EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: APRIL 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,705.100000000 USD

INTENT DATE: 04/23/2026 DELIVERY DATE: 04/27/2026

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DEUTSCHE BANK AG 5

118 H MACQUARIE FUTURES US 34

624 H BOFA SECURITIES 55

661 C JP MORGAN SECURITIES 1

737 C ADVANTAGE FUTURES 27

TOTAL: 61 61

MONTH TO DATE: 22,256

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2026: 61 CONTRACTs NOTICES FOR 6,100 OZ or 0.1877TONNES

total notices so far: 22,206 contracts FOR 2,220,600 OZ OR 69.225 TONNES

SILVER NOTICES: 13 NOTICE(S) FILED FOR 65,000 OZ /

total number of notices filed so far this month : 3301 CONTRACTS (NOTICES) for 16.505 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A STRONG QUEUE JUMP OF 42 CONTRACTS OR 0.210 MILLION OZ/NEW STANDING REDUCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 13 CONTRACT QUEUE JUMP WHERE 65,000 ADDITIONAL OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES HUGELY TO 16.5150 MILLION OZ PLUS 1.970 MILLION OZ OF EXCHANGE FOR RISK//NEW TOTALS STANDING 18.485 MILLION OZ

SUMMARY OF OUR APRIL 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 34.045 MILLION OZ..WILL BE SMALL THIS MONTH.

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 65,000 OZ QUEUE JUMP//NEW STANDING ADVANCES TO 16.515MILLION OZ PLUS 1.970 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 18.485 MILLION OZ

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR STRONG 86 CONTRACT QUEUE JUMP FOR 8600OZ/ (0.2674 TONNES)/NEW STANDING ADVANCES TO 69.4059 TONNES

MARCH:: SMALL INITIAL STANDING FOR GOLD FOR MARCH AT 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 46 CONTRACT QUEUE JUMP OF 4400 OZ OR 0.2320 TONNESAND THEN WE ADD BY OUR THREE EXCHANGE FOR RISK: 22.3818///NEW STANDING ADVANCES TO 67.6648 TONNES OF GOLD./

APRIL: INITIAL STANDING FOR GOLD; 52.600 TONNES FOLLOWED BY TODAY’S 8600OZ QUEUE JUMP(0.2674 TONNES) //NEW STANDING ADVANCES TO 69.4059TONNES.

STANDING FOR THE LAST 4 MONTHS JANUARY TO APRIL:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 8600 OZ QUEUE JUMP (0.2674TONNES): NEW STANDING ADVANCES TO 69.4059 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 71.34 TONNES// WILL BE VERY SMALL THIS MONTH

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONG

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE 1607 CONTRACTS TO AN OI OF 112,566

EFP ISSUANCE 755 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 755 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1537 CONTRACTS AND ADD TO THE 755 E.FP. ISSUED

WE OBTAIN A STRONG SIZED LOSS OF 822 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR LOSS OF $2.35

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 4.110 MILLION PAPER OZ

OCCURRED WITH OUR LOSS IN PRICE.OF $2.35

2.ASIAN AFFAIRS APRIL 24 /2025

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR 1537 CONTRACTS UP TO AN OI OF 364,471 CONTRACTS (OI) , HAVING ADVANCED FROM OUR NEW LOW OI SET THIS MONTH AND SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 354,581 SET APRIL6/2026. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 354,581 WITH GOLD AT AN EXTREMELY HIGH $4,700.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD ZERO T.A.S. LIQUIDATION DURING THURSDAY’S TRADING. IT SEEMS THAT THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE WITH THE BANKERS TAKING THE SHORT SIDE, SUPPLYING THE NECESSARY PAPER, AS WELL AS COVERING THEIR SHORTFALL. THERE ARE ALSO SOME SPECULATORS WHO CONTINUALLY GO TO THE SHORT SIDE AND THEY WILL BE ANNHILATED ON CENTRAL BANK COMMAND!!

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE MASSIVE AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS APRIL CONTRACT MONTH!!

THE STRONG SIZED GAIN ON OUR TWO EXCHANGES OCCURRED DESPITE OUR LOSS IN PRICE IN GOLD.

WE THUS HAD A TINY GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 103 CONTRACTS (OR 0.32 TONNES) WITH OUR LOSS IN PRICE, AS WE WERE INFORMED OF A SMALL 552 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE..

THEN WE WERE NOTIFIED TODAY OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0.0 TONNES OF GOLD.

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 0 EXCHANGE FOR RISK FOR FAR.

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO APRIL:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 0 EXCHANGE FOR RISK SO FAR.

DETAILS ON OUR NEW APRIL COMEX CONTRACT MONTH//

IN TOTAL WE HAD A TINY SIZED GAIN ON OUR TWO EXCHANGES OF 103 CONTRACTS WITH OUR LOSS IN PRICE ($28.35). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH APRIL/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A SMALL SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 552 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING THIS WEEK WITH MUCH FAILURE DURING LONDON LBMA/OTC OPTION EXPIRY WEEK!! (APRIL FIRST DAY NOTICE)

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD.

FOR MARCH WE HAVE 3 EXCHANGE FOR RISK ISSUANCES SO FAR FOR 7196 CONTRACTS OR 719,600 OZ/22.3818 TONNES.. AS DELIVERIES OF GOLD THESE PAST SEVERAL MONTHS HAVE BEEN HUGE!!

APRIL: 0 SO FAR HAVE BEEN ISSUED

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

AND NOW APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 8700 OZ (0.2574 TONNES) QUEUE JUMP. THUS STANDING FOR GOLD AT THE COMEX ADVANCES TO 69.4059TONNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING APRIL,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $28.35)

WE HAD ZERO T.A.S. SPREADER LIQUIDATION // COMEX SESSION// WITH OUR LOSS IN PRICE , OUR LONG SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI //

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

WEDNESDAY NIGHT//THURSDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 7 MONTHS:

STANDING FOR GOLD OCT THROUGH TO APRIL:

PRIL:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

4. JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR LATEST QUEUE JUMP OF 0.0298 TONNES TO WHICH THIS IS ADDED TO ALL OTHER QUEUE JUMPS OF 41.2082 / NEW QUEUE JUMP ADVANCES TO: 41.233 TONNES//STANDING ADVANCES TO: 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES/NEW STANDING ADVANCES TO 157.879 TONNES

MARCH: INITIAL STANDING: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TO WHICH WE THEN ADD OUR THREE EXCHANGE FOR RISK FOR 22.3818 TONNES// GOLD STANDING ADVANCES TO: 67.6648 TONNES/

APRIL: INITIAL STANDING: A VERY STRONG 52.600 TONNES FOLLOWED BY TODAY’S SMALL 8,600 OZ QUEUE JUMP (2.4105TONNES). THUS STANDING FOR GOLD AT THE COMEX ADVANCES TO 69.4059 TONNES

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $28.35

WE HAD 5049 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES : 103 CONTRACTS OR 10,300 OZ OR 0.3203 TONNES

INITIAL GOLD COMEX

APRIL DELIVERY MONTH

APRIL2332026

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | ENTRIES; 1 i) Brinks 200,814.846.OZ (6246 kilobars) total 200,814.846 oz 6.246 tonnes |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 61 CONTRACTS OR 6100 OZ 3.430 TONNES OF GOLD |

| No of oz to be served (notices) | 58 Contracts 5800 OZ 0.1804TONNES |

| Total monthly oz gold served (contracts) so far this month | 22,206 notices 2,220,600 oz 69.225 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 1

0 ENTRY

DEPOSITS/CUSTOMER

0 ENTRY

xxxxxxxxxxxxxxxxxx

comex withdrawals:

ENTRIES; 1

i) Brinks 200,814.846.OZ

(6246 kilobars)

total 200,814.846 oz

6.246 tonnes

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs

adjustments: / / 0

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF APRIL OI STANDS AT 119 CONTRACTS HAVING A LOSS OF 659 CONTRACTS.

WE HAD 745 CONTRACTS SERVED UPON THURSDAY SO WE GAINED A STRONG 86 CONTRACT QUEUE JUMP CONTRACTS. THUS 8600OZ OF ADDITIONAL GOLD WILL STAND ON THIS SIDE OF THE BORDER AND THIS EQUATES TO 0.2674TONNES.(QUEUE JUMP)

MAY LOST 112 CONTRACTS TO AN OI OF 3424 AS MAY BECOMES THE FRONT MONTH.

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI FELL BY 1139 CONTRACTS UP TO AN OI OF 263,642

We had 61 contracts filed for today representing 6100oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 61 notices issued from their client or customer account. The total of all issuance by all participants equate to 0 contract(s) of which 1 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for APRIL. /2026. contract month, we take the total number of notices filed so far for the month (22,256) to which we add the difference between the open interest for the front month of APRIL ( 119 CONTRACTS) minus the number of notices served upon today 61 x 100 oz per contract) equals 2,231,400OZ OR (69.4059 Tonnes of gold)

THUS: INITIAL total number of gold ounces standing for APRIL. /2026. contract month, we take the total number of notices filed so far for the month (22,256) to which we add the difference between the open interest for the front month of APRIL (119 CONTRACTS) minus the number of notices served upon today 61 x 100 oz per contract) equals 2,231,400 OZ OR (69.4059Tonnes of gold)

new total of gold standing in APRIL is 69.4059 TONNES//

TOTAL COMEX GOLD STANDING FOR APRIL 69.4059 TONNES TONNES WHICH IS NOW HUGE FOR THIS NORMALLY VERY ACTIVE ACTIVE DELIVERY MONTH OF APRIL.

confirmed volume THURSDAY confirmed 165,939 poor

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,937,269.176 oz 60.25 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,937,269.176tonnes oz 60.25 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 29,241,185.152 oz

TOTAL REGISTERED GOLD 15,665,991.922 487.278 onnes

TOTAL OF ALL ELIGIBLE GOLD 13,575,193.180 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,728,722 oz ((REG GOLD- PLEDGED GOLD)=

427.000 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

APRIL DELIVERY MONTH

APRIL23

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1 entries i) Brinks 1,200,179.565 oz total withdrawal 1,200,179.565 oz |

| Deposits to the Dealer Inventory | 0 entries xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT 0) entries |

| No of oz served today (contracts) | 13 CONTRACT(S) (65,000 OZ |

| No of oz to be served (notices) | 2Contracts (0.010 MILLION oz) |

| Total monthly oz silver served (contracts) | 3301contracts 16.505 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 entries

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

0) entries

total deposit: nil oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

1 entries

i) 1 entries

i) Brinks 1,200,179.565 oz

total withdrawal 1,200,179.565 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments:4

a) Asahi: 406,627.730 oz

b) Brinks 737,577.950 oz

c) JPmorgan: 792,312.300 oz

d) Manfra: 223,298.440 oz

total oz leaving the dealer to customer accts 2,159,816.02 oz

Thursday volume: 102,063 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 77,117 MILLION OZ//.TOTAL REG + ELIGIBLE. 315.152 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL /2026 OI: 15 OPEN INTEREST CONTRACTS FOR A GAIN OF 4 CONTRACTS. WE HAD 9 CONTRACTS SERVED ON THURDAY, SO WE GAINED A SMALL 13 CONTRACTS OR 65,000 OZ UNDERWENT ANOTHER QUEUE JUMP. STANDING THUS ADVANCES TO 16.515 MILLION OZ WHICH IS HUGE FOR THIS NORMALLY SMALL NON ACTIVE DELIVERY MONTH OF APRIL. BUT WE MUST ADD OUR SECOND EXCHANGE FOR RISK TOTALING 194 CONTRACTS OR .970 MILLION OZ. THIS IS ADDED TO OUR FIRST EXCHANGE FOR RISK ISSUED ON THURSDAY FOR 1.0 MILLION OZ//TOTAL EX FOR RISK: 1.970 TONNES. NEW TOTAL SILVER STANDING AT THE COMEX ADVANCES TO 18.485 MILLION OZ.

MAY SAW A LOSS OF 4016 CONTRACTS DOWNTO 30,616 CONTRACTS. MAY BECOMES THE NEW FRONT MONTH. WE HAVE 5 MORE READING DAYS BEFORE FIRST DAY NOTICE

JUNE SAW A LOSS OF 49 CONTRACTS DOWN TO 1220 OI CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 13 or 65,000 oz

CONFIRMED volume THURSDAY; 102,063 huge

AND NOW APRIL. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 3301 X5,000 oz = 16.505 MILLION oz

to which we add the difference between the open interest for the front month of APRIL (15) AND the number of notices served upon today (13 )x (5000 oz)

Thus the standings for silver for the APRIL 2026 contract month: (3301 )Notices served so far) x 5000 oz + OI for the front month of APRIL (15) minus number of notices served upon today (13)x 5000 oz equals silver standing for the APRIL..contract month equating to 16.515 MILLION OZ.+ 1.970 MILLIONEXCHANGE FOR RISK WHICH MUST BE ADDED TO NORMAL DELIVERIES..NEW TOTALS 18.485 MILLION OZ

NEW STANDING: 18.485 MILLION OZ WHICH IS HUGE FOR A GENERALLY LOUSY DELIVERY MONTH OF APRIL.

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 77,117 million oz of registered silver

JPMorgan as a percentage of total silver: 142.322/315.152 million: 44.93

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

APRIL 24/2026/WITH GOLD UP $13.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 23/2026/WITH GOLD DOWN 28.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.000 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1050.91 TONNES

APRIL 22/2026/WITH GOLD UP 26.40 TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 21/2026/WITH GOLD DOWN 11.90TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 17/2026/WITH GOLD UP $71.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 1.15 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 16/2026/WITH GOLD DOWN $15.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.285 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1051.783 TONNES

APRIL 15/2026/WITH GOLD DOWN $24.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.289 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1049.478 TONNES

APRIL 14/2026/WITH GOLD UP $83.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.714 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1047.192 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 10/2026/WITH GOLD DOWN $11.90 TODAY/SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.724 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.42 TONNES

APRIL 9/2026/WITH GOLD UP $42.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.429 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.990 TONNES

APRIL 8/2026/WITH GOLD UP $88.95 TODAY/NO CHANGES IN GOLD AT THE GLD A//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 7/2026/WITH GOLD UP $5.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.429 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 6/2026/WITH GOLD UP $5.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/INVENTORY RESTS AT 1050.99 TONNES

APRIL 2/2026/WITH GOLD DOWN $132.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.714 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1050.99 TONNES

APRIL 1/2026/WITH GOLD UP $134.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 1.143 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1047.276 TONNES

MAR 31/2026/WITH GOLD UP $119.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.429 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1046.133 TONNES

MAR 30/2026/WITH GOLD UP $33.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.143 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1049.562

MAR 27/2026/WITH GOLD UP $103.55 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.285 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.705

MAR 26/2026/WITH GOLD DOWN $213.05 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.580 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.42

MAR 25/2026/WITH GOLD UP $155.30 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.300 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1053.000

MAR 24/2026/WITH GOLD DOWN $7.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.286 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1052.705

MAR 23/2026/WITH GOLD DOWN $165.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 5.149 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1056.991

MAR 20/2026/WITH GOLD DOWN $39,55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.855 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1062.135

MAR 19/2026/WITH GOLD DOWN $XXX TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 2.57 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1066.99

MAR 18/2026/WITH GOLD DOWN $111.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.144 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1069.564 TONNES

MAR 17/2026/WITH GOLD UP $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 0.857 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.708 TONNES

MAR 16/2026/WITH GOLD DOWN $60.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4/327 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1071/.565 TONNES

MAR 13/2026/WITH GOLD DOWN $61.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.428 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1075.852 TONNES

MAR 12/2026/WITH GOLD DOWN $49.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 3.715 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1077.28 TONNES

MAR 11/2026/WITH GOLD DOWN $70.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 2.858 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1073.565 TONNES

MAR 10/2026/WITH GOLD UP $137.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 2.614 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.707 TONNES

GLD INVENTORY: 1046.62 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

APRIL 24WITH SILVER UP 0.92: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.54 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 487,23MILLION OZ

APRIL 23WITH SILVER DOWN $2.35: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.489 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 488,773MILLION OZ

APRIL 22 WITH SILVER UP 1.43: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262MILLION OZ

aPRIL 21 WITH SILVER DOWN 3.71: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262 MILLION OZ

APRIL 17 WITH SILVER UP $3.09: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.453 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.900 MILLION OZ

APRIL 16 WITH SILVER DOWN $1.00: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.132 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.477 MILLION OZ

APRIL 15 WITH SILVER UP $0.01: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.588 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.579 MILLION OZ

APRIL 14 WITH SILVER UP $3.99: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.633 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.991 MILLION OZ

APRIL 13 WITH SILVER DOWN 0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.589 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.624 MILLION OZ

APRIL 10 WITH SILVER DOWN 0.16: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.724 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 492.213 MILLION OZ

APRIL 9 WITH SILVER UP $0.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.173 MILLION OZ INTO THE SLV// // :INVENTORY RESTS AT 492.937 MILLION OZ

APRIL 8 WITH SILVER UP $3.50: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 7 WITH SILVER DOWN $0.89: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 6 WITH SILVER UP $0.41: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL WITHDRAWAL OF 0.224 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 2 WITH SILVER DOWN $3.57: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.091 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.988 MILLION OZ

APRIL 1 WITH SILVER UP $1.38: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND WITHDRAWAL OF 0.453 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 491.079 MILLION OZ

MAR 31 WITH SILVER UP $4.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND FRAUDULENT WITHDRAWAL OF 3.893 MILLION OZ FROM THE SLV // :INVENTORY RESTS AT 491.532 MILLION OZ

MAR 30 WITH SILVER UP $0.74: NO CHANGES IN SILVER INVENTORY AT THE SLV: // :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 27 WITH SILVER UP $1.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV// :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 26 WITH SILVER DOWN $4.75: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 25 WITH SILVER UP $3.25: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 24 WITH SILVER DOWN $0.15: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT DEPOSIT OF 10.505 MILLION OZ INTO THE SLV :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 23 WITH SILVER UP $0.06: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// NO CHANGE IN INVENTORY/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 20 WITH SILVER DOWN $1.92: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.490 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 19 WITH SILVER DOWN $6.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.9444 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 490.761 MILLION OZ

MAR 18 WITH SILVER DOWN $2.36: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 1.087 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 494.792 MILLION OZ.

MAR 17 WITH SILVER DOWN $0.89: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 493.705 MILLION OZ.

MAR 16 WITH SILVER DOWN $0.57: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.536 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 497.056 MILLION OZ.

MAR 13 WITH SILVER DOWN $3.83: NO CHANGES IN SILVER INVENTORY AT THE SLV// . ./ :INVENTORY RESTS AT 499.592

MAR 12 WITH SILVER DOWN $0.51 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 3.713 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 499.592 MILLION OZ

MAR 11 WITH SILVER DOWN $3.96 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 1.812 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 503.305 MILLION OZ

MAR 10 WITH SILVER UP $5. HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.63 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 505.117 MILLION OZ

MAR 9 WITH SILVER DOWN $0.30 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.54 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 506.747 MILLION OZ

CLOSING INVENTORY 487.23 MILLION OZ OF SILVER

ANDREW MAGUIRE LIVE FROM THE VAULT 269

AEM TAKING OVER FINNISH ASSETS

AEM JUST MADE A BID FOR FINNIISH ASSETS. IS THIS A GOOD DEAL?

Yes, Agnico Eagle Mines (AEM) announced a major consolidation of Finnish gold assets on April 20, 2026, through three linked transactions totaling roughly $3.7–3.8 billion (with potential additional contingent payments). This builds on its existing Kittila mine (Europe’s largest primary gold mine) in the Central Lapland Greenstone Belt.

reuters.com

Deal Breakdown

- Rupert Resources (primarily the advanced Ikkari gold project): ~C$2.9 billion (US$2.1 billion) mainly in AEM shares + up to ~C$700 million in contingent value rights (CVRs) tied to future milestones like reserve growth and production. AEM already owned ~13.9% of Rupert. prnewswire.com

- Aurion Resources: C$481 million all-cash. AEM already held ~9.9%. Aurion brings a large contiguous land package (761 km²). northernminer.com

- B2Gold’s 70% stake in Fingold JV: US$325 million cash (giving AEM 100% of the JV once combined with Aurion’s portion). theglobeandmail.com

Total land position: ~2,492 km² (from ~355 km² today), creating a contiguous district around Kittila and Ikkari (Ikkari is ~50 km from Kittila). Expected closing: Q3 2026, subject to approvals.

reuters.com

Why AEM Sees It as Strategic

- Production upside: Aims for a multi-asset hub producing ~500,000 oz gold annually within the next decade (more than doubling current Finnish output). Ikkari has a solid resource base (e.g., 3.5 Moz probable reserves at 2.1 g/t). mining.com

- Synergies: Up to $500 million in operational, development, and construction savings by removing property boundaries, sharing infrastructure (Kittila has 20+ years of operating experience in Finland), and accelerating exploration/development. bullpen.finance

- Exploration potential: Large, under-explored land package with upside at Ikkari, Pahtavaara (past-producing), and early-stage targets. Also prospective for critical minerals.

- Jurisdiction: Finland is a top-tier, stable mining country with strong infrastructure.

This mirrors AEM’s successful district-scale approach in Canada (e.g., Abitibi). CEO Ammar Al-Joundi called it a “multi-decade regional platform” in a “world-class gold belt.”

agnicoeagle.com

Is This a Good Deal?For AEM shareholders — It looks solid to positive on paper for a long-term holder:

- Pros: High-quality assets in a familiar jurisdiction, meaningful production growth, significant synergies, and exploration leverage. AEM has a strong balance sheet, low costs, and a track record of integrating assets efficiently. Paying partly in stock (for Rupert) preserves cash and aligns with targets’ shareholders.

- Cons/Risks: Large outlay (~$3.8B); integration/permitting/execution risks in a cold, remote area; gold price sensitivity (though AEM is a low-cost producer); dilution from share issuance; and CVR payouts if milestones hit. Markets reacted with some AEM share weakness initially amid broader gold miner sell-off and “digest the deal” sentiment. quiverquant.com

- Valuation context: At current gold prices and with synergies/exploration upside, analysts and coverage view it as a logical consolidation play rather than overpaying for “blue sky.” It’s not a cheap bolt-on but builds scale where AEM already has expertise.

Overall market reaction: Targets (Rupert, Aurion) jumped on premiums. AEM shares dipped modestly as investors weighed the size and timeline (production ramp over years, not immediate). No major red flags in reporting—it’s seen as a strategic “hub-building” move amid industry consolidation trends.

cruxinvestor.comBottom line: For a high-quality, patient gold major like AEM with Finland experience, this appears to be a good strategic deal that strengthens its portfolio for the long haul. It’s less about short-term accretion and more about creating a durable, multi-decade production and exploration engine. Whether it’s “great” depends on gold prices, execution, and final costs—standard mining risks apply.If you’re an investor in AEM (or considering it), this adds growth without changing the company’s conservative, high-margin style. Always do your own due diligence or check full filings/investor presentations for resource details, costs, and timelines. Gold sector deals like this often look better in hindsight if the district delivers.

END

ASIAN TRADING AND NEWS BEFORE START OF TRADING OVER THERE;

Europe set for lower open despite INTC surging 19% as crude remains elevated – Newsquawk EU Market Open

Friday, Apr 24, 2026 – 02:18 AM

- Israel is on high alert in anticipation of a possible renewed war this weekend, according to Al Arabiya, citing Channel 13.

- Speaker of the Iranian Parliament Ghalibaf resigns from the negotiating team following the intervention of the IRGC, N12 news reported.

- US President Trump said the US is to work with Lebanon to protect itself from Hezbollah and that the Israel-Lebanon ceasefire is to be extended by three weeks.

- NQ futures outperformed after Intel surged over 19% after-hours as the Co. provided a solid Q1 report while raising its guidance.

- US President Trump said the US will put a tariff on the UK if the digital service tax is not dropped.

- APAC stocks traded mostly in the red, ex. Nikkei 225; European equity futures are indicative of a softer open with the Euro Stoxx 50 futures -0.7%.

- Looking ahead, highlights include UK Retail Sales (Mar), German Ifo Survey (Apr), Canadian Retail Sales (Feb), US UoM Survey Final (Apr), CBR Policy Announcement (Apr), Speakers include SNB’s Schlegel, Supply from Italy, Earnings from Procter & Gamble & Eni.

SNAPSHOT

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- US President Trump posted that the meeting between Israel and Lebanon went well, the US is to work with Lebanon to protect itself from Hezbollah and that the Israel-Lebanon ceasefire is to be extended by three weeks. He added that it would be great to resolve simultaneously with Iran.

- US Secretary of State Rubio said there is optimism we will be closer to permanent peace following the Lebanon ceasefire extension.

- US President Trump said ‘don’t rush me’, regarding Iran war length, adding that the US will take out Iran’s ‘wiseguy ships’ if we see them and noted maybe Iran loaded during hiatus, and will knock them out, but we have been speaking and they want to make a deal. He went on to say that the US has no pressure and could make a deal with Iran, but want to make the best one. He said the Strait will open when Iran makes a deal, and if no deal, will finish it up militarily.

- US President Trump posted that “Iran’s Navy is lying at the bottom of the Sea, their Air Force is demolished, their Anti-Aircraft and Radar Weaponry is gone, their leaders are no longer with us, the Blockade is airtight and strong and, from there, it only gets worse — Time is not on their side! A Deal will only be made when it’s appropriate and good for the United States of America, our Allies and, in fact, the rest of the World.”

- US military is developing plans to target Iran’s Hormuz defences if the ceasefire fails, CNN reported.

- Iranian Media Journalist Khalili said the resignation of Ghalibaf from the chairmanship of the negotiating delegation is not true. This reiterated reports by journalist Ghaderi stating that Israel Channel 12 news that Ghalibaf has resigned from negotiating team is completely false.

- Speaker of the Iranian Parliament Ghalibaf resigns from the negotiating team following the intervention of the IRGC, N12 news reported.

- Fars News reported that recent sound of defense systems in Tehran and several other cities in Iran was in response to the presence of micro-aircraft and small drones, including the “Orbitor” type, in several parts of the country. This pushes back from earlier reports by Al Araby stating that activating air defences in Tehran was a test.

- Israel said it did not launch any attack in Iran, Al Araby reported citing Ynet.

- Iranian Foreign Ministry Spokesman said they have not yet decided to participate in a new round of negotiations with Washington and transferring highly enriched uranium is not an option, and reducing concentration is an option on the table, Al Jazeera reported.

- Iran does not consider the nuclear issue as part of the negotiations, Tasnim reported. Negotiations with US are only for the end of the war. The situation is getting worse for US.

- There is no change in the ceasefire status with Iran, Al Jazeera reported citing US defense official.

- Pakistani sources told Al Arabiya that negotiations between the US and Iran are continuing despite the current stalemate. The decision to participate inside Iran has not yet been finalized.

- An Iranian bulk carrier carrying rice was escorted by IRGC naval vessels and safely crossed the Sea of Oman and reached Iran, despite the US Navy’s attempts to seize it, according to Fars News.

- Iran’s IRGC navy laid more mines in the Strait of Hormuz this week, according to a US official and a source cited by Axios.

- Iranian Foreign Minister Araghchi says the battlefield and diplomacy are fully coordinated fronts in the same war; Iranians are all united, more than ever before.

- There are Israeli and American officials who believe that Mojtaba Khamenei is not functioning as the Supreme Leader of Iran, does not give orders, and does not control Iran, two sources familiar with the details told i24NEWS.

- Israel on high alert in anticipation of a possible renewed war this weekend, according to Al Arabiya citing Channel 13.

- Israeli Defense Minister Katz said Israel is prepared to renew the war against Iran, and the IDF is prepared for defense and attack and the targets are marked.

- Hezbollah said it has launched rockets at Israel’s Shtula region in response to Israel violating ceasefire and targeting towns in southern Lebanon.

- Continued violations of the ceasefire in Lebanon by Israel, reports of Israeli warplane attacks in Rashaf, Southern Lebanon, via Tasnim.

- Lebanese media reported that Israel has conducted airstrikes on the town of Al-Qasir in southern Lebanon a few hours after US President Trump announced the 3-week ceasefire extension, IRIB reported.

- Israel’s ambassador to the UN said the extension of the Lebanon ceasefire is not 100% certain and that Israel is forced to answer every time a threat is detected, Tasnim reported citing CNN.

US TRADE

EQUITIES

- US stocks ended lower in a choppy session. Early optimism over potential progress in US-Iran talks reversed late in the session on fresh geopolitical headlines. Sectors were mixed, with technology lagging and utilities outperforming. Technology was hit by software stocks after weak earnings from IBM and ServiceNow weighed on the sector, but losses were capped by gains in semiconductors after strong earnings from Mobileye. Meanwhile, Tesla fell after missing revenue expectations and raising capex, while Meta announced 10% layoffs and Microsoft flagged voluntary retirements.

- SPX -0.41% at 7,108, NDX -0.57% at 26,783, DJI -0.36% at 49,310, RUT -0.37% at 2,775.

TARIFFS/TRADE

- US President Trump said the US will put a tariff on the UK if the digital service tax is not dropped.

- US President Trump said car companies are coming from Canada, Mexico and Japan, all the chip companies are coming back to the US and that the US is leading China in AI. He goes on to further say that the US will have close to 50% of the chip market pretty soon.

- US Commerce Secretary Lutnick said the US negotiated a great deal with Taiwan on chips and expects USD 1tln in chip fabs.

- EU warns that US trade deal risks unravelling with proposed changes, according to Bloomberg citing sources.

- Canada is reportedly to seek talks with the EU regarding access to ‘Made in Europe’ scheme, according to FT.

- EU and US are expected to announce today that they’ve concluded an agreement to cooperate on critical minerals, Politico reports, citing officials and diplomats. EU Trade Chief is to give a presser at 16:45 BST.

NOTABLE HEADLINES

- US President Trump said Kevin Warsh is terrific, while he repeats criticism on Fed Chair Powell and said Powell should have lowered rates.

APAC TRADE

EQUITIES

- APAC stocks traded mostly in the red, ex. Nikkei 225, as bourses caught up to the selloff seen stateside, as risk-off flows dominated the tape after the reports that Israel is on high alert in anticipation of a possible renewed war this weekend.

- ASX 200 slipped further below the 8,800 handle, as losses in IT offset the gains made by Energy names.

- Nikkei 225 outperformed, supported by the tech sector as chips benefitted from Intel’s earnings (see more below). Ibiden, one of Japan’s biggest electronics companies, hit a new ATH while Canon fell after cutting its FY profitability guidance.

- Hang Seng and Shanghai Comp traded with the biggest losses, albeit just slightly, after a flurry of earnings. China Telecom reported Q1 net that fell by 17% Y/Y while autos underperformed.

- US equity futures are mixed, with NQ futures the clear outperformer after Intel surged over 19% after-hours as the Co. provided a solid Q1 report while raising its guidance.

- European equity futures are indicative of a softer open with the Euro Stoxx 50 futures -0.7% after cash closed -0.3% on Thursday.

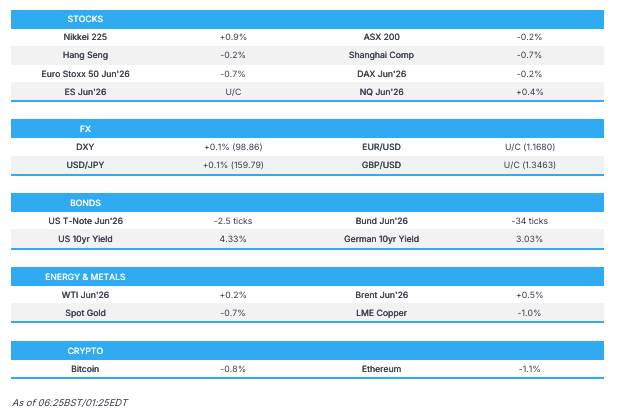

FX

- DXY traded muted, failing to find a clear directional bias after finding resistance at the 50-SMA and topped just shy of the 20-SMA in Thursday’s session.

- EUR/USD held above 1.1680, ahead of the German IFO survey, in which business climate is expected at 84.8 (prev. 86.4). To recap Thursday’s flash PMIs, the services sector was hit the hardest, falling deeper into contractionary, while highlighting price pressures for the EZ not seen since the pandemic.

- GBP/USD traded in a tight 1.3454-1.3473 range, with Retail Sales expected as European traders begin to sit at their desks. Markets are expecting a better reading compared to the February print, but still remaining subdued. Commonly used as a proxy, Barclaysʼ Consumer Spend report for March showed steady card spending with strong essential activity offsetting slower discretionary growth.

- USD/JPY steadily ground higher, as the JPY underperformed its G10 peers despite hotter CPI and PPI prints that should, in theory, support the Yen. The latest data is most likely not going to affect policymakers at the BoJ, in which a 97% probability of a hold is priced in. Currently, USD/JPY trades just shy of 159.80.

- Antipodeans were mixed, as the Kiwi outperformed after being the laggard in the prior session.

FIXED INCOME

- 10yr UST futures rotated in a tight 3 tick range as markets digested the latest geopolitical updates, with the 10yr yield currently trading at 4.33%. The nearest level that could provide some near-term resistance lies at 4.35%, while downside to 4.25% could be seen ahead of the Fed rate decision next week.

- Bund futures, similarly, oscillated in a narrow range ahead of the German IFO survey. German debt found support at the 125 handle as the 10yr yield hit 3.05%, ahead of an ECB policy meeting in which the Governing Council is expected to hold rates at 2.0%.

- 10yr JGB futures briefly topped above the 130 handle before trickling lower. Hotter CPI and Services PPI failed to drive Japanese debt, with the BoJ nearly fully pricing in a hold at next week’s policy meeting.

- Australia sells AUD 1bln vs exp. AUD 1bln 2.50% 2030 AGB: b/c 3.82x (prev. 3.44x), average yield 4.6947% (prev. 4.2888%).

- US sells USD 26bln of 5-year TIPS; tail 0.2bps.

COMMODITIES

- Crude futures have held onto Thursday’s gains but came off best levels, with Brent back below the USD 106/bbl handle while WTI pulled back slightly from the USD 97/bbl handle. Just before the futures open, US President Trump announced the 3-week extension of the Israel-Lebanon ceasefire. Trump highlighted that the talks went very well and that the US will work with Lebanon to protect itself from Hezbollah; crude prices were unreactive following the post by President Trump. Updates on the Iran conflict have been limited, with the latest report by CNN detailing that the US military are developing plans to target Iran’s Hormuz defences if the ceasefire fails.

- Precious metals traded muted, with spot gold oscillating in a tight USD 4687-4711/oz range. This comes ahead of a light data schedule. CME announced that they are to cut the initial margin on its COMEX 100 gold futures and COMEX 5000 silver futures to 6% (prev. 7%) and 11% (prev. 14%), respectively.

- Base metals lack direction. 3M LME Copper gapped back below USD 13.3k/t and currently holds below, catching up to the risk-off tone in the latter part of Thursday’s session.

- US President Trump said that the US does not have an oil shortage and are taking millions of barrels of oil from Venezuela.

- US President Trump set to extend US ship waiver to ease oil and gas deliveries, according to Bloomberg citing sources familiar with Trump’s plans on the Jones Act waiver.

- Imports of Russian fuel oil to Singapore have jumped with volume in April, already more than double the average monthly amount in 2025, according to FT citing Vortexa data.

- The fire at Russia’s Tuapse oil terminal is under control.

- CME cuts initial margin on its Comex 100 gold futures to 6% from 7% and Comex 5000 silver futures to 11% from 14%.

CRYPTO

- Bitcoin slipped back below USD 78k.

NOTABLE ASIA-PAC HEADLINES

- Japanese Finance Minister Katayama said speculative activity is increasing due to oil prices and will take decisive action on speculative activity, based on the agreement with the US. She added that Japan will continue to closely coordinate with the US and that there are no plans to change currency swap lines with the US.

- Japanese Trade Minister Akazawa said regulatory moves for energy conservation is not being considered and not expecting an immediate hike in power rates.

- Chinese EV makers are reportedly focusing on building in-house chips to improve autonomy and making cars smarter.

DATA RECAP

- Japanese Core Inflation Rate YoY (Mar) Y/Y 1.8% vs. Exp. 1.7% (Prev. 1.6%, Low. 1.4%, High. 1.9%).

- Japanese Inflation Rate YoY (Mar) Y/Y 1.5% (Prev. 1.3%).

- Japanese Inflation Rate Ex-Food and Energy YoY (Mar) Y/Y 2.4% (Prev. 2.5%).

- Japanese Inflation Rate MoM (Mar) M/M 0.4% (Prev. -0.2%).

- Japanese Services PPI Y/Y 3.1% vs exp. 3.0% (prev. 2.7%).

GEOPOLITICS

OTHER

- An internal Pentagon email explores options to punishing NATO allies that the US believes failed to support the US operations against Iran, according to a US official. Options include: Suspending Spain from NATO, reviewing the US position on British claims to the Falkland Islands, suspending difficult countries from important or prestigious positions at NATO.

- US official said Russia is to be included in G20 summit invitations.

EU/UK

NOTABLE HEADLINES

- SNB’s Schlegel said the Bank will not hesitate to move rates into negative territory and that a move below zero is a bigger step than a normal cut.

- SNB Vice Chairman said SNB has a greater willingness to intervene in the FX market, Reuters reported.

- BoE’s Breeden said equity markets look overvalued and could decline, according to the BBC.

- END

EUROPE OPENING FOR TRADING

NQ outperforms as INTC +28% premarket, Brent on $107/bbl handle, UoM finals ahead – Newsquawk US Market Open

Friday, Apr 24, 2026 – 05:49 AM

- “Israeli media: A limited operation against Iran may be carried out to avoid a prolonged war”, Al Arabiya reports.

- Chinese Securities Regulator says that China is to allow qualified foreign investors to trade treasury futures from April 24, 2026, for hedging purposes only.

- Downbeat sentiment across European bourses, SAP +6% after a EUR 10bln share buyback; NQ outperforms, with INTC +23% post-earnings.

- FX price action lacklustre, CHF and JPY dodge intervention comments, UoM Final ahead

- Fixed falters as energy climbs, Gilts lag again in catch-up trade and after further hawkish impetus into the BoE.

- Crude underpinned as eyes remain on US-Iran ceasefire heading into the weekend.

- Looking ahead, highlights include Canadian Retail Sales (Feb), US UoM Survey Final (Apr), CBR Policy Announcement (Apr).

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

MIDDLE EAST

- US President Trump posted that the meeting between Israel and Lebanon went well, the US is to work with Lebanon to protect itself from Hezbollah and that the Israel-Lebanon ceasefire is to be extended by three weeks.

- US President Trump said nobody is trying to get through the US blockade.

- US President Trump said the Israel-Lebanon talks in the Oval Office went well and it would be great to resolve simultaneously with Iran. Looking forward to the next meeting with Israeli PM Netanyahu. Great chance of peace between Israel and Lebanon this year. Everyone seems united against Hezbollah. Israel-Lebanon peace should be an easy one. Israel will have to defend itself if they are shot at. Israel will be surgical in their self-defence. Iran has to cut its Hezbollah funding.

- Tanker Helga arrives at Iraq’s Basra offshore terminal to load 2mln BPD of crude, sources say; Helga is the second tanker to reach Basra terminals since the Hormuz closure.

- “Israeli media: A limited operation against Iran may be carried out to avoid a prolonged war”, Al Arabiya reported.

- Pakistani official noted of a state of uncertainty regarding the second round of talks, “and we await Iran’s response”, Al Arabiya reported.

- Israel again attacks southern Lebanon, claiming retaliation for overnight rocket fire, Al Jazeera reported.

- Lebanese press Al-Jumhuriya noted of accelerated diplomatic efforts toward a Lebanon–Israel non-aggression agreement, driven by the US–Saudi–Egypt initiative, Journalist Kais reported. Plan revives idea of containing (not dismantling) Hezbollah’s weapons. Key proposed terms:. Israel withdraws to ceasefire line. Lebanese army deploys in south. Hezbollah moves north of Litani River. Start of weapons containment plan. Border disputes (Blue Line) adjusted. Prisoner releases, return of civilians, reconstruction. Deal would have international (especially US) guarantees. Coordination includes Iran to ensure Shiite/Hezbollah involvement. Parallel effort to resolve internal Lebanese political divisions. Saudi envoy pushing for meeting of Lebanon’s top leaders to create a unified position.

- “Iranian Foreign Ministry: Araqchi held two called with the Pakistani army chief and foreign minister to discuss a ceasefire.”, Al Araby reported.

- Iranian Vice President said any attack on oil wells will be met with strikes on attackers’ oil facilities; said it will be beyond “eye for an eye” response, Mehr News reported.

- Senior IRGC Commander said Tehran is secure and its borders are stronger than before, Press TV reported.

- The US has put a USD 10mln bounty on the leader of the Iran-backed Shiite militia group in Iraq, CBS reported.

- Lebanese media reported that Israel have conducted airstrikes on the town of Al-Qasir in southern Lebanon a few hours after US President Trump announced the 3-week ceasefire extension, IRIB reported.

- Israel’s ambassador to the UN said the extension of the Lebanon ceasefire is not 100% certain and that Israel is forced to answer every time a threat is detected, Tasnim reported citing CNN.

- US military are developing plans to target Iran’s Hormuz defences if the ceasefire fails, CNN reported.

- Israel-Lebanon talks have gotten underway in the White House, according to reported.

- Hezbollah said it has launched rockets at Israel’s Shtula region in response to Israel violating ceasefire and targeting towns in southern Lebanon.

- Israeli military said several launches crossed from Lebanon towards Israel were intercepted.

- An internal Pentagon email explores options to punishing NATO allies that the US believes failed to support the US operations against Iran, according to a US official. Options include:. Suspending Spain from NATO. Reviewing the US position on British claims to the Falkland Islands. Suspending difficult countries from important or prestigious positions at NATO.

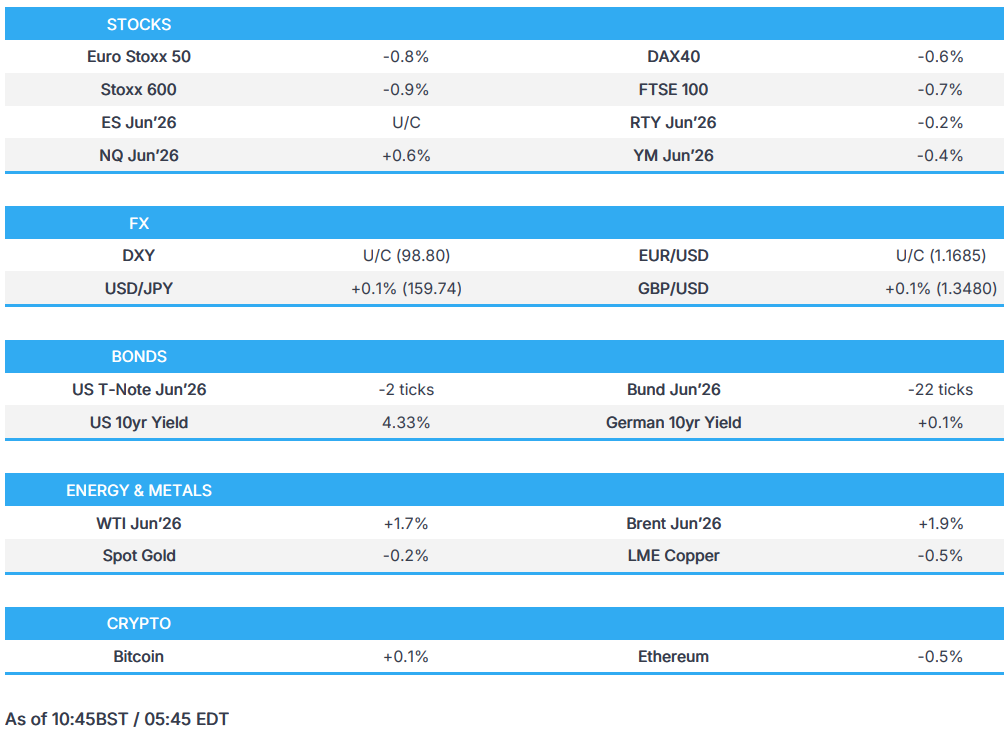

EQUITIES

- European bourses started the European session with broad based losses, continuing the downbeat mood seen across APAC trade. From an index perspective, the IBEX 35 (-1.3%) lags peers, whilst the AEX (-0.1%) fares a bit better vs peers.

- European sectors hold a strong negative bias. Energy leads, buoyed by strength in underlying oil prices. Also for the sector, Siemens Energy (+2.4%) gains post-earnings after it reported a mixed set of results, but raised its FY outlook; elsewhere, Eni (+1%) beat on its Adj. EBIT metric, and announced a 90% increase to its share buyback, citing an upbeat commodities outlook. Tech and Telecoms complete the top three. The Tech sector has been boosted today by post-earnings strength in SAP (+6.4%). The Co. reported better-than-expected operating profit and revenue, with cloud metrics also topping expectations. It also said it will buy back EUR 10bln of shares. To the bottom of the pile resides Autos, Basic Resources and Retail. The autos sector is underperforming this morning with seemingly broad-based losses; Volvo (+1%) reported Q1 metrics today, where its metrics were mixed, but ultimately indicating resilience amidst challenges.

- US equity futures are mixed, with the NQ (+0.5%) outperforming, whilst ES (U/C) and RTY (-0.3%) lag. The tech-heavy index has been buoyed by significant pre-market strength in Intel (+23%, strong earnings and guidance), TSMC (+3%, Taiwan eases fund limits) and AMD (+7.4%). Ahead, US Michigan final sentiment is expected to see consumer sentiment at 47.6 (prev. 53.3, current conditions at 50.1 (prev. 55.8), expectations at 46.1 (prev. 51.7), while one-year inflation expectations are seen up to 4.8% (prev. 3.8%), and five-year expectations at 3.4% (prev. 3.2%). Canada retail sales are seen rising 0.2% M/M (prev. 0.9%).

- Intel (+23%) after stronger-than-expected earnings and revenue in Q1, robust Q2 guidance, growing signs of a business revival, strong data centre and foundry growth, and optimism around rising AI-related CPU and advanced packaging demand.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- FX price action is lacklustre on the final trading day of the week. DXY leads marginally, while CHF and JPY are slightly lower.

- DXY trades tentatively and broadly in tandem with oil prices. A light calendar ahead with the Fed on blackout ahead of next week’s meeting and only UoM final data on the docket. USD-specific news light, though the Japanese Finance Minister said overnight there were no plans to change currency swap lines with the US. DXY still remains supported above 100 and 200 DMAs at 98.50; upside resistance is 98.90, which marks the session high.

- SNB Chairman Schlegel was on the wires a couple of times. He said they have “unrestricted” room for manoeuvre when it comes to the policy rate and FX intervention – Vice Chair Martin also echoed these remarks. EUR/CHF is unchanged on the session; it attempted to approach 0.92, but the move faltered at 0.9199.

- Katayama is also on the wires, she said “will take decisive action on speculative activity”, JPY unchanged, in a signal that markets are becoming comfortable with the Finance Minister’s threats. USD/JPY unchanged, looks at 160 to the upside. BoJ rate decision next week, likely to remain on hold, with all eyes on Governor Ueda’s tone at the presser.

- GBP shrugged off strong UK Retail Sales for March, as it does not change the narrative into next week’s BoE, where a hold is the base case. The data showed upside was driven by an increase in fuel sales, with retailers reporting that motorists were filling their tanks when buying following the start of the Middle East conflict. Online sales saw upside and are potentially indicative of a robust spring sale period. However, the core figures were in line/softer-than-expected, and potentially point to some greater-than-expected caution among consumers during the early stages of the Middle East conflict. EUR/GBP and Cable both unchanged, the former on a 0.8670 handle.

FIXED INCOME

- A modestly bearish session for fixed benchmarks, initial action a function of the modest and since increasing energy upside as we count down to and participants position into a potentially risk-packed weekend.

- Amidst this, USTs post downside of a handful of ticks in a thin 110-30 to 111-03 band. Ahead, the US docket is light, and we look to next week’s FOMC.

- Bunds post slightly larger downside, perhaps as Dutch TTF has been leading oil benchmarks throughout the morning. Currently, in the red by c. 30 ticks but also in a relatively narrow 125.20-44 band. The European docket is light, aside from Italian supply (should be well received, particularly after the sizeable demand at last week’s syndications); as such, price action will likely be dictated by geopolitical developments.

- Gilts gapped lower at the open, acknowledging the pressure in fixed peers seen late-Thursday. Opened at 87.10, lower by 41 ticks. Thereafter, slipped another 28 to an 86.82 low and has held there since; the second bout of pressure spurred by further energy upside and a hawkish BoE DMP. The DMP spurred end-2026 BoE pricing to 59bps of tightening from c. 54bps this morning and significantly above the 23bps implied this time last week.

- To recap the day’s data. UK Retail Sales were strong on a headline level but in-line/soft on a core basis, with consumer motor fuel purchases driving the headline, no implications for the BoE next week (hold expected, guidance in focus). Thereafter, Germany’s Ifo was soft across the board, with no real follow-through to EGBs.

- Italy sold EUR 2.5bln vs exp. EUR 2.25-2.5bln 2.20% 2028 BTP Short Term: b/c 1.63x (prev. 1.78x) & average yield 2.80% (prev. 2.89%).

- Australia sold AUD 1bln vs exp. AUD 1bln 2.50% 2030 AGB: b/c 3.82x (prev. 3.44x), average yield 4.6947% (prev. 4.2888%).

COMMODITIES