GOLD PRICE CLOSED: DOWN $2.00 TO $1910.40

SILVER PRICE CLOSED: DOWN $0.23 AT $22.88

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1908.60

Silver ACCESS CLOSE: 22.84

Shanghai Gold Benchmark Price

USD oz  AM1987.82

AM1987.82

PM1995.91

Historical SGE Fix

New York price at the time: $1911.00

premium $84.00

xxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $26,172 UP 83 Dollars

Bitcoin: afternoon price: $26,129 UP 40 dollars

Platinum price closing $905.05 UP $3.00

Palladium price; $1252.75 UP $35.75

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,586.68 DOWN 5.76 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1528.07 DOWN 3.25 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1778.37 DOWN 0.50 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,911.300000000 USD

INTENT DATE: 09/12/2023 DELIVERY DATE: 09/14/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 24

323 H HSBC 33

363 H WELLS FARGO SEC 22

435 H SCOTIA CAPITAL 28

624 H BOFA SECURITIES 47

657 C MORGAN STANLEY 8

661 C JP MORGAN 173 2

686 C STONEX FINANCIA 1

690 C ABN AMRO 3

732 C RBC CAP MARKETS 2

737 C ADVANTAGE 18

905 C ADM 16 1

TOTAL: 189 189

JPMorgan stopped 2/189 contracts.

FOR SEPT.:

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2023. CONTRACT: 189 NOTICES FOR 18,900 OZ or .5878 TONNES

total notices so far: 3822 contracts for 382,200 oz (11.888 tonnes)

FOR SEPT:

SILVER NOTICES: 33 NOTICE(S) FILED FOR 165,000 OZ/

total number of notices filed so far this month : 2590 for 12,950,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $2.00

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 884.89 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 23 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.009 MILLION OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 440.736 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 929 CONTRACTS TO 125,292 AND FURTHER FORM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY $0.01 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. TAS ISSUANCE WAS A GOOD SIZED 400 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 400 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.01). BUT WERE UNSUCCESSFUL IN KNOCKING SOME SILVER CONTRACTS AS WE HAD A HUGE SIZED LOSS OF 829 CONTRACTS ON BOTH EXCHANGES ALONG WITH MINOR T.A.S.LIQUIDATION THROUGHOUT THE TUESDAY COMEX SESSION

WE MUST HAVE HAD:

A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS( 100 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 14.420 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 15,000 OZ//NEW TOTAL 13.350 MILLION OZ + OUR CRIMINAL ISSUANCE OF 200 EXCHANGE FOR RISK CONTRACTS OR 1.00 MILLION OZ OF FUTURE SILVER STANDING FOR METAL//NEW TOTALS EXCHANGE FOR RISK: 2.0 MILLION OZ: NEW TOTALS SILVER STANDING: 15.350 MILLION OZ// /// / //HUGE SIZED COMEX OI LOSS/ SMALL SIZED EFP ISSUANCE/VI) GOOD SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 400 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL 26 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 8 days, total 5331 contracts: OR 26.655 MILLION OZ (666 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 26.655 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 26.655 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 929 CONTRACTS DESPITE OUR GAIN IN PRICE OF $0.01 IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL EFP ISSUANCE CONTRACTS: 100 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR SEPT OF 14.2 MILLION OZ FOLLOWED BY TODAY’S 15,000 OZ E.F.P JUMP TO LONDON.+ 1.0 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL FOR EXCHANGE FOR RISK = 2.0 MILLION OZ//NEW TOTALS STANDING 15.350 MILLION OZ// /// WE HAVE A HUGE SIZED LOSS OF 829 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GOOD SIZED 400 CONTRACTS//MINOR FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION. THE NEW TAS ISSUANCE TUESDAY NIGHT (400) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 33 NOTICE(S) FILED TODAY FOR 165,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 5932 CONTRACTS TO 441,221 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: 205 CONTRACTS

WE HAD A STRONG SIZED INCREASE IN COMEX OI ( 6137 CONTRACTS) DESPITE OUR $11.20 LOSS IN PRICE//TUESDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 12.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 18,700 OZ QUEUE JUMP//NEW TOTAL STANDING 14.435 TONNES + /A FAIR (AND CRIMINAL) ISSUANCE OF 1746 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR $11.20 LOSS IN PRICE WITH RESPECT TO TUESDAY’S TRADING.WE HAD A VERY STRONG SIZED GAIN OF 10,613 OI CONTRACTS (33.010 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4681 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 441,221

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,613 CONTRACTS WITH 5932 CONTRACTS INCREASED AT THE COMEX// AND A STRONG 4681 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 10,613 CONTRACTS OR 33.010 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1746 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4681 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (5932) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 10,613 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 12.656 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 18700 OZ/// 3) ZERO LONG LIQUIDATION WITH STRONG TAS LIQUIDATION DURING THE COMEX SESSION //4) STRONG SIZED COMEX OPEN INTEREST GAIN/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1746 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT :

TOTAL EFP CONTRACTS ISSUED: 17,735 CONTRACTS OR 1,773,500 OZ OR 55.163 TONNES IN 8 TRADING DAY(S) AND THUS AVERAGING: 2216 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES 55,163 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 55.163/3550 x 100% TONNES 1.54% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 55.163 TONNES (SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 929 CONTRACTS OI TO 125,318 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A SMALL 100 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 100 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 100 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 903 CONTRACTS AND ADD TO THE 100 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 829 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 4.145 MILLION OZ

OCCURRED DESPITE OUR TINY $0.01 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 13.99 PTS OR 0.45% //Hang Seng CLOSED DOWN 16.67 PTS OR 0.09%/ /The Nikkei CLOSED DOWN 69.85 PTS OR 0.21% //Australia’s all ordinaries CLOSED DOWN 0.77 % /Chinese yuan (ONSHORE) closed UP AT 7.2828 /OFFSHORE CHINESE YUAN UP TO 7.2839 /Oil UP TO 89.20 dollars per barrel for WTI and BRENT UP AT 92/42 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 5932 CONTRACTS TO 441,221 DESPITE OUR LOSS IN PRICE OF $11.20 ON TUESDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4681 EFP CONTRACTS WERE ISSUED: : DEC 4681 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4681 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 10,613 CONTRACTS IN THAT 4681 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 5932 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $11.20//TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A FAIR 1746 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (14.435) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 14.435 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $11.20) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A VERY STRONG GAIN OF 10,613 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A STRONG T.A.S. LIQUIDATION ON THE FRONT END OF TUESDAY’S TRADING. THE T.A.S. ISSUED ON TUESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 33.010 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPT. (12.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 18,700 OZ//NEW STANDING 14.435 TONNES // ALL OF THIS WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $12.20.

WE HAD – REMOVED 205 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 10,613 CONTRACTS OR 1,061,300 OZ OR 33.010 TONNES.

Estimated gold volume today:// 158,234 awful

final gold volumes/yesterday 172,959 awful//speculators have left the gold arena

//SEPT 13/ /// THE SEPT. 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 160,755.000 OZ JPMorgan 5000 kilobars . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 189 notice(s) 18900 OZ 0.5878 TONNES |

| No of oz to be served (notices) | 819 contracts 819,00 oz 2.5474 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3822 notices 382200 OZ 11.888 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: nil oz

we had 1 customer withdrawals

i) Out of JPMorgan: 160,755.000 oz (5000 kilobar)

total withdrawals 160,755.000 oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER.

For the front month of SEPTEMBER we have an oi of 1008 contracts having GAINED 183 contracts. We had

4 contracts were served on TUESDAY, so we gained an additional 187 CONTRACTS or AN ADDITIONAL 18,700 oz will stand for delivery in this non active delivery month of Sept.

Oct gained 411 contracts to 25,210 contracts.

NOV GAINED 6 CONTRACTS to stand at 18

December GAINED 3865 contracts UP to 379,482 contracts.

We had 189 contracts filed for today representing 18,900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 173 notices were issued from their client or customer account. The total of all issuance by all participants equate to 189 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 2 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2023. contract month,

we take the total number of notices filed so far for the month (3822 x 100 oz ), to which we add the difference between the open interest for the front month of SEPT (1008 CONTRACTS) minus the number of notices served upon today 189 x 100 oz per contract equals 454,100 OZ OR 14.435 TONNES the number of TONNES standing in this non active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month: No of notices filed so far (3822) x 100 oz + (1008) {OI for the front month} minus the number of notices served upon today (189) x 100 oz) which equals 454,100 oz standing OR 14.435 TONNES

TOTAL COMEX GOLD STANDING: 14.435 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,035,284.466 OZ 63.395 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 20,881 552.420 OZ

TOTAL REGISTERED GOLD 10,850,669.474 (337.50 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,030,882.942 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,815,385 OZ (REG GOLD- PLEDGED GOLD) 274,195 tonnes//dropping like a stone

END

SILVER/COMEX

SEPT 13

//2023// THE SEPT 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 23,117.828oz Delaware . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil |

| No of oz served today (contracts) | 33 CONTRACT(S) (165,000 OZ) |

| No of oz to be served (notices) | 80 contracts (400,000 oz) |

| Total monthly oz silver served (contracts) | 2590 Contracts (12,950,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 deposit customer account:

total customer deposit nil oz

JPMorgan has a total silver weight: 136.901 million oz/274.209 million or 50.00%

Comex withdrawals 1

i) Out of Delaware 23,117.828 oz

total: 23,117.828 oz

adjustments:

TOTAL REGISTERED SILVER: 42.449 MILLION OZ//.TOTAL REG + ELIGIBLE. 274.209 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF SEPT /2023 OI: 113 CONTRACTS HAVING LOST 63 CONTRACT(S). WE HAD 60

CONTRACTS SERVED ON TUESDAY. SO WE LOST 3 CONTRACTS OR 15,000 OZ WERE IMMEDIATELY E.F.P.d TO LONDON IN ORDER TO TAKE DELIVERY OVER THERE. NO SILVER COULD BE FOUND OVER HERE.

OCT LOST 31 CONTRACTS TO STAND AT 1074.

NOVEMBER LOST 5 CONTRACTS TO STAND AT 102

DEC. LOST 433 CONTRACTS TO STAND AT 113,251 .

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 33 for 165,000 oz

Comex volumes// est. volume today 48,502 poor

Comex volume: confirmed yesterday 44,728 poor

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 2590 x 5,000 oz = 12,950,000 oz

to which we add the difference between the open interest for the front month of SEPT (113) and the number of notices served upon today 33 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2023 contract month: 2590 (notices served so far) x 5000 oz + OI for the front month of SEPT (135) – number of notices served upon today (33 )x 500 oz of silver standing for the SEPT contract month equates to 13.350 million oz. + OUR 1.0 MILLION EXCHANGE FOR RISK..NEW TOTALS EXCHANGE FOR RISK: 2.0 MILLION OZ//NEW TOTAL STANDING FOR SILVER: 15.350 MILLION OZ//

There are 42.145 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

SEPT 13/WITH GOLD DOWN $2.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 12/WITH GOLD DOWN $11.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 11/WITH GOLD UP $4.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 8/WITH GOLD UP $0.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 7/WITH GOLD DOWN $0.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.22 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.69 TONNES

SEPT 6/WITH GOLD DOWN $8.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.81 TONNES

SEPT 5/WITH GOLD DOWN $13.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.97 TONNES

SEPT 1/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 31/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 30/WITH GOLD UP $8.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.59 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.23 TONNES

AUGUST 29/WITH GOLD UP 17.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.6 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.64 TONNES

AUGUST 28/WITH GOLD UP $6.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / //INVENTORY RESTS AT 884.04 TONNES

AUGUST 25/WITH GOLD DOWN $6.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 884.04 TONNES

AUGUST 24/WITH GOLD UP $0.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //INVENTORY RESTS AT 884.91 TONNES

AUGUST 23/WITH GOLD UP $21.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 4.32 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 884.91 TONNES

AUGUST 22/WITH GOLD UP $2.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.87 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 889.23 TONNES

AUGUST 21/WITH GOLD UP $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.60 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 890.10 TONNES

AUGUST 18/WITH GOLD UP $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 887.50 TONNES

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 16/WITH GOLD DOWN $7.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 15/WITH GOLD DOWN $7,45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 895.87 TONNES

AUGUST 14/WITH GOLD DOWN $2.10 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.75 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 899.63 TONNES

AUGUST 11/WITH GOLD DOWN $2.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 903.31 TONNES

AUGUST 10/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 9/WITH GOLD DOWN $8.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 8/WITH GOLD DOWN $9.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES FORM THE GLD /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 7/WITH GOLD DOWN $5.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///INVENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

GLD INVENTORY: 886.64 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 13/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1,009 MILLION OZ INTO THE SLV//: // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 12/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 11/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 7/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 6/WITH SILVER DOWN 36 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.373 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 5/WITH SILVER DOWN 69 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 734,000 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 437.891 MILLION OZ

SEPT 1/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 440.00 MILLION OZ

AUGUST 31/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 438.625 MILLION OZ

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.834 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 443.210 MILLION OZ

AUGUST 29/WITH SILVER UP 49 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 183,000 OF SILVER INTO THE THE SLV// /.////INVENTORY RESTS AT 445.044 MILLION OZ

AUGUST 28/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.281 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 444.861 MILLION OZ

AUGUST 25/WITH SILVER UP ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 446.145 MILLION OZ

AUGUST 24/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.651 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 448.896 MILLION OZ

AUGUST 23/WITH SILVER UP 94 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FROM THE SLV// /.////INVENTORY RESTS AT 450.547 MILLION OZ

AUGUST 22/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: /.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 21/WITH SILVER UP 59 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 917,0000 OZ FROM THE SLV//.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 18/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 16/WITH SILVER DOWN 13 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 15/WITH SILVER DOWN 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 14/WITH SILVER DOWN 3 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.459 MILLION OZ INTOTHE SLV/: //////INVENTORY RESTS AT 452.565 MILLION OZ

AUGUST 11/WITH SILVER DOWN 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.926 MILLION OZ INTOTHE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 452.106 MILLION OZ

AUGUST 10/WITH SILVER UP 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 9/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 8/WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 7/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

CLOSING INVENTORY 440.736 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

3,Chris Powell of GATA provides to us very important physical commentaries

Sad to report the death of Michael Kosares

(GATA)

Monetary metals advocate and USAGold founder Michael Kosares dies

Submitted by admin on Tue, 2023-09-12 21:24Section: Daily Dispatches

9:21p ET Tuesday, September 12, 2023

Dear Friend of GATA and Gold:

Monetary metals investors and believers in free and transparent markets and limited and accountable government have lost a devoted advocate: Michael J. Kosares.

Kosares, founder of the USAGold coin and bullion dealership in Colorado and author of many financial commentaries cited by GATA, died last week at age 75 after fighting cancer for six years

Mike supported and encouraged GATA for many years and his passing is a special loss to us. His son, Jonathan, who succeeds to management of USAGold, wrote of Mike today: “A truly gifted writer, he made economics accessible, displaying again and again a remarkable ability to simplify even the most complex subjects for his readers.”

We will always remember Mike’s friendship and work for our cause.

Jonathan’s eulogy for his father has been posted at USAGold’s internet site here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

For a pittance, miners can work public land but there’s a push to make them pay

Submitted by admin on Tue, 2023-09-12 21:52Section: Daily Dispatches

By Lisa Friedman

The New York Times

Tuesday, September 12, 2023

Since Ulysses S. Grant was in the White House, any company that mines gold or other metals from public land has been able to haul it away without paying a dime in royalties to the federal government.

As demand is spiking for copper, nickel, cobalt, and other metals and minerals that are essential for electric vehicles and other clean energy technologies, the Biden administration says Congress needs to fix the Gold Rush-era General Mining Law so it can better manage the mineral resources buried under millions of acres of public land.

A top priority: Require companies to pay something in exchange for what they take. Unlike companies that extract oil, gas, and coal from federal lands, hardrock miners pay no royalties to the federal government.

The call to impose a fee of 4 to 8% of the net value of what is mined could translate into as much as $97 million annually and draws sharp opposition from mining operators.

Today the Biden administration said the law needed to be updated to ensure the United States developed a supply of critical minerals that are “responsibly sourced” to achieve Mr. Biden’s clean energy goals.

“The biggest takeaway from our report is that our 150-year-old-law, the 1872 mining law, needs to be reformed and brought into the 21st century,” Tommy Beaudreau, the deputy secretary of the Interior Department, said.

Developing reliable and responsible domestic sources for critical minerals is “central to the clean energy and technology revolution that are shaping our future for the better,” he said. …

… For the remainder of the report:

END

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES//

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES: LITHIUM

This is an extremely important discovery in the uSA and they will be able to mine cheaply due to concentration

(zerohedge)

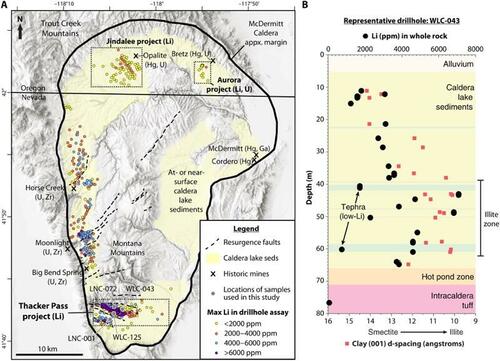

$1.5 Trillion Dollars Worth Of ‘White Gold’ Found In Supervolcano On Nevada-Oregon Border

TUESDAY, SEP 12, 2023 – 09:45 PM

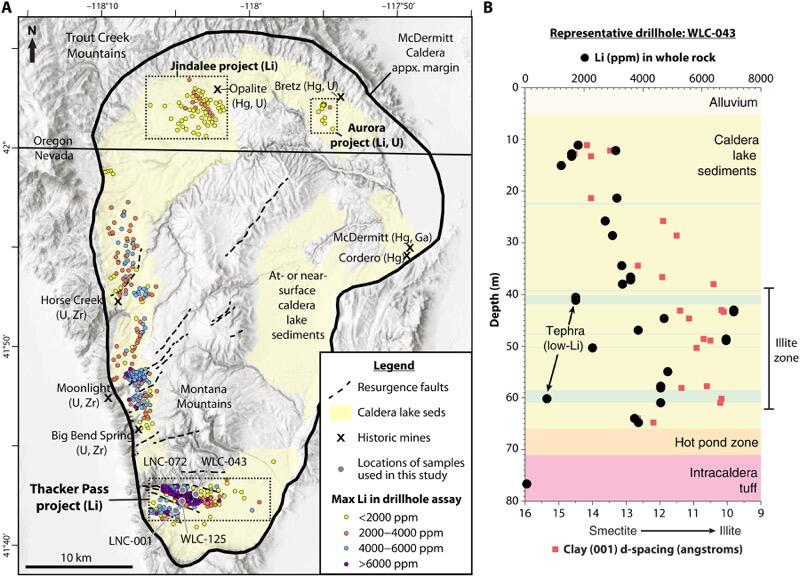

An ancient supervolcano along the Nevada-Oregon border contains what could be the world’s largest single deposit of lithium. The findings could reshape the West’s supply of the critical metal — and might even change the geopolitical game with China.

Researchers from Lithium Americas Corporation, GNS Science, and Oregon State University published their findings in the Journal for Science Advances on Aug. 31. They found the McDermitt Caldera, a caldera measuring 28 miles long and 22 miles wide, on the Nevada-Oregon border, contains around 20 to 40 million metric tons of lithium – a figure that would dwarf deposits in Australia and Chile.

Commenting on the findings is Anouk Borst, a geologist at KU Leuven University and the Royal Museum for Central Africa in Tervuren, Belgium, who told Chemistry World that the McDermitt Caldera deposit “could change the dynamics of lithium globally, in terms of price, security of supply and geopolitics.”

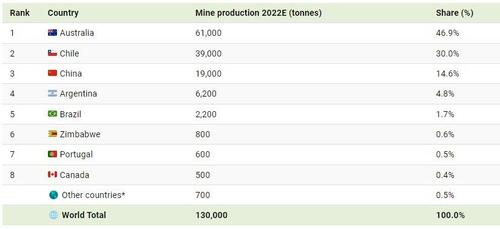

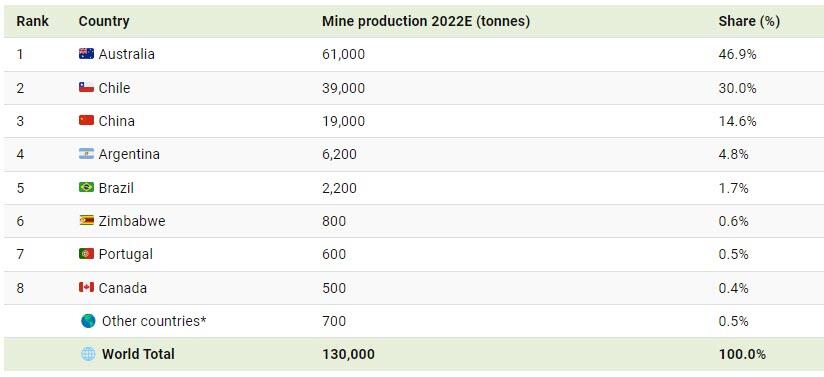

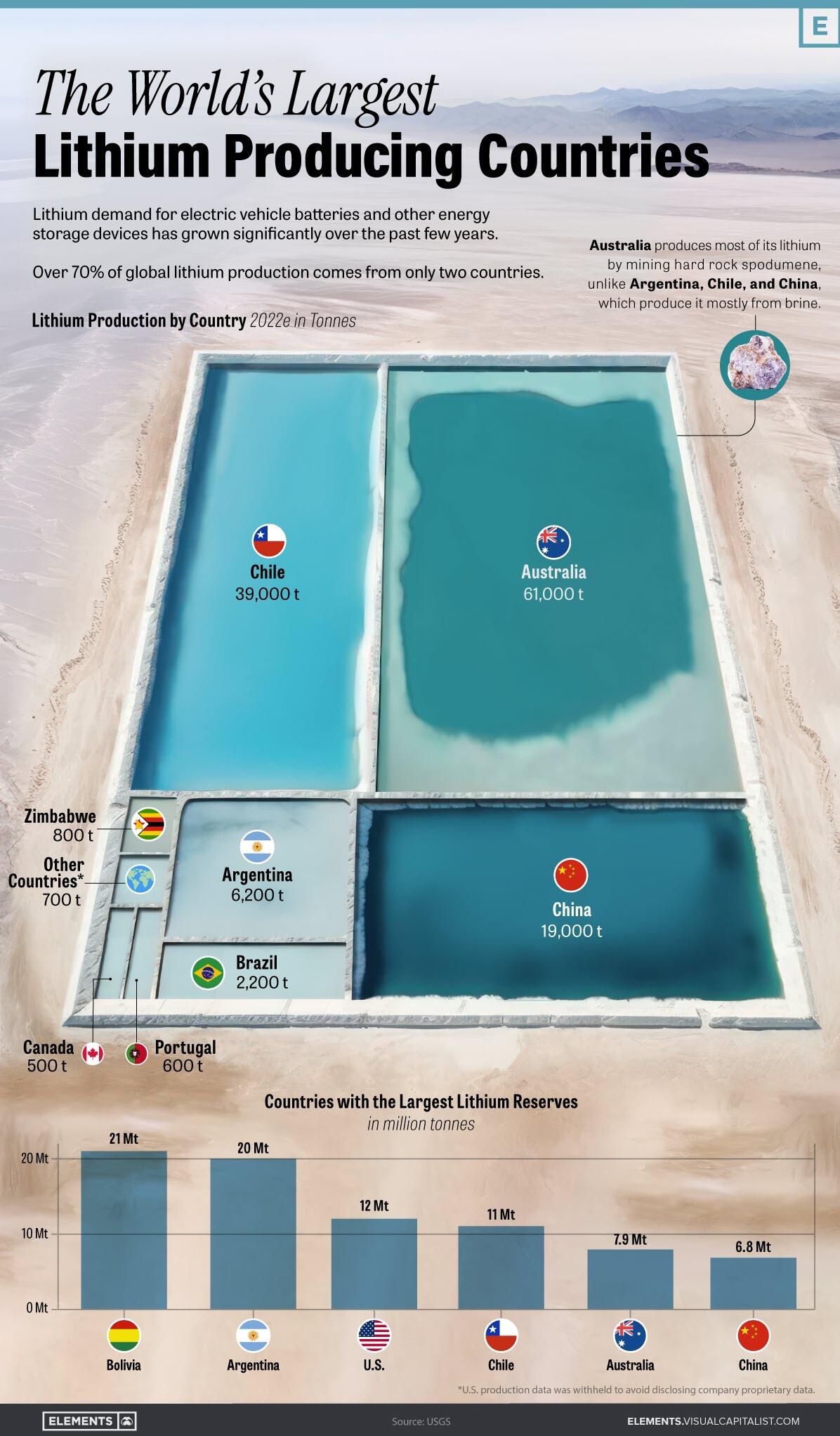

Data from the United States Geological Survey, presented by Visual Capitalist Bruno Venditti, shows the US lags behind the world in terms of lithium production.

Even though the US has the third largest reserves.

If you can believe it, the US only has one producing lithium mine – Silver Peak – in Nevada (about halfway between Las Vegas and Carson City) – while worldwide demand is surging due to the government-forced clean energy transition. We noted in July that Exxon Mobil Corp. was in the beginning stages of possibly becoming a ‘lithium kingpin.’

Thomas Benson, a geologist with Lithium Americas Corporation and co-author of the new study, expects mining operations at the McDermitt Caldera to begin in early 2026.

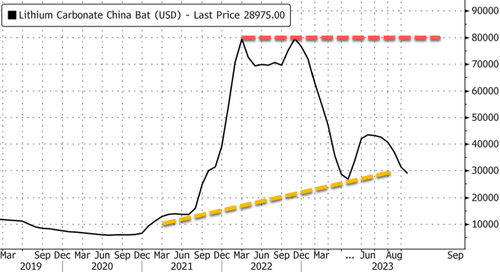

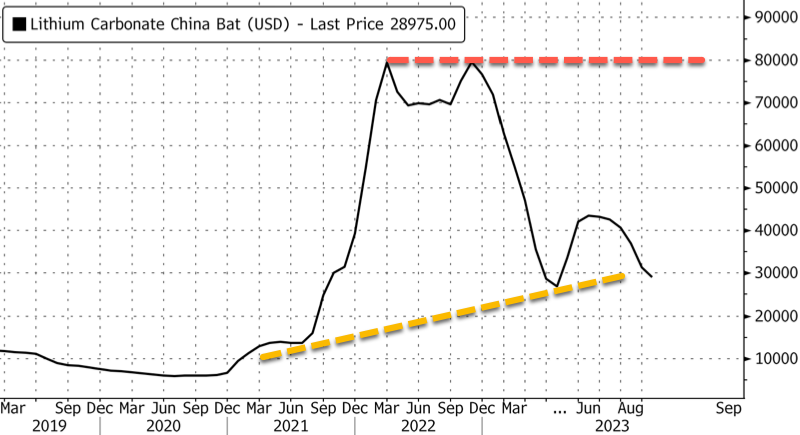

Lithium prices have been on a rollercoaster of a ride since Coivd. Battery-grade lithium carbonate prices in China (priced in dollars) were as low as $5,850 per ton in the summer of 2020 and jumped as much as 1,200% through the peak of $80,000 in early 2022. Prices have since collapsed to $30,000.

Daily Mail pointed out, “As of 2022, the average battery-grade lithium carbonate price was $37,000 per metric ton, meaning the volcano is potentially sitting on $1.48 trillion worth of the precious metal.”

McDermitt Caldera positions Nevada as possibly the epicenter of the ‘green energy white gold rush’ amid a massive push by the Biden administration to force people to drive electric vehicles — all because they say there’s a ‘climate emergency.’

END

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2828

OFFSHORE YUAN: UP TO 7.2839

SHANGHAI CLOSED DOWN 13.99 PTS OR 0.45%

HANG SENG CLOSED DOWN 16.64PTS OR .09%

2. Nikkei closed DOWN 69.85 OR 0.21%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 104.43 EURO FALLS TO 1.0721 DOWN 22 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.698 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.45/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ON SHORE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.6815***/Italian 10 Yr bond yield UP to 4.472*** /SPAIN 10 YR BOND YIELD UP TO 3.747…**

3i Greek 10 year bond yield RISES TO 4.055

3j Gold at $1911.25 silver at: 22.87 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 61 /100 roubles/dollar; ROUBLE AT 96.55//

3m oil into the 89 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.45// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.698% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8934 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9587well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.319 UP 5 BASIS PTS…

USA 30 YR BOND YIELD: 4.383 UP 5 BASIS PTS/

USA 2 YR BOND YIELD: 4.5039 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.90…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 2 BASIS PTS AT 4.4570

end

2.a Overnight: Newsquawk and Zero hedge:

USA EARLY MORNING REPORT

Futures Drift Lower Ahead Of CPI Report

WEDNESDAY, SEP 13, 2023 – 08:07 AM

S&P 500, Nasdaq 100 futures drifted lower overnight, and were last down modestly ahead of the US CPI release (previewed here), as European markets tumbled across the board on signs the region is quickly sliding into stagflation. As of 7:40am, S&P and Nasdaq 100 futures traded down 0.1% as Apple looked set for a second day of declines after China flagged security problems with iPhones, while saying it isn’t barring purchases. . The dollar remains steady ahead of the US CPI release due later Wednesday, while European stocks and German bunds slipped as markets boost bets on ECB policy tightening. Gold is down slightly and oil is up 0.68% rising to a new 2023 high after deficit warnings from the International Energy Agency.

In premarket trading, electric-vehicle makers including XPeng and Nio lead a drop in US-listed Chinese stocks after the European Union launched an investigation into Chinese subsidies for EVs. Apple fell 0.5%, erasing earlier gains, as China flagged security problems with iPhones. Here are some other notable premarket movers:

- Ford gains 1.6% after UBS double-upgrades its rating to buy from sell, citing greater-than-expected earnings resilience driven by the automaker’s Ford Pro segment.

- Grab fell 6.3% as some investors took money out for investing in IPO of Ryde, a smaller ride-hailing rival based in Singapore, according to Aletheia Capital.

- Rocket Pharmaceuticals shares jump 18% after the gene-therapy developer said it’s in alignment with the US Food and Drug Administration on the global Phase 2 trial of RP-A501 for Danon disease, which is a fatal inherited cardiomyopathy.

- Workhorse rose 18% after saying it received IRS approval as a qualified manufacturer for the Commercial Clean Vehicle Credit.

Arm Holdings Plc’s long-anticipated initial public offering is set to price Wednesday in the largest listing of the year. Arm is now looking to price the IP0 shares a dollar or more above the $47 to $51 target range, Bloomberg News reported.

Traders are bracing for the US CPI data (full preview here) on Wednesday and a faster-than-forecast print would likely rattle markets given the economic concerns in Europe. Economists at Bloomberg Economics say a third month of subdued core inflation would bolster the case for the Federal Reserve to cease rate increases, although the recent surge in oil prices means that headline inflation is about to jump the most since Since 2022.

Here is a bank by bank summary of CPI forecasts:

- 3.7% – Barclays

- 3.7% – Citigroup

- 3.7% – HSBC

- 3.7% – UBS

- 3.6% – Bank of America

- 3.6% – Goldman Sachs

- 3.6% – JP Morgan Chase

- 3.6% – Morgan Stanley

- 3.6% – Wells Fargo

“Markets appear on edge ahead of US inflation and the ECB’s rate decision,” Citigroup Inc. strategists including Luis Costa and Alexander Rozhetskin wrote in a note. “With oil edging above $90, fears of stickier inflation are increasing, while some reports indicate that the ECB’s latest staff projection might prompt a more hawkish stance.”

The US data are expected to send a mixed message on the US economy, according to Bloomberg Economics. Monthly headline inflation is seen at 0.6%, while annualized core inflation will stay near the Fed’s 2% target for a third straight month.

“Given stocks are currently quite directionless a faster-than-expected CPI reading can raise investors nerves and refocus their minds on the risks of high energy price volatility,” said Janet Mui, head of market analysis at RBC Brewin Dolphin. “If both headline and core surprised up then it could trigger a negative market reaction.”

In Europe, the Stoxx 600 Index retreated 0.9% and the Stoxx 50 fell 0.7%. FTSE 100 outperforms peers, dropping 0.2%, IBEX lags, dropping 1.2%. Here are the most notable European movers:

- European auto shares rise, sending the Stoxx 600 Automobiles & Parts Index to its biggest intraday gain since July 27, after the EU began an investigation into Chinese subsidies for electric vehicles.

- HHLA shares jump as much as 48%, the most intraday on record, after a unit of MSC offered to buy part of the Hamburg port services provider for €16.75 per A-share.

- On The Beach shares gain as much as 15% after the online seller of packaged vacations forecast full-year adjusted pretax profit at the top end of market expectations.

- Aroundtown shares rise as much as 5.8% after Goldman Sachs raises PT on the stock by 15% to €1.50, saying the German real estate firm has “sufficient headroom” on debt leverage.

- Redrow shares gain as much as 4.1% after the UK homebuilder delivers an earnings statement which Goodbody says is “comforting.”

- TeamViewer shares rise as much as 3.4% in Frankfurt, the most in a month, after the German software maker said it will cut back on its sponsorship deal with Manchester United from the start of the 2024 to 2025 season to boost profits.

- AB Foods shares drop as much as 1.1% after Deutsche Bank cut its recommendation on the British conglomerate to hold from buy, citing limited scope for further earnings upside.

- Unieuro shares fall as much as 9.8% in Milan as Banca Akros downgraded the Italian consumer electronics chain to reduce from neutral.

- Knorr-Bremse, Alstom shares fall as Barclays rates the companies underweight, citing high valuations and headwinds.

- Kingspan shares decline as much as 3% after JPMorgan downgraded the stock to neutral from overweight, saying catalysts have largely played out for the company, while stocks in the construction sector could be vulnerable for the rest of the year.

Markets in Europe were looking past the US data to the ECB’s meeting on Thursday. After reports that the central bank’s new economic estimates will show an inflation forecast for 2024 above 3%, traders upped wagers on policy makers raising rates at the meeting to a 70% chance, compared with a 20% probability earlier this month. The German two-year yield — among the most sensitive to monetary policy — rose five basis points to 3.18%, the highest level since mid-August.

In the UK, the pound sank as much as 0.4% against the greenback, before paring losses. Data showed the economy shrank at the fastest pace in seven months in July as strikes and wet weather hit activity harder than expected. That may prompt a pause when policy makers decide next week whether to raise interest rates again.

Earlier in the session, Asian stocks slipped, with tech stocks in Japan and China leading the drop as traders geared up for the release of US inflation figures. The MSCI Asia Pacific Index fell as much as 0.4% as tech names including Alibaba, Hitachi and Tencent headlined the losses. All equity benchmark gauges in the region were in the red as caution reigned ahead of the US inflation print which is likely to help shape the outlook for Federal Reserve policy. There’s “a heightened risk” that the data may come in above consensus expectations, which will push up Treasury yields and “put a ceiling on the bulls” for the Asian equity benchmark, according to Kelvin Wong, senior market analyst at Oanda.

- A gauge of Chinese tech firms listed in Hong Kong headed for its longest run of declines since April, while a tech-heavy small-cap index in South Korea dropped more than 1%.

- Japan’s Nikkei 225 swung between gains and losses with early advances seen following mixed PPI data and the improvement in BSI large industry surveys, although the index eventually slipped with money markets now pricing the BoJ to exit negative rates in January compared to a previous pricing of an exit in September next year.

- Australia’s ASX 200 declined as tech stocks mirrored the underperformance seen in US counterparts and with nearly all sectors on the retreat aside from energy and utilities after further upside in oil prices.

- India’s Sensex index closed higher for the ninth straight session, its longest winning run since April, and outperformed regional peers as banks and energy companies rallied. The S&P BSE Sensex rose 0.4% to 67,466.99 in Mumbai, while the NSE Nifty 50 Index advanced by the same magnitude to close above the 20,000-mark for the first time ever.

In FX, the Bloomberg Dollar Spot Index edged up 0.2%, recovering from a 0.7% slide on Monday. All G-10 FX traded lower versus the dollar; NZD and CAD are the strongest performers in G-10 FX, SEK and AUD underperform. Sterling at ~$1.24 after UK GDP data. The pound tested a three-month low and the euro weakened. Traders ramped up bets price pressures will force the European Central Bank to hike rates at its meeting on Thursday even as the German government was said to predict a contraction for this year and the UK economy shrank at the quickest pace in seven months.

- EUR/USD falls 0.4% as investors wait to see whether the European Central Bank will hold off from raising interest rates at its meeting on Thursday

- GBP/USD slides 0.4%, approaching its lowest in three months after data showed that the UK labour market was showing signs of cooling

- USD/JPY climbs 0.8% to 147.42

Data dependence remains “the law of the land” when it comes to the dollar’s path, TD Securities strategists including Mark McCormick wrote in a note. “While our signals are currently biased in favor of the USD, we’re suspicious about the durability of the King’s return”

In rates, Treasuries traded near session lows reached during London morning amid bigger losses in bunds after Reuters reported that the European Central Bank expects inflation to hold above 3% next year. US yields are cheaper by 1bp-2bp across the curve led by long-end, steepening 2s10s, 5s30s spreads by ~1bp; US 10-year around 4.30% is 2bp cheaper on the day, bunds by an additional 2bp in the sector. Two-year TSY yields, which are more sensitive to Fed policy than longer maturities, stayed above 5%, while their 10-year peers held at 4. Short-dated European yields edged up, while UK gilts were little changed; European money markets shifted to price in a 25bp of rate hikes from the ECB this year, with 17bp of hike premium priced in for Thursday’s policy decision after the Reuters report dropped late Tuesday. Dollar IG issuance slate empty overnight and expected to be muted because of CPI; eleven names priced $19 billion Tuesday, taking weekly volume to $30 billion, and one elected to stand down. Treasury auction cycle concludes with $20 billion 30-year reopening; Tuesday’s 10-year stopped on the screws as it drew highest yield since 2007; WI 30-year yield at 4.380% is above auction stops since 2011 and ~19bp cheaper than last month’s. Focal points of US session are August CPI data and 30-year bond sale, following decent demand for Tuesday’s 10-year note auction.

In commodities, Crude gained after the IEA warned supply cuts by Saudi Arabia and Russia will drive volatility. West Texas Intermediate climbed for a second day and Brent extended gains above $92 per barrel as the IEA said production cuts will create a “significant supply shortfall.” Spot gold falls roughly $3 to trade near $1,911/oz.

To the day ahead now, and data releases include the US CPI print for August, along with UK GDP for July and Euro Area industrial production for July.

Market Snapshot

- S&P 500 futures little changed at 4,462.25

- MXAP down 0.2% to 161.48

- MXAPJ down 0.2% to 502.29

- Nikkei down 0.2% to 32,706.52

- Topix little changed at 2,378.64

- Hang Seng Index little changed at 18,009.22

- Shanghai Composite down 0.4% to 3,123.07

- Sensex up 0.5% to 67,530.25

- Australia S&P/ASX 200 down 0.7% to 7,153.91

- Kospi little changed at 2,534.70

- STOXX Europe 600 down 0.5% to 452.95

- German 10Y yield little changed at 2.66%

- Euro down 0.1% to $1.0740

- Brent Futures up 0.8% to $92.78/bbl

- Gold spot down 0.1% to $1,912.42

- U.S. Dollar Index little changed at 104.70

Top Overnight News from Bloomberg

- Tech stocks were in retreat as Oracle Corp. posted slowing cloud sales, while the euro and pound weakened on concern the Europe faces a growing threat of stagflation.

- The European Central Bank’s decision is a cliffhanger for investors, but even participants in the meeting have no inkling of the likely outcome, according to people familiar with the matter.

- The new Cold War is a business opportunity, and Mexico looks better placed than almost any other country to seize it.

- The global economy is shifting toward a higher-for-longer period for interest rates, making the coming flurry of monetary decisions across the developed world pivotal in mapping out that plateau.

- Apple Inc.’s biggest day of the year has arrived, and the company is set to unveil updated versions of its iPhone, smartwatch and AirPods.

- Arm Holdings Ltd.’s initial public offering is already oversubscribed by 10 times and bankers plan to stop taking orders by Tuesday afternoon, according to people familiar with the matter.

- The luxury armored train carrying North Korean leader Kim Jong Un crossed into Russia ahead of a summit with President Vladimir Putin that the US said would focus on supplying weapons for Moscow’s war on Ukraine.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were pressured following the tech-led declines on Wall St owing to the post-Apple event disappointment and with participants cautious ahead of the upcoming US CPI data. ASX 200 declined as tech stocks mirrored the underperformance seen in US counterparts and with nearly all sectors on the retreat aside from energy and utilities after further upside in oil prices. Nikkei 225 swung between gains and losses with early advances seen following mixed PPI data and the improvement in BSI large industry surveys, although the index eventually slipped with money markets now pricing the BoJ to exit negative rates in January compared to a previous pricing of an exit in September next year. Hang Seng and Shanghai Comp were initially kept afloat amid strength in the energy names and with developers underpinned as some cities further loosened restrictions for the sector, but then conformed to the soured mood.

Top Asian News

- China will extend tariff exemptions for imports of some US products until April 30th, 2024.

- Japanese Finance Minister Suzuki said PM Kishida asked him to stay on in the current job in the cabinet reshuffle, while he added that they need to respond appropriately to market moves and will decide on the size and content of the new economic package from now on, according to Reuters.

- PBoC will support prices to rise moderately, and will pay close attention to the effect of financial policies, via Central Bank Publication. Will strengthen the guidance of expectations.

European bourses are in the red, Euro Stoxx 50 -0.8%, following on from risk-off sentiment seen in the Asian markets overnight. Within Europe, sectors are primarily in the red featuring underperformance in Retail and Consumer Discretionary following earnings from Inditex while Auto names saw marked upside after von der Leyen’s announcement on Chinese EVs, though much of this has since pared. Stateside, futures are marginally weaker with the general tone a tentative one ahead of the US CPI report, ES -0.1%; NQ & RTY in-fitting. As a reminder, Asia-Pacific stocks were pressured following the tech-led declines on Wall St owing to the post-Apple event disappointment and with participants cautious ahead of the upcoming US CPI data

Top European News

- Hamburg Port Surges on MSC Bid as Billionaire Kühne Circles

- ECB Says Italy Bank Tax May Create Problems of Legal Uncertainty

- Sharp Decline in UK Economy in July Revives Recession Risk

- Tullow Shares Slump 11% After 1H Miss, Oil Guidance Narrowed

- Kingspan Says Deal Discussions With Carlisle Have Ended

- Saudi Oil Cuts Threaten Surge in Price Volatility, IEA Warns

FX

- The DXY is on a modestly firmer footing overall, but caged to a tight range above 104.50 in the run-up to the US CPI metrics later today.

- EUR and GBP are modestly softer against the Buck whilst the GBP is modestly softer against the EUR following soft UK GDP data and hawkish ECB sources.

- The antipodeans trade on either side of the spectrum, with the NZD resilient against the Buck following yesterday’s notable losses, whilst the AUD remains subdued by the woes in China alongside the broader cautious mood ahead of the US inflation metrics.

- Substantial strength was seen in the Polish Zloty after the Polish PM’s Adviser said the PLN has weakened beyond the optimal level for Poland and added the optimal level for EUR/PLN is between 4.40-4.60 range.

- Polish PM Adviser says the PLN has weakened beyond the optimal level for Poland; says optimal level for EUR/PLN is between 4.40-4.60 range; have the tools to ensure the PLN is at an optimal level.

- PBoC set USD/CNY mid-point at 7.1894 vs exp. 7.2783 (prev. 7.1986)

Fixed Income

- EGBs are under modest pressure with participants skewing their expectations hawkishly following Tuesday’s late-doors ECB sources piece; BTP-Bund yield spread has hit multi-month highs as a result, though remains markedly shy of the YTD peak.

- Gilts are firmer in contrast following particularly soft GDP data which has prompted a number of desks to trim their UK 2023 growth view, though a 25bp hike in September continues to be the base case from a market pricing perspective.

- Stateside, USTs are a touch softer taking cues from the above EGB move with US participants entirely focused on the upcoming CPI release.

Commodities

- Crude benchmarks are modestly firmer following the rally seen yesterday, which resulted in the contracts settling higher by around USD 1.50/bbl apiece.

- The weekly Private Inventory data proved to be bearish, with builds seen in headline crude stocks; following on from bullishly-received OPEC OMR and subsequent Brent oil price forecast upgrade via the EIA.

- Spot gold is subdued amid the firmer Dollar, but the yellow metal’s prices remain north of USD 1,900/oz and in a tight range in the run-up to the US CPI report, with the 21 DMA to the upside at USD 1,916.44/oz while downside levels include yesterday’s low of USD 1,907.62/oz.

- Base metals meanwhile now trade relatively mixed and with the breadth of the market narrow as markets await the US CPI data, 3M LME copper is back towards the session highs above USD 8,400/t after finding a floor near USD 8,350/t overnight.

- US Energy Inventory Data (bbls): Crude +1.2mln (exp. -1.9mln), Gasoline +4.2mln (exp. +0.2mln), Distillate +2.6mln (exp. +1.3mln), Cushing -2.4mln.

- All Libyan eastern oil ports have reopened following a shutdown on September 9th due to a storm, via the port agent.

- Hungarian Farm Minister Nagy says they have agreed on a unilateral extension of the import ban on Ukrainian grains beyond September 15th, agreement with Romania, Slovakia and Bulgaria. Ban will be imposed on a broader range of products.

- IEA OMR: Maintains 2023 and 2024 global oil demand growth forecast steady; says extension of oil-output cuts by Saudi and Russia will lock in a substantial market deficit through Q4 2023; OPEC+ cuts tempered by sharply higher Iranian oil flows.

Geopolitics

- Russian-installed Governor of Sevastopol said Ukraine launched an air attack on Sevastopol in Crimea, while the air attack sparked a fire at Sevastapol’s shipyard and 24 people were injured, according to Reuters.

- Russian President Putin and North Korean leader Kim met at the Vosotchny Cosmodrome for talks. Russian President Putin responded that it is why they have come to the Vostochny Cosmodrome when asked if Russia will help North Korea build satellites, while he added that they will discuss all issues and that North Korean Leader Kim is showing a big interest in Russian rocket equipment.

- Romanian Defence Ministry says elements of possible drone found on Romanian territory (NATO).

- North Korea fired projectiles believed to be ballistic missiles which landed outside of Japan’s exclusive economic zone, according to NHK citing the Japanese Coast Guard.

- Taiwan’s Defence Ministry said 28 Chinese military aircraft entered Taiwan’s air defence zone on Wednesday morning and some Chinese aircraft crossed the Bashi channel to carry out drills with Chinese carrier Shandong, while it also showed a picture of a Taiwanese warship shadowing the Shandong.

US Event Calendar

- 07:00: Sept. MBA Mortgage Applications -0.8%, prior -2.9%

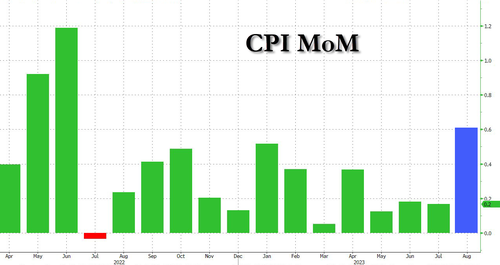

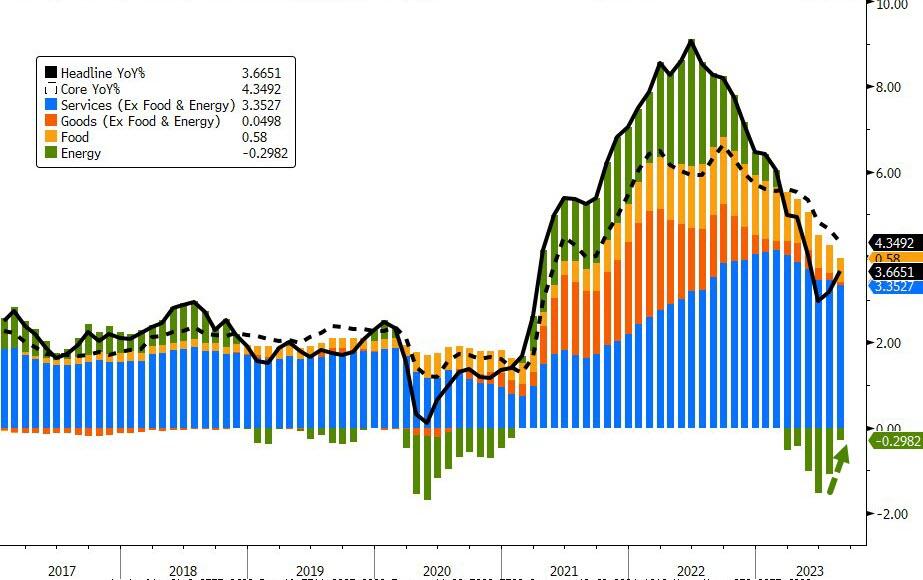

- 08:30: Aug. CPI YoY, est. 3.6%, prior 3.2%

- 08:30: Aug. CPI MoM, est. 0.6%, prior 0.2%

- 08:30: Aug. CPI Ex Food and Energy YoY, est. 4.3%, prior 4.7%

- 08:30: Aug. CPI Ex Food and Energy MoM, est. 0.2%, prior 0.2%

- 08:30: Aug. Real Avg Weekly Earnings YoY, prior 0.2%

- 08:30: Aug. Real Avg Hourly Earning YoY, prior 1.1%

- 14:00: Aug. Monthly Budget Statement, est. -$230b, prior -$219.6b

DB’s Jim Reid concludes the overnight wrap

Welcome to what is likely to be the most inflationary monthly US CPI day since June 2022 when the headline YoY rate was 9.1%. This will be followed by a knife-edge ECB’s policy decision tomorrow where market pricing is now pointing to a 53% chance of a hike. So it doesn’t get much more finely balanced than that.

For the US CPI print today, our economists are expecting monthly headline CPI to come in at +0.61%, which as discussed would be the fastest pace of monthly inflation since June 2022 thanks to the impact of higher gasoline prices. That’s in line with the consensus for a +0.6% print, as well as inflation swaps that are pricing in a +0.64% print so broadly speaking that’s the level markets will be benchmarking against. Assuming we get a monthly 0.6% print, then that would push up the year-on-year CPI print by four-tenths to +3.7%. But since higher gasoline prices won’t affect the core CPI number, they see that coming in at just +0.22% on a monthly basis, which would take the year-on-year core CPI print down four-tenths to 4.3%. See their full preview here for further details.

Whilst energy prices are expected to push up the CPI print today, there was little sign of further relief in the pipeline ahead, since Brent Crude oil prices closed above $92/bbl for the first time since November. That came as data from OPEC showed that oil markets faced a 3.3 million barrel per day shortfall in Q4, which is creating a very tight market. It’s also led to a notable uptick in inflation expectations, with the 2yr US breakeven (+4.4bps) now at 2.24%, which is its highest level since late April. This drove the 2yr Treasury yield back above 5% and to its highest level in over two weeks (+3.0bps to 5.02%) but a decline in real rates meant that the 10yr yield still ended the day -0.9bps lower at 4.28%.

With fresh signs of inflationary pressures, investors also moved to price in a growing chance that the ECB would in fact go ahead with another hike tomorrow. In fact, overnight index swaps are now pricing a better-than-even chance of a 25bp hike at 53%, up from 41% on Monday and 24% a week earlier. So this is something markets have been taking increasingly seriously. Then late yesterday evening we saw a Reuters story saying the updated ECB forecasts will see 2024 inflation at above 3%, bolstering the case for another hike on Thursday, according to “a source with direct knowledge of the discussion”. While a 2024 inflation forecast a touch above 3% would not be a major surprise, such a story shortly before the meeting is rather unusual for the ECB. The euro initially rallied by around +0.30% against the dollar following the report but has given half back in Asia.

Against that backdrop, but before the Reuters report, sovereign bond yields moved modestly higher across Europe on Tuesday, with those on 10yr bunds (+0.4bps), OATs (+0.8bps) and BTPs (+0.7bps) all rising. And there were larger moves at the front-end, with yields on 2yr German debt up +3.1bps.

It was a different story in the UK, where yields on 10yr gilts fell by -5.6bps yesterday. That followed some weaker-than-expected employment data, with the number of payrolled employees falling -1k in August (vs. +30k expected). Furthermore, the unemployment rate over the three months to July rose from 4.2% to 4.3%, which is its highest level since September 2021. In response, investors moved to lower the odds of another hike from the BoE next week to 77.5%, which is the smallest chance of a September hike since early June.

Equities generally saw a weak performance yesterday, with the S&P 500 down by -0.57%, whilst Europe’s STOXX 600 also fell -0.18%. Tech stocks led the moves lower in the US, with the NASDAQ (-1.04%) and the “Magnificent Seven” (-1.52%) posting larger declines. That included Apple, which fell -1.71% after the company unveiled their new iPhone. The stock did partially recover late in the US session having traded -2.5% lower intra-day, and was actually a mid-ranking performer amid the “Magnificent Seven” by the end of the day (with Tesla the weakest at -2.23%). Staying with tech, Oracle (c.$300bn market cap) fell -13.5%, its’ worst day since 2002 after a cloud sales disappointment. On the other hand, energy stocks in the S&P 500 (+2.31%) were the biggest sectoral outperformer thanks to the latest rise in commodity prices. The Dow Jones index (-0.05%) and small cap Russell 2000 (+0.01%) were near flat.

Asian equity markets are softer this morning due to a sell-off in tech stocks. As I type, the Nikkei (-0.31%), Hang Seng (-0.14%), CSI (-0.66%), Shanghai Composite (-0.18%) and KOSPI (-0.12%) are edging lower. S&P 500 (-0.17%) and NASDAQ 100 (-0.13%) futures are also trading in the red.

In terms of data, producer prices in Japan rose +3.2% y/y in August (+3.3% expected), slowing from a revised +3.4% increase in the prior month.

Elsewhere, South Korea’s unemployment rate on a seasonally adjusted basis unexpectedly dropped to a record low of 2.4% in August from a level of +2.8% in July, thus putting pressure on the Bank of Korea to retain a hawkish bias.

There were a few other data releases out yesterday. One was the ZEW survey from Germany, where the current situation reading fell to a 3-year low of -79.4 (vs. -75.5 expected), but the expectations indicator ticked up to -11.4 (vs. -15.0 expected). Separately in the US, the NFIB’s small business optimism index fell to 91.3 in August (vs. 91.5 expected), ending a run of three consecutive increases in the measure.

To the day ahead now, and data releases include the US CPI print for August, along with UK GDP for July and Euro Area industrial production for July.

2 B) NOW NEWSQUAWK (EUROPE/REPORT)/

US futures tentative pre-CPI while EGBs/Gilts react to sources & GDP – Newsquawk US Market Open

WEDNESDAY, SEP 13, 2023 – 06:35 AM

- European bourses are in the red following the risk-off sentiment in APAC trade, US futures tentative pre-CPI

- European autos saw brief marked outperformance on von der Leyen’s comments, though this has since pared

- DXY is on a firmer footing with EUR & GBP softer while the PLN experienced marked appreciation after the Polish PM’s advisor spoke

- EGBs softer after hawkish ECB sources while Gilts remain in the green after particularly soft growth data; USTs under marginal pressure pre-CPI/supply

- Crude benchmarks are modestly firmer continuing Tuesday’s upside while metals are mixed/subdued as the USD remains resilient

- Looking ahead, highlights include US CPI & supply

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses are in the red, Euro Stoxx 50 -0.8%, following on from risk-off sentiment seen in the Asian markets overnight.

- Within Europe, sectors are primarily in the red featuring underperformance in Retail and Consumer Discretionary following earnings from Inditex while Auto names saw marked upside after von der Leyen’s announcement on Chinese EVs, though much of this has since pared.

- Stateside, futures are marginally weaker with the general tone a tentative one ahead of the US CPI report, ES -0.1%; NQ & RTY in-fitting.

- As a reminder, Asia-Pacific stocks were pressured following the tech-led declines on Wall St owing to the post-Apple event disappointment and with participants cautious ahead of the upcoming US CPI data.

- Click here for more detail.

FX

- The DXY is on a modestly firmer footing overall, but caged to a tight range above 104.50 in the run-up to the US CPI metrics later today.

- EUR and GBP are modestly softer against the Buck whilst the GBP is modestly softer against the EUR following soft UK GDP data and hawkish ECB sources.

- The antipodeans trade on either side of the spectrum, with the NZD resilient against the Buck following yesterday’s notable losses, whilst the AUD remains subdued by the woes in China alongside the broader cautious mood ahead of the US inflation metrics.

- Substantial strength was seen in the Polish Zloty after the Polish PM’s Adviser said the PLN has weakened beyond the optimal level for Poland and added the optimal level for EUR/PLN is between 4.40-4.60 range.

- Polish PM Adviser says the PLN has weakened beyond the optimal level for Poland; says optimal level for EUR/PLN is between 4.40-4.60 range; have the tools to ensure the PLN is at an optimal level.

- PBoC set USD/CNY mid-point at 7.1894 vs exp. 7.2783 (prev. 7.1986)

- Click here for more detail.

- Click here for the Option Expires for the NY Cut.

FIXED INCOME

- EGBs are under modest pressure with participants skewing their expectations hawkishly following Tuesday’s late-doors ECB sources piece; BTP-Bund yield spread has hit multi-month highs as a result, though remains markedly shy of the YTD peak.

- Gilts are firmer in contrast following particularly soft GDP data which has prompted a number of desks to trim their UK 2023 growth view, though a 25bp hike in September continues to be the base case from a market pricing perspective.

- Stateside, USTs are a touch softer taking cues from the above EGB move with US participants entirely focused on the upcoming CPI release.

- Click here for more detail.

COMMODITIES

- Crude benchmarks are modestly firmer following the rally seen yesterday, which resulted in the contracts settling higher by around USD 1.50/bbl apiece.

- The weekly Private Inventory data proved to be bearish, with builds seen in headline crude stocks; following on from bullishly-received OPEC OMR and subsequent Brent oil price forecast upgrade via the EIA.