GOLD PRICE CLOSED: DOWN $0.20 TO $1918.80

SILVER PRICE CLOSED: DOWN $0.21 AT $22.97

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1919.10

Silver ACCESS CLOSE: 22.97

Shanghai Gold Benchmark Price

USD oz  AM1983.16

AM1983.16

PM1984.71

Historical SGE Fix

New York price at the time: $1915.00

premium $70.00

xxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $25,706 UP 89 Dollars

Bitcoin: afternoon price: $25,877 UP 260 dollars

Platinum price closing $909.85 DOWN $4.30

Palladium price; $1218.00 UP $3.35

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,625.52 UP 11.50 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1538.68 UP 5.20 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1793.92 UP 6,21 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,918.100000000 USD

INTENT DATE: 09/06/2023 DELIVERY DATE: 09/08/2023

FIRM ORG FIRM NAME ISSUED STOPPED

323 H HSBC 4

363 H WELLS FARGO SEC 3

435 H SCOTIA CAPITAL 2

624 H BOFA SECURITIES 6

737 C ADVANTAGE 5 1

905 C ADM 11

TOTAL: 16 16

MONTH TO DATE: 3,616

JPMorgan stopped 0/16 contracts.

FOR SEPT.:

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2023. CONTRACT: 16 NOTICES FOR 1600 OZ or .0497 TONNES

total notices so far: 3616 contracts for 361,600 oz (11.247 tonnes)

FOR SEPT:

SILVER NOTICES: 49 NOTICE(S) FILED FOR 245,000 OZ/

total number of notices filed so far this month : 2339 for 11,695,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $0.20

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/SMALL CHANGES IN GOLD INVENTORY AT THE GLD: / A WITHDRAWAL OF 3.22 TONNES OF GOLD OUT OF THE GLD//

INVENTORY RESTS AT 886.69 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 21 CENTS AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE SLV:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 436.518 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC (AND T.A.S. ASSISTED) SIZED 2425 CONTRACTS TO 125,854 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.36 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. TAS ISSUANCE WAS A GOOD SIZED 588 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 588 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.36). AND WERE SUCCESSFUL IN KNOCKING SOME SILVER CONTRACTS AS WE HAD A HUGE SIZED LOSS OF 1789 CONTRACTS ON BOTH EXCHANGES ALONG WITH HUGE T.A.S.LIQUIDATION THROUGHOUT THE COMEX SESSION WHICH TOOK CARE OF MOST OF THE OI LOSS.

WE MUST HAVE HAD:

A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS( 620 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 14.420 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF 645,000 OZ//NEW TOTAL 12.810 MILLION OZ/// / //HUGE SIZED COMEX OI LOSS/ GOOD SIZED EFP ISSUANCE/VI) GOOD SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE (588 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL 16 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 4 days, total 2241 contracts: OR 11.205 MILLION OZ (560 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 11.205 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 11.205 MILLION OZ

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2425 CONTRACTS WITH OUR LOSS IN PRICE OF $0.36 IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD EFP ISSUANCE CONTRACTS: 620 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR SEPT OF 14.420 MILLION OZ FOLLOWED BY TODAY’S 645,000 OZ QUEUE JUMP. /// WE HAVE A HUGE SIZED LOSS OF 1805 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GOOD SIZED 588 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION. THE NEW TAS ISSUANCE WEDNESDAY NIGHT (588) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 49 NOTICE(S) FILED TODAY FOR 245,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1974 CONTRACTS TO 436,698 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: 140 CONTRACTS

WE HAD A FAIR SIZED INCREASE IN COMEX OI ( 1834 CONTRACTS) WITH OUR $8.80 LOSS IN PRICE//WEDNESDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 12.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 800 OZ QUEUE JUMP//NEW TOTAL STANDING 13.7356 TONNES + /A FAIR (AND CRIMINAL) ISSUANCE OF 1262 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR $8.80 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A TINY SIZED LOSS OF 117 OI CONTRACTS (0.3639 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1857 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 436,698

IN ESSENCE WE HAVE A TINY SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 117 CONTRACTS WITH 1974 CONTRACTS DECREASED AT THE COMEX// AND A FAIR 1857 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 117 CONTRACTS OR 0.3639 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1262 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1857 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (1974) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 117 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 12.656 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 800 OZ/// 3) ZERO LONG LIQUIDATION WITH HUGE TAS LIQUIDATION DURING THE COMEX SESSION //4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1262 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT :

TOTAL EFP CONTRACTS ISSUED: 9126 CONTRACTS OR 912,600 OZ OR 28.39 TONNES IN 4 TRADING DAY(S) AND THUS AVERAGING: 2281 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY(S) IN TONNES 28/39 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 28.39/3550 x 100% TONNES 0.788% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 28.39 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 2425 CONTRACTS OI TO 125,854 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A GOOD 620 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 620 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 620 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2425 CONTRACTS AND ADD TO THE 620 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1805 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 8.945 MILLION OZ

OCCURRED WITH OUR $0.36 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 35.72 PTS OR 1.13% //Hang Seng CLOSED DOWN 247.91 PTS OR 1.34% /The Nikkei CLOSED DOWN 249.94 PTS OR 0.75% //Australia’s all ordinaries CLOSED DOWN 1.13 % /Chinese yuan (ONSHORE) closed 7.3275 /OFFSHORE CHINESE YUAN DOWN TO 7.3392 /Oil UP TO 87.06 dollars per barrel for WTI and BRENT UP AT 90.18 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1974 CONTRACTS TO 436,698 WITH OUR LOSS IN PRICE OF $8.80 ON WEDNESDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1857 EFP CONTRACTS WERE ISSUED: : DEC 1857 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1857 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A TINY TOTAL OF 117 CONTRACTS IN THAT 1857 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 1974 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $8.80//WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A FAIR 1262 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (13.7356) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 13.7356 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $8.80) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A TINY GAIN OF 23 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A STRONG T.A.S. LIQUIDATION ON THE FRONT END OF WEDNESDAY’S TRADING. THE T.A.S. ISSUED ON WEDNESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 0.3639 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPT. (12.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 800 OZ//NEW STANDING 13.7356 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $8.80.

WE HAD – REMOVED 140 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET LOSS ON THE TWO EXCHANGES 117 CONTRACTS OR 11700 OZ OR 0.3639 TONNES.

Estimated gold volume today:// 112,887 awful

final gold volumes/yesterday 156,190 poor//speculators have left the gold arena

//SEPT 7/ /// THE SEPT. 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 96,227.940 OZ Brinks 2993 KILOBARS . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 16 notice(s) 1600 OZ .0497 TONNES |

| No of oz to be served (notices) | 800 contracts 80000 oz 2.480 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3616 notices 361600 OZ 11.247 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: nil oz

we had 1 customer withdrawals

i) Out of Brinks: 96,227.940 oz (2993 kilobars)

total withdrawals 96,227.940 oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER.

For the front month of SEPTEMBER we have an oi of 816 contracts having LOST 48 contracts. We had

56 contracts were served on WEDNESDAY, so we gained an additional 8 CONTRACTS or AN ADDITIONAL 800 oz will stand for delivery in this non active

delivery month of Sept.

Oct LOST 696 contracts to 27,418 contracts.

NOV. GAINED 5 CONTRACTS to stand at 5

December LOST 1530 contracts down to 375,978 contracts.

We had 16 contracts filed for today representing 1600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 16 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2023. contract month,

we take the total number of notices filed so far for the month (3616 x 100 oz ), to which we add the difference between the open interest for the front month of SEPT (816 CONTRACTS) minus the number of notices served upon today 16 x 100 oz per contract equals 441,600 OZ OR 13.7356 TONNES the number of TONNES standing in this non active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month: No of notices filed so far (3616) x 100 oz + (816) {OI for the front month} minus the number of notices served upon today (16) x 100 oz) which equals 441,600 oz standing OR 13.7356 TONNES

TOTAL COMEX GOLD STANDING: 13.7356 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,011,076.496 OZ 62.55 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,147,312.587 OZ

TOTAL REGISTERED GOLD 10 ,853.948.876 (337.60 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,293,363.711 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,843,355 OZ (REG GOLD- PLEDGED GOLD) 275.06 tonnes//dropping like a stone

END

SILVER/COMEX

SEPT 7

//2023// THE SEPT 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 719,197.360 oz Brinks CNT . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 606,969.000 o Loomis |

| No of oz served today (contracts) | 49 CONTRACT(S) (245,000 OZ) |

| No of oz to be served (notices) | 223 contracts (1,115,000 oz) |

| Total monthly oz silver served (contracts) | 2339 Contracts (11,695,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposit customer account:

i)Into Loomis: 606,969.000 oz

total customer deposits: 606,969.000 oz

JPMorgan has a total silver weight: 138.666 million oz/277.683 million or 50.03%

Comex withdrawals 2

i) Out of Brinks 118,961.460 oz

ii) Out of CNT: 660,235.900 oz

total: 719,197.360 oz

adjustments: 0

TOTAL REGISTERED SILVER: 43.769 MILLION OZ//.TOTAL REG + ELIGIBLE. 277.683 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF SEPT /2023 OI: 272 CONTRACTS HAVING GAINED 122 CONTRACT(S). WE HAD 7

CONTRACTS SERVED ON WEDNESDAY. SO WE GAINED 129 CONTRACTS OR 645,000 OZ WERE QUEUE JUMPED IN ORDER TO RECEIVE SOME METAL OVER HERE.

OCT GAINED 0 CONTRACTS TO STAND AT 1142.

NOVEMBER GAINED 8 CONTRACTS TO STAND AT 85

DEC. LOST 2613 CONTRACTS TO STAND AT 113,513 .

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 49 for 245,000 oz

Comex volumes// est. volume today 49,230 poor

Comex volume: confirmed yesterday 71,386 fair

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 2339 x 5,000 oz = 11,695,000 oz

to which we add the difference between the open interest for the front month of SEPT (272) and the number of notices served upon today 49x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2023 contract month: 2339 (notices served so far) x 5000 oz + OI for the front month of SEPT (272) – number of notices served upon today (49 )x 500 oz of silver standing for the SEPT contract month equates to 12.810 million oz.

There are 43.769 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

SEPT 7/WITH GOLD DOWN $0.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.22 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.69 TONNES

SEPT 6/WITH GOLD DOWN $8.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.81 TONNES

SEPT 5/WITH GOLD DOWN $13.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.97 TONNES

SEPT 1/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 31/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 30/WITH GOLD UP $8.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.59 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.23 TONNES

AUGUST 29/WITH GOLD UP 17.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.6 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.64 TONNES

AUGUST 28/WITH GOLD UP $6.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / //INVENTORY RESTS AT 884.04 TONNES

AUGUST 25/WITH GOLD DOWN $6.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 884.04 TONNES

AUGUST 24/WITH GOLD UP $0.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //INVENTORY RESTS AT 884.91 TONNES

AUGUST 23/WITH GOLD UP $21.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 4.32 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 884.91 TONNES

AUGUST 22/WITH GOLD UP $2.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.87 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 889.23 TONNES

AUGUST 21/WITH GOLD UP $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.60 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 890.10 TONNES

AUGUST 18/WITH GOLD UP $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 887.50 TONNES

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 16/WITH GOLD DOWN $7.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 15/WITH GOLD DOWN $7,45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 895.87 TONNES

AUGUST 14/WITH GOLD DOWN $2.10 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.75 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 899.63 TONNES

AUGUST 11/WITH GOLD DOWN $2.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 903.31 TONNES

AUGUST 10/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 9/WITH GOLD DOWN $8.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 8/WITH GOLD DOWN $9.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES FORM THE GLD /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 7/WITH GOLD DOWN $5.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///INVENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

GLD INVENTORY: 886.69 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 7/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 6/WITH SILVER DOWN 36 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.373 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 5/WITH SILVER DOWN 69 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 734,000 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 437.891 MILLION OZ

SEPT 1/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 440.00 MILLION OZ

AUGUST 31/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 438.625 MILLION OZ

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.834 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 443.210 MILLION OZ

AUGUST 29/WITH SILVER UP 49 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 183,000 OF SILVER INTO THE THE SLV// /.////INVENTORY RESTS AT 445.044 MILLION OZ

AUGUST 28/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.281 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 444.861 MILLION OZ

AUGUST 25/WITH SILVER UP ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 446.145 MILLION OZ

AUGUST 24/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.651 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 448.896 MILLION OZ

AUGUST 23/WITH SILVER UP 94 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FROM THE SLV// /.////INVENTORY RESTS AT 450.547 MILLION OZ

AUGUST 22/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: /.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 21/WITH SILVER UP 59 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 917,0000 OZ FROM THE SLV//.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 18/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 16/WITH SILVER DOWN 13 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 15/WITH SILVER DOWN 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 14/WITH SILVER DOWN 3 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.459 MILLION OZ INTOTHE SLV/: //////INVENTORY RESTS AT 452.565 MILLION OZ

AUGUST 11/WITH SILVER DOWN 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.926 MILLION OZ INTOTHE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 452.106 MILLION OZ

AUGUST 10/WITH SILVER UP 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 9/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 8/WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 7/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

CLOSING INVENTORY 436.518 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

3,Chris Powell of GATA provides to us very important physical commentaries

Because the yen is closing at its all time low, the price of gold in Yen is reaching its all time high

(London’s Financial Times)

Inflation worries fuel Japanese rush to buy gold

Submitted by admin on Wed, 2023-09-06 11:33Section: Daily Dispatches

By Leo Lewis and David Keohane

Financial Times, London

Tuesday, September 5, 2023

The retail price of gold in Japan has jumped to an all-time high as the yen extends its historic slide against the U.S. dollar and cash-laden households rush to find a hedge against inflation.

Buying of yen-denominated gold at the nation’s largest dealer has driven the price of the yellow metal above the Y10,000-per-gramme level for the first time in recent days. It was trading at Y10,100 today, according to retail prices published by Tanaka Kikinzoku, one of Japan’s largest gold retailers.

The retail gold price in Japan — the main reference price for the metal in the country — tracks global spot prices, which have been pushed up by the coronavirus pandemic, the war in Ukraine, and tensions between China and the U.S. It also reflects a sharp fall this year in the yen, which recently passed Y146.5 against the dollar — a level that last year triggered verbal market intervention by the Japanese authorities. …

… For the remainder of the report:

https://www.ft.com/content/f7a5f1fb-7882-4c43-975d-05b06518334c

end

Ted Butler: Silver is a sure thing

Submitted by admin on Wed, 2023-09-06 18:40Section: Daily Dispatches

By Ted Butler

SilverSeek.com

Tuesday, September 5, 2023

I have contended for nearly 40 years that silver has been manipulated and suppressed in price by means of excessive short selling on the Comex, mostly by commercial traders which happen to be mostly banks. As a result of this decades-long price suppression, the law of supply and demand has become artificially distorted. The low price has reduced supply and current production and increased demand (both industrial and investment) to the point where a wholesale physical shortage has emerged.

Since a physical shortage is the most bullish circumstance possible in any commodity, it stands to reason one should expect silver prices to climb sharply to address the deepening silver shortage – thus, the high degree of bullishness I have expressed.

But it is not enough to be extremely bullish. Proper appreciation must be given to the past 40 years of price suppression. To see where the price of silver is headed, one must understand the mechanics of the Comex price suppression.

The reason why I’m so bullish on silver at this time is because I think the big commercials won’t add to short positions aggressively on the next silver rally. That they won’t add aggressively to shorts someday is a certainty and what makes it a certainty is the deepening physical supply/demand shortage. That’s why I’m so bullish that I am jumping out of my skin.

We are getting close to the point where futures contract positioning on the Comex, which has been the sole determinant for the price suppression in silver for 40 years, is about to run its course as the main price influence. …

… For the remainder of the analysis:

https://silverseek.com/article/silver-sure-thing

* * *

Silver: A Sure Thing?

September 06, 2023

Ted Butler

I have contended for the past near-40 years, that silver has been manipulated and suppressed in price by means of excessive short selling on the COMEX, mostly by commercial traders which happen to be mostly banks. As a result of this decades-long price suppression, the law of supply and demand has become artificially distorted. The low price has reduced supply and current production and increased demand (both industrial and investment) to the point where a wholesale physical shortage has emerged.

Since a physical shortage is the most bullish circumstance possible in any commodity, it stands to reason one should expect silver prices to climb sharply to address the deepening silver shortage – thus, the high degree of bullishness I’ve expressed. But it is not enough to be extremely bullish. Proper appreciation must be given to the past 40 years of price suppression. To see where the price of silver is headed, one must understand the mechanics of the COMEX price suppression.

The reason why I’m so bullish on silver at this time is because I think the big commercials won’t add to short positions aggressively on the next silver rally. Knowing that they won’t add aggressively to shorts someday is a certainty and what makes it a certainty is the deepening physical supply/demand shortage. That’s why I’m so bullish that I am jumping out of my skin.

We are getting close to the point where futures contract positioning on the COMEX, which has been the sole determinant for the price suppression in silver for 40 years, is about to run its course as the main price influence. Should the big commercial shorts on the COMEX stand aside from aggressively adding to short positions, it means the game has changed and physical investment demand and industrial user inventory stockpiling will set prices. That’s when you are really going to have to hold on to your hats.

There is growing evidence that a physical “run” on silver is already underway in the silver ETFs, led by SLV, the largest, but also in other silver ETFs. This also involves the PSLV, with a withdrawal of 1.7 million ounces. There can be no doubt that silver is leaving the SLV and other silver ETFs. In the prior week, more than 6 million ounces came out of SLV, with this week’s withdrawals topping 7 million ounces in SLV alone, plus more in other silver ETFs. At a time of a fairly strong price rally, it is highly counterintuitive for any silver to be leaving, as strong prices usually lead to deposits in SLV.

The standout, by far, in last week’s silver COT report was the refusal of the big 4 and big 8 commercial shorts to add new short positions and, in fact, their buyback of short positions on what was a sharp silver rally. And with the deepening and obvious physical silver shortage picking up steam every day, there is not the slightest suggestion these big shorts should want to add shorts at a time of the first genuine physical silver shortage in history.

The net result of 40 years of illegal speculative price determination and suppression on the COMEX has resulted in a physical silver shortage for the first time in history. You can see the evidence of the shortage all around, if you know where to look – like in the physical turnover in the COMEX silver warehouses and the bleeding of physical silver from the silver ETFs. At some point in the near future, the physical shortage will become so pronounced that it will overwhelm the sole price determinant until now – paper positioning on the COMEX.

The Code Red market emergency that I started writing about in July is very much in full force and about to make its presence felt. The prospects of a price explosion are now better than ever, thanks to the unmistakable deepening physical shortage and the likely continued refusal of the 4 and 8 big shorts to add aggressively to short positions. That silver will explode in price in the not-too-distant future looks like a sure thing. Don’t let any last-minute price smashes scare you out of silver positions, as such rigged downdrafts would appear to be the tail-end of a 40-year epic silver price manipulation.

(For those long-time readers, yes, I have used the title “A Sure Thing?” before, including back on Nov 18, 2008, when silver was close to $9 and would find itself close to $50 two and a half years later).

Ted Butler

September 6, 2023

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES//BIX WEIR

| Bix Weir | 12:59 PM (27 minutes ago) | ||

| to me | |||

| The FDIC is so afraid of the losses on the books of the banks that they made the decision to REMOVE the silver on “Unrealized Losses” during their quarterly presentation! What is showed was a REVERSAL of the trend that things were getting better! $50B more losses in Q2 than Q1 and Q3 is looking even WORSE! ALERT! FDIC White Washes Bank Q2 “Unrealized Losses” So You Don’t PANIC!! Q3=BIG TROUBLE! (Bix Weir)https://youtu.be/dkT6d-B_7GU |

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

Sam Bankman-Fried Loses Appeal To Be Released From Brooklyn Jail

WEDNESDAY, SEP 06, 2023 – 05:45 PM

Less than a month after disgraced former crypto billionaire, Sam Bankman-Fried’s bail was revoked and he was thrown in prison – where his vegan diet and supplies of Adderall were replaced with water, bread and peanut butter – on Wednesday afternoon the crypto fraudster who desperately tried to bribe every Democrat he could find (and almost succeeded), lost an appeal asking to released from a Brooklyn jail after complaining he cannot properly prepare for his trial over the collapse of his FTX cryptocurrency exchange.Sam Bankman-Fried leaving Manhattan Federal Court on July 26

In rejecting Bankman-Fried’s request, the 2nd U.S. Circuit Court of Appeals in Manhattan nonetheless said it would ask the next available three-judge panel to consider it.

As we reported on Aug 11, U.S. District Judge Lewis Kaplan revoked Bankman-Fried’s $250 million bail after finding that the former billionaire likely tampered with witnesses at least twice. Bankman-Fried quickly appealed, arguing he would be unable to “properly prepare” for his scheduled Oct. 3 trial from behind bars.

Prosecutors, who accused the 31-year-old of stealing billions from FTX customers to plug holes at his Alameda Research hedge fund – pushed for Bankman-Fried to be jailed after he shared the personal writings of Caroline Ellison, Alameda’s former chief executive and his onetime romantic partner, with a New York Times reporter.

Bankman-Fried has pleaded not guilty to fraud and conspiracy charges, and said he shared Ellison’s writings to defend his reputation, not to intimidate her.

Ellison is cooperating with prosecutors and will testify against him.

According to Reuters, in court papers on Tuesday, Bankman-Fried’s lawyers said the arrangement to give him several hours a day to review evidence on a laptop at the Metropolitan Detention Center in Brooklyn has proven inadequate.

They said he “lost more than four hours on Friday when he had to return to his cell for a prisoner count, and lost more time over the weekend” and let’s not even mention the fact that SBF’s Brooklyn prison is hardly known for serving the 3-Michelin star vegan meals SBF has grown accustomed to.Sam Bankman-Fried at a hearing on Aug. 22.

The U.S. Attorney’s office in Manhattan said the jail has authorized Bankman-Fried’s purchase of a second laptop.

Bankman-Fried’s lawyers have not sought to delay the trial. Kaplan said last week that he would consider such a request.

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.3275

OFFSHORE YUAN: DOWN TO 7.3392

SHANGHAI CLOSED DOWN 35.72 PTS OR 1.13%

HANG SENG CLOSED DOWN 247.91 PTS OR 0.75%

2. Nikkei closed DOWN 249.94 OR 1.34%

3. Europe stocks SO FAR: ALL MIXED

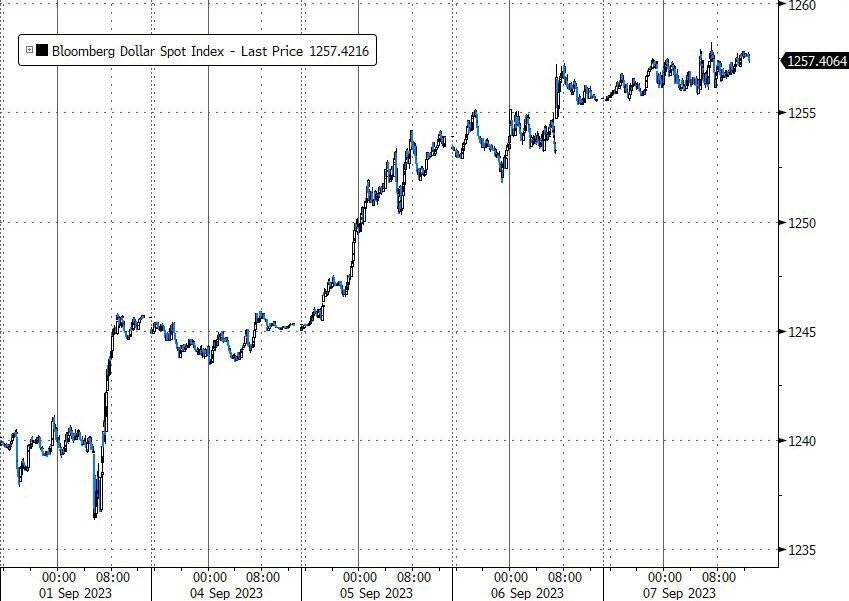

USA dollar INDEX UP TO 104.95 EURO FALLS TO 1.0705 DOWN 18 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.643 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.32/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ON SHORE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.6345***/Italian 10 Yr bond yield UP to 4.354*** /SPAIN 10 YR BOND YIELD RISES TO 3.670…**

3i Greek 10 year bond yield RISES TO 3.960

3j Gold at $1921.75 silver at: 23.02 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 10 /100 roubles/dollar; ROUBLE AT 98.04//

3m oil into the 87 dollar handle for WTI and 90 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.32// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.643% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8925 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9555well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

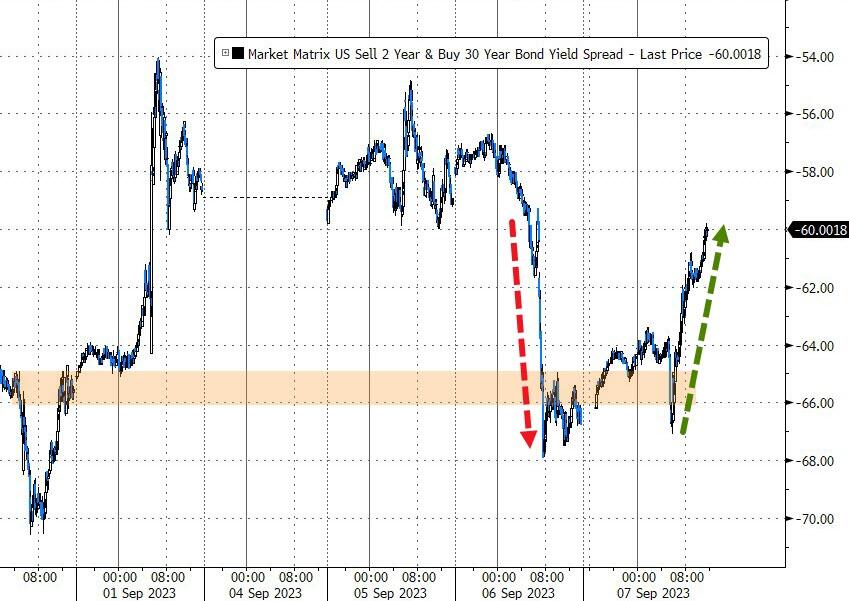

USA 10 YR BOND YIELD: 4.278 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.360 DOWN 0 BASIS PTS/

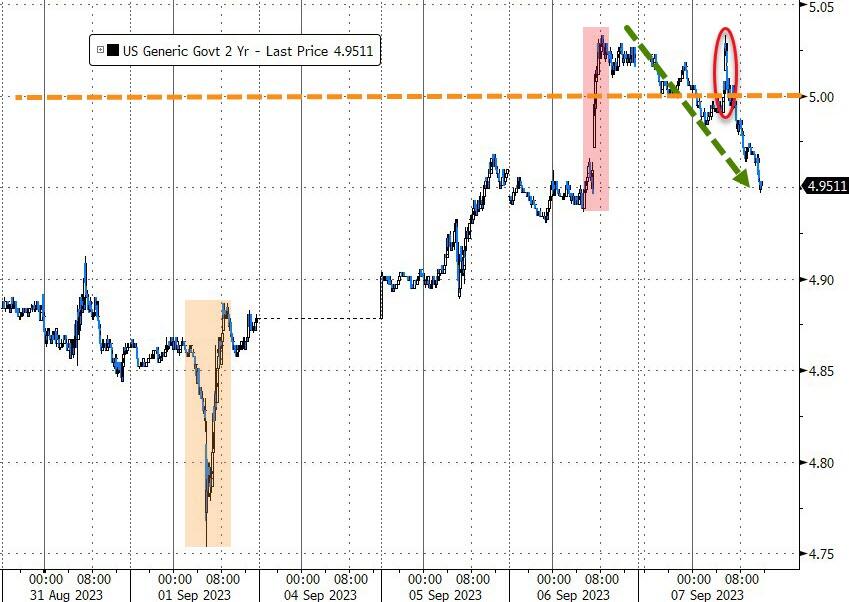

USA 2 YR BOND YIELD: 5.001 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.83…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 5 BASIS PTS AT 4.526

end

2.a Overnight: Newsquawk and Zero hedge:

USA EARLY MORNING REPORT

Futures Slide, Apple Tumbles After China Broadens iPhone Ban, Dollar Surges Slamming Yuan To 16 Year Low

THURSDAY, SEP 07, 2023 – 08:14 AM

US stocks futures slumped, led by tech shares as Apple tumbled another 3% in premarket trading after Bloomberg reported that China – Apple’s biggest foreign market and global production base -seeks to expand a ban on the use of iPhones in sensitive departments to government-backed agencies and state companies. As of 730am ET, S&P futures were down 0.4%, while Nasdaq futures tumbled 0.7% as a 2% drop in Nvidia added to Apple’s woes. The dollar climbed to a six-month high and the yuan tumbled to the lowest level since 2007 as investors ramped up bets on further Fed policy tightening. Bond yields are lower, following the decline in European yields; commodities are also mostly lower with a modest decline in oil prices. Today, we get jobless claims data (exp. 234K, vs 228 prior), QSS and the revisions to Nonfarm Productivity and Unit Labor Costs. Keep an eye on the bond market moves following claims data. Fed’s Harker, Williams, Bostic, and Logan will speak today.

In premarket trading, all eyes are on Apple, which has tumbled by 3% or more for a second session. As Market Ear notes, that means Apple has gone from trading “well” above the 50 day moving average, to trading below the 100 day in 2 sessions. We haven’t seen that in a long time. Note the 200 day is down at 164-ish at the moment.

Nvidia was the other big mover, falling 2.1%, and putting the stock on track for a second session of steep losses, as a weak start to September is making for the worst monthly decline since last December. The entire AI space seems to be having indigestion as C3.ai – with the famous AI stock ticker0 fell 9.6% after the artificial intelligence software company gave a tepid revenue forecast and said that profitability will take longer than expected. Here are some other notable premarket movers:

- ChargePoint fell 10% after the electric-vehicle charging company forecast revenue for the third quarter that missed the average analyst estimate.

- UiPath shares rose 4.8% after the robotic process automation software company reported second-quarter results that beat expectations and gave an outlook. RBC highlighted profitability as a highlight of the report.

- Yext shares slump 15% after the infrastructure-software company’s third-quarter revenue forecast came in below the average analyst estimate at the midpoint.

Stock moves aside, the Bloomberg Dollar Spot Index is on track for an eighth consecutive week of gains, which would be the longest ever run of increases in data going back to 2005. Signs that the US economy is headed for a soft landing are bolstering bets that the Fed will keep borrowing costs higher for longer, which would burnish the greenback’s appeal.

The surging dollar pushed the USDCNY up 0.1% to 7.3275 with the onshore yuan hitting a 16-year low against the dollar as pessimism around China’s economy builds; export data showed China’s trade slump eased in August

The dollar’s enduring strength has been at the forefront of the market narrative this week, with investors focusing on a string of economic reports that underscore robust US growth while Europe and China weaken. In fact, one can argue that the seasonally adjusted and goalseeked (in bold) US data has made Bidenomics decouple from the rest of the world, in what is one giant political stunt. When reality – and seasonal unadjustments – finally reasserts, watch as US econ data craters in the coming weeks and sends the dollar collapsing.

Meanwhile, the euro sank on data showing German industrial output declined, while the Chinese yuan dropped to a 16-year low in onshore trading.

“You are seeing a clear slowing in growth outside the US so in that context the dollar will do well, especially as you also have ongoing Fed hawkishness,” said Peter Kinsella, head of global currency strategy at asset manager Union Bancaire Privee Ubp SA.

Meanwhile, European stocks erased most of an earlier decline but were still red, as some luxury stocks bounced back and drugmakers rose. The Stoxx Europe 600 fell 0.2% putting the benchmark on course for a seventh consecutive day of losses, in what would be the longest losing streak since February 2018. Here are the most notable European movers:

- Direct Line shares jump as much as 18%, the most on record, after the insurer agreed to sell its brokered commercial insurance business lines to RSA. The asset sale removes the risk of a potential equity raise, according to Citi.

- Jet2 shares gain as much as 8.4%, the most intraday since November, after the UK holiday firm said that it’s on track to exceed current market expectations for profit before foreign exchange revaluations and tax for the year.

- Melrose Industries shares rise as much as 8.9%, the most in more than four months, after the investment firm reported first-half earnings that JPMorgan said beat its expectations and prompted an upgrade to its estimates.

- Tod’s shares gain as much as 5.8%, before trimming their advance, after the Italian luxury shoemaker reported first-half earnings that beat estimates. Mediobanca notes an “outstanding” margin improvement, with the update showing the results of a revamp for the group’s brands.

- Synthomer slides as much as 33% in London trading after the UK-based maker of additives for adhesive products reported a first-half pretax loss and proposed a 6-for-1 rights issue to cut leverage and avoid the risk of breaching debt covenants. Barclays says the rights issue will be heavily dilutive.

- Shares in UK veterinary services company CVS Group tumble as much as 35%, the most in more than four years, while retailer Pets at Home plunges as much as 13% after the country’s Competition and Markets Authority launches a review of the vet sector.

- STMicro and other European chip stocks fell after Bloomberg reported that China plans to expand a ban on the use of iPhones to government-backed agencies and state companies.

Asian equities closed lower, with Chinese stocks among the worst performers, weighed down by property developers. The MSCI Asia Pacific Index slid 0.7%, set for a third day of losses. Tech was the worst performing sector as solid US data overnight spurred bets for further Federal Reserve tightening. The materials sector was also a major drag as Australia’s largest mining stock BHP Group traded ex-dividend. Almost all equity benchmarks in the region were in the red, with the Bloomberg dollar index rising to a fresh six-month high. Focus was also on China’s developer stocks, which rallied Wednesday as bets for further policy support drove speculative buying. The sector retreated Thursday, weighing on the broader Chinese and Hong Kong market. South Korean and Australian indexes slide, while Japanese stocks nurse smaller losses.

- Hang Seng and Shanghai Comp conformed to the downbeat mood as the latest Chinese trade data showed a continued contraction in the nation’s exports and imports but was not as bad as feared, while tech stocks were pressured by frictions after the FCC chair asked US government agencies to address the threat posed by Chinese cellular connectivity modules and a lawmaker called for an investigation into SMIC for potentially violating US sanctions by supplying components to Huawei. Furthermore, China reportedly banned government officials from using iPhones at work and was said to be seeking to extend this to state firms and agencies.

- Australia’s ASX 200 was dragged lower by underperformance in the commodity-related sectors and amid the key data from Australia’s largest trade partner.

- Japan’s Nikkei 225 swung between gains and losses with early support from currency weakness and reports that Japan will put together economic measures around October, although the index eventually succumbed to the selling pressure.

- Indian stocks extended their winning streak to a fifth day, the longest such stretch since mid-July, led by a rally in banks and Larsen & Toubro and triggering confidence among one set of derivatives participants that the guage is set to retest record highs. The S&P BSE Sensex rose 0.6% to 66,265.56 in Mumbai, while the NSE Nifty 50 Index advanced by a similar measure to 19,727.05. Infrastructure giant Larsen & Toubro closed at a record high after rising more than 4% on report that it is likely to win an order worth nearly $3 billion from Saudi Aramco. A sub-gauge of bank stocks saw a late rally led by Axis Bank, HDFC Bank and ICICI Bank.

In FX, the Bloomberg Dollar Spot Index gained 0.1%, heading for its third day of gains and the highest level since March, and record 8th straight week of increases, after US economic data reinforced the case for more monetary tightening. Money-market pricing indicates a 50% chance of a 25 basis point hike at the Federal Reserve’s November meeting; a 60% chance was briefly priced after the release of the ISM survey on Wednesday.

- USD/CNY climbed 0.1% to 7.3275 with the onshore yuan hitting a 16-year low against the dollar as pessimism around China’s economy builds; export data showed China’s trade slump eased in August

- EUR/USD slid 0.1% to 1.0715 after German industrial output fell for the third month in July, spelling concern around Europe’s biggest economy.

- GBP/USD is also underperforming its G-10 rivals, falling 0.3% versus the greenback. Data showing a notable drop in UK house prices and falling inflation expectations in a BOE survey have both played their part.

In rates, Treasuries were slightly richer across the curve, with gains led by front-end as 2-year yields edge back below 5%, following a wider bull-steepening rally in gilts. Front-end yields were richer by 2bp-3bp, with 2s10s and 5s30s steeper by 1bp-2bp; US 10-year around 4.27%, about 1bp richer on the day, with bunds and gilts outperforming by 1.5bp and 6bp in the sector. Gilts lead core European bonds higher, with UK yields richer by 9bp to 6bp across the curve in sharp bull- steepening in early London session. Dollar IG issuance slate includes Slovenia 10Y and five other names; 10 issuers priced a combined $14.4b Wednesday, a day after 20 companies raised $36.2b; issuers paid about 10bps in new-issue concessions, driven by order books that were 2.5 times oversubscribed. US economic data includes 2Q final nonfarm productivity and initial jobless claims (8:30am New York time)

In commodities, crude futures declined, with WTI falling 0.7% to trade near $86.90. Spot gold adds 0.2%.

Bitcoin is essentially flat on the session in a continuation of the recent relatively rangebound performance after last week’s much more pronounced action. BTC currently holding above 25.7k, in tight parameters of circa. USD 200.

Looking to the day ahead now, and data releases include German industrial production and Italian retail sales for July, whilst in the US we’ll get the weekly initial jobless claims. From central banks, we’ll hear from the Fed’s Harker, Goolsbee, Williams, Bostic, Bowman and Logan, the ECB’s Wunsch, Holzmann, Villeroy, Knot and Elderson, as well as BoC Governor Macklem. We’ll also get the BoE’s decision maker panel survey.

Market Snapshot

- S&P 500 futures down 0.4% to 4,455.75

- MXAP down 0.7% to 161.72

- MXAPJ down 0.9% to 503.15

- Nikkei down 0.8% to 32,991.08

- Topix down 0.4% to 2,383.38

- Hang Seng Index down 1.3% to 18,202.07

- Shanghai Composite down 1.1% to 3,122.35

- Sensex up 0.3% to 66,059.18

- Australia S&P/ASX 200 down 1.2% to 7,171.01

- Kospi down 0.6% to 2,548.26

- STOXX Europe 600 down 0.2% to 453.45

- German 10Y yield little changed at 2.62%

- Euro down 0.1% to $1.0711

- Brent Futures down 0.2% to $90.43/bbl

- Gold spot up 0.1% to $1,919.04

- U.S. Dollar Index little changed at 104.94

Top Overnight News

- 1) China’s trade numbers come in slightly better than feared as signs of growth stabilization emerge – exports dropped 8.8% Y/Y (vs. the Street’s -9% forecast and vs. -14.5% in Jul) while imports fell 7.3% (vs. the Street’s -9% forecast and vs. -12.4% in Jul). RTRS

- 2) China plans to expand a ban on the use of iPhones in sensitive departments to government-backed agencies and state companies, a sign of growing challenges for Apple Inc. in its biggest foreign market and global production base. BBG

- 3) The U.S. Commerce Department should end all technology exports to Huawei and China’s top semiconductor firm following the discovery of new chips in Huawei phones that may violate trade restrictions, the chair of the House of Representatives’ committee on China said. RTRS

- 4) Five of China’s major state banks said they will start to lower interest rates on existing mortgages for first-home loans, part of a series of support measures announced by Beijing in recent weeks. RTRS

- 5) A sharp decline in car making fueled a deepening downturn in German industry as production fell for the third consecutive month in July, intensifying pressure on the government to do more to lift the economy out of the doldrums. The 0.8 per cent month-on-month decline reported by Germany’s statistical office exceeded the 0.5 per cent fall forecast by economists. FT

- 6) US and EU are near a deal to resolve a steel tariff dispute and impose new tariffs aimed at curbing excess steel production in China and elsewhere. BBG

- 7) US crude inventories fell by 5.5 million barrels last week, the API is said to have reported. That would bring total holdings to the lowest in nine months if confirmed by the EIA today. Supplies at Cushing declined, while those of gasoline tumbled by more than 5 million — the most in more than five months. BBG

- 8) Disney & Comcast have agreed to accelerate the timeline for Disney to buy Comcast’s stake in Hulu (the goal is to strike a deal by the end of the month, and Comcast says it will direct the proceeds towards accelerated buybacks). Barron’s

- 9) Boaz Weinstein and his group of bidders revised their offer for Sculptor to include beefed up equity commitments and eliminated debt financing risks, people familiar said. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were pressured as the region took its cue from the losses stateside where stocks and bonds declined in the aftermath of hawkish ISM Services data, while participants also digested the latest Chinese trade data. ASX 200 was dragged lower by underperformance in the commodity-related sectors and amid the key data from Australia’s largest trade partner. Nikkei 225 swung between gains and losses with early support from currency weakness and reports that Japan will put together economic measures around October, although the index eventually succumbed to the selling pressure. Hang Seng and Shanghai Comp conformed to the downbeat mood as the latest Chinese trade data showed a continued contraction in the nation’s exports and imports but was not as bad as feared, while tech stocks were pressured by frictions after the FCC chair asked US government agencies to address the threat posed by Chinese cellular connectivity modules and a lawmaker called for an investigation into SMIC for potentially violating US sanctions by supplying components to Huawei. Furthermore, China reportedly banned government officials from using iPhones at work and was said to be seeking to extend this to state firms and agencies.

Top Asian News

- China seeks to broaden the Apple (AAPL) iPhone ban to state firms and agencies, according to Bloomberg.

- FCC chair asked US government agencies to address the threat posed by Chinese cellular connectivity modules and to consider adding Chinese firms Quectel and Fibocom to the list of companies posing national security risks.

- US House Speaker McCarthy said China has the responsibility to repair relations with the world. It was also reported that the US Ambassador to Japan said Japan has done everything right according to science regarding the Fukushima water release and that is in direct contrast with what China has done during the COVID pandemic.

- China’s Big 4 banks adjusted rates for some existing first-home mortgages, according to Reuters.

- Chinese Premier Li says China will further open up and offer bigger market for countries including Australia; both side should properly handle differences in spirit of mutual respect

European bourses spent the morning in the red but have benefitted from a broader yield-induced pick up in sentiment, Euro Stoxx 50 +0.2%. Sectors are now mainly in the green, outperformance in Utilities whilst Basic Resources and Tech continue to lag. On Tech, the sector is impaired by marked pre-market downside in Apple -2.7%, following reports of a further crackdown by China in iPhones. Action which is also affecting US futures, ES -0.2% and NQ -0.5%; though, they are off lows given the mentioned influence of yields and as attention turns to the busy afternoon docket.

Top European News

- BoE Monthly Decision Maker Panel data – August 2023: One-year ahead CPI inflation expectations decreased to 4.8% in August, down from 5.4% in July. Three-year ahead CPI inflation expectations decreased slightly to 3.2% in August, down 0.1 percentage points relative to July. Expected year-ahead wage growth remained the same at 5.0% on the month in August, and the three-month moving average decreased slightly by 0.1 percentage points to 5.1%.

- German IFO Institute maintains its 2023 GDP forecast at -0.4%, whilst lowering its 2024 forecast to +1.4% from +1.5%

FX

- Dollar eases off post-ISM peaks and trades mixed vs peers pre-IJC and more Fed speak, DXY confined to 104.980-800 range.

- Sterling suffers after drop in UK house prices and DMP 1 year inflation expectations, Cable below 1.2500 and Fib support at one stage.

- Euro defends 1.0700 vs Greenback again and aided by 1.85bln option expiries.

- Kiwi regains composure and sight of 0.5900 against Buck as NZ manufacturing sales rebound.

- Yen benefits from retreat in US Treasury yields and bounces from 147.87 to 147.37.

- Aussie draws encouragement from not so weak Chinese imports and exports, AUD/USD closer to 0.6400 than 0.6350.

- PBoC set USD/CNY mid-point at 7.1986 vs exp. 7.3121 (prev. 7.1969)

Fixed Income

- Gilts correct higher and overtake debt peers on UK specifics including weak data and a decline in inflation expectations.

- 10 year bond extends from 93.78 to 94.44, while Bunds and T-note lag within 130.35-87 and 109-21/29 respective ranges.

- OATs and Bonos bid after somewhat mixed French and Spanish auctions, BTPs underpinned ahead of new Valore issuance due in early October.

- Italian Treasury offers a new issue of the BTP Valore from October 2nd-6th, five year maturity.

Commodities

- Another session of consolidation for the crude benchmarks, continuing Wednesday’s pullback, despite bullish inventory data and Saudi lifting its Asia OSPs, with markets broadly looking to Fed speak and US data points.

- Strike action at Chevron’s LNG facilities in Australia has been pushed back from the scheduled start of today until Friday.

- Spot gold is benefitting from the subdued risk tone ahead of data and Fed speak while base metals pullback in-line with APAC trade despite better-than-feared Chinese trade figures.

- US Energy Private Inventory Data (bbls): Crude -5.5mln (exp. -2.1mln), Gasoline -5.1mln (exp. -1mln), Distillate +0.3mln (exp. +0.2mln), Cushing -1.4mln.

- Texas declared a grid emergency as the heat stoked demand for power, while it warned that rolling blackouts may be needed amid grid emergency, according to Reuters.

US Event Calendar

- 08:30: Aug. Continuing Claims, est. 1.72m, prior 1.73m

- 08:30: 2Q Nonfarm Productivity, est. 3.4%, prior 3.7%

- 08:30: 2Q Unit Labor Costs, est. 1.9%, prior 1.6%

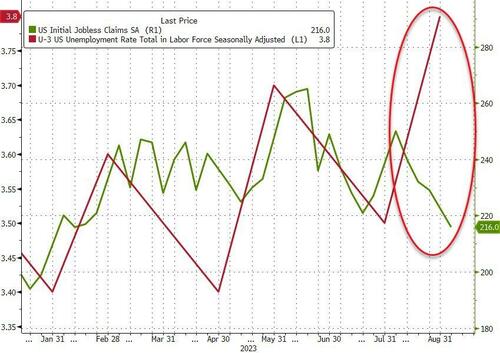

- 08:30: Sept. Initial Jobless Claims, est. 234,000, prior 228,000

Central Bank Speakers:

- 10:00: Fed’s Harker Speaks on Future of Fintech

- 11:45: Fed’s Goolsbee Delivers Welcome Remarks at Chicago Fed Event

- 14:00: St. Louis Fed Hosts Public Engagement on Presidential Search

- 15:30: Fed’s Williams Speaks at Bloomberg Market Forum

- 15:45: Fed’s Bostic Speaks on Economic Outlook

- 16:55: Fed’s Bowman Speaks on Panel About Future of Money

- 19:00: Fed’s Bostic Speaks on Economic Mobility

- 19:05: Fed’s Logan Speaks on Monetary Policy in Dallas

DB’s Jim Reid concludes the overnight wrap

Markets witnessed a fresh selloff over the last 24 hours, with bonds and equities losing ground after the latest ISM services index came in much stronger than expected. The headline number was at 54.5 (vs. 52.5 expected), which was above every economist’s expectation on Bloomberg, as well as the highest level since February. So it made a change from the more downbeat data over recent weeks, such as the negative revisions in last Friday’s jobs report. On top of that, the employment component (54.7) hit a 21-month high, new orders (57.5) were at a 6-month high, and there were even signs of fresh momentum on inflation, since the prices paid component rose for a second consecutive month to 58.9.

Whilst the data came in better than expected, the problem for markets was that the release led to growing speculation that the Fed might not be done with their hiking cycle after all. In fact, fed funds futures moved to price in a 50% chance of a hike by the time of the November meeting, up from 46% on Tuesday. So by the close, the market saw it as even odds whether we’ll get another hike. And looking further out, the rate priced in for the December 2024 meeting hit a new high for the cycle of 4.45%, which just shows how investors are becoming increasingly sceptical about the prospect of rate cuts any time soon.

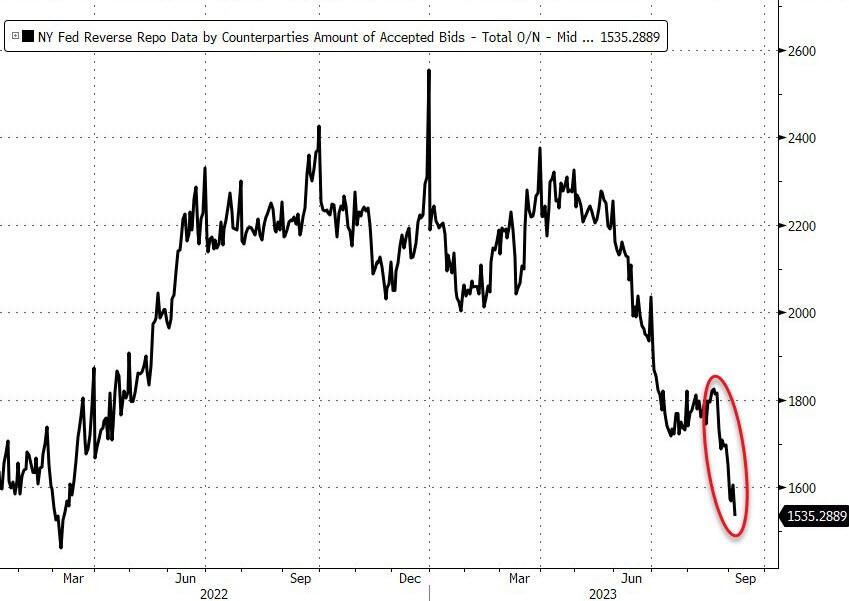

With the prospect of another rate hike in sight, September is sticking to its usual reputation of being a poor month for markets. That included a fresh bond selloff yesterday, which sent the 10yr Treasury yield up +2.0bps to 4.28%, while the 2yr moved back above 5% for the first time since last Monday (+5.6bps to 5.02%). The 10yr real yield was up +1.5bps to 1.97%, just 1bp from its post-GFC high seen last month. The effect of higher yields became increasingly evident in the real economy as well yesterday, as we got the latest weekly data from the Mortgage Bankers Association. That showed that mortgage applications for home purchases fell to its lowest level since April 1995 last week, which just shows how rates at these levels are having an effect.

Those bond moves were echoed in Europe, where yields on 10yr bunds (+4.3bps), OATs (+4.7bps) and BTPs (+6.3bps) all moved higher on the day. That comes with just one week to go until the ECB’s next decision, and as in the US, yesterday brought growing speculation about whether the ECB might hike again after all. For instance, overnight index swaps moved to price in a 33% chance of a hike by the close, up from 25% the previous day. In part, that followed comments from several ECB speakers. The more hawkish members kept the option of a September hike firmly on the table, with the Dutch central bank governor Knot saying that the decision was a “close call”, whilst Slovakia’s Kazimir said that the ECB should “take one more step”, that a hike next week was preferable to waiting in September and delivering another hike later in the year. Meanwhile, Italy’s Visco said he believed “we are near the level where we can stop raising rates”. So by no means full confidence in a pause from one of the more dovish ECB voices.

The main outlier in the bond space was the UK, where gilts outperformed after Bank of England officials struck a more dovish tone than had been expected. For instance, BoE Governor Bailey said that policy was “near the top of the cycle”, and markets moved to price in a slightly more dovish path for rate hikes as a result. Yields on 10yr gilts only ended the day up +0.8bps, with the 2yr yield down -3.2bps, whilst sterling the weakest-performing G10 currency as it fell -0.45% against the US Dollar.

This backdrop proved bad news for equities, with the S&P 500 down -0.70% on the day, though it did partially recover in the US afternoon having traded down -1.21% at its intraday low. Tech stocks were the biggest underperformer, and the NASDAQ (-1.06%) and the FANG+ Index (-1.47%) both saw a decent pullback. It was much the same story in Europe as well, where the STOXX 600 (-0.57%) lost ground for a 6th consecutive session, albeit with sizeable variations among the individual country indices. For instance, the DAX only fell -0.19%, whereas Italy’s FTSE MIB fell -1.54%.

Another factor not helping matters were the latest run-up in oil prices. For example, Brent crude was up another +0.62% to close at $90.60/bbl. That’s its 7th consecutive daily advance and leaves prices up to their highest level since November. In the meantime, WTI prices were also up +0.98% to $87.54/bbl. So that raises the risk that inflation persists a bit more than previously expected, and the recent runup in gasoline prices has already led to expectations of a stronger August CPI print next week.

Overnight in Asia, we’ve seen that negative tone continue in markets, with losses across all the major indices. That includes the Hang Seng (-0.95%), the CSI 300 (-0.86%), the KOSPI (-0.68%), the Shanghai Comp (-0.58%) and the Nikkei (-0.34%). And looking forward, this weakness is also evident among equity futures, with those on the S&P 500 (-0.11%) and the DAX (-0.27%) pointing lower as well. However, there were some signs of improvement in China’s data, with exports only down -8.8% in dollar terms year-on-year in August (vs. -9.0% expected), which is up from a -14.5% decline in July. Likewise, imports were down -7.3% yoy (vs. -9.0% expected), which was also an improvement from the -12.4% reading in July.

Elsewhere yesterday, the Bank of Canada held their target for the overnight rate at 5%, in line with expectations. However, their statement said that the Governing Council “remains concerned about the persistence of underlying inflationary pressures, and is prepared to increase the policy interest rate further if needed.” Following the decision, yields on 10yr government debt closed -0.6bps lower. Similar to the US, overnight index swaps imply a very close call on whether we see another rate hike, and by the close they were pricing in a 48% chance of a further hike by the end of the year.

Yesterday also saw the release of the Fed’s Beige Book, which summarises anecdotal information gathered by the regional Feds. On the consumer side, this noted strong tourism spending, which “most contacts considered the last stage of pent-up demand for leisure travel”. But it pointed out that “job growth was subdued across the nation”. In other Fed news, the Senate confirmed Philip Jefferson as Vice Chair of the Fed for a four-year term, and Lisa Cook was confirmed for a full 14-year term as a Governor on the Federal Reserve Board.

Finally, data showed that German factory orders had contracted by -11.7% in July (vs. -4.3% expected). That’s the largest slump since the pandemic-related decline in April 2020. Separately, the German construction PMI for August came in at 41.5, which was its 17th consecutive month in contractionary territory.

To the day ahead now, and data releases include German industrial production and Italian retail sales for July, whilst in the US we’ll get the weekly initial jobless claims. From central banks, we’ll hear from the Fed’s Harker, Goolsbee, Williams, Bostic, Bowman and Logan, the ECB’s Wunsch, Holzmann, Villeroy, Knot and Elderson, as well as BoC Governor Macklem. We’ll also get the BoE’s decision maker panel survey.

2 B) NOW NEWSQUAWK (EUROPE/REPORT)/

Equities pare back losses on lower yields; NQ lags on AAPL pressure; Fed speak due – Newsquawk US Market Open

THURSDAY, SEP 07, 2023 – 06:19 AM