OCT 24//GOLD CLOSED DOWN ONLY BY $1.30 AFTER A RAID ORCHESTRATED BY OUR BANKERS AS OPTIONS EXPIRY WEEK BEGINS//SILVER CLOSED DOWN ONLY 8 CENTS TO $22.96//PLATINUM CLOSED DOWN $11.55 TO $888.70//PALLADIUM WAS DOWN $6.40 TO $1126,85//ESSENTIAL READING MATERIAL TODAY: DR LACALLE AND ESPECIALLY CONRAD BLACK//UPDATES ON ISRAEL VS HAMAS//COVID UPDATES// VACCINE INJURIES//USA DATA ON PMI//SWAMP STORIES FOR YOU TONIGHT//

435 H SCOTIA CAPITAL 9 661 C JP MORGAN 10 1 737 C ADVANTAGE 70 880 H CITIGROUP 75 905 C ADM 5

TOTAL: 85 85 MONTH TO DATE: 10,962

JPMorgan stopped 1.85 contracts.

FOR OCT.:

GOLD: NUMBER OF NOTICES FILED FOR OCT/2023. CONTRACT: 85 NOTICES FOR 85,000 OZ or 0.2643 TONNES

total notices so far: 10,962 contracts for 1,096,200 oz (34.096 tonnes)

FOR OCT:

SILVER NOTICES:1 NOTICE(S) FILED FOR 5,000 OZ/

total number of notices filed so far this month : 512 for 2,560,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES

GLD

WITH GOLD DOWN $1.30//

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : / HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.17 TONNES OF GOLD OUT OF THE GLD//

INVENTORY RESTS AT 860.07 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN 8 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 2.52 MILLION OZ INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 444.391 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY STRONG SIZED 693CONTRACTS TO 124,506 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS SMALL SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG $0.33 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. WE HAD SOME SPEC SHORT COVERING EPISODE IN MONDAY’S COMEX TRADING.. TAS ISSUANCE WAS A HUGE SIZED 791 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 791 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAD 693OI. CONTRACTS REMOVED FROM PRELIMINARY OI TO FINAL! WHAT AN ABSOLUTE FRAUD

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.33). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A TINY SIZED GAIN OF 42 OI CONTRACTS ON OUR TWO EXCHANGES AS THE SPEC SHORTS TRIED AGAIN DESPERATELY TO COVER THEIR SHORTFALLS WITH LITTLE SUCCESS.

WE MUST HAVE HAD:

A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS( 125 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.530 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP + 0 CONTRACTS OF EXCHANGE FOR RISK FOR 0.000 MILLION OZ TODAY+ 4.2 MILLION OZ EXCHANGE FOR RISK PRIOR////NEW STANDING IS THUS 2.640 MILLION OZ NORMAL SILVER DELIVERY + 4.2 EXCHANGE FOR RISK = 6.84 MILLION OZ/////SMALL SIZED COMEX OI GAIN/ SMALL SIZED EFP ISSUANCE/VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1104CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL – REMOVED 693 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT:

TOTAL CONTRACTS for 16 days, total 17,087 contracts: OR 85.435 MILLION OZ (1067 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 85.435 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 85.435 MILLION OZ (THIS IS GOING TO BE A STRONG MONTH FOR EFP ISSUANCE//

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 693 CONTRACTS WITH OUR STRONG LOSS IN PRICE OF $0.33 IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL EFP ISSUANCE CONTRACTS: 125 ISSUED FOR OCT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. . WE HAVE A SMALL INITIAL SILVER OZ STANDING FOR SEPT OF 1.532 MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP:+ A NEW ISSUANCE OF 0 CONTRACTS OF EXCHANGE FOR RISK FOR 0.000 MILLION OZ. THUS NEW TOTAL OF SILVER STANDING: 2.640 MILLION OZ+ 4.2 MILLION OZ EXCHANGE FOR RISK = 6.84 MILLION OZ//// /// WE HAVE A STRONG SIZED LOSS OF 568 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 791 CONTRACTS//LITTLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION. THE NEW TAS ISSUANCE MONDAY NIGHT A HUGE (791) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 1 NOTICE(S) FILED TODAY FOR 5,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 3116 CONTRACTS TO 461,986 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED 556 CONTRACTS

WE HAD A FAIR SIZED INCREASE IN COMEX OI ( 3116 CONTRACTS) WITH OUR $6.80 LOSS IN PRICE//MONDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 16.562 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 8300 OZ QUEUE JUMP /NEW STANDING ADVANCES TO 34.221 TONNES/ + /A HUGE (AND CRIMINAL) ISSUANCE OF 3632 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR$6.80 LOSS IN PRICEWITH RESPECT TO MONDAY’S TRADING.WE HAD A STRONG SIZED GAIN OF 6250 OI CONTRACTS (19.440 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3134CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 461,986

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6250 CONTRACTS WITH 3116 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 3134 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 6250CONTRACTS OR19.440TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A HUGE 3632 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3134 CONTRACTS) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (3116) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 6,250 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR OCT. AT 16.562 TONNES FOLLOWED BY TODAY’S 8300 OZ QUEUE JUMP//NEW STANDING 34.221 TONNES// /// 3) ZERO LONG LIQUIDATION AND LITTLE TAS LIQUIDATION BUT SOME SPEC SHORT COVERINGS DURING THE COMEX SESSION //4) STRONG SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: HUGE T.A.S. ISSUANCE: 3632 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT :

TOTAL EFP CONTRACTS ISSUED: 68,897 CONTRACTS OR 6,889,700 OZ OR 214.29 TONNES IN 16 TRADING DAY(S) AND THUS AVERAGING: 4306 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16TRADING DAY(S) IN TONNES 214.29TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 214.29/3550 x 100% TONNES 6.02% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 214.29 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A STRONG SIZED 693 CONTRACTS OI TO 124,506 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A SMALL 125 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 125and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 125 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 693 CONTRACTS AND ADD TO THE 125 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 568 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 2.84 MILLION OZ

OCCURRED WITH OUR $0.33 LOSS IN PRICE …..(SOME SHORT COVERINGS)

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 22.95 PTS OR 0.78% //Hang Seng CLOSED DOWN 180.60 PTS OR 1.05% /The Nikkei CLOSED UP 62.80 PTS OR 0.20% //Australia’s all ordinaries CLOSED UP 0.22 % /Chinese yuan (ONSHORE) closed UP AT 7.3100 /OFFSHORE CHINESE YUAN CLOSED UP TO 7.3188 /Oil DOWN TO 85.64 dollars per barrel for WTI and BRENT DOWN AT 90.04/ Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 3116CONTRACTS TO 461,986 DESPITE OUR STRONG LOSS IN PRICE OF $6.80 ON MONDAY. OUR SHORT SPECULATORS COVERED A BIT OF THEIR POSITIONS DURING COMEX TRADING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF OCT..… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3134 EFP CONTRACTS WERE ISSUED: : DEC 3134 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3134 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 6250 CONTRACTS IN THAT 3672LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 3116 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $6.80//MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A HUGE 3632 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: OCT (34.221) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 34.221 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $6.80) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG GAIN OF 6806TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A SOME T.A.S. LIQUIDATION ON THE FRONT END OF MONDAY’S TRADING. THE T.A.S. ISSUED ON MONDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. IT DID HAVE SOME SPECULATOR SHORT COVERING WITH THE MASSIVE PRICE INCREASE.

WE HAVE GAINED A TOTAL OI OF 19.44 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR OCT. (16.562 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 8,300 OZ QUEUE JUMP //NEW TOTALS STANDING:34.221 TONNES ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $6.80. FOR THE PAST SEVERAL WEEKS, THE SPECULATORS HAVE GONE MASSIVELY SHORT WITH OUR BANKERS NET LONG. THE BIG QUESTION IS NOW HOW MUCH GOLD WILL THE BANKERS PULL FROM OUR SHORT SPECULATORS. SPECULATORS YESTERDAY ADDED TO THEIR HUGE SHORTS.

WE HAD REMOVED 556 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 6250 CONTRACTS OR 62500 OZ OR 19.44 TONNES.

Total monthly oz gold served (contracts) so far this month

10,962 notices 1,096,200 OZ 34.096 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposit:

total dealer deposits: 0 oz

customer deposits: 1

i) Into ASAHI 31,974.376 oz

total customer deposits: 31,974.376 oz

we had 1 customer withdrawals

i) Out of Brinks: 11,027.790 OZ (343 kilobars)

total withdrawals 11,027.790 oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCTOBER we have an oi of 125 contracts having LOST 296 contracts. We had 379 contracts filed on Monday, so we gained 83 contracts or an additional 8300 oz will stand for delivery at the comex in this active delivery month of October. Our short speculators have been met with physical delivery demands by the bank. The only way they can obtain gold is through these EFP’s where delivery is taken in London on a T + 2 basis. We had the commencement of gold speculator short covering last Thursday and this action by the banker longs will continue until the specs have been annihilated

NOV LOST 116 CONTRACTS to stand at 1466

December GAINED 1988 contracts up to 370,498 contracts.

We had 85 contracts filed for today representing 8500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 10 notices were issued from their client or customer account. The total of all issuance by all participants equate to 85 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the OCT. /2023. contract month, we take the total number of notices filed so far for the month (10,962 x 100 oz ), to which we add the difference between the open interest for the front month of OCT. (125 CONTRACTS) minus the number of notices served upon today 85 x 100 oz per contract equals 1,100,200 OZ OR 34.221 TONNES the number of TONNES standing in this active month of OCT.

thus the INITIAL standings for gold for the OCT.contract month: No of notices filed so far (10,962) x 100 oz + (125) {OI for the front month} minus the number of notices served upon today (85) x 100 oz) which equals 1,100,200oz standing OR 34.221 TONNES

TOTAL COMEX GOLD STANDING: 34.221 TONNES WHICH IS HUGE FOR AN ACTIVE BUT GENERALLY WEAK DELIVERY MONTH. (OCT). Somebody is after a considerable amount of gold from the comex.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 19,850,264.173 OZ

TOTAL REGISTERED GOLD 9,977,102.543 (310.329 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 9,873,161.630 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,063,851(REG GOLD- PLEDGED GOLD) 250.81 tonnes//dropping like a stone

END

SILVER/COMEX

OCT 24

//2023// THE OCT 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

6052.163 oz

Brinks Delaware

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

559,541.399 oz ASAHI Delaware

No of oz served today (contracts)

1 CONTRACT(S) (5,000 OZ)

No of oz to be served (notices)

16 contracts (80,000 oz)

Total monthly oz silver served (contracts)

512 Contracts (2,560,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit: 0

total: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i) Into ASAHI 558,541.800 oz

ii) Into Delaware: 999.599.01

total customer deposit 559,541.399 oz

JPMorgan has a total silver weight: 134.441 million oz/270.485 million or 49.55%

Comex withdrawals 2

i) Out of Brinks: 3014.600 oz

ii) out of Delaware: 3037.563 oz

total: 6052.163 oz

adjustments: 0

TOTAL REGISTERED SILVER: 37.633 MILLION OZ//.TOTAL REG + ELIGIBLE. 270.435 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF OCT /2023 OI: 17 CONTRACTS HAVING LOST 3 CONTRACT(S). WE HAD 3 NOTICES FILED

ON MONDAY, SO WE GAINED 0 CONTRACTS AS WE HAD A QUEUE JUMP OF NIL OZ

NOVEMBER LOST 12 CONTRACTS TO STAND AT 429

DEC. LOST 1173 CONTRACTS TO STAND AT 96,959 .

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1 for 5,000 oz

Comex volumes// est. volume today 47,873//poor

Comex volume: confirmed yesterday 54,509 poor

To calculate the number of silver ounces that will stand for delivery in OCT. we take the total number of notices filed for the month so far at 512 x 5,000 oz = 2,560,000 oz

to which we add the difference between the open interest for the front month of OCT (17) and the number of notices served upon today 1 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the OCT/2023 contract month: 512 (notices served so far) x 5000 oz + OI for the front month of OCT (17) – number of notices served upon today (1 )x 500 oz of silver standing for the OCT contract month equates to 2.640 million oz + .0 MILLION oz of exchange for risk today + 4.2 million oz prior//new totals: 6.840 million oz.

There are 37.633 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

OCT 24/WITH GOLD DOWN $1.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 3.17 TONNES OF GOLD OUT OF THE GLD//WHAT A MASSIVE FRAUD! //: //: // INVENTORY RESTS AT 860.07 TONNES

OCT 23/WITH GOLD DOWN $6.80 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE 15.00 TONNES OF GOLD INTO THE GLD//WHAT A MASSIVE FRAUD! //: //: // INVENTORY RESTS AT 863.24 TONNES

OCT 20/WITH GOLD UP $14.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: // INVENTORY RESTS AT 848.24 TONNES

OCT 19/WITH GOLD UP $12.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 5.19 TONNES OF GOLD FROM THE GLD//: //: // INVENTORY RESTS AT 848.24 TONNES

OCT 18/WITH GOLD UP $32.55 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD//: //: // INVENTORY RESTS AT 853.43 TONNES

OCT 17/WITH GOLD UP $1.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: //: // INVENTORY RESTS AT 855.45 TONNES

OCT 16/WITH GOLD DOWN $6.45 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD //: // INVENTORY RESTS AT 855.45 TONNES

OCT 13/WITH GOLD UP $57.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / /// // INVENTORY RESTS AT 862.37 TONNES

OCT 12/WITH GOLD DOWN $3.00 TODAY:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD//: / /// // INVENTORY RESTS AT 862.37 TONNES

OCT 11/WITH GOLD UP $11.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD:HUGE CHANGES: / /// // INVENTORY RESTS AT 861.51 TONNES

OCT 10/WITH GOLD UP $30.60 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:HUGE CHANGES: A WITHDRAWAL OF 5.77 TONNES OF GOLD FROM THE GLD// /// // INVENTORY RESTS AT 861.81 TONNES

OCT 6/WITH GOLD UP $13.05 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:HUGE CHANGES: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD// /// // INVENTORY RESTS AT 867.58 TONNES

OCT 5/WITH GOLD DOWN $1.35 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD:HUGE CHANGES: A MASSIVE WITHDRAWAL OF 5.77 TONNES OF GOLD FROM THE GLD// /// // INVENTORY RESTS AT 869.31 TONNES

OCT 4/WITH GOLD DOWN $7.40 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD/// : // //INVENTORY RESTS AT 875.08 TONNES

OCT 3/WITH GOLD DOWN $6.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD/// : // //INVENTORY RESTS AT 875.08 TONNES

OCT 2/WITH GOLD DOWN $19.35 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: LD/ : // //INVENTORY RESTS AT 873,64 TONNES

SEPT 29/WITH GOLD DOWN $11.15 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: LD/ : // //INVENTORY RESTS AT 873,64 TONNES

SEPT 28/WITH GOLD DOWN $13.45 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A HUGE WITHDRAWAL OF 4.88 TONNES OF GOLD OUT OF THE GLD/ : // //INVENTORY RESTS AT 873,64 TONNES

SEPT 26/WITH GOLD DOWN $XXX TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT 05 THE GLD/ : // //INVENTORY RESTS AT 878.52 TONNES

SEPT 26/WITH GOLD DOWN $13.40 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT 05 THE GLD/ : // //INVENTORY RESTS AT 878.52 TONNES

SEPT 22/WITH GOLD UP $5.70 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD/ : // //INVENTORY RESTS AT 878.83 TONNES

SEPT 21/WITH GOLD DOWN $25.60 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.58 TONNES OF GOLD FROM THE GLD/ : // //INVENTORY RESTS AT 878.25 TONNES

SEPT 19/WITH GOLD UP $0.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD : // //INVENTORY RESTS AT 880.217 TONNES

SEPT 18/WITH GOLD UP $8.40 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD : A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 880.217 TONNES

SEPT 15/WITH GOLD UP $13.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 1.055 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 879.70 TONNES

SEPT 14/WITH GOLD UP $1.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 4.63 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 882.01 TONNES

SEPT 13/WITH GOLD DOWN $2.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 12/WITH GOLD DOWN $11.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 11/WITH GOLD UP $4.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 8/WITH GOLD UP $0.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 7/WITH GOLD DOWN $0.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.22 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.69 TONNES

SEPT 6/WITH GOLD DOWN $8.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.81 TONNES

SEPT 5/WITH GOLD DOWN $13.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.97 TONNES

SEPT 1/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

GLD INVENTORY: 860.07 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

OCT 24/WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE DEPOSIT OF 2.52 MILLION OZ INTO THE SLV/// /// /INVENTORY RESTS AT 444.391 MILLION OZ

OCT 23/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ /// /INVENTORY RESTS AT 441.871 MILLION OZ

OCT 20/WITH SILVER UP 50 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:.A WITHDRAWAL OF 2.658 MILLION OZ FROM THE SLV/ /// /INVENTORY RESTS AT 441.871 MILLION OZ

OCT 19/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. A /// /INVENTORY RESTS AT 444.529 MILLION OZ

OCT 18/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF 3.207 MILLLION OZ FROM THE SLV///// /.////INVENTORY RESTS AT 444.529 MILLION OZ

OCT 17/WITH SILVER UP 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 447.736 MILLION OZ

OCT 16/WITH SILVER DOWN 9 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:. : //A WITHDRAWAL OF 2.664 MILLION OZ OUT OF THE SLV// /.////INVENTORY RESTS AT 447.730 MILLION OZ

OCT 13/WITH SILVER UP 90 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:. : //A WITHDRAWAL OF 1.375 MILLION OZ OUT OF THE SLV// /.////INVENTORY RESTS AT 450.394 MILLION OZ

OCT 12/WITH SILVER DOWN 19 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV:. : //A WITHDRAWAL OF 0.825 MILLION OZ OUT OF THE SLV// /.////INVENTORY RESTS AT 451.769 MILLION OZ

OCT 11/WITH SILVER UP 17 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:. : //A WITHDRAWAL OF .366 MILLION OZ OUT OF THE SLV// /.////INVENTORY RESTS AT 452.594 MILLION OZ

OCT 10/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:. : //A DEPOSIT OF 1.833 MILLION OZ INTO THE SLV// /.////INVENTORY RESTS AT 452.960 MILLION OZ

OCT 6/WITH SILVER UP 69 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:. : //A DEPOSIT OF 0.916 MILLION OZ INTO THE SLV// /.////INVENTORY RESTS AT 451.127 MILLION OZ

OCT 5/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : //A MASSIVE DEPOSIT OF 8.328 MILLION OZ INTO THE SLV// /.////INVENTORY RESTS AT 450.211 MILLION OZ

OCT 4/WITH SILVER DOWN 34 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 441.883 MILLION OZ

OCT 3/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 441.883 MILLION OZ

OCT 2/WITH SILVER DOWN 98 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 441.883 MILLION OZ

SEPT 29/WITH SILVER DOWN 28 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF 0.183 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 441.883 MILLION OZ

SEPT 28/WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF 4.88 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 442.066 MILLION OZ

SEPT 27/WITH SILVER DOWN 20 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF .641 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 448.392 MILLION OZ

SEPT 26/WITH SILVER DOWN 20 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:. A WITHDRAWAL OF .641 MILLION OZ FROM THE SLV: // /.////INVENTORY RESTS AT 448.392 MILLION OZ

SEPT 22/WITH SILVER UP 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 449.492 MILLION OZ

SEPT 21/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 449,033 MILLION OZ

SEPT 19/WITH SILVER UP 0 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.1 MILLION OZ INTO THE SLV. : // /.////INVENTORY RESTS AT 449.033 MILLION OZ

SEPT 18/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 1.651 MILLION OZ INTO THE SLV. : // /.////INVENTORY RESTS AT 441.332 MILLION OZ

SEPT 15/WITH SILVER UP 37 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.31 MILLION OZ FROM THE SLV. : // /.////INVENTORY RESTS AT 439.681 MILLION OZ

SEPT 14/WITH SILVER DOWN 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: : // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 13/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1,009 MILLION OZ INTO THE SLV//: // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 12/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO THE SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 11/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 7/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 6/WITH SILVER DOWN 36 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.373 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 5/WITH SILVER DOWN 69 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 734,000 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 437.891 MILLION OZ

SEPT 1/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 440.00 MILLION OZ

CLOSING INVENTORY 444.871 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

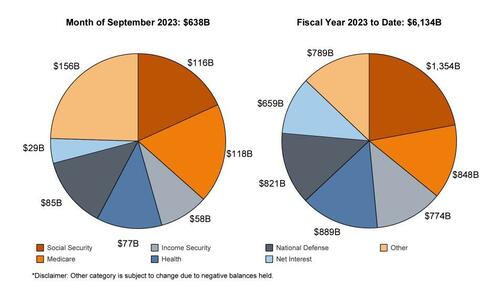

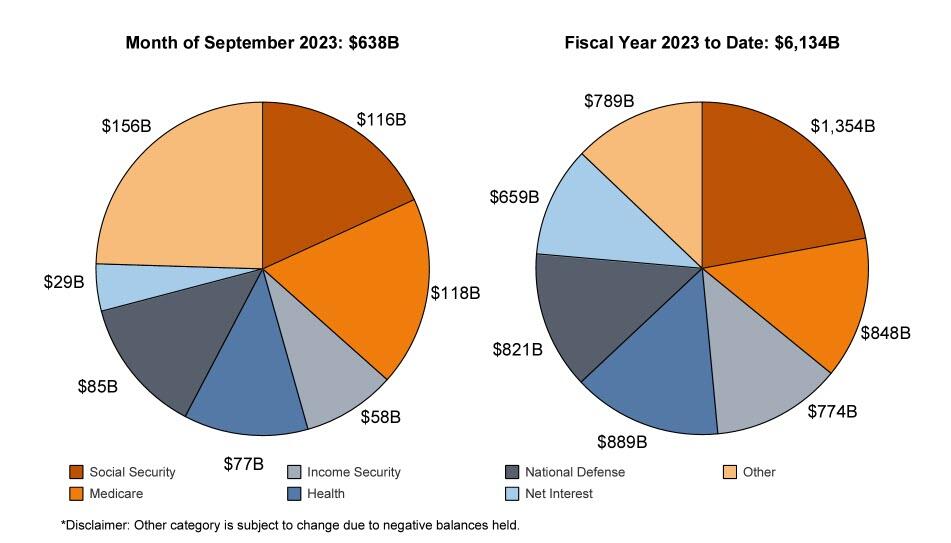

Biden Administration Runs Third-Largest Budget Deficit In History

The Biden administration ran a $1.695 trillion budget deficit in fiscal 2023. It was the third-largest deficit in US history. The only time the US government ran bigger deficits was during the COVID years of 2020 and 2021.

The deficit would have been even higher had it not been for an accounting move in August that reversed student loan forgiveness.

Last year, the Treasury expensed $333.65 trillion for the student loan forgiveness plan signed by President Biden. When the Supreme Court struck the scheme down, the Treasury had to reverse that expense. That means the actual shortfall was more than $2 trillion this year — $3 trillion higher than the official numbers.

The 2023 budget shortfall was bigger than any run during the Obama administration during the Great Recession, and yet this economy is supposedly strong. Typically, strong economies result in smaller deficits as tax revenue rises.

That was not the case in fiscal 2023. Federal Receipts fell by 9.3% to $4.44 trillion.

Treasury Secretary Janet Yellen was quick to blame falling tax receipts for the big deficit and said it underscores “the importance of President Biden’s enacted and proposed policies to reform the tax system.

But the big problem is on the spending side of the ledger. Strong receipts last year papered over the spending problem.

The US government blew through $6.13 trillion in fiscal 2023. That was down slightly from last year’s total expenditures, but the numbers were skewed by student loan forgiveness accounting. If you factor out the reversal of student loan forgiveness, the Biden administration spent $6.46 trillion in fiscal 2023, an 8.8% year-over-year increase in actual spending.

The Biden administration already wants more money. The president recently proposed a $100 billion aid package for Israel, Ukraine and other “national security” priorities.

Keep in mind that the feds now have a credit card with no limit.

And despite the caterwauling of a few Republicans, virtually nobody in Washington DC is interested in addressing this spending problem.

The fundamental issue wasn’t that the US government didn’t have enough money. The fundamental problem was, and still is, that the US government spends too much money. Despite the pretend spending cuts, the debt ceiling deal didn’t address that problem. Even with the new plan in place, spending will go up. And it’s already historically high. That means big budget deficits will continue and the national debt will mount.

It’s easy to finger-point at President Biden and blame him for the spending problem, but this isn’t exclusive to the current administration. Trump also borrowed and spent like the proverbial drunken sailor.

To put the deficit in perspective, prior to the pandemic, the US government had only run deficits over $1 trillion four times — all in the aftermath of the 2008 financial crisis. Trump almost hit the $1 trillion mark in 2019 and was on pace to run a trillion-dollar deficit prior to the pandemic when the US supposedly enjoyed the “best economy” ever. The economic catastrophe caused by the government’s response to COVID-19 gave policymakers an excuse to spend with no questions asked. Now the Biden administration has settled into the new status quo – running ’08 financial crisis-like deficits every single year.

THE BIGGER PROBLEM

This rapid increase in the national debt is happening during a time of sharply rising interest rates. This is a big problem for a government that primarily depends on borrowing to pay its bills.

Interest expense rose by 23% to $879 billion. Net interest, excluding intragovernmental transfers to trust funds, rose by 39% to $659 billion. Both of those numbers broke records.

Gross interest payments amounted to 3.28% as a share of gross domestic product, according to a Treasury Department official quoted by Reuters. That was the highest since 2001. The net share of interest expense came in at 2.45%, the highest since 1998.

The average interest rate on the debt is now at the highest level since 2011, coming in at 2.92% as of the end of August. But that’s still relatively low, and the debt is more than double what it was back in the good ol’ days of 2011.

Meanwhile, the average interest rate is poised to climb rapidly. A lot of the debt currently on the books was financed at very low rates before the Federal Reserve started its hiking cycle. Every month, some of that super-low-yielding paper matures and has to be replaced by bonds yielding much higher rates. That means interest payments will quickly climb much higher unless rates fall.

To give you an idea of where we’re heading, T-bills currently yield about 5.5%, the two-year yield is over 5% and the 10-year currently yields close to 5%.

Rising interest rates drove interest payments to over 35% as a percentage of total tax receipts. In other words, the government is already paying more than a third of the taxes it collects on interest expense.

If interest rates remain elevated, or continue rising, interest expenses could climb rapidly into the top three federal expenses. (You can read a more in-depth analysis of the national debt HERE.)

Peter Schiff provided some context in a tweet.

US debt was 119% of GDP in 1946. Budget surpluses in 4 of the next 5 years reduced it to 68% by 1953, the largest was 4.3% in 1948, the equivalent to $1.16 trillion in today’s dollars. The same reduction today requires about $30 trillion of tax hikes and spending cuts by 2030.”

In his podcast, Schiff called this a “fiscal timebomb in the process of exploding.”

It’s a compounding situation. We have to borrow the money to pay that interest. Every nickel that the government pays in interest on the debt it has to borrow. All that additional borrowing adds to the national debt, which then has to be financed at a higher rate.”

If the national debt climbs to $40 trillion (and given the current deficits it won’t take long) and interest rates remain at 5% (which Jerome Powell says will be necessary to tackle inflation) interest payments on the debt alone would skyrocket around $2 trillion per year. That means that even if the US government balanced the budget so receipts covered all spending minus interest payments, we’d still be facing a $2 trillion annual deficit.

Of course, there won’t be a balanced budget. So, let’s assume the federal government can maintain the current deficit level of around $1 trillion annually (minus interest expense). Even with this overly optimistic scenario, the Treasury would be running a $3 trillion annual budget deficit. (That’s the current $1 trillion deficit plus $2 trillion in interest expenses.)

And the most likely scenario is spending will continue to climb, along with the budget deficits. There’s no telling how high the annual deficits could run.

This is a fiscal powder keg. All it needs is a match.

END

Peter Schiff: Jerome Powell Isn’t Qualified To Be In Any Economic Club

Last week, Federal Reserve Chairman Jerome Powell delivered a speech at the Economic Club of New York luncheon. In his podcast, Peter Schiff broke down some of the Fed chair’s comments and concluded that Powell is not qualified to be a member of any economic club.

Peter opened the discussion by saying Powell is not the person to bring in if you want accurate answers about the economy.

He doesn’t know what’s going on. And if he does, he’s not going to be honest. He’s going to lie. He probably doesn’t know. He’s clueless. And he lies on top of that.”

Peter said that if the Economic Club of New York asked him all the same questions they asked Powell, all of his answers would be the exact opposite.

I’m sure that most of the members of the Economic Club of New York, maybe all the members, know more about economics than Jerome Powell. Because you have to flunk a test about economics in order to qualify to be a member of the Federal Reserve. In fact, you probably can’t even get to be a Federal Open Market Committee member if you actually know anything about economics.”

There are a number of things Powell said that seem to support Peter’s assertion.

The Economy Isn’t Spending

Powell claimed the Fed needs to weaken the economy in order to bring down inflation. Peter said the notion that economic growth causes inflation is a “complete fallacy” and a “Keynesian myth.”

The problem is that Powell and many others in the mainstream misdefine economic growth. When they say, “economic growth,” they really mean consumer spending. They’re looking at metrics such as retail sales and GDP growth.

That’s not economic growth. That’s just spending. That’s not growing the economy. That’s spending what a growing economy produces.”

When you look at retail sales numbers, much of that increase is due to rising prices. And to maintain the spending spree, Americans are borrowing a lot of money. In fact, the “unsinkable” American consumer is growing in debt. Meanwhile, many people have taken on second and third jobs just to make ends meet.

If you’re just looking at the spending, and you think, ‘Oh, we have this really strong economy,’ No! It’s not a strong economy. You’re looking at inflation! … Inflation is driving this spending.”

That means you don’t have to “weaken” the economy to reduce inflation. You just need to reduce spending. You certainly don’t want people to stop working. If they aren’t working, they aren’t producing.

That means there’s less stuff. That puts upward pressure on prices. We want everybody to keep working. We just want them to stop spending everything they earn. They need to take some of their paychecks and save it — put it in the bank.”

But Powell thinks spending is the economy and the consumer drives things by buying stuff.

No! The consumer is the caboose. He’s driven by the real engine of the economy, which is production. That’s what we need more of. We need a stronger economy, but we need less spending, less consumption, more savings, more investment.”

The Pandemic Caused Inflation?

Powell also claimed the pandemic caused price inflation. He acts as if everything was fine until the pandemic and then prices just started going up.

The pandemic is not why we have inflation. The Fed is why we have inflation. Congress, the president are why we have inflation. And not just Biden, but Trump and the presidents before him. They were all contributing to the inflation problem that we’re dealing with today.”

It is true that the inflation problem got worse during COVID. But it wasn’t the pandemic. It was the government response to the pandemic.

The pandemic was a health problem. What the government did was turn it into an inflation problem. Because they overreacted, number one. They forced people to stop working. And then they ran huge deficits to send people stimulus checks to buy stuff that they weren’t making. It was the worst combination of monetary and fiscal policy ever devised.”

That raises a question. If Powell doesn’t know where price inflation came from, how is he going to get rid of it?

The Banking Crisis Isn’t Over

Referencing the collapse of Silicon Valley Bank and other financial institutions last spring, Powell was asked if the banking crisis is over. He said we handled it and it’s basically behind us.

Peter disagreed.

It’s just getting started. That was the tip of the iceberg.”

Peter said all you have to do to see the underlying problem is to look at how much value banks of lost on their mortgage-backed securities and Treasuries since the March bailout.

It’s been an enormous collapse. And so the banks today are in far worse shape than they were back in March when Silicon Valley Bank failed. The Fed should know this because the Fed is the biggest loser of them all. The Fed has more Treasuries and mortgage-backed securities on its balance sheet than anybody else. So, the Fed is the biggest loser, and somehow they think the crisis is behind us when it’s all out in front of us, and it’s about to be playing out in front of their eyes.”

The “Problem” of Low Inflation

Powell worried out loud that inflation could potentially get too low. He said that was the problem in the past and now we have the problem of high inflation.

Peter said “low” inflation was never a problem.

That was a made-up problem so they could have an excuse to create more inflation. Now we’ve got a real problem of inflation being too high.”

In 2020, Powell started talking about inflation averaging. Instead of targeting 2%, Fed officials pivoted to an average 2% target over time.

They wanted to justify letting inflation get to two-and-a-quarter, two-and-a-half. They didn’t want to have to put in the brakes when we hit two. They wanted to make up for all the years where we were below two. So, they redefined their target to an average inflation rate of 2%. No one talks about that now. I mean, they haven’t officially changed that, but how many years are we going to have to have 1% inflation to average it down to two?

In fact, we really need falling prices in order to get the average back to 2%. But the central bankers never want to do that. They just want to average up.

Powell Doesn’t Consider Fiscal Policy

When asked about government borrowing and spending, and the massive budget deficits, Powell said he doesn’t consider fiscal policy at all when developing monetary policy. He also insisted the Fed doesn’t change monetary policy based on fiscal policy. He talked as if fiscal policy isn’t part of the central bank’s mandate.

Peter said it has everything to do with their mandate.

Where’s the inflation coming from? It’s coming from the budget deficits that he monetizes. And government spending is driving inflation. If you’re trying to ‘slow down’ the economy, or just trying to cool consumption, if the government is increasing spending, that is counteracting what you’re trying to do. How could you avoid that? How can you not care about that?”

Peter said the whole idea behind Fed independence is so the central bank can push back against reckless fiscal policy.

The Fed is supposed the be the chaperone here at this spending party, and if Congress is spending too much money, well, jack up rates. Make it harder for them to do that. Raise the cost of borrowing so that they cut back.”

Peter said it’s like a doctor ignoring a patient’s symptoms and prescribing whatever treatment he fancies.

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.3100

OFFSHORE YUAN: UP TO 7.3188

SHANGHAI CLOSED UP 22.95 PTS OR 0.78%

HANG SENG CLOSED DOWN 180.60 PTS OR 1.05%

2. Nikkei closed UP 62.80 PTS OR 0.20 %

3. Europe stocks SO FAR: ALL MOSTLY GREEN

USA dollar INDEX DOWN TO 105.68 EURO FALLS TO 1.0638 DOWN 31 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.845 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 149.75/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP// OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.8315***/Italian 10 Yr bond yield DOWN to 4.814*** /SPAIN 10 YR BOND YIELD DOWN TO 3.9240…**

3i Greek 10 year bond yield FALLS TO 4.191

3j Gold at $1961.00 silver at: 22.81 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 98 /100 roubles/dollar; ROUBLE AT 93.35//

3m oil into the 85 dollar handle for WTI and 90 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 149.75// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.845% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8929 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9499 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.857 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.996 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 5.086 UP 22 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 28.10…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.6170

end

2.a Overnight: Newsquawk and Zero hedge:

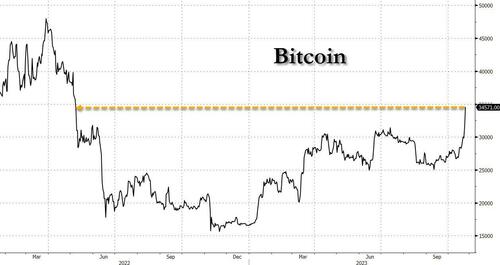

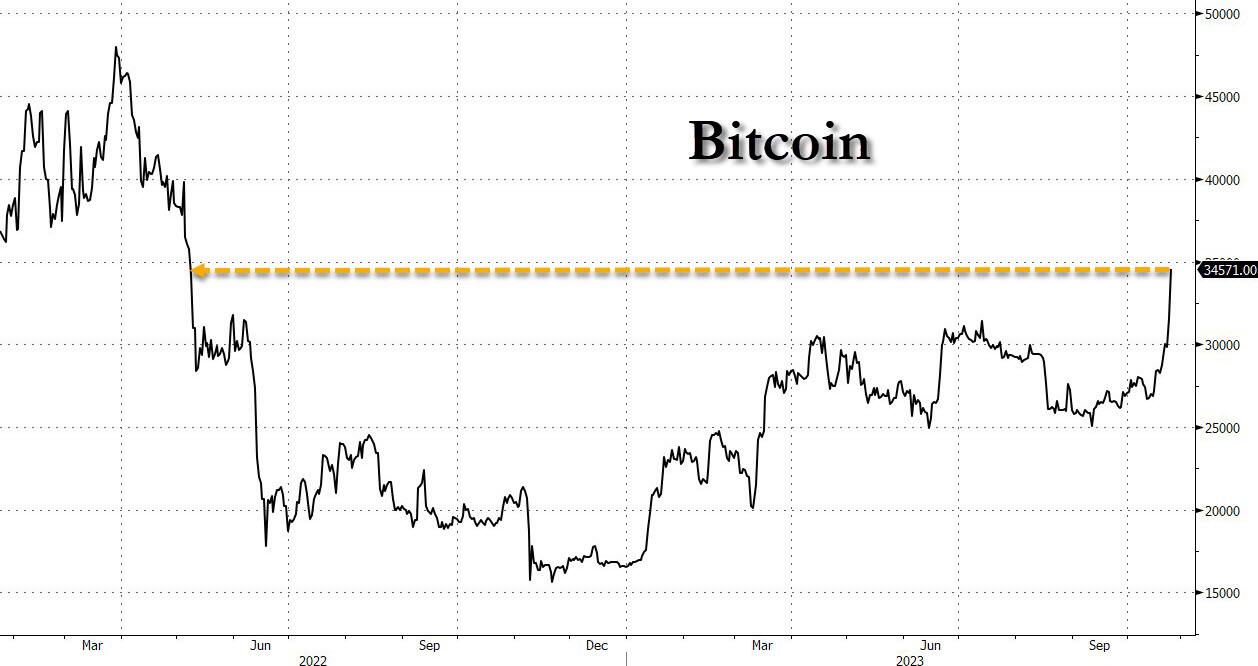

Futures Rise, Bitcoin Erupts Ahead Of Mega-Tech Earnings

TUESDAY, OCT 24, 2023 – 08:19 AM

Global stocks rose, US index futures jumped and bitcoin erupted higher ahead of closely-watched earnings from tech gigacaps Microsoft and Alphabet later today (full preview here). As of 8:00am ET, S&P futures were up 0.6%, at session highs and set to snap a five-day losing streak with Nasdaq futures also higher by 0.6%. Treasuries stabilized, with the US 10-year yield dropping as low as 4.80% before reversing gains, amid growing speculation that the recent selloff was excessive. Treasury 10-year yields slipped as much as five basis points to a one-week low before paring the move. Europe’s Stoxx 600 index edged higher.

Bitcoin topped $35,000, rising to the highest level since May 2022, while the euro swung to a loss against the dollar as data showed the French and German economies struggling.

In premarket trading, shares in cryptocurrency-linked companies gained in US premarket trading, with Marathon Digital, Riot Platforms, Hut 8 Mining and Cleanspark all surging at least 12%. Nvidia and Arm Holdings rose, set to extend gains, after Bloomberg reported that Nvidia is using Arm technology to develop processors in personal computers. Intel shares were on track to fall for a third consecutive session. NVDA up 1.6%. ARM shares rise 2.6%. Spotify was down 2.5% even as third-quarter results and fourth-quarter guidance beat the average analyst estimate. Its forecast for monthly active users was also better than expected. Citi wrote that the stock’s negative reaction was surprising. Here are some other notable premarket movers:

Cadence Design Systems shares decline 3.3% after the electronic design automation software company’s fourth-quarter adjusted earnings per share forecast did not meet consensus expectations.

DraftKings advances 3.5% after MoffettNathanson raises the online sports-betting company to buy from neutral, citing its expense management and revenue that continues to top expectations.

IonQ drops as much as 20%, on track to hit a four-month low, after the quantum computing company said in a statement its co-founder and chief science officer Dr. Chris Monroe, will leave the company.

Medpace jumps 7.9% after the health-care services provider boosted its current-year revenue forecast and gave a range for next year that was ahead of expectations. The company also reported third-quarter revenue and earnings per share that beat estimates.

Redfin rises 11% after the online real estate company said that funds managed by Apollo Capital Management agreed to commit up to $250 million of financing in the form of a first lien term loan facility.

TrueBlue shares drop 17% after the staffing company’s third-quarter earnings and fourth-quarter revenue forecast fell short of analyst expectations, with the firm noting that the operating environment “remains soft.”

VMware Inc. shares drop 5.3% moving closer to the $142.50, the amount that shareholders would receive if they elected to get paid in cash rather than stock in Broadcom’s acquisition of the cloud-computing company.

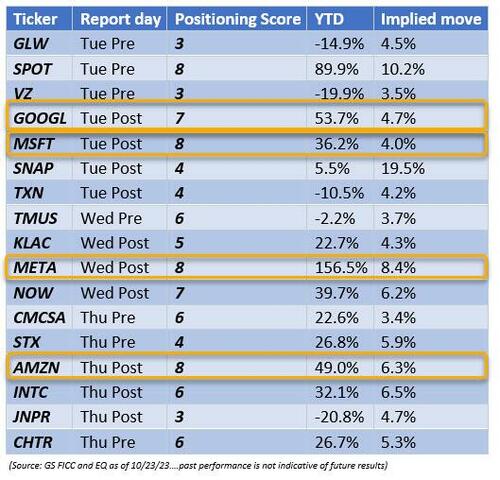

As noted earlier, all eyes now turn to the giga caps tech companies with MSFT and GOOGL reporting after the close today(full preview here). Mark Haefele, chief investment officer at UBS Global Wealth Management, said he expects a strong outcome from top technology and growth firms, despite the earnings season’s sluggish start so far.

Treasuries have stadied after some of the market’s most prominent bears warned of an economic slowdown, sparking bets the declines have overshot and that the Federal Reserve will need to lower interest rates. Wild swings in government debt are unsettling investors as a resilient economy makes it hard to work out when the Fed will halt rate hikes. Surging government issuance and geopolitical tensions are also clouding the outlook.

“I don’t think you should be pounding the table saying this is the absolute best time to buy,” said Patrick Armstrong, chief investment officer at Plurimi Wealth LLP. “But I would not be shorting.”

Brent crude halted two days of losses, climbing above $90 per barrel. French President Emmanuel Macron called for an international coalition to fight Hamas and warned other Iranian-backed militant groups not to open new fronts in the war, as he met with Prime Minister Benjamin Netanyahu during a trip to Israel.

European stocks are also higher with the Stoxx 600 rising 0.2% as it looks to snap a 5-day losing streak; basic resources and utilities stocks as the biggest outpeformers, while banks and automobiles lead declines as Barclays shares slumped after a trading division miss and lower guidance. Here are some of the biggest European movers:

Hermes rises as much as 3.3% in Paris trading after third-quarter sales beat estimates, with analysts noting that the luxury-goods maker held up across all regions, benefiting from its exposure to a wealthy and loyal customer base against a slower macroeconomic backdrop

Logitech shares rise as much as 11% to April 2022 high after the Swiss maker of keyboards, webcams and other computer accessories reported sales for the second quarter that beat analysts’ average estimate

Stora Enso rises as much as 7.2%, the most since July, after third-quarter results from the Finnish paper and packaging company beat “low buy-side Ebit expectations,” according to Jefferies analysts

Puma shares jump as much as 5.7% after the sportswear brand’s constant-currency third-quarter revenue beat consensus estimates, reassuring analysts who noted a recent run of weakness in the stock

Norsk Hydro shares rise as much as 6.7% in early trading, the most in nearly a year, after the aluminum supplier reported third-quarter results

Nemetschek shares rise as much as 8.8%, the most since April, after the software company raised full-year guidance on the back of stronger-than-expected preliminary 3Q results

Nordnet shares advance as much as 8.7%, the most since Nov. 2022, after the Swedish investment and savings platform’s third-quarter results come in ahead expectations

Barclays shares fall as much as 8.7% after the British lender reduced its guidance for UK net interest margin, which Citi expects to be met with “significant disappointment”

DSV falls as much as 2.6% after the Danish logistics group lowered and narrowed its guidance for the full year. While its third-quarter earnings arrived broadly in line with analysts expectations

Sandoz slipped as much as 4.6%% at open after reporting revenue in line with guidance, with analysts noting the slowdown in North American sales

Bunzl drops as much as 6.8%, the most since Aug. 2022, after the UK distribution company’s third-quarter underlying revenue growth lagged analyst expectations

Softcat shares fall as much as 13%, the biggest intraday drop since 2020, after the UK IT reseller said its operating profit growth will be weighted toward 2H of fiscal 2024 due to tough comparisons in 1H

As Bloomberg’s Jan-Patrick Barnert notes, European stock market declines the past few months have been broad-based across major benchmarks, but with the correction now at 10% or more in several regions, there could be a rebound coming, given oversold conditions and the Stoxx 600 at a major technical level. All that is needed would be convinced buyers.

However, that may be a tough call. Headline risks from geopolitics are far from over, plus there’s ongoing uncertainty regarding the European economic cycle — and more importantly tightening credit. There is some doubt if investors are already in the dip-buying mood. Instead, they may move hedging away from one-day event risk to adjusting positions that they can work with even among longer term unknows. This could finally spur some cautious dip-buying.

Earlier in the session, Asian stocks swung between gains and losses, as investors looked to corporate earnings and Treasury market moves for cues after the regional stock benchmark tumbled to an 11-month low on Monday. The MSCI Asia Pacific Index closed up 0.3%. In Asia, most Chinese stock gauges rose after the nation’s sovereign wealth fund bought exchange-traded funds to shore up prices. The rebound in Chinese equities “shows that while it may still be too early to call a bottom, the authorities are making it a rule to step on the brakes whenever there looks like there’s overwhelming downward momentum,” said Raymond Chen, fund manager at Zizhou Investment Asset Management.

The Hang Seng Index fell to its lowest level since last November as trading resumed after a holiday. Japanese stocks declined, with EV and tech supplier Nidec tumbling 10% after a quarterly earnings miss. Stocks climbed in Singapore and Indonesia. The volatile session follows a four-day slide in the key regional gauge, amid concerns over China’s economy as well as geopolitical risks in the Middle East and high US interest rates. Traders were closely monitoring moves in bond markets after some prominent investors said the historic rout in US Treasuries has gone too far. Treasury 10-year yields fell slightly in Asian trading.

Hang Seng and Shanghai Comp opened mixed with the former playing catch-up following its long weekend, whilst the latter gained as reports also suggested US and China held the first working group meeting.

Japan’s Nikkei 225 gave up the 31k level in early trade as the prior day’s firming of the JPY weighed on the export-heavy index.

Australia’s ASX 200 traded in the green with the upside led by Metals & Mining following the prior session’s gains in the complex, although gold names lag after the precious metal unwound some geopolitical risk premium after the weekend.

In FX, the Bloomberg Dollar Spot Index is flat. The Aussie is the best performer among the G-10’s, rising 0.4% versus the greenback.

In rates US treasuries were mixed, reversing gains that initially pushed 10-year yields back below 4.80%, with the curve flatter as front-end trades cheaper on the day, unwinding a portion of Monday’s aggressive rally. Long-end Treasuries outperformed, with 30-year yields little changed; 10-year yields were around 4.865% and slightly cheaper on the day after breaching 4.80% in early London session, trailing bunds and gilts by 6bp and 4bp in the sector; long-end outperformance in Treasuries flattens the curve, tightening 2s10s, 5s30s spreads by 2.5bp and 3bps. In Europe, bunds outperform after October PMI figures for Germany and euro-area broadly miss median estimates. US auction cycle starts with 2-year note sale at 1pm New York time. The Treasury auction cycle includes $51b 2-year note, followed by 5- and 7-year notes Wednesday and Thursday. The WI 2-year yield at ~5.05% is 3.5bp richer than September’s auction, which stopped on the screws. The dollar IG issuance slate empty so far after just one deal was priced on Monday; around $20 billion in new bond sales are expected this week.

In commodities, oil prices advance, with WTI rising 0.4% to trade near $86. Spot gold falls 0.4%.

Bitcoin surges over 8%, fueled by expectations of fresh demand from exchange-traded funds.

Turning to the day ahead. In terms of data, we have the global flash PMIs for October in the US, UK, Japan, Germany, France, and the Eurozone. In the US, we also have the October Philadelphia Fed non-manufacturing activity (8:30am), S&P Global PMIs (9:45am) and Richmond Fed manufacturing index (10am). In the UK, we have the September jobless claims change results and the August unemployment rate, as well as the German November GfK consumer confidence, and the Euro Area Bank Lending Survey. Finally, we have earnings releases from both Microsoft and Alphabet, as well as Visa, Coca-Cola, Danaher, Texas Instruments, Verizon, General Electric, NextEra Energy, Fiserv, HCA Healthcare, General Motors, and Dow Inc.

Market Snapshot

S&P 500 futures up 0.2% to 4,249.50

MXAP up 0.3% to 152.08

MXAPJ up 0.3% to 476.22

Nikkei up 0.2% to 31,062.35

Topix little changed at 2,240.73

Hang Seng Index down 1.1% to 16,991.53

Shanghai Composite up 0.8% to 2,962.24

Sensex down 1.3% to 64,571.88

Australia S&P/ASX 200 up 0.2% to 6,856.86

Kospi up 1.1% to 2,383.51

STOXX Europe 600 down 0.3% to 431.74

German 10Y yield little changed at 2.79%

Euro down 0.2% to $1.0648

Brent Futures down 0.3% to $89.52/bbl

Gold spot up 0.1% to $1,974.11

U.S. Dollar Index up 0.15% to 105.70

Top Overnight News

China is set to unleash fresh fiscal stimulus to shore up its economic recovery, drawing on a well-used playbook that relies heavily on debt and state spending but falls short on the deeper reforms called for by a growing number of analysts. China’s parliament is set to approve just over 1 trillion yuan ($137 billion) in additional sovereign debt issuance when it concludes a five-day meeting that began on Oct. 20. RTRS

Xi Jinping made his first known visit to China’s central bank since he became president a decade ago, according to people familiar with the matter, underscoring the government’s increased focus on shoring up the economy and financial markets. BBG

The BOJ announced an unscheduled bond operation on Tuesday, as it sought to slow a rise in Japanese government bond (JGB) yields that had brought them to fresh decade highs. Japan’s central bank offered to buy 300 billion yen ($2.00 billion) in bonds with maturities of five to 10 years and 100 billion yen worth with maturities of 10-25 years from Wednesday. RTRS

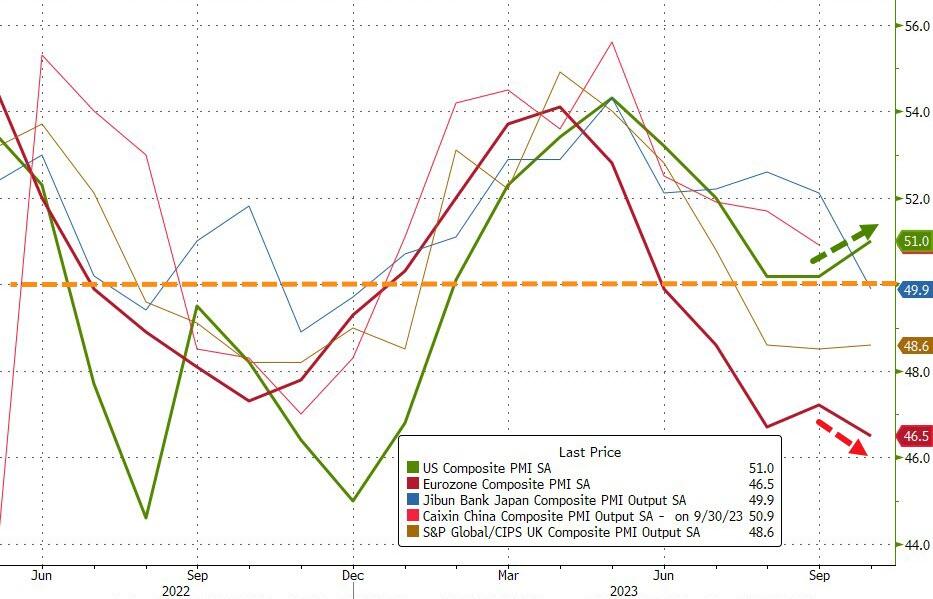

Europe’s flash PMIs fall short of expectations in Oct, w/manufacturing at 43 (down from 43.4 in Sept and below the Street’s 43.7 forecast) and services at 47.8 (down from 48.7 in Sept and below the Street’s 48.6 forecast). The region’s economy saw its downturn accelerate, with private sector output falling at the fastest pace in more than 10 years (ex-COVID). RTRS

The Biden administration is concerned that Israel lacks achievable military objectives in Gaza, and that the Israel Defense Forces are not yet ready to launch a ground invasion with a plan that can work, senior administration officials said. NYT

The US ramped up its rhetoric toward Iran, saying it would hold Tehran accountable for drone and rocket attacks on US troops by its proxies in the Middle East, even as Washington tries to avert a wider regional war. BBG

Global demand for oil will reach its peak this decade, the IEA predicted for the first time, amid growing demand for EVs and the cooling of China’s economy. The agency also lowered its projections for gas consumption for a fourth straight year, according to its annual World Energy Outlook. BBG

Jamie Dimon said central banks’ forecasts were “dead wrong” about 18 months ago. “I don’t think it makes a piece of difference whether rates go up 25 basis points or more, like zero, none, nada,” he said. Also at the FII summit in Riyadh, Ray Dalio voiced pessimism on the global economy, and Larry Fink said he expects the Fed to raise rates further. BBG

Bitcoin jumped to the highest since May 2022 — topping $35,000 before paring some gains — after a court ruled the SEC must reconsider Grayscale’s bid for a spot Bitcoin ETF. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed following a similar lead from Wall Street with Mainland China leading the gains overnight. ASX 200 traded in the green with the upside led by Metals & Mining following the prior session’s gains in the complex, although gold names lag after the precious metal unwound some geopolitical risk premium after the weekend. Nikkei 225 gave up the 31k level in early trade as the prior day’s firming of the JPY weighed on the export-heavy index. Hang Seng and Shanghai Comp opened mixed with the former playing catch-up following its long weekend, whilst the latter gained as reports also suggested US and China held the first working group meeting.

Top Asian News

The US Treasury Department said the US and China held the first meeting of the economic working group which serves as a channel to discuss bilateral economic policies, according to Reuters.

Former Chinese Vice Premier Liu He has retained his position as office director for a key economic policymaking body headed by Chinese President Xi, according to SCMP sources.

Japan aims to set shared standards with the US and Europe on subsidies for EVs, chips and other “critical fields”, according to Nikkei citing the Japanese Minister of Economy, Trade and Industry.

Japan will extend until Spring 2024 subsidies to curb utility bills and will extend until April 2024 subsidies to curb fuel prices, according to a draft economic package cited by Reuters.

BoJ unscheduled bond purchases: offered to buy JPY 100bln in 10-25yr JGBs and JPY 300bln in 5-10yr, according to Reuters.

PBoC injected CNY 593bln via 7-day reverse repos with the rate at 1.80% for a CNY 522bln net daily injection.

PBoC set USD/CNY mid-point at 7.1786 vs exp. 7.2992 (prev. 7.1792).

BoJ is said to see little need to change forward guidance, according to Bloomberg citing officials; adds is considering whether to tweak YCC given US yield concerns. Discussion over YCC is reportedly not due to the growing risk of upward price fluctuations but the impact on Japanese yields from the upside in US rates. Officials see there being little need to remove the following line from its guidance “If necessary, we will not hesitate to take additional monetary easing measures.”

Chinese President Xi has made an unprecedented visit to the PBoC in a “sign of focus on the economy”, according to Bloomberg.

European bourses were initially pressured from soft PMIs and as EZ credit standards continued to tighten. Since then, the space has recovered back into the green as newsflow slows somewhat but has featured favourable updates that Israel is willing to delay its Gaza ground invasion by a few days, Euro Stoxx 50 +0.5%. Within Europe, sectors are being dictated by earnings with Basic Resources outperforming after favourable reports from sector heavyweights while Banking names lag post-Barclays. US futures have been directionally in-fitting but with magnitudes slightly more contained than those in Europe, ES +0.4% and above 4250; NQ +0.7% continues to outperform ahead of numerous mega-cap corporate updates incl. Microsoft & Alphabet. General Electric Co (GE) Q3 2023 (USD): Adj. EPS 0.82 (exp. 0.56), Adj. Revenue 16.50bln (exp. 15.7bln). Raises FY Adj. EPS view 2.55-2.65 (prev. 2.10-2.30; exp. 2.36), FY organic Revenue view “low teens” (prev. “low double digits”). +6.0% in pre-market trade.

Top European News

German Economy Minister has promised industry EUR 50bln in tax relief over the coming four years, according to Handelsblatt. Additionally, Habeck is reportedly planning industrial policy which is geared towards state support and is looking to loosen the debt brake to attain this, via Welt & Suddeutsche Zeitung.

REUTERS POLL: BoE to hold the Bank Rate at 5.25% on Nov 2nd, according to 61 out of 73 economists; 12 expect 25bps rise to 5.50%; first BoE rate cut to 5.0% to come in Q3 2023 (unch. from Sept poll).

FX

Aussie and Euro flank G10 ranks as AUD/USD rebounds through 0.6350 with incentive from hawkish RBA rhetoric, but EUR/USD loses 1.0650+ status after disappointing EZ PMIs.

DXY regains poise between 105.350-780 parameters as US Treasuries top out pre-PMIs and 2 year supply.

Yen pivots 149.50 vs Dollar amidst more BoJ source reports touting the potential for YCC tweak.

Sterling straddles 1.2250 in wake of roughly in line UK PMIs and dip in ILO jobless rate.

RBA’s Bullock says the Board will not hesitate to raise the cash rate further if there is a material upward revision to the outlook for inflation. It is possible that the inflation goal can be achieved with the cash rate at its current level but there are risks that could see inflation return to target more slowly than currently forecast.

Fixed Income

Bonds extend bull-flattening correction before petering out.

Bunds reach 129.12 from 128.22, Gilts climb from 92.71 to 93.34 and T-note fades at 106-22 compared to 106-08+ overnight low ahead of US PMIs and 2 year note auction.

Commodities

Commodities have experienced some modest divergence with crude benchmarks initially firmer but slipping in the wake of another batch of soft PMIs from the EZ; price action which was exacerbated by PMI-induced EUR pressure and associated USD strength as a result, pushing the contracts to eventual session lows of USD 85.09/bbl and USD 89.46/bbl for WTI & Brent Dec’23 respectively.

Thereafter, the crude complex has moved back marginally into the green amid reports around China’s Xi and details within the latest Axios piece.

Spot gold has dipped marginally into the red amid the EUR-driven bout of USD strength. Though, the yellow metal remains comfortably above technical figures with the 10-DMA closest at USD 1935/oz compared to the current USD 1965/oz session trough which itself is just USD 1 above Monday’s base.

Base metals are similarly supported after Monday’s marked pressure and perhaps deriving support from the Chinese-driven APAC session, the mentioned PBoC/Xi visit and numerous well-received European earnings in the space.

Geopolitics: Israel-Hamas

Israel confirmed two hostages released by Hamas were handed over to the Israeli military, according to a statement.

US President Biden, when asked about a ceasefire, said we should have hostages released, according to Reuters.

IDF said it has “attacked several Hezbollah targets, including a surveillance and monitoring post in southern Lebanon”, according to Al Arabiya.

“Israeli occupation forces storm the village of Burqa, north of Nablus in the West Bank, amid gunfire”, according to Al Jazeera.

US official said Iran is seeking to escalate the conflict in the region, according to Bloomberg, adding Iranian fingerprints are all over the uptick in attacks while adding US presence in the Middle East includes intel sharing.

Russian Foreign Minister says “US reinforcements in the Middle East threaten to escalate tensions, according to Al Arabiya.

China’s Foreign Minister had a call with the Israeli Foreign Minister on Monday, according to Chinese state media.

US President Biden spoke with Israeli PM Netanyahu on Monday and discussed the war in Gaza, according to Axios citing a White House official.

Israel is willing to delay its ground invasion of Gaza by a few days to allow for talks on releasing a large number of hostages that Hamas is holding, via Axios citing officials. Though, officials add that even if a hostage deal is attained they will not drop plans for a ground assault into Gaza.

Geopolitics: Other

Russian President Vladimir Putin suffered a cardiac arrest in the presidential bedroom on Sunday, an insider group revealed; he regained consciousness, according to Sky News Australia citing unverified Telegram reports. Subsequently, Russian Kremlin says President Putin is fine, reports of ill-health are fake. Adds, talks of a Putin body double is an absurd hoax.

“Iran-backed militants have launched a drone attack against the al-Omar oil field, which hosts the largest US base in Syria, causing two explosions in the area”, according to Iran International citing Syrian press.

US Navy announces interception of missiles and drones launched by the Houthis across the Red Sea days ago”, according to Al Arabiya.

US Secretary of State Blinken is to host China’s top diplomat Wang Yi in Washington between Oct 26-28th, according to a senior admin official cited by Reuters, adding that the US is concerned over China’s recent destabilising actions in the South China Sea.

The EU still lacks “very clear evidence” of unfair practices to launch a formal probe into China’s wind power industry, according to Reuters sources.

US Event Calendar

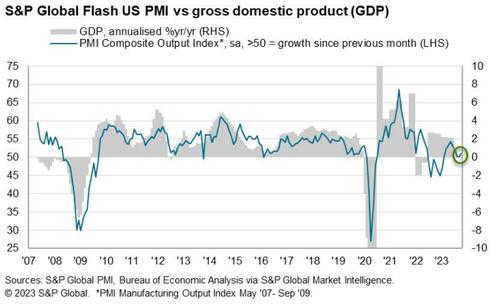

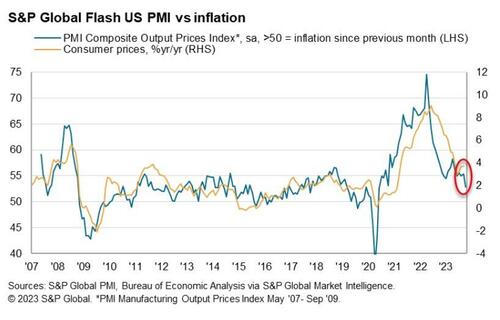

09:45: Oct. S&P Global US Services PMI, est. 49.9, prior 50.1

09:45: Oct. S&P Global US Manufacturing PM, est. 49.5, prior 49.8

09:45: Oct. S&P Global US Composite PMI, est. 50.0, prior 50.2

10:00: Oct. Richmond Fed Index, est. 3, prior 5

DB’s Jim Reid concludes the overnight wrap