GOLD PRICE CLOSED: DOWN $8.80 TO $1919.00

SILVER PRICE CLOSED: DOWN $0.36 AT $23.18

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1916.70

Silver ACCESS CLOSE: 23.17

Shanghai Gold Benchmark Price

USD oz  AM1983.16PM

AM1983.16PM

1984.71

Historical SGE Fix

New York price at the time: $1925.00

premium $59.00

xxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $25,731 DOWN 15 Dollars

Bitcoin: afternoon price: $25,617 DOWN 129 dollars

Platinum price closing $914.15 DOWN $9.20

Palladium price; $1214.65 DOWN $5.95

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,614.18 DOWN 13.69 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1532.86 DOWN 0 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1787.06 DOWN 9.33 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,926.200000000 USD

INTENT DATE: 09/05/2023 DELIVERY DATE: 09/07/2023

FIRM ORG FIRM NAME ISSUED STOPPED

323 H HSBC 13

363 H WELLS FARGO SEC 11

435 H SCOTIA CAPITAL 7

624 H BOFA SECURITIES 19

661 C JP MORGAN 45

690 C ABN AMRO 1

737 C ADVANTAGE 10 5

905 C ADM 1

TOTAL: 56 56

JPMorgan stopped 0/56 contracts.

FOR SEPT.:

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2023. CONTRACT: 56 NOTICES FOR 5,600 OZ or .1742 TONNES

total notices so far: 3600 contracts for 360,000 oz (11.197 tonnes)

FOR SEPT:

SILVER NOTICES: 7 NOTICE(S) FILED FOR 35,000 OZ/

total number of notices filed so far this month : 2290 for 11,450,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $8.80

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/SMALL CHANGES IN GOLD INVENTORY AT THE GLD: / A WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 889.81 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 36 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.373 MILLION OZ OZ SILVER OUT OF THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 436.518 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 1709 CONTRACTS TO 128,279 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS STRONG SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.69 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. TAS ISSUANCE WAS A GIGANTIC SIZED 2111 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 2111 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.69). BUT WERE SUCCESSFUL IN KNOCKING SOME SILVER CONTRACTS AS WE HAD A HUGE SIZED LOSS OF 1483 CONTRACTS ON BOTH EXCHANGES ALONG WITH HUGE T.A.S.LIQUIDATION THROUGHOUT THE COMEX SESSION.

WE MUST HAVE HAD:

A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS( 276 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 14.420 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 90,000 OZ//NEW TOTAL 12.165 MILLION OZ/// / //STRONG SIZED COMEX OI GAIN/ SMALL SIZED EFP ISSUANCE/VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE (2210 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL 853 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 3 days, total 1621 contracts: OR 8.105 MILLION OZ (540 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 8.105 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 8.105 MILLION OZ

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1709 CONTRACTS WITH OUR LOSS IN PRICE OF $0.69 IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL EFP ISSUANCE CONTRACTS: 276 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR SEPT OF 14.420 MILLION OZ FOLLOWED BY TODAY’S 90,000 OZ E.F.P. TO LONDON /// WE HAVE A HUGE SIZED LOSS OF 1433 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GIGANTIC 2111 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION. THE NEW TAS ISSUANCE TUESDAY NIGHT (2264) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 7 NOTICE(S) FILED TODAY FOR 35,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1208 CONTRACTS TO 438,672 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: 2066 CONTRACTS

WE HAD A SMALL SIZED INCREASE IN COMEX OI ( 198 CONTRACTS) DESPITE OUR $13,50 LOSS IN PRICE//TUESDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 12.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 5800 OZ QUEUE JUMP//NEW TOTAL STANDING 13.710 TONNES + /A HUGE (AND CRIMINAL) ISSUANCE OF 2210 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR $13.50 LOSS IN PRICE WITH RESPECT TO TUESDAY’S TRADING.WE HAD A TINY SIZED GAIN OF 198 OI CONTRACTS (0.6158 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1406 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 438,672

IN ESSENCE WE HAVE A TINY SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 198 CONTRACTS WITH 1208 CONTRACTS DECREASED AT THE COMEX// AND A FAIR 1406 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 198 CONTRACTS OR 0.5158 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A HUGE 2210 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1406 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (1208) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 198 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 12.656 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 5800 OZ/// 3) ZERO LONG LIQUIDATION WITH HUGE TAS LIQUIDATION DURING THE COMEX SESSION //4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: HUGE T.A.S. ISSUANCE: 868 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT :

TOTAL EFP CONTRACTS ISSUED: 7271 CONTRACTS OR 727,100 OZ OR 22.61 TONNES IN 3 TRADING DAY(S) AND THUS AVERAGING: 2423 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES 22.61 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 22.61/3550 x 100% TONNES 0.616% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 22.61 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 1709 CONTRACTS OI TO 128,279 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A SMALL 276 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 276 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 276 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1709 CONTRACTS AND ADD TO THE 276 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1433 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 7.165 MILLION OZ

OCCURRED WITH OUR $0.69 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED UP 3.71 PTS OR 0.12% //Hang Seng CLOSED DOWN 6.93 PTS OR 0.04% /The Nikkei CLOSED UP 204.26 PTS OR 0.62% //Australia’s all ordinaries CLOSED DOWN 0.73 % /Chinese yuan (ONSHORE) closed DOWN 7.3034 /OFFSHORE CHINESE YUAN DOWN TO 7.3075 /Oil UP TO 86.29 dollars per barrel for WTI and BRENT UP AT 89.42 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1208 CONTRACTS TO 438,672 WITH OUR LOSS IN PRICE OF $13.50 ON TUESDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1406 EFP CONTRACTS WERE ISSUED: : DEC 1406 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1406 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A TINY TOTAL OF 198 CONTRACTS IN THAT 1406 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 1208 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $13.50//TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A GOOD 2264 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (13.710) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 13.710 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $13.50) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A TINY GAIN OF 198 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A HUGE T.A.S. LIQUIDATION ON THE FRONT END OF TUESDAY’S TRADING. THE T.A.S. ISSUED ON TUESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 0.6158 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPT. (12.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 5800 OZ//NEW STANDING 13.710 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $13.50.

WE HAD – REMOVED 2066 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 198 CONTRACTS OR 19800 OZ OR 0.6158 TONNES.

Estimated gold volume today:// 145,901 poor

final gold volumes/yesterday 204,481 fair raid//speculators have left the gold arena

//SEPT 6/ /// THE SEPT. 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 144,879.742 OZ Brinks . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 56 notice(s) 5600 OZ .1742 TONNES |

| No of oz to be served (notices) | 808 contracts 80800 oz 2.513 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3600 notices 360000 OZ 11.197 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: nil oz

we had 1 customer withdrawals

i) Out of Brinks: 144,879.742 oz

total withdrawals 144,879.742 oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER.

For the front month of SEPTEMBER we have an oi of 864 contracts having LOST 70 contracts. We had

128 contracts were served on TUESDAY, so we gained an additional 58 CONTRACTS or AN ADDITIONAL 5800 oz will stand for delivery in this non active

delivery month of Sept.

Oct GAINED 8 contracts to 28,114 contracts.

December LOST 877 contracts down to 377,508 contracts.

We had 56 contracts filed for today representing 5600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 45 notices were issued from their client or customer account. The total of all issuance by all participants equate to 56 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2023. contract month,

we take the total number of notices filed so far for the month (3600 x 100 oz ), to which we add the difference between the open interest for the front month of SEPT (864 CONTRACTS) minus the number of notices served upon today 56 x 100 oz per contract equals 440,800 OZ OR 13.710 TONNES the number of TONNES standing in this non active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month: No of notices filed so far (3600) x 100 oz + (864) {OI for the front month} minus the number of notices served upon today (56) x 100 oz) which equals 440,800 oz standing OR 13.710 TONNES

TOTAL COMEX GOLD STANDING: 13.710 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,011,076.496 OZ 62.55 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,243,540.527 OZ

TOTAL REGISTERED GOLD 10 ,853.948.876 (337.60 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,359,591.631 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,843,355 OZ (REG GOLD- PLEDGED GOLD) 275.06 tonnes//dropping like a stone

END

SILVER/COMEX

SEPT 6

//2023// THE SEPT 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 581,787.109 oz Loomis . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 7 CONTRACT(S) (35,000 OZ) |

| No of oz to be served (notices) | 143 contracts (715,000 oz) |

| Total monthly oz silver served (contracts) | 2290 Contracts (11,450,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 deposits customer account:

total customer deposits: nil oz

JPMorgan has a total silver weight: 138.666 million oz/277.377 million or 49.81%

Comex withdrawals 1

i) Out of Loomis 581,787.109 oz

total: 581,787.109 oz

adjustments: 1 dealer to customer Manfra

581,263.743 oz

TOTAL REGISTERED SILVER: 43.769 MILLION OZ//.TOTAL REG + ELIGIBLE. 277.785 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF SEPT /2023 OI: 150 CONTRACTS HAVING LOST 176 CONTRACT(S). WE HAD 132

CONTRACTS SERVED ON TUESDAY. SO WE LOST 18 CONTRACTS OR 90,000 OZ WERE IMMEDIATELY E.F.P’d TO LONDON AS THERE WAS NO METAL OVER HERE FOR THESE GUYS.

OCT LOST 4 CONTRACTS TO STAND AT 1142.

NOVEMBER GAINED 72 CONTRACTS TO STAND AT 77

DEC. LOST 1720 CONTRACTS TO STAND AT 116,126 .

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 7 for 35,000 oz

Comex volumes// est. volume today 67,243 poor

Comex volume: confirmed yesterday 94,243 strong

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 2290 x 5,000 oz = 11,450,000 oz

to which we add the difference between the open interest for the front month of SEPT (150) and the number of notices served upon today 7x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2023 contract month: 2290 (notices served so far) x 5000 oz + OI for the front month of SEPT (150) – number of notices served upon today (7 )x 500 oz of silver standing for the SEPT contract month equates to 12.165 million oz.

There are 43.769 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

SEPT 6/WITH GOLD DOWN $8.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.81 TONNES

SEPT 5/WITH GOLD DOWN $13.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.97 TONNES

SEPT 1/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 31/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 30/WITH GOLD UP $8.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.59 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.23 TONNES

AUGUST 29/WITH GOLD UP 17.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.6 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.64 TONNES

AUGUST 28/WITH GOLD UP $6.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / //INVENTORY RESTS AT 884.04 TONNES

AUGUST 25/WITH GOLD DOWN $6.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 884.04 TONNES

AUGUST 24/WITH GOLD UP $0.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //INVENTORY RESTS AT 884.91 TONNES

AUGUST 23/WITH GOLD UP $21.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 4.32 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 884.91 TONNES

AUGUST 22/WITH GOLD UP $2.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.87 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 889.23 TONNES

AUGUST 21/WITH GOLD UP $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.60 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 890.10 TONNES

AUGUST 18/WITH GOLD UP $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 887.50 TONNES

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 16/WITH GOLD DOWN $7.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 15/WITH GOLD DOWN $7,45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 895.87 TONNES

AUGUST 14/WITH GOLD DOWN $2.10 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.75 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 899.63 TONNES

AUGUST 11/WITH GOLD DOWN $2.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 903.31 TONNES

AUGUST 10/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 9/WITH GOLD DOWN $8.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 8/WITH GOLD DOWN $9.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES FORM THE GLD /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 7/WITH GOLD DOWN $5.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///INVENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 31/WITH GOLD UP $9.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 28/WITH GOLD UP $14.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 915,82 TONNES

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

GLD INVENTORY: 889.81 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 6/WITH SILVER DOWN 36 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.373 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 5/WITH SILVER DOWN 69 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 734,000 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 437.891 MILLION OZ

SEPT 1/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 440.00 MILLION OZ

AUGUST 31/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 438.625 MILLION OZ

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.834 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 443.210 MILLION OZ

AUGUST 29/WITH SILVER UP 49 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 183,000 OF SILVER INTO THE THE SLV// /.////INVENTORY RESTS AT 445.044 MILLION OZ

AUGUST 28/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.281 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 444.861 MILLION OZ

AUGUST 25/WITH SILVER UP ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 446.145 MILLION OZ

AUGUST 24/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.651 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 448.896 MILLION OZ

AUGUST 23/WITH SILVER UP 94 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FROM THE SLV// /.////INVENTORY RESTS AT 450.547 MILLION OZ

AUGUST 22/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: /.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 21/WITH SILVER UP 59 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 917,0000 OZ FROM THE SLV//.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 18/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 16/WITH SILVER DOWN 13 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 15/WITH SILVER DOWN 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 14/WITH SILVER DOWN 3 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.459 MILLION OZ INTOTHE SLV/: //////INVENTORY RESTS AT 452.565 MILLION OZ

AUGUST 11/WITH SILVER DOWN 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.926 MILLION OZ INTOTHE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 452.106 MILLION OZ

AUGUST 10/WITH SILVER UP 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 9/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 8/WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 7/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 31/WITH SILVER UP 45 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 28/WITH SILVER UP 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.930 MILLION OZ

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

CLOSING INVENTORY 436.518 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

Peter Schiff: Fed Isn’t Making Any Progress Against Inflation

BY TYLER DURDEN

WEDNESDAY, SEP 06, 2023 – 01:05 PM

Peter Schiff recently appeared on Fox Digital and poured a bucket of cold water on those who believe the Federal Reserve is winning the inflation fight. In fact, the Fed isn’t making any progress at all.

Peter started the interview by noting that the Bureau of Labor Statistics (BLS) has revised the nonfarm payroll numbers down for all seven months this year.

If we’ve done something seven times in a row, it doesn’t seem very random. Because if these were random numbers, sometimes they’d be too high, sometimes they’d be too low. Like, it’s difficult to toss heads seven times in a row. So, if you toss it seven times in a row, maybe the coin is not fair.”

Peter said he thinks the BLS is biased in its assumptions and thinks the labor market is stronger than it actually is.

Obviously, unemployment picked up. So, that’s a sign of weakness. Average hourly earnings — up less than expected, which is problematic because prices continue to rise.”

Peter also noted there was a big spike in spending last month, but a very small gain in incomes.

The way consumers handled that was raiding their savings.”

The savings rate plunged to 3.5%.

In fact, American consumers have blown through nearly all of the excess savings they accumulated during the government pandemic lockdowns. Aggregate savings peaked at $2.1 trillion in August 2021. As of June, the San Francisco Fed estimated that aggregate savings had dropped to $190 billion.

That’s a sign that the economy is weak because consumers need that rainy day fund, right? Because it’s raining. They’re having a hard time.”

And Peter said it also shows the Fed isn’t making any progress in its inflation fight.

Consumers keep spending and reducing their savings in spite of the rate hikes. The rate hikes are supposed to reduce spending and increase savings. That’s how they bring down inflation. But nothing has worked, and so inflation is going to get worse.”

When you boil it all down, this is stagflation.

The economy is weakening, the labor market is weakening, but consumer prices are strengthening.”

Peter said he thinks we’ve bottomed out on headline CPI and noted that we really haven’t seen much of a reduction in core CPI.

So, now we’re bending back up again and the Fed is at five-and-a-half. They’re no closer to getting 2% inflation than when they had rates at zero.”

Meanwhile, federal budget deficits continue to spiral upward. The government is spending more instead of less.

Nothing has worked, and the markets are completely wrong on their benign outlook for future inflation.”

Peter said the “proper response” would be for the Fed to continue to raise rates while the federal government cuts spending. Of course, the Biden administration isn’t going to cut spending. And while you might see another quarter-point rate hike in September, it’s not going to be enough.

We actually need much higher interest rates. The problem is we can’t afford them. So any interest rate high enough to fight inflation is too high for the markets. And in fact, not only does the Fed create a recession. But it creates a financial crisis, and that financial crisis will be considerably worse than the one we had in 2008.”

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

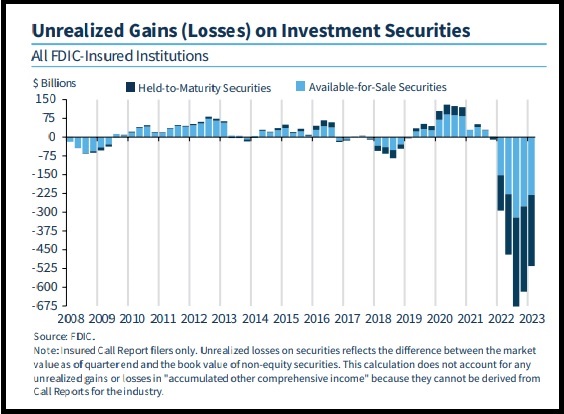

RUSS MARTENS:

Study Finds 75 Percent of U.S. Banks Didn’t Hedge Interest Rate Risk; Unrealized Losses on Securities $516 Billion at End of First Quarter

By Pam Martens and Russ Martens: September 6, 2023 ~

A group of academics have conducted a study that found that during the fastest pace of Fed interest rate hikes in 40 years, the majority of U.S. banks failed to hedge their interest rate risk. The report’s findings include the following:

“Over three quarters of all reporting banks report no material use of interest rate swaps.”

“Only 6% of aggregate assets in the U.S. banking system are hedged by interest rate swaps.”

“Banks with the most fragile funding – i.e., those with highest uninsured leverage — sold or reduced their hedges during the monetary tightening. This allowed them to record accounting profits but exposed them to further rate increases. These actions are reminiscent of classic gambling for resurrection: if interest rates had decreased, equity would have reaped the profits, but if rates increased, then debtors and the FDIC would absorb the losses.”

The use of the phrase “classic gambling” to describe 75 percent of the U.S. banking system by highly credentialed academics might be something that the U.S. Senate Banking Committee might want to hold a hearing about with some sense of urgency.

Not to put too fine a point on it, but this is the year in which banking regulators were left scratching their heads at the dizzying speed at which multiple banks collapsed. In the span of seven weeks this spring, running from March 10 to May 1, the second, third, and fourth largest bank failures in U.S. history occurred. In order of size, those were: First Republic Bank (May 1), Silicon Valley Bank (March 10) and Signature Bank (March 12). The largest bank failure in U.S. history, Washington Mutual, occurred in 2008 during the financial crisis.

An equally disturbing finding in the report is that the very largest banks in the U.S. – the ones that pose systemic risk to both the banking system and the U.S. economy – only hedge “one third of their securities.” The report notes that “Overall, largest banks rely on hedging most, but these hedges leave the vast majority of interest rate risk unhedged.”

The researchers write the following regarding the collapse of Silicon Valley Bank:

“One might conjecture that banks more exposed to solvency runs would have larger incentives to avoid further asset value declines and thus avoid failure, so they might want to increase their hedging activities. Instead, we find that banks with higher uninsured leverage (higher share of uninsured deposit funding) sold or reduced their hedges during 2022. Because of reduced hedges, these banks went on to suffer larger losses when interest rates increased further. A case study of the recently failed Silicon Valley Bank (SVB) is illustrative. SVB hedged about 12% of all [of their own] securities at the end of 2021. By the end of 2022, they hedged only 0.4% of all [of their own] securities. During this period, the duration of their assets increased by almost two years. So, every additional percentage point increase in the policy rate led to a two-percentage point larger decrease in asset values than it would have in 2021. Reduction in hedges by the banks with more fragile funding is suggestive of gambling for resurrection. Selling profitable hedges allows weak banks to increase current accounting earnings. At the same time these banks have taken a large risk, which is profitable for bank shareholders on the upside, but the losses are borne by the FDIC on the downside.”

Shareholders eventually pay the piper as well. The publicly-traded parent company of Silicon Valley Bank, SVP Financial Group, has gone from a share price of more than $300 in February to a closing share price of 5 cents yesterday. For more on how this federally-insured bank was operated, see our report: Silicon Valley Bank Was a Wall Street IPO Pipeline in Drag as a Federally-Insured Bank; FHLB of San Francisco Was Quietly Bailing It Out.

As a result of this lack of hedging, according to the FDIC’s quarterly report for the quarter ending March 31, 2023, unrealized losses on securities at U.S. banks stood at the staggering sum of $515.5 billion.

The study on hedging is titled: Limited Hedging and Gambling for Resurrection by U.S. Banks During the 2022 Monetary Tightening? Its authors are Erica Jiang, Assistant Professor of Finance and Business Economics at USC Marshall School of Business; Gregor Matvos, Chair in Finance at the Kellogg School of Management, Northwestern University; Tomasz Piskorski, Professor of Real Estate in the Finance Division at Columbia Business School; and Amit Seru, Professor of Finance at Stanford Graduate School of Business.

END

3,Chris Powell of GATA provides to us very important physical commentaries

My estimation along with Alasdair Macleod is that China has accumulated over 50,000 tonnes of gold

(JanNieuwenhuijs)

Jan Nieuwenhuijs: Estimated Chinese gold reserves rise above 5,000 tonnes

Submitted by admin on Tue, 2023-09-05 13:58Section: Daily Dispatches

1:57p ET Tuesday, September 5, 2023

Dear Friend of GATA and Gold:

Gold researcher Jan Nieuwenhuijs, who has closely followed the gold market in China for many years, today provides his estimates of China’s official gold reserves and the amount of gold held by the country’s residents. It’s a lot in both respects.

Nieuwenhuijs’ analysis is headlined “Estimated Chinese Gold Reserves Cross 5,000 Tonnes” and it’s posted at the Gainseville Coins internet site here:

https://www.gainesvillecoins.com/blog/estimated-chinese-gold-reserves-cross-5000-tons

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Argentina, in dollar love affair, agonizes over divorcing the peso

Submitted by admin on Tue, 2023-09-05 21:48Section: Daily Dispatches

By Marc Jones, Eliana Raszewski, and Rodrigo Campos

Reuters

Tuesday, September 5, 2023

María Barro, a 65-year-old domestic worker in Buenos Aires, buys a few dollars each month with her peso salary, a hedge against Argentina’s persistent inflation now running at over 100% and a steady devaluation of the little-loved local peso.

The peso currency is now in the crosshairs of the country’s dark-horse presidential front-runner, libertarian radical Javier Milei, who has pledged to eventually scrap the central bank and dollarize the economy, Latin America’s third largest.

Milei — facing a tight three-way battle with traditional political candidates on the right and left ahead of an Oct. 22 vote — says savers like Barro underscore why Argentina should shed the peso.

“I try to buy dollars, no matter how little,” said Barro, who started to buy greenbacks on parallel markets in 2022 when 2,000 pesos got her $10. Now it would get her $2.70. “Pesos go like water and every day they are worth less.”

Barro supports the idea of a dollarized economy in theory but says she doesn’t like Milei’s aggressive style, which involves regular expletive-laced tirades against rivals and even the Pope. She is still undecided about her vote.

Milei’s dollarization plan has sharply divided opinion. His backers argue it is the solution to inflation near 115% while detractors say it an impractical idea that would sacrifice the country’s ability to set interest rates, control how much money is in circulation, and serve as the lender of last resort. …

… For the remainder of the report:

end

CHRIS POWELL.

A MUST READ..

How serious is the threat of gold confiscation?

Submitted by admin on Tue, 2023-09-05 23:02Section: Daily Dispatches

11:30p ET Tuesday, September 5, 2023

Dear Friend of GATA and Gold:

Doug Casey’s colleague at International Man, Jeff Thomas, today ruminates on the possibility that in a currency crisis, such as one prompted by an anti-U.S. bloc’s creation of a gold-backed currency, the U.S. government will resort to some form of confiscation of gold from investors.

After all, as Thomas notes, the United States has attempted confiscation before. In 1998 South Korea undertook a remarkably successful campaign to persuade its people to donate their gold to the government as a matter of patriotism to avert default on the country’s debt to the International Monetary Fund:

https://en.wikipedia.org/wiki/Gold-collecting_campaign

China may be providing for a similar emergency. As money manager Willem Middlekoop and others have noted, the Chinese government’s recent encouragement to its people to buy gold may be part of a policy of “storing gold with the people”:

Thomas writes: “If the U.S. and the European Union could come up with a large volume of gold quickly, they could issue a gold-backed currency themselves. It’s a simple equation: The more gold they have = the more backed notes they can produce = the more power they continue to hold. By seizing upon the private supply of their citizens, they would increase their holdings substantially in short order

“Either that or they could just give up their dominance of world trade and power. What would you guess their choice would be?

“It is entirely possible that the U.S. government (and very likely the EU) has already made a decision to confiscate. They may have carefully laid out the plan and have set implementation to coincide with a specific gold price.”

*

Maybe, but any currency purporting to be “gold-backed” would probably not gain much credence unless it was convertible to gold for whoever held it, or convertible somewhere, if only among governments. Otherwise what would “gold-backed” really mean except another confidence trick when confidence already has been lost?

In any case, the currency of any country with gold reserves is already “gold-backed.” For example, in its annual reports the Reserve Bank of Australia used to acknowledge candidly the market-rigging purpose of gold reserves, as in the RBA’s report for 2003.

“Foreign currency reserve assets and gold,” the report said, “are held primarily to support intervention in the foreign exchange market”:

The bank’s more recent annual reports, like last year’s —

— are not as explicit, subsuming gold with the bank’s “foreign reserves,” which “are held to give the bank the capacity to intervene in the foreign exchange market.” The bank adds reassuringly, “Such interventions occur rarely.” (You know — only when investors seem about to profit at the central bank’s expense.)

But it’s all plain enough. Any gold reserves are potentially backing for a currency, if there is convertibility somewhere — and the necessity for convertibility somewhere, if only among governments rather than investors, would seem to limit the potential for confiscation.

Thomas’ commentary is headlined “Don’t Dismiss the Possibility of Gold Confiscation” and it’s posted at the International Man site here:

For whatever it may still be worth, 16 years ago GATA went to the source about confiscation. We pestered the U.S. Treasury Department long enough to obtain a formal statement of policy.

Essentially the department replied that upon proclamation of an emergency by the president of the United States, pursuant to the Trading with the Enemy Act of 1917 and the International Emergency Economic Powers Act of 1977, the Treasury Department would have the power to seize or freeze any gold or silver or any gold- or silver-related asset, like shares of mining companies. But, the Treasury Department added, investors in the monetary metals shouldn’t get too paranoid about this, because pursuant to the same laws and proclamation, the department would claim the power to seize or freeze any damned thing it wanted to. (That’s not the anthem means when it comes to the part about “the land of the free and the home of the brave.”)

GATA’s correspondence with the Treasury Department about confiscation is here:

https://www.gata.org/node/5606

Nine years ago GATA noted that Australian law already provides for confiscation of gold and silver:

https://www.gata.org/node/13573

Other nominally democratic, free-market countries may have similar laws. Do they have citizens prepared to resist totalitarianism? Or could they be persuaded, as South Koreans seem to have been, that expropriation to compensate for government’s financial mismanagement is actually patriotism?

Maybe the first conclusion to be drawn from all this as government finances become more reckless is that people should amass as much monetary metal they can and then find a safe planet to keep it on. (Thanks if you can alert your secretary/treasurer to any such planets.)

This really isn’t investment advice — more like advice for life in an increasingly crazy world.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.3034

OFFSHORE YUAN: DOWN TO 7.3073

SHANGHAI CLOSED UP 3.71 PTS OR 0.12%

HANG SENG CLOSED UP 6.93 PTS OR 0.04%

2. Nikkei closed UP 204.26 OR 0.62%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 104.66 EURO RISES TO 1.0745 UP 20 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.645 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.42/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ON SHORE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.6215***/Italian 10 Yr bond yield UP to 4.333*** /SPAIN 10 YR BOND YIELD RISES TO 3.663…**

3i Greek 10 year bond yield RISES TO 3.899

3j Gold at $1926.30 silver at: 23.42 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 4 /100 roubles/dollar; ROUBLE AT 97.95//

3m oil into the 86 dollar handle for WTI and 89 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.42// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.645% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8900 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9562well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.295 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.361 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.949 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.82…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 3 BASIS PTS AT 4.574

end

2.a Overnight: Newsquawk and Zero hedge:

USA EARLY MORNING REPORT

Futures Stumble After German Factory Orders Collapse And Surging Oil Spark Stagflation Fears

WEDNESDAY, SEP 06, 2023 – 08:13 AM

US equity futures and global markets are lower this morning with bond yields and the USD flat as collapsing German eco data and elevated oil prices reignited stagflation concerns across the euro area. As of 7:45am, emini S&P and Nasdaq 100 futures were down 0.2%. The Bloomberg Dollar Spot Index edged higher along with the Japanese yen, while oil-linked currencies retreated as Brent crude dipped from 2023 highs; commodities are weaker with a sell-off in energy and metals complexes. Treasury yields were little changed in a lackluster day for bond markets. Gold fell for a second day, while Bitcoin climbed for the first time in three days.

In premarket trading, tech is underperforming; sentiment was dented by headlines that China’s government workers were told not to use iPhones. As a result, the world’s biggest company, AAPL, is trading -0.7% pre-mkt with MegaCap names all in the red; meanwhile keep an eye on the Huawei chip story. Yesterday’s Fedspeak was dovish, but we have three speakers today and four speakers tomorrow, so let’s see if the tone sharpens. Corporate mentions of ‘recession’ have fallen ~75% from their 22 Q2 peak and are now below their 5-yr average (62 vs. 82). Today’s macro data focus includes ISM Services, Beige Book, and Mortgage Applications (they dropped -2.9% after rising 2.3% last week).

The Stoxx 600 index retreated 0.7%, falling for the sixth straight session (see below) after German factory orders plummeted in July, showing that the woes of Europe’s biggest economy are continuing into the third quarter.

It also bears asking: with China and Europe imploding, just how much longer can the lie of US “economic growth” continue? Fears of stumbling growth and sticky inflation were also fanned by Brent crude prices holding just below $90 per barrel after the largest OPEC+ oil producers extended their supply cuts to year-end.

The collapsing economy in Europe and the ongoing economic collapse in China put pressure on equity futures in the US, if only for the moment, where signs are mounting that the Federal Reserve won’t cut interest rates any time soon. Because, you see, under the economic miracle of Bidenomics, the US can decouple from the rest of the world.

“The euro zone and UK are dabbling with recession, which markets had forgotten about three months ago,” said Rupert Thompson, chief economist at Kingswood Holdings. “It’s clear growth will head in the wrong direction in the coming months, which means equity markets will remain under downward pressure.”

Meanwhile, the soaring dollar forced Japan, whose yen may as well be renamed to lira, issued its strongest warning in weeks against rapid declines in the yen on Wednesday, with its top currency official saying the nation is ready to take action amid speculative moves in the market. The yen plumbed a 10-month low against the greenback. Shortly after, China’s central bank offered the most forceful guidance on record with its daily reference rate for the yuan, as the managed currency weakened toward a level unseen since 2007.

Going back to equity markets, European bourses are lower in a rather muted session, with the Stoxx 50 down 0.6% as stocks react to recent cross-asset moves. Banks are the main underperformers while other cyclical sectors such as miners and energy give up early strength. Real estate continues to trade well as the peak rate narrative in Europe continues to get traction (despite a slew of European Central Bank officials’ warning: don’t assume no action at next week’s meeting). The retrace higher in yields continues to get attention given the implications for equity valuations along with USD strength while the gap higher in oil risks fuelling a resurgence in global inflation. The UBS desk has been 60:40 better to buy on hedge fund demand in energy and semis while it has been a better seller of staples and telcos. It has also been active two-way in software with long-only buying and hedge-fund selling. Telcos are in focus following news of a stake build in Spain Telefonica. Here are the notable European movers:

- InPost gains as much as 11% as company reported 2Q earnings that beat expectations thanks to rising parcel volume, higher pricing in Poland and reduction of losses in UK

- Swiss Life rises as much as 3.1% after the life insurer reported 1H earnings analysts describe as “mixed,” praising the share buyback program but noting subdued real estate numbers

- Telefonica jumps as much as 3.7% after the government-backed Saudi Telecom Co. invested about $2.25b to snap up a nearly 10% stake in the Spanish telecommunications operator

- Halfords gains as much as 4.3% after the car parts and bicycle retailer reported revenue growth for the 20-week period to Aug. 18. A solid update with strong performance strong overall, Liberum says

- Clas Ohlson gains as much as 11.5% after the Swedish retail group reported better-than-expected first-quarter earnings, with Kepler Cheuvreux lauding the firm’s cost control and strong margins

- Bridgepoint rises as much as 3.3% after it announced a deal to add Energy Capital Partners which Morgan Stanley says is strategically consistent with previously identified aim to diversify capabilities

- European renewable-energy stocks fall, with an index tracking the sector hitting a three-year low, as sentiment further soured as Barclays initiated Vestas with an underweight rating

- Darktrace drops as much as 9.3% before paring losses after the UK cybersecurity company reported results that Jefferies analysts say show “strong underlying progress, but not without debate”

- Idorsia falls as much as 9.5% after the Swiss drug developer repurchased the rights for aprocitentan from Janssen Biotech, Jefferies says the deal removes some hopes Janssen would acquire the firm

- WH Smith drops as much as 6% after the UK newsagent and bookstore provided an update which RBC said was in line with expectations overall. Investec lowered its above-consensus estimates.

Earlier in the session, Asian stocks were mixed as losses in Chinese equities amid caution on the impact of government stimulus countered gains in Japan on a forex boost. The MSCI Asia Pacific Index fluctuated in a narrow range, with Tencent and Samsung among the biggest drags while Toyota and Sony provided support. Hong Kong and mainland China indexes were among the region’s worst performers as investors continued to monitor Beijing’s measures to stem the economic slide. That said, Chinese property developers notched dramatic gains on speculation that further stimulus is forthcoming.

- The Hang Seng and Shanghai Comp suffered from tech weakness but losses stemmed as developers surged on hopes of further support measures and with Sunac up by over 60% after its return to the Stock Connect; additionally, further support came via China’s Premier Li and reports of a Hong Kong Financial task force meeting.

- “The big trend for investors is to reduce exposure to Chinese equities, so every time there is some government measures to boost the market, people will sell into it,” said Vey-Sern Ling, managing director at Union Bancaire Privee. “That will be the case until we start to see positive impact from the measures, like better macro numbers and better housing sales.”

- Japan’s Nikkei 225 bucked the trend after it reclaimed the 33,000 status and with tailwinds from a weaker currency.

- Australia’s ASX 200 was dragged lower by tech and with most sectors pressured aside from energy which benefitted from the higher oil prices, while better-than-expected GDP data for Australia failed to inspire a turnaround.

- Key stock gauges in India extended their winning run to a fourth straight session, the longest such streak since mid-July, led by gains in consumer-focused companies and index major HDFC Bank. The S&P BSE Sensex rose 0.2% to 65,880.52 in Mumbai, while the NSE Nifty 50 Index advanced by a similar magnitude. The MSCI Asia Pacific Index was up 0.1% for the day. A gauge of consumer-focused companies on NSE climbed 0.8% on optimism for strong demand in the upcoming festive period in the country.

In FX, the US economy’s perplexing resilience has boosted the dollar, with conviction growing that the European Central Bank will hold off raising interest rates at its meeting next week. The Bloomberg Dollar Spot Index rises 0.1%, adding to Wednesday’s gain, and near a 5-1/2-month high against a basket of developed-market currencies after a run of seven weekly gains. The yen is off its best levels, having earlier benefited from some modest jawboning by the Japanese government. The euro got a brief boost from comments by ECB rate-setter Klaas Knot, who said markets may be underestimating the chances of a September interest-rate hike. “Our long-term view is that the dollar is overvalued, but for now cyclical pressures are in the other direction, so the pressure is for the dollar to strengthen,” said Thompson, who expects the ECB to hold rates steady next week.

In rates, treasuries held small gains as the US trading day begins, trimming yields from the highest levels in a week reached amid Tuesday’s corporate new-issue explosion and crude oil price jumping to YTD highs. Yields are lower across the curve by 1bp-2bp, 10-year around 4.25%, down from session high near 4.27%. Yields climbed 8bp-9bp Tuesday as 20 corporate borrowers raised a combined $36.2b, the most in a day since April 2020, reinforcing the reputation of the first trading day after US Labor Day as magnet for IG issuers; Nippon Life Insurance Co. has announced a benchmark-sized offering for Wednesday’s session. Focal points of US session include ISM services gauge at 10am New York time and comments by Boston Fed’s Collins at 8:30am.

In commodities, crude futures decline, with WTI falling 0.7% to trade near $86.10. Spot gold falls 0.1%. Goldman Sachs warned of upside risks to its end-year Brent target of $86 per barrel and UBS Global Wealth Management forecast Brent and US WTI benchmark to end the year at $95 and $91 per barrel, respectively.

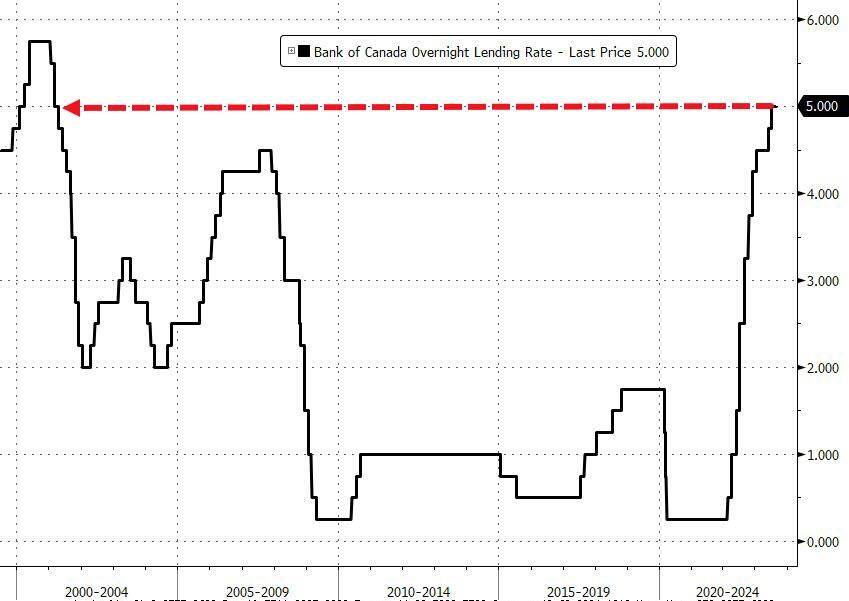

Looking to the day ahead now, and data releases include German factory orders for July, Euro Area retail sales for July, and the August construction PMIs from Germany and the UK. Over in the US, we’ll also get the ISM services index for August, the final services and composite PMIs for August, and the July trade balance. From central banks, the Bank of Canada will announce their latest policy decision, the Federal Reserve will release their Beige Book, and we’ll hear remarks from BoE Governor Bailey and the Fed’s Collins and Logan.

Market Snapshot

- S&P 500 futures down 0.2% to 4,492.00

- MXAP little changed at 162.86

- MXAPJ down 0.4% to 507.38

- Nikkei up 0.6% to 33,241.02

- Topix up 0.6% to 2,392.53

- Hang Seng Index little changed at 18,449.98

- Shanghai Composite up 0.1% to 3,158.08

- Sensex down 0.4% to 65,549.72

- Australia S&P/ASX 200 down 0.8% to 7,257.05

- Kospi down 0.7% to 2,563.34

- STOXX Europe 600 down 0.7% to 453.51

- German 10Y yield little changed at 2.63%

- Euro up 0.1% to $1.0733

- Brent Futures down 0.8% to $89.36/bbl

- Gold spot down 0.1% to $1,923.72

- U.S. Dollar Index little changed at 104.74

Top Overnight News

- China ordered officials at central government agencies not to use Apple’s iPhones and other foreign-branded devices for work or bring them into the office, people familiar with the matter said. The move by Beijing could have a chilling effect for foreign brands in China. Apple dominates the high-end smartphone market in the country and counts China as one of its biggest markets, relying on it for about 19% of its overall revenue. WSJ

- The White House is seeking detailed information on Huawei’s latest flagship smartphone, which analysts have described as an important milestone for the Chinese tech group four years after US restrictions crippled its handset business. FT

- Speculative bets that Chinese authorities will widen support for its property sector sent some of the country’s ailing developers surging by the most on record. Heavily indebted developers with depressed valuations were among those to rally the most, with Sunac China Holdings Ltd. soaring 68% alongside a spike in trading volume. China Evergrande Group closed up 83% — capping the biggest gain since its 2009 listing. BBG

- Xi was “reprimanded” over China’s current direction by retired party elders at a recent retreat, with a warning that the country can’t survive further turmoil. Nikkei

- Taiwan’s CPI for Aug overshoots the Street at +2.52% (up from +1.88% in Jul and ahead of the consensus +2.1% forecast), although the core number eases to +2.56% (down from +2.73% in July). BBG

- Universal Music has struck a deal to reshape the economics of music streaming, with changes aimed at directing more money to professional musicians and away from a “sea of noise” that chief executive Lucian Grainge has criticized this year. The world’s largest record company and the French streaming service Deezer have agreed an arrangement they expect will lift payouts to professional artists by 10 per cent, in the first big shift in the music streaming business model since the launch of Spotify in 2008. FT

- ECB officials warn markets that next week’s meeting outcome hasn’t been decided. ECB’s Knot warns markets not to underestimate the risk of a rate hike at next week’s meeting. RTRS / BBG

- Investors are warning hedge funds that they will face redemptions and further pressure to cut their fees unless they can improve their performance, highlighting the strain placed on the industry by a dramatic rise in global borrowing costs. FT

- Enbridge agreed to buy three utilities from Dominion Energy in a $9.4 billion deal to create North America’s largest natural gas provider. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly in the red following the subdued handover from Wall Street where sentiment was clouded by the higher yield environment, a stronger dollar and rising oil prices. ASX 200 was dragged lower by tech and with most sectors pressured aside from energy which benefitted from the higher oil prices, while better-than-expected GDP data for Australia failed to inspire a turnaround. Nikkei 225 bucked the trend after it reclaimed the 33,000 status and with tailwinds from a weaker currency. Hang Seng and Shanghai Comp suffered from tech weakness but losses stemmed as developers surged on hopes of further support measures and with Sunac up by over 60% after its return to the Stock Connect; additionally, further support came via China’s Premier Li and reports of a Hong Kong Financial task force meeting.

Top Asian News

- China’s Premier Li says they expect to achieve around the 5% economic growth target which was set earlier in the year.

- Chinese diplomat Liu said the US and China are major trading partners and that China opposes decoupling.

- US Commerce Secretary Raimondo said she does not expect any changes to Trump-era tariffs on China until the ongoing USTR review is completed, according to a CNBC interview.

- BoJ Board Member Takata said Japan’s economy is recovering moderately and Japan is seeing early signs of achieving 2% inflation, while he added that there is a sign of change in Japan’s trend inflation as rising wages push up inflation expectations. However, he believes the BoJ must patiently maintain easy policy given very high uncertainty on the outlook and noted that inflation is already exceeding the BoJ’s 2% target but there is some distance to achieving it stably and in a sustainable fashion.

- Japan Chief Cabinet Secretary Matsuno says it is important for FX to move stably reflecting fundamentals, sharp FX movers are undesirable. Will respond appropriately to FX moves if necessary, without ruling out any option.

European bourses are in the red, Euro Stoxx 50 -0.5%, in a similar fashion to the subdued APAC handover though performance for both regions lifted off lows towards the China close. Pressure in Europe also emanated from soft German data, though this comes with mitigating factors, and hawkish commentary from ECB’s Knot. Sectors are similarly lower aside from Telecom, where support stems from reports that Saudi’s STC has amassed a near-10% stake in Telefonica. Stateside, futures are also under pressure, ES -0.3%, but to a slightly lesser extent than the above action as the region is more tentative ahead of key US data and Central Bank speak. Apple (AAPL) iPhone and other foreign-branded devices have been banned in China for use by government officials at work, according to WSJ sources.

Top European News

- ECB’s Knot says markets may underestimate a September hike, via Bloomberg; the September decision will be a close call. A further hike is only a possibility and not a certainty. Advises caution against pessimism on the blocs economy. ECB inflation outlook won’t differ much from the last quarter.

- German Chancellor Scholz says to the Bundestag that he wants to propose a German pact to make the nation more fast, modern and secure. Will continue to promote the establishment of innovative firms such as chip factories. Rules out a debt-financed stimulus programme for Germany.

- Germany’s IFW sees 2023 German GDP -0.5% vs. prev. view of -0.3%, 2024 at +1.3% vs. prev. view +1.8% and 2025 at +1.5%.

FX

- DXY dips, but retains a firm underlying bid within 104.590-870 range irrespective of intervention.

- Yen pares losses vs. Buck after Japanese jawboning, but USD/JPY fails to breach 147.00 having peaked around 147.81.

- Euro underpinned against Buck as EGB/UST spreads converge, but EUR/USD capped ahead of 1.0750 and top of 2.53 bn expiry band starting at 1.0740.

- Aussie elevated near 0.6400 vs Greenback as Yuan rebounds from overnight lows sub-7.3200 in response to onshore and offshore intervention.

- Loonie lags pre-BoC as oil comes off the boil and Usd/Cad straddles 1.3650.

- PBoC set USD/CNY mid-point at 7.1969 vs exp. 7.3097 (prev. 7.1783)

- China’s major state-owned banks were seen withdrawing yuan liquidity in the offshore FX market and were seen selling dollars in the onshore spot FX market, according to sources cited by Reuters.

Fixed Income

- Bonds off worst levels in Europe before solid UK and German auctions, but Bunds and Gilts remain below par between 130.48-131.16 and 93.36-70 respective parameters.

- T-note idling within tight 110-05/109-29 band awaiting US trade data, services ISM, Fed speakers and latest Beige Book.

Commodities

- A session of consolidation for crude after Tuesday’s Russia and Saudi induced gains; WTI Oct’23 and Brent Nov’23 are lower by around USD 0.70/bbl having slipped through and tested the USD 86.00/bbl and USD 89.00/bbl figures respectively.

- Gas markets are attentive to the commencement of Australian LNG strikes on Thursday.

- While metals feature near unchanged performance for spot gold, base metals are softer but in a similar fashion to Chinese bourses that have lifted off lows.

- US Congress is set to sell off a 1mln bbl emergency reserve of gasoline which was created in the aftermath of Hurricane Sandy amid questions about the reserve’s usefulness, according to Bloomberg.

- Russian President Putin spoke by phone to Saudi Crown Prince MBS, according to Ria; both praised high-level of OPEC+ coordination.

Geopolitics

- India’s Foreign Minister said he doesn’t think the absence of Russian President Putin and Chinese President Xi from G20 has anything to do with India. Furthermore, he stated that G20 countries are negotiating to arrive at a consensus and have a declaration but added that there is a very sharp North-South divide and a sharper East-West polarisation.

US event Calendar

- 07:00: Sept. MBA Mortgage Applications -2.9%, prior 2.3%

- 08:30: July Trade Balance, est. -$68b, prior -$65.5b

- 09:45: Aug. S&P Global US Composite PMI, est. 50.4, prior 50.4

- 09:45: Aug. S&P Global US Services PMI, est. 51.0, prior 51.0

- 10:00: Aug. ISM Services Index, est. 52.5, prior 52.7

- 14:00: Federal Reserve Releases Beige Book

DB’s Jim Reid concludes the overnight wrap