sorry that today’ report is not too details as I was not feeling well throughout the day.

thanks

h

GOLD PRICE CLOSED: DOWN $1.35 TO $1818.35

SILVER PRICE CLOSED: DOWN $0.08 AT $20.88

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1819.70.

Silver ACCESS CLOSE: 20.96

SEPT 27//SHANGHAI GOLD

Shanghai Gold Benchmark Price

USD oz  AM2014.57

AM2014.57

PM1985.03

Historical SGE Fix

premium $122,00

xxxxxxxxxxxxxxxxxx

Bitcoin morning price:,

Bitcoin: afternoon price: $27,532 DOWN 253 dollars

Platinum price closing $860.75 DOWN $9.60

Palladium price; $1148.70 DOWN $22.05

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,494,60 down 6.40 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1493.64 DOWN 16.30 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1724.93 DOWN 17.40 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: OCTOBER 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,818.500000000 USD

INTENT DATE: 10/04/2023 DELIVERY DATE: 10/06/2023

FIRM ORG FIRM NAME ISSUED STOPPED

323 C HSBC 139

323 H HSBC 2

357 C WEDBUSH 4

435 H SCOTIA CAPITAL 7

726 C CUNNINGHAM COM 3

737 C ADVANTAGE 134 7

TOTAL: 148 148

MONTH TO DATE: 8,735

JPMorgan stopped 0/148 contracts.

FOR OCT.:

GOLD: NUMBER OF NOTICES FILED FOR OCT/2023. CONTRACT: 148 NOTICES FOR 14800 OZ or .4603 TONNES

total notices so far: 8735 contracts for 873500 oz (27.169 tonnes)

FOR OCT:

SILVER NOTICES:17 NOTICE(S) FILED FOR 85,000 OZ/

total number of notices filed so far this month : 334 for 1,670,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $1.35

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : / HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A HUGE WITHDRAWAL OF OF 5.77 TONNES OF GOLD INTO THE GLD.

INVENTORY RESTS AT 869.31 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 8 CENTS AT THE SLV// WOW!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE DEPOSIT OF 8.328 MILLION OZ// (MASSIVE FRAUD)

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 450.211 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY STRONG SIZED 569 CONTRACTS TO 125,278 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS STRONG SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG $0.34 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. TAS ISSUANCE WAS A GIGANTIC SIZED 952 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 922 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.34). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A GIGANTIC SIZED GAIN OF 2027 OI CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

A MEGA HUMONGOUS ISSUANCE OF EXCHANGE FOR PHYSICALS( 2596 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.530 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 80,000 OZ QUEUE JUMP//NEW STANDING 1.785 MILLION O///STRONG SIZED COMEX OI LOSS/ HUGE SIZED EFP ISSUANCE/VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 922 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -569 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 4 days, total 9522 contracts: OR 47.610 MILLION OZ (2380 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 47.610 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 47.610 MILLION OZ (THIS IS GOING TO BE A HUGE MONTH FOR EFP ISSUANCE//AND MOST LIKELY A NEW RECORD)

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 569 CONTRACTS WITH OUR STRONG LOSS IN PRICE OF $0.34 IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A MEGA HUMONGOUS EFP ISSUANCE CONTRACTS: 2596 ISSUED FOR OCT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A SMALL INITIAL SILVER OZ STANDING FOR SEPT OF 1.532 MILLION OZ FOLLOWED BY TODAY’S 80,000 OZ QUEUE JUMP:NEW TOTAL STANDING 1.785 MILLION OZ /// WE HAVE A HUGE SIZED GAIN OF 2027 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GIGANTIC SIZED 922 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION. THE NEW TAS ISSUANCE WEDNESDAY NIGHT (922) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 17 NOTICE(S) FILED TODAY FOR 85,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A TINY SIZED 1857 CONTRACTS TO 431,374 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: + ADDED 139 CONTRACTS

WE HAD A TINY SIZED DECREASE IN COMEX OI ( 148 CONTRACTS) WITH OUR $7.40 LOSS IN PRICE//WEDNESDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 16.562 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG 24,400 OZ QUEUE JUMP/NEW STANDING 27.767 TONNES/ + /A STRONG (AND CRIMINAL) ISSUANCE OF 1060 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR $7.40 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 5293 OI CONTRACTS (16.463 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5145 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 431,374

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5293 CONTRACTS WITH 148 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 5145 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5293 CONTRACTS OR 16.463 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG 1060 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5145 CONTRACTS) ACCOMPANYING THE TINY SIZED GAIN IN COMEX OI (148) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 5293 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 16.562 TONNES FOLLOWED BY TODAY’S 18,600 OZ QUEUE JUMP//NEW STANDING 27.039 TONNES// /// 3) ZERO LONG LIQUIDATION BUT CONSIDERABLE TAS LIQUIDATION AND SOME SPEC SHORT COVERINGS DURING THE COMEX SESSION //4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 2041 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT :

TOTAL EFP CONTRACTS ISSUED: 19,402 CONTRACTS OR 1,940,200 OZ OR 60.348 TONNES IN 4TRADING DAY(S) AND THUS AVERAGING: 4851 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN4 TRADING DAY(S) IN TONNES 60.348 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 60.348/3550 x 100% TONNES 1.69% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 60.348 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A STRONG SIZED 569 CONTRACTS OI TO 125,278 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A MEGA GIGANTIC 2596 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 3326 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2596 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 569 CONTRACTS AND ADD TO THE 2596 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2027 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 10.135 MILLION OZ

OCCURRED DESPITE OUR HUGE $0.34 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED //Hang Seng CLOSED UP 18.03 PTS OR 0.10% /The Nikkei CLOSED UP 548.48 PTS OR 1.80% //Australia’s all ordinaries CLOSED UP 0.50 % /Chinese yuan (ONSHORE) closed /OFFSHORE CHINESE YUAN CLOSED UP TO 7.3169 /Oil DOWN TO 82.76 dollars per barrel for WTI and BRENT DOWN AT 84.65 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 148 CONTRACTS TO 431,374 DESPITE OUR STRONG LOSS IN PRICE OF $7.40 ON TUESDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF OCT..… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5145 EFP CONTRACTS WERE ISSUED: : DEC 5145 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5145 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 5293 CONTRACTS IN THAT 5145 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A TINY SIZED GAIN OF 148 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $7.40//WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A FAIR 1060 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: OCT (27.767) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 27.767 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $7.40) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG GAIN OF 5293 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A CONSIDERABLE T.A.S. LIQUIDATION ON THE FRONT END OF TUESDAY’S TRADING. THE T.A.S. ISSUED ON TUESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 16.463 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR OCT. (16.562 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 24,400 OZ QUEUE JUMP//NEW TOTALS STANDING:27.767 TONNES ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $7.40. FOR THE PAST WEEK, THE SPECULATORS HAVE GONE MASSIVELY SHORT WITH OUR BANKERS NET LONG. THE BIG QUESTION IS WHEN WILL THE BANKERS PULL THE PLUG ON OUR SPECS.

WE HAD + ADDED 139 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 5293 CONTRACTS OR 529,300 OZ OR 16.463 TONNES.

Estimated gold volume today:// 165,517 poor

final gold volumes/yesterday 205,170 fair/

//speculators have left the gold arena

//OCT 5/ /// THE OCT. 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 30,537.725 oz OZ ASAHIA HSBC 2 KILOBARS MALCA . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 148 notice(s) 14800 OZ .4603 TONNES |

| No of oz to be served (notices) | 192 contracts 19200 oz 0.597 TONNES |

| Total monthly oz gold served (contracts) so far this month | 8753 notices 875300 OZ 26.167 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: 0 oz

customer deposits: 0

total customer deposits: 0 oz

we had 3 customer withdrawals

i) Out of Brinks: 64.302 oz (2 kilobars)

ii) Out of Malca: 1003.749 oz

iii) Out of Asahi: 29,469.674 oz

total withdrawals 30,537.725. oz

Adjustments; 4 dealer to customer

i)HSBC: 4822.60 oz

ii) Looms: 6365.898 oz

iii) Malca 6751.710oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCTOBER we have an oi of 340 contracts having GAINED 65 contracts. We had 179 contracts filed on Wednesday, so we gained 244 contracts or an additional 22400 oz will stand for delivery in this active delivery month of October. Somebody, for the 4th day in a row, was in urgent need of a huge supply of physical gold over here.

NOV LOST 100 CONTRACTS to stand at 1102

December LOST 2928 contracts down to 368,986 contracts.

We had 148 contracts filed for today representing 14800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 148 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT. /2023. contract month, we take the total number of notices filed so far for the month (8735 x 100 oz ), to which we add the difference between the open interest for the front month of OCT. (340 CONTRACTS) minus the number of notices served upon today 148 x 100 oz per contract equals 892,700 OZ OR 27.767 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT. contract month: No of notices filed so far (8735) x 100 oz + (340) {OI for the front month} minus the number of notices served upon today (148) x 100 oz) which equals 892,700 oz standing OR 27.767 TONNES

TOTAL COMEX GOLD STANDING: 27.767 TONNES WHICH IS HUGE FOR AN ACTIVE BUT GENERALLY WEAK DELIVERY MONTH. (OCT). Somebody is after a considerable amount of gold from the comex.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,023,223.140 OZ 62.93 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 20,786,829.070 OZ

TOTAL REGISTERED GOLD 10,190,827.783 (316.94 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,596,001.287 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,167,604 OZ (REG GOLD- PLEDGED GOLD) 254.04 tonnes//dropping like a stone

END

SILVER/COMEX

OCT 5

//2023// THE OCT 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 136,954.962 oz Brinks Delaware . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 607,580.100 oz CNT |

| No of oz served today (contracts) | 17 CONTRACT(S) (85,000 OZ) |

| No of oz to be served (notices) | 23 contracts (115,000 oz) |

| Total monthly oz silver served (contracts) | 334 Contracts (1,670,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposit customer account:

i) Into CNT: 607,580.100 oz

total customer deposit 607,580.100oz

JPMorgan has a total silver weight: 136.236 million oz/273.225 million or 48.38%

Comex withdrawals 2

i) Out of Brinks 122,871.300oz

ii)out of Delaware 14,083.662 o

total: 136,954.962 oz

adjustments: 0

TOTAL REGISTERED SILVER: 37.638 MILLION OZ//.TOTAL REG + ELIGIBLE. 273.225 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF OCT /2023 OI: 50 CONTRACTS HAVING LOST 115 CONTRACT(S). WE HAD 133 NOTICES FILED

ON MONDAY, SO WE GAINED 18 CONTRACTS AS WE HAD A QUEUE JUMP OF 90,000 OZ

NOVEMBER LOST 27 CONTRACTS TO STAND AT 522

DEC. LOST 3379 CONTRACTS TO STAND AT 109.729 .

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 34 for 170,000 oz

Comex volumes// est. volume today 57,976 //fair

Comex volume: confirmed yesterday 75,724 strong//

To calculate the number of silver ounces that will stand for delivery in OCT. we take the total number of notices filed for the month so far at 334 x 5,000 oz = 1,670,000 oz

to which we add the difference between the open interest for the front month of OCT (40) and the number of notices served upon today 17 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT/2023 contract month: 347 (notices served so far) x 5000 oz + OI for the front month of OCT (40) – number of notices served upon today (17 )x 500 oz of silver standing for the OCT contract month equates to 1.785 million oz.

There are 37.638 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

OCT 5/WITH GOLD DOWN $1.35 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:HUGE CHANGES: A MASSIVE WITHDRAWAL OF 5.77 TONNES OF GOLD FROM THE GLD// /// // INVENTORY RESTS AT 869.31 TONNES

OCT 4/WITH GOLD DOWN $7.40 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD/// : // //INVENTORY RESTS AT 875.08 TONNES

OCT 3/WITH GOLD DOWN $6.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD/// : // //INVENTORY RESTS AT 875.08 TONNES

OCT 2/WITH GOLD DOWN $19.35 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: LD/ : // //INVENTORY RESTS AT 873,64 TONNES

SEPT 29/WITH GOLD DOWN $11.15 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: LD/ : // //INVENTORY RESTS AT 873,64 TONNES

SEPT 28/WITH GOLD DOWN $13.45 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A HUGE WITHDRAWAL OF 4.88 TONNES OF GOLD OUT OF THE GLD/ : // //INVENTORY RESTS AT 873,64 TONNES

SEPT 26/WITH GOLD DOWN $XXX TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT 05 THE GLD/ : // //INVENTORY RESTS AT 878.52 TONNES

SEPT 26/WITH GOLD DOWN $13.40 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT 05 THE GLD/ : // //INVENTORY RESTS AT 878.52 TONNES

SEPT 22/WITH GOLD UP $5.70 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD/ : // //INVENTORY RESTS AT 878.83 TONNES

SEPT 21/WITH GOLD DOWN $25.60 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.58 TONNES OF GOLD FROM THE GLD/ : // //INVENTORY RESTS AT 878.25 TONNES

SEPT 19/WITH GOLD UP $0.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD : // //INVENTORY RESTS AT 880.217 TONNES

SEPT 18/WITH GOLD UP $8.40 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD : A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 880.217 TONNES

SEPT 15/WITH GOLD UP $13.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 1.055 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 879.70 TONNES

SEPT 14/WITH GOLD UP $1.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 4.63 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 882.01 TONNES

SEPT 13/WITH GOLD DOWN $2.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 12/WITH GOLD DOWN $11.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 11/WITH GOLD UP $4.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 8/WITH GOLD UP $0.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 7/WITH GOLD DOWN $0.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.22 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.69 TONNES

SEPT 6/WITH GOLD DOWN $8.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.81 TONNES

SEPT 5/WITH GOLD DOWN $13.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.97 TONNES

SEPT 1/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 31/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 30/WITH GOLD UP $8.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.59 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.23 TONNES

AUGUST 29/WITH GOLD UP 17.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.6 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.64 TONNES

AUGUST 28/WITH GOLD UP $6.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / //INVENTORY RESTS AT 884.04 TONNES

AUGUST 25/WITH GOLD DOWN $6.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 884.04 TONNES

AUGUST 24/WITH GOLD UP $0.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //INVENTORY RESTS AT 884.91 TONNES

AUGUST 23/WITH GOLD UP $21.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 4.32 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 884.91 TONNES

AUGUST 22/WITH GOLD UP $2.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.87 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 889.23 TONNES

AUGUST 21/WITH GOLD UP $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.60 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 890.10 TONNES

AUGUST 18/WITH GOLD UP $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 887.50 TONNES

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

GLD INVENTORY: 869.31 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 5/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : //A MASSIVE DEPOSIT OF 8.328 MILLION OZ INTO THE SLV// /.////INVENTORY RESTS AT 450.211 MILLION OZ

OCT 4/WITH SILVER DOWN 34 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 441.883 MILLION OZ

OCT 3/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 441.883 MILLION OZ

OCT 2/WITH SILVER DOWN 98 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 441.883 MILLION OZ

SEPT 29/WITH SILVER DOWN 28 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF 0.183 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 441.883 MILLION OZ

SEPT 28/WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF 4.88 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 442.066 MILLION OZ

SEPT 27/WITH SILVER DOWN 20 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF .641 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 448.392 MILLION OZ

SEPT 26/WITH SILVER DOWN 20 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF .641 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 448.392 MILLION OZ

SEPT 22/WITH SILVER UP 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 449.492 MILLION OZ

SEPT 21/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 449,033 MILLION OZ

SEPT 19/WITH SILVER UP 0 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.1 MILLION OZ INTO THE SLV. : // /.////INVENTORY RESTS AT 449.033 MILLION OZ

SEPT 18/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 1.651 MILLION OZ INTO THE SLV. : // /.////INVENTORY RESTS AT 441.332 MILLION OZ

SEPT 15/WITH SILVER UP 37 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.31 MILLION OZ FROM THE SLV. : // /.////INVENTORY RESTS AT 439.681 MILLION OZ

SEPT 14/WITH SILVER DOWN 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: : // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 13/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1,009 MILLION OZ INTO THE SLV//: // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 12/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO THE SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 11/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 7/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 6/WITH SILVER DOWN 36 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.373 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 5/WITH SILVER DOWN 69 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 734,000 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 437.891 MILLION OZ

SEPT 1/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 440.00 MILLION OZ

AUGUST 31/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 438.625 MILLION OZ

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.834 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 443.210 MILLION OZ

AUGUST 29/WITH SILVER UP 49 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 183,000 OF SILVER INTO THE THE SLV// /.////INVENTORY RESTS AT 445.044 MILLION OZ

AUGUST 28/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.281 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 444.861 MILLION OZ

AUGUST 25/WITH SILVER UP ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 446.145 MILLION OZ

AUGUST 24/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.651 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 448.896 MILLION OZ

AUGUST 23/WITH SILVER UP 94 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FROM THE SLV// /.////INVENTORY RESTS AT 450.547 MILLION OZ

AUGUST 22/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: /.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 21/WITH SILVER UP 59 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 917,0000 OZ FROM THE SLV//.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 18/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

CLOSING INVENTORY 441.883 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

This is a big story : a massive 77 tonnes of central bank buying. This is real physical moving into central bank coffers!

Central Bank Gold Buying Continued To Sizzle In August

THURSDAY, OCT 05, 2023 – 09:25 AM

Central bank gold buying continues to sizzle.

Central banks globally added a net 77 tons to their reserves in August, according to the latest data compiled by the World Gold Council.

It was the third straight month of net purchases. Over the last three months, net gold buying by central banks totaled 219 tons.

In March, April and May, central banks reported net gold sales, primarily due to Turkey selling 160 tons of gold over that three-month period. According to the World Gold Council, this was a specific response to local market dynamics and didn’t likely reflect a change in the Turkish central bank’s long-term gold strategy.

Turkey returned to buying gold in June and added another 14.7 tons in August, joining China, Poland and Uzbekistan as the biggest buyers for the month.

According to the World Gold Council, the Turkish government reinstated gold import quotas in early August. There was some speculation that domestic shortages could lead to central bank gold sales to meet demand, but this clearly wasn’t the case.

The People’s Bank of China ranked as the largest buyer in August, adding 28.9 tons of gold to its holdings. It was the 10th consecutive month of buying for the Chinese central bank. China is the largest gold buyer year-to-date, having increased its official reserves by 166 tons since the beginning of the year and 217 tons since it resumed official purchases last November. The People’s Bank of China now officially holds 2,165 tons of gold, making up 4% of its total reserves.

China has a history of adding to reserves and then going silent.

The People’s Bank of China accumulated 1,448 tons of gold between 2002 and 2019, and then reported nothing for more than two years before resuming reporting last fall.

Many speculate that the Chinese continued to add gold to its holdings off the books during those silent years.

In fact, there has always been speculation that China holds far more gold than it officially reveals. As Jim Rickards pointed out on Mises Daily back in 2015, many people speculate that China keeps several thousand tons of gold “off the books” in a separate entity called the State Administration for Foreign Exchange (SAFE).

Last year, there were large unreported increases in central bank gold holdings. Central banks that often fail to report purchases include China and Russia. Many analysts believe China is the mystery buyer stockpiling gold to minimize exposure to the dollar.

The National Bank of Poland added 14.9 tons of gold to its reserves. That brings its year-to-date total to 88 tons.

In the fall of 2021, Bank of Poland President Adam Glapiński said the central bank planned to add 100 tons of gold to its reserves in 2022. It’s unclear why the bank didn’t follow through, but it is now just 12 tons short of that stated goal.

When he announced the plan to expand its gold reserves, Glapiński said holding gold was a matter of financial security and stability.

Gold will retain its value even when someone cuts off the power to the global financial system, destroying traditional assets based on electronic accounting records. Of course, we do not assume that this will happen. But as the saying goes – forewarned is always insured. And the central bank is required to be prepared for even the most unfavorable circumstances. That is why we see a special place for gold in our foreign exchange management process.”

India has been buying relatively small amounts of gold for the last four months. The Reserve Bank of India increased its holdings by 1.9 tons in August.

The RBI added 7 tons in Q1. Since resuming buying in late 2017, the Reserve Bank of India has purchased over 200 tons of gold. In August 2020, there were reports that the RBI was considering significantly raising its gold reserves.

Russia reported a 3.1-ton increase in its gold reserves. This brings the country’s gold holdings back to where they were at the beginning of the year. Russia was a big buyer prior to its invasion of Ukraine. Last month, there were reports that Russia would recommence the buying of foreign currency and gold in the coming months, but there were few details about the plan.

Uzbekistan has cycled back to buying with an 8.7-ton gold purchase. It is not uncommon for banks that buy from domestic production – such as Uzbekistan and Kazakhstan – to switch between buying and selling.

Kazakhstan reported a small half-ton purchases in August.

Three other central banks bought gold in August.

- The Czech Republic – 1.7 tons

- Kyrgyz Republic – 0.7 tons

- Singapore – 1.6 tons

There were no significant sales reported in August.

Bloomberg reported that Bolivia “monetized” 17 tons of its gold reserves between May and August following the enactment of a law authorizing the central bank to utilize its gold reserves. But according to the World Gold Council, it’s unclear what is meant by “monetize.” Currently, data Central Bank of Bolivia gold reserves is not available after April.

The WGC characterized central bank gold buying as “healthy.”

Even accounting for the net sales earlier in the year, the pace of buying so far this year suggests that we are on course for another strong annual total.”

Even with Turkey’s big sales earlier this year, net central bank gold purchases totaled 387 tons through the first half of the year. That was the highest first-half total since the organization started compiling quarterly data in 2000. This continued the trend of increasing gold reserves we saw last year.

Total central bank gold buying in 2022 came in at 1,136 tons. It was the highest level of net purchases on record dating back to 1950, including since the suspension of dollar convertibility into gold in 1971. It was the 13th straight year of net central bank gold purchases.

According to the 2023 Central Bank Gold Reserve Survey recently released by the World Gold Council, 24% of central banks plan to add more gold to their reserves in the next 12 months. Seventy-one percent of central banks surveyed believe the overall level of global reserves will increase in the next 12 months. That was a 10-point increase over last year.

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

James Rickards..

Something “Big & Stupid” Is Coming…

WEDNESDAY, OCT 04, 2023 – 09:45 AM

Authored by James Rickards via DailyReckoning.com,

With debt levels reaching all-time highs in major developed and developing economies, and with debt-to-GDP ratios also in record territory (not including contingent liabilities such as Social Security, health care and other entitlements, which make matters worse), it seems time to consider just how nations will deal with this problem.

The debt crisis may not be imminent, but it is unavoidable. When it happens, it may present the greatest financial disaster of all time. It’s never too soon for investors to consider the fallout.

When you issue debt in a currency you print, there’s no need for default in the sense of non-payment.

You can just have the central bank buy the debt (by printing money). This is the situation today in the U.S., Japan, the U.K. and the European Monetary Union (the countries that use the euro). They all have huge debt burdens, but they all have central banks that can simply buy the debt by printing money to avoid default.

Non-Payment Is Not the Issue

There are many bad consequences to printing money and storing up debt on central bank balance sheets, but non-payment of debt is not one of them. This is the mantra of the Modern Monetary Theorists (MMT) and their thought leader Stephanie Kelton.

In my view, MMT is garbage as economic policy, but the no-default tenet is valid. George Soros says the same thing.

That said, we are well past the point where the debt can be managed with real growth. That threshold is about a 90% debt-to-GDP ratio. A 60% debt-to-GDP ratio is even more comfortable and can be managed.

Unfortunately, the major reserve currency economies are all well past the 90% ratio as are those of many smaller countries. The U.S. ratio is 134%, an all-time high. The U.K. ratio is 102%. France is 111%. Spain is 112%. Italy is 145%.

China reports a figure of 77% but this is highly misleading because it ignores provincial debt for which Beijing is ultimately responsible. China’s actual figure is over 200% when provisional debt is included.

The champion debtor is Japan at 261%. The only major economy with a halfway respectable ratio is Germany at 67%. It’s Germany’s misfortune that they are probably responsible for the rest of Europe through the ECB Target2 system.

All these countries are headed for default. But we must consider the different ways to conduct a default.

There are three basic ways to default: non-payment, inflation and debt restructuring. You can take non-payment off the table for the reason mentioned above — you can always just print the money.

The same goes for restructuring. Inflation is clearly the best way to default. You pay back the money in nominal terms, but it’s worth very little in real terms. The creditor loses and the debtor countries win.

Nice and Easy Does It

The key to inflating away the real value of debt is to go slowly. It’s like stealing money from your mother’s purse. If she has $50 and you take $40, she’ll notice. If you take one dollar, she won’t notice. But a dollar stolen every day adds up over time.

This is what the U.S. did from 1945–1980. At the end of World War II, the U.S. debt-to-GDP ratio was 120% (about where it is now). By 1980, the ratio was 30%, which is entirely manageable.

Of course, nominal debt and GDP soared, but nominal GDP went up faster than nominal debt, so the ratio fell. If you can keep inflation around 3% and interest rates around 2% and exert fiscal discipline (which we did under Eisenhower, Kennedy, Nixon and Ford), the nominal GDP will grow faster than nominal debt (due to the Fed capping rates).

If you improve the ratio by, say, 2% per year and keep it up for 35 years (1945–1980), you can cut the ratio by 70%. That’s what we did.

The key was to do it slowly (like stealing from your mom’s purse). Almost no one noticed the decline in the real value of money until we got to the blow-off stage (1978–1981). But by then it was mission accomplished.

So there are two ways to deal with excessive debt: fiscal discipline and inflation. From 1945–1980, the U.S. did just that. If you run inflation at 3% and interest rates are 2%, you melt the real value of debt. If you exert fiscal discipline relative to GDP, you decrease the nominal debt-to-GDP ratio.

We did both.

The reason the debt-to-GDP ratio is back up to 134% is that Bush 45, Obama, Trump and Biden ignored the formula. Since 2000, fiscal policy has been reckless so the formula doesn’t work. The problem isn’t really “money printing” (most of the money the Fed prints just comes back to the Fed as excess reserves, so it doesn’t do anything in the real economy).

The problem is that nominal debt is going up faster than nominal GDP, so the debt-to-GDP ratio goes up. This dynamic will be made much worse by the huge increase in interest rates over the past 18 months.

You can’t borrow your way out of a debt crisis. We have also been unable to generate much inflation. Inflation ran below 2% for almost all of the 2009–2019 recovery.

Japan Writ Large

Looking at the global picture, it’s important to understand that Japan is just a bigger version of the U.S. They don’t have fiscal discipline and they can’t get inflation to save their lives. The only way out for Japan is hyperinflation, which will come but not yet.

Japan can probably keep the debt game going for a while. The crash will come when the currency collapses. When I started in banking, USD/JPY was 400. Those were the days!

A debt crisis is on the way. Something big and stupid (in the words of the brilliant analyst Stephanie Pomboy) is coming from policymakers to address the issue. But the solution won’t be a policy and it won’t be a plan. A crisis will just happen almost overnight and seem to come from nowhere.

But it will come.

END

This is important: Citibank has 85.5% of its deposits lack FDIC insurance

(Pam and Russ Martens)

Pam and Russ Martens: Despite Citibank’s record bailout in 2008, 85.5% of its deposits lack FDIC insurance

Submitted by admin on Thu, 2023-10-05 11:35Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Thursday, October 5, 2023

As evidenced by the speech that the chairman of the Federal Deposit Insurance Corp., Martin Gruenberg, delivered at a conference yesterday, the FDIC is very much aware that both the level of uninsured deposits and the concentration of those uninsured deposits among a handful of mega banks is a serious problem for the U.S. banking system.

Gruenberg didn’t name names, but we will do that in this article.

Gruenberg pointed out in his speech that year-end data for the three banks that failed this past spring indicated that anywhere from 90% to 70% of their deposits were uninsured. (During a banking panic, uninsured deposits are typically those that head for the exits at the fastest clip.)

But those three failed banks (Silicon Valley Bank, Signature Bank, and First Republic Bank) were minnows compared to the asset-size of the banking whales that now account for most uninsured deposits in the U.S. banking system.

According to the FDIC, as of June 30 there were 4,645 federally-insured commercial banks and savings associations in the United States. Uninsured deposits at all 4,645 institutions totaled $7.134 trillion at the end of the second quarter.

But according to call reports filed by JPMorgan Chase Bank, Bank of America, Wells Fargo, and Citigroup’s Citibank, as of June 30, just those four banks accounted for $4.185 trillion of uninsured deposits, or 59% of all uninsured deposits at all 4,645 federally-insured institutions. …

… For the remainder of the analysis:

END

(Bloomberg)

Forex reserves remain Asia’s first defense vs. relentless dollar

Submitted by admin on Wed, 2023-10-04 17:11Section: Daily Dispatches

By Subhadip Sircar and Swati Pandey

Bloomberg News

Wednesday, October 4, 2023

The dollar’s recent rally has been relentless. But Asia’s central banks have the firepower to limit the fallout.

Policy makers in the region have more than $5.5 trillion of foreign-exchange reserves that they can deploy to shore up their currencies, according to calculations by TD Securities, using data compiled by Bloomberg. The stockpile reached a record high of $5.9 trillion in 2021.

Focus is shifting to what steps authorities in the region may take after verbal warnings and stronger fixings failed to arrest the downdraft in their currencies. While exporters stand to benefit if their currencies weaken, a sustained bout of depreciation risks triggering capital outflows.

“Asian central banks have the firepower from their FX reserves like last year to intervene if they choose to,” said Alex Loo, Singapore-based Asia FX and macro-strategist at TD. “We think jawboning efforts may suffice for now.” …

… For the remainder of the report:

END

Your weekend reading material

(Alasdair Macleod)

Alasdair Macleod: Unwinding the financial system

Submitted by admin on Thu, 2023-10-05 11:25Section: Daily Dispatches

By Alasdair Macleod

Head of Research, GoldMoney, Toronto

via Schiff Gold, White Plains, New York

Thursday, October 5, 2023

This article looks at the collateral side of financial transactions and some significant problems that are already emerging.

At a time when there is a veritable tsunami of dollar credit in foreign hands overhanging markets, it is obvious that continually falling bond prices will ensure bear markets in all financial asset values leading to dollar liquidation. This unwinding corrects an accumulation of foreign-owned dollars and dollar denominated assets since the Second World War both in and outside the U.S. financial system.

Furthermore, collapsing collateral values, which are increasingly required backing for changing values in over $400 trillion nominal in interest rate swaps, are a new driver for the crisis, forcing bond liquidation, driving prices down, and yields higher. We are in a doom loop.

What action can the authorities take to ensure that counterparty risk from widespread failures won’t take out inadequately capitalised regulated exchanges?

It seems that they acted some time ago by giving central security depositories (the Depository Trust and Clearing Corp., Euroclear, and Clearstream) the right to pool securities on their registers and lend them out as collateral. Your investments, which you think you own, can be absorbed into the failing financial system without your knowledge.

This seems particularly relevant, given the appointment of JPMorgan Chase as custodian of the large gold exchange-traded fund, SPDR Trust (GLD). In a test case in the New York courts concerning Lehman’s failure, JPMC was given legal protection should it seize its customers’ assets.

This important erosion of property rights is poorly understood. But as the financial distortions are unwound, leading to unintended consequences such as bank failures and ultimately the collapse of the dollar-based fiat currency regime, the implication is that holders of physical gold ETFs will be left owning an empty shell at a time when they might have expected some protection from the collapse of the value of credit. …

… For the remainder of the analysis:

https://schiffgold.com/commentaries/unwinding-the-financial-system/

END

3,Chris Powell of GATA provides to us very important physical commentaries

end

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES//

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:ORANGE JUICE

END

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED

OFFSHORE YUAN: UP TO 7.3169

SHANGHAI CLOSED

HANG SENG CLOSED UP 18.03 PTS OR 0.10%

2. Nikkei closed UP 548.48 PTS OR 1.80 %

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 106.36 EURO RISES TO 1.0524 UP 18 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.807 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 148.85/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP// OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.9200***/Italian 10 Yr bond yield DOWN to 4.895*** /SPAIN 10 YR BOND YIELD DOWN TO 4.025…**

3i Greek 10 year bond yield RISES TO 4.330

3j Gold at $1822.60 silver at: 21.11 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 16 /100 roubles/dollar; ROUBLE AT 99.74//

3m oil into the 82 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 148.85// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.807% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9144 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9624 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.741 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.872 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 5.039 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 27.56…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 1 BASIS PTS AT 4.633

end

2.a Overnight: Newsquawk and Zero hedge:

USA EARLY MORNING REPORT

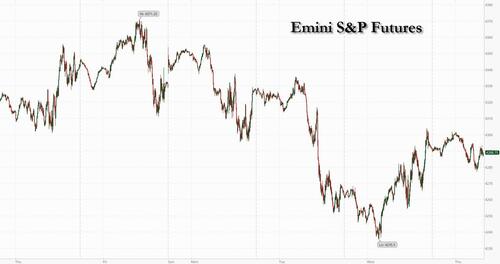

Nervous Futures Erase Early Losses With All Eyes On Yields

THURSDAY, OCT 05, 2023 – 08:16 AM

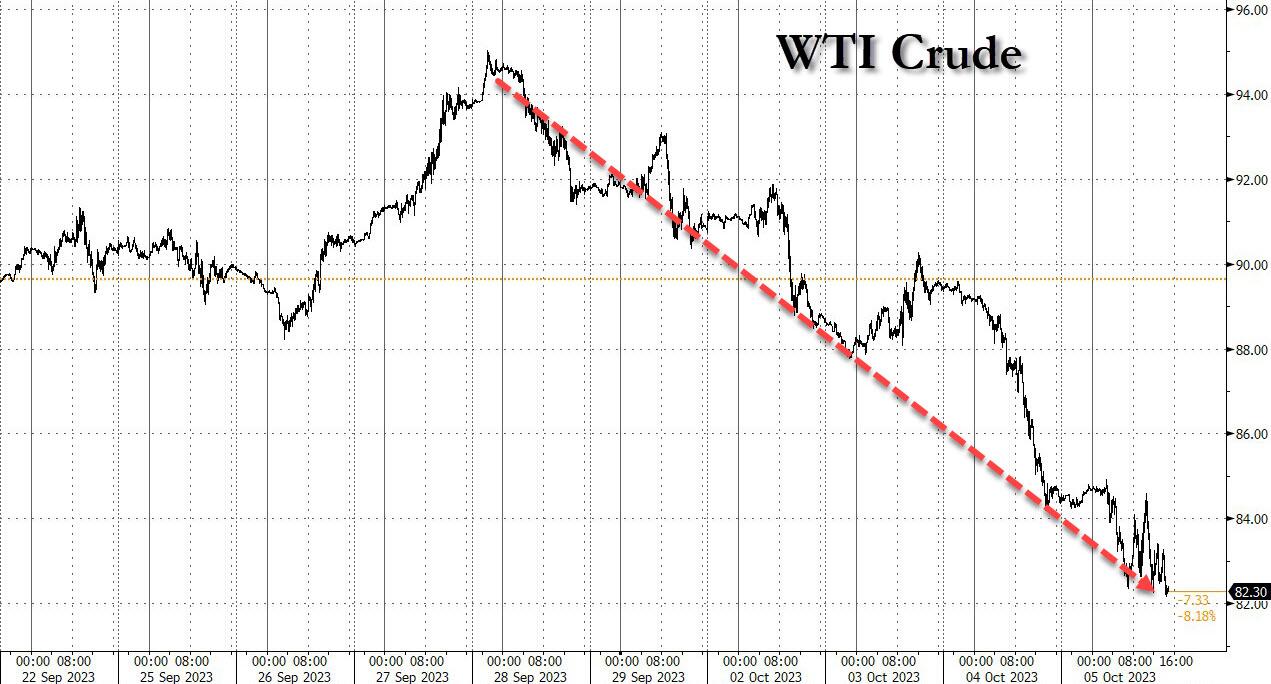

US equity futures were flat on Thursday, reversing earlier modest losses, with Asia and Europe both solidly in the green after days of losses as global markets steadied thanks to bonds halting their rout as investors looked ahead to more weak labor market data tomorrow. As of 7:45am, S&P 500 futures were unchanged at 4,298 and the yield on 10-year Treasuries was flat 4.71%. The dollar was steady while commodities extended their losses dragged by Energy. WTI has lost ~$10 in six trading sessions, -10.8%, and is virtually unchanged on the year after breaching $95 late last week. Today’s macro data focus includes Jobless Claims and Job Cuts; there are two Fed speakers and announcements on the next wave of bond auctions. Tomorrow we get the Sept NFP which according to JPM “may mean more than next week’s CPI.”

In premarket trading, Clorox falls as much as 4.1% after the cleaning-products maker said preliminary net sales dropped by 23%-28% in the quarter ended Sept 30 after a cyberattack that disrupted production. Prior to the attack, disclosed in mid-August, Clorox had been expecting “mid-single-digits” organic sales growth in the quarter. MaxCyte owner of a platform used in the cell therapy market, slumps 22% after the company posted preliminary third-quarter revenue that disappointed as customer demand wanes. It’s London shares slumped 30%. Rivian Automotive falls as much as 8% after the electric-vehicle maker announced plans to issue $1.5 billion in convertible debt and reported preliminary third-quarter revenue. Here are some other notable premarket movers:

- BioXcel Therapeutics (BTAI) falls 6.4% after Truist Securities analyst Robyn Karnauskas downgraded the biotech firm to hold from buy.

- Cambium Networks’ (CMBM) shares are plummeting 32%, after the wireless networking infrastructure company reported preliminary third-quarter revenue that prompted at least two analyst downgrades.

- Ceridian HCM Holding Inc. (CDAY) shares are up 2.1% after Needham upgraded the human capital management software company to buy from hold.

- Clorox (CLX) — the cleaning-products maker reeling from a cyberattack that disrupted production — falls 4.4% after saying preliminary net sales dropped by 23%-28% in the quarter ended Sept. 30.

- Nanobiotix ADRs (NBTX) sink 20% after the company said 10 deaths occurred within 180 days of enrollment of a dose-expansion trial for its investigational treatment for patients with locally advanced head and neck cancer.

- Orchard Therapeutics ADRs (ORTX) surge 97% after Japan’s Kyowa Kirin agreed to acquire the UK biopharmaceutical company for $387.4 million, or $16 per American depository share.

- UWM Holdings Corp. (UWMC) shares are up 2.8% after BTIG upgraded the mortgage finance company to buy from neutral.

Investor sentiment remains fragile after a painful selloff spiked volatility across markets this week driven by US bond yields soared to multi-year highs. Weekly US jobless claims data is due later today, and the monthly payrolls report will be released on Friday, which could cement bets on a November rate hike. Currently, swaps price a one-in-four chance of a Fed move next month.

“Friday’s payrolls data, and next week’s inflation number will decide whether the 10-year Treasury yield goes up to 5% or down to 4.5%,” Societe Generale strategist Kenneth Broux said. A higher-than-forecast jobs number could trigger “another wave of dollar-buying and bond-selling,” he added.

Despite nascent signs of market calm, strategists remain skeptical about the long-term economic toll of higher-for-longer interest rates. Echoing similar concerns from JPM and Goldman, overnight Barclays analysts wrote in a note that global bonds are doomed to keep falling unless a sustained slump in equities revives the appeal of fixed-income assets.

“There is no magic level of yields that, when reached, will automatically draw in enough buyers to spark a sustained bond rally,” analysts led by Ajay Rajadhyaksha said. “In the short term, we can think of one scenario where bonds rally materially. If risk assets fall sharply in the coming weeks.”

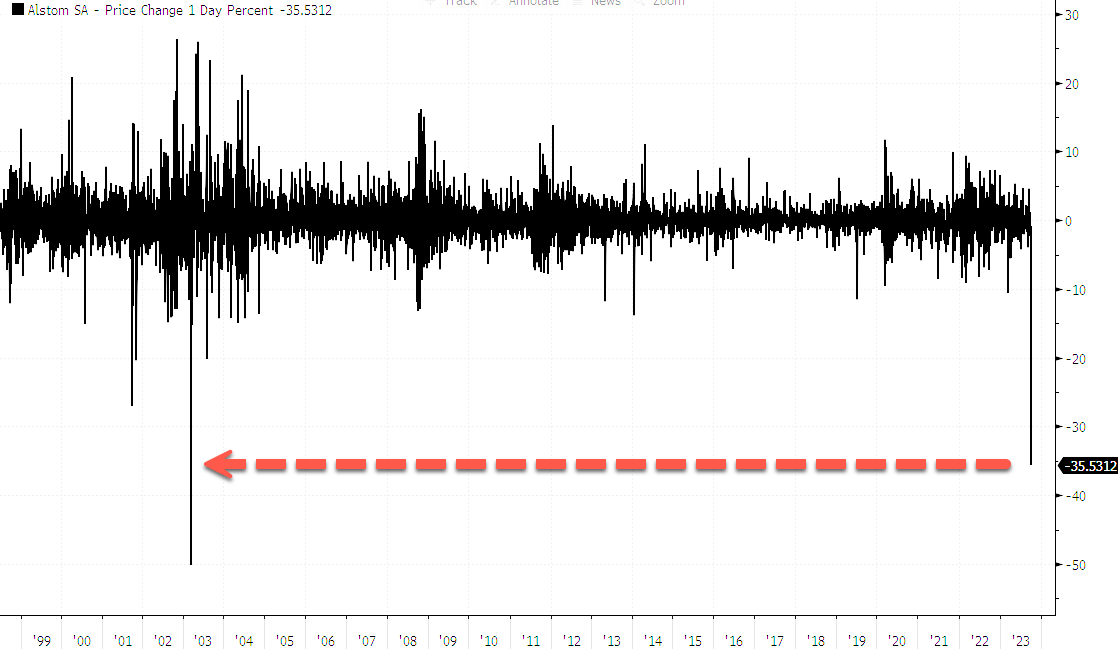

European stocks rose to session highs, with the Stoxx 600 rising 0.5% after a three-day decline. Among individual movers in Europe, Alstom SA shares plunged 35% after the French train maker slashed its financial guidance due to delays on UK contracts and a rise in inventories. Here are the biggest European movers:

- Pandora shares jumped as much as 10% in Copenhagen trading after the jewelry maker presented new financial targets, indicating higher growth rates and profitability over the next three years.

- SMA Solar shares jump as much as 17%, most since June, after the maker of photovoltaic systems boosted its sales forecast for the third time this year. Oddo also upgraded the German firm to outperform.

- Sandoz shares gain as much as 5.6% after the maker of copycat medicines that was spun off from Novartis gets a new overweight rating at Morgan Stanley, an outperform recommendation at ZKB, and is started with a buy at Berenberg based on its encouraging biosimilar pipeline.

- Redcare Pharmacy shares gain as much as 6.8% after the German online pharmacy reported what analysts said was “strong growth” in its preliminary third-quarter results.

- Imperial Brands gains as much as 1.9% after the cigarette maker announced a buyback of as much as £1.1 billion. The news could help the stock rally from recent lows, with UK regulatory concerns looking “overdone,” according to Citi.

- Alstom shares plunge as much as 38%, falling to the lowest level since 2005, after the French rail-equipment maker slashed its free cash flow forecast on a jump in inventories.

- Metro Bank shares slumped as much as 29% to a record low after Bloomberg News reported the UK lender has hired Morgan Stanley to explore a potential capital raise.

- Cofinimmo falls as much as 6.2% after an offering of shares in the Belgian real estate firm prices via BNP Paribas, ING, Belfius/Kepler and KBC at €60 apiece, representing about 7% discount to last close.

Earlier in the session, Asian stocks rebounded after a three-day slide that pushed the regional benchmark into a technical correction, as risk sentiment improved following an easing of this week’s selloff in US Treasuries. The MSCI Asia Pacific Index climbed 1.5%, the most in five weeks, driven by gains in the financial and technology groups. Equity benchmarks in Japan and Taiwan were among the top performers in the region. US stocks advanced overnight after data showing job gains cooled, helping ease fears over the Federal Reserve’s policy path and halting the recent surge in bond yields. Oil fell the most in more than a year overnight, helping lessen concern over inflation.

- Hang Seng initially lagged amid very light news flow and the continued absence of mainland participants, while the latest Hong Kong PMI data printed at a deeper-than-previous contraction. However, the momentum eventually picked up in Hong Kong amid the brightened mood across regional counterparts and after Sunac China’s offshore debt restructuring plans received court approval.

- Australia’s ASX 200 was positive following mostly improved trade data and with the gains led by yield-sensitive sectors including real estate and tech.

- Nikkei 225 outperformed on bargain buying with the index set to snap a five-day losing streak.

- KOSPI gained as participants shrugged off the firmer-than-expected CPI data which the BoK expects to stabilise into year-end.

In FX, the Bloomberg Dollar Spot Index pared an earlier fall to rise 0.1% ahead of initial jobless claims data due Thursday

- EUR/USD pared earlier gains to trade little changed on the day

- GBP/USD snapped Wednesday’s gain, falling 0.1% to 1.2119

- USD/JPY dropped 0.1% to 148.98 after hitting the day’s low of 148.26

In rates, Treasuries steadied, with the benchmark 10-year note reversing an earlier move higher to trade around 4.71%, some 4bps lower on the day, and well off 16-year highs hit this week. European government bonds edged lower; 10-year gilt yields rose 5 basis points to 4.63% while 10-year bund yields were 4 basis points higher at 2.95% German and UK long-end yields are up by 5bps and 4bps respectively. US 5s30s spread exceeds 17bp, widest since May, while 2s10s inversion lessens further. Front-end swaps price in around 7bp of rate-hike premium for Fed’s November policy meeting, down from around 9bp at Monday’s close. Dollar IG issuance slate includes MuniFin 3Y; two borrowers priced combined $1b on Wednesday as issuers paid 5bps in new-issue concession on order books that were 5.9 times covered.

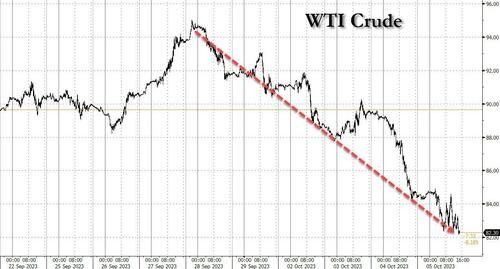

In commodities, oil prices add to Wednesday’s sharp decline, with WTI falling 1.2% to trade near $83.30. Spot gold is up 0.1%.

Bitcoin is subdued but remains north of $27,500 with price action uneventful.

Today’s US economic data slate includes September Challenger job cuts (7:30am), August trade balance and initial jobless claims (8:30am). Scheduled Fed speakers include Mester (9am), Kashkari (10:40am), Barkin (11:30am), Daly (12pm) and Barr (12:15pm).

Market Snapshot

- S&P 500 futures little changed at 4,294.50

- STOXX Europe 600 up 0.5% to 442.16

- MXAP up 1.1% to 154.02

- MXAPJ up 0.6% to 482.08

- Nikkei up 1.8% to 31,075.36

- Topix up 2.0% to 2,263.76

- Hang Seng Index up 0.1% to 17,213.87

- Shanghai Composite up 0.1% to 3,110.48

- Sensex up 0.7% to 65,692.31

- Australia S&P/ASX 200 up 0.5% to 6,925.49

- Kospi little changed at 2,403.60

- German 10Y yield little changed at 2.94%

- Euro up 0.1% to $1.0515

- Brent Futures up 0.1% to $85.93/bbl

- Gold spot up 0.0% to $1,821.90

- U.S. Dollar Index little changed at 106.72

Top Overnight News

- Taiwan’s headline CPI climbs to +2.93% in Sept (up from +2.53% in Aug and above the Street’s +2.5% forecast) while core eases to +2.48% (down from +2.57% in Aug). South Korea’s core CPI was flat M/M and inline w/the Street at +3.3%, but the headline number rose to +3.7%, up from +3.4% in Aug and ahead of the Street’s +3.5% forecast. WSJ

- Belgium’s intelligence service has been monitoring Alibaba’s main logistics hub in Europe for espionage following suspicions Beijing has been exploiting its growing economic presence in the west. FT

- UK construction activity fell more than expected in September and posted its biggest slide since May 2020, driven by a steep downturn in housing, according to a closely watched survey. FT

- Germany’s trade numbers for Aug fall short of expectations, with exports -1.2% (vs. the Street -0.6%) and imports -0.4% (vs. the Street +0.5%). RTRS

- Vladimir Putin’s cabinet is turning to increasingly irregular revenue-raising measures to fund a rapid rise in defense spending, which has tripled since Russia’s full-scale invasion of Ukraine. The Russian government has said it aims to spend a staggering Rbs10.8tn ($108bn) on defense next year, three times the amount allocated in 2021, the last year before the invasion, and 70 per cent more than was planned for this year. FT

- Ukrainian president Volodymyr Zelenskyy has said he is confident he still has broad US backing despite “strange” voices in Congress and the exclusion of more aid for Kyiv from a US spending deal. FT

- Deficits suddenly matter – it’s been decades since investors had to grapple with elevated spending/debt pushing Treasury yields higher, but this is now a growing part of the present narrative. WSJ

- JPMorgan Chase has stepped up the pace at which it is securitising billions of dollars of its loan portfolio in anticipation of proposed new US capital requirements for large banks, according to people familiar with the matter. FT

- Amazon and Microsoft’s cloud services face a UK antitrust probe into whether they made it hard for customers to switch or mix providers. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded higher as risk assets found reprieve after yields eased back from recent peaks following weak US ADP jobs data and a slump in oil prices. ASX 200 was positive following mostly improved trade data and with the gains led by yield-sensitive sectors including real estate and tech. Nikkei 225 outperformed on bargain buying with the index set to snap a five-day losing streak. KOSPI gained as participants shrugged off the firmer-than-expected CPI data which the BoK expects to stabilise into year-end. Hang Seng initially lagged amid very light news flow and the continued absence of mainland participants, while the latest Hong Kong PMI data printed at a deeper-than-previous contraction. However, the momentum eventually picked up in Hong Kong amid the brightened mood across regional counterparts and after Sunac China’s offshore debt restructuring plans received court approval.

Top Asian News

- Alibaba’s (9988 HK) logistics arm in Liege, Belgium is under scrutiny from Belgian intelligence over the use of sensitive data, according to FT.

- Sunac China’s (1918 HK) offshore debt restructuring plans received approval from a Hong Kong court.

- US Commerce Secretary Raimondo said TikTok poses national security risks, while she hopes to make some chips funding announcements this fall, according to Reuters.

- Taiwan is to probe four firms accused of helping Huawei build chip plants although Taipei said no violations of US trade sanctions have been confirmed so far, according to Nikkei.

- Apple (AAPL) supplier Foxconn (2317 TW) says Q4 is expected to grow significantly compared to Q3; with H2 a traditional peak season for the ICT industry, operations will ramp up sequentially. New product launch in September led to a strong revenue growth compared to prev. quarter, but the revenue experienced a decline YoY due to a high base. In Q3 for cloud and networking products, due to conservative customers pull-in revenue experienced a decline YY. For September, due to increasing allocations in smart consumer electronics products and rising shipment in auto components, revenue for components and other products showed significant growth YY, according to Reuters.

European bourses are choppy but ultimately trade flat at the time of writing in what has thus far been a session void of incremental macro news. Sectors in Europe are mixed, with outperformance in the Travel & Leisure sector as airlines welcome yesterday’s pullback in crude prices. Conversely, to the downside, Energy names lag. US futures saw broad-based losses with sentiment turning sour since the European cash open, coinciding with a slight rise in yields.

Top European News

- ECB’s Kazimir said September EZ core inflation confirmed ECB expectations and reiterated that he believes the last rate hike was the final one. He said we need to be convinced we are at the top of the rate cycle based on data available in December and March meetings, and when asked what would trigger a December hike, said this is not a scenario I’d like. He added we are trajectory of declining inflation, and inflation decline is taking somewhat longer. Kazimir added we should not at the moment use other tools such as balance sheet until we are certain we do not need to hike rates further, according to Reuters.

- ECB’s de Guindos said the current level of interest rates to help tame inflation; adding “we’re data dependent”. He added it is premature to discuss rate cuts.

- Low water levels after recent dry weather are preventing cargo vessels from sailing fully loaded on the Rhine river in Germany, with surcharges added to usual freight rates, according to traders cited by Reuters.

- BoE Monthly Decision Maker Panel data – September 2023: One-year ahead CPI inflation expectations increased slightly to 4.9% in September, up from 4.8% in August. Three-year ahead CPI inflation expectations remained flat at 3.2% in September. Expected year-ahead wage growth remained unchanged at 5.1% on a three-month moving average basis, though the single month reading for September at 5.2% was 0.2 percentage points higher than in August.

FX

- DXY index remains relatively contained between 106.500-840 confines and the Buck stayed broadly softer awaiting Challenger Layoffs, jobless claims and NFP on Friday for the next major fundamental driver.

- Antipodeans narrowly outperform with the AUD gleaning support from a wider-than-expected trade surplus.

- Pound was flagging even before a more contractionary than feared UK construction PMI. Cable remains capped by the 10 DMA and retreated towards 1.2100.

- Fix demand and exporter supply underpinned the Yen on the way from sub-149.00 to 148.27, and before the upturn in yields.

Fixed Income

- Having bounced further Wednesday’s lows, bonds are showing traits of fatigue and a reversion to the bear trend that was in place before their midweek reprieve.

- Bunds have regrouped after their retreat to 127.21 and are back above par alongside Eurozone peers bar Bonos.

- Gilts are underwater following a reverse from 92.37 to 91.94, irrespective of a deeper than anticipated contraction in the UK construction PMI.

- T-notes are lagging within a 107-09/106-31+ range ahead of Challenger Layoffs, jobless claims, trade and another busy slate of Fed orators.

- France sold EUR 9.94bln vs exp. EUR 9-10.5bln 3.50% 2033, 2.50% 2043, and 3.00% 2054 OAT.

- Spain sold EUR 6.44bln vs exp. EUR 5.5-6.5bln 3.50% 2029, 2.35% 2033 and 1.00% 2042 Bono.

Commodities

- Crude futures remain on the backfoot following yesterday’s mammoth decline which saw both contracts settle lower by over USD 5/bbl apiece.

- Dutch TTF is softer despite a twist in the Australian LNG saga in which unions are likely to vote to resume strikes at Chevron facilities after Australia’s Offshore Alliance said Chevron reneged on commitment given to FWC

- Spot gold is flat intraday awaiting tomorrow’s US labour market report, with the yellow metal uneventful within yesterday’s USD 1,815.50-30.39/oz parameters.