THIS IS OPTIONS EXPIRY WEEK: TODAY ENDS COMEX EXPIRY AND FRIDAY OTC/LONDON OPTIONS

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: APRIL 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,675.400000000 USD

INTENT DATE: 04/27/2026 DELIVERY DATE: 04/29/2026

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DEUTSCHE BANK AG 10

363 H WELLS FARGO SECURITI 6

523 C INTERACTIVE BROKERS 3

661 C JP MORGAN SECURITIES 24 11

686 C STONEX FINANCIAL INC 1

690 C ABN AMRO CLR USA LLC 1

TOTAL: 28 28

MON

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2026: 28 CONTRACTs NOTICES FOR 2800 OZ or 0.077TONNES

total notices so far: 22,309 contracts FOR 2,230,900 OZ OR 69.390 TONNES

SILVER NOTICES: 1 NOTICE(S) FILED FOR 5,000 OZ /

total number of notices filed so far this month : 3309 CONTRACTS (NOTICES) for 16.545 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A STRONG QUEUE JUMP OF 42 CONTRACTS OR 0.210 MILLION OZ/NEW STANDING REDUCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 3 CONTRACT EXCHANGE FOR PHYSICAL TRANSFER TO LONDON WHERE 15,000 OZ WILL TAKE DELIVERY OVER ON THEIR SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS REDUCES SLIGHTLY TO 16.560 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER THREE ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.725 MILLION OZ//

SUMMARY OF OUR APRIL 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 40.59 MILLION OZ..WILL BE SMALL THIS MONTH.

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 15,000 OZ EXCHANGE FOR PHYSICAL JUMP//NEW STANDING REDUCES TO 16.560MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.725 MILLION OZ

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 278 CONTRACT QUEUE JUMP FOR 27800 OZ/ (0.8646 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 71 CONTRACTS FOR 74,100 OZ OR 2.304 TONNES.

MARCH:: SMALL INITIAL STANDING FOR GOLD FOR MARCH AT 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 46 CONTRACT QUEUE JUMP OF 4400 OZ OR 0.2320 TONNESAND THEN WE ADD BY OUR THREE EXCHANGE FOR RISK: 22.3818///NEW STANDING ADVANCES TO 67.6648 TONNES OF GOLD./

APRIL: INITIAL STANDING FOR GOLD; 52.600 TONNES FOLLOWED BY TODAY’S 27,800 OZ QUEUE JUMP(0.8646 TONNES) //NEW STANDING ADVANCES TO 70.286TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR 741 CONTRACTS/74100 OZ OR 2.304 TONNES//NEW STANDING ADVANCES TO 72.590 TONNES

STANDING FOR THE LAST 4 MONTHS JANUARY TO APRIL:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR FIRST EXCHANGE FOR RISK FOR 74,100 OZ OR 2.304 TONNES/NEW STANDING: 72.590 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 75.701 TONNES// WILL BE VERY SMALL THIS MONTH

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONG

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE 6005 CONTRACTS TO AN OI OF 104,688, A NEW ALL TIME LOW WITH AN EXCEPTIONALLY HIGH PRICE FOR SILVER (APRIL 28)

EFP ISSUANCE 640 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 640 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 6005 CONTRACTS AND ADD TO THE 640 E.FP. ISSUED

WE OBTAIN A MEGA STRONG SIZED LOSS OF 5365 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR LOSS OF $1.39

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 25.280 MILLION PAPER OZ

OCCURRED WITH OUR LOSS IN PRICE.OF $1.39

2.ASIAN AFFAIRS APRIL 28 /2025

SHANGHAI CLOSED DOWN 7.71 PTS OR 0.19%

HANG SENG CLOSED DOWN 229.15 PTS OR 0.88%

Nikkei CLOSED DOWN 637.36 PTS OR 1.05%

//Australia’s all ordinaries CLOSED UP 0.22%

//Chinese yuan (ONSHORE) CLOSED DOWN 6.8340

/ OFFSHORE CLOSED DOWN AT 6.8378 Oil UP TO 98.53 dollars per barrel for WTI and BRENT UP TO 111.00 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING 6.8340 (DOWN) OFFSHORE YUAN TRADING DOWN TO 6.8378 ONSHORE YUAN TRADING ABOVE OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL 871 CONTRACTS UP TO AN OI OF 366,322 CONTRACTS (OI) , HAVING ADVANCED FROM OUR NEW LOW OI SET THIS MONTH AND SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 354,581 SET APRIL6/2026. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 354,581 WITH GOLD AT AN EXTREMELY HIGH $4,700.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD ZERO T.A.S. LIQUIDATION DURING MONDAY’S TRADING. IT SEEMS THAT SOME OF THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE BUT ALSO SOME SPECULATORS GOING TO THE SHORT SIDE WITH THE BANKERS NOW TAKING THE LONG SIDE,AND CENTRAL BANKS SUPPLYING THE NECESSARY PAPER, AS WELL AS COVERING THEIR SHORTFALL. THERE ARE ALSO SOME SPECULATORS WHO CONTINUALLY GO TO THE SHORT SIDE AND AND OF COURSE THEY WILL BE ANNHILATED ON CENTRAL BANK COMMAND!!

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE MASSIVE AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS APRIL CONTRACT MONTH!!

THE FAIR SIZED GAIN ON OUR TWO EXCHANGES OCCURRED DESPITE OUR LOSS IN PRICE IN GOLD. WE ARE NOW IN THE LAST DAYS OF THE MONTH AND THUS OUR TWO SPREADERS ARE IN FULL FORCE DURING OPTIONS EXPIRY MONTH: THE COMEX OPTIONS EXPIRY CONCLUDES TODAY AND LONDON/OTC EXPIRES THIS FRIDAY.

WE THUS HAD A FAIR GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 1475 CONTRACTS (OR 4.587 TONNES) WITH OUR LOSS IN PRICE, AS WE WERE INFORMED OF A SMALL 604 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE..

THEN WE WERE NOTIFIED TODAY OF A 741 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 74,100 OZ OR 2.304 TONNES OF GOLD.

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH APRIL

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 1 EXCHANGE FOR RISK FOR FAR I.E. 741 CONTRACTS FOR 74100 OZ OR 2.314 TONNES

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO APRIL:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 1 EXCHANGE FOR RISK SO FAR FOR 74100 OZ OR 2.304 TONNES.

DETAILS ON OUR NEW APRIL COMEX CONTRACT MONTH//

IN TOTAL WE HAD A GOOD SIZED GAIN ON OUR TWO EXCHANGES OF 4721 CONTRACTS DESPITE OUR LOSS IN PRICE ($41.10). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH APRIL/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A FAIR SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 1127 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT IS NOW IN FULL FORCE DURING THIS WEEK DURING LONDON COMEX AND LBMA/OTC OPTION EXPIRY WEEK!! (INITIAL MAY CONTRACT MONTH)

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD.

FOR MARCH WE HAVE 3 EXCHANGE FOR RISK ISSUANCES SO FAR FOR 7196 CONTRACTS OR 719,600 OZ/22.3818 TONNES.. AS DELIVERIES OF GOLD THESE PAST SEVERAL MONTHS HAVE BEEN HUGE!!

APRIL: 1 SO FAR HAVE BEEN ISSUED FOR 74,100 OZ OR 2.304 TONNES.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

AND NOW APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ (0.2574 TONNES) QUEUE JUMP TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL ISSUANCE OF 74,100 OZ OR 2.304 TONNES//. THUS NEW STANDING FOR GOLD AT THE COMEX ADVANCES TO 72.590TONNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING APRIL,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $41.40)

WE HAD ZERO T.A.S. SPREADER LIQUIDATION // COMEX SESSION// WITH OUR LOSS IN PRICE , OUR LONG SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI //

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

MONDAY NIGHT//TUESDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

NOW A LITTLE REVIEW OF GOLD STANDING THESE PAST 7 MONTHS:

STANDING FOR GOLD OCT THROUGH TIL APRIL

ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31

OCTOBER…

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

4. JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR LATEST QUEUE JUMP OF 0.0298 TONNES TO WHICH THIS IS ADDED TO ALL OTHER QUEUE JUMPS OF 41.2082 / NEW QUEUE JUMP ADVANCES TO: 41.233 TONNES//STANDING ADVANCES TO: 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES/NEW STANDING ADVANCES TO 157.879 TONNES

MARCH: INITIAL STANDING: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TO WHICH WE THEN ADD OUR THREE EXCHANGE FOR RISK FOR 22.3818 TONNES// GOLD STANDING ADVANCES TO: 67.6648 TONNES/

APRIL: INITIAL STANDING: A VERY STRONG 52.600 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP (2.4105TONNES) TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 741 CONTRACTS//74,100 OZ OR 2.304 TONNES. THUS STANDING FOR GOLD AT THE COMEX ADVANCES TO 72.590 TONNES

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $41.10

WE HAD 3246 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES : 1475 CONTRACTS OR 147,500 OZ OR 4.587 TONNES

INITIAL GOLD COMEX

APRIL DELIVERY MONTH

APRIL28 2026

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | ENTRIES; 2 i) Brinks 16,879.275 oz (525 kilobars) ii) HSBC 12,063.755 oz total withdrawal: 28,943.034 oz 0.900 tonnes |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 28 CONTRACTS OR 2800 OZ 0.0871 TONNES OF GOLD |

| No of oz to be served (notices) | 288 Contracts 28800 OZ 0.8958TONNES |

| Total monthly oz gold served (contracts) so far this month | 22,309 notices 2,230,900 oz 69.390 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 1

0 ENTRY

DEPOSITS/CUSTOMER

0 ENTRY

xxxxxxxxxxxxxxxxxx

comex withdrawals:

ENTRIES; 2

i) Brinks 16,879.275 oz (525 kilobars)

ii) HSBC 12,063.755 oz

total withdrawal: 28,943.034 oz

0.900 tonnes

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs

adjustments: / / 1

DEALER TO CUSTOMER ACCOUNT/// BRINKS:

a) Brinks 64,237.698

(1998 kilobars)

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF APRIL OI STANDS AT 316 CONTRACTS HAVING A GAIN OF 253 CONTRACTS.

WE HAD 25 CONTRACTS SERVED UPON MONDAY SO WE GAINED A STRONG 278 CONTRACT QUEUE JUMP CONTRACTS. THUS 27,800OZ OF ADDITIONAL GOLD WILL STAND ON THIS SIDE OF THE BORDER AND THIS EQUATES TO 0.8646TONNES.(QUEUE JUMP)

MAY LOST 339 CONTRACTS TO AN OI OF 2978 AS MAY BECOMES THE FRONT MONTH.

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI LOST BY 1084 CONTRACTS UP TO AN OI OF 261,440

We had 28 contracts filed for today representing 2800oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 24 notices issued from their client or customer account. The total of all issuance by all participants equate to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for APRIL. /2026. contract month, we take the total number of notices filed so far for the month (22,309) to which we add the difference between the open interest for the front month of APRIL ( 316 CONTRACTS) minus the number of notices served upon today 28 x 100 oz per contract) equals 2,259,700 OZ OR (70.286 Tonnes of gold) Then we add our first exchange for risk of 741 contracts/74100 oz or 2.304 tonnes//new standing advances to 72.590 tonnes

THUS: INITIAL total number of gold ounces standing for APRIL. /2026. contract month, we take the total number of notices filed so far for the month (22,309) to which we add the difference between the open interest for the front month of APRIL (316 CONTRACTS) minus the number of notices served upon today 28 x 100 oz per contract) equals 2,259,700 OZ OR (70.286Tonnes of gold) to which we add our first exchange for risk of 741 contracts/74100oz or 2.304 tonnes//

new total of gold standing in APRIL is 72.590 TONNES//

TOTAL COMEX GOLD STANDING FOR APRIL 72.590 TONNES TONNES WHICH IS NOW HUGE FOR THIS NORMALLY VERY ACTIVE ACTIVE DELIVERY MONTH OF APRIL.

confirmed volume MONDAY confirmed 100,118

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,923,030.696 oz 59.81 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,923,030.696 tonnes oz 59.81 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 29,187,645.904 oz

TOTAL REGISTERED GOLD 15,604,254.174 OZ 485.35 onnes

TOTAL OF ALL ELIGIBLE GOLD 13,583,391.730 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,681.224 oz ((REG GOLD- PLEDGED GOLD)=

425.54 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

APRIL DELIVERY MONTH

APRIL28

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 0 entries |

| Deposits to the Dealer Inventory | 0 entries xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT (0) entries oz |

| No of oz served today (contracts) | 1 CONTRACT(S) (5,000 OZ |

| No of oz to be served (notices) | 3Contracts (0.015 MILLION oz) |

| Total monthly oz silver served (contracts) | 3309 contracts 16.545 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 entries

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

0) entries

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

0 entries

the comex is being drained of silver

the comex is being drained of silver

adjustments:2

dealer to customer acct

a) JPMorgan: 639,483.900 oz

dealer to customer:

b) Loomis 14,692.400 oz

total oz leaving the dealer to customer accts 684,791.500 oz

Monday volume: 72,805 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 75.715 MILLION OZ//.TOTAL REG + ELIGIBLE. 315.181 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL /2026 OI: 4 OPEN INTEREST CONTRACTS FOR A LOSS OF 10 CONTRACTS. WE HAD 7 CONTRACTS SERVED ON MONDAY, SO WE LOST A SMALL 3 CONTRACTS OR 15,000 OZ UNDERWENT AN EXCHANGE FOR PHYSICAL TRANSFER JUMP TO LONDON. STANDING THUS REDUCES TO 16.560 MILLION OZ WHICH IS HUGE FOR THIS NORMALLY SMALL NON ACTIVE DELIVERY MONTH OF APRIL. BUT WE MUST ADD OUR 4TH EXCHANGE FOR RISK OF 17 CONTRACTS OR 85,000 OZ. NEW TOTAL EXCHANGE FOR RISK ON 4 OCCASIONS IS 233 CONTRACTS OR 1.165 MILLION OZ. THIS IS ADDED TO OUR OTHER THREE EXCHANGE FOR RISK ISSUED//TOTAL FOR THE 4 EX FOR RISK: 1.165 MILLION OZ. NEW TOTAL SILVER STANDING AT THE COMEX ADVANCES TO 17.725 MILLION OZ.

MAY SAW A LOSS OF 9072 CONTRACTS DOWNTO 17,676 CONTRACTS. MAY BECOMES THE NEW FRONT MONTH. WE HAVE 3 MORE READING DAYS BEFORE FIRST DAY NOTICE

JUNE SAW A GAIN OF 15 CONTRACTS UP TO 1266 OI CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1 or 5,000 oz

CONFIRMED volume MONDAY; 72,805 strong

AND NOW APRIL. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 3309 X5,000 oz = 16.545 MILLION oz

to which we add the difference between the open interest for the front month of APRIL (4) AND the number of notices served upon today (1 )x (5000 oz)

Thus the standings for silver for the APRIL 2026 contract month: (3309 )Notices served so far) x 5000 oz + OI for the front month of APRIL (XX) minus number of notices served upon today (1)x 5000 oz equals silver standing for the APRIL..contract month equating to 16.560 MILLION OZ.+ 1.165 MILLIONEXCHANGE FOR RISK/3 OCCASIONS// WHICH MUST BE ADDED TO NORMAL DELIVERIES..NEW TOTALS 17.775 MILLION OZ

NEW STANDING: 17.640 MILLION OZ WHICH IS HUGE FOR A GENERALLY LOUSY DELIVERY MONTH OF APRIL.

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 75.715 million oz of registered silver

JPMorgan as a percentage of total silver: 142.322/315.181 million: 44.93

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

APRIL 28/2026/WITH GOLD DOWN $85.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 27/2026/WITH GOLD DOWN $41.10 TODAY/NO CHANGES IN GOLD AT THE GLD: // //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 24/2026/WITH GOLD UP $13.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 23/2026/WITH GOLD DOWN 28.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.000 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1050.91 TONNES

APRIL 22/2026/WITH GOLD UP 26.40 TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 21/2026/WITH GOLD DOWN 11.90TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 17/2026/WITH GOLD UP $71.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 1.15 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 16/2026/WITH GOLD DOWN $15.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.285 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1051.783 TONNES

APRIL 15/2026/WITH GOLD DOWN $24.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.289 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1049.478 TONNES

APRIL 14/2026/WITH GOLD UP $83.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.714 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1047.192 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 10/2026/WITH GOLD DOWN $11.90 TODAY/SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.724 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.42 TONNES

APRIL 9/2026/WITH GOLD UP $42.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.429 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.990 TONNES

APRIL 8/2026/WITH GOLD UP $88.95 TODAY/NO CHANGES IN GOLD AT THE GLD A//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 7/2026/WITH GOLD UP $5.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.429 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 6/2026/WITH GOLD UP $5.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/INVENTORY RESTS AT 1050.99 TONNES

APRIL 2/2026/WITH GOLD DOWN $132.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.714 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1050.99 TONNES

APRIL 1/2026/WITH GOLD UP $134.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 1.143 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1047.276 TONNES

MAR 31/2026/WITH GOLD UP $119.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.429 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1046.133 TONNES

MAR 30/2026/WITH GOLD UP $33.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.143 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1049.562

MAR 27/2026/WITH GOLD UP $103.55 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.285 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.705

MAR 26/2026/WITH GOLD DOWN $213.05 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.580 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.42

MAR 25/2026/WITH GOLD UP $155.30 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.300 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1053.000

MAR 24/2026/WITH GOLD DOWN $7.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.286 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1052.705

MAR 23/2026/WITH GOLD DOWN $165.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 5.149 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1056.991

MAR 20/2026/WITH GOLD DOWN $39,55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.855 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1062.135

MAR 19/2026/WITH GOLD DOWN $XXX TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 2.57 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1066.99

MAR 18/2026/WITH GOLD DOWN $111.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.144 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1069.564 TONNES

MAR 17/2026/WITH GOLD UP $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 0.857 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.708 TONNES

MAR 16/2026/WITH GOLD DOWN $60.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4/327 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1071/.565 TONNES

MAR 13/2026/WITH GOLD DOWN $61.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.428 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1075.852 TONNES

MAR 12/2026/WITH GOLD DOWN $49.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 3.715 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1077.28 TONNES

MAR 11/2026/WITH GOLD DOWN $70.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 2.858 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1073.565 TONNES

MAR 10/2026/WITH GOLD UP $137.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 2.614 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.707 TONNES

GLD INVENTORY: 1044.337 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

APRIL 28 WITH SILVER DOWN $2.05: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 27 WITH SILVER DOWN $1.39: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 24 WITH SILVER UP 0.92: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.54 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 487,23MILLION OZ

APRIL 23WITH SILVER DOWN $2.35: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.489 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 488,773MILLION OZ

APRIL 22 WITH SILVER UP 1.43: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262MILLION OZ

aPRIL 21 WITH SILVER DOWN 3.71: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262 MILLION OZ

APRIL 17 WITH SILVER UP $3.09: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.453 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.900 MILLION OZ

APRIL 16 WITH SILVER DOWN $1.00: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.132 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.477 MILLION OZ

APRIL 15 WITH SILVER UP $0.01: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.588 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.579 MILLION OZ

APRIL 14 WITH SILVER UP $3.99: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.633 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.991 MILLION OZ

APRIL 13 WITH SILVER DOWN 0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.589 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.624 MILLION OZ

APRIL 10 WITH SILVER DOWN 0.16: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.724 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 492.213 MILLION OZ

APRIL 9 WITH SILVER UP $0.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.173 MILLION OZ INTO THE SLV// // :INVENTORY RESTS AT 492.937 MILLION OZ

APRIL 8 WITH SILVER UP $3.50: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 7 WITH SILVER DOWN $0.89: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 6 WITH SILVER UP $0.41: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL WITHDRAWAL OF 0.224 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 2 WITH SILVER DOWN $3.57: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.091 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.988 MILLION OZ

APRIL 1 WITH SILVER UP $1.38: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND WITHDRAWAL OF 0.453 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 491.079 MILLION OZ

MAR 31 WITH SILVER UP $4.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND FRAUDULENT WITHDRAWAL OF 3.893 MILLION OZ FROM THE SLV // :INVENTORY RESTS AT 491.532 MILLION OZ

MAR 30 WITH SILVER UP $0.74: NO CHANGES IN SILVER INVENTORY AT THE SLV: // :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 27 WITH SILVER UP $1.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV// :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 26 WITH SILVER DOWN $4.75: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 25 WITH SILVER UP $3.25: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 24 WITH SILVER DOWN $0.15: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT DEPOSIT OF 10.505 MILLION OZ INTO THE SLV :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 23 WITH SILVER UP $0.06: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// NO CHANGE IN INVENTORY/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 20 WITH SILVER DOWN $1.92: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.490 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 19 WITH SILVER DOWN $6.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.9444 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 490.761 MILLION OZ

MAR 18 WITH SILVER DOWN $2.36: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 1.087 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 494.792 MILLION OZ.

MAR 17 WITH SILVER DOWN $0.89: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 493.705 MILLION OZ.

MAR 16 WITH SILVER DOWN $0.57: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.536 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 497.056 MILLION OZ.

MAR 13 WITH SILVER DOWN $3.83: NO CHANGES IN SILVER INVENTORY AT THE SLV// . ./ :INVENTORY RESTS AT 499.592

MAR 12 WITH SILVER DOWN $0.51 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 3.713 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 499.592 MILLION OZ

MAR 11 WITH SILVER DOWN $3.96 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 1.812 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 503.305 MILLION OZ

MAR 10 WITH SILVER UP $5. HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.63 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 505.117 MILLION OZ

MAR 9 WITH SILVER DOWN $0.30 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.54 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 506.747 MILLION OZ

CLOSING INVENTORY 487.234 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

MATHEW PIEPENBURG…

JOHN RUBINO

ALASDAIR MACLEOD.

Impasse at Hormuz

The Strait’s closure cannot be quickly resolved. The damage to the world’s economy is immense, destroying fiat currencies. That’s why gold is the only pure safe haven.

| Alasdair MacleodApr 28∙Paid |

Introduction

Even America’s NATO partners openly admit that the conflict with Iran was ill-advised. And it is clear that the campaign has failed and a face-saving exit is being sought by the US: that’s why threats are followed by deadlines being extended. Don’t forget that this campaign was originally meant to be resolved over a weekend — and here we are in an uneasy truce two months on with the Hormuz Straits closed.

Iran knows it has control over the situation. It also has the conditional backing of China and Russia. This is why it is in no hurry to compromise. Stalemate.

The rest of the world will have to dig in, for Hormuz will be closed for the foreseeable future, which could be months. The best hope is that the US quietly backs down without appearing to, and that Israel doesn’t force Iran to retaliate. The situation remains extremely fragile.

Economic consequences

Not only are supplies of energy and essential commodities being withheld from global markets, but other exporting nations of these commodities are curbing their supplies to protect their own industries. China is a prime example likely to be followed by others. The X tweet below by Lucas Ekwueme shows how the combination of Gulf and Chinese export restrictions is intensifying the consequences of the blockade.

Secondary effects of the energy crises are hitting commodity markets. Sulphuric acid, whose global supplies are being more than halved, is essential for fertiliser production, leaching copper, nickel, and uranium from ore, and chemical manufacturing to mention a few. Soaring energy prices affect energy-intensive production of commodities such as aluminium. JPMorgan recently warned of a two million tonne aluminium deficit driving prices above the 2022 price spike.

Directly and indirectly, every commodity and every economy is affected. There is no doubt that higher commodity prices will lead to a vicious combination of economic slump and higher prices, forcing G7 central banks to expand credit without limit to pay for them. Virtually all G7 nations are in debt traps making the expansion of credit unfundable, other than through very short-term debt instruments.

This is the hyperinflation playbook — a collapsing economy with a collapsing currency. Essentially driven by political priorities, there is no escape. Reflecting their debt traps, the dollar, yen, sterling, and euro will see soaring bond yields, ameliorated only by desperate quantitative easing by central banks focusing on their employment mandates at the expense of their fiat currencies. The UK experienced these conditions in 1975-76, when long gilt yields rose to over 16%, and that was when government debt to GDP was only 40% compared with over 100% today.

The UK was saved by enforced budget discipline by the IMF as condition for a bailout loan and by the timely discovery of North Sea oil. No such salvation is available now. The chart below of the US long bond yield tells us that the combination of a debt trap and commodity-driven price inflation is clearly set to drive yields far higher:

It is close to breaking out on the upside with catastrophic consequences. And already being unprecedently expensive relative to bond yields, equity markets will crash. The chart below shows how exposed the S&P500 Index is to higher bond yields.

This chart captures the normally close negative correlation between the long bond yield and the S&P 500 index. When the bond yield rises, equities should decline and vice-versa. The valuation disparity today is over three times as great than during the dot-com bubble (both arrowed), which was an extreme in investor behaviour. Relative to bonds, equities are probably the most overvalued in history, leading other G7 equity markets into bubble territory in common.

Why are equities ignoring the certainty of a crash? The likely answer is that global equities are linked with the US stock market, where non-American investors hold over $22 trillion of equities. American equity values are driven by US investors who are notoriously oblivious of events outside the US. A problem in the Middle East? Who cares? It’s on the other side of the world.

This attitude is amplified by extreme bubble behaviour, such as during the dot-com era when any student of investor motivation would easily recognise excessive public greed and the abandonment of all caution. Market psychology today is no different.

Credit and gold

Current careless investor attitudes extend beyond financial markets, which are entirely credit obligations to physical gold, silver, and commodities, all without counterparty risk. Gold and silver as money have a remarkably stable long-term relationship with commodity values. It is credit, including fiat currencies whose unanchored values are declining, which is the problem. This is illustrated by how the fiat dollar it has declined measured in gold:

Few take this decline with the seriousness it merits. Since 1968, US$1,000 have lost $993 of purchasing power to date, and the pace of the dollar’s depreciation is visibly accelerating. It now faces what looks like its final test, a further collapse in its value sparked by the closure of Hormuz.

The sheer impossibility of the US Treasury and the Fed to prevent it should be obvious to anyone pausing to think. With a government debt to GDP of over 120% and an overriding political priority to accelerate credit expansion in a vain attempt to stave off an economic and financial crisis, the fiat dollar’s days are numbered.

It is time for everyone with financial wealth to wake up, get out of the various forms of credit, including fiat currencies, and move into real legal money without counterparty risk, which is gold. Fail to do so and you will be left with nothing.

3.CHRIS POWELL AND HIS GATA DISPATCHES:

ANDREW MAGUIRE LIVE FROM THE VAULT 269

5. COMMODITY REPORT//..

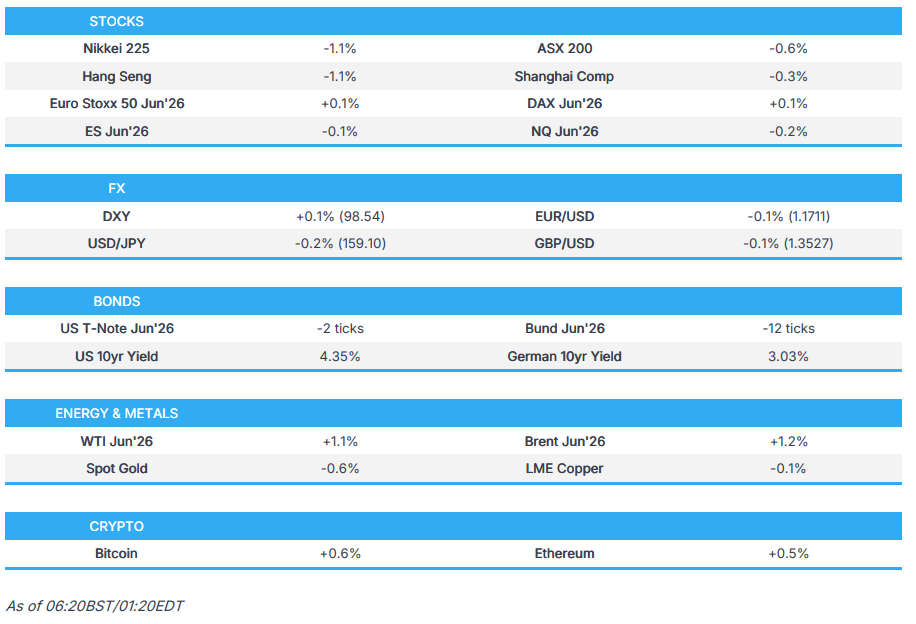

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

SHANGHAI CLOSED DOWN 7.71 PTS OR 0.19%

HANG SENG CLOSED DOWN 229.15 PTS OR 0.88%

Nikkei CLOSED DOWN 637.36 PTS OR 1.05%

//Australia’s all ordinaries CLOSED UP 0.22%

//Chinese yuan (ONSHORE) CLOSED DOWN 6.8340

/ OFFSHORE CLOSED DOWN AT 6.8378 Oil UP TO 98.53 dollars per barrel for WTI and BRENT UP TO 111.00 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING 6.8340 (DOWN) OFFSHORE YUAN TRADING DOWN TO 6.8378 ONSHORE YUAN TRADING ABOVE OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS MONDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.8340

OFFSHORE YUAN: DOWN TO 6.8378

1.HANG SANG CLOSED DOWN 229.15 PTS OR 0.88%

2. Nikkei closed DOWN 637.36 PTS OR 1.05%

WEST TEXAS INTERMEDIATE OIL UP TO 98.53

BRENT; 111.00

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 98.49/// EURO FALLS TO 1.1698 DOWN 23 BASIS PTS

3b Japan 10 YR bond yield:FALLS TO. +2.469 DOWN 1 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 159.52… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.643 DOWN 4 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: 6.8340( DOWN AND OFFSHORE: DOWN AT 6.8378

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD UP TO +3.0620 Italian 10 Yr bond yield UP to 3.893// SPAIN 10 YR BOND YIELD UP TO 3.527%

3i Greek 10 year bond yield UP TO 3.829%

3j Gold at $4627.40 //Silver at: 73.47 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 29 100 roubles/75.16

3m oil (WTI) into the 98 dollar handle for WTI and 111 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 159.52 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.464% DOWN 1 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.643 DOWN 4 PTS..: USA/SF this 0.7843 as the Swiss Franc . Euro vs SF: 0.9234

USA 10 YR BOND YIELD: 4.359 UP 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.960 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 3.822 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 45.05 UP 2 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD

10 YR UK BOND YIELD: 5.000 UP 5 PTS

30 YR UK BOND YIELD: 5.674 UP 3 BASIS PTS

10 YR CANADA BOND YIELD: 3.503 UP 4 BASIS PTS

5 YR CANADA BOND YIELD: 3.116 UP 3 BASIS PTS.

1a New York Opening report

Futures Tumble On AI Spending Fears As Brent Hits 2 Week High

Tuesday, Apr 28, 2026 – 08:34 AM

US equity futures are lower, dragged by tech, following a report that OpenAI missed revenue and user targets and there growing internal pushback against Sam Altman’s notorious aggressive spending (the company has $1.5 trillion in commitment it won’t be able to meet), which is hitting semiconductors and the broader supply chain. AS of 8:15am ET, S&P futures are down 0.7% and Nasdaq futures dropped 1.2% as concerns resurfaced over whether the vast amounts of investment in artificial intelligence will pay off. In pre market trading, Semis and Mag7 are under pressure. Defensives are leading Cyclicals ex-Energy. SoftBank, a key backer of ChatGPT’s owner, plunged 9.9% in Tokyo. US-based OpenAI partners including Oracle and CoreWeave fell in premarket trading. Nvidia was poised to drop 2.9% from a record high. Meanwhile, Brent rose above $111 a barrel, with the Strait of Hormuz still shut. Bond yields are 2-4bps higher as the yield curve flattens and USD appreciates, following the price of oil. Commodities continue to be led by Energy with WTI rising above $100/bbl after Trump signaled he was unlikely to accept Iran’s latest proposal to end the conflict which included a proposed a plan that would reopen the Strait of Hormuz while leaving questions about its nuclear program for later negotiations. There is material weakness in precious metals with silver’s underperformance possibly tied to Tech weakness. Today’s macro data focus is on weekly ADP, home price data, regional Fed activity indicators, and Consumer Confidence (though spending has de-coupled from sentiment). US economic data calendar slate includes weekly ADP employment change (8:15am), February FHFA house price index, S&P CS home prices (9am), April Richmond Fed manufacturing index and Conference Board consumer confidence (10am) and Dallas Fed services activity (10:30am)

In premarket trading, OpenAI partners such as CoreWeave (CRWV -7%) and Oracle (ORCL -7%) are falling after the Wall Street Journal reported that the AI startup recently failed to meet targets for sales and new users, reviving worries about spending ahead of tech earnings. Stocks linked to the buildout of AI infrastructure — from computing providers to the makers of semiconductors and power equipment used in data centers — are also down after the Wall Street Journal report on OpenAI.

- Magnificent Seven stocks are also mostly lower: Nvidia falls 2% on the OpenAI report (Apple +0.4%, Alphabet -0.1%, Amazon -0.9%, Meta Platforms -0.8%, Microsoft -1.2%, Tesla -1.2%)

- Celestica (CLS) falls 13% after the maker of electronic components reported first-quarter results that featured smaller upside to expectations than in recent quarters. While it raised its full-year forecast, analysts said the company had been facing high expectations.

- Dynatrace (DT) gains 4% on a report that Starboard Value LP took a stake and is pushing the company to better capitalize on the shift to artificial intelligence.

- Erasca (ERAS) slides 40% after the biotech said one patient withdrew from the trial after a severe treatment-related adverse event and later died, according to a filing.

- General Motors (GM) rises 4% after raising its profit outlook for the year by $500 million, saying its pickups and sport utility vehicles continue to sell even as gasoline prices soar due to the war in Iran.

- LendingClub (LC) rises 9% after the online lender’s first-quarter revenue and net interest income beat the average analyst estimate.

- Nucor (NUE) rises 2% after the steelmaker reported first-quarter earnings per share that beat the average analyst estimate as steel shipments were stronger than expected.

- Rambus (RMBS) plunges 17% after the semiconductor device manufacturer reported first-quarter results that were largely in line with expectations, which analysts said was a disappointment in the wake of recent strength in the stock.

- Sanmina (SANM) rises 7% after the electronics contract manufacturing services company’s second-quarter results beat expectations and it gave a full-year outlook that is seen as positive.

- Solaris Energy (SEI) rallies 5% after the firm’s first-quarter Ebitda beat the average analyst estimate.

- Spotify Technology falls 11% after reporting results that underwhelmed Wall Street, forecasting operating income in the current quarter that missed analysts’ estimates.

- UPS (UPS) falls 3% after the courier left financial guidance unchanged. Its profit beat expectations in the first quarter.

In other corporate news, Barclays traders struggled to capitalize on a volatile quarter with returns falling short of their US rivals. Eneos is said to be the last remaining bidder for some of Chevron’s Asian assets in a deal that might be valued at more than $2 billion. Google and the Department of Defense signed a deal allowing the Pentagon to use Google’s AI models on classified work, the Information reported.

Futures are sharply lower after closing at a new all time high yesterday. The market’s hottest theme took a knock from a report that OpenAI failed to meet internal targets, fueling internal concerns that it may struggle to support its spending on AI infrastructure, the WSJ reported. OpenAI partners including Oracle, CoreWeave and AMD fell in premarket trading, while SoftBank tumbled 10% in Japan. Resurgent optimism about AI had prompted the market’s charge as the rest of the market lagged due to rising oil prices. Wednesday’s earnings from four hyperscalers will offer the rally another test.

“The single most important line item isn’t revenue or margins; it’s capex,” said Amanda Lyons, IT-sector lead and head of research at Energy Group Capital. “Any hint of slowing spend would be taken negatively for the ecosystem, but a sharp step-up would likely raise questions around returns.”

The WSJ report is reviving worries about how fast companies can monetize their huge AI spending (while still investing enough to compete), leaving Alphabet, Amazon.com, Meta and Microsoft with a delicate message to convey tomorrow. For context, OpenAI revealed in March that it was generating $2 billion in revenue per month, while Bloomberg has reported that Anthropic is on track for annual revenue of almost $20 billion.

“The rising oil price is starting to feature in macro data,” said Anna Macdonald at Hargreaves Lansdown. “The longer the crisis rolls on, the more severe the impacts will be, and the more we expect it will dominate investor attention.”

The AI theme is playing out in other ways too. Battery maker CATL raised $5 billion after a Hong Kong share placement amid surging demand for data center energy storage. The shares have soared 139% since their debut. And Arizona’s data-center building boom is coming up against community opposition and dwindling water availability.

Ahead of this week’s policy meetings by the Federal Reserve, ECB and Bank of England, traders expect officials to keep rates on hold. The outlook gets cloudier for subsequent meetings, with everything hinging on the duration of the Middle East war. Money markets see the ECB and BOE hiking as soon as June, while odds are for the Fed to keep rates on hold for the rest of the year.

Brent advanced for a seventh straight day. The White House said President Donald Trump will address a proposal from Iran to resume oil flows through Hormuz “very soon.” The dollar rose alongside global bond yields. WTI rose above $100 as tankers laden with Iranian oil idle just shy of the US blockade line. There’s not much sign of progress toward ending the war, with Trump planning to address the matter “very soon.” The president has told his advisers he’s not satisfied with Iran’s latest suggestions, the NYT reported, citing people briefed on the discussions.

European stocks have swung to session lows, with Stoxx 600 down 0.6%. European stocks swing between gains and losses on a busy earnings day, with healthcare weighing after Novartis missed profit estimates and reported its first sales decline in almost two years. The energy subindex is the best-performing sector as Brent rose above $110 again. Here are the biggest movers Tuesday:

- SIG Group shares gain as much as 12%, the most since 2020, as the Swiss maker of carton packaging posted stronger-than-expected profits, putting it on track to recover from a challenging year

- BP shares rise as much as 3.3% after 1Q profit beat analyst estimates. Analysts at RBC Capital note outstanding downstream and trading results

- Nexans shares rise as much as 9.6% and on course to close at a new all-time high, after the cable and electrification specialist bolstered its position in the US through the acquisition of Republic Wire

- AAK gains as much as 8.6%, the most since July, after the Swedish maker of vegetable oils and fats reported earnings. DNB Carnegie says the print is “strong on all points” with volumes growing and “good” free cash flows

- Zealand Pharma gains as much as 7.2% after the Danish drug developer’s partner Boehringer Ingelheim said patients using its experimental obesity shot — called survodutide — experienced weight loss above 16% in a late-stage trial

- Nordic Semiconductor gains as much as 9.1% after the Norwegian chipmaker reported its latest earnings. Analyst sees a strong report from the company, with a broadening out of revenue trends and strong 2Q guidance

- Novartis shares fall as much as 5.1%, the most in more than a year, after the Swiss drugmaker reported weaker-than-expected core operating profit for the first quarter, as well as a drop in revenue

- Barclays declines as much as 4.3% after the British lender booked an extra £105m provision for missold car loans and announced an impairment of roughly £200m for a “single name” charge said to be tied to the UK property lender Market Financial Solutions

- Air Liquide fallsas much as 5.2% with analysts saying a miss in the French chemicals firm’s Large Industries division isappoints especially in light of hopes that the company could benefit from supply chain disruption in the Middle East

- Valmet shares fall as much as 9.1%, to the lowest in more than a year, after first-quarter orders and adjusted Ebita undershot expectations, and the Finnish machinery supplier announced plans for temporary layoffs to save costs

- Telenor shares fall as much as 10%, the most since 2020, after the telecom reduced Ebitda growth targets for its core Nordic markets and on the group level. The move comes less than three months since the guidance was first issued

- Sweco shares drop as much as 8.8%, hitting their lowest level since May 2024, after the architecture and engineering consultancy reported sales and earnings that fell short of consensus expectations

- Wartsila falls as much as 6.2%, the most since March 3, after the Finnish marine and energy industrial equipment maker reported its latest earnings. Analysts say the report, while a beat, is not necessarily reassuring

Earlier, Asian stocks traded lower but continued to hold near a February peak as traders awaited earnings from key companies in the global technology sector. The MSCI Asia Pacific Index fluctuated before falling as much as 0.4%, dragged by information technology firms. Financials were among the biggest boosts. Key gauges declined in Hong Kong, Australia and India while South Korean equities gained. The Topix gauge closed higher after Bank of Japan held interest rates as expected. Among the region’s tech firms that rely on outlays from the global hyperscalers, Advantest saw its stock slide Tuesday on a weak outlook and an indication of capacity constraints. Its fellow Japanese chip-equipment maker Tokyo Electron is among Asian firms reporting later this week, along with Chinese EV maker BYD.

Of the 150 S&P 500 companies to have reported so far this earnings season, 80% have beaten analysts’ forecasts, while 13% have missed. Earnings revisions for 2026, measured by Citigroup’s Earnings Revisions Index, have been improving since the start of the month. Companies have been holding or lifting guidance even as executives repeatedly flag an uncertain macroeconomic backdrop, according to JPMorgan strategists.

In FX, the Bloomberg Dollar Spot Index is up by 0.2% and reversing an earlier decline against the yen sparked by the Bank of Japan holding rates in a split decision.

In rates, bond markets are under pressure as oil prices rise, with Brent topping $111 to increase inflationary concerns. Treasury front-end yields are higher by 2bp-3bp, underperforming long end as Fed-dated swaps price in less easing; 10-year is 2bp higher near 4.36%, just off session high reached during London morning, outperforming German and UK counterparts by about 1bp-2bp. European bonds jolted by a jump in ECB CPI inflation expectations in March, though the initial drop on that has eased. German two-year yields up five basis points as traders increase ECB rate-hike bets and a similar move for two-year gilts, but declines have pared at the long-end in Europe and the UK. US session includes 7-year note auction at 1pm, the week’s third and final coupon auction following small tails for Monday’s 2- and 5-year note sales.

BlackRock Investment Institute said the war and elevated inflation will keep government bond yields higher for longer. But companies don’t seem to be feeling the hit yet. The fallout from the conflict, which broke out two-thirds of the way through the quarter, “has barely been visible,” says Bloomberg Opinion columnist John Authers, while current earnings forecasts look “very, very stretched.”

In commodities, June WTI crude futures are up almost 5%, rising above $101 and at session highs as blockades of the Strait of Hormuz curtail supply. Gold prices sinking, down by around $75 and testing $4,600/oz.

US economic data calendar slate includes weekly ADP employment change (8:15am), February FHFA house price index, S&P CS home prices (9am), April Richmond Fed manufacturing index and Conference Board consumer confidence (10am) and Dallas Fed services activity (10:30am)

Market Snapshot

- S&P 500 mini -0.7%

- Nasdaq 100 mini -1.2%

- Russell 2000 mini -0.6%

- Stoxx Europe 600 -0.5%

- 10-year Treasury yield +3 basis points at 4.37%

- VIX +0.2 points at 18.26

- Bloomberg Dollar Index +0.2% at 1198.04

- euro -0.2% at $1.1697

- WTI crude +4.8% at $101 barrel

Top Overnight News

- President Donald Trump signaled he was unlikely to accept Iran’s latest proposal to end the conflict after Tehran proposed a plan that would reopen the Strait of Hormuz while leaving questions about its nuclear program for later negotiations. CNN

- OpenAI recently missed its own targets for new users and revenue, stumbles that have raised concern among some company leaders about whether it will be able to support its massive spending on data centers. WSJ

- China’s top leadership on Tuesday pledged to take more “forceful” measures to strengthen energy security and shore up business confidence, as the country faces economic headwinds from the protracted US – Iran standoff in the ME. Nikkei

- The BoJ kept interest rates steady on Tuesday but three of its nine-member board proposed hiking borrowing costs, signaling policymakers’ concerns over inflationary pressures from the Middle East conflict. The central bank also sharply revised up its price forecasts and stressed vigilance to the risk of an inflation overshoot, signaling a strong chance of a rate hike in coming months. RTRS

- Investors are reverting to a pre-war playbook of betting Asian stocks will outpace US peers due to the region’s central role in the AI boom. The MSCI Asia Pacific Index’s 14% surge so far this month has outpaced the S&P 500’s 9.9% gain. BBG

- ECB survey reveals a spike in inflation expectations as consumers react to fallout from the Iran war. Additionally, the survey revealed a larger than expected tightening of credit standards due to higher perceived risks and lower risk tolerance. ECB

- Keir Starmer faces a high-stakes vote today on whether to begin an investigation into his assurances to Parliament that due process was followed in Peter Mandelson’s appointment as US ambassador. BBG

- Wall Street dealers’ Treasury holdings have jumped to the highest level since the global financial crisis as the Trump administration’s cut to regulation nudges banks back into the $31tn debt market. FT

- Foreign-based automakers have warned the Trump administration that they are looking at pulling their cheapest car models out of the U.S. market if the U.S.-Mexico-Canada Agreement isn’t renewed or is watered down, according to people familiar with the discussions. WSJ

- Thus far in 2026, there have been 25 IPOs greater than $25 million in value, totaling $14 billion in gross proceeds. This represents a nearly 80% increase in both the number and value of IPOs relative to this time last year. Roughly 40% of this year’s IPOs have been Industrials companies compared with the historical annual average of 10% since 1995. In contrast, there have been no IPOs YTD in the Information Technology sector despite the sector representing 25% of IPOs since 1995: GS

Iran News

- US President Trump has told advisers he is not satisfied with Iran’s latest proposal to reopen the Strait of Hormuz and end the war, NYT reported; a US official said that accepting it [the Iran proposal] could appear to deny Trump a victory. The proposal also called on the United States to end its naval blockade, but would have set aside questions about what to do with Iran’s nuclear program. A US official also said that accepting it [the Iran proposal] could appear to deny Trump a victory. US officials say Iran’s leadership has not authorised its negotiators to make concessions on the nuclear deal, frustrating any attempts to forge a compromise or peace agreement. At the heart of the debate over whether to accept the Iranian proposal were discussions in the Trump administration about the issue of economic leverage and what further American military operations would be needed to get Tehran to make significant concessions in negotiations. Some administration officials believe that continuing the blockade for two more months would cause significant long-term damage to Tehran’s energy industry. “Without a resumption of military action, there is little reason to think the Iranian position will shift.”.