APRIL 27/GOLD CLOSED DOWN $41.10 TO $4679.80 WITH SILSVER DOWN $1.39 TO $75.02//PLATINUM CLOSED DOWN $30.85 TO $1990.75 WHILE PALLADIUM CLOSED DOWN $31.40 TO $1481.50//GOLD COMMENTARY TONIGHT COURTESY OF ALASDAIR MACLEOD// IMPORTANT COMMENTARIES RE CHINA TONIGHT//EUROPEAN COMMENTARIES ON GERMANY AND THE UK//ISRAEL/USA VS IRAN UPDATES/ISRAEL TBN//HEZBOLLAH VS ISRAEL UPDATES/RUSSIA VS UKRAINE UPDATES/MARK CRISPIN MILLER ON VACCINE INJURIES//OIL REPORT FOR TONIGHT//USA ECONOMIC REPORT; A MUST READ ACCOUNT OF THE MIDDLE EAST CONFLICT FROM GEOVEST!!//SWAMP STORIES FOR YOU TONIGHT//

099 H DEUTSCHE BANK AG 7 624 H BOFA SECURITIES 17 685 C RJ OBRIEN 25 690 C ABN AMRO CLR USA LLC 1

TOTAL: 25 25 MONTH TO DATE: 22,281

JPMORGAN STOPPED 1/61

APRIL 27

APRIL COMEX MONTH

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2026: 25 CONTRACTs NOTICES FOR 2500 OZ or 0.077TONNES

total notices so far: 22,281 contracts FOR 2,228,100 OZ OR 69.303 TONNES

FOR APRIL 27

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 7 NOTICE(S) FILED FOR 35,000 OZ /

total number of notices filed so far this month : 3308 CONTRACTS (NOTICES) for 16.540 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $41.10 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/// NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 1046.622 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $1.39 AT THE SLV: NO CHANGES IN SILVER INVENTORY AT THE SLV //// : INVENTORY RESTS AT THE SLV AT 487.234 MILLION OZ//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 487.234 MILLION OZ

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 2182 CONTRACTS TO A NEW RECORD LOW OF 110,384 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR GAIN OF $0.92 IN SILVER PRICING AT THE COMEX WITH RESPECT TO FRIDAY’S // TRADING. ON APRIL 27, TODAY, WE HAVE REACHED AT OUR RECORD LOW OI OF 110,384 SURPASSING OUR PREVIOUS LOW OF 111,576 SET EARLIER IN THE MONTH OF MARCH/(2026).

NOW ON A NET BASIS OUR SPECULATORS HAVE REVERTED BACK TO GOING SHORT. THE FRBNY ON A NET BASIS IS PROVIDING THE NECESSARY PAPER TO OUR LONGS ALONG WITH SOME BULLION BANKS AND THEN A HUGE NUMBERS OF LONGS ,OUR CENTRAL BANKERS, TAKE THE LONG SIDE AND TENDER FOR PHYSICAL AT 4 PM EACH NIGHT. BECAUSE OF THE HUGE SHORTFALL IN PHYSICAL SILVER IN LONDON THERE IS A LOTTERY TO SEE WHO GETS ANY OF THE PHYSICAL SILVER AVAILABLE THAT WHICH THEY ARE OBLIGATED TO DELIVER. THEY WAIT PATIENTLY FOR THEIR PHYSICAL METAL AND IF NOBODY GETS ANY THEY THEN COME BACK THE NEXT DAY AND SO ON. THIS IS IN LONDON, THE HOME OF PHYSICAL SILVER!!

WE ARE FINALLY MOVING TO A MUCH HIGHER BASE IN SILVER PRICING AT MAJOR SUPPORT LEVEL OF $70.00. SHORTLY WE WILL AGAIN ATTEMPT TO BREAK THE MAJOR 100 DOLLAR BARRIER. THE SHORT SPECULATORS WERE AGAIN LED BY OUR HIGH FREQUENCY TRADERS THIS WEEK WHICH WILL EXPLAIN THE EXTREMELY LOW OI AND A MUCH HIGHER SILVER BASE!!

WE HAVE A MEGA HUGE SIZED LOSS OF 1513 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A STRONG SIZED 669 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD SOME LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO FRIDAY TRADING/// MONTHLY SPREADERS FINISHED ON MARCH 31.. WE HAD A HUGE 1017 CONTRACT T.A.S. ISSUANCE!! / THEY DESPERATELY AGAIN TODAY TRYING TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $100.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON FRIDAY WITH SILVER’S RISE IN PRICE

THE PRICE STILL FINISHED ABOVE THE MAGIC NUMBER OF $70.00 SILVER SPOT PRICE BUT STILL BELOW THE $100.00 MARK CLOSING AT $76.41 UP 0.92. WE ARE NOW WITNESSING HAVING MANY HUGE T.A.S ISSUANCES // TODAY’S WAS AT A HUGE SIZED 1017 T.A.S. CONTRACTS !!. THE CROOKS ARE BECOMING MORE DESPERATE TO STOP SILVER BREAKING ABOVE THE 100.00 DOLLAR MARK!! AND NOW THE HUGE SUPPORT LEVEL OF 70 DOLLARS!!.MAMMOTH SIZE T.A.S ISSUANCES ARE BECOMING THE NORM AT THE COMEX NOW!!

THERE IS NO NEXT LINE IN THE SAND ONCE THE 100.00 DOLLAR SILVER IS PIERCED AGAIN. WE HAD A STRONG SIZED 669 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR MEGA HUGE SIZED 720 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING//AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE.

IN ESSENCE WE HUGE LOSS OF 1513 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR GAIN IN PRICE OF $0.92. WE HAD HUGE GOVERNMENT (FRBY) COMEX CONTRACTS TRADING ALL WEEK AND A MAJOR PORTION WILL BE REMOVED BY DAYS END. (I RECORD THIS FOR YOU ON A DAILY BASIS). THE STICKY SPECULATOR LONGS STILL REMAIN STOIC

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE.

THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, THROUGHOUT MONTH. TOTAL TAS ISSUED ON FRIDAY NIGHT//SATURDAY MORNING: A HUGE SIZED 1017 CONTRACTS. DESPITE MANY COMPLAINTS THAT THROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED FRBNY BANKERS).

THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS AS ONE UNIT, BUT SELL THE SHORT SIDE FIRST AND THEN LIQUIDATE THE LONG SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS NOW ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1.1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

THUS:

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A STRONG QUEUE JUMP OF 42 CONTRACTS OR 0.210 MILLION OZ/NEW STANDING REDUCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 5 CONTRACT QUEUE JUMP WHERE 5000 ADDITIONAL OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES HUGELY TO 16.540 MILLION OZ PLUS WE MUST ADD OUR 3RD EXCHANGE FOR RISK ISSUANCE OF 199 CONTRACTS OR 0.995 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER TWO ISSUANCES OF 2.965//NEW TOTAL SILVER STANDING 19.540 MILLION OZ//

SUMMARY OF OUR APRIL 2026 COMEX CONTRACT MONTH:

WE HAD:

/ HUGE COMEX OI LOSS+// STRONG SIZED 669 EFP ISSUANCE CONTRACTS (/ VI) A HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE 1017 CONTRACTS

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 167 SILVER CONTRACT//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL.. ACCUMULATION

TOTAL CONTRACTS for 17 DAY(S), total 7478 contracts: OR 37.390 MILLION OZ (439 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 37.390 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 37.390 MILLION OZ..WILL BE SMALL THIS MONTH.

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1979 CONTRACTS DESPITE OUR GAIN IN PRICE OF $0.92 IN SILVER PRICING AT THE COMEX// FRIDAY,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED CONTRACT EFP ISSUANCE 669 CONTRACTS ISSUED FOR MAY, AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS). WE HAD A 12 SIZED CONTRACT QUEUE JUMP FOR 60,000 OZ//STANDING ADVANCES TO 16.575 MILLION OZ// PLUS 2.965 MILLION OZ EXCHANGE FOR RISK //3ISSUANCES//NEW TOTAL ADVANCES TO 19.54 MILLION OZ

LAST 12 MONTHS OF SILVER DELIVERIES

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 65,000 OZ QUEUE JUMP//NEW STANDING ADVANCES TO 16.540MILLION OZ PLUS 2.965 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 19.540 MILLION OZ

THE NEW TAS ISSUANCE THURSDAY (1017) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED NO DOUBT WITH FUTURE TRADING!

WE HAD 7 NOTICE(S) FILED TODAY FOR 35,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY BANKERS

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 980 OI CONTRACTS UP TO 365,451 ADVANCING FROM ITS ALL TIME LOW OF 354,581 OI AND CLOSER TO THE RECORD HIGH (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE HAVE NOW ADVANCED PAST THE PREVIOUS ALL TIME LOWS OF 357,136 SET APRIL 2/.2026. WE ARE STILL QUITE A WAY FROM OUR TWO DECADES OLD: 390,000 CONTRACTS LOW SET IN THE YEAR OF 2001 WITH TRADING FOR GOLD AT $260.00. THUS DURING EARLY APRIL WE HAD AN ALL TIME LOW OI IN COMEX (354,531) BUT WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE COMEX SHIP, NOBODY WANT TO PLAY IN THIS CROOKED CASINO!!

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 2790 CONTRACTS //.

WE HAD A SMALL GAIN IN COMEX OI (980 ONTRACTS) . THIS STRONG GAIN IN OI OCCURRED WITH GAIN IN PRICE OF $13.95 //FRIDAY///.

LAST 12 MONTHS OF GOLD DELIVERIES: (MAY THROUGH TO /APRIL)

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

2 JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

3.JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 5 CONTRACT QUEUE JUMP FOR 500 OZ/ (0.0155 TONNES)/NEW STANDING ADVANCES TO 69.420 TONNES

E.F.P. ISSUANCE/FOR OPENING APRIL. GOLD CONTRACT

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 798CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT A LOW OF 365,451ADVANCING FROM OUR RECORD LOW OF 354,581 AND WE NOW WITNESSING A LOWER COMEX OI BUT WITH AN EXTREMELY HIGH

SILVER ALSO HAS AN ULTRA SMALL SIZED AND EXTREMELY LOW COMEX OI OF 110,384 ONTRACTS// RISING FROM PREVIOUS ALL TIME LOW SET MARCH 23/2026 OF 111,576 CONTRACTS.

IN ESSENCE WE HAVE A FAIR SIZED GAIN IN TOTAL CONTRACTS IN COMEX GOLD ON THE TWO EXCHANGES OF 1778 CONTRACTS WITH 3770 CONTRACTS INCREASED AT THE COMEX// AND A SMALL SIZED 778 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON.

THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1778 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED AND CRIMINAL 720 CONTRACTS AND THESE ISSUANCES ARE GENERALLY USED TO INITIATE A RAID WHEN CALLED UPON.

GOLD PRICE ON FRIDAY ROSE BY $13.95

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(798 ) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI OF 980 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES 1778 CONTRACTS!!

WE HAVE 1) NOW REVERTED TO OUR NORMAL FORMAT OF BANKER (FRBNY) GOING ON THE SHORT SIDE AND SOME NEWBIE SPECULATORS GOING TO THE LONG SIDE//

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.012 TONNES TO ALL OTHER QUEUE JUMPS//NEW QUEUE JUMP TOTALS INCREASES: 41.233 TONNES// /// TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK FOR 31.251 TONNES//NEW STANDING FINISHED AT 157.878 TONNES

MARCH:: SMALL INITIAL STANDING FOR GOLD FOR MARCH AT 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 46 CONTRACT QUEUE JUMP OF 4400 OZ OR 0.2320 TONNESAND THEN WE ADD BY OUR THREE EXCHANGE FOR RISK: 22.3818///NEW STANDING ADVANCES TO 67.6648 TONNES OF GOLD./

APRIL: INITIAL STANDING FOR GOLD; 52.600 TONNES FOLLOWED BY TODAY’S 8600OZ QUEUE JUMP(0.2674 TONNES) //NEW STANDING ADVANCES TO 69.4059TONNES.

STANDING FOR THE LAST 4 MONTHS JANUARY TO APRIL:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 500 OZ QUEUE JUMP (0.0155TONNES): NEW STANDING ADVANCES TO 69.420 TONNES

3) SOME T.A.S. LIQUIDATION, AND SOME GOVT LIQUIDATION // WITH A STRONG GAIN OF EQUITY SHARES/APRIL 24 HAVING 1)A $13.95 COMEX PRICE GAIN AND YET WE HAD 2) SPEC LONGS PILING HUGELY ON A NET BASIS, + EASTERN CENTRAL BANKERS ALSO PILING INTO THE LONG SIDE. WE HAD A FAIR SIZED GAIN OF 1778 CONTRACTS ON OUR TWO EXCHANGES AND AS WELL A STRONG AMOUNT OF GOLD WILL STAND FOR DELIVERY IN APRIL. (69.420 TONNES). //, CENTRAL BANKERS TENDERED FOR PHYSICAL WITH THEIR PURCHASES OF CONTRACTS../ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED FRIDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL

4)A STRONG SIZED COMEX OI GAIN 5) V) SMALL SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD (778) AND A SMALL T.A.S. ISSUANCE (552) FOR RAID PURPOSES

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 23,734 CONTRACTS OR 2,373,400 OZ OR 73.823TONNES IN 17TRADING DAY(S) AND THUS AVERAGING: 1396 EFP CONTRACTS PER TRADING ,DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN17TRADING DAY(S) IN TONNES: 73.823 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2025, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 73.823 TONNES DIVIDED BY 3550 x 100% TONNES = 2.070% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2023 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2024: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES

2025: AND NOW 2026

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 71.34 TONNES// WILL BE VERY SMALL THIS MONTH

SPREADERS:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONG

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE 2182 CONTRACTS TO AN OI OF 110,587, A NEW ALL TIME LOW WITH AN EXCEPTIONALLY HIGH PRICE FOR SILVER

EFP ISSUANCE 669 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 669 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2182 CONTRACTS AND ADD TO THE 669 E.FP. ISSUED

WE OBTAIN A MEGA STRONG SIZED LOSS OF 1513 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $0.92

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 7.565 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $0.92

2.ASIAN AFFAIRS APRIL 27 /2025

SHANGHAI CLOSED UP 6.44 PTS OR 0.16%

HANG SENG CLOSED DOWN 18.57 PTS OR 0.07%

Nikkei CLOSED UP 579.80 PTS OR 0.97%

//Australia’s all ordinaries CLOSED DOWN 0.17%

//Chinese yuan (ONSHORE) CLOSED DOWN 6.8238

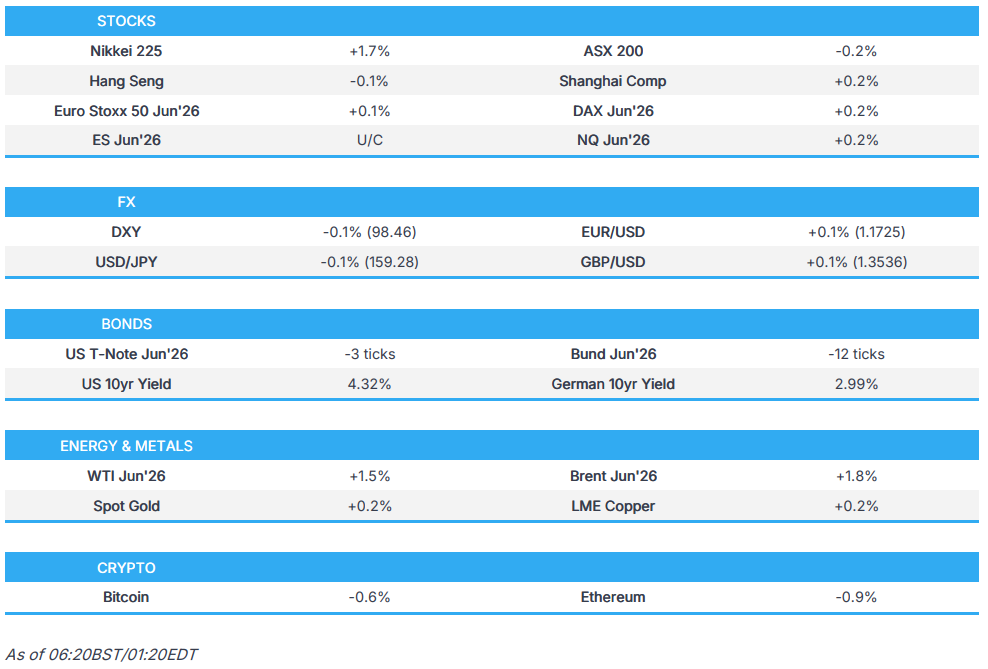

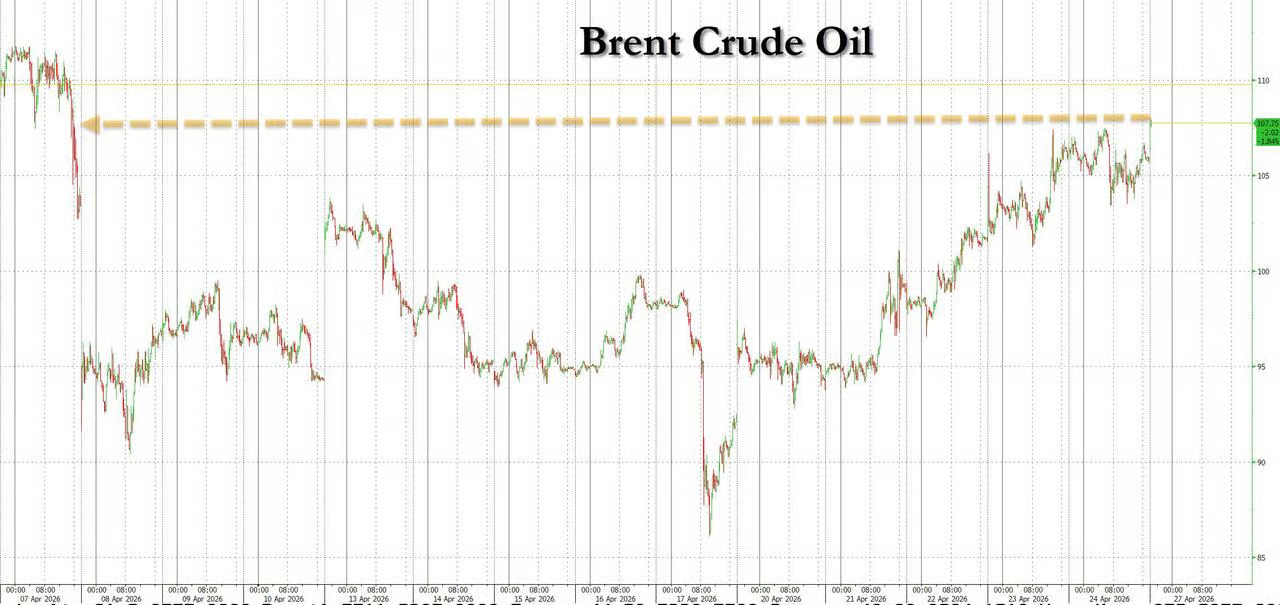

/ OFFSHORE CLOSED DOWN AT 6.8240 Oil UP TO 96,74 dollars per barrel for WTI and BRENT UP TO 108.11 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING 6.8238 (DOWN) OFFSHORE YUAN TRADING DOWN TO 6.8240 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL 980 CONTRACTS UP TO AN OI OF 365,451 CONTRACTS (OI) , HAVING ADVANCED FROM OUR NEW LOW OI SET THIS MONTH AND SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 354,581 SET APRIL6/2026. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 354,581 WITH GOLD AT AN EXTREMELY HIGH $4,700.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD ZERO T.A.S. LIQUIDATION DURING THURSDAY’S TRADING. IT SEEMS THAT THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE WITH THE BANKERS TAKING THE SHORT SIDE, SUPPLYING THE NECESSARY PAPER, AS WELL AS COVERING THEIR SHORTFALL. THERE ARE ALSO SOME SPECULATORS WHO CONTINUALLY GO TO THE SHORT SIDE AND THEY WILL BE ANNHILATED ON CENTRAL BANK COMMAND!!

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE MASSIVE AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS APRIL CONTRACT MONTH!!

THE SMALL SIZED GAIN ON OUR TWO EXCHANGES OCCURRED WITH OUR GAIN IN PRICE IN GOLD.

WE THUS HAD A FAIR GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 1778 CONTRACTS (OR 5.53 TONNES) WITH OUR GAIN IN PRICE, AS WE WERE INFORMED OF A SMALL 798 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE..

THEN WE WERE NOTIFIED TODAY OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0.0 TONNES OF GOLD.

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 0 EXCHANGE FOR RISK FOR FAR.

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO APRIL:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 0 EXCHANGE FOR RISK SO FAR.

DETAILS ON OUR NEW APRIL COMEX CONTRACT MONTH//

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 1778 CONTRACTS WITH OUR GAIN IN PRICE ($13.95). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH APRIL/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A SMALL SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 720 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING THIS WEEK WITH MUCH FAILURE DURING LONDON LBMA/OTC OPTION EXPIRY WEEK!! (APRIL FIRST DAY NOTICE)

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD.

FOR MARCH WE HAVE 3 EXCHANGE FOR RISK ISSUANCES SO FAR FOR 7196 CONTRACTS OR 719,600 OZ/22.3818 TONNES.. AS DELIVERIES OF GOLD THESE PAST SEVERAL MONTHS HAVE BEEN HUGE!!

APRIL: 0 SO FAR HAVE BEEN ISSUED

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

AND NOW APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ (0.2574 TONNES) QUEUE JUMP. THUS STANDING FOR GOLD AT THE COMEX ADVANCES TO 69.420TONNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING APRIL,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $13.95)

WE HAD ZERO T.A.S. SPREADER LIQUIDATION // COMEX SESSION// WITH OUR GAIN IN PRICE , OUR LONG SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI //

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

FRIDAY NIGHT//SATURDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL FRIDAY EVENING/SATURDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 7 MONTHS:

STANDING FOR GOLD OCT THROUGH TO APRIL:

ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

4. JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR LATEST QUEUE JUMP OF 0.0298 TONNES TO WHICH THIS IS ADDED TO ALL OTHER QUEUE JUMPS OF 41.2082 / NEW QUEUE JUMP ADVANCES TO: 41.233 TONNES//STANDING ADVANCES TO: 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES/NEW STANDING ADVANCES TO 157.879 TONNES

MARCH: INITIAL STANDING: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TO WHICH WE THEN ADD OUR THREE EXCHANGE FOR RISK FOR 22.3818 TONNES// GOLD STANDING ADVANCES TO: 67.6648 TONNES/

APRIL: INITIAL STANDING: A VERY STRONG 52.600 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP (2.4105TONNES). THUS STANDING FOR GOLD AT THE COMEX ADVANCES TO 69.420 TONNES

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $13.95

WE HAD 2790 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES : 1778 CONTRACTS OR 177,800 OZ OR 5.53 TONNES

Total monthly oz gold served (contracts) so far this month

22,281 notices 2,228,100 oz 69.308 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 1

0 ENTRY

DEPOSITS/CUSTOMER

0 ENTRY

xxxxxxxxxxxxxxxxxx

comex withdrawals:

ENTRIES; 1

ENTRIES; 1

i) JPMORGAN: 24,596.214 OZ

0.788 tonnes

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs

adjustments: / / 1

CUSTOMER TO DEALER ACCOUNT BRINKS:

2799.000 OZ

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF APRIL OI STANDS AT 63 CONTRACTS HAVING A LOSS OF 56 CONTRACTS.

WE HAD 61 CONTRACTS SERVED UPON FRIDAY SO WE GAINED A 5 CONTRACT QUEUE JUMP CONTRACTS. THUS 500OZ OF ADDITIONAL GOLD WILL STAND ON THIS SIDE OF THE BORDER AND THIS EQUATES TO 0.0155TONNES.(QUEUE JUMP)

MAY LOST 107 CONTRACTS TO AN OI OF 3417 AS MAY BECOMES THE FRONT MONTH.

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI FELL BY 1118 CONTRACTS UP TO AN OI OF 262,524

We had 25 contracts filed for today representing 2500oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for APRIL. /2026. contract month, we take the total number of notices filed so far for the month (22,281) to which we add the difference between the open interest for the front month of APRIL ( XXXX CONTRACTS) minus the number of notices served upon today 25 x 100 oz per contract) equals 2,231,900 OZ OR (69.420 Tonnes of gold)

THUS: INITIAL total number of gold ounces standing for APRIL. /2026. contract month, we take the total number of notices filed so far for the month (22,281) to which we add the difference between the open interest for the front month of APRIL (XXX CONTRACTS) minus the number of notices served upon today 25 x 100 oz per contract) equals 2,231,900 OZ OR (69.420Tonnes of gold)

new total of gold standing in APRIL is 69.420 TONNES//

TOTAL COMEX GOLD STANDING FOR APRIL 69.420 TONNES TONNES WHICH IS NOW HUGE FOR THIS NORMALLY VERY ACTIVE ACTIVE DELIVERY MONTH OF APRIL.

confirmed volume MONDAY confirmed 117,139 AWFUL ESPECIALLY FOR A MONDAY

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,937,269.176 oz 60.12 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,937,269.176 tonnes oz 60.12 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 29,216,588.938 oz

TOTAL REGISTERED GOLD 15,668,491.872 OZ 487.35 onnes

TOTAL OF ALL ELIGIBLE GOLD 13,548,097.066 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,731,222 oz ((REG GOLD- PLEDGED GOLD)=

427.09 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

APRIL DELIVERY MONTH

APRIL27

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

0 entries

Deposits to the Dealer Inventory

0 entries

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Deposits to the Customer Inventory

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

(1) entries

i) Into HSBC 29,280.310. oz

total deposit 29,280.310 oz

No of oz served today (contracts)

7 CONTRACT(S) (35,000 OZ

No of oz to be served (notices)

2Contracts (0.010 MILLION oz)

Total monthly oz silver served (contracts)

3308contracts 16.540 MILLION oz

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

DEPOSITS INTO DEALER ACCOUNTS

0 entries

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1) entries

i) Into HSBC 29,280.310. oz

total deposit 29,280.310 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

0 entries

the comex is being drained of silver

the comex is being drained of silver

adjustments:1 dealer to customer acct

a) Stonex: 777,165,770 oz

total oz leaving the dealer to customer accts 777,165.770 oz

Friday volume: 73,898 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 76.340 MILLION OZ//.TOTAL REG + ELIGIBLE. 315.181 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL /2026 OI: 14 OPEN INTEREST CONTRACTS FOR A LOSS OF 1 CONTRACT. WE HAD 13 CONTRACTS SERVED ON FRIDAY, SO WE GAINED A SMALL 12 CONTRACTS OR 60,000 OZ UNDERWENT ANOTHER QUEUE JUMP. STANDING THUS ADVANCES TO 16.575 MILLION OZ WHICH IS HUGE FOR THIS NORMALLY SMALL NON ACTIVE DELIVERY MONTH OF APRIL. BUT WE MUST ADD OUR THIRD EXCHANGE FOR RISK TOTALING 199 CONTRACTS OR .995 MILLION OZ. THIS IS ADDED TO OUR OTHER TWO EXCHANGE FOR RISK ISSUED//TOTAL FOR THE 3 EX FOR RISK: 2.965 TONNES. NEW TOTAL SILVER STANDING AT THE COMEX ADVANCES TO 19.540 MILLION OZ.

MAY SAW A LOSS OF 3868 CONTRACTS DOWNTO 26,778 CONTRACTS. MAY BECOMES THE NEW FRONT MONTH. WE HAVE 4 MORE READING DAYS BEFORE FIRST DAY NOTICE

JUNE SAW A GAIN OF 31 CONTRACTS UP TO 1255 OI CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 7 or 35,000 oz

CONFIRMED volume FRIDAY; 73,898 strong

AND NOW APRIL. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 3308 X5,000 oz = 16.540 MILLION oz

to which we add the difference between the open interest for the front month of APRIL (XX) AND the number of notices served upon today (7 )x (5000 oz)

Thus the standings for silver for the APRIL 2026 contract month: (3308 )Notices served so far) x 5000 oz + OI for the front month of APRIL (XX) minus number of notices served upon today (7)x 5000 oz equals silver standing for the APRIL..contract month equating to 16.575 MILLION OZ.+ 2.965 MILLIONEXCHANGE FOR RISK/3 OCCASIONS// WHICH MUST BE ADDED TO NORMAL DELIVERIES..NEW TOTALS 19.540 MILLION OZ

NEW STANDING: 19.540 MILLION OZ WHICH IS HUGE FOR A GENERALLY LOUSY DELIVERY MONTH OF APRIL.

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 76.370 million oz of registered silver

JPMorgan as a percentage of total silver: 142.322/315.181 million: 44.93

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

APRIL 27/2026/WITH GOLD DOWN $41.10 TODAY/NO CHANGES IN GOLD AT THE GLD: // //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 24/2026/WITH GOLD UP $13.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 23/2026/WITH GOLD DOWN 28.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.000 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1050.91 TONNES

APRIL 22/2026/WITH GOLD UP 26.40 TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 21/2026/WITH GOLD DOWN 11.90TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 17/2026/WITH GOLD UP $71.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 1.15 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 16/2026/WITH GOLD DOWN $15.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.285 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1051.783 TONNES

APRIL 15/2026/WITH GOLD DOWN $24.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.289 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1049.478 TONNES

APRIL 14/2026/WITH GOLD UP $83.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.714 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1047.192 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 10/2026/WITH GOLD DOWN $11.90 TODAY/SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.724 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.42 TONNES

APRIL 9/2026/WITH GOLD UP $42.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.429 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.990 TONNES

APRIL 8/2026/WITH GOLD UP $88.95 TODAY/NO CHANGES IN GOLD AT THE GLD A//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 7/2026/WITH GOLD UP $5.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.429 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 6/2026/WITH GOLD UP $5.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/INVENTORY RESTS AT 1050.99 TONNES

APRIL 2/2026/WITH GOLD DOWN $132.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.714 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1050.99 TONNES

APRIL 1/2026/WITH GOLD UP $134.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 1.143 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1047.276 TONNES

MAR 31/2026/WITH GOLD UP $119.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.429 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1046.133 TONNES

MAR 30/2026/WITH GOLD UP $33.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.143 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1049.562

MAR 27/2026/WITH GOLD UP $103.55 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.285 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.705

MAR 26/2026/WITH GOLD DOWN $213.05 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.580 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.42

MAR 25/2026/WITH GOLD UP $155.30 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.300 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1053.000

MAR 24/2026/WITH GOLD DOWN $7.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.286 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1052.705

MAR 23/2026/WITH GOLD DOWN $165.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 5.149 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1056.991

MAR 20/2026/WITH GOLD DOWN $39,55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.855 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1062.135

MAR 19/2026/WITH GOLD DOWN $XXX TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 2.57 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1066.99

MAR 18/2026/WITH GOLD DOWN $111.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.144 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1069.564 TONNES

MAR 17/2026/WITH GOLD UP $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 0.857 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.708 TONNES

MAR 16/2026/WITH GOLD DOWN $60.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4/327 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1071/.565 TONNES

MAR 13/2026/WITH GOLD DOWN $61.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.428 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1075.852 TONNES

MAR 12/2026/WITH GOLD DOWN $49.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 3.715 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1077.28 TONNES

MAR 11/2026/WITH GOLD DOWN $70.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 2.858 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1073.565 TONNES

MAR 10/2026/WITH GOLD UP $137.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 2.614 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.707 TONNES

GLD INVENTORY: 1046.62 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

APRIL 27 WITH SILVER DOWN $1.39: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 24 WITH SILVER UP 0.92: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.54 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 487,23MILLION OZ

APRIL 23WITH SILVER DOWN $2.35: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.489 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 488,773MILLION OZ

APRIL 22 WITH SILVER UP 1.43: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262MILLION OZ

aPRIL 21 WITH SILVER DOWN 3.71: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262 MILLION OZ

APRIL 17 WITH SILVER UP $3.09: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.453 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.900 MILLION OZ

APRIL 16 WITH SILVER DOWN $1.00: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.132 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.477 MILLION OZ

APRIL 15 WITH SILVER UP $0.01: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.588 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.579 MILLION OZ

APRIL 14 WITH SILVER UP $3.99: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.633 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.991 MILLION OZ

APRIL 13 WITH SILVER DOWN 0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.589 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.624 MILLION OZ

APRIL 10 WITH SILVER DOWN 0.16: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.724 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 492.213 MILLION OZ

APRIL 9 WITH SILVER UP $0.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.173 MILLION OZ INTO THE SLV// // :INVENTORY RESTS AT 492.937 MILLION OZ

APRIL 8 WITH SILVER UP $3.50: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 7 WITH SILVER DOWN $0.89: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 6 WITH SILVER UP $0.41: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL WITHDRAWAL OF 0.224 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 2 WITH SILVER DOWN $3.57: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.091 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.988 MILLION OZ

APRIL 1 WITH SILVER UP $1.38: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND WITHDRAWAL OF 0.453 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 491.079 MILLION OZ

MAR 31 WITH SILVER UP $4.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND FRAUDULENT WITHDRAWAL OF 3.893 MILLION OZ FROM THE SLV // :INVENTORY RESTS AT 491.532 MILLION OZ

MAR 30 WITH SILVER UP $0.74: NO CHANGES IN SILVER INVENTORY AT THE SLV: // :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 27 WITH SILVER UP $1.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV// :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 26 WITH SILVER DOWN $4.75: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 25 WITH SILVER UP $3.25: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 24 WITH SILVER DOWN $0.15: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT DEPOSIT OF 10.505 MILLION OZ INTO THE SLV :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 23 WITH SILVER UP $0.06: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// NO CHANGE IN INVENTORY/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 20 WITH SILVER DOWN $1.92: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.490 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 19 WITH SILVER DOWN $6.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.9444 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 490.761 MILLION OZ

MAR 18 WITH SILVER DOWN $2.36: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 1.087 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 494.792 MILLION OZ.

MAR 17 WITH SILVER DOWN $0.89: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 493.705 MILLION OZ.

MAR 16 WITH SILVER DOWN $0.57: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.536 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 497.056 MILLION OZ.

MAR 13 WITH SILVER DOWN $3.83: NO CHANGES IN SILVER INVENTORY AT THE SLV// . ./ :INVENTORY RESTS AT 499.592

MAR 12 WITH SILVER DOWN $0.51 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 3.713 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 499.592 MILLION OZ

MAR 11 WITH SILVER DOWN $3.96 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 1.812 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 503.305 MILLION OZ

MAR 10 WITH SILVER UP $5. HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.63 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 505.117 MILLION OZ

MAR 9 WITH SILVER DOWN $0.30 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.54 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 506.747 MILLION OZ

The silver shortage is a clash between industrial and investment demands. Markets have relied on China’s exports, now likely being withdrawn, leading to significantly higher prices.

We are beginning to see the initial consequences of a clash between industrial use and investor demand for silver. Global mine supply has declined moderately over the last decade, partially made up by an increase in scrap supply. This has led to supply deficits over the last five years, and allowing for net investment in exchange-traded funds we are heading for the eighth consecutive year of deficits.

These estimates are compiled by Metal Focus for the Silver Institute. But we are left wondering whether they actually capture the full demand picture, particularly the use of silver in photovoltaics. Presumably, use of silver has become more efficient over the last decade, but does an increase of only 21% for total industrial use since 2017, and a decline of 2.7% since 2023, really tell the whole story?

India has stepped up her demand to an estimated 7,000 tonnes last year as well, compared with about 4,000 tonnes in 2024. Both China and India are now seeing investment demand increasing, not just because Asians generally have a greater acceptance of silver as sound money, but because they see it as a cheap alternative to gold.

Increasingly, the picture is one of strong industrial demand coupled with growing coin and bar demand against a background of stagnant supply. To try and assess the seriousness of this dual demand squeeze, we need to look at it from China’s viewpoint because it has been her policy suppressing the silver price until recently.

As the second largest producer of silver, China has been drawing down on stocks to satisfy Western industrial demand. That is coming to an end and the market is now tightening.

In the table above, the bottom line is that over the last decade, China’s stock of silver has stopped growing and post-covid it is in increasing deficit.

For decades, China has been suppressing the price by supplying silver from its own mines and more recently drawing down above-ground reserves. Until 2020, there was no net drawdown but in 2025 that accelerated significantly. Presumably, it led to China abandoning her price suppression policy, particularly in the second half of 2025 when the price began to rise sharply. The loss of control over global silver markets can be seen in the next table by comparing her net supply into global markets with the supply deficit:

Global demand was escalating to the point where last year the supply deficit was over 9,900 tonnes according to the Silver Institute’s estimates. But insufficient supply into the west from China was a growing problem from 2022 onwards. Quite simply, China’s policy had to change.

China’s imports of silver for the first three months of the current year are a staggering 1,626 tonnes. That’s an annualised rate of 6,500 tonnes. We don’t know what her exports are, but an AI search reveals analysts pencilling in about 1,000 tonnes over the same period, a decline in the pace of last year consistent with the new export licencing regime which applies from 1st January. For now, this is only a guess.

Silver’s price prospects

China’s silver policy is now at a crossroads. Last year, the US finally recognised silver as a critical metal, which means there is now a new strategic buyer in the market. If China continues to support her industrial users by making strategic stocks available, she could end up supplying the Americans. Additionally, the rising price of gold, which reflects an accelerating decline in the purchasing power of the dollar and other G7 currencies, will further stimulate demand from investors throughout Asia.

In short, silver availability will continue to be tight. While Metal Focus forecasts a small deficit for 2026 at 76.3 million ounces (2,543 tonnes), UBS forecasts a more credible 296 million ounces (9,210 tonnes). With the hard stop on global supply and China reducing her exports of bar and powder, the squeeze that drove lease rates to 40% in London last October is unlikely to be the last.

The trigger for the next price rise is bound to be gold. Analysts are only beginning to appreciate the financial destruction to currency purchasing powers from the Iran conflict. It is a fair bet that the consequences for the global economy will bring forward their ultimate destruction, increasing monetary demand for silver from nearly 3 billion Chinese and Indian citizens at a considerably quicker rate than the likely decline in industrial demand.

3.CHRIS POWELL AND HIS GATA DISPATCHES:

ANDREW MAGUIRE LIVE FROM THE VAULT 269

AEM TAKING OVER FINNISH ASSETS

THIS IS A SENSATIONAL DEAL FOR AEM!!

AEM JUST MADE A BID FOR FINNISH ASSETS. IS THIS A GOOD DEAL?

Yes, Agnico Eagle Mines (AEM) announced a major consolidation of Finnish gold assets on April 20, 2026, through three linked transactions totaling roughly $3.7–3.8 billion (with potential additional contingent payments). This builds on its existing Kittila mine (Europe’s largest primary gold mine) in the Central Lapland Greenstone Belt.

reuters.com

Deal Breakdown

Rupert Resources (primarily the advanced Ikkari gold project): ~C$2.9 billion (US$2.1 billion) mainly in AEM shares + up to ~C$700 million in contingent value rights (CVRs) tied to future milestones like reserve growth and production. AEM already owned ~13.9% of Rupert. prnewswire.com

Aurion Resources: C$481 million all-cash. AEM already held ~9.9%. Aurion brings a large contiguous land package (761 km²). northernminer.com

B2Gold’s 70% stake in Fingold JV: US$325 million cash (giving AEM 100% of the JV once combined with Aurion’s portion). theglobeandmail.com

Total land position: ~2,492 km² (from ~355 km² today), creating a contiguous district around Kittila and Ikkari (Ikkari is ~50 km from Kittila). Expected closing: Q3 2026, subject to approvals.

reuters.com

Why AEM Sees It as Strategic

Production upside: Aims for a multi-asset hub producing ~500,000 oz gold annually within the next decade (more than doubling current Finnish output). Ikkari has a solid resource base (e.g., 3.5 Moz probable reserves at 2.1 g/t). mining.com

Synergies: Up to $500 million in operational, development, and construction savings by removing property boundaries, sharing infrastructure (Kittila has 20+ years of operating experience in Finland), and accelerating exploration/development. bullpen.finance

Exploration potential: Large, under-explored land package with upside at Ikkari, Pahtavaara (past-producing), and early-stage targets. Also prospective for critical minerals.

Jurisdiction: Finland is a top-tier, stable mining country with strong infrastructure.

This mirrors AEM’s successful district-scale approach in Canada (e.g., Abitibi). CEO Ammar Al-Joundi called it a “multi-decade regional platform” in a “world-class gold belt.”

agnicoeagle.com

Is This a Good Deal?For AEM shareholders — It looks solid to positive on paper for a long-term holder:

Pros: High-quality assets in a familiar jurisdiction, meaningful production growth, significant synergies, and exploration leverage. AEM has a strong balance sheet, low costs, and a track record of integrating assets efficiently. Paying partly in stock (for Rupert) preserves cash and aligns with targets’ shareholders.

Cons/Risks: Large outlay (~$3.8B); integration/permitting/execution risks in a cold, remote area; gold price sensitivity (though AEM is a low-cost producer); dilution from share issuance; and CVR payouts if milestones hit. Markets reacted with some AEM share weakness initially amid broader gold miner sell-off and “digest the deal” sentiment. quiverquant.com

Valuation context: At current gold prices and with synergies/exploration upside, analysts and coverage view it as a logical consolidation play rather than overpaying for “blue sky.” It’s not a cheap bolt-on but builds scale where AEM already has expertise.

Overall market reaction: Targets (Rupert, Aurion) jumped on premiums. AEM shares dipped modestly as investors weighed the size and timeline (production ramp over years, not immediate). No major red flags in reporting—it’s seen as a strategic “hub-building” move amid industry consolidation trends.

cruxinvestor.comBottom line: For a high-quality, patient gold major like AEM with Finland experience, this appears to be a good strategic deal that strengthens its portfolio for the long haul. It’s less about short-term accretion and more about creating a durable, multi-decade production and exploration engine. Whether it’s “great” depends on gold prices, execution, and final costs—standard mining risks apply.If you’re an investor in AEM (or considering it), this adds growth without changing the company’s conservative, high-margin style. Always do your own due diligence or check full filings/investor presentations for resource details, costs, and timelines. Gold sector deals like this often look better in hindsight if the district delivers.

END

5. COMMODITY REPORT//..HELIUM

.Micro-Cap Oil Stock Soars On Helium Offtake Deal As Gulf Shock Spurs Hunt For Reliable Supplies

Monday, Apr 27, 2026 – 01:45 PM

The Hormuz chokepoint, with the U.S.-Iran conflict about to enter its third month, remains closed, and global energy flows are being rewired. One industrial gas we’ve identified as facing supply disruption risks is helium, which threatens to upend end markets ranging from semiconductor production to medical imaging.

Earlier this month, we published a note titled “Wyoming’s Helium Empire Ascends As Qatar Gas Goes Flat.” The note focused on how ExxonMobil stands out as a major beneficiary of the helium disruption in the Gulf region.

We previously cited UBS analyst Manav Gupta, who noted:

XOM’s LaBarge facility in Wyoming, provides 20% of the world’s supply, which has not been impacted by recent events in the Middle East. With an estimated eight decades worth of helium left to produce there, LaBarge is poised to play a significant role through the end of this century.

That leaves the market searching for alternative helium suppliers that could become net beneficiaries of the Gulf-related supply shock.

One potential beneficiary is U.S. Energy Corp., which announced Monday that it has signed a five-year helium offtake agreement with an unnamed investment-grade global industrial gas company, giving the company its first contracted revenue stream tied to its Big Sky Carbon Hub in Montana.

The deal covers 100% of Phase 1 helium production, up to 1.2 million cubic feet per month, or 14.4 million cubic feet annually, under a take-or-pay structure. Phase 1 commercial operations remain targeted for early next year.

“The execution of this agreement with an investment-grade industrial gas company with global distribution infrastructure represents a defining milestone for U.S. Energy and validates years of development work at Big Sky,” USEG CEO Ryan Smith wrote in a press release.

Smith noted, “This contract establishes long-term, contracted helium revenues and meaningfully de-risks Phase 1 commercial operations at Big Sky. It also reflects the strength we’re seeing in the helium market today, where constrained global supply and increasing demand for reliable volumes are supporting a step up in long-term pricing.”

He said under the agreement, helium pricing is fixed at $285 per MCF on a plant-gate basis, with no deductions, meaning the buyer assumes transportation, processing, and downstream costs.

Smith added that this agreement reduces risk for Big Sky’s Phase 1 development by locking in long-term cash flow with a creditworthy counterparty.

USEG shares surged 35% by late morning in the US cash session.

USEG appears to be positioning itself as a major domestic helium supplier – not quite as big as XOM’s LaBarge – but large enough to be noticed by the market, at a time when Gulf-related disruptions are exposing fragile energy supply chains worldwide.

END

ASIAN AFFAIRS APRIL 27/2026

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS MONDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 6.44 PTS OR 0.16%

HANG SENG CLOSED DOWN 18.57 PTS OR 0.07%

Nikkei CLOSED UP 579.80 PTS OR 0.97%

//Australia’s all ordinaries CLOSED DOWN 0.17%

//Chinese yuan (ONSHORE) CLOSED DOWN 6.8238

/ OFFSHORE CLOSED DOWN AT 6.8240 Oil UP TO 96,74 dollars per barrel for WTI and BRENT UP TO 108.11 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING 6.8238 (DOWN) OFFSHORE YUAN TRADING DOWN TO 6.8240 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS MONDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.8238

OFFSHORE YUAN: DOWN TO 6.8240

1.HANG SANG CLOSED DOWN 18.57 PTS OR 0.07%

2. Nikkei closed UP 579.80 PTS OR 0.97%

WEST TEXAS INTERMEDIATE OIL UP TO 96.74

BRENT; 108.11

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 98.14/// EURO RISES TO 1.1745 UP 33 BASIS PTS

3b Japan 10 YR bond yield:RISES TO. +2.474 UP 4 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 159.17… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.681 UP 2 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: 6.8238( DOWN AND OFFSHORE: DOWN AT 6.8240

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD UP TO +3.0146 Italian 10 Yr bond yield UP to 3.821// SPAIN 10 YR BOND YIELD UP TO 3.472%

3i Greek 10 year bond yield UP TO 3.773%

3j Gold at $4709.60 //Silver at: 75.53 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 34 100 roubles/74.91

3m oil (WTI) into the 96 dollar handle for WTI and 107 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 159.17 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.474% UP 4 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.681 UP 2 PTS..: USA/SF this 0.7835 as the Swiss Franc . Euro vs SF: 0.9205

USA 10 YR BOND YIELD: 4.319 UP 1 BASIS PTS…