 0.2%, prior 0.2%

- PCE Deflator YoY, est. 3.3%, prior 3.0%

- PCE Core Deflator MoM, est. 0.2%, prior 0.2%

- PCE Core Deflator YoY, est. 4.2%, prior 4.1%

- 09:45: Aug. MNI Chicago PMI, est. 44.2, prior 42.8

DB’s Jim Reid concludes the overnight wrap

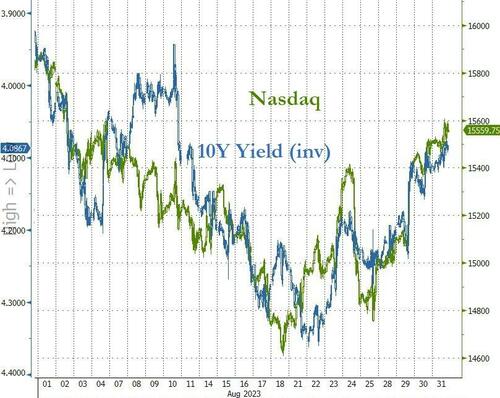

Markets had plenty to chew on yesterday, as the latest round of data offered support to both sides of the hard vs soft landing debate. We again had some underwhelming US releases which suggested that growth and inflation were slowing further which could be used to support either side of the debate. However for yesterday the soft landing argument continued to win out with yields on 10yr Treasuries (-0.7bps) inching down to a 3-week low of 4.11% and the S&P 500 (+0.38%) hitting a 3-week high. But in Europe, markets saw a clear underperformance thanks to resilient inflation numbers from Germany and Spain, which added to speculation that the ECB might deliver a 10th consecutive rate hike next month.

With the conflicting releases, all eyes are now on tomorrow’s US jobs report to see if that can shift the narrative one way or the other. Our US economists are expecting nonfarm payrolls to slow down further to 150k, and yesterday we had some further evidence of a softening labour market from the ADP’s report of private payrolls. That showed growth of +177k in August (vs. +195k expected), which is the smallest gain since March. On top of that, there was a continued slowdown in pay growth, with the rate among job-changers down to +9.5% year-on-year, which is the slowest since June 2021, whilst the rate among job-stayers fell to the slowest since September 2021, at +5.9%.

That ADP report came just before the second estimate of Q2 GDP growth, which indicated that the economy was a bit weaker than previously thought. For instance, overall growth came in at an annualised rate of +2.1%, which was down from the initial estimate of +2.4%. And more promisingly for the Fed, both PCE and core PCE for Q2 were each revised down a tenth, with the latest estimate putting them at +2.5% and +3.7% respectively.

These indications of a slowing economy led to a fresh rally among US markets. The main reason for that is because expectations of another rate hike from the Fed have continued to come down, and now stand beneath 50% for the first time since last week. So bad news on the economy is still being treated as good news (for now), since optimism about fewer rate hikes is outweighing the prospects of slower growth. In turn, that led to a rally among US Treasuries, although one that lost steam during the day with yields on 2yr Treasuries (-1.0bps) and 10yr Treasuries (-0.7bps) down only a little by the close. The 2yr yield had traded as much as -6bps lower shortly after the US data in the morning. As discussed, equities put in another decent performance as well, with the S&P 500 (+0.38%), advancing for a 4th consecutive session. On a sectoral basis, it was tech stocks that led the advance once again, and the NASDAQ (+0.54%) hit a 4-week high.

Over in Europe it was a rather different story, since the latest data suggested that inflation was proving more resilient than expected. In particular, the German flash CPI print for August only fell back to +6.4% on the EU-harmonised measure (vs. +6.3% expected). At the same time, Spanish inflation ticked up three-tenths to +2.4%, whilst Irish inflation was also up three-tenths to +4.9%. That sets the stage for the Euro-Area wide print this morning, which is out at 10am London time. Following yesterday’s prints, our European economists see both the headline and core inflation prints coming in at between +5.3% and +5.4%. This would represent a near stable headline reading (+5.3% prev.) and a slight easing in core (+5.5% prev.).

Those CPI numbers led to growing expectations that the ECB might proceed with another hike at their next decision in two weeks’ time. Indeed, market pricing is now suggesting a 55% chance of a 25bp hike at the September meeting, so back up to its level prior to the underwhelming flash PMI data last week. It also led to a significant underperformance among European sovereign bonds, with yields on 10yr bunds (+3.4bps), OATs (+3.7bps) and BTPs (+4.4bps) all moving higher on the day, whilst the STOXX 600 fell -0.15%. The big concern now is that the European outlook is looking increasingly stagflationary, with inflation remaining stubborn whilst there’s few signs of growth either. On the topic of European inflation, our economists yesterday published the results of their latest dbDIG consumer survey, which has shown an uptick in inflation expectations during July and August. See their note here.

Overnight in Asia, several equity markets have lost ground this morning, which follows the release of the official PMIs from China. They showed that manufacturing contracted for a fifth consecutive month, with a 49.7 reading but it was higher than the 49.2 reading expected by the consensus, and above the 49.3 reading in June. However, the non-manufacturing PMI fell a bit more than expected to 51.0 (vs. 51.2 expected).

Against that backdrop, most of the major indices have struggled this morning, with declines for the CSI 300 (-0.54%), the Shanghai Comp (-0.53%), the KOSPI (-0.36%) and the Hang Seng (-0.26%). The main exception is in Japan, where the Nikkei (+0.80%) and other indices including the TOPIX (+0.79%) have seen a decent advance this morning. That comes amidst better-than-expected retail sales data overnight, which grew by +2.1% in July (vs. +0.8% expected). That said, industrial production fell by -2.0% (vs. -1.4% expected).

Looking at yesterday’s other data, there were further signs of resilience in the US housing market, as pending home sales unexpectedly grew by +0.9% in July (vs. -1.0% expected). That said, the July data was before the most recent rise in mortgage rates into August, and separate data from the MBA yesterday showed that the 30yr average fixed rate remained at 7.31% in the week ending August 25.

To the day ahead now, and data releases include the Euro Area flash CPI print for August, as well as the unemployment rate for July. In the US we’ve got the weekly initial jobless claims, PCE inflation for July, and the MNI Chicago PMI for August. From central banks, we’ll hear from the Fed’s Bostic and Collins, ECB Vice President de Guindos and the ECB’s Schnabel, and the BoE’S Pill. We’ll also get the ECB’s accounts of their June meeting. Finally, earnings releases include Lululemon, Dollar General and Broadcom.

2 B) NOW NEWSQUAWK (EUROPE/REPORT)/

ECB pricing shifts dovishly post-HICP/Schnabel; Focus turns to PCE & IJC – Newsquawk US Market Open

THURSDAY, AUG 31, 2023 – 06:08 AM

- European bourses are mostly firmer after a packed morning ahead of an equally busy US agenda, ES +0.1%

- EUR & EZ yields slump after Flash HICP and balanced commentary from Schnabel on a hike/skip for upcoming meetings

- Pricing for a 25bp hike by the ECB in September down to a 30% chance from over 60% in recent sessions

- DXY bid as a result and pressuring peers, Cable dented further by Pill backing a steady for longer strategy vs overtightening

- Crude continues to climb while XAU is near unchanged and torn between the risk tone & USD upside

- APAC traded negative despite the firmer handover with mixed Chinese PMIs influencing

- Looking ahead, highlights include US PCE Price Index (Jul), IJC & Challenger Layoffs, speeches from Fed’s Collins, ECB’s de Guindos.

EUROPEAN TRADE

EQUITIES

- European bourses are modestly firmer, Euro Stoxx 50 +0.1%, having trimmed initial upside throughout a session of significant Central Bank updates.

- Downside which has occurred despite a dovish-shift to pricing for the ECB post-HICP & Schnabel; within Europe, Real Estate leads the sectors while Banking names lag as both areas of the economy take impetus from yield action.

- Though, the Banking pressure is offset somewhat by marked upside in UBS +4.5% post-earnings; SAP modestly firmer after CRM earnings, CRM +5.5% in pre-market.

- Stateside, futures are mixed around the unchanged mark with some slight underperformance in the NQ -0.1% ahead of key data and despite the broader European-driven yield action.

- Click here for more detail.

- Click here and here for a recap of the main European equity updates.

FX

- DXY rebounds firmly from 103.000 to 103.550, while Euro reels from 1.0939 to 1.0865 vs the Buck after mixed EZ data and less hawkish remarks from ECB’s Schnabel.

- Yen relishes softer yields as it continues consolidation against Greenback either side of 146.00 irrespective of mixed Japanese macro releases.

- Sterling buffeted as BoE’s Pill warns against complacency on inflation given second round effects, but backs a steady for longer strategy rather than overtightening.

- Cable wanes around 1.2700 pivot, EUR/GBP eases from 0.8598 towards 0.8560.

- PBoC sets USD/CNY mid-point at 7.1811 vs exp. 7.2765 (prev. 7.1816)

- China’s major state-owned banks seen selling USD in onshore spot foreign exchange market; Banks spotted swapping CNY for USD in onshore forwards market, via Reuters citing sources.

- Brazil’s 2024 Budget Law revenue measures will reportedly reach BRL 168bln, according to Estadao sources. The revenue package will consider ending the deductibility of Interest on Equity for all sectors.

- Click here for more detail.

- Click here for the Option Expires for the NY Cut.

FIXED INCOME

- Bonds approaching month end on the up, but not before overcoming several wobbles.

- Bunds towards top of 132.87-131.83 range and perhaps latching on to soft EZ core inflation and less hawkish vibes from ECB’s Schnabel.

- Gilts also bid between 95.28-94.66 parameters as BoE’s Pill states preference for a longer period of steady rates rather than overtightening.

- T-note more restrained within 111-00/110-24+ confines awaiting PCE, IJC, Fed’s Collins and Chicago PMI.

- Following the European data and ECB speakers, pricing for a 25bp hike at the September meeting has dropped to a 30% probability from over 60% in recent sessions.

- UK DMO intends to hold 15 Gilt auctions between October-December, and a syndicated sale of a new long-dated conventional in November.

- Click here for more detail.

COMMODITIES

- Crude benchmarks are a touch firmer on the session with specific details light as we await an update from the BSEE on how much, if any, production has been lost due to Hurricane Idalia.

- Gas markets are bid but off highs while spot gold is little changed and torn between the softer risk tone and stronger USD.

- For Ags., Reuters citing Turkish sources reported that President Erdogan is to meet Russia President Putin in Sochi on September 4th to discuss Ukraine and the grain deal. As a reminder, earlier in the week reports indicated that the nation’s Foreign Ministers are to speak in today’s session as Turkey looks to bring Russia back to the Black Sea grain deal.

- Click here for more detail.

NOTABLE US HEADLINES

- Salesforce Inc (CRM) Q2 2023 (USD): Adj. EPS 2.12 (exp. 1.90), Revenue 8.60bln (exp. 8.52bln). Shares +5.6%, in pre-market.

- US officials are reportedly mulling a pathway to let more firms tap the Federal Home Loan Banks, according to Bloomberg.