EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MAY 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,545.200000000 USD

INTENT DATE: 04/29/2026 DELIVERY DATE: 05/01/2026

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DEUTSCHE BANK AG 741

118 C MACQUARIE FUTURES US 513 152

118 H MACQUARIE FUTURES US 302

363 H WELLS FARGO SECURITI 1199

435 H SCOTIA CAPITAL (USA) 38

661 C JP MORGAN SECURITIES 1587 384

690 C ABN AMRO CLR USA LLC 2

905 C ADM 34

TOTAL: 2,476 2,476

MONTH TO DATE: 2,476

GOLD: NUMBER OF NOTICES FILED FOR MAY/2026: 2476 CONTRACTs NOTICES FOR 247,600 OZ or 7.701 TONNES

total notices so far: 2476 contracts FOR 247,600 OZ OR 7.701 TONNES

SILVER NOTICES: 4580 NOTICE(S) FILED FOR 22.900 MILLION OZ /

total number of notices filed so far this month : 4580 CONTRACTS (NOTICES) for 22.90 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF 1 CONTRACTS OR 0.005 MILLION OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ

SUMMARY OF OUR APRIL 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/.

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 278 CONTRACT QUEUE JUMP FOR 27800 OZ/ (0.8646 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD.

MARCH:: SMALL INITIAL STANDING FOR GOLD FOR MARCH AT 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 46 CONTRACT QUEUE JUMP OF 4400 OZ OR 0.2320 TONNESAND THEN WE ADD BY OUR THREE EXCHANGE FOR RISK: 22.3818///NEW STANDING ADVANCES TO 67.6648 TONNES OF GOLD./

APRIL: INITIAL STANDING FOR GOLD; 52.600 TONNES FOLLOWED BY TODAY’S 27,800 OZ QUEUE JUMP(0.8646 TONNES) //NEW STANDING ADVANCES TO 70.286TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK FOR 2239 CONTRACTS/223900 OZ OR 6.964 TONNES//NEW STANDING ADVANCES TO 77.726 TONNES

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES.

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88 TONNES// WILL BE VERY SMALL THIS MONTH

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONG

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE 2107 CONTRACTS TO AN OI OF 99.154, A NEW ALL TIME LOW WITH AN EXCEPTIONALLY HIGH PRICE FOR SILVER (APRIL 30)

EFP ISSUANCE 300 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 300 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2107 CONTRACTS AND ADD TO THE 300 E.FP. ISSUED

WE OBTAIN A MEGA STRONG SIZED LOSS OF 1807 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR LOSS OF $1.95

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 13.170 MILLION PAPER OZ

OCCURRED WITH OUR LOSS IN PRICE.OF $1.95

2.ASIAN AFFAIRS APRIL 30 /2025

SHANGHAI CLOSED UP 4.64 PTS OR 0.11%

HANG SENG CLOSED DOWN 335.31 PTS OR 1.28%

Nikkei CLOSED DOWN 584.96 PTS OR 0.98%

//Australia’s all ordinaries CLOSED UP 1.59%

//Chinese yuan (ONSHORE) CLOSED UP 6.8265

/ OFFSHORE CLOSED UP AT 6.8317 Oil UP TO 106.64 dollars per barrel for WTI and BRENT DOWN TO 109.68 Stocks in Europe OPENED ALL MOSTLY GREEN

ONSHORE USA/ YUAN TRADING 6.8265 (UP) OFFSHORE YUAN TRADING UP TO 6.8317 ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR 2200 CONTRACTS DOWN TO AN OI OF 367,330 CONTRACTS (OI) , HAVING ADVANCED FROM OUR NEW LOW OI SET THIS MONTH AND SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 354,581 SET APRIL6/2026. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 354,581 WITH GOLD AT AN EXTREMELY HIGH $4,700.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD CONSIDERABLE T.A.S. LIQUIDATION DURING WEDNESDAY’S TRADING ALONG WITH MONTHLY SPREADER LIQUIDATION. IT SEEMS THAT SOME OF THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE BUT ALSO SOME SPECULATORS GOING TO THE SHORT SIDE WITH THE BANKERS NOW TAKING THE LONG SIDE,AND CENTRAL BANKS SUPPLYING THE NECESSARY PAPER, AS WELL AS COVERING THEIR SHORTFALL. THERE ARE ALSO SOME SPECULATORS WHO CONTINUALLY GO TO THE SHORT SIDE AND AND OF COURSE THEY WILL BE ANNHILATED ON CENTRAL BANK COMMAND!!

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE MASSIVE AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS APRIL CONTRACT MONTH!!

THE FAIR SIZED LOSS ON OUR TWO EXCHANGES OCCURRED WITH OUR LOSS IN PRICE IN GOLD. WE ARE NOW IN THE LAST DAYS OF THE MONTH AND THUS OUR TWO SPREADERS ARE IN FULL FORCE DURING OPTIONS EXPIRY MONTH: THE COMEX OPTIONS EXPIRY CONCLUDED ALREADY

WE THUS HAD A FAIR LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 1165 CONTRACTS (OR 3.623 TONNES) WITH OUR LOSS IN PRICE, AS WE WERE INFORMED OF A FAIR CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.EQUATING TO 1035 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A ZERO EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS TOTALLING 0 CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD.

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH APRIL

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO APRIL:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

DETAILS ON OUR NEW APRIL COMEX CONTRACT MONTH//

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 7486 CONTRACTS DESPITE OUR LOSS IN PRICE ($85.85). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH APRIL/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A FAIR SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 1175 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT IS NOW IN FULL FORCE DURING THIS WEEK DURING LONDON COMEX AND LBMA/OTC OPTION EXPIRY WEEK!! (INITIAL MAY CONTRACT MONTH)

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD.

FOR MARCH WE HAVE 3 EXCHANGE FOR RISK ISSUANCES SO FAR FOR 7196 CONTRACTS OR 719,600 OZ/22.3818 TONNES.. AS DELIVERIES OF GOLD THESE PAST SEVERAL MONTHS HAVE BEEN HUGE!!

APRIL: 2 EXCHANGE FOR RISK NOTIFICATION HAVE BEEN ISSUED FOR 223,900 OZ OR 6.964 TONNES.

MAY : ZERO SO FAR!

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

AND NOW APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING MAY,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $45.70)

WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION AND SPREADER LIQUIDATION // COMEX SESSION// WITH OUR LOSS IN PRICE , OUR LONG SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI //

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

WEDNESDAY NIGHT//THURSDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

NOW A LITTLE REVIEW OF GOLD STANDING THESE PAST 7 MONTHS:

STANDING FOR GOLD OCT THROUGH TIL APRIL

ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31

OCTOBER…

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

4. JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR LATEST QUEUE JUMP OF 0.0298 TONNES TO WHICH THIS IS ADDED TO ALL OTHER QUEUE JUMPS OF 41.2082 / NEW QUEUE JUMP ADVANCES TO: 41.233 TONNES//STANDING ADVANCES TO: 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES/NEW STANDING ADVANCES TO 157.879 TONNES

MARCH: INITIAL STANDING: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TO WHICH WE THEN ADD OUR THREE EXCHANGE FOR RISK FOR 22.3818 TONNES// GOLD STANDING ADVANCES TO: 67.6648 TONNES/

APRIL: INITIAL STANDING: A VERY STRONG 52.600 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP (2.4105TONNES) TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1498 CONTRACTS//149,800 OZ OR 4.659 TONNES.TOTAL EXCHANGE FOR RISK THUS FAR THIS MONTH TOTALS TWO FOR 2239 CONTRACTS//223,900 OZ OR 6.964 TONNES. THUS STANDING FOR GOLD AT THE COMEX ADVANCES TO 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 12.24 TONNES

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $45.70

WE HAD 2147 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET LOSS ON THE TWO EXCHANGES : 1165 CONTRACTS OR 116,500 OZ OR 3.623 TONNES

INITIAL GOLD COMEX

MAY DELIVERY MONTH

APRIL30 2026

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | ENTRIES; 0 |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 2426 CONTRACTS OR 242,600 OZ 7.701 TONNES OF GOLD |

| No of oz to be served (notices) | 1461 Contracts 146100 OZ 4.544TONNES |

| Total monthly oz gold served (contracts) so far this month | 242600 notices 242,600 oz 7.701 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 1

0 ENTRY

DEPOSITS/CUSTOMER

0 ENTRY

xxxxxxxxxxxxxxxxxx

comex withdrawals:

ENTRIES; 0

xxxx

adjustments: 2 DEALER TO CUSTOMER

a) Brinks 280,967.589 oz

b) JPMorgan 143,039.799 oz

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF MAY OI STANDS AT 3937 CONTRACTS HAVING A GAIN OF 31 CONTRACTS.

THUS BY DEFINITION, THE INITIAL AMOUNT OF GOLD WILLING TO STAND FOR DELIVERY AT THE COMEX FOR THIS MAY CONTRACT MONTH IS AS FOLLOWS:

3937 NOTICES X 100 OZ PER NOTICE

EQUALS 393,700 OZ

OR 12.24 TONNES OF GOLD WHICH IS PRETTY GOOD FOR A NON ACTIVE DELIVERY MONTH

.

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI LOST BY 2557 CONTRACTS DOWN TO AN OI OF 259,659

JULY LOST 15 CONTRACTS DOWN TO AN OI OF 866.

We had 2476 contracts filed for today representing 247,600oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 1587 notices issued from their client or customer account. The total of all issuance by all participants equate to 2476 contract(s) of which 0384 notices were stopped (received) by j.P. Morgan dealer and 267 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (2,476) to which we add the difference between the open interest for the front month of MAY (3937 CONTRACTS) minus the number of notices served upon today 2476 x 100 oz per contract) equals 393,700 OZ OR (12.24 Tonnes of gold)

THUS: INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (2476) to which we add the difference between the open interest for the front month of MAY (3937 CONTRACTS) minus the number of notices served upon today 2476 x 100 oz per contract) equals 393,700 OZ OR (12.24Tonnes of gold)

new total of gold standing in MAY is 12.24 TONNES//

TOTAL COMEX GOLD STANDING FOR MAY 12.24 TONNES TONNES WHICH IS NOW STRONG FOR THIS NORMALLY NON ACTIVE DELIVERY MONTH OF MAY.

confirmed volume WEDNESDAY confirmed 138,103 really awful!! many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

the number provided do not match from yesterday!!!

total pledged gold: 1,947,780.204 oz 60.58 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,947,780.204 tonnes oz 60.58 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 29,321,938.266 oz

TOTAL REGISTERED GOLD 15,765,316.599 OZ 490.367 onnes

TOTAL OF ALL ELIGIBLE GOLD 13,556,621.667 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,817.536 oz ((REG GOLD- PLEDGED GOLD)=

429.783 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

MAY DELIVERY MONTH

APRIL30

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2 entries i) Out of Delaware 14,550.806 oa ii0 out of JPMorgan: 602,506.900 oz total withdrawal: 617,057.706 oz |

| Deposits to the Dealer Inventory | 0 entries xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT 1 ENTRY i) Into Delaware: 6717.606 oz total deposit 6717.606 oz |

| No of oz served today (contracts) | 4580 CONTRACT(S) (22.900 MILLION OZ |

| No of oz to be served (notices) | 1Contracts (0.005 MILLION oz) |

| Total monthly oz silver served (contracts) | 4580 contracts 22.900 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 entries

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 ENTRY

i) Into Delaware: 6717.606 oz

total deposit 6717.606 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

2 entries

i) Out of Delaware 14,550.806 oa

ii0 out of JPMorgan: 602,506.900 oz

total withdrawal: 617,057.706 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments:2

customer acct to dealer account

a) CNT 1,204,983.341 oz

b) Delaware 75,073.75 oz

total oz leaving customer accts to dealer 1.28 million oz

Wednesday volume: 50,187 oz// fair

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 80.834 MILLION OZ//.TOTAL REG + ELIGIBLE. 314.627 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR APRIL

silver open interest data:

FRONT MONTH OF MAY /2026 OI: 6299 OPEN INTEREST CONTRACTS FOR A LOSS OF 2411 CONTRACTS.

THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER WILLING TO STAND IS AS FOLLOWS

6299 NOTICES X 5000 OZ PER NOTICE

EQUALS

31.495 MILLION OZ WHICH IS PRETTY GOOD FOR MAY/SILVER ACTIVE DELIVERY MONTH

JUNE SAW A LOSS OF 26 CONTRACTS DOWN TO 1439 OI CONTRACTS

JULY SAW A LOSS OF 117 CONTRACTS DOWN TO 71,111 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 4580 or 15,000 oz

CONFIRMED volume WEDNESDAY; 50,189 fair

AND NOW MAY. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MY. we take the total number of notices filed for the month so far at 4580 X5,000 oz = 22.900 MILLION oz

to which we add the difference between the open interest for the front month of MAY (6299) AND the number of notices served upon today (4580 )x (5000 oz)

Thus the standings for silver for the MAY 2026 contract month: (4580 )Notices served so far) x 5000 oz + OI for the front month of MAY (6299) minus number of notices served upon today (4580)x 5000 oz equals silver standing for the APRIL..contract month equating to 31.495 MILLION OZ.+

NEW STANDING: 31.495 MILLION OZ WHICH IS PRETTY GOOD FOR THIS ACTIVE DELIVERY MONTH OF MAY.

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 80.834 million oz of registered silver

JPMorgan as a percentage of total silver: 141.719/314.627 million: 45.22

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

APRIL 30/2026/WITH GOLD UP $19.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 5.142 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1039.195 TONNES

APRIL 29/2026/WITH GOLD DOWN $45.70 TODAY/NO CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 28/2026/WITH GOLD DOWN $85.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 27/2026/WITH GOLD DOWN $41.10 TODAY/NO CHANGES IN GOLD AT THE GLD: // //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 24/2026/WITH GOLD UP $13.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 23/2026/WITH GOLD DOWN 28.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.000 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1050.91 TONNES

APRIL 22/2026/WITH GOLD UP 26.40 TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 21/2026/WITH GOLD DOWN 11.90TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 17/2026/WITH GOLD UP $71.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 1.15 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 16/2026/WITH GOLD DOWN $15.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.285 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1051.783 TONNES

APRIL 15/2026/WITH GOLD DOWN $24.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.289 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1049.478 TONNES

APRIL 14/2026/WITH GOLD UP $83.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.714 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1047.192 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 10/2026/WITH GOLD DOWN $11.90 TODAY/SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.724 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.42 TONNES

APRIL 9/2026/WITH GOLD UP $42.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.429 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.990 TONNES

APRIL 8/2026/WITH GOLD UP $88.95 TODAY/NO CHANGES IN GOLD AT THE GLD A//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 7/2026/WITH GOLD UP $5.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.429 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 6/2026/WITH GOLD UP $5.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/INVENTORY RESTS AT 1050.99 TONNES

APRIL 2/2026/WITH GOLD DOWN $132.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.714 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1050.99 TONNES

APRIL 1/2026/WITH GOLD UP $134.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 1.143 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1047.276 TONNES

MAR 31/2026/WITH GOLD UP $119.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.429 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1046.133 TONNES

MAR 30/2026/WITH GOLD UP $33.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.143 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1049.562

MAR 27/2026/WITH GOLD UP $103.55 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.285 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.705

MAR 26/2026/WITH GOLD DOWN $213.05 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.580 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.42

MAR 25/2026/WITH GOLD UP $155.30 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.300 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1053.000

MAR 24/2026/WITH GOLD DOWN $7.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.286 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1052.705

MAR 23/2026/WITH GOLD DOWN $165.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 5.149 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1056.991

MAR 20/2026/WITH GOLD DOWN $39,55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.855 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1062.135

MAR 19/2026/WITH GOLD DOWN $XXX TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 2.57 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1066.99

MAR 18/2026/WITH GOLD DOWN $111.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.144 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1069.564 TONNES

MAR 17/2026/WITH GOLD UP $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 0.857 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.708 TONNES

MAR 16/2026/WITH GOLD DOWN $60.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4/327 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1071/.565 TONNES

MAR 13/2026/WITH GOLD DOWN $61.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.428 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1075.852 TONNES

MAR 12/2026/WITH GOLD DOWN $49.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 3.715 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1077.28 TONNES

MAR 11/2026/WITH GOLD DOWN $70.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 2.858 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1073.565 TONNES

MAR 10/2026/WITH GOLD UP $137.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 2.614 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.707 TONNES

GLD INVENTORY: 1039.195 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

APRIL 30 WITH SILVER UP $2.03: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.991 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 485.243MILLION OZ

APRIL 29 WITH SILVER DOWN $1.95: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 28 WITH SILVER DOWN $2.05: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 27 WITH SILVER DOWN $1.39: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 24 WITH SILVER UP 0.92: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.54 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 487,23MILLION OZ

APRIL 23WITH SILVER DOWN $2.35: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.489 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 488,773MILLION OZ

APRIL 22 WITH SILVER UP 1.43: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262MILLION OZ

aPRIL 21 WITH SILVER DOWN 3.71: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262 MILLION OZ

APRIL 17 WITH SILVER UP $3.09: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.453 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.900 MILLION OZ

APRIL 16 WITH SILVER DOWN $1.00: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.132 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.477 MILLION OZ

APRIL 15 WITH SILVER UP $0.01: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.588 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.579 MILLION OZ

APRIL 14 WITH SILVER UP $3.99: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.633 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.991 MILLION OZ

APRIL 13 WITH SILVER DOWN 0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.589 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.624 MILLION OZ

APRIL 10 WITH SILVER DOWN 0.16: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.724 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 492.213 MILLION OZ

APRIL 9 WITH SILVER UP $0.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.173 MILLION OZ INTO THE SLV// // :INVENTORY RESTS AT 492.937 MILLION OZ

APRIL 8 WITH SILVER UP $3.50: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 7 WITH SILVER DOWN $0.89: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 6 WITH SILVER UP $0.41: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL WITHDRAWAL OF 0.224 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 2 WITH SILVER DOWN $3.57: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.091 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.988 MILLION OZ

APRIL 1 WITH SILVER UP $1.38: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND WITHDRAWAL OF 0.453 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 491.079 MILLION OZ

MAR 31 WITH SILVER UP $4.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND FRAUDULENT WITHDRAWAL OF 3.893 MILLION OZ FROM THE SLV // :INVENTORY RESTS AT 491.532 MILLION OZ

MAR 30 WITH SILVER UP $0.74: NO CHANGES IN SILVER INVENTORY AT THE SLV: // :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 27 WITH SILVER UP $1.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV// :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 26 WITH SILVER DOWN $4.75: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 25 WITH SILVER UP $3.25: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 24 WITH SILVER DOWN $0.15: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT DEPOSIT OF 10.505 MILLION OZ INTO THE SLV :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 23 WITH SILVER UP $0.06: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// NO CHANGE IN INVENTORY/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 20 WITH SILVER DOWN $1.92: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.490 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 19 WITH SILVER DOWN $6.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.9444 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 490.761 MILLION OZ

MAR 18 WITH SILVER DOWN $2.36: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 1.087 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 494.792 MILLION OZ.

MAR 17 WITH SILVER DOWN $0.89: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 493.705 MILLION OZ.

MAR 16 WITH SILVER DOWN $0.57: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.536 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 497.056 MILLION OZ.

MAR 13 WITH SILVER DOWN $3.83: NO CHANGES IN SILVER INVENTORY AT THE SLV// . ./ :INVENTORY RESTS AT 499.592

MAR 12 WITH SILVER DOWN $0.51 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 3.713 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 499.592 MILLION OZ

MAR 11 WITH SILVER DOWN $3.96 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 1.812 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 503.305 MILLION OZ

MAR 10 WITH SILVER UP $5. HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.63 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 505.117 MILLION OZ

MAR 9 WITH SILVER DOWN $0.30 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.54 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 506.747 MILLION OZ

CLOSING INVENTORY 485.243 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

MATHEW PIEPENBURG…

ALASDAIR MACLEOD

JESSE COLUMBO

This is a post from Jesse Colombo’s The Bubble Bubble Report—a bestselling newsletter focusing on precious metals investing and global economic risks. We specialize in detailed reports and analyses.

Gold & Silver Volatility Has Plunged

Extremely low levels of volatility in gold and silver typically signal the end of corrections and the beginning of new rallies.

| Jesse ColomboApr 30∙Paid |

In today’s update, I’d like to highlight an interesting observation shared on X by Bob Coleman, Founder and President of Idaho Armored Vaults, and add my own perspective. In short, he noted that both gold and silver volatility indexes, which I will explain in more detail shortly, have declined significantly from their peaks earlier this year, a development that typically signals that corrections or pullbacks in the metals have run their course and are setting the stage for a rebound.

The gold and silver volatility indexes referred to here are the CBOE Gold ETF Volatility Index and the CBOE Silver ETF Volatility Index, which measure the market’s expectation of 30-day volatility in gold and silver prices, respectively, based on options pricing for the SPDR Gold Shares ETF (GLD) and the iShares Silver Trust ETF (SLV), similar to how the VIX measures expected volatility for stocks.

When these volatility indexes reach extremely high levels, they signal emotional extremes where moves are becoming stretched and a reversal is likely. That is what occurred in late January, when I pointed out that precious metals were trading like meme stocks and urged caution for those trading, as opposed to long-term holding, especially when using leverage.

When the volatility indexes cool off and pull back, however, that typically reflects a period of consolidation and often precedes a significant breakout once the consolidation has run its course. In a bull market, declining volatility during a pullback often indicates that the correction is stabilizing, and that is exactly what is happening right now, as I will show in the next two charts.

The first chart shows the price of gold alongside the Gold Volatility Index and its 200-day moving average. Note how spikes in the index, such as in the spring of 2025, the fall of 2025, and January 2026, led to pullbacks or periods of consolidation as extreme bullish sentiment cooled, which is a healthy and normal pattern. That is how all markets function, and there is no escaping it, as I showed here.

Next, take a look at the lows in the Gold Volatility Index, as marked by the red arrows, and see how they align with lows in the price of gold. This behavior is especially pronounced during a strong uptrend in volatility, as indicated by the steep upward slope of the index’s 200-day moving average, which is the case right now.

Under these conditions, when the index pulls back to the 200-day moving average, it is a strong signal that the lows are likely in for both volatility and the price of gold, and that is what has occurred over the past few trading days.

Next, let’s take a look at the price of silver alongside the Silver Volatility Index and its 200-day moving average, where the same principles apply as in the prior chart of gold. Spikes in volatility, such as in the fall of 2025 and early 2026, typically lead to cool-off periods, while lows in volatility, particularly pullbacks to the 200-day moving average, often precede rallies in both volatility and the price of silver, which is the current setup.

Interestingly, the signal from the Gold Volatility Index aligns with the one given by the indicator I pay closest attention to, Williams %R, which helps identify when an asset is overbought or oversold. While Williams %R is based purely on price and uses a completely different methodology than the volatility indexes discussed earlier, both are now conveying the same message.

In my update on Monday, I showed that gold was nearing oversold conditions according to Williams %R, and after the declines of the past two days, it is now fully oversold. In an uptrend like the one gold is currently in, that typically signals that a rebound is near (learn more). That is not to say gold cannot go any lower, but it indicates that the pullback has largely run its course and that the odds now favor the upside.

Like gold, silver is now officially at oversold levels:

It’s also worth noting that the lows in the Gold Volatility Index and the Williams %R indicator have aligned with gold’s pullback to its key $4,300 to $4,600 support zone, and those conditions point to a high probability of a rebound from these levels in the near term.

To learn more about support and resistance zones, I recommend reading my two-part tutorial on the topic (Part 1 and Part 2).

Similarly, silver has pulled back to its $60 to $70 support zone at the same time that the Silver Volatility Index and Williams %R have reached their lows, a combination that significantly increases the odds of a rebound from this zone in the near term:

To conclude, the sharp decline in gold and silver’s volatility indexes is a clear sign that the speculative fervor seen in January has been effectively flushed out, which was necessary for the still-young secular precious metals bull market to continue in a healthy manner. The oversold readings in both metals further confirm that they are stretched to the downside, and the odds now favor a rebound in the near term. Conditions like these have historically marked some of the best opportunities to “buy the dip.”

Disclaimer: the information provided in The Bubble Bubble Report and related content is for informational and educational purposes only and should not be construed as investment, financial, or trading advice. Nothing in this publication constitutes a recommendation, solicitation, or offer to buy or sell any securities, commodities, or financial instruments.

All investments carry risk, and past performance is not indicative of future results. Readers should conduct their own research and consult with a qualified financial advisor before making any investment decisions. The author and publisher disclaim any liability for financial losses or damages incurred as a result of reliance on the information provided.

3.CHRIS POWELL AND HIS GATA DISPATCHES:

Royal Canadian Mint reviewing allegations about tainted Colombian gold

Submitted by admin on Tue, 2026-04-28 13:13 Section: Daily Dispatches

From the Canadian Press

via CTV News, Toronto

Monday, April 27, 2026

OTTAWA, Ontario, Canada — The Royal Canadian Mint says it has initiated a full review in response to allegations some of its gold comes from a region of Colombia where drug cartels control mines.

Mint spokesperson Deneen Perrin says as soon as the mint learned of the allegations raised by the New York Times, it “immediately and fully” suspended the refining of any material from the supply chain in question

In a report published Monday, the newspaper suggests some of the mint’s gold comes from Colombian mines controlled by the Clan del Golfo drug cartel. …

… For the remainder of the report:

end

Barrick picks a NY primary listing for IPO of North American gold assets

Submitted by admin on Tue, 2026-04-28 12:21 Section: Daily Dispatches

By Robb M. Stewart and Adriano Marchese

The Wall Street Journal

Tuesday, April 28, 2026

Barrick Mining plans to list its prized North American gold assets in New York as part of an initial public offering set to be completed before the end of the year.

The mining company said today it has identified what it believes is the optimal structure for a separate listing of the assets, including a primary listing in New York and a secondary listing in Toronto.

Not disclosed are details such as where the company that will house the North American operations will be based and domiciled, and the percentage of the assets that Barrick plans to float beyond what the company affirmed will be a minority interest. …

… For the remainder of the report:

end

U.S. trade chief urges allies to pay more for critical minerals to undermine China

Submitted by admin on Sun, 2026-04-26 19:29 Section: Daily Dispatches

By Aime Williams

Financial Times, London

Wednesday, April 22 2026

President Trump’s top trade official has told U.S. allies they must pay more for critical minerals sourced from outside China as Washington tries to break Beijing’s stranglehold on supplies.

Jamieson Greer, the U.S. trade representative, said American allies must be ready to pay a “national security premium” for the minerals, which would be sourced from within a proposed group of trading partners including Europe.

The U.S. wants the club of countries to trade minerals at set minimum prices to protect their investments in mining and processing, and could hit outside producers — such as China — with steep tariffs or other barriers to prevent them driving down prices.

But the proposal has already alarmed some allies, according to people familiar with private talks between Washington and foreign officials, who fear the fledgling scheme will raise costs for businesses and attract trade retaliation from China. …

… For the remainder of the report:

4.ANDREW MAGUIRE LIVE FROM THE VAULT 269

5. COMMODITY REPORT//..

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 4.64 PTS OR 0.11%

HANG SENG CLOSED DOWN 335.31 PTS OR 1.28%

Nikkei CLOSED DOWN 584.96 PTS OR 0.98%

//Australia’s all ordinaries CLOSED UP 1.59%

//Chinese yuan (ONSHORE) CLOSED UP 6.8265

/ OFFSHORE CLOSED UP AT 6.8317 Oil UP TO 106.64 dollars per barrel for WTI and BRENT DOWN TO 109.68 Stocks in Europe OPENED ALL MOSTLY GREEN

ONSHORE USA/ YUAN TRADING 6.8265 (UP) OFFSHORE YUAN TRADING UP TO 6.8317 ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.8265

OFFSHORE YUAN: UP TO 6.8317

1.HANG SANG CLOSED DOWN 335.31 PTS OR 1.28%

2. Nikkei closed DOWN 584.96 PTS OR 0.98%

WEST TEXAS INTERMEDIATE OIL UP TO 106.64

BRENT; 109.68

3. Europe stocks SO FAR: ALL MOSTLY GREEN

USA dollar INDEX DOWN TO 98.29/// EURO FALLS TO 1.1715 UP 38 BASIS PTS

3b Japan 10 YR bond yield:RISES TO. +2.519 UP 5 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 157.127… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.747 UP 10 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: 6.8265( UP AND OFFSHORE: UP AT 6.8317

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT DOWN this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +3.0720 Italian 10 Yr bond yield DOWN to 3.909// SPAIN 10 YR BOND YIELD DOWN TO 3.537%

3i Greek 10 year bond yield UP TO 3.861%

3j Gold at $4639.35 //Silver at: 73.63 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 6/ 100 roubles/75.11

3m oil (WTI) into the 106 dollar handle for WTI and 109 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 157.127 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.519% UP 5 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.747 UP 10 PTS..: USA/SF this 0.7854 as the Swiss Franc . Euro vs SF: 0.9162

USA 10 YR BOND YIELD: 4.396 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.987 UP 0 BASIS PTS/

USA 2 YR BOND YIELD: 3.898 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 45.19 UP 12 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD

10 YR UK BOND YIELD: 5.012 DOWN 6 PTS

30 YR UK BOND YIELD: 5.668 DOWN 6 BASIS PTS

10 YR CANADA BOND YIELD: 3.592 DOWN 2 BASIS PTS

5 YR CANADA BOND YIELD: 3.241 DOWN 2 BASIS PTS.

1a New York Opening report

Futures Jump After Overnight Rollercoaster Session As Oil Unexpectedly Tumbles, Yen Soars

Thursday, Apr 30, 2026 – 08:19 AM

Futures erase an overnight slide, and have resumed their ascent trading near all time highs, despite a hawkish Fed statement but stronger Mag7 earnings. The hawkish Fed followed by a less hawkish press conference, plus the news that Powell is staying on seemingly removing a cut, actually have bond yields lower pre-mkt by 2-4bp as the Dollar weakens on what appears to be BOJ intervention which has sent the USDJPY plunging most since 2022. As of 8:00am ET, S&P futures are up 0.4%, erasing a 0.5% drop earlier in the session; Nasdaq futures gain 0.6%: in premarket trading Alphabet is the big gainer from the major tech companies that reported, with Amazon rising too but Meta and Microsoft falling (META -9% AMZN +2.3%, GOOG +6%, and MSFT -1.8%). Semis continue to trade higher as well as Discretionary, Industrials and Materials while Financials, Healthcare and Staples lower as Cyclicals lead Defensives. Energy names are mostly lower after striking rollercoaster in the price of oil. In commodities, energy is weaker, metals are higher led by precious, and Ags are mostly higher. Today’s US economic data calendar slate includes jobless claims, personal income and spending, 1Q employment cost index and first estimate of Q1 GDP (8:30am), April MNI Chicago PMI (9:45am, several minutes earlier for subscribers) and March Leading Index (10am)

In premarket trading, Mag 7 are mixed (NVDA +0.8%, AAPL +0.4%, TSLA +0.08%)

- Alphabet (GOOGL) jumps 7% after reporting high demand for its cloud and artificial intelligence offerings, giving investors confidence that its unprecedented investments in AI infrastructure will pay off.

- Amazon.com (AMZN) climbs 3% after the e-commerce and cloud-computing company reported first-quarter results that beat expectations on key metrics. Analysts are broadly positive on the report, saying that the acceleration of Amazon Web Services is underway.

- Meta Platforms (META) falls 9% after the Facebook parent gave a forecast for capital expenditures that was higher than expected, a sign that investors remain skeptical about AI-related spending in some instances.

- Microsoft (MSFT) slips about 2% after the software company reported third-quarter results. Some analysts said the pace of growth in its Azure cloud-computing business may have underwhelmed.

- Blue Owl Capital (OWL) gains 4% as fee-related earnings and assets increased as the alternative investment firm leaned on other parts of its business amid souring sentiment toward private credit.

- Carvana (CVNA) rises 11% after the company reported revenue for the first quarter that beat the average analyst estimate as used-car volumes hit a record.

- Caterpillar (CAT) climbs 5% after posting first-quarter earnings that beat Wall Street expectations as surging electricity demand from artificial intelligence data centers boosted sales of the company’s power-generation equipment.

- Chipotle Mexican Grill Inc. (CMG) gains 4% after eeking out higher sales last quarter, suggesting the chain is starting to win back diners who previously balked at the rising price of its burritos.

- Eli Lilly (LLY) rises 7% after raising its full-year sales outlook on the strength of its weight-loss drugs and high hopes for its new obesity pill.

- Ford (F) falls 4% after warning that an unexpected rise in commodity costs will weigh on earnings.

- FormFactor (FORM) rises 10% after the semiconductor manufacturing company reported first-quarter results that beat expectations on key metrics, although analysts were especially positive on the company’s gross margins.

- KLA Corp. (KLAC) falls 4% after analysts note the tepid growth rate at the semiconductor capital equipment company when compared to peers.

- Merck (MRK) gains 3% after the drugmaker reported sales for the first quarter that topped Wall Street’s expectations.

- Procept Biorobotics (PRCT) gains 15% after the medical and surgical equipment manufacturer reported revenue for the first quarter that surpassed expectations.

- Stellantis (STLA) is down 5% after the carmaker posted first-quarter results that included disappointing numbers from North America.

- Qualcomm (QCOM) jumps 11% after the company posted mixed results, but said that it was “excited” by its entry into data centers, where a “leading hyperscaler custom silicon engagement is on track for initial shipments later this calendar year.”

- Quanta Services (PWR) gains 6% after the provider of contracting services to electric utility companies reported adjusted earnings per share for the first quarter that beat the average analyst estimate.

- Royal Caribbean Cruises (RCL) rises 7% after posting first quarter adjusted EPS that topped estimates.

- Smurfit Westrock (SW) falls 5% after the packaging company reported first-quarter adjusted Ebitda that missed analyst estimates.

- Wayfair

tumbles 8% after the ecommerce firm reported adjusted earnings per share for the first quarter that missed the average analyst estimate.

tumbles 8% after the ecommerce firm reported adjusted earnings per share for the first quarter that missed the average analyst estimate.

In other corporate news, Starwood Capital is “temporarily suspending” share repurchases from its Starwood REIT to preserve liquidity while waiting for the commercial real estate market to improve. Stellantis shares fell after analysts pointed to the automaker’s worse-than-expected financial performance in North America. And Pop Mart reported a sharp slowdown in US sales, underscoring its challenges in diversifying beyond the Labubu toy. In other AI news, OpenAI has met a key milestone for securing AI capacity in the US several years ahead of schedule, boosting the startup’s ambitious plans for data center expansion. SoftBank plans to establish and list an AI and robotics company called Roze in the US. And banks that recently signed a $40 billion bridge loan with SoftBank for its investment in OpenAI are said to have attracted more lenders to the deal in syndication.

Market sentiment got a boost as global benchmark Brent crude oil erased an intraday jump of as much as 7.1% to above $126 a barrel. Axios had reported that President Donald Trump was slated to receive a briefing Thursday on new plans for potential military action in Iran, clouding hopes for an imminent peace agreement. It was unclear what prompted the oil reversal, although there has been speculation that the BOJ is intervening in both FX and oil.

From swings in oil prices to a divided Federal Reserve keeping rates on hold and impressive megacap tech earnings, traders are grappling with a barrage of whipsawing headlines. That’s testing a global equity rally that has wiped out war-related losses and pushed US markets to new highs as investors still look for signs of an end to the conflict.

“Equities are caught in between escalating Middle East tensions and strong fundamental earnings data being released,” said Wolf von Rotberg, equity strategist at Bank J Safra Sarasin Ltd. “Oil prices moving toward $150/bbl would likely increasingly impact the consumer in the US, which would also mark a turning point for equity markets. Thus, a deal is required to see a continued move higher over coming months.”

For stocks, “earnings expectations are behaving like a force of nature, and that is more important than anything else,” writes Bloombing Opinion columnist John Authers. Traders are also looking at the playbook from Ukraine and the tariff turmoil, but “it’s hard to believe they’re not over-confident.”

On balance, the frenzy of earnings after the close had a reassuring message, and a clear winner: Alphabet’s Google was able to point to solid growth at its cloud computing unit, which recorded estimate-beating sales of $20 billion last quarter, justifying its AI spending.

Meta was the loser of the pack, with shares sliding after it boosted full-year capex to as much as $145 billion. Investors are concerned that the investments may not pay off, as Meta’s AI system still trails its peers. “So far, Meta’s stand-alone app hasn’t had the amount of engagement vs. other frontier labs,” said BI analyst Mandeep Singh. Amazon was relatively well received, with revenue from its cloud division up 28%, the fastest growth rate since 2Q 2022. Microsoft slightly underwhelmed with a forecast for a “modest acceleration” in Azure cloud sales in the second half of the calendar year.

Japan’s currency strengthened as much as 1.6% against the dollar to 157.85, its lowest since April 17, after Japan’s top currency official Atsushi Mimura echoed Minister of Finance Satsuki Katayama’s warning earlier Thursday that “the timing for taking bold steps is nearing.”

In politics, the 74-day shutdown of the Department of Homeland Security is nearing an end after House Speaker Mike Johnson united Republicans behind a two-part budget plan to fully fund the department. Members of Trump’s administration are said to have told Anthropic that they don’t agree with the company’s plan to grant access to its Mythos technology to roughly 70 companies and organizations.

European Stocks turned positive, with the Stoxx 600 now up by 0.4% having fallen as much as 0.7% ahead of the European Central Bank’s interest-rate decision today. BNP Paribas fell after the lender reported higher credit provisions than expected. Credit Agricole and Societe Generale also dropped after results.Here are the biggest movers Thursday:

- Arcadis shares gain as much as 14%, the steepest intraday gain since July 2020, after the Dutch engineering services firm’s first-quarter results met with a positive response from Degroof Petercam analysts

- Glencore shares gain as much as 2.6% after the trading and mining giant posted strong profits, with 2026 full-year marketing Ebit expected to “comfortably exceed the top end of the range”

- United Utilities, the water utility company, rises as much as 12% to a record high following an £800m equity raise announcement. Analysts say the raise supports accelerated asset base growth and upgraded return targets

- Magnum Ice Cream shares rise as much as 13%, the biggest jump since its listing in December last year, after the former Unilever unit reported strong first-quarter volumes

- Delivery Hero gains as much as 6.6% after the food delivery firm said it’s confident of achieving upper half of its Ebitda guidance range. That comes after 1Q results beat estimates and showed a modest recovery in its core market Asia

- Puma shares rose as much as 4.1% on Thursday after reporting gross profit margin and sales for the first quarter that beat the average analyst estimate, with analysts saying the results were solid and showed progress

- BNP Paribas shares dropped as much as 5.3% amid a wider decline for its French peers. The lender reported what analysts say are mixed results with a beat driven by its Corporate Centre unit, while the Arval unit disappointed

- SocGen shares decline as much as 6.7% on earnings that KBW called lackluster after fixed income revenue missed estimates. Profit beat consensus as equity trading and French retail units jumped from a year earlier

- Stellantis shares fall as much as 10% after the carmaker posted first-quarter results where key North America numbers disappointed, with analysts seeing a somewhat mixed print

- Erste Group Bank shares slide as much as 4.6% after the lender reported what a Barclays analyst called a low-quality profit beat helped by one-off gains, with adjusted earnings falling short of expectations

- Weir Group shares fall as much as 9.9% after the mining equipment provider reported first-quarter orders that analysts said look weak relative to peers

- Technip Energies shares slump as much as 10%, the most since October 2023, after the French engineering and technology company reported weaker-than-expected earnings for the first quarter and cut its guidance

Asian stocks slumped as Brent crude surged to a four-year high, fueling inflation concerns and dragging currencies lower across the region’s emerging economies. The MSCI Asia Pacific Index slid as much as 1.6%, the most intraday since April 2, before paring some declines. Equity benchmarks in Indonesia, South Korea and the Philippines were among the top losers. All sectors on the regional gauge fell, except energy. Thursday’s losses pared the MSCI Asia gauge’s April gain to under 13%. It was still on course for its best month since November 2022, with a rally in tech names having overshadowed the impact of the US-Iran war on the broader market. Asian tech shares outperformed earlier on Thursday, following indications of continued high spending on AI infrastructure by the likes of Alphabet and Meta Platforms. Samsung Electronics’ chip arm beat expectations with a 48-fold jump in profit. However, those gains faded as the session progressed, suggesting investors likely trimmed positions ahead of the long weekend. Many of the region’s markets will be shut on Friday.

In FX, the yen the standout in currencies on increasing intervention risks, Bloomberg Dollar Spot Index down 0.4%. The pound and UK bonds gained after the Bank of England left interest rates unchanged, with several policymakers saying they might consider future hikes given high energy prices.

In rates, treasuries rebounded after the surge in oil and a hawkish hold by the Fed drove bonds lower on Wednesday. US front-end yields are more than 5bp lower on the day, steepening 2s10s and 5s30s spreads by 2bp-3bp. 10-year, lower by about 4bp at session low 4.39%, trails 7bp drop for UK 10-year. US 30-year is back below 4.98% after topping 5% late Wednesday for the first time since July. UK gilts rally after Bank of England held rates steady, meeting expectations.

In commodities, oil prices reversed an earlier spike which took them to a wartime high, after Axios reported that US President Donald Trump will receive a briefing on new military options for action in Iran, signaling the potential for fresh escalation in the Middle East. The two sides showed little sign of breaking their impasse and agreeing to another round of peace talks, with Trump saying his navy’s blockade is working. However, shortly after the European open, oil tumbled with Brent now falling back toward $114.Gold prices higher and back above $4,600/oz.

US economic data calendar slate includes jobless claims, personal income and spending, 1Q employment cost index and first estimate of Q1 GDP (8:30am), April MNI Chicago PMI (9:45am, several minutes earlier for subscribers) and March Leading Index (10am)

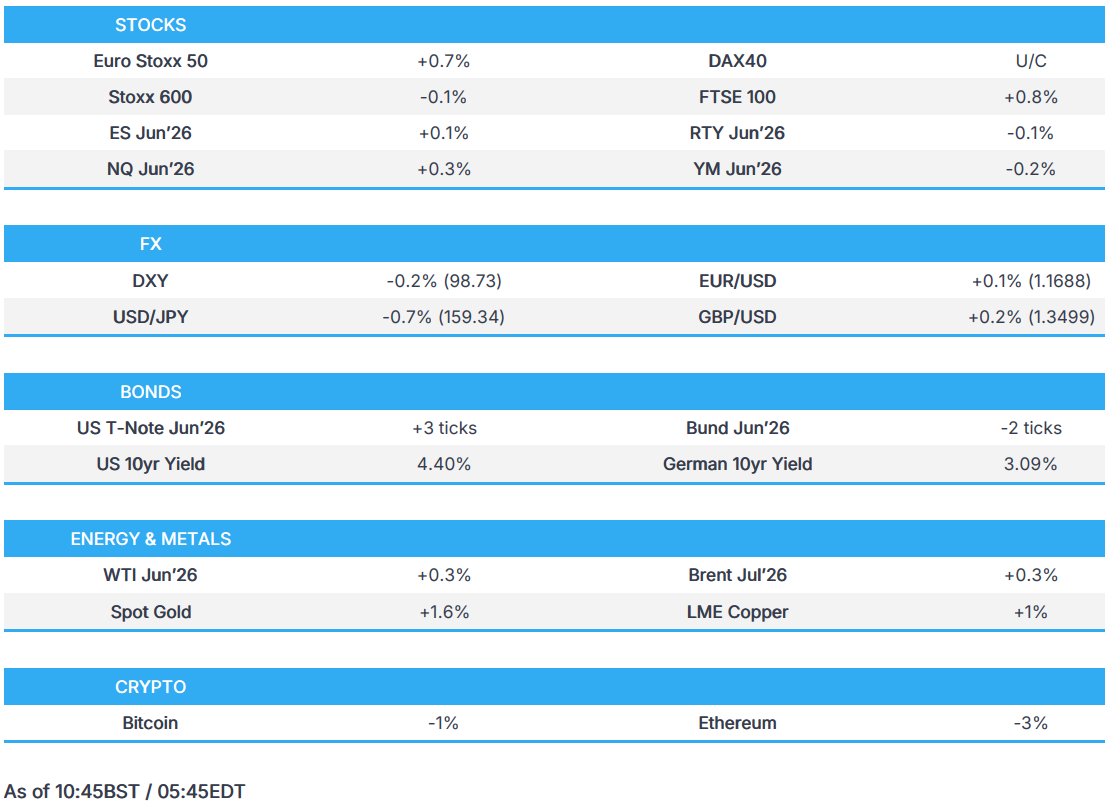

Market Snapshot

- S&P 500 mini +0.4%

- Nasdaq 100 mini +0.5%

- Russell 2000 mini +0.2%

- Stoxx Europe 600 +0.2%

- DAX +0.2%

- CAC 40 -0.8%

- 10-year Treasury yield -3 basis points at 4.4%

- VIX -0.5 points at 18.31

- Bloomberg Dollar Index -0.2% at 1199.46

- euro +0.1% at $1.169

- WTI crude +0.1% at $107.01/barrel

Top Overnight News